As filed with the U.S. Securities and Exchange Commission on August 15, 2022.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

Under

The Securities Act of 1933

Nuvectis Pharma, Inc.

(Exact name of Registrant as specified in its charter)

| Delaware | 2834 | 86-2405608 |

| (State of incorporation | (Primary Standard Industrial | (I.R.S. Employer |

| or organization) | Classification Code Number) | Identification Number) |

1 Bridge Plaza

Suite 275

Fort Lee, NJ, 07024

(201) 614-3150

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Ron Bentsur, M.B.A.

Chairman and Chief Executive Officer

Nuvectis Pharma, Inc.

1 Bridge Plaza

Suite 275

Fort Lee, NJ, 07024

(201) 614-3151

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copy to:

Matthew W. Mamak

Alston & Bird LLP

90 Park Avenue

New York, NY 10016

(212) 210-1256

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | | Accelerated filer | ¨ | |

| Non-accelerated filer | x | | Smaller reporting company | x | |

| | | Emerging growth company | x | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting ¨

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. Neither we nor the selling security holders may sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities, and it is not soliciting offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

PRELIMINARY PROSPECTUS SUBJECT TO COMPLETION DATED AUGUST , 2022

1,015,598 Shares of Common Stock

Up to 909,091 Shares of Class Common Stock Issuable Upon Exercise of the Pre-Funded Warrants

Up to 2,040,170 Shares of Class Common Stock Issuable Upon Exercise of the Preferred Investment Options

Nuvectis Pharma, Inc.

This prospectus relates to the offer and resale from time to time by the selling securityholders named in this prospectus (the “Selling Shareholders”) of shares of common stock, par value $0.00001 per share (“Common Stock”) of Nuvectis Pharma, Inc., a Delaware corporation (“Nuvectis”, the “Company”, “we”, “us” or “our) consisting of (i) up to: 1,015,598 shares of our Common Stock issued in connection with our private placement offering (the “Shares”); (ii) up to 2,040,170 shares of Common Stock that may be obtained upon the exercise of preferred investment options to purchase shares of Common Stock (the “Investment Options”); and (iii) up to 909,091 pre-funded warrants to purchase shares of Common Stock issued in a private placement (the “Pre-Funded Warrants”).

We will not receive any proceeds from the sale of the securities under this prospectus, although we could receive up to $19,765,056 upon the exercise of all of the Investment Options and Pre-Funded Warrants. Any amounts we receive from such exercises will be used for working capital and other general corporate purposes.

Information regarding the Selling Shareholders, the amounts of shares of Common Stock that may be sold by them and the times and manner in which they may offer and sell the shares of common stock under this prospectus is provided under the sections titled “Selling Shareholders” and “Plan of Distribution,” respectively, in this prospectus. We have not been informed by any of the Selling Shareholders that they intend to sell the common stock covered by this prospectus and do not know when or in what amount the Selling Shareholders may offer the common stock for sale. The Selling Shareholders may sell any, all, or none of the common stock offered by this prospectus.

Our Common Stock is listed on the Nasdaq Capital Market under the symbol “NVCT”. On August 12, 2022, the last reported sale price of our common stock was $8.71 per share.

We are an “emerging growth company” and a “smaller reporting company” as defined under the U.S. federal securities laws and, as such, have elected to comply with certain reduced reporting requirements.

Investing in our common stock involves a high degree of risk. See “Risk factors” beginning on page 8.

Neither the Securities and Exchange Commission nor any other state securities commission has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

You should rely only on the information contained in this prospectus. We have not authorized any dealer, salesperson or other person to provide you with information concerning us, except for the information contained in this prospectus. The information contained in this prospectus is complete and accurate only as of the date on the front cover page of this prospectus, regardless of the time of delivery of this prospectus or the sale of any securities. This prospectus is not an offer to sell these securities and we are not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

The date of this prospectus is August 15, 2022.

Table of Contents

About this Prospectus

In this prospectus, unless the context suggests otherwise, references to “Nuvectis Pharma,” “Nuvectis,” the “Company,” “we,” “us” and “our” refer to Nuvectis Pharma, Inc.

This prospectus is part of a registration statement on Form S-1 that we filed with the Securities and Exchange Commission (the “SEC”). Under this registration process, the Selling Shareholders may, from time to time, sell the securities offered by them described in this prospectus through any means described in the section titled “Plan of Distribution”. We will not receive any proceeds from the sale by such Selling Holders of the securities offered by them described in this prospectus. This prospectus also relates to the issuance by us of the shares of Common Stock issuable upon the exercise of any Investment Option or Pre-Funded Warrant. We will receive proceeds from any exercise of the Investment Options and Pre-Funded Warrants for cash.

Neither we nor the Selling Shareholders have authorized anyone to provide you with any information or to make any representations other than those contained in this prospectus or any applicable prospectus supplement or any free writing prospectuses prepared by or on behalf of us or to which we have referred you. Neither we nor the Selling Shareholders take responsibility for and can provide no assurance as to the reliability of, any other information that others may give you. Neither we nor the Selling Shareholders will make an offer to sell these securities in any jurisdiction where the offer or sale is not permitted.

We may also provide a prospectus supplement or post-effective amendment to the registration statement to add information to, or update or change information contained in, this prospectus. Any statement contained in this prospectus will be deemed to be modified or superseded for purposes of this prospectus to the extent that a statement contained in such prospectus supplement or post-effective amendment modifies or supersedes such statement. Any statement so modified will be deemed to constitute a part of this prospectus only as so modified, and any statement so superseded will not be deemed to constitute a part of this prospectus. You should read both this prospectus and any applicable prospectus supplement or post-effective amendment to the registration statement together with the additional information to which we refer you in the section of this prospectus titled “Where You Can Find More Information.”

Prospectus Summary

This summary highlights information contained in greater detail elsewhere in this prospectus and does not contain all of the information that you should consider in making your investment decision. Before investing in our Common Stock, you should carefully read this entire prospectus, including our financial statements and the related notes thereto included elsewhere in this prospectus. You should also consider, among other things, the information set forth under the sections titled “Risk Factors,” “Special Note Regarding Forward-Looking Statements,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” in each case appearing elsewhere in this prospectus. Unless the context otherwise requires, we use the terms “Nuvectis,” “Nuvectis Pharma,” the “Company,” “we,” “us,” “our” and similar designations in this prospectus to refer to Nuvectis Pharma, Inc. and, where appropriate, our subsidiaries.

Overview

We are a biopharmaceutical company focused on the development of novel targeted small molecule therapeutics for the treatment of cancer in genetically defined patient populations. Our precision medicine approach translates key scientific insights relating to the oncogenic drivers and pathway addiction of cancer into potent and highly selective anticancer drugs. In addition, we will investigate the relevance of specific mutations and other DNA alterations as a potential patient selection marker and to identify synthetic lethality targets. This work could support our use of a tumor agnostic development strategy wherein we enroll patients based on the cancer’s genetic and molecular features without regard to the type or location of the cancer.

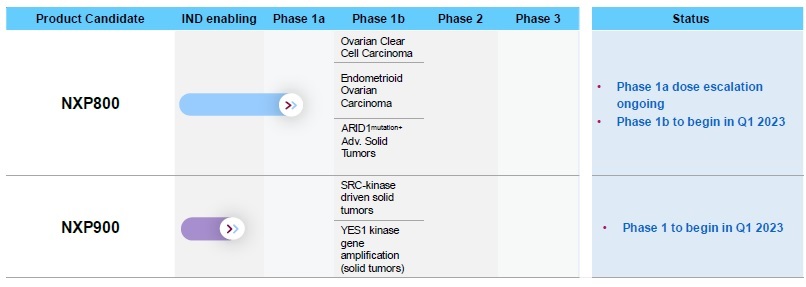

NXP800 (HSF1-Pathway Inhibitor)

We have licensed exclusive world-wide commercial rights to NXP800, a clinical-stage novel Heat Shock Factor 1 (“HSF1”) pathway inhibitor, which was developed at the Institute for Cancer Research (“ICR”) in London, England. Cancer cells actively exploit HSF1 to overcome diverse stresses and promote biological activities crucial for their survival, progression, immune evasion, and metastasis.

