Table of Contents

As filed with the Securities and Exchange Commission on November 10, 2022

Registration No. 333-260337

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 4

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

KinderCare Learning Companies, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 8351 | 87-1653366 | ||

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

5005 Meadows Road

Lake Oswego, OR 97035

(503) 872-1300

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Tom Wyatt

Chief Executive Officer

5005 Meadows Road

Lake Oswego, OR 97035

(503) 872-1300

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Ian D. Schuman, Esq. Stelios G. Saffos, Esq. R. Charles Cassidy III, Esq. Latham & Watkins LLP 1271 Avenue of the Americas New York, New York 10020 Telephone: (212) 906-1200 Fax: (212) 751-4864 | Joshua N. Korff, Esq. Michael Kim, Esq. Kirkland & Ellis LLP 601 Lexington Avenue New York, New York 10022 Telephone: (212) 446-4800 Fax: (212) 446-4900 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☒ | Smaller reporting company | ☐ | |||

| Emerging growth company | ☐ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion, dated , 2022

PROSPECTUS

Shares

KinderCare Learning Companies, Inc.

Common Stock

This is an initial public offering of shares of common stock of KinderCare Learning Companies, Inc. We are offering shares of our common stock.

Prior to this offering, there has been no public market for our common stock. The initial public offering price is expected to be between $ and $ per share. We have applied to list our common stock on the New York Stock Exchange under the symbol “KLC.”

The underwriters have an option for a period of 30 days after the date of this prospectus, to purchase from us from time to time, in whole or in part, up to an aggregate of shares of our common stock.

Following this offering, investment funds affiliated with or advised by affiliates of Partners Group Holding AG will continue to own a controlling interest in our common stock, owning % of our common stock. As a result, we expect to be a “controlled company” within the meaning of the corporate governance standards of the New York Stock Exchange.

We intend to use the net proceeds from this offering to (i) repay $ of our outstanding First Lien Notes, repay $ of the loans outstanding under our Second Lien Facility and then repay $ of the loans outstanding under our First Lien Term Loan Facility, (ii) redeem $ of the shares of common stock received by members of management from vested Class B Units of KC Parent, LLC in connection with the Reorganization and (iii) pay fees and expenses in connection with this offering. We intend to use the remainder, if any, of the net proceeds to us from this offering for general corporate purposes. See “Use of Proceeds.”

Investing in our common stock involves risk. See “Risk Factors” beginning on page 22 to read about factors you should consider before buying shares of our common stock.

| Price to Public | Underwriting Discounts(1) | Proceeds, before expenses | ||||||||||

Per Share | $ | $ | $ | |||||||||

Total | $ | $ | $ | |||||||||

| (1) | See “Underwriting (Conflicts of Interest)” for additional information regarding underwriting compensation. |

Neither the Securities and Exchange Commission (the “SEC”) nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

Delivery of the shares of our common stock will be made on or about , 2022.

| Barclays | Morgan Stanley | Jefferies | ||

(in alphabetical order) | ||||

| BofA Securities | Goldman Sachs & Co. LLC | Baird | ||

| Citigroup | Credit Suisse | Macquarie Capital | ||

| Loop Capital Markets | Ramirez & Co., Inc. | R. Seelaus & Co., LLC | ||

Prospectus dated , 2022

Table of Contents

KINDERCARE LEARNING COMPANIES TM Confidence for Life.

Table of Contents

| ii | ||||

| ii | ||||

| ii | ||||

| iii | ||||

| iv | ||||

| iv | ||||

| 1 | ||||

| 22 | ||||

| 47 | ||||

| 49 | ||||

| 51 | ||||

| 52 | ||||

| 54 | ||||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 57 | |||

| 84 | ||||

| 110 | ||||

| 116 | ||||

| 137 | ||||

| 140 | ||||

| 144 | ||||

| 150 | ||||

| 153 | ||||

MATERIAL U.S. FEDERAL INCOME TAX CONSEQUENCES FOR NON-U.S. HOLDERS OF OUR COMMON STOCK | 155 | |||

| 160 | ||||

| 161 | ||||

| 170 | ||||

| 170 | ||||

| 170 | ||||

| F-1 | ||||

i

Table of Contents

You should rely only on the information included elsewhere in this prospectus and any free writing prospectus prepared by or on behalf of us that we have referred to you. Neither we nor the underwriters have authorized anyone to provide you with additional information or information different from that included elsewhere in this prospectus or in any free writing prospectus prepared by or on behalf of us that we have referred to you. If anyone provides you with additional, different or inconsistent information, you should not rely on it. Offers to sell, and solicitations of offers to buy, shares of our common stock are being made only in jurisdictions where offers and sales are permitted.

No action is being taken in any jurisdiction outside the United States to permit a public offering of common stock or possession or distribution of this prospectus in that jurisdiction. Persons who come into possession of this prospectus in jurisdictions outside the United States are required to inform themselves about and to observe any restriction as to this offering and the distribution of this prospectus applicable to those jurisdictions.

This prospectus includes estimates regarding market and industry data that we prepared based on our management’s knowledge and experience in the markets in which we operate, together with information obtained from various sources, including publicly available information, industry reports and publications, surveys, our clients, suppliers, trade and business organizations and other contacts in the markets in which we operate. Management estimates are derived from publicly available information released by independent industry analysts and third-party sources, as well as data from our internal research, and are based on assumptions made by us upon reviewing such data and our knowledge of such industry and markets which we believe to be reasonable. In addition, certain of the sources were published before the novel coronavirus (“COVID-19”) pandemic and therefore do not reflect any impact of the COVID-19 pandemic.

In presenting this information, we have made certain assumptions that we believe to be reasonable based on such data and other similar sources and on our knowledge of, and our experience to date in, the markets for the products we distribute. Market share data is subject to change and may be limited by the availability of raw data, the voluntary nature of the data gathering process and other limitations inherent in any statistical survey of market share. In addition, client preferences are subject to change. Accordingly, you are cautioned not to place undue reliance on such market share data.

The Company reports on a 52- or 53-week fiscal year comprised of 13- or 14-week quarters, with the fiscal year ending on the Saturday closest to December 31. The fiscal years ended January 1, 2022 and December 28, 2019 are 52-week fiscal years with 13-week fourth quarters. The fiscal year ended January 2, 2021 is a 53-week fiscal year with a 14-week fourth quarter. References in this prospectus to “fiscal 2021” refer to the fiscal year ended January 1, 2022, “fiscal 2020” refer to the fiscal year ended January 2, 2021 and “fiscal 2019” refer to the fiscal year ended December 28, 2019.

