Table of Contents

As filed with the Securities and Exchange Commission on October 1, 2021

File No. 000-56320

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 2 to

FORM 10

GENERAL FORM FOR REGISTRATION OF SECURITIES

PURSUANT TO SECTION 12(b) OR 12(g) OF

THE SECURITIES EXCHANGE ACT OF 1934

AB COMMERCIAL REAL ESTATE PRIVATE DEBT FUND, LLC

(Exact name of registrant as specified in its charter)

| Delaware | 87-1137341 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

| 1345 Avenue of the Americas New York, New York | 10105 | |

| (Address of principal executive offices) | (Zip Code) | |

(212) 486-5800

(Registrant’s telephone number, including area code)

with copies to:

Ralph R. Mazzeo

Kenneth Rasamny

Michael Darby

Dechert LLP

Cira Centre

2929 Arch Street

Philadelphia, Pennsylvania 19104-2808

Securities to be registered pursuant to Section 12(b) of the Act:

Title of each class to be so registered | Name of each exchange on which each class is to be registered | |

| None | N/A |

Securities to be registered pursuant to Section 12(g) of the Act:

Limited liability company units

(Title of class)

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☐ | Smaller reporting company | ☐ | |||

| Emerging growth company | ☒ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Table of Contents

| Page | ||||||

| EXPLANATORY NOTE | 1 | |||||

| Forward-Looking Statements | 1 | |||||

| Item 1. | Business | 2 | ||||

| Item 1A. | Risk Factors | 34 | ||||

| Item 2. | Financial Information | 59 | ||||

| Item 3. | Properties | 66 | ||||

| Item 4. | Security Ownership of Certain Beneficial Owners and Management | 67 | ||||

| Item 5. | Directors and Executive Officers | 67 | ||||

| Item 6. | Executive Compensation | 67 | ||||

| Item 7. | Certain Relationships and Related Transactions, and Director Independence | 68 | ||||

| Item 8. | Legal Proceedings | 72 | ||||

| Item 9. | Market Price of and Dividends on the Registrant’s Common Equity and Related Stockholder Matters | 72 | ||||

| Item 10. | Recent Sales of Unregistered Securities | 73 | ||||

| Item 11. | Description of Registrant’s Securities to Be Registered | 73 | ||||

| Item 12. | Indemnification of Directors and Officers | 76 | ||||

| Item 13. | Financial Statements and Supplementary Data | 76 | ||||

| Item 14. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 76 | ||||

| Item 15. | Financial Statements and Exhibits | 76 | ||||

-i-

Table of Contents

AB Commercial Real Estate Private Debt Fund, LLC is filing this registration statement on Form 10 (the “Registration Statement”) to register our limited liability company units (“Units”) pursuant to Section 12(g) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). We will be subject to the registration requirements of Section 12(g) of the Exchange Act because we anticipate that our Units will be held of record by 2,000 or more persons.

In this Registration Statement, except where the context suggests otherwise, the terms “we,” “us,” “our” and the “Company” refer to AB Commercial Real Estate Private Debt Fund, LLC, a Delaware limited liability company, together with its subsidiaries. We refer to AllianceBernstein L.P., our investment adviser, as “AB” or the “Investment Manager,” and to State Street Bank and Trust Company or its affiliates, our administrator, as the “Administrator.” The term “Members” refers to holders of our Units. The term “LLC Agreement” refers to our Amended and Restated Limited Liability Company Operating Agreement.

We are an “emerging growth company,” as defined in the Jumpstart Our Business Startups Act of 2012, as amended (the “JOBS Act”). As a result, we are eligible to take advantage of certain reduced disclosure and other requirements that are otherwise applicable to public companies including, but not limited to, not being subject to the auditor attestation requirements of Section 404(b) of the Sarbanes-Oxley Act of 2002, as amended, (the “Sarbanes-Oxley Act”). See “Item 1. Business — Operating and Regulatory Structure — Emerging Growth Company Status.”

As a result of the registration of our Units pursuant to the Exchange Act, following the effectiveness of Registration Statement, we will be subject to the requirements of the Exchange Act and the rules promulgated thereunder. In particular, we will be required to file Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, and Current Reports on Form 8-K and otherwise comply with the disclosure obligations of the Exchange Act applicable to issuers filing registration statements to register a class of securities pursuant to Section 12(g) of the Exchange Act. The U.S. Securities and Exchange Commission (the “SEC”) maintains an Internet Website (http://www.sec.gov) that contains the reports mentioned in this section.

This Registration Statement contains forward-looking statements that involve substantial risks and uncertainties. Such statements involve known and unknown risks, uncertainties and other factors, and undue reliance should not be placed thereon. These forward-looking statements are not historical facts, but rather are based on current expectations, estimates and projections about the Company, our current and prospective portfolio investments, our industry, our beliefs and opinions, and our assumptions. Words such as “anticipates,” “expects,” “intends,” “plans,” “will,” “may,” “continue,” “believes,” “seeks,” “estimates,” “would,” “could,” “should,” “targets,” “projects,” “outlook,” “potential,” “predicts” and variations of these words and similar expressions are intended to identify forward-looking statements. These statements are not guarantees of future performance and are subject to risks, uncertainties and other factors, some of which are beyond our control and difficult to predict and could cause actual results to differ materially from those expressed or forecasted in the forward-looking statements, including without limitation:

| • | general economic and market conditions, particularly affecting the real estate industry; |

| • | adverse conditions in the areas where our Portfolio Investments (as defined herein) or the properties underlying such Portfolio Investments are located and local real estate conditions; |

| • | an economic downturn could disproportionately impact the investments that we intend to target, potentially causing us to experience a decrease in investment opportunities and diminished demand for capital from our Portfolio Investments; |

| • | pandemics or other serious public health events, such as the recent global outbreak of a novel strain of the coronavirus, commonly known as “COVID-19”; |

| • | a contraction of available credit and/or an inability to access the equity markets could impair our lending and investment activities; |

| • | interest rate volatility could adversely affect our results, particularly if we elect to use leverage as part of our investment strategy; |

| • | our future operating results; |

| • | our business prospects; |

| • | our contractual arrangements and relationships with third parties; |

| • | competition with other entities and our affiliates for investment opportunities; |

| • | the speculative and illiquid nature of our investments; |

| • | the use of borrowed money to finance a portion of our investments; |

| • | the adequacy of our financing sources and working capital; |

Table of Contents

| • | the loss of key personnel; |

| • | the ability of the Investment Manager to locate suitable investments for us and to monitor and administer our investments; |

| • | the ability of the Investment Manager to attract and retain highly talented professionals; |

| • | limitations imposed on our business and our ability to satisfy requirements to maintain our exclusion from registration under the Investment Company Act of 1940, as amended (the “Company Act”) or to maintain our qualification as a real estate investment trust, or REIT, for U.S. federal income tax purposes; |

| • | the effect of legal, tax and regulatory changes; and |

| • | the other risks, uncertainties and other factors we identify under “Item 1A. Risk Factors” and elsewhere in this Registration Statement. |

Although we believe that the assumptions on which these forward-looking statements are based are reasonable, any of those assumptions could prove to be inaccurate, and as a result, the forward-looking statements based on those assumptions also could be inaccurate. In light of these and other uncertainties, the inclusion of a projection or forward-looking statement in this Registration Statement should not be regarded as a representation by us that our plans and objectives will be achieved. These risks and uncertainties include those described or identified in the section entitled “Item 1A. Risk Factors” and elsewhere in this Registration Statement. These forward-looking statements apply only as of the date of this Registration Statement. Moreover, we assume no duty and do not undertake to update the forward-looking statements.

