| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-255934-01 | ||

| Dated February 2, 2022 | BMO 2022-C1 |

Free Writing Prospectus

Structural and Collateral Term Sheet

| ||

BMO 2022-C1 Mortgage Trust

| ||

$1,122,007,709 (Approximate Mortgage Pool Balance) | ||

$965,676,000 (Approximate Offered Certificates) | ||

BMO Commercial Mortgage Securities LLC Depositor | ||

| | ||

Commercial Mortgage Pass-Through Certificates, Series 2022-C1 | ||

| | ||

Bank of Montreal Starwood Mortgage Capital LLC KeyBank National Association SSOF SCRE AIV, L.P. German American Capital Corporation Mortgage Loan Sellers

| ||

| BMO Capital Markets | Deutsche Bank Securities | KeyBanc Capital Markets |

| Co-Lead Managers and Joint Bookrunners | ||

Bancroft Capital, LLC

| Drexel Hamilton Co-Manager | |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

| Dated February 2, 2022 | BMO 2022-C1 |

This material is for your information, and none of BMO Capital Markets Corp., KeyBanc Capital Markets Inc., Deutsche Bank Securities Inc., Bancroft Capital, LLC and Drexel Hamilton, LLC (the “Underwriters”) are soliciting any action based upon it. This material is not to be construed as an offer to sell or the solicitation of any offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal.

The depositor has filed a registration statement (including the prospectus) with the Securities and Exchange Commission (File No. 333-255934) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the Securities and Exchange Commission for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or BMO Capital Markets Corp., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling 1-866-864-7760. The Offered Certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more Classes of Certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these Certificates, a contract of sale will come into being no sooner than the date on which the relevant Class has been priced and we have verified the allocation of Certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

Neither this document nor anything contained in this document shall form the basis for any contract or commitment whatsoever. The information contained in this document is preliminary as of the date of this document, supersedes any previous such information delivered to you and will be superseded by any such information subsequently delivered prior to the time of sale. These materials are subject to change, completion or amendment from time to time. The information should be reviewed only in conjunction with the entire offering document relating to the Commercial Mortgage Pass-Through Certificates, Series 2022-C1 (the “Offering Document”). All of the information contained herein is subject to the same limitations and qualifications contained in the Offering Document. The information contained herein does not contain all relevant information relating to the underlying mortgage loans or mortgaged properties. Such information is described elsewhere in the Offering Document. The information contained herein will be more fully described elsewhere in the Offering Document. The information contained herein should not be viewed as projections, forecasts, predictions or opinions with respect to value. Prior to making any investment decision, prospective investors are strongly urged to read the Offering Document its entirety. Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this free writing prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This document has been prepared by the Underwriters for information purposes only and does not constitute, in whole or in part, a prospectus for the purposes of Regulation (EU) 2017/1129 (as amended or superseded) and/or Part VI of the Financial Services and Markets Act 2000 (as amended) or other offering document.

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) which have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the Computational Materials’ accuracy, appropriateness or completeness in any particular context; or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of these securities. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the securities may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of the Underwriters or any of their respective affiliates make any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the securities. The information in this presentation is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Mortgage Loan Sellers or which was otherwise reviewed by us.

This document contains forward-looking statements. If and when included in this document, the words “expects”, “intends”, “anticipates”, “estimates” and analogous expressions and all statements that are not historical facts, including statements about our beliefs or expectations, are intended to identify forward-looking statements. Any forward-looking statements are made subject to risks and uncertainties which could cause actual results to differ materially from those stated. Those risks and uncertainties include, among other things, declines in general economic and business conditions, increased competition, changes in demographics, changes in political and social conditions, regulatory initiatives and changes in consumer preferences, many of which are beyond our control and the control of any other person or entity related to this offering. The forward-looking statements made in this document are made as of the date hereof. We have no obligation to update or revise any forward-looking statement.

BMO Capital Markets is a trade name used by BMO Financial Group for the wholesale banking businesses of Bank of Montreal, BMO Harris Bank N.A. (member FDIC), Bank of Montreal Europe p.l.c, and Bank of Montreal (China) Co. Ltd, the institutional broker dealer business of BMO Capital Markets Corp. (Member FINRA and SIPC) and the agency broker dealer business of Clearpool Execution Services, LLC (Member FINRA and SIPC) in the U.S., and the institutional broker dealer businesses of BMO Nesbitt Burns Inc. (Member Investment Industry Regulatory Organization of Canada and Member Canadian Investor Protection Fund) in Canada and Asia, Bank of Montreal Europe p.l.c. (authorized and regulated by the Central Bank of Ireland) in Europe and BMO Capital Markets Limited (authorized and regulated by the Financial Conduct Authority) in the UK and Australia.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY-GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of any email communication to which this document is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) no representation that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

THE CERTIFICATES REFERRED TO IN THESE MATERIALS ARE SUBJECT TO MODIFICATION OR REVISION (INCLUDING THE POSSIBILITY THAT ONE OR MORE CLASSES OF CERTIFICATES MAY BE SPLIT, COMBINED OR ELIMINATED AT ANY TIME PRIOR TO ISSUANCE OR AVAILABILITY OF A FINAL PROSPECTUS) AND ARE OFFERED ON A “WHEN, AS AND IF ISSUED” BASIS.

THE UNDERWRITERS MAY FROM TIME TO TIME PERFORM INVESTMENT BANKING SERVICES FOR, OR SOLICIT INVESTMENT BANKING BUSINESS FROM, ANY COMPANY NAMED IN THESE MATERIALS. THE UNDERWRITERS AND/OR THEIR AFFILIATES OR RESPECTIVE EMPLOYEES MAY FROM TIME TO TIME HAVE A LONG OR SHORT POSITION IN ANY CERTIFICATE OR CONTRACT DISCUSSED IN THESE MATERIALS.

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 2 | ||

| Structural and Collateral Term Sheet | BMO 2022-C1 | |

| Indicative Capital Structure | ||

Classes of Certificates | Expected Ratings | Approximate | Approximate Initial Available Certificate Balance or Notional Amount(1) | Approximate Initial Retained Certificate Balance. Notional Amount or Percentage Interest(1)(2) | Approximate Initial Credit Support(3)(4) | Initial | Pass-Through | Expected Weighted Avg. Life (yrs.)(6) | Expected Principal Window(6) | |||

| Offered Certificates | (Fitch / S&P / KBRA)* | |||||||||||

| Class A-1 | AAAsf/AAA(sf)/AAA(sf) | $17,581,000 | $17,029,000 | $552,000 | 30.000% | % | (7) | 2.57 | 3/22-9/26 | |||

| Class A-2 | AAAsf/AAA(sf)/AAA(sf) | $150,154,000 | $145,436,000 | $4,718,000 | 30.000% | % | (7) | 4.86 | 9/26-2/27 | |||

| Class A-3 | AAAsf/AAA(sf)/AAA(sf) | $67,774,000 | $65,644,000 | $2,130,000 | 30.000% | % | (7) | 7.05 | 12/28-12/29 | |||

| Class A-4 | AAAsf/AAA(sf)/AAA(sf) | (8) | (8) | (8) | 30.000% | % | (7) | (8) | (8) | |||

| Class A-5 | AAAsf/AAA(sf)/AAA(sf) | (8) | (8) | (8) | 30.000% | % | (7) | (8) | (8) | |||

| Class A-AB | AAAsf/AAA(sf)/AAA(sf) | $25,170,000 | $24,379,000 | $791,000 | 30.000% | % | (7) | 7.35 | 2/27-9/31 | |||

| Class X-A | AAAsf/AAA(sf)/AAA(sf) | $863,881,000 | (9) | $836,737,000 | (9) | $27,144,000 | (9) | N/A | % | Variable IO(10) | N/A | N/A |

| Class A-S | AAAsf/AAA(sf)/AAA(sf) | $93,541,000 | $90,602,000 | $2,939,000 | 21.500% | % | (7) | 9.88 | 1/32-1/32 | |||

| Class B | AA-sf/AA+(sf)/AA(sf) | $52,273,000 | $50,631,000 | $1,642,000 | 16.750% | % | (7) | 9.95 | 1/32-2/32 | |||

| Class C | A-sf/A+(sf)/A-(sf) | $49,522,000 | $47,966,000 | $1,556,000 | 12.250% | % | (7) | 9.96 | 2/32-2/32 | |||

| Non-Offered Pooled Certificates(11) | ||||||||||||

| Class X-B | A-sf/A+(sf)/AAA(sf) | $101,795,000 | (9) | $98,597,000 | (9) | $3,198,000 | (9) | N/A | % | Variable IO(10) | N/A | N/A |

| Class X-D | BBB-sf/BBB-(sf)/BBB-(sf) | $55,024,000 | (9) | $53,295,000 | (9) | $1,729,000 | (9) | N/A | % | Variable IO(10) | N/A | N/A |

| Class X-F | BB+sf/BB+(sf)/BB+(sf) | $13,756,000 | (9) | $13,324,000 | (9) | $432,000 | (9) | N/A | % | Variable IO(10) | N/A | N/A |

| Class X-G | NR/BB-(sf)/NR | $17,883,000 | (9) | $17,321,000 | (9) | $562,000 | (9) | N/A | % | Variable IO(10) | N/A | N/A |

| Class X-H | NR/B-(sf)/NR | $23,385,000 | (9) | $22,650,000 | (9) | $735,000 | (9) | N/A | % | Variable IO(10) | N/A | N/A |

| Class X-J | NR/NR/NR | $24,761,779 | (9) | $23,983,323 | (9) | $778,456 | (9) | N/A | % | Variable IO(10) | N/A | N/A |

| Class D | BBBsf/BBB+(sf)/BBB+(sf) | $31,639,000 | $30,645,000 | $994,000 | 9.375% | % | (7) | 9.96 | 2/32-2/32 | |||

| Class E | BBB-sf/BBB-(sf)/BBB-(sf) | $23,385,000 | $22,650,000 | $735,000 | 7.250% | % | (7) | 9.96 | 2/32-2/32 | |||

| Class F | BB+sf/BB+(sf)/BB+(sf) | $13,756,000 | $13,324,000 | $432,000 | 6.000% | % | (7) | 9.96 | 2/32-2/32 | |||

| Class G | NR/BB-(sf)/NR | $17,883,000 | $17,321,000 | $562,000 | 4.375% | % | (7) | 9.96 | 2/32-2/32 | |||

| Class H | NR/B-(sf)/NR | $23,385,000 | $22,650,000 | $735,000 | 2.250% | % | (7) | 9.96 | 2/32-2/32 | |||

| Class J | NR/NR/NR | $24,761,779 | $23,983,323 | $778,456 | 0.000% | % | (7) | 9.96 | 2/32-2/32 | |||

| Class S(12) | N/A | N/A | N/A | N/A | N/A | N/A | N/A | N/A | ||||

| Class R(12) | N/A | N/A | N/A | N/A | N/A | N/A | N/A | N/A | ||||

| Non-Offered Vertical Risk Retention Interest (11) | ||||||||||||

| Uncertificated VRR Interest(13) | NR/NR/NR | $21,521,930 | (13) | N/A | N/A | (14) | %(15) | (15) | 8.84 | 3/22-2/32 | ||

| Non-Offered Loan-Specific Certificates(11)(16) | ||||||||||||

| 360 Rosemary | (DBRS)* | |||||||||||

| Class 360A | AA(low)(sf) | $20,750,000 | N/A | N/A | 43.085% | % | (17) | 9.96 | 2/32-2/32 | |||

| Class 360X | A(sf) | $39,245,000 | N/A | N/A | N/A | % | Variable IO(17) | N/A | N/A | |||

| Class 360B | A(low)(sf) | $18,495,000 | N/A | N/A | 33.130% | % | (17) | 9.96 | 2/32-2/32 | |||

| Class 360C | BBB(low)(sf) | $18,650,000 | N/A | N/A | 23.093% | % | (17) | 9.96 | 2/32-2/32 | |||

| Class 360D | BB(low)(sf) | $17,919,000 | N/A | N/A | 13.449% | % | (17) | 9.96 | 2/32-2/32 | |||

| Class 360E | B(low)(sf) | $18,838,000 | N/A | N/A | 3.310% | % | (17) | 9.96 | 2/32-2/32 | |||

| Class 360RR(18) | NR | $6,150,000 | N/A | N/A | 0.000% | % | (17) | 9.96 | 2/32-2/32 | |||

| 111 River Street | (KBRA)* | |||||||||||

| Class 111A | AA-(sf) | $11,837,000 | N/A | N/A | 41.489% | % | (17) | 4.96 | 2/27-2/27 | |||

| Class 111B | A-(sf) | $13,826,000 | N/A | N/A | 32.023% | % | (17) | 4.96 | 2/27-2/27 | |||

| Class 111C | BBB-(sf) | $16,738,000 | N/A | N/A | 20.563% | % | (17) | 4.96 | 2/27-2/27 | |||

| Class 111D | BB-(sf) | $17,465,000 | N/A | N/A | 8.606% | % | (17) | 4.96 | 2/27-2/27 | |||

| Class 111E | B(sf) | $12,569,000 | N/A | N/A | 0.000% | % | (17) | 4.96 | 2/27-2/27 | |||