As used in this prospectus, unless the context otherwise requires, references to:

| • | the “Company,” “KinderCare,” “we,” “us” and “our” mean KinderCare Learning Companies, Inc. and, unless the context otherwise requires, its consolidated subsidiaries; |

| • | “ARPA” means the American Rescue Plan Act; |

| • | “CAA” means the Consolidated Appropriations Act; |

| • | “CARES Act” means the Coronavirus Aid, Relief and Economic Security Act; |

| • | “Credit Agreements” means, collectively, the First Lien Credit Agreement and the Second Lien Credit Agreement; |

ii

Table of Contents

| • | “Credit Facilities” means, collectively, the First Lien Facilities and the Second Lien Facility; |

| • | “DGCL” means the Delaware General Corporation Law; |

| • | “Exchange Act” means the Securities Exchange Act of 1934, as amended; |

| • | “First Lien Credit Agreement” means that certain credit agreement, dated as of August 13, 2015 (as amended, restated, amended and restated, supplemented or modified from time to time), governing the First Lien Facilities, by and among KinderCare Learning Companies, Inc. (f/k/a KC Holdco, LLC), as Holdco, KC Sub, LLC and KUEHG Corp. (as successor to KC Mergersub, Inc.), as the Borrower, Credit Suisse AG, Cayman Islands Branch, as administrative agent and collateral agent and the other parties from time to time party thereto; |

| • | “First Lien Facilities” means collectively, the First Lien Revolving Facility and the First Lien Term Loan; |

| • | “First Lien Notes” means $50.0 million initial aggregate principal amount of first lien notes issued by KUEHG Corp. pursuant to the Notes Purchase Agreement; |

| • | “First Lien Revolving Facility” means the $140.0 million first lien revolving credit facility; |

| • | “First Lien Term Loan Facility” means the $1,200.0 million first lien term loan facility; |

| • | “GAAP” means U.S. generally accepted accounting principles; |

| • | “Governmental Stimulus” means incremental funding arising from governmental acts relating to the COVID-19 pandemic to support the ECE industry, including without limitation, the CARES Act, CAA and ARPA, which funding we expect to continue for the foreseeable future; |

| • | “Notes Purchase Agreement” means that certain First Lien Note Purchase Agreement, dated as of July 6, 2020, by and among KUEHG Corp., certain members of KC Parent, LLC and Wilmington Trust, National Association, as administrative agent and collateral agent; |

| • | “Parent” means, prior to the Reorganization, KC Parent, LLC; |

| • | “PG” means investment funds affiliated with or advised by affiliates of Partners Group Holding AG, which own a controlling interest in us; |

| • | “Second Lien Credit Agreement” means that certain credit agreement, dated as of August 22, 2017 (as amended, amended and restated, supplemented or modified time to time), governing the Second Lien Facility, by and among KinderCare Learning Companies, Inc. (f/k/a KC Holdco, LLC), as Holdco, KC Sub, LLC and KUEHG Corp. as the Borrower, Credit Suisse AG, Cayman Islands Branch, as administrative agent and collateral agent and the other parties from time to time party thereto; |

| • | “Second Lien Facility” means the $210.0 million second lien term loan facility; |

| • | “Securities Act” means the Securities Act of 1933, as amended; |

| • | “Services Agreement” means the services agreement, dated August 13, 2015, by and between KinderCare Education LLC and an advisory affiliate of PG, as amended; and |

| • | “Stockholders Agreement” means the stockholders agreement to be effective following the Reorganization and upon the consummation of this offering, by and among PG, certain other existing stockholders and KinderCare. |

Unless otherwise indicated, information in this prospectus concerning economic conditions, our industry, our markets and our competitive position is based on a variety of sources, including information from independent industry analysts and publications, as well as our own estimates and research. This information involves a number of assumptions and limitations, and you are cautioned not to give undue weight to such estimates.

iii

Table of Contents

This prospectus includes trademarks and service marks owned by us, including Champions, Early Foundations, KinderCare, KinderCare Education and Rainbow. This prospectus also contains trademarks, trade names and service marks of other companies, which are the property of their respective owners. Solely for convenience, trademarks, trade names and service marks referred to in this prospectus may appear without the ®, ™ or SM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the right of the applicable licensor to these trademarks, trade names and service marks. We do not intend our use or display of other parties’ trademarks, trade names or service marks to imply, and such use or display should not be construed to imply, a relationship with, or endorsement or sponsorship of us by, these other parties.

Certain financial measures presented in this prospectus are not recognized under GAAP. EBIT, EBITDA, Adjusted EBITDA, and Adjusted net income (loss) (collectively referred to as the “non-GAAP financial measures”) are not presentations made in accordance with GAAP, and should not be considered as an alternative to net income or loss, income or loss from operations, or any other performance measure in accordance with GAAP, or as an alternative to cash provided by operating activities as a measure of our liquidity. EBIT is defined as net income (loss) adjusted for net interest expense and income tax expense (benefit). EBITDA is defined as EBIT adjusted for depreciation and amortization. Adjusted EBITDA is defined as EBITDA adjusted for COVID-19 related costs, equity-based compensation, management and advisory fee expenses, acquisition-related costs and other costs because these charges do not relate to the core operations of our business. Adjusted net income (loss) is defined as net income (loss) before income tax adjusted for amortization of intangible assets, COVID-19 related costs, equity-based compensations, management and advisory fee expenses, acquisitions-related costs and other costs.

We present EBIT, EBITDA, Adjusted EBITDA and Adjusted net income (loss) because we consider them to be important supplemental measures of our performance and believe they are useful to securities analysts, investors and other interested parties. Specifically, Adjusted EBITDA and Adjusted net income (loss) allow for an assessment of our operating performance without the effect of charges that do not relate to the core operations of our business. We believe Adjusted EBITDA is helpful to investors in highlighting trends in our core operating performance compared to other measures, which can differ significantly depending on long-term strategic decisions regarding capital structure, the tax jurisdictions in which companies operate and capital investments.

We believe the use of Adjusted net income (loss) provides investors with consistency in the evaluation of the Company as it provides a meaningful comparison of past, present and future operating results, as well as a more useful financial comparison to our peers. We believe this supplemental measure can be used to assess the financial performance of our business without regard to certain costs that are not representative of our continuing operations.

EBIT, EBITDA, Adjusted EBITDA and Adjusted net income (loss) have limitations as analytical tools and should not be considered in isolation or as a substitute for analysis of our results as reported under GAAP. Some of these limitations are:

| • | they do not reflect the significant interest expense or the cash requirements necessary to service interest or principal payments on indebtedness; |

| • | they do not reflect income tax expense or the cash requirements for income tax liabilities; |

| • | although depreciation and amortization are non-cash charges, the assets being depreciated and amortized will have to be replaced in the future, and EBIT, EBITDA, Adjusted EBITDA and Adjusted net income (loss) do not reflect cash requirements for such replacements; |

iv

Table of Contents

| • | they do not reflect our cash used for capital expenditures or contractual commitments; |

| • | they do not reflect changes in or cash requirements for working capital; and |

| • | other companies, including other companies in our industry, may calculate these measures differently than we do, limiting their usefulness as a comparative measure. |

v

Table of Contents

A Letter from Tom Wyatt, our Chief Executive Officer

As a father of two daughters and grandfather to four grandchildren, I know firsthand the joy that comes with raising a family. I also know well the daily juggle that parents with young children face balancing work and personal lives. Childcare was a lifeline then, much like it is today for millions of working parents across the country. When I first joined KinderCare in 2012, I immediately began to spend time in our centers and at our onsite programs. When I saw the incredible interactions that teachers had with children in their care and the smiles on children’s faces, I was reminded of my early days as a parent. I knew right away that working at KinderCare was more than a professional opportunity, it was a personal mission. Today, our shared mission makes every role at our Company a movement we are all proud to be a part of.

Since we opened our first center in 1969, our commitment to delivering the highest quality care possible for families, regardless of who they are or where they live, has never changed. Today, with over 2,000 locations nationwide, we are a collection of thousands of big and little stories written every day; a community of approximately 38,000 passionate employees striving to make each child’s potential shine; a human-powered network in 40 states and the District of Columbia working individually and collectively. Through it all, what we do for children and families remains constant. We are caregivers. We are educators. We impart a lifetime love of learning. We are also so much more. We are builders; of confidence in children; of unshakable self-worth; of conviction that our children can carry with them as they take their first steps and every step toward taking on the world.