| ITEM 1. | BUSINESS |

Overview

We are a Delaware limited liability company formed on June 1, 2021 to operate as a private investment fund generally for qualified US investors. We intend to qualify and elect to be taxed as a real estate investment trust under the Internal Revenue Code of 1986, as amended (the “Code”). Our board of directors (the “Board”) will be appointed to serve the Company. However, pursuant to an investment management agreement (the “Management Agreement”) between us and the Investment Manager, the Board will delegate to the Investment Manager all rights, power, authority, discretion, duties and responsibilities in respect of the Company, including without limitation, responsibility for the investment activities of the Company and the day-to-day management and administration of the Company. The Board will remain responsible for overseeing the performance of the Investment Manager. The investment management services provided by the Investment Manager will be in accordance with our investment objectives and policies, subject to the oversight by the Board. To achieve certain tax, regulatory and/or administrative efficiencies, we may invest through or otherwise utilize one or more subsidiary investment vehicles (each, a “Subsidiary”) that are managed and/or sponsored by the Investment Manager or its affiliates. The discussion in this Registration Statement relating to investments made by us or other actions may relate to such investments or other actions made by a Subsidiary, as applicable. Our investment objective is to generate attractive risk-adjusted returns through a diversified portfolio of commercial real estate-related investments that are predominantly credit investments secured by commercial real estate located in the United States, principally through investments made pursuant to the investment program described herein.

We, directly or indirectly (including through a Subsidiary), will invest in a portfolio of primarily debt investments, or participations therein (collectively, the “Portfolio Investments”) that may include, without limitation, the following: directly originated commercial real estate mortgage loans, including senior and junior mezzanine loans, B-notes, second mortgages, other subordinated loans, (together, “Directly Originated Loans”); legacy, new issue, and single-borrower commercial mortgage backed securities (“CMBS”); commercial real estate-related securities; performing, sub-performing and non-performing loans; and net lease assets. While we intend to focus primarily on loans directly secured by commercial real estate-related assets, we will also have the flexibility, subject to compliance with the real estate investment trust (“REIT”) qualification requirements, to invest in other types of debt investments, including unsecured debt of entities that directly or indirectly own real property or real estate-related debt. We may also invest in commercial real estate-related preferred and common equity interests where doing so is in keeping with our investment objective. We retain ultimate discretion on our investment profile.

The Board

We intend to adopt our LLC Agreement on the date of the Initial Closing (as defined below). Pursuant to the LLC Agreement, the Board will be comprised of at least 3 directors but not more than 9 directors. As of the date of the Initial Closing, we expect that the following individuals will serve as directors: Matthew Bass, Peter J. Gordon, Edward Gellert and Marguerite Brogan. On the date of our Initial Closing, it is expected that each director will be an employee of, or otherwise affiliated with, the Investment Manager or its affiliates. After the Initial Closing, one or more additional or replacement directors, including persons that may be affiliated with the Investment Manager or its affiliates, may be appointed by the Board, as determined by the Board in its sole discretion.

2

Table of Contents

Pursuant to the Management Agreement, the Board will delegate to the Investment Manager all rights, power, authority, discretion, duties and responsibilities in respect of the Company, including without limitation, responsibility for the investment activities of the Company and the day-to-day management and administration of the Company. The Members have no authority or right to act on behalf of the Company in connection with any matter.

The Investment Manager

The Investment Manager is a global investment advisor that provides investment management services to both institutional and individual investors through a broad line of investment products. The Investment Manager is registered with the SEC as an investment adviser under the Investment Advisers Act of 1940, as amended (the “Advisers Act”).

Pursuant to the terms of the Management Agreement, the Board will delegate to the Investment Manager all rights, power, authority, discretion, duties and responsibilities in respect of the Company, including without limitation:

| • | managing and supervising the development of our Private Offering, as defined below, including determination of the specific terms of the Units, approval of marketing materials and negotiating and coordinating the other agreements and services related to our Private Offering; |

| • | obtaining market research and economic and statistical data in connection with the investment objectives and policies discussed herein; |

| • | identifying, sourcing, evaluating and monitoring investment opportunities consistent with the investment objectives and policies discussed herein, including but not limited to, locating, analyzing and selecting potential investments and, within the discretionary limits and authority granted to the Investment Manager by the Board, making investments in and disposing of our assets; |

| • | structuring and conducting negotiations on our behalf with respect to prospective acquisitions, purchases, sales, exchanges or other dispositions of investments, with sellers, purchasers, and other counterparties and, if applicable, their respective agents, advisors and representatives, and determining the structure and terms of such transactions; |

| • | serving as advisor with respect to decisions regarding any of our financings and hedging strategies; |

| • | engaging and supervising various service providers on our behalf (including without limitation, the Administrator and consultants and other experts); |

| • | providing accounting and administrative services, including but not limited to, the performance of administrative functions required for day to day operations; and |

| • | managing communications with Members, including written and electronic communications, and establishing technology infrastructure to assist in supporting and servicing Members. |

The above summary is provided to illustrate the material functions which the Investment Manager will perform for us, and it is not intended to include all of the services which may be provided to us.

Investment Program

Investment Objective

Our investment objective is to generate attractive risk-adjusted returns through investments primarily in loans secured by high quality commercial real estate properties located in the United States. The Investment Manager will seek to prioritize capital preservation and stable income for investors by building a portfolio of investments primarily through directly originated loans secured by high-quality commercial real estate properties, including senior mortgage loans, mezzanine loans, and B-notes. Our investment strategy also allows for the acquisition of discounted loans with room to restructure in order to improve recoverability above the price paid or achieve an enhanced income stream. To a lesser extent, the Investment Manager will invest in the following: legacy, new issue, and single-borrower CMBSs; commercial real estate-related securities; performing, sub-performing and non-performing/distressed loans; and net lease assets. While we intend to focus mainly on loans directly secured by commercial real estate-related assets, we will also have the flexibility to invest in other types of debt investments, including unsecured debt of entities that directly or indirectly own real property or real estate-related debt, and may invest in commercial real estate-related preferred and common equity interests where doing so is in keeping with the investment objective. This embedded diversification enables the Team (as defined below) to invest across real estate debt opportunities in various stages of an economic cycle, and to capitalize on dislocations in the markets over time.

3

Table of Contents

The Investment Manager

We are a Delaware limited liability company managed by AllianceBernstein L.P. (the “Investment Manager” or “AB”), a SEC registered investment adviser. The team focused on managing the Company is comprised of investment and asset management professionals from AB’s Commercial Real Estate Debt Group (collectively, the “Team”). The 16 investment professionals on the Team have significant experience across all aspects of real estate transactions and capital structures, uniquely positioning us to source, underwrite, and manage investment opportunities throughout the real estate universe.

Having spent the majority of their careers focused on investing in commercial real estate debt, the Team believes it is highly skilled at identifying attractive opportunities, structuring and negotiating creative financing solutions and proactively addressing issues that may arise with an underperforming investment to maximize value and provide downside protection for investors.

