As the PARA OPS product line is identified as a firearm in the United States, it must be determined whether an additional level of control is imposed by the NFA. Under NFA regulations, there are only two possible types of NFA firearm that PARA OPS could be defined as: (1) a "any other weapon" ("AOW") or (2) a "destructive device". Sale of either of these to consumers is permissible but requires a lengthy approval process conducted by the ATF (the background check process on the consumer); whereas sale to law enforcement agencies, military bodies, or government agencies is a more expedient approval process (usually less than 7 days). Further, the AOW classification requires only a $5 transfer tax to consumers whereas a destructive device classification results in a $200 transfer tax to consumers (such tax being borne by the consumer). While our PARA OPS is non-lethal (the kinetic energy of our projectile is well below lethal threshold), we have determined that the current version of our PARA OPS devices are "destructive devices" because the measurement of the bore of our device is currently in excess of the one-half inch in diameter, the maximum size for AOW.

As a result, initial sales of our PARA OPS devices in the United States are expected to come primarily from law enforcement agencies until we reduce the bore diameter of our device to less than one-half inch in diameter for the consumer market. In July 2022, we entered into a consulting agreement with an FFL engineering firm, Bachstein Consulting LLC, in the United States to finalize the prototype for the PARA OPS single and multi-shot devices, including LRIP during Q1 Fiscal 2023. We are currently pursuing development through Fiscal 2023 and the first half of Fiscal 2024 of a non-pyrotechnic energy actuator for PARA OPS in conjunction with a smaller diameter cartridge and projectile which, together, we expect would result in a next-generation version of PARA OPS products that would be considered non-firearms in most jurisdictions. The distribution of our PARA OPS in the United States will be done directly with FFL distributors/firearm dealers for civilian sales. Today, all 50 states of the United States allow civilians to own a firearm subject to the firearm laws of the state (which vary by state). We expect the sales of our PARA OPS devices will position us well for significant recurring revenues through the sale of subsequent ammunition over the next 12 months (see Item 3.D. - "Risk Factors - We have Significant Non-Recurring Revenue").

For the non-lethal ARWEN products, we maintain a firearm business license (the "Firearm Business License") issued by the Chief Firearms Office of the Ontario Ministry of the Solicitor General and we are also registered under the Controlled Goods Program in Canada. For further information, see Item 4.B. - "Digitization and Counter Threat". Additionally, we maintain a Federal Explosives License/Permit for the manufacturing of explosives and a FFL for manufacturer and sale of destructive devices, both issued by the ATF in the United States. These are currently under renewal. All sales of our ARWEN launchers are made directly to law enforcement agencies.

Rest of the World

As our current focus is commercializing PARA OPS in the United States, we have not begun analyzing the related government regulations for the rest of the world.

Digitization and Counter-Threat

Firearm Business License

In Canada, we maintain a Firearm Business License with the Chief Firearms Officer of the Ontario Ministry of Solicitor General for our following business activities:

- Manufacture, modification and assembly: prohibited weapons, ammunition, restricted firearms, prohibited devices, prohibited ammunition, prohibited handguns, non-restricted firearms, prohibited firearms;

- Retail sales (including consignment sales): restricted firearms and non-restricted firearms;

- Consignment sales: prohibited firearms including prohibited handguns;

- Gunsmithing: prohibited firearms, prohibited handguns, non-restricted firearms, restricted firearms;

- Transportation of inventory: prohibited firearms, ammunition, prohibited handguns, non-restricted firearms, prohibited ammunition, prohibited devices, restricted firearms, prohibited weapons;

- Storage of firearms: restricted firearms, non-restricted firearms, prohibited firearms, prohibited handguns.

- Export: ammunition, prohibited handguns, non-restricted firearms, prohibited ammunition, prohibited firearms, prohibited weapons, prohibited devices;

- Possession for the purpose of instruction: restricted firearms, ammunition, non-restricted firearms, prohibited handguns.

- Import: prohibited firearms, non-restricted firearms, prohibited devices, prohibited ammunition, ammunition, prohibited weapons, prohibited handguns and restricted firearms.

The Firearm Business License is delivered for the purposes of: (i) the performance of a contract entered into by the Government of Canada, the government of a province, the government of a municipality acting on behalf of a police force, or a police force, or by a person acting on behalf of such a government or a police force; and (ii) the development, modification or testing of a prohibited firearm, prohibited weapon, prohibited device or prohibited ammunition, or any component or part thereof, for the purpose of training, or supplying goods or training materials used in the training of, a public officer as defined in subsection 117.07(2) of the Criminal Code (Canada), who is acting in the course of his or her duties or employment.

As of the date of this Annual Report, we believe to be fully compliant with all the conditions under which the Firearm Business License is delivered and maintained.

We have applied for and received a Firearms Business License that covers off any potential scenario that we may from time to time be involved in which such a license would be required. We are currently not in the retail or consignment sale of firearms and do not expect to be in this type of business.

For greater clarity, we use real firearms in the development and testing of our products as well as in training users on their use. Any device such as the TASCS IFM or TASCS NORS must be developed and tested on the weapon platforms for which it is designed. The Shot Counter is designed to work on automatic weapons in military and police inventories. These types of weapons are classified as prohibited and are solely utilized in the development and testing of the product. Replica systems are utilized for static demonstration, trade shows and other non-firing events.

We procure ammunition such as those required for mortars, grenade launchers and others weapon types to conduct testing and evaluation. On occasion, we may need to export ammunition in support of demonstrations.

Controlled Goods Program

In Canada, an individual or organization must register in the Controlled Goods Program with the Public Services and Procurement Canada if they need to:

- examine, possess or transfer controlled goods (munitions);

- transfer controlled goods outside of Canada; or

- receive bid solicitation documents containing controlled goods or controlled technology.

We are registered in the Controlled Goods Program and believe we are in compliance as of the date of this Annual Report.

Economic Dependence

As an early-stage company, the revenue stream in Fiscal 2021 for the TASCS system was concentrated on one United States military customer. We recognized 98.3% of the total revenue (US $0.8 million) for this United States military customer during Fiscal 2021 (see Item 5.E. - "Critical Accounting Estimates"). We have delivered the remaining milestone and recognized the remaining 2.7% of the total revenue during the first quarter of Fiscal 2022. While we expect follow-on orders for our TASCS IFM 81mm mortar system they are likely to be under multi-year Joint Fires programs beginning in Fiscal 2024, and there is no assurance of such orders in Fiscal 2023.

Since September 30, 2021, we have further diversified our revenue base as a result of the Police Ordnance Acquisition. Additionally, on December 1, 2021, we entered into a master professional services agreement (the "MPSA") with GDMS to support the development of digitization solutions for future Canadian land C41SR programs under Strong, Secure, Engaged: Canada's Defence Policy. This includes TAK integration and other digitization services over 12 months. The MPSA serves as the master agreement and governs the basic terms and conditions for all future statements of work ("SOW") but does not in itself give rise to financial rights or obligations for either GDMS or us nor does it ensure that a future SOW will be awarded. Accordingly, there are no material terms in the MPSA except for the termination provision. At its sole discretion, GDMS may terminate the MPSA and/or a SOW by written notice to us. Under such event, GDMS will be liable for work rendered or expenses incurred prior to the effective date of such termination for which payment has not been made to us. GDMS may also terminate the MPSA immediately in the event of default (as defined in the GDMS). Concurrently with entering in the MPSA, we entered into a SOW with GDMS for the first phase of the project which was delivered by the end of Q3 Fiscal 2022 and fully collected. GDMS accounted for 41% of our Fiscal 2022 consolidated revenue. During Q1 Fiscal 2023 we entered into another SOW with GDMS for USD$0.1 million, which we delivered by the end of the quarter. With the anticipated commercial launch of PARA OPS product line in Fiscal 2023 and continued product sales from the ARWEN launchers, we anticipate our total consolidated revenue will continue to diversify with various customers, resulting in less dependence on limited customers to drive positive cash flows and profitability.

Foreign Operations

We established office space in Stafford, Virginia to conduct United States business development activities and anticipated light assembly and distribution for our non-lethal, Digitization, and Counter-Threat business lines. We released this space in the summer of 2023 and rented alternative space in the premises of our outsourced PARA OPS devices manufacturer in North Carolina for greater economy and convenience.

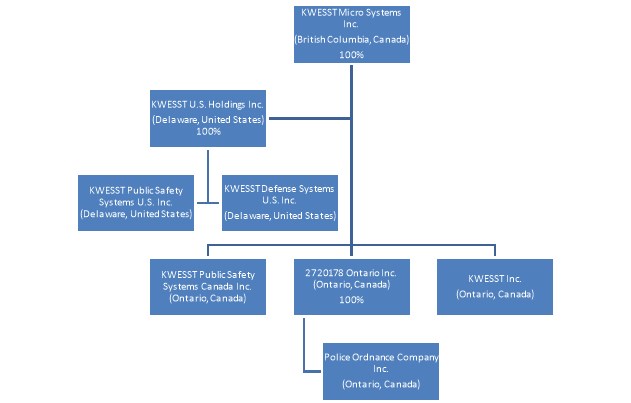

C. Organizational Structure

The following chart illustrates our wholly-owned subsidiaries:

KWESST U.S. Holdings Inc.

