Hartford Schroders Private Opportunities Fund

Filed: 10 Jun 24, 8:57am

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number: 811-23776

HARTFORD SCHRODERS PRIVATE OPPORTUNITIES FUND

(Exact name of registrant as specified in charter)

690 Lee Road, Wayne, Pennsylvania 19087

(Address of Principal Executive Offices) (Zip Code)

Thomas R. Phillips, Esquire

Hartford Funds Management Company, LLC

690 Lee Road

Wayne, Pennsylvania 19087

(Name and Address of Agent for Service)

Copy to:

John V. O’Hanlon, Esquire

Dechert LLP

One International Place, 40th Floor

100 Oliver Street

Boston, Massachusetts 02110-2605

Registrant’s telephone number, including area code: (610) 386-4068

Date of fiscal year end: March 31

Date of reporting period: March 31, 2024

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

(a)

|

| 1 | S&P 500 Index is a market capitalization-weighted price index composed of 500 widely held common stocks. Indices are unmanaged and not available for direct investment. Past performance does not guarantee future results. |

| 2 | The Consumer Price Index is defined by the Bureau of Labor Statistics as a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services. |

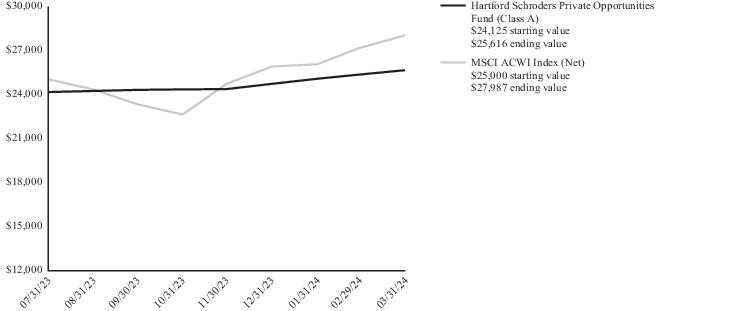

| Inception 07/31/2023 Sub-advised by Schroder Investment Management North America Inc. and its sub-sub-adviser, Schroders Capital Management (US), Inc. | Investment objective – The Fund seeks to provide long-term capital appreciation. |

| Cumulative Total Returns | |

| for the Period Ended 03/31/2024 | |

| Since Inception1 | |

| Class A2 | 6.18% |

| Class A3 | 2.47% |

| Class I2 | 6.20% |

| Class SDR2 | 6.20% |

| MSCI ACWI Index (Net) | 11.95% |

| 1 | Inception: 07/31/2023 |

| 2 | Without sales charge |

| 3 | Reflects maximum sales charge of 3.50% |

| Operating Expenses* | Gross | Net |

| Class A | 4.99% | 2.26% |

| Class I | 4.39% | 1.66% |

| Class SDR | 4.14% | 1.41% |

| * | Expenses as shown in the Fund’s most recent prospectus. Gross expenses do not reflect contractual fee waivers or expense reimbursement arrangements. Net expenses reflect such arrangements in instances when they reduce gross expenses. These arrangements remain in effect until 09/30/2024 unless the Fund’s Board of Trustees approves an earlier termination. Expenses shown include acquired fund fees and expenses. Actual expenses may be higher or lower. Please see accompanying Financial Highlights for expense ratios for the period ended 03/31/2024. |

| 2 |

| 3 |

| Composition by Strategy | |

| as of 03/31/2024 | |

| Category | Percentage of Net Assets |

| Direct Investments | |

| Direct Equity | 19.7% |

| Secondary Direct Equity | 14.2 |

| Total | 33.9% |

| Other Assets & Liabilities | 66.1 |

| Total | 100.0% |

| 4 |

| MSCI ACWI Index (Net) (reflects reinvested dividends net of withholding taxes but reflects no deduction for fees, expenses or other taxes) is designed to capture large and mid cap securities across developed markets and emerging markets countries. |

| Additional Information Regarding MSCI Indices. Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI’s express written consent. |