Please see key professional biographies below:

| • | Matthew Bass has served as Head of Private Alternatives and a member of the Operating Committee since 2019. As head of AB’s Private Alternatives strategic business unit, he is responsible for the leadership and strategic growth of the business, which includes all of AB’s private market investment strategies. From 2010 to 2019, Bass held various roles in the firm’s Alternatives business (including as head of Alternatives and Multi-Asset Business Development, and COO), where he was responsible for business strategy, sourcing of new investment teams, product development and capital raising. Prior to joining the firm in 2010, Bass was a program director at the US Department of the Treasury, responsible for the design and implementation of various real estate and real estate capital-markets programs pursuant to the Troubled Asset Relief Program. Before that, he was a vice president at The Blackstone Group’s GSO Capital Partners unit, where he was involved in analyzing, evaluating and executing private debt and equity investments. Bass began his career in the Financial Institutions Investment Banking Group at UBS. He holds a BS in Finance from Lehigh University. |

| • | Peter J. Gordon has served as Chief Investment Officer and Head of US Commercial Real Estate Debt (CRED) in AB’s Real Estate Debt Group since 2020. CRED oversees approximately $7.2 billion in committed capital from insurance companies, pension funds and banks, across four vintage closed-end funds and various other institutional mandates. Prior to stepping into his role as Chief Investment Officer, Gordon spent four years as a Managing Director at AB, running originations for the Commercial Real Estate Debt Platform. Prior to joining the firm in 2016, Gordon served as managing director and head of commercial real estate (CRE) whole loan originations at Angelo, Gordon & Co., a global alternative investment management firm, where he led the CRE whole loan team, responsible for sourcing, pricing, financing and structuring transactions as well as managing assets in the investment portfolio. Prior to that, Gordon was a senior member of the real estate finance and investment banking groups at both Goldman Sachs and Morgan Stanley, where he was involved in all aspects of commercial real estate lending, from originations for balance sheet and commercial mortgage-backed securities to loan structuring, syndication and securitization. Gordon holds a BS in mathematics from the University of St. Andrews in Scotland and an MBA from Columbia University. |

| • | Edward Gellert has served as a Managing Director for Real Estate Debt Investments at AB since 2018. From 2007 to 2018, Gellert was a senior portfolio manager at Avenue Capital Group, where he directed the investment activities of the Avenue Real Estate Strategy. He has approximately 32 years of real estate industry experience, including investment and portfolio management, lending, distressed-focused investing, deal sourcing and the operation and development of real estate assets. He also served as chairman, CEO and president of ACRE Realty Investors. Before joining Avenue in 2004, Gellert founded EDGE Partners, where he served as a co-managing member of joint-venture entities that developed, repositioned and owned over 1.2 million square feet of properties. Previously, he sourced and arranged distressed debt and property acquisitions for Argent Ventures and Amroc Investments and was an analyst and asset manager for BRT Realty Trust. Gellert holds a BSM from the AB Freeman School of Business at Tulane University. |

4

Table of Contents

| • | Marguerite (Midge) Brogan joined AB in 2020 as a Managing Director, with broad responsibility for finance, reporting, and asset management functions across the US Commercial Real Estate Debt platform. Previously, she managed Park Praedium, a company she founded in 2009, where she advised on workouts, recapitalizations and restructurings within commercial real estate. From 2015 to 2017, Brogan was a Managing Director for Colony NorthStar. Prior to that, she served as a Managing Director for Sabal Financial Group, and for the Global Real Estate Group at Lehman Brothers. Brogan holds a BS in business management (cum laude) from Boston College, and an MBA with concentrations in finance and real estate from The George Washington University. She is also a member of 100 Women in Finance and W/X New York Women Executives in Real Estate, and was named one of the Top 50 Women Real Estate Professionals in 2004. |

| • | David Sotolov has served as a Managing Director for Real Estate Debt Investments at AB since 2021. Prior to joining the firm in 2021, he was a managing director at Annaly Capital Management from 2018-2021, where he managed all West Coast investments for the Annaly Commercial Real Estate Group. Prior to that, Sotolov spent 11 years at iStar, most recently as executive vice president and head of West Coast Investments, focusing on senior debt, mezzanine debt and preferred equity; joint venture equity; ground-up development; and ground lease acquisitions. Prior to that, he served as a loan originator for Fremont Investment & Loan. Sotolov attended the University of California, Los Angeles. |

| • | Yanshu Li has served as Head of Asset Management for Commercial Real Estate Debt in AB’s Real Estate Group since 2019. Prior to joining AB in 2019, she managed KG Realty Investments, a value-add residential real estate investment company which she co-founded in 2013. From 2010-2013, she worked as an associate in the Commercial Real Estate Debt group at Blackstone, focusing on high-yield debt origination, structuring and asset management. From 2006 to 2009, Li was an associate in the CMBS Large Loan Group at Morgan Stanley, responsible for underwriting debt investments across all property types. Li holds a BA in economics from Princeton University. |

Market Opportunity

The Team believes that current economic conditions, combined with commercial real estate fundamentals, create a compelling opportunity to generate a significant yield premium in commercial real estate debt. The COVID-19 pandemic abruptly ended over ten years of expansion in the U.S. economy and caused significant distress in the commercial real estate markets. In 2020, commercial real estate transaction activity dropped to its lowest level in seven years with volume declining between 11%–67% year-over-year across all property types. Distress has been largely concentrated either in specific property types (i.e., hospitality, retail) and/or poorly capitalized borrowers. Commercial real estate in dense major markets has also been impacted by the pandemic, due to a combination of fear of infection and mobility of the population. While retail was undergoing a secular shift prior to the pandemic, its challenges were further amplified by COVID-19. Hospitality was impacted the fastest, as travel (domestic and international, leisure and business, group and transient) ground to a halt instantly and has just begun to recover.

As a result of these dynamics, equity values have re-set inconsistently across certain sectors in selective markets, creating compelling entry points for investors. While terms have varied by transaction in favor of the lender, liquidity continues to accelerate, and real estate capital markets have quickly rebounded to pre-COVID levels. Additionally, the supply of maturing loans over the next several years are expected to be significant, generating consistent demand for mortgage loans, particularly on transitional and pre-stabilized assets. There will be a growing need to support transitional real estate, a trend that has been accelerated by the pandemic. The Team believes that lending markets will continue to be inefficient and volatile, especially in regulated sectors, creating space for private alternative lenders to step in. Borrowers also increasingly favor large, non-regulated institutional platforms that can deliver a wide array of products, that are solution-oriented, and have a strong track record of execution.

The Team believes that risk-adjusted returns of directly originated loans secured by pre-stabilized assets look compelling over the next several years due to the following factors:

| • | Reduced property valuations inconsistently across sectors in selective markets; |

| • | Wider loan spreads than the last several years; |

| • | Moderated LTVs; and |

| • | An increase in “lender-friendly” loan structures and covenants. |

Investment Strategy

AB believes that its established commercial real estate debt platform is well positioned to capitalize on this investment opportunity. Due to the breadth and experience of the Team, we believe we are able to identify mispriced areas of a real estate capital structure on which many of our peers are not able to capitalize. Lending conditions over the foreseeable future are expected to favor experienced lenders, supported by lower property valuations across certain property types in some sectors, tighter covenant structures, and an uneven expected economic recovery. This market dynamic creates a compelling opportunity for private lenders like AB to generate attractive risk-adjusted returns. Further, it is expected that most of our loan investments will be floating rate based, which could provide value protection in a rising interest rate environment.

The Team is highly selective and focuses on pursuing idiosyncratic investment opportunities across various property types, geographies, sizes, sponsorship, and business plans that exhibit strong underlying fundamentals and intrinsic value. The Team also seeks to avoid situations involving potential binary outcomes or excessive cyclical risk, instead focusing on investments where the downside is protected by the underlying real estate collateral. Our investments will be selective, focusing on unique, income-oriented opportunities across various property types located in diverse geographies across the United States. Furthermore, the investment strategy allows for the acquisition of discounted loans with room to restructure and modify those loans in order to improve recoverability above the price paid.