On May 2, 2022, we incorporated a wholly-owned United States holding subsidiary in Delaware (United States).

KWESST Public Safety Systems U.S. Inc.

On May 2, 2022, we incorporated a wholly-owned United States subsidiary in Delaware (United States), for the PARA OPS product line in the United States (see Item 4.B. - Business Overview).

KWESST Defense Systems U.S. Inc. (formerly KWESST U.S., Inc.)

On January 28, 2021, we incorporated a wholly-owned United States subsidiary in Delaware (United States), named KWESST U.S., Inc., and established an office in Stafford, Virginia (United States) to further pursue Digitization and Counter-Threat business opportunities in the United States. On June 3, 2022, we amended the certificate of incorporation of the subsidiary to change the name to KWESST Defense Systems U.S. Inc.

KWESST Public Safety Systems Canada Inc.

On April 6, 2022, we incorporated a wholly-owned subsidiary in Ontario (Canada), for the PARA OPS business line in Canada (see Item 4.B. - Business Overview).

2720178 Ontario Inc. and Police Ordnance Company Inc.

On December 15, 2021, we acquired 2720178 Ontario Inc., which owns all of the issued and outstanding shares of Police Ordnance, a company incorporated in Ontario (Canada) (see Item 4.A. - History and Development of the Company - Principal Capital Expenditures and Divestitures). These are wholly-owned subsidiaries of KWESST.

KWESST Inc.

On April 24, 2017, we incorporated a company in Ontario (Canada) named KWESST Inc. for the Digitization and Counter-Threat business lines.

On September 17, 2020, pursuant to the Qualifying Transaction (as defined below), KWESST Inc. amalgamated with 2751530 Ontario Ltd. ("Subco"), with the amalgamated company retaining the name of "KWESST Inc."

D. Property, Plants and Equipment

We do not own any real estate property. We operate from leased premises in three different locations, as detailed in the following table:

| Location | Area | Premise Use | Expiry Date |

| | (approx.) | | |

| 155 Terence Matthews, Unit#1, Ottawa, Ontario, Canada | 7,200 sq. ft. | Corporate offices and administration, R&D | April 30, 2026 |

| | | | (renewal extension of 5 years) |

| 557 Massey Road, Guelph, Ontario, Canada | 5,500 sq. ft. | Storage, distribution, and training of non-lethal ARWEN products, Para Ops engineering and sales | July 30, 2026 (renewal |

extension of 2 years to 2028) |

| 70 Mosswood BVLD, Suite 100 Youngsville, NC 27596 | 1,500 sq. ft | Address and US facility of ATF/Federal Firearms license for Para Ops, ARWEN and KWESST serialized products. Also used for product testing and sales demonstrations, product development and support. | June 2026 |

At September 30, 2023, the carrying value of our total tangible fixed assets was approximately $0.4 held in Ottawa, Ontario, Canada.

ITEM 4A. UNRESOLVED STAFF COMMENTS

Not applicable.

ITEM 5. OPERATING AND FINANCIAL REVIEW AND PROSPECTS

The following Operating and Financial Review and Prospects section is intended to help the reader understand the factors that have affected the Company's financial condition and results of operations for the historical period covered by the financial statements and management's assessment of factors and trends which are anticipated to have a material effect on the Company's financial condition and results in future periods. This section is provided as a supplement to, and should be read in conjunction with, our Consolidated Financial Statements and the other financial information contained elsewhere in this document. Our Consolidated Financial Statements have been prepared in accordance with International Reporting Standards as issued by the International Accounting Standards Board ("IFRS"). Our discussion contains forward-looking statements based on current expectations that involve risks and uncertainties, such as our plans, objectives and intentions. Our actual results may differ from those indicated in such forward-looking statements.

A. Operating Results

Overview

During Fiscal 2023, we had some significant highlights to our operating results:

- On May 2, 2023, we announced that The Canadian Department of National Defence ("DND") awarded a CAD $136 million dollar five-year defense contract to the JV Group (KWESST, Akkodis (MODIS) Canada and Thales Canada). KWESST's workshare under the joint venture agreement is up to 20% which would represent approximately CAD $27.2M (or an average of $5.4M per year) of the contract.

- As of the date of this filing, the DSEF program is now ramping up and KWESST has filled 2 of the 11 positions at the end of fiscal Q1 2024. The customer has issued three Statements of Work (SOWs) for three initial taskings to commence transition from the program incumbent (ADGA). KWESST is in the process of hiring, supplying, and submitting for approval to the customer approximately 11 resources under these SOWs which would represent an annualized revenue of approximately $2.2 million. To date, 5 candidates have accepted offers conditional upon their approval by the client and the issuance of security clearances. An additional 2 candidates are currently undergoing evaluation, with plans to identify and screen the remaining candidates in the upcoming weeks.

- On July 19, 2023, we announced the July 2023 Private Placement, that we had entered into a placement agency agreement (the "Placement Agency Agreement") with ThinkEquity and a securities purchase agreement (the "Securities Purchase Agreement") and a registration rights agreement (the "Registration Rights Agreement") with the Selling Securityholders, all of whom are accredited or institutional accredited investors. Under the Securities Purchase Agreement, on July 21, 2023 we sold 1,542,194 Common Shares at a price of USD$2.26 (CAD$2.98) per share and 930,548 Pre-Funded Warrants at a price of USD$2.26 (CAD$2.98) per warrant to the Selling Securityholders, with each Common Share and Pre-funded Warrant being bundled with one Warrant. Although the Common Shares and Pre-Funded Warrants were each bundled with a Warrant, each security was issued separately.

- On August 4, 2023, we shipped a prototype BLDS system to a NATO country customer for test and evaluation. Completion of the contract requires activation of certain capabilities designed into the system, notably a software bridge from the hardware sensors to a standard threat library of laser signatures, which is underway.

Additionally, we completed our cross-border listing on Nasdaq and our Common Shares began trading on December 7, 2022, under the stock symbol "KWE" and certain of our outstanding warrants under the symbol "KWESW" on the same day. On December 9, 2022, we closed our U.S. IPO and the Canadian Offering for aggregate gross proceeds of USD$14.1 million, before deducting underwriting and offering costs (see Item 5.B - Liquidity and Capital Resources for further details). In advance of the Nasdaq listing, on October 28, 2022, we effected the Reverse Split of our Common Shares to meet Nasdaq's initial listing requirements. All information respecting to outstanding Common Shares and other securities of KWESST, including net loss per share, in the current and comparative periods presented herein give effect to the Reverse Split.

Results of Operations

The following selected financial data has been extracted from the audited Fiscal 2023 financial statements.

| | | | | | | | | | | | Change | | | Change | |

| | | | | | | | | | | | 2023 vs | | | 2022 vs | |

| | | | | | | | | | | | 2022 | | | 2021 | |

| | | 2023 | | | 2022 | | | 2021 | | | % | | | % | |

| | | | | | | | | | | | | | | | |

| Revenue | $ | 1,234,450 | | $ | 721,519 | | $ | 1,275,804 | | | 71% | | | -43% | |

| Cost of sales | | (1,425,828 | ) | | (536,735 | ) | | (798,888 | ) | | 166% | | | -33% | |

| Gross profit (loss) | | (191,378 | ) | | 184,784 | | | 476,916 | | | -204% | | | -61% | |

| Gross margin % | | -15.5% | | | 25.6% | | | 37.4% | | | | | | | |

| | | | | | | | | | | | | | | | |

| Operating Expenses | | | | | | | | | | | | | | | |

| General and administrative | | 7,244,762 | | | 4,915,263 | | | 4,057,167 | | | 47% | | | 21% | |

| Selling and marketing | | 3,024,283 | | | 3,296,373 | | | 3,484,159 | | | -8% | | | -5% | |

| R&D | | 1,644,565 | | | 2,064,493 | | | 2,138,138 | | | -20% | | | -3% | |

| | | | | | | | | | | | | | | | |

| Total operating expenses | | 11,913,610 | | | 10,276,129 | | | 9,679,464 | | | 16% | | | 6% | |

| | | | | | | | | | | | | | | | |

| Operating loss | | (12,104,988 | ) | | (10,091,345 | ) | | (9,202,548 | ) | | 20% | | | 10% | |

| | | | | | | | | | | | | | | | |

| Other income (expenses) | | | | | | | | | | | | | | | |

| Share issuance costs | | (1,985,074 | ) | | - | | | - | | | N/A | | | N/A | |

| Net finance costs | | (668,034 | ) | | (506,002 | ) | | (107,751 | ) | | 32% | | | 370% | |

