UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act File Number 811-23658

Forum Real Estate Income Fund

___________________________________________

(Exact name of registrant as specified in charter)

240 Saint Paul Street, Suite 400

Denver, CO 80206

___________________________________________

(Address of principal executive offices) (Zip code)

Darren Fisk

Forum Capital Advisors, LLC

240 Saint Paul Street, Suite 400

Denver, CO 80206

___________________________________________

(Name and address of agent for service)

Registrant’s telephone number, including area code: (303) 501-8860

Date of fiscal year end: December 31

Date of reporting period: December 31, 2023

Item 1. Reports to Stockholders

(a) The following is a copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1).

![]()

Forum Real Estate Income Fund

Founders Shares

Class I Shares

Annual Report December 31, 2023 |

Investor Information: 1-303-501-8860 |

This report and the financial statements contained herein are submitted for the general information of shareholders and are not authorized for distribution to prospective investors unless preceded or accompanied by an effective prospectus. Nothing contained herein is to be considered an offer of sale or solicitation of an offer to buy shares of the Forum Real Estate Income Fund. Such offering is made only by prospectus, which includes details as to offering price and other material information.

TABLE OF CONTENTS

1 | ||

5 | ||

7 | ||

8 | ||

13 | ||

14 | ||

15 | ||

16 | ||

17 | ||

19 | ||

33 | ||

34 | ||

36 | ||

38 |

Dear Shareholder:

We are pleased to present the 2023 annual report for Forum Real Estate Income Fund.

Forum Real Estate Income Fund (the “Fund”) was created to deliver access to institutional-quality commercial real estate debt investments not typically available to individual investors, with the primary objectives of maximizing current income and preserving capital, and a secondary emphasis on achieving long-term capital appreciation.

The Fund leverages the expertise of two established investment managers, Forum Capital Advisors LLC (“FCA” or “the Adviser”) and Janus Henderson Investors US LLC (“Janus” or “the Sub-adviser”) to source, evaluate, and monitor its differentiated and diversified institutional real estate portfolio. At the time of this report, the Fund’s portfolio primarily includes CMBS, agency and non-agency securitizations, preferred equity positions, and senior and mezzanine loans.

FCA, together with its affiliates (collectively, “Forum”1), has completed over $2.5 billion2 in real estate transactions in its history, including the origination of over $595.5 million3 in multifamily investments since Forum’s inception in 2007. Janus, whose mission is to help clients define and achieve superior financial outcomes through differentiated insights, disciplined investments, and world-class service., has $308.3 billion in client assets under management4 and employs over 340 investment professionals nationwide4. Together, the combined experience of Forum and Janus presents the Fund with what we believe is the unique capacity to identify and procure income-producing, institutional-quality real estate related investments across both the public and private sectors.

The Fund is taxed as a REIT, which qualifies it to obtain certain tax attributes that could result in a lower net effective tax rate, and higher after-tax dividend proceeds to certain types of investors, when compared to most non-REIT fixed income alternatives. FCA also believes that this structure generally helps simplify the year-end tax reporting process, as investors receive one Form 1099 from the Fund, as opposed to several federal and state K-1s5.

____________

1 Forum Investment Group LLC is primarily comprised of Forum Capital Advisors LLC and FCA Capital Markets LLC, and is affiliated with Forum Real Estate Group, LLC (collectively, “Forum”).

2 Figures represent Forum’s current and historical multifamily portfolio, including stabilized properties (defined as a property that has achieved 92% occupancy), assets that are under construction or development (defined as a property that is under construction and has not yet received its final certificate of occupancy), assets in lease up (defined as a property that has received final certificate of occupancy but is not yet stabilized at 92% occupancy), and assets that have been sold as of December 31, 2023. Includes assets owned by Forum related parties and affiliates. Commercial/land projects are excluded.

3 Figures reflect the Forum Structured Finance team’s historical multifamily portfolio from December 2015 through December 2023. The team originated $254.7 million prior to joining Forum, and $340.8 million since joining Forum in 2021 ($71.8 million has been originated through a separate Forum private offering).

4 Obtained directly from Janus Henderson Investors US LLC as of September 30, 2023.

5 This information is provided for informational purposes only and is not intended to be relied upon as tax, legal, or investment advice.

1

FORUM REAL ESTATE INCOME FUND

|

Performance

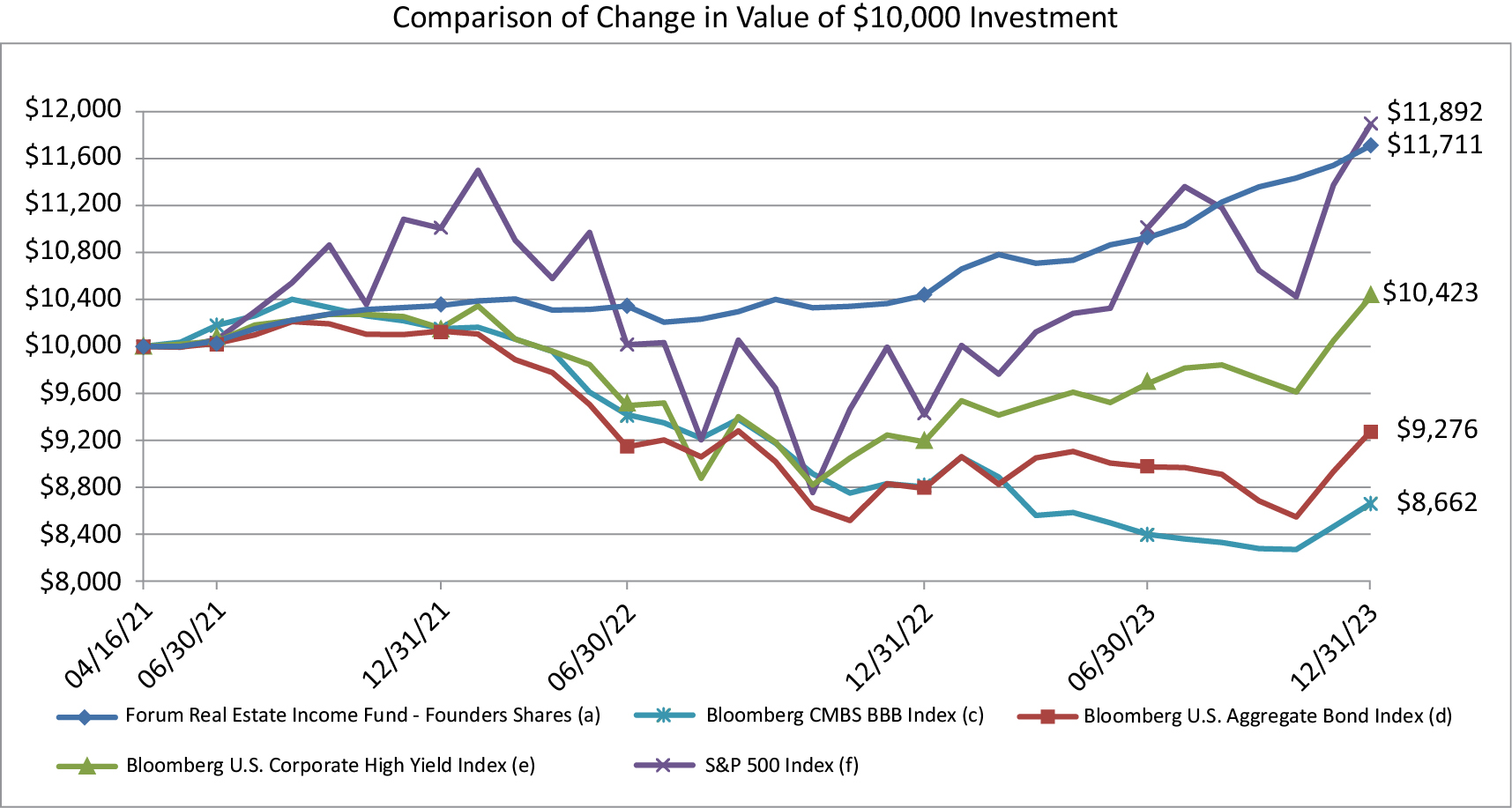

The Fund continues to seek to fulfill its primary objective of providing current income to shareholders, paying a 9.29% cumulative annual dividend in 20236. Additionally, the Fund’s net return of 12.24%6 compares favorably to that of its primary benchmark, the Bloomberg CMBS BBB Index (-1.61%).

Market Update

Years from now, investors may look back on the fourth quarter of 2023 and remember it for one thing: the perceived end of the Federal Reserve’s rate-hiking cycle. Optimism surrounding such a pivot appeared to start bubbling into markets in early November and skyrocketing in mid-December when Federal Reserve Chair Jay Powell carried out an unexpected about-face.

We cannot be certain what precipitated such an abrupt conversion. With the Chair’s comments that every move is data-dependent, there appeared to be ample data points indicating the economy was softening and inflation was easing.

Whatever the reasons may have been, in our view, the apparent result was a seemingly positive ending to 2023. Yields plummeted, and a tsunami of buyers flooded the public markets. Fortunately for investors in listed CRE, the shelves were well stocked with REITs, which as a sector spiked in excess of 20% in the last two months of the year, taking it from deep in the red to plus 9% (Bloomberg). In the end, the rally turned a ho-hum year in equities into a blockbuster, with the Dow, S&P 500 and NASDAQ ending the year up 16%, 26%, and 44%, respectively (Bloomberg). Bonds trended in the same direction (of the indexes we use for comparison in our monthly fact sheets, only Bloomberg CMBS BBB Index failed to climb into positive territory for the year).