The Team believes our allocations to private real estate debt investments can generate attractive risk-adjusted returns for the following reasons:

| • | Illiquidity and complexity premia—Commercial real estate debt markets often offer a significant return premium relative to corporate and/or other public credit markets owing to the idiosyncrasy and relative illiquidity of the asset class, which necessitates experienced underwriting. Investment opportunities targeted by the Company offer the potential for attractive yields on both an absolute and relative basis to more liquid fixed-income alternatives such as high yield bonds and broadly syndicated bank loans. |

| • | Downside protection—Loans secured by commercial real estate typically have better capital preservation attributes due to the physical nature of the collateral and the clear path for the lenders to take back the asset if necessary. |

| • | Diversification—Our portfolio is expected to be diversified geographically and across property types and sponsors. Furthermore, commercial real estate loans have idiosyncratic risk exposures and are not highly correlated to traditional equity and fixed income markets. |

| • | Inflation protection—Most of the investments are expected to be structured with a spread over LIBOR (soon to be SOFR), as will the leverage utilized, providing a natural hedge against rising interest rates and inflation. |

| • | Experienced management team—The deep and diverse experience stemming from AB’s existing real estate debt platform helps to enhance deal flow, underwriting, risk management, and other processes. |

The Investment Manager will seek to consistently apply our investment philosophy throughout the investment lifecycle, from deal selection to portfolio management, and combines fundamental, valuation-based analysis and principles with proven underwriting frameworks.

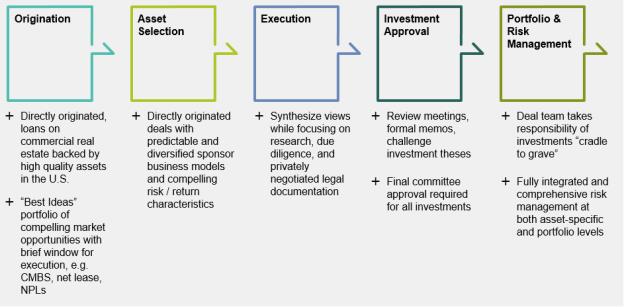

Investment Process

Having formed longstanding industry relationships with financial sponsors, developers, real estate operating companies, investment banks and brokers, the Team will seek to create a diversified portfolio of investments across various property types, geographies, deal sizes, financial sponsors, and business plan stages, focusing on those with strong underlying fundamentals and intrinsic value. With experience through multiple investment cycles, the Team will also seek to avoid situations involving potentially binary outcomes or excessive economic cycle risk.

Investments by the Company will be subjected to a rigorous investment management process that has already been established and is currently implemented by the Team. The Team’s risk-focused approach is rooted in detailed underwriting and in building portfolios with asymmetric risk-reward dynamics, focusing on capital preservation and downside protection. The Team will leverage its collective and diverse investment expertise and processes established and honed since 2013 to help produce compelling risk-adjusted returns.

An overview of the investment process is illustrated below:

| 1. | Transaction Sourcing & Screening Methodology: (i) Twice-weekly pipeline/production calls to review potential deals overseen by senior Team members; (ii) Opportunities sourced by the Team from direct borrower relationships, repeat clients, and the CRE brokerage network; (iii) Screen transactions with a deal summary presentation identifying investment thesis, risk parameters and targeted return. |

| 2. | Initial Underwriting: (i) Evaluate risk parameters including market/submarket, property/portfolio characteristics, borrower/partner, structure, and exit strategy; (ii) Discuss return targets outline pricing justification; alternative investments and comparable transactions; (iii) The Investment Sub Committee assesses investment thesis, approves issuing term sheet and identifies key risks and deal terms to focus on during underwriting. |

5

Table of Contents

| 3. | Complete Due Diligence & Determine Valuation: (i) Evaluate risk parameters and identify mitigants; (ii) Use independent third-party data to assess value. |

| 4. | Investment Committee: (i) Assess viability, risks and mitigants of investment thesis; (ii) Justify return and compare to other real estate investment alternatives; (iii) Approve transaction. |

| 5. | Asset Management: Regular monitoring of loan and collateral activity via online servicer portals, including monthly and as-needed monitoring for major lease approvals, loan cash management, construction progress & budget rebalancing, loan modification requests, loan payoff, loan extension requirements, market trends (sales comps, micro-market news); quarterly monitoring of property rent roll, property financials, leasing activity reports, business plan updates from borrowers, interest reserve rebalancing; and annual monitoring of guarantor financials and covenants. The Team engages in frequent discussions with the servicer as well as open dialogue and in-person meetings with borrowers and engages in regular calls and meetings with local brokers and market data providers. |

| 6. | Exit Strategy: As part of the underwriting process for every investment, evaluate the feasibility of multiple exit strategies, including refinance and collateral sale. Additionally, several tools are at the Team’s disposal to protect investors’ capital if it needs to work through challenges at underlying properties, including in default scenarios (such as forbearance, note sale, deed in escrow, deed-in-lieu of foreclosure and foreclosure). |

Leverage

Where appropriate, certain portfolio investments may be leveraged using both direct and/or structural leverage. Direct leverage may include the utilization of bank credit facilities, subscription facilities, and repurchase agreements. We may incur leverage directly or may form direct or indirect bankruptcy remote special purpose subsidiaries that may hold all or any portion of our investment portfolio and enter into credit facilities that may hold all or any portion of our investment portfolio and enter into credit facilities or issue debt in collateralized loan obligations or otherwise. Use of structural leverage may include syndicating senior participations in originated senior loans to other investors while retaining a subordinated debt position. We may also choose to syndicate pari passu interests of originated mortgage positions or syndicate participating interests in an originated subordinated debt position if the Investment Manager believes such an approach is consistent with our investment strategy. The overall leverage will vary as a percentage of investment value and depending upon the composition of the portfolio. Following the twenty-four month period after the Initial Closing, we will endeavor not to incur direct debt if, upon the incurrence thereof, the ratio of total direct debt-to-equity of the Company as a whole will exceed 3:1, or 300%, at the portfolio level and 4:1, or 400%, on individual assets. It is anticipated that such leverage provided under credit facilities will contain certain customary affirmative and negative covenants and events of default typical of such facilities. Our assets may be pledged to secure such indebtedness, as more fully described in the LLC Agreement.

Market risks are inherent in all investments to varying degrees. In fact, certain investment practices described above can, in some circumstances, potentially increase the adverse impact on our investment portfolio. See “Item 1A. Risk Factors—Certain Market Risks Generally.”

The descriptions of specific strategies that we may be engaged in described in this Registration Statement should not be understood as in any way limiting our investment activities. We may engage in any investment strategy including ones that are not described herein that the Investment Manager considers appropriate for our investment objective. Our investment program is speculative and entails substantial risks, and there can be no assurance that our investment objective will be achieved.

Risk Factor Summary

An investment in our securities involves certain risks. The risk factors described below are a summary of the principal risk factors associated with an investment in our units. These are not the only risks we face. You should carefully consider these risk factors, together with the risk factors set forth in “Item 1A. Risk Factors” and elsewhere in this Registration Statement and other reports and documents we file with the SEC.