| Foreign exchange gain (loss) | | (98,275 | ) | | 28,780 | | | (3,742 | ) | | -441% | | | -869% | |

| Change in fair value of warrant liabilities | | 5,841,192 | | | - | | | - | | | N/A | | | N/A | |

| Loss on disposals | | (291,181 | ) | | (1,165 | ) | | (1,331 | ) | | N/A | | | N/A | |

| Total other income (expenses), net | | 2,798,628 | | | (478,387 | ) | | (112,824 | ) | | -685% | | | 324% | |

| Loss before income taxes | | (9,306,360 | ) | | (10,569,732 | ) | | (9,315,372 | ) | | -12% | | | 13% | |

| Deferred tax recovery | | - | | | 49,442 | | | - | | | N/A | | | N/A | |

| Net loss | $ | (9,306,360 | ) | $ | (10,520,290 | ) | $ | (9,315,372 | ) | | -12% | | | 13% | |

| EBITDA loss | $ | (7,685,818 | ) | $ | (9,737,239 | ) | $ | (9,066,631 | ) | | -21% | | | 7% | |

| Adjusted EBITDA loss(1) | $ | (10,778,926 | ) | $ | (7,304,670 | ) | $ | (6,599,351 | ) | | 48% | | | 11% | |

| Loss per share - basic and diluted | $ | (2.28 | ) | $ | (14.41 | ) | $ | (14.72 | ) | | -84% | | | -2% | |

| Weighted average common shares - basic | | 4,082,275 | | | 730,302 | | | 632,721 | | | 459% | | | 15% | |

(1) EBITDA and Adjusted EBITDA are non-IFRS measures. See "Non-IFRS Measures".

In the following table, we have reconciled the EBITDA and Adjusted EBITDA to the most comparable IFRS financial measure.

| | | | | | | | | Nine months | |

| | | Year ended | | | Year ended | | | ended | |

| | | September 30, | | | September 30, | | | September 30, | |

| | | 2023 | | | 2022 | | | 2021 | |

| | | | | | | | | | |

| Net loss as reported under IFRS | $ | (9,306,360 | ) | $ | (10,520,290 | ) | $ | (9,315,372 | ) |

| Net finance costs | | 668,034 | | | 506,002 | | | 107,751 | |

| Depreciation and amortization | | 952,508 | | | 326,491 | | | 140,990 | |

| Deferred tax recovery | | - | | | (49,442 | ) | | - | |

| EBITDA loss | | (7,685,818 | ) | | (9,737,239 | ) | | (9,066,631 | ) |

| Other adjustments: | | | | | | | | | |

| Stock-based compensation | | 373,554 | | | 1,960,072 | | | 2,462,207 | |

| Share issuance costs | | 1,985,074 | | | - | | | - | |

| Professional fees relating to financings | | - | | | 500,112 | | | - | |

| Fair value adjustment on derivatives | | (5,841,192 | ) | | - | | | - | |

| Foreign exchange loss (gain) | | 98,275 | | | (28,780 | ) | | 3,742 | |

| Loss on disposals | | 291,181 | | | 1,165 | | | 1,331 | |

| Adjusted EBITDA loss | $ | (10,778,926 | ) | $ | (7,304,670 | ) | $ | (6,599,351 | ) |

Current Year Variance Analysis (2023 vs. 2022)

For Fiscal 2023, KWESST's net loss was $9.3 million. Fiscal 2023 adjusted EBITDA loss was $10.8 million, an increase of 48% compared to the prior year, mainly due to increased operating expenses driven by increased personnel costs, consulting costs, professional fees, insurance costs, regulatory and compliance costs, and tradeshows. The adjustments to EBITDA loss for Fiscal 2023 included share insurance costs relating to warrant liabilities, and the change in fair value of derivative liabilities, all of which are related to the warrants issued in the U.S. IPO and Canadian Offering and the July 2023 Private Placement (see Notes 15 and 16 of the Fiscal 2023 financial statements). There has been a lower volume of stock-based grants in the last 12 months resulting in a material reduction in stock-based compensation expense in the current year compared to Fiscal 2022.

Revenue

Total revenue increased by $0.5 million in the year compared Fiscal 2022, mainly due to an additional $0.4 million generated from our digitization business line and $0.1 million from our non-lethal business line (driven from sale of ARWEN products).

We expect revenue to increase as we have formally received work tasks under the recently announced Canadian Government Contract amongst Modis Canada Inc., Thales Canada Inc., KWESST Inc. and the Canadian DND, dated May 1, 2023 (the "Canadian Government Contract") and we have commenced hiring and staffing those requirements. We continue to work towards a commercial launch of our PARA OPS, which we now expect to be in 1H Fiscal 2024.

Gross Profit

Our gross profit was a negative $0.2 million in the year compared to a positive gross profit of $0.2 million in Fiscal 2022. The decrease is due mainly to onerous contracts and consultant fees that have since been eliminated. As we are in the pre-revenue stage for most product lines, we expect continued fluctuation in gross profit / margin during Fiscal 2024 as we ramp up anticipated revenue in the year.

Operating Expenses ("OPEX")

Total OPEX was $11.9 million for YTD Fiscal 2023 compared to $10.3 million in YTD Fiscal 2022 for a total increase of $1.6M. Excluding share-based compensation, total OPEX was $11.5 million compared to $8.3 million, a 39% increase over the comparable prior year due to the following factors:

- G&A increased by $2.3 million, or 47%, primarily due to the impairment charge on the Phantom intangible asset, the retention bonus earned by our former CFO, an increase in salaries due to increase in corporate headcount and related compensation consistent with increased compliance requirements and associated risk from the Nasdaq listing, higher consulting fees and retention bonuses relating to key personnel in the non-lethal business line. Additionally, we incurred an increase in D&O insurance, professional fees, and compliance costs due to KWESST's Nasdaq listing in December 2022 and subsequent regulatory filing compliance.

- S&M decreased by $0.3 million, or 8%, primarily due to a $0.4 million decrease in share-based compensation expense, coupled with lower U.S. business development consulting costs in YTD Fiscal 2023. This was partially offset by an increase in tradeshow spend to promote our products and consulting fees.

- R&D decreased by $0.4 million, or 20%, primarily due to $0.2 million decrease in share-based compensation expense in Fiscal 2023 in comparison to the prior year. R&D expenses further decreased due to reallocating most of our engineering resources to deliver on customer contracts. The related costs are reported as part of cost of sales (for delivered performance obligations to customers) and work-in-progress inventories. These costs included an increase in payroll costs due to the strong local demand for skilled, experienced engineers.

Other income (expenses), net

For Fiscal 2023, our total other income was $2.8 million, compared to total other expenses of $0.5 million. The change in other income (expenses), net was driven mainly by the $5.8 million favorable change in fair value of warrant liabilities as a result of the remeasurement of the warrant liabilities at September 30, 2023, driven by a decrease in the underlying common share price on September 30, 2023. Under IFRS, we are required to remeasure the warrant liabilities at each reporting date until they are exercised or expired. This was partially offset by:

- $0.2 million increase in net finance costs is primarily due to the recognition of the remaining unamortized accretion costs and interest expense relating to the repayment of all outstanding loans, following the closing of the U.S. IPO and Canadian Offering;

- $2.0 million in Share Offering Costs relating to the U.S. IPO and Canadian Offering and the July 2023 Private Placement. Under IFRS, we are required to allocate proportionately the total underwriting and share offering costs (collectively "Share Offering Costs") between equity and warrant liabilities resulting from the U.S. IPO and Canadian Offering and the July 2023 Private Placement. The portion of the Share Offering Costs allocated to warrant liabilities were expensed; and

- $0.1 million increase in foreign exchange loss due to appreciation in the U.S. currency during the year.

Prior Year Variance Analysis (2022 vs. 2021)

Revenue

We generated $0.7 million in revenue for Fiscal 2022, a decrease of 43% over last year's revenue. The decline in revenue was driven mainly due to the timing of expected contracts and a smaller contract awarded by GDMS-C and CC-T during the current year compared to the USD$0.8 million contract awarded by a United States military customer in Fiscal 2021. This was partially offset by $0.3 million from the ARWEN product line as a result of the Police Ordnance acquisition made in late Q1 Fiscal 2022. The ARWEN revenue excludes $0.4 million for deliveries in relation to open customer orders at the closing of the Police Ordnance acquisition which were recognized as a reduction of intangible assets.

We expect revenue to ramp up during Fiscal 2023 with new anticipated military contracts, coupled with the pending commercial launch of our PARA OPS, scheduled for Q2 Fiscal 2023, and full year revenue results from the ARWEN product line.

Gross Profit

Our gross profit was $0.2 million for Fiscal 2022, or gross margin of 25.6%, compared to $0.5 million in Fiscal 2021 with gross margin of 37.4%. The fluctuation in gross profit / margin is primarily due to our pre-commercialization phase.