In contrast to the volatility of the public markets, it was largely more of the same at the property levels. The collapse in rates occurred late in the quarter, so we only caught the initial stages of the move, which came in the form of a pick-up in activity in the fast-adjusting CMBS market. We believe how quickly and to what degree potentially lower rates and a more benign outlook take hold in the broader lending markets will be major drivers of CRE sentiment and returns in 2024. Our hunch is that traditional lenders may prove to be a bit apprehensive given legacy issues and the challenges of the last year, but we also think there remains an abundance of liquidity, which we believe may lead to a healthy response from more opportunistic players and new entrants to CRE lending.

Strategy

We believe the Fund’s 2023 returns would have been meaningfully lower without the extensive optionality built into our investment platform (the flexibility inherent in our broad mandate and extensive sourcing). With a deep and growing pipeline, healthy debt markets, and compelling yields, we entered the year expecting the bulk of the best opportunities to come from private markets. However, the significant and rapid rise in interest rates seemed to suppress borrowing activity, as lenders generally appeared to pull back (or exit the market altogether). As a result, underwriting likely became more difficult, and developers hit the pause button while they tried to work the higher cost of capital into their models.

____________

6 The cumulative annual dividend for 2023 is comprised of 100% net investment income and reflects that of FORFX only. As FORAX was launched in February 2023, cumulative annual data, including the annual net return is unavailable for the year ended December 31, 2023.

2

FORUM REAL ESTATE INCOME FUND

|

This is where the optionality of our platform comes into play. While the logjam in private markets seemed to be hindering deal flow, attractive opportunities appeared to be emerging in the CMBS market, which is where the vast majority of the Fund’s 2023 returns were generated. So, while in hindsight we began the year stalking what wound up being sparse hunting grounds, we were able to shift rapidly to what we believed to be a more target-rich environment; a testament to our ability to be nimble, as well as to the depth and diversity of the CRE debt markets. In a fast-changing economic climate with lots of uncertainty, our portfolio management team is constructed to navigate an expansive and varied investment landscape.

Outlook

We believe our Fund is an “all-weather” vehicle rooted in a bottom-up, research-driven investment process. Macro is important — we believe CRE is the landlord to the global economy — and we pay attention, but it is not where we perceive there to be an investment edge. Last year, we said glancing into our crystal ball was like peering through yogurt. It seems no less murky this year. With that caveat, here are a couple thoughts on 2024, one high-level macro, the other more CRE centric.

Because our focus is on defense, our default macro approach involves a lot of scouring for things that to us appear unsustainable. Our list is longer than any other time in the last five years or so, but the two areas we are going to focus on are geopolitics and debt, which we believe fall firmly in the “concerning” bucket.

Geopolitics is a rabbit hole we are generally reluctant to go down, knowing we can barely scratch the surface in this limited space. The below may not stand out as the most important, or even most pressing, global problems, however our perspective is tied to the goal of identifying fragility or unsustainability that could potentially have significant and/or sudden economic repercussions.

• Gaza — The potential for broader and intensifying Middle East conflict.

• Ukraine — What appears to be the dwindling likelihood of a desirable outcome, and the potentially painful and unpredictable realignment for Europe/NATO.

• Energy — Governmental policies potentially leaving much of Western world susceptible to major shortfalls or disruptions.

• U.S. as Global Cop — Continuing to protect vulnerable global supply chains with limited allies and an armed forces that is stretched thin (particularly the Navy).

• Taiwan — The potential threat of an emboldened China.

3

FORUM REAL ESTATE INCOME FUND

|

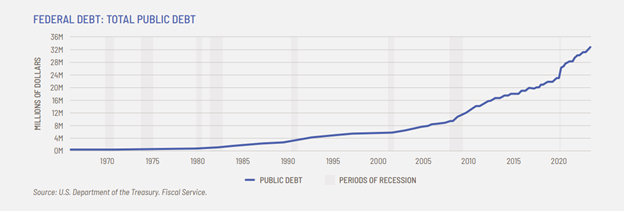

With respect to debt, see the chart below. We are aware that there may exist more daunting sovereign debt predicaments beyond our borders, and that this country, with its reserve currency status, is uniquely positioned to push the envelope. However, is it sustainable?

Perhaps such unknowns could prove too much for markets to shake off in 2024. However, we believe there at least appears to be growing interest in discussing/addressing many of these oft neglected, or even “off-limits,” issues. While many have been content to dodge these topics and divert attention to more trivial matters, we have noticed that the business community has begun pushing these issues to the forefront and promoting thoughtful debate.

On the heels of a couple lean years on the transaction front, the recent burst of optimism surrounding potential rate cuts appears to be giving rise to some itchy trigger fingers in CRE markets. Our inclination would be to resist this by maintaining underwriting discipline, staying focused on fundamentals, and avoiding an overconfident approach to leverage. There is still work to be done at the operating level, with each sector grappling with its own idiosyncratic challenges, ranging from supply and expense headwinds to demand degradation. Sometimes early is wrong, so it is probably a good time to keep another of our CRE dictums top of mind: income is fleeting, basis is forever. We suspect there will be some tasty looking cheese hitting the market in the near future, but, if history repeats, some of that cheese will be perched on a trap, in which case it’ll be much better to be the second mouse on the scene.

Sincerely,

Jay Miller, President

All statements made herein are opinions of Forum Capital Advisors LLC, unless otherwise stated, and should not be construed as investment advice and/or recommendations.

Dividends are not a direct reflection of Fund performance. The Fund can pay dividends from any source, including income and realized gains. The Fund’s dividend proceeds may exceed its earnings, in which case portions of dividends that the Fund makes may be a return of capital that shareholders originally invested.

4

The Fund’s performance figures* for the period ended December 31, 2023, compared to its benchmarks:

Fund/Index | One Year | Annualized | ||||

Forum Real Estate Income Fund – Founders Shares(a) | 12.24 | % | 6.00 | % | ||

Forum Real Estate Income Fund – Class I Shares | N/A |

| 8.76 | %(b) | ||

Fund Benchmarks |

|

| ||||

Bloomberg CMBS BBB Index(c) | (1.61 | )% | (5.18 | )% | ||

Bloomberg U.S. Aggregate Bond Index(d) | 5.53 | % | (2.74 | )% | ||

Bloomberg U.S. Corporate High Yield Index(e) | 13.45 | % | 1.54 | % | ||

S&P 500 Index(f) | 26.29 | % | 6.60 | % | ||

____________

* The Fund’s past performance does not guarantee future results. The investment return and principal value of an investment in the Fund will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. The returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. Current performance of the Fund may be lower or higher than the performance quoted. Returns are calculated using the traded net asset value or “NAV” on December 31, 2023. Performance data current to the most recent month end may be obtained by visiting www.forumcapadvisors.com or by calling 1-303-501-8860.

(a) The Founders Shares of the Fund commenced operations on April 16, 2021. The performance is based on average annual returns.

(b) The Class I Shares of the Fund commenced operations on February 22, 2023. The performance is based on cumulative returns.

(c) The Bloomberg CMBS BBB Index measures BBB-rated market of U.S. Agency and U.S. Non-Agency conduit and fusion CMBS deals with a minimum current deal size of $300mn. The index includes both U.S. Aggregate eligible and Non-U.S. Aggregate eligible securities.

(d) The Bloomberg U.S. Aggregate Bond Index is a market capitalization-weighted index, meaning the securities in the index are weighted according to the market size of each bond type. Most U.S. traded investment grade bonds are represented. Municipal bonds and Treasury Inflation-Protected Securities are excluded, due to tax treatment issues. The index includes Treasury securities, Government agency bonds, mortgage-backed bonds, corporate bonds, and a small amount of foreign bonds traded in U.S. Dollars. Index returns assume reinvestment of dividends. Investors may not invest in an Index directly. Unlike the Fund’s returns, Index returns do not reflect any fees or expenses.

5

FORUM REAL ESTATE INCOME FUND December 31, 2023 |

(e) The Bloomberg U.S. Corporate High Yield Index measures the USD-denominated, high yield fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on Bloomberg EM country definition, are excluded.

(f) The S&P 500 Index measures the performance of 500 widely held stocks in the U.S. equity market. Standard and Poor’s chooses member companies for the index based on market size, liquidity and industry group representation. Included are the stocks of industrial, financial, utility, and transportation companies.

6

Portfolio Composition* as of December 31, 2023

Top 10 Holdings** | % of | ||

DBCCRE 2014-ARCP Mortgage Trust | 6.1 | % | |

BPR Trust 2022-OANA | 5.1 | % | |

Med Trust 2021-MDLN | 5.1 | % | |

Royal Urban Renewal, LLC | 5.0 | % | |

CSMC 2021-WEHO | 4.7 | % | |

2023-MIC Trust | 4.5 | % | |

BX Trust 2021-BXMF | 4.2 | % | |

Extended Stay America Trust 2021-ESH | 3.8 | % | |

BX Commercial Mortgage Trust 2021-SOAR | 3.7 | % | |

FREMF 2020-KF95 Mortgage Trust | 3.7 | % | |

45.9 | % | ||

____________

* Composition of holdings are subject to change.