| 111RR Interest(19) | NR | $3,815,000 | N/A | N/A | (20) | %(21) | (21) | 4.96 | 2/27-2/27 | |||

| * | It is a condition of issuance that the offered certificates and certain classes of non-offered certificates receive the ratings set forth above. The anticipated ratings shown are those of S&P Global Ratings, a Standard & Poor’s Financial Services LLC business (“S&P”), Fitch Ratings, Inc. (“Fitch”), Kroll Bond Rating Agency, LLC (“KBRA”) and DBRS, Inc. (“DBRS”), as indicated. Subject to the discussion under “Ratings” in the Preliminary Prospectus, the ratings on the certificates address the likelihood of the timely receipt by holders of all payments of interest to which they are entitled on each distribution date and, except in the case of the interest only certificates, the ultimate receipt by holders of all payments of principal to which they are entitled on or before the applicable rated final distribution date. Certain nationally recognized statistical rating organizations, as defined in Section 3(a)(62) of the Securities Exchange Act of 1934, as amended, that were not hired by the depositor may use information they receive pursuant to Rule 17g-5 under the Securities Exchange Act of 1934, as amended, or otherwise to rate the offered certificates. We cannot assure you as to what ratings a non-hired nationally recognized statistical rating organization would assign. See “Risk Factors—Other Risks Relating to the Certificates— Nationally Recognized Statistical Rating Organizations May Assign Different Ratings to the Certificates; Ratings of the Certificates Reflect Only the Views of the Applicable Rating Agencies as of the Dates Such Ratings Were Issued; Ratings May Affect ERISA Eligibility; Ratings May Be Downgraded” in the Preliminary Prospectus. S&P, Fitch, KBRA and DBRS have informed us that the “sf” designation in the ratings represents an identifier of structured finance product ratings. For additional information about this identifier, prospective investors can go to the related rating agency’s website. The depositor and the underwriters have not verified, do not adopt and do not accept responsibility for any statements made by the rating agencies on those websites. Credit ratings referenced throughout this Term Sheet are forwardlooking opinions about credit risk and express a rating agency’s opinion about the willingness and ability of an issuer of securities to meet its financial obligations in full and on time. Ratings are not indications of investment merit and are not buy, sell or hold recommendations, a measure of asset value or an indication of the suitability of an investment. |

| (1) | Approximate, subject to a variance of plus or minus 5% and further subject to any additional variances described in the footnotes below. In addition, the notional amounts of the Class X-A, Class X-B, Class X-D, Class X-F, Class X-G, Class X-H and Class X-J certificates (the “pooled Class X certificates”) may vary depending upon the final pricing of the classes of pooled principal balance certificates (as defined in footnote (7) below) whose certificate balances comprise such notional amounts, and, if as a result of such pricing (a) the pass-through rate of any class of pooled Class X certificates, as applicable, would be equal to zero at all times, such class of certificates will not be issued on the closing date of this securitization or (b) the pass-through rate of any class of pooled principal balance certificates whose certificate balance comprises |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 3 | ||

| Structural and Collateral Term Sheet | BMO 2022-C1 | |

| Indicative Capital Structure | ||

such notional amount is at all times equal to the weighted average of the net interest rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as in effect from time to time, the certificate balance of such class of pooled principal balance certificates may not be part of, and there would be a corresponding reduction in, such notional amount of the related class of pooled Class X certificates.

| (2) | On the closing date for this transaction, SSOF SCRE AIV, L.P. as “retaining sponsor” (as such term is defined in Regulation RR) for this securitization, is expected to satisfy its risk retention obligations by: (i) causing a “majority-owned affiliate” (as defined in Regulation RR) to purchase an “eligible vertical interest” (as defined in Regulation RR), in the form of certificates (collectively referred to herein as the “Sabal VRR Interest Portion”) (x) representing approximately 3.1421% of the initial certificate balance, notional amount or percentage interest, as applicable, of each class of pooled certificates (as defined in footnote (7) below), other than the Class R Certificates, as set forth in the table above under “Approximate Initial Retained Certificate Balance, Notional Amount or Percentage Interest” and (y) representing approximately 3.08184% of the aggregate principal balance of all the “ABS Interests” (as described below), and (ii) causing one or more other retaining parties to acquire from the depositor, on the closing date for this transaction, additional portions of an “eligible vertical interest” in the form of a “single vertical security” with an initial principal balance of approximately $21,521,930 (the “Combined Uncertificated VRR Interest” and, together with the interest described in sub-clause (i)(y) above, the “Aggregate VRR”), which Aggregate VRR is expected to represent at least 5% of the aggregate principal balance of all the “ABS interests” (i.e., the sum of the aggregate initial certificate balance of all of the pooled certificates (other than the Class R certificates) and the initial principal balance of the Uncertificated VRR Interest) issued by the issuing entity on the closing date for this transaction, as described under “Credit Risk Retention”. The Combined Uncertificated VRR Interest will consist solely of the “Uncertificated VRR Interest” (as defined under “Credit Risk Retention”). The Combined Uncertificated VRR Interest will be retained by certain retaining parties in accordance with the credit risk retention rules applicable to this securitization transaction. “Eligible vertical interest” and “single vertical security” will have the meanings given to such terms in Regulation RR. See “Credit Risk Retention” in the preliminary prospectus. The Combined Uncertificated VRR Interest is not offered hereby. |

| (3) | “Approximate Initial Credit Support” means, with respect to any class of non-uncertificated VRR retained pooled principal balance certificates (as defined in footnote (7) below), the quotient, expressed as a percentage, of (i) the aggregate of the initial certificate balances of all classes of non-uncertificated VRR retained pooled principal balance certificates, if any, junior to such class of non-uncertificated VRR retained pooled principal balance certificates, divided by (ii) the aggregate of the initial certificate balances of all classes of non-uncertificated VRR retained pooled principal balance certificates. The approximate initial credit support percentages set forth for the Class A-1, Class A-2, Class A-3, Class A-4, Class A-5 and Class A-AB certificates are represented in the aggregate. The approximate initial credit support percentage shown for each class of non-uncertificated VRR retained pooled principal balance certificates does not take into account the subordination provided by any trust subordinate companion loan (as defined in footnote (16) below), provided that payments on each trust subordinate companion loan are generally subordinate to payments on the related senior loans in the related loan combination as and to the extent provided in the related co-lender agreement. The approximate initial credit support percentages shown in the table above with respect to the non-uncertificated VRR retained pooled principal balance certificates do not take into account the Combined Uncertificated VRR Interest. |

| (4) | “Approximate Initial Credit Support” means, with respect to any class of loan-specific principal balance certificates (as defined in footnote (16) below), the quotient, expressed as a percentage, of (i) the aggregate of the initial certificate balances of all classes of loan-specific principal balance certificates backed by the same trust subordinate companion loan as the subject class of loan-specific principal balance certificates, if any, junior to the subject class of loan-specific certificates, divided by (ii) the sum of (A) the aggregate of the initial certificate balances of all classes of loan-specific principal balance certificates backed by the same trust subordinate companion loan as the subject class of loan-specific principal balance certificates and (B) (x) with respect to the 111 River Street loan-specific certificates (as defined in footnote (16) below), approximately 95% of the aggregate outstanding principal balance of the senior loans included in the 111 River Street loan combination as of the cut-off date and (y) with respect to the 360 Rosemary loan-specific certificates (as defined in footnote (16) below), the aggregate outstanding principal balance of the senior loans included in 360 Rosemary loan combination, in each case as of the cut-off date. The approximate initial credit support percentages shown in the table above with respect to the 111 River Street loan-specific principal balance certificates do not take into account the 111RR Interest. |

| (5) | Approximate per annum rate as of the closing date. |

| (6) | Determined assuming no prepayments prior to the maturity date or any anticipated repayment date, as applicable, for any mortgage loan or trust subordinate companion loan and based on the modeling assumptions described under “Yield, Prepayment and Maturity Considerations” in the preliminary prospectus. |

| (7) | For any distribution date, the pass-through rate for each class of the Class A-1, Class A-2, Class A-3, Class A-4, Class A-5, Class A-AB, Class A-S, Class B, Class C, Class D, Class E, Class F, Class G, Class H and Class J certificates (collectively, the “pooled principal balance certificates” or the “non-uncertificated VRR retained pooled principal balance certificates”), and collectively with the pooled Class X certificates, the Class S certificates and the Class R certificates, the “pooled certificates” or “non-uncertificated VRR retained pooled certificates”) will generally be equal to one of (i) a fixed per annum rate, (ii) the weighted average of the net interest rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as in effect from time to time, (iii) a rate equal to the lesser of a specified per annum rate and the weighted average rate described in clause (ii), or (iv) the weighted average rate described in clause (ii) less a specified percentage, but no less than 0.000%. The trust subordinate companion loans will not be taken into account in determining pass-through rates on the non-uncertificated VRR retained pooled principal balance certificates. See “Description of the Certificates—Distributions—Pass-Through Rates” in the preliminary prospectus. |

| (8) | The exact initial certificate balances of the Class A-4 and Class A-5 certificates are unknown and will be determined based on the final pricing of those classes of certificates. However, the respective initial certificate balances (and corresponding available and retained portions thereof), weighted average lives and principal windows of the Class A-4 and Class A-5 certificates are expected to be within the applicable ranges reflected in the following chart. The aggregate initial certificate balance of the Class A-4 and Class A-5 certificates is expected to be approximately $509,661,000 subject to a variance of plus or minus 5%. |

Class of Certificates | Expected Range of Initial Certificate Balances | Expected Range of Initial Available Certificate Balances | Expected Range of Initial Retained Certificate Balances | Expected Range of Weighted Avg. Lives (Yrs) | Expected Range of Principal Windows |

| Class A-4 | $0 - $206,488,000 | $0 - $200,000,000 | $0 - $6,488,000 | N/A - 9.75 | N/A - 9/31-12/31 |

| Class A-5 | $303,173,000 - $509,661,000 | $293,647,000 - $493,647,000 | $9,526,000 - $16,014,000 | 9.87 - 9.82 | 12/31-1/32 - 9/31-1/32 |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 4 | ||

| Structural and Collateral Term Sheet | BMO 2022-C1 | |

| Indicative Capital Structure | ||

| (9) | The pooled Class X certificates will not have certificate balances and will not be entitled to receive distributions of principal. Interest will accrue on each class of pooled Class X certificates at the related pass through rate based upon the related notional amount. The notional amount of each class of the pooled Class X certificates will be equal to the certificate balance or the aggregate of the certificate balances, as applicable, from time to time of the class or classes of the non-uncertificated VRR retained pooled principal balance certificates identified in the same row as such class of pooled Class X certificates in the chart below (as to such class of pooled Class X certificates, the “corresponding pooled principal balance certificates”): |

| Class of Pooled Class X Certificates | Class(es) of Corresponding Pooled Principal Balance Certificates |

| Class X-A | Class A-1, Class A-2, Class A-3, Class A-4, Class A-5, Class A-AB and Class A-S |

| Class X-B | Class B and Class C |

| Class X-D | Class D and Class E |

| Class X-F | Class F |

| Class X-G | Class G |

| Class X-H | Class H |

| Class X-J | Class J |

| (10) | The pass-through rate for each class of pooled Class X certificates will generally be a per annum rate equal to the excess, if any, of (i) the weighted average of the net interest rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as in effect from time to time, over (ii) the pass-through rate (or, if applicable, the weighted average of the pass-through rates) of the class or classes of corresponding pooled principal balance certificates as in effect from time to time, as described in the preliminary prospectus. |

| (11) | The classes of certificates set forth below “Non-Offered Pooled Certificates”, “Non-Offered Vertical Risk Retention Interest” and “Non-Offered Loan-Specific Certificates” in the table are not offered hereby. |

| (12) | Neither the Class S certificate nor the Class R certificates will have a certificate balance, notional amount, pass-through rate, rating or rated final distribution date. A specified portion of the excess interest accruing after the related anticipated repayment date on any mortgage loan with an anticipated repayment date will, to the extent collected, be allocated to the Class S certificates as set forth in “Description of the Certificates—Distributions—Excess Interest”. The Class R certificates will represent the residual interests in each of four separate REMICs, as further described in the preliminary prospectus. The Class R certificates will not be entitled to distributions of principal or interest. |

| (13) | Constitutes the Combined Uncertificated VRR Interest Balance, which consists solely of the principal balance of the Uncertificated VRR Interest. |

| (14) | Although the approximate initial credit support percentages shown in the table above with respect to the non-uncertificated VRR retained pooled principal balance certificates do not take into account the Combined Uncertificated VRR Interest, losses incurred on the mortgage loans will be allocated between the Combined Uncertificated VRR Interest, on the one hand, and the non-uncertificated VRR retained pooled principal balance certificates, on the other hand, pro rata in accordance with the principal balance of the Combined Uncertificated VRR Interest and the aggregate outstanding certificate balance of the non-uncertificated VRR retained principal balance certificates. See “Credit Risk Retention” and “Description of the Certificates” in the preliminary prospectus. The non-uncertificated VRR retained pooled principal balance certificates are also collectively referred to as the “pooled principal balance certificates”. |