As access to high-quality early childhood education has become increasingly recognized as an essential building block of our country’s economic future, KinderCare’s leadership matters now more than ever. Over 17.5 million workers, or about 20% of the American workforce, rely on childcare every day. It is also estimated that nearly 2 million women have left the workforce as a result of the COVID-19 pandemic—a key factor is lack of access to childcare.

Success at work and at home builds stronger communities one child at a time. Studies show that quality early education increases the likelihood of children obtaining higher education credentials and increases self-sufficiency and productivity later in life. This benefit to communities is reinforced by childcare’s contribution to broader economic outcomes including workforce attraction, retention and productivity and economic growth overall.

From their earliest weeks, children build critical social, emotional and academic skills that lay the groundwork for the rest of their educational journey. At KinderCare, as children take their first steps and every step into their future, they do so with confidence.

Our Company purpose is grounded in four pillars that promote a great experience for our children, families and staff and drive profitable growth in the business:

Educational Excellence

Every family wants the best care and education for their child. We deliver that through (i) our proprietary curriculum, (ii) our commitment to accreditation – the third-party validation of the high standards in our centers and sites and (iii) through assessments that consistently prove KinderCare children are better prepared for kindergarten than their peers outside our programs.

People & Engagement

Our industry-first, data-driven talent assessment tools help us hire the best teachers and center staff who will thrive in our classrooms. Our annual employee and family engagement surveys build culture

v

Table of Contents

and connections, and help identify how to best serve children and families and drive business performance. Our approach has helped us win the Gallup Exceptional Workplace Award six years in a row – one of only four employers globally to do so.

Health & Safety

We hold sacred our responsibility to protect and nurture the children in our care. Our rigorous safety standards across all classrooms are reinforced by ongoing training and measurement tools, including third party validation. We help children build healthy bodies and minds by providing them with nutritious meals, physical activity programs and dedicated mental and emotional wellness resources.

Operations & Growth

We bring our high-quality standards to more families and communities each year. We do this by building new centers and inviting smaller high-quality providers to join the KinderCare family. We work with school administrators and public and private employers to expand access to our programs. As we grow our reach, we reinvest in all our pillars to elevate our impact.

These pillars guide each of our employees every day in classrooms across the country. While our footprint is large, it is the footsteps of each child in our care that inspires us. Our unwavering devotion to their children gives families confidence and peace of mind to pursue their dreams and to integrate work and life. Because strong and vibrant communities depend on access to high-quality childcare for all, we serve the full socioeconomic spectrum of families, including those of modest means. This is not a requirement from regulators, it is a matter of principle to which we have held true for the last 50 years and remains core to our mission today.

I am honored to lead KinderCare into this next phase of our journey and invite you to join me in championing the working families of this country and their children.

Tom Wyatt

Chief Executive Officer

vi

Table of Contents

This summary highlights selected information contained elsewhere in this prospectus. Because this is only a summary, it does not contain all the information that may be important to you. You should read the entire prospectus carefully, especially “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes included elsewhere in this prospectus, before deciding to invest in our common stock.

Our Company

We are the largest private provider of high-quality early childhood education and care services (“ECE”) in the United States by center capacity. We are a mission driven organization, rooted in a commitment to providing all children with the very best start in life. We serve children ranging from six weeks to 12 years of age across our market leading footprint of 1,501 early childhood education centers with capacity of more than 195,000 children and 764 before- and after-school sites located in 40 states and the District of Columbia as of October 1, 2022. We believe families choose us because of our differentiated, inclusive approach and our commitment to delivering every child a high-quality educational experience in a nurturing and engaging environment. We operate all of our centers under the KinderCare platform and utilize a consistent curriculum and operational approach across our network.

We offer a differentiated value proposition to the children, families, schools and employers we serve, driven by our market-leading scale and commitment to quality, access and inclusion. We leverage our extensive network of community-based centers, employer-sponsored programs, and before- and after-school sites, to meet parents where they are, which is an important factor in the context of evolving work styles as a result of the novel coronavirus (“COVID-19”) pandemic and the increasing availability of hybrid work arrangements. We utilize our proprietary curriculum with the goal of generating superior outcomes for children of all abilities and backgrounds. We use third-party assessment tools that consistently show children in our centers outperform their peers in other programs in readiness for kindergarten. We voluntarily seek accreditation at all of our centers and onsite programs, demonstrating our commitment to best practices for our sector. Our commitment to transparent, third-party validation of the quality and impact of our offerings is a critical factor for parents when selecting a center for their children. Our culture promotes high levels of employee engagement, which leads to better financial performance of our centers. Our expertise helping families access public subsidies for childcare is a core competency and drives greater levels of diversity and access in our centers.

We have built a reputation as a leader in early childhood education and care across our three go-to-market channels: KinderCare Learning Centers, KinderCare Education at Work and Champions.

| • | KinderCare Learning Centers (“KCLC”) is the largest private provider of community-based early childhood education centers in the United States by center capacity. As of October 1, 2022, KCLC operates approximately 1,400 KCLC centers. Most KCLC centers are accredited by accrediting bodies such as the National Association for the Education of Young Children (“NAEYC”). The accreditation process evaluates curriculum, evidence of learning, operating practices and health and safety protocols. The majority of the unaccredited centers are newer to our fleet of centers – either as newly built centers or as acquisitions and are currently in various stages of the two-year accreditation process. Families typically become aware of KCLC through our strong brand recognition, public relations campaigns, digital and direct marketing efforts and word of mouth references before enrolling directly in a center. KCLC serves families with children between six weeks and 12 years of age. KCLC represented 76.6% and 79.2% of our fiscal 2021 and fiscal 2020 revenue, respectively. |

| • | KinderCare Education at Work (“KCE at Work”) is a leading provider of employer-sponsored childcare programs. As of October 1, 2022, KCLC operates approximately 70 onsite employer-sponsored centers. |

1

Table of Contents

The KCLC centers and onsite employer-sponsored centers together comprise our early childhood education centers. We work closely with employers to design programs that effectively address the childcare needs of their employees. Our ability to offer both onsite centers, as well as access to our own leading KinderCare center network, provides flexibility and accessibility to a broad range of employees, which is becoming more important due to the increasing availability of hybrid work arrangements. We currently serve more than 600 employers through onsite programs and tuition discount benefit programs for employees. KCE at Work represented 19.7% and 17.8% of our fiscal 2021 and fiscal 2020 revenue, respectively. |

| • | Champions is a leading private provider of before- and after-school programs in the United States. Our outsourced model provides an attractive value proposition to schools and districts. We provide staff, teachers and curriculum to deliver high-quality supplemental education and care to families and children onsite at schools we serve, and have 764 sites as of October 1, 2022. Champions represented 3.7% and 3.0% of our fiscal 2021 and fiscal 2020 revenue, respectively. |