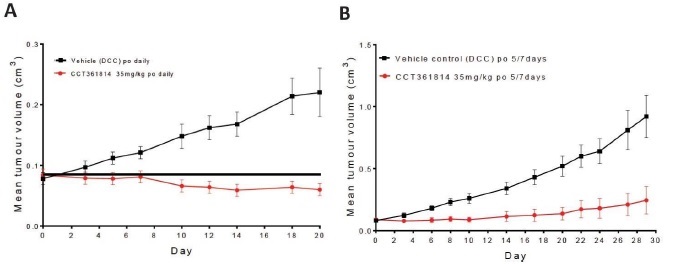

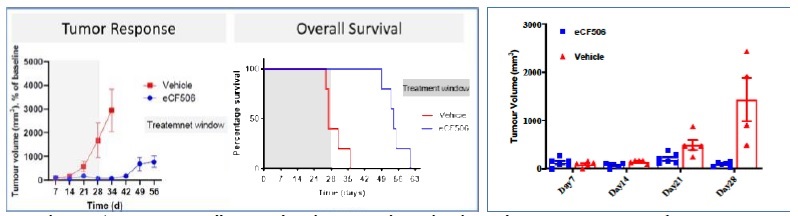

In preclinical studies, treatment with NXP800 inhibited tumor growth in xenografts models of human ovarian cancer. In addition, a genetic mutation in the AT-rich interactive domain-containing protein 1A (“ARID1a”) gene has been identified as a potential biomarker for treatment sensitivity and patient selection. Based on this work, we plan to clinically investigate NXP800 in Ovarian Clear Cell Carcinoma (“OCCC”) and endometrioid ovarian carcinoma, and to investigate the utility of ARID1a deficiency as a patient selection marker. The genetic screening for the ARID1a mutation is a standard part of the commercially available screening panels being utilized in the clinic for cancer patients.

The ongoing Phase 1 study of NXP800 is comprised of two parts: dose-escalation Phase 1a, initiated in December 2021, to be followed by an expansion Phase 1b. In the Phase 1a, the safety and tolerability of NXP800 is being evaluated in patients with advanced solid tumors to identify a dose and dosing schedule for the Phase 1b. In the Phase 1b, the safety and preliminary anti-tumor activity of NXP800 will be evaluated, initially in patients with OCCC and endometrioid carcinoma and possibly in patients with other types of solid tumors. Additional preclinical studies are currently being conducted to identify development opportunities for NXP800 in additional solid tumor types.

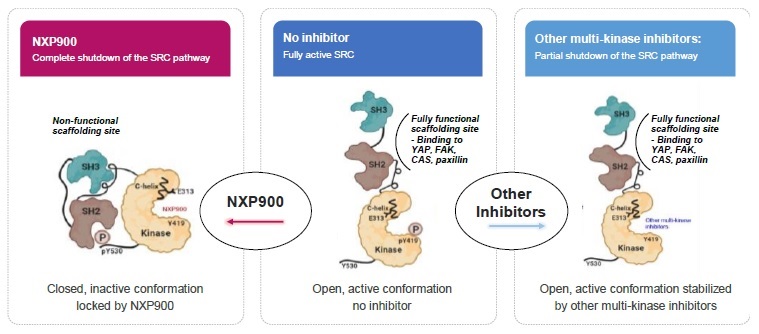

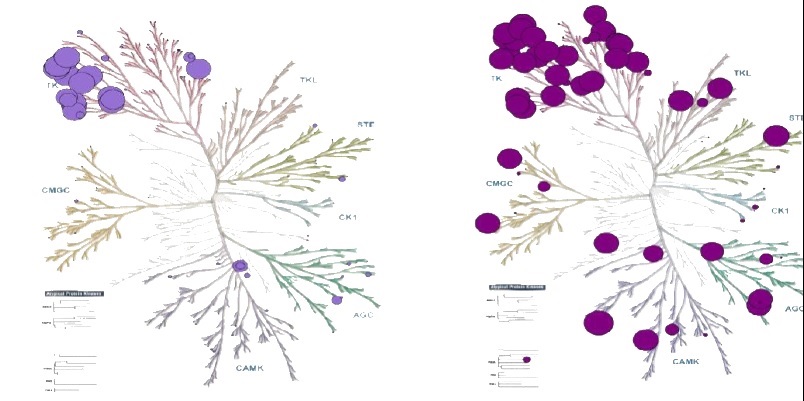

NXP900

NXP900 is a preclinical-stage drug candidate designed to preferentially inhibit the Proto-oncogene c-Src (“SRC”) and YES1 kinases. NXP900 was discovered at the University of Edinburgh. SRC is aberrantly activated in many cancer types, including solid tumors such as breast, colon, prostate, pancreatic and ovarian, while remaining predominantly inactive in non-cancerous cells. Increased SRC activity is generally associated with late-stage cancers, metastatic potential and resistance to therapy, and correlates with poor clinical prognosis. YES1 gene amplification has been reported to be implicated in several tumors including lung, head and neck, bladder and esophageal cancers. Furthermore, it has been found that YES1 gene amplification is a key mechanism of resistance to Epidermal Growth Factor Receptor (“EGFR”) or (Human Epidermal Growth Factor Receptor 2 (“HER2”) inhibitors. A recent, peer reviewed study published in Nature Communication which was not sponsored by the Company, has shown positive effects of using NXP900 in combination with the leading EFGR inhibitor, Tagrisso, to overcome Tagrisso resistance in Tagrisso-resistant cell lines.

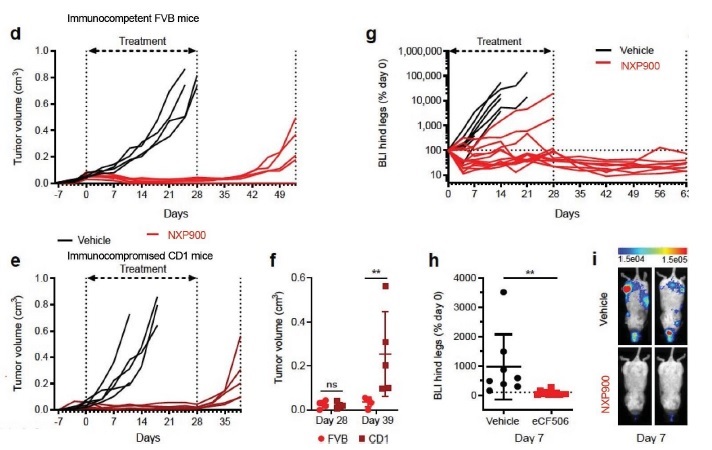

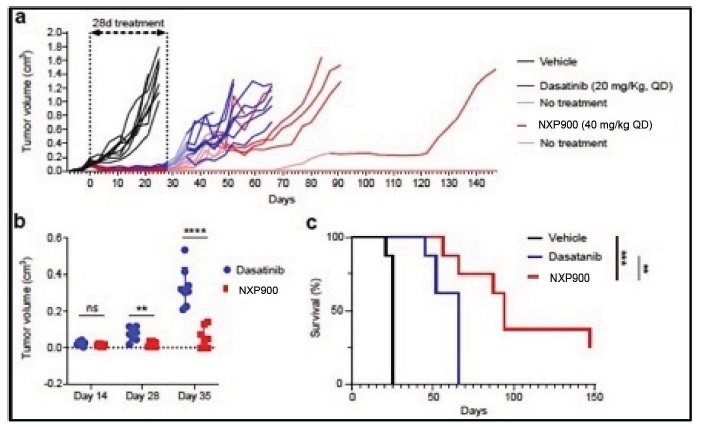

Preclinically, NXP900 has been shown to inhibit SRC and YES1 kinases and substantially inhibit growth of primary tumors and bone metastases in several triple negative breast cancer (“TNBC”) animal models.