| (15) | Although it does not have a specified pass-through rate (other than for tax reporting purposes), the effective interest rate for the Combined Uncertificated VRR Interest will be the weighted average of the net mortgage interest rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as in effect from time to time. |

| (16) | The Class 360A, Class 360X, Class 360B, Class 360C, Class 360D, Class 360E and Class 360RR certificates are collectively referred to as the “360 Rosemary loan-specific certificates”, and the Class 111A, Class 111B, Class 111C, Class 111D, and Class 111E certificates are collectively referred to as the “111 River Street loan-specific certificates” (which were issued together with the Uncertificated 111RR Interest). The 360 Rosemary loan-specific certificates and 111 River Street loan-specific certificates collectively constitute the “loan-specific certificates”. The Class 360A, Class 360B, Class 360C, Class 360D, Class 360E and Class 360RR certificates (the foregoing, collectively, the “360 Rosemary loan-specific principal balance certificates”) and the Class 111A, Class 111B, Class 111C, Class 111D and Class 111E certificates (the foregoing, collectively, the “111 River Street loan-specific principal balance certificates”), collectively constitute the “loan-specific principal balance certificates” (and, collectively with the pooled principal balance certificates, constitute the “principal balance certificates”). The Class 360X certificates, together with the pooled Class X certificates, collectively constitute the “Class X certificates”). The loan-specific certificates will only be entitled to receive distributions from, and will only incur losses with respect to, the 360 Rosemary trust subordinate companion loan or the 111 River Street trust subordinate companion loan (each, a “trust subordinate companion loan” and collectively, the “trust subordinate companion loans”), as applicable. Each trust subordinate companion loan will be included as an asset of the issuing entity but will not be part of the mortgage pool backing the pooled certificates. No class of pooled certificates will have any interest in either trust subordinate companion loan. See “Description of the Mortgage Pool—The Loan Combinations—The 360 Rosemary Pari Passu-AB Loan Combination” and “—The 111 River Street Pari Passu-AB Loan Combination” in the preliminary prospectus. |

| (17) | The pass-through rates for the loan-specific principal balance certificates, in each case, will equal one of the following per annum rates: (i) a fixed rate, (ii) the net mortgage rate (adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) on the related trust subordinate companion loan, (iii) the lesser of a specified rate and the net mortgage rate on the trust subordinate companion loan described in clause (ii), or (iv) the net mortgage rate on the related trust subordinate companion loan described in clause (ii) less a specified rate. The pass-through rate with respect to the Class 360X certificates will be a per annum rate equal to the excess, if any of, (i) the net mortgage rate (adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) on the related trust subordinate companion loan as in effect from time to time, over (ii) the weighted average of the pass-through rates of the Class 360A and Class 360B certificates in effect from time to time, as described in the preliminary prospectus. See “Description of the Certificates—Distributions—Pass-Through Rates” in the preliminary prospectus. |

| (18) | Bank of Montreal is the only sponsor (and will act as “retaining sponsor” (as such term is defined in Regulation RR)), with respect to the securitization transaction constituted by the issuance of the 360 Rosemary loan-specific certificates. In connection therewith, the Class 360RR certificates (the “360 Rosemary Loan-Specific HRR Certificates”) will be purchased and retained by a third party purchaser contemplated by Rule 7 of Regulation RR (the “360 Rosemary Retaining Third Party Purchaser”), in accordance with the credit risk retention rules applicable to the securitization transaction constituted by the issuance of the 360 Rosemary loan-specific certificates. |

| (19) | Bank of Montreal is the only sponsor (and will act as “retaining sponsor” (as such term is defined in Regulation RR)) with respect to the securitization transaction constituted by the issuance of the 111 River Street loan-specific certificates and the 111RR Interest. In connection therewith, Bank of Montreal is expected to acquire from the depositor on the closing date an “eligible vertical interest” (as such term is defined in Regulation RR) in the form of an uncertificated interest with an initial principal balance of approximately $3,815,000 (the “111RR Interest”), which is expected to represent approximately 5.0% of the aggregate initial principal balance of all 111 River Street loan-specific certificates and the 111RR Interest. The 111RR Interest is expected to be retained by Bank of Montreal or its “majority-owned affiliate” (as such term is defined in Regulation RR) in accordance with the credit risk retention rules applicable to such securitization transaction. The 111RR Interest is not a class of certificates and is not offered hereby. |

| (20) | Although the approximate initial credit support percentages shown in the table with respect to the 111 River Street loan-specific certificates do not take into account the 111RR Interest, losses incurred on the 111 River Street trust subordinate companion loan will be allocated between the 111RR Interest, on the one hand, and the other classes of 111 River Street loan-specific certificates, on the other hand, pro rata in accordance with their respective outstanding principal balances. |

| (21) | Except for tax reporting purposes, the 111RR Interest does not have a specified pass-through rate; however, the effective interest rate on the 111RR Interest will be a per annum rate equal to the net mortgage rate (adjusted, if necessary, to accrue interest on the basis of a 360-day year consisting of twelve 30-day months) as in effect from time to time on the related trust subordinate companion loan. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 5 | ||

| Structural and Collateral Term Sheet | BMO 2022-C1 | |

| Summary of Transaction Terms | ||

| Securities Offered: | $965,676,000 monthly pay, multi-class, commercial mortgage REMIC Pass-Through Certificates. |

| Co-Lead Managers and Joint Bookrunners: | BMO Capital Markets Corp., Deutsche Bank Securities Inc. and KeyBanc Capital Markets Inc. |

| Co-Managers: | Bancroft Capital, LLC and Drexel Hamilton, LLC |

| Mortgage Loan Sellers: | Bank of Montreal (“BMO”) (36.2%), Starwood Mortgage Capital LLC (“SMC”) (19.6%), KeyBank National Association (“KeyBank”) (18.0%), SSOF SCRE AIV, L.P. (“Sabal”) (13.1%), German American Capital Corporation (“GACC”) (9.4%) and BMO/SMC (3.6%). |

| Master Servicer: | KeyBank National Association. |

| Special Servicers: | CWCapital Asset Management LLC (with respect to all serviced loans other than the 360 Rosemary mortgage loan and the 111 River Street mortgage loan), Situs Holdings LLC (solely with respect to the 360 Rosemary mortgage loan) and KeyBank National Association (solely with respect to the 111 River Street mortgage loan) |

| Directing Holder/Controlling Class Representative: | Sabal Strategic Opportunities Fund, L.P. |

| Trustee: | Wilmington Trust, National Association. |

| Certificate Administrator: | Computershare Trust Company, National Association. |

| Operating Advisor: | Park Bridge Lender Services LLC. |

| Asset Representations Reviewer: | Park Bridge Lender Services LLC. |

| Rating Agencies: | Standard and Poor’s (“S&P”), Fitch Ratings, Inc. (“Fitch”) and Kroll Bond Rating Agency, LLC (“KBRA”). |

| U.S. Credit Risk Retention: | For a discussion on the manner in which SSOF SCRE AIV, L.P. as retaining sponsor, intends to satisfy the U.S. credit risk retention requirements, see “Credit Risk Retention” in the Preliminary Prospectus. |

| EU Credit Risk Retention: | The transaction is not structured to satisfy the EU risk retention and due diligence requirements. |

| Closing Date: | On or about February 28, 2022. |

| Cut-off Date: | With respect to each mortgage loan, the related due date in February 2022, or in the case of any mortgage loan that has its first due date after February 2022, the date that would have been its due date in February 2022 under the terms of that mortgage loan if a monthly debt service payment were scheduled to be due in that month. |

| Distribution Date: | The 4th business day after the Determination Date in each month, commencing in March 2022. |

| Determination Date: | 11th day of each month, or if the 11th day is not a business day, the next succeeding business day, commencing in March 2022. |

| Assumed Final Distribution Date: | The Distribution Date in February 2032 which is the latest anticipated repayment date of the Certificates. |

| Rated Final Distribution Date: | The Distribution Date in February 2055. |

| Tax Treatment: | The Publicly Offered Certificates are expected to be treated as REMIC “regular interests” for U.S. federal income tax purposes. |

| Form of Offering: | The Class A-1, Class A-2, Class A-3, Class A-4, Class A-5, Class A-AB, Class X-A, Class A-S, Class B and Class C Certificates (the “Publicly Offered Certificates”) will be offered publicly. The Class X-B, Class X-D, Class X-F, Class X-G, Class X-H, Class X-J, Class D, Class E, Class F, Class G, Class H, Class J, Class S and Class R Certificates (the “Privately Offered Certificates”) will be offered domestically to Qualified Institutional Buyers and to Institutional Accredited Investors (other than the Class R Certificates) and to institutions that are not U.S. Persons pursuant to Regulation S. |

| SMMEA Status: | The Certificates will not constitute “mortgage related securities” for purposes of SMMEA. |

| ERISA: | The Publicly Offered Certificates are expected to be ERISA eligible. |

| Optional Termination: | On any Distribution Date on which the aggregate principal balance of the pool of mortgage loans is less than 1% of the aggregate principal balance of the mortgage loans as of the cut-off date (solely for the purposes of this calculation, if such right is being exercised after the distribution date in February 2032 and the Coleman Highline Phase IV mortgage loan is still an asset of the issuing entity, then such mortgage loan will be excluded from the then-aggregate stated principal balance of the pool of mortgage loans and from the initial pool balance), certain entities specified in the Preliminary Prospectus will have the option to purchase all of the remaining mortgage loans (and all property acquired through exercise of remedies in respect of any mortgage loan) at the price specified in the Preliminary Prospectus. Refer to “Pooling and Servicing Agreement—Termination; Retirement of Certificates” in the Preliminary Prospectus. |

| Minimum Denominations: | The Publicly Offered Certificates (other than the Class X-A and Class X-B Certificates) will be issued in minimum denominations of $10,000 and integral multiples of $1 in excess of $10,000. The Class X-A and Class X-B Certificates will be issued in minimum denominations of $1,000,000 and in integral multiples of $1 in excess of $1,000,000. |

| Settlement Terms: | DTC, Euroclear and Clearstream Banking. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 6 | ||

| Structural and Collateral Term Sheet | BMO 2022-C1 | |

| Summary of Transaction Terms | ||

| Analytics: | The transaction is expected to be modeled by Intex Solutions, Inc. and Trepp, LLC and is expected to be available on Bloomberg, L.P., BlackRock Financial Management, Inc., CMBS.com, Inc., Moody’s Analytics, Markit Group Limited, RealINSIGHT, Thompson Reuters Corporation, Intercontinental Exchange | ICE Data Services and KBRA Analytics, LLC. |

| Risk Factors: | THE CERTIFICATES INVOLVE CERTAIN RISKS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. REFER TO THE “SUMMARY OF RISK FACTORS” AND “RISK FACTORS” SECTIONS OF THE PRELIMINARY PROSPECTUS. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 7 | ||

| Structural and Collateral Term Sheet | BMO 2022-C1 | |

| Collateral Characteristics | ||

Mortgage Loan Seller | Number of Mortgage Loans | Number of Mortgaged Properties | Aggregate | % of IPB |

| BMO | 19 | 28 | $406,438,584 | 36.2% |

| SMC | 16 | 42 | $220,342,335 | 19.6% |

| KeyBank | 14 | 58 | $201,852,000 | 18.0% |

| Sabal | 24 | 69 | $147,374,790 | 13.1% |

| GACC | 3 | 3 | $106,000,000 | 9.4% |

| BMO/SMC | 1 | 34 | $40,000,000 | 3.6% |

| Total: | 77 | 234 | $1,122,007,709 | 100.0% |

| Loan Pool(1) | ||

| Initial Pool Balance (“IPB”): | $1,122,007,709 | |

| Number of Mortgage Loans: | 77 | |

| Number of Mortgaged Properties: | 234 | |

| Average Cut-off Date Balance per Mortgage Loan: | $14,571,529 | |

| Weighted Average Current Mortgage Rate: | 3.79281% | |

| 10 Largest Mortgage Loans as % of IPB: | 38.0% | |

| Weighted Average Remaining Term to Maturity: | 108 months | |

| Weighted Average Seasoning: | 2 months | |

| Credit Statistics(1) | ||

| Weighted Average UW NCF DSCR(2)(3): | 2.60x | |

| Weighted Average UW NOI Debt Yield(2)(4): | 10.9% | |

| Weighted Average Cut-off Date Loan-to-Value Ratio (“LTV”)(2)(4)(5): | 53.4% | |

| Weighted Average Maturity Date/ARD LTV(2)(5): | 50.8% | |

| Other Statistics | ||

| % of Mortgage Loans with Additional Debt: | 23.3% | |

| % of Mortgage Loans with Single Tenants(6): | 16.7% | |

| % of Mortgage Loans secured by Multiple Properties: | 32.7% | |

| Amortization | ||

| Weighted Average Original Amortization Term(7): | 344 months | |

| Weighted Average Remaining Amortization Term(7): | 342 months | |

| % of Mortgage Loans with Interest-Only: | 69.8% | |

| % of Mortgage Loans with Amortizing Balloon: | 12.0% | |

| % of Mortgage Loans with Partial Interest-Only followed by Amortizing Balloon: | 14.5% | |