| 5 |

| Investments †—33.9% | Investment Type | Acquisition Date | Cost | Fair Value | |||||

| Direct Investments—33.9% | |||||||||

| Direct Equity—19.7% | |||||||||

| Germany—4.4% | |||||||||

| Information Technology—4.4% | |||||||||

| Fremman 1 MM Co-investment 7 Rocket SCSp*(1)(2)(3)(4)(5) | Limited Partnership Interest | 02/13/2024 | $ 951,727 | $ 936,131 | |||||

| Luxembourg—4.8% | |||||||||

| Information Technology—4.8% | |||||||||

| Stirling Square Capital Partners Eagle Co-Investment SCSp*(2)(3)(4)(5) | Limited Partnership Interest | 11/13/2023 | 1,012,232 | 1,012,622 | |||||

| United States—10.5% | |||||||||

| Health Care—3.1% | |||||||||

| Resurgens II Co-Invest C LP*(2)(3)(4)(5) | Limited Partnership Interest | 11/15/2023 | 654,762 | 653,206 | |||||

| Utilities—7.4% | |||||||||

| Greenbelt Capital Partners Saber LP*(1)(2)(4)(5) | Limited Partnership Interest | 10/25/2023 | 1,250,000 | 1,576,587 | |||||

| 3,868,721 | 4,178,546 | ||||||||

| Secondary Direct Equity—14.2% | |||||||||

| Luxembourg—4.4% | |||||||||

| Health Care—4.4% | |||||||||

| Procemsa Build-Up SCSp*(1)(2)(3)(4)(5) | Limited Partnership Interest | 11/16/2023 | 702,997 | 939,994 | |||||

| United States—9.8% | |||||||||

| Industrials—9.8% | |||||||||

| VSC EV3 (Parallel) LP*(1)(2)(3)(4)(5) | Limited Partnership Interest | 12/19/2023 | 734,376 | 797,136 | |||||

| TRP Continuation Fund (Genox) LP*(1)(2)(3)(4)(5) | Limited Partnership Interest | 02/22/2024 | 1,095,745 | 1,263,035 | |||||

| 2,533,118 | 3,000,165 | ||||||||

| Total Investments (Cost $6,401,839) | $ 7,178,711 | ||||||||

| Other Assets and Liabilities – 66.1% | 13,969,919 | ||||||||

| Total Net Assets – 100.0% | $ 21,148,630 | ||||||||

| * | Non-income producing. |

| (1) | Investment valued using significant unobservable inputs. |

| (2) | All or a portion of this security is held through Hartford Funds SPV, LLC, a wholly-owned subsidiary of the Fund (See Note 1). |

| (3) | Investment has been committed to but has not been fully funded by the Fund. |

| (4) | Investment does not allow redemptions or withdrawals except at discretion of its general partner, manager or advisor. |

| (5) | Restricted security. |

| 6 |

| Description | Total | Level 1 | Level 2 | Level 3 | ||||

| Assets | ||||||||

| Direct Investments | $ 5,512,883 | $ — | $ — | $ 5,512,883 | ||||

| Total | $ 5,512,883 | $ — | $ — | $ 5,512,883 |

| Direct Investments | Total | |||||||

| Beginning balance | $ — | $ — | ||||||

| Purchases | 4,734,845 | 4,734,845 | ||||||

| Sales | — | — | ||||||

| Total realized gain/(loss) | — | — | ||||||

| Net change in unrealized appreciation/(depreciation) | 778,038 | 778,038 | ||||||

| Transfers into Level 3 | — | — | ||||||

| Transfers out of Level 3 | — | — | ||||||

| Ending balance | $ 5,512,883 | $ 5,512,883 | ||||||

| The change in net unrealized appreciation/(depreciation) relating to the Level 3 investments held at March 31, 2024 was $778,038. | ||||||||

