Filed by EO Charging

pursuant to Rule 425 under the Securities Act of 1933

and deemed filed pursuant to Rule 14a-12

under the Securities Exchange Act of 1934

Subject Company: First Reserve Sustainable Growth Corp.

SEC File No.: 001-40169

Date: September 17, 2021

infrastructure | Market insight | 17 September 2021 | Oliver Carr

A Spotlight on SPACs

The special purpose acquisition company (SPAC) has become a mainstay of publicly listing companies in the US. With the rapidly developing global EV market flocking to New York based SPACs, will regulatory tweaks be enough to tempt some of this activity to London? inspiratia explores the promises and drawbacks of the SPAC and discusses the process with a company that is experiencing it first-hand

In 2020, 55% of the companies to go public in the US were SPACs. So far this year [to August 2021], that figure has risen to 63%, generating US$124 billion (£90bn €105bn) in proceeds. However, the rapidly growing share of new SPAC IPOs has been outstripping the share of total proceeds raised.

A SPAC – sometimes called a Blank Cheque Company – is a vehicle used to raise capital from private and retail investors to acquire a private company. The SPAC itself will conduct an IPO to get listed on a stock exchange with minimal assets or operation. Investors in the SPAC are, at this point, relying on the reputation and expertise of the founders or sponsors to convert their investment into a worthwhile acquisition.

Once sufficient funds have been raised and a target for the acquisition has been found, the SPAC then performs a reverse merger, whereby the combined company becomes listed on the stock exchange, usually under the name of the acquired one.

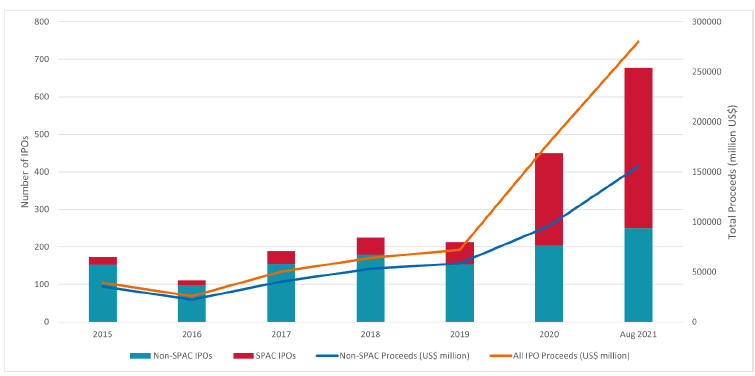

As seen below, the rise of the SPAC has been inexorable, yet there are still those who are sceptical about whether this growth is sustainable in the long term, or even that the market is not already saturated.

Annual count and proceeds of IPOs on US stock exchanges, 2015 – Aug 2021

Source | SPAC Analytics, inspiratia

“There was a wave of SPACs last year in the US however a lot of them are still looking for acquisitions,” says Sunjay Malhotra, corporate finance senior associate in the London office of Pinsent Masons. “You of course hear about all of the high-profile, multi-billion-dollar acquisitions by SPACs, but there are still a lot of SPACs that are looking for an appropriate target.”

| 1 | Phone: +44 2073519451 | Email: info@inspiratia.com |

The inside view from EO Charging

EO was founded in 2015 and has now sold over 50,000 charging station in 35 countries. In August this year [2021], the company announced that it was signing a business combination agreement with a NASDAQ listed SPAC of FRSG Corporation (First Reserve Sustainable Growth), in a deal valued at US$675 million (£490m €573m). This transaction was notable as being the first such acquisition of a UK-based EV charging business by a US SPAC. EO’s rationale for this strategy was clear and simple.

“It comes down to the size of the opportunity,” says Charlie Jardine, CEO and founder of EO Charging – and panellist at inspiratia’s upcoming New Energy Infrastructure and Energy Storage Summit.

“Typically, start-up companies have a significant need to scale quickly. For us, it’s a 10–20-year play. Going public is a great way to get access to sufficient capital to build a global business.”

