UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

___________________________________________

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act File Number 811-23712

___________________________________________

Sweater Cashmere Fund

(Exact name of registrant as specified in charter)

___________________________________________

2000 Central Ave

Boulder, CO 80301

(Address of principal executive offices) (Zip code)

Jesse Randall

2000 Central Ave

Boulder, CO 80301

(Name and address of agent for service)

Copies to:

Jonathan D. Van Duren

Greenberg Traurig, LLP

77 West Wacker Drive, Suite 3100

Chicago, Illinois 60601

___________________________________________

Registrant’s telephone number, including area code: (888) 577-7987

Date of fiscal year end: March 31

Date of reporting period: March 31, 2023

Item 1. Reports to Stockholders.

(a) The following is a copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1)

i

SHAREHOLDER LETTER

Intro

In early 2022, Sweater Ventures set out on a mission to change the venture capital (“VC”) industry by opening up access to the general public and allowing for both accredited and non-accredited investors to invest in the VC asset class. Following the Sweater Cashmere Fund’s (“Cashmere Fund” or “Fund”) inception on April 13, 2022, the Fund opened to its waitlist in May 2022 and was fully open to the public shortly thereafter.

In its first fiscal period of operations, from April 13, 2022 through March 31, 2023, the Sweater Cashmere Fund delivered a total return of 3.18%, with 2.94% attributed to portfolio company valuation markups, and 0.24% distributed as profits to investors. It was a challenging year for venture capital, total capital raised fell by 80% between Q1 2022 and Q1 2023 according to Carta’s State of Private Markets: Q1 2023 Report. Public markets didn’t fare much better, with the S&P SmallCap 600 Index® (the Fund’s “Benchmark Index”) declining by -7.06% for the period since the Fund’s inception date of April 13, 2022 through March 31, 2023.1 During this same period, the Cashmere Fund was able to achieve a lower level of volatility relative to the Benchmark Index due in part, we believe, to the Fund’s robust diligence process, strong deal pipeline, and strategic timing of capital deployment. Although the Fund’s absolute returns were below our internal expectations for the period, its relative returns demonstrated strong performance, outperforming its Benchmark Index.

While the Cashmere Fund’s first fiscal period performance was positive, the venture capital landscape as a whole has experienced a slowdown, as measured by the Preqin Private Capital Quarterly Index. This has had an impact on various aspects of the ecosystem, such as fundraising, deal pricing, capital calls, and shifts in funding sources in terms of geography and demographics. In an effort to keep Fund investors informed, we’ve summarized some of our thoughts on the state of venture below.

Private Capital Fundraising

We believe the recent slowdown in venture returns can be attributed in part to institutional investors holding back on deploying capital to fund managers. This is due to a variety of factors, including concerns over economic volatility, geopolitical uncertainty, and pricing corrections. As a result, we have observed that many VC funds are taking longer to raise or call capital, resulting in less capital deployed to startups. This lack of funding has had a cascading impact on the startup ecosystem, leading to lower valuations and longer funding cycles. Furthermore, the institutional investors who have deployed capital in recent months have increasingly focused on larger, more established funds, leaving early-stage and smaller funds with fewer resources to invest, in our opinion.

While there was a decline in global VC fundraising in 2022, we believe the continued high level of capital commitments from institutional investors indicates that venture capital is positioned to be a strong asset class going forward. In fact, global VC fundraising exceeded $200 billion for the fifth consecutive year in 2022, with $252.6 billion raised across 1,371 funds according to PitchBook’s 2022 private market fundraising report. However, recent geopolitical uncertainty and fluctuations in public markets have made institutional investors more cautious, we believe, causing them to take a more measured approach towards deploying capital. This has led to a lower amount of capital being deployed and longer fundraising cycles, but the demand for venture capital remains strong, from what we’ve observed, especially in North America, where global investors are drawn to the region’s strong venture capital ecosystem and stable currency.

The Cashmere Fund has created new avenues for retail investors to access venture markets. By democratizing access to venture opportunities, we hope to close the current investor funding gap and support the growth of promising startups. In 2022, private markets are attracting more and more interest from retail investors, who represent a significant source of capital with over $50 trillion in assets according to McKinsey’s global private markets review. In fact, according to a recent survey from Preqin, over a third of private market managers anticipate having a retail-oriented vehicle in the next five years.

____________

1 Investments held by the Fund do not match those in the Benchmark Index, and the performance of the Fund will differ.

1

Early Stage Venture Funding

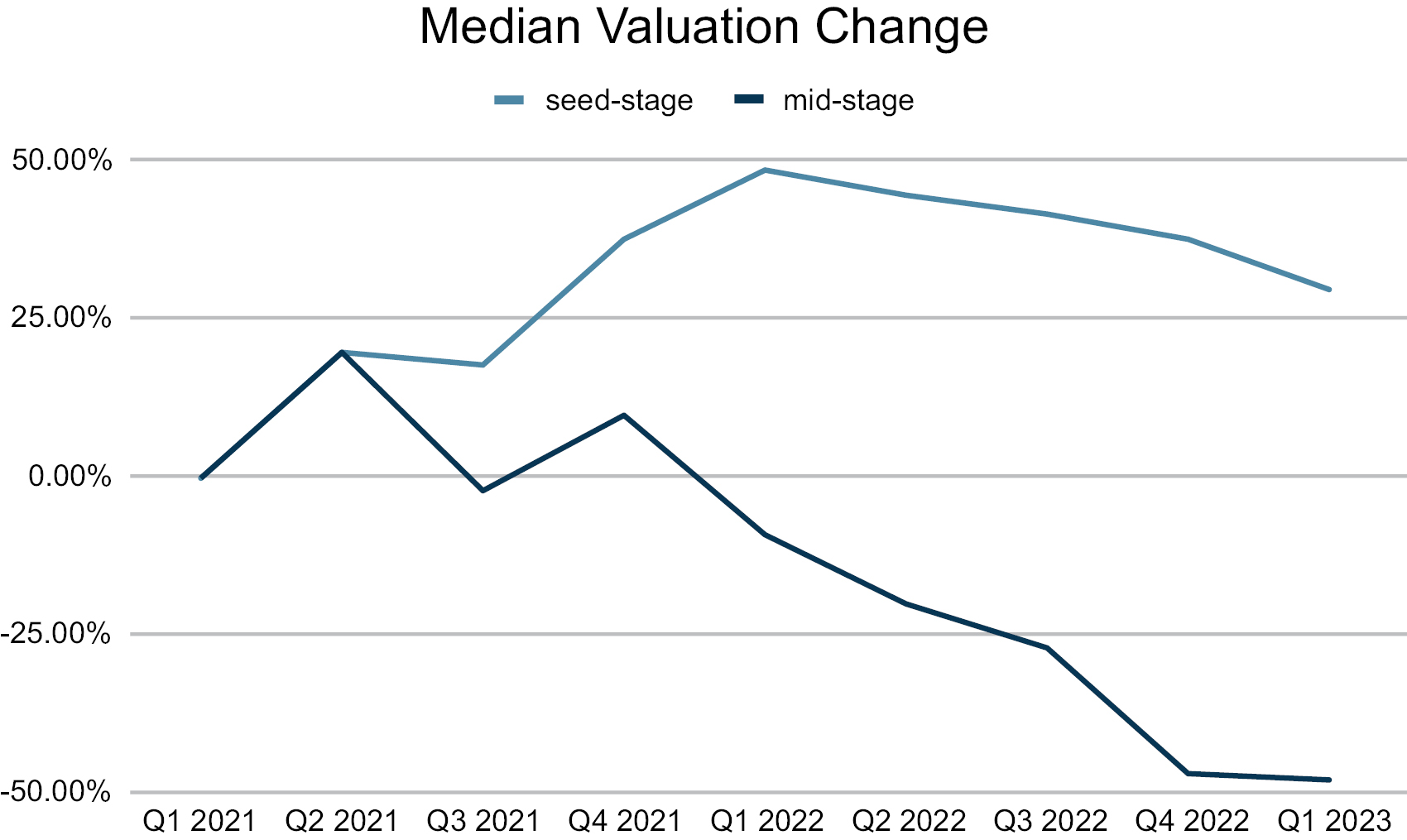

Despite the turbulence in the broader venture capital market, seed-stage funding remained relatively unscathed in the first half of 2022 as investors remained optimistic about seed-stage ventures. Seed valuations peaked in Q1 2022 and saw slight tapering between Q3 2022 and Q1 2023 as investors sought more reasonable pricing relative to other stages (see chart below).

Source: eShares Inc., d/b/a Carta Inc. | Series C data was used as a proxy for mid-stage

Seed deal count and size remained elevated through 2022 as a new wave of microfunds have reinforced seed-stage activity, and Q1 of 2023 has seen a slight improvement from Q4 of 2022. According to Pitchbook, the median deal size for seed companies increased to $3 million in Q1 of 2023, up from $2.6 million in 2022. The resilience of seed-stage valuations can be attributed to a combination of factors, including a shift towards higher-quality startups and investor optimism towards emerging sectors such as generative Artificial Intelligence, in our opinion. We believe these trends suggest that the early-stage VC market continues to offer potential opportunities for investors, particularly those focused on supporting innovative startups.