| 7 |

| Other Abbreviations: | |

| SCSp | Société en Commandite Cpéciale |

| 8 |

| Assets: | |

| Investments in securities, at market value | $ 7,178,711 |

| Cash | 14,269,021 |

| Foreign currency | 75 |

| Other assets | 18,085 |

| Total assets | 21,465,892 |

| Liabilities: | |

| Payables: | |

| To affiliates (("Investment Manager") see Note 6) | 13,898 |

| Investment management fees | 4,446 |

| Transfer agent fees | 13,044 |

| Accounting services fees | 48,083 |

| Board of Trustees' fees | 20,155 |

| Audit and tax fees | 128,171 |

| Pricing fees | 56,700 |

| Legal fees | 31,080 |

| Accrued expenses | 1,685 |

| Total liabilities | 317,262 |

| Commitments and contingencies (see Note 10) | |

| Net assets | $ 21,148,630 |

| Summary of Net Assets: | |

| Capital stock and paid-in-capital | $ 20,250,000 |

| Distributable earnings (loss) | 898,630 |

| Net assets | 21,148,630 |

| Class A: Net asset value per share | $ 10.52 |

| Shares outstanding | 100,963 |

| Net Assets | $ 1,061,819 |

| Class I: Net asset value per share | $ 10.49 |

| Shares outstanding | 101,253 |

| Net Assets | $ 1,061,983 |

| Class SDR: Net asset value per share | $ 10.49 |

| Shares outstanding | 1,813,894 |

| Net Assets | $ 19,024,828 |

| Cost of investments | $ 6,401,839 |

| Cost of foreign currency | $ 75 |

| 9 |

| Investment Income: | |

| Interest | $ 487,878 |

| Total investment income, net | 487,878 |

| Expenses: | |

| Investment management fees | 163,156 |

| Transfer agent fees | |

| Class A | 4,048 |

| Class I | 4,050 |

| Class SDR | 44,181 |

| Distribution fees | |

| Class A | 4,755 |

| Custodian fees | 750 |

| Registration and filing fees | 36,532 |

| Accounting services fees | 129,833 |

| Board of Trustees' fees | 53,669 |

| Chief Compliance Officer fees | 7 |

| Audit and tax fees | 132,750 |

| Legal fees | 59,093 |

| Pricing fees | 56,700 |

| Other expenses | 5,932 |

| Total expenses (before waivers and reimbursements) | 695,456 |

| Expense reimbursements | (445,967) |

| Investment management fee waivers | (135,963) |

| Distribution fee reimbursements | (4,755) |

| Total waivers and reimbursements | (586,685) |

| Total expenses | 108,771 |

| Net Investment Income (Loss) | 379,107 |

| Net Realized Gain (Loss) on Foreign Currency Transactions on: | |

| Other foreign currency transactions | (7,349) |

| Net Realized Gain (Loss) on Foreign Currency Transactions | (7,349) |

| Net Changes in Unrealized Appreciation (Depreciation) of: | |

| Investments | 776,872 |

| Net Changes in Unrealized Appreciation (Depreciation) | 776,872 |

| Net Gain (Loss) on Investments and Foreign Currency Transactions | 769,523 |

| Net Increase (Decrease) in Net Assets Resulting from Operations | $ 1,148,630 |

| 10 |

| For the Period Ended March 31, 2024(1) | |

| Operations: | |

| Net investment income (loss) | $ 379,107 |

| Net realized gain (loss) on foreign currency transactions | (7,349) |

| Net changes in unrealized appreciation (depreciation) of investments | 776,872 |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 1,148,630 |

| Distributions to Shareholders: | |

| Class A | (9,760) |

| Class I | (12,701) |

| Class SDR | (227,539) |

| Total distributions | (250,000) |

| Capital Share Transactions: | |

| Sold | 20,000,000 |

| Issued on reinvestment of distributions | 250,000 |

| Net increase (decrease) from capital share transactions | 20,250,000 |

| Net Increase (Decrease) in Net Assets | 21,148,630 |

| Net Assets: | |

| Beginning of period | — |

| End of period | $ 21,148,630 |

| (1) | Commenced operations on July 31, 2023. |

| 11 |

| Increase (decrease) in cash | |

| Cash flows from operating activities | |

| Net increase in net assets resulting from operations | $ 1,148,630 |

| Adjustments to reconcile net increase in net assets resulting from operations to net cash used for operating activities: | |