** Excludes money market position.

7

Units/ | Reference | Coupon | Maturity | Fair Value | |||||||

PRIVATE INVESTMENTS – EQUITY — 3.9% |

| ||||||||||

REAL ESTATE COMMON EQUITY — 1.1% |

| ||||||||||

40 | CRIMSON DEVCO, LLC(a),(b),(c) | N/A | N/A | N/A | $ | 1,000,000 | |||||

| |||||||||||

REAL ESTATE PREFERRED EQUITY — 2.8% |

| ||||||||||

969,784 | IOTA Multifamily Development(a),(b) | Cash: 6.000%, PIK: 6.250% | 12.250 | 04/01/25 |

| 930,864 | |||||

1,735,112 | Zephyr Preferred Equity(a),(b),(e) | Cash: 7.000%, PIK: 1-Month Term SOFR + 5.000% | 17.321 | 06/14/27 |

| 1,735,112 | |||||

| 2,665,976 | ||||||||||

TOTAL PRIVATE INVESTMENTS – EQUITY |

| 3,665,976 | |||||||||

Principal | ||||||||||

PRIVATE INVESTMENTS – MEZZANINE LOANS — 16.5% | ||||||||||

267,489 | Advantis MCA FV, LLC(a),(b),(e),(f) | 1-Month Term SOFR + 11.900%; 1-Month Term SOFR floor 1.530% | 17.220 | 07/22/25 | 267,489 | |||||

148,623 | Advantis MCA Harbor, LLC(a),(b),(e),(f) | 1-Month Term SOFR + 11.900%; 1-Month Term SOFR floor 3.480% | 17.220 | 04/18/25 | 148,623 | |||||

2,220,009 | FCREIF Nimbus Everett(a),(b),(g) | N/A | 12.000 | 08/31/24 | 2,188,753 | |||||

2,521,552 | FCREIF Van Ness(a),(b),(h) | Cash: 5.000%, PIK: 7.500% | 12.500 | 07/23/24 | 2,498,359 | |||||

1,520,000 | Lexington So Totowa, LLC(a),(b),(e) | Cash: 1-Month Term SOFR + 11.250% | 16.570 | 06/30/24 | 1,520,000 | |||||

4,813,784 | Royal Urban Renewal, LLC(a),(b),(d) | Cash: 6.500%, PIK: 5.500% | 12.000 | 10/01/24 | 4,739,772 | |||||

3,164,177 | Trent Development – Kerf Apartments Loan(a),(b),(d) | Cash: 6.000%, PIK: 6.000% | 12.000 | 09/23/24 | 3,116,860 | |||||

1,101,516 | West University Gainesville Mezz, LLC(a),(b),(e),(f) | SOFR30A + 10.350%; SOFR30A floor 0.250% | 15.670 | 12/03/24 | 1,101,516 | |||||

TOTAL PRIVATE INVESTMENTS – MEZZANINE LOANS | 15,581,372 |

See accompanying notes which are an integral part of these financial statements.

8

FORUM REAL ESTATE INCOME FUND As of December 31, 2023 |

Principal | Reference | Coupon | Maturity | Fair Value | |||||||

COMMERCIAL MORTGAGE-BACKED SECURITIES (“CMBS”) — 92.0% |

| ||||||||||

AGENCY CMBS — 15.7% |

| ||||||||||

3,293,687 | FREMF 2018-KSW4 Mortgage Trust(e) | SOFR30A + 5.114% | 10.445 | 10/25/28 | $ | 2,934,682 | |||||

2,180,108 | FREMF 2019-KF70 Mortgage Trust(e),(i),(j) | SOFR30A + 6.114% | 11.445 | 09/25/29 |

| 2,120,188 | |||||

3,530,103 | FREMF 2020-KF95 Mortgage Trust(e),(i) | SOFR30A + 9.000% | 14.331 | 12/25/30 |

| 3,485,995 | |||||

2,911,258 | FREMF 2021-KF98 Mortgage Trust(e),(i) | SOFR30A + 8.500% | 13.831 | 12/25/30 |

| 2,890,065 | |||||

1,500,000 | Multifamily Connecticut Avenue Securities Trust 2019-01 – Class CE(e),(i) | SOFR30A + 8.864% | 14.202 | 10/25/49 |

| 1,441,219 | |||||

2,000,000 | Multifamily Connecticut Avenue Securities Trust 2020-01(e),(i) | SOFR30A + 7.614% | 12.952 | 03/25/50 |

| 1,965,926 | |||||

| 14,838,075 | ||||||||||

| |||||||||||

NON-AGENCY CMBS — 76.3% |

| ||||||||||

4,000,000 | 2023-MIC Trust(e),(i),(j) | N/A | 9.532 | 12/05/38 |

| 4,256,016 | |||||

16,800,000 | BAMLL Commercial Mortgage Securities Trust 2016-ISQ – Class XA(e),(i) | N/A | 0.758 | 08/14/34 |

| 296,933 | |||||

8,540,000 | BAMLL Commercial Mortgage Securities Trust 2016-ISQ – Class XB(e),(i) | N/A | 0.254 | 08/14/34 |

| 52,161 | |||||

50,880,592 | BBCMS Trust 2015-VFM(e),(i) | N/A | 0.258 | 03/12/36 |

| 226,788 | |||||

5,000,000 | BPR Trust 2022-OANA(e),(i),(j) | 1-Month Term SOFR + 3.695% | 9.057 | 04/15/37 |

| 4,815,320 | |||||

1,020,000 | BX Commercial Mortgage Trust 2019-XL(e),(i) | 1-Month Term SOFR + 2.764% | 8.126 | 10/15/36 |

| 1,004,232 | |||||

3,713,620 | BX Commercial Mortgage Trust 2021-SOAR(e),(i),(j) | 1-Month Term SOFR + 3.864% | 9.226 | 06/15/38 |

| 3,523,943 | |||||

2,267,485 | BX Commercial Mortgage Trust | 1-Month Term SOFR + 4.067% | 9.429 | 05/15/38 |

| 2,165,061 | |||||

3,500,000 | BX Commercial Mortgage Trust 2021-VOLT(e),(i),(j) | 1-Month Term SOFR + 2.514% | 7.876 | 09/15/36 |

| 3,344,239 | |||||

1,492,531 | BX Trust 2019-MMP – Class D(e),(i) | 1-Month Term SOFR + 1.644% | 7.006 | 08/15/36 |

| 1,424,366 | |||||

995,021 | BX Trust 2019-MMP – Class F(e),(i) | 1-Month Term SOFR + 2.836% | 8.198 | 08/15/36 |

| 927,730 | |||||

2,500,000 | BX Trust 2021-ARIA(e),(i) | 1-Month Term SOFR + 3.257% | 8.619 | 10/15/36 |

| 2,349,150 | |||||

4,223,093 | BX Trust 2021-BXMF(e),(i) | 1-Month Term SOFR + 3.464% | 8.826 | 10/15/26 |

| 3,941,480 | |||||

1,582,331 | BX Trust 2021-MFM1(e),(i) | 1-Month Term SOFR + 4.014% | 9.376 | 01/15/34 |

| 1,553,164 | |||||

2,000,000 | BX Trust 2022-LBA6(e),(i) | 1-Month Term SOFR + 4.200% | 9.562 | 01/15/39 |

| 1,928,938 | |||||

3,000,000 | BXHPP Trust 2021-FILM(e),(i) | 1-Month Term SOFR + 1.214% | 6.576 | 08/15/36 |

| 2,697,600 | |||||

4,533,020 | CSMC 2021-WEHO(e),(i) | 1-Month Term SOFR + 4.084% | 9.446 | 04/15/24 |

| 4,458,134 | |||||

See accompanying notes which are an integral part of these financial statements.

9

FORUM REAL ESTATE INCOME FUND As of December 31, 2023 |

Principal | Reference | Coupon | Maturity | Fair Value | |||||||

NON-AGENCY CMBS — 76.3% (continued) |

| ||||||||||

100,000 | DBCCRE 2014-ARCP Mortgage Trust – Class C(e),(i) | N/A | 4.935 | 01/10/34 | $ | 99,055 | |||||

290,000 | DBCCRE 2014-ARCP Mortgage Trust – Class D(e),(i) | N/A | 4.935 | 01/10/34 |

| 287,002 | |||||

5,800,000 | DBCCRE 2014-ARCP Mortgage Trust – Class F(e),(i) | N/A | 4.935 | 01/10/34 |

| 5,719,241 | |||||

2,500,000 | DROP Mortgage Trust 2021-FILE(e),(i) | 1-Month Term SOFR + 1.264% | 6.626 | 10/15/43 |

| 2,315,083 | |||||

3,640,416 | Extended Stay America Trust 2021-ESH(e),(i),(j) | 1-Month Term SOFR + 3.814% | 9.176 | 07/15/38 |

| 3,571,270 | |||||

1,667,000 | Hudson's Bay Simon JV Trust 2015-HBS – Class B7(i) | N/A | 4.666 | 08/05/34 |

| 1,402,734 | |||||

67 | Hudson's Bay Simon JV Trust 2015-HBS – Class BFL(e),(i) | 1-Month Term SOFR + 2.514% | 7.860 | 08/05/34 |

| 67 | |||||

5 | Hudson's Bay Simon JV Trust 2015-HBS – Class DFL(e),(i) | 1-Month Term SOFR + 4.014% | 9.360 | 08/05/34 |

| 5 | |||||

1,500,000 | ILPT Commercial Mortgage Trust 2022-LPF2(e),(i) | 1-Month Term SOFR + 5.940% | 11.302 | 10/15/39 |

| 1,430,247 | |||||

125,000 | KNDL 2019-KNSQ Mortgage Trust(e),(i) | 1-Month Term SOFR + 2.196% | 7.558 | 05/15/36 |