Certain Market Risks Generally

| • | Our investment activities will be affected by economic and market conditions and changes in applicable laws, currency exchange controls, and political and socioeconomic circumstances. |

| • | Deterioration in market conditions and the real estate market could have a material adverse effect on our financial performance and borrowers’ ability to meet their debt obligations comprising our Portfolio Investments. |

| • | Adverse conditions in the areas where our Portfolio Investments or the properties underlying such Portfolio Investments are located and fluctuations in the global credit markets may have an adverse effect on the value of our Portfolio Investments. |

| • | We operate in a highly competitive industry. |

Certain Regulatory, Legal, Tax and Operational Risks

| • | Change in, change in interpretation of, or newly enacted laws or regulations and any failure by us to comply with these laws or regulations may have an adverse effect on us and increase our tax liability. |

| • | We are a newly formed entity and have no operating history. |

| • | We depend on the Investment Manager’s ability to develop and implement investment strategies that achieve our investment objectives and on the reliability, accuracy and analysis of the Investment Manager’s analytical models. |

| • | Members will not be permitted to engage in the active management and affairs of the Company. |

| • | We are dependent upon our counterparties and certain third-party service providers. |

| • | If we fail to maintain our exclusion from the definition of an “investment company” under the Company Act, we would be regulated as an investment company and be subject to additional regulatory restrictions. |

| • | We may be subject to risks associated with our acquisition of loans that were originated by banks. |

| • | Failure to be properly licensed may have a material adverse effect on us and our operations. |

| • | Failure to qualify as a REIT under the Code could have a material adverse effect on us. |

| • | REIT requirements may restrict our operations, limit our ability to hedge effectively, may cause us to incur tax liabilities and may force us to make distributions to Members. |

| • | We may incur tax liabilities that would reduce the cash flow available for distributions. |

| • | We may make in-kind distributions to Members. |

| • | Dividends payable by REITs do not qualify for the reduced tax rates available for some dividends. |

| • | Risk associated with certain of our assets and investments could affect our ability to qualify as a REIT. |

| • | We have the ability to incur significant leverage. |

Certain Risks Associated with the Units

| • | The Units are not freely transferable and therefore provide limited liquidity to investors. |

| • | Our Incentive Fee may create an incentive for the Investment Manager to make riskier or more speculative investments. |

| • | A failure in our cyber security systems or information systems could significantly disrupt our business. |

| • | We, the Investment Manager and/or its affiliates may enter into separate agreements with certain Members on different terms than those described in this Registration Statement. |

| • | We may suspend distributions, the calculation of our NAV and/or the calculation of the NAV of Units. |

Certain Investment Risks

| • | Our Portfolio Investments may be risky, and you could lose all or part of your investment. |

| • | We are subject to the risks inherent in the ownership and operation of real estate and real estate-related businesses and assets. |

| • | We have not yet identified our Portfolio Investments with certainty. |

| • | We intend to invest in certain long-term, illiquid investments. |

| • | We will depend on the diligence of our Investment Manager. |

| • | The Investment Manager’s ability to manage certain Portfolio Investments may be limited. |

| • | Real estate loans that we originate or acquire may become non-performing after their acquisition. |

| • | Our Portfolio Investments may be subject to greater risks of delinquency and foreclosure than other loans. |

| • | Any insurance proceeds received with respect to a property relating to one of our investments may not be sufficient to recover our economic position with respect to such investment. |

| • | Borrowers that we make loans to may not be able to achieve their business plans, and such loans may go into default. |

| • | We may purchase participations and/or co-lender interests in real estate loans. |

| • | There are no restrictions on the credit quality of the collateral securing the loans in which we invest. |

| • | Changes to, or the elimination of, LIBOR could have a material adverse effect on our investments. |

| • | We are subject to risks associated with mortgage loans secured by leased properties. |

| • | We are subject to risks associated with our investments in Collateralized Mortgage Backed Securities. |

| • | We may be subject to lender liability claims. |

| • | We may invest in certain subordinated classes of securities and certain derivative agreements. |

| • | Transactions denominated in foreign currencies subject us to foreign currency risks. |

| • | Our performance may be adversely affected due to environmental risks, including climate change. |

Other Risks

| • | We may not be able to realize returns on our investments in a timely manner, or at all. |

| • | The concentration of our investment portfolio in the commercial real estate sector may increase the losses suffered by us or reduce our ability to hedge our exposure and to dispose of depreciating assets. |

| • | We may invest in securities subject to transfer restrictions or for which no liquid market exists. |

| • | We may expose ourselves to risks if we engage in hedging transactions. |

| • | Risks associated with the COVID-19 pandemic may adversely affect our investments and operations. |

| • | We may suffer losses as a result of the adverse impact of any future terrorist attacks. |

| • | Reduced disclosure requirements applicable to emerging growth companies may make our units less attractive to investors. |

Investment Manager Fees

We will pay the Investment Manager a management fee pursuant to the Management Agreement (the “Management Fee”) and an incentive fee pursuant to the LLC Agreement (the “Incentive Fee”). The cost of both the Management Fee and the Incentive Fee will ultimately be borne by the Members.

6

Table of Contents

Management Fee

We will pay the Investment Manager, on a quarterly basis, a Management Fee in respect of each Member, in arrears, equal to the Applicable Percentage (as defined below) of such Member multipled by the sum of (i) the net asset value (“NAV”) of the Units and (ii) all unfunded commitment amounts under any Portfolio Investments with ongoing funding obligations, e.g., delayed-draw term loans, each of (i) and (ii) as of the last day of each calendar quarter. For the avoidance of doubt, the Management Fee will not be charged with respect to any portion of the Company’s assets that are attributable to direct leverage.

A Member’s “Applicable Percentage” is set forth below:

Aggregate Capital Commitment of a Member | Applicable Percentage | |||

$50,000 - $500,000 | 1.50 | % | ||

$500,001 - $1,000,000 | 1.40 | % | ||

$1,000,001 - $3,000,000 | 1.30 | % | ||

$3,000,001 - $5,000,000 | 1.15 | % | ||

$5,000,001 and over | 1.00 | % | ||

Notwithstanding the foregoing, with respect to any Member that makes a Capital Commitment on the Initial Closing Date (each, a “Founding Member”), the Management Fee shall be waived (and shall not be charged) with respect to such Founding Member (including any additional Capital Commitments made by such Founding Member) until the six month anniversary of the Initial Closing Date.

Payment of the Management Fee will be made within ten (10) days of the last day of each calendar quarter, or as soon as reasonably practicable thereafter.

The Management Fee charged with respect to a Member will be prorated for any capital contribution or repurchase of Units that is effective other than as of the first day of a calendar quarter.

The Investment Manager may, in its discretion, reduce, waive or calculate differently the Management Fee charged at the Company level with regard to the Units held by certain Members, including, without limitation, with respect of a Member that is a partner, member or employee of the Investment Manager or its affiliates, such person’s family members and trusts or other entities established for the benefit of such person or his or her family members (each, a “Related Investor”), so long as such reduction, waiver or calculation does not result in a preferential dividend under Section 562(c) of the Code.

The Management Fee may exceed the expenses borne by the Investment Manager on our behalf.