“We don’t currently sell EO Chargers in the US, but we have big global aspirations and America represents a rapidly growing EV market – so the US will be a focal point for us in the future. FRSG’s experience in not only going public but in the energy transition space is also going to add a significant amount of value to us and our team as we scale globally.”

“One of the strategic advantages of a SPAC is speed to market. We will be able to get to market relatively quickly compared to a traditional IPO. The market for EVs has continually moved towards EO’s fleet-focused mission and value proposition - it’s growing very quickly, and the opportunity is now”

Problems could be looming for New York SPACs

An excess of targetless SPACs on the NASDAQ is a great opportunity for smaller start-ups in the EV space that are looking to raise funds and get themselves on the market quickly. However, some commentators are concerned that this imbalance could lead to problems for the market in the near future.

Most SPAC sponsors have a time limit of around two years to complete a transaction, after which the investors’ money must be returned, minus agreed expenses. Given sponsors typically receive a large equity share of the final company, they are heavily incentivised to find a target and sell it to investors, even if that target company is not the safest bet.

This could lead to a frenzy of activity from late 2022 when the initial wave of US SPAC managers will start to feel the heat. Particularly if the number of private start-ups in the target market continues to lag behind the number of SPACs receiving listings.

So, what sort of companies could rise up and fill this demand?

“It could be that certain companies may have difficulty fulfilling all the requirements for a NASDAQ IPO,” ponders Pinsent Masons’ corporate finance senior associate, Sunjay Malhotra, “or that they simply don’t have the management time or financial resource to complete all necessary formalities for a NASDAQ IPO – my understanding is that SPACs are a slightly quicker route to market in the US than a direct IPO.”

“When you invest in a tech company, it is always speculative because the outcome for that company is usually binary - it will either succeed or it will fail. But the rewards for investors if a tech company is successful are going to be huge.”

The biggest concern with SPACs has historically been the protections afforded to investors as there are less stringent disclosure requirements than a traditional IPO.

Charlie Jardine makes the point that after an agreement is put in place, there is more onus on the investor to scrutinise the companies that they are investing in, something he feels will do no harm to EO Charging.

“You’ve got to look at the company itself. We’ve got real paying customers and a real business that was already profitable last year. That in itself is a really compelling story. Of course, SPACs have taken some criticism. But fundamentally, you have to look beyond just the path to capital markets and into the financial trajectory of the company. We have both emerging and name brand B2B customers who have committed to five, ten, fifteen-year full fleet transitions contributing to a strong base of Annual Recurring Revenue, and this is just the start,” comments Jardin.

“The bottleneck is down to vehicle availability. From a charging point of view, part of our business plan is predicated on deployment of vehicles into the marketplace. That’s a macro trend that’s out of our control. But fundamentally, the market is growing extremely quickly, 300-400% year-on-year. So investors that believe in the future of EVs will also believe in the value of the charging market.”

| 2 | Contact us: Phone: +442073519451 | Email: info@inspiratia.com |

London makes a play for a share of the SPAC market

As all the attention is being pulled towards New York, European markets have been feeling distinctly left out of this growth. Comparative to the NYSE, SPACs are not even on the map in the UK, with London Stock Exchange (LSE) listed SPACs raising a measly £30 million (€35.2m US$41.4m) in 2020.

“The US simply has a deeper pool of capital.” Pinsent Masons’ Malhotra states. “There are more investors with deeper pockets than there are in the UK. There were also some EV SPACs early on in the SPAC wave in the US, such as Nikola and Fisker. Once you’ve seen a peer tread that path, it makes it much easier for other investors to follow.”

The Financial Conduct Authority (FCA) has recently brought in new rules that are designed to make it easier to put SPACs on the LSE. Of these, the headlines are:

Firstly, getting rid of the presumptions of suspension for SPACs that have raised over a £100 million (€177m US$138m). Making it possible for a company to trade throughout the merging process.

Secondly, introducing new investor protections. Ensuring that the shareholders’ money is kept in a ring-fenced pool that can be redeemed from if they do not approve of a proposed transaction. Those shareholders also must approve any acquisition.