| Purchases of investment securities | $ (6,401,839) |

| Increase in other assets | (18,085) |

| Increase in investment management fees payables | 4,446 |

| Increase in accounting services fees payables | 48,083 |

| Increase in payable to affiliates ("Investment Manager") | 13,898 |

| Increase in transfer agent fees payable | 13,044 |

| Increase in Board of Trustees' fees payables | 20,155 |

| Increase in audit and tax fees payable | 128,171 |

| Increase in pricing fees payable | 56,700 |

| Increase in legal fees payable | 31,080 |

| Increase in accrued expenses | 1,685 |

| Net change in unrealized appreciation (depreciation) of investments in securities | (776,872) |

| Net Cash used for operating activities | $ (5,730,904) |

| Cash flows from financing activities | |

| Proceeds from shares sold | $ 20,000,000 |

| Net cash provided by financing activities | $ 20,000,000 |

| Net increase in cash and foreign currency | $ 14,269,096 |

| Cash and foreign currency, beginning of period | $ — |

| Cash and foreign currency, end of period | $ 14,269,096 |

| Supplemental disclosure of cash flow information: | |

| Reinvestment of dividends | $ 250,000 |

| (1) Commenced operations on July 31, 2023. |

| 12 |

| — Selected Per-Share Data(1) — | — Ratios and Supplemental Data — | |||||||||||||||||||||||||||

| Class | Net Asset Value at Beginning of Period | Net Investment Income (Loss) | Net Realized and Unrealized Gain (Loss) on Investments | Total from Investment Operations | Dividends from Net Investment Income | Distributions from Capital Gains | Total Dividends and Distributions | Net Asset Value at End of Period | Total Return(2) | Net Assets at End of Period (000s) | Ratio of Expenses to Average Net Assets Before Adjust- ments(3) | Ratio of Expenses to Average Net Assets After Adjust- ments(3) | Ratio of Net Investment Income (Loss) to Average Net Assets | Portfolio Turnover | ||||||||||||||

| Hartford Schroders Private Opportunities Fund(4) | ||||||||||||||||||||||||||||

| For the Period Ended March 31, 2024 | ||||||||||||||||||||||||||||

| A | $ 10.00 | $ 0.27 | $ 0.35 | $ 0.62 | $ (0.10) | $ — | $ (0.10) | $ 10.52 | 6.18% (5) | $ 1,062 | 7.67% (6) | 1.00% (6) | 3.59% (6) | 0.00% (7) | ||||||||||||||

| I | 10.00 | 0.27 | 0.35 | 0.62 | (0.13) | — | (0.13) | 10.49 | 6.20 (5) | 1,062 | 6.98 (6) | 1.00 (6) | 3.59 (6) | 0.00 (7) | ||||||||||||||

| SDR | 10.00 | 0.26 | 0.36 | 0.62 | (0.13) | — | (0.13) | 10.49 | 6.20 (5) | 19,025 | 6.26 (6) | 1.00 (6) | 3.45 (6) | 0.00 (7) | ||||||||||||||

| FINANCIAL HIGHLIGHTS FOOTNOTES | |

| (1) | Information presented relates to a share outstanding throughout the indicated period. Net investment income (loss) per share amounts are calculated based on average shares outstanding unless otherwise noted. |

| (2) | Total return is calculated assuming a hypothetical purchase of beneficial shares on the opening of the first day at the net asset value and a sale on the closing of the last day at the net asset value of each period reported. Dividends and distributions, if any, are assumed for purposes of this calculation, to be reinvested at net asset value at the end of the distribution day. |

| (3) | Adjustments include waivers and reimbursements, if applicable. (see Expenses in the accompanying Notes to Financial Statements). |

| (4) | Commenced operations on July 31, 2023. |

| (5) | Not annualized. |

| (6) | Annualized. Ratios do not reflect the proportionate share of income and expenses of the underlying Investment Funds. |

| (7) | Reflects the Fund's portfolio turnover for the period July 31, 2023 through March 31, 2024. |