We remain focused on investments in early stage startups, predominantly in Seed and Series A stages. Further, we will continue to carefully assess a startup’s burn and runway during the diligence process as we aim to identify startups that have an estimated 18 – 24 months of runway and the durability to weather unstable economic conditions.

Conclusion

Irrespective of seed-stage resilience, we believe there are a variety of indicators that suggest a correction in venture capital markets is underway. According to Carta data, seed-stage valuations fell by 17% and mid-stage valuations fell by approximately 44% between Q1 22 and Q1 23 alone. While the decline in valuations in 2022 may cause concern, corrections are often transitory and, in our view, can lead to more attractive risk-adjusted deal pricing.

The Cashmere Fund is focused on long-term investing strategies, as it seeks to take advantage of the current market opportunity to invest in what we believe are quality companies with strong balance sheets, experienced management teams, and differentiated business models at attractive valuations. Since its inception through March 31, 2023, the Cashmere Fund invested in 22 early-stage portfolio companies across various industries, which we believe positions the Fund to benefit from the potential upside of these sectors should the market stabilize. The Fund also invested in three portfolio funds.

2

Moreover, investing in a downturn may enable early-stage investors, such as the Fund, to acquire larger equity stakes in companies at lower valuations, which we believe can lead to greater return potential over the long term. This approach aligns with our focus on generating long-term stable returns for investors in the Cashmere Fund.

While we recognize the current correction in the venture capital markets, we remain optimistic about the potential for growth in the industries we invest in. We believe that the Cashmere Fund, along with its network of investors, companies, and partners, will continue to act as a catalyst for innovation and value creation in the industries we invest in.

We are closely monitoring the health of venture markets, but we remain committed to investing the Fund’s assets throughout this cycle to support the venture ecosystem. We believe that the timing of the Fund’s launch gives us a strategic advantage, as macro market corrections often create opportunities for healthier risk-adjusted deal pricing. Additionally, our evergreen fund structure provides us with a critical tool for mitigating risks around market timing, we believe. This structure, in our view, allows us to take a long-term perspective and provides us with greater flexibility and stability.

We would like to thank our investors for their commitment to the Cashmere Fund and the venture ecosystem as a whole. We are very optimistic about the Fund’s prospects and we remain committed to producing long-term returns for our investors.

The views expressed in this report are exclusively those of the Fund’s investment adviser, Sweater Industries, LLC, as of March 31, 2023. Any such views are subject to change at any time based on market or other conditions, and the Fund disclaims any responsibility to update such views. These views are not intended to be a forecast of future events, a guarantee of future results or advice. Because investment decisions for the Fund are based on numerous factors, these views may not be relied upon as an indication of trading intent on behalf of the Fund. The information contained herein has been prepared from sources believed to be reliable but is not guaranteed by the Fund as to its accuracy or completeness. Past performance is not indicative of future results. There is no assurance that the Fund’s investment objectives will be achieved.

“New Portfolio Additions”

Below is a summary of the equity investments in portfolio companies and portfolio funds in which the Fund invested during the period from its April 13, 2022 inception through March 31, 2023. Information about each company has been provided by the company or another third-party source that the Fund believes to be reliable, but is not guaranteed by the Fund as to its accuracy or completeness. The Fund holdings discussed in this report may not have been held by the Fund for the entire period, and both current and future Fund investments are subject to risk. The Fund’s portfolio composition is subject to review in accordance with the Fund’s investment strategy and should be expected to change over time. Please see the Schedule of Investments for a complete list of the Fund’s investments and their values as of March 31, 2023.

EdInvent, Inc. dba Accredible

• Accredible is a SaaS solution in the digital credentialing space that provides higher education institutions, certification providers, professional associations, corporate training organizations, and LXPs (learning experience platforms) with the tools they need to create credentialing programs.

After Services, Inc.

• After.com, Inc. is an end-of-life software experience focused on providing alternative after-life products and services such as cremation. Time sensitive, end-of-life arrangements are coordinated seamlessly through the technology, servicing both bereaved families seeking immediate care of a lost loved one and for individuals pre-planning their own final arrangements.

Cabinet Health P.B.C.

• Cabinet Health P.B.C. has developed glass containers and sustainable refill packets to eliminate single-use plastic from medicine.

3

Curate Capital Fund I, LP

• Curate Capital Fund I, LP is a venture capital fund that invests in innovative and influential female founders. Curate was founded and is ultimately run by Carrie Colbert.

EarlyBird Central, Inc.

• EarlyBird Central, Inc. is a family wealth-building platform allowing parents to open custodial investment accounts that can be funded with gifts and contributions from a child’s entire community, even before birth. As as an investment advisor focused on the youngest generation, EarlyBird Central, Inc. believes its fintech platform empowers families to invest in a diverse, modern portfolio for children in their lives.

FEAT Socks, Inc.

• FEAT Clothing is a high-end brand designed at the intersection of the comfort of loungewear and the performance of activewear, yet styled for the office. The products are designed to be worn throughout the day, no matter your activity.

Frances Valentine, LLC

• Frances Valentine, LLC is a modern American lifestyle brand featuring apparel, handbags, shoes, and jewelry. Frances Valentine, LLC offers products through an omnichannel approach, including e-commerce, owned retail, trunk shows, and carefully selected retail partners.

Ganas Ventures I

• Ganas Ventures I is a $10M venture capital fund investing in pre-seed and seed stage community-driven startups throughout the United States and Latin America.

GO, Inc.

GO, Inc. is a tech-enabled, car-subscription company offering an alternative to car ownership.

Drupely Inc. dba Graza

• Graza is an omni-channel olive oil company that sells extra-virgin olive oils (EVOO) at prices that won’t break the bank. Both of Graza’s products (Drizzle 500ml finishing oil and Sizzle 750 ml cooking oil) are never blended and made from single varietal Picual olives sourced from Jaen, Spain, a prosperous agricultural region. Graza EVOO comes in chef inspired, first-to-market squeeze bottles.

Eliot Street, Inc. dba Guest House

• Guest House is a technology platform for real estate services intended to bring retail to real estate by staging homes where buyers can shop. The company’s platform curates furniture, art, and goods enabling customers to shop during open houses, events, and online.

Havenly, Inc.

• Havenly, Inc. is an online platform for interior design services with their own line of products and services

Hearth Display, Inc.

• Hearth Display, Inc. launched a digital touchscreen that replaces family bulletin boards. The digital bulletin board creates a family management system through an automated text-based assistant, consolidated family scheduling features, task management and routine builders.

4

IQ Bar, Inc.

• Launched in 2018, IQ Bar, Inc. is a “brain + body” nutrition company. Their primary product line centers on low-carb, plant protein bars packed with brain nutrients (like the Lion’s Mane adaptogen). IQ Bar, Inc also recently expanded into hydration with its IQMIX stick pack line, and ultimately plans on releasing a coffee mix called IQJOE.

IsoTalent, Inc.

• IsoTalent, Inc. is a recruiting platform aligning incentives of internal hiring managers, external recruiters, and applicants. Their hourly-rate recruiting model is managed globally on a single platform.

Lazzaro Medical, Inc.

• Lazzaro Medical, Inc. has developed a robotic, minimally-invasive surgery and device designed to cure Tracheobronchomalacia (“TBM”). TBM is a common disease where the throat collapses and causes difficulty breathing, chronic cough, and recurring infections.

Nada Holdings, Inc.

• Nada Holdings, Inc. is a real estate finance, banking, and investing platform intended to make homeownership simple and accessible. The platform seeks to democratize the $36 trillion home equity market by reimagining the antiquated ownership model, fractionalizing homeowner equity, and allowing investments in real estate for as low as $250.

Nomadica

• Nomadica offers a sommelier-curated collection of premier canned wines through both direct-to-consumer and wholesale/retail. Nomadica is based out of Los Angeles, but they source their wine blends from exclusive vineyards domestically and internationally. Nomadica has 5 core taste profiles — red, white, rose, sparkling white, and sparkling rose — sold direct-to-consumer on their website and in select retail locations nationally.

Parallel Health, Inc.

• Parallel Health, Inc. is a next-generation skin health company providing effective, targeted solutions powered by microbiome science, genomics, and machine learning. With Parallel Health, Inc., consumers and patients can access expertise and clinical guidance, a personalized genomic assessment to understand their skin microbiome, as well as personalized, targeted microbiome skincare products and prescriptions.

Pear Suite, Inc.

• Pear Suite, Inc. is a digital health platform that enables healthcare organizations, like providers, insurance plans, and community organizations, to communicate directly with individuals in their audiences, collect health data on social drivers of health, and navigate patients to care and services.

Shappi, Inc.

• Shappi, Inc. is a logistics and shipping platform designed to connect international shoppers with travelers to deliver products by renting the traveler’s unused luggage space.

Stonks Y Combinator Summer 2022 Access Fund

• Stonks Y Combinator Summer 2022 Access Fund is both a technology platform and a venture capital fund. Stonks Y Combinator Summer 2022 Access Fund invested $50,000 into each of the 35 startups who came out of YCombinator’s Summer 2022 cohort.

The Last Gameboard, Inc.

• The Last Gameboard, Inc. launched a touchscreen device for social gaming. The product features a custom OS, patented methods of integrating physical game pieces, shapes and hand gestures.