Whether these rule changes are enough to guide any of the New York bound activity to London remains to be seen. However, Malhotra concludes by indicating that that particular ship has already sailed, “The FCA, the LSE and the UK government are all trying to make the UK a more attractive place to invest. Nevertheless, there are still a lot of British companies who see NASDAQ as the gold standard and so are choosing to list in the US.”

“A recent such high-profile company to do that was the company behind the Oxford-AstraZeneca vaccine, Vaccitech plc, which chose to list on NASDAQ rather than listing in the UK (notwithstanding that its Covid vaccine has not been approved in the US).”

“The Listing Rule changes are broadly welcomed, but I don’t think that it will lead to a flood of SPACs listing on the LSE.”

This topic and much more will be discussed at the fourth edition of inspiratia’s New Energy Infrastructure & Energy Storage Summit 2021, sponsored by AFRY and Squire Patton Boggs, which returns on 30 September with industry leaders to celebrate the strides in flexibility and energy storage, and discuss what comes next. Book your tickets here.

inspiratia is a powerful business development tool for practitioners in the global infrastructure and renewables sectors. Its specialist teams are uniquely qualified to deliver precise, timely and insightful analysis, forecasts and business information supporting clients to identify opportunities, trends, scenarios and risks.

Its briefings and webinar series offer instant access to decision-makers, content-rich presentations and debate with industry leaders covering the most critical issues and challenges affecting the infrastructure and renewables sectors. For more information or a demonstration of the service we offer, please contact us (info@inspiratia.com) (+44(0)2073519451)

| 3 | Contact us: Phone: +442073519451 | Email: info@inspiratia.com |

Forward Looking Statements

The information in this document includes “forward-looking statements”. All statements, other than statements of present or historical fact included in this presentation, regarding First Reserve Sustainable Growth Corp.’s (“FRSG”) proposed acquisition of EO, FRSG’s ability to consummate the transaction, the benefits of the transaction and the combined company’s future financial performance, as well as the combined company’s strategy, future operations, estimated financial position, estimated revenues and losses, projected costs, prospects, plans and objectives of management are forward-looking statements. When used in this press release, the words “could,” “should,” “will,” “may,” “believe,” “anticipate,” “intend,” “estimate,” “expect,” “project,” the negative of such terms and other similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain such identifying words. These forward-looking statements are based on EO’s current expectations and assumptions about future events and are based on currently available information as to the outcome and timing of future events. Except as otherwise required by applicable law, EO disclaims any duty to update any forward-looking statements, all of which are expressly qualified by the statements in this section, to reflect events or circumstances after the date of this press release. EO cautions you that these forward-looking statements are subject to numerous risks and uncertainties, most of which are difficult to predict and many of which are beyond the control of either FRSG or EO. In addition, EO cautions you that the forward-looking statements contained in this document are subject to the following factors: (i) the occurrence of any event, change or other circumstances that could delay the business combination or give rise to the termination of the Business Combination Agreement and Plan of Reorganization, dated as of August 12, 2021, by and among FRSG, Charge Merger Sub, Inc., Juuce Limited (“EO”) and EO Charging (“EOC”), and the other agreements related to the business combination (including catastrophic events, acts of terrorism, the outbreak of war, COVID-19 and other public health events), as well as management’s response to any of the foregoing; (ii) the outcome of any legal proceedings that may be instituted against FRSG, EO, their affiliates or their respective directors and officers following announcement of the transactions; (iii) the inability to complete the business combination due to the failure to obtain approval of the stockholders of FRSG, regulatory approvals, or other conditions to closing in the transaction agreement; (iv) the risk that the proposed business combination disrupts FRSG’s or EO’s current plans and operations as a result of the announcement of the transactions; (v) EO’s ability to realize the anticipated benefits of the business combination, which may be affected by, among other things, competition, the pace and depth of EV adoption generally, and the ability of EO to accurately estimate supply and demand for its EV charging products and services, and to grow and manage growth profitably following the business combination; (vi) risks relating to the uncertainty of the projected financial information with respect to EO, including the conversion of pre-orders into binding orders; (vii) costs related to the business combination; (viii) changes in applicable laws or regulations, governmental incentives and fuel and energy prices; (ix) the possibility that EO may be adversely affected by other economic, business, and/or competitive factors; (x) the amount of redemption requests by FRSG’s public stockholders; and (xi) such other factors affecting FRSG that are detailed from time to time in FRSG’s filings with the SEC. Should one or more of the risks or uncertainties described in this press release, or should underlying assumptions prove incorrect, actual results and plans could differ materially from those expressed in any forward-looking statements. Additional information concerning these and other factors that may impact the operations and projections discussed herein can be found in FRSG’s final prospectus for its initial public offering dated March 4, 2021 (SEC File No. 333-252717), which was filed with the SEC on March 5, 2021, and its periodic filings with the SEC, including its Quarterly Reports on Form 10-Q for the periods ended March 31, 2021 and June 30, 2021. FRSG’s SEC filings are available publicly on the SEC’s website at www.sec.gov.