Our operating strategy is designed to deliver a high-quality experience for every child and family we serve across all of our centers and sites. This self-reinforcing strategy is anchored in four pillars:

| • | Educational Excellence. We leverage our proprietary curriculum combined with third-party assessment tools and voluntary accreditation to deliver a high-quality educational experience and provide objective validation of the quality and impact of our programs. |

| • | People & Engagement. We utilize a proprietary, data-driven approach to attract, hire and develop exceptional talent. We instill a culture that builds emotional connections between our employees and our mission and values, driving high engagement across our organization. Our internal surveys consistently demonstrate that a more engaged workforce leads to better financial performance of our centers. |

| • | Health & Safety. We consistently adhere to strict procedures across all of our centers to provide a healthy, safe environment for our children and our workforce and to deliver confidence and peace of mind to families. Our procedures address both the physical and mental health of children and are informed by input from the Center for Disease Control and Prevention (the “CDC”) and other third-party experts. |

| • | Operations & Growth. Our operational excellence enables us to deliver profitable growth and to fund consistent reinvestment into our service offerings. We utilize a robust technology platform and proprietary operating procedures to deliver a high-quality, consistent experience across our centers and sites. Our technology platform closely monitors activity across all centers and sites and allows us to stay connected with families on a daily basis through digital channels. We utilize this proprietary data to continuously refine our operations and adapt to changing market conditions and consumer preferences. |

Our History

We have provided children and families with high-quality ECE for over 50 years. Throughout our history, we have empowered parents seeking to enter the workforce with options for excellent early childhood education and care. We have remained committed to providing broad access to our services throughout our history and, over the past decade, have become a leading advocate in our industry, working with legislators to promote greater access to early education for all families.

In 2012, John T. (“Tom”) Wyatt became our CEO to lead our business transformation. Our primary stockholder, PG, acquired control of KinderCare in 2015 to further support this transformation. From 2012 to 2017, Tom and our leadership team implemented and refined our current operating strategy, based on our four pillars described above, to enhance our value to children and families and to drive improved operating performance. During this period, we optimized our center footprint by closing more than 380 centers, drove compound same center

2

Table of Contents

revenue growth of 4.5% and increased same center occupancy from 56% to 69%. We also made significant investments in our curriculum, human capital and technology infrastructure to accelerate growth and strengthen our commitment to quality.

Since 2017, we have executed on our multi-faceted growth strategy to extend our center footprint and reinforce our position as the largest private ECE provider in the United States by center capacity. We acquired 175 centers between fiscal 2018 and fiscal 2021 and opened 84 new greenfield centers. During the nine months ended October 1, 2022, we acquired four additional centers and opened eight new greenfield centers. We established our Growth Delivery, New Center Enrollment and New Center Operations teams, and developed and refined our new center management processes, enabling us to quickly and consistently implement our operating procedures and curriculum while driving growth in inquiries and enrollment. In fiscal 2019, prior to the onset of the COVID-19 pandemic, we grew to $1.9 billion in revenue, had $29 million in net loss and had $180 million in Adjusted EBITDA. From fiscal 2017 to fiscal 2019, we achieved 4.5% compound same center revenue growth. We increased same center occupancy to 72% in early 2020 from 69% in 2017. During this time we also maintained our cost of services excluding depreciation and impairment at approximately 79.2% to 79.4% of revenue.

In March 2020, government-mandated closures of childcare centers, intended to curb the spread of COVID-19, significantly reduced enrollment across our industry. We kept more than 420 centers open to provide childcare to first responders, critical healthcare providers and families working in essential services. We undertook several actions to manage costs and improve liquidity, including curtailing all non-critical business spending, furloughing employees, temporarily reducing the salaries of the executive team and negotiating rent and benefit holidays or deferrals where possible. During the second half of 2020, we reopened 1,021 centers and approximately 320 before- and after-school sites.

In fiscal 2021, we had $1.8 billion in revenue, $88 million in net income and $320 million in Adjusted EBITDA. Our same center revenue increased by 32% primarily due to an increase in same center occupancy to 63%. Our cost of services excluding depreciation and impairment decreased to 72.0% of revenue due to the impact of leveraging fixed costs over higher enrollments and $161 million for reimbursement of center operating expenses from Governmental Stimulus.

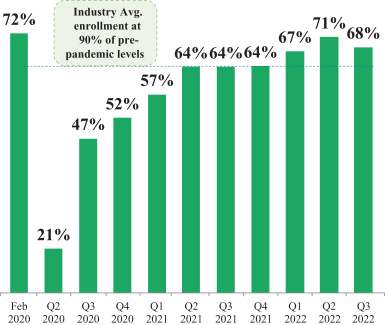

During the nine months ended October 1 , 2022, we had $1.6 billion in revenue, $184 million in net income and $393 million in Adjusted EBITDA. Our same center revenue increased by 17% for the nine months ended October 1, 2022 compared to the nine months ended October 2, 2021, primarily due to higher tuition rates and an increase in same center occupancy to 69% from 62%. Our cost of services excluding depreciation and impairment improved to 64.1% of revenue during the nine months ended October 1, 2022 as compared to 75.0% for the nine months ended October 2, 2021 due to reimbursements from Governmental Stimulus and the impact of leveraging fixed costs over higher enrollments. For the three months ended October 1, 2022, our same center occupancy was 68%, which represents 95% of our occupancy prior to the COVID-19 pandemic, above the industry average of 90% of pre-pandemic occupancy levels. The decline in occupancy from 71% in the second

3

Table of Contents

quarter of 2022 to 68% in the third quarter of 2022 is in line with pre-pandemic historical trends as enrollment typically decreases during the summer months.

Our Industry

We compete in the U.S. ECE market. Over 17.5 million workers, or 20% of the American workforce, rely on childcare every day. According to the Bureau of Economic Research, the U.S. market for private expenditures on education-focused care for children zero to five years of age was $15.2 billion in 2019, and served annual enrollments of approximately 2.5 million children according to management estimates, while the total spending in the United States on childcare was approximately $42 billion, according to the Consumer Expenditure Survey in 2018. From 2012 to 2019, according to the Bureau of Economic Research, private expenditures on education-focused care grew from $10.5 billion to $15.2 billion, representing a compound annual growth rate over the period of 4.7%. We estimate that the market for private expenditures on education-focused care is expected to grow at a compound annual growth rate of 6.4% between 2021 and 2026, excluding any impact from Governmental Stimulus.

The ECE market is highly fragmented with more than 109,000 centers in the United States in 2017, according to the Office of Child Care. We estimate that the top three providers, including KinderCare, represented approximately 5% of total capacity as of January 1, 2020. The COVID-19 pandemic caused many providers to experience significant financial challenges and reduced enrollments due to government restrictions and consumer behavior. As a result, according to Child Care Aware of America, approximately 16,000 centers permanently closed between December 2019 and March 2021, leaving families with fewer options for organized care.

According to management estimates, the employer-sponsored ECE market represented a small but meaningful portion of the overall ECE market with expenditures of approximately $3 billion in 2019. Increasingly, employers recognize the benefits of offering employees access to flexible, high-quality, affordable ECE options on either a full-time or back-up care basis. Evolving work styles are driving a preference for flexible ECE solutions with care options both onsite at corporate offices and in the communities in which employees live.

4

Table of Contents

The market for before- and after-school programs serves children enrolled in pre-K-12 schools. According to the National Center for Education Statistics, there are more than 100,000 schools across the United States. Schools have long recognized the benefits of providing their families with access to before- and after-school care and education programs, though many schools have struggled to effectively manage and deliver such offerings. The lack of before- and after school care onsite creates challenges for children and families who need to travel to and from other providers, such as the YMCA, to access full-day care solutions. Third-party providers, such as Champions, are in the early stages of serving this market opportunity at scale.