| 122,817 | |||||

4,976,118 | Med Trust 2021-MDLN(e),(i),(j) | 1-Month Term SOFR + 5.364% | 10.726 | 11/15/38 |

| 4,780,298 | |||||

1,800,000 | MKT 2020-525M Mortgage Trust(e),(i) | N/A | 2.941 | 02/12/40 |

| 537,050 | |||||

1,800,000 | Morgan Stanley Capital I Trust 2019-MEAD(e),(i) | N/A | 3.177 | 11/10/36 |

| 1,516,541 | |||||

3,600,000 | NCMF Trust 2022-MFP(e),(i),(j) | 1-Month Term SOFR + 5.128% | 10.490 | 03/15/39 |

| 3,459,290 | |||||

2,962,567 | OPEN Trust 2023-AIR(e),(i) | 1-Month Term SOFR + 9.429% | 14.791 | 10/15/28 |

| 2,970,474 | |||||

1,500,000 | SMRT 2022-MINI – Class E(e),(i) | 1-Month Term SOFR + 2.700% | 8.062 | 01/15/39 |

| 1,414,137 | |||||

1,500,000 | SMRT 2022-MINI – Class F(e),(i) | 1-Month Term SOFR + 3.350% | 8.712 | 01/15/39 |

| 1,383,936 | |||||

3,407,000 | VASA Trust 2021-VASA(e),(i) | 1-Month Term SOFR + 4.014% | 9.376 | 07/15/39 |

| 1,930,093 | |||||

354,000 | Worldwide Plaza Trust 2017-WWP(e),(i) | N/A | 3.596 | 11/10/36 |

| 20,804 | |||||

| 71,925,399 | ||||||||||

TOTAL COMMERCIAL MORTGAGE-BACKED SECURITIES |

| 86,763,474 | |||||||||

See accompanying notes which are an integral part of these financial statements.

10

FORUM REAL ESTATE INCOME FUND As of December 31, 2023 |

Shares | Fair Value | |||||

SHORT-TERM INVESTMENTS — 6.8% |

|

| ||||

MONEY MARKET FUNDS — 6.8% |

|

| ||||

6,400,078 | Fidelity Treasury Portfolio – Institutional Class, 5.15%(k) | $ | 6,400,078 |

| ||

|

| |||||

TOTAL SHORT-TERM INVESTMENTS |

| 6,400,078 |

| |||

TOTAL INVESTMENTS — 119.2% | $ | 112,410,900 |

| |||

TOTAL LIABILITIES IN EXCESS OF OTHER ASSETS — (19.2)% |

| (18,142,697 | ) | |||

TOTAL NET ASSETS — 100.0% | $ | 94,268,203 |

| |||

Principal | Interest | Maturity | Fair Value | ||||||||

| REVERSE REPURCHASE AGREEMENTS — (19.1)% |

|

| ||||||||

(3,224,000 | ) | Lucid Management Reverse Repo BPR Trust | 6.815 | 01/18/24 | $ | (3,224,000 | ) | ||||

(2,218,000 | ) | Lucid Management Reverse Repo BX Trust | 6.860 | 01/18/24 |

| (2,218,000 | ) | ||||

(1,646,000 | ) | Lucid Management Reverse Repo ESA Trust | 6.985 | 01/18/24 |

| (1,646,000 | ) | ||||

(2,055,000 | ) | Royal Bank Canada Reverse Repo BX Mtg. Trust | 7.200 | 03/20/24 |

| (2,055,000 | ) | ||||

(1,248,000 | ) | Royal Bank Canada Reverse Repo FREMF Mtg. Trust | 7.450 | 02/09/24 |

| (1,248,000 | ) | ||||

(2,931,000 | ) | Royal Bank Canada Reverse Repo FRN Trust | 6.840 | 05/07/24 |

| (2,931,000 | ) | ||||

(2,746,000 | ) | Royal Bank Canada Reverse Repo Med Trust | 7.350 | 02/09/24 |

| (2,746,000 | ) | ||||

(1,981,000 | ) | Royal Bank Canada Reverse Repo NCMF Trust | 7.100 | 02/26/24 |

| (1,981,000 | ) | ||||

| TOTAL REVERSE REPURCHASE AGREEMENTS | $ | (18,049,000 | ) | |||||||

See accompanying notes which are an integral part of these financial statements.

11

FORUM REAL ESTATE INCOME FUND As of December 31, 2023 |

LLC — Limited Liability Company

SOFR — Secured Overnight Financing Rate

PIK — Payment In Kind

SOFR30A — United States 30 Day Average SOFR Secured Overnight Financing Rate

(a) Denotes an illiquid and restricted security that either: (a) cannot be offered for public sale without first being registered, or availing of an exemption from registration, under the Securities Act of 1933; or (b) is subject to a contractual restriction on public sales. The total of these illiquid and restricted securities represents 20.42% of Net Assets. The total value of these securities is $19,247,348 (see Note 5).

(b) The value of this security has been determined in good faith under policies adopted by the Board of Trustees. Level 3 securities fair valued under procedures established by the Board of Trustees, represents 20.42% of Net Assets. The total value of these securities is $19,247,348.

(c) Non-income producing security.

(d) Interest on loans funded from interest reserve.

(e) Variable or floating rate security, the interest of which adjusts periodically based on changes in current interest rates and prepayments on the underlying pool of assets. The rate shown represents the rate on December 31, 2023.

(f) Cash portion of interest is included in principal of loans.

(g) The Fund’s ownership of this investment is through a wholly owned subsidiary, FCREIF Nimbus Everett, LLC. Effective August 31, 2023, payments are received in 100% cash. Prior to August 31, 2023, payments were made as 6% cash and 6% PIK.

(h) The Fund’s ownership of this investment is through a wholly owned subsidiary, FCREIF Van Ness SFO, LLC.

(i) Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities are restricted and may be resold in transactions exempt from registration normally to qualified institutional buyers. The total value of these securities is $83,828,792, which represents 88.93% of total net assets of the Fund.

(j) All or a portion of this security has been pledged as collateral for securities sold under agreement to repurchase. Total market value of underlying collateral for open reverse repurchase agreements at December 31, 2023 was $26,113,093.

(k) Rate disclosed is the seven-day effective yield as of December 31, 2023.

Portfolio Composition as of December 31, 2023

Types of Holdings | % of | ||

Commercial Mortgage – Backed Securities | 92.0 | % | |

Private Investments – Mezzanine Loans | 16.5 | % | |

Private Investments – Equity | 3.9 | % | |

Short-Term Investments | 6.8 | % | |

Liabilities in Excess of Other Assets | (19.2 | )% | |

100.0 | % | ||

See accompanying notes which are an integral part of these financial statements.

12

Assets: |

|

| ||

Investments in Securities at Market Value (cost $113,911,333) | $ | 112,410,900 |

| |

Receivable for Fund Shares Sold |

| 204,810 |

| |

Dividends and Interest Receivable |

| 727,985 |

| |

Due from Advisor |

| 62,440 |

| |

Prepaid Expenses and Other Assets |

| 64,461 |

| |

Total Assets |

| 113,470,596 |

| |

|

| |||

Liabilities: |

|

| ||

Payable for Securities Sold Under Agreements to Repurchase (proceeds $18,049,000) | $ | 18,049,000 |

| |

Payable for Investment Securities Purchased |

| 54,303 |

| |

Shareholder Servicing Fees Payable – Class I (Note 3) |

| 3,461 |

| |

Distribution Payable |

| 649,741 |

| |

Loan Interest Reserve |

| 24,902 |

| |

Reverse Repurchase Interest Payable |

| 119,579 |

| |

Subscriptions Received in Advance |

| 1,000 |

| |

Accrued Expenses and Other Liabilities |

| 300,407 |

| |

Total Liabilities |

| 19,202,393 |

| |

Commitments and Contingencies (Note 10) |

|

| ||

Net Assets | $ | 94,268,203 |

| |

|

| |||

Components of Net Assets: |

|

| ||

Paid-in Capital (no par value; unlimited shares authorized) | $ | 96,552,463 |

| |

Total Accumulated Deficit |

| (2,284,260 | ) | |

Net Assets | $ | 94,268,203 |

| |

|

| |||

Net Asset Value Per Share |

|

| ||

Founders Shares: |

|

| ||

Net Assets | $ | 76,903,521 |

| |

Shares of Beneficial Interest Outstanding |

| 8,212,519 |

| |

Net Asset Value and Redemption Price per Share | $ | 9.36 |

| |

|

| |||

Class I Shares: |

|

| ||

Net Assets | $ | 17,364,682 |

| |

Shares of Beneficial Interest Outstanding |

| 1,854,692 |

| |

Net Asset Value and Redemption Price per Share | $ | 9.36 |

|

See accompanying notes which are an integral part of these financial statements.

