| Exhibit 99.1 |

FY22EarningsPRESENTATION February 7, 2023

Disclaimer SIGNA SPORTS UNITED 2 These forward-looking statements include, but are not limited to, statements regarding future events, the estimated or anticipated future results and benefits of SSU following the business combination, future opportunities for SSU, future planned products and services, business strategy and plans, objectives of management for future operations of SSU, market size and growth opportunities, competitive position, technological and market trends, and other statements that are not historical facts. These statements are based on the current expectations of SSU’s management and are not predictions of actual performance. These forward-looking statements are provided for illustrative purposes only and are not intended to serve as, and must not be relied on, by any investor as a guarantee, an assurance, a prediction or a definitive statement of fact or probability. Actual events and circumstances are difficult or impossible to predict and will differ from assumptions. All forward-looking statements are based upon estimates and forecasts and reflect the views, assumptions, expectations, and opinions of the Company, which are all subject to change due to various factors including, without limitation, changes in general economic conditions as a result of the war in Ukraine, significant inflation, higher financing costs, an increase in energy costs, a negative consumer sentiment and COVID-19. Any such estimates, assumptions, expectations, forecasts, views or opinions, whether or not identified in this Presentation, should be regarded as indicative, preliminary and for illustrative purposes only and should not be relied upon as being necessarily indicative of future results. Forward-looking statements appear in a number of places in this Presentation and include, but are not limited to, statements regarding our intent, belief or current expectations. Forward-looking statements are based on our management’s beliefs and assumptions and on information currently available to our management. Such statements are subject to risks and uncertainties, and actual results may differ materially from those expressed or implied in the forward-looking statements due to various factors. The forward-looking statements in this Presentation may include, without limitations, statements about: • our future financial condition and operating results; • our ability to remain in compliance with financial covenants under our financing arrangements; • our ability to extend, renew or refinance our existing debt; • our liquidity and losses from operations and projected cash flows and related impact on our ability to continue as a going concern; • our growth, expansion and acquisition prospects and strategies, the success of such strategies, and the benefits we believe can be derived from such strategies; • our ability to effectively manage our inventory and inventory reserves; • impairments of our goodwill or other intangible assets; • changes in consumer spending patterns and overall levels of consumer spending; • our ability to further upgrade our information technology systems and infrastructure, including our accounting processes and functions, and other risks associated with the systems that operate our online retail operations; • our ability to continue to remedy weaknesses in our internal controls; • costs as a result of operating as a public company; • our assumptions regarding interest rates and inflation; • changes affecting currency exchange rates; • continuing business disruptions arising from the on-going war in Ukraine and in the aftermath of the coronavirus pandemic; • our financial condition and ability to obtain financing in the future to implement our business strategy and fund capital expenditures, acquisitions and other general corporate activities; • estimated future capital expenditures needed to preserve our capital base; • changes in general economic conditions in the Federal Republic of Germany (“Germany”), and the European Union and the Unites States of America, including changes in the unemployment rate, the level of energy and consumer prices, wage levels, etc.; • the further development of online sports markets, in particular the levels of acceptance of internet retailing; • our behavior on mobile devices and our ability to attract mobile internet traffic and convert such traffic into purchases of our goods; • our ability to offer our customers an inspirational and attractive online purchasing experience; • demographic changes, in particular with respect to Germany; • changes in our competitive environment and in our competition level; • the occurrence of accidents, terrorist attacks, natural disasters, fires, environmental damage, or systemic delivery failures; • our inability to attract and retain qualified personnel, consultants and collaborators; • political changes; • changes in laws and regulations; • our expectations relating to dividend payments and forecasts of our ability to make such payments; and • other factors discussed in “Item 3. Key Information — D. Risk Factors” in our 20-F filing as of February 7, 2023. Forward-looking statements are subject to known and unknown risks and uncertainties and are based on potentially inaccurate assumptions that could cause actual results to differ materially from those expected or implied by the forward-looking statements. Actual results could differ materially from those anticipated in forward-looking statements for many reasons, including the factors described in “Item 3. Key Information—D. Risk Factors” in in our 20-F filing as of February 7, 2023. Accordingly, you should not rely on these forward-looking statements, which speak only as of the date of this Presentation. You should, however, review the factors and risks we describe in the reports we will file from time to time with the SEC after the date of this Presentation. In addition, statements such as “we believe” and similar statements reflect our beliefs and opinions on the relevant subject. These statements are based on information available to us as of the date of this Presentation. And while we believe that information provides a reasonable basis for these statements, that information may be limited or incomplete. Our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all relevant information. These statements are inherently uncertain, and you are cautioned not to rely unduly on these statements. Although we believe the expectations reflected in the forward-looking statements were reasonable at the time made, we cannot guarantee future results, level of activity, performance or achievements. Moreover, neither we nor any other person assumes responsibility for the accuracy or completeness of any of these forward-looking statements. You should carefully consider the cautionary statements contained or referred to in this section in connection with the forward-looking statements contained in this Presentation and any subsequent written or oral forward-looking statements that may be issued by us or persons acting on our behalf. Totals have been calculated on the basis of non-rounded euro amounts and may differ from a calculation based on the reported million euro amounts.

Agenda 01. Financial Update 02. commercial change 03. outlook Appendix SIGNA SPORTS UNITED 3

Source: Company information. Note: Core markets represent markets with inventory held in-country. FY19 metrics restated for continuing operations only, as a result of discontinued operations related to Athleisure, pro forma for WCRC, Midwest Sports and Tennis Express. (1) SSU financial year end as of 30 Sep 22. FY22 metrics for continuing operations only, as a result of discontinued operations related to Athleisure, pro forma for WCRC, Midwest Sports and Tennis Express. WCRC closed concurrently with de-SPAC transaction on Dec 14, 21. Tennis Express acquisition closed on Dec 31, 21. FY19 PF FY221 Visits (m) GEOGRAPHIC expansion SSU FY19 – FY22: consolidated positions in most significant sports retail markets SIGNA SPORTS UNITED Active Customers (m) FY19 PF FY221 Net Orders (m) FY19 PF FY221 scale increase over the past 3 years JP AUS / NZ USA SSU Core Market Expansion SSU Core Markets SSU Non-Core Markets

SIGNA SPORTS UNITED 5 challenging Environment – focus on core markets SSU is a buy-and-build strategy; the assets that we have acquired typically operate from a scaled logistics infrastructure serving markets internationally Our businesses are characterized by market-leading positions in core markets and promising international positions where we have competed intensively to win market share and establish SSU’s brands The combination of supply chain disruptions and a deterioration in consumer confidence due to the conflict in Ukraine, has resulted in competitive, overstocked markets significantly impacting profitability, particularly in international markets The current market environment requires SSU to retrench focus on core markets with strong competitive positions and unit economics Clear assessment and focused plan to return the business to run rate profitability1 in FY24: comprehensive strategic realignment assessment underway with a focus on generating long-term shareholder value Adapt commercial and operating models and improve inventory management Focus on core markets and operations Deliver transaction synergies Proactive commitments achieved to ensure financial flexibility in a persistent adverse operating environment Near-term challenges accelerate long-term opportunity to consolidate the highly fragmented specialist sports retail market (1) On an Adjusted EBITDA basis.

Defined near-term plan to adapt the operating model and return the business to profitability Comprehensive assessment of long-term strategy Actions Taken to Respond to Challenging Market in the next 12-18 months SIGNA SPORTS UNITED 6 Cost initiatives Trade Working Capital Financial Flexibility Strategic ReAlignment Comprehensive cost reduction program Logistics consolidation Targeted inventory reduction Focus on terms to achieve structural long-term benefits SSU’s banks have agreed on a temporary relief of covenants €130M commitment secured from major shareholder Ensures runway even in a persistent adverse operating environment

01. Financial update 02. commercial change 03. Outlook APPENDIX Financial Update

FY20 FY21 FY22 Operating in adverse market conditions SIGNA SPORTS UNITED 8 SUPPLY CHALLENGES EASING AS DEMAND DETERIORATED WITH INFLATION SPIKE GLOBAL SUPPLY CHAIN PRESSURE INDEX EU CONSUMER CONFIDENCE INDEX Source: Factset as of December 31, 2022 1.2 (22.2) LEGACY SSU NET REVENUE ORGANIC YOY GROWTH FY22 Reported YoY growth +30.6% +16% organic CAGR vs. pre-Covid (FY22 vs. FY19) Note: Metrics are presented for continuing operations only, as a result of the discontinued operations related to Athleisure. Refer to Note 11- Discontinued Operations. Legacy SSU excluding Midwest Sports, Tennis Express and WCRC. FY22 Set-up: limited visibility on supply, robust consumer confidence Cautious build-up of inventory where possible to mitigate potential future supply shocks (e.g. Omicron) Unforeseen conflict in Ukraine resulting in inflation shock and deterioration in consumer sentiment, materially impacting disposable spending and competitive environment Accelerating market contraction of sports retail market FY23 Set-up: supply chains improved, low consumer confidence, overstocked markets Decelerating contraction of the sports retail market, expected to improve gradually Timing of demand normalization dependent on wage growth and lower inflation; Germany and UK most affected Market overstock and cost inflation will impact sports retail industry profitability in FY23 Dislocations driving organic and inorganic consolidation which will result in an improved market structure Start of conflict in Ukraine 0.1 (6.5) FY23 FY20 FY21 FY22 FY23