We plan to initially develop NXP900 in solid tumors where SRC and/or YES1 are implicated. We anticipate submitting an IND or an equivalent submission with a foreign agency in early 2023.

Since our inception in 2020, we have devoted all of our efforts and financial resources to organizing and staffing our company, business planning, raising capital, acquiring, discovering product candidates and securing related intellectual property rights and conducting research and development activities for our programs. We do not have any products approved for sale and have not generated any revenue from product sales. We may never be able to develop or commercialize a marketable product. We have not yet successfully completed any pivotal clinical trials, obtained any regulatory approvals, manufactured a commercial-scale drug, or conducted sales and marketing activities.

Our Strategy

Our strategy is to build a global biopharmaceutical company through the identification, development, and commercialization of therapeutics to address unmet medical needs in oncology with an initial focus on patients with OCCC and endometrioid ovarian cancers. We intend to leverage our core competencies of target selection, drug profiling and clinical and regulatory execution to build a pipeline of product candidates targeting cancers driven by genetic alterations. The key elements driving our business strategy include:

| ➢ | establishing a leadership position in targeted oncology therapeutics, utilizing the synthetic lethality approach by inhibiting the HSF1 pathway in ARID1a-mutated cancers and/or protein deficiency as a biomarker; |

| ➢ | advancing our lead product candidate, NXP800, through clinical development towards regulatory decision-making in OCCC and endometrioid ovarian cancer; |

| ➢ | maximizing the therapeutic potential for NXP800 by leveraging in vivo preclinical data in additional ARID1a-mutated tumor types, as a monotherapy and possibly in combination with other approved therapies; |

| ➢ | positioning NXP900 as a differentiated SRC kinase inhibitor with improved activity against solid tumors compared to the existing SRC kinase inhibitors; |

| ➢ | maximizing the therapeutic potential of NXP900 by generating additional in vivo preclinical data to highlight the benefits of inhibiting YES1 on antitumor activity; |

| ➢ | deploying our proven clinical, regulatory and business development/licensing expertise to further expand our targeted oncology pipeline for patients with unmet medical needs; and |

| ➢ | evaluating opportunities to accelerate development timelines and enhancing the commercial potential of our products in collaboration with third parties, including potential ex-U.S. collaboration opportunities. |

Risk Factors

An investment in our Common Stock is subject to a broad range of risks and should only be made after a careful consideration of such risks. For a discussion of some of the risks you should consider before purchasing our Common Stock, you are urged to carefully review and consider the section entitled “Risk Factors.”

Risk Factor Summary

Our business is subject to a number of risks, including risks that may prevent us from achieving our business objectives or may adversely affect our business, financial condition, results of operations, cash flows and prospects that you should consider before making a decision to invest in our Common Stock. These risks are discussed more fully in the section titled “Risk factors” beginning on page 8, of this prospectus include the following:

| ➢ | We have a limited operating history, have not completed any clinical trials to date, have no products approved for commercial sale and have not generated any revenue, which may make it difficult for investors to evaluate our current business and likelihood of success and viability. |

| ➢ | We have incurred losses since our inception and have not generated any revenue. We expect to incur continued losses for the foreseeable future and may never achieve or maintain profitability. |

| ➢ | Our ability to generate revenue and achieve profitability depends significantly on our ability to achieve several objectives relating to the discovery or identification, development, regulatory approval and commercialization of our current or future product candidates. |

| ➢ | We will require substantial additional capital to finance our operations and achieve our goals. If we are unable to raise capital when needed or on terms acceptable to us, we may be forced to delay, reduce or eliminate our research or product development programs, any future commercialization efforts or other operations. |

| ➢ | We are substantially dependent on the success of our lead product candidate, NXP800, for which we commenced a Phase 1 clinical trial in December 2021. |

| ➢ | Clinical trials are very expensive, time consuming and difficult to design and implement, and involve uncertain outcomes. Furthermore, results of earlier preclinical studies and clinical trials may not be predictive of results of future preclinical studies or clinical trials. Our current or future product candidates may not have favorable results in later clinical trials, if any, or receive regulatory approval. |

| ➢ | If we fail to demonstrate safety and efficacy to our stakeholders, we may need to terminate development programs, our reputation may be harmed, and our business will suffer. |

| ➢ | The COVID-19 pandemic could adversely impact our business, including our clinical trials and clinical trial operations. |

| ➢ | The development and commercialization of pharmaceutical products are subject to extensive regulation, and we may not obtain regulatory approvals for NXP800, NXP900, or any future product candidate, on a timely basis or at all. |

| ➢ | The manufacture of any of our current or future product candidates is complex. Our third-party manufacturers may encounter difficulties or interruptions in production, which could delay or entirely halt their ability to supply any of our current or future product candidates for clinical trials or, if approved, for commercial sale. |

| ➢ | Our future success depends on our ability to retain our executive officers and key employees and to attract, retain and motivate qualified personnel and manage our human capital. |

| ➢ | We currently have 10 full-time employees and we will need to grow the size and capabilities of our organization, and we may experience difficulties in managing this growth. |

| ➢ | If we are unable to obtain and maintain patent protection or other necessary rights for our products and technology, or if the scope of the patent protection obtained is not sufficiently broad or our rights under licensed patents is not sufficiently broad, our competitors could develop and commercialize products and technology similar or identical to ours, and our ability to successfully commercialize our products and technology may be adversely affected. |

Corporate Information

We were incorporated in July 2020 under the laws of the State of Delaware under the name Centry Pharma, Inc., and changed our name to Nuvectis Pharma, Inc. in July 2021. Our principal executive offices are located at 1 Bridge Plaza, 2nd Floor, Fort Lee, NJ 07024, and our telephone number is (201) 614-3150. Our website address is www.nuvectis.com. The information contained in or accessible from our website is not incorporated into this prospectus, and you should not consider it part of this prospectus. We have included our website address in this prospectus solely as an inactive textual reference.

Implications of being an emerging growth company and a smaller reporting company

We qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, as amended. As an emerging growth company, we may take advantage of specified reduced disclosure and other requirements that are otherwise applicable generally to public companies. These provisions include:

| ➢ | being permitted to only two years of audited financial statements in addition to any required unaudited interim financial statements with correspondingly reduced “Management’s Discussion and Analysis of Financial Condition and Results of Operations” disclosure in this prospectus; |

| ➢ | reduced disclosure about our executive compensation arrangements; and |

| ➢ | not being required to hold advisory votes on executive compensation or to obtain stockholder approval of any golden parachute arrangements not previously approved; and an exemption from the auditor attestation requirement in the assessment of our internal control over financial reporting. |

We may take advantage of these exemptions for up to five years or such earlier time that we are no longer an emerging growth company.

We would cease to be an emerging growth company on the date that is the earliest of (i) the last day of the fiscal year in which we have total annual gross revenues of $1.07 billion or more; (ii) the last day of our fiscal year following the fifth anniversary of the date of the completion of our initial public offering; (iii) the date on which we have issued more than $1.0 billion in nonconvertible debt during the previous three years; or (iv) the date on which we are deemed to be a large accelerated filer under the rules of the Securities and Exchange Commission (“SEC”). We may choose to take advantage of some but not all of these exemptions. We have taken advantage of reduced reporting requirements in this prospectus. Accordingly, the information contained herein may be different from the information you receive from other public companies in which you hold stock.

We have elected not to “opt out” of the exemption for the delayed adoption of certain accounting standards and, therefore, we will adopt new or revised accounting standards at the time private companies adopt the new or revised accounting standard and will do so until such time that we either (i) irrevocably elect to “opt out” of such extended transition period or (ii) no longer qualify as an emerging growth company.