13

Investment Income: |

|

| ||

Interest Income | $ | 9,211,942 | (1) | |

Dividend Income |

| 97,486 |

| |

Total Investment Income |

| 9,309,428 |

| |

|

| |||

Expenses: |

|

| ||

Interest Expense from Reverse Repurchase Agreements |

| 1,037,959 |

| |

Investment Advisory Fees |

| 1,016,398 |

| |

Legal Fees |

| 759,212 |

| |

Audit and Tax Fees |

| 155,790 |

| |

Chief Compliance Officer and Principal Financial Officer Fees |

| 120,000 |

| |

Trustees’ Fees |

| 105,000 |

| |

Administration Fees |

| 103,332 |

| |

Other Expenses |

| 65,358 |

| |

Registration Fees |

| 62,543 |

| |

Transfer Agent Fees |

| 58,398 |

| |

Pricing Fees |

| 48,673 |

| |

Insurance Fees |

| 39,696 |

| |

Shareholder Reporting Fees |

| 24,813 |

| |

Custody Fees |

| 13,505 |

| |

Shareholder Servicing Fees – Class I (Note 3) |

| 5,807 |

| |

Total Expenses |

| 3,616,484 |

| |

Expenses Waived by Adviser |

| (1,016,398 | ) | |

Expenses Reimbursed by Adviser |

| (344,143 | ) | |

Net Expenses |

| 2,255,943 |

| |

Net Investment Income |

| 7,053,485 |

| |

|

| |||

Realized and Unrealized Gain (Loss) on Investments: |

|

| ||

Net Realized Loss from Investments |

| (328,731 | ) | |

Net Change in Unrealized Appreciation on Investments |

| 1,317,798 |

| |

Net Realized and Unrealized Gain |

| 989,067 |

| |

|

| |||

Net Increase in Net Assets Resulting From Operations | $ | 8,042,552 |

|

____________

(1) Includes paid-in kind interest of $1,303,646.

See accompanying notes which are an integral part of these financial statements.

14

For the | For the | |||||||

Increase (Decrease) in Net Assets from: |

|

|

|

| ||||

Operations: |

|

|

|

| ||||

Net Investment Income | $ | 7,053,485 |

| $ | 4,433,423 |

| ||

Net Realized Loss from Investments |

| (328,731 | ) |

| (542,132 | ) | ||

Net Change in Unrealized Appreciation (Depreciation) on Investments |

| 1,317,798 |

|

| (3,660,820 | ) | ||

Net Increase in Net Assets Resulting From Operations |

| 8,042,552 |

|

| 230,471 |

| ||

|

|

|

| |||||

Distributions to Shareholders: |

|

|

|

| ||||

Distributions: |

|

|

|

| ||||

Founders Shares |

| (5,895,691 | ) |

| (4,452,726 | ) | ||

Class I Shares(1) |

| (568,794 | ) |

| — |

| ||

Total Distributions to Shareholders |

| (6,464,485 | ) |

| (4,452,726 | ) | ||

|

|

|

| |||||

Beneficial Interest Transactions: |

|

|

|

| ||||

Proceeds From Shares Issued: |

|

|

|

| ||||

Founders Shares |

| 24,826,189 |

|

| 7,868,186 |

| ||

Class I Shares(1) |

| 24,919,076 |

|

| — |

| ||

Distributions Reinvested: |

|

|

|

| ||||

Founders Shares |

| 981,995 |

|

| 554,671 |

| ||

Class I Shares(1) |

| 55,835 |

|

| — |

| ||

Redemptions: |

|

|

|

| ||||

Founders Shares |

| (6,823,712 | ) |

| (5,357,196 | ) | ||

Class I Shares(1) |

| (7,791,529 | ) |

| — |

| ||

Net Increase From Beneficial Interest Transactions |

| 36,167,854 |

|

| 3,065,661 |

| ||

|

|

|

| |||||

Total Increase (Decrease) In Net Assets |

| 37,745,921 |

|

| (1,156,594 | ) | ||

|

|

|

| |||||

Net Assets: |

|

|

|

| ||||

Beginning of Period |

| 56,522,282 |

|

| 57,678,876 |

| ||

End of Period | $ | 94,268,203 |

| $ | 56,522,282 |

| ||

|

|

|

| |||||

Share Activity: |

|

|

|

| ||||

Shares Sold: |

|

|

|

| ||||

Founders Shares |

| 2,666,660 |

|

| 825,908 |

| ||

Class I Shares(1) |

| 2,684,129 |

|

| — |

| ||

Shares Reinvested: |

|

|

|

| ||||

Founders Shares |

| 106,301 |

|

| 59,129 |

| ||

Class I Shares(1) |

| 6,004 |

|

| — |

| ||

Shares Redeemed: |

|

|

|

| ||||

Founders Shares |

| (734,324 | ) |

| (574,883 | ) | ||

Class I Shares(1) |

| (835,441 | ) |

| — |

| ||

|

|

|

| |||||

Net Increase in Shares of Beneficial Interest Outstanding |

| 3,893,329 |

|

| 310,154 |

| ||

____________

(1) Reflects operations for the period from February 22, 2023 (commencement of operations) to December 31, 2023.

See accompanying notes which are an integral part of these financial statements.

15

Increase/(Decrease) in Cash: |

|

| ||

Cash Flows Provided by (Used in) Operating Activities: |

|

| ||

Net Increase in Net Assets Resulting from Operations | $ | 8,042,552 |

| |

Adjustments to Reconcile Net Increase (Decrease) in Net Assets Resulting from Operations to Net Cash Provided by (Used in) Operating Activities: |

|

| ||

Purchases of Long-Term Portfolio Investments |

| (64,144,898 | ) | |

Proceeds from Sales of Long-Term Portfolio Investments |

| 26,541,852 |

| |

Purchases of Short-Term Investments, Net |

| (1,303,178 | ) | |

Change in Unrealized Appreciation on Investments |

| (1,317,798 | ) | |

Net Realized Loss on Investments |

| 328,731 |

| |

Net Amortization on Investments |

| (134,707 | ) | |

Return of Capital Distributions Received |

| 109,269 |

| |

Payment In Kind Interest |

| (1,303,646 | ) | |

Loan Origination Proceeds |

| 52,100 |

| |

Net Paydown Gains |

| (346,231 | ) | |

Decrease in Due from Advisor Receivable |

| 213,993 |

| |

Increase in Dividends and Interest Receivable |

| (330,451 | ) | |

Increase in Prepaid Expenses and Other Assets |

| (8,904 | ) | |

Increase in Shareholder Servicing Fees Payable |

| 3,461 |

| |

Increase in Reverse Repurchase Interest Payable |

| 34,640 |

| |

Decrease in Loan Interest Reserve |

| (316,601 | ) | |

Increase in Accrued Expenses and Other Liabilities |

| 57,232 |

| |

Net Cash Used in Operating Activities |

| (33,822,584 | ) | |

|

| |||

Cash Flows Provided by (Used in) Financing Activities: |

|

| ||

Proceeds from Sales of Shares and Change in Receivable for Fund Shares Sold and Payable for Subscriptions Received in Advance |

| 49,539,455 |

| |

Payment for Redemption of Shares |

| (14,615,241 | ) | |

Dividends Paid to Shareholders, Net of Reinvestments and Change in Distribution Payable |

| (5,205,830 | ) | |

Proceeds from Reverse Repurchase Agreements |

| 111,890,000 |

| |

Sales from Reverse Repurchase Agreements |

| (107,795,000 | ) | |

Net Cash Provided by Financing Activities |

| 33,813,384 |

| |

|

| |||

Net Decrease in Cash |

| (9,200 | ) | |

|

| |||

Beginning Cash Balance |

| 9,200 |

| |

|

| |||

Ending Cash Balance | $ | — |

| |

|

| |||

Supplemental Non-Cash Information: |

|

| ||

Interest Paid | $ | 1,003,319 |

| |

Reinvested Dividends | $ | 1,037,830 |

|

See accompanying notes which are an integral part of these financial statements.

16

Per share operating performance.

For a capital share outstanding throughout each period.

For the | For the Period | |||||||||||

December 31, | December 31, | |||||||||||

Net Asset Value, Beginning of Period | $ | 9.16 |

| $ | 9.84 |

| $ | 10.00 |

| |||

|

|

|

|

|

| |||||||

From Operations: |

|

|

|

|

|

| ||||||

Net Investment Income(2) |

| 0.96 |

|

| 0.72 |

|

| 0.27 |

| |||

Net Realized and Unrealized Gain (Loss) on Investments |

| 0.11 |

|

| (0.68 | ) |

| 0.10 |

| |||

Total From Operations |

| 1.07 |

|

| 0.04 |

|

| 0.37 |

| |||

|

|

|

|

|

| |||||||

Less Distributions: |

|

|

|

|

|

| ||||||

Net Investment Income |

| (0.87 | ) |

| (0.72 | ) |

| (0.40 | ) | |||

Net Realized Gains |

| — |

|

| — |

|

| (0.13 | ) | |||

Total Distributions |

| (0.87 | ) |

| (0.72 | ) |

| (0.53 | ) | |||

|

|

|

|

|

| |||||||

Net Asset Value, End of Period | $ | 9.36 |

| $ | 9.16 |

| $ | 9.84 |

| |||

|

|

|

|

|

| |||||||

Total Return(4) |

| 12.24 | % |

| 0.46 | % |

| 3.70 | %(3) | |||

|

|

|

|

|

| |||||||

Ratios and Supplemental Data: |

|

|

|

|

|

| ||||||

Net assets, end of period (in 000’s) | $ | 76,904 |

| $ | 56,522 |

| $ | 57,679 |

| |||

|

|

|

|

|

| |||||||

Including interest expense: |

|

|

|

|

|

| ||||||

Ratio of gross expenses to average net assets |

| 5.33 | % |

| 4.98 | % |

| 4.18 | %(5) | |||

Ratio of net expenses to average net assets |

| 3.33 | % |

| 2.93 | % |

| 2.55 | %(5) | |||

Ratio of net investment income to average net assets |

| 10.40 | % |

| 7.55 | % |

| 3.94 | %(5) | |||

Excluding interest expense: |

|

|

|

|

|

| ||||||

Ratio of gross expenses to average net assets |

| 3.80 | % |

| 4.19 | % |

| 3.88 | %(5) | |||

Ratio of net expenses to average net assets(6) |

| 1.80 | % |

| 2.14 | % |

| 2.25 | %(5) | |||

Ratio of net investment income to average net assets |

| 11.93 | % |

| 8.34 | % |

| 4.24 | %(5) | |||

Portfolio turnover rate |

| 34 | % |

| 30 | % |

| 49 | %(3) | |||

____________

(1) The Fund commenced operations April 16, 2021.