We believe the market opportunity for scaled, quality ECE providers will continue to grow due to the following trends and market dynamics:

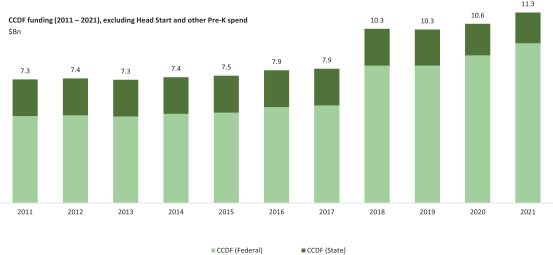

Broad recognition of the benefit of ECE drives growth in private spend and consistent public subsidy funding. Studies consistently show that organized early childhood education fosters the development of cognitive and social skills, better preparing children for success in school and life and achieving long-term benefits for society, including a 28% increase in likelihood of graduating high school if such child had received high-quality early education according to the Perry Preschool Project. The U.S. government has consistently passed bipartisan public funding to support ECE to catalyze these societal benefits. Federal subsidies for ECE, primarily provided through the Child Care and Development Fund (“CCDF”), authorized under the Child Care and Development Block Grant (“CCDBG”) Act, increased from $4.9 billion in 2008 to $9.5 billion in 2021.

The government funding available through the CCDF has increased since 2011:

Trends in labor force participation continue to support robust demand for high-quality ECE. As of 2021, 67% of children under the age of six were in dual income households, an increase from 65% in 2016 according to National Kids Count. The labor force participation rate of women ages 20 to 44 in the United States increased from 73% in 2011 to 74% in 2021 according to the U.S. Bureau of Labor Statistics, representing an estimated 2.6 million additional women in the workforce. Among millennials, over 80% cite work-life integration, of which access to high-quality childcare is a key component, as the most important factor in job selection according to a Forbes article published in 2020. However, in 2018, more than 80% of parents with children under the age of five reported challenges in finding affordable, quality care according to the Affordable Child Care and Early Learning for All Families report published in 2018 by the Center for American Progress. These trends are expected to drive sustained growth in the ECE market.

5

Table of Contents

Reduced capacity from COVID-19 pandemic-related center closings creates opportunity for high-quality ECE providers. Government restrictions and shifts in consumer behavior caused many operators to experience significant financial challenges and reduced enrollments during the COVID-19 pandemic. As a result, according to Child Care Aware of America, approximately 16,000 centers permanently closed between December 2019 and March 2021. This reduced capacity has increased demand for scaled providers, such as KinderCare, and has created incremental opportunities for greenfield expansion or acquisitions.

Evolving work styles have increased the need for flexible ECE offerings. We believe providers that offer ECE via a variety of delivery channels are best positioned to meet the demands of parents regardless as to how future work styles evolve. Many employers are actively implementing blended models, balancing the amount of time employees spend working remotely versus in the office. In response to the evolving landscape, the mix of demand for ECE provided in communities, at corporate offices and onsite in schools is expected to evolve. In many cases, parents are expected to take advantage of the services offered through multiple channels to best meet their needs.

Over $50 billion in Governmental Stimulus provides meaningful support for ECE. The U.S. federal government has acknowledged the importance of the ECE market through recently passed federal governmental acts designed to support continued access to ECE for parents. The CARES Act, signed into law on March 27, 2020, provided $3.5 billion in stimulus funding for childcare assistance.

The Consolidated Appropriations Act (“CAA”), passed in December 2020, includes $10 billion in stimulus funding for the CCDBG to supplement state general revenue funds to support the childcare needs of working families and to stabilize childcare providers. The American Rescue Plan Act (“ARPA”), passed in March 2021, includes $15 billion in stimulus funding for the CCDBG and an additional $24 billion for a COVID-19 childcare relief and stabilization fund, which provides states with resources to offer immediate grants to childcare providers. All stimulus funding under the CAA and ARPA must be distributed by December 31, 2024.

Scaled providers are uniquely qualified to navigate complex public subsidy and stimulus funding channels. Each state has unique and disparate processes to administer funds received from the CCDF, making it difficult for many families and providers to access public subsidy and stimulus funding. Scaled providers with the expertise, resources and infrastructure necessary to understand each state’s requirements and support families through the application process are best positioned to capture enrollments supported by public funds. We expect public subsidy funding for ECE to continue to grow, furthering the importance of this capability.

Our Competitive Strengths

We believe the following are our core strengths that differentiate us from our competition:

Market leader with significant scale advantages. We are the largest private provider of ECE in the United States by center capacity with nearly 40% greater center capacity based on our estimates than the next largest operator. Our scale enables us to (i) identify best practices within our network and apply them across all of our centers and onsite programs, (ii) consistently invest in our curriculum, teachers and rigorous health and safety protocols across all our centers and sites, (iii) invest in our technology infrastructure to better manage our operations, (iv) identify opportunities for expansion through greenfield centers and acquisitions, (v) help our families access public subsidy funding by engaging with over 800 government agencies and (vi) serve as a leading, visible advocate for our industry with legislators.

Diverse set of offerings that enable broad access to our services. We believe we are the only ECE provider with the ability to reach families in their communities, at their places of employment and onsite at their children’s schools. Our mix of community-based and onsite centers makes us well-suited to address families’ ECE needs,

6

Table of Contents

especially as work styles evolve and hybrid work arrangements become increasingly available. The flexibility of our KCE at Work offering allows us to provide tailored programs to employers seeking flexible, employer-sponsored care solutions for their employees. Our before- and after-school programs extend our offerings to older children at their schools, expanding the population of families and children that we are able to effectively serve.

Commitment to educational excellence across our footprint. We have intentionally designed our curriculum for children of all abilities, and we continuously enhance and refine our curriculum to drive better outcomes. As educational quality for young children can be difficult for parents to assess, we utilize objective, third-party assessment tools and accreditation to demonstrate the impact of our programs. We voluntarily seek accreditation at all of our centers and onsite programs. Very few providers embrace accreditation across their entire center network. In addition, our internal studies with third-party assessment tools show that on average, children who begin attending KinderCare centers as infants are six weeks ahead of their peers at two years of age and nine months ahead at five years of age and KinderCare kindergartners test at least two months ahead of expectations for first grade.

Strong workforce engagement which inspires our best talent to do their best work. We utilize a holistic approach to attract, train and develop a talented workforce, at scale, and drive workforce engagement. Our approach fosters stronger connections with families and better center financial performance. Our workforce culture is a fundamental driver of employee engagement as we strive to maintain a culture that is mission driven, inclusive and values the input of each of our employees. Also, we are the only early education company to utilize a predictive, data-driven selection tool in our hiring practices. Our internal research shows that centers with higher employee and family engagement generated, on average, 1.5 and 2.5 times higher revenue growth in our network in 2018 and 2019, respectively. In 2021, 72% of our workforce considered themselves engaged, nearly double the U.S. population average. Through our continued focus on engagement, we have received the Gallup Exceptional Workplace Award every year from 2017 to 2022, making us one of only four companies worldwide to win this award six years in a row.

Technology infrastructure supporting efficient, data-driven decisions across our business. We invest significant resources into our technology infrastructure to support our centers and site operations and our interactions with current and prospective families. We leverage our proprietary OneCMS platform to provide real-time key performance indicator (“KPI”) tracking and reporting across all of our centers. Our OneCMS platform drives consistency, economies of scale and efficient integration of greenfield and acquired centers. We utilize a Salesforce-based client relationship management (“CRM”) system to manage inquiries from new families and effectively enroll and onboard new children and families into our centers and sites. We engage with our families through our robust mobile platform to connect them with their centers and provide daily updates on their child’s activity and developmental progress. All of these systems generate valuable data that we leverage to inform decision-making, improve learning outcomes and increase family engagement and retention.