| % of Mortgage Loans with Interest-Only followed by ARD-Structure: | 3.7% | |

| Lockboxes(8) | ||

| % of Mortgage Loans with Hard Lockboxes: | 44.6% | |

| % of Mortgage Loans with Springing Lockboxes: | 29.9% | |

| % of Mortgage Loans with Soft Lockboxes: | 9.8% | |

| % of Mortgage Loans with No Lockbox: | 9.4% | |

| % of Mortgage Loans with Springing (Residential); Hard (Commercial) Lockbox: | 3.6% | |

| % of Mortgage Loans with Soft (Residential); Hard (Commercial) Lockbox: | 2.7% | |

| Reserves | ||

| % of Mortgage Loans Requiring Monthly Tax Reserves: | 66.8% | |

| % of Mortgage Loans Requiring Monthly Insurance Reserves: | 55.7% | |

| % of Mortgage Loans Requiring Monthly CapEx Reserves: | 60.6% | |

| % of Mortgage Loans Requiring Monthly TI/LC Reserves(9): | 48.4% | |

| (1) | The Loan Pool includes a cross-collateralized group of loans including Loan Nos. 36 and 37. All metrics to the crossed loans are presented on an aggregate basis. |

| (2) | In the case of Loan Nos. 1, 2, 4, 5, 6, 7, 8, 9, 10, 11, 15, 20 and 22, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date/ARD LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 2, 4, 6, 7, 10 and 22, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date/ARD LTV calculations exclude the related Subordinate Companion Loans. In the case of Loan No. 5, the loan amortizes on a non-standard amortization schedule. Calculations are based on the assumed principal and interest schedule beginning November 2028. |

| (3) | For the mortgage loans that are interest-only for the entire term and accrue interest on an Actual/360 basis, the Monthly Debt Service Amount ($) was calculated as 1/12th of the product of (i) the Original Balance ($), (ii) the Interest Rate % and (iii) 365/360. |

| (4) | In the case of Loan No. 13, the Cut-off Date LTV and UW NOI Debt Yield are based on Cut-off Date Principal Balance after netting out a $1,500,000 holdback reserve. The Cut-off Date LTV and UW NOI Debt Yield based on Cut-off Date Principal Balance without netting out the holdback reserve are 62.7% and 8.6%, respectively. |

| (5) | In the case of Loan Nos. 1, 9, 18 and 23, the Cut-off Date LTV and the Maturity Date/ARD LTV are calculated by using an appraised value based on an as-portfolio assumption. In the case of Loan Nos. 2 and 38 the Cut-off Date LTV and Maturity/ARD LTV are calculated by using an appraised value based on an as stabilized assumption. In the case of Loan No. 20, the Cut-off Date LTV and Maturity LTV are calculated by using an appraised value based on an as complete assumption for 15 of the mortgage properties. In the case of Loan No. 7, the Cut-off Date LTV and Maturity/ARD LTV are calculated by using an appraised value based on a market value assuming present value of ICAP tax savings are excluded and outstanding leasing costs reserved assumption. Refer to “Description of the Mortgage Pool—Certain Calculations and Definitions—Appraised Value” in the Preliminary Prospectus for additional details. |

| (6) | Excludes mortgage loans that are secured by multiple properties with multiple tenants and includes one mortgage loan that is secured by both single-tenant properties and multi-tenant properties. |

| (7) | Excludes 48 mortgage loans that are interest-only for the entire term or until the anticipated repayment date. |

| (8) | For a more detailed description of lockboxes, refer to “Description of the Mortgage Pool—Certain Calculations and Definitions” and “—Certain Terms of the Mortgage Loans—Mortgaged Property Accounts” in the Preliminary Prospectus. |

| (9) | Calculated only with respect to the Cut-off Date Balance of mortgage loans secured or partially secured by office, retail, mixed use, self storage (with commercial space), multifamily (with commercial space), parking garage and industrial properties. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 8 | ||

| Structural and Collateral Term Sheet | BMO 2022-C1 | |

| Collateral Characteristics | ||

| Ten Largest Mortgage Loans | ||||||||||||

| No. | Loan Name | City, State | Mortgage Loan Seller | No. of Prop. | Cut-off Date Balance | % of IPB | Square Feet / Rooms / Units | Property Type | UW NCF DSCR(1) | UW NOI Debt Yield(1) | Cut-off Date LTV(1) | Maturity Date/ARD LTV(1) |

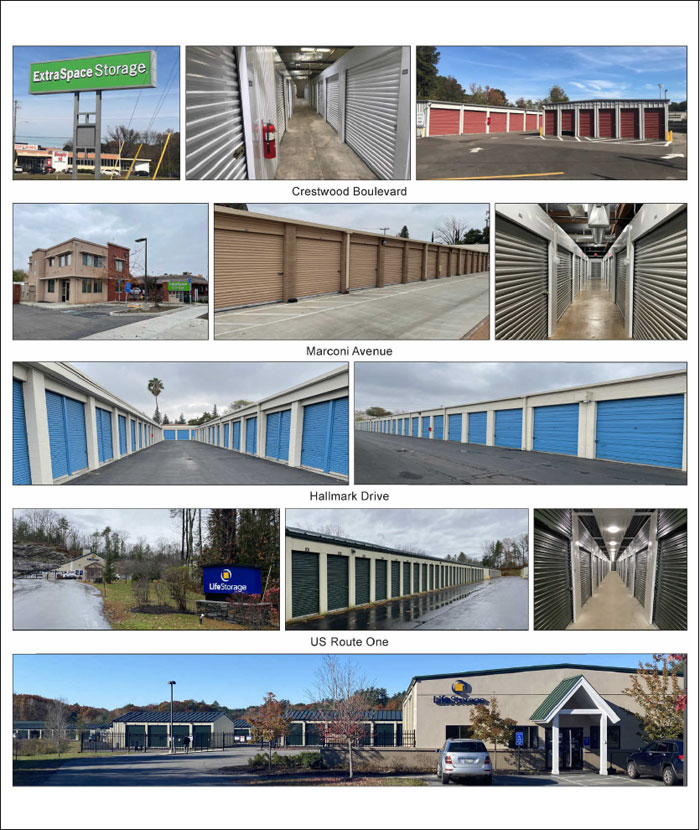

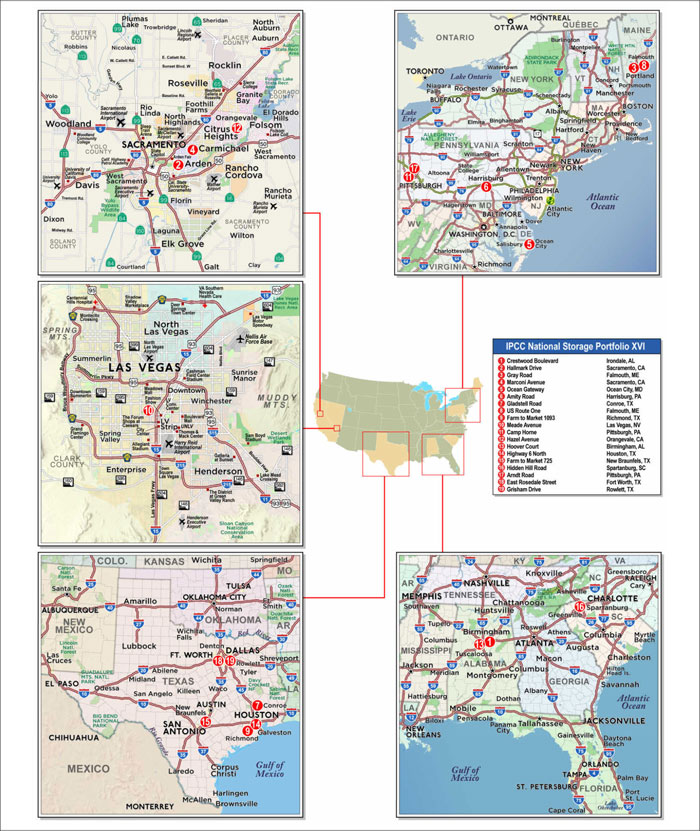

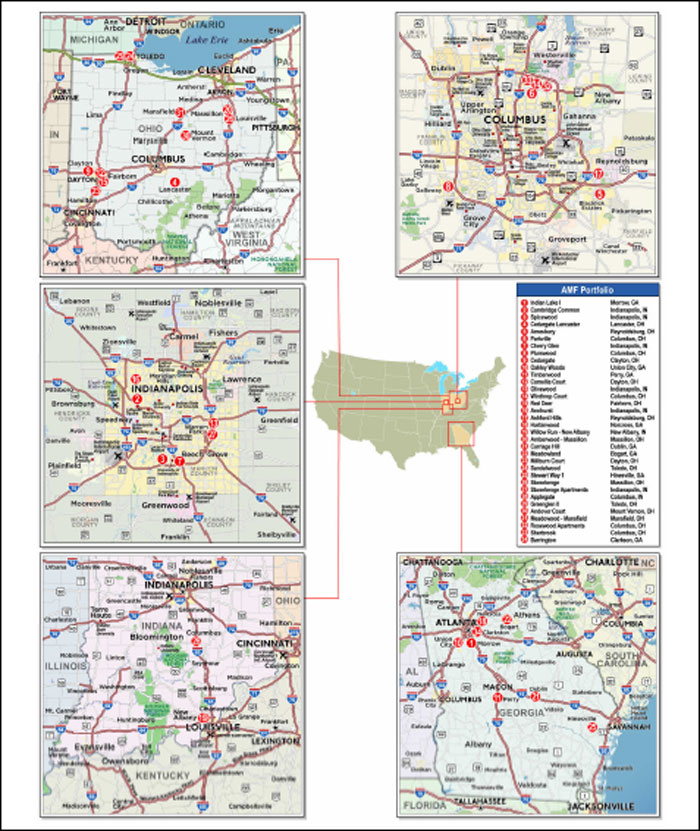

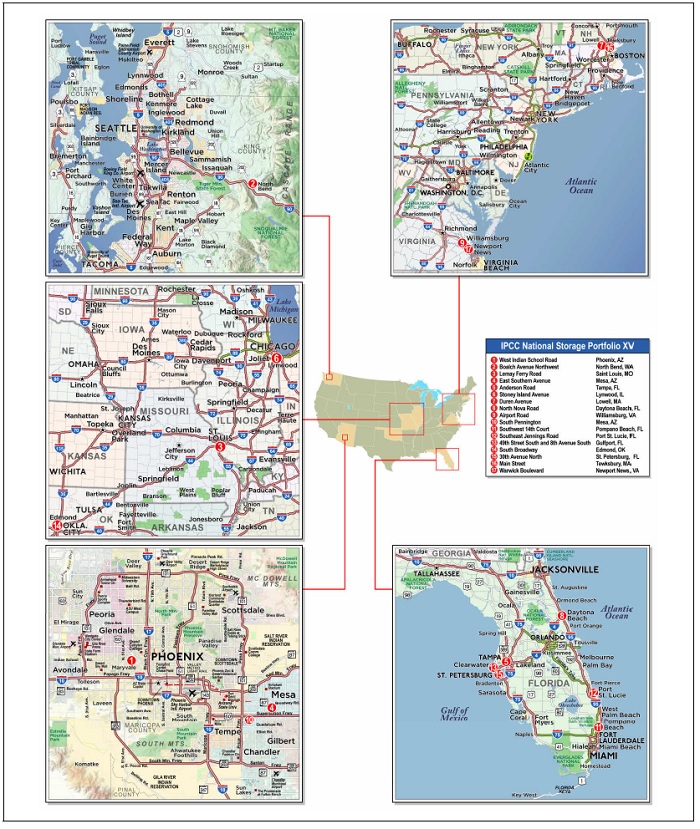

| 1 | IPCC National Storage Portfolio XVI | Various, Various | KeyBank | 19 | $60,000,000 | 5.3% | 1,133,018 | Self Storage | 2.29x | 8.6% | 47.8% | 47.8% |