Incentive Fee

At the end of each calendar quarter, the Investment Manager will be entitled to receive an incentive fee (the “Incentive Fee”) equal to the difference between (x) the product of (A) 15% and (B) the difference between (1) Core Earnings of the Company for the most recent 12 month period (or such lesser number of completed calendar quarters, if applicable), and (2) the product of (I) the weighted average of the Company’s NAV of the three previous calendar quarters (or such lesser number of completed calendar quarters, if applicable) and the Company’s NAV as of the beginning of the then current calendar quarter, and (II) 6% per annum, and (y) the sum of the Incentive Fee previously paid to the Investment Manager with respect to the first three calendar quarters of the most recent 12 month period (or such lesser number of completed calendar quarters, if applicable); provided, that no Incentive Fee shall be payable to the Investment Manager with respect to any calendar quarter unless the Core Earnings for the twelve (12) most recently completed calendar quarters (or such lesser number of completed calendar quarters following the date of the Initial Closing (the “Initial Closing Date”)) is greater than zero. The Incentive Fee shall be prorated for partial periods, to the extent necessary, based on the number of days elapsed or remaining in such periods as the case may be. Unless otherwise determined by the Investment Manager, the Company’s NAV at the beginning of a calendar quarter for purposes of this Incentive Fee calculation shall be equal to the Company’s NAV as of the end of the previous calendar quarter as increased by capital contributions and decreased by repurchases.

For purposes of the foregoing, “Core Earnings” means the net income (loss) attributable to the holders of Units, computed in accordance with GAAP, including realized gains and losses not otherwise included in net income (loss), and excluding (i) the Incentive Fee, (ii) depreciation and amortization, (iii) any unrealized gains or losses or other similar non-cash items that are included in net income for the Applicable Period, regardless of whether such items are included in other comprehensive income or loss or in net income and (iv) one-time events pursuant to changes in GAAP and certain material non-cash income or expense items, in each case after discussions between the Investment Manager and the Board and approved by a majority of the Board. “Applicable Period” means the calendar quarter (or part thereof) for which the calculation of the Incentive Fee is being made.

For the avoidance of doubt, the Investment Manager will be entitled to receive an Incentive Fee with respect to any Units that are repurchased at the end of any calendar quarter (in connection with repurchases of such Units pursuant to the Unit repurchase plan) in an amount calculated as described above with the relevant period being the portion of the calendar quarter for which such Unit was outstanding, and proceeds for any such Unit repurchase will be reduced by the amount of any such Incentive Fee.

In the sole discretion of the Company, the Incentive Fee may be waived, reduced or calculated differently with respect to the Units held by certain Members, including, without limitation, a Related Investor, so long as such waiver, reduction or calculation does not result in a preferential dividend under Section 562(c) of the Code.

7

Table of Contents

For the avoidance of doubt, because the Incentive Fee is calculated at the Company level in the aggregate and not charged separately with respect to each Member, it is possible that the Company may be charged the Incentive Fee despite the Member’s particular investment in the Company having a negative performance during a calendar quarter.

Expenses

Company-Related Transaction Fees

Any transaction or similar fees (such as acquisition, disposition, financing or other similar fees, but not including servicing fees) from third parties (“Transaction Fees”), will be paid to the Company (and thereby reflected in the NAV of Units held by all of the Members on a pro rata basis), subject to compliance with the REIT qualification requirements. The Company may retain the Investment Manager and/or one or more affiliates of the Investment Manager to perform and receive fees for asset management, leasing, construction management, loan servicing, special servicing or other similar services, which fees will not cause a reduction in the Management Fee or otherwise be deemed to constitute Transaction Fees, if the Company believes that the Investment Manager or its affiliates can provide such services more effectively and at a cost that is comparable to prevailing market rates for such services.

Company Operating Expenses

The Investment Manager will be responsible for the cost of its staff, systems, premises and general overhead incurred in performing its duties to the Company.

We will bear all direct costs, fees and expenses incurred in connection with our management and operations, including but not limited to the following, which we refer to as “Company Expenses”:

| • | investment expenses (including any expenses that the Investment Manager reasonably determines to be related to investments, including expenses related to due diligence, sourcing, purchasing, structuring, originating, disposing, monitoring, financing or hedging of our or each Subsidiary’s assets, such as brokerage commissions, expenses relating to clearing and settlement charges, custodial fees, bank service fees and interest expense, whether or not the investment was consummated); |

| • | expenses related to owning and operating real assets; |

| • | servicing fees and expenses including such expenses incurred or such fees paid to the Investment Manager or its affiliates in its capacity as servicer if the Company believes the Investment Manager or its affiliates can provide such services more effectively and at a cost that is comparable to prevailing market rates for such services; |

| • | expenses incurred in connection with collection of monies owed to the Company or any Subsidiary; |

| • | expenses relating to compliance with REIT qualification requirements; |

| • | costs for forming and maintaining any Subsidiaries; |

| • | expenses arising out of or related to the foreclosure on collateral securing one or more investments of the Company, and, thereafter, expenses associated with holding, valuing, disposing of, trading, financing, negotiating and structuring such foreclosed collateral (including the costs of structuring, establishing, maintaining and liquidating any vehicles established to hold or facilitate the holding of such foreclosed collateral); |

| • | legal expenses; |

| • | professional fees (including, without limitation, expenses of asset managers, consultants and experts or master servicing or special servicing fees payable to a third party servicer or to the Investment Manager or its affiliates) relating to investments; |

| • | accounting expenses; |

| • | auditing and tax preparation and other tax-related expenses; |

| • | research-related expenses to the extent that such services fall within the safe harbor of Section 28(e) of the Exchange Act (including, without limitation, news and quotation services, market data services, and fees to third-party providers of research and/or portfolio risk management services); |

| • | travel-related expenses (including costs related to transportation, lodging and accomodations, meals and entertainment); |

| • | interest expense, initial and variation margin requirements, appraisal fees and expenses; |

| • | broken deal expenses and other transactional charges; |

8

Table of Contents

| • | fees or costs, and all other out-of-pocket expenses incurred in connection with the preparation and distribution of reports to the Members and the operation and administration of the Company’s costs and expenses incurred in connection with the organization and offering and sale of Units (including, without limitation, all legal expenses, printing and mailing costs, insurance costs, filing and registration fees); |

| • | the Management Fee; |

| • | the Incentive Fee; |

| • | the costs and expenses of third-party risk management products and services (including, without limitation, the costs of risk management software or database packages); |

| • | any insurance, indemnity or litigation expense (including premiums for policies taken out to cover members of the Board and officers of the Investment Manager, regardless of whether or not those policies cover liability that is not indemnifiable pursuant to the terms of the LLC Agreement); |

| • | fees of the Administrator; |

| • | expenses associated with the Company’s or any Subsidiary’s administrative and reporting costs, financial statements and tax returns, including the meeting expenses of the Board or the Members; |

| • | expenses related to regulatory compliance; |

| • | expenses related to the procurement, maintenance, enhancement and use of software programs and systems; |

| • | expenses of certain in-house services performed by the Investment Manager in respect of the Company if the Investment Manager believes it can provide such services more effectively and at a cost that is comparable to prevailing market rates for such services; |

| • | compensation payable to the Company’s chief financial officer, chief accounting officer and other staff of the Company (which such compensation shall be allocated among the Company and other applicable clients of the Investment Manager on a basis that the Investment Manager believes in good faith to be fair and reasonable); |

| • | expenses incurred in connection with complying with provisions in other agreements, including “most favored nations” provisions; |

| • | any extraordinary expenses (including, to the extent permitted by law, if applicable, indemnification or litigation expenses and any judgments or settlements paid in connection therewith or other costs or expenses arising therefrom); |

| • | any taxes, fees or other governmental charges levied against the Company; |

| • | wind-up and liquidation expenses (and expenses comparable to the foregoing); and |

| • | other similar expenses related to the Company. |

Generally, Company Expenses (other than any expenses that we determine in our sole discretion should be reflected in the NAV of the Units held by a particular Member), will be reflected in the NAV of Units of all of the Members on a pro rata basis. To the extent that Company Expenses to be borne by the Investment Manager or its affiliates, we will reimburse such party for such expenses.