5

True Footage, Inc.

• True Footage, Inc. is a residential appraisal company founded in 2019 and launched in 2021. Their core business is a tech-enabled appraisal company for both in-person and desktop appraisals. They also have a software platform that improves the efficiency and objectivity of the appraisal process. Currently, True Footage is operating in 32 U.S. states providing appraisals for over 300 banks and appraisal management companies as customers.

Wyndly Health, Inc.

• Wyndly Health, Inc. provides an FDA-approved medicine and telehealth, for allergy immunotherapy for the 50 million Americans suffering from severe allergies.

6

SWEATER CASHMERE FUND

Performance

March 31, 2023 (unaudited)

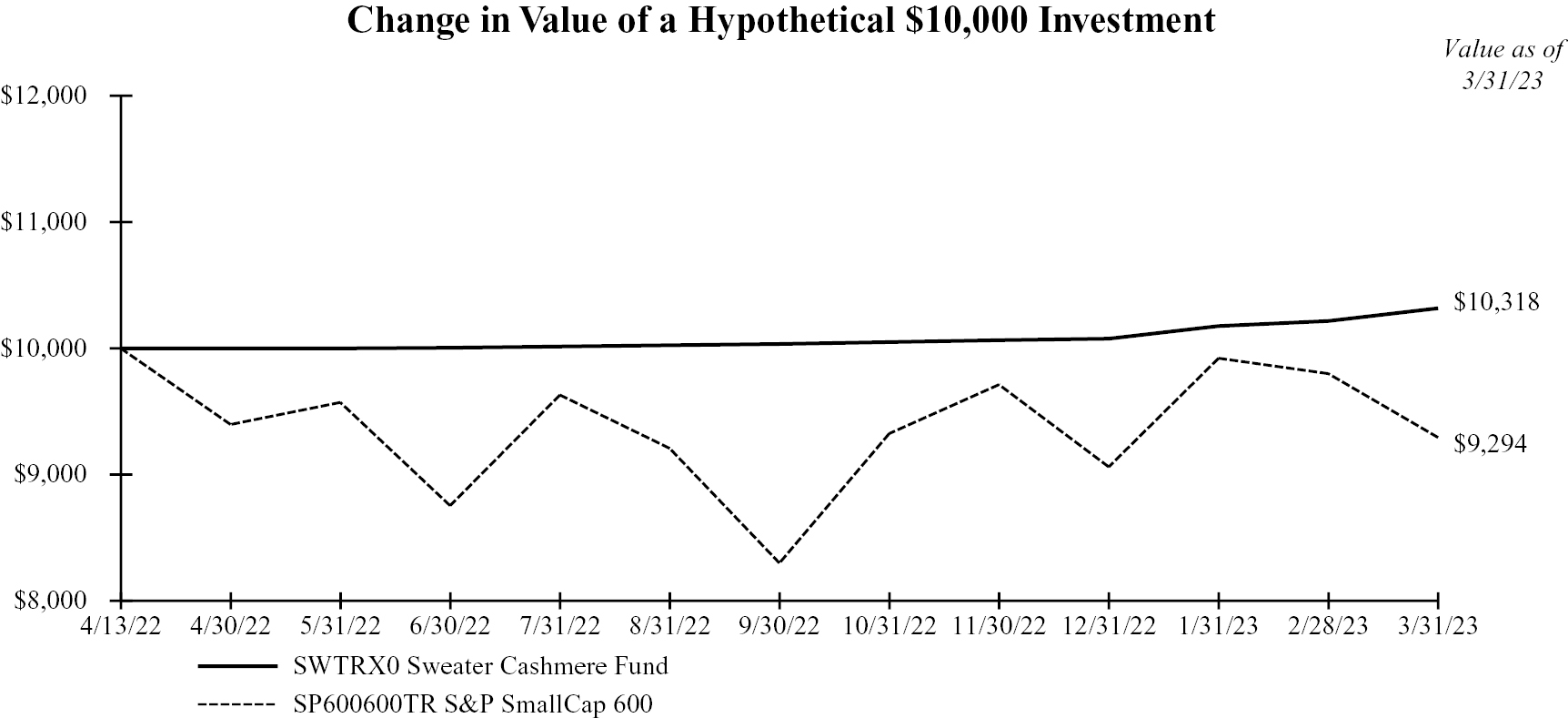

Total Return Information as of March 31, 2023

Sweater Cashmere Fund | Cumulative | ||

Return | 3.18 | % | |

| |||

Fund Benchmark |

| ||

S&P SmallCap 600® Index* | -7.06 | % | |

____________

* The S&P SmallCap 600® is an index of small-cap stocks managed by Standard & Poor’s. It tracks a broad range of small-sized companies that meet specific liquidity and stability requirements. Investors cannot invest directly in an index. Index returns, unlike Fund returns, do not reflect any fees or expenses. Index returns assume reinvestment of all distributions. Investments held by the Fund do not match those in the index and the performance of the Fund will differ.

This graph illustrates the hypothetical investment of $10,000 from April 13, 2022 (inception date) to March 31, 2023.

The performance data quoted here represents past performance. Current performance may be lower or higher than the performance data quoted above. Investment return and principal value will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost. The returns shown assume reinvestment of all distributions, and do not reflect the deduction of taxes that shareholder would pay on Fund distributions or on the redemption of Fund shares. Fund returns would have been lower if a portion of the fees had not been waived and reimbursed by the Fund’s Adviser. Past performance is no guarantee of future results. Please read the Fund’s Prospectus carefully before investing.

7

SWEATER CASHMERE FUND

Portfolio Composition (unaudited)

Fund Vertical Diversification

The following table provides a breakdown of the Fund, by the industry verticals that the underlying securities represent, as a percentage of net assets as of March 31, 2023.

Vertical | Percent of | ||

Consumer Goods and Retail | 12.8 | % | |

Consumer Technology | 15.1 | % | |

Education Technology | 2.1 | % | |

Financial Technology | 1.8 | % | |

Healthcare | 10.8 | % | |

Human Resource Technology | 9.2 | % | |

Logistics | 2.1 | % | |

Mobility Technology | 4.2 | % | |

Private Investment Companies | 3.6 | % | |

Property Technology | 5.5 | % | |

Short-Term Investments | 35.1 | % | |

Liabilities in excess of other assets | (2.3 | )% | |

TOTAL | 100.0 | % | |

Fund Security Type Diversification

The following chart provides a visual breakdown of the Fund, by the security type that the underlying securities represent, as a percentage of net assets as of March 31, 2023.

Security Type | Percent of | ||

Convertible Debt in Portfolio Companies | 4.2 | % | |

Equity Investments in Portfolio Companies | 24.8 | % | |

Portfolio Funds | 3.6 | % | |

Simple Agreements for Future Equity in Portfolio Companies | 34.6 | % | |

Short-Term Investments | 35.1 | % | |

Liabilities in Excess of Other Assets | (2.3 | )% | |

TOTAL | 100.0 | % | |

8

Sweater Cashmere Fund

SCHEDULE OF INVESTMENTS

March 31, 2023

Fair Value | |||

Convertible Debt in Portfolio Companies — 4.2% |

| ||

Consumer Goods and Retail — 4.2% |

| ||

Cabinet Health P.B.C., Principal $500,000, 4.55%, due 2/3/251,3 | $ | 500,000 | |

Total Convertible Debt in Portfolio Companies (Cost $500,000) |

| 500,000 | |

| |||

Equity Investments in Portfolio Companies — 24.8% |

| ||

Consumer Goods and Retail — 4.6% |

| ||

IQ Bar, Inc. Series B Preferred Stock, shares 41,5531,2,3 |

| 250,000 | |

Nomadica Series Seed-6 Preferred Stock, shares 462,1071,2,3 |

| 300,370 | |

| 550,370 | ||

| |||

Consumer Technology — 6.4% |

| ||

GO, Inc., Series Seed-1 Preferred Stock, shares 400,1601,2,3 |

| 500,000 | |

Havenly, Inc. Series C-1 Preferred Stock, shares 63,8481,2,3 |

| 249,997 | |

Total Consumer Technology |

| 749,997 | |

| |||

Human Resource Technology — 9.2% |

| ||

IsoTalent, Inc. Series Seed-1 Preferred Stock, shares 764,2921,2,3 |

| 1,084,377 | |

| |||

Property Technology — 4.6% |

| ||

Eloit Street, Inc. dba Guest House Series C-2 Preferred Stock, shares 2,012,8821,2,3 |

| 300,000 | |

True Footage Inc. Series A Prime Preferred Stock, shares 38,8361,2,3 |

| 250,000 | |

Total Property Technology |

| 550,000 | |

| |||

Total Equity Investments in Portfolio Companies (Cost $2,799,996) |

| 2,934,744 | |

| |||

Portfolio Funds — 3.6% |

| ||

Private Investment Companies — 3.6% |

| ||

Curate Capital Fund I, LP1,2,4,5 |

| 158,404 | |

Ganas Ventures I, a series of Ganas Ventures, LP1,2,4 |

| 115,921 | |

Stonks Y Combinator Summer 2022 Access Fund, a Series of Stonks Funds, LP – Class A1,2,4,5 |

| 149,527 | |

Total Portfolio Funds (Cost $445,000) |

| 423,852 | |

| |||

Simple Agreements for Future Equity in Portfolio Companies — 34.6% |

| ||

Consumer Goods and Retail — 4.% |

| ||

Drupely, Inc. dba Graza1,2,3 |

| 220,000 | |

FEAT Socks, Inc.1,2,3 |

| 250,000 | |

Total Consumer Goods and Retail |

| 470,000 | |

| |||

Consumer Technology — 8.7% |

| ||

After Services, Inc. — Tranche 11,2,3 |

| 267,500 | |

After Services, Inc. — Tranche 21,2,3 |

| 267,500 | |

Hearth Display, Inc.1,2,3 |

| 250,000 | |

The Last Gameboard, Inc.1,2,3 |

| 250,000 | |

Total Consumer Technology |

| 1,035,000 | |

| |||

Education Technology — 2.1% |

| ||

EdInvent, Inc. dba Accredible1,2,3 |

| 250,000 | |

| |||

Financial Technology — 1.8% |

| ||

EarlyBird Central, Inc.1,2,3 |

| 210,000 | |

See accompanying Notes to Financial Statements

9

Sweater Cashmere Fund

SCHEDULE OF INVESTMENTS — (CONTINUED)