We are also a “smaller reporting company,” meaning that the market value of our stock held by non-affiliates is less than $700 million and our annual revenue was less than $100 million during the most recently completed fiscal year. We may continue to be a smaller reporting company after this offering if either (i) the market value of our stock held by non-affiliates is less than $250 million or (ii) our annual revenue was less than $100 million during the most recently completed fiscal year and the market value of our stock held by non-affiliates is less than $700 million. If we are a smaller reporting company at the time we cease to be an emerging growth company, we may continue to rely on exemptions from certain disclosure requirements that are available to smaller reporting companies. Specifically, as a smaller reporting company we may choose to present only the two most recent fiscal years of audited financial statements in our Annual Report on Form 10-K and, similar to emerging growth companies, smaller reporting companies have reduced disclosure obligations regarding executive compensation.

Recent Developments

Private Placement of Shares of Common Stock, Preferred Investment Options, and Pre-Funded Warrants

On July 27, 2022, we entered into definitive agreements for the issuance and sale in a private placement (the “Private Placement”) of 1,015,598 shares of its common stock, par value $0.00001 (the “Common Stock”) and pre-funded warrants to purchase up to an aggregate of 909,091 shares of Common Stock at a purchase price of $8.25 per share, referred to as the Pre-Funded Warrants. The investors in the Private Placement also received preferred investment options to purchase up to an aggregate of 1,924,689 shares of Common Stock, referred to as the Investor Investment Options. The Investor Investment Options will have an exercise price of $9.65, will become exercisable commencing six months following the date of issuance and will have a term of three and one-half years from the date of issuance.

The Private Placement closed on July 29, 2022. Gross proceeds to the Company from the Private Placement are approximately $15.9 million. The Company intends to use the net proceeds from the Private Placement for working capital and other general corporate purposes. See “Use of Proceeds.”

In connection with the Private Placement, the Company entered into a registration rights agreement (the “Registration Rights Agreement”) with the Selling Shareholders. Pursuant to the Registration Rights Agreement, the Company is required to file a resale registration statement (the “Registration Statement”) with the Securities and exchange Commission (the “SEC”) to register for resale of the Shares, the shares issuable upon exercise of the Pre-Funded Warrants and the Investment Options (as defined below) by August 15, 2022. Pursuant to the Registration Rights Agreement, the Registration Statement shall be declared effective within 45 days after July 27, 2022, or in the event of a full review by the SEC, 75 days from July 27, 2022. The Company will be obligated to pay certain liquidated damages to the investor if the Company fails to file the resale registration statement when required, fails to cause the Registration Statement to be declared effective by the SEC when required, of if the Company fails to maintain the effectiveness of the Registration Statement.

H.C. Wainwright & Co. (“Wainwright) acted as the placement agent in connection with the Private Placement. Pursuant to the engagement agreement, Wainwright was paid a cash fee equal to 7% of the gross proceeds and a management fee of 1% of the gross proceeds. The Company also paid Wainwright $85,000 for non-accountable expenses. As part of their compensation, certain designees of Wainwright received preferred investment options to purchase up to an aggregate of 115,481 shares of Common Stock, referred to as the Placement Agent Investment Options (and together with the Investor Investment Options, the “Investment Options”). The Placement Agent Investment Options have an exercise price of $10.3125, per share will become exercisable commencing six months following the date of issuance and have a term of three and one-half years from the date of issuance.

The Offering

| Shares of common stock outstanding immediately prior to the Private Placement. | | 12,717,794 |

| | | |

| Shares of common stock offered by the Selling Shareholders | | Up to 1,015,598 shares |

| | | |

| Pre-funded warrants offered by the Selling Shareholders | | Up to 909,091 pre-funded warrants |

| | | |

| Preferred investment options offered by the Selling Shareholders | | Up to 2,040,170 preferred investment options |

| | | |

| Use of proceeds | | We are not selling any securities under this prospectus and we will not receive any proceeds from the sale of shares of Common Stock by the Selling Shareholders. We will receive up to an aggregate of approximately $19,764,147 from the exercise of the preferred investment options, assuming the exercise in full of all of the preferred investment options. We will receive up to an aggregate of approximately $909 from the exercise of the pre-funded warrants. We intend to use the net proceeds of the Private Placement for working capital and general corporate purposes. See “Use of Proceeds.” |

| | | |

| Nasdaq Capital Market symbol | | “NVCT” |

| | | |

| Risk factors | | Investment in our Common Stock involves substantial risks. You should read this prospectus carefully, including the section entitled “Risk Factors” and the financial statements and the related notes to those statements included in this prospectus, before investing in our Common Stock. |

| | | |

| The number of shares of our Common Stock outstanding after the Private Placement is based on 14,642,483 shares of our Common Stock outstanding as of August 5, 2022, and excludes: |

| ➢ | 296,590 shares of Common Stock issuable upon exercise of options outstanding under our 2021 Global Equity Incentive Plan as amended and restated (the “2021 Plan”), at a weighted average exercise price of $3.99 per share as of June 30, 2022; |

| ➢ | 228,893 shares of Common Stock issuable upon the exercise of warrants under the 2021 Plan to purchase Common Stock and underwriter warrants associated with the 2022 IPO at a weighted exercise price of $3.41 per share as of June 30, 2022; |

| ➢ | 193,557 shares of restricted stock granted to the Company’s three founders on July 27, 2021; |

| ➢ | 349,580 shares of restricted stock issued under the 2021 Plan; |

| ➢ | 752,937 shares of Common Stock to be reserved for future issuance under the 2021 Plan; and |

| ➢ | 2,040,170 shares of Common Stock issuable upon the exercise of the Investment Options. |

Special Note Regarding Forward-looking Statements

Certain matters discussed in this report may constitute forward-looking statements for purposes of the Securities Act of 1933, as amended (the “Securities Act”) and the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from the future results, performance or achievements expressed or implied by such forward-looking statements. The words “may,” “will,” “should,” “expect,” “plan,” “anticipate,” “could,” “intend,” “target,” “project,” “contemplate,” “believe,” “estimate,” “predict,” “would,” “potential,” “continue,” “anticipate,” “believe,” “estimate,” “may,” “expect” and similar expressions are generally intended to identify forward-looking statements. These forward-looking statements are based on management’s current expectations and assumptions about future events, which are inherently subject to uncertainties, risks and changes in circumstances that are difficult to predict.

Our actual results may differ materially from the results anticipated in these forward-looking statements due to a variety of factors, including, without limitation, those discussed under the captions “Risk Factors,” and elsewhere in this report. All written or oral forward-looking statements attributable to us are expressly qualified in their entirety by these cautionary statements. Such forward-looking statements include, but are not limited to, statements about:

| ⮚ | our expectations for increases or decreases in expenses; |

| ⮚ | the success and timing of our clinical trials and preclinical studies, including safety and efficacy of our product candidates, patient accrual, unexpected or expected safety events, and the usability of data generated from our trials; |

| ➢ | expectations for incurring capital expenditures to expand our research and development and manufacturing capabilities; |

| ➢ | estimates of the sufficiency of our existing cash and cash equivalents and investments to finance our operating requirements, including expectations regarding the value and liquidity of our investments; |

| ➢ | expectations for generating revenue or becoming profitable on a sustained basis; |

| ➢ | the impact of health epidemics, including the COVID-19 pandemic, on our business and the actions we may take in response thereto; |

| ➢ | developments and projections relating to our competitors and industry; |

| ➢ | our expectations about how market trends will affect our business; |

| ➢ | our and our licensors’ ability to obtain, establish, maintain, protect and enforce intellectual property and proprietary protection for our products and technologies and to avoid claims of infringement, misappropriation or other violation of third-party intellectual property and proprietary rights; |

| ➢ | our ability to attract and retain key personnel and to manage our future growth effectively; |

| ➢ | expectations for future capital requirements; |

| ➢ | the volatility of the trading price of our Common Stock; and |

| ➢ | our expectations regarding the period during which we qualify as an emerging growth company under the Jumpstart Our Business Startups Act. |

We have based the forward-looking statements contained in this prospectus primarily on our current expectations and projections about future events and trends that we believe may affect our business, financial condition, results of operations, prospects, business strategy and financial needs. The outcome of the events described in these forward-looking statements is subject to risks, uncertainties, assumptions and other factors described in the section captioned “Risk Factors” and elsewhere in this prospectus. These risks are not exhaustive. Other sections of this prospectus include additional factors that could adversely impact our business and financial performance. Furthermore, new risks and uncertainties emerge from time to time and it is not possible for us to predict all risks and uncertainties that could have an impact on the forward- looking statements contained in this prospectus. We cannot assure you that the results, events and circumstances reflected in the forward-looking statements will be achieved or occur, and actual results, events or circumstances could differ materially from those described in the forward-looking statements. You should, however, review the factors and risks and other information we describe in the reports we will file from time to time with the SEC after the date of this prospectus. See “Where You Can Find More Information.”