| 13 |

| 1. | Organization: |

| Hartford Schroders Private Opportunities Fund (the "Fund") is organized as a Delaware statutory trust that is registered under the Investment Company Act of 1940, as amended (the "1940 Act"). The Fund operates as a closed-end, tender offer fund pursuant to which it may conduct quarterly tender offers for the repurchase of the Fund’s outstanding common shares of beneficial interest at net asset value. The investment objective of the Fund is to seek to provide long-term capital appreciation. The Fund commenced operations on July 31, 2023. | |

| The Fund offers three separate classes of shares: Class A, Class I and Class SDR. Class A Shares, Class I Shares and Class SDR Shares are subject to different fees and expenses. The Fund's prospectus provides description of each share class expenses, sales charges and minimum investments. | |

| The Fund may invest in the shares of one or more wholly owned and controlled Subsidiaries (each, a “Subsidiary”). Investments in a Subsidiary are expected to provide the Fund with exposure to investments within the limitations of Subchapter M of the Internal Revenue Code of 1986, as amended (the "Code"). Each Subsidiary is managed pursuant to compliance policies and procedures that are the same, in all material respects, as the policies and procedures adopted by the Fund. However, unlike the Fund, a Subsidiary is not subject to diversification requirements. The Fund is the sole shareholder of each Subsidiary, and shares of a Subsidiary are not sold or offered to other investors. | |

| As of March 31, 2024, there is one active Subsidiary: the Hartford Funds SPV, LLC, registered in Delaware on December 16, 2022. The Schedule of Investments (Consolidated), Statement of Assets and Liabilities (Consolidated), Statement of Operations (Consolidated), Statements of Changes in Net Assets (Consolidated), Statement of Cash Flows (Consolidated) and Financial Highlights (Consolidated) of the Fund include the accounts of the Subsidiary. All inter-company accounts and transactions have been eliminated in the consolidation for the Fund. As of March 31, 2024, total assets of the Fund were $21,465,892, of which $7,178,711 or 33.4% was held in the Hartford Funds SPV, LLC. | |

| The Fund is a non-diversified, closed-end management investment company and applies the specialized accounting and reporting under Accounting Standards Codification ("ASC") Topic 946, “Financial Services – Investment Company.” |

| 2. | Significant Accounting Policies: |

| The following is a summary of significant accounting policies of the Fund used in the preparation of its financial statements, which are in accordance with United States Generally Accepted Accounting Principles ("U.S. GAAP"). The preparation of financial statements in accordance with U.S. GAAP may require management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates. |

| a) | Determination of Net Asset Value – The Net Asset Value (“NAV”) per share is determined for each class of the Fund’s shares as of the close of business on the last business day of each calendar month, each date that a Share is offered, as of the date of any distribution and at such other times as the Board shall determine (each, a “Determination Date”). If the New York Stock Exchange (the “Exchange”) is closed due to weather or other extraordinary circumstances on a day it would typically be open for business, the Fund may treat such day as a typical business day and accept purchase and repurchase requests and calculate the Fund’s NAV in accordance with applicable law. In determining its net asset value, the Fund will value its investments as of the relevant Determination Date. The net asset value for each class of shares is determined by dividing the value of the Fund’s net assets attributable to a class of shares by the number of shares outstanding for that class. Information that becomes known to the Fund after the NAV has been calculated on a particular day will not generally be used to retroactively adjust the NAV determined earlier that day. |

| b) | Investment Valuation and Fair Value Measurements – For purposes of calculating the NAV, the Fund will value its investments in Direct Investments, Secondary Investments and Primary Investments (collectively "Investment Funds") at fair value as determined in good faith under the Valuation Procedures (the "Valuation Procedures"). The fair value of such investments as of each Determination Date ordinarily will be the capital account value of the Fund’s interest in such investments as provided by the relevant general partner, managing member or affiliated investment adviser of the Investment Fund (the "Investment Manager") as of or prior to the relevant Determination Date; provided that such values will be adjusted for any other relevant information available at the time the Fund values its portfolio, including capital activity and material events occurring between the reference dates of the Investment Manager’s valuations and the relevant Determination Date. |