Expertise helping families access public subsidy funding for childcare. We proactively work with prospective and current families to help them access public subsidy funding. The process for accessing public subsidy funding is complex and burdensome, causing many families to forego applying for available resources. Our dedicated Subsidy Team assists families with understanding the requirements of programs available to them and with completing the administrative steps necessary to access public subsidy funding. Our scale allows us to invest in the expertise, resources and infrastructure needed to effectively navigate these programs across our network of centers. Our frequent interactions and relationships with government institutions position us as a leading advocate for our industry to help build continued growing public funding support for our sector.

High-quality management team demonstrating deep industry experience across education and multi-site consumer industries and track record of profitable growth. Our experienced management team has executed on its strategic initiatives with respect to people, education and financial performance. The combined expertise and

7

Table of Contents

experience of our management team covers early childcare, multi-site platforms and education, representing more than 135 years of relevant professional experience. Our Company is managed by a seasoned team of professionals led by Chief Executive Officer Tom Wyatt who, with more than 40 years of experience leading successful childcare and multi-site platforms, has guided our Company to achieve the highest standards of excellence in ECE. Chief Academic Officer Dr. Elanna Yalow is responsible for the development of KinderCare’s educational programs as well as public policy and accreditation initiatives. Paul Thompson, President, and Anthony (“Tony”) Amandi, Chief Financial Officer, have 33 and 22 years of relevant experience, respectively, and provide strong continuity of operational expertise. Since installing Tom as Chief Executive Officer, our management team demonstrated consistent profitable growth, achieving a compound same center revenue growth of 4.5% from 2012 to 2019.

Our Growth Strategies

We intend to extend our position as the largest private ECE provider in the United States by center capacity through our key growth strategies, as follows:

Increase enrollments and occupancy at our existing centers. We employ a multi-pronged strategy to increase enrollments and occupancy. Our commitment to inclusive access and transparent, third-party validation across our offerings allows us to provide a differentiated value proposition to families seeking ECE. We leverage our strong brand recognition, public relations campaigns, digital and direct marketing campaigns and word-of-mouth references to attract families to our centers. As a scaled provider, we are well-positioned to benefit from the combined impacts of growing ECE demand and supply reductions driven by COVID-19 pandemic-related center closures. Given our scale and operational expertise and resources, we possess a unique ability to serve families supported by public subsidy funding and the agility to meet evolving family preferences toward flexible and accredited providers.

Leverage dedicated teams and data-driven research to open new greenfield centers. We consistently open new greenfield centers that generate attractive returns and complement our existing center network. We opened 84 new greenfield centers from fiscal 2018 to fiscal 2021. During the nine months ended October 1, 2022, we opened eight new greenfield centers. We maintain a robust pipeline of new center opportunities and employ a disciplined and data driven approach in selecting locations for new greenfield centers. We utilize dedicated, specialized teams to oversee the development and opening of each new center. This approach creates a scalable, repeatable and highly efficient process while ensuring we are creating the best experience for families and center staff. When evaluating our new center occupancy after eight weeks of operation, we have seen improvements in occupancy each year from 2017 to 2019. Class of 2020 center performance was negatively impacted by the COVID-19 pandemic due to temporary closures of centers and delayed opening dates, and as such occupancy rates were approximately at par with class of 2017 centers. Class of 2021 and 2022 centers performed in line with pre-COVID expectations, approximately 20 and 15 percentages points improved, respectively, from 2017 levels when we began our growth journey.

Continue to expand our flexible employer-sponsored program offerings. We provide employers with a diverse, flexible offering to best meet the needs of their workforce, positioning us to grow our employer client base as work styles evolve. In addition to offering access to our own network of approximately 1,400 KCLC centers, we also offer onsite employer-sponsored centers providing employers with the ability to design flexible programs to meet the shifting needs of their employees. We also offer tuition benefits programs, which allow employers to provide discounted access to our centers. Since 2019, we have grown our number of employer relationships from approximately 400 to more than 600 as of October 1, 2022. These relationships include approximately 70 onsite employer-sponsored centers.

8

Table of Contents

Re-invest revenue from consistent price increases to enhance our value proposition for families. We consistently invest in all aspects of our service offering to deliver high-quality, accessible ECE. We also offer competitive compensation and benefits packages as well as periodic salary increases for our teachers and staff. We implement regular price increases across our centers to support these investments. Over the past three years, our annual tuition price increases ranged from 2-6% across all of our centers. Rate increases vary by age and center. We have found that parents appreciate our investment in delivering a high-quality ECE solution for their children and are supportive of reasonable annual price increases to facilitate such investments. Additionally, while our rates for children of a given age increase each year, these rates generally decrease as children get older. Our pricing methodology indexes rates against our entry level infant tuition rates; toddler rates are set at approximately 97%, two-year old rates are set at approximately 88% and preschool rates are set at approximately 81% of infant tuition rates. As a result, the out-of-pocket costs paid by parents typically decrease as children age, despite our annual rate increases.

Increase the number of sites served and grow enrollments in programs offered by Champions. We actively pursue opportunities to offer Champions before- and after-school programs to additional schools and to grow enrollment in programs offered at existing sites. Champions offers high-quality, education-focused accredited programs conveniently onsite at the schools we serve, while removing the administrative burden for the school to operate these programs. From 2015 to 2019, we grew our revenues from Champions at a compound annual growth rate of more than 13%. We currently have 764 sites, a small percentage of the over 100,000 schools in the United States, providing significant opportunity to continue to grow our footprint.

Opportunistically pursue strategic acquisitions and partnerships. We continue to grow our footprint by acquiring centers through our disciplined acquisition approach. We acquired 175 centers between fiscal 2018 and fiscal 2021. During the nine months ended October 1, 2022, we acquired four additional centers. We maintain a robust pipeline of targets, ranging in size from single site to multi-site providers, to support our inorganic growth trajectory. We quickly transition newly acquired centers onto our technology platform, implement our proprietary curriculum and center management processes and rebrand such centers. Given the significant fragmentation in our industry, we expect to continue to pursue acquisitions that meet our criteria and complement our existing network. Additionally, we expect to pursue acquisitions to add new brands that will allow us to target and serve specific populations as well as to potentially grow our presence in attractive international markets.

Environmental, Social and Governance (“ESG”) Considerations

Our mission is to provide high-quality ECE to families of all backgrounds and means. We believe that widespread investment in early childhood care and education produces long-term societal benefits including stronger, healthier communities and a more productive economy.

We are working to formalize our commitment to sustainable and impactful business practices through our ESG initiatives, policies, and goals and we remain committed to advancing our ESG strategic priorities.