March 31, 2023

Fair Value | ||||

Healthcare — 10.8% |

|

| ||

Lazzaro Medical, Inc.1,2,3 | $ | 262,500 |

| |

Parallel Health, Inc.1,2,3 |

| 262,500 |

| |

Pear Suite, Inc.1,2,3 |

| 250,000 |

| |

Wyndly Health, Inc.1,2,3 |

| 500,000 |

| |

Total Healthcare |

| 1,275,000 |

| |

|

| |||

Logistics — 2.1% |

|

| ||

Shappi, Inc.1,2,3 |

| 250,000 |

| |

|

| |||

Mobility Technology — 4.2% |

|

| ||

Frances Valentine, LLC1,2,3 |

| 500,000 |

| |

|

| |||

Property Technology — 0.9% |

|

| ||

Nada Holdings, Inc.1,2,3 |

| 108,000 |

| |

Total Simple Agreements for Future Equity in Portfolio Companies (Cost $4,000,000) |

| 4,098,000 |

| |

|

| |||

Short-Term Investments — 35.1% |

|

| ||

Goldman Sachs Financial Square Government Fund – Institutional Class, 4.73%, shares 4,158,0116 | $ | 4,158,011 |

| |

Total Short-Term Investments (Cost $4,158,011) |

| 4,158,011 |

| |

|

| |||

Total Investments (Cost $11,903,007) — 102.3% |

| 12,114,607 |

| |

Liabilities in excess of other assets — (2.3%) |

| (268,065 | ) | |

Net Assets — 100% | $ | 11,846,542 |

| |

____________

P.B.C. — Public Benefit Corporation

LP — Limited Partnership

LLC — Limited Liability Company

1 Restricted security. (See Note 7)

2 Non-Income Producing

3 Level 3 securities fair valued using significant unobservable inputs. (See Note 2)

4 Investment valued using net asset value per share (or its equivalent) as a practical expedient. Please see Note 2 in the Notes to the Financial Statements for respective investment strategies, unfunded commitments, and redemptive restrictions.

5 Affiliated investment for which ownership exceeds 5% of the investment’s capital. (See Note 6)

6 Rate disclosed represents the seven day yield as of period end.

See accompanying Notes to Financial Statements

10

Sweater Cashmere Fund

STATEMENT OF ASSETS AND LIABILITIES

March 31, 2023

Assets: |

| ||

Unaffiliated investments, at fair value (cost $7,424,996) | $ | 7,648,665 | |

Affiliated investments, at fair value (cost $320,000) |

| 307,931 | |

Short-term investments, at fair value (cost $4,158,011) |

| 4,158,011 | |

Receivable for fund shares sold |

| 5,576 | |

Interest income receivable |

| 18,488 | |

Prepaid expenses |

| 38,244 | |

Deferred offering costs (Note 3) |

| 8,524 | |

Total assets |

| 12,185,439 | |

| |||

Liabilities: |

| ||

Payable for audit and tax fees |

| 130,000 | |

Payable for marketing fees |

| 93,347 | |

Due to Adviser (Note 3) |

| 28,318 | |

Payable for transfer agent fees |

| 25,176 | |

Payable for legal fees |

| 22,989 | |

Payable for fund accounting and administration fees |

| 18,973 | |

Payable for other accrued expenses |

| 15,165 | |

Payable for custody fees |

| 4,929 | |

Total liabilities |

| 338,897 | |

Commitments and contingencies (Note 8) |

| ||

| |||

Net Assets | $ | 11,846,542 | |

Components of Net Assets: |

| ||

Paid-in capital (unlimited number of shares authorized) | $ | 11,544,033 | |

Total distributable earnings |

| 302,509 | |

Net Assets | $ | 11,846,542 | |

| |||

Shares of beneficial interest issued and outstanding |

| 575,566 | |

Net asset value per share1 | $ | 20.58 |

____________

1 An early repurchase fee will apply for any shares repurchased within 545 days of purchase (Note 4).

See accompanying Notes to Financial Statements.

11

Sweater Cashmere Fund

STATEMENTS OF OPERATIONS

For the Period Ended March 31, 20231

Investment income: |

|

| ||

Interest income from unaffiliated investments | $ | 120,064 |

| |

Total investment income |

| 120,064 |

| |

|

| |||

Expenses: |

|

| ||

Marketing fees |

| 1,093,808 |

| |

Offering costs |

| 226,994 |

| |

Investment management fees (Note 3) |

| 203,896 |

| |

Insurance fees |

| 175,865 |

| |

Audit and tax fees |

| 130,000 |

| |

Transfer agent fees |

| 120,617 |

| |

Fund accounting and administration fees |

| 107,038 |

| |

Chief compliance & financial officer fees |

| 105,723 |

| |

Trustee fees |

| 87,750 |

| |

Legal fees |

| 82,942 |

| |

Miscellaneous fees |

| 60,382 |

| |

Shareholder reporting fees |

| 29,679 |

| |

Custody fees |

| 17,543 |

| |

Registration fees |

| 6,914 |

| |

Organizational costs |

| 6,670 |

| |

Total expenses |

| 2,455,821 |

| |

Contractual waiver of fees and reimbursement of expenses (Note 3) |

| (1,974,626 | ) | |

Voluntary reimbursement of expenses (Note 3) |

| (481,195 | ) | |

Net expenses |

| — |

| |

Net investment income |

| 120,064 |

| |

Net change in unrealized appreciation on unaffiliated investments |

| 223,669 |

| |

Net change in unrealized depreciation on affiliated investments |

| (12,069 | ) | |

Net change in unrealized appreciation on investments |

| 211,600 |

| |

Net increase in net assets from operations | $ | 331,664 |

|

____________

1 Reflects operations for the period from April 14, 2022 (commencement of operations) to March 31, 2023. Prior to the commencement of operations date, the Fund had been inactive except for matters related to the Fund’s establishment, designation and planned registration.

See accompanying Notes to Financial Statements.

12

Sweater Cashmere Fund

STATEMENTS OF CHANGES IN NET ASSETS

For the | ||||

Increase (Decrease) in Net Assets from: |

|

| ||

Operations: |

|

| ||

Net investment income | $ | 120,064 |

| |

Net change in unrealized appreciation on investments |

| 211,600 |

| |

Net increase in net assets resulting from operations |

| 331,664 |

| |

|

| |||

Distributions to shareholders |

|

| ||

From net investment income |

| (29,155 | ) | |

Total distributions to shareholders |

|

| ||

|

| |||

Capital Transactions: |

|

| ||

Net proceeds from shares sold |

| 11,824,655 |

| |

Reinvestment of distributions |

| 29,155 |

| |

Cost of shares redeemed2 |

| (409,777 | ) | |

Net increase in net assets from capital transactions |

| 11,444,033 |

| |

Total increase in net assets |

| 11,746,542 |

| |

|

| |||

Net Assets: |

|

| ||

Beginning of period3 |

| 100,000 |

| |

End of period | $ | 11,846,542 |

| |

|

| |||

Capital Share Transactions: |

|

| ||

Shares sold |

| 589,546 |

| |

Shares reinvested |

| 1,450 |

| |

Shares redeemed |

| (20,430 | ) | |

Net increase in capital shares outstanding | $ | 570,566 |

| |

____________

1 Reflects operations for the period from April 14, 2022 (commencement of operations) to March 31, 2023. Prior to the commencement of operations date, the Fund had been inactive except for matters related to the Fund’s establishment, designation and planned registration.

2 Net of redemption fees received of $6,584.

3 The investment adviser made the initial share purchase of $100,000 on February 7, 2022. The total initial share purchase of $100,000 included 5,000 shares which were purchased at $20.00 per share.

See accompanying Notes to Financial Statements.