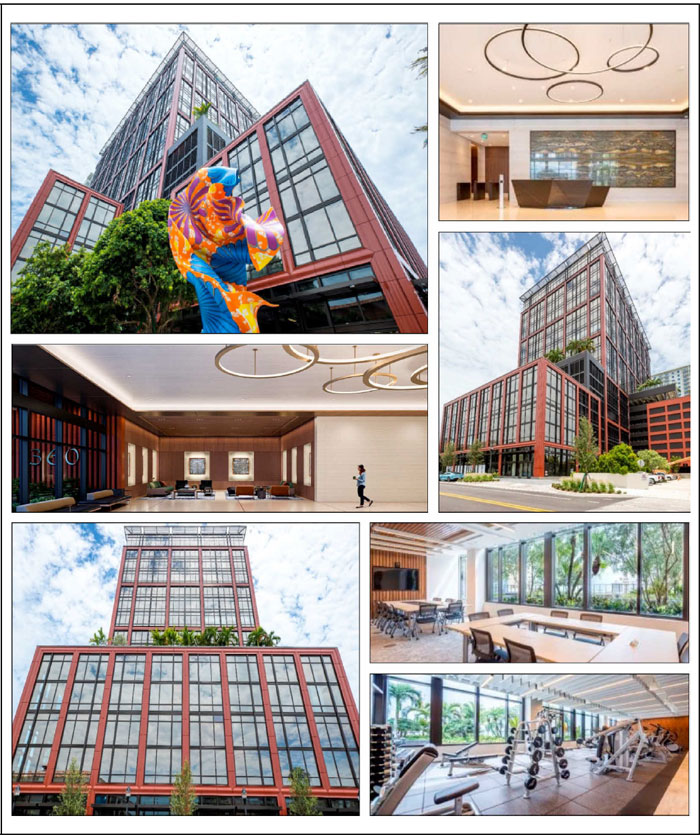

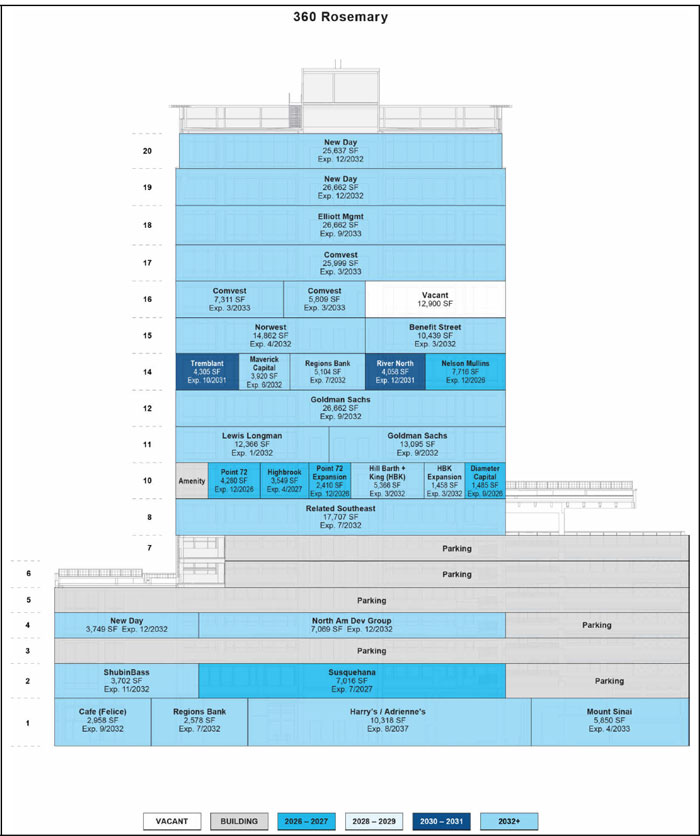

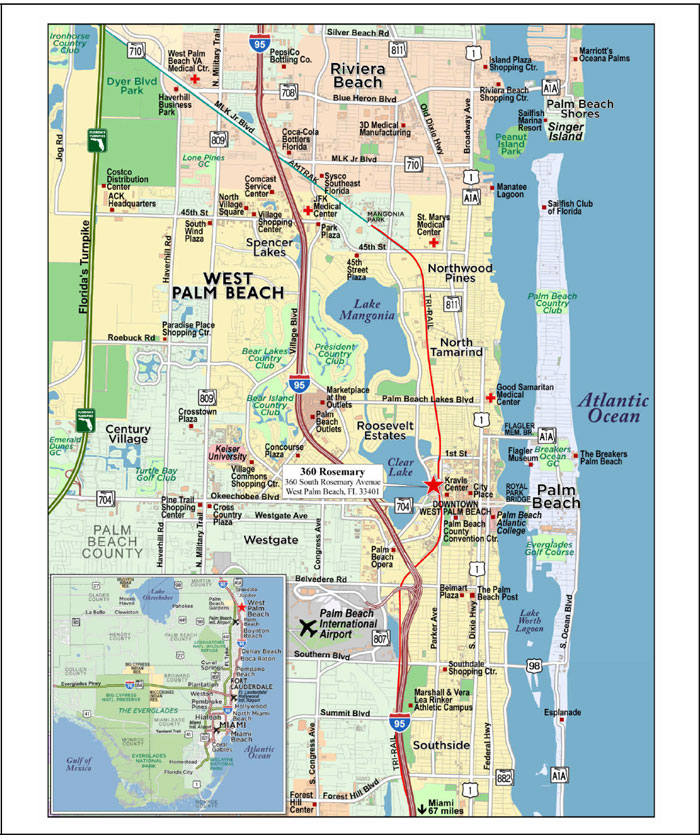

| 2 | 360 Rosemary | West Palm Beach, FL | BMO | 1 | $45,000,000 | 4.0% | 313,002 | Office | 4.35x | 17.8% | 26.6% | 26.6% |

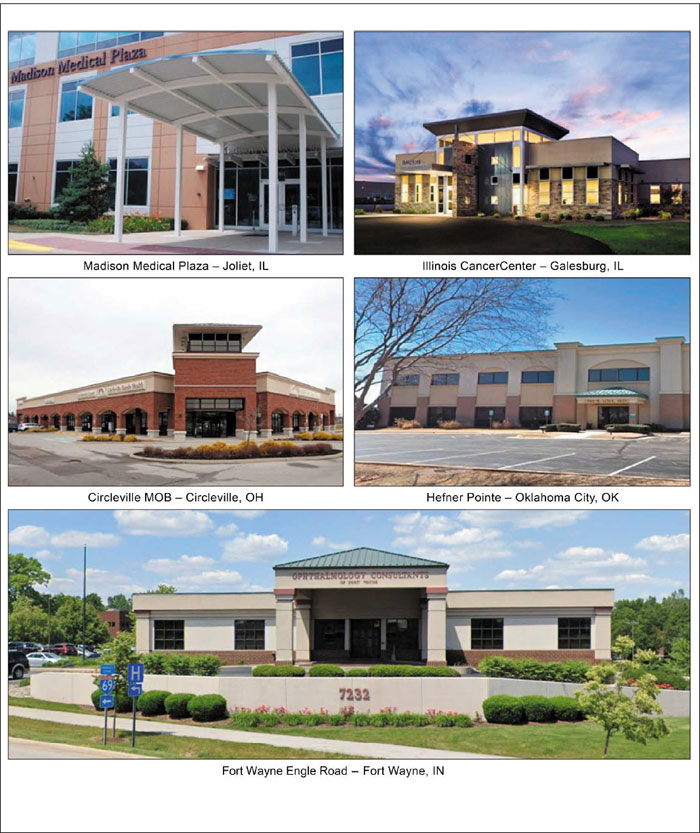

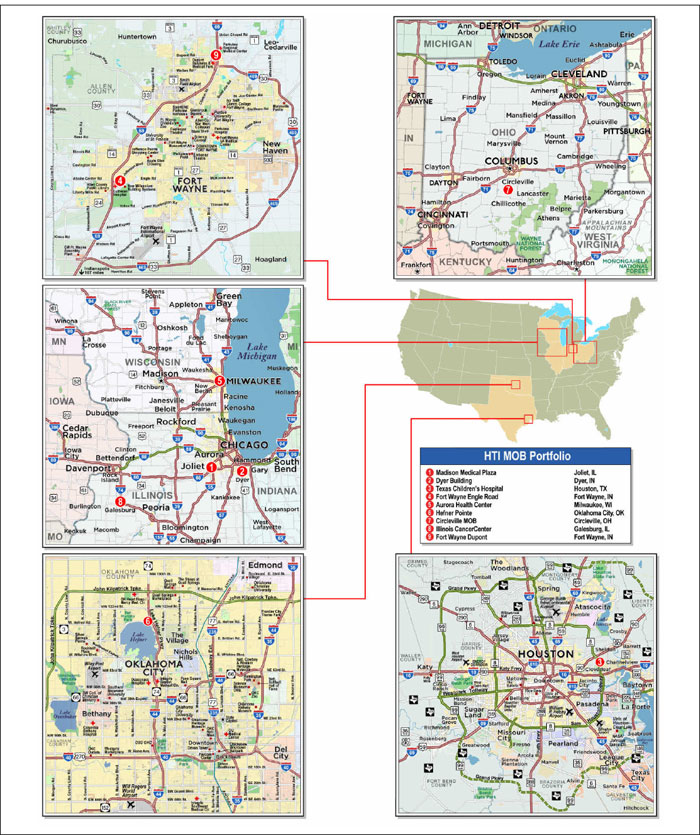

| 3 | HTI MOB Portfolio | Various, Various | BMO | 9 | $42,750,000 | 3.8% | 232,854 | Office | 3.79x | 11.5% | 55.5% | 55.5% |

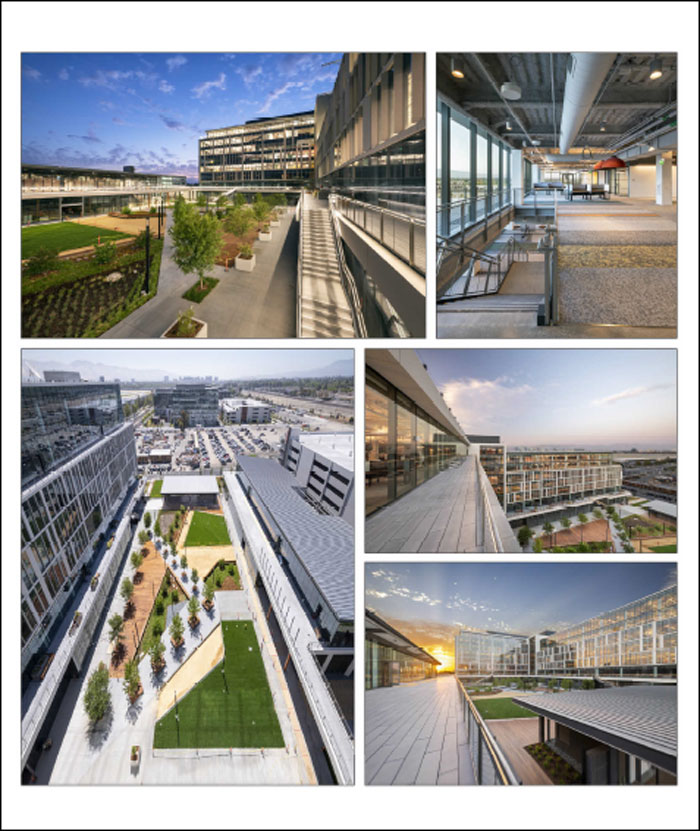

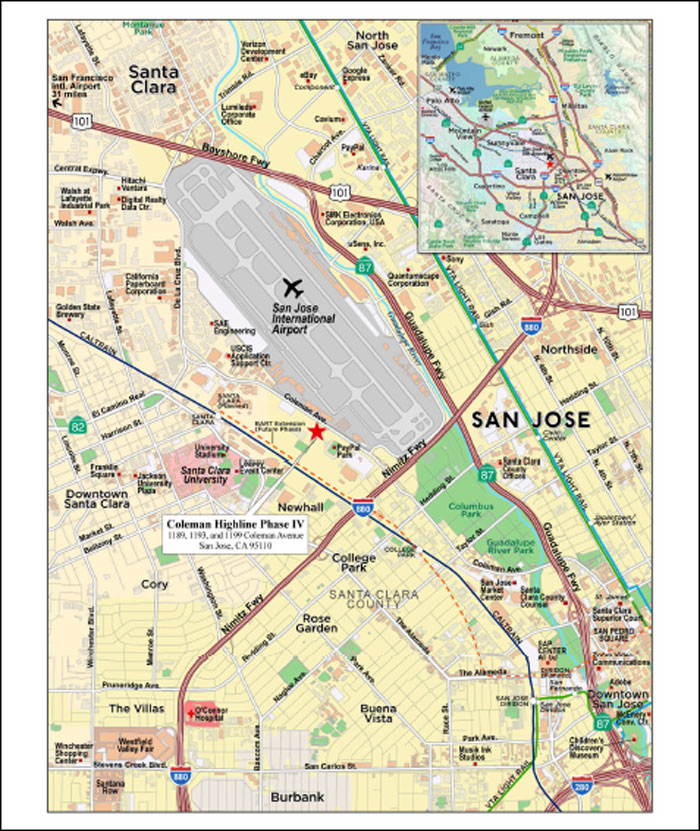

| 4 | Coleman Highline Phase IV | San Jose, CA | BMO | 1 | $41,400,000 | 3.7% | 657,934 | Office | 5.54x | 14.1% | 31.0% | 31.0% |

| 5 | AMF Portfolio | Various, Various | BMO/SMC | 34 | $40,000,000 | 3.6% | 3,299 | Multifamily | 1.51x | 9.8% | 61.3% | 56.9% |