In addition, statements that “we believe” and similar statements reflect our beliefs and opinions on the relevant subject. These statements are based upon information available to us as of the date of this prospectus, and while we believe such information forms a reasonable basis for such statements, such information may be limited or incomplete, and our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all potentially available relevant information. These statements are inherently uncertain and investors are cautioned not to unduly rely upon these statements.

You should read this prospectus and the documents that we reference in this prospectus and have filed as exhibits to the registration statement of which this prospectus forms a part with the understanding that our actual future results, levels of activity, performance and achievements may be materially different from what we expect. We qualify all of our forward-looking statements by these cautionary statements.

The forward-looking statements made in this prospectus relate only to events as of the date on which such statements are made. We undertake no obligation to update any forward-looking statements after the date of this prospectus or to conform such statements to actual results or revised expectations, except as required by law.

Risk Factors

Risk Factors

Investing in our Common Stock involves a high degree of risk. You should consider carefully the risks and uncertainties described below, together with all of the other information in this prospectus, including the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our financial statements and related notes, before making a decision to invest in our Common Stock. Our business, results of operations, financial condition and prospects could also be harmed by risks and uncertainties that are not presently known to us or that we currently believe are not material. If any of the risks actually occur, our business, platform, reputation, brand, results of operations, financial condition and prospects could be materially and adversely affected. In such event, the market price of our Common Stock could decline, and you could lose all or part of your investment.

Risks Related to Our Finances and Capital Requirements

Our limited operating history may make it difficult for you to evaluate the success of our business to date and to assess our future viability.

We are a clinical stage biopharmaceutical company with a limited operating history. We were incorporated in Delaware in July 2020 and commenced operations in May 2021. Our operations to date have been limited to organizing and staffing our company, business planning, raising capital, identifying, investigating, licensing and evaluating potential product candidates, and establishing arrangements with third parties for the manufacture of initial quantities of our lead product candidate and component materials. Our lead product candidate is in early clinical development, and our second drug candidate is in preclinical development. We have not yet demonstrated our ability to successfully initiate, conduct or complete any clinical trials, obtain marketing approvals, manufacture a commercial-scale product or arrange for a third party to do so on our behalf, or conduct sales, marketing and distribution activities necessary for successful product commercialization. Consequently, any predictions about our future success or viability may not be as accurate.

We will need to transition at some point from a company with a research and development focus to a company capable of supporting commercial activities related to the full product life cycle. We may not be successful in such a transition.

We have incurred losses since inception and anticipate that we will continue to incur losses for the foreseeable future. We may never achieve or maintain profitability.

Investment in biopharmaceutical product development is a highly speculative undertaking and entails substantial upfront capital expenditures and significant risk that our current or potential future product candidates will fail to demonstrate adequate efficacy or an acceptable safety profile, gain regulatory approval and become commercially viable. We are still in the early stages of development of our product candidates and initiated our first clinical trial in December 2021. We have no products approved for commercial sale and have not generated any revenue from product sales to date. We continue to incur significant research and development and other expenses related to our ongoing operations. In addition, as a business with a limited operating history, we may encounter unforeseen expenses, difficulties, complications, delays and other known and unknown factors, such as the COVID-19 pandemic.

We have incurred losses in each period since we commenced operations. Since inception through the end of June 30, 2022, we had an accumulated deficit of $19.4 million. Those losses mainly include the following: (1), $6.3 million in research and development expenses excluding licensing agreements, (2) in connection with the exclusive licensing agreement related to our lead product candidate, NXP800, we paid an upfront payment of $3.5 million, and (3) in connection with the exclusive licensing agreement related to NXP900, we also paid an upfront payment of $3.5 million. We expect to continue to incur significant losses for the foreseeable future, and we expect these losses to increase substantially if and as we continue our research and development efforts and submit IND applications for our lead product candidate; conduct preclinical studies and clinical trials for our current and future product candidates; seek marketing approvals for any current or future product candidate that successfully completes clinical trials; experience any delays or encounter any issues with any of the above; establish a sales, marketing and distribution infrastructure and scale-up manufacturing capabilities to commercialize any current or future product candidates for which we may obtain regulatory approval; obtain, expand, maintain, enforce and protect our intellectual property portfolio; hire additional clinical, regulatory and scientific personnel; and operate as a public company.

Risk Factors

Our lead product candidate, NXP800, is in clinical development and our second product candidate, NXP900, is in the preclinical stage of development. Both product candidates will require additional preclinical studies, clinical development, regulatory review and approval, substantial investment, access to sufficient clinical and commercial manufacturing capacity and significant marketing efforts before we can generate any revenue from product sales. The Phase 1 study for NXP800 started in December 2021 and NXP900 has yet to enter clinical trials. To date, we have not generated any revenue from our product candidates. Our ability to generate revenue will depend on a number of factors, including, but not limited to:

| ➢ | the timely completion of our preclinical studies and clinical trials, which may be significantly slower or more costly than anticipated and will depend upon the performance of third-party contractors; |

| ➢ | successful submissions of IND applications to the FDA and any additional comparable applications; |

| ➢ | completion of IND enabling studies necessary for the IND or comparable submission, as appropriate; |

| ➢ | whether we are required by the FDA or similar foreign regulatory authorities to conduct additional clinical trials or other studies to support the approval and commercialization of our current or future product candidates; |

| ➢ | the FDA’s and similar foreign regulatory authorities’ acceptance of the safety, potency, purity, efficacy and risk to benefit profile of our current or future product candidates; |

| ➢ | the prevalence, duration and severity of potential side effects or other safety issues experienced with our current or future product candidates, if any; |

| ➢ | the timely receipt of necessary marketing approvals from the FDA and similar foreign regulatory authorities; |

| ➢ | the actual and perceived availability, cost, risk profile and safety and efficacy of our current or future product candidates, if approved, relative to existing and future alternative cancer therapies and competitive product candidates and technologies; |

| ➢ | our ability and the ability of third parties with whom we contract to manufacture adequate clinical and commercial supplies of our current or future product candidates, to remain in good standing with regulatory authorities and to develop, validate and maintain commercially viable manufacturing processes that are compliant with cGMP; |

| ➢ | our ability to successfully develop a commercial strategy and to commercialize any current or future product candidate in the United States and internationally, if approved for marketing, reimbursement, sale and distribution in such countries and territories, whether alone or in collaboration with others; |

| ➢ | patient demand for our current or future product candidates, if approved; and |

| ➢ | our ability to establish and enforce intellectual property rights in and to our current or future product candidates. |

Many of the factors listed above are beyond our control and could cause us to experience significant delays or prevent us from obtaining regulatory approvals or commercializing our current and future product candidates. Even if we can commercialize any current or future product candidates, we may not achieve profitability soon after generating product sales, if ever.

Risk Factors

We will require substantial additional funding. Raising additional capital may cause dilution to our existing stockholders, or require us to relinquish proprietary rights. If we are unable to raise capital as needed, we may be compelled to delay, reduce or eliminate our product development programs or commercialization efforts.

