UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 1-K

ANNUAL REPORT

PURSUANT TO REGULATION A OF THE SECURITIES ACT OF 1933

For the fiscal year ended April 30, 2023

reAlpha Tech Corp.

(Exact name of registrant as specified in its charter)

| Delaware | 86-3425507 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

6515 Longshore Loop, Suite 100

Dublin, OH 43017

(Full mailing address of principal executive offices)

+1-707-732-5742

(Issuer’s telephone number, including area code)

Common Stock, par value $.001

(Title of each class of securities issued pursuant to Regulation A)

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

The information contained in this Annual Report on Form 1-K (this “Form 1-K”) includes some statements that are not historical and that are considered “forward-looking statements.” Such forward-looking statements include but are not limited to, statements regarding our development plans for our business; our strategies and business outlook; anticipated development of our company, the property manager, each LLCs of our company; and various other matters (including contingent liabilities and obligations and changes in accounting policies, standards and interpretations). These forward-looking statements express the property manager’s expectations, hopes, beliefs, and intentions regarding the future. In addition, without limiting the foregoing, any statements that refer to projections, forecasts for other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipates,” “believes,” “continue,” “could,” “estimates,” “expects,” “intends,” “may,” “might,” “plans,” “possible,” “potential,” “predicts,” “projects,” “seeks,” “should,” “will,” “would” and similar expressions and variations, or comparable terminology, or the negatives of any of the foregoing, may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking.

You should thoroughly read this annual report and the documents that we refer to herein with the understanding that our actual future results may be materially different from and/or worse than what we expect. We qualify all of our forward-looking statements by these cautionary statements including those made in Risk Factors appearing elsewhere in this annual report. Other sections of this annual report include additional factors which could adversely impact our business and financial performance. New risk factors emerge from time to time and it is not possible for our management to predict all risk factors, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. Except for our ongoing obligations to disclose material information under the Federal securities laws, we undertake no obligation to release publicly any revisions to any forward-looking statements, to report events or to report the occurrence of unanticipated events. These forward-looking statements speak only as of the date of this annual report, and you should not rely on these statements without also considering the risks and uncertainties associated with these statements and our business.

All forward-looking statements attributable to us are expressly qualified in their entirety by these risks and uncertainties. These risks and uncertainties, along with others, are detailed under the headings “Risk Factors” in our registration statement on Form S-11 originally filed by the Company with the Securities and Exchange Commission on August 8, 2023, as may be amended, and in our subsequent period reports filed from time to time with the Commission. Should one or more of these risks or uncertainties materialize, or should any of the parties’ assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. You should not place undue reliance on any forward-looking statements and should not make an investment decision based solely on these forward-looking statements. We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

PART II

Item 1. Business

Company Overview – Our Mission

reAlpha Tech Corp. (Fka reAlpha Asset Management, Inc) is a Delaware corporation formed in April 2021 (“reAlpha” or the “Company”). We are a real estate technology company with a mission to develop, utilize and commercialize our artificial intelligence (“AI”) focused technology stack to empower retail investor participation in short-term rental properties..

We were founded on the belief that every person should have the access and the freedom to pursue wealth creation through real estate. However, we believe there are significant entry barriers for the average individual and that the lucrative returns are currently taken mainly by private equity firms and larger-scale developers. We intend to develop and buy technologies to democratize access to short-term rental investments. To support this goal, we are creating a new model for property ownership and real estate investment.

Our business model is built with technologies for analyzing and acquiring short-term rental properties that meet the Investment Criteria (as defined in the “Business” section of this prospectus) for syndication purposes, and which we call Target Properties. Once the Target Properties are acquired, they are prepared for rent and listed on short-term rental sites. Our technologies help us not only identify short-term viable properties , but also optimize their performance by generating listing descriptions using the surrounding attractions of the location, analyzing guest reviews in the area, and suggesting improvements. Once our technologies are fully developed and ready to be commercialized, we intend to make some of these technologies available for commercial use by other customers on a licensing fee basis, pay-per-use basis or other fee arrangements.

The Company plans to make Target Properties available to investors via the Company’s subsidiary, Roost Enterprises, Inc. (“Rhove”). Rhove will create and manage limited liability companies (each, a “Syndication LLC”) to syndicate one or more of the Target Properties through exempt offerings. Once the Syndication LLCs are in place, Rhove will launch exempted offerings to sell membership interests in such properties to investors, through the purchase of membership interests in the Syndication LLCs, pursuant to Regulation A or Regulation D, each as promulgated under the Securities Act of 1933, as amended (the “Securities Act”) (each, a “Syndication”). To further facilitate the investment process in the Syndication LLCs, the Company is currently working on the reAlpha App (hereafter referred to as the “reAlpha App,” “App” or “app”).

The membership interests will provide an ownership stake in a Syndication LLC and in turn in the Target Properties. We refer to such investors as Syndicate Members, who differ significantly to the holders of our common stock. To date, we have not yet developed a secondary trading market for equity interests in our Syndication LLCs. While the potential establishment of such a market is under consideration, no final decision has been made to implement a secondary trading market at this time.

Rights among Syndicate Members may vary among each other depending on the specific terms and conditions agreed to in the offering documents pursuant to which the holder becomes a Syndicate Member. By becoming a Syndicate Member, the holder will not acquire any rights to the Company’s common stock and, therefore, will not be entitled to vote, receive a dividend or exercise any other rights of a stockholder of the Company. Likewise, acquiring shares of common stock of the Company will not provide the stockholders the status of Syndicate Member. Both Syndicate Members and our stockholders will receive the same quarterly financial metric information of our listed properties through the reAlpha App and the reAlpha website, which will also be available to the general public without a login, concurrently with our consolidated quarterly results (as more fully described under “Segments - Platform Services” below). Syndicate members that have access to the reAlpha App will only receive personalized financial information respective to their individual holdings in each of our Syndications.

To implement our business model, we plan to acquire properties through the Rhove SBU (as defined above) that satisfy our Investment Criteria (as defined below) (the “Target Properties”). Then, if needed, we renovate the Target Properties, prepare them for rent, list them on short-term rental sites and arrange for the Target Properties to be managed, internally or through third-parties. We expect that in the future these investors will become Syndicate Members through the purchasing of membership interests in our Syndication LLCs. In addition to managing the property operations, whether internally or through third-parties, we will also manage the financial performance of the asset, such as evaluating if the after-repair value or appreciated value of the property is higher than the purchase price, or whether the property is ready to generate the expected profitability.

1

Once our business model is fully implemented, we expect that Syndicate Members will hold up to 100% ownership of the Syndication LLC, and we would generate revenue through fees from the reAlpha App. Further, we expect that our other technologies, including the reAlphaBRAIN, reAlphaHUMINT, BnBGPT, and future technologies, will generate revenue through licensing fees, usage fees and other fee arrangement methods that the Company will employ to capitalize on its developing technologies and platform.

We believe our business is hard to replicate, and provides innovative solutions to investors wishing to participate in the real estate investment market. For instance, the following table provides a few of the barriers to entry for investors in the real estate investment market, and how we intend to facilitate such process with our business model:

| The average person does not: | Proposed solution: | |

| Have access to wholesale real-estate market prices. | As a bulk buyer, we will have access to the wholesale real estate market, which most people do not even know exists. This includes a bulk portfolio acquisition strategy. | |

| Have the cash for a 25% down payment. | reAlpha has strategic partnerships with lending institutions, which will allow us to close on property acquisitions within two to three weeks rather than the two to three months customary period for property acquisitions. | |

| Have the time to buy, renovate and manage an investment property. | reAlpha, through the Rhove SBU, handles the acquisition, renovation, onboarding and property management. Syndicate Members never have to answer a guest or pick up a paintbrush. | |

| Want to deal with a complex mortgage process (personal guarantee, negotiation with lenders, personal credit checks). | reAlpha, through the Rhove SBU, eliminates the entire process for Syndicate Members. Syndicate Members will never need to give a personal guarantee and their credit will never be checked when financing directly through reAlpha. | |

| Qualification + Mortgage Lending Restrictions - Income determines how much an individual can leverage/borrow. | By fractionalizing the ownership process, we expect Syndicate Members can own a smaller percentage of a home or group of homes rather than covering an entire down payment and being required to go through loan qualification requirements required by lenders. |

Through these property acquisition investments, our goal is to obtain: (i) consistent cash flow from short-term tenants; (ii) long-term capital appreciation of our properties’ value after repair and/or renovations in appreciating markets; and (iii) favorable tax treatment of long-term capital gains.