Operating Expenses

Total operating expenses were $10.3 million for Fiscal 2022, a 6% increase over the prior year. Excluding share-based compensation (non-cash item), total OPEX was $8.3 million compared to $7.2 million over the prior year. This represents a 15% increase which was driven mostly by accrued bonuses to our employees and management (none in the prior year) for their significant contributions in positioning KWESST for future success, coupled with higher professional fees incurred relating to a brokered private placement financing effort during the Spring 2022 that did not close due to very challenging global equity market conditions where S&P 500 index and Nasdaq index declined by approximately 20.6% and 29.5%, respectively from January 1, 2022, to June 30, 2022. We subsequently completed a successful cross-border listing on Nasdaq with a U.S. IPO and concurrent Canadian Offering, which both closed in December 2022. Professional fees relating to this effort were capitalized and reported as deferred share offering costs in our consolidated statements of financial position at September 30, 2022.

The above increase was partially offset by lower spend on advertising and promotion as well as no royalty and license costs in the current year compared to the previous year.

Our R&D expenses during Fiscal 2022 comprised of costs incurred in performing R&D activities, including new product development, continued product enhancement, materials and supplies, salaries and benefits (including share-based compensation), engineering consulting costs, patent procurement costs, and estimated R&D-related facility costs. Where we qualify for Canadian investment tax credits for qualified scientific research and experimental development expenditures, we record this income as a reduction of R&D expenses. Additionally, in accordance with IFRS, we capitalize development costs only if development costs can be measured reliably, the product or process is technically or commercially feasible, future economic benefits are probable, and we have the intention and sufficient resources to complete the development and to use or sell the asset. Accordingly, we capitalized $1.2 million of development costs during Fiscal 2022 for PARA OPS and Phantom, compared to $83 thousand for Phantom during Fiscal 2021. See Note 9 of the audited consolidated financial statements for Fiscal 2022.

Finance Costs

Net finance costs were $0.5 million for Fiscal 2022, a 370% increase over Fiscal 2021 driven mainly by an increase in borrowings during Fiscal 2022 and full year accretion cost on the accrued royalties liability relating to the acquisition of the PARA OPS system.

Net Loss and Adjusted EBITDA Loss

We incurred a net loss of $10.5 million or $14.41 per basic share for Fiscal 2022, compared to the net loss of $9.3 million or $14.72 per basic share for Fiscal 2021. After adjusting for share-based compensation and other items (see table above), our Adjusted EBITDA loss was $7.3 million, compared to Adjusted EBITDA loss of $6.6 million in Fiscal 2021.

The increase in net loss and Adjusted EBITDA loss was primarily due to lower revenue and higher OPEX as noted above.

Selected Annual and Quarterly Information

The following selected financial information is taken from the audited financial statements for the years ended September 30, 2023, 2022 and 2021.

| | | Year ended | | | Year ended | | | Nine months ended | |

| | | September 30, | | | September 30, | | | September 30, | |

| | | 2023 | | | 2022 | | | 2021 | |

| Statement of Operations data: | | | | | | | | | |

| Revenue | $ | 1,234,450 | | $ | 721,519 | | $ | 1,275,804 | |

| Gross profit | $ | (191,378 | ) | $ | 184,785 | | $ | 476,916 | |

| Gross margin % | | -15.5% | | | 25.6% | | | 37.4% | |

| Operating loss | $ | (12,104,988 | ) | $ | (10,091,345 | ) | $ | (9,202,548 | ) |

| Net loss | $ | (9,306,360 | ) | $ | (10,520,290 | ) | $ | (9,315,372 | ) |

| Loss per share - basic and diluted | $ | (2.28 | ) | $ | (14.41 | ) | $ | (14.72 | ) |

| | | | | | | | | | |

| | | September 30, | | | September 30, | | | September 30, | |

| | | 2023 | | | 2022 | | | 2021 | |

| Financial Position data: | | | | | | | | | |

| Cash | $ | 5,407,009 | | $ | 170,545 | | $ | 2,688,105 | |

| Total assets | $ | 11,758,832 | | $ | 11,758,832 | | $ | 8,717,846 | |

| Total non-current liabilities | $ | 1,439,577 | | $ | 1,434,628 | | $ | 1,434,628 | |

| Total shareholders' equity (deficit) | $ | 3,935,620 | | $ | 6,123,728 | | $ | 6,123,728 | |

See Item 4.A - Operating Results - Results of Operations for additional details and for the comparison discussion between the periods presented above.

Summary of Quarterly Results

The following table summarizes selected results for the eight most recent completed quarters to September 30, 2023.

| | | | | 2023 | | | | | | | | | | 2022 | | | | | | |

| ($ in thousands) | | Q4 | | | Q3 | | | Q2 | | | Q1 | | | Q4 | | | Q3 | | | Q2 | | | Q1 | |

| Revenue | | 606 | | | 150 | | | 161 | | | 317 | | | 255 | | | 282 | | | 166 | | | 17 | |

| Net loss | | (2,419 | ) | | (3,452 | ) | | (1,227 | ) | | (2,208 | ) | | (2,345 | ) | | (2,600 | ) | | (2,290 | ) | | (2,290 | ) |

Quarterly Results Trend Analysis

We experienced volatility with our quarterly revenue during Fiscal 2023 due to ramp up of new military contracts, which is expected to continue into Fiscal 2024 as we launch PARA OPS coupled with an increase in operating expenses as highlighted in the Results of Operations. Additionally, we expect further volatility with our quarterly net loss due to the remeasurement of warrant liabilities at each reporting period, with the change in fair value recorded through P&L.

Fourth Quarter Fiscal 2023

The following table summarizes our results of operations for the respective periods:

| | Three months ended September 30, | |

| | | 2023 | | | 2022 | |

| Revenue | $ | 605,445 | | $ | 255,371 | |

| Operating Expenses | | | | | | |

| General and administrative | | 2,798,250 | | | 1,504,376 | |

| Selling and marketing | | 685,637 | | | 364,913 | |

| R&D | | 618,028 | | | 454,048 | |

| Total operating expenses | | 4,101,915 | | | 2,323,337 | |

| Net loss | $ | (5,854,335 | ) | $ | (2,344,944 | ) |

Revenue

Total revenue increased by $0.3 million in Q4 ended September 30, 2023 compared to Q4 of Fiscal 2022, mainly due to an additional $0.4 million generated from our digitization business line offset by a $0.1 million decrease from our non-lethal business line (driven from sale of ARWEN products).

Operating Expenses

Total OPEX was $4.1 million for Q4 FY2023 compared to $2.3 million in Q4 of Fiscal 2022 for a total increase of $1.8M, a 77% increase over the comparable prior year quarter due to the following factors:

- G&A increased by $1.3 million, or 86%, primarily due to the impairment charge on the Phantom intangible asset incurred in Q4 Fiscal 2023, depreciation from $176K in PP&E additions throughout Fiscal 2023, offset by a decrease in salaries due to employee and management bonuses accrued during Fiscal 2022, as well as a decrease in consulting costs compared to Q4 of Fiscal 2022.

- S&M increased by $0.3 million, or 88%, primarily due to consulting fees incurred in Q4 Fiscal 2023compared to lower investor relations and promotion spend in Q4 of Fiscal 2022.

- R&D increased by $0.2 million, or 36%, primarily due to the majority of the LEC and Phantom R&D expenditures being capitalized in Q4 of Fiscal 2022 whereas fewer R&D expenses capitalized in Q4 of Fiscal 2023 from the write-off of the Phantom project, resulting in higher R&D operating costs in Q4 of Fiscal 2023. The related costs are reported as part of cost of sales (for delivered performance obligations to customers) and work-in-progress inventories.

Net Loss

As a result of the above, our net loss was $5.9 million for the quarter ended September 30, 2023, a $3.5 million increase from the Q4 period in Fiscal 2022; however, the Company has made significant efforts to reduce S&M and R&D costs throughout remaining quarters in Fiscal 2023.

B. Liquidity and Capital Resources

Financial Condition

The following table summarizes our financial position:

| | September 30, | | September 30, | | September 30, | |

| | | 2023 | | | 2022 | | | 2021 | |

| Assets | | | | | | | | | |

| Current | $ | 6,842,074 | | $ | 1,516,393 | | $ | 4,055,697 | |

| Non-current | | 4,916,758 | | | 5,807,070 | | | 4,662,149 | |

| Total assets | $ | 11,758,832 | | $ | 7,323,463 | | $ | 8,717,846 | |

| | | | | | | | | | |

| Liabilities | | | | | | | | | |

| Current | $ | 6,383,635 | | $ | 6,925,880 | | $ | 1,159,490 | |

| Non-current | | 1,439,577 | | | 1,400,474 | | | 1,434,628 | |

| Total liabilities | | 7,823,212 | | | 8,326,354 | | | 2,594,118 | |

| Net assets | $ | 3,935,620 | | $ | (1,002,891 | ) | $ | 6,123,728 | |

| | | | | | | | | | |

| Working capital (1) | $ | 458,439 | | $ | (5,409,487 | ) | $ | 2,896,207 | |

(1) Working capital is calculated as current assets less current liabilities.