| Certain Investment Funds are valued based on the latest NAV reported by the Investment Manager. This is commonly referred to as using NAV as a practical expedient which allows for estimation of the fair value of a private investment based on NAV or its equivalent if the NAV of the private fund is calculated in a manner consistent with ASC 946. |

| 14 |

| The Fund is designed to invest primarily in private equity investments of various types for which market quotations are not expected to be readily available. With respect to such investments, the Trust's Board of Trustees (the "Board") has designated Hartford Funds Management Company, LLC (the "Investment Manager" or "HFMC") as its valuation designee to determine the fair valuations of such investments pursuant to Rule 2a-5 under the 1940 Act (the "Valuation Designee"). The Valuation Designee determines the fair value of the security or other instrument under policies and procedures established by and under the supervision of the Board of Trustees of the Fund. The Valuation Designee has delegated the day-to-day responsibility for implementing the Valuation Procedures to the Valuation Committee (the "Valuation Committee"). The Valuation Committee will consider all available relevant factors in determining an investment’s fair value. The Valuation Designee reports fair value matters to the Audit Committee of the Fund’s Board of Trustees. The fair value of the Fund’s investments in Investment Funds, determined by the Valuation Committee in accordance with the Valuation Procedures, are estimates. Ordinarily, the fair value of an Investment Fund is based on the net asset value of the Investment Fund reported by its Investment Manager. If the Valuation Committee determines that the most recent net asset value reported by the Investment Manager of the Investment Fund does not represent fair value or if the Investment Manager of the Investment Fund fails to report a net asset value to the Fund, a fair value determination is made by the Valuation Committee in accordance with the Valuation Procedures. In making that determination, the Valuation Committee will consider whether it is appropriate, in light of all relevant circumstances, to value such Investment Fund at the net asset value last reported by its Investment Manager, or whether to adjust such net asset value to reflect a premium or discount (adjusted net asset value). The Valuation Committee uses a variety of methods such as earnings and multiple analysis, discounted cash flow analysis and market data from third party pricing services. The Valuation Committee makes assumptions that are based on market conditions existing at the determination date. | |

| In certain circumstances, the Valuation Committee may determine that cost best approximates the fair value of a particular Investment Fund. | |

| Prices of foreign equities that are principally traded on certain foreign markets will generally be adjusted monthly pursuant to a fair value pricing service in order to reflect an adjustment for the factors occurring after the close of certain foreign markets but before the NYSE Close. Securities and other instruments that are primarily traded on foreign markets may trade on days that are not business days of the Fund. The value of the foreign securities or other instruments in which the Fund invests may change on days when a shareholder will not be able to purchase or request the repurchase of shares of the Fund. | |

| Fixed income investments (other than short-term obligations) and non-exchange traded derivatives held by the Fund are normally valued at prices supplied by independent pricing services in accordance with the Valuation Procedures. Short-term investments maturing in 60 days or less are generally valued at amortized cost, which approximates fair value. | |

| Exchange-traded derivatives, such as options, futures and options on futures, are valued at the last sale price determined by the exchange where such instruments principally trade as of the close of such exchange ("Exchange Close"). If a last sale price is not available, the value will be the mean of the most recently quoted bid and ask prices as of the Exchange Close. If a mean of the bid and ask prices cannot be calculated for the day, the value will be the most recently quoted bid price as of the Exchange Close. Over-the-counter derivatives are normally valued based on prices supplied by independent pricing services in accordance with the Valuation Procedures. | |

| Investments valued in currencies other than U.S. dollars are converted to U.S. dollars using the prevailing spot currency exchange rates obtained from independent pricing services for calculation of the NAV. As a result, the NAV of the Fund’s shares may be affected by changes in the value of currencies in relation to the U.S. dollar. The value of securities or other instruments traded in markets outside the United States or denominated in currencies other than the U.S. dollar may be affected significantly on a day that the Exchange is closed and the market value may change on days when an investor is not able to purchase, or request the repurchase of shares of the Fund. | |