To finance these property acquisition investments, we may engage in leverage financing to enhance total returns to our Syndicate Members and investors through a combination of senior financing on our real estate acquisitions, secured facilities, and capital markets financing transactions. We will seek to secure conservatively structured leverage that is long-term, non-recourse, non-mark-to-market financing to the extent obtainable on a cost-effective basis.

2

Segments

We operate in two reportable segments consisting of (i) platform services and (ii) rental business. Our platform services segment offers and develops AI-based products and services to customers in the real-estate industry, while our rental business focuses on purchasing properties for syndication, which process is powered by our platform services technologies, as further described below.

(i) Platform Services

Our platform services segment technologies include: (i) reAlpha BRAINTM, (ii) reAlpha App, (iii) reAlpha HUMINT, (iv) BnBGPT, and (v) myAlphie.

Both the Syndicate Members that have access to the reAlpha App, or our website, and holders of our common stock will have access to certain quarterly financial metrics of the Syndicated properties, including: (i) occupancy rates of the property; (ii) average daily rental rates of the property; and (iii) periodical information of each property, such as gross revenue, total expenses, net revenue, cash flows, and others. This information will be made available to both Syndicate Members and the general public through the reAlpha App, our website, which is available to holders of our common stock that are non-Syndicate Members, and upon release of our consolidated quarterly results via press release or other appropriate method. This feature is not yet developed, but we intend to make available such quarterly financial metrics in the fourth quarter of 2023 or later. Other personalized financial information that will be available only to Syndicate Members through our App and website, include their total shares owned in the Syndication LLC, expressed in dollar and percentage values, dividends paid under that specific Syndication LLC, based on that Syndicate Member’s ownership percentage, and others. Holders of our common stock will not have access to this personalized information available in the App, unless they are also Syndicate Members.

Further, the reAlpha BRAINTM technology will also provide the Company information about future properties that could become Target Properties for Syndication, provided they satisfy the Investment Criteria. These properties which will be “ranked” by our reAlpha Score, which would provide the property’s profitability potential. Although we have not yet generated revenues through the use and subscription of our technologies, we expect that once all of our technologies are fully operational, we will generate revenue through subscriptions of our technologies and fee based revenues from conducting Syndications on the reAlpha App .

reAlpha BRAIN’s analysis and data will allow us to not only identify properties with high short-term rental viability, but also optimize their performance by generating listing descriptions using the surrounding attractions of the location, analyzing guest reviews in the area, and suggesting improvement to the acquired properties that will be listed on the reAlpha App for Syndication. Once our technologies are fully developed and ready to be commercialized, we intend to make some of these technologies available for commercial use by other customers on a licensing fee basis, pay-per-use basis or other fee arrangements.

Each of our technologies and platforms are more fully described below.

3

reAlpha BRAINTM

reAlpha BRAINTM will bring machine learning (“ML”) and AI to the world of short-term rental investment. This platform will utilize a natural language processing (“NLP”) program to scan through large quantities of data regarding properties and ML algorithms to choose the properties that have higher than expected industry standard return on investment. For this, it will gather and integrate a variety of data relevant to the properties from multiple sources including wholesalers, various multiple listing service (“MLS”) data sources, realtors, small Airbnb “mom and pop” operators, and other larger property owners. For instance, it will collect data on the properties’ price, house structure and sale history from different MLS’ listings in the U.S. This data, combined with the information about the neighborhood appeal, accessibility and safety of the neighborhood surrounding the properties enables the algorithm to learn the hidden patterns underlying high return short-term rental investments. This will allow reAlpha to predict how likely a particular property will generate expected profitability. The platform will convey this knowledge by assigning each property with a “reAlpha Score” ranging from 0-100. The higher the value, the more favorable a property is for investment.

Currently, the process of analyzing a property as a potential investment typically begins with an email received from a real-estate agent’s distribution list to which reAlpha has subscribed. However, we use multiple other sources outside of inbound emails to identify properties, including, but not limited to, MLS, proprietary data sellers such as AirDNA, and others. In the email scenario, the reAlpha BRAINTM will include an AI email parser based on NLP that looks for the property of concern within the unstructured email and extracts its street address. This address will then be used to query various data providers for a detailed description of the property’s structure, neighborhood and finances. This ML model, which is being built and will be hosted on the Amazon Sagemaker platform provided by Amazon Web Services (“AWS”), will then calculate the reAlpha Score for that property.

The model will also continuously improve and learn over time. As the Company makes its decision to invest in properties, the model will check the effectiveness of its recommendations to reduce false positives and false negatives. As of May 2023, the reAlpha BRAINTM has analyzed over 1,500,000 homes. We have halted further analysis by reAlpha BRAIN until the effectiveness of this registration statement.

reAlpha BRAINTM is currently operational internally within reAlpha. However, new developments on the AI system are expected to improve its accuracy. reAlpha BRAINTM is expected to be released publicly for commercial use in the second quarter of 2024 on a licensing fee basis.

reAlpha App (Trademarked as reAlpha M3TM)

The reAlpha App was designed to support our mission to make real estate ownership accessible and user friendly. The reAlpha App allows Syndicate Members to acquire equity interests in the Syndication LLCs, which are the entities that hold the ownership of the Target Properties. Further, the app will allow Syndicate Members to monitor the financial metrics and performance of those properties in which they have invested, as described above. The next version of the App may contain additional non-material information that may not be available to holders of our common stock through our public filings with the SEC, unless they have downloaded the app and become a Syndicate Member. For instance, the App may include information such as, but not limited to: (i) the number of bedrooms and bathrooms in a property; (ii) square footage of the property; (iii) total number of guests the property can support; or (iv) the year the property was built. At this point, however, we do not intend to provide such real-time visibility to holders of our common stock for individual property financials. Finally, the App will also fetch property listing data as well as data on short-term rental market trends from multiple third party API providers and display the consolidated data for a particular property in an easily accessible format.

At this time, the Company does not plan on becoming a licensed broker-dealer. The reAlpha App is managed by us, however, we utilize a third party broker-dealer, currently Dealmaker Securities LLC, licensed with the SEC/FINRA, to conduct the exempt offerings.

While the mobile version of the reAlpha App is still under development, the web version is already operational. As part of our internal restructuring changes described above, the reAlpha App will be combined with the Syndication Platform technology acquired through the Rhove acquisition. This new platform will facilitate all future offerings of Syndicate LLCs and will be renamed as “reAlpha Rhove”. We expect the integration of these technologies to be completed in the third quarter of 2023.

The Company expects to earn revenue from the reAlpha App on a fee basis from all Syndications conducted through the platform, which will be derived from the short-term rental’s Gross Receipts (as defined below). These fees currently include property management fees, asset management fees, and sourcing fees.