We expect our expenses to increase in parallel with our ongoing activities, particularly as we continue our discovery and preclinical development activities to identify new product candidates and initiate clinical trials of, and seek marketing approval for, any of our current or future product candidates. In addition, if we obtain marketing approval for any of our current or future product candidates, we expect to incur significant commercialization expenses related to product sales, marketing, manufacturing, and distribution. Furthermore, we expect to incur significant additional costs associated with operating as a public company. Accordingly, we will need to obtain substantial additional funding in connection with our continuing operations. We cannot be certain that additional funding will be available on acceptable terms, or at all. Until such time, if ever, as we can generate substantial product revenue, we expect to finance our operations through a combination of public or private equity offerings, debt financings, governmental funding, collaborations, strategic partnerships and alliances or marketing, distribution or licensing arrangements with third parties. To the extent that we raise additional capital through the sale of equity or convertible debt securities, your ownership interest will be diluted, and the terms of these securities may include liquidation or other preferences that adversely affect your rights as a stockholder. Debt financing and preferred equity financing, if available, may involve agreements that include covenants limiting or restricting our ability to take specific actions, such as incurring additional debt, making capital expenditures or declaring dividends.

If we raise additional funds through collaborations, strategic alliances or marketing, distribution or licensing arrangements with third parties, we may have to relinquish valuable rights to our technologies, future revenue streams, research programs or product candidates or grant licenses on terms that may not be favorable to us.

If we are unable to raise capital when needed or on attractive terms, we could be forced to delay, reduce or eliminate our discovery and preclinical development programs or any future commercialization efforts.

Major public health issues, and specifically the pandemic caused by the coronavirus COVID-19 outbreak, could have an adverse effect on our clinical trials, financial condition, results of operations, and other aspects of our business.

In March 2020, the World Health Organization declared the outbreak of COVID-19 to be a pandemic. The COVID-19 pandemic is having widespread, rapidly evolving, and unpredictable impacts on global society, economies, financial markets, and business practices. During 2021, there was a wide distribution of several vaccinations and medicines to overcome the pandemic. We have shifted our operations to co-exist along with the pandemic, including encouragement of vaccinations to all of our employees worldwide.

The uncertainty to which the COVID-19 pandemic impacts the Company’s business, affects management’s judgment and assumptions relating to accounting estimates in a variety of areas that depend on these estimates and assumptions. COVID-19 did not have a material influence on these estimates and judgements since the Company began operations in 2021.

The Company continues to face relative uncertainty as to the remaining intensity and duration of and the nature and timeline for recovery from the COVID-19 pandemic going forward and how all of that impacts the Company, including the extent to which potentially permanent changes clinical trial operations have been caused by the pandemic. The Company has taken the approach of managing the pandemic (to the extent that it continues to remain a significant factor) via strengthening its balance sheet and cash assets and avoiding debt while focusing on cost controls. Some factors from the COVID-19 outbreak or any outbreak caused by any variant of COVID-19 that may delay or otherwise adversely affect our clinical trial programs, as well as adversely impact our business generally, include:

| ➢ | delays or difficulties in clinical site initiation, including difficulties in recruiting clinical sites, and delays enrolling patients in our clinical trials or increased rates of patients withdrawing from our clinical trials following enrollment as a result of contracting COVID-19, being forced to quarantine, or not otherwise being able to complete study assessments, particularly for older patients or others with a higher risk of contracting COVID-19; |

Risk Factors

| ➢ | diversion of healthcare resources, including clinical trial investigators and staff, away from the conduct of clinical trials to focus on pandemic concerns which could result in delays to our partner companies’ clinical trials; |

| ➢ | limitations on travel, including limitations on domestic and international travel, and government-imposed quarantines or restrictions imposed by key third parties that could interrupt key trial activities, such as clinical trial site initiations and monitoring; |

| ➢ | interruption of, or delays in receiving, supplies of our product candidates from our contract manufacturing organizations due to staffing shortages, or production slowdowns or stoppages; |

| ➢ | disruptions and delays caused by potential workplace, laboratory and office closures and an increased reliance on employees working from home across the healthcare system; and |

| ➢ | disruptions in or delays to regulatory approvals, inspections, reviews or other regulatory activities as a result of the spread of COVID-19 affecting the operations of the FDA or other regulatory authorities. |

We currently rely on third parties for certain functions or services in support of our clinical trials and key areas of our operations. If these third parties themselves are adversely impacted by restrictions resulting from the COVID-19 outbreak, we will likely experience delays and/or realize additional costs. As a result, our ability to commence and complete clinical trials in timely fashion, obtain regulatory approvals for, and to commercialize, our current and future product candidates may be delayed or disrupted.

Risks Related to the Development of our Product Candidates

Our discovery and preclinical development approach focuses on the development of precision medicines for patients with genetically defined cancers and may never lead to marketable products.

The patient populations for our product candidates and potential future product candidates are limited to those with specific target mutations and may not be completely defined but are substantially smaller than the general treated cancer population and we will need to screen and identify these patients with the targeted mutations. Successful identification of patients is dependent on several factors, including achieving certainty as to how specific genetic alterations respond to our current product candidates or any future product candidate and, if necessary, developing companion diagnostics to identify such genetic alterations. Furthermore, even if we are successful in identifying patients, we cannot be certain that the resulting patient populations for each mutation will be large enough to allow us to successfully obtain approval for each mutation type and commercialize our products and achieve profitability. In addition, even if our approach is successful in showing clinical benefit by downregulating the HSF1 pathway in tumors harboring an ARID1a mutation or alteration, we may never successfully identify additional oncogenic mutations for other genes. We do not know if our approach of treating patients with genetically defined cancers will be successful; and if our approach is unsuccessful, our business will suffer.

We are very early in our development efforts and are substantially dependent on our lead product candidate, NXP800. If we are unable to advance NXP800, NXP900 or any of our other future product candidates through preclinical and clinical development, obtain regulatory approval and ultimately commercialize NXP800, NXP900 or any of our other future product candidates, or experience significant delays in doing so, our business will be materially harmed.

NXP800, our lead product candidate, only recently started to be tested in human subjects. Our ability to generate product revenues will depend heavily on the successful clinical development and eventual commercialization of NXP800 or future product candidates. Our second drug candidate, NXP900, has begun IND-enabling studies or similar studies required by a foreign regulatory agency. Depending on the results of these IND-enabling studies, we may not be able to submit an IND application with the FDA or a similar submission with a foreign regulatory agency and, therefore, may not be able to conduct clinical trials for NXP900. In addition, our drug development programs may contemplate the development of companion diagnostics, which are assays or tests to identify an appropriate patient population. Companion diagnostics are subject to regulation as medical devices and must themselves receive marketing authorization from the FDA or certain other foreign regulatory agencies before they may be marketed. If a companion diagnostic is essential to the safe and effective use of any of our current and future product candidates, the FDA must conclude that the companion diagnostic meets the applicable standard for safety and effectiveness or for substantial equivalence for use with our product candidates before either the product candidates or companion diagnostic may be marketed in the United States.

Risk Factors

Negative results in the development of our lead product candidate may also prevent or delay our ability to continue or conduct clinical programs or receive regulatory approvals for our other future product candidates. For example, although we believe, based on preclinical studies of OCCC models that demonstrated tumor growth inhibition, that this cancer type might be particularly sensitive to NXP800, this may not prove true in clinical testing for any or all of the target indications. Moreover, anti-tumor activity may be different in each tumor type that we plan to evaluate in clinical trials. Therefore, even though we plan to potentially pursue tumor-agnostic clinical development of NXP800, the tumor response may be low in patients with some cancers compared to others. As a result, we may be required to discontinue development of NXP800 for patients with those tumor types and/or mutations due to insufficient clinical benefit, while continuing development in a more limited population of patients. Consequently, in order to obtain regulatory approval, we may have to reach agreement with the FDA on defining the optimal patient population, study design and size, any of which may require significant additional resources and delay our clinical trials and ultimately the approval, if any, of any of our other future product candidates.