13

Sweater Cashmere Fund

STATEMENT OF CASH FLOWS

For the Period Ended March 31, 20231

Cash flows provided by operating activities: |

|

| ||

Net increase in net assets from operations | $ | 331,664 |

| |

Purchases of investments |

| (7,744,996 | ) | |

Net change in unrealized appreciation on investments |

| (211,600 | ) | |

Change in short-term investments, net |

| (4,158,011 | ) | |

|

| |||

(Increase) in assets: |

|

| ||

Interest income receivable |

| (18,488 | ) | |

Deferred offering costs |

| (8,524 | ) | |

Prepaid expenses |

| (38,244 | ) | |

|

| |||

Increase in liabilities: |

|

| ||

Audit and tax fees |

| 130,000 |

| |

Marketing fees |

| 93,347 |

| |

Due to Adviser fees |

| 28,318 |

| |

Transfer agent fees |

| 25,176 |

| |

Legal fees |

| 22,989 |

| |

Fund accounting and administration fees |

| 18,973 |

| |

Other accrued expenses |

| 15,165 |

| |

Custody fees |

| 4,929 |

| |

Net cash used in operating activities |

| (11,509,302 | ) | |

|

| |||

Cash flows provided by financing activities: |

|

| ||

Proceeds from shares sold, net of receivable for fund shares sold |

| 11,819,079 |

| |

Cost of shares repurchased, net of redemption fees |

| (409,777 | ) | |

Net cash provided by financing activities |

| 11,409,302 |

| |

|

| |||

Net Decrease in Cash |

| (100,000 | ) | |

|

| |||

Cash, beginning of period |

| 100,000 |

| |

End of period |

| — |

| |

|

| |||

Non-cash financing activities not included herein consist of $29,155 of reinvested dividends. |

|

|

____________

1 Reflects operations for the period from April 14, 2022 (commencement of operations) to March 31, 2023. Prior to the commencement of operations date, the Fund had been inactive except for matters related to the Fund’s establishment, designation and planned registration.

See accompanying Notes to Financial Statements.

14

Sweater Cashmere Fund

FINANCIAL HIGHLIGHTS

Per share operating performance.

For a capital share outstanding throughout the period.

For the Period | ||||

Net asset value, beginning of period | $ | 20.00 |

| |

Income from Investment Operations: |

|

| ||

Net investment income2 |

| 0.29 |

| |

Net realized and unrealized gain |

| 0.32 |

| |

Total from investment operations |

| 0.61 |

| |

Less Distributions: |

|

| ||

From net investment income |

| (0.05 | ) | |

Total distributions |

| (0.05 | ) | |

Redemption Fees2: |

| 0.02 |

| |

Net asset value, end of period | $ | 20.58 |

| |

Total return3,4 |

| 3.18 | % | |

|

| |||

Ratios and Supplemental Data: |

|

| ||

Net assets, end of period (in thousands) | $ | 11,847 |

| |

|

| |||

Ratio of expenses to average net assets: |

|

| ||

Gross5,6 |

| 30.02 | % | |

Net5,6,7 |

| 0 | % | |

Ratio of net investment income (loss) to average net assets: |

|

| ||

Net5,6,7 |

| 1.47 | % | |

|

| |||

Portfolio turnover rate4 |

| 0 | % | |

____________

1 Reflects operations for the period from April 14, 2022 (commencement of operations) to March 31, 2023. Prior to the commencement of operations date, the Fund had been inactive except for matters related to the Fund’s establishment, designation, and planned registration.

2 Based on average shares outstanding for the period.

3 Based on the net asset value as of period end. Assumes an investment at net asset value at the beginning of the period and reinvestment of all distributions during the period. Returns shown do not include payment of an early repurchase fee for shares redeemed within 545 days of purchase. The return would have been lower if certain expenses had not been waived or reimbursed by the Adviser.

4 Not annualized.

5 Annualized, with the exception of non-recurring organizational costs.

6 The ratios of expenses and net investment income to average net assets do not reflect the Fund’s proportionate share of income and expenses of underlying investment companies in which the Fund invests, including management and performance fees. As of March 31, 2023, the Fund’s underlying investment companies included a range of management fees from 0.00% to 2.00% (unaudited) and performance fees from 0.00% to 20.00% (unaudited).

7 Represents the ratios of expenses and net investment income (loss) inclusive of fee waivers and/or expenses reimbursements (Note 3).

15

Sweater Cashmere Fund

NOTES TO THE FINANCIAL STATEMENTS

March 31, 2023

1. Organization

Sweater Cashmere Fund (the “Fund”) was organized on June 17, 2021, as a statutory trust under the laws of the state of Delaware. The Fund is a non-diversified, closed-end management investment company that operates as an interval fund pursuant to Rule 23c-3 of the Investment Company Act of 1940, as amended (the “1940 Act”). The Fund has an inception date of April 13, 2022 and commenced operations on the following business day.

The Fund’s investment objective is to generate long-term capital appreciation primarily through an actively managed portfolio that provides investors with exposure to private, venture capital investments. The Fund will seek to achieve its investment objective through investing primarily in equity securities (e.g., common stock, preferred stock, and equity-linked securities convertible into equity securities) of private, operating growth companies (“Portfolio Companies”) and, to a lesser extent, interests in professionally managed private venture capital funds (“Portfolio Funds”). The Fund anticipates acquiring interests in the Portfolio Companies both directly from the issuer, including through co-investing with venture capital funds and other investors, and from third party holders of these interests in secondary transactions.

Sweater Industries, LLC, an investment adviser registered under the Investment Advisers Act of 1940 (the “Advisers Act”), as amended, serves as the Fund’s investment adviser (the “Adviser”). The Fund’s Board of Trustees (the “Board” or “Board of Trustees”) has the overall responsibility for the management and supervision of the business operations of the Fund.

2. Significant accounting policies

The price of the Fund’s shares of beneficial interest (“Shares”) is based on its net asset value (“NAV”). The NAV per Share equals the total value of the Fund’s assets as of the applicable Business Day, less its liabilities (including accrued fees and expenses), divided by the number of its outstanding Shares.

The Fund will generally calculate its NAV as of the close of regular trading (4:00 p.m. Eastern Time) on the New York Stock Exchange (the “NYSE”) each day the NYSE is open (each, a “Business Day”). Although the Fund will typically determine its NAV on each Business Day, the Fund’s calculation of its NAV is subject to valuation risk.

Basis of Presentation and Use of Estimates — The Fund is an investment company and as a result, maintains its accounting records and has presented these financial statements in accordance with the reporting requirements under Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 946, Financial Services — Investment Companies (“ASC 946”). The policies are in conformity with generally accepted accounting principles (“GAAP”), which requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statement, as well as reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from these estimates.

Income Recognition and Expenses — Interest income is recognized on an accrual basis as earned. Dividend income is recorded on the ex-dividend date. Expenses are recognized on an accrual basis as incurred. The Fund bears all expenses incurred in the course of its operations, including, but not limited to, the following: all costs and expenses related to portfolio transactions and positions for the Fund’s account; professional fees; costs of insurance; registration expenses; marketing expenses; and expenses of meetings of the Board. Expenses are subject to the Fund’s Expense Limitation Agreement (see Note 3).

All cash, receivables and current payables are carried on the Fund’s books at their net realizable value.

Investment Transactions — Investment transactions are accounted for on a trade date basis. Cost is determined and gains and losses are based upon the identified cost basis for publicly traded investments and a dollar-for-dollar cost depletion for the Fund’s private investments for both financial statement and federal income tax purposes.

16

Sweater Cashmere Fund

NOTES TO THE FINANCIAL STATEMENTS

March 31, 2023

2. Significant accounting policies (cont.)

Federal Income Taxes — The Fund has elected and intends to continue to elect to be treated, and expects each year to qualify, as a regulated investment company (“RIC”) under the provisions of Subchapter M of the Internal Revenue Code of 1986, as amended. As such, the Fund generally will not be subject to U.S. federal corporate income tax, provided that it distributes substantially all of its net taxable income and gains on a timely basis and meets the other quarterly compliance requirements.

The Fund recognizes the tax benefits or expenses of uncertain tax positions only when the position is “more likely than not” to be sustained assuming examination by tax authorities. Management has reviewed the Fund’s tax positions and concluded that no provision for unrecognized tax benefits or expenses should be recorded related to uncertain tax positions taken in the Fund’s current tax year and all open tax years.

Distributions to shareholders — Following the disposition by the Fund of securities of Portfolio Companies, or the receipt by the Fund of distribution proceeds from a Portfolio Fund, the Fund will make cash distributions of the net profits, if any, to shareholders once each fiscal year at such time as the Board determines in its sole discretion (or more often at such times determined by the Board, if necessary for the Fund to maintain its status as a RIC and in accordance with the Investment Company Act). The Fund intends to establish reasonable reserves to meet Fund obligations prior to making distributions.