4

reAlpha HUMINT

In addition to the AI being utilized in our technologies, we added a human factor that analyzes short-term rental profitability. There are various qualitative features of a short term rental property that affect its profitability. For instance, the aesthetics of the interiors, as well as the color, decoration and design of the property’s exteriors, the look and feel of its neighborhood, condition of the amenities, etc. A property that is well-designed and tastefully decorated, coupled with amenities in good condition, requires less renovation and repair work before it is ready to be listed on platforms such as Airbnb. Such features can be collected by manually observing the photos, videos and the street view of the property and cannot be automatically fetched from a third party source.

reAlpha HUMINT is a platform that complements the AI technology, reAlpha BRAINTM, and allows analysts at reAlpha to input such features about a property and factor it into property evaluation.

reAlpha HUMINT is operational for our internal use and is not currently under further active development. However, we plan to commercialize this technology sometime in 2024.

BnBGPT

BnBGPT is an AI tool that is powered by a “Generative Pre-trained Transformer” language model, or “GPT”. BnBGPT is intended to complement our other AI and non-AI technologies and be used internally to simplify the process of generating personalized and effective home descriptions. BnBGPT is designed for both realtors and hosts (e.g., someone that owns a property listed on Airbnb’s platform), with features that help them save time and money while creating descriptions that we believe will help them stand out in a crowded market. By harnessing the power of AI, our BnBGPT app ensures that each description is personalized and effective, giving users a competitive edge in the marketplace.

For Realtors. Our app will offer a feature that generates advertising content directly from uploaded images and they can be used by realtors to advertise their properties, eliminating the need for professional copywriters and other costly marketing tools. This makes it easy for realtors to create descriptions that truly capture the essence of a home and highlight its unique features and benefits.

For Hosts. Our app will offer features that simplify the process of creating descriptions for listings on Airbnb, VRBO, Booking.com, and other such platforms. Our app will automatically organize these descriptions into sections, making it easy to highlight key features of a space and provide important information about guest access. Additionally, the app will include the proximity data of attractions near the property (e.g., restaurants, museums, areas of interest for tourists in the area and others), making it easier to highlight those for the host. This helps hosts spend less time writing descriptions and more time focusing on providing a great guest experience.

BnBGPT is currently operational for our internal use, and we are currently using BnBGPT for testing purposes before it becomes commercialized. BnBGPT is expected to be released publicly for commercial use in the third quarter of 2023. BnBGPT is also under active development with work being done to improve the quality of the descriptions generated by the app’s AI-based technology. The current revenue model for BnBGPT is pay-per-use with a number of free credits for new users. This is subject to change as we evolve the product and commercialize to generate revenue from the technology.

5

myAlphie

myAlphie is a digital platform that facilitates connections between local vendors and multi-family home real estate communities, particularly for the process of apartment turnovers. Apartment turnovers occur when one tenant vacates a unit and a new one moves in. Traditionally, various disparate and outdated tools have been used by apartment management companies to manage this turnover process. We developed myAlphie to provide a consolidated solution through its mobile app and portal. myAlphie incorporates various features, including in-app payments, task workforce management, shared calendars, and a vendor-client rating system. The platform’s design aims to create an efficient and user-friendly digital marketplace for those that seek to find home service solutions. myAlphie facilitates all in-app payments using Stripe, an online payment processing solutions company, as a payment gateway to transfer money from property managers, to the application, to the vendors. Through myAlphie’s app, we generated revenue by receiving fees for connecting, via the app, multi-family home real estate communities and local vendors offering home services.

We sold myAlphie, effective May 17, 2023, as further described above under “Recent Developments – Sale of myAlphie LLC.”

(ii) Rental Business

Our Properties

Our properties consist of five (5) single-family residences (“SFRs”). We generally target certain markets in the single-family property sector of the real estate industry, which markets and properties are determined by our technologies (see “Segments - Platform Services” section above, and “Investment Criteria for Properties to be Syndicated” and “Market Selection for Properties to be Syndicated” below). These properties are designed to be short-term rental properties, which are acquired for Syndication purposes and held for a period of one to six years, then potentially disposed of once that property has generated our internal target returns, which may also depend on various other factors, including, but not limited to, the appreciation value of such property over time, economic conditions, interest rate fluctuations and others. Short-term rentals are utilized for various purposes, including vacations, relocations, renovations, extended work trips, special events, temporary work assignments, or seasonal activities.

General competitive conditions affecting us include those identified in the “Competition and Competitive Strengths” section below.

As of April 30, 2023, we owned and operated five properties located in Texas and Florida, which are all intended to be used as short-term rental properties. The following table presents certain additional information about our real estate investments as of April 30, 2023:

| Properties(1) | General Character | Year Built | Location | Mortgage Loan Amount | Interest Rate | Maturity | Use of Property | Nature of Title(2) | ||||||||||||

| 825 Austrian Road | SFR | Grand Prairie, Texas | $ | 247,000 | 7.50% | 1/01/2053 | Short Term Rental | Warranty Deed | ||||||||||||

| 790 Pebble Beach Drive | SFR | Champions Gate, Florida | $ | 276,553 | 4.75% + Prime or 8.25%, Whichever is Greater | 2/11/2024 | Short Term Rental | Warranty Deed | ||||||||||||

| 612 Jasmine Lane | SFR | Davenport, Florida | $ | 337,242 | 4.75% + Prime or 8.25%, Whichever is Greater | 2/11/2024 | Short Term Rental | Warranty Deed | ||||||||||||

| 7676 Amazonas Street | SFR | Kissimmee, Florida | $ | 266,204 | 4.75% + Prime or 8.25%, Whichever is Greater | 2/10/2024 | Short Term Rental | Warranty Deed | ||||||||||||

| 2540 Hamlet Lane(3) |

| SFR | Kissimmee, Florida | $ | 342,000 | 4.75% + Prime or 8.25%, Whichever is Greater | 4/15/2024 | Short Term Rental | Warranty Deed | |||||||||||

| Total | $ | 1,469,000 | ||||||||||||||||||

| (1) | These properties do not have, and did not have at any time, tenants occupying 10% or more of the rentable square footage in, as these are single family residential properties licensed and operated by us as short-term rentals. We do not have any leases in place for any of our properties. |

| (2) | We own simple interests in all of our properties. |

| (3) | Sold after April 30, 2023 |

6

Property Improvements

We focus on acquiring rent-ready properties. Such rent-ready properties may not need a significant upgrade. A “significant upgrade” is defined as an upgrade to a property valued at more than 15% of the total purchase price for such property. However, even rent-ready properties may need some modifications and/or refreshing of fittings/furnishings. We determine the budgets and the need for such upgrades on a case by case basis, and the Syndication LLC bears the cost of such upgrades. If the Syndication LLC is managed by Rhove or another third-party, we will provide guidance on the budget and needs for improvements in each individual instance, and the Managing Member of the Syndication LLC will require our approval for certain matters that exceed the agreed upon budget. In some situations, we may still buy properties which may need significant upgrades, if we believe that the long-term potential of such properties outweighs its initial upgrade costs. Currently, only one of the properties that we own was significantly upgraded. We do not have any present plans for any further proposed improvement to any of our current properties.

Insurance

We maintain insurance for our properties, including (i) general liability; (ii) business income and loss of rent; (iii) property insurance; (iv) flood insurance, if appropriate; and (v) hazard insurance with minimum coverage levels equal to the building replacement cost of each asset. We believe that our properties are adequately insured, consistent with industry standards.

When applicable, we will also purchase insurance policies covering our joint ventures, partnerships, co-tenancies and other co-ownership arrangements or participations, as well as their general partners, co-general partners, managers, co-managers, developers, co-developers, construction managers, property managers, our Sponsor, our Manager or any of the foregoing or their respective affiliates. We will purchase deal level insurance policies for individual investments or blanket policies covering multiple investments and participants and their respective affiliates. These types of policies may include commercial general liability insurance, professional liability insurance, excess liability insurance, or other policy applicable to the specific situation. We will directly pay for any such policies or allocate premiums to or among our investments and their participants and respective affiliates on an estimated basis. To date, the Company has not required such additional policies. However, we may or may not require them in the future.