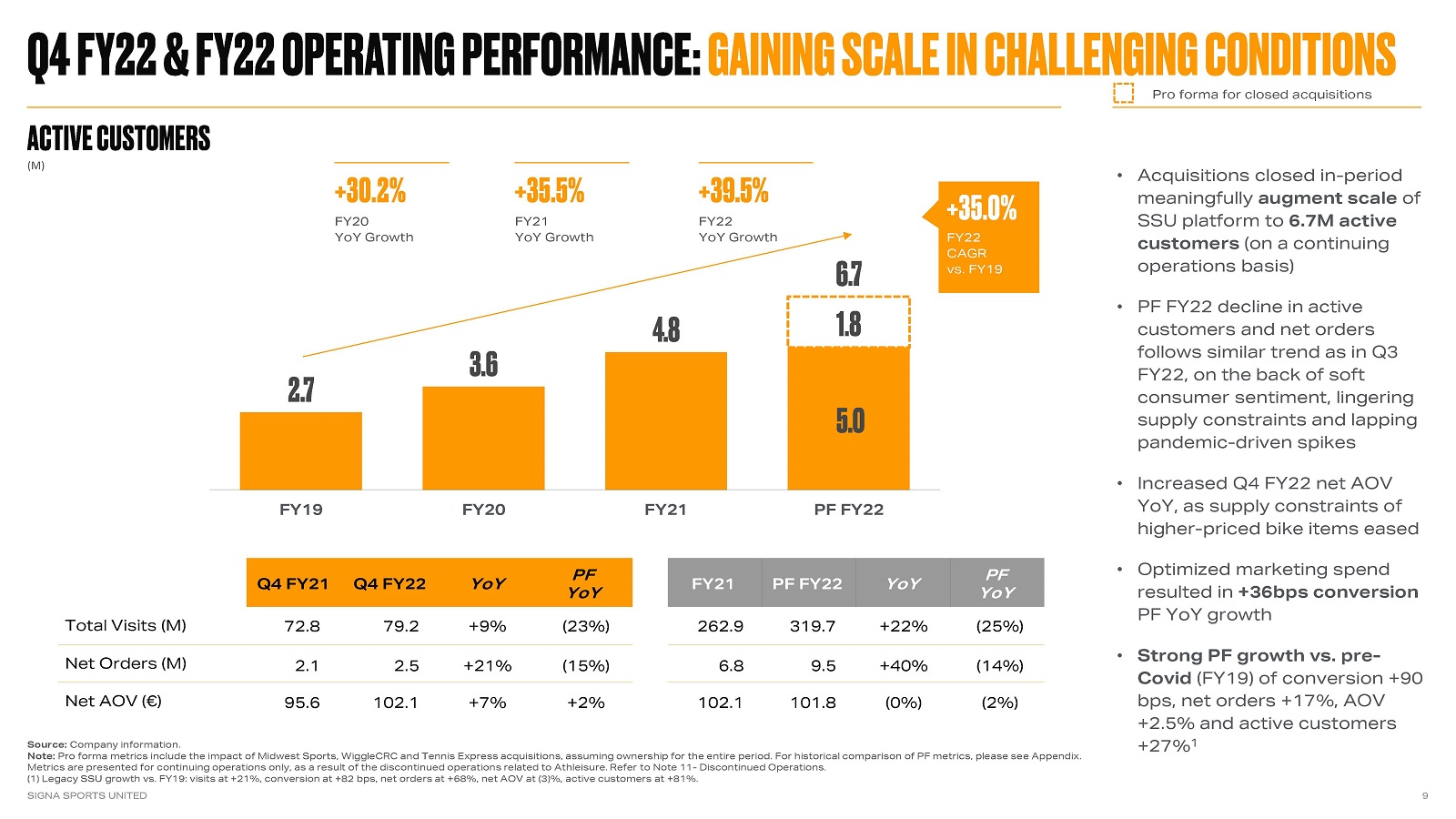

Q4 FY22 & FY22 OPERATING PERFORMANCE: gaining scale in challenging conditions SIGNA SPORTS UNITED 9 ACTIVE CUSTOMERS (M) Source: Company information. Note: Pro forma metrics include the impact of Midwest Sports, WiggleCRC and Tennis Express acquisitions, assuming ownership for the entire period. For historical comparison of PF metrics, please see Appendix. Metrics are presented for continuing operations only, as a result of the discontinued operations related to Athleisure. Refer to Note 11- Discontinued Operations. (1) Legacy SSU growth vs. FY19: visits at +21%, conversion at +82 bps, net orders at +68%, net AOV at (3)%, active customers at +81%. Q4 FY21 Q4 FY22 YoY PF YoY Total Visits (M) Net Orders (M) Net AOV (€) 72.8 79.2 +9% (23%) 2.1 2.5 +21% (15%) 95.6 102.1 +7% +2% Pro forma for closed acquisitions FY21 PF FY22 YoY PF YoY 262.9 319.7 +22% (25%) 6.8 9.5 +40% (14%) 102.1 101.8 (0%) (2%) FY22YoY Growth +39.5% FY21YoY Growth +35.5% FY20YoY Growth +30.2% FY22CAGR vs. FY19 +35.0% Acquisitions closed in-period meaningfully augment scale of SSU platform to 6.7M active customers (on a continuing operations basis) PF FY22 decline in active customers and net orders follows similar trend as in Q3 FY22, on the back of soft consumer sentiment, lingering supply constraints and lapping pandemic-driven spikes Increased Q4 FY22 net AOV YoY, as supply constraints of higher-priced bike items eased Optimized marketing spend resulted in +36bps conversion PF YoY growth Strong PF growth vs. pre-Covid (FY19) of conversion +90 bps, net orders +17%, AOV +2.5% and active customers +27%1