Investment Valuation

In December 2020, the Securities and Exchange Commission (“SEC”) adopted a new rule providing a framework for fund valuation practices (“Rule 2a-5”). Rule 2a-5 establishes requirements for determining fair value in good faith for purposes of the 1940 Act. The Fund was required to comply with Rule 2a-5 by September 8, 2022 and as a result, the Board has approved valuation procedures for the Fund (the “Valuation Procedures”) which are used for determining the fair value of any Fund investments for which a market quotation is not readily available. The valuation of the Fund’s investments is performed in accordance with the principles found in Rule 2a-5 and in conjunction with FASB’s ASC Topic 820, Fair Value Measurements and Disclosures (“ASC 820”). The Board has designated the Adviser as the valuation designee of the Fund. As valuation designee, the Adviser performs the fair value determination relating to any and all Fund investments, subject to the conditions and oversight requirements described in the Valuation Procedures. In furtherance of its duties as valuation designee, the Adviser has formed a valuation committee (the “Valuation Committee”), to perform fair value determinations and oversee the Adviser’s day-to-day functions related to the fair valuation of the Fund’s investments. The Valuation Committee may consult with representatives from the Fund’s outside legal counsel or other third-party consultants in their discussions and deliberations.

Shares of mutual funds, including money-market funds, are fair valued at their reported NAV.

A substantial portion of the Fund’s assets consist of securities of Equity Investments in Portfolio Companies, which may be made through Simple Agreements for Future Equity and Convertible Debt, and Portfolio Funds for which there are no readily available market quotations. New purchases of Equity Investments in Portfolio Companies and Portfolio Funds may be valued at acquisition cost initially.

The information available in the marketplace for such Portfolio Companies, their securities and the status of their businesses and financial conditions is often extremely limited, outdated, and difficult to confirm. Such securities are valued by the Adviser at fair value as determined pursuant to the Valuation Procedures. In determining fair value, the Adviser is required to consider all appropriate factors relevant to value and all indicators of value available to the Adviser. The determination of fair value necessarily involves judgment in evaluating this information in order to determine the price that the Fund might reasonably expect to receive for the security upon its current sale. The most relevant information may often be that information which is provided by the issuer of the securities. Given the nature, timeliness, amount, and reliability of information provided by the issuer, fair valuations may become more difficult and uncertain as such information is unavailable or becomes outdated.

Certain investments for which market quotations are not readily available or for which market quotations are deemed not to represent fair value may be valued using a market approach, an income approach, or both approaches, as appropriate. The market approach uses prices and other relevant information generated by market transactions

17

Sweater Cashmere Fund

NOTES TO THE FINANCIAL STATEMENTS

March 31, 2023

2. Significant accounting policies (cont.)

involving identical or comparable assets or liabilities (including a business). The income approach uses valuation techniques to convert future amounts (for example, cash flows or earnings) to a single present amount (discounted). The measurement is based on the value indicated by current market expectations about those future amounts. In following these approaches, the types of factors that we may take into account in determining the fair value of our investments include, as relevant and among other factors: available current business data (e.g., information available through regulatory filings, press releases, news feeds and financial press), including relevant and applicable market trading and transaction comparables; applicable market yields and multiples; information provided by the company (e.g., letters to investors, financials, information provided pursuant to financial document reporting obligations); security covenants; call protection provisions; information rights; the nature and realizable value of any collateral; the portfolio company’s ability to make payments; its earnings and discounted cash flows; the markets in which the portfolio company does business; comparisons of financial ratios of peer companies that are public; M&A comparables; and enterprise values.

In valuing Portfolio Fund investments held in the Fund, the Adviser will rely primarily on unaudited valuation statements received from such funds on a quarterly basis, and (when available) audited values received on an annual basis. It will usually be the case, however, that the most recently reported value by such funds will be as of a date that is a quarter in arrears than the date as of which the Fund is calculating its NAV. In these circumstances, and in other situations where the Adviser determines that the consideration of the following factors is relevant to determining the value of an interest in a Portfolio Fund, such fund’s reported value will generally be adjusted for cash flows to/from such fund due to capital drawdowns/distributions that may have occurred since the date of the most recently available reported values; changes in the valuation of relevant indices; and such other factors that the Adviser deems appropriate, as well as any publicly available information regarding such fund’s portfolio companies and/or assets (i.e., idiosyncratic factors). Other factors that may be relevant in determining the value of an interest in a Portfolio Fund, include (i) information provided to the Fund or to the Adviser by such fund, or the failure to provide such information as agreed to in such fund’s offering materials or other agreements with the Fund; (ii) relevant news and other public sources; (iii) known secondary market transactions in the fund’s interests (to the extent deemed a credible indication of value); and (iv) significant market events that may not otherwise be captured by changes in valuation of relevant indices discussed above. As part of the Adviser’s ongoing due diligence process, the Adviser will compare its fair valuation of the Fund’s interests in a Portfolio Fund to such fund’s quarterly valuation statement for that particular period — if provided by the Portfolio Fund — for purposes of determining whether any adjustments to the implementation of the Valuation Procedures should be made going forward.

When determining the price for an investment to be fair valued, the Adviser is required to seek to determine the price that the Fund might reasonably expect to receive from the current sale of that asset or liability in an arm’s-length transaction. The price generally may not be determined based on what the Fund might reasonably expect to receive for selling an asset or liability at a later time or if it holds the asset or liability to maturity. Fair value determinations are typically based upon all available factors that the Adviser deems relevant at the time of the determination and may be based on analytical values determined by the Adviser using proprietary or third-party valuation models.

The Fund’s financial statements, which are prepared in accordance with GAAP, follow the requirements for valuation set forth in ASC 820, which defines and establishes a framework for measuring fair value under GAAP and expands financial statement disclosure requirements relating to fair value measurements.

The three-level hierarchy for fair value measurement is defined as follows:

• Level 1 — Unadjusted price quotations in active markets/exchanges for identical assets or liabilities that the Fund has the ability to access

• Level 2 — Other observable inputs (including, but not limited to, quoted prices for similar assets or liabilities in markets that are active, quoted prices for identical or similar assets or liabilities in markets that are not active, inputs other than quoted prices that are observable for the assets or liabilities (such as interest rates, yield curves, volatilities, prepayment speeds, loss severities, credit risks and default rates) or other market — corroborated inputs)

18

Sweater Cashmere Fund

NOTES TO THE FINANCIAL STATEMENTS

March 31, 2023

2. Significant accounting policies (cont.)

• Level 3 — Unobservable inputs based on the best information available in the circumstances, to the extent observable inputs are not available (including the Fund’s own assumptions used in determining the fair value of investments)

Investments in private investment companies that are reported in the Fund’s statement of assets and liabilities at NAV per share (or its equivalent) without further adjustment, as a practical expedient of fair value, are excluded from the fair value hierarchy.

In certain cases, the inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, an investment’s level within the fair value hierarchy is based on the lowest level of input that is significant to the overall fair value measurement. The Adviser’s assessment of the significance of a particular input to the fair value measurement in its entirety requires judgment and consideration of factors specific to the investment.

The Fund expects that it will hold a high proportion of Level 3 investments relative to its total investments, which is directly related to the Fund’s investment strategy and target investments.

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. The following is a summary of the inputs used to determine fair value of the Fund’s investments as of March 31, 2023:

Investments | Practical | Level 1 | Level 2 | Level 3 | Total | ||||||||||

Security Type |

|

|

|

|

| ||||||||||

Convertible Debt in Portfolio Companies | $ | — | $ | — | $ | — | $ | 500,000 | $ | 500,000 | |||||

Equity Investments in Portfolio |

| — |

| — |

| — |

| 2,934,744 |

| 2,934,744 | |||||

Portfolio Funds* |

| 423,852 |

| — |

| — |

| — |

| 423,852 | |||||

Simple Agreements for Future Equity in Portfolio Companies* |

| — |

| — |

| — |

| 4,098,000 |

| 4,098,000 | |||||

Short-Term Investments |

| — |

| 4,158,011 |

| — |

| — |

| 4,158,011 | |||||

Total | $ | 423,852 | $ | 4,158,011 | $ | — | $ | 7,532,744 | $ | 12,114,607 | |||||

____________

* All sub-categories within the security type represent their respective evaluation status. For a detailed breakout, please refer to the Schedule of Investments.

The following is a roll-forward of the activity in investments in which signifcant unobservable inputs (Level 3) were used in determing fair value on a recurring basis:

Beginning | Transfers | Purchases or | Sales or | Net | Distributions | Change in net | Ending | |||||||||||||||||

Convertible Debt in Portfolio Companies | $ | — | $ | — | $ | 500,000 | $ | — | $ | — | $ | — | $ | — | $ | 500,000 | ||||||||

Equity Investments in Portfolio Companies |

| — |

| — |

| 2,799,996 |

| — |

| — |

| — |

| 134,748 |

| 2,934,744 | ||||||||

Simple Agreements for Future Equity in Portfolio Companies |

| — |

| — |

| 4,000,000 |

| — |

| — |

| — |

| 98,000 |

| 4,098,000 | ||||||||

$ | — | $ | — | $ | 7,299,996 | $ | — | $ | — | $ | — | $ | 232,748 | $ | 7,532,744 | |||||||||

The change in net unrealized appreciation (depreciation) included in the Statement of Operations attributable to Level 3 investments that were held as of March 31, 2023 is $232,748.