Our working capital was positive $0.5 million at September 30, 2023, an increase of $5.9 million from September 30, 2022. The increase was primarily due to net proceeds from the U.S. IPO and Canadian Offering and the July 2023 Private Placement, offset partially by an increase to inventory and prepaid expenses, repayment of all outstanding loans, payments of overdue accounts payables and certain accrued liabilities, and net operating loss for Fiscal 2023. Current liabilities include warrant liabilities, a non-cash liability item (see Note 15 of Fiscal 2023 financial statements). Excluding warrant liabilities, working capital would be $6.8 million. These warrant liabilities will be extinguished when the warrants are exercised or expired. If exercised, the proceeds will provide us with additional capital to fund our future working capital requirements. There is no assurance that any warrants will be exercised.

Total assets increased by $4.4 million from September 30, 2022, mainly due to an increase of $5.3 million in currents assets made up mostly of net proceeds of the U.S. IPO and Canadian Offering and the July 2023 Private Placement, offset partially by inventory and prepaid expenses, repayment of all outstanding loans, payments of overdue accounts payables and certain accrued liabilities.

Total liabilities decreased by $0.5 million from September 30, 2022, to $7.8 million at September 30, 2023, mainly due to a reduction in current liabilities from having paid aged accounts payable subsequent to the closing of our NASDAQ IPO. While we have significantly paid the outstanding accounts payable and fully repaid all outstanding loans during the current year, these were offset by the recognition of warrant liabilities at fair value as noted above. As at September 30, 2023, we had $4.3 million of warrant liabilities.

Available Liquidity

Our approach to managing liquidity is to ensure, to the extent possible, that we always have sufficient liquidity to meet our liabilities as they come due. We regularly perform cash flow forecasts to ensure that we have sufficient cash to meet our operational needs while maintaining sufficient liquidity. At this time, we do not use any derivative financial instruments to hedge our currency risk.

On July 21, 2023, we closed the July 2023 Private Placement pursuant to which we received aggregate gross proceeds of USD$5.59 million (or CAD$7.4 million), before underwriting and offering costs (see below, Capital Resources, for further details including our expected use of proceeds). On December 9, 2022, we closed both the U.S. IPO and Canadian Offering pursuant to which we received aggregate gross proceeds of USD$14.1 million (or CAD$19.4 million), before underwriting and offering costs (see below, Capital Resources, for further details including our expected use of proceeds).

At September 30, 2023, our cash position was $5.4 million, an increase of $5.2 million since September 30, 2022 primarily due to net proceeds from the U.S. IPO and Canadian Offering and the July 2023 Private Placement, offset partially by repayment of all outstanding loans, payments of overdue accounts payables and certain accrued liabilities, and net operating loss for Fiscal 2023.

As an early-stage company, we have not yet reached commercial production for most of our other products and have incurred significant losses and negative operating cash flows from inception that have primarily been funded from financing activities. Our ability to continue as a going concern and realize our assets and discharge our liabilities in the normal course of business is dependent upon closing timely additional sales orders, timely commercial launch of new products, and the ability to raise additional debt or equity financing, when required. There are various risks and uncertainties affecting our future financial position and our performance. However, we may require additional capital in the event we fail to implement our business plan, which could have a material adverse effect on our financial condition and/or financial performance. There is no assurance that we will be able to raise additional capital as they are required in the future. Potential sources of capital may include additional equity and/or debt financings. In our view, the availability of capital will be affected by, among other things, capital market conditions, the success of our PARA OPS system commercialization efforts, timing for winning new customer contracts, potential acquisitions, and other relevant considerations (see Risk Factors). In the event we raise additional funds by issuing equity securities, our existing shareholders will likely experience dilution, and any additional incurrence of indebtedness would result in increased debt service obligations and could require us to agree to operational and financial covenants that could further restrict our operations. Any failure to raise additional funds on terms favorable to us or at all may require us to significantly change or curtail our current or planned operations in order to conserve cash until such time, if ever, that sufficient proceeds from operations are generated, and could result in us not being in a position to advance our commercialization strategy or take advantage of business opportunities.

Consolidated Statements of Cash Flows

The following table summarizes our consolidated statements of cash flows for the respective periods:

| | September 30, | | | September 30, | | | September 30, | |

| | | 2023 | | | 2022 | | | 2021 | |

| Total cash provided by (used in): | | | | | | | | | |

| Operating activities | $ | (14,078,630 | ) | $ | (4,256,596 | ) | $ | (6,255,213 | ) |

| Investing activities | | (1,440,733 | ) | | (1,113,793 | ) | | (1,073,192 | ) |

| Financing acitivities | | 20,755,827 | | | 2,852,829 | | | 6,942,750 | |

| Net cash outflows | $ | 5,236,464 | | $ | (2,517,560 | ) | $ | (385,655 | ) |

| Cash, beginning of period | | 170,545 | | | 2,688,105 | | | 3,073,760 | |

| Cash, end of period | $ | 5,407,009 | | $ | 170,545 | | $ | 2,688,105 | |

Cash used by operating activities

Cash flow used in operating activities increased by $9.8 million to $14.1 million for the year ended September 30, 2023 primarily due to payments on overdue payables as well as unpaid voluntary deferred wages, consulting fees, and bonuses until we closed the U.S. IPO and Canadian Offering, coupled with significant prepaid expenses during the year ended September 30, 2023. Prepaid expenses increased by $0.4 million mainly due to the renewal of D&O and commercial insurance coverage, capital market advisory services, and retention bonus for our head of PARA OPS (refundable in the event he voluntarily terminates prior to a specified date as set by us).

Cash used by investing activities

Cash flow used in investing activities was $1.4 million for the year ended September 30, 2023, an increase of $0.3 million from the comparable period, mainly due to additional investment in the product development of our PARA OPS, coupled with additional low-rate initial production equipment for PARA OPS.

Cash provided by financing activities

Cash flow provided by financing activities was $20.8 million in Fiscal 2023 compared to $2.9 million in Fiscal 2022 primarily due to net proceeds generated from the U.S. IPO and Canadian Offering and the July 2023 Private Placement, partially offset by repayment of all outstanding borrowings during the year ended September 30, 2023.

Capital Resources

Our objective in managing our capital is to safeguard our ability to continue as a going concern and to sustain future development of the business. Our senior management is responsible for managing the capital through regular review of financial information to ensure sufficient resources are available to meet operating requirements and investments to support its growth strategy. Our Board is responsible for overseeing this process. From time to time, we could issue new Common Shares or debt to maintain or adjust our capital structure. We are not subject to any externally imposed capital requirements.

Our primary sources of capital to date have been borrowings, security offerings, exercise of stock options and warrants, and, to a lesser extent, pre-commercial revenue. The following is a breakdown of our capital:

| | September 30, | | September 30, | | September 30, | |

| | | 2023 | | | 2022 | | | 2021 | |

| Debt: | | | | | | | | | |

| Lease obligations | $ | 429,523 | | $ | 275,621 | | $ | 307,909 | |

| Related party loans | | - | | | - | | | - | |

| Borrowings | | - | | | 2,278,774 | | | 53,251 | |

| Warrant liabilities | | 4,335,673 | | | - | | | - | |

| Equity: | | | | | | | | | |

| Share capital | | 33,379,110 | | | 19,496,640 | | | 17,215,068 | |

| Warrants | | 1,042,657 | | | 1,959,796 | | | 1,848,389 | |

| Contributed surplus | | 4,769,115 | | | 3,551,330 | | | 2,458,211 | |

| Accumulated other comprehensive loss | | (39,663 | ) | | (101,418 | ) | | (8,991 | ) |

| Accumulated deficit | | (35,215,599 | ) | | (25,909,239 | ) | | (15,388,949 | ) |

| Total capital | $ | 8,700,816 | | $ | 1,551,504 | | $ | 6,484,888 | |

During Fiscal 2023, we fully repaid all outstanding loans following the closing of the U.S. IPO and Canadian Offering.

Contractual Obligations and Commitments

At September 30, 2023, our contractual obligations and commitments were as follows:

| | | | | | | | | | | | | | | 5 years and | |

| Payment due: | | Total | | Within 1 Year | | 1 to 3 years | | 3 to 5 years | | | beyond | |

| Minimum royalty commitments | $ | 2,350,000 | | $ | 150,000 | | $ | 400,000 | | $ | 500,000 | | $ | 1,300,000 | |

| Accounts payable and accrued liabilities | | 1,649,876 | | | 1,649,876 | | | - | | | - | | | - | |

| Lease obligations | | 558,755 | | | 197,367 | | | 355,430 | | | 5,958 | | | - | |

| Total contractual obligations | $ | 4,558,631 | | $ | 1,997,243 | | $ | 755,430 | | $ | 505,958 | | $ | 1,300,000 | |

Shares Outstanding

At September 30, 2023, our authorized capital consists of an unlimited number of Common Shares with no stated par value.