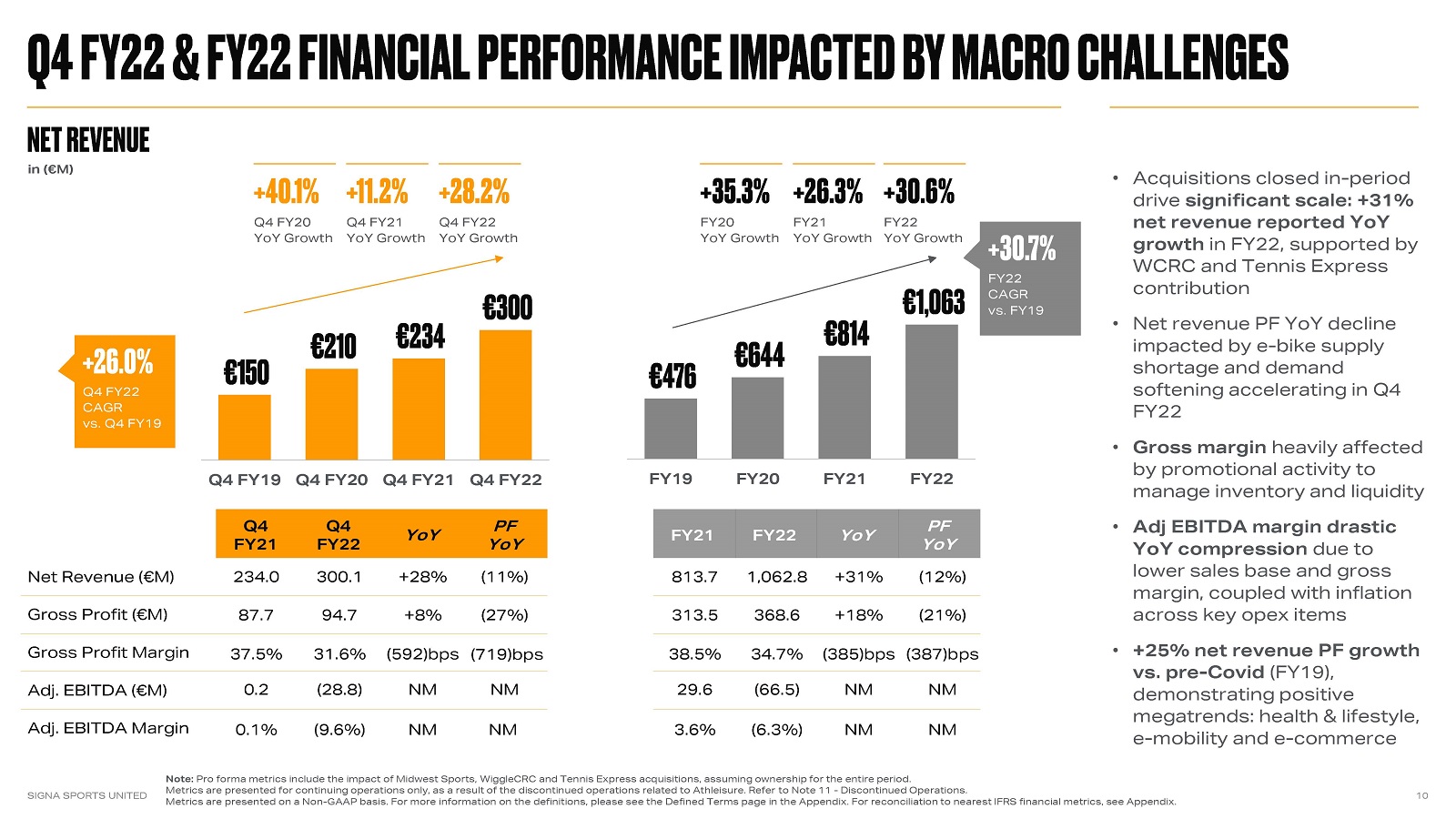

FY21 FY22 YoY PF YoY Q4 FY22 & FY22 financial PERFORMANCE impacted by macro challenges SIGNA SPORTS UNITED 10 NET REVENUE Note: Pro forma metrics include the impact of Midwest Sports, WiggleCRC and Tennis Express acquisitions, assuming ownership for the entire period. Metrics are presented for continuing operations only, as a result of the discontinued operations related to Athleisure. Refer to Note 11 - Discontinued Operations. Metrics are presented on a Non-GAAP basis. For more information on the definitions, please see the Defined Terms page in the Appendix. For reconciliation to nearest IFRS financial metrics, see Appendix. ` Q4 FY21 Q4 FY22 YoY PF YoY Net Revenue (€M) Gross Profit (€M) Gross Profit Margin Adj. EBITDA (€M) Adj. EBITDA Margin Q4 FY21YoY Growth +11.2% Q4 FY22YoY Growth +28.2% 234.0 300.1 +28% (11%) 87.7 94.7 +8% (27%) 37.5% 31.6% (592)bps (719)bps 0.2 (28.8) NM NM 0.1% (9.6%) NM NM 813.7 1,062.8 +31% (12%) 313.5 368.6 +18% (21%) 38.5% 34.7% (385)bps (387)bps 29.6 (66.5) NM NM 3.6% (6.3%) NM NM FY21YoY Growth +26.3% FY22YoY Growth +30.6% Q4 FY20YoY Growth +40.1% FY20YoY Growth +35.3% Q4 FY22CAGR vs. Q4 FY19 +26.0% FY22CAGR vs. FY19 +30.7% Acquisitions closed in-period drive significant scale: +31% net revenue reported YoY growth in FY22, supported by WCRC and Tennis Express contribution Net revenue PF YoY decline impacted by e-bike supply shortage and demand softening accelerating in Q4 FY22 Gross margin heavily affected by promotional activity to manage inventory and liquidity Adj EBITDA margin drastic YoY compression due to lower sales base and gross margin, coupled with inflation across key opex items +25% net revenue PF growth vs. pre-Covid (FY19), demonstrating positive megatrends: health & lifestyle, e-mobility and e-commerce in (€M)

Operating Cost overview SIGNA SPORTS UNITED ADJUSTED EBITDA MARGIN BRIDGE 11 Note: Metrics are presented for continuing operations only, as a result of the discontinued operations related to Athleisure. Refer to Note 11- Discontinued Operations. Metrics are presented on a Non-GAAP basis. (1) For more information on the definitions, please see the Defined Terms page in the Appendix. For reconciliation to nearest IFRS financial metrics, see Appendix. FY21% OF NET SALES FY22% OF NET SALES CHANGE (bps) COMMENTS Gross Margin 38.5% 34.7% (385) Low-mid end of assortment: competitive and overstocked High end of assortment: persistent supply chain challenges Personnel (10.2%) (12.7%) (250) Lower revenue base and strategic new hires Wage inflation Logistics (10.0%) (11.5%) (151) Cost inflation, higher returns (product mix) Increased split orders during logistics consolidation Marketing (7.7%) (8.4%) (69) Increase in paid marketing to offset drop in organic traffic IT / Other (7.1%) (8.4%) (134) Lower revenue base and investing in re-platforming Public company costs Adj. EBITDA(1) 3.6% (6.3%) (989)

Free cash flow impacted by operating conditions SIGNA SPORTS UNITED 12 Note: Metrics are presented for continuing operations only, as a result of the discontinued operations related to Athleisure. Refer to Note 11- Discontinued Operations. Metrics are presented on a Non-GAAP basis. Cash flow from Continuing Operating Activities includes (€1.9M) of Effect of exchange rate changes on cash and cash equivalents. Top line growth and Adj EBITDA profitability of (€66.5M) weakened significantly, in line with deteriorating market conditions over the course of FY22 Significant inventory build-up of (€40.4M) due to softening demand Reported change in TWC of (€4.7M) impacted by 9-month contribution of acquisitions; working capital development less favorable on a full-year pro forma basis Elevated €45.5M Capex associated with: Logistics consolidation Technology projects to re-platform acquired assets Significant cash outflows related to listing and WCRC acquisition Cash flow from Continuing Financing Activities mainly associated with funding commitments Strong PF liquidity position as of FY22 CASH FLOW BRIDGE in (€M)

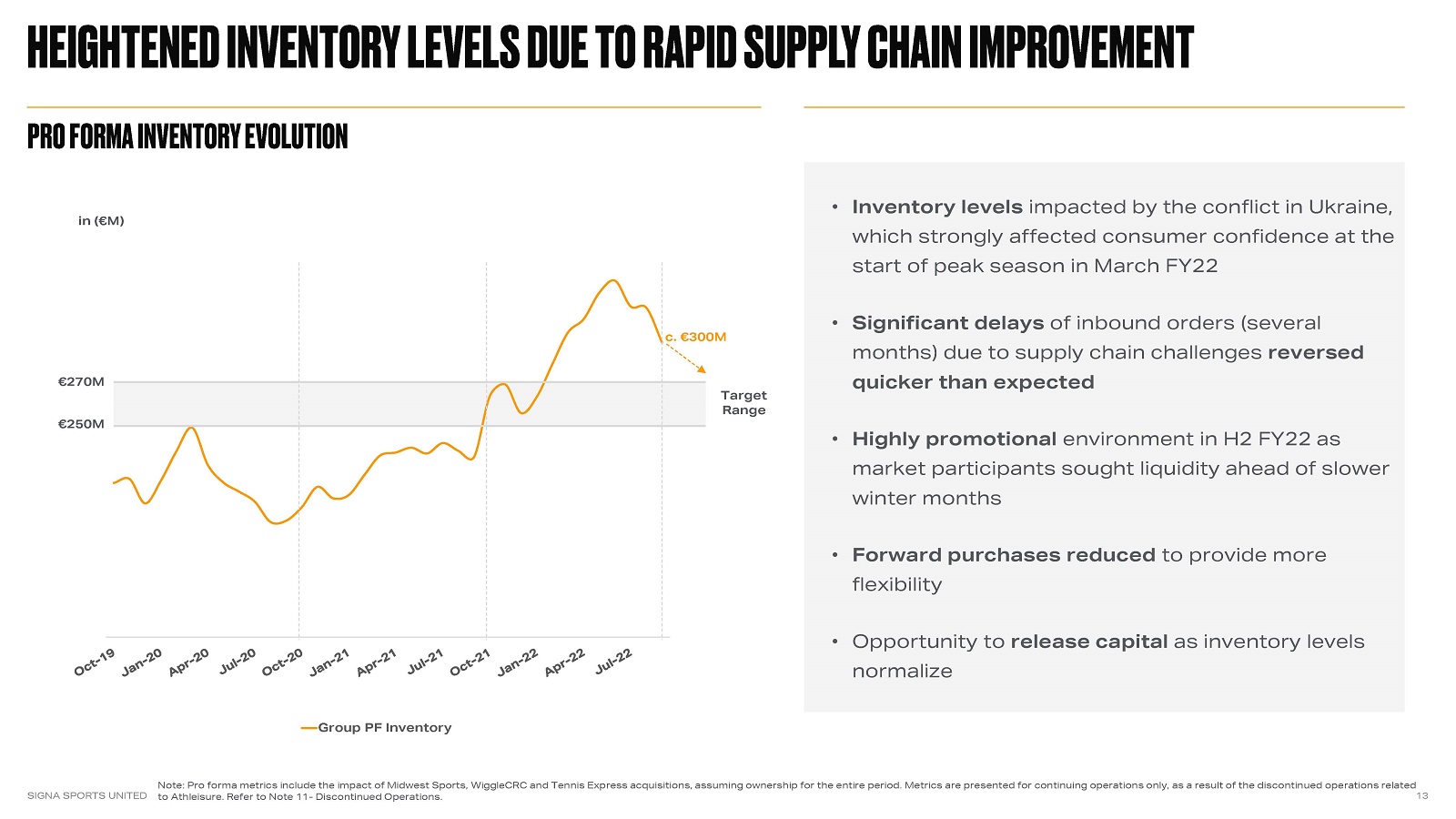

Inventory levels impacted by the conflict in Ukraine, which strongly affected consumer confidence at the start of peak season in March FY22 Significant delays of inbound orders (several months) due to supply chain challenges reversed quicker than expected Highly promotional environment in H2 FY22 as market participants sought liquidity ahead of slower winter months Forward purchases reduced to provide more flexibility Opportunity to release capital as inventory levels normalize Heightened inventory levels due to rapid supply chain improvement SIGNA SPORTS UNITED 13 Note: Pro forma metrics include the impact of Midwest Sports, WiggleCRC and Tennis Express acquisitions, assuming ownership for the entire period. Metrics are presented for continuing operations only, as a result of the discontinued operations related to Athleisure. Refer to Note 11- Discontinued Operations. (4.1)% in (€M) €270M €250M Target Range PRO FORMA INVENTORY EVOLUTION c. €300M