We may experience setbacks that could delay or prevent regulatory approval of, or our ability to commercialize, our current or future product candidates, including:

| ➢ | negative or inconclusive results from our preclinical studies or clinical trials or positive results from the clinical trials of others for product candidates similar to ours leading to their approval, and evolving to a decision or requirement to conduct additional preclinical testing or clinical trials or abandon a program; |

| ➢ | product-related side effects experienced by patients or subjects in our clinical trials or by individuals using drugs or therapeutics that we, the FDA, other regulators or others view as relevant to the development of our current or future product candidates; |

| ➢ | delays in submitting IND applications or comparable foreign applications or delays or failure in obtaining the necessary approvals from regulators to commence a clinical trial, or a suspension or termination of a clinical trial once commenced; |

| ➢ | conditions imposed by the FDA or comparable foreign authorities regarding the scope or design of our clinical trials, including our clinical endpoints; |

| ➢ | delays in enrolling subjects in clinical trials, including due to the COVID-19 pandemic, and completion of clinical trials, including under GCP or good laboratory practice (“GLP”) requirements; |

| ➢ | inability to maintain compliance with regulatory requirements, including cGMPs, and complying effectively with other requirements pertaining to the quality of our current or future product candidates; |

| ➢ | high drop-out rates of subjects from clinical trials; |

| ➢ | inadequate supply or quality of our current or future product candidates or other materials necessary for the conduct of our clinical trials; |

| ➢ | greater than anticipated clinical trial costs; |

| ➢ | inability to compete with other therapies; |

| ➢ | poor efficacy of our current or future product candidates during clinical trials; |

Risk Factors

| ➢ | trial results taking longer than anticipated; |

| ➢ | trials being subjected to fraud or data capture failure or other technical mishaps leading to the invalidation of our trials; |

| ➢ | the results of our trials not supporting application for conditional approval in the European Union; |

| ➢ | unfavorable FDA or other regulatory agency inspection and review of a clinical trial site; |

| ➢ | failure of our third-party contractors or investigators to comply with regulatory requirements or otherwise meet their contractual obligations in a timely manner, or at all; |

| ➢ | delays related to the impact of the spread of the COVID-19 pandemic, including the impact of COVID-19 on the FDA’s ability to continue its normal operations; |

| ➢ | delays and changes in regulatory requirements, policy and guidelines, including the imposition of additional regulatory oversight around clinical development generally or with respect to our technology in particular; or |

| ➢ | varying interpretations of data by the FDA and similar foreign regulatory agencies. |

In addition, because we have limited financial and personnel resources and are focusing primarily on developing our lead product candidate, we may forgo or delay pursuit of other future product candidates that may prove to have greater commercial potential and may fail to capitalize on viable commercial products or profitable market opportunities. If we do not accurately evaluate the commercial potential or target market for a future product candidate, we may relinquish valuable rights to those future product candidates through collaboration, licensing, or other royalty arrangements in cases in which it would have been more advantageous for us to retain sole development and commercialization rights to such future product candidates.

Clinical drug development involves a lengthy and expensive process with uncertain outcomes, clinical trials are difficult to design and implement, and any of our clinical trials could produce unsuccessful results or fail at any stage in the process.

Clinical trials conducted on humans are expensive and can take many years to complete, and outcomes are inherently uncertain. Failure can occur at any time during the process. Additionally, any positive results of preclinical studies and early clinical trials of a drug candidate may not be predictive of the results of later-stage clinical trials, such that drug candidates may reach later stages of clinical trials and fail to show the desired safety and efficacy traits despite having shown indications of those traits in preclinical studies and early-stage clinical trials. A number of companies in the pharmaceutical industry have suffered significant setbacks in advanced clinical trials due to lack of efficacy or adverse safety profiles, notwithstanding promising results in preclinical studies or earlier phases of clinical trials. Therefore, the results of any future clinical trials we conduct may not be successful.

Clinical trials may be delayed, suspended or prematurely terminated because costs are greater than we anticipate or for a variety of reasons, such as:

| ➢ | delay or failure in reaching agreement with the FDA or a comparable foreign regulatory authority on a trial design that we are able to execute; |

Risk Factors

| ➢ | delay or failure in obtaining authorization to commence a trial, including approval from the appropriate independent review board (“IRB”) to conduct testing of a candidate on human subjects, or inability to comply with conditions imposed by a regulatory authority regarding the scope or design of a clinical trial; |

| ➢ | delay in reaching, or failure to reach, agreement on acceptable terms with prospective CROs and clinical trial sites, the terms of which can be subject to extensive negotiation and may vary significantly among different CROs and trial sites; |

| ➢ | inability, delay or failure in identifying and maintaining a sufficient number of trial sites, many of which may already be engaged in other clinical programs; |

| ➢ | delay or failure in recruiting and enrolling suitable volunteers or patients to participate in a trial; |

| ➢ | delay or failure in developing and validating companion diagnostics, if they are deemed necessary, on a timely basis; |

| ➢ | failure of patients to complete a trial or return for post-treatment follow-up; |

| ➢ | inability to monitor patients adequately during or after treatment; |

| ➢ | clinical sites and investigators deviating from trial protocols, failing to conduct the trial in accordance with regulatory requirements or dropping out of a trial; |

| ➢ | failure to initiate or delay of or inability to complete a clinical trial as a result of a clinical hold imposed by the FDA or comparable foreign regulatory authority due to observed safety findings or other reasons; |

| ➢ | negative or inconclusive results in our clinical trials, and our decision to or regulators’ requirement that we conduct additional preclinical studies, clinical trials or that we abandon one or more of our product development programs; or |

| ➢ | inability to manufacture sufficient quantities of a drug candidate of acceptable quality for use in clinical trials. |

We rely and plan to continue to rely on CROs, contract manufacturing organizations (“CMOs”) and clinical trial sites to ensure the proper and timely conduct of our clinical trials. Although we have and expect that we will have agreements in place with CROs and CMOs governing their contracted activities and conduct, we will have limited influence over their actual performance. As a result, we ultimately do not and will not have control over a CRO’s or CMO’s compliance with the terms of any agreement it may have with us, its compliance with applicable regulatory requirements, or its adherence to agreed-upon time schedules and deadlines, and a future CRO or CMO’s failure to perform those obligations could subject any of our clinical trials to delays or failure.

Further, we may also encounter delays if a clinical trial is suspended or terminated by us, by any IRB or ethics committee, by a Data Safety Monitoring Board, or by the FDA or European Medicines Agency (“EMA”), or other regulatory authority. A suspension or termination may be due to a number of factors, including failure to conduct the clinical trial in accordance with regulatory requirements, inspection of the clinical trial operations or trial site by the FDA, EMA or other regulatory authorities, exposing participants to health risks caused by unforeseen safety issues or adverse side effects, development of previously unseen safety issues, failure to demonstrate a benefit from using a drug candidate, or changes in governmental regulations or administrative actions. Therefore, we cannot predict with any certainty the schedule for commencement or completion of any currently ongoing, planned or future clinical trials.

Many of the factors that cause, or lead to, a delay in the commencement or completion of clinical trials may also ultimately lead to the denial of marketing approval for our current or future product candidates.

If we experience delays in the commencement or completion of, or suspension or termination of, any clinical trial for our drug candidates, the commercial prospects of the drug candidate could be harmed, and our ability to generate product revenues from the drug candidate may be delayed or eliminated. In addition, any delays in completing our clinical trials will increase our costs, slow down our drug candidate development and approval process and jeopardize regulatory approval of our drug candidates and our ability to commence sales and generate revenues.

Risk Factors

The occurrence of any of these events could harm our business, financial condition, results of operations and prospects significantly.

Difficulty in enrolling patients could delay or prevent clinical trials of our current or future product candidates.