(2) Based on average shares outstanding for the period.

(3) Not annualized for periods of less than one year.

(4) Total returns are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distributions, if any, and excludes the effect of sales charges. Had the Adviser not waived expenses, total returns would have been lower.

(5) Annualized.

(6) Effective September 29, 2022, the share expense cap was changed from 2.25% to 1.80% of average net assets.

See accompanying notes which are an integral part of these financial statements.

17

FORUM REAL ESTATE INCOME FUND Class I Shares |

Per share operating performance.

For a capital share outstanding throughout each period.

For the Period | ||||

Net Asset Value, Beginning of Period | $ | 9.38 |

| |

|

| |||

From Operations: |

|

| ||

Net Investment Income(2) |

| 0.83 |

| |

Net Realized and Unrealized Loss |

| (0.05 | ) | |

Total From Operations |

| 0.78 |

| |

|

| |||

Less Distributions: |

|

| ||

Net Investment Income |

| (0.80 | ) | |

Total Distributions |

| (0.80 | ) | |

|

| |||

Net Asset Value, End of Period | $ | 9.36 |

| |

|

| |||

Total Return(3),(4) |

| 8.76 | % | |

Ratios and Supplemental Data: |

|

| ||

Net assets, end of period (in 000’s) | $ | 17,365 |

| |

|

| |||

Including interest expense: |

|

| ||

Ratio of gross expenses to average net assets(5) |

| 5.43 | % | |

Ratio of net expenses to average net assets(5) |

| 3.43 | % | |

Ratio of net investment income to average net assets(5) |

| 10.48 | % | |

Excluding interest expense: |

|

| ||

Ratio of gross expenses to average net assets(5) |

| 3.90 | % | |

Ratio of net expenses to average net assets(5) |

| 1.90 | % | |

Ratio of net investment income to average net assets(5) |

| 12.01 | % | |

Portfolio turnover rate(3) |

| 34 | % | |

____________

(1) Reflects operations for the period from February 22, 2023 (commencement of operations) to December 31, 2023.

(2) Based on average shares outstanding for the period.

(3) Not annualized for periods of less than one year.

(4) Total returns are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distributions, if any, and excludes the effect of sales charges. Had the Adviser not waived expenses, total returns would have been lower.

(5) Annualized.

See accompanying notes which are an integral part of these financial statements.

18

1. ORGANIZATION

Forum Real Estate Income Fund (the “Fund”) was organized as a Delaware statutory trust on April 5, 2021, and is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as a non-diversified closed-end management investment company. The Fund operates as an interval fund pursuant to Rule 23c-3 under the 1940 Act. The primary investment objectives of the Fund are to maximize current income and preserve investor capital, with a secondary focus on long-term capital appreciation. The Fund offers three classes of shares: Founders Shares, which commenced operations on April 16, 2021; Class I Shares, which commenced operations on February 22, 2023; and Class W, which is not currently available for purchase. Forum Capital Advisors LLC, an investment adviser registered under the Investment Advisers Act of 1940 (the “Advisers Act”), as amended, serves as the Fund’s investment adviser (the “Adviser”). Janus Henderson Investors US LLC (“Janus”), an investment adviser registered under the Advisers Act, serves as the Sub-Adviser to the Fund.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The following is a summary of significant accounting policies followed by the Fund in preparation of its financial statements. These policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”). The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates. The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standard Codification (“ASC”) Topic 946 “Financial Services — Investment Companies”.

Securities Valuation — Common and preferred equity securities listed on an exchange are valued at the last reported sale price at the close of the regular trading session of the primary exchange on the business day the value is being determined. Fixed-income securities, having a remaining maturity of greater than 60 days, are typically valued at the evaluated prices formulated by an independent pricing service. Each security type has a primary and secondary pricing source. If neither the primary nor any secondary pricing source can provide a price or logic to determine a price, the Valuation Designee (as defined below) will provide a fair value price for the security.

Fair Valuation Process — The 1940 Act requires a fund to value its portfolio investments using the market value of its portfolio securities when market quotations are “readily available” and, when a market quotation is not readily available or if the investment is not a security, by using the investment’s fair value as determined in good faith by the fund’s board. The Board of Trustees (“Board”) of the Fund has designated the Adviser to manage and implement the day-to-day valuation of the Fund’s portfolio investments, in accordance with the Fund’s valuation policies and procedures. In addition, pursuant to Rule 2a-5 under the 1940 Act, the Board has designated the Adviser as the “valuation designee” (“Valuation Designee”) to make fair value determinations for all of the Fund’s investments for which market quotations are not readily available. The Valuation Designee has established a Valuation Committee, which assists in carrying out the valuation of Fund holdings and performs fair value determinations pursuant to the standards and procedures set forth in such policies and procedures. The Valuation Designee may consult with the Fund’s outside legal counsel or other third-party consultants in their discussions and deliberations. Due to the inherent uncertainties of valuation, certain estimated fair values may differ significantly from the values that would have been realized had a ready market for these investments existed, and these differences could be material.

19

FORUM REAL ESTATE INCOME FUND December 31, 2023 |

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES – (Continued) |

Fund investments are valued in accordance with ASC Topic 820, Fair Value Measurements and Disclosure (“ASC Topic 820”), issued by the FASB, which defines fair value as the amount that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the applicable measurement date.

Investments that are listed or traded on an exchange and are freely transferrable, such as interests in public REITS or certain short-term investments, are Level 1 securities and valued at the closing price on the principal exchange on which the investment is listed or traded. Other investments for which market quotations are readily available will be valued using end-of-day pricing quotes obtained from an independent third-party fixed income pricing service on a daily basis.

Certain investments, such as CMBS, that are publicly traded but for which no readily available market quotations exist, are generally valued on the basis of information furnished by an independent pricing service that uses a valuation matrix which incorporates both dealer-supplied valuations and electronic data processing techniques. Such investments are classified as Level 2 securities. To assess the continuing appropriateness of pricing sources and methodologies, the Adviser regularly performs price verification procedures and issues challenges as necessary to independent pricing services, and any differences are reviewed in accordance with the valuation procedures. The Valuation Designee will utilize a number of factors to determine if the quotations are representative of fair value, including through comparison of prices to multiple sources and monitoring of significant valuation events. The Sub-Adviser may also provide relevant information to the Adviser in its capacity as Valuation Designee.

Securities that are not publicly traded or whose market prices are not readily available, as will be the case for a substantial portion of Private Mezzanine Loans and direct real estate investments, will initially be valued at acquisition cost until a fair value is determined by the Adviser in good faith pursuant to the policies adopted by the Adviser and approved by the Board, based on, among other things, the input of the Adviser and independent valuation firm(s) engaged to review the Fund’s investments. Such investments are classified as Level 3 securities. The Adviser and independent valuation firm(s) will use a variety of approaches to establish the fair value of these investments in good faith. The approaches used will generally include widely recognized and utilized valuation approaches and methodologies, including an analysis of discounted cash flows, comparable credit spreads, publicly traded comparable companies and comparable transactions and will also consider recent transaction prices and other factors in the valuation. An independent, third-party valuation firm will generally review all of the Fund’s Level 3 investments on a semi-annual basis. In the interim between third-party evaluations, the Adviser monitors these investments on a daily basis and the Valuation Committee reviews each Level 3 investment on a monthly basis as set forth in the procedures adopted by Adviser and approved by the Board.

The Valuation Designee provides the Board with reports on a quarterly basis, or more frequently if necessary, identifying valuation activity with respect to Level 1, Level 2, and Level 3 holdings in the Fund’s portfolio. Fair value determinations are based upon all available inputs that the Valuation Designee deems relevant, which may include indicative dealer quotes, values of like securities, recent portfolio company financial statements and forecasts for the investment, and valuations prepared by independent valuation firms.

20

FORUM REAL ESTATE INCOME FUND December 31, 2023 |

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES – (Continued) |

U.S. GAAP establishes a single authoritative definition of fair value, sets out a framework for measuring fair value and requires additional disclosures about fair value measurement. GAAP establishes a hierarchy that prioritizes inputs to valuation methods. The three levels of input are:

Level 1 — Unadjusted quoted prices in active markets for identical and/or similar assets and liabilities that the Fund has the ability to access at the measurement date.

Level 2 — Other significant observable inputs other than quoted prices included in Level 1 for the asset or liability, either directly or indirectly. These inputs may include quoted prices for similar investments or identical investments in an active market, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data.

Level 3 — Significant unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Fund’s own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available.