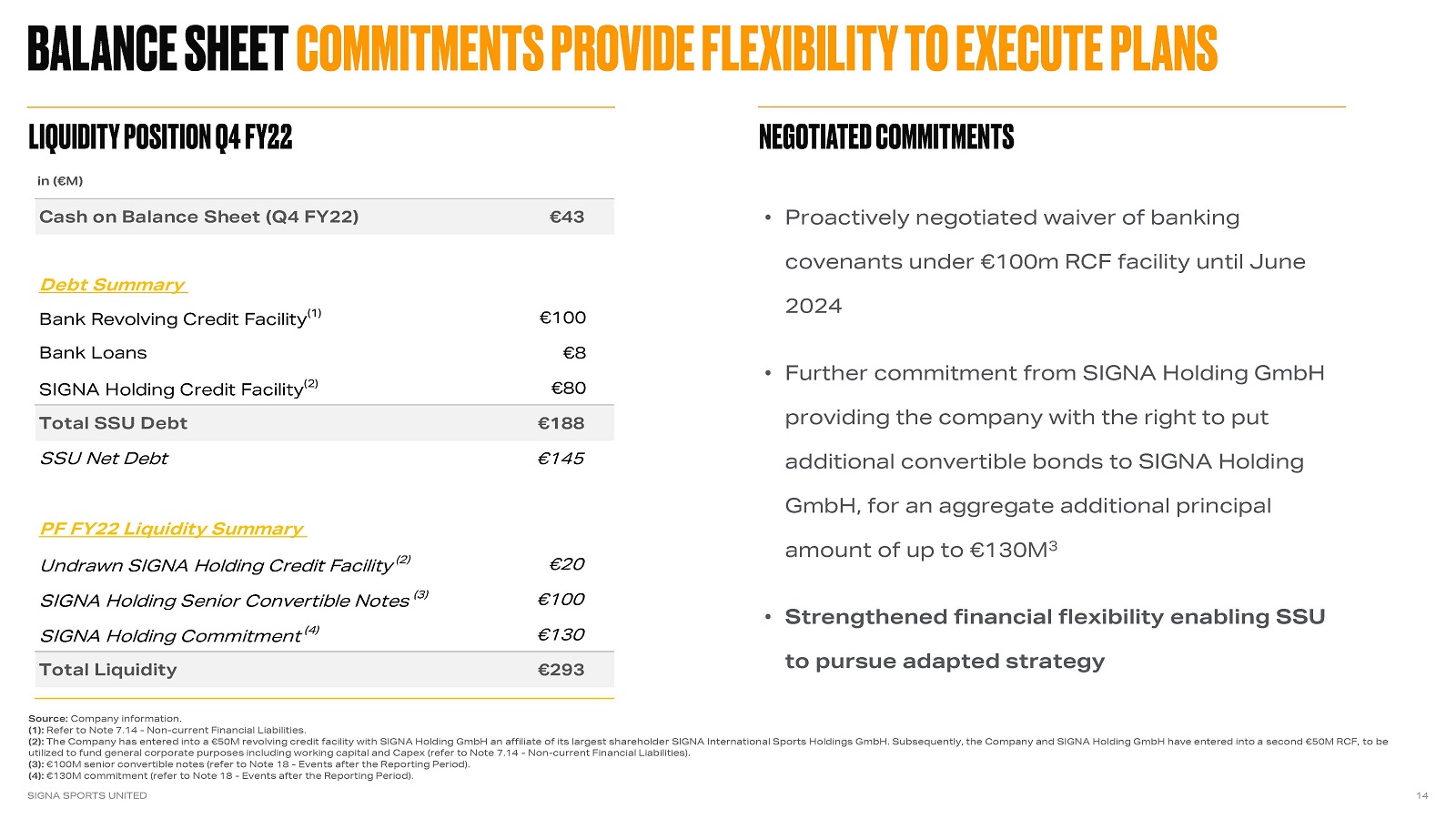

balance sheet commitments provide flexibility to execute plans SIGNA SPORTS UNITED 14 Source: Company information. (1): Refer to Note 7.14 - Non-current Financial Liabilities. (2): The Company has entered into a €50M revolving credit facility with SIGNA Holding GmbH an affiliate of its largest shareholder SIGNA International Sports Holdings GmbH. Subsequently, the Company and SIGNA Holding GmbH have entered into a second €50M RCF, to be utilized to fund general corporate purposes including working capital and Capex (refer to Note 7.14 - Non-current Financial Liabilities). (3): €100M senior convertible notes (refer to Note 18 - Events after the Reporting Period). (4): €130M commitment (refer to Note 18 - Events after the Reporting Period). Proactively negotiated waiver of banking covenants under €100m RCF facility until June 2024 Further commitment from SIGNA Holding GmbH providing the company with the right to put additional convertible bonds to SIGNA Holding GmbH, for an aggregate additional principal amount of up to €130M3 Strengthened financial flexibility enabling SSU to pursue adapted strategy LIQUIDITY POSITION Q4 FY22 NEGOTIATED COMMITMENTS in (€M)

01. Financial update 02. commercial change 03. Outlook APPENDIX Commercial change

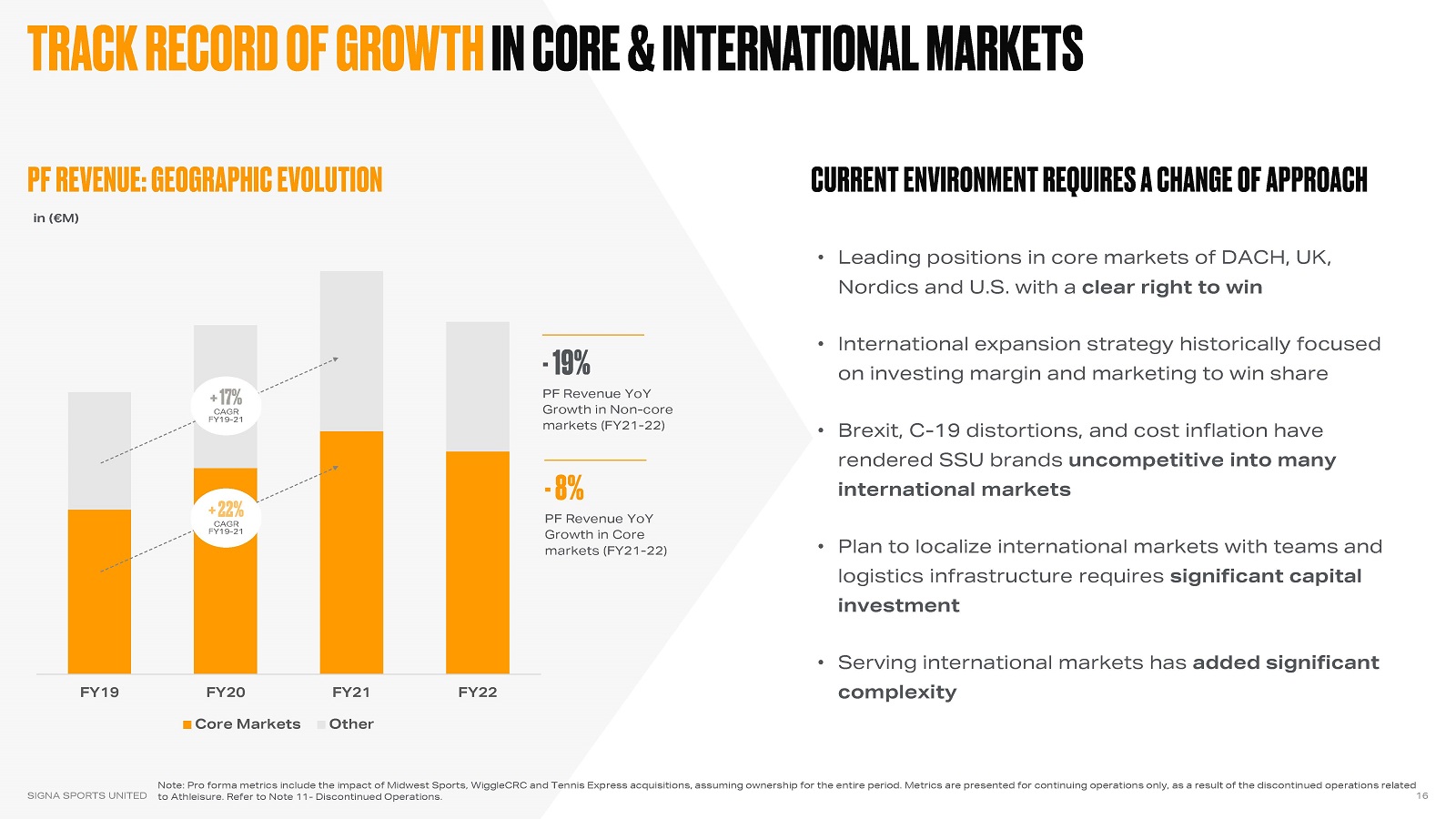

Track record of growth in core & international markets 16 PF Revenue: geographic Evolution Note: Pro forma metrics include the impact of Midwest Sports, WiggleCRC and Tennis Express acquisitions, assuming ownership for the entire period. Metrics are presented for continuing operations only, as a result of the discontinued operations related to Athleisure. Refer to Note 11- Discontinued Operations. Current Environment Requires a Change of Approach Leading positions in core markets of DACH, UK, Nordics and U.S. with a clear right to win International expansion strategy historically focused on investing margin and marketing to win share Brexit, C-19 distortions, and cost inflation have rendered SSU brands uncompetitive into many international markets Plan to localize international markets with teams and logistics infrastructure requires significant capital investment Serving international markets has added significant complexity in (€M) SIGNA SPORTS UNITED PF Revenue YoY Growth in Core markets (FY21-22) - 8% PF Revenue YoY Growth in Non-core markets (FY21-22) - 19% + 22%CAGR FY19-21 + 17%CAGR FY19-21