The following table shows the outstanding Common Shares and dilutive securities at September 30, 2023:

| | | | | | Average | | | | |

| | | September 30, | | | price | | | Proceeds if | |

| | | 2023(1) | | | (CAD $) | | | Exercised | |

| Common shares | | 5,616,782 | | | | | | | |

| Founders' warrants | | 106,000 | | $ | 14.00 | | $ | 1,484,000 | |

| Warrants | | 21,429 | | $ | 0.61 | | $ | 13,072 | |

| Pre-funded warrants | | 1,129,548 | | $ | 0.01 | | $ | 11,295 | |

| Warrant liabilities | | 4,824,727 | | $ | 5.63 | | $ | 27,163,213 | |

| Over-allotment warrants | | 375,000 | | $ | 6.63 | | $ | 2,486,250 | |

| U.S. Underwriter warrants | | 258,587 | | $ | 5.14 | | $ | 1,329,137 | |

| Stock options | | 389,907 | | $ | 2.72 | | $ | 1,060,480 | |

| Restricted stock units (RSUs) | | 1,071 | | $ | - | | $ | - | |

| Agents' compensation options: | | | | | | | | | |

| Common shares | | 50,848 | | $ | 5.47 | | $ | 278,253 | |

| Warrants | | 50,848 | | $ | 6.63 | | $ | 336,868 | |

| | | | | | | | | | |

| Total common shares and dilutive securities | | 12,824,747 | | | | | $ | 34,162,568 | |

(1) Represents the number of shares to be issued upon exercise.

U.S. IPO and Canadian Offering

On December 9, 2022, we closed the U.S. IPO and Canadian Offering. In the U.S. IPO, we sold 2.5 million U.S. Common Units at a public offering price of US$4.13 per unit, consisting of one Common Share and one Warrant. The Warrants have a per share exercise price of US$5.00, could be exercised immediately, and expire five years from the date of issuance. In connection with the closing of the U.S. IPO, the underwriter partially exercised its over-allotment option to purchase an additional 199,000 pre-funded common share purchase warrants and 375,000 warrants to purchase Common Shares. All these warrants will expire on December 8, 2027.

In the Canadian Offering, we sold 726,392 units, each consisting of one Common Share and one warrant to purchase one Common Share, at a price to the public of US$4.13 per unit. The warrants will have a per Common Share exercise price of US$5.00, are exercisable immediately and expire five years from the date of issuance.

The closing of the U.S. IPO and Canadian Offering resulted in aggregate gross proceeds of US$14.1 million (CAD $19.4 million). After underwriting discounts and offering expenses, the net proceeds were US$11 million (CAD $15 million). See Note 16(a) of Fiscal 2023 financial statements for further details.

Use of Proceeds

As of September 30, 2023, the Company has used all of the US $11M of the net proceeds as outlined below:

| | | | Expected Use | | | Expected Use of | | | Actual Expenditures | |

| | | | of Proceeds In | | | Proceeds In | | | to Sep 30, 2023 In | |

| | Use of Net Proceeds from the US IPO (1) | | U.S . Dollars | | | CAD Dollars | | | CAD Dollars (8) | |

| | Repayment of non-secured borrowings: | | | | | | | | | |

| | Issued in March 2022 (2) | $ | 1,460,000 | | $ | 2,000,200 | | $ | 2,027,517 | |

| | Issued in August 2022 (3) | $ | 220,000 | | $ | 301,400 | | $ | 338,976 | |

| | CEBA loans (4) | $ | 51,000 | | $ | 69,870 | | $ | 70,000 | |

| | Product development (5) | $ | 529,000 | | $ | 724,730 | | $ | 683,450 | |

| | Corporate, general & administration, and working capital: | | | | | | | | | |

| | General and administrative (6) | $ | 2,469,000 | | $ | 3,382,530 | | $ | 4,128,985 | |

| | Selling and marketing | $ | 1,355,000 | | $ | 1,856,350 | | $ | 2,447,930 | |

| | Research and development, net | $ | 296,000 | | $ | 405,520 | | $ | 1,287,581 | |

| | Negative working capital at September 30, 2022 (excluding above loans) | $ | 2,286,226 | | $ | 3,132,130 | | $ | 3,132,130 | |

| | Unallocated working capital (7) | $ | 2,297,213 | | $ | 3,147,182 | | $ | 903,342 | |

| | Total use of net proceeds | $ | 10,963,439 | | $ | 15,019,911 | | $ | 15,019,911 | |

(1) For Canadian dollars denominated expenses, the amounts were converted at a rate of $1.37 to USD$1.00 on as reported by the Bank of Canada on December 16, 2022.

(2) The net proceeds were used to fund the Corporation's working capital.

(3) On December 13, 2022, one of the two non-secured loans issued in August 2022 was settled for KWESST Units (same terms as those Units offered in the Canadian Offering).

(4) This is net of $23,077 forgivable amount as we have repaid the CEBA loans due to the Canadian Government the repayment deadline for the forgivable amount.

(5) Estimate of Product development costs subsequent to IPO.

(6) Includes litigation settlement for two cases: $27,179 for an ex-employee & $141,123 for an ex-consultant. Excludes non-cash items such as depreciation, share-based costs & impairment costs

(7) Remaining unallocated costs incurred to PP&E additions, inventory additions and FX.

(8) Use of proceeds calculated on a first in, first out basis.

Shares for Debt Settlement

On December 13, 2022, we issued 56,141 units to settle $12,000 of the Unsecured Loans and USD$223,321 of the Secured Loan, including unpaid accrued interest and 10% premium at maturity. See Note 13(a) of Q2 Fiscal 2023 for further details.

Private Placement

On July 21, 2023, we closed the July 2023 Private Placement, resulting in the issuance of 1,542,194 Common Shares, for aggregate gross proceeds of USD$5,588,397 (approximately CAD$7.4M).

As a part of the July 2023 Private Placement, the Company issued 1,542,194 Common Shares at a price of US$2.26 (CAD$2.98) per Common Share and 930,548 pre-funded warrants at a price of US$2.259 (CAD$2.979) per pre-funded warrant (each a "Pre-funded Warrant"), with each Common Share and Pre-funded Warrant being bundled with one common share purchase warrant of the Company (each a "Common Warrant"). Each Pre-Funded Warrant entitles the holder to acquire one Common Share at an exercise price of US$0.001 per Common Share, and each Common Warrant is immediately exercisable and entitles the holder to acquire one Common Share at an exercise price of US$2.66 (CAD$3.50) per Common Share for a period of 60 months following the closing of the July 2023 Offering. Although the Common Shares and Pre-funded Warrants are each bundled with a Common Warrant, each security is issued separately. See Note 16(a) of Fiscal 2023 financial statements for further details.

Use of Proceeds

As of September 30, 2023, the Company has used $0.9M of the $6.3M net proceeds from the July 2023 Private Placement for general working capital purposes. Use of proceeds is estimated on a first in, first out basis.

Use of Proceeds from Prior Financings

The following table provides an approximate breakdown on the initial allocation of the use of funds for the 2021 brokered private placement and the actual use of proceeds:

| | | 2021 Financing | |

| | | | | | Estimated and | | | | |

| | | | | | Unaudited Actual | | | | |

| | | Expected | | | Use of Funds from | | | Proceeds | |

| | | Allocation of | | | April 29, 2021 to | | | Unspent as at | |

| | | Net Proceeds | | | September 30, | | | September 30, | |

| Use of Proceeds (1) | | | | | 2022 | | | 2022 | |

| Products development: (2) | | | | | | | | | |

| TASCS IFM (3) | $ | 400,000 | | $ | 314,087 | | $ | 85,913 | |

| BLDS | | 200,000 | | | 305,788 | | | (105,788 | ) |

| Phantom | | 500,000 | | | 793,852 | | | (293,852 | ) |

| GreyGhost | | 200,000 | | | 15,840 | | | 184,160 | |

| ATAK | | 500,000 | | | 304,162 | | | 195,838 | |

| LEC | | 500,000 | | | 761,943 | | | (261,943 | ) |

| | | | | | | | | | |

| Total products development | | 2,300,000 | | | 2,495,672 | | | (195,672 | ) |

| Other specific allocations: | | | | | | | | | |

| Repayment of CEO and employee loans | | 191,600 | | | 191,600 | | | - | |

| Repayment of unsecured borrowings | | 310,527 | | | 310,527 | | | - | |

| Prepaid royalties to DEFSEC (4) | | 150,000 | | | 150,000 | | | - | |

| Total allocated proceeds | | 2,952,127 | | | 3,147,799 | | | (195,672 | ) |

| Unallocated proceeds for working capital | | 2,516,366 | | | 2,320,694 | | | 195,672 | |

| Transferred from 2020 Financing | | 235,345 | | | 235,345 | | | - | |

| Total use of proceeds | $ | 5,703,838 | | $ | 5,703,838 | | $ | - | |

Notes:

(1) Excludes non-cash transactions settled in Common Shares.