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

The inputs or methodology used for valuing investments are not necessarily an indication of the risk associated with investing in those investments. The following tables summarize the inputs used as of December 31, 2023, for the Fund’s assets and liabilities measured at fair value:

Assets | Level 1 | Level 2 | Level 3 | Total | ||||||||

Private Investments – Equity | $ | — | $ | — | $ | 3,665,976 | $ | 3,665,976 | ||||

Private Investments – Mezzanine Loans |

| — |

| — |

| 15,581,372 |

| 15,581,372 | ||||

Commercial Mortgage Backed Securities |

| — |

| 86,763,474 |

| — |

| 86,763,474 | ||||

Short-Term Investments |

| 6,400,078 |

| — |

| — |

| 6,400,078 | ||||

$ | 6,400,078 | $ | 86,763,474 | $ | 19,247,348 | $ | 112,410,900 | |||||

Liabilities | Level 1 | Level 2 | Level 3 | Total | ||||||||

Reverse Repurchase Agreements | $ | — | $ | 18,049,000 | $ | — | $ | 18,049,000 | ||||

$ | — | $ | 18,049,000 | $ | — | $ | 18,049,000 | |||||

There were no transfers between levels during the current period presented. It is the Fund’s policy to record transfers into or out of levels at the end of the reporting period.

21

FORUM REAL ESTATE INCOME FUND December 31, 2023 |

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES – (Continued) |

The following table summarizes the valuation techniques and significant unobservable inputs used for the Fund’s investments that are categorized in Level 3 of the fair value hierarchy as of December 31, 2023:

Level 3 Investments | Fair Value | Valuation | Unobservable | Range of | Impact to | ||||||

Private Investments – Equity | $ | 2,665,976 | Market Yield Analysis | Selected Market Spreads | 12.00% to 12.25%/12.09% | Decrease | |||||

Private Investments – Mezzanine Loans |

| 15,581,372 | Market Yield Analysis | Selected Market Spreads | 10.35% to 12.50%/11.89% | Decrease | |||||

Total Level 3 Investments | $ | 18,247,348 | |||||||||

Certain of the Fund’s Level 3 investments in “Private Investments — Equity” have been valued using unadjusted inputs that have not been internally developed by the Fund, including indicative broker quotations. As a result, fair value assets of $1,000,000 have been excluded from the preceding table.

The following is a reconciliation of assets in which Level 3 inputs were used in determining value:

Beginning | Transfers | Transfers | Purchases | Sales | Net | Accretion of | Return of Capital | Change in net | Ending | ||||||||||||||||||||||||

Private Investments – Equity | $ | 2,859,814 | $ | — | $ | — | $ | 1,795,734 | $ | (874,942 | ) | $ | — | $ | 6,672 | $ | (86,815 | ) | $ | (34,487 | ) | $ | 3,665,976 | ||||||||||

Private Investments – Mezzanine Loans |

| 21,446,217 |

| — |

| — |

| 2,259,101 |

| (8,107,673 | ) |

| — |

| 3,712 |

| (22,454 | ) |

| 2,469 |

|

| 15,581,372 | ||||||||||

$ | 24,306,031 | $ | — | $ | — | $ | 4,054,835 | $ | (8,982,615 | ) | $ | — | $ | 10,384 | $ | (109,269 | ) | $ | (32,018 | ) | $ | 19,247,348 | |||||||||||

The total change in unrealized appreciation included in the Statement of Operations attributable to Level 3 investments still held on December 31, 2023 is $40,775.

Payable for securities sold under agreements to repurchase — The Fund may use leverage to provide additional funds to support its investment activities. The Fund primarily intends to enter into financing transactions using reverse repurchase agreements. A reverse repurchase agreement involves the purchase of a security by the Fund and a simultaneous agreement by the seller (generally a bank or dealer) to repurchase the security from the Fund at a specified date or upon demand. This technique offers a method of earning income on idle cash. These securities involve the risk that the seller will fail to repurchase the security, as agreed. In that case, the Fund will bear the risk of market value fluctuations until the security can be sold and may encounter delays and incur costs in liquidating the security.

If a reverse repurchase agreement counterparty defaults, the Fund may suffer time delays and incur costs or possible losses in connection with the disposition of the securities underlying the reverse repurchase agreement. In the event of a default, instead of the contractual fixed rate of return, the rate of return to the Fund will depend on intervening fluctuations of the market values of the underlying securities and the accrued interest thereon. In such an event, the Fund would have rights against the counterparty for breach of contract with respect to any losses resulting from those market fluctuations.

22

FORUM REAL ESTATE INCOME FUND December 31, 2023 |

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES – (Continued) |

Reverse Repurchase agreements outstanding as of December 31, 2023 were as follows:

Reverse Repurchase Agreements | ||||||||||||||||||

Remaining Contractual Maturity of the Agreements | ||||||||||||||||||

Counterparty | Overnight | Up to | 30-90 | Greater | Total | Rate | ||||||||||||

Lucid Management |

|

|

|

|

|

| ||||||||||||

Asset backed securities | $ | — | $ | 2,218,000 | $ | — | $ | — | $ | 2,218,000 | 6.86 | % | ||||||

Asset backed securities |

| — |

| 3,224,000 |

| — |

| — |

| 3,224,000 | 6.82 | % | ||||||

Asset backed securities |

| — |

| 1,646,000 |

| — |

| — |

| 1,646,000 | 6.99 | % | ||||||

Royal Bank of Canada |

|

|

|

|

|

| ||||||||||||

Asset backed securities |

| — |

| — |

| 1,248,000 |

| — |

| 1,248,000 | 7.45 | % | ||||||

Asset backed securities |

| — |

| — |

| 2,055,000 |

| — |

| 2,055,000 | 7.20 | % | ||||||

Asset backed securities |

| — |

| — |

| — |

| 2,931,000 |

| 2,931,000 | 6.84 | % | ||||||

Asset backed securities |

| — |

| — |

| 1,981,000 |

| — |

| 1,981,000 | 7.10 | % | ||||||

Asset backed securities |

| — |

| — |

| 2,746,000 |

| — |

| 2,746,000 | 7.35 | % | ||||||

Total repurchase agreements | $ | — | $ | 7,088,000 | $ | 8,030,000 | $ | 2,931,000 | $ | 18,049,000 |

| |||||||

Cash and Cash Equivalents — Cash and cash equivalents include cash and overnight investments in interest-bearing demand deposits with a financial institution with maturities of three months or less. The Fund maintains deposits with a high quality financial institution in an amount that is in excess of federally insured limits.

Security Transactions and Investment Income — Investment security transactions are accounted for on a trade date basis. Cost is determined and gains and losses are based upon the specific identification method for both financial statement and federal income tax purposes. Interest income is recorded on the accrual basis. Purchase discounts and premiums on securities are accreted and amortized over the life of the respective securities using the effective interest method. The Fund elected not to measure an allowance for credit losses for accrued interest receivables. Interest is not accrued and interest receivable is written off when deemed uncollectible.

Loan origination income is charged to the borrowers during loan originations. This income is received at the time of closing and then deferred to be recognized as non-interest income over the term of the loan. For the year ended December 31, 2023, the Fund earned loan origination income of $8,740 and has $43,360 of unearned loan origination income. Earned loan origination income is included in the Interest Income amount in the Statement of Operations.

Federal Income Taxes — The Fund has elected to be taxed as a REIT. The Fund’s qualification and taxation as a REIT depend upon the Fund’s ability to meet on a continuing basis, through actual operating results, certain qualification tests set forth in the U.S. federal tax laws. Those qualification tests involve the percentage of income that the Fund earns from specified sources, the percentage of the Fund’s assets that falls within specified categories, the diversity of the ownership of the Fund’s shares, and the percentage of the Fund’s taxable income that the Fund distributes. No assurance can be given that the Fund will in fact satisfy such requirements for any taxable year. If the Fund qualifies as a REIT, the Fund generally will be allowed to deduct dividends paid to shareholders and, as a result, the Fund generally will not be subject to U.S. federal income tax on that portion of the Fund’s ordinary income and net capital gain that the Fund annually distributes to shareholders, as long as the Fund meets the minimum distribution requirements under the Code. The Fund intends to make distributions to shareholders on a regular basis as necessary to avoid material U.S. federal income tax and to comply with the REIT distribution requirements.

23

FORUM REAL ESTATE INCOME FUND December 31, 2023 |

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES – (Continued) |

Management has analyzed the Fund’s tax positions taken on income tax returns for all open tax years and has concluded that as of December 31, 2023, no provision for income tax is required in the Fund’s financial statements. The Fund’s federal and state income and federal excise tax returns for tax years for which the applicable statutes of limitations have not expired are subject to examination by the Internal Revenue Service and state departments of revenue. The Fund’s 2022 and 2023 tax years are open to examination as of December 31, 2023.

Reclassification — GAAP requires that certain components of net assets be reclassified to reflect permanent differences between financial and tax reporting. These reclassifications have no effect on net assets or net asset value per share.

Distribution to Shareholders — Distributions from net investment income of the Fund, if any, are declared and paid on a monthly basis. Distributions of net realized gains, if any, are declared annually. Distributions to shareholders of the Fund are recorded on the ex-dividend date and are determined in accordance with income tax regulations, which may differ from GAAP. For tax purposes, a distribution that for purposes of GAAP is composed of return of capital and net investment income may be subsequently re-characterized to also include capital gains. Shareholders will be informed of the tax characteristics of the distributions after the close of the 2023 fiscal year.

Indemnification — The Fund indemnifies its officers and Trustees for certain liabilities that may arise from the performance of their duties to the Fund. Additionally, in the normal course of business, the Fund enters into contracts that contain a variety of representations and warranties and which provide general indemnities. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred. However, management of the Fund expects the risk of loss due to these warranties and indemnities to be remote.