SIGNA SPORTS UNITED 17 focused plan to return the business to run rate profitability* in FY24 (1/2) * On an Adj. EBITDA basis for FY24 Deliver transaction synergies 03 Adapt commercial and operating models 02 Focus on core markets 01

SIGNA SPORTS UNITED 18 focused plan to return the business to run rate profitability* in FY24 (2/2) Focus area Alter positioning outside of core markets Optimize pricing and service levels for contribution Refocus international partnerships Scale back international partnerships Pause international logistics expansion Efficient stock management Improve order economics Optimize cost base Reduce complexity with common operating procedures impact Revenue synergy e.g. cross-sell own brands Cost synergies in procurement Efficiency from consolidating logistics footprint and technology Increased revenue Increased gross margin Reduced personnel costs Reduced logistics costs Reduced technology costs 01 Focus on core markets 02 Adapt commercial and operating models 03 Deliver transaction synergies Increased gross margin Reduction in working capital Increased stock turn Reduced marketing costs Reduced logistics costs Reduced overhead costs * On an Adj. EBITDA basis for FY24 Lower revenues Increased gross margin Reduced marketing costs Reduced overhead costs Reduced capex

SIGNA SPORTS UNITED 19 Impact of Changes to Operating Approach in Fy23 Focus on core markets and changes in the commercial model to result in lower sales, particularly in international markets, but sales to be at a higher contribution Significant gross margin contraction expected through H1 FY23 to reach target inventory levels, especially in overstocked categories at the lower end of the bike market; gross margins to start to recover from H2 FY23 Focus on lean operating processes to result in accelerating cost benefits from FY24 Transaction synergies to start to accrue from FY24 as IT re-platforming, logistics consolidation, and procurement benefits kick in Focus on reducing inventory levels expected to release €30-40M of capital in FY23 Capex expected to be €35-40M in FY23, as various IT and logistics projects are completed Waiver and capital commitments ensure financial flexibility to execute strategic realignment

outlook 01. Financial Update 02. commercial change 03. Outlook APPENDIX

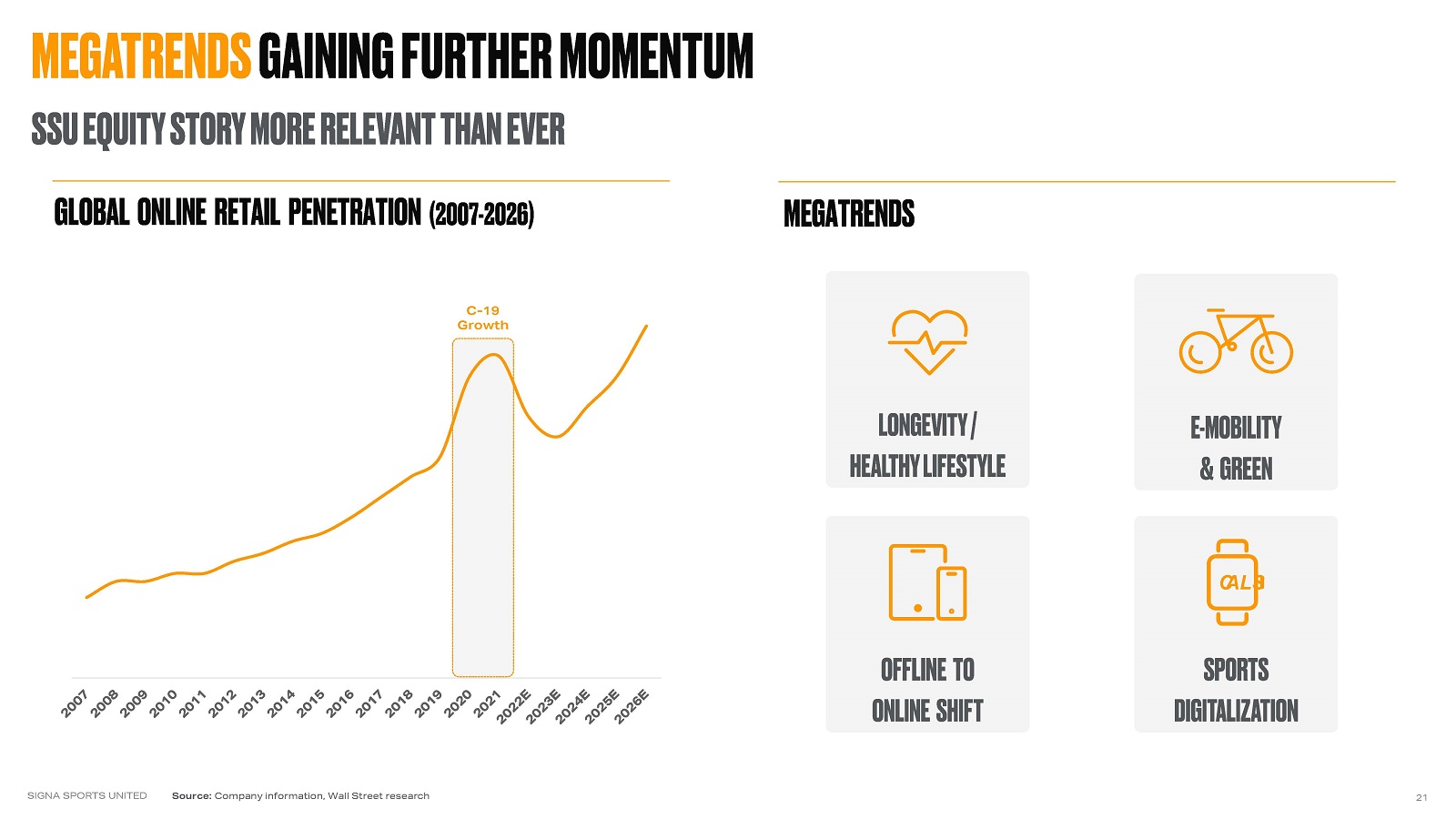

C-19 Growth SIGNA SPORTS UNITED 21 Source: Company information, Wall Street research MEGATRENDS GLOBAL ONLINE RETAIL PENETRATION (2007-2026) SSU Equity Story MORE RELEVANT THAN EVER LONGEVITY / HEALTHY LIFESTYLE E-MOBILITY & GREEN OFFLINE TO ONLINE SHIFT SPORTS DIGITALIZATION MEGATRENDS GAINING FURTHER MOMENTUM

