united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

Investment Company Act file number 811-23765

AOG Institutional Diversified Master Fund

(Exact name of registrant as specified in charter)

11911 Freedom Drive, Suite 730, Reston, VA 20190

(Address of principal executive offices) (Zip code)

Peter Sattelmair

11911 Freedom Drive, Suite 730, Reston, VA 20190

(Name and address of agent for service)

Registrant's telephone number, including area code: 703-757-8020

Date of fiscal year end: 9/30

Date of reporting period: 9/30/23

ITEM 1. REPORTS TO SHAREHOLDERS.

(a) Include a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Act (17 CFR 270.30e-1).

|

| AOG Institutional Fund |

| (Formerly AOG Institutional Diversified Fund) |

| Annual Report |

| September 30, 2023 |

TABLE OF CONTENTS

| Letter to Shareholders (Unaudited) | Page 1 |

| Risk Disclosure (Unaudited) | Page 4 |

| Portfolio Review (Unaudited) | Page 5 |

| Statement of Assets and Liabilities | Page 6 |

| Statement of Operations | Page 7 |

| Statement of Changes in Net Assets | Page 8 |

| Statement of Cash Flows | Page 9 |

| Financial Highlights | Page 10 |

| Notes to Financial Statements | Page 11 |

| Audit Opinion | Page 20 |

| Supplemental Information (Unaudited) | Page 21 |

| Notice of Privacy Policy (Unaudited) | Page 27 |

AOG Institutional Fund

Letter to Shareholders (Unaudited)

September 30, 2023

The AOG Institutional Fund’s (AOGFX) fiscal year ending September 30, 2023, was the first full year of operations and reporting undertaken by the Fund, after launching in January of 2022. The Fund’s investment objective is to seek total return, with the primary qualitative goal to position AOGFX to serve as a core alternative investment solution for investors. We manage the Fund to enable an accredited Advisor or Investor to pair AOGFX with public stocks and bonds, and thereby approximate the Endowment Model1. The result is to provide the potential benefits of institutional investing to non-institutional investors.

We have a broad mandate across the entire universe of alternative investments, which allows us to act tactically and take advantage of the most atractive investment opportunities regardless of asset class. Our approach of tiering both vintages and opportunities allows us to strike a balance between atractive short-term gains and long-term performance. We believe this strategy is essential for accommodating investors with varying time horizons, ensuring that AOGFX can remain an adaptable and atractive choice for a diverse range of shareholders.

Fiscal year 2023 marked a period of significant enhancements within AOGFX. We have completed our transition to operating as a closed-end interval fund, featuring daily NAV calculations. In May, we began quarterly income distributions and in September, we added quarterly liquidity options2. In April, Aaron Rosen, CFA, was hired to serve as Portfolio Manager, adding significant expertise and an additional sourcing network. As a result, our pipeline of new opportunities has significantly expanded our capabilities and access to institutional opportunities and has resulted in new allocations and a strategic reevaluation of certain existing investments, all aimed at optimizing our portfolio’s performance in the years to come.

In the 2022 fiscal period, AOGFX delivered an exceptional outperformance of 22.49% compared to a ‘typical’ 60/40 stock & bond portfolio (2.33% vs.-20.16%). However, the opposite was true in fiscal year 2023, with AOGFX returning 1.27% net to investors, while a 60/40 portfolio3 yielded a return of 13.23%. This turbulence is likely more indicative of the volatile environment in public equities, and especially bonds during these two periods than anything else. Nevertheless, when we examine our absolute performance on a since-inception basis, we remain ahead of the 60/40 portfolio by nearly 800 basis points4 (2.06% vs. -5.88%). Further setting us apart is the notably lower volatility we offered, with a standard deviation5 of just 2.13%, as opposed to the 14.20% standard deviation associated with the 60/40 portfolio. While our since-inception relative performance remains robust, it is fair to acknowledge that on an absolute basis it fell short of expectations, a topic we will further review below.

| 1 | The Endowment Model has the following as its primary investment characteristics: broad diversification across all asset classes, low allocations to assets with low expected returns, and high allocations to illiquid assets such as private equity, private credit, real estate, and venture capital. |

| 2 | The Fund has adopted a fundamental policy to make annual repurchase offers in the third calendar quarter of each year, at per-class NAV, of not less than 5% and no more than 25% of the Fund’s outstanding Shares on the repurchase request deadline. In addition to this minimum repurchase offer, the Fund may, in the sole discretion of the Board, make additional writen tender offers of its outstanding Shares pursuant to Rule 13e-4 of the Exchange Act at such times and in such amounts as the Board may determine, with such discretionary repurchases to typically occur on March 15, June 15, and December 15 of each year. |

| 3 | A 60/40 portfolio is represented here by the S&P500 Index and Barclays Aggregate Bond Index, respectively. |

| 4 | One basis point is equivalent to 0.01%. |

| 5 | Standard Deviation is defined as a statistical calculation that investors use as a measure of price variability. Standard deviation measures the dispersion of a dataset relative to its mean. |

1

AOG Institutional Fund

Letter to Shareholders (Unaudited) (Continued)

September 30, 2023

For simplicity, we often categorize alternative investments into four specific sectors: Private Equity/Venture Capital (“PE/VC”), Private Credit/Debt, Private Real Estate, and Other. For the fiscal year, Private Credit/Debt stood out as the best performing alternative asset class in the portfolio (contributing +$0.46/share of NAV) and we expect to continue to actively increase allocations to this asset class. The first half of the year was characterized by markdowns in both Real Estate and PE/VC, after multi-year runs of outsized performance in each. While PE/VC rebounded in the second half (full-year contributing +$0.29/share of NAV), Real Estate ended the fiscal period as the only alternative asset class with negative atribution during the full fiscal year (contributing -$0.28/share).

With the significant outperformance of broad real estate in prior years, and the expected economic impact of continued rising interest rates and federal overspending becoming clearer, we started paring back holdings in this sector where liquidity was available. As subsequent economic conditions began causing early signs of weakness in portfolio valuations, redemptions were accelerated, allowing us to avoid further negative performance effects. We are now significantly underweight in the Real Estate sector, decreasing from 46% to 8% of the AOGFX portfolio during the fiscal year. Currently, we find it more advantageous owning real estate debt than equity, which allows us to stay senior in the capital stack until the current buyer-seller imbalance equalizes, and cap rates standardize. Additionally, as existing real estate debt comes due, and lending standards are likely to become more rigorous, we think it will inevitably force more pressured sales. We expect this combination to cause value impairments in certain existing equity real estate portfolios, while creating atractive buying opportunities for those investing new capital as opportunities arise.

As a consequence of our strategic move to redeem a substantial portion of our real estate equity holdings, we deliberately but temporarily increased our cash and short-term Treasuries positions during the later part of the fiscal year. These holdings, currently yielding accretive returns, provided us with a more liquid foundation, enabling us to respond swiftly to emerging, atractive opportunities in the market. This approach allowed us to efficiently allocate resources to new investment prospects.

Within our investment pipeline, we identified generational opportunities within select niche private credit arenas, where seizing these opportunities required a nimble and proactive approach. Consequently, we strategically increased our Private Credit exposure within AOGFX from 20% to 35%, and if all outstanding capital calls were met today, the sector would represent just over 50% of the portfolio. What excited us about these credit opportunities extended beyond their atractive return prospects; it was the seemingly misunderstood risk mitigants that indicated an inherent potential for asymmetric risk-reward dynamics. While many traditional lending facilities are in retreat, credits with strong covenants and guarantees have, at least temporarily, been available at abnormally high rates of return.

Another area of significant growth within AOGFX with immediate atractive opportunities to allocate is the direct and co-investment arenas, notably within private equity secondary markets and select off-market transactions. Some of these opportunities were directly sourced and negotiated by our team, while others were shared with us by private firms with whom we maintain established relationships. These opportunities also materialized swiftly and had short windows for execution, and fortunately our surplus liquidity was again essential in capturing these opportunities. Several of these investments have already demonstrated significant appreciation, further bolstering our confidence in their future performance.

2

AOG Institutional Fund

Letter to Shareholders (Unaudited) (Continued)

September 30, 2023

Additionally, AOGFX was able to negotiate low or no underlying fees whatsoever on many of these investments.

The AOGFX cash and Treasury holdings have been reduced by almost 50% since the end of the fiscal year, as we have proactively deployed these resources through recent capital calls. Furthermore, we have several pending commitments expected to be called before the end of the calendar year in some exciting additional investments. With these developments, we anticipate that cash and Treasuries will constitute approximately 5% of the total fund by December 31st, aligning more closely with our long-term expectations.

While more muted temporary performance was not entirely unexpected during the portfolio transitioning and incubation periods, we are witnessing signs of a shift in the tide. We are now entering a period where some of our premier investments have incubated and/or called down additional capital, allowing them to get to a point in their life cycle where we expect them to contribute significantly more accretive return streams to AOGFX. We believe this bodes very well for future performance.

Sincerely,

AOGFX Management Team

3

AOG Institutional Fund

Letter to Shareholders (Unaudited) (Continued)

September 30, 2023

IMPORTANT INFORMATION

An investor should consider the Fund’s investment objectives, risks, and charges and expenses carefully before investing or sending money. This and other important information can be found in the Fund’s prospectus. To obtain a prospectus, please 877-600-3573 or visit aogfunds.com. Please read the prospectus carefully before investing.

Investment in the AOG Institutional Fund (“AOGFX Fund”) is speculative and involves substantial risks, including the risk of loss of a Shareholder’s entire investment. Investors may not have immediate access to invested capital for an indefinite period of time and must have the financial ability, sophistication/experience, and willingness to bear the risks of an illiquid investment. No public market for Shares exists, and none is expected to develop in the future. An investor’s participation in the Fund is a long-term commitment, with no certainty of return. No guarantee or representation is made that a Fund will achieve its investment objective, and investment results may vary substantially from year to year.

Opinions expressed are subject to change at any time, are not guaranteed, and should not be considered investment advice. Diversification does not assure a profit nor protect against loss in a declining market. There is no guarantee that the Fund can or will pay distributions or if any of the distributions will be derived from return of capital. Shareholders will be subject to annual fees and operating expenses that can be found in the Fund’s prospectus.

The AOG Institutional Fund is distributed by UMB Distribution Services, LLC.

See accompanying notes to financial statements for additional important information and risk considerations.

4

| AOG Institutional Fund |

| PORTFOLIO REVIEW (Unaudited) |

| September 30, 2023 |

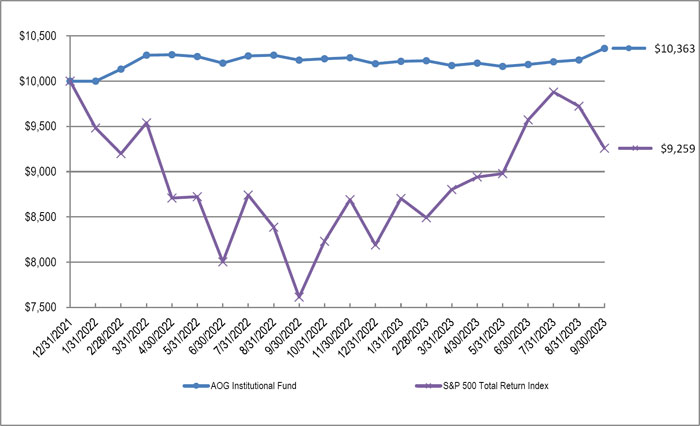

The Fund’s performance figures* for the periods ended September 30, 2023, compared to its benchmark:

| Annualized | ||

| Since Inception | ||

| One Year | (12/31/2021) | |

| AOG Institutional Fund | 1.27% | 2.06% |

| S&P 500 Total Return Index (a) | 21.62% | (4.31)% |

Comparison of the Change in Value of a $10,000 Investment

| (a) | The S&P 500 Total Return Index is a widely accepted, unmanaged index of U.S. stock market performance which does not take into account charges, fees and other expenses. Investors cannot invest directly in an index. |

| * | The performance data quoted here represents past performance. Current performance may be lower or higher than the performance data quoted above. Investment return and principal value will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost. Total returns are calculated using the traded NAV as September 30, 2023. The returns shown assume reinvestment of all distributions, and do not reflect the deduction of taxes that shareholder would pay on Fund distributions or on the redemption of Fund shares. Past performance is no guarantee of future results. Please read the Fund’s Prospectus carefully before investing. For performance information current to the most recent month-end, please call 1-877-600-3573. |

| Holdings By Asset Class as of September 30, 2023 | % of Net Assets | |||

| AOG Institutional Diversfied Master Fund (“Master Fund”) | 107.7 | % | ||

| Liabilities in Excess of Other Assets | (7.7 | )% | ||

| 100.0 | % | |||

5

| AOG Institutional Fund |

| STATEMENT OF ASSETS AND LIABILITIES |

| September 30, 2023 |

| Assets: | ||||

| Investments in Master Fund, at Cost | $ | 66,589,472 | ||

| Investments in Master Fund, at Value | $ | 67,747,105 | ||

| Deferred offering costs | 130,467 | |||

| Prepaid Expenses and Other Assets | 6,275 | |||

| Total Assets | 67,883,847 | |||

| Liabilities: | ||||

| Accrued advisory fees | 80,618 | |||

| Payable for Fund Shares Redeemed | 4,616,345 | |||

| Accrued offering costs | 151,722 | |||

| Accrued audit fees | 45,000 | |||

| Accrued legal fees | 47,820 | |||

| Accrued professional fees | 10,417 | |||

| Other accrued expenses | 40,996 | |||

| Total Liabilities | 4,992,918 | |||

| Net Assets | $ | 62,890,929 | ||

| Total Shares of Beneficial Interest Outstanding | ||||

| ($0 par value, unlimited shares authorized) | 4,058,562 | |||

| Net Asset Value and Offering Price Per Share | ||||

| (Net assets / Total shares of beneficial interest outstanding) | $ | 15.50 | ||

| Composition of Net Assets: | ||||

| Paid-in-Capital | $ | 61,743,315 | ||

| Accumulated Earnings | 1,147,614 | |||

| Net Assets | $ | 62,890,929 |

See accompanying notes to financial statements.

6

| AOG Institutional Fund |

| STATEMENT OF OPERATIONS |

| For The Year Ended September 30, 2023 |

| Net Investment Income (Loss) Allocated From the Master Fund: | ||||

| Dividend and Interest Income | $ | 2,061,828 | ||

| Expenses | (1,048,770 | ) | ||

| Net Investment Income Allocated From the Master Fund | 1,013,058 | |||

| Fund Expenses: | ||||

| Investment Advisory Fees | 98,997 | |||

| Offering costs | 154,480 | |||

| Administration Fees | 108,124 | |||

| Audit Fees | 47,500 | |||

| Legal Fees | 47,821 | |||

| Transfer Agent Fees | 44,264 | |||

| Printing Expenses | 28,897 | |||

| Fund Accounting Fees | 19,308 | |||

| Chief Compliance Officer and Chief Financial Officer Fees | 18,313 | |||

| Trustees’ Fees | 2,115 | |||

| Custody Fees | 1,128 | |||

| Registration & Filing Fees | 986 | |||

| Miscellaneous Expenses | 7,643 | |||

| Total Expenses | 579,576 | |||

| Net Investment Income | 433,482 | |||

| Net Realized and Unrealized Gain/(Loss) on Investments: | ||||

| Net Realized Loss on Investments Allocated From Master Fund | (81,120 | ) | ||

| Distributions of Realized Gains by Underlying Investments Allocated from Master Fund | 148,652 | |||

| Net Realized Gain | 67,532 | |||

| Net Change in Unrealized Appreciation on Investments Allocated From Master Fund | 750,609 | |||

| Net Realized and Unrealized Gain on Investments | 818,141 | |||

| Net Increase in Net Assets Resulting From Operations | $ | 1,251,623 |

See accompanying notes to financial statements.

7

| AOG Institutional Fund |

| STATEMENTS OF CHANGES IN NET ASSETS |

| Year Ended | Period Ended | |||||||

| September 30, | September 30, | |||||||

| 2023 | 2022* | |||||||

| Operations: | ||||||||

| Net Investment Income/(Loss) | $ | 433,482 | $ | (79,698 | ) | |||

| Net Realized Gain/(Loss) on Investments | (81,120 | ) | (234,482 | ) | ||||

| Distributions of Realized Gains by Underlying Investments | 148,652 | 79,118 | ||||||

| Net Change in Unrealized Appreciation on Investments | 750,609 | 407,024 | ||||||

| Net Increase in Net Assets Resulting From Operations | 1,251,623 | 171,962 | ||||||

| Distributions to Shareholders From: | ||||||||

| Distributions Paid from Earnings | (320,669 | ) | — | |||||

| Return of Capital | (272,884 | ) | — | |||||

| Total Distributions to Shareholders | (593,553 | ) | — | |||||

| Beneficial Interest Transactions: | ||||||||

| Proceeds from Shares Issued | 17,392,000 | 49,179,000 | ||||||

| Distributions Reinvested | 6,242 | — | ||||||

| Cost of Shares Redeemed | (4,616,345 | ) | — | |||||

| Net Increase in Net Assets Resulting From Beneficial Interest Transactions | 12,781,897 | 49,179,000 | ||||||

| Net Increase in Net Assets | 13,439,967 | 49,350,962 | ||||||

| Net Assets: | ||||||||

| Beginning of Year/Period | 49,450,962 | 100,000 | ||||||

| End of Year/Period | $ | 62,890,929 | $ | 49,450,962 | ||||

| Share Activity: | ||||||||

| Shares Issued | 1,140,001 | 3,211,440 | ||||||

| Shares Reinvested | 411 | — | ||||||

| Shares Redeemed | (299,957 | ) | — | |||||

| Net Increase in Total Shares Outstanding | 840,455 | 3,211,440 | ||||||

| * | The AOG Institutional Fund commenced operations on December 31, 2021. |

See accompanying notes to financial statements.

8

| AOG Institutional Fund |

| STATEMENT OF CASH FLOWS |

| For The Year Ended September 30, 2023 |

| Cash Flows From Operating Activities: | ||||

| Net Increase in Net Assets Resulting From Operations | $ | 1,251,623 | ||

| Adjustments to Reconcile Net Increase in Net Assets Resulting From Operations to Net Cash Used for Operating Activities: | ||||

| Purchases of Long-Term Portfolio Investments | (17,458,419 | ) | ||

| Change in Unrealized Appreciation on Investments | (750,609 | ) | ||

| Changes in Assets and Liabilities: | ||||

| (Increase)/Decrease in Assets: | ||||

| Due From Investment Adviser | 8,425 | |||

| Deferred Offering Costs | (113,181 | ) | ||

| Prepaid Expenses and Other Assets | (6,275 | ) | ||

| Increase/(Decrease) in Liabilities: | ||||

| Accrued Advisory Fees | 80,618 | |||

| Accrued Audit Fees | 15,000 | |||

| Accrued Legal Fees | 47,820 | |||

| Payable for Fund Shares Redeemed | 4,616,345 | |||

| Accrued offering costs | 83,139 | |||

| Accrued Professional Fees | 7,896 | |||

| Accrued Miscellaneous Fees | 29,274 | |||

| Net Cash Used for Operating Activities | (12,188,344 | ) | ||

| Cash Flows From Financing Activities: | ||||

| Proceeds from Shares Issued | 17,392,000 | |||

| Payment on Shares Redeemed | (4,616,345 | ) | ||

| Cash Distributions Paid to Shareholders, Net of Reinvestments | (587,311 | ) | ||

| Net Cash Provided by Financing Activities | 12,188,344 | |||

| Net Increase in Cash | — | |||

| Cash at Beginning of Year | — | |||

| Cash at End of Year | $ | — | ||

| Supplemental Disclosure of Non-Cash Activity: | ||||

| Non-cash Financing Activities not Included Above Consists of Reinvestment of Distributions | $ | 6,242 |

See accompanying notes to financial statements.

9

| AOG Institutional Fund |

| FINANCIAL HIGHLIGHTS |

The table below sets forth financial data for one share of beneficial interest outstanding throughout each year/period.

| Year Ended | Period Ended | |||||||

| September 30, | September 30, | |||||||

| 2023 | 2022* | |||||||

| Net Asset Value, Beginning of Year/Period | $ | 15.37 | $ | 15.00 | ||||

| Income From Operations: | ||||||||

| Net investment income/(loss) (a) | 0.12 | (0.06 | ) | |||||

| Net gain from investments (both realized and unrealized) | 0.16 | 0.43 | ||||||

| Total from operations | 0.28 | 0.37 | ||||||

| Less Distributions: | ||||||||

| From net investment income | (0.08 | ) | — | |||||

| From return of capital | (0.07 | ) | — | |||||

| Total Distributions | (0.15 | ) | — | |||||

| Net Asset Value, End of Year/Period (d) | $ | 15.50 | $ | 15.37 | ||||

| Total Return (b, d) | 1.86 | % | 2.47 | % (c) | ||||

| Ratios/Supplemental Data | ||||||||

| Net assets, end of year/period (in 000’s) | $ | 62,891 | $ | 49,451 | ||||

| Ratio of Expenses to Average Net Assets (f) | 2.89 | % | 2.65 | % (e) | ||||

| Ratio of Expenses to Average Net Assets (excluding waivers) (f) | 2.89 | % | 2.71 | % (e) | ||||

| Ratio of Net Investment Income/(Loss) to Average Net Assets (f) | 0.77 | % | (0.49 | )% (e) | ||||

| * | The AOG Institutional Fund commenced operations on December 31, 2021. |

| (a) | Per share amounts are calculated using the average shares method, which appropriately presents the per share data for the year/period. |

| (b) | Total returns are historical in nature and assume changes in share price, reinvestment of dividends and capital gains distributions, if any. |

| (c) | Not Annualized. |

| (d) | Includes adjustments made in accordance with accounting principles generally accepted in the United States and consequently, the net asset value for financial statement purposes and the returns based upon those net assets may differ from the net asset values and returns used for shareholder processing. |

| (e) | Annualized. |

| (f) | Includes income and expenses allocated from the Master Fund. |

See accompanying notes to financial statements.

10

| AOG Institutional Fund |

| NOTES TO FINANCIAL STATEMENTS |

| September 30, 2023 |

| 1. | ORGANIZATION |

The AOG Institutional Fund, formerly, the AOG Diversified Institutional Fund (the “Fund”) is a Delaware statutory trust registered under the 1940 Act as a non-diversified, closed-end management investment company. The Fund commenced operations on December 31, 2021.

The Fund and the AOG Institutional Fund (the “Feeder Fund”) operates in a master feeder structure and invests substantially all of their assets in shares of the AOG Institutional Diversified Master Fund (the “Master Fund”). The Fund adopted a policy to provide a limited degree of liquidity to its shareholders (“Shareholders”) by conducting one repurchase offer in the third quarter of each year at the net asset value (“NAV”) per share, of not less than 5% nor more than 25% of the Fund’s outstanding Shares, on the repurchase request deadline (the “Repurchase Policy”). As a result of the adoption of the Repurchase Policy, and in connection with the Fund’s operation as an interval fund, the Fund will no longer operate as a feeder fund within a master-feeder structure . The Master Fund has submitted an application with the Securities and Exchange Commission (“SEC”) to become de-registered under the Investment Company Act, but will continue to exist as a wholly owned subsidiary of the Fund. On September 26, 2023, pursuant to Rule 477 under the Securities Act of 1933, Tender Fund’s registration statement on Form N-2 was withdrawn. The Tender Fund is awaiting approval from the SEC to become deregistered under the Investment Company Act. The Board of Trustees (the “Board”) intends to dissolve the Tender Fund.

In pursuing the Fund’s investment objective, AOG Wealth Management, (the “Adviser”) will seek to achieve the Fund’s investment objective in income-producing assets and assets selected for long-term capital appreciation. The Adviser intends to invest the Fund’s assets primarily in portfolio investments, including a mix of liquid, traditional equity and fixed income investments as well as liquid, alternative and non-traditional investments (collectively, “Portfolio Investments”). In general, the Fund’s Portfolio Investments are expected to include the following types of investments, both liquid and illiquid: (i) alternative investment funds, including privately offered pooled investment vehicles and publicly offered funds; such as interval funds, tender offer funds, and business development companies that are offered in public offerings or private placements to investors that meet certain suitability standards (collectively, “Investment Funds”), (ii) direct investments in U.S. and non-U.S. equity and fixed income assets which may be substantially similar to those made by Investment Funds, including, but not limited to, notes, bonds, and asset-backed securities, made in co-investment transactions with such Investment Funds; (iii) REITs and other real estate investments; (iv) energy and natural resource investments, including, but not limited to MLPs, oil and gas funds and other energy and natural resource funds; (v) commodity investments, including, but not limited to, commodity pools and precious metals; (vi) absolute return investments, including but not limited to, to managed futures funds, hedge funds and other absolute return investment vehicles; and (vii) U.S. and non-U.S. equity investments, without limitation on an issuer’s capitalization size or specific markets or sectors. The investment objective of the Fund is non-fundamental and, therefore, may be changed without the approval of the Shareholders The financial statements of the Master Fund, including the Schedule of Investments, are attached to this report and should be read in conjunction with the Fund’s financial statements.

As of September 30, 2023, the Fund has a 100% ownership interest in the Master Fund.

| 2. | SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES |

The following is a summary of significant accounting policies followed by the Fund in the preparation of its financial statements. These policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”). The preparation of financial statements in accordance with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of income and expenses for the period. Actual results could differ from those estimates. The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standard Codification Topic 946 “Financial Services – Investment Companies” including FASB Accounting Standard Update (“ASU”) 2013-08.

11

| AOG Institutional Fund |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| September 30, 2023 |

Net Asset Value Determination – The Fund calculates its Net Asset Value (“NAV”) as of the close of each business day effective August 25, 2023, each date that Shares are offered or repurchased, as of the date of any distribution and at such other times as the Board of Trustees (the “Board”) shall determine (each, a “Determination Date”). In determining its NAV, the Fund values its investments as of the relevant Determination Date. The NAV of each Fund equals the value of the total assets of the Fund, less all of its liabilities, including accrued fees and expenses, each determined as of the relevant Determination Date.

Investment in the Master Fund – The Fund’s investment in the Master Fund is valued at an amount equal to the net asset value of the investment without discount or premium, which approximates fair value. Income, expense and net realized gain (losses) of the Master Fund, are allocated each day to the Fund based on its pro-rata ownership of the Master Fund. The more relevant disclosure regarding fair value measurements impacting the Fund is related to the Master Fund’s investment portfolio. Such disclosure can be found in the Notes to the Master Fund’s attached financial statements.

Valuation of Investments – The Adviser oversees the valuation of the Fund’s investments. The Board has approved valuation procedures for the Fund (the “Valuation Procedures”).

The Valuation Procedures provide that the Master Fund will value its investments in Investment Funds and direct private equity investments at fair value. The fair value of such investments as of each Determination Date ordinarily will be the capital account value of the Fund’s interest in such investments as provided by the relevant Investment Fund manager as of or prior to the relevant Determination Date; provided that such values will be adjusted for any other relevant information available at the time the Fund values its portfolio, including capital activity and material events occurring between the reference dates of the Investment Fund manager’s valuations and the relevant Determination Date.

The valuation of each of the Fund’s investments is performed in accordance with the principles found in Rule 2a-5 of the 1940 Act and in conjunction with FASB’s Accounting Standards Codification Topic 820, Fair Value Measurements and Disclosures (“ASC 820-10”). A meaningful input in the Fund’s Valuation Procedures will be the valuations provided by the Investment Fund managers. Specifically, the value of the Fund’s investment in Investment Funds generally will be valued using the “practical expedient,” in accordance with ASC 820-10, based on the valuation provided to the Adviser by the Investment Fund in accordance with the Investment Fund’s own valuation policies. Generally, Investment Fund managers value investments of their Investment Funds at their market price if market quotations are readily available. In the absence of observable market prices, Investment Fund managers value investments using valuation methodologies applied on a consistent basis. For some investments little market activity may exist. The determination of fair value by Investment Fund managers is then based on the best information available in the circumstances and may incorporate management’s own assumptions and involves a significant degree of judgment, taking into consideration a combination of internal and external factors, including the appropriate risk adjustments for nonperformance and liquidity risks. Investments for which market prices are not observable include private investments in the equity of operating companies, real estate properties or certain debt positions.

Market quotations will not be readily available for most of the Fund’s investments. To the extent the Fund holds securities or other instruments that are not investments in Investment Funds or direct private equity investments, the Fund will generally value such assets as described below.

Equity Securities – Securities listed on a securities exchange, market or automated quotation system for which quotations are readily available (except for securities traded on NASDAQ), including securities traded over the counter, are valued at the last quoted sale price on an exchange or market (foreign or domestic) on which they are traded on the valuation date (or at approximately 4:00 p.m. Eastern Time if such exchange is normally open at that time), or, if there is no such reported sale on the valuation date, at the most recent quoted bid price. For securities traded on NASDAQ, the NASDAQ Official Closing Price will be used. If such prices are not available or determined to not represent the fair value of the security as of the Fund’s pricing time, the security will be valued at fair value as determined in good faith using methods approved by the Board.

12

| AOG Institutional Fund |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| September 30, 2023 |

Money Market Securities and other Debt Securities – If available, money market securities and other debt securities are priced based upon valuations provided by recognized independent, third-party pricing agents. Such values generally reflect the last reported sales price if the security is actively traded. The third-party pricing agents may also value debt securities by employing methodologies that utilize actual market transactions, broker-supplied valuations, or other methodologies designed to identify the market value for such securities. Such methodologies generally consider such factors as security prices, yields, maturities, call features, ratings and developments relating to specific securities in arriving at valuations. Money market securities and other debt securities with remaining maturities of sixty days or less may be valued at their amortized cost, which approximates market value. If such prices are not available or determined to not represent the fair value of the security as of the Fund’s pricing time, the security will be valued at fair value as determined in good faith using methods approved by the Board.

Valuation of Fund of Funds – The Fund may invest in portfolios of open-end or closed-end investment companies (the “Underlying Funds”). The Underlying Funds value securities in their portfolios for which market quotations are readily available at their market values (generally the last reported sale price) and all other securities and assets at their fair value to the methods established by the board of directors of the Underlying Funds.

Open-end investment companies are valued at their respective net asset values as reported by such investment companies. The shares of many closed-end investment companies, after their initial public offering, frequently trade at a price per share, which is different than the net asset value per share. The difference represents a market premium or market discount of such shares. There can be no assurance that the market discount or market premium on shares of any closed-end investment company purchased by the Fund will not change.

Exchange-Traded Funds – The Fund may invest in exchange-traded funds (“ETFs”). ETFs are a type of fund bought and sold on a securities exchange. An ETF trades like common stock and represents a fixed portfolio of securities. The Fund may purchase an ETF to gain exposure to a portion of the U.S. or a foreign market. The risks of owning an ETF generally reflect the risks of owning the underlying securities they are designed to track, although a potential lack of liquidity on an ETF could result in it being more volatile. Additionally, ETFs have fees and expenses that reduce their value.

Fair Value Procedures – Securities for which market prices are not “readily available” or which cannot be valued using the methodologies described above are valued in accordance with Fair Value Procedures established by the Board and implemented through the Fair Value Pricing Committee established by the Board. The members of the Fair Value Pricing Committee report, as necessary, to the Board regarding portfolio valuation determinations. The Board, from time to time, will review these methods of valuation and will recommend changes which may be necessary to ensure that the investments of the Fund are valued at fair value.

Some of the more common reasons that may necessitate a security being valued using Fair Value Procedures include: the security’s trading has been halted or suspended; the security has been de-listed from a national exchange; the security’s primary trading market is temporarily closed at a time when under normal conditions it would be open; the security has not been traded for an extended period of time; the security’s primary pricing source is not able or willing to provide a price; trading of the security is subject to local government-imposed restrictions; or a significant event with respect to a security has occurred after the close of the market or exchange on which the security principally trades and before the time the Fund calculates NAV. When a security is valued in accordance with the Fair Value Procedures, the Fair Value Pricing Committee will determine the value after taking into consideration relevant information reasonably available to the Fair Value Pricing Committee.

The Fund utilizes various methods to measure the fair value of all of its investments on a recurring basis. GAAP establishes a hierarchy that prioritizes inputs to valuation methods. The three levels of input are:

Level 1 – Unadjusted quoted prices in active markets for identical assets and liabilities that the Fund has the ability to access.

Level 2 – Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument in an inactive

13

| AOG Institutional Fund |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| September 30, 2023 |

market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data.

Level 3 – Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Fund’s own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available.

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities. The following table summarizes the inputs used as of September 30, 2023 for the Fund’s assets measured at fair value:

| Investments | ||||||||||||||||||||

| Assets | Level 1 | Level 2 | Level 3 | Valued at NAV* | Total | |||||||||||||||

| Master Fund | $ | — | $ | — | $ | — | $ | 67,747,105 | $ | 67,747,105 | ||||||||||

| Total | $ | — | $ | — | $ | — | $ | 67,747,105 | $ | 67,747,105 | ||||||||||

| * | Investments valued using NAV as the practical expedient, an indicator of fair value, are listed in a separate column to permit reconciliation to totals presented on the Statement of Assets and Liabilities. |

There were no transfers into or out of Levels 2 or 3 during the year.

Security Transactions and Investment Income – Investment security transactions are accounted for on a trade date basis. Realized gains and losses from sales of securities are based upon the specific identification method for both financial statement and federal income tax purposes. Dividend income is recorded on the ex-dividend date and interest income is recorded on the accrual basis.

Expenses – The Fund, and therefore, the Shareholders, bear all expenses incurred in the business of the Fund, and, through its investment in the Master Fund, a pro-rata portion of the operating expenses of the Master Fund. Additionally, the Fund bears certain ongoing offering costs associated with the Fund’s continuous offering of shares. In connection with the Fund’s operations as an Interval Fund, the outstanding liabilities of the Master Fund have been transferred to the Fund.

Offering Costs – In connection with the conversion of the Fund to an Interval Fund structure, certain offering costs were incurred. These offering costs will be amortized on a straight line basis over the first twelve months of the Interval Fund’s operations. Offering costs consist primarily of legal fees in connection with the preparation of the registration statement and related filings. As of September 30, 2023, the total offering costs expensed were $154,480.

Federal Income Taxes – The Fund intends to continue to qualify as a “regulated investment company” under Subchapter M of the Internal Revenue Code of 1986, as amended, and, if so qualified, will not be liable for federal income taxes to the extent all earnings are distributed to Shareholders on a timely basis. Therefore, no federal income tax provision has been recorded.

14

| AOG Institutional Fund |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| September 30, 2023 |

The Fund recognizes the tax benefits of uncertain tax positions only where the position is “more likely than not” to be sustained assuming examination by tax authorities. Management has analyzed the Fund’s tax positions and has concluded that no liability for unrecognized tax benefits should be recorded related to uncertain tax positions for the open tax year ended September 30, 2022, or is expected to be taken on returns filed for the year ended September 30, 2023. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the Statement of Operations. During the year ended September 30, 2023, the Fund did not incur any interest or penalties. The Fund identifies its major tax jurisdictions as U.S. federal and foreign jurisdictions where the Fund makes significant investments; however, the Fund is not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will change materially in the next twelve months.

Distributions to Shareholders – Distributions from investment income, if any, are declared and paid quarterly and are recorded on the ex-dividend date. Distributions from net realized capital gains, if any, are declared and paid at least annually and are recorded on the ex-dividend date. The character of income and gains to be distributed is determined in accordance with income tax regulations, which may differ from GAAP. These “book/tax” differences are considered either temporary (i.e., deferred losses, capital loss carry forwards) or permanent in nature. To the extent these differences are permanent in nature, such amounts are reclassified within the composition of net assets based on their federal tax-basis treatment. Temporary differences do not require reclassification. These reclassifications have no effect on net assets, results from operations or NAV per share of the Fund.

Indemnification – In the normal course of business the Fund will enter into contracts with third-party service providers that contain a variety of representations and warranties and that provide general indemnifications. Additionally, under the Fund’s organizational documents, the officers and trustees are indemnified against certain liabilities arising out of the performance of their duties to the Fund. The Fund’s maximum exposure under these arrangements is unknown, as it involves possible future claims that may or may not be made against the Fund. Based on experience, the Adviser is of the view that risk of loss to the Fund in connection with the Fund’s indemnification obligations is remote; however, there can be no assurance that such obligations will not result in material liabilities that adversely affect the Fund.

| 3. | AGREEMENTS |

Investment advisory services are provided to the Fund by the Adviser pursuant to an investment advisory agreement entered into between the Fund and the Adviser (the “Investment Advisory Agreement”. Effective November 16, 2022, and pursuant to the Investment Advisory Agreement, the Fund pays the Adviser a fee (the “Management Fee”), accrued daily and payable monthly, at the annual rate of 1.49% of the Fund’s average daily Managed Assets. Prior to November 16, 2022, the Fund paid the Adviser a management fee accrued daily and payable monthly, at the annual rate of 0.50% of the Fund’s average daily Managed Assets. “Managed Assets” means the total assets of the Fund (including any assets attributable to money borrowed for investment purposes) minus the sum of the Fund’s accrued liabilities (other than money borrowed for investment purposes) and calculated before giving effect to any repurchase of shares on such date. The Management Fee is paid to the Adviser out of the Fund’s assets and, therefore, decreases the net profits or increases the net losses of the Fund. See the “Board Considerations – Approval of New Advisory Agreement” at the end of this report for additional information.

The Adviser has contractually agreed to waive fees and/or to reimburse expenses to the extent necessary to keep Fund Operating Expenses (defined below) incurred by the Fund from exceeding 2.95% of the Fund’s average daily net assets until January 11, 2024 (the “Initial Term Date”). “Fund Operating Expenses” are defined to include all expenses incurred in the business of the Fund, provided that the following expenses (“excluded expenses”) are excluded from the definition of Fund Operating Expenses: (i) any class-specific expenses (including distribution and service (12b-1) fees and shareholder servicing fees), (ii) Nasdaq Fund Secondaries expenses, if the Fund elects to utilize Nasdaq Fund Secondaries in a given year, (iii) any acquired fund fees and expenses, (iv) short sale dividend and interest expenses, and any other interest expenses incurred by the Fund in connection with its investment activities, (v) fees and expenses incurred in connection with a credit facility, if any, obtained by the Fund, (vi) taxes, (vii) certain insurance costs, (viii) transactional costs, including legal costs and brokerage fees and commissions, associated with the acquisition and disposition of the Fund’s Portfolio Investments and other investments, (ix) non

15

| AOG Institutional Fund |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| September 30, 2023 |

routine expenses or costs incurred by the Fund, including, but not limited to, those relating to reorganizations, litigation, conducting shareholder meetings and liquidations and (x) other expenditures which are capitalized in accordance with generally accepted accounting principles. In addition, the Adviser may receive from the Fund the difference between the Fund Operating Expenses (not including excluded expenses) and the contractual expense limit to recoup all or a portion of its prior fee waivers or expense reimbursements made during the rolling three-year period preceding the date of the recoupment if at any point Fund Operating Expenses (not including excluded expenses) are below the contractual expense limit (i) at the time of the fee waiver and/or expense reimbursement and (ii) at the time of the recoupment. The Investment Advisory Agreement will continue in effect from year to year for successive one-year terms after the Initial Term End Date unless terminated by the Board or the Adviser. The agreement may be terminated: (i) by the Board, for any reason at any time; or (ii) by the Adviser, upon ninety (90) days’ prior written notice to the Fund. If the agreement is terminated by the Adviser, the effective date of such termination will be the last day of the current term. If the Investment Advisory Agreement is terminated by the Adviser, the effective date of such termination will be the last day of the current term. The Advisor did not waive any fees for the year ended September 30, 2023.

Employees of PINE Advisors, LLC (“PINE”) serve as the Fund’s Chief Compliance Officer and Chief Financial Officer. PINE receives an annual base fee for the services provided to the Fund. PINE is reimbursed for certain out-of-pocket expenses by the Fund. Service fees paid by the Fund for the year ended September 30, 2023 are disclosed in the Statement of Operations as Chief Compliance Officer and Chief Financial Officer Fees.

| 4. | PURCHASE, EXCHANGE AND REPURCHASE OF SHARES |

The Fund has adopted a policy to provide a limited degree of liquidity to Shareholders by conducting one repurchase offer in the third calendar quarter of each year at the net asset value (“NAV”) per Share, of not less than 5% nor more than 25% of the Fund’s outstanding Shares, on the repurchase request deadline. In the repurchase offer, the Fund will offer to repurchase Shares at their NAV as determined by the Board (the “Repurchase Pricing Date”). Each repurchase offer will be for not less than 5% nor more than 25% of the Fund’s Shares outstanding, but if the amount of Shares tendered for repurchase exceeds the amount the Fund intended to repurchase, the Fund will generally repurchase less than the full number of Shares tendered. In such event, Shareholders will have their Shares repurchased on a pro rata basis, and tendering Shareholders will not have all of their tendered Shares repurchased by the Fund. Shareholders tendering shares for repurchase will be asked to give written notice of their intent to do so by the date specified in the notice describing the terms of the applicable repurchase offer. While not offered by the Fund, Shareholders may also have the opportunity for liquidity through participation in the Nasdaq Fund Secondaries Auction Process.

In addition to this minimum repurchase offer, the Fund may, in the sole discretion of the Fund’s Board, make additional written tender offers of its outstanding Shares pursuant to Rule 13e-4 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), at such times and in such amounts as the Board may determine, with such repurchases typically to occur on March 15, June 15, and December 15 of each year.

During the year ended September 30, 2023, the Fund had Repurchase Offers as follows:

| Number of | Redemption | ||||

| Repurchase | Repurchase Request | Repurchase | % of Shares | Shares | Price per |

| Offer Notice | Deadline | Offer Amount | Repurchased | Repurchased | Share |

| September 1, 2023 | September 29, 2023 | 5.00% | 6.88% | 299,957.44 | $15.39 |

Upon obtaining requisite Board approval, which the Fund expects to seek 24-36 months after it commenced operations, the Fund may make its shares available for secondary transfers on a periodic basis through an auction conducted via Nasdaq Fund Secondaries, LLC and its registered broker dealer and alternative trading system subsidiary, NFSTX, LLC (collectively, “Nasdaq Fund Secondaries”). As of September 30, 2023, the Fund has not requested Board approval to commence the Nasdaq Fund Secondaries auction process and has not accepted purchases of shares through Nasdaq Fund Secondaries.

16

| AOG Institutional Fund |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| September 30, 2023 |

| 5. | AGGREGATE UNREALIZED APPRECIATION AND DEPRECIATION – TAX BASIS |

The identified cost of investments for federal income tax purposes, and its respective unrealized appreciation and depreciation on September 30, 2023, were as follows:

| Gross Unrealized | Gross Unrealized | Net Unrealized | ||||||||||||

| Tax Cost | Appreciation | Depreciation | Appreciation | |||||||||||

| $ | 66,589,472 | $ | 1,174,541 | $ | (16,908 | ) | $ | 1,157,633 | ||||||

| 6. | DISTRIBUTIONS TO SHAREHOLDERS AND TAX COMPONENTS OF CAPITAL |

The tax character of distributions paid was as follows:

| Fiscal Year Ended | ||||

| September 30, 2023 | ||||

| Ordinary Income | $ | 320,669 | ||

| Long-Term Capital Gain | — | |||

| Return of Capital | 272,884 | |||

| $ | 593,553 | |||

There were no distributions for the fiscal year ended September 30, 2022.

As of September 30, 2023, the components of accumulated earnings on a tax basis were as follows:

| Undistributed | Undistributed | Post October Loss | Capital Loss | Other | Unrealized | Total | ||||||||||||||||||||

| Ordinary | Long-Term | and | Carry | Book/Tax | Appreciation/ | Distributable Earnings/ | ||||||||||||||||||||

| Income | Gains | Late Year Loss | Forwards | Differences | (Depreciation) | (Accumulated Deficit) | ||||||||||||||||||||

| $ | — | $ | — | $ | — | $ | — | $ | (10,019 | ) | $ | 1,157,633 | $ | 1,147,614 | ||||||||||||

The difference between book basis and tax basis accumulated net investment income/loss and unrealized appreciation from investments is primarily attributable to the tax adjustments for the Fund’s wholly-owned subsidiary.

For the year ended September 30, 2023, the following reclassifications for non-deductible expenses, which had no impact on results of operations or net assets, were recorded to reflect tax character.

| Paid | ||||||

| In | Distributable | |||||

| Capital | Earnings | |||||

| $ | (1,826 | ) | $ | 1,826 | ||

| 7. | RISKS |

An investment in the Fund is speculative and involves substantial risks, including the risk of loss of a Shareholder’s entire investment. No guarantee or representation is made that the Fund will achieve its investment objective, and investment results may vary substantially from year to year. Additional risks of investing in the Fund are set forth below.

Certain risk factors below discuss the risks of investing in the Investment Funds.

17

| AOG Institutional Fund |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| September 30, 2023 |

Competition – The business of investing in private markets opportunities is highly competitive, uncertain, and successfully sourcing investments can be problematic given the high level of investor demand some investment opportunities receive. There are no assurances that the Fund will be able to invest fully its assets or that suitable investment opportunities will be available.

Credit Risk – There is a risk that debt issuers will not make payments, resulting in losses to the Fund, and default perceptions could reduce the value and liquidity of securities and may cause the Fund to incur expenses in seeking recovery of principal or interest on its portfolio holdings. Lower-quality bonds, known as “high yield” or “junk” bonds, present a significant risk for loss of principal and interest and involve an increased risk that the bond’s issuer, obligor or guarantor may not be able to make its payments of interest and principal.

Distressed, Special Situations and Venture Investments – Investments in distressed companies and new ventures are subject to greater risk of loss than investments in companies with more stable operations or financial condition.

Equity Securities Risk – When the Fund invests in equity securities, the Fund’s investments in those securities are subject to price fluctuations based on a number of reasons of issuer-specific and broader economic or international considerations. They may also decline due to factors which affect a particular industry or industries. In addition, equity securities prices may be particularly sensitive to rising interest rates, as the cost of capital rises and borrowing costs increase. The prices of common equity securities are also sensitive to the market risks described above. Common equity securities in which the Fund may invest are structurally subordinated to other instruments in a company’s capital structure in terms of priority to corporate income and are therefore inherently riskier than preferred stock or debt instruments of such issuers. In addition, dividends on common equity securities which the Fund may hold are not fixed and there is no guarantee that the issuers of the common equity securities in which the Fund invests will declare dividends in the future or that, if declared, they will remain at current levels or increase over time.

Multiple Levels of Expense – Shareholders will pay the fees and expenses of the Fund and will bear the fees, expenses and carried interest (if any) of the Investment Funds in which the Fund invests.

Private Markets Investment Funds – The managers of the Investment Funds in which the Fund may invest may have relatively short track records and may rely on a limited number of key personnel. The portfolio companies in which the Investment Funds may invest also have no, or relatively short, operating histories, may face substantial competitive pressures from larger companies, and may also rely on a limited number of key personnel. The Fund will not necessarily have the opportunity to evaluate the information that an Investment Fund uses in making investment decisions.

Real Estate Securities Risks – The Fund may invest in publicly-traded and non-traded real estate investment trusts (“REITs”) or Investment Funds that hold real estate as well as invest in real estate directly through entities owned or controlled directly or indirectly by the Fund, including one or more entities that qualify as a REIT for federal income tax purposes such (a “REIT Subsidiary”). As a result, its portfolio may be significantly impacted by the performance of the real estate market and may experience more volatility and be exposed to greater risk than a more diversified portfolio. The value of companies investing in real estate is affected by, among other things: (i) changes in general economic and market conditions; (ii) changes in the value of real estate properties; (iii) risks related to local economic conditions, overbuilding and increased competition; (iv) increases in property taxes and operating expenses; (v) changes in zoning laws; (vi) casualty and condemnation losses; (vii) variations in rental income, neighborhood values or the appeal of property to tenants; (viii) the availability of financing; and (ix) changes in interest rates and leverage.

REIT Risk – REIT share prices may decline because of adverse developments affecting the real estate industry and real property values. In general, real estate values can be affected by a variety of factors, including supply and demand for properties, the economic health of the country or of different regions, and the strength of specific industries that rent properties. Qualification as a REIT under the Code in any particular year is a complex analysis that depends on a number of factors. There can be no assurance that the entities in which the Fund invests with the

18

| AOG Institutional Fund |

| NOTES TO FINANCIAL STATEMENTS (Continued) |

| September 30, 2023 |

expectation that they will be taxed as a REIT will qualify as a REIT. An entity that fails to qualify as a REIT would be subject to a corporate level tax, would not be entitled to a deduction for dividends paid to its shareholders and would not pass through to its shareholders the character of income earned by the entity.

Restricted and Illiquid Investments Risk – The Fund’s investments are also subject to liquidity risk, possibly preventing the Fund from selling such illiquid securities at an advantageous time or price, or possibly requiring the Fund to dispose of other investments at unfavorable times or prices to satisfy its obligations. The Adviser may be unable to sell restricted and other illiquid securities at the most opportune times or at prices approximating the value at which they purchased such securities.

| 8. | CAPITAL SHARE TRANSACTIONS |

For the year ended September 30, 2023 capital share transactions were as follows:

| Shares | Dollars | |||||||

| Shares issued | 1,140,001 | $ | 17,392,000 | |||||

| Shares reinvested | 411 | 6,242 | ||||||

| Shares redeemed | (299,957 | ) | (4,616,345 | ) | ||||

| Net Capital Share Transactions | 840,455 | $ | 12,781,897 | |||||

| 9. | SUBSEQUENT EVENTS |

Subsequent events after the date of the Statement of Assets and Liabilities have been evaluated through the date the financial statements were issued. Management has determined that no events or transactions occurred requiring adjustment or disclosure in the financial statements.

19

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Shareholders and Board of Trustees of

AOG Institutional Fund

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of AOG Institutional Fund (formerly AOG Institutional Diversified Fund) (the “Fund”) as of September 30, 2023, the related statements of operations, changes in net assets and cash flows, and the financial highlights for the year then ended, and the related notes, (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of September 30, 2023, the results of its operations, changes in net assets, its cash flows and the financial highlights for the year then ended, in conformity with accounting principles generally accepted in the United States of America.

The Fund’s financial statements and financial highlights for the period ended September 30, 2022, were audited by other auditors whose report dated November 29, 2022, expressed an unqualified opinion on those financial statements and financial highlights.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audit. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audit in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement whether due to error or fraud.

Our audit included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of September 30, 2023, by correspondence with the custodian or by other auditing procedures as appropriate in the circumstances. Our audit also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audit provides a reasonable basis for our opinion.

We have served as the Fund’s auditor since 2023.

COHEN & COMPANY, LTD.

Philadelphia, Pennsylvania

December 5, 2023

COHEN & COMPANY, LTD.

800.229.1099 | 866.818.4538 fax | cohencpa.com

Registered with the Public Company Accounting Oversight Board

20

| AOG Institutional Fund |

| SUPPLEMENTAL INFORMATION (Unaudited) |

| September 30, 2023 |

Change in Independent Registered Public Accounting Firm

Effective March 6, 2023, BBD LLP (“BBD”) ceased to serve as the independent registered public accounting firm for the Funds. The Audit Committee of the Board of Trustees approved the replacement of BBD as a result of Cohen & Company, Ltd.’s (“Cohen”) acquisition of BBD’s investment management group. On May 27, 2023, the Audit Committee of the Board of Trustees also recommended and approved the appointment of Cohen as the Funds’ independent registered public accounting firm for the fiscal year ending September 30, 2023.

The reports of BBD, LLP on the Funds’ financial statements for the last fiscal year contained no adverse opinion or disclaimer of opinion and were not qualified or modified as to uncertainty, audit scope, or accounting principles. During the Funds’ most recent fiscal year, and through May 27, 2023, there were no disagreements with BBD, LLP on any matter of accounting principles or practices, financial statement disclosure, or auditing scope or procedure, which disagreements, if not resolved to the satisfaction of BBD, LLP, would have caused them to make reference to the subject matter of the disagreements in connection with their reports on the Funds’ financial statements for such years. During the most recent fiscal year, and through May 27, 2023, there were no reportable events as defined in Item 304(a)(1)(v) of Regulation S-K promulgated by the SEC.

The Funds requested BBD, LLP to furnish them with a letter addressed to the SEC stating whether or not it agrees with the above statements. A copy of such letter will be filed as an Exhibit to the Form N-CSR filing.

21

| AOG Institutional Fund |

| SUPPLEMENTAL INFORMATION (Unaudited) (Continued) |

| September 30, 2023 |

Board Considerations - Approval of New Advisory Agreement

The Board previously approved the Advisory Agreement on July 6, 2022, which increased the management fee from 0.50% to 1.49% (the “Existing Advisory Agreement”). On September 20, 2022, the Fund commenced solicitation of, and on October 14, 2022 received, the vote of the outstanding voting securities of the Fund needed to approve the Existing Advisory Agreement, and on or about November 16¸2022, the Fund entered into the Existing Advisory Agreement with the Adviser. On April 17, 2023, the Board approved the new Advisory Agreement (the “New Advisory Agreement”). On May 12, 2023, the Fund commenced solicitation of, and on June 2, 2023, received, the vote of the outstanding voting securities of the Fund needed to approve the New Advisory Agreement. Furthermore, on August 25, 2023, the Fund entered into the New Advisory Agreement with the Adviser. Other than the change of the payor of the management fee from the Master Fund to the Fund, and the removal of the Tender Fund as a party, the terms of the Existing Advisory Agreement and the New Advisory Agreement are substantially similar. In considering the approval and recommendation to the shareholders of the Fund of the New Advisory Agreement, the Board reconsidered those factors previously reviewed by it at the July 6 meeting, and the substantially similar terms of the Existing Advisory Agreement and the New Advisory Agreement.

The Board, half of which is comprised solely of trustees who are not “interested persons” (as defined under the Investment Company Act) of the Fund (“Independent Trustees”), reviewed the New Advisory Agreement at the special meeting held on April 17, 2023. In determining whether to approve the New Advisory Agreement, the Board evaluated information relevant to its consideration of the New Advisory Agreement at this meeting. The Board also considered its regular discussions with management regarding the viability and performance challenges of the Fund.

In considering the New Advisory Agreement, the Board reviewed and analyzed various factors with respect to the Fund that it determined were relevant, including the factors below, and made the following conclusions. In their deliberations, the Board did not identify any single factor as determinative but considered all factors together.

In addition to the specific factors considered by the Board below, the Board also considered broader factors, such as the responsibility, attention, and diligence the Adviser would need to devote to the Fund, the fees charged by comparable funds, and ensuring that the management fee was competitive to attract portfolio management talent and expand the personnel needed to support a fund whose investor base extended beyond the Advisor’s existing clients. In addition, the Board considered the superior performance of the Fund relative to its peers, the long-term strategic direction for the Fund, and the administrative and operational demands of operating a fund utilizing the Fund’s unique liquidity feature supplied by Nasdaq Fund Secondaries LLC, in its evaluation of the management fee.

Nature and Quality of Services Provided to the Fund

The Board analyzed the nature, extent and quality of the services provided by the Adviser to the Fund, noting that the Adviser has served as the Fund’s investment adviser since its inception in 2021. The Board concluded that the nature and quality of the services provided by the Adviser to the Fund was appropriate and that the Fund was likely to continue to benefit from services provided under the New Advisory Agreement.

Scope and Costs of Services Provided

As part of its review at the meeting, the Board considered the fees realized, and the costs incurred, by the Adviser in providing investment advisory services to the Fund and the profitability to the Adviser of having a relationship with the Fund, as well as the projected profitability information provided. The Board noted the fee waivers and unreimbursed expenses for the Fund since inception. At the meeting, the Board considered the financial information and condition of the Adviser and determined it to be sound. In light of all of the information that it received and considered; the Board concluded that the management fee was reasonable.

Economies of Scale and Fee Levels Reflecting Those Economies

The Board compared the Fund’s proposed fees under the New Advisory Agreement to the comparative data provided and discussed potential economies of scale. The Board noted that the Fund’s proposed advisory fee structure under

22

| AOG Institutional Fund |

| SUPPLEMENTAL INFORMATION (Unaudited) (Continued) |

| September 30, 2023 |

the New Advisory Agreement does not contain any breakpoint reductions as the Fund grows in size. However, the Board noted that the Adviser had committed to review the possibility of incorporating breakpoints in the future should assets grow significantly. The Board concluded that the proposed fee structure under the New Advisory Agreement was reasonable given the Fund’s current and projected asset size under the New Advisory Agreement.

Benefits Derived from the Relationship with the Fund

The Board noted that the Adviser currently derives ancillary benefits from its association with the Fund in the form of research products and services received from unaffiliated broker-dealers who execute portfolio trades for the Fund. The Board determined such products and services have been used for legitimate purposes relating to the Fund by providing assistance in the investment decision-making space.

In addition to the above factors, the Board also discussed certain considerations adverse to the proposal, including: the time and expense associated with conducting a proxy solicitation among investors for the various proposals; the uncertainty of obtaining the requisite vote to approve the proposals; the confusion the proposals might cause investors following the 2022 proposal to amend and restate the investment management agreement; the uncertainty regarding the outcome of the proposals and the impact on the Fund’s capital raising efforts; the attention and time that the proposals would require from the personnel of the Adviser which would potentially distract from investment management duties; and the competition among interval funds if the proposals were adopted and the Fund began to compete with other interval funds.

Based on its evaluation of the above factors, as well as other factors relevant to their consideration of the New Advisory Agreement, the trustees, all of whom are Independent Trustees, concluded that the approval of the New Advisory Agreement was in the best interest of the Fund and its shareholders.

23

| AOG Institutional Fund |

| SUPPLEMENTAL INFORMATION (Unaudited) (Continued) |

| September 30, 2023 |

Trustees and Officers of the Fund. Set forth below are the names, years of birth, position with the Fund and length of time served, and the principal occupations and other directorships held during at least the last five years of each of the persons currently serving as a Trustee or officer of the Fund. There is no stated term of office for the Trustees and officers of the Fund. Nevertheless, an independent Trustee must retire from the Board as of the end of the calendar year in which such independent Trustee first attains the age of seventy-five years; provided, however, that, an independent Trustee may continue to serve for one or more additional one calendar year terms after attaining the age of seventy-five years (each calendar year a “Waiver Term”) if, and only if, prior to the beginning of such Waiver Term: (1) the Nominating Committee (a) meets to review the performance of the independent Trustee; (b) finds that the continued service of such independent Trustee is in the best interests of the Fund; and (c) unanimously approves excepting the independent Trustee from the general retirement policy set out above; and (2) a majority of the Trustees approves excepting the independent Trustee from the general retirement policy set forth above. Unless otherwise noted, the business address of each Trustee or officer is, as applicable, AOG Institutional Fund, 11911 Freedom Drive, Suite 730, Reston, VA 20190.

Trustees

| Name and Year of Birth | Position with Fund and Length of Time Served | Principal Occupations in the Past 5 Years | Other Directorships Held in the Past 5 Years |

| Interested Trustees | |||

| Frederick Baerenz (1961) | President and Chief Executive Officer; Indefinite; Since Inception | President and Chief Executive Officer of AOG Wealth Management since 2000. | None |

| Michelle Whitlock (1990) | Indefinite; Since Inception | Chief Financial Officer of AOG Wealth Management since 2019; Director of Client Services, 2014 – 2019 | None |

| Name and Year of Birth | Position with Fund and Length of Time Served | Principal Occupations in the Past 5 Years | Other Directorships Held in the Past 5 Years |

| Independent Trustees | |||

| John Grady (1961) | Trustee; Indefinite; Since Inception | Attorney/Partner at DLA Piper LLP, 2016 – 2019; Practus LLP, 2019 – January 2021. Chief Compliance Officer of ABR Dynamic Funds, January 2021 – Present. | None |

| Maureen E. O’Toole (1957) | Trustee; Indefinite; Since June 2023 | Managing Director at Actis since 2019 and Morgan Stanley Investment Management since 2016. | None |

| Betsy Cochrane (1978) | Trustee; Indefinite; Since June 2023 | Executive Vice President, Senior Counsel at Greenbacker Capital Management, LLC, 2021- 2023; Member, US Commodity Futures Trading Commission Global Markets Advisory Committee’s Sub-Committee on Margin Requirements for Uncleared Swaps, 2020- 2022; Assistant General Counsel, Director, Barings LLC, 2012-2020. | None |

24

| AOG Institutional Fund |

| SUPPLEMENTAL INFORMATION (Unaudited) (Continued) |

| September 30, 2023 |

Officers

| Name and Year of Birth | Position with Fund and Length of Time Served | Principal Occupations in Past 5 Years |

| Frederick Baerenz (1961) | President and Chief Executive Officer; Indefinite; Since Inception | President and Chief Executive Officer of AOG Wealth Management since 2000. |

| Peter Sattelmair (1977) | Chief Financial Officer and Treasurer; Indefinite; Since May 2023 | Director, PINE Advisor Solutions (2021 – present); Director of Fund Operations and Assistant Treasurer, Transamerica Asset Management (2014 – 2021). |

| Jesse Hallee (1976) | Secretary; Indefinite; Since Inception | Senior Vice President and Associate General Counsel; Ultimus Fund Solutions, LLC, 2022-Present; Vice President and Senior Managing Counsel, Ultimus Fund Solutions, LLC, 2019 – 2022; Vice President and Managing Counsel, State Street Bank and Trust Company, 2013 – 2019. |

| Alexander Woodcock (1989) | Chief Compliance Officer; Indefinite; Since 2022 | Director of PINE Advisor Solutions since 2022; CEO and CCO of PINE Distributors LLC since 2022; Adviser Chief Compliance Officer of Destiny Advisors LLC since 2022; Fund Chief Compliance Officer of THOR Financial Technologies Trust since 2022; Vice President of Compliance Services, SS&C ALPS from 2019 to 2022; Manager of Global Operations Oversight, Oppenheimer Funds from 2014 to 2019. |

The Fund’s Statement of Additional Information (“SAI”) includes additional information about the Trustees and is available free of charge, upon request, by calling toll-free at 1-703-757-8020.

25

| AOG Institutional Fund |

| SUPPLEMENTAL INFORMATION (Unaudited) (Continued) |

| September 30, 2023 |

Shareholder Meeting