19

Sweater Cashmere Fund

NOTES TO THE FINANCIAL STATEMENTS

March 31, 2023

2. Significant accounting policies (cont.)

The following is a summary of quantitative information about significant unobservable valuation inputs for Level 3 Fair Value Measurements for investments held as of March 31, 2023:

Fair Value | Valuation | Unobservable | Range of | ||||||

Equity Investments in Portfolio Companies | $ | 1,084,377 | Market Approach | Calibration | 2.27% – 19.20%/ | ||||

Simple Agreements for Future Equity in Portfolio Companies |

| 1,598,000 | Market Approach | Calibration | (18.21)% – 40.09%/ | ||||

Total Level 3 Investments(2) | $ | 2,682,377 | |||||||

____________

(1) To the extent the unobservables inputs increase or decrease there is a corresponding increase or decrease in fair value.

(2) Certain Level 3 investments of the Fund, totaling fair value assets of $4,850,367, have been recorded at fair value using unadjusted third-party inputs (for example, third-party transactions, or recent transaction price). As such, these investments have been excluded from the preceding table.

The following is the fair value measurement of investments that are measured at NAV per share (or its equivalent) as a practical expedient:

Portfolio Funds* | Investment | Fair | Unfunded | Redemption | Redemption Notice Period | Lock Up | ||||||||

Curate Capital Fund I, LP | Early Stage Technology | $ | 158,404 | $ | — | None | Not Applicable | Not Applicable | ||||||

Ganas Ventures I, a series of Ganas Ventures, LP | Early Stage Technology |

| 115,921 |

| 125,000 | None | Not Applicable | Not Applicable | ||||||

Stonks Y Combinator Summer 2022 Access Fund, a Series of Stonks Funds, LP – Class A | Early Stage Technology |

| 149,527 |

| — | None | Not Applicable | Not Applicable | ||||||

____________

* Refer to the Schedule of Investment for industry classifications of individual securities.

3. Fees and Transactions with Related Parties and Other Agreements

The Fund has entered into an Investment Management Agreement with the Adviser, pursuant to which the Adviser provides general investment advisory services for the Fund. For providing these services, the Investment Adviser receives a fee from the Fund, accrued daily and paid monthly in arrears, at an annual rate equal to 2.50% of the Fund’s average daily net assets. For the period from April 14, 2022 (commencement of operations) to March 31, 2023, the Fund accrued $203,896 in investment management fees.

The Adviser has entered into an expense limitation agreement (“Expense Limitation Agreement”) with the Fund, pursuant to which the Adviser has agreed to waive its management fees and/or reimburse Fund expenses to the extent necessary so that the Fund’s total annual operating expenses (excluding any taxes, interest, brokerage commissions, acquired fund fees and expenses, and extraordinary expenses, such as litigation or reorganization costs, but inclusive of organizational costs and offering costs) (“Operating Expenses”) do not exceed 5.90% of the Fund’s average daily net assets. The Expense Limitation Agreement is in effect through August 15, 2024.

20

Sweater Cashmere Fund

NOTES TO THE FINANCIAL STATEMENTS

March 31, 2023

3. Fees and Transactions with Related Parties and Other Agreements (cont.)

The Fund has agreed to repay the Adviser for any management fees waived and/or Fund expenses the Adviser reimbursed pursuant to the Expense Limitation Agreement, provided the repayments do not cause the Fund’s Operating Expenses to exceed the expense limitation in place at the time the management fees were waived and/or the Fund expenses were reimbursed, or any expense limitation in place at the time the Fund repays the Adviser, whichever is lower. Any such repayments must be made within three years after the Adviser waived the fee or reimbursed the expense. During the period from April 14, 2022 (commencement of operations) to March 31, 2023, the Adviser did not recoup any expenses. As of March 31, 2023, $1,974,626 is subject to recoupment through March 31, 2026. For the period from April 14, 2022 (commencement of operations) to March 31, 2023, the Adviser voluntarily reimbursed $481,195 of Fund expenses which are not subject to recoupment. Additionally, $209,030 of the $214,930 waived organizational costs, incurred as of March 31, 2022, are subject to recoupment through March 31, 2025. The remaining $5,900 of waived organizational costs were voluntarily waived by the Adviser and are not subject to recoupment.

For the period from April 14, 2022 (commencement of operations) to March 31, 2023 organizational costs of $6,670 have been expensed as incurred and are subject to the Fund’s Expense Limitation Agreement. Organizational expenses consist of costs incurred to establish the Fund and enable it to legally do business. The Fund’s offering costs of $235,518 consist of legal fees for preparing the prospectus and statement of additional information in connection with the Fund’s registration and public offering, state registration fees and insurance. Offering costs are accounted for as a deferred charge and then are amortized on a straight-line basis over the first twelve months of the Fund’s operations. As of March 31, 2023, $8,524 of offering costs remain as an unamortized deferred asset, while $226,994 has been expensed subject to the Fund’s Expense Limitation Agreement.

In consideration of the services rendered by those Trustees who are not “interested persons” (as defined in Section 2(a)19 of the 1940 Act) of the Trust (“Independent Trustees”), the Fund pays each Independent Trustee an annual retainer of $25,000. In addition, for the Fund’s first fiscal year of operations ending March 31, 2023, the Fund paid each Independent Trustee an additional one-time fee of $4,250 in recognition of services the Independent Trustees provided prior to the Fund’s commencement of operations. Independent Trustees are also reimbursed by the Fund for expenses they incur relating to their services as Trustees, including travel and other expenses incurred in connection with attendance at in-person Board and Committee meetings. The Independent Trustees do not receive any other compensation from the Fund. Trustees that are interested persons are not compensated by the Fund.

Certain officers of the Fund and members of the Board are also officers of the Adviser.

Employees of PINE Advisors LLC (“PINE”) serve as officers of the Fund. PINE receives a monthly fee for the services provided to the Fund. The Fund also reimburses PINE for certain out-of-pocket expenses incurred on the Fund’s behalf.

UMB Fund Services, Inc. serves as the Fund’s Administrator, Accounting Agent, and Transfer Agent. UMB Bank, n.a. serves as the Fund’s Custodian.

4. Capital share transactions

Fund shares are continually offered under Rule 415 of the Securities Act of 1933, as amended. As an interval fund, the Fund has adopted a fundamental policy requiring it to make semiannual (twice a year) repurchase offers pursuant to Rule 23c-3 of the 1940 Act. Each semiannual repurchase offer will be for 5% of the Fund’s Shares at NAV. An early repurchase fee will be applied for Shares held less than 545 days. For Shares held for 185 days or less, a 2.00% fee will be applied. For Shares held between 186 and 365 days, a 1.5% fee will be applied. For Shares held between 366 days and 545 days, a 0.50% fee will be applied. Early repurchase fees will be based on the value of the Shares redeemed.

21

Sweater Cashmere Fund

NOTES TO THE FINANCIAL STATEMENTS

March 31, 2023

4. Capital share transactions (cont.)

During the period from April 14, 2022 (commencement of operations) to March 31, 2023, the Fund completed one repurchase offer. The result of this repurchase offer is as follows:

Required | ||

Commencement Date | January 27, 2023 | |

Repurchase Request Deadline | February 28, 2023 | |

Repurchase Pricing Date | February 28, 2023 | |

Repurchase Pricing Date Net Asset Value | $20.38 | |

Shares Repurchased | 20,430 | |

Value of Shares Repurchased (Before Redemption Fees) | $416,361 | |

Percentage of Shares Repurchased | 3.53% |

5. Investment transactions

Purchases and sales of investments for the period from April 14, 2022 (commencement of operations) to March 31, 2023, were $7,744,996 and $0, respectively.

6. Affiliated Investments

Issuers that are considered affiliates, as defined in Section 2(a)(3) of the 1940 Act, of the Fund at period-end are noted in the Fund’s Schedule of Investments. The table below reflects transactions during the period with entities that are affiliates as of March 31, 2023 and may include acquisitions of new investments, prior year holdings that become affiliated during the period, and prior period affiliated holdings that are no longer affiliated as of period-end.

Non-Controlled Affiliate | Beginning | Purchases or | Sales or | Change in | Net | Return of | Ending | Investment | |||||||||||||||||

Curate Capital Fund I, LP | $ | — | $ | 170,000 | $ | — | $ | (11,596 | ) | $ | — | $ | — | $ | 158,404 |

| — | ||||||||

Stonks Y Combinator Summer 2022 Access Fund, a Series of Stonks Funds, LP – Class A |

| — |

| 150,000 |

| — |

| (473 | ) |

| — |

|

| $ | 149,527 |

| — | ||||||||

$ | — | $ | 320,000 | $ | — | $ | (12,069 | ) | $ | — |

|

| $ | 307,931 | $ | — | |||||||||

7. Restricted securities

Restricted securities include securities that have not been registered under the Securities Act of 1933, as amended, and securities that are subject to restrictions on resale. The Fund may invest in restricted securities that are consistent with the Fund’s investments objectives and investment strategies. Investments in restricted securities are valued at fair value as determined in good faith in accordance with procedures adopted by the Board.