9

Table of Contents

Summary Risk Factors

We are subject to a number of risks, including risks that may prevent us from achieving our business objectives or that may adversely affect our business, financial condition and results of operations. You should carefully consider the risks discussed in the section titled “Risk Factors,” including the following risks, before investing in our common stock:

Risks Related to our Business

| • | Changes in the demand for childcare and workplace solutions, influenced by a permanent shift in workforce demographics, economic conditions, office environments, unemployment rates, and the failure to anticipate and respond to changing preferences and expectations, may affect our operating results. |

| • | Our business depends largely on our ability to hire and retain qualified teachers, key management, key employees and maintain strong employee engagement. |

| • | The COVID-19 pandemic has disrupted our business, financial condition and results of operations and will continue to adversely impact our business. |

| • | Adverse publicity could impact demand for our services, as well as the value of our brands and reputation as a provider of choice. |

| • | Our continued profitability depends on our ability to offset our increased costs through tuition increases. |

| • | Governmental universal childcare benefit programs and changes in the spending policies or budget priorities for government funding of childcare and education could impact demand for our services. |

| • | We have identified a material weakness in our internal control over financial reporting. |

Risks Related to our Capital Structure, Indebtedness and Capital Requirements

| • | We may face risks related to our indebtedness. |

| • | The terms of our Credit Facilities impose operating and financial restrictions on us that may impair our ability to respond to changing barriers and economic conditions. |

| • | We may require additional capital to meet our financial obligations and support business growth, and this capital may not be available on acceptable terms or at all. |

| • | Acquisitions have played a part in our strong growth portfolio, and contribute to our competitive industry profile, but they also present many risks and may disrupt our operations. We also may not realize the financial and strategic goals that were contemplated at the time of the transaction. |

| • | We are a holding company with no operations of our own, and we depend on our subsidiaries for cash. |

Risks Related to Intellectual Property, Information Technology and Data Privacy and Security

| • | We rely significantly on the use of our IT systems, as well as the technology of our third-party service providers and any significant failure, inadequacy, interruption or data security incident of our IT systems, or those of our third-party service providers, could disrupt our business operations. |

| • | If we are unable to adequately protect our intellectual property rights, our business, financial condition and results of operations may be materially and adversely affected. |

| • | Our collection, use, storage, disclosure, transfer and other processing of personal information could give rise to significant costs and liabilities, including as a result of governmental regulation, uncertain or inconsistent interpretation and enforcement of legal requirements or differing views of personal privacy rights, which may have a material adverse effect on our reputation, business, financial condition and results of operations. |

10

Table of Contents

| • | We are subject to payment-related risks that may result in higher operating costs or the inability to process payments, either of which could harm our brand, reputation, business, financial condition and results of operations. |

Risks Related to our Common Stock and this Offering

| • | If our stock price fluctuates after this offering, you could lose a significant part of your investment. |

| • | We are a “controlled company” within the meaning of the rules and, as a result, will qualify for, and may rely on, exemptions from certain corporate governance requirements. You will not have the same protections afforded to stockholders of companies that are subject to such requirements. |

| • | Some provisions of our charter documents and Delaware law may have anti-takeover effects that could discourage an acquisition of us by others, even if an acquisition would be beneficial to our stockholders, and may prevent attempts by our stockholders to replace or remove our current management. |

| • | Changes in tax laws or to any of the several factors upon which our tax rate is dependent could impact our future tax rates and net income and affect our profitability. |

General Risks

| • | Our business, financial condition and results of operations may be materially and adversely affected by various litigation and regulatory proceedings. |

| • | Inadequacy of our insurance coverage could have a material and adverse effect on our business, financial condition and results of operations. |

| • | Becoming a public company will increase our compliance costs significantly and require the expansion and enhancement of a variety of financial and management control systems and infrastructure and the hiring of significant additional qualified personnel. |

| • | We will be exposed to risks relating to evaluations of controls required by Section 404 of the Sarbanes-Oxley Act. |

| • | Natural disasters, geo-political events and other highly disruptive events could materially and adversely affect our business, financial condition and results of operations. |

| • | Discovery of any environmental contamination may affect our operating results. |

Our business also faces a number of other challenges and risks discussed throughout this prospectus. You should read the entire prospectus carefully, especially “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes included elsewhere in this prospectus, before deciding to invest in our common stock.

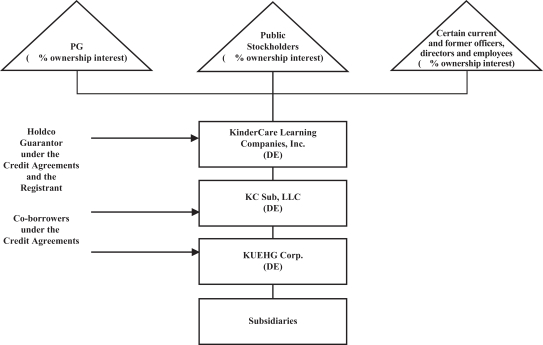

The Reorganization and Our Organizational Structure

We operate as a Delaware corporation under the name KinderCare Learning Companies, Inc. Shortly after the effectiveness of the registration statement of which this prospectus forms a part:

| • | Pursuant to our existing amended and restated certificate of incorporation, each of our outstanding shares of Class A common stock will automatically convert to shares of common stock at a conversion ratio determined by our board of directors in connection with this offering, and each of our outstanding shares of Class B common stock will automatically convert to shares of common stock at a conversion ratio determined by our board of directors in connection with this offering. The conversion ratios for the conversion of Class A common stock to shares of common stock and the conversion of Class B common stock to shares of common stock may be different. |

11

Table of Contents

| • | KC Parent, LLC, our direct parent, will liquidate and distribute our common stock then held by KC Parent, LLC to unitholders of KC Parent, LLC in proportion to their interests in KC Parent, LLC. |

| • | The holders of the Class A Units of KC Parent, LLC will receive shares of common stock in connection with the Reorganization in proportion to their interests in KC Parent, LLC. The Class B Units of KC Parent, LLC will vest in connection with the Reorganization and the holders of the Class B Units will receive shares of common stock in proportion to their fully vested interests in KC Parent, LLC. The Class B-1 Units will automatically accelerate and vest based on the expected value to be received by the Partners Group Members (as defined in Parent’s limited liability company agreement). Our board of directors has determined that the Class B-2 Units and Class B-3 Units will be deemed to have vested as well. $ of the shares of common stock that the prior holders of the Class B Units will receive will be redeemed with the proceeds of this offering. See “Use of Proceeds.” |

We collectively refer to the foregoing organizational transactions as the “Reorganization.”

The diagram below depicts our organizational structure after giving effect to the Reorganization, including this offering.

Our Corporate Information

KinderCare Learning Companies, Inc. is a Delaware corporation. On January 2, 2022, KC Holdco, LLC, a Delaware limited liability company, converted into a Delaware corporation through a Delaware law statutory conversion and was renamed KinderCare Learning Companies, Inc. Upon consummation of this offering, assuming the sale of shares in this offering and the redemption of $ of common stock, PG will own approximately % of our shares of common stock. See “Principal Stockholders” and “Use of Proceeds.”

Our principal executive office is located at 5005 Meadows Road, Lake Oswego, OR 97035 and our telephone number at that address is 503-872-1300. We maintain a website at www.kindercare.com. We have included our website address in this prospectus as an inactive textual reference only. The information contained on, or that can be accessed through, our website is not a part of, and should not be considered as being incorporated by reference into, this prospectus.