Organization and Offering Expenses

We will reimburse the Investment Manager for our organizational and offering expenses, including shared organizational and offering expenses of our predecessor fund that did not ultimately commence investment operations as intended (“Organizational Expenses”).

As of September 30, 2021, the Investment Manager has incurred a total of approximately $1.2 million in documented costs and expenses on our behalf. Upon successful completion of the Private Offering, we expect to reimburse the Investment Manager or its affiliates for these costs and expenses. Each Member will be solely responsible for its own legal and tax counsel and any out-of-pocket expenses incurred in connection with its investment in the Company.

Pursuant to an Expense Limitation Agreement, the Investment Manager may determine to cap Organizational Expenses and Company Expenses in the aggregate that are borne by the Company to the extent necessary to prevent Organizational Expenses and Company Expenses, on an annualized basis, from exceeding a percentage determined by the Investment Manager in its discretion. This cap will be maintained until the third anniversary of the Initial Closing. Pursuant to the cap, any fees waived and expenses borne by the Investment Manager may be reimbursed by the Company during the period of time following the end of the amortization period

9

Table of Contents

and ending on the third anniversary of the start of the amortization period, provided that no reimbursement payment will be made that would cause the Company’s expenses to exceed the same cap. Extraordinary expenses (including, but not limited to, litigation expenses, indemnification expenses, lender liability expenses and other expenses not incurred in the ordinary course of the Company’s business), the Management Fee, the Incentive Fee, interest expenses, financing costs and expenses, and reserves for and costs associated with determining current expected credit losses, will not be included as Company Expenses for purposes of calculating the expense cap.

Administration Agreement

We will enter into an administrative services agreement (the “Administration Agreement”) with State Street Bank and Trust Company or its affiliates (the “Administrator”).

Pursuant to the terms of the Administration Agreement, the Administrator will act as administrator to us and to provide accounting, NAV calculation and certain other administrative services to us. The Administrator will receive negotiated fees paid out of our assets based upon the nature and extent of the services performed by the Administrator. The Administrator will be reimbursed by us for all reasonable out-of-pocket expenses. The Administration Agreement may be terminated by either party in accordance with the terms of the Administration Agreement.

The Administrator will be without liability for any loss, liability, claim or expense suffered or incurred by the Company unless caused by the Administrator’s fraud, willful default, gross negligence or willful misconduct, or that of the Administrator’s agents or employees. The Administrator will not be liable for any loss or damage arising from causes beyond its reasonable control. Further, the Administrator will not be liable for any special, indirect, incidental, or consequential damages of any kind whatsoever (including, without limitation, attorneys’ fees) in any way due to the Company’s use of the services provided under the Administration Agreement or the performance or failure to perform of the Administrator’s obligations under the Administration Agreement. In addition, pursuant to the Administration Agreement, the Company will indemnify the Administrator from and against any loss, liability, claim or expense (including reasonable attorneys’ fees and disbursements) suffered or incurred by the Administrator in connection with the performance of its duties under the Administration Agreement, including, without limitation, any liability or expense suffered or incurred as a result of the acts or omissions of the Company or any third party agent or authorized price source or as a result of acting upon any instructions reasonably believed by the Administrator to have been duly authorized by the Company. However, this indemnity will not apply to any liability or expense occasioned by or resulting from the fraud, willful default, gross negligence or willful misconduct of the Administrator in the performance of its duties under the Administration Agreement.

The Administrator may delegate to its affiliates any or all of its duties under the Administration Agreement. In providing services as an Administrator, the Administrator does not act as guarantor or offeror of the Units. The Administrator’s furnishing of such services does not constitute an endorsement or recommendation by the Administrator of an investment in the Company. Moreover, the Administrator is not responsible for any trading decisions of the Company (all of which are made by the Investment Manager), the effect of such trading decisions on the NAV of the Units or the monitoring of the Company’s investment strategy, objective or restrictions. The Administrator is a service provider to the Company and is not responsible for the preparation of this Registration Statement or the activities of the Investment Manager and therefore accepts no responsibility for any information contained in this Registration Statement. In performing its responsibilities with respect to calculating the value of the assets of the Company, the Administrator does and is entitled to rely upon values provided by Company, the Investment Manager, their affiliates and/or third parties.

We reserve the right to amend the Administration Agreement and change the administrative services arrangements of the Company without notice to or consent from the Members.

Our Private Offering

We expect that the Company will fall outside of the definition of an “investment company” under the Company Act, by satisfying the conditions of Section 3(c)(5)(C) of the Company Act, which excludes from the definition of an investment company persons that are primarily engaged in investing in interests in real estate. We expect to conduct private offerings of our Units to investors in reliance on exemptions from the registration requirements of the Securities Act of 1933, as amended (the “Securities Act”). Our initial private offering of Units (the “Private Offering”) is expected to be conducted in reliance on Regulation D under the Securities Act. Any investors in our Private Offering will be required to be “accredited investors” as defined in Regulation D of the Securities Act. The criteria required of Regulation D under the Securities Act may not apply to investors in subsequent offerings. Investments by U.S. investors in the Private Offering will also be subject to state securities laws. Further, due to certain anti-money laundering restrictions and economic sanctions concerns, Units may not be offered, sold, transferred, or delivered, directly or indirectly, to certain unacceptable investors. Our LLC Agreement also will impose additional restrictions upon the ownership of the Units to ensure, among other things, that we qualify and maintain our status as a REIT under the Code.

10

Table of Contents

We expect to enter into separate subscription agreements with a number of investors for the Private Offering. Each investor will make a capital commitment (a “Capital Commitment”) to purchase Units pursuant to a subscription agreement (a “Subscription Agreement”). We refer to the initial date on which Capital Commitments are first accepted by or on behalf of the Company from Members as the “Initial Closing”, and each such date on which Capital Commitments are accepted as a “closing.” Thereafter, subsequent closings for additional Capital Commitments from new and existing Members may generally be held as of the end of the calendar quarter, subject to our discretion to hold closings at any other time. The Initial Closing is expected to occur during the fourth calendar quarter of 2021.

Each Capital Commitment made by a Member at a closing will have its own lock-up period (a “Lock-Up Period”). The Lock- Up Period for each Capital Commitment will be the period commencing on the applicable closing and ending on the third anniversary of such closing. Upon the expiration of a Member’s Lock-Up Period, such Member may choose to be released from its Remaining Commitment (as defined below), subject to certain post-commitment period obligations.

A Member’s “Remaining Commitment” will be equal to such Capital Commitment reduced by amounts contributed to the Company in respect of capital calls and post-commitment period capital calls and increased by (i) the amount of any unused capital contributions that are returned to such Member pursuant to the last sentence of the following paragraph and (ii) distributions to such Member that represent a return of capital (and not current income (as defined below)). Each Capital Commitment made by a Member will be accounted for separately, including for purposes of determining Remaining Commitments and capital calls. In no event will a Member be required to make a capital contribution in respect of its Capital Commitment in excess of its Remaining Commitment.

Each Capital Commitment (or a portion thereof, as applicable) of a Member will last until (i) the Company determines to repurchase all or any portion of such Member’s Units that are attributable to such Capital Commitment (or such portion thereof, as applicable), as discussed below (which for the avoidance of doubt, will not become available pursuant to a Member’s repurchase request until the expiration of the Lock-Up Period), (ii) such Member has chosen to be released from its Remaining Commitments after the expiration of its Lock-Up Period (except with respect to post commitment period obligations) or (iii) the Company has elected to wind up (the “Commitment Period”).