(2) Includes concept & design, initial prototype, market testing, and pre-production including a few demo units. Costs includes internal labor costs, outsourced engineering costs, and materials (no overhead allocation).

(3) Net of customer funding of $1.0 million.

(4) In connection with the PARA OPS System acquisition.

Off-Balance Sheet Arrangements

We have no off-balance sheet arrangements that have or are reasonably likely to have, a current or future effect on our results of operations, financial condition, revenues or expenses, liquidity, capital expenditures or capital resources.

C. Research and Development, Patents and Licences, etc.

See Item 5.A. - Operating Results - Results of Operations for a description of our research and development activities during the last three fiscal years.

See Item 4.B. - Business Overview - Proprietary Protection for a listing of patents and product development in progress.

D. Trend Information

See Item 5.A. - Operating Results - Results of Operations and Item 5.B. - Liquidity and Capital Resources for trend information.

E. Critical Accounting Estimates.

The following is a summary of critical accounting policies, requiring management to make significant estimates and assumptions:

Revenue

Revenue is recognized upon transfer of control of products or services to customers at an amount that reflects the transaction price we expect to receive in exchange for the products or services. Our contracts with customers may include the delivery of multiple products and services, which are generally capable of being distinct and accounted for as separate performance obligations. The accounting for a contract or contracts with a customer that contain multiple performance obligations requires us to allocate the contract or contracts transaction price to the identified distinct performance obligations.

Revenue from contracts with customers is recognized, for each performance obligation, either over a period of time or at a point in time, depending on which method reflects the transfer of control of the goods or services underlying the particular obligation to the customer.

For performance obligations satisfied over time, we recognize revenue over time using an input method, based on costs incurred to date relative to total estimated costs at completion, to measure progress toward satisfying such performance obligation (for non-recurring engineering services, the input method is based on hours). Under this method, costs that do not contribute to our performance in transferring control of goods or services to the customer are excluded from the measurement of progress toward satisfying the performance obligation. In certain other situations, we might recognize revenue at a point in time, when the criteria to recognize revenue over time are not met. In any event, when the total anticipated costs exceed the total anticipated revenues on a contract, such loss is recognized in its entirety in the period it becomes known. Refer to Note 18 of Fiscal 2023 financial statements for timing of revenue recognition.

We may enter into contractual arrangements with a customer to deliver services on one project with respect to more than one performance obligation, such as non-recurring engineering, procurement, and training. When entering into such arrangements, we allocate the transaction price by reference to the stand-alone selling price of each performance obligation. Accordingly, when such arrangements exist on the same project, the value of each performance obligation is based on its stand-alone price and recognized according to the respective revenue recognition methods described above. For example, for non-recurring engineering services rendered over a contract period the revenue is recognized using the percentage of completion method; whereas for training services the revenue is recognized after the training is delivered (i.e. point in time).

We account for a contract modification, which consists of a change in the scope or price (or both) of a contract, as a separate contract when the remaining goods or services to be delivered after the modification are distinct from those delivered prior to the modification and the price of the contract increases by an amount of consideration that reflects our stand-alone selling price of the additional promised goods or services. When the contract modification is not accounted for as a separate contract, we recognize an adjustment to revenue on a cumulative catch-up basis at the date of contract modification. There was no contract modification in the fiscal years ended September 30, 2023, 2022, and 2021.

The timing of revenue recognition often differs from performance payment schedules, resulting in revenue that has been earned but not billed. These amounts are included in unbilled receivables. At September 30, 2023, and 2022, we had an immaterial amount of unbilled receivable. Amounts billed in accordance with customer contracts, but not yet earned, are recorded and presented as part of contract liabilities. At September 30, 2023 there was $121 thousand of contract liabilities (2022 - $47 thousand).

When a contract includes a significant financing component, the value of such component is excluded from the transaction price and is recognized separately as finance income or expense, as applicable.

Accounting for acquisitions and contingent consideration

During Fiscal 2022, we acquired Police Ordnance and accounted for it pursuant to IFRS 3, Business Combinations. Areas of significant estimation in connection with the accounting of this transaction included:

- the estimated fair value of raw and work-in-progress inventories and intangible assets for the purchase price allocation; and

- the volatility assumption used in the Black Scholes option model to estimate the fair value of the warrants issued to the selling shareholders given our short history as a public company.

During Fiscal 2021, we acquired the PARA OPS system and accounted for it pursuant to IFRS 2, Share-Based Payment. Areas of significant estimation in connection with the acquisition of the PARA OPS system included:

- the determination of the discount rate for the present value of the minimum annual royalty payments to DEFSEC; and

- the volatility assumption used in the Black Scholes option model to estimate the fair value of the warrants issued to DEFSEC given our short history as a public company (see Item 5.E - Critical Accounting Estimates - Accounting for share-based compensation).

For further details on the above acquisitions, refer to Note 4 of the Fiscal 2023 financial statements.

Impairment of long-lived assets

We review property and equipment for impairment whenever events or changes in circumstances indicate the carrying amount may not be recoverable. An impairment loss is recognized the carrying value of an asset exceeds its recoverable amount. The recoverable amount is the higher of an asset's fair value less costs to sell and value in use. For the purpose of assessing impairment, assets are grouped at the lowest levels for which there are separately identifiable cash flows, referred as the cash generating unit ("CGU").

In accordance with IFRS, if the sum of the undiscounted expected future cash flows from a long-lived asset is less than the carrying value of that asset, then we recognize an asset impairment charge. The impairment charge is determined based on the excess of the asset's carrying value over its fair value, which generally represents the discounted future cash flows from that asset.

Because we are an early-commercial stage technology company, management exercises significant judgment in establishing key assumptions and estimates to determine the recoverable amount of our CGU, including future cash flows based on historical and budgeting operating results, growth rates, tax rates, and appropriate after-tax discount rates. The actual results may vary and may cause significant adjustments in future periods.

Impairment of non-financial assets

We review non-financial assets for impairment whenever events or changes in circumstances indicate the carrying amount of the assets may be impaired. If the recoverable amount of the respective non-financial asset is less than our carrying amount, it is considered to be impaired. Management exercises significant judgement in estimating the recoverable amount for non-financial assets (see Item 5.E - Critical Accounting Estimates - Impairment of long-lived assets).

Accounting for share-based compensation

We measure share-based compensation at fair value. Key inputs in the Black Scholes option model is the volatility assumption, forfeiture rate, and expected life of our Common Shares. Due to our limited trading history, management has established a relevant peer group of listed companies and selected the weighted average of their volatilities over a period of three to five years, where available. Starting in Fiscal 2021, we have commenced to incorporate a percentage of our stock volatility in the overall calculation of the volatility assumption. We rely on our stock volatility to estimate the fair value of share-based compensation as well as for warrants. As a result of our limited trading history, we have assumed a forfeiture rate of 0%, which will be reassessed annually. The expected life is estimated based on our trading history.

Accounting for Unsecured Loans

Due to the issuance of bonus Common Shares as part of the unsecured loans transactions during Fiscal 2022, we are required to allocate a percentage of the gross proceeds between the bonus Common Shares and the debt component based on their relative fair value. To measure the fair value of the unsecured loans, we used the income approach and estimated a market discount rate ranging from 22% - 24% to discount the future cash flows of the unsecured loans. Management selected a discount rate based on review of the debt cost for comparable public companies.

For further information on the unsecured loans, see Note 12 of the Fiscal 2022 financial statements.

Broker compensation options

As a result of the private placement in April 2021, we issued broker compensation options. To measure the fair value of the broker compensation options, we used the Monte Carlo valuation model and exercised judgment in estimating the life, risk free rate, and volatility.

For further information on the broker compensation options see Note 16(c) of the Fiscal 2023 financial statements.

ITEM 6. DIRECTORS, SENIOR MANAGEMENT AND EMPLOYEES

A. Directors and Senior Management

The following table sets forth the name of each of our directors and executive officers, as well as such individual's place of residence, position with us, principal business activities performed outside those with us and period of service as a director (if applicable).

Directors and Executive Officers

| Name | Position With | Age | Principal Business Activity | Director/Officer Since |

| | KWESST Micro | | Outside KWESST Micro | |

| David Luxton | Executive Chairman and Director | 71 | N/A | October 24, 2019(1) |

Ontario, Canada | | | | |

| Sean Homuth | President, CEO(6) | 45 | N/A | June 12, 2023(2) |

Ontario, Canada | | | | |

Paul Mangano (3) Maine, United States | Director | 65 | Founder and Owner, Surculus Advisors LLC and General Manager, Steiner Optics Inc. (up to April 2022), CEO of OnPoint Systems, Inc. since August 2022 | September 17, 2020 |

| Paul Fortin (3) Ontario, Canada | Director | 55 | Senior Associate, David Pratt & Associates and Independent Advisor

| September 17, 2020 |

John McCoach (3)

British Columbia, Canada | Director | 66 | Director and Chairman of the Audit Committee, Xybion Digital Inc.; Vice Chairman, Royal Canadian Marine Search and Rescue

| November 28, 2017(4) |

Kris Denis

Ontario, Canada | Interim Chief Financial Officer and Chief Compliance Officer

| 42 | N/A | November 27, 2023(5) |

Rick Hillier

Ontario, Canada | Director | 68 | Consultant | December 6, 2023(7) |

Notes:

(1) Date on which Mr. Luxton became a director of KWESST.

(2) Mr. Homuth became CEO of KWESST on November 27, 2023. From June 12, 2023 to November 26, 2023, Mr. McLeod served as President and CEO of KWESST.

(3) A member of the Audit Committee. Mr. McCoach is Chair of the Audit Committee.

(4) Date on which Mr. McCoach became a director of Foremost.

(5) Date on which Mr. Denis became interim Chief Financial Officer of KWESST

(6) As at September 30, 2023, Mr. Jeffrey McLeod held the office of Director, President and Chief Executive Officer of the Company, until his resignation on October 31, 2023.

(7) Mr. Hillier was appointed to the Board of December 6, 2023.

The following are brief biographies of our directors and executive officers.

David Luxton, Executive Chairman and Director

David Luxton is an entrepreneur in the defense and security industry. He is a former Canadian infantry officer, and former senior official with the Canadian and British governments. In 1990 he founded Simunition, a business that develops and sells simulated munitions for realistic close quarters combat training for military and law enforcement. Between 2003 and 2009, he led the expansion of the Allen-Vanguard Corporation, a company in the IED countermeasures business, from approximately $3,000,000 to a run rate of approximately $300,000,000 in annual revenues, then served as Chairman from 2010 to October 2021. Between 2015 and 2018, he was the Executive Chairman of United Tactical Systems, LLC, a company offering non-lethal products for law enforcement, military and personal defense. From 2003 to the date of this Annual Report, he has been President & Owner of DEFSEC, a company that specializes in strategic transactions in the defense and security industry. Furthermore, from 2016 to 2020, he was a Senior Strategic Advisor to the University of Ottawa. Since 2019, he has been the Executive Chairman of KWESST. He holds a SMDP postgraduate studies from the University of Oxford. He entered into a confidentiality and non-disclosure agreement through his consulting agreement with us on October 1, 2019.

Sean Homuth, President and Chief Executive Officer

Mr. Homuth is a senior financial executive with more than 20 years of experience working with both Canadian and U.S. public companies across a broad range of industries. He has experience with a variety of financing (equity, debt, royalty) and M&A transactions. Since 2008, he has spent the majority of his time in various senior executive roles with emerging companies. Mr. Homuth is a Chartered Professional Accountant (CPA, CA Ontario) and a Certified Public Accountant (Illinois).

Paul Mangano - Director

Prior to being invited to join our Board, Mr. Mangano founded and owned Surculus Advisors LLC since 2016, a boutique management consulting firm providing advice, leadership, specialized expertise and transaction consultation services to the industrial and high-tech sectors including aerospace, defense and security. Further, since August 2022, he is the CEO of Onpoint Systems, Inc. From August 2020 to April 2022, he was the General Manager of Steiner Optics Inc., a division of Beretta. Prior to forming Surculus Advisors LLC, from 2006 to 2015, he served as the President of L-3 Communication's Public Safety & Sporting business unit. Mr. Mangano graduated with a BA in Economics from Harvard University and an MBA in High Technology from Northeastern University.

Paul Fortin - Director

Prior to being invited to join our Board, Paul Fortin was the director of international business development at Borden Ladner Gervais LLP, a full-service law firm, from 2011 to 2019. Since March 2020, he has been working with David Pratt & Associates as a Senior Associate and is an independent advisor within the defense and security industry. Mr. Fortin graduated from Carleton University with a Bachelor's degree in Political Science and from Algonquin College with a specialization in Product Marketing Management.

John McCoach - Director

Prior to being invited to join our Board, John McCoach held multiple senior positions in various companies, including seven years as the President of the TSXV. John McCoach was a member of the Capital Markets Authority Implementation Organization Board of Directors from 2016 to 2021. Mr. McCoach is an independent director and the current Audit Committee Chairman of Xybion Digital Inc. since November 2021. He also served as Interim CEO and as a director of Foremost Ventures Corp., a position he held from 2018 until the Qualifying Transaction with KWESST Inc. Finally, Mr. McCoach is an active crew member, and Vice Chairman of, Royal Canadian Marine Search and Rescue.

Kris Denis - Interim Chief Financial Officer and Chief Compliance Officer

Mr. Denis has 20 years' experience in all aspects of financial management with private and public companies, large and small, across a wide range of industries. Mr. Denis has spent the majority of his career in increasingly senior positions with publicly traded companies. Mr. Denis is a Chartered Professional Accountant (CPA, CA Ontario).

Rick Hillier - Director

General (Retired) Rick Hillier served over 35 years in the Canadian Armed Forces, culminating his career as the Chief of Defence Staff from 2005-2008. His leadership, geopolitical knowledge and experience on multinational operations, at the tactical, operational and strategic levels, prepares him to help position the Company for success and navigate the Company through its next stages of growth.

Board Diversity Matrix

| Board Diversity Matrix (As of January 17, 2024) |

| Country of Principal Executive Offices: | Canada |

| Foreign Private Issuer | Yes |

| Disclosure Prohibited under Home Country Law | No |

| Total Number of Directors | 5 |

| | Female | Male | Non-Binary | Did Not Disclose Gender |

| Part I: Gender Identity | |

| Directors | 0 | 5 | - | - |

| Part II: Demographic Background | |

| Under-represented person in Home Country | 0 |

| LGBTQ+ | 0 |

| White | 5 |

On August 6, 2021, the SEC approved Nasdaq Listing Rule 5605(f) regarding board diversity. Under the rule, NASDAQ-listed companies, that are also foreign issuers, are required to include, or explain why it has not included (as the case may be), at least one "Diverse" director prior to December 31, 2023 and at least two "Diverse" directors by December 31, 2025. Under Nasdaq Listing Rule 5605(f)(2)(D), boards of directors composed of five or fewer members must have one director who is "Diverse."

The composition of our Board does not currently include an individual who is "Diverse" under the Nasdaq Listing Rule 5605(f), as presented in the above Board Diversity Matrix. We are mindful of the benefit that diversity can provide in maximizing the effectiveness and decision-making abilities of our Board. In this regard, we are committed to increasing diversity on our Board and moving forward, in our searches for new director candidates, we will consider the level of diversity, including representation of underrepresented individuals and female representation, on the Board, which will be one of several factors used in the search process.

B. Compensation

Compensation for Fiscal 2023

The aggregate amount of compensation paid during the year ended September 30, 2023 (including accrued amount at September 30, 2023), directly and indirectly, including directors' fees, to our named executive officers and directors in their capacity as such, was $1.5 million (Fiscal 2022: $1.2 million).

This discussion describes our compensation program for each person who acted as President and CEO, CFO and the three most highly-compensated executive officers (or three most highly-compensated individuals acting in a similar capacity), other than the CEO and the CFO, whose total compensation was more than $150,000 in our last fiscal year and who was performing a policy-making function in respect of the Company (each a "NEO" and collectively the "NEOs"). This section addresses our philosophy and objectives and provides a review of the process that the Board follows in deciding how to compensate the NEOs. This section also provides discussion and analysis of the Board's specific decisions about the compensation of the NEOs for the fiscal year ended September 30, 2023. We had five (6) NEOs during the fiscal year ended September 30, 2023, namely: David Luxton, Executive Chairman and Director, Sean Homuth, CFO and CCO, Jeffery MacLeod, former President and CEO, Steven Archambault, former CFO, VP, Corporate Services & Compliance, and interim Corporate Secretary, Harry Webster, Genreal Manager and Richard Bowes, VP, Operations of Digitzation & Tactical Products.

Compensation Philosophy and Objectives

Our current executive compensation program is designed to provide short and long-term rewards to our executives that are consistent with individual and corporate performance and their contribution to our short and long-term objectives. Our objectives with respect to compensation of executive officers are to provide compensation levels necessary to attract and retain high quality executives, and to motivate key executives to contribute to our interests. These objectives are to be met by the principal components of our executive compensation program, which has been focused on a combination of base compensation, cash bonus remuneration, and long-term incentives in the form of stock options or other security-based compensation.

The executive compensation program adopted by us and applied to our executive officers is designed to:

(a) attract and retain qualified and experienced executives who will contribute to our growth and success;