12

Table of Contents

THE OFFERING

| Common stock offered by us | shares. | |

| Common stock to be outstanding after this offering | shares (or shares, if the underwriters exercise in full their option to purchase additional shares of common stock) including the impact of the redemption of $ of shares of common stock described in “—Use of Proceeds” below. | |

| Option to purchase additional shares from us | shares. | |

| Use of proceeds | We estimate that the net proceeds to us from our sale of shares in this offering, after deducting underwriting discounts and estimated offering expenses payable by us, will be approximately $ (or $ , if the underwriters exercise in full their option to purchase additional shares of common stock), assuming an initial public offering price of $ per share (the midpoint of the price range set forth on the cover page of this prospectus). We intend to use the net proceeds from this offering to (i) repay $ of our outstanding First Lien Notes, repay $ of the loans outstanding under our Second Lien Facility and then repay $ of the loans outstanding under our First Lien Term Loan Facility, (ii) redeem $ of the shares of common stock received by members of management from vested Class B Units of KC Parent, LLC in connection with the Reorganization and (iii) pay fees and expenses in connection with this offering. We intend to use the remainder, if any, of the net proceeds to us from this offering for general corporate purposes. See “Use of Proceeds.” | |

| Symbol | “KLC.” | |

| Controlled company | Following this offering, we will be a “controlled company” within the meaning of the corporate governance rules of the New York Stock Exchange. See “Management—Director Independence and Controlled Company Exception.” | |

| Conflicts of interest | Affiliates of Barclays Capital Inc., Morgan Stanley & Co. LLC and Credit Suisse Securities (USA) LLC are lenders under our First Lien Facilities and Credit Suisse Securities (USA) LLC will receive 5% or more of the net proceeds of this offering due to the repayment of borrowings thereunder. Therefore, Barclays Capital Inc., Morgan Stanley & Co. LLC and Credit Suisse Securities (USA) LLC are deemed to have a conflict of interest within the meaning of FINRA Rule 5121. Accordingly, this offering is being conducted in accordance with Rule 5121, which requires, among other things, that a “qualified independent underwriter” participate in the preparation of, and exercise the usual standards of “due diligence” with respect to, the registration statement and this prospectus. Jefferies LLC has agreed to act as a qualified independent underwriter for this offering and to undertake the legal responsibilities and liabilities of an underwriter under the Securities Act, including specifically those inherent in Section 11 thereof. Jefferies LLC will not receive any additional fees for | |

13

Table of Contents

| serving as a qualified independent underwriter in connection with this offering. | ||

| Risk factors | Investing in our common stock involves a high degree of risk. See “Risk Factors” beginning on page 22 of this prospectus for a discussion of factors you should carefully consider before investing in our common stock. | |

The number of shares of common stock to be outstanding after this offering excludes:

| • | shares of common stock reserved for future issuance under our Amended and Restated 2022 Incentive Award Plan (the “A&R 2022 Plan”), which will become effective once the registration statement of which this prospectus forms a part is declared effective, as well as any shares of common stock that become available pursuant to provisions in the A&R 2022 Plan that automatically increase the share reserve under the A&R 2022 Plan; |

| • | shares of common stock reserved for future issuance under our 2022 Employee Stock Purchase Plan (the “ESPP”), which will become effective once the registration statement of which this prospectus forms a part is declared effective, as well as any shares of common stock that become available pursuant to provisions in the ESPP that automatically increase the share reserve under the ESPP; |

| • | up to shares of common stock issuable upon the exercise of options outstanding under our A&R 2022 Plan as of , 2022 with a weighted average exercise price of $ per share (taking into account the automatic conversion of our Class B common stock into shares of our common stock); and |

| • | shares of common stock issuable upon the vesting of restricted stock under our A&R 2022 Plan outstanding as of , 2022 (taking into account the automatic conversion of our Class B common stock into shares of our common stock). |

Unless otherwise indicated, all information contained in this prospectus:

| • | assumes an initial public offering price of $ per share, which is the midpoint of the price range set forth on the cover page of this prospectus; |

| • | assumes the underwriters’ option to purchase additional shares will not be exercised; |

| • | assumes the Reorganization has been consummated prior to the closing of this offering; and |

| • | gives effect to our third amended and restated certificate of incorporation and our amended and restated bylaws. |

14

Table of Contents

SUMMARY CONSOLIDATED FINANCIAL AND OPERATING DATA

We present below our summary consolidated statements of operations and of cash flow data for the nine months ended October 1, 2022 and October 2, 2021 and for the fiscal years ended January 1, 2022, January 2, 2021 and December 28, 2019, and our consolidated balance sheet data as of October 1, 2022, January 1, 2022 and January 2, 2021. We have derived this information from our unaudited condensed consolidated interim financial statements and audited consolidated annual financial statements included elsewhere in this prospectus. In our opinion, the unaudited condensed consolidated interim financial statements have been prepared on a basis consistent with our audited consolidated annual financial statements and contain all adjustments, consisting only of normal and recurring adjustments, necessary for a fair statement of such financial statements.

The historical results presented below are not necessarily indicative of the results to be expected for any future period. You should read the summary consolidated financial and operating data presented below in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes included elsewhere in this prospectus.

Consolidated Statements of Operations Data

| Nine Months Ended | Fiscal Years Ended | |||||||||||||||||||

| October 1, 2022 | October 2, 2021 | January 1, 2022 | January 2, 2021 | December 28, 2019 | ||||||||||||||||

| (in thousands, except per share/unit data) | ||||||||||||||||||||

Revenue | $ | 1,590,601 | $ | 1,332,299 | $ | 1,807,814 | $ | 1,366,556 | $ | 1,875,664 | ||||||||||

Operating expenses | ||||||||||||||||||||

Cost of services (excluding depreciation and impairment) | 1,020,253 | 999,543 | 1,301,617 | 1,152,063 | 1,486,430 | |||||||||||||||

Depreciation and amortization | 62,776 | 61,233 | 82,313 | 87,919 | 99,255 | |||||||||||||||

Selling, general, and administrative expenses | 181,443 | 137,919 | 204,182 | 158,409 | 202,701 | |||||||||||||||

Impairment losses | 11,727 | 5,387 | 7,302 | 38,645 | 22,908 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total operating expenses | 1,276,199 | 1,204,082 | 1,595,414 | 1,437,036 | 1,811,294 | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Income (loss) from operations | 314,402 | 128,217 | 212,400 | (70,480 | ) | 64,370 | ||||||||||||||

Interest expense, net | 68,825 | 72,236 | 96,564 | 99,353 | 102,626 | |||||||||||||||

Other income, net | (550 | ) | (547 | ) | (631 | ) | (1,039 | ) | (1,027 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Income (loss) before income taxes | 246,127 | 56,528 | 116,467 | (168,794 | ) | (37,229 | ) | |||||||||||||

Income tax expense (benefit) | 62,503 | 15,046 | 28,058 | (39,298 | ) | (8,088 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net income (loss) | $ | 183,624 | $ | 41,482 | $ | 88,409 | $ | (129,496 | ) | $ | (29,141 | ) | ||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Other comprehensive income (loss), net of tax: | ||||||||||||||||||||

Change in net gains (losses) on cash flow hedges | — | 4,946 | 6,742 | 787 | (11,537 | ) | ||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total comprehensive income (loss) | $ | 183,624 | $ | 46,428 | $ | 95,151 | $ | (128,709 | ) | $ | (40,678 | ) | ||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net income (loss) per common share/member’s interest unit | ||||||||||||||||||||

Basic | $ | 0.23 | $ | 0.06 | | $ | 0.12 | $ | (0.18 | ) | $ | (0.04 | ) | |||||||

Diluted | $ | 0.23 | $ | 0.06 | $ | 0.12 | $ | (0.18 | ) | $ | (0.04 | ) | ||||||||

Weighted average number of common shares/member’s interest units outstanding | ||||||||||||||||||||

Basic | 790,461 | 750,181 | 757,614 | 727,838 | 706,664 | |||||||||||||||

Diluted | 790,818 | 750,181 | 757,614 | 727,838 | 706,664 | |||||||||||||||

15

Table of Contents

Pro Forma Presentation