Syndication of Properties

Investment Criteria for Properties to be Syndicated

We continuously evolve our investment strategies depending on the market conditions. Due to global supply chain issues, we are focusing on rent-ready properties. Such rent-ready properties may not need a significant upgrade. A “significant upgrade” is defined as an upgrade to a property valued at more than 15% of the total purchase price for such property. However, even rent-ready properties may need some modifications and/or refreshing of fittings/furnishings. We decide the budgets for such upgrades on a case by case basis. In some situations, we may still buy properties which may need significant upgrades, if we believe that the long-term potential of such properties outweighs its initial upgrade costs. Currently, only one of our properties that we own was significantly upgraded.

We determine our Target Properties utilizing our investment criteria, which evaluates acquisition investments using our proprietary algorithms (the “Investment Criteria”). Investment decisions made pursuant to our Investment Criteria may include single-family homes, multifamily units, experiential properties, golf resort homes, resort communities and others.

We plan to have continuously assess property acquisition investments using our Investment Criteria and intend to purchase properties that include, but are not limited to, the following primary characteristics:

| ● | Target Properties identified by our reAlpha Score algorithms (described below) are considered for acquisition; and |

| ● | Target Properties with a minimum of three (3) bedrooms and two (2) bathrooms per unit. |

We also intend to regularly consider syndicating properties outside of these ranges depending on market conditions, uniqueness, and condition of the Target Property.

7

Business Process for Syndications

Once we have decided to acquire a property using our Investment Criteria, we intend to use the following steps to maximize its value:

| 1. | A Syndication LLC buys the Target Property using short-term leverage provided by one of our lending partners. Specifically, we currently have a master credit facility of up to $200 million with Churchill Funding I LLC, which has yet to be utilized (see “reAlpha Acquisitions Churchill, LLC” above), and both W Financial Fund, LP and Select Portfolio Servicing, Inc., commercial loan companies, have previously assisted us in the acquisition of our properties. |

| 2. | Rhove will act as the initial managing member of each Syndication LLC (the “Managing Member”), pursuant to each of the Syndication LLC’s operating agreements, and will arrange for the renovation of the purchased Target Property in accordance with our property improvement policy, at the cost of that Syndication LLC, if needed. Each of the Syndication LLC’s operating agreements will indicate that the Managing Member will hold a “Managing Membership Interest” in the Syndication LLC, which includes any and all rights, powers and benefits to which the Syndication LLC members are entitled under the Syndication LLC’s operating agreement, together with all obligations of the Managing Member to comply with the terms and provisions of the Syndication LLC’s operating agreement. The Managing Member Interest, however, does not include rights to ownership or profits or losses or any rights to receive distributions from operations or upon the liquidation or winding-up of such Syndication LLC, except for a property management fee of 15-30% of the purchased property’s rental revenue (more fully described below).The Managing Member Interests may be assigned without the consent of the other Syndication LLC members. |

| 3. | Within a reasonable period, which we expect to be between 1 to 12 months, the Managing Member will refinance the Target Property by swapping the short-term loan with a long-term loan from any one of our lending partners. If current market conditions or lending opportunities are poor, we may choose to not refinance or refinance out of the respective reasonable time frame. |

| 4. | The new Syndication LLC will offer up to 100% of its membership interests for purchase through an offering on the reAlpha App. Rhove, or the Managing Member, will continue to hold the membership interests of the Syndication LLC that are not purchased by investors through our offerings until we sell the full 100% to investors through the reAlpha App. However, such membership interests may never be sold, in which case those interests will continue to be held by Rhove, or the Managing Member. |

| 5. | Our Syndicate Members may receive distributions proportional to their membership, on a quarterly basis, based on the free cash flows after taxes from the overall performance of the property on Airbnb and similar digital hospitality platforms. |

| 6. | After the Target Property has generated the target returns the property may be sold to book the profit for the Syndication LLC. |

| 7. | This profit, if any, may be used to purchase further properties in the same Syndication LLC for our benefit and the benefit of the Syndicate Members. The Syndicate Members may choose to invest further in new properties or redeem their investments. |

Although we may sell properties, we intend to hold and manage the Syndications for a period of one to six years. The Managing Member may receive a gross fee of 15% to 30% of the Syndicated property’s rental revenue as a property management fee pursuant to the Syndication LLC’s operating agreement. The 15 to 30% fee is of gross receipts generated by the property. “Gross Receipts” includes: (i) receipts from the short-term or long-term rental of the property; (ii) receipts from rental escalations, late charges and/or cancellation fees; (iii) receipts from tenants for reimbursable operating expenses; (iv) receipts from concessions granted or goods or services provided in connection with the property or to the tenants or prospective tenants; (v) other miscellaneous operating receipts; and (vi) proceeds from rent or business interruption insurance, excluding (A) tenants’ security or damage deposits until the same are forfeited by the person making such deposits, (B) property damage insurance proceeds, and (C) any award or payment made by any governmental authority in connection with the exercise of any right of eminent domain.

8

As each of our syndicated properties reaches what we believe to be its appropriate disposition value, based on internal metrics, we will consider disposing of the property. The determination of when a particular property should be sold or otherwise disposed of will be made after consideration of relevant factors, including prevailing and projected economic conditions, whether the value of the property is anticipated to appreciate or decline substantially, and how any existing leases on a property may impact the potential sales price. The Managing Member will utilize the reAlpha Score to measure properties against set key performance indexes and determine when to objectively dispose of a property. The Managing Member may determine that it is in the best interests of stockholders to sell a property earlier than one year or to hold a property for more than six years. When we determine to sell a particular property, we intend to achieve a selling price that captures the capital appreciation for investors based on then-current market conditions. We cannot assure you that this objective will be realized.

Each Syndication LLC will be charged a market rate property disposition fee that is paid by the seller at the time of the sale, consisting of realtor fees and closing costs (taxes and other related costs). This disposition fee should cover property sale expenses such as brokerage commissions, and title, escrow and closing costs upon the disposition and sale of a property. It is expected that this disposition fee charged will range from 6% to 8% of the property sale price. Following the sale of a property, the Company expects to re-invest the proceeds of such sale, minus the property disposition fee described in this paragraph, into more properties for our portfolio and for the Syndicate Members to have the opportunity to invest in.

Further, the properties may be also managed by third-party property management firms at the Managing Member’s discretion. The services provided by such third-party property manager would include (i) ensuring compliance with local and other applicable laws and regulations; (ii) handling tenant access to properties; (iii) and any other action deemed necessary by the property manager or desirable for the performance of any of the services under our respective management agreement. Customarily, these management agreements are subject to a property management fee between 15% and 30% of the short-term rental gross revenue generated. As we achieve scale in the number of properties owned and operated, we may seek to bring property management in-house. In the event we manage a property, such property management fees would then be retained by us. If a short-term rental property is vacant and not producing rental income, the property management fee will not be paid during any such period of vacancy, including properties managed by third-parties.

The operating expenses that each Syndication LLC will be responsible for, as described above, include, but is not limited to: (i) mortgage principal and interest; (ii) property tax; (iii) homeowner insurance; (iv) utilities; (v) landscaping; (vi) pool maintenance costs; (vii) routine maintenance and repairs; (viii) HOA fees; and (ix) pest control. We will share the expenses related to the short-term rental properties with the Syndicate Members and will bear its own operating and management expenses in proportion to the ownership of the Syndication LLC.