| Foreign currency contracts represent agreements to exchange currencies on specific future dates at predetermined rates. Foreign currency contracts are valued using foreign currency exchange rates and forward rates as provided by an independent pricing service on the Determination Date. | |

| Investments in open-end mutual funds are valued at the respective NAV of each open-end mutual fund on the Determination Date. Shares of investment companies listed and traded on an exchange are valued in the same manner as any exchange-listed equity security. Such open-end mutual funds and listed investment companies may use fair value pricing as disclosed in their prospectuses. | |

| Financial instruments for which prices are not available from an independent pricing service may be valued using quotations obtained from one or more dealers that make markets in the respective financial instrument in accordance with the Valuation Procedures. |

| 15 |

| U.S. GAAP defines fair value as the price that the Fund would receive to sell an asset or pay to transfer a liability in an orderly transaction between market participants. The U.S. GAAP fair value measurement standards require disclosure of a fair value hierarchy for each major category of assets and liabilities. Various inputs are used in determining the fair value of the Fund’s investments. These inputs are summarized into three broad hierarchy levels. This hierarchy is based on whether the valuation inputs are observable or unobservable. These levels are: |

| • | Level 1 – Quoted prices in active markets for identical investments. Level 1 may include exchange traded instruments, such as domestic equities, some foreign equities, options, futures, mutual funds, exchange traded funds, rights and warrants. |

| • | Level 2 – Observable inputs other than Level 1 prices, such as quoted prices for similar investments; quoted prices in markets that are not active; or other inputs that are observable or can be corroborated by observable market data. Level 2 may include debt investments that are traded less frequently than exchange traded instruments and which are valued using independent pricing services; foreign equities, which are principally traded on certain foreign markets and are adjusted monthly pursuant to a fair value pricing service in order to reflect an adjustment for the factors occurring after the close of certain foreign markets but before the NYSE Close; senior floating rate interests, which are valued using an aggregate of dealer bids; short-term investments, which are valued at amortized cost; and swaps, which are valued based upon the terms of each swap contract. |

| • | Level 3 – Significant unobservable inputs that are supported by limited or no market activity. Level 3 may include financial instruments whose values are determined using indicative market quotes or require significant management judgment or estimation. These unobservable valuation inputs may include estimates for current yields, maturity/duration, prepayment speed, and indicative market quotes for comparable investments along with other assumptions relating to credit quality, collateral value, complexity of the investment structure, general market conditions and liquidity. This category may include investments where trading has been halted or there are certain restrictions on trading. While these investments are priced using unobservable inputs, the valuation of these investments reflects the best available data and management believes the prices are a reasonable representation of exit price. |

| Asset Class | Valuation Technique | Unobservable Input(1) | Range of Input | Fair Value at March 31, 2024 | Weighted Average of Input (2) | Impact to Valuation from an Increase in Input(3) | ||||||

| Direct Investments | Market Comparable Companies | Enterprise value to EBITDA Multiple | 11.4x | $1,576,587 | N/A | Increase | ||||||

| Direct Investments | Recent Transaction | Recent Transaction Price | N/A | 936,131 | N/A | N/A | ||||||

| Secondary Investments | Market Comparable Companies | Enterprise value to EBITDA Multiple | 9.5x - 16.0x | 3,000,165 | 12.73x | Increase |

| c) | Investment Transactions and Investment Income – Investment transactions are recorded as of the trade date for financial reporting purposes. |

| The Fund’s primary sources of income are investment income and gains recognized upon distributions from portfolio investments and unrealized appreciation/depreciation in the fair value of its portfolio investments. The Fund generally recognizes investment income and realized gains/losses based on the characterization of distributions provided by the administrator/investment manager of the portfolio investment on the date notice is received. Distributions often occur at irregular intervals, and the exact timing of distributions from the portfolio investments may not be known until notice is received. It is estimated that distributions will occur over the life of the portfolio investments. |