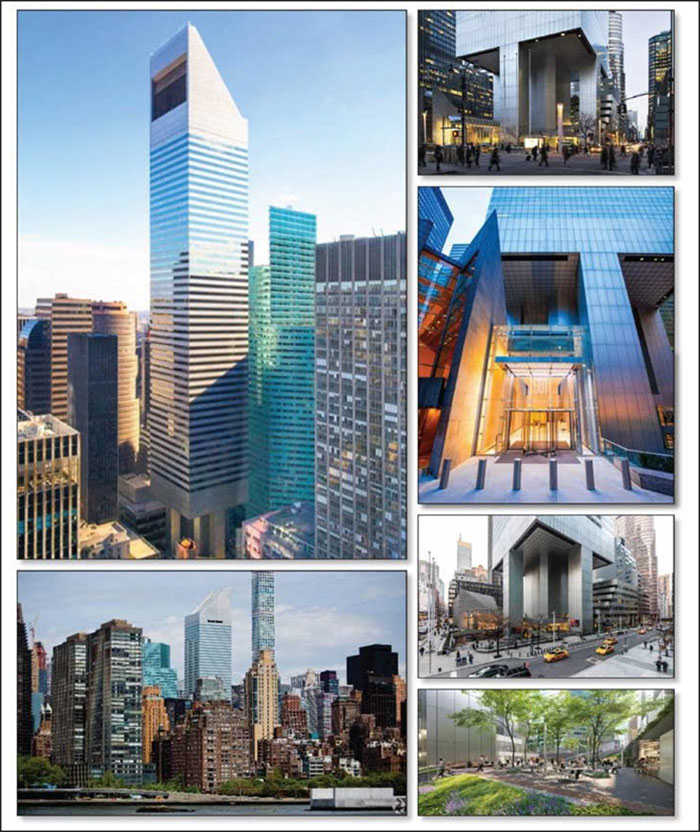

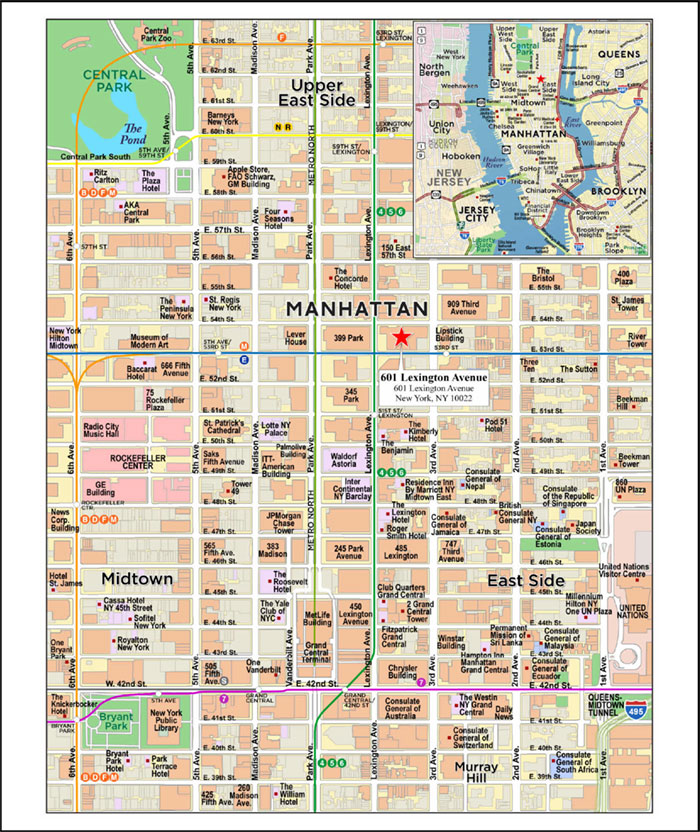

| 6 | 601 Lexington Avenue | New York, NY | GACC | 1 | $40,000,000 | 3.6% | 1,675,659 | Office | 4.50x | 13.2% | 42.5% | 42.5% |

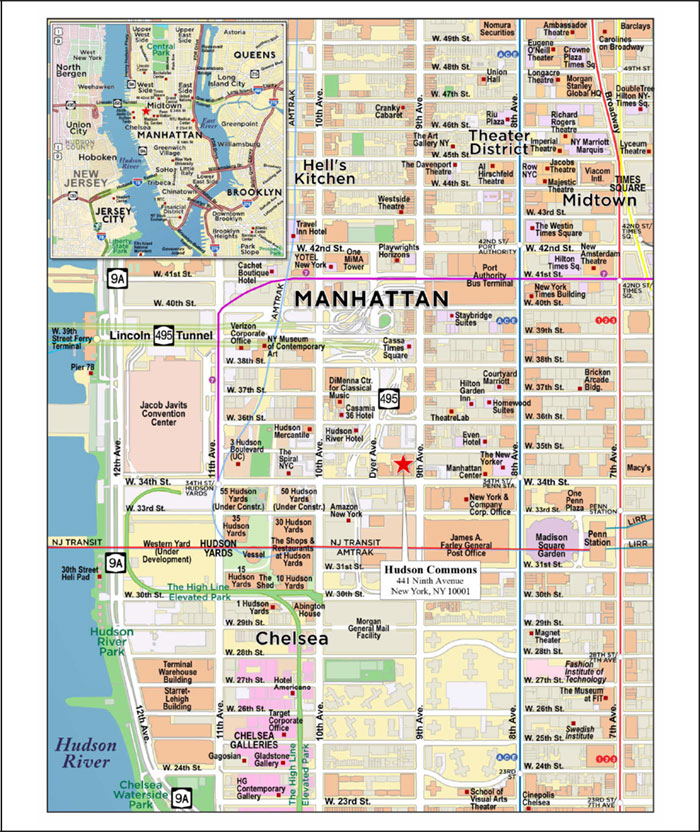

| 7 | Hudson Commons | New York, NY | GACC | 1 | $40,000,000 | 3.6% | 697,960 | Office | 2.54x | 9.4% | 29.6% | 29.6% |

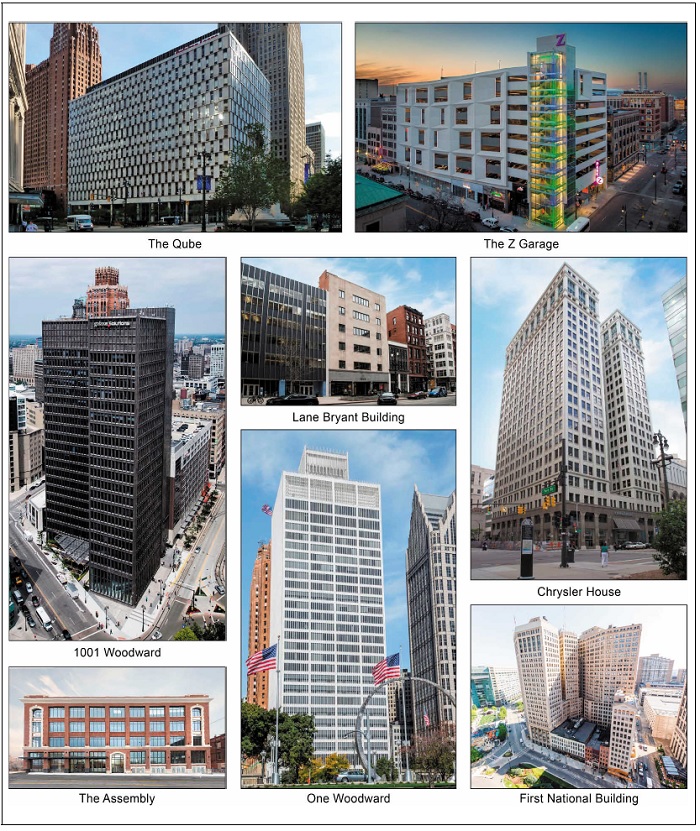

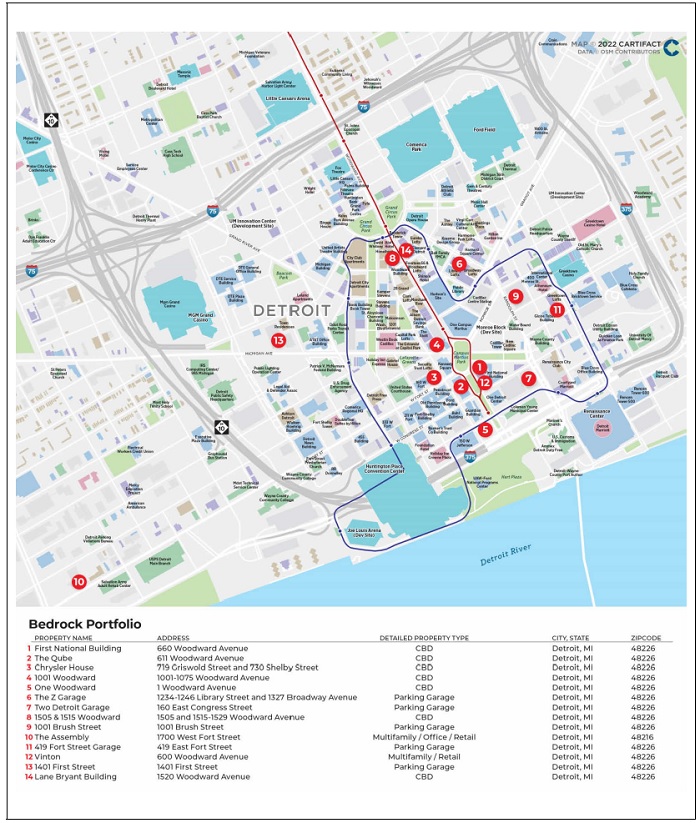

| 8 | Bedrock Portfolio | Detroit, MI | SMC | 14 | $40,000,000 | 3.6% | 2,694,627 | Various | 3.30x | 13.6% | 59.4% | 59.4% |

| 9 | IPCC National Storage Portfolio XV | Various, Various | KeyBank | 17 | $40,000,000 | 3.6% | 912,654 | Self Storage | 2.29x | 8.7% | 46.9% | 46.9% |

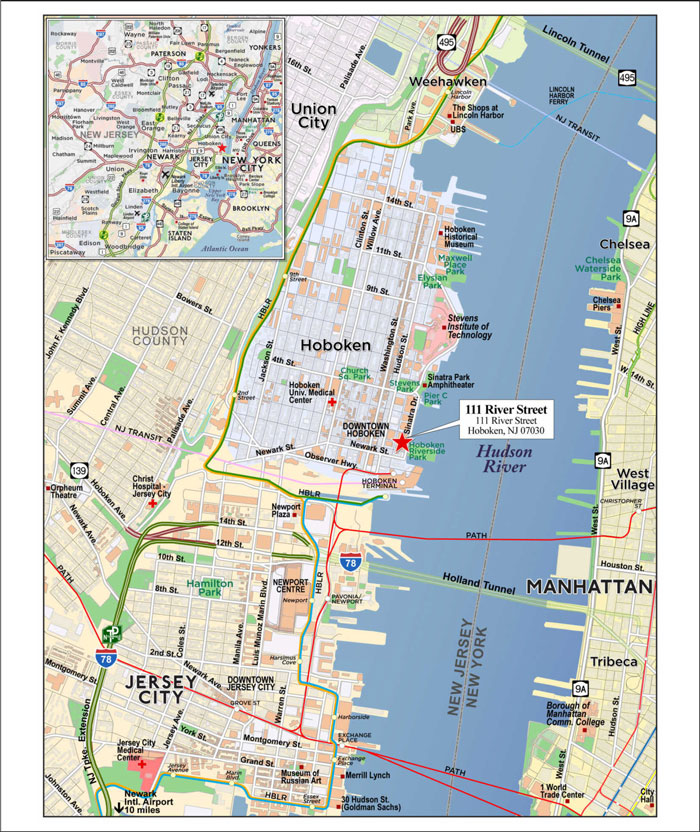

| 10 | 111 River Street | Hoboken, NJ | BMO | 1 | $37,500,000 | 3.3% | 557,719 | Office | 5.08x | 16.9% | 31.8% | 31.8% |

| Top 3 Total/Weighted Average | 29 | $147,750,000 | 13.2% | 3.35x | 12.2% | 43.6% | 43.6% | |||||

| Top 5 Total/Weighted Average | 64 | $229,150,000 | 20.4% | 3.43x | 12.2% | 44.4% | 43.6% | |||||

| Top 10 Total/Weighted Average | 98 | $426,650,000 | 38.0% | 3.47x | 12.2% | 43.4% | 43.0% | |||||

| Non-Top 10 Total/Weighted Average(2)(3) | 136 | $695,357,709 | 62.0% | 2.06x | 10.1% | 59.5% | 55.6% | |||||

| (1) | In the case of Loan Nos. 1, 2, 4, 5, 6, 7, 8, 9, 10, 11, 15, 20 and 22, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date/ARD LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 2, 4, 6, 7, 10 and 22, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date/ARD LTV calculations exclude the related Subordinate Companion Loans. In the case of Loan No. 5, the loan amortizes on a non-standard amortization schedule. Calculations are based on the assumed principal and interest schedule beginning November 2028. |

| (2) | The Non-Top 10 Total/Weighted Average includes a cross-collateralized group of loans including Loan Nos. 36 and 37. All metrics to the crossed loans are presented on an aggregate basis. |

| (3) | In the case of Loan No. 13, the Cut-off Date LTV and UW NOI Debt Yield are based on Cut-off Date Principal Balance after netting out a $1,500,000 holdback reserve. The Cut-off Date LTV and UW NOI Debt Yield based on Cut-off Date Principal Balance without netting out the holdback reserve are 62.7% and 8.6%, respectively. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 9 | ||

| Structural and Collateral Term Sheet | BMO 2022-C1 | |

| Collateral Characteristics | ||

| Pari Passu Companion Loan Summary | |||||||||

No. | Loan Name | Mortgage Loan Seller | Trust Cut-off Date Balance | Aggregate Pari Passu Loan Cut-off Date Balance(1) | Controlling Pooling/Trust & Servicing Agreement | Master Servicer | Special Servicer | Related Pari Passu Loan(s) Securitizations | Related Pari Passu Loan(s) Original Balance |