Syndicate Member Exempt Offerings

To make the business model available to retail investors, the Company, will launch in exempt offerings conducted pursuant to Regulation A or Regulation D, each as promulgated under the Securities Act of 1933, as amended.

To achieve this goal, the Company’s subsidiary, Rhove, will create and manage Syndication LLCs to syndicate one or more of the Target Properties. Once the Syndication LLCs are in place, Rhove will launch exempted offerings to sell equity interests in such properties to investors pursuant to Regulation A or Regulation D, each as promulgated under the Securities Act of 1933, as amended. To further facilitate the investment process in the Syndication LLCs, the Company is currently working on the reAlpha App.

We expect that Rhove, as the Managing Member, or one of the subsidiaries of the Rhove SBU, will maintain management control of each of the Syndication LLCs. When this phase is fully implemented, we expect Syndicate Members to collectively own 100% of the Syndication LLCs and we shall account for the Syndication LLCs in accordance with applicable U.S. GAAP.

In the past, the Company has launched the following exempt offerings for different purposes:

| ● | On March 22, 2021, reAlpha 1011 Gallagher LLC, a subsidiary of the Company, offered securities pursuant to rule 506(b) of Regulation D, as an initial testing of our business model. Two accredited investors participated in this offering, both of which had a pre-existing relationship with the Company’s founders; and |

| ● | On March 3, 2023, the Company opened its first Regulation CF Syndication listed under reAlpha 612 Jasmine Lane Inc., our wholly-owned subsidiary (also referred to herein as “Jasmine Holdco”) under Section 4(a)(6) of the Securities Act with the assistance of Dealmaker Securities LLC, a SEC/FINRA registered broker-dealer. This Regulation CF offering will be terminated by June 30, 2023. After effectiveness of this Registration Statement, the Company will no longer be able to conduct Regulation CF offerings per Rule 227.100(b)(2) of Regulation CF. |

9

Market Selection for Properties to be Syndicated

We intend to focus our business efforts on the markets in which Airbnb and similar platforms operate, which include some or all of the following characteristics:

| ● | sufficient inventory to make it feasible to achieve scale in the local market (100 – 500 homes); |

| ● | large universities and skilled workforce; |

| ● | popular with travelers; |

| ● | favorable competitive landscape with respect to other institutional residence buyers; and/or |

| ● | hotel room capacity and occupancy rates in given destinations. |

During our testing phase, we acquired properties in Dallas, Texas, which was our initial target market. We have expanded our target market to include Florida, Georgia, South Carolina, North Carolina, Alabama, Texas, Tennessee, Nevada, and Arizona (the “Sunbelt States”), with a strong focus in Florida.

According to Roofstock’s “Sun Belt real estate: Stats and trends for 2022” the Sunbelt States have experienced significant recent growth, providing opportunities in real estate investment. Home appreciation rates in these states have been higher than the national average, increasing the value of real estate assets. The population in these states has also grown rapidly, driven by factors such as job opportunities, lower cost of living, and favorable climate.

As noted by Bankrate in its recent article “Housing market heat shifts to Southeast” the travel and hospitality industry in the Sunbelt States has also grown significantly, driven by increased tourism and a growing number of short-term rental properties. This has created opportunities for real estate investors to purchase properties for short-term rental use, generating higher rental income than traditional long-term rentals.

Additionally, household incomes in the Sunbelt States have increased at a faster pace than the national average, providing a larger pool of potential homebuyers and renters. The desirability of living in these states has also increased, with many individuals and families seeking a better quality of life, warmer weather, and outdoor recreational opportunities.

Overall, the recent growth in the Sunbelt States has created numerous opportunities for real estate investment, particularly in the short-term rental market. Investors can benefit from the high demand for properties in these states, generating strong rental income and capital appreciation over time. Now, we have moved into the Orlando, Florida market. We believe that this market offers strong growth in population, jobs, rental rates, and value appreciation. Additionally, we have selected Tampa, Ft. Lauderdale, and Panhandle areas in Florida as our next markets.

We will focus on acquiring properties as outlined below with seventy five percent (75%) or greater for rent-ready assets. This is subject to change as market conditions shift.

Rent-Ready Short-Term Rentals

This category comprises homes that have been operating as short-term rentals and include:

| ● | required licensing and short-term rentals designation in place; |

| ● | furnishing and/or furniture; and |

| ● | minimum of six (6) months of operating history. |

The benefits of investing in this category may include:

| ● | immediate cash flow; |

| ● | immediate optionality for long term debt; and |

| ● | reduced hold time before Syndication. |

10

Repositioning to Short-Term Rentals

This category comprises homes that have not been operating historically as short-term rentals. Properties that fit this category will include:

| ● | partially/fully renovated or new construction homes; |

| ● | properties with strong locational attributes such as: (i) a positive five-year trend related to population growth, to median income growth, and/or tourism revenue growth, (ii) potential for real estate appreciation and (v) close proximity to attractions and destinations such as parks, beaches, malls, restaurants and amusement parks; and |

| ● | properties located in areas where laws are supportive of short-term rental use. |

Multi-Unit Properties

Multi-unit properties are defined as two (2) or more units on the same folio/property. Properties with four (4) units or less are considered residential and treated in the same fashion as single-family homes. The investment criteria is the same for Multi-unit residential properties as it is for traditional residential acquisition targets.

One of the reasons to purchase multi-unit properties is the ability to leverage economies of scale related to vendors and operating costs to potentially reduce total expenses. In addition, costs such as management fees and other property services are potentially reduced on a per unit basis. Finally, we may expect to see lower operating expense percentages and increased listing exposure and optionality for guests.

We expect to revisit market statistics and market selection criteria on a periodic basis. Selected markets may not necessarily meet every single criterion. In the future, we expect that will expand to other states in the U.S., and subsequently globally. At this time, we have not set a timeline for expansion. We may also evaluate certain additional markets in the future.

Investment Decisions For Properties to be Syndicated

While we will employ our proprietary AI-based technologies and platform, and our real estate professionals, to identify suitable properties for Syndication acquisition, the Company will be responsible for final decisions. We will use the methodology described below and our bespoke technologies to reach buy or sell decisions. We have developed an investment approach that combines the experience of our management, the reAlpha Score and an approach that emphasizes market research, underwriting standards and down-side analysis of the risks of each investment.

Notwithstanding, the Company accounts for unknown or contingent liabilities arising out of the properties that we finally acquire. For any assets acquired not currently operating as rent-ready properties, an amount up to six (6) months of recurring operating expenses will be set aside as reserves. This reserve amount is in addition to any proposed, budgeted and/or actual expenses incurred related to the renovation of a property.

To execute our disciplined investment approach, we plan to closely monitor the profit and loss of each investment.

The following is a summary of our methodology for property acquisition:

11

Local Market Research

We research the acquisition and underwriting of each transaction. The research focuses on finding any “red flags” that may influence the decision to acquire a property. A red flag is a notification for further scrutiny of such properties. These “red flags’’ include (i) heavy regulation on short-term rentals at a state, county, or homeowner’s association (“HOA”) level; (ii) homes that have been on the market for longer than a year, or (iii) areas where natural disasters are common and damaging. The red flags analysis related to extreme weather conditions helps us estimate potential damages and related insurance costs to make better decisions. Additionally, we consider things such as tourist numbers and market size, seasonality, walkability, proximity to airports, restaurants and entertainment and events that would attract renters.

Once a deeper analysis of such red flagged properties is completed, the management team may or may not decide to purchase such properties.