Recent Accounting Pronouncements — On June 30, 2022, the FASB issued ASU 2022-03, which (1) clarifies the guidance in ASC 820 on the fair value measurement of an equity security that is subject to a contractual sale restriction and (2) requires specific disclosures related to such an equity security. ASU 2022-03’s amendments are effective for annual periods beginning after December 15, 2023. Management is still considering the impact from adoption.

3. INVESTMENT ADVISORY AGREEMENT AND TRANSACTIONS WITH RELATED PARTIES

The business activities of the Fund are overseen by the Board, which is responsible for the overall management of the Fund.

During the reporting period, as compensation for its services, the Fund paid to the Adviser a monthly advisory fee at an annual rate of 1.50% of its average daily Net Assets. Janus acts as the Fund’s Sub-Adviser and assists the Adviser in identifying and evaluating potential investments for the Fund. Any additional sub-adviser chosen by the Investment Adviser will be paid by the Adviser based only on the portion of Fund assets allocated to any such sub-adviser by the Adviser. Janus is paid by the Adviser, and not by the Fund. For the year ended December 31, 2023, the Adviser earned advisory fees of $1,016,398.

The Adviser and the Fund have entered into an Expense Limitation Agreement (the “Agreement”) pursuant to which the Adviser has contractually agreed to waive its management fee and/or pay or reimburse the ordinary annual operating expenses of the Fund to the extent necessary to limit the Fund’s operating expenses to 2.05% of the Class W Shares average daily net assets, 1.90% of the Class I Shares average daily net assets, and 1.80% of the Founders Shares average daily net

24

FORUM REAL ESTATE INCOME FUND December 31, 2023 |

3. INVESTMENT ADVISORY AGREEMENT AND TRANSACTIONS WITH RELATED PARTIES – (Continued) |

assets. Ordinary operating expenses include organization and offering costs, but exclude brokerage commissions and other similar transactional expenses, interest (including interest incurred on borrowed funds and interest incurred in connection with bank and custody overdrafts), other borrowing costs and fees (including commitment fees), taxes, litigation and indemnification expenses, judgments, and extraordinary expenses.

The Adviser is entitled to seek reimbursement from the Fund of fees waived or expenses paid or reimbursed to the Fund under the Expense Limitation Agreement for a period ending three years after the date of the waiver, payment or reimbursement, subject to the limitation that a reimbursement will not cause a Class’s operating expenses (after giving effect to the reimbursement) to exceed the lesser of (a) the expense limitation amount in effect at the time such fees were waived or expenses paid or reimbursed, or (b) the expense limitation amount. During the year ended December 31, 2023, the Adviser waived expenses of $1,016,398 and reimbursed expenses of $344,143 and did not recoup any expenses.

As of December 31, 2023, the Adviser may seek recoupment for previously waived or reimbursed fees and expenses, subject to the limitations noted above, no later than the dates and in no greater amounts than as outlined below:

Date of Expiration | Amount | ||

December 31, 2026 | $ | 1,360,541 | |

December 31, 2025 | $ | 1,202,561 | |

December 31, 2024 | $ | 618,712 | |

The Fund has established a Shareholder Servicing Plan with respect to Class I Shares that allows the Fund to pay shareholder servicing fees to certain intermediaries with respect to Shareholders holding Class I Shares. Under the Shareholder Servicing Plan, the Fund may pay to qualified recipients up to 0.10% on an annualized basis of the aggregate net assets of the Fund attributable to Class I Shares (the “Shareholder Servicing Fee”). Because these fees are paid out of the Class I Shares’ assets on an ongoing basis, over time these fees will increase the cost of an investment in Class I Shares. Class W Shares and Founders Shares are not subject to the Shareholder Servicing Fee. During the year ended December 31, 2023, Class I Shareholders incurred $5,807 of Shareholder Servicing Fees subject to the Fund’s Shareholder Servicing Plan.

In addition, certain affiliates provide services to the Fund as follows:

Foreside Financial Services, LLC (”Distributor”) — Foreside acts as Distributor to the Fund on a best-efforts basis, subject to various conditions, pursuant to a Distribution Agreement (the “Distribution Agreement”) between the Fund and the Distributor. The Distributor may enter into agreements with selected broker-dealers, banks, or other financial intermediaries for distribution of shares of the Fund. For these services, the Distributor receives an annual fee from the Adviser. The Adviser and/or its affiliates may make payments to selected affiliated or unaffiliated third parties (including the parties who have entered into sub-distribution agreements with the Distributor) from time to time in connection with the sale of Shares and/or the services provided to common shareholders. These payments will be made by the Adviser and/or its affiliates and will not represent an additional charge to the Fund.

A Trustee and certain officers of the Fund are affiliated with the Adviser.

In consideration of the services rendered by those Trustees who are not “interested persons” (as defined in Section 2(a)(19) of the 1940 Act) of the Trust (“Independent Trustees”), the Fund pays each Independent Trustee an annual retainer in the amount of $35,000 payable quarterly. Trustees that are interested persons will not be compensated by the Fund. The Trustees do not receive any pension or retirement benefits.

25

FORUM REAL ESTATE INCOME FUND December 31, 2023 |

3. INVESTMENT ADVISORY AGREEMENT AND TRANSACTIONS WITH RELATED PARTIES – (Continued) |

Employees of PINE Advisor Solutions, LLC (“PINE”) serve as officers of the Fund. PINE receives a monthly fee for the services provided to the Fund. The Fund also reimburses PINE for certain out-of-pocket expenses incurred on the Fund’s behalf.

UMB Fund Services, Inc. (“UMBFS”) serves as the Fund’s fund accountant, transfer agent and administrator. UMB Bank, n.a., an affiliate of UMBFS, serves as the Fund’s custodian. The Fund’s allocated fees incurred for fund accounting, fund administration, transfer agency and custody services are reported on the Statement of Operations.

4. INVESTMENT TRANSACTIONS

The cost of purchases including payment of interest in-kind and proceeds from sales and paydowns of investment securities, other than U.S. Government securities and short-term investments, for the year ended December 31, 2023, amounted to $65,398,646 and $26,294,878, respectively.

From time to time, the Fund may co-invest with other investment vehicles managed by the Fund’s Adviser or its affiliates, including by means of splitting loans, participating in loans or other means of syndicating loans. The Fund is not obligated to provide, nor has it provided, any financial support to the other managed investment vehicles. As such, the Fund’s risk is limited to the reported fair value of its investment in any such loan. As of December 31, 2023, there was one co-invested loan held by the Fund and an affiliate of the Fund.

5. RESTRICTED SECURITIES

Restricted securities include securities that have not been registered under the Securities Act of 1933, as amended, and securities that are subject to restrictions on resale. The Fund may invest in restricted securities that are consistent with the Fund’s investment objective and investment strategies. Investments in restricted securities are valued at net asset value as a practical expedient for fair value, or fair value as determined in good faith in accordance with procedures adopted by the Board. It is possible that the estimated value may differ significantly from the amount that might ultimately be realized in the near term, and the difference could be material.

As of December 31, 2023, the Fund invested in the following restricted securities:

Original | Principal/ | Cost | Value | % of | Unfunded | |||||||||||

Advantis MCA FV, LLC | 7/22/2022 | 267,489 | $ | 260,687 | $ | 267,489 | 0.3 | % | $ | 967,660 | ||||||

Advantis MCA Harbor, LLC | 10/18/2022 | 148,623 |

| 141,521 |

| 148,623 | 0.2 | % |

| 993,334 | ||||||

CRIMSON Devco, LLC | 12/17/2021 | 40 |

| 1,000,000 |

| 1,000,000 | 1.1 | % |

| — | ||||||

FCREIF Nimbus Everett | 8/31/2021 | 2,220,009 |

| 2,214,459 |

| 2,188,753 | 2.3 | % |

| — | ||||||

FCREIF Van Ness | 10/13/2021 | 2,521,552 |

| 2,521,552 |

| 2,498,359 | 2.6 | % |

| — | ||||||

IOTA Multifamily Development | 3/31/2022 | 969,784 |

| 967,255 |

| 930,864 | 1.0 | % |

| 31,626 | ||||||

Lexington So Totowa, LLC | 5/20/2022 | 1,520,000 |

| 1,509,900 |

| 1,520,000 | 1.6 | % |

| — | ||||||

Royal Urban Renewal, LLC | 9/29/2021 | 4,813,784 |

| 4,813,784 |

| 4,739,772 | 5.0 | % |

| 81,584 | ||||||

Trent Development – Kerf Apartments Loan | 9/23/2021 | 3,164,177 |

| 3,164,177 |

| 3,116,860 | 3.3 | % |

| — | ||||||

West University Gainesville Mezz, LLC | 5/18/2022 | 1,101,516 |

| 1,101,516 |

| 1,101,516 | 1.2 | % |

| 128,484 | ||||||

Zephyr Preferred Equity | 6/15/2023 | 1,735,112 |

| 1,688,041 |

| 1,735,112 | 1.8 | % |

| 3,525,164 | ||||||

18,462,086 | $ | 19,382,892 | $ | 19,247,348 | 20.4 | % | $ | 5,727,852 | ||||||||

26

FORUM REAL ESTATE INCOME FUND December 31, 2023 |

6. AGGREGATE UNREALIZED APPRECIATION AND DEPRECIATION

The Statement of Assets and Liabilities represents cost for financial reporting purposes. Aggregate cost for federal tax purposes is $113,911,333 and differs from fair value by net unrealized appreciation (depreciation) of securities as follows:

Unrealized Appreciation | $ | 966,819 |

| |

Unrealized Depreciation |