| 1 | IPCC National Storage Portfolio XVI | KeyBank | $60,000,000 | $117,000,000 | BMO 2022-C1 | KeyBank | CWCapital | Future Securitization(s) | $57,000,000 |

| 2 | 360 Rosemary | BMO | $45,000,000 | $85,000,000 | BMO 2022-C1 | KeyBank | Situs | Future Securitization(s) | $40,000,000 |

| 4 | Coleman Highline Phase IV | BMO | $41,400,000 | $245,000,000 | BBCMS 2022-C14(2) | Midland Loan Services(2) | Midland Loan Services(2) | Future Securitization(s) | $203,600,000 |

| 5 | AMF Portfolio | BMO/SMC | $40,000,000 | $172,000,000 | BBCMS 2021-C12 | KeyBank | LNR | BBCMS 2021-C12 GSMS 2021-GSA3 Future Securitization(s) | $84,000,000 $38,000,000 $10,000,000 |

| 6 | 601 Lexington Avenue | GACC | $40,000,000 | $723,300,000 | BXP 2021-601L | Wells Fargo | Situs | BXP 2021-601L BANK 2022-BNK39 Benchmark 2022-B32 Future Securitization | $426,700,000 $110,000,000 $25,000,000 $121,600,000 |

| 7 | Hudson Commons | GACC | $40,000,000 | $305,000,000 | COMM 2022-HC | KeyBank | CWCapital | COMM 2022-HC | $265,000,000 |

| 8 | Bedrock Portfolio | SMC | $40,000,000 | $430,000,000 | Benchmark 2022-B32 | Midland Loan Services | Ellington | Benchmark 2022-B32 Future Securitization(s) | $125,000,000 $265,000,000 |

| 9 | IPCC National Storage Portfolio XV | KeyBank | $40,000,000 | $86,000,000 | BMO 2022-C1(3) | KeyBank(3) | CWCapital(3) | Future Securitization(s) | $46,000,000 |

| 10 | 111 River Street | BMO | $37,500,000 | $77,500,000 | BMO 2022-C1 | KeyBank | KeyBank | Future Securitization(s) | $40,000,000 |

| 11 | 2 Riverfront Plaza | BMO | $37,500,000 | $110,000,000 | BMO 2022-C1(3) | KeyBank(3) | CWCapital(3) | Future Securitization(s) | $72,500,000 |

| 15 | NYC MFRT Portfolio | BMO | $30,000,000 | $60,200,000 | BMO 2022-C1 | KeyBank | CWCapital | Future Securitization(s) | $30,200,000 |

| 20 | Wyndham National Hotel Portfolio | Sabal | $18,914,095 | $137,127,186 | UBS 2019-C18 | Wells Fargo | Rialto | UBS 2019-C18 BBCMS 2021-C10 BBCMS 2021-C11 WFCM 2021-C60 Future Securitization(s) | $3,000,000 $25,000,000 $20,000,000 $10,000,000 $67,000,000 |

| 22 | Meadowood Mall | BMO | $17,933,084 | $79,702,597 | WFCMT 2021-C61 | Wells Fargo | CWCapital | WFCM 2021-C61 Future Securitization(s) | $19,000,000 $43,000,000 |

| (1) | In the case of Loan Nos. 2, 4, 6, 7, 10 and 22, the Aggregate Pari Passu Loan Cut-off Date Balance excludes the related Subordinate Companion Loan(s). |

| (2) | In the case of Loan No. 4, upon the securitization of the related controlling pari passu companion loan, the related loan combination will be serviced and administered pursuant to the pooling and servicing agreement for the BBCMS 2022-C14 securitization transaction by the parties thereto, which is expected to close prior to the BMO 2022-C1 transaction. |

| (3) | In the case of Loan Nos. 9 and 11, until the securitization of the related controlling pari passu companion loan, the related loan combination will be serviced and administered pursuant to the pooling and servicing agreement for the BMO 2022-C1 securitization transaction by the parties thereto. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 10 | ||

| Structural and Collateral Term Sheet | BMO 2022-C1 | |

| Collateral Characteristics | ||

| Additional Debt Summary |

| Additional Debt Summary |

No. | Loan Name | Trust | Pari Passu | Subordinate | Total Debt | Mortgage Loan UW NCF | Total Debt UW NCF DSCR | Mortgage | Total Debt Cut-off Date | Mortgage | Total Debt UW NOI Debt Yield |

| 2 | 360 Rosemary | $45,000,000 | $40,000,000 | $125,000,000 | $210,000,000 | 4.35x | 1.76x | 26.6% | 65.8% | 17.8% | 7.2% |

| 4 | Coleman Highline Phase IV | $41,400,000 | $203,600,000 | $268,500,000 | $513,500,000 | 5.54x | 2.64x | 31.0% | 65.0% | 14.1% | 6.7% |

| 5 | AMF Portfolio | $40,000,000 | $132,000,000 | $13,000,000 | $185,000,000 | 1.51x | 1.51x | 61.3% | 65.9% | 9.8% | 9.1% |

| 6 | 601 Lexington Avenue | $40,000,000 | $683,300,000 | $276,700,000 | $1,000,000,000 | 4.50x | 3.25x | 42.5% | 58.8% | 13.2% | 9.5% |

| 7 | Hudson Commons | $40,000,000 | $265,000,000 | $202,000,000 | $507,000,000 | 2.54x | 1.53x | 29.6% | 49.2% | 9.4% | 5.7% |

| 10 | 111 River Street | $37,500,000 | $40,000,000 | $76,250,000 | $153,750,000 | 5.08x | 2.56x | 31.8% | 63.0% | 16.9% | 8.5% |

| 22 | Meadowood Mall | $17,933,084 | $61,769,513 | $27,979,523 | $107,682,120 | 2.98x | 1.81x | 35.1% | 47.4% | 19.9% | 14.7% |

| (1) | In the case of Loan Nos. 2, 4, 6, 7, 10, and 22, subordinate debt represents one or more Subordinate Companion Loans. |

| (2) | In the case of Loan No. 5 subordinate debt represents a subordinate mezzanine loan. |

| (3) | Mortgage Loan UW NCF DSCR, Mortgage Loan Cut-off Date LTV and Mortgage Loan UW NOI Debt Yield calculations include any related Pari Passu Companion Loans (if applicable),but exclude the related Subordinate Companion Loans. In the case of Loan No. 5, the loan amortizes on a non-standard amortization schedule. Calculations are based on the assumed principal and interest schedule beginning November 2028. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 11 | ||

| Structural and Collateral Term Sheet | BMO 2022-C1 | |

| Collateral Characteristics | ||

| Mortgaged Properties by Type(1) |

Weighted Average | ||||||||

| Property Type | Property Subtype | Number of Properties | Cut-off Date Principal Balance | % of IPB | UW NCF DSCR(2)(3) | UW NOI Debt Yield(2)(4) | Cut-off Date LTV(2)(4)(5) | Maturity Date/ARD LTV(2)(5) |

| Office | CBD | 13 | $271,201,600 | 24.2% | 3.95x | 13.6% | 39.1% | 39.1% |

| Medical | 10 | 46,550,000 | 4.1 | 3.71x | 11.5% | 56.2% | 56.2% | |

| Suburban | 3 | 19,697,000 | 1.8 | 2.24x | 10.4% | 66.9% | 64.1% | |

| Subtotal: | 26 | $337,448,600 | 30.1% | 3.82x | 13.1% | 43.0% | 42.9% | |

| Retail | Anchored | 8 | $111,514,608 | 9.9% | 2.18x | 10.7% | 58.8% | 51.9% |

| Single Tenant | 3 | 53,990,000 | 4.8 | 2.27x | 9.7% | 57.6% | 57.6% | |

| Unanchored | 6 | 47,573,538 | 4.2 | 2.02x | 9.3% | 59.2% | 58.6% | |

| Regional Mall | 1 | 17,933,084 | 1.6 | 2.98x | 19.9% | 35.1% | 30.7% | |

| Shadow Anchored | 3 | 16,945,500 | 1.5 | 1.74x | 10.4% | 65.6% | 57.4% | |

| Subtotal: | 21 | $247,956,731 | 22.1% | 2.19x | 10.9% | 57.3% | 53.3% | |

| Self Storage | Self Storage | 56 | $177,662,346 | 15.8% | 2.28x | 8.9% | 52.0% | 51.5% |

| Multifamily | Garden | 44 | $122,557,425 | 10.9% | 1.69x | 9.3% | 61.5% | 55.8% |

| Low Rise | 14 | 28,763,939 | 2.6 | 1.75x | 7.6% | 62.3% | 62.3% | |

| Mid Rise | 3 | 16,765,000 | 1.5 | 2.26x | 8.2% | 62.9% | 62.9% | |

| Student Housing | 1 | 2,489,468 | 0.2 | 1.49x | 8.7% | 62.4% | 49.6% | |

| Subtotal: | 62 | $170,575,832 | 15.2% | 1.76x | 8.9% | 61.8% | 57.5% | |

| Hospitality | Extended Stay | 3 | $47,285,198 | 4.2% | 1.83x | 12.2% | 61.5% | 50.8% |

| Limited Service | 44 | 18,914,095 | 1.7 | 1.69x | 15.0% | 63.8% | 46.7% | |

| Subtotal: | 47 | $66,199,293 | 5.9% | 1.79x | 13.0% | 62.2% | 49.6% | |

| Industrial | Warehouse / Other | 1 | $31,500,000 | 2.8% | 2.21x | 8.7% | 58.7% | 58.7% |

| Flex | 2 | 13,925,000 | 1.2 | 2.18x | 10.6% | 59.8% | 56.1% | |

| Warehouse | 2 | 11,350,000 | 1.0 | 1.39x | 8.9% | 61.3% | 57.7% | |

| Warehouse / Distribution | 1 | 2,392,654 | 0.2 | 2.04x | 9.7% | 54.2% | 54.2% | |

| Subtotal: | 6 | $59,167,654 | 5.3% | 2.04x | 9.2% | 59.3% | 57.7% | |

| Mixed Use | Multifamily / Retail | 6 | $35,018,854 | 3.1% | 1.92x | 8.5% | 57.3% | 56.7% |

| Office / Retail | 1 | 8,750,000 | 0.8 | 2.49x | 9.6% | 62.9% | 62.9% | |

| Office / Multifamily | 1 | 4,130,000 | 0.4 | 1.65x | 9.8% | 63.5% | 56.4% | |

| Retail / Multifamily | 1 | 3,300,000 | 0.3 | 2.01x | 8.0% | 62.3% | 62.3% | |

| Multifamily / Office / Retail | 1 | 1,276,000 | 0.1 | 3.30x | 13.6% | 59.4% | 59.4% | |

| Subtotal: | 10 | $52,474,854 | 4.7% | 2.03x | 8.9% | 59.1% | 58.1% | |

| Other | Parking Garage | 5 | $8,222,400 | 0.7% | 3.30x | 13.6% | 59.4% | 59.4% |

| Manufactured Housing | Manufactured Housing | 1 | $2,300,000 | 0.2% | 1.45x | 8.3% | 65.9% | 59.7% |

| Total / Weighted Average: | 234 | $1,122,007,709 | 100.0% | 2.60x | 10.9% | 53.4% | 50.8% | |

| (1) | Because this table presents information relating to the mortgaged properties and not mortgage loans, the information for mortgage loans secured by more than one mortgaged property is based on allocated loan amounts, individual appraised values, net cash flow or net operating income with respect to such individual mortgaged properties, as applicable. |

| (2) | In the case of Loan Nos. 1, 2, 4, 5, 6, 7, 8, 9, 10, 11, 15, 20 and 22, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date/ARD LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 2, 4, 6, 7, 10 and 22, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date/ARD LTV calculations exclude the related Subordinate Companion Loans. In the case of Loan No. 5, the loan amortizes on a non-standard amortization schedule. Calculations are based on the assumed principal and interest schedule beginning November 2028. |

| (3) | For the mortgage loans that are interest-only for the entire term or until the anticipated repayment date and accrue interest on an Actual/360 basis, the Monthly Debt Service Amount ($) was calculated as 1/12th of the product of (i) the Original Balance ($), (ii) the Interest Rate % and (iii) 365/360. |

| (4) | In the case of Loan No. 13, the Cut-off Date LTV and UW NOI Debt Yield are based on Cut-off Date Principal Balance after netting out a $1,500,000 holdback reserve. The Cut-off Date LTV and UW NOI Debt Yield based on Cut-off Date Principal Balance without netting out the holdback reserve is 62.7% and 8.6%, respectively. |

| (5) | In the case of Loan Nos. 1, 9, 18 and 23, the Cut-off Date LTV and the Maturity Date/ARD LTV are calculated by using an appraised value based on an as-portfolio assumption. In the case of Loan Nos. 2 and 38 the Cut-off Date LTV and Maturity/ARD LTV are calculated by using an appraised value based on an as stabilized assumption. In the case of Loan No. 20, the Cut-off Date LTV and Maturity LTV are calculated by using an appraised value based on an as complete assumption for 15 of the mortgage properties. In the case of Loan No. 7, the Cut-off Date LTV and Maturity/ARD LTV are calculated by using an appraised value based on a market value assuming present value of ICAP tax savings are excluded and outstanding leasing costs reserved assumption. Refer to “Description of the Mortgage Pool—Certain Calculations and Definitions—Appraised Value” in the Preliminary Prospectus for additional details. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 12 | ||