Market Analysis. When we enter a market where we do not own any properties, we first determine what the demographic and real estate trends have been. More specifically, we look to see positive trends in statistics such as, but not limited to:

| ● | historical and projected population growth; |

| ● | historical and projected median income/median income growth; |

| ● | historical real estate property appreciation; |

| ● | historical rental rate growth; |

| ● | laws, ordinances, restrictions related to short term rentals; |

| ● | residential inventory supply; and |

| ● | annual tourism demand. |

Submarket Analysis. In our submarket analysis, we look for all the same stats/trends as completed at the market level but for a smaller geographical area such as a specific city and/or zip code. Additionally, we will look to see positive trends in statistics such as, but not limited to:

| ● | total short term rental demand in the submarket; |

| ● | active short term rental listings in the submarket; |

| ● | average submarket daily rates based on seasonality; |

| ● | average submarket occupancy; and |

| ● | licensing requirements. |

Property Analysis. In our property analysis, we look to analyze the subject property or properties to determine:

| ● | age and construction type, including roof, doors and windows; |

| ● | property condition; |

| ● | level and finesse of finishes in the property; |

| ● | is there any deferred maintenance to be done in the property before putting it in the market; |

| ● | age/condition of major mechanical components including roof, plumbing and appliances; |

| ● | upcoming capital expenditures; and |

| ● | recurring maintenance. |

12

Disposition Policies

Generally, we intend to hold and manage the properties we acquire for a period of one to five years. As each of our properties reaches what we believe to be its appropriate disposition value, we will consider disposing of the property. The determination of when a particular property should be sold or otherwise disposed of will be made after consideration of relevant factors, including prevailing and projected economic conditions, whether the value of the property is anticipated to appreciate or decline substantially, and how any existing leases on a property may impact the potential sales price. The Company will utilize the reAlpha Score to measure properties against set key performance indexes and determine when to objectively dispose of a property. The Company may determine that it is in the best interests of shareholders to sell a property earlier than one year or to hold a property for more than five years. The Company reserves the right to hold properties for longer.

When we determine to sell a particular property, we intend to achieve a selling price that captures the capital appreciation for investors based on then-current market conditions. We cannot assure you that this objective will be realized.

Following the sale of a property, the Company expects to re-invest the proceeds of such sale, net of the property disposition fee as described below, into more properties for the benefit of ourselves and the investing Syndicate Members investing in that property.

Property Disposition Fee

Upon the disposition and sale of a property, each property will be charged a market rate property disposition fee that should cover property sale expenses such as brokerage commissions, and title, escrow and closing costs. It is expected that this disposition fee charged will range from six to eight percent of the property sale price.

Property Management Agreement

The Company will appoint Rhove as the initial manager of each LLC pursuant to its operating agreement. The Company may, however, subsequently appoint a third-party property management company to serve as property manager to manage the underlying property of each LLC pursuant to a specific property management agreement.

The services provided by the property manager would include:

| ● | Ensuring compliance with local landlord/tenant and other applicable laws; |

| ● | Handling tenant access to properties; and |

| ● | Investigating, selecting, and, on behalf of the applicable property, engaging and conducting business with such persons as the property manager deems necessary to ensure the proper performance of its obligations under the property management agreement, including but not limited to consultants, insurers, cleaning personnel, insurance agents, maintenance providers, bookkeepers and accountants and any and all persons acting in any other capacity deemed by the property manager necessary or desirable for the performance of any of the services under the property management agreement. |

Each property management agreement would terminate on the earlier of: (i) the Company’s discretion to terminate a property management agreement at predetermined renewal periods or by paying a termination fee, (ii) after the date on which the relevant property has been liquidated and the obligations connected to the property (including, contingent obligations) have been terminated, (iii) upon notice by one party to the other party of a party’s material breach of a property management agreement or (iv) such other date as agreed between the parties to the property management agreement.

We expect each LLC to indemnify the property manager out of its assets against all liabilities and losses (including amounts paid in respect to judgments, fines, penalties or settlement of litigation, including legal fees and expenses) to which it becomes subject by virtue of serving as property manager under the respective property management agreements with respect to any act or omission that has not been determined by a final, non-appealable decision of a court, arbitrator or other tribunal of competent jurisdiction to constitute fraud, willful misconduct or gross negligence.

13

Competition and Competitive Strengths

We face competition from different sources in our technology operations and of acquiring properties. We believe that we will disrupt the consumption patterns for financial investment and services through our innovative AI-based technologies, but will continue to face competition from other firms including large technology companies, and smaller, new financial technology entrants.

We believe that the key competitive factors in our technology market include:

| ● | the reAlpha App and other of our platform and technology features, quality and functionality being developed; |

| ● | security and trust; |

| ● | cloud-based architecture; |

| ● | our proprietary technology to make objective and strategic investments in property and market selection. |

We seek to differentiate ourselves from competitors primarily through the integration of AI into our technologies for the real estate market, the development of our reAlpha App, which will be available in mobile App version in the future with a focus on accessibility, customer experience, and trust. We believe that our ability to continue innovating quickly further differentiates our developing platforms from our competition. We believe we compete favorably across all key competitive factors and that we have developed a business model that is difficult to replicate.

Our reAlpha App is continuously developed to provide exceptional quality and functionality. We believe this dedication to innovation sets us apart from competitors and allows us to deliver superior user experiences. We also prioritize the security and trust of our users and investors. By implementing robust security measures and ensuring data integrity, we instill confidence in our platform, which we believe sets us apart as a trustworthy and reliable choice in the financial technology market.

Further, our cloud-based architecture offers scalability, flexibility, and seamless accessibility. This infrastructure enables us to handle increasing volumes of data and transactions efficiently, empowering us to deliver a seamless user experience and respond swiftly to evolving market demands.

We believe that our focus on innovation, security, and scalability gives us a competitive edge in the financial technology space. As we navigate the competitive landscape, we remain committed to continuously enhancing our technology offerings, fortifying our security measures, and leveraging cloud-based advantages. We believe that these efforts position us as a frontrunner in transforming the financial investment and services landscape through our AI-driven solutions.

We further believe that our competition in acquiring properties for investment purposes are individual investors, small private investment partnerships looking for one-off acquisitions of investment properties that can either be leased or restored and sold, and larger investors, including private equity funds and real estate investments trusts (“REITs”), that are seeking to capitalize on the same market opportunity that we have identified. Our primary competitors in acquiring portfolios include large and small private equity investors, public and private REITs, and other sizable private institutional investors. These same competitors may also compete with us for investors. Competition may increase the prices for properties that we would like to purchase, reduce the amount of rent we may charge for our properties, reduce the occupancy of our portfolio, and adversely impact our ability to achieve attractive total returns. We also face competition from other real estate platform companies such as Opendoor Technologies Inc. (NASDAQ: OPEN), Roofstock, Inc., Fundrise LLC, Invitation Homes, Pacaso, as well as a range of emerging new entrants. There are a number of established and emerging competitors in the real estate platform market. The market is fragmented, rapidly evolving, competitive, and with relatively low barriers to entry.

14

Although our competitors may be more established and better funded than we are, we believe that our acquisition platform, Investment Criteria, extensive in-market property operations infrastructure, and local expertise in our markets provide us with competitive advantages. We consider our competitive differentiators in our market to primarily be:

| ● | our focus on the short-term rental market, compared to other established players in the industry that focus on long-term rentals; |

| ● | Syndicate Member rewards program that allows for utilization of properties when they are unoccupied, which is currently being developed; |

| ● | consistent short-term rental income with use of optimum amounts of leverage; |

| ● | lower minimum investment amounts; and |

| ● | favorable tax treatment associated with long-term capital gains. |

Employees

As of August 24, 2023, we had 9 full-time employees in the U.S. and 8 in our India office. We believe that we maintain good relations with our employees.