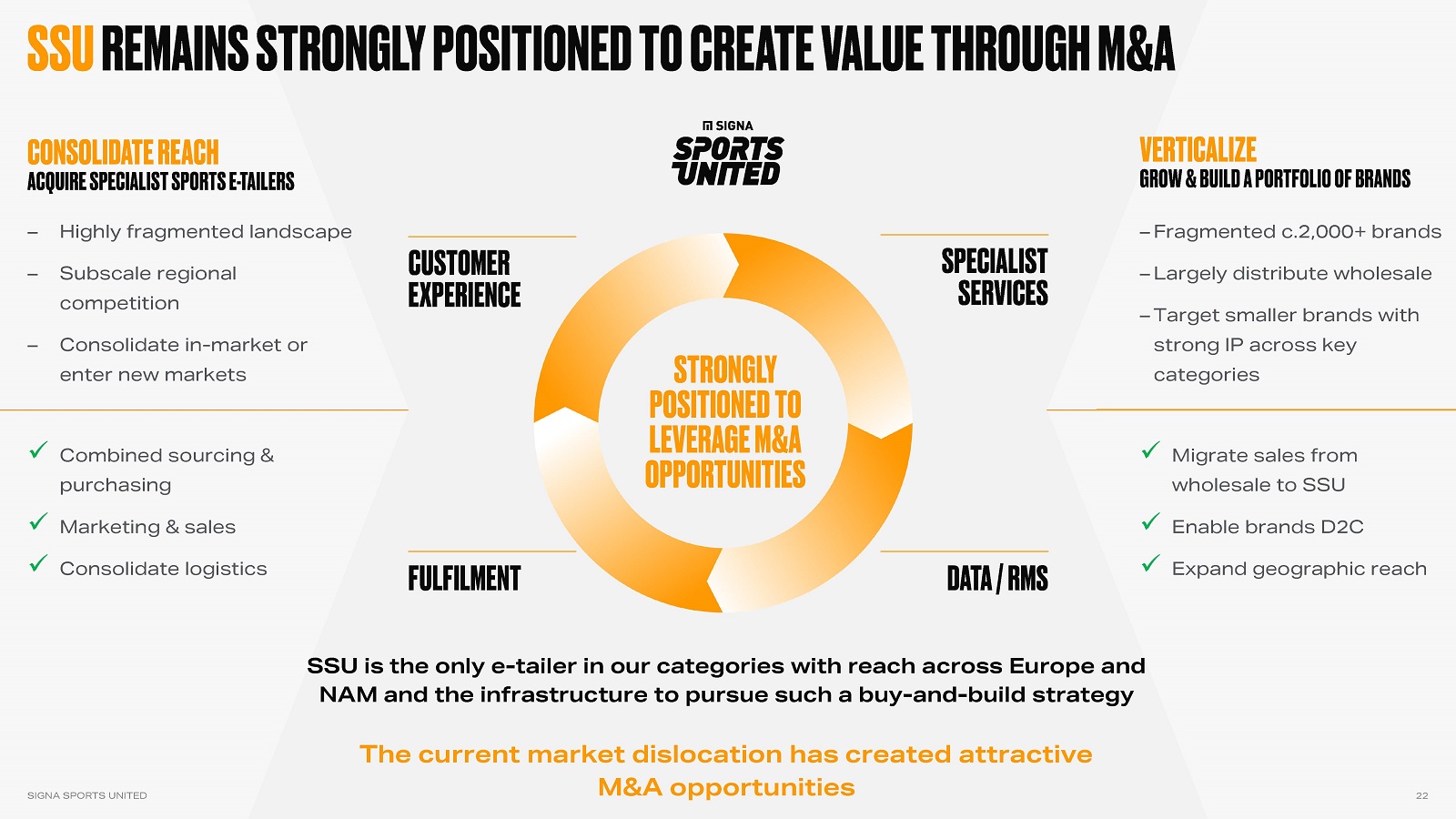

SIGNA SPORTS UNITED 22 CUSTOMEREXPERIENCE FULFILMENT SPECIALISTSERVICES Data / RMS SSU is the only e-tailer in our categories with reach across Europe and NAM and the infrastructure to pursue such a buy-and-build strategy The current market dislocation has created attractive M&A opportunities Highly fragmented landscape Subscale regional competition Consolidate in-market or enter new markets Fragmented c.2,000+ brands Largely distribute wholesale Target smaller brands with strong IP across key categories Combined sourcing & purchasing Marketing & sales Consolidate logistics Migrate sales from wholesale to SSU Enable brands D2C Expand geographic reach Strongly positioned to Leverage M&A Opportunities Consolidate reach Acquire specialist Sports e-Tailers Verticalize Grow & build a portfolio of brands SSU remains Strongly POSITIONED TO CREATE VALUE through M&A

Near-term challenges accelerate long-term opportunity SIGNA SPORTS UNITED 23 Intact structural megatrends behind online specialist sports retail Market dislocation is accelerating industry consolidation Strategic realignment to increase SSU’s competitiveness for sustainable and profitable growth Targeted investments across logistics and IT to enable long-term cost structure Accelerate M&A activities to take advantage of attractive buying opportunities

APPENDIX 01. Financial Update 02. Commercial change 03. Outlook APPENDIX

SSU commitment to sustainability SIGNA SPORTS UNITED 25 Note: (1) SIGNA Sports United ESG report available on https://investor.signa-sportsunited.com/esg/ FY22: defining SSU’s sustainability guidelines 1st SSU ESG report released in FY22 Understand and contain carbon footprint Improve sustainable product lifecycle Encourage recycling Increase diversity across the organisation Foster an environment in which employees develop best Promoting fair play for our people and the planet, by encouraging a sustainable and active lifestyle Conduct company-wide ESG Materiality Assessment Further define ESG strategy Identify concrete levers and set action plan and goals for all businesses Target: 2nd ESG report to be published in 2023 Climate neutral company for 3rd consecutive year FY23: Turning our vision into action

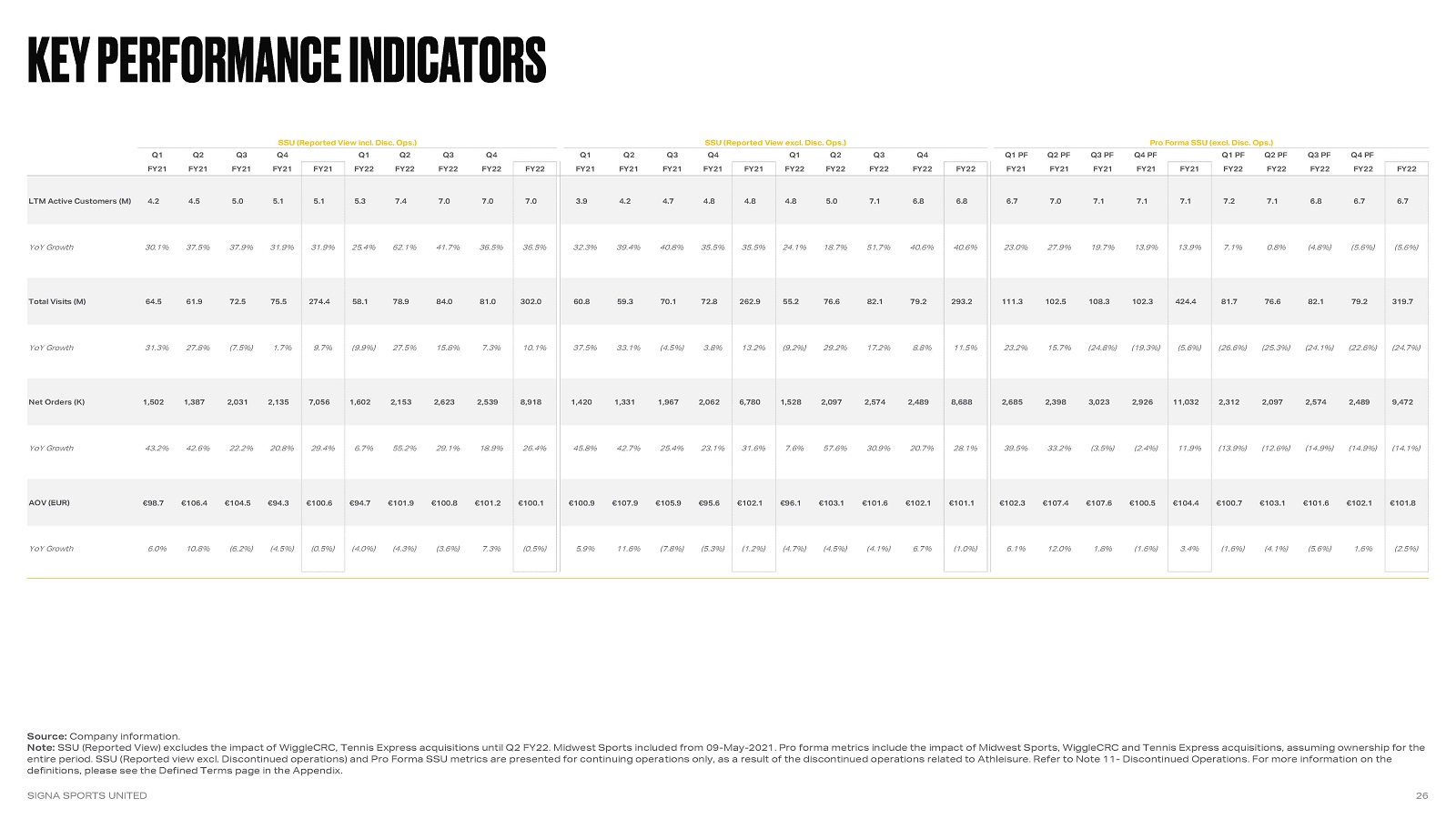

Key performance indicators SIGNA SPORTS UNITED 26 Source: Company information. Note: SSU (Reported View) excludes the impact of WiggleCRC, Tennis Express acquisitions until Q2 FY22. Midwest Sports included from 09-May-2021. Pro forma metrics include the impact of Midwest Sports, WiggleCRC and Tennis Express acquisitions, assuming ownership for the entire period. SSU (Reported view excl. Discontinued operations) and Pro Forma SSU metrics are presented for continuing operations only, as a result of the discontinued operations related to Athleisure. Refer to Note 11- Discontinued Operations. For more information on the definitions, please see the Defined Terms page in the Appendix.