Important Information for Investors and Stockholders About the Proposed Business Combination and Where to Find It

In connection with the proposed business combination, a registration statement on Form F-4 is expected to be filed by EOC with the SEC. The Form F-4 will include preliminary and definitive proxy statements to be distributed to holders of FRSG’s common stock in connection with FRSG’s solicitation of proxies for the vote by FRSG’s stockholders in connection with the proposed business combination and other matters as described in the Form F-4, as well as a prospectus of EOC relating to the offer of the securities to be issued in connection with the completion of the business combination. FRSG, EO and EOC urge investors, stockholders and other interested persons to read, when available, the Form F-4, including the proxy statement/prospectus incorporated by reference therein, as well as other documents filed with the SEC in connection with the proposed business combination, as

these materials will contain important information about EOC, EO, FRSG and the proposed business combination. Such persons can also read FRSG’s final prospectus dated March 4, 2021 (SEC File No. 333-252717) for a description of the security holdings of FRSG’s officers and directors and their respective interests as security holders in the consummation of the proposed business combination. After the Form F-4 has been filed and declared effective, the definitive proxy statement/prospectus will be mailed to FRSG’s stockholders as of a record date to be established for voting on the proposed business combination. Stockholders will also be able to obtain copies of such documents, without charge, once available, at the SEC’s website at www.sec.gov, or by directing a request to: First Reserve Sustainable Growth Corp., 290 Harbor Drive, Fifth Floor, Stamford, CT 06902, Attn: Neil A. Wizel. The information contained on, or that may be accessed through, the websites referenced in this press release is not incorporated by reference into, and is not a part of, this press release.

No Offer or Solicitation.

This communication is not a proxy statement or solicitation of a proxy, consent, or authorization with respect to any securities or in respect of the proposed business combination and shall not constitute an offer to sell or a solicitation of an offer to buy the securities of FRSG, EO or EOC, nor shall there be any sale of any such securities in any state or jurisdiction in which such offer, solicitation, or sale would be unlawful prior to registration or qualification under the securities laws of such state or jurisdiction. No offer of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act, as amended, or exemptions therefrom.

Participants in the Solicitation

EO, EOC, FRSG and their respective directors, officers and other members of their management and employees may be deemed participants in the solicitation of proxies of FRSG’s stockholders in connection with the proposed business combination. Security holders may obtain more detailed information regarding the names, affiliations and interests of certain of FRSG’s executive officers and directors in the solicitation by reading FRSG’s final prospectus for its initial public offering dated March 4, 2021 (SEC File No. 333-252717), which was filed with the SEC on March 5, 2021, and the proxy statement/prospectus and other relevant materials filed with the SEC in connection with the proposed business combination when they become available. Information regarding the persons who may, under SEC rules, be deemed participants in the solicitation of proxies of FRSG’s stockholders in connection with the proposed business combination will be set forth in the proxy statement for the proposed business combination when available. Information concerning the interests of EO’s, EOC’s and FRSG’s participants in the solicitation, which may, in some cases, be different than those of their stockholders generally, will be set forth in the proxy statement/prospectus relating to the proposed business combination when it becomes available.