Legal Proceedings

Ohio Subpoena

On May 2, 2022, we received a subpoena duces tecum and requests for depositions of three senior managers of the Company from the Ohio Division of Securities (the “ODS”), all related to the Company’s Regulation A securities offering in the State of Ohio, and based on Ohio Revised Code 1707.23. The depositions were taken in July 2022. The ODS has not asserted any securities violations by the Company other than a late notice filing for its offering. The Company is fully cooperating with the ODS.

Massachusetts Consent Order

On April 15, 2022, we entered into a consent order (the “Consent Order”) with the Securities Division of the Office of the Secretary of the Commonwealth of Massachusetts (the “MSD”) following an investigation by the MSD into whether the Company had engaged in acts or practices that violated the Massachusetts Uniform Securities Act (the “Massachusetts Act”) and the regulations promulgated thereunder (the “Massachusetts Regulations”). For purposes of the Consent Order, the Company did not admit or deny the findings of fact or law or any of the allegations contained therein. The Consent Order provides that it is not intended to form the basis of any disqualification under Section 3(a)(39) of the Securities Exchange Act of 1934, or Rules 504(b)(3) and 506(d)(i) of Regulation D, Rule 262(a) of Regulation A and Rule 503(a) of Regulation CF under the Securities Act of 1933. Likewise, the Consent Order provides that it is not intended to form a basis of a disqualification under Section 204(a)(2) of the Uniform Securities Act of 1956 or Section 412(d) of the Uniform Securities Act of 2002. MSD alleged in the Consent Order that the Company initially failed to disclose a then ongoing criminal proceeding taking place in India against the Company’s CEO that involves allegations of fraud and forgery. MSD also alleged that the Company posted sample stock images of properties on its website, along with corresponding property “scores,” purchase dates, and addresses, despite not actually owning these properties. MSD further alleged that the Company failed to disclose a potential conflict of interest in connection with the Company’s real estate acquisitions. The MSD finally alleged that the Company failed to file notice with the MSD and submit a consent for service of process before marketing and selling shares to investors in Massachusetts. In the Consent Order the MSD noted that “[e]xcept in any action by the Division to enforce the obligations of the Consent Order, any acts performed or documents executed in settlement of this matter: (A) may not be deemed or used as an admission of, or evidence of, the validity of any alleged wrongdoing, liability, or lack of any wrongdoing or liability; and (B) may not be deemed or used as an admission of, or evidence of, any such alleged fault or omission of the Company in any civil, criminal, arbitral, or administrative proceeding in any court, administrative agency, or tribunal.”

Under the terms of the Consent Order, the Company is censured, barred from offering or selling securities in Massachusetts, and ordered to cease and desist from committing future violations of the Massachusetts Act and the Massachusetts Regulations. Pursuant to the Consent Order, on April 21, 2022, the Company paid a $375,000 administrative fine and offered to rescind the purchases of each of the fourteen Massachusetts investors who acquired the Company’s common stock in its Regulation A offering. Such investors paid an aggregate amount of $19,500 to purchase the Company’s common stock. Seven out of the fourteen Massachusetts investors elected to rescind the purchase and the Company has already refunded them a total of $11,500. The Company has fully complied with the terms of the Consent Order.

15

The Company engaged counsel to make all the necessary securities filings. However, the Company’s then-counsel did not make any blue-sky filings until MSD informed of such irregularity to the Company.

A copy of the Consent Order was filed on Form 1-U on April 15, 2022, as Exhibit 6.5 thereto, and is Exhibit 99.1 to the Offering Statement. For additional information on the Consent Order, we refer you to Exhibit 99.1. As of the date of this filing, we have sold $4.468 million of shares to investors other than our former parent company, reAlpha Tech Corp. (which as of the date of this Direct Listing no longer exists, and $500,000 to our former parent company, for aggregate sales of $4.968 million. The holdings that belonged to our former parent company have been assigned to reAlpha Tech Corp. post the Downstream Merger (as defined above). For additional information on the India proceeding involving Mr. Devanur see “India Proceeding Involving Giri Devanur” section below.

Parent Company Litigation

On December 27, 2021, Ms. Valentina Isakina, a board advisor of our former parent company, reAlpha Tech Corp., (the “Parent Company”) filed a lawsuit in the Southern District of Ohio against the Parent Company in connection with her termination package. After three months of service, the Parent Company discontinued her services as she was not the right fit for the Parent Company’s needs. reAlpha Tech Corp. contends that pursuant to the terms of her employment agreement, she was offered 12,500 shares of reAlpha Tech Corp., to vest over a period of time, however, she never accepted the shares.

Ms. Isakina, on the other hand, contends she is owed up to 5% from reAlpha Tech Corp. in connection with an alleged agreement to serve on the board of directors. reAlpha Tech Corp. denies the existence of such agreement. The parties are in the process of completing discovery. There is no trial set, and we believe the matter will be resolved in late 2023 or in 2024.

India Proceeding Involving Giri Devanur

In 2006, Mr. Devanur became the CEO of an India-based company named Gandhi City Research Park, Private Limited (“Gandhi City Research Park”). Gandhi City Research Park was liquidated as a result of the Lehman Brothers collapse in 2009. In 2010, an investor in Gandhi City Research Park filed a fraud complaint with the Cubbon Park Police Station in Bengaluru, India, against, among others, Mr. Devanur. In 2014, the Cubbon Park Police dismissed all claims. Subsequently, in 2015 the investor appealed the Cubbon Park Police’s decision before the Lower Court. In November 2018, the Lower Court issued a criminal summons against, among others, Mr. Devanur. Mr. Devanur petitioned the High Court to quash the summons. By order dated March 27, 2023, the High Court granted Mr. Devanur’s petition and ordered the Lower Court to reconsider the investor’s appeal. On August 3, 2023, the Lower Court decided to uphold the Cubbon Park Police’s decision and close the criminal case against Mr. Devanur.

Malpractice Lawsuit

On May 8, 2023, the Company filed a malpractice lawsuit with the United States District Court for the Southern District of Ohio, Eastern Division, against Buchanan, Ingersoll & Rooney, PC (“Buchanan”), Rajiv Khanna (“Khanna”) and Brian S. North (“North,” together with Buchanan and Khanna, the “Buchanan Legal Counsel”). The complaint alleges that the Buchanan Legal Counsel failed to provide proper and timely legal advice during the Company’s Tier 2 Regulation A offering, resulting in late Blue Sky notice filings with all required states prior to the Company offering and selling securities in those states. As a result, the Company was subject to a number of inquiries, investigations, and subpoenas by the various states, incurring significant legal fees and fines, lost opportunity due to pausing its Regulation A campaign, in addition to the loss of a $20 million institutional investment. The Company is seeking the forfeit of all legal fees associated with this matter, the award of legal fees to bring this matter to action, and further legal and equitable relief as the Court deems just and proper.

16

Trademarks

We own or otherwise have rights to the trademarks, service marks, patents and copyrights, including those mentioned in this prospectus, used in conjunction with the operation of our business. This prospectus includes our own trademarks, which are protected under applicable intellectual property laws, as well as trademarks, service marks, copyrights, and trade names of other companies, which are the property of their respective owners. We do not intend our use or display of other companies’ trademarks, service marks, copyrights, or trade names to imply a relationship with, or endorsement or sponsorship of us by, any other companies. Solely for convenience, trademarks and tradenames referred to in this prospectus may appear without the ®, ™, or SM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights to these trademarks and tradenames.

As of the date of this prospectus, we have two registered trademarks and four pending trademark applications in the United States, and have filed a provisional patent application for the reAlpha BRAIN. Our U.S. trademark registrations and applications are reflected in the chart below. We are using certain other marks that have not been registered, such as reAlpha M3, reAlpha AI, reAlpha BRAIN, and reAlpha Hub. We may choose to add new or retire old patents or trademarks for these technologies as the landscape of such technologies keeps changing rapidly.