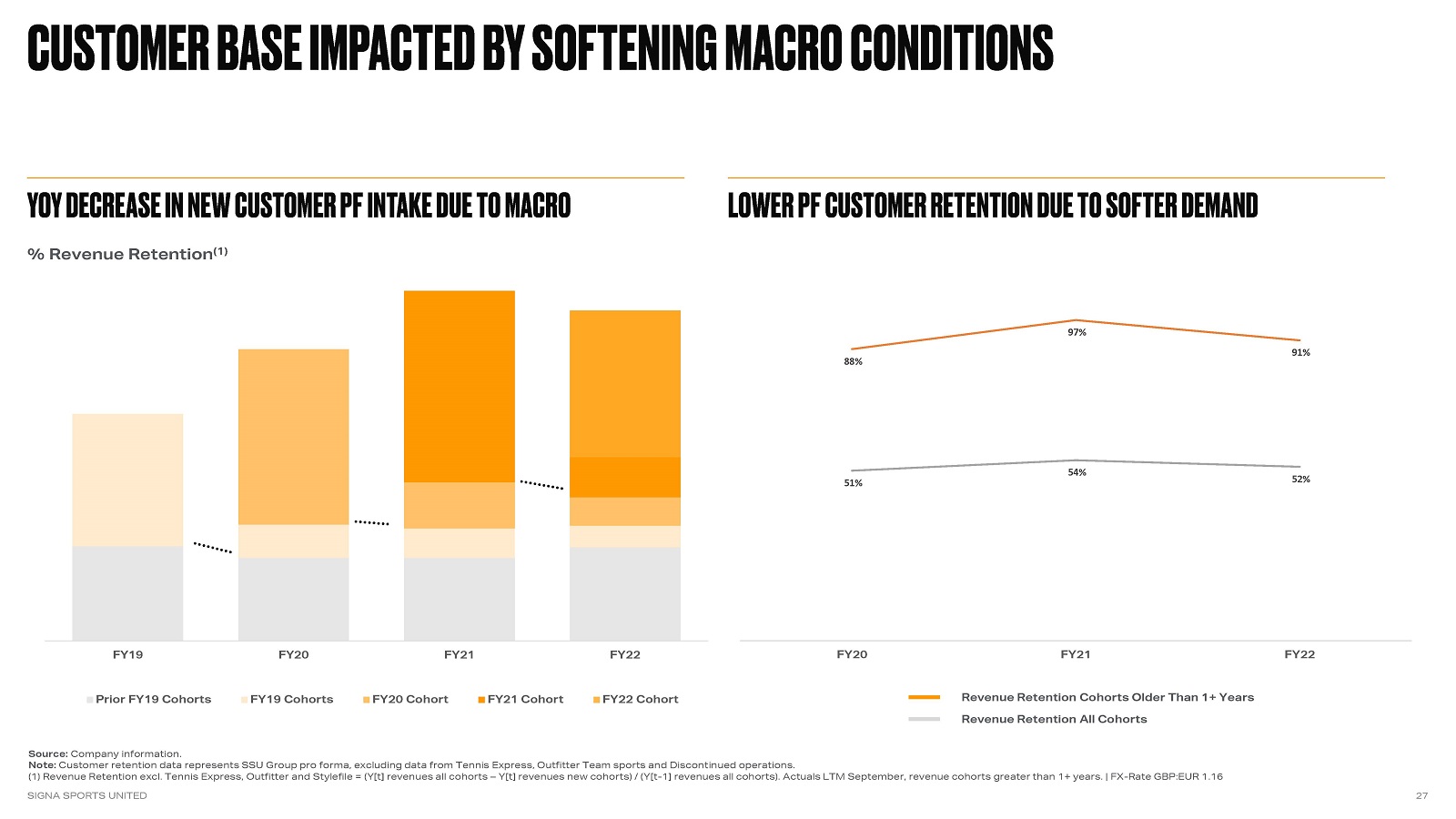

customer base impacted by softening macro conditions SIGNA SPORTS UNITED 27 Source: Company information. Note: Customer retention data represents SSU Group pro forma, excluding data from Tennis Express, Outfitter Team sports and Discontinued operations.(1) Revenue Retention excl. Tennis Express, Outfitter and Stylefile = (Y[t] revenues all cohorts – Y[t] revenues new cohorts) / (Y[t-1] revenues all cohorts). Actuals LTM September, revenue cohorts greater than 1+ years. | FX-Rate GBP:EUR 1.16 Yoy Decrease in NEW CUSTOMER PF INTAKE due to macro % Revenue Retention(1) Lower PF CUSTOMER RETENTION due to softer demand Revenue Retention Cohorts Older Than 1+ Years Revenue Retention All Cohorts

Reconciliation of Reported P&L at current scope SIGNA SPORTS UNITED 28 Source: Company information. Note: Discontinued operations related to Athleisure. Refer to Note 11- Discontinued Operations. For more information on the definitions, please see the Defined Terms page in the Appendix. Metrics are presented on a Non-GAAP basis. in (€M)

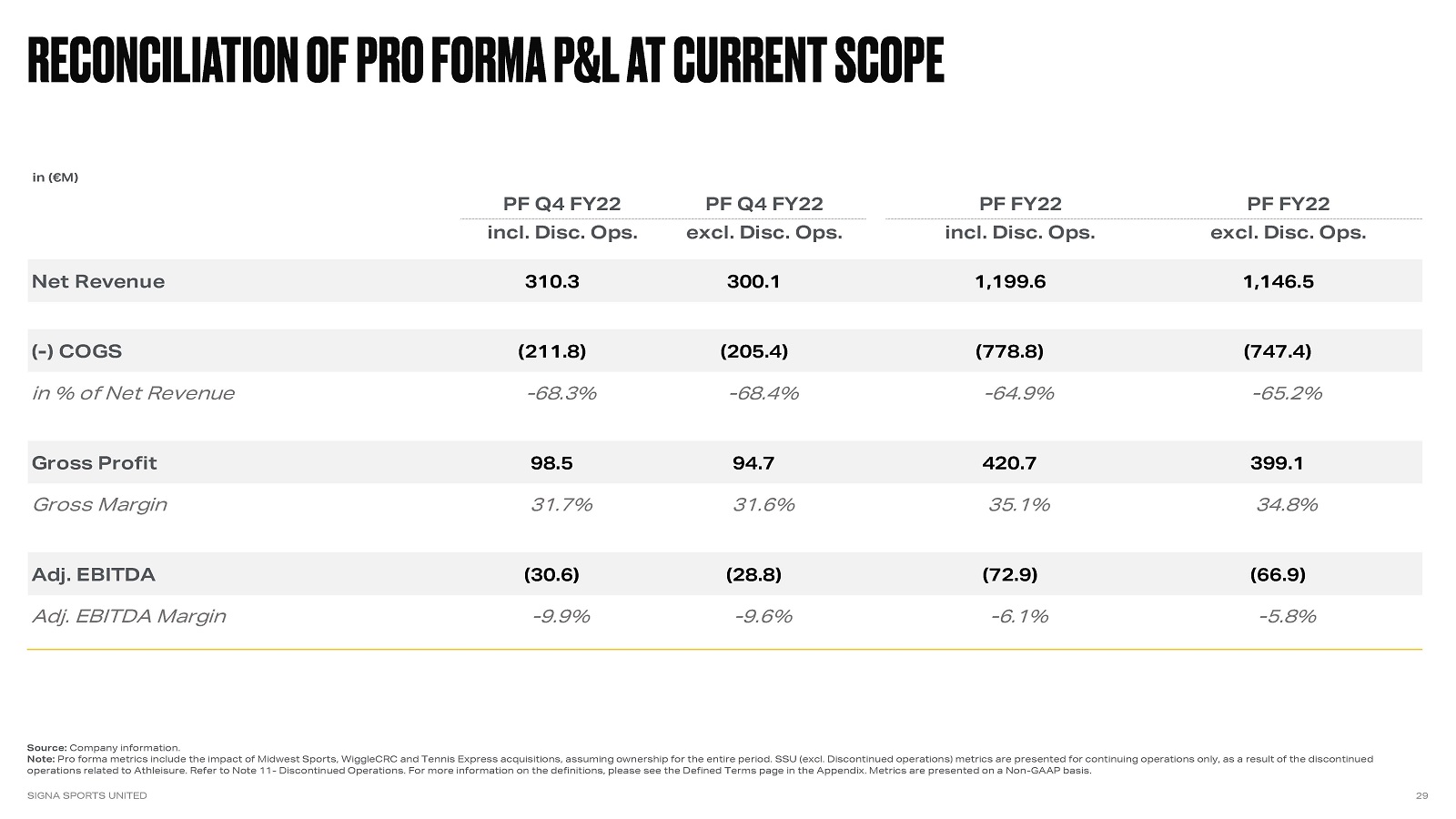

Reconciliation of pro forma P&L at current scope SIGNA SPORTS UNITED 29 Source: Company information. Note: Pro forma metrics include the impact of Midwest Sports, WiggleCRC and Tennis Express acquisitions, assuming ownership for the entire period. SSU (excl. Discontinued operations) metrics are presented for continuing operations only, as a result of the discontinued operations related to Athleisure. Refer to Note 11- Discontinued Operations. For more information on the definitions, please see the Defined Terms page in the Appendix. Metrics are presented on a Non-GAAP basis. in (€M)