| 16 |

| Realized gains and losses from the sale of portfolio investments represent the difference between the original cost of the portfolio investments, as adjusted for return of capital distributions (net cost), and the net proceeds received at the time of the sale, disposition or distribution date. The Fund records realized gains and losses on portfolio investments when securities are sold, distributed to the partners or written-off as worthless. The Fund recognizes the difference between the net cost and the estimated fair value of portfolio investments owned as the net change in unrealized appreciation/depreciation on investments in the Consolidated Statement of Operations. | |

| Return of capital distributions received from portfolio investments are accounted for as a reduction to cost. | |

| Interest income, including amortization of premium or discount using the effective interest method and interest on paid-in-kind instruments, is recorded on an accrual basis. Dividend income is recorded on the ex-dividend date or the date the Fund becomes aware of the dividend. | |

| Dividend income from domestic securities is accrued on the ex-dividend date. In general, dividend income from foreign securities is recorded on the ex-date; however, dividend notifications in certain foreign jurisdictions may not be available in a timely manner and as a result, the Fund will record the dividend as soon as the relevant details (i.e., rate per share, payment date, shareholders of record, etc.) are publicly available.Interest income, including amortization of premium, accretion of discounts and additional principal received in-kind in lieu of cash, is accrued on a daily basis. | |

| Idle cash and currency balances may be swept into overnight sweep accounts that earn interest, which are classified as interest income on the Consolidated Statement of Operations. |

| d) | Taxes – The Fund may be subject to taxes imposed on realized gains on securities of certain foreign countries in which the Fund invests. The Fund may also be subject to taxes withheld on foreign dividends and interest from securities in which the Fund invests. The amount of any foreign taxes withheld and foreign tax expense is included on the accompanying Consolidated Statement of Operations as a reduction to net investment income or net realized or unrealized gain (loss) on investments in these securities, if applicable. |

| e) | Foreign Currency Transactions – Assets and liabilities denominated in currencies other than U.S. dollars are translated into U.S. dollars at the exchange rates in effect on the Valuation Date. Purchases and sales of investments, income and expenses are translated into U.S. dollars at the exchange rates on the dates of such transactions. |

| The Fund does not isolate that portion of portfolio investment valuation resulting from fluctuations in the foreign currency exchange rates from the fluctuations arising from changes in the market prices of investments held. Exchange rate fluctuations are included with the net realized and unrealized gain or loss on investments in the accompanying financial statements. | |

| Net realized foreign exchange gains or losses arise from sales of foreign currencies and the difference between asset and liability amounts initially stated in foreign currencies and the U.S. dollar value of the amounts actually received or paid. Net unrealized foreign exchange gains or losses arise from changes in the value of other assets and liabilities at the end of the reporting period, resulting from changes in the exchange rates. |

| f) | Fund Share Valuation and Dividend Distributions to Shareholders – The Fund intends to distribute substantially all of its net investment income and capital gains to shareholders at least once a year. Dividends, if any, from net investment income of the Fund and capital gains of the Fund are normally declared and paid annually. Payments will vary in amount, depending on investment income received and expenses of operation. It is likely that many of the Investment Funds in whose securities the Fund invests will not pay any dividends, and this, together with the Fund’s relatively high expenses, means that there can be no assurance the Fund will have substantial income or pay dividends. The Fund is not a suitable investment for any investor who requires regular dividend income. |

| g) | Basis for Consolidation – The Fund may invest all of its assets in a wholly-owned subsidiary. All intercompany balances, revenues, and expenses have been eliminated in consolidation. The Subsidiary acts as an investment vehicle in order to enter into certain investments for the Fund consistent with the investment objectives and policies specified in the Prospectus and Statement of Additional Information. |

| 3. | Securities and Other Investments: |

| a) | Restricted Securities – The Fund may invest in securities that are subject to legal or contractual restrictions on resale. These securities generally may be resold in transactions exempt from registration or to the public if the securities are registered. Disposal of these securities may involve time-consuming negotiations and expense, and prompt sale at an acceptable price may be difficult. Information regarding restricted securities, if applicable, is included at the end of the Fund's Consolidated Schedule