U.S. Trademark Registrations and Applications

| Mark | Class(es) | App. No. | Filing Date | Status | Next Deadline(1) | Applicant/Registrant | ||||||

| ReAlpha | 036, 037 | 90670051 | 2021-04-25 | Registered | 2027-11-30 | reAlpha Tech Corp. | ||||||

| Invest in real | 036 | 90796901 | 2021-06-26 | Registered | 2028-04-12 | reAlpha Tech Corp. | ||||||

| ReAlpha HUMINT | 035, 042 | 90670061 | 2021-04-25 | Pending | 2023-10-18 | reAlpha Tech Corp. | ||||||

| INVESTMENT PROPERTY OFFERING | 042 | 97603076 | 2022-09-22 | Pending | N/A | reAlpha Tech Corp. | ||||||

| Vacation Capitalist | 036 | 97703446 | 2022-12-05 | Pending | N/A | reAlpha Tech Corp. | ||||||

| BnBGPT | 042 | 97938022 | 2023-05-16 | Pending | N/A | reAlpha Tech Corp. |

| (1) | A trademark registration does not expire after a set period of time, and may remain in effect as long as the owner continues to use the trademark in commerce and timely files the required registration maintenance documents. |

Patents

We currently maintain one provisional patent application, and we intend to continue to apply to patents when applicable to create significant trade-secret intellectual property regarding our technologies, algorithms and platforms. Our current patent application for reAlpha BRAINTM is based on a system for analyzing, evaluating, and ranking properties using artificial intelligence. If granted, this patent will expire 20 years from the date of its original filing date.

| ● | Patent Application Number 17944255: “reAlpha BRAIN” (filed September 14, 2022). |

Our Corporate Structure

Formation

reAlpha Tech Corp., the former parent entity of the Company, was originally incorporated in Delaware on November 30, 2020. Then, on April 22, 2021, we incorporated the Company (f/k/a reAlpha Asset Management, Inc.), a subsidiary of our former parent company, in Delaware. Following the Downstream Merger on March 21, 2023, reAlpha Tech Corp merged with and into reAlpha Asset Management, Inc., with the Company surviving the merger, and subsequently the Company changed its name to reAlpha Tech Corp. This was a strategic move by us to consolidate both our technology capabilities and our real estate syndication business.

17

Our promoter upon incorporation in Delaware was our former parent, reAlpha Tech Corp.

Our principal executive office is located at 6515 Longshore Loop, Suite 100, Dublin, OH 43017. Our phone number is (707) 732-5742. Our corporate website is located at www.realpha.com. Information on our website is not part of this prospectus.

Internal Restructuring

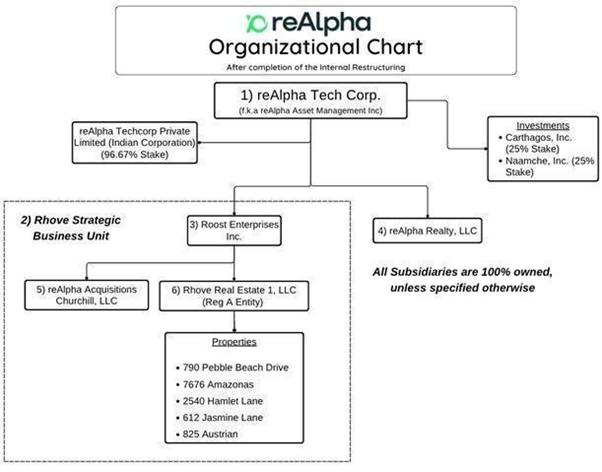

As a result of the Downstream Merger and the Rhove acquisition the Company will change its internal organizational structure. We expect this internal restructuring change to be completed by the end of the third quarter of 2023. We expect these changes will have no material effect on our financial statements or accounting policies.

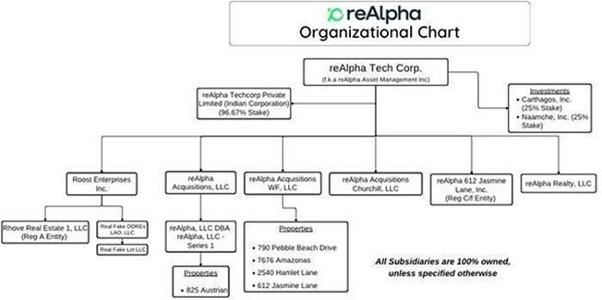

The following diagram summarizes the Company’s current internal restructuring by legal entity as of April 30, 2023*:

18

The following diagram summarizes the Company’s internal restructuring by the legal entity after completion of our internal restructuring to better reflect our business model**:

| * | Explanatory Note: |

| 1. | reAlpha Tech Corp. or the Company (f.k.a. reAlpha Asset Management Inc.) is the entity that resulted from the Downstream Merger. Also, as a result of the Downstream Merger, the Company owns a 25% stake in Naamche, Inc., an artificial intelligence (“AI”) studio, a 25% stake in Carthagos Inc., a design studio, and a 96.67% stake in reAlpha Techcorp India Private Limited, a subsidiary that provides business support services for finance, marketing and technology. |

| 2. | Roost, Inc., Rhove Real Estate 1, LLC, reAlpha Acquisitions Churchill, LLC, and future Syndication LLCs are collectively known as the “Rhove Strategic Business Unit” or the “Rhove SBU”. The purpose of Rhove SBU is to perform Syndications. |

19

| 3. | Roost Enterprises, Inc. (“Rhove”) is a wholly-owned subsidiary of the Company that provides real estate technology solutions. | |

| 4. | ReAlpha Realty, LLC is a wholly-owned subsidiary of the Company registered in Florida as a real estate brokerage. Its primary function is to act as agent and/or advisor to acquisitions completed by the Rhove SBU, the Company or any affiliated companies. |

| 5. | reAlpha Acquisitions Churchill, LLC is a wholly-owned subsidiary of the Company that was created to hold the properties acquired by the Company utilizing financing provided by Churchill Finance I, LLC. |

| 6. | Rhove Real Estate 1, LLC is a wholly-owned subsidiary of the Company that was created to offer securities pursuant to Regulation A before the reAlpha acquisition of Rhove. After we complete our internal restructuring changes, we intend to use this entity for future property Syndications using the SEC qualified Regulation A offering. We refer to properties that have been offered through a Syndication LLC as a “Syndicated” property. |

| ** | Explanatory Note: The following entities will be dissolved to effectuate our internal restructuring changes: |

| 1. | reAlpha, LLC dba reAlpha Series 1, LLC is a wholly-owned subsidiary of the Company that was created to hold the property located at 825 Austrian Rd, Grand Prairie TX 75050; |

| 2. | reAlpha Acquisitions, LLC is a wholly-owned subsidiary of the Company that holds reAlpha, LLC dba reAlpha Series 1, LLC; |

| 3. | reAlpha Acquisitions WF, LLC is a wholly-owned subsidiary of the Company that was created to hold the properties located at 790 Pebble Beach Dr, Kissimmee FL 3474, 612 Jasmine Ave, Davenport, FL 33897, 7676 Amazonas St, Kissimmee, FL 34747, and 2540 Hamlet Lane, Kissimmee, FL 34746; and |

| 4. | reAlpha 612 Jasmine Lane, Inc. is a wholly-owned subsidiary of the Company that was created to hold the property located at 612 Jasmine Ave, Davenport, FL 33897 upon completion of the Regulation CF offering of such property. |

| 5. | Real Fake DOREs LAO, LLC is a Wyoming limited liability company and a subsidiary of Rhove that was created to hold Real Fake Lot LLC, which is an Ohio limited liability company holding a small lot of land of insignificant value in Brickhaven, OH. |

20

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations