| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-255181-01 | ||

November 1, 2021

Free Writing Prospectus

Structural and Collateral Term Sheet

$918,586,612

(Approximate Initial Mortgage Pool Balance)

$781,946,000

(Offered Certificates)

3650R 2021-PF1 Commercial Mortgage Trust

As Issuing Entity

3650 REIT Commercial Mortgage Securities II LLC

As Depositor

Commercial Mortgage Pass-Through Certificates, Series 2021-PF1

3650 Real Estate Investment Trust 2 LLC

Citi Real Estate Funding Inc.

German American Capital Corporation

As Sponsors and Mortgage Loan Sellers

STATEMENT REGARDING THIS FREE WRITING PROSPECTUS

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-255181) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc., Deutsche Bank Securities Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of the email communication to which this free writing prospectus is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) no representation being made that these materials are accurate or complete and that these materials may not be updated or (3) these materials possibly being confidential, are, in each case, not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

| Citigroup | Deutsche Bank Securities |

Co-Lead Managers and Joint Bookrunners

| |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-255181) the “Registration Statement”) for the offering to which this communication relates. Before you invest, you should read the prospectus in the Registration Statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc. or Deutsche Bank Securities Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

| CERTIFICATE SUMMARY |

The securities offered by this structural and collateral term sheet (this “Term Sheet”) are described in greater detail in the preliminary prospectus, dated on or about November 1, 2021, included as part of our registration statement (SEC File No. 333-255181) (the “Preliminary Prospectus”). The Preliminary Prospectus contains material information that is not contained in this Term Sheet (including, without limitation, a summary of risks associated with an investment in the offered securities under the heading “Summary of Risk Factors” and a detailed discussion of such risks under the heading “Risk Factors”). The Preliminary Prospectus is available upon request from Citigroup Global Markets Inc. or Deutsche Bank Securities Inc. This Term Sheet is subject to change.

For information regarding certain risks associated with an investment in this transaction, refer to “Summary of Risk Factors” and “Risk Factors” in the Preliminary Prospectus. Capitalized terms used but not otherwise defined in this Term Sheet have the respective meanings assigned to those terms in the Preliminary Prospectus.

The Securities May Not Be a Suitable Investment for You

The securities offered by this Term Sheet are not suitable investments for all investors. In particular, you should not purchase any class of securities unless you understand and are able to bear the prepayment, credit, liquidity and market risks associated with that class of securities. For those reasons and for the reasons set forth under the headings “Summary of Risk Factors” and “Risk Factors” in the Preliminary Prospectus, the yield to maturity of, the aggregate amount and timing of distributions on and the market value of the offered securities are subject to material variability from period to period and give rise to the potential for significant loss over the life of those securities. The interaction of these factors and their effects are impossible to predict and are likely to change from time to time. As a result, an investment in the offered securities involves substantial risks and uncertainties and should be considered only by sophisticated institutional investors with substantial investment experience with similar types of securities and who have conducted appropriate due diligence on the mortgage loans and the securities. Potential investors are advised and encouraged to review the Preliminary Prospectus in full and to consult with their legal, tax, accounting and other advisors prior to making any investment in the offered securities described in this Term Sheet.

The securities offered by these materials are being offered when, as and if issued. This Term Sheet is not to be construed as an offer to sell or the solicitation of any offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. The information contained in this Term Sheet may not pertain to any securities that will actually be sold. The information contained in this Term Sheet may be based on assumptions regarding market conditions and other matters as reflected in this Term Sheet. We make no representations regarding the reasonableness of such assumptions or the likelihood that any of such assumptions will coincide with actual market conditions or events, and this Term Sheet should not be relied upon for such purposes. We and our affiliates, officers, directors, partners and employees, including persons involved in the preparation or issuance of this Term Sheet may, from time to time, have long or short positions in, and buy or sell, the securities mentioned in this Term Sheet or derivatives thereof (including options). Information contained in this Term Sheet is current as of the date appearing on this Term Sheet only. Information in this Term Sheet regarding the securities and the mortgage loans backing any securities discussed in this Term Sheet supersedes all prior information regarding such securities and mortgage loans. None of Citigroup Global Markets Inc. or Deutsche Bank Securities Inc. provides accounting, tax or legal advice.

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-255181) the “Registration Statement”) for the offering to which this communication relates. Before you invest, you should read the prospectus in the Registration Statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc. or Deutsche Bank Securities Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

2

| CERTIFICATE SUMMARY |

The issuing entity will be relying on an exclusion or exemption from the definition of “investment company” under the Investment Company Act of 1940, as amended (the “Investment Company Act”), contained in Section 3(c)(5) of the Investment Company Act or Rule 3a-7 under the Investment Company Act, although there may be additional exclusions or exemptions available to the issuing entity. The issuing entity is being structured so as not to constitute a “covered fund” for purposes of the Volcker Rule under the Dodd-Frank Act (both as defined in “Risk Factors—General Risk Factors—Legal and Regulatory Provisions Affecting Investors Could Adversely Affect the Liquidity of the Offered Certificates” in the Preliminary Prospectus). See also “Legal Investment” in the Preliminary Prospectus.

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-255181) the “Registration Statement”) for the offering to which this communication relates. Before you invest, you should read the prospectus in the Registration Statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc. or Deutsche Bank Securities Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

3

| CERTIFICATE SUMMARY |

| OFFERED CERTIFICATES | |||||||

Offered Classes | Expected Ratings | Approximate Initial Certificate Balance or Notional | Approximate Initial Credit Support(3) | Initial Pass-Through Rate(4) | Pass-Through Rate Description | Expected | Expected Principal Window(5) |

| Class A-1 | AAA(sf)/AAAsf/AAA(sf) | $26,952,000 | 30.000% | % | (6) | 2.63 | 12/21 – 10/26 |

| Class A-3 | AAA(sf)/AAAsf/AAA(sf) | $141,041,000 | 30.000% | % | (6) | 6.65 | 04/28 – 12/28 |

| Class A-4 | AAA(sf)/AAAsf/AAA(sf) | (7) | 30.000% | % | (6) | (7) | (7) |

| Class A-5 | AAA(sf)/AAAsf/AAA(sf) | (7) | 30.000% | % | (6) | (7) | (7) |

| Class A-SB | AAA(sf)/AAAsf/AAA(sf) | $22,719,000 | 30.000% | % | (6) | 6.89 | 10/26 – 05/31 |

| Class X–A | AAA(sf)/AAAsf/AAA(sf) | $691,236,000(8) | N/A | % | Variable IO(9) | N/A | N/A |

| Class X-B | NR/A-sf/AAA(sf) | $90,710,000(8) | N/A | % | Variable IO(9) | N/A | N/A |

| Class A-S | AAA(sf)/AAAsf/AAA(sf) | $48,226,000 | 24.750% | % | (6) | 9.93 | 10/31 – 11/31 |

| Class B | AA-(sf)/AA-sf/AA(sf) | $43,633,000 | 20.000% | % | (6) | 9.99 | 11/31 – 11/31 |

| Class C | NR/A-sf/A-(sf) | $47,077,000 | 14.875% | % | (6) | 9.99 | 11/31 – 11/31 |

| NON-OFFERED CERTIFICATES(10) | |||||||

Non-Offered Classes | Expected Ratings | Approximate Initial Certificate Balance or Notional | Approximate Initial Credit Support(3) | Initial Pass-Through Rate(4) | Pass-Through Rate Description | Expected | Expected Principal Window(5) |

| Class X-D | NR/BBB-sf/BBB(sf) | $40,648,000(8) | N/A | % | Variable IO(9) | N/A | N/A |

| Class D | NR/BBBsf/BBB+(sf) | $29,854,000 | 11.625% | % | (6) | 9.99 | 11/31 – 11/31 |

| Class E | NR/BBB-sf/BBB(sf) | $10,794,000(11) | 10.450% | % | (6) | 9.99 | 11/31 – 11/31 |

| Class F-RR | NR/BBB-sf/BBB-(sf) | $14,468,000(11) | 8.875% | % | (6) | 9.99 | 11/31 – 11/31 |

| Class G-RR | NR/BB-sf/BB-(sf) | $26,409,000 | 6.000% | % | (6) | 9.99 | 11/31 – 11/31 |

| Class J-RR | NR/B-sf/B-(sf) | $11,482,000 | 4.750% | % | (6) | 9.99 | 11/31 – 11/31 |

| Class NR-RR | NR/NR/NR | $43,633,611 | 0.000% | % | (6) | 9.99 | 11/31 – 11/31 |

| Class Z(12) | NR/NR/NR | N/A | N/A | N/A | N/A | N/A | N/A |

| Class R(13) | NR/NR/NR | N/A | N/A | N/A | N/A | N/A | N/A |

| (1) | It is a condition of issuance that the offered certificates and certain classes of non-offered certificates receive the ratings set forth above. The anticipated ratings shown are those of S&P Global Ratings, acting through Standard & Poor’s Financial Services LLC (“S&P”), Fitch Ratings, Inc. (“Fitch”) and Kroll Bond Rating Agency, LLC (“KBRA” and, together with S&P and Fitch, the “Rating Agencies”). Subject to the discussion under “Ratings” in the Preliminary Prospectus, the ratings on the certificates address the likelihood of the timely receipt by holders of all payments of interest to which they are entitled on each distribution date and, except in the case of the interest-only certificates, the ultimate receipt by holders of all payments of principal to which they are entitled on or before the applicable rated final distribution date. Certain nationally recognized statistical rating organizations, as defined in Section 3(a)(62) of the Securities Exchange Act of 1934, as amended, that were not hired by the depositor may use information they receive pursuant to Rule 17g-5 under the Securities Exchange Act of 1934, as amended, or otherwise to rate the offered certificates. We cannot assure you as to what ratings a non-hired nationally recognized statistical rating organization would assign. See “Risk Factors—Other Risks Relating to the Certificates—Nationally Recognized Statistical Rating Organizations May Assign Different Ratings to the Certificates; Ratings of the Certificates Reflect Only the Views of the Applicable Rating Agencies as of the Dates Such Ratings Were Issued; Ratings May Affect ERISA Eligibility; Ratings May Be Downgraded” in the Preliminary Prospectus. The Rating Agencies have informed us that the “sf” designation in the ratings represents an identifier of structured finance product ratings. For additional information about this identifier, prospective investors can go to the related Rating Agency’s website. The depositor and the underwriters have not verified, do not adopt and do not accept responsibility for any statements made by the Rating Agencies on those websites. Credit ratings referenced throughout this Term Sheet are forward-looking opinions about credit risk and express a rating agency’s opinion about the willingness and ability of an issuer of securities to meet its financial obligations in full and on time. Ratings are not indications of investment merit and are not buy, sell or hold recommendations, a measure of asset value or an indication of the suitability of an investment. |

| (2) | Approximate, subject to a variance of plus or minus 5% and further subject to any additional variances described in the footnotes below. In addition, the notional amounts of the Class X-A, Class X-B, and Class X-D, certificates (collectively, the “Class X Certificates”) may vary depending upon the final pricing of the Class A-1, Class A-3, Class A-4, Class A-5, Class A-SB, Class A-S, Class B, Class C, Class D, Class E, Class F-RR, Class G-RR, Class J-RR, and Class NR-RR certificates (collectively, the “Principal Balance Certificates”), and, if as a result of such pricing (a) the pass-through rate of any class of Class X Certificates, would be equal to zero at all times, such class of Class X Certificates will not be issued on the closing date of this securitization (the “Closing Date”) or (b) the pass-through rate of any class of Principal Balance Certificates whose certificate balance comprises such notional amount is at all times equal to the weighted average of the net interest rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as in effect from time to time (the “WAC Rate”), the certificate balance of such class of Principal Balance Certificates may not be part of, and there would be a corresponding reduction in, such notional amount of the related class of Class X Certificates. |

| (3) | The initial credit support percentages set forth the certificates are approximate and, for the Class A-1, Class A-3, Class A-4, Class A-5, and Class A-SB certificates, are represented in the aggregate. |

| (4) | Approximate per annum rate as of the Closing Date. |

| (5) | Determined assuming that there are no prepayments, modifications or losses in respect of the mortgage loans and that there are no extensions or forbearances of maturity dates or anticipated repayment dates of the mortgage loans and based on the assumptions set forth under “Yield and Maturity Considerations—Weighted Average Life” in the Preliminary Prospectus. |

| (6) | For any distribution date, the pass-through rate for each class of the Class A-1, Class A-3, Class A-4, Class A-5, Class A-SB, Class A-S, Class B, Class C, Class D, Class E, Class F-RR, Class G-RR, Class J-RR and Class NR-RR certificates will generally be equal to one of (i) a fixed per annum rate, (ii) the WAC Rate, (iii) the lesser of a specified per annum rate and the WAC Rate, or (iv) the WAC Rate less a specified percentage, but no less than 0.000%. See “Description of the Certificates—Distributions—Pass-Through Rates” in the Preliminary Prospectus. |

| (7) | The exact initial certificate balances of the Class A-4 and Class A-5 certificates are unknown and will be determined based on the final pricing of those classes of certificates. However, the respective approximate initial certificate balances, weighted average lives and expected principal windows of the Class A-4 and |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-255181) the “Registration Statement”) for the offering to which this communication relates. Before you invest, you should read the prospectus in the Registration Statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc. or Deutsche Bank Securities Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

4

| CERTIFICATE SUMMARY |

| Class A-5 certificates are expected to be within the applicable ranges reflected in the following chart. The aggregate initial certificate balance of the Class A-4 and Calass A-5 certificates is expected to be approximately $452,298,000 subject to a variance of plus or minus 5%. |

Class of Certificates | Expected Range of Approximate Initial Certificate Balances | Expected Range of Weighted Avg. Lives (Yrs) | Expected Range of Principal Windows |

| Class A-4 | $0 – $195,000,000 | N/A – 9.27 | N/A / 02/30 – 07/31 |

| Class A-5 | $257,298,000 – $452,298,000 | 9.76 – 9.55 | 07/31-10/31 / 02/30 – 10/31 |

| (8) | The Class X Certificates will not have certificate balances and will not be entitled to receive distributions of principal. Interest will accrue on each class of Class X Certificates at the related pass-through rate based upon the related notional amount. The notional amount of each class of the Class X Certificates will be equal to the aggregate of the certificate balances, as applicable, from time to time of the class or classes of the Principal Balance Certificates identified in the same row as such class of Class X Certificates in the chart below (as to such class of Class X Certificates, the “Corresponding Principal Balance Certificates”): |

| Class of Class X Certificates | Class(es) of Corresponding Principal Balance Certificates |

| Class X-A | Class A-1, Class A-3, Class A-4, Class A-5, Class A-SB and Class A-S |

| Class X-B | Class B and Class C |

| Class X-D | Class D and Class E |

| (9) | The pass-through rate for each class of Class X Certificates will generally be a per annum rate equal to the excess, if any, of (i) the WAC Rate over (ii) the pass-through rate (or, if applicable, the weighted average of the pass-through rates) of the class or classes of Corresponding Principal Balance Certificates as in effect from time to time, as described in the Preliminary Prospectus. See “Description of the Certificates—Distributions—Pass-Through Rates” in the Preliminary Prospectus. |

| (10) | The classes of certificates set forth below “Non-Offered Certificates” in the table are not offered by this Term Sheet. |

| (11) | The initial certificate balance of each of the Class E and Class F-RR certificates is subject to change based on final pricing of all Principal Balance Certificates and Class X Certificates and the final determination of the amounts of the Class F-RR, Class G-RR, Class J-RR and Class NR-RR certificates (collectively, the “HRR Certificates”) that will be retained by the retaining sponsor (or its majority-owned affiliate) as described under “Credit Risk Retention” to satisfy the U.S. risk retention requirements of 3650 Real Estate Investment Trust 2 LLC, as retaining sponsor. For more information regarding the methodology and key inputs and assumptions used to determine the sizing of the HRR Certificates, see “Credit Risk Retention” in the Preliminary Prospectus. |

| (12) | The Class Z certificates will not have a certificate balance, notional amount, pass-through rate, assumed final distribution date, rating or rated final distribution date. The Class Z certificates will only entitle holders to excess interest accrued on the mortgage loans with an anticipated repayment date. See “Description of the Mortgage Pool—Certain Terms of the Mortgage Loans—ARD Loans” in the Preliminary Prospectus. |

| (13) | The Class R certificates will not have a certificate balance, notional amount, pass-through rate, assumed final distribution date, rating or rated final distribution date. The Class R certificates represent the residual interests in each real estate mortgage investment conduit created with respect to this securitization, as further described in the Preliminary Prospectus. The Class R certificates will not be entitled to distributions of principal or interest. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-255181) the “Registration Statement”) for the offering to which this communication relates. Before you invest, you should read the prospectus in the Registration Statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc. or Deutsche Bank Securities Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

5

| MORTGAGE POOL CHARACTERISTICS |

| Mortgage Pool Characteristics(1) | |

| Initial Pool Balance(2) | $918,586,612 |

| Number of Mortgage Loans | 35 |

| Number of Mortgaged Properties | 42 |

| Average Cut-off Date Balance | $26,245,332 |

| Weighted Average Mortgage Rate | 3.40618% |

| Weighted Average Remaining Term to Maturity/ARD (months)(3) | 110 |

| Weighted Average Remaining Amortization Term (months)(4) | 314 |

| Weighted Average Cut-off Date LTV Ratio(5)(6) | 57.1% |

| Weighted Average Maturity Date/ARD LTV Ratio(3)(5) | 54.2% |

| Weighted Average UW NCF DSCR(7) | 2.69x |

| Weighted Average Debt Yield on Underwritten NOI(6)(8) | 10.2% |

| % of Initial Pool Balance of Mortgage Loans that are Amortizing Balloon | 13.7% |

| % of Initial Pool Balance of Mortgage Loans that are Interest Only then Amortizing Balloon | 5.7% |

| % of Initial Pool Balance of Mortgage Loans that are Interest Only | 64.6% |

| % of Initial Pool Balance of Mortgage Loans that are Interest Only – ARD | 16.1% |

| % of Initial Pool Balance of Mortgaged Properties with Single Tenants | 29.7% |

| % of Initial Pool Balance of Mortgage Loans with Mezzanine Debt | 8.5% |

| % of Initial Pool Balance of Mortgage Loans with Subordinate Debt | 16.1% |

| (1) | The Cut-off Date LTV Ratio, Maturity Date/ARD LTV Ratio, UW NCF DSCR, Debt Yield on Underwritten NOI and Cut-off Date Balance Per SF / Unit / Room information for each mortgage loan is presented in this Term Sheet (i) if such mortgage loan is part of a Whole Loan (as defined under “Collateral Overview—Whole Loan Summary” below), based on both that mortgage loan and any related pari passu companion loan(s) but, unless otherwise specifically indicated, without regard to any related subordinate companion loan(s), and (ii) unless otherwise specifically indicated, without regard to any other indebtedness (whether or not secured by the related mortgaged property, ownership interests in the related borrower or otherwise) that currently exists or that may be incurred by the related borrower or its owners in the future. |

| (2) | Subject to a permitted variance of plus or minus 5%. |

| (3) | Unless otherwise indicated, mortgage loans with anticipated repayment dates are presented as if they were to mature on the anticipated repayment date. |

| (4) | Excludes mortgage loans that are interest-only for the entire term. |

| (5) | The Cut-off Date LTV Ratios and Maturity Date/ARD LTV Ratios presented in this Term Sheet are generally based on the “as-is” appraised values of the related mortgaged properties (as set forth on Annex A to the Preliminary Prospectus), provided that such LTV ratios may be calculated based on (i) “as-stabilized” or similar values in certain cases where the completion of certain hypothetical conditions or other events at the property are assumed and/or where reserves have been established at origination to satisfy the applicable condition or event that is expected to occur, or (ii) the Cut-off Date Balance or Balloon Balance, as applicable, net of a related earnout or holdback reserve, or (iii) the “as-is” appraised value for a portfolio of mortgaged properties that includes a premium relating to the valuation of the portfolio of mortgaged properties as a whole rather than as the sum of individually valued mortgaged properties, in each case as further described in the definitions of “Appraised Value”, “Cut-off Date LTV Ratio” and “Maturity Date/ARD LTV Ratio” under “Description of the Mortgage Pool—Certain Calculations and Definitions” in the Preliminary Prospectus. |

| (6) | The Cut-off Date LTV Ratio, Debt Yield on Underwritten NOI and Debt Yield on Underwritten NCF with respect to the Echo-Westlake Multi mortgage loan are each calculated net of a $1,000,000 holdback reserve. |

| (7) | The UW NCF DSCR for each mortgage loan is generally calculated by dividing the Underwritten NCF for the related mortgaged property or mortgaged properties by the annual debt service for such mortgage loan, as adjusted in the case of mortgage loans with a partial interest only period by using the first 12 amortizing payments due instead of the actual interest only payment due. |

| (8) | The Debt Yield on Underwritten NOI for each mortgage loan is generally calculated as the related mortgaged property’s Underwritten NOI divided by the Cut-off Date Balance of such mortgage loan, and the Debt Yield on Underwritten NCF for each mortgage loan is generally calculated as the related mortgaged property’s Underwritten NCF divided by the Cut-off Date Balance of such mortgage loan. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-255181) the “Registration Statement”) for the offering to which this communication relates. Before you invest, you should read the prospectus in the Registration Statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc. or Deutsche Bank Securities Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

6

| KEY FEATURES OF THE CERTIFICATES |

| Co-Lead Managers and Joint Bookrunners: | Citigroup Global Markets Inc. Deutsche Bank Securities Inc.

|

| Depositor: | 3650 REIT Commercial Mortgage Securities II LLC

|

Initial Pool Balance:

| $918,586,612 |

| Master Servicer: | Midland Loan Services, a Division of PNC Bank, National Association

|

| Special Servicer: | 3650 REIT Loan Servicing LLC

|

| Certificate Administrator: | Wells Fargo Bank, National Association

|

| Trustee: | Wells Fargo Bank, National Association

|

| Operating Advisor: | Park Bridge Lender Services LLC

|

| Asset Representations Reviewer: | Park Bridge Lender Services LLC

|

| Risk Retention Consultation Parties: | 3650 Real Estate Investment Trust 2 LLC, Citi Real Estate Funding Inc. and German American Capital Corporation

|

| Credit Risk Retention: | For a discussion on the manner in which the U.S. credit risk retention requirements are being satisfied by 3650 Real Estate Investment Trust 2 LLC, as retaining sponsor for this securitization transaction, see “Credit Risk Retention” in the Preliminary Prospectus. Note that this securitization transaction is not structured to satisfy European or United Kingdom risk retention and due diligence requirements.

3650 Real Estate Investment Trust 2 LLC, as the “retaining sponsor” (as defined in the credit risk retention rules), intends satisfy the U.S. credit risk retention requirement through the purchase by one or more of its “majority-owned affiliates” (as defined in the credit risk retention rules), from the underwriters and the placement agents, on the Closing Date, of each of the Class F-RR, Class G-RR, Class J-RR and Class NR-RR certificates comprising the “horizontal risk retention certificates” (collectively, the “HRR Certificates”). The aggregate estimated fair value of the HRR Certificates will equal at least 5.01% of the estimated fair value of all of the certificates (other than the Class R certificates) issued by the issuing entity necessary to satisfy the credit risk retention rules. See “Credit Risk Retention” in the Preliminary Prospectus.

|

| Closing Date: | On or about November 18, 2021

|

| Cut-off Date: | With respect to each mortgage loan, the due date in November 2021 for that mortgage loan (or, in the case of any mortgage loan that has its first due date subsequent to November 2021, the date that would have been its due date in November 2021 under the terms of that mortgage loan if a monthly payment were scheduled to be due in that month)

|

| Determination Date: | The 11th day of each month or next business day, commencing in December 2021 |

| Distribution Date: | The 4th business day after the Determination Date, commencing in December 2021 |

| Interest Accrual: | Preceding calendar month

|

| ERISA Eligible: | The offered certificates are expected to be ERISA eligible, subject to the exemption conditions described in the Preliminary Prospectus

|

| SMMEA Eligible: | No |

| Payment Structure: | Sequential Pay |

| Day Count: | 30/360 |

| Tax Structure: | REMIC |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-255181) the “Registration Statement”) for the offering to which this communication relates. Before you invest, you should read the prospectus in the Registration Statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc. or Deutsche Bank Securities Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

7

| KEY FEATURES OF THE CERTIFICATES |

Rated Final Distribution Date: | November 2054 |

Cleanup Call:

| 1.0% |

| Minimum Denominations: | $10,000 minimum for the offered certificates (other than the Class X-A and Class X-B certificates); $1,000,000 minimum for the Class X-A and Class X-B certificates; and integral multiples of $1 thereafter for all the offered certificates

|

Delivery:

| Book-entry through DTC |

Analytics:

| Expected to be available on Bloomberg, L.P., CMBS.com, Inc., Thomson Reuters Corporation, Trepp, LLC, Intex Solutions, Inc., Moody’s Analytics, BlackRock Financial Management, Inc., RealINSIGHT, KBRA Analytics, LLC, Markit Group Limited, and DealView Technologies Ltd/StructureIt |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-255181) the “Registration Statement”) for the offering to which this communication relates. Before you invest, you should read the prospectus in the Registration Statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc. or Deutsche Bank Securities Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

8

| TRANSACTION HIGHLIGHTS |

| ■ | $781,946,000 (Approximate) New-Issue Multi-Borrower CMBS: |

| — | Overview: The mortgage pool consists of 35 fixed-rate commercial mortgage loans that have an aggregate Cut-off Date Balance of $918,586,612 (the “Initial Pool Balance”), have an average mortgage loan Cut-off Date Balance of $26,245,332 and are secured by 42 mortgaged properties located throughout 17 states. |

| — | LTV: 57.1% weighted average Cut-off Date LTV Ratio |

| — | DSCR: 2.69x weighted average Underwritten NCF Debt Service Coverage Ratio |

| — | Debt Yield: 10.2% weighted average Debt Yield on Underwritten NOI |

| — | Credit Support: 30.000% credit support to Class A-1 / A-3/ A-4/ A-5 / A-SB |

| ■ | Loan Structural Features: |

| — | Amortization: 19.3% of the mortgage loans by Initial Pool Balance have scheduled amortization: |

| – | 13.7% of the mortgage loans by Initial Pool Balance have amortization for the entire term with a balloon payment due at maturity |

| – | 5.7% of the mortgage loans by Initial Pool Balance have scheduled amortization following a partial interest only period with a balloon payment due at maturity |

| — | Hard Lockboxes: 58.3% of the mortgage loans by Initial Pool Balance have a Hard Lockbox in place |

| — | Cash Traps: 79.8% of the mortgage loans by Initial Pool Balance have cash traps triggered by certain declines in cash flow, all at levels equal to or greater than (i) a 1.05x coverage or (ii) a 4.50% debt yield, that fund an excess cash flow reserve |

| — | Reserves: The mortgage loans require amounts to be escrowed for reserves as follows: |

| – | Real Estate Taxes: 28 mortgage loans representing 67.3% of the Initial Pool Balance |

| – | Insurance: 17 mortgage loans representing 37.8% of the Initial Pool Balance |

| – | Replacement Reserves (Including FF&E Reserves): 26 mortgage loans representing 65.5% of the Initial Pool Balance |

| – | Tenant Improvements / Leasing Commissions: 14 mortgage loans representing 62.2% secured by office, industrial, retail, self storage (with commercial tenants), mixed use and multifamily (with commercial tenants) properties |

| — | Predominantly Defeasance Mortgage Loans: 75.8% of the mortgage loans by Initial Pool Balance permit defeasance only after an initial lockout period |

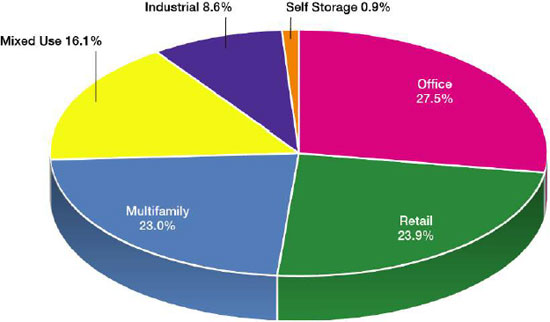

| ■ | Multiple-Asset Types > 5.0% of the Initial Pool Balance: |

| — | Office: 27.5% of the mortgaged properties by allocated Initial Pool Balance are office properties |

| — | Retail: 23.9% of the mortgaged properties by allocated Initial Pool Balance are retail properties (16.9% are anchored retail properties) |

| — | Multifamily: 23.0% of the mortgaged properties by allocated Initial Pool Balance are multifamily properties (4.0% are mid rise multifamily properties) |

| — | Mixed Use: 16.1% of the mortgaged properties by allocated Initial Pool Balance are mixed use properties |

| — | Industrial: 8.6% of the mortgaged properties by allocated Initial Pool Balance are industrial properties |

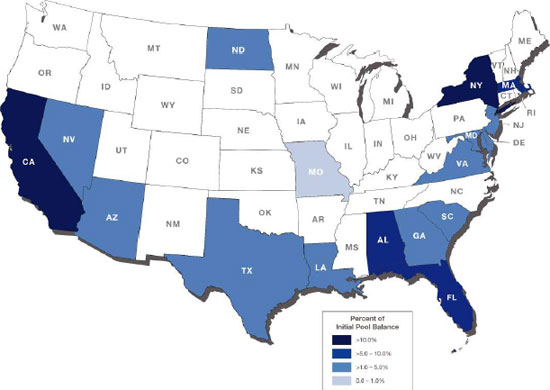

| ■ | Geographic Diversity: The 42 mortgaged properties are located throughout 17 states, with only two states having greater than 10.0% of the allocated Initial Pool Balance: California (30.9%) and New York (21.2%). |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-255181) the “Registration Statement”) for the offering to which this communication relates. Before you invest, you should read the prospectus in the Registration Statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc. or Deutsche Bank Securities Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

9

| COLLATERAL OVERVIEW |

Mortgage Loans by Loan Seller

| Mortgage Loan Seller | Mortgage Loans | Mortgaged Properties | Aggregate Cut-off Date Balance | % of Initial Pool Balance | |||||

| 3650 Real Estate Investment Trust 2 LLC | 25 | 25 | $572,500,817 | 62.3 | % | ||||

| German American Capital Corporation | 4 | 6 | 119,351,796 | 13.0 | |||||

| Citi Real Estate Funding Inc. | 4 | 4 | 99,065,000 | 10.8 | |||||

| 3650 Real Estate Investment Trust 2 LLC, German American Capital Corporation(1) | 1 | 1 | 77,900,000 | 8.5 | |||||

| Citi Real Estate Funding Inc., German American Capital Corporation(2) | 1 | 6 | 49,768,999 | 5.4 | |||||

| Total | 35 | 42 | $918,586,612 | 100.0 | % | ||||

| (1) | 3650 Real Estate Investment Trust 2 LLC and German American Capital Corporation Association are co-sponsors with respect to the CX – 350 & 450 Water Street mortgage loan (8.5%), which mortgage loan is evidenced by three (3) promissory notes: (i) notes A-4-2 and A-4-3, with an aggregate outstanding principal balance of $52,900,000 as of the cut-off date, as to which 3650 Real Estate Investment Trust 2 LLC is acting as mortgage loan seller and (ii) note A-1-7, with an aggregate outstanding principal balance of $25,000,000 as of the cut-off date, as to which German American Capital Corporation Association is acting as mortgage loan seller. |

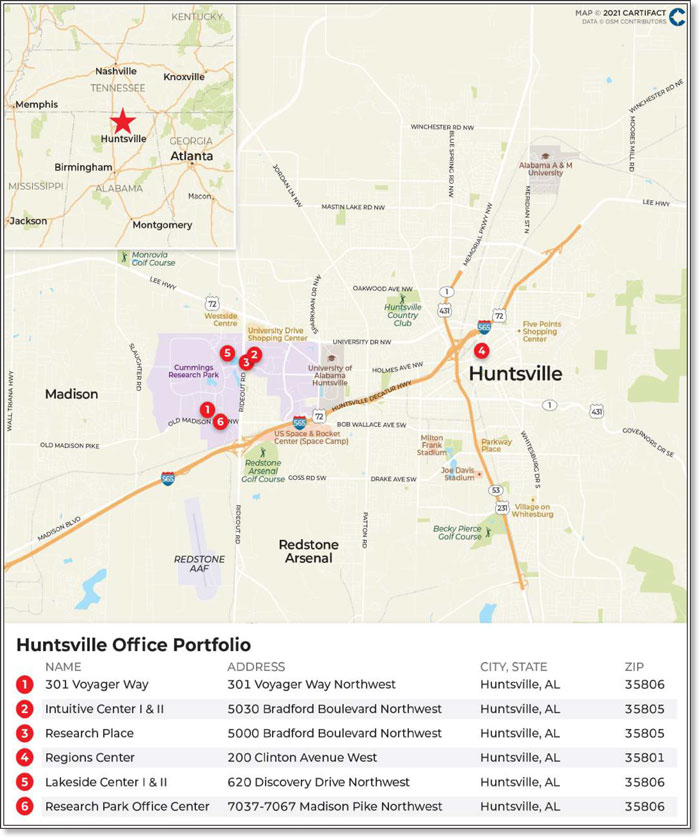

| (2) | Citi Real Estate Funding Inc. and German American Capital Corporation Association are co-sponsors with respect to the Huntsville Office Portfolio mortgage loan (5.4%), which mortgage loan is evidenced by four (4) promissory notes: (i) notes A-1-1 and A-1-3, with an aggregate outstanding principal balance of $24,884,499 as of the cut-off date, as to which Citi Real Estate Funding Inc. is acting as mortgage loan seller and (ii) notes A-2-2, and A-2-3, with an aggregate outstanding principal balance of $24,884,499 as of the cut-off date, as to which German American Capital Corporation Association is acting as mortgage loan seller. |

Ten Largest Mortgage Loans(1)(2)

| # | Mortgage Loan Name | Cut-off Date Balance | % of Initial Pool Balance | Property Type | Property Size SF/Units/ Rooms | Cut-off Date Balance Per SF/Unit/ Room | UW NCF DSCR | UW NOI Debt Yield | Cut-off Date LTV Ratio(3) | ||||||||||||||||

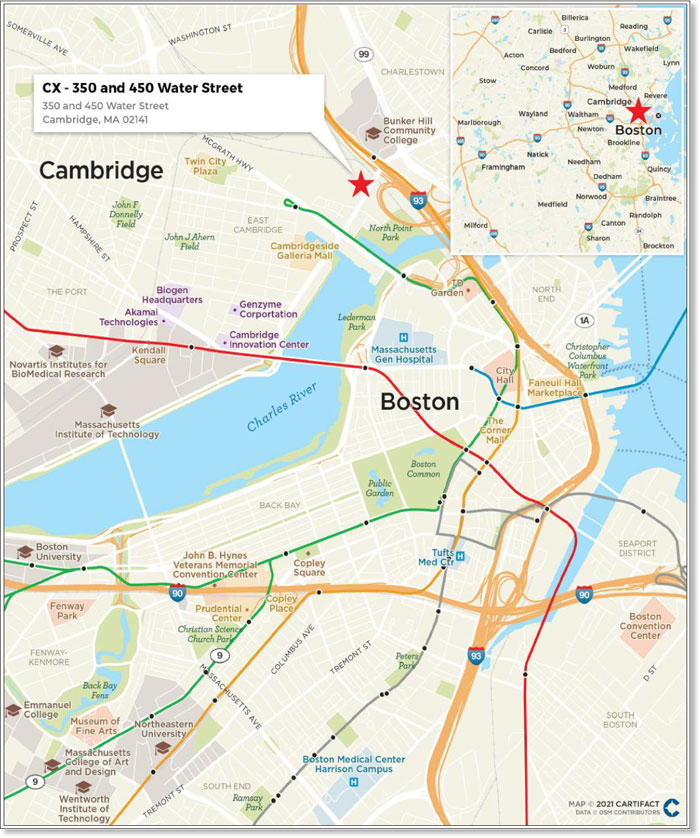

| 1 | CX - 350 & 450 Water Street | $77,900,000 | 8.5 | % | Mixed Use | 915,233 | $889 | 3.50 | x | 9.9 | % | 41.7 | % | ||||||||||||

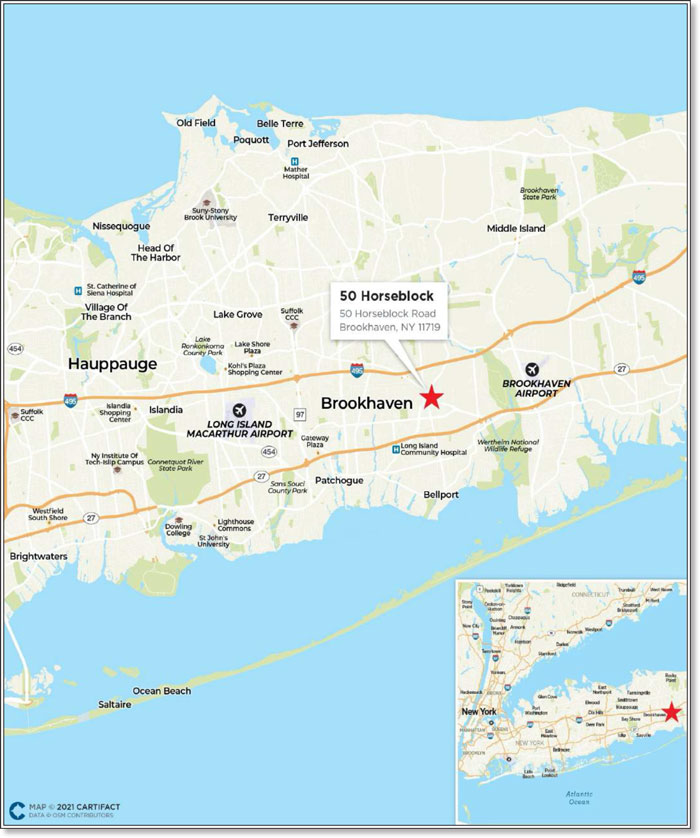

| 2 | 50 Horseblock | 59,000,000 | 6.4 | Industrial | 472,278 | $125 | 2.70 | x | 9.0 | % | 64.6 | % | |||||||||||||

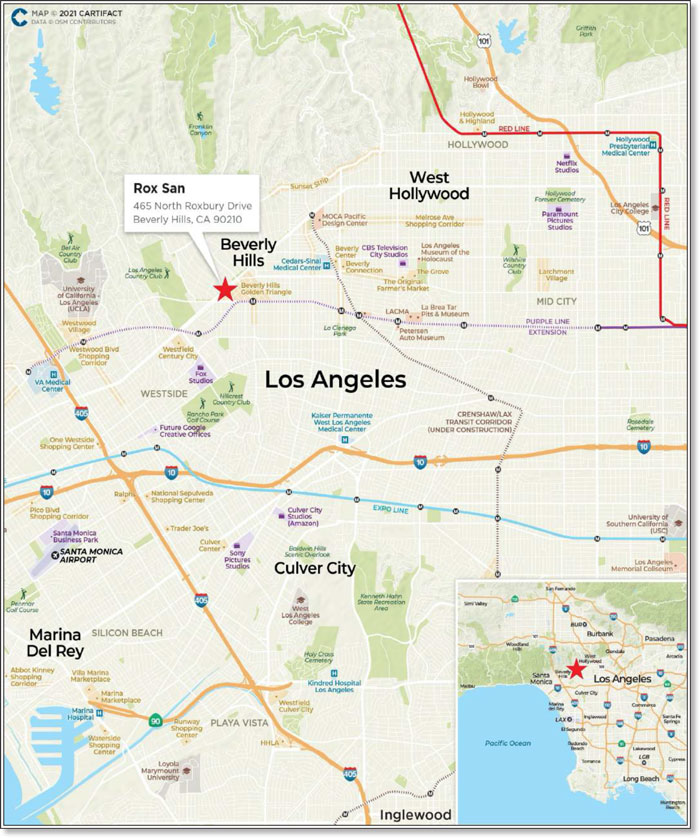

| 3 | Rox San | 52,000,000 | 5.7 | Office | 57,666 | $902 | 2.28 | x | 7.6 | % | 65.0 | % | |||||||||||||

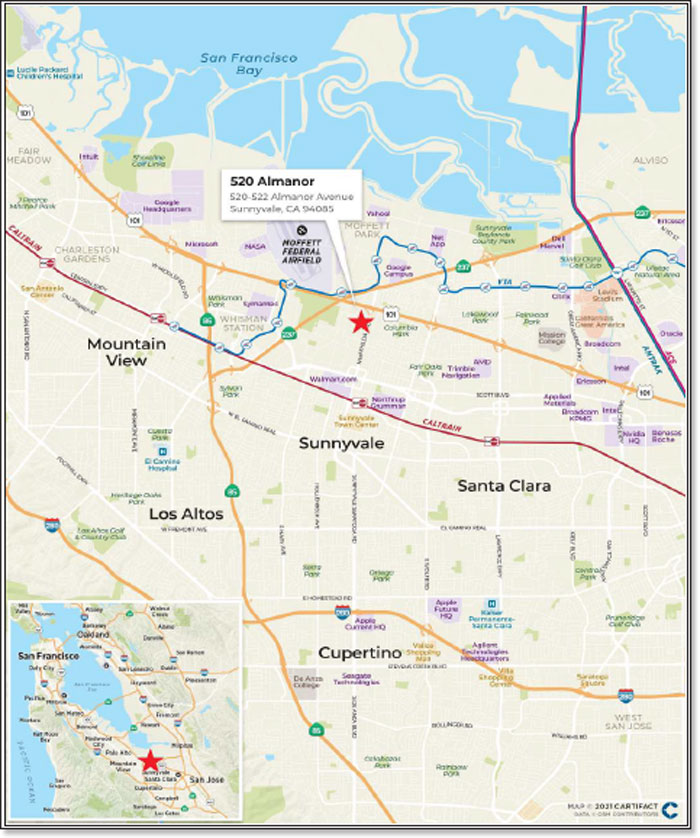

| 4 | 520 Almanor | 50,000,000 | 5.4 | Office | 231,220 | $439 | 5.00 | x | 13.0 | % | 40.0 | % | |||||||||||||

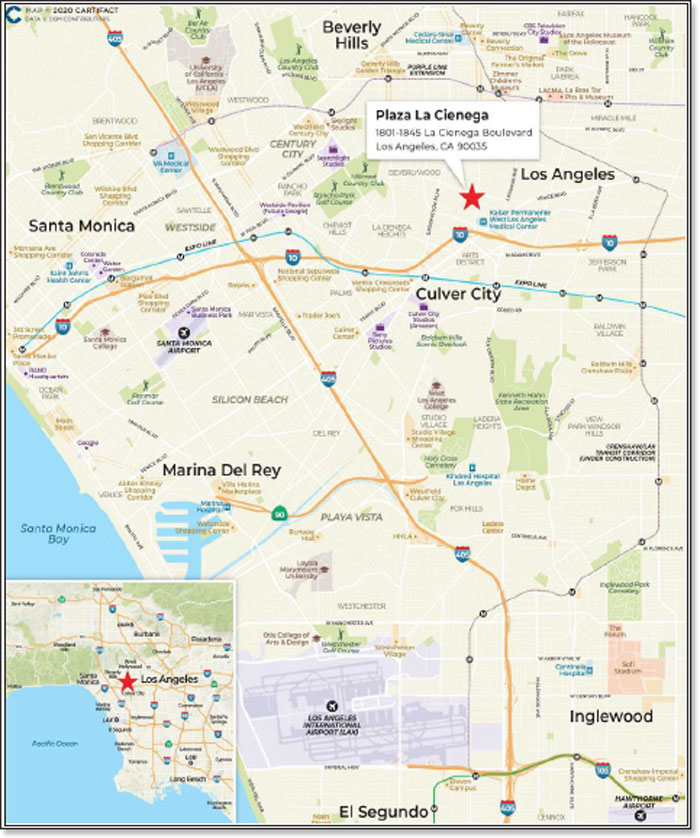

| 5 | Plaza La Cienega | 50,000,000 | 5.4 | Retail | 305,890 | $294 | 2.37 | x | 8.9 | % | 54.9 | % | |||||||||||||

| 6 | Huntsville Office Portfolio | 49,768,999 | 5.4 | Office | 1,033,888 | $77 | 1.88 | x | 11.7 | % | 68.3 | % | |||||||||||||

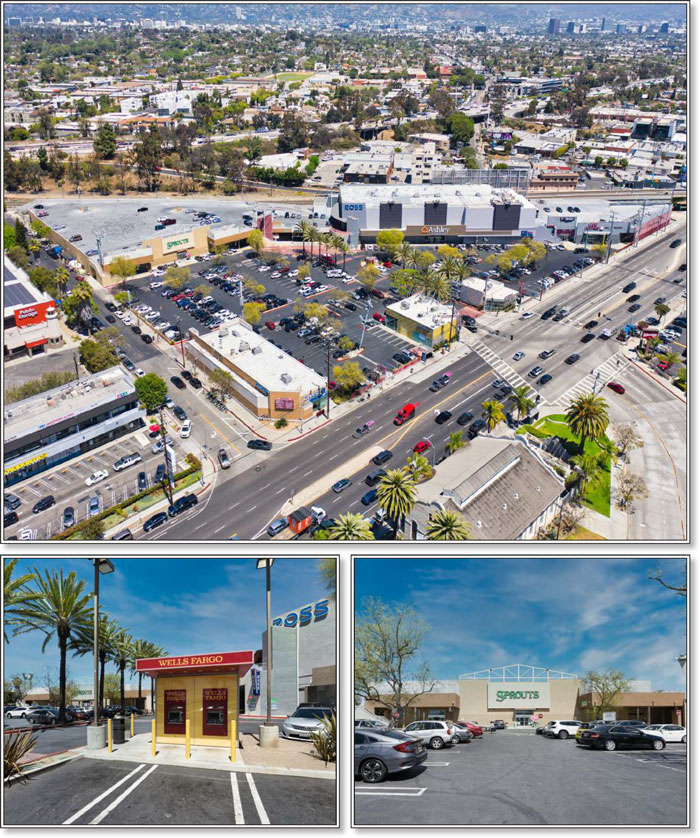

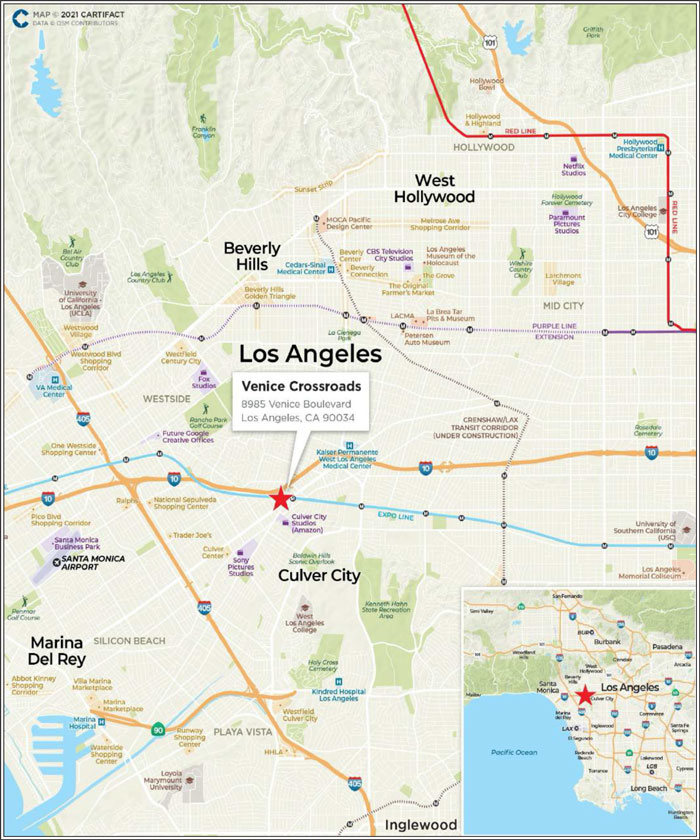

| 7 | Venice Crossroads | 45,100,000 | 4.9 | Retail | 157,819 | $286 | 3.09 | x | 9.4 | % | 55.0 | % | |||||||||||||

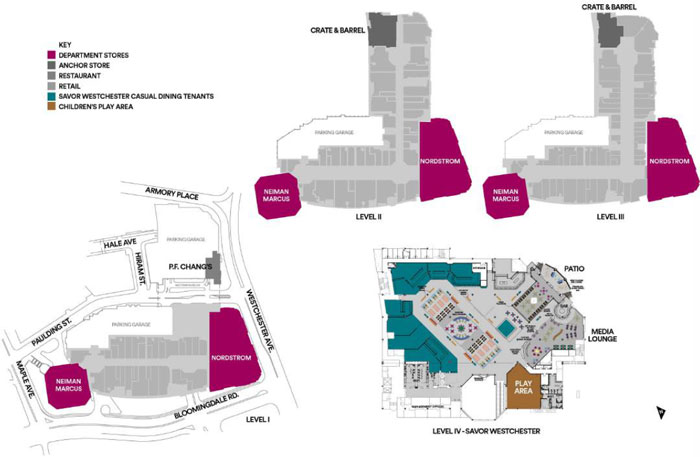

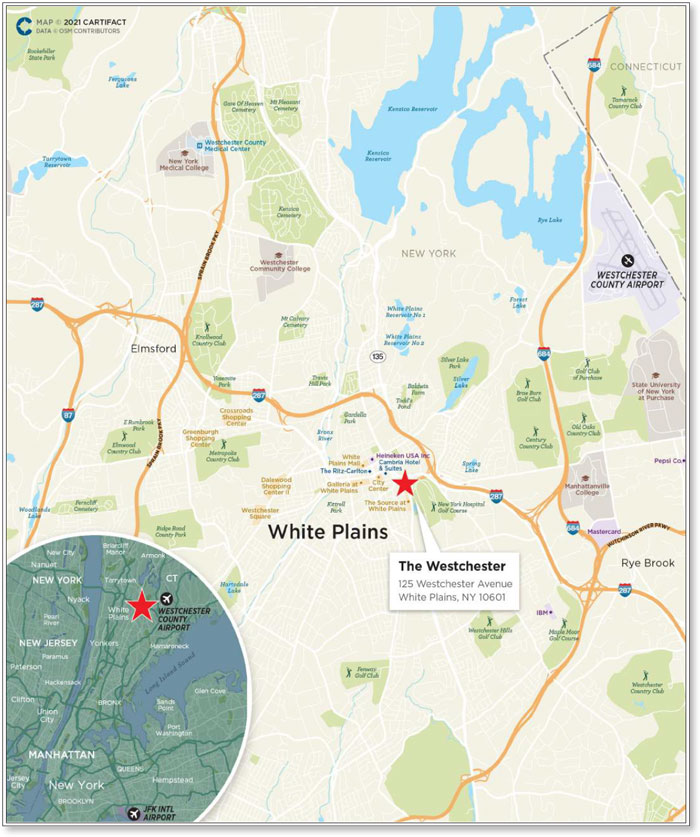

| 8 | The Westchester | 45,000,000 | 4.9 | Retail | 809,311 | $424 | 3.61 | x | 12.3 | % | 53.0 | % | |||||||||||||

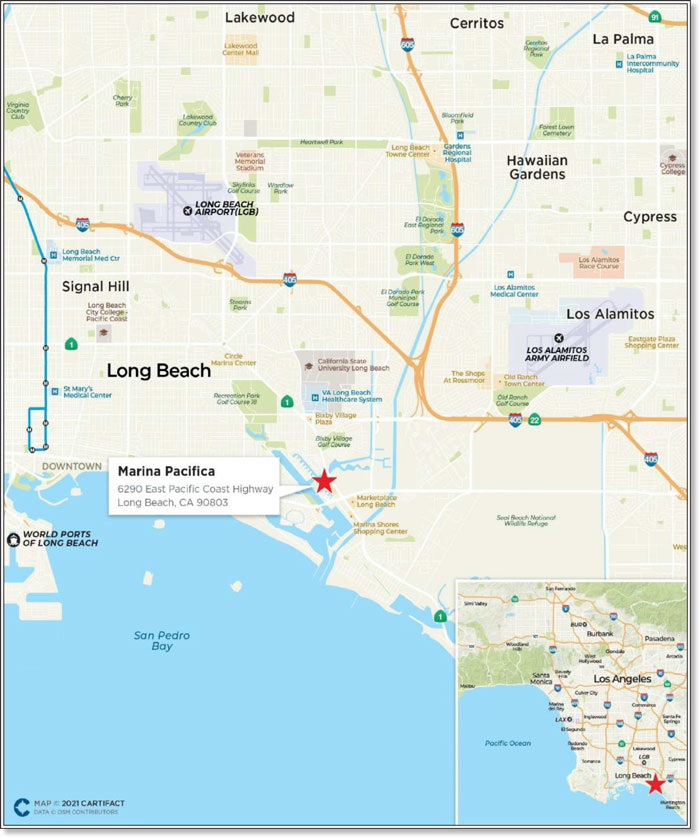

| 9 | Marina Pacifica | 33,104,772 | 3.6 | Retail | 297,227 | $111 | 1.48 | x | 19.1 | % | 34.1 | % | |||||||||||||

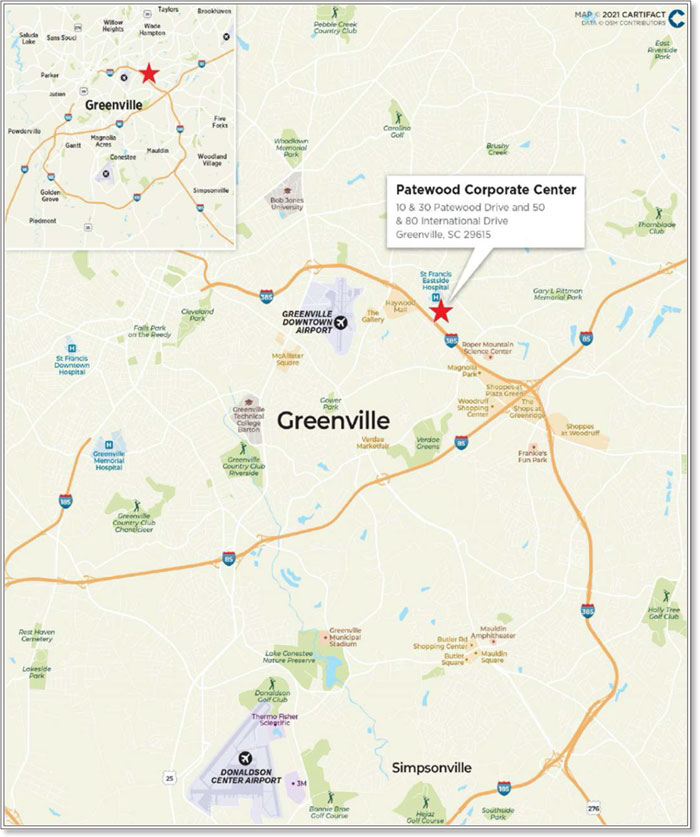

| 10 | Patewood Corporate Center | 30,000,000 | 3.3 | Office | 447,282 | $153 | 2.11 | x | 9.1 | % | 61.5 | % | |||||||||||||

| Top 10 Total / Wtd. Avg. | $491,873,771 | 53.5 | % | 2.90 | x | 10.7 | % | 53.7 | % | ||||||||||||||||

| Remaining Total / Wtd. Avg. | 426,712,841 | 46.5 | 2.45 | x | 9.6 | %(4) | 61.0 | %(4) | |||||||||||||||||

| Total / Wtd. Avg. | $918,586,612 | 100.0 | % | 2.69 | x | 10.2 | % | 57.1 | % | ||||||||||||||||

| (1) | See footnotes to table entitled “Mortgage Pool Characteristics” above. |

| (2) | With respect to each mortgage loan that is part of a Whole Loan (as identified under “Collateral Overview—Whole Loan Summary” below), the Cut-off Date Balance Per SF/Unit/Room, UW NCF DSCR, UW NOI Debt Yield and Cut-off Date LTV Ratio are calculated based on both that mortgage loan and any related pari passu companion loan(s), but without regard to any related subordinate companion loan(s) or other indebtedness. |

| (3) | With respect to certain of the mortgage loans identified above, the Cut-off Date LTV Ratios have been calculated using “as-stabilized” or similar hypothetical values. Such mortgage loans are identified under the definition of “Appraised Value” set forth under “Description of the Mortgage Pool—Certain Calculations and Definitions” in the Preliminary Prospectus. |

| (4) | The UW NOI Debt Yield and Cut-off Date LTV Ratio with respect to the Echo-Westlake Multi mortgage loan are each calculated net of a $1,000,000 holdback reserve. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-255181) the “Registration Statement”) for the offering to which this communication relates. Before you invest, you should read the prospectus in the Registration Statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc. or Deutsche Bank Securities Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

10

| COLLATERAL OVERVIEW (continued) |

Whole Loan Summary

Mortgage Loan Name(1) | Mortgage Loan Cut-off Date Balance | Mortgage Loan as Approx. % of Initial Pool Balance | Aggregate Pari Passu Companion Loan Cut-off Date Balance | Aggregate Subordinate Companion Loan Cut-off Date Balance | Whole Loan Cut-off Date Balance | Controlling Pooling/Trust and Servicing Agreement (“Controlling PSA”)(2) | Master Servicer / Outside Servicer | Special Servicer / Outside Special Servicer |

| CX - 350 & 450 Water Street | $77,900,000 | 8.5% | $736,100,000 | $411,000,000 | $1,225,000,000 | CAMB 2021-CX2 | KeyBank | Situs |

| 520 Almanor | $50,000,000 | 5.4% | $51,600,000 | — | $101,600,000 | Benchmark 2021-B30 | Midland | CWCapital |

| Plaza La Cienega | $50,000,000 | 5.4% | $40,000,000 | — | $90,000,000 | 3650R 2021-PF1 | Midland | Midland |

| Huntsville Office Portfolio | $49,768,999 | 5.4% | $29,861,399 | — | $79,630,398 | 3650R 2021-PF1 | Midland | Midland |

| The Westchester | $45,000,000 | 4.9% | $298,000,000 | $57,000,000 | $400,000,000 | CSMC 2020-WEST | Midland | Pacific Life Insurance Company |

| Patewood Corporate Center | $30,000,000 | 3.3% | $38,500,000 | — | $68,500,000 | 3650R 2021-PF1 | ||

| 2 Washington | $26,500,000 | 2.9% | $105,000,000 | — | $131,500,000 | BMARK 2021-B29 | Midland | LNR |

| One SoHo Square | $25,176,796 | 2.7% | $444,823,204 | $315,000,000 | $785,000,000 | SOHO 2021-SOHO | KeyBank | Midland |

| Icon One Daytona | $25,000,000 | 2.7% | $25,000,000 | — | $50,000,000 | 3650R 2021-PF1 | ||

| PetSmart HQ | $23,000,000 | 2.5% | $45,000,000 | — | $68,000,000 | 3650R 2021-PF1 | ||

| Centene | $15,600,000 | 1.7% | $31,200,000 | — | $46,800,000 | 3650R 2021-PF1 |

| (1) | Each of the mortgage loans included in the issuing entity that is secured by a mortgaged property or portfolio of mortgaged properties identified in the table above, together with the related companion loan(s) (none of which is included in the issuing entity), is referred to in this Term Sheet as a “Whole Loan”. See “Description of the Mortgage Pool—The Whole Loans” in the Preliminary Prospectus. |

| (2) | Each Whole Loan will be serviced under the related Controlling PSA and, in the event the Controlling Note is included in the related securitization transaction, the controlling class representative (or an equivalent entity) under such Controlling PSA will generally be entitled to exercise the rights of the controlling note holder for the subject Whole Loan. See, however, the chart entitled “Whole Loan Controlling Notes and Non-Controlling Notes” below and “Description of the Mortgage Pool—The Whole Loans” in the Preliminary Prospectus for information regarding the party that will be entitled to exercise such rights in the event the Controlling Note is held or deemed to be held by a third party or included in a separate securitization transaction. |

Mortgage Loans with Existing Mezzanine Debt or Subordinate Debt(1)

Mortgage Loan Name | Mortgage Loan Cut-off Date Balance | Aggregate Pari Passu Companion Loan Cut-off Date Balance | Aggregate Mezzanine Debt Cut-off Date Balance | Aggregate Subordinate Companion Loan Cut-off Date Balance | Cut-off Date Total Debt Balance(2) | Wtd. Avg Cut-off Date Total Debt Interest Rate(2) | Cut-off Date Mortgage Loan LTV(3) | Cut-off Date Total Debt LTV(2) | Cut-off Date Mortgage Loan UW NCF DSCR(3) | Cut-off Date Total Debt UW NCF | Cut-off Date Mortgage Loan UW NOI Debt Yield(3) | Cut-off Date Total Debt UW NOI Debt Yield(2) |

| CX - 350 & 450 Water Street | $77,900,000 | $736,100,000 | — | $411,000,000 | $1,225,000,000 | 2.79200% | 41.7% | 62.7% | 3.50x | 2.32x | 9.9% | 6.6% |

| The Westchester | $45,000,000 | $298,000,000 | — | $57,000,000 | $400,000,000 | 3.25000% | 53.0% | 61.8% | 3.61x | 3.10x | 12.3% | 10.6% |

| Patewood Corporate Center | $30,000,000 | $38,500,000 | $10,000,000(4) | — | $78,500,000 | 4.87777% | 61.5% | 70.5% | 2.11x | 1.56x | 9.1% | 8.0% |

| One SoHo Square | $25,176,796 | $444,823,204 | $120,000,000 | $315,000,000 | $905,000,000 | 3.03300% | 34.8% | 67.0% | 4.88x | 2.28x | 13.6% | 7.1% |

| PetSmart HQ | $23,000,000 | $45,000,000 | $12,000,000 | — | $80,000,000 | 5.43800% | 61.5% | 72.4% | 2.26x | 1.51x | 10.5% | 8.9% |

| (1) | See footnotes to table entitled “Mortgage Pool Characteristics” above. |

| (2) | All “Total Debt” calculations set forth in the table above include any related pari passu companion loan(s), any related subordinate companion loan(s) and any related mezzanine debt. |

| (3) | “Cut-off Date Mortgage Loan LTV”, “Cut-off Date Mortgage Loan UW NCF DSCR” and “Cut-off Date Mortgage Loan UW NOI Debt Yield” calculations include any related pari passu companion loan(s) and exclude any related subordinate companion loan(s). |

| (4) | The borrower has requested that the lender enter into a loan modification in order to convert approximately $5,000,000 of the existing mezzanine debt to preferred equity, which would continue to bear interest at the same rate as the mezzanine loan. See “Description of the Mortgage Pool—Additional Indebtedness—Preferred Equity” in the Preliminary Prospectus for additional information. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-255181) the “Registration Statement”) for the offering to which this communication relates. Before you invest, you should read the prospectus in the Registration Statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc. or Deutsche Bank Securities Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

11

| COLLATERAL OVERVIEW (continued) |

WHOLE LOAN SUMMARY (1)(2)

Mortgaged Property Name | Servicing of Whole Loan | Note Detail | Controlling Note | Current Holder of | Current or | Aggregate Cut-off | |

| CX – 350 & 450 Water Street(6) | Outside Serviced | Notes A-1-1, A-2-1, A-3-1, A-4-1, B-1, B-2, B-3, B-4 | Yes (Note A-1) | — | CAMB 2021-CX2 | $696,000,000 | |

| Notes A-1-2, A-1-4, A-1-5, A-1-6, A-1-8, A-1-9 | No | DBRI | Not Identified | $225,161,224 | |||

| Note A-1-3, A-3-2 | No | — | Benchmark 2021-B30 | $94,000,000 | |||

| Notes A-1-7, A-4-2, A-4-3 | No | — | 3650R 2021-PF1 | $77,900,000 | |||

| Notes A-2-2, A-2-3, A-2-4, A-2-5 | No | BANA | Not Identified | $107,959,184 | |||

| Note A-3-3 | No | JPMCB | Not Identified | $23,979,592 | |||

| 520 Almanor | Outside Serviced | Note A-1 | Yes | — | Benchmark 2021-B30 | $51,600,000 | |

| Note A-2 | No | — | 3650R 2021-PF1 | $50,000,000 | |||

| Plaza La Cienega | Serviced | Note A-1 | Yes | — | 3650R 2021-PF1 | $50,000,000 | |

| Note A-2 | No | — | Benchmark 2021-B30 | $20,000,000 | |||

| Note A-3 | No | CREFI | Not Identified | $20,000,000 | |||

| Huntsville Office Portfolio | Serviced | Notes A-1-1, A-1-3, A-2-2, A-2-3 | Yes (Note A-1-1) | — | 3650R 2021-PF1 | $49,768,999 | |

| Note A-1-2, A-2-1 | No | — | Benchmark 2021-B28 | $29,861,399 | |||

| The Westchester(6) | Outside Serviced | Notes A-1, B Note | Yes | — | CSMC 2020-WEST | $250,000,000 | |

| Note A-2-A | No | — | CSAIL 2021-C20 | $35,000,000 | |||

| Note A-2-B | No | — | WFCM 2021-C60 | $20,000,000 | |||

| Notes A-2-C, A-3-B | No | — | 3650R 2021-PF1 | $45,000,000 | |||

| Note A-3-A | No | — | CSAIL 2020-C19 | $50,000,000 | |||

| Patewood Corporate Center | Serviced | Note A-1 | Yes | — | 3650R 2021-PF1 | $30,000,000 | |

| Note A-2 | No | 3650 REIT | Not Identified | $38,500,000 | |||

| 2 Washington | Outside Serviced | Note A-1, A-2 | No | — | Benchmark 2021-B29 | $80,000,000 | |

| Note A-3 | Yes | — | Benchmark 2021-B28 | $25,000,000 | |||

| Note A-4, A-5 | No | — | 3650R 2021-PF1 | $26,500,000 | |||

| One SoHo Square(6) | Outside Serviced | Notes A-1-S, A-2-S, A-3-S, B-1, B-2, B-3 | Yes | — | SOHO 2021-SOHO | $316,000,000 | |

| Notes A-1-C-1, A-1-C-3, A-2-C-1, A-2-C-5 | No | — | Benchmark 2021-B28 | $135,000,000 | |||

| Note A-1-C-2 | No | WFB | Not Identified | $70,000,000 | |||

| Notes A-1-C-4, A-1-C-7, A-1-C-8, A-2-C-2, A-2-C-3 | No | — | Benchmark 2021-B29 | $112,000,000 | |||

| Notes A-1-C-5, A-1-C-6 | No | — | BBCMS 2021-C11 | $75,000,000 | |||

| Notes A-2-C-4, A-2-6 | No | — | 3650R 2021-PF1 | $25,176,796 | |||

| Note A-3-C-1, A-3-C-2, A-3-C-3 | No | — | MSC 2021-L7 | $51,823,204 | |||

| Icon One Daytona | Serviced | Note A-1 | Yes | — | 3650R 2021-PF1 | $25,000,000 | |

| Note A-2 | No | 3650 REIT | Not Identified | $25,000,000 | |||

| PetSmart HQ | Serviced | Note A-1 | Yes | — | 3650R 2021-PF1 | $23,000,000 | |

| Notes A-2, A-3 | No | 3650 REIT | Not Identified | $45,000,000 | |||

| Centene | Serviced | Note A-1 | Yes | — | 3650R 2021-PF1 | $15,600,000 | |

| Notes A-2, A-3 | No | 3650 REIT | Not Identified | $31,200,000 | |||

| (1) | The holder(s) of one or more specified controlling notes (collectively, the “Controlling Note”) will be the “controlling note holder(s)” (collectively, the “Controlling Note Holder”) entitled (directly or through a representative) to (a) approve or, in some cases, direct material servicing decisions involving the related Whole Loan (while the remaining such holder(s) generally are only entitled to non-binding consultation rights in such regard), and (b) in some cases, replace the applicable special servicer with respect to such Whole Loan with or without cause. See “Description of the Mortgage Pool—The Whole Loans” and “The Pooling and Servicing Agreement—Directing Holder” in the Preliminary Prospectus. |

| (2) | The holder(s) of the note(s) other than the Controlling Note (each, a “Non-Controlling Note”) will be the “non-controlling note holder(s)” generally entitled (directly or through a representative) to certain non-binding consultation rights with respect to any decisions as to which the holder of the Controlling Note has consent rights involving the related Whole Loan, subject to certain exceptions, including that in certain cases where the related Controlling Note is a B-note, C-note or other subordinate note, such consultation rights will not be afforded to the holder(s) of the Non-Controlling Notes until after a control trigger event has occurred with respect to either such Controlling Note(s) or certain certificates backed thereby, in each case as set forth in the related co-lender agreement. See “Description of the Mortgage Pool—The Whole Loans” in the Preliminary Prospectus. |

| (3) | Unless otherwise specified, with respect to each Whole Loan, any related unsecuritized Controlling Note and/or Non-Controlling Note may be further split, modified, combined and/or reissued (prior to its inclusion in a securitization transaction) as one or multiple Controlling Notes or Non-Controlling Notes, as the case may be, subject to the terms of the related co-lender agreement (including that the aggregate principal balance, weighted average interest rate and certain other material terms cannot be changed). In connection with the foregoing, any such split, modified, combined or re-issued Controlling Note or Non-Controlling Note, as the case may be, may be transferred to one or multiple parties (not identified in the table above) prior to its inclusion in a future commercial mortgage securitization transaction. |

| (4) | Unless otherwise specified, with respect to each Whole Loan, each related unsecuritized pari passu companion loan (whether controlling or non-controlling) is expected to be contributed to one or more future commercial mortgage securitization transactions. Under the column “Current or Anticipated Holder of Securitized Note”, (i) the identification of a securitization trust means we have identified an outside securitization (a) that has closed or (b) as to which a preliminary prospectus or final prospectus has been filed with the SEC or (c) as to which a preliminary offering circular or final offering circular has been printed, that, in each such case, has included or is expected to include the subject Controlling Note or Non-Controlling Note, as the case may be, (ii) “Not Identified” means the subject Controlling Note or Non-Controlling Note, as the case may be, has not been securitized and no preliminary prospectus or final prospectus has been filed with the SEC nor has any preliminary offering circular or final offering circular been printed that identifies any future outside securitization that is expected to include the subject Controlling Note or Non-Controlling Note, and (iii) “Not Applicable” means the subject Controlling Note or Non-Controlling Note is not intended to be contributed to a future commercial mortgage securitization transaction. In the case of an outside securitization that has not closed, there is no assurance that such securitization will close. Under the column “Current Holder of Unsecuritized Note”, “—” means the subject Controlling Note or Non-Controlling Note is not an unsecuritized note and is currently held (or is expected to be held) by the securitization trust referenced under the “Current or Anticipated Holder of Securitized Note” column. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-255181) the “Registration Statement”) for the offering to which this communication relates. Before you invest, you should read the prospectus in the Registration Statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc. or Deutsche Bank Securities Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

12

| COLLATERAL OVERVIEW (continued) |

| (5) | Entity names have been abbreviated for presentation. |

“3650 REIT” means 3650 Real Estate Investment Trust 2 LLC

“CREFI” means Citi Real Estate Funding Inc.

“GACC” means German American Capital Corporation

“DBRI” means DBR Investments Co. Limited

“BANA” mean Bank of America, National Association

“JPMCB” means JPMorgan Chase Bank, National Association

“WFB” means Wells Fargo Bank National Association

| (6) | The subject Whole Loan is an AB Whole Loan or a Pari Passu-AB Whole Loan, and the Controlling Note as of the date hereof (as identified in the chart above) is a related subordinate note. See “Description of the Mortgage Pool—The Whole Loans—The Non-Serviced AB Whole Loans” in the Preliminary Prospectus. |

Previously Securitized Mortgaged Properties(1)

Mortgaged Loan Name | Mortgage Loan Seller | City | State | Property Type | Cut-off Date Balance / Allocated Cut-off Date Balance | % of Initial Pool Balance | Previous Securitization |

| Rox San | 3650 REIT | Beverly Hills | California | Office | $52,000,000 | 5.7% | JPMBB 2015-C31 |

| Plaza La Cienega | CREFI | Los Angeles | California | Retail | $50,000,000 | 5.4% | JPMBB 2013-C14 |

| Venice Crossroads | 3650 REIT | Los Angeles | California | Retail | $45,100,000 | 4.9% | COMM 2013-LC6 |

| Patewood Corporate Center | 3650 REIT | Greenville | South Carolina | Office | $30,000,000 | 3.3% | GPMT 2018-FL1 |

| Tanglewood Apartments | 3650 REIT | Westwego | Louisiana | Multifamily | $30,000,000 | 3.3% | WFCM 2015-C26 |

| One SoHo Square | GACC | New York | New York | Office | $25,176,796 | 2.7% | GSMS 2019-SOHO |

| 747 Amsterdam Avenue | CREFI | New York | New York | Mixed Use | $21,000,000 | 2.3% | GSMS 2013-GC13 |

| 93 East Apartments | 3650 REIT | Atlanta | Georgia | Multifamily | $21,000,000 | 2.3% | BSPRT 2018-FL4, BSPRT 2019-FL5 |

| Falls of West Oaks | 3650 REIT | Houston | Texas | Multifamily | $19,500,000 | 2.1% | JPMCC 2012-LC9 |

| Carrington Court Apartments | 3650 REIT | Grand Forks | North Dakota | Multifamily | $10,901,009 | 1.2% | WFRBS 2011-C3 |

| Jupiter Park Self Storage | CREFI | Jupiter | Florida | Self Storage | $8,400,000 | 0.9% | COMM 2015-DC1 |

| (1) | The table above includes mortgage loans secured by mortgaged properties for which the most recent prior financing of all or a significant portion of such mortgaged properties was included in a securitization. Information under “Previous Securitization” represents the most recent such securitization with respect to each of those mortgaged properties. The information in the above table is based solely on information provided by the related borrower or obtained through searches of a third-party database, and has not otherwise been confirmed by the mortgage loan sellers. |

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-255181) the “Registration Statement”) for the offering to which this communication relates. Before you invest, you should read the prospectus in the Registration Statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc. or Deutsche Bank Securities Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

13

| COLLATERAL OVERVIEW (continued) |

Property Types

| Property Type / Detail | Number of Mortgaged Properties | Aggregate Cut-off Date Balance(1) | % of Initial Pool Balance(1) | Wtd. Avg. Underwritten NCF DSCR(2)(3) | Wtd. Avg. Cut-off Date LTV Ratio(2)(3) | Wtd. Avg. Debt Yield on Underwritten NOI(2)(3) | ||||||||||||

| Office | 14 | $252,995,795 | 27.5 | % | 2.97 | x | 56.8 | % | 10.6 | % | ||||||||

| Suburban | 5 | 121,010,000 | 13.2 | 3.37 | x | 52.6 | % | 11.0 | % | |||||||||

| CBD | 7 | 74,945,795 | 8.2 | 2.89 | x | 57.0 | % | 12.3 | % | |||||||||

| Medical | 2 | 57,040,000 | 6.2 | 2.22 | x | 65.6 | % | 7.7 | % | |||||||||

| Retail | 6 | $219,954,772 | 23.9 | % | 2.64 | x | 52.4 | % | 11.3 | % | ||||||||

| Anchored | 4 | 154,954,772 | 16.9 | 2.37 | x | 52.3 | % | 11.1 | % | |||||||||

| Super Regional Mall | 1 | 45,000,000 | 4.9 | 3.61 | x | 53.0 | % | 12.3 | % | |||||||||

| Single Tenant | 1 | 20,000,000 | 2.2 | 2.52 | x | 52.0 | % | 11.2 | % | |||||||||

| Multifamily | 13 | $211,001,009 | 23.0 | % | 2.37 | x | 63.5 | % | 9.4 | % | ||||||||

| Garden | 8 | 127,801,009 | 13.9 | 1.92 | x | 66.3 | % | 8.4 | % | |||||||||

| Mid Rise | 2 | 36,500,000 | 4.0 | 2.01 | x | 65.3 | % | 8.0 | % | |||||||||

| High Rise | 1 | 26,500,000 | 2.9 | 2.82 | x | 60.6 | % | 9.9 | % | |||||||||

| Townhomes | 1 | 10,200,000 | 1.1 | 2.25 | x | 70.0 | % | 8.8 | % | |||||||||

| Cooperative | 1 | 10,000,000 | 1.1 | 8.24 | x | 22.1 | % | 25.5 | % | |||||||||

| Mixed Use | 6 | $147,570,036 | 16.1 | % | 2.96 | x | 50.5 | % | 9.6 | % | ||||||||

| Office/Lab | 1 | 77,900,000 | 8.5 | 3.50 | x | 41.7 | % | 9.9 | % | |||||||||

| Retail/Office | 3 | 45,325,000 | 4.9 | 2.85 | x | 53.4 | % | 9.6 | % | |||||||||

| Multifamily/Retail | 1 | 14,120,036 | 1.5 | 1.36 | x | 74.1 | % | 7.9 | % | |||||||||

| Industrial/Multifamily | 1 | 10,225,000 | 1.1 | 1.58 | x | 72.0 | % | 9.2 | % | |||||||||

| Industrial | 2 | $78,665,000 | 8.6 | % | 2.43 | x | 65.2 | % | 9.1 | % | ||||||||

| Flex | 2 | 78,665,000 | 8.6 | 2.43 | x | 65.2 | % | 9.1 | % | |||||||||

| Self Storage | 1 | $8,400,000 | 0.9 | % | 1.55 | x | 68.9 | % | 8.8 | % | ||||||||

| Total | 42 | $918,586,612 | 100.0 | % | 2.69 | x | 57.1 | % | 10.2 | % | ||||||||

| (1) | Calculated based on the mortgaged property’s allocated loan amount for mortgage loans secured by more than one mortgaged property. |

| (2) | Weighted average based on the mortgaged property’s allocated loan amount for mortgage loans secured by more than one mortgaged property. |

| (3) | See footnotes to the table entitled “Mortgage Pool Characteristics” above. |

|

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-255181) the “Registration Statement”) for the offering to which this communication relates. Before you invest, you should read the prospectus in the Registration Statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc. or Deutsche Bank Securities Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

14

| COLLATERAL OVERVIEW (continued) |

Geographic Distribution

| Property Location | Number of Mortgaged Properties | Aggregate | % of Initial | Aggregate | % of Total Appraised Value | Underwritten | % of Total Underwritten NOI | ||||||||||||||

| California | 9 | $283,694,772 | 30.9 | % | $765,900,000 | 12.9 | % | $40,682,872 | 13.5 | % | |||||||||||

| New York | 8 | 194,351,796 | 21.2 | 2,369,850,000 | 39.8 | 128,118,114 | 42.6 | ||||||||||||||

| Massachusetts | 1 | 77,900,000 | 8.5 | 1,954,000,000 | 32.9 | 80,703,532 | 26.8 | ||||||||||||||

| Alabama | 6 | 49,768,999 | 5.4 | 116,550,000 | 2.0 | 9,346,062 | 3.1 | ||||||||||||||

| Florida | 3 | 49,000,000 | 5.3 | 163,800,000 | 2.8 | 8,808,687 | 2.9 | ||||||||||||||

| South Carolina | 1 | 30,000,000 | 3.3 | 111,300,000 | 1.9 | 6,266,483 | 2.1 | ||||||||||||||

| Louisiana | 1 | 30,000,000 | 3.3 | 46,000,000 | 0.8 | 2,740,938 | 0.9 | ||||||||||||||

| Texas | 2 | 30,000,000 | 3.3 | 46,200,000 | 0.8 | 2,536,817 | 0.8 | ||||||||||||||

| Georgia | 2 | 27,500,000 | 3.0 | 42,350,000 | 0.7 | 2,204,860 | 0.7 | ||||||||||||||

| Virginia | 1 | 27,000,000 | 2.9 | 39,800,000 | 0.7 | 2,126,440 | 0.7 | ||||||||||||||

| Maryland | 1 | 26,750,000 | 2.9 | 40,900,000 | 0.7 | 2,109,013 | 0.7 | ||||||||||||||

| Arizona | 1 | 23,000,000 | 2.5 | 110,500,000 | 1.9 | 7,132,809 | 2.4 | ||||||||||||||

| North Dakota | 2 | 21,101,009 | 2.3 | 31,070,000 | 0.5 | 1,893,495 | 0.6 | ||||||||||||||

| Nevada | 1 | 20,000,000 | 2.2 | 38,450,000 | 0.6 | 2,237,852 | 0.7 | ||||||||||||||

| Delaware | 1 | 14,120,036 | 1.5 | 19,050,000 | 0.3 | 1,117,010 | 0.4 | ||||||||||||||

| New Jersey | 1 | 10,000,000 | 1.1 | 45,300,000 | 0.8 | 2,546,561 | 0.8 | ||||||||||||||

| Missouri | 1 | 4,400,000 | 0.5 | 6,100,000 | 0.1 | 383,353 | 0.1 | ||||||||||||||

| Total | 42 | $918,586,612 | 100.0 | % | $5,947,120,000 | 100.0 | % | $300,954,898 | 100.0 | % | |||||||||||

| (1) | Calculated based on the mortgaged property’s allocated loan amount for mortgage loans secured by more than one mortgaged property. |

| (2) | Aggregate Appraised Values and Underwritten NOI reflect the aggregate values without any reduction for the pari passu companion loan(s). |

| (3) | For multi-property loans that do not have underwritten cash flow information reported on a property level basis, Underwritten NOI is allocated based on each respective property’s allocated loan amount. |

|

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-255181) the “Registration Statement”) for the offering to which this communication relates. Before you invest, you should read the prospectus in the Registration Statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc. or Deutsche Bank Securities Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

15

| COLLATERAL OVERVIEW (continued) |

| Distribution of Cut-off Date Balances | |||||||||

| Range of Cut-off Date Balances ($) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||

| 4,400,000 - 9,999,999 | 4 | $28,800,000 | 3.1 | % | |||||

| 10,000,000 - 19,999,999 | 11 | 152,486,045 | 16.6 | ||||||

| 20,000,000 - 29,999,999 | 9 | 215,426,796 | 23.5 | ||||||

| 30,000,000 - 39,999,999 | 3 | 93,104,772 | 10.1 | ||||||

| 40,000,000 - 49,999,999 | 3 | 139,868,999 | 15.2 | ||||||

| 50,000,000 - 59,999,999 | 4 | 211,000,000 | 23.0 | ||||||

| 60,000,000 - 77,900,000 | 1 | 77,900,000 | 8.5 | ||||||

| Total | 35 | $918,586,612 | 100.0 | % | |||||

| Distribution of UW NCF DSCRs(1) | |||||||||

| Range of UW NCF DSCR (x) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||

| 1.35 - 1.99 | 11 | $225,534,816 | 24.6 | % | |||||

| 2.00 - 2.49 | 11 | $278,550,000 | 30.3 | ||||||

| 2.50 - 2.99 | 6 | $147,325,000 | 16.0 | ||||||

| 3.00 - 4.99 | 5 | $207,176,796 | 22.6 | ||||||

| 5.00 - 8.24 | 2 | $60,000,000 | 6.5 | ||||||

| Total | 35 | $918,586,612 | 100.0 | % | |||||

| (1) See footnotes (1) and (7) to the table entitled “Mortgage Pool Characteristics” above. | |||||||||

| Distribution of Amortization Types(1) | |||||||||

| Amortization Type | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||

| Interest Only | 23 | $593,151,796 | 64.6 | % | |||||

| Interest Only - ARD | 3 | 147,900,000 | 16.1 | ||||||

| Amortizing Balloon | 5 | 125,569,816 | 13.7 | ||||||

| Interest Only, Amortizing Balloon(2) | 4 | 51,965,000 | 5.7 | ||||||

| Total | 35 | $918,586,612 | 100.0 | % | |||||

| (1) All of the mortgage loans will have balloon payments at maturity date or have an anticipated repayment date, as applicable. | |||||||||

| (2) Original partial interest only periods range from 12 to 60 months. | |||||||||

| Distribution of Lockbox Types | |||||||||

| Lockbox Type | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||

| Hard | 15 | $535,145,603 | 58.3 | % | |||||

| None | 8 | 185,500,000 | 20.2 | ||||||

| Springing | 10 | 153,766,009 | 16.7 | ||||||

| Hard (Commercial) / Soft (Residential) | 2 | 44,175,000 | 4.8 | ||||||

| Total | 35 | $918,586,612 | 100.0 | % | |||||

| Distribution of Cut-off Date LTV Ratios(1) | |||||||||

| Range of Cut-off Date LTV Ratios (%) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||

| 22.1 - 54.9 | 10 | $342,506,568 | 37.3 | % | |||||

| 55.0 - 64.9 | 10 | 254,200,000 | 27.7 | ||||||

| 65.0 - 69.9 | 10 | 255,985,007 | 27.9 | ||||||

| 70.0 - 74.1 | 5 | 65,895,036 | 7.2 | ||||||

| Total | 35 | $918,586,612 | 100.0 | % | |||||

| (1) See footnotes (1), (5) and (6) to the table entitled “Mortgage Pool Characteristics” above. | |||||||||

| Distribution of Maturity Date/ARD LTV Ratios(1) | |||||||||

| Range of Maturity Date/ARD LTV Ratios (%) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||

| 11.2 - 49.9 | 5 | $196,181,568 | 21.4 | % | |||||

| 50.0 - 54.9 | 7 | 206,995,007 | 22.5 | ||||||

| 55.0 - 59.9 | 8 | 156,160,036 | 17.0 | ||||||

| 60.0 - 70.0 | 15 | 359,250,000 | 39.1 | ||||||

| Total | 35 | $918,586,612 | 100.0 | % | |||||

| (1) See footnotes (1), (3), and (5) to the table entitled “Mortgage Pool Characteristics” above. | |||||||||

| Distribution of Loan Purpose | |||||||||

| Loan Purpose | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||

| Refinance | 27 | $712,596,612 | 77.6 | % | |||||

| Acquisition | 7 | 146,990,000 | 16.0 | ||||||

| Recapitalization | 1 | 59,000,000 | 6.4 | ||||||

| Total | 35 | $918,586,612 | 100.0 | % | |||||

| Distribution of Mortgage Rates | |||||||||

| Range of Mortgage Rates (%) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||

| 2.555 - 3.4990 | 18 | $598,120,795 | 65.1 | % | |||||

| 3.500 - 3.9990 | 11 | 215,565,817 | 23.5 | ||||||

| 4.000 - 4.5500 | 6 | 104,900,000 | 11.4 | ||||||

| Total | 35 | $918,586,612 | 100.0 | % | |||||

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (“SEC”) (SEC File No. 333-255181) the “Registration Statement”) for the offering to which this communication relates. Before you invest, you should read the prospectus in the Registration Statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or Citigroup Global Markets Inc. or Deutsche Bank Securities Inc. or any other underwriter or dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-831-9146.

16

| COLLATERAL OVERVIEW (continued) |

| Distribution of Debt Yield on Underwritten NOI(1) | |||||||||

| Range of Debt Yields on Underwritten NOI (%) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||

| 7.6 - 8.5 | 8 | $194,870,036 | 21.2 | % | |||||

| 8.6 - 9.5 | 15 | 338,941,009 | 36.9 | ||||||

| 9.6 - 10.5 | 4 | 141,400,000 | 15.4 | ||||||

| 10.6 - 11.5 | 2 | 30,325,000 | 3.3 | ||||||

| 11.6 - 12.5 | 2 | 94,768,999 | 10.3 | ||||||

| 12.6 - 25.5 | 4 | 118,281,568 | 12.9 | ||||||

| Total | 35 | $918,586,612 | 100.0 | % | |||||

| (1) See footnotes (1), (6) and (8) to the table entitled “Mortgage Pool Characteristics” above. | |||||||||

| Distribution of Debt Yield on Underwritten NCF(1) | |||||||||

| Range of Debt Yields on Underwritten NCF (%) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||

| 7.6 - 8.0 | 8 | $194,870,036 | 21.2 | % | |||||

| 8.1 - 9.0 | 14 | 293,841,009 | 32.0 | ||||||

| 9.1 - 10.0 | 6 | 236,268,999 | 25.7 | ||||||

| 10.1 - 11.0 | 1 | 10,325,000 | 1.1 | ||||||

| 11.1 - 12.0 | 2 | 65,000,000 | 7.1 | ||||||

| 12.1 - 25.1 | 4 | 118,281,568 | 12.9 | ||||||

| Total | 35 | $918,586,612 | 100.0 | % | |||||

| (1) See footnotes (1), (6) and (8) to the table entitled “Mortgage Pool Characteristics” above. | |||||||||

| Mortgage Loans with Original Partial Interest Only Periods | |||||||||

| Original Partial Interest Only Period (months) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||

| 12 | 1 | $19,500,000 | 2.1 | % | |||||

| 24 | 2 | $24,065,000 | 2.6 | % | |||||

| 60 | 1 | $8,400,000 | 0.9 | % | |||||

| Distribution of Original Terms to Maturity/ARD(1) | |||||||||

| Original Term to Maturity/ARD (months) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||

| 84 - 119 | 5 | $163,281,568 | 17.8 | % | |||||

| 120 | 30 | 755,305,044 | 82.2 | ||||||

| Total | 35 | $918,586,612 | 100.0 | % | |||||

| (1) See footnote (3) to the table entitled “Mortgage Pool Characteristics” above. | |||||||||

Distribution of Remaining Terms to Maturity/ARD(1) | |||||||||

| Range of Remaining Terms to Maturity/ARD (months) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||

| 77 - 96 | 5 | $163,281,568 | 17.8 | % | |||||

| 97 - 116 | 12 | 278,071,045 | 30.3 | ||||||

| 117 - 120 | 18 | 477,233,999 | 52.0 | ||||||

| Total | 35 | $918,586,612 | 100.0 | % | |||||

| (1) See footnote (3) to the table entitled “Mortgage Pool Characteristics” above. | |||||||||

| Distribution of Original Amortization Terms(1) | |||||||||

| Original Amortization Term (months) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||

| Interest Only | 26 | $741,051,796 | 80.7 | % | |||||

| 120 | 1 | 33,104,772 | 3.6 | ||||||

| 360 | 8 | 144,430,044 | 15.7 | ||||||

| Total | 35 | $918,586,612 | 100.0 | % | |||||

| (1) All of the mortgage loans will have balloon payments at maturity or have an anticipated repayment date, as applicable. | |||||||||

| Distribution of Remaining Amortization Terms(1) | |||||||||

| Range of Remaining Amortization Terms (months) | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||

| Interest Only | 26 | $741,051,796 | 80.7 | % | |||||

| 119 - 353 | 1 | 33,104,772 | 3.6 | ||||||

| 354 - 360 | 8 | 144,430,044 | 15.7 | ||||||

| Total | 35 | $918,586,612 | 100.0 | % | |||||

| (1) All of the mortgage loans will have balloon payments at maturity or have an anticipated repayment date, as applicable. | |||||||||

| Distribution of Prepayment Provisions | |||||||||

| Prepayment Provision | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||

| Defeasance | 30 | $696,405,044 | 75.8 | % | |||||

| Yield Maintenance or Defeasance | 4 | 189,076,796 | 20.6 | ||||||

| Yield Maintenance | 1 | 33,104,772 | 3.6 | ||||||

| Total | 35 | $918,586,612 | 100.0 | % | |||||

| Distribution of Escrow Types | |||||||||

| Escrow Type | Number of Mortgage Loans | Cut-off Date Balance | % of Initial Pool Balance | ||||||

| Real Estate Tax | 28 | $618,509,816 | 67.3 | % | |||||

| Replacement Reserves(1) | 26 | $601,909,816 | 65.5 | % | |||||

| TI/LC(2) | 14 | $434,743,807 | 62.2 | % | |||||

| Insurance | 17 | $347,370,007 | 37.8 | % | |||||

| (1) Includes mortgage loans with FF&E reserves. | |||||||||