22

Sweater Cashmere Fund

NOTES TO THE FINANCIAL STATEMENTS

March 31, 2023

7. Restricted securities (cont.)

Additional information on each restricted investment held by the Fund on March 31, 2023 is as follows:

Investments | Initial | Cost | Fair | % of | |||||||

After Services, Inc. – Tranche 1 | 6/6/2022 | $ | 250,000 | $ | 267,500 | 2.3 | % | ||||

After Services, Inc. – Tranche 2 | 6/6/2022 |

| 250,000 |

| 267,500 | 2.3 | % | ||||

Cabinet Health, P.B.C. | 2/14/2023 |

| 500,000 |

| 500,000 | 4.2 | % | ||||

Curate Capital Fund I, LP | 7/1/2022 |

| 170,000 |

| 158,404 | 1.3 | % | ||||

Drupely, Inc. dba Graza | 6/17/2022 |

| 200,000 |

| 220,000 | 1.9 | % | ||||

EarlyBird Central, Inc. | 6/3/2022 |

| 200,000 |

| 210,000 | 1.8 | % | ||||

EdInvent, Inc. dba Accredible | 7/29/2022 |

| 250,000 |

| 250,000 | 2.1 | % | ||||

Eloit Street, Inc. dba Guest House | 11/8/2022 |

| 300,000 |

| 300,000 | 2.5 | % | ||||

Feat Socks, Inc. | 6/15/2022 |

| 250,000 |

| 250,000 | 2.1 | % | ||||

Frances Valentine, LLC | 11/18/2022 |

| 500,000 |

| 500,000 | 4.2 | % | ||||

Ganas Ventures I, a series of Ganas Ventures, LP | 7/1/2022 |

| 125,000 |

| 115,921 | 1.0 | % | ||||

GO, Inc. Series Seed-1 Preferred Stock | 11/18/2022 |

| 500,000 |

| 500,000 | 4.2 | % | ||||

Havenly Inc., Series C-1 | 2/10/2023 |

| 249,997 |

| 249,997 | 2.1 | % | ||||

Hearth Display Inc. | 1/6/2023 |

| 250,000 |

| 250,000 | 2.1 | % | ||||

IQ Bar, Inc. | 8/12/2022 |

| 250,000 |

| 250,000 | 2.1 | % | ||||

IsoTalent, Inc. Series Seed-1 Preferred Stock | 7/8/2022 |

| 1,000,000 |

| 1,084,377 | 9.1 | % | ||||

Lazzaro Medical, Inc. | 7/1/2022 |

| 250,000 |

| 262,500 | 2.2 | % | ||||

Nada Holdings, Inc. | 6/17/2022 |

| 100,000 |

| 108,000 | 0.9 | % | ||||

Nomadica Series Seed-6 Preferred Stock | 7/1/2022 |

| 250,000 |

| 300,370 | 2.5 | % | ||||

Parallel Health, Inc. | 6/28/2022 |

| 250,000 |

| 262,500 | 2.2 | % | ||||

Pear Suite, Inc. | 11/14/2022 |

| 250,000 |

| 250,000 | 2.1 | % | ||||

Shappi, Inc. | 9/16/2022 |

| 250,000 |

| 250,000 | 2.1 | % | ||||

Stonks Y Combinator Summer 2022 Access Fund, a Series of Stonks Funds, LP – Class A | 9/16/2022 |

| 150,000 |

| 149,527 | 1.3 | % | ||||

The Last Gameboard, Inc. | 12/9/2022 |

| 250,000 |

| 250,000 | 2.1 | % | ||||

True Footage Inc. Series A Prime Preferred Stock | 7/29/2022 |

| 250,000 |

| 250,000 | 2.1 | % | ||||

Wyndly Health, Inc. | 9/13/2022 |

| 500,000 |

| 500,000 | 4.2 | % | ||||

$ | 7,744,996 | $ | 7,956,596 | 67.2 | % | ||||||

8. Commitments and contingencies

In the normal course of business, the Fund will enter into contracts that contain a variety of representations, provide general indemnifications, set forth termination provisions and compel the contracting parties to arbitration in the event of dispute. From time to time, the Fund may be a party to arbitration, or legal proceedings, in the ordinary course of business, including proceedings relating to the enforcement of provisions of such contracts. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that would be subject to arbitration, generally.

23

Sweater Cashmere Fund

NOTES TO THE FINANCIAL STATEMENTS

March 31, 2023

8. Commitments and contingencies (cont.)

In the normal course of business, the Fund may enter into agreements to purchase and sell investments. Such agreements are subject to certain rights of the issuer’s and ultimately, issuer approval. As of March 31, 2023, the Fund has unfunded commitments in the amount of $125,000 for Ganas Ventures I, a series of Ganas Ventures, LP. At March 31, 2023, the Fund reasonably believes its assets will provide adequate cover to satisfy all its unfunded commitments.

9. Indemnifications

The Fund indemnifies the Fund’s officers and Board of Trustees for certain liabilities that might arise from their performance of their duties to the Fund. Additionally, in the normal course of business the Fund enters into contracts that contain a variety of representations and warranties and which provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred. However, based on experience, the Fund expects the risk of loss to be remote.

10. Federal tax information

At March 31, 2023, gross unrealized appreciation and depreciation of investments owned by the Fund, based on cost for federal income tax purposes were as follows:

Cost of investments | $ | 11,896,273 |

| |

|

| |||

Gross unrealized appreciation | $ | 239,482 |

| |

Gross unrealized depreciation |

| (21,148 | ) | |

Net unrealized appreciation on investments | $ | 218,334 |

|

The difference between cost amounts for financial statement and federal income tax purposes is due primarily to timing differences in recognizing certain gains and losses in security transactions.

The Fund has selected a tax year-end of September 30.

As of September 30, 2022, the components of accumulated earnings (deficit) on a tax basis were as follows:

Undistributed ordinary income | 29,153 | |

Undistributed long-term capital gains | — | |

Tax accumulated earnings | 29,153 | |

Accumulated capital and other losses | — | |

Unrealized appreciation on investments | — | |

Unrealized deferred compensation | — | |

Total accumulated earnings (deficit) | 29,153 |

Income distributions and capital gain distributions are determined in accordance with income tax regulations, which may differ from generally accepted accounting principles. For the tax year ended September 30, 2022, the fund did not make any income or capital gain distributions.

11. Risk factors

An investment in the Fund involves a high degree of risk and may be considered speculative. The following list is not intended to be a comprehensive listing of all the potential risks associated with the Fund. The Fund’s prospectus provides further details regarding the Fund’s risks and considerations.

• The Fund’s inception date was April 13, 2022 and it has a very limited operating history. The Adviser expects that it may take up to two years for the Fund to become primarily invested in Portfolio Companies and Portfolio Funds. Fund performance may be lower during this “ramp-up” period, and may also be more volatile, than would be the case after the Fund is more fully invested. If the Fund were to fail to successfully implement its

24

Sweater Cashmere Fund

NOTES TO THE FINANCIAL STATEMENTS

March 31, 2023

11. Risk factors (cont.)

investment strategies or achieve its investment objective, performance may be negatively impacted, and any resulting liquidation of the Fund could create negative transaction costs for the Fund and tax consequences for investors. There can be no assurance that the Fund will be able to identify, structure, complete and realize upon investments that satisfy its investment objective, or that it will be able to fully invest its offering proceeds.

• The Adviser is newly formed and has no prior experience managing investment portfolios. The Adviser may be unable to successfully execute the Fund’s investment strategy or achieve the Fund’s investment objective.

• There is no public market for Fund Shares and none is expected to develop. Shares are subject to substantial restrictions on transferability. Although the Fund began making semiannual offers to repurchase its Shares beginning in February 2023 (expected to be limited to no more than 5% of the Fund’s outstanding Shares for each such offer), these offers may be oversubscribed and there is no guarantee that you will be able to sell all of the Shares you desire in any semiannual repurchase offer.

• While venture capital investments offer the opportunity for significant gains, these investments also involve an extremely high degree of business and financial risk and can result in substantial losses. Investments in start-up and growth-stage private companies typically involve greater risks than investments in shares of companies that have traded publicly on an exchange for extended periods of time.

• Private companies in which the Fund invests are generally not subject to SEC reporting requirements, are not required to maintain accounting records in accordance with generally accepted accounting principles and are not required to maintain effective internal controls over financial reporting.

• The Fund’s investments in Portfolio Companies may be heavily negotiated and may incur significant transactions costs for the Fund.

• A significant portion of the Fund’s investment portfolio will be illiquid investments recorded at fair value as determined in good faith in accordance with policies and procedures approved by the Board and, as a result, there may be uncertainty as to the value of Fund investments and the NAV of Fund Shares.

12. Subsequent events

In preparing these financial statements, management has evaluated subsequent events through the date of issuance of the financial statements included herein and has determined that there are no subsequent events that require disclosure or adjustment to the financial statements.

25

Sweater Cashmere Fund

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Shareholders and the Board of Trustees of Sweater Cashmere Fund:

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of Sweater Cashmere Fund (the Fund), including the schedule of investments, as of March 31, 2023, the related statements of operations, changes in net assets, and cash flows for the period from April 14, 2022 (commencement of operations) to March 31, 2023, and the related notes to the financial statements (collectively, the financial statements), and the financial highlights for the period from April 14, 2022 (commencement of operations) to March 31, 2023. In our opinion, the financial statements and financial highlights present fairly, in all material respects, the financial position of the Fund as of March 31, 2023, the results of its operations, cash flows, changes in net assets and financial highlights for the period from April 14, 2022 (commencement of operations) to March 31, 2023, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements and financial highlights based on our audit. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Fund in accordance with U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.