Identifying and qualifying patients to participate in clinical studies of our current or future product candidates is critical to our success. The timing of completion of our clinical studies depends in part on the speed at which we can recruit patients to participate in testing our current or future product candidates and we may experience delays in our clinical trials if we encounter difficulties in enrollment. Further, because we are focused on patients with specific indications and genetic mutations, our ability to enroll eligible patients may be limited and may result in slower enrollment than we anticipate. Our clinical trials will compete with other clinical trials for current or future product candidates that are in the same therapeutic areas as our current or future product candidates, which may reduce the number and types of patients available to us.

Clinical trials may be subject to delays as a result of patient enrollment taking longer than anticipated or greater than anticipated subject withdrawal. We may not be able to initiate or continue clinical trials for our current or future product candidates if we are unable to locate and enroll a sufficient number of eligible patients to participate in these trials as required by the FDA or foreign regulatory authorities. We cannot predict how successful we will be at enrolling subjects in future clinical trials. The enrollment of patients depends on many factors, including:

| ➢ | patient eligibility and exclusion criteria defined in the protocol; |

| ➢ | the size of the patient population required for analysis of the clinical trial’s primary endpoints and the process for identifying patients; |

| ➢ | potential disruptions caused by the COVID-19 pandemic, including difficulties in initiating clinical sites, enrolling and retaining participants, diversion of health care resources away from clinical trials, travel or quarantine policies that may be implemented, and other factors; |

| ➢ | the proximity of patients to clinical trial sites; |

| ➢ | the design of the trial; |

| ➢ | our ability to recruit clinical trial investigators with the appropriate competencies and expertise; |

| ➢ | clinicians’ and patients’ perceptions as to the potential advantages and risks of the product candidate being studied in relation to other available therapies, including any new products that may be approved for the indications we are investigating; |

| ➢ | the availability of competing commercially available therapies and other competing product candidates’ clinical trials; |

| ➢ | our ability to obtain and maintain clinical trial subject informed consents; and |

| ➢ | the risk that subjects enrolled in clinical trials will drop out of the trials before completion. |

If we are unable to locate and enroll sufficient eligible patients to participate, as required by the FDA or similar regulatory authorities, we may be unable to initiate or continue clinical trials for our current or future product candidates. If necessary, we intend to engage third parties to develop companion diagnostics for use in our clinical trials. If such third parties are unsuccessful, our difficulty in identifying patients with the targeted genetic mutations for our clinical trials would be increased. If we are unable to include patients with the targeted genetic mutations or patients with well-defined serious unmet medical needs, we may be unable to participate in the FDA’s expedited review and development programs, including breakthrough therapy designation and fast track designation, or otherwise seek to accelerate clinical development and regulatory timelines.

Risk Factors

Our preclinical studies and clinical trials may fail to demonstrate adequately the safety, potency, purity, efficacy or any other necessary pharmacological properties of any of our current or future product candidates, which would prevent or delay development, regulatory approval and commercialization.

Before obtaining regulatory approvals for the commercial sale of our current or future product candidates, including NXP800 and NXP900, we must demonstrate through lengthy, complex and expensive preclinical studies and clinical trials that our current or future product candidates are both safe and effective for use in each target indication. Preclinical and clinical testing is expensive and can take many years to complete, and its outcome is inherently uncertain. Failure can occur at any time during the preclinical study and clinical trial processes, and, because our current product candidates are in an early stage of development, there is a high risk of failure.

The results of preclinical studies and early clinical trials of our current or future product candidates may not be predictive of the results of later-stage clinical trials. Although product candidates may demonstrate promising results in preclinical studies and early clinical trials, they may not prove to be effective in subsequent clinical trials. Additionally, while we initiated the first clinical trial for NXP800 in December 2021, clinical trials for any of our current or future product candidates, as is the case with all oncology drugs, it is likely that there may be side effects associated with their use. Results of our trials could reveal a high and unacceptable severity and prevalence of these or other side effects. In such an event, our trials could be suspended or terminated, and the FDA or comparable foreign regulatory authorities could order us to halt or cease further development of or deny approval of our current or future product candidates for any or all targeted indications. Drug-related side effects could also affect patient recruitment into the study or patient willingness to remain in the study and therefore affect our ability to complete clinical trials. Drug-related side effects could also result in potential product liability claims. Any of these occurrences may harm our business, financial condition and prospects significantly.

The FDA and comparable foreign regulatory authorities may not accept data from any preclinical or clinical trials we may conduct in foreign countries.

The FDA’s acceptance of data generated for patients recruited outside the United States from clinical trials conducted in whole or in part outside the United States may be subject to certain conditions, if accepted at all.

Although the FDA has the authority to accept foreign data as part or even the sole basis for marketing approval, the FDA generally does not approve an application on the basis of foreign data alone unless (i) the data is applicable to the U.S. population and U.S. medical practice, (ii) the trials were performed by clinical investigators of recognized competence and pursuant to GCP regulations, and (iii) the FDA’s clinical trial requirements were met. Many foreign regulatory authorities have similar approval requirements. In addition, any clinical study conducted in whole or in part outside of the United States would be subject to the applicable local laws of the jurisdiction where the trial was conducted. We cannot guarantee that the FDA or comparable foreign regulatory authority will accept data from trials conducted in whole or in part outside of the United States, which may result in the need for additional trials.

We may not be able to submit IND applications to commence additional clinical trials on the timelines we expect, and even if we are able to, the FDA may not permit us to proceed.

Our CTA and IND for NXP800 with the MHRA and the FDA, respectively have been approved. However, if we experience manufacturing delays or any other delays, we may be unable to file additional CTAs, IND applications or other clinical research authorizations for other product candidates on our expected timelines. Moreover, while we have obtained CTA and IND approvals, we cannot be sure that issues will not arise that suspend or terminate such clinical trials. Any failure to file CTAs, IND applications or other clinical research authorizations will adversely impact our expected timelines to obtain regulatory acceptance for the commencement of our trials and may prevent us from completing our clinical trials or commercializing our products on a timely basis, if at all.

We currently have no marketing and sales organization and have limited experience in marketing products. If we are unable to establish marketing and sales capabilities or enter into agreements with third parties to market and sell any approved product candidates, we may not be able to generate product revenue.

We will have to compete with other pharmaceutical and biotechnology companies to recruit, hire, train and retain marketing and sales personnel. If we are unable or decide not to establish internal sales, marketing, and distribution capabilities, we may pursue arrangements with third-party sales, marketing, and distribution collaborators regarding the sales and marketing of our products, if approved.

Risk Factors

There can be no assurance that we will be able to develop in-house sales and distribution capabilities or establish or maintain relationships with third-party collaborators to commercialize any product in the United States or overseas.

We face substantial competition, which may result in others discovering, developing or commercializing products before or more successfully than we do.

While we believe that our scientific knowledge, technology, and development expertise provide us with competitive advantages, we face potential competition from many different sources, including major pharmaceuticals, specialty pharmaceuticals and biotechnology companies, academic institutions and government agencies, and public and private research institutes that conduct research, development, manufacturing, and commercialization. Many of our competitors have significantly greater financial resources and expertise in research and development, manufacturing, preclinical testing, regulatory approvals, and product marketing than we do. Our competitors may compete with us in recruiting and retaining qualified scientific and management personnel and establishing clinical trial sites and patient recruitment for clinical trials, as well as in acquiring technologies complementary to, or necessary for, our programs. As a result, our competitors may discover, develop, license, or commercialize products earlier or more successfully than we do.

If our product candidates, NXP800 and NXP900, are approved for the indications for which we are currently conducting or planning preclinical and clinical trials, they will likely compete with competitor drugs and other drugs that are currently in development. The availability of reimbursement from government and other third-party payors will also significantly affect the pricing and competitiveness of our products. Our competitors may also obtain FDA or other regulatory approval for their products more rapidly than we do, which could result in our competitors establishing a strong market position before we are able to enter the market.

Risks Related to Government Regulation