| Structural and Collateral Term Sheet | BMO 2022-C1 | |

| Collateral Characteristics | ||

| Mortgaged Properties by Location(1) |

Weighted Average | |||||||

State | Number of Properties | Cut-off Date | % of | UW NCF DSCR(2)(3) | UW NOI Debt Yield(2)(4) | Cut-off Date LTV(2)(4)(5) | Maturity Date/ARD LTV(2)(5) |

| New York | 20 | $152,147,660 | 13.6% | 2.80x | 9.8% | 46.2% | 46.2% |

| Florida | 17 | 124,701,132 | 11.1 | 2.76x | 12.5% | 45.7% | 43.5% |

| New Jersey | 4 | 91,262,000 | 8.1 | 3.28x | 12.4% | 48.8% | 48.4% |

| California | 11 | 86,627,599 | 7.7 | 3.81x | 11.3% | 43.1% | 43.1% |

| Texas | 13 | 74,667,925 | 6.7 | 1.92x | 10.6% | 57.7% | 48.7% |

| Michigan | 20 | 71,164,936 | 6.3 | 2.67x | 11.7% | 59.9% | 57.4% |

| Illinois | 13 | 56,859,425 | 5.1 | 2.46x | 9.6% | 60.7% | 59.5% |

| Washington | 7 | 50,536,438 | 4.5 | 2.03x | 9.0% | 61.4% | 61.4% |

| Ohio | 22 | 49,804,191 | 4.4 | 1.73x | 10.2% | 60.3% | 51.1% |

| Oregon | 2 | 32,031,004 | 2.9 | 2.20x | 8.8% | 58.8% | 58.5% |

| South Dakota | 2 | 28,488,880 | 2.5 | 2.12x | 12.3% | 60.0% | 51.2% |

| Arizona | 7 | 27,955,670 | 2.5 | 2.30x | 10.0% | 59.7% | 58.2% |

| Pennsylvania | 6 | 27,699,086 | 2.5 | 1.99x | 9.9% | 58.6% | 50.4% |

| Missouri | 6 | 26,274,704 | 2.3 | 1.86x | 9.4% | 63.1% | 59.7% |

| Indiana | 12 | 25,798,645 | 2.3 | 2.55x | 10.4% | 59.6% | 56.4% |

| Wisconsin | 3 | 25,005,922 | 2.2 | 2.73x | 10.8% | 59.9% | 58.6% |

| Tennessee | 5 | 22,099,803 | 2.0 | 2.41x | 10.6% | 57.2% | 56.1% |

| Nevada | 3 | 21,390,120 | 1.9 | 2.85x | 18.2% | 37.6% | 33.4% |

| Oklahoma | 4 | 17,841,884 | 1.6 | 3.45x | 12.4% | 52.6% | 52.3% |

| Alabama | 4 | 15,858,284 | 1.4 | 1.97x | 8.7% | 53.6% | 50.1% |

| Minnesota | 2 | 13,968,541 | 1.2 | 2.73x | 11.0% | 55.1% | 55.1% |

| Massachusetts | 3 | 12,446,179 | 1.1 | 2.43x | 9.3% | 58.1% | 58.1% |

| South Carolina | 2 | 11,240,646 | 1.0 | 2.44x | 9.3% | 57.8% | 57.8% |

| Georgia | 8 | 9,158,157 | 0.8 | 1.51x | 9.8% | 61.3% | 56.9% |

| Virginia | 4 | 7,734,629 | 0.7 | 1.74x | 9.1% | 57.7% | 53.9% |

| Maine | 2 | 7,235,899 | 0.6 | 2.29x | 8.6% | 47.8% | 47.8% |

| North Carolina | 2 | 6,348,315 | 0.6 | 2.25x | 9.4% | 53.5% | 53.5% |

| Vermont | 1 | 5,800,000 | 0.5 | 2.97x | 10.3% | 63.7% | 63.7% |

| Kansas | 6 | 5,538,207 | 0.5 | 2.43x | 12.7% | 63.9% | 58.5% |

| Wyoming | 6 | 3,852,252 | 0.3 | 1.69x | 15.0% | 63.8% | 46.7% |

| Maryland | 2 | 3,812,350 | 0.3 | 2.27x | 8.8% | 48.2% | 47.8% |

| Nebraska | 4 | 2,183,106 | 0.2 | 1.69x | 15.0% | 63.8% | 46.7% |

| New Mexico | 3 | 2,034,027 | 0.2 | 1.69x | 15.0% | 63.8% | 46.7% |

| Montana | 2 | 786,082 | 0.1 | 1.69x | 15.0% | 63.8% | 46.7% |

| Iowa | 2 | 710,375 | 0.1 | 1.69x | 15.0% | 63.8% | 46.7% |

| Louisiana | 1 | 385,221 | 0.0 | 1.69x | 15.0% | 63.8% | 46.7% |

| Utah | 1 | 315,370 | 0.0 | 1.69x | 15.0% | 63.8% | 46.7% |

| North Dakota | 1 | 200,896 | 0.0 | 1.69x | 15.0% | 63.8% | 46.7% |

| Colorado | 1 | 42,149 | 0.0 | 1.69x | 15.0% | 63.8% | 46.7% |

| Total / Weighted Average: | 234 | $1,122,007,709 | 100.0% | 2.60x | 10.9% | 53.4% | 50.8% |

| (1) | Because this table presents information relating to the mortgaged properties and not mortgage loans, the information for mortgage loans secured by more than one mortgaged property is based on allocated loan amounts, individual appraised values, net cash flow or net operating income with respect to such individual mortgaged properties, as applicable. |

| (2) | In the case of Loan Nos. 1, 2, 4, 5, 6, 7, 8, 9, 10, 11, 15, 20 and 22, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date/ARD LTV calculations include the related Pari Passu Companion Loan(s). In the case of Loan Nos. 2, 4, 6, 7, 10 and 22, the UW NCF DSCR, UW NOI Debt Yield, Cut-off Date LTV and Maturity Date/ARD LTV calculations exclude the related Subordinate Companion Loans. In the case of Loan No. 5, the loan amortizes on a non-standard amortization schedule. Calculations are based on the assumed principal and interest schedule beginning November 2028. |

| (3) | For the mortgage loans that are interest-only for the entire term or until the anticipated repayment date and accrue interest on an Actual/360 basis, the Monthly Debt Service Amount ($) was calculated as 1/12th of the product of (i) the Original Balance ($), (ii) the Interest Rate % and (iii) 365/360. |

| (4) | In the case of Loan No. 13, the Cut-off Date LTV and UW NOI Debt Yield are based on Cut-off Date Principal Balance after netting out a $1,500,000 holdback reserve. The Cut-off Date LTV and UW NOI Debt Yield based on Cut-off Date Principal Balance without netting out the holdback reserve is 62.7% and 8.6%, respectively. |

| (5) | In the case of Loan Nos. 1, 9, 18 and 23, the Cut-off Date LTV and the Maturity Date/ARD LTV are calculated by using an appraised value based on an as-portfolio assumption. In the case of Loan Nos. 2 and 38 the Cut-off Date LTV and Maturity/ARD LTV are calculated by using an appraised value based on an as stabilized assumption. In the case of Loan No. 20, the Cut-off Date LTV and Maturity LTV are calculated by using an appraised value based on an as complete assumption for 15 of the mortgage properties. In the case of Loan No. 7, the Cut-off Date LTV and Maturity/ARD LTV are calculated by using an appraised value based on a market value assuming present value of ICAP tax savings are excluded and outstanding leasing costs reserved assumption. Refer to “Description of the Mortgage Pool—Certain Calculations and Definitions—Appraised Value” in the Preliminary Prospectus for additional details. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 13 | ||

| Structural and Collateral Term Sheet | BMO 2022-C1 | |

| Collateral Characteristics | ||

| Cut-off Date Principal Balance |

Weighted Average | |||||||||||

| Range of Cut-off Date Principal Balances | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(1)(2) | UW NOI DY(1)(3) | Cut-off Date LTV(1)(3)(4) | Maturity Date/ARD LTV(1)(4) | ||

| $1,425,000 | - | $4,999,999 | 23 | $73,511,945 | 6.6% | 4.00742% | 110 | 1.82x | 9.2% | 62.5% | 57.6% |

| $5,000,000 | - | $9,999,999 | 19 | 130,841,250 | 11.7 | 3.87612% | 112 | 2.12x | 9.3% | 61.5% | 59.4% |

| $10,000,000 | - | $19,999,999 | 16 | 220,327,377 | 19.6 | 3.93276% | 112 | 2.30x | 11.6% | 58.2% | 52.8% |

| $20,000,000 | - | $29,999,999 | 4 | 101,300,000 | 9.0 | 4.28436% | 119 | 1.89x | 10.3% | 58.2% | 53.3% |

| $30,000,000 | - | $39,999,999 | 6 | 206,877,137 | 18.4 | 4.02987% | 108 | 2.48x | 10.4% | 54.3% | 52.4% |

| $40,000,000 | - | $60,000,000 | 9 | 389,150,000 | 34.7 | 3.39103% | 102 | 3.32x | 11.8% | 44.5% | 44.0% |

| Total / Weighted Average: | 77 | $1,122,007,709 | 100.0% | 3.79281% | 108 | 2.60x | 10.9% | 53.4% | 50.8% | ||

| Mortgage Interest Rates |

Weighted Average | |||||||||||

| Range of Mortgage Interest Rates | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(1)(2) | UW NOI DY(1)(3) | Cut-off Date LTV(1)(3)(4) | Maturity Date/ARD LTV(1)(4) | ||

| 2.49450 | - | 3.24999 | 3 | $124,150,000 | 11.1% | 2.72653% | 98 | 4.60x | 12.9% | 43.1% | 43.1% |

| 3.25000 | - | 3.74999 | 27 | 401,422,000 | 35.8 | 3.53720% | 106 | 2.53x | 10.2% | 51.1% | 49.4% |

| 3.75000 | - | 3.99999 | 19 | 256,274,344 | 22.8 | 3.87372% | 108 | 2.83x | 12.5% | 51.2% | 49.8% |

| 4.00000 | - | 4.24999 | 12 | 95,870,134 | 8.5 | 4.04616% | 119 | 2.03x | 9.7% | 62.0% | 58.7% |

| 4.25000 | - | 4.49999 | 8 | 156,877,137 | 14.0 | 4.37653% | 119 | 1.74x | 9.4% | 61.4% | 55.8% |

| 4.50000 | - | 4.74999 | 4 | 31,725,000 | 2.8 | 4.69939% | 111 | 1.60x | 8.2% | 57.9% | 57.2% |

| 4.75000 | - | 5.44000 | 4 | 55,689,095 | 5.0 | 5.04306% | 100 | 1.54x | 11.8% | 62.3% | 51.1% |

| Total / Weighted Average: | 77 | $1,122,007,709 | 100.0% | 3.79281% | 108 | 2.60x | 10.9% | 53.4% | 50.8% | ||

| Original Term to Maturity in Months |

Weighted Average | |||||||||

| Original Term to Maturity in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(1)(2) | UW NOI DY(1)(3) | Cut-off Date LTV(1)(3)(4) | Maturity Date/ARD LTV(1)(4) |

| 60 | 7 | $154,208,084 | 13.7% | 3.38373% | 59 | 3.91x | 13.7% | 34.9% | 34.0% |

| 84 | 4 | 55,895,500 | 5.0 | 3.76348% | 83 | 2.94x | 12.6% | 60.3% | 59.6% |

| 120 | 66 | 911,904,125 | 81.3 | 3.86378% | 118 | 2.35x | 10.3% | 56.1% | 53.1% |

| Total / Weighted Average: | 77 | $1,122,007,709 | 100.0% | 3.79281% | 108 | 2.60x | 10.9% | 53.4% | 50.8% |

| Remaining Term to Maturity in Months |

| Weighted Average | |||||||||||

| Range of Remaining Term to Maturity in Months | Number of Loans | Cut-off Date Principal Balance | % of IPB | Mortgage Rate | Remaining Loan Term(1) | UW NCF DSCR(1)(2) | UW NOI DY(1)(3) | Cut-off Date LTV(1)(3)(4) | Maturity Date/ARD LTV(1)(4) | ||

| 55 | - | 60 | 7 | $154,208,084 | 13.7% | 3.38373% | 59 | 3.91x | 13.7% | 34.9% | 34.0% |

| 82 | - | 94 | 5 | 74,809,595 | 6.7 | 4.03819% | 86 | 2.62x | 13.2% | 61.2% | 56.3% |

| 115 | - | 120 | 65 | 892,990,030 | 79.6 | 3.84289% | 119 | 2.37x | 10.2% | 55.9% | 53.3% |

| Total / Weighted Average: | 77 | $1,122,007,709 | 100.0% | 3.79281% | 108 | 2.60x | 10.9% | 53.4% | 50.8% | ||