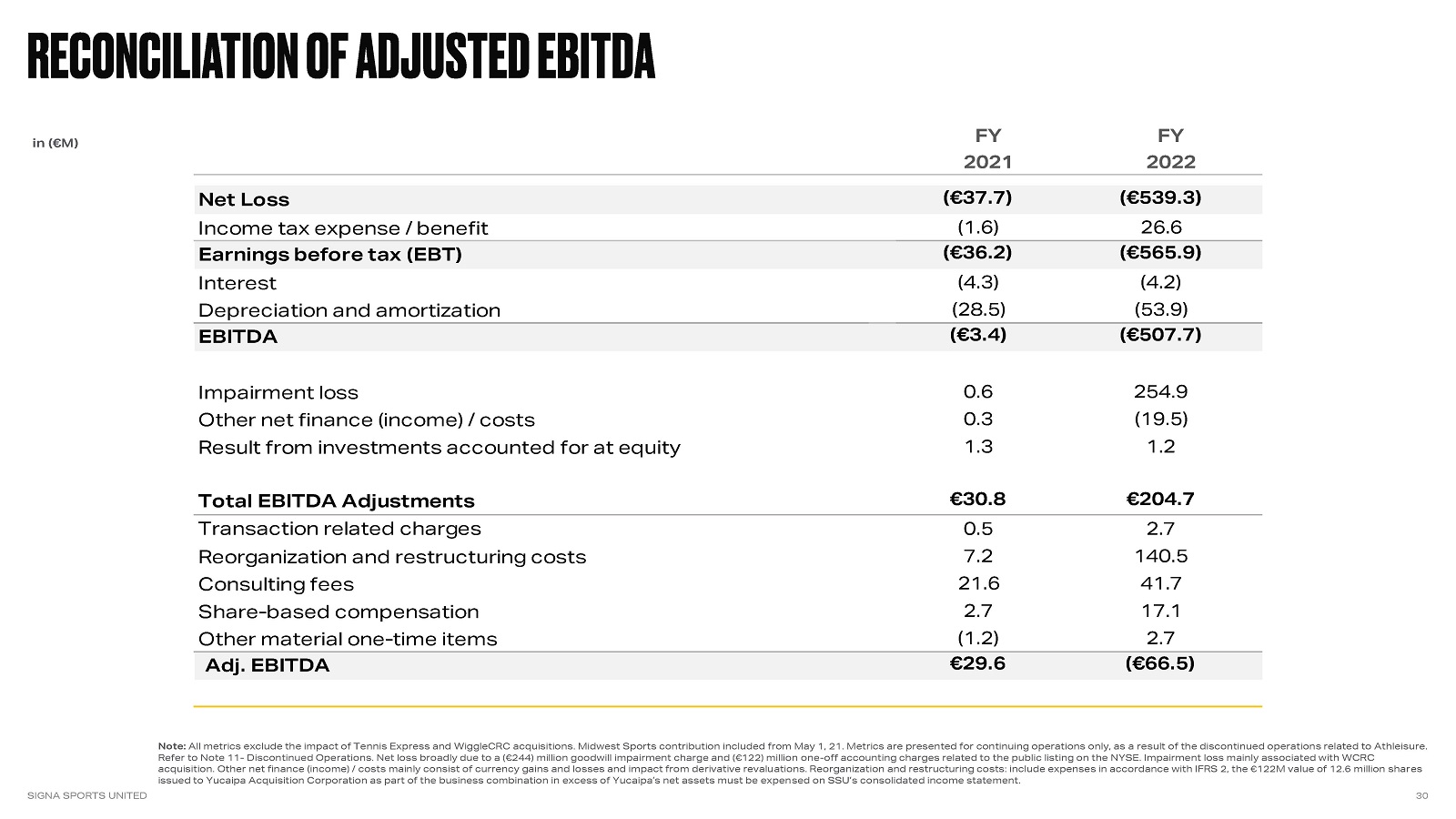

Reconciliation of Adjusted EBITDA SIGNA SPORTS UNITED 30 Note: All metrics exclude the impact of Tennis Express and WiggleCRC acquisitions. Midwest Sports contribution included from May 1, 21. Metrics are presented for continuing operations only, as a result of the discontinued operations related to Athleisure. Refer to Note 11- Discontinued Operations. Net loss broadly due to a (€244) million goodwill impairment charge and (€122) million one-off accounting charges related to the public listing on the NYSE. Impairment loss mainly associated with WCRC acquisition. Other net finance (income) / costs mainly consist of currency gains and losses and impact from derivative revaluations. Reorganization and restructuring costs: include expenses in accordance with IFRS 2, the €122M value of 12.6 million shares issued to Yucaipa Acquisition Corporation as part of the business combination in excess of Yucaipa’s net assets must be expensed on SSU’s consolidated income statement. in (€M)

SSU FINANCIAL POSITION AS OF FY22 SIGNA SPORTS UNITED 31 CAP TABLE(1) Source: Company information. Note: For further information on terms of warrants, see SEC F-1 filing as of Dec 23, 2021. (1): Excludes 51.0M earnout shares issuable to SISH upon meeting certain share price targets. Earnout shares are split into six equal tranches of 8.5M shares issuable at SSU common stock share prices of $12.50, $15.00, $17.50, $20.00, $22.50, and $25.00. Excludes 14.6M Ordinary Shares underlying the €100M convertible bonds that may be deemed to be beneficially held by SIGNA European Invest Holding AG (see 20-F filing as of Feb 7, 2023). (2): Refer to Note 7.14 - Non-current Financial Liabilities. (3): The Company has entered into a €50M revolving credit facility with SIGNA Holding GmbH an affiliate of its largest shareholder SIGNA International Sports Holdings GmbH. Subsequently, the Company and SIGNA Holding GmbH have entered into a second €50M RCF, to be utilized to fund general corporate purposes including working capital and Capex (refer to Note 7.14 - Non-current Financial Liabilities). (4): €100M senior convertible notes (refer to Note 18 - Events after the Reporting Period). (5): €130M commitment (refer to Note 18 - Events after the Reporting Period). LIQUIDITY POSITION in (€M)

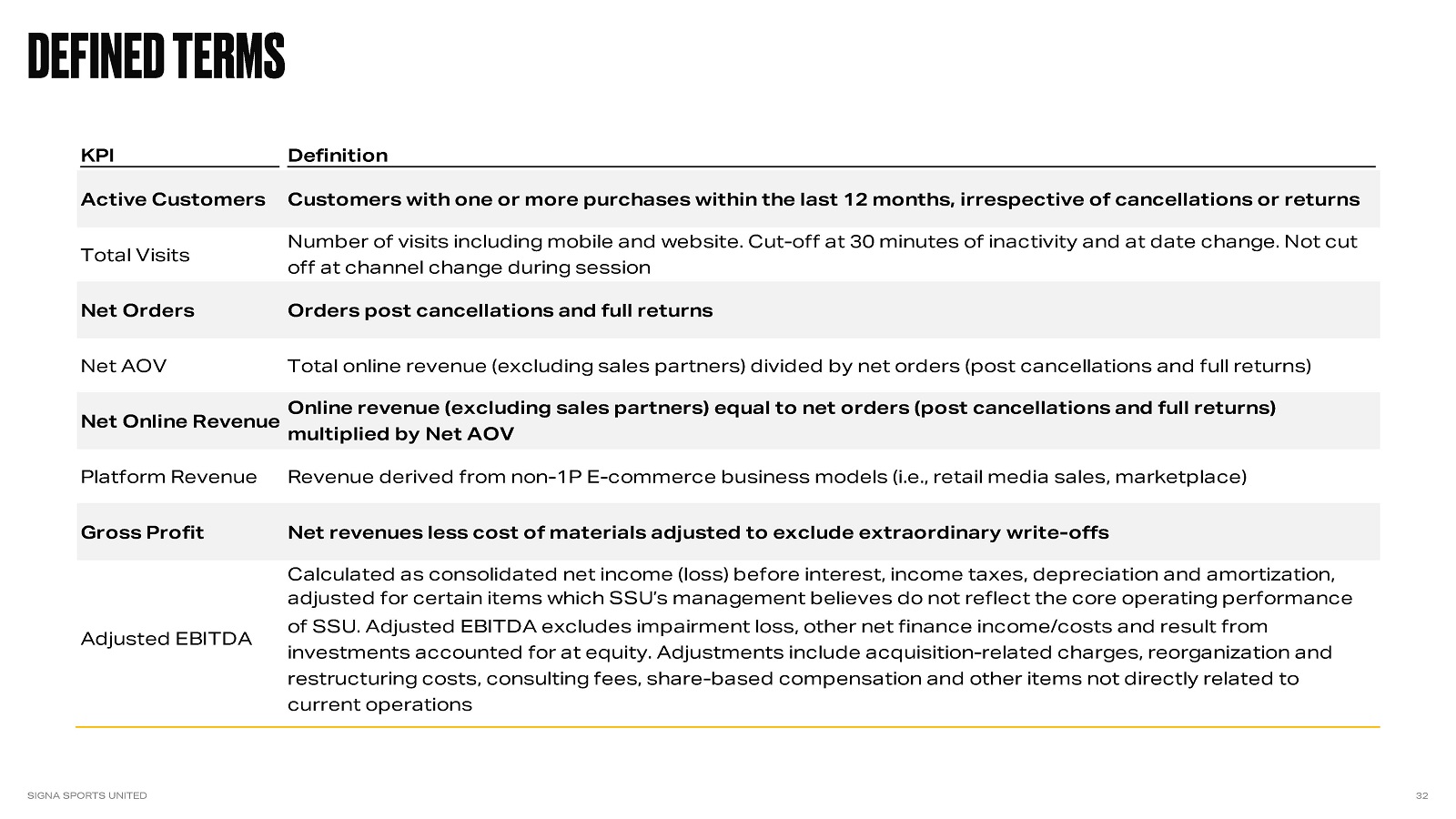

Defined Terms SIGNA SPORTS UNITED 32

THANK YOU SIGNA SPORTS UNITED 33 SSU Investor Relations https://investor.signa-sportsunited.com SSU Investors Contact Alima Levy a.levy@signa-sportsunited.com +49 174 7304938