Investors will be required to purchase Units each time we provide notice of a capital call, which be delivered at least 5 business days prior to which a capital call is due, in an aggregate amount not to exceed their respective Capital Commitments. All capital calls will generally be made pro rata in accordance with the investors’ Capital Commitments.

We are currently offering one class of Units. We may issue additional classes of Units in the future (or we may enter into agreements with certain Members that alter, modify or change the terms of the Units held by such Members), which may differ from the Units described herein, including, without limitation, in respect of a Related Investor. New classes of Units may be established by us without providing prior notice to, or receiving consent from, existing Members. The terms of such classes will be determined by us in our sole discretion. See “Item 7. Certain Relationships and Related Transactions, and Director Independence—Transactions with Related Persons; Policies and Procedures for Review of Related Party Transactions—The Investment Manager—Diverse Member Group.”

We may, directly or indirectly, borrow for working capital purposes, including, but not limited to, paying fees and expenses or managing cash flows from Capital Commitments. In connection therewith, we will be authorized to pledge, charge, mortgage, assign, transfer and grant security interests to a lender in (i) all Capital Commitments, our right to initiate drawdowns and collect the capital contributions of the Members and to enforce their obligations to make capital contributions to purchase Units, and (ii) a Company collateral account into which the payment by the Members of their remaining Capital Commitment are to be made. We refer to any such financing as a “Commitment Facility.” In connection with any Commitment Facility, and as further described in the LLC Agreement, each Member will remain absolutely and unconditionally obligated to fund capital calls duly issued by us or by the lender under a Commitment Facility (including, without limitation, those required as a result of the failure of any other Member to fund capital calls), without setoff, counterclaim or defense, including without limitation any defense of fraud or mistake, or any defense under any bankruptcy or insolvency law, including Section 365 of the Bankruptcy Code, subject in all cases to the Members’ rights to assert such claims against us in one or more separate actions; provided that, any such claims will be subordinate to all payments due to the lenders under a Commitment Facility.

A Member that defaults in respect of its remaining Capital Commitment may be subject to certain remedies, including forfeiture of its Units.

The NAV per Unit will be calculated by the Administrator (as defined below) as of each Valuation Date pursuant to the procedures determined by the Investment Manager. Generally, the last business day of each calendar quarter or such other date designated by us to accept the purchase of Units, as determined in our sole discretion, will be the “Valuation Date.” The NAV per Unit will be determined by dividing the value of the total assets of the Company less the liabilities of the Company by the total number of Units outstanding as at any Valuation Date. Liabilities will be determined based upon generally accepted accounting principles, subject to our right, in consultation with the Investment Manager, to provide reserves or holdbacks for estimated accrued expenses, liabilities or contingencies, including general reserves or holdbacks for unspecified contingencies (even if not required by generally accepted accounting principles). In calculating the NAV per unit, income and expenditure are treated as accruing from day-to-day.

In connection with any capital call, the per Unit price for the corresponding purchase of Units will be determined by the Company in accordance with the policies described herein. In particular, in the event that Units are issued as of the first business day of a calendar quarter, the per Unit price of such Units will be equal to the NAV per Unit established by the Company as of the immediately preceding Valuation Date (i.e., the last business day of the immediately preceding calendar quarter). In the event that Units are issued on any day that is not the first business day of the calendar quarter, we will use the methods described above, to the extent reasonably possible, to determine the NAV per Unit as of such issuance date.

Reinvestment Plan

With respect to each Capital Commitment made by a Member at a Closing, the Member will be required to either (i) opt into our reinvestment plan (the “Reinvestment Plan”), whereby the Member will have its current income distributions automatically withheld and reinvested into the Company (with additional Units of the Company corresponding to such reinvestment being issued to such Member), which we refer to as a “Reinvestment Election”, or (ii) opt out of the Reinvestment Plan, which we refer to as a “Distribution Election”, in each case, as elected in the Subscription Agreement of such Member. Any Member that does not make any such election in its Subscription Agreement will, by default, be deemed to have made a Distribution Election.

11

Table of Contents

A Member may elect to change its election from a Distribution Election to a Reinvestment Election (and vice-versa) by providing written notice to us no later than September 30th in any given fiscal year, to go into effect for the following fiscal year. Notwithstanding the foregoing, we may, in our sole and absolute discretion, accept such written notices on a later date. Such election may only be revoked prior to September 30th of such year unless otherwise determined by us. A Member who provides timely notice in a fiscal year to change its election from a Reinvestment Election to a Distribution Election for the upcoming fiscal year will not receive current income distributions for income generated during the fourth quarter as the amount of such distributions will be reflected in its NAV as of the date of the change in election. Accordingly, the first applicable distribution or reinvestment of current income (as applicable) with respect to such Member will not reflect such Member’s election change.

We will confirm to each Member each distribution or reinvestment of Current Income (as applicable) made pursuant to the Reinvestment Plan as soon as practicable following the date of such distribution or reinvestment of Current Income. With respect to Units that are subject to a reduced Management Fee, such reduced Management Fee will attach and apply to any corresponding Units issued pursuant to the Reinvestment Plan. We will pay for any expenses for administering the Reinvestment Plan. We may terminate the Reinvestment Plan upon notice in writing mailed to each Member at least thirty (30) days prior to the effectiveness of such termination. We may amend or supplement Reinvestment Plan at any time. We will at all times act in good faith and use our best efforts within reasonable limits to ensure the full and timely performance of all services to be performed pursuant to the Reinvestment Plan and to comply with applicable law, but we assume no responsibility and shall not be liable for loss or damage due to errors.

Term

The Company is intended to have a perpetual life. However, the Company may be liquidated at any time at the determination of the Board.

Operating and Regulatory Structure

REIT Qualification

We expect to elect to be taxed as a REIT beginning with our taxable year that begins on the date of the Initial Closing. We believe that we are organized and will operate in such a manner as to qualify for taxation as a REIT under the U.S. federal income tax laws. To qualify as a REIT, we must meet on a continuing basis, through our organization and actual investment and operating results, various requirements under the Code relating to, among other things, the sources of our gross income, the composition and values of our assets, our distribution levels and the diversity of ownership of our securities. If we fail to qualify as a REIT in any taxable year and do not qualify for certain statutory relief provisions, we will be subject to U.S. federal income tax at regular corporate rates and may be precluded from qualifying as a REIT for the subsequent four taxable years following the year during which we failed to qualify as a REIT. Even if we qualify for taxation as a REIT, we may be subject to some U.S. federal, state and local taxes on our income or property. In addition, subject to maintaining our qualification as a REIT, a portion of our business may be conducted through, and a portion of our income may be earned with respect to, our taxable REIT subsidiaries, (“TRSs”), should we decide to form TRSs in the future, which are subject to corporate income tax. Any distributions paid by us generally will not be eligible for taxation at the preferential U.S. federal income tax rates that currently apply to certain distributions received by individuals from taxable corporations, unless such distributions are attributable to qualified dividends received by us from a TRS, should we decide to form a TRS in the future.

Company Act Exclusion

We are not registered as an investment company under the Company Act. If we were obligated to register as an investment company, we would have to comply with a variety of substantive requirements under the Company Act that impose, among other things:

| • | limitations on our capital structure or the use of leverage; |

| • | restrictions on specified investments; |

| • | prohibitions on transactions with affiliates; and |

| • | compliance with reporting, record keeping, and other rules and regulations that would significantly change our operations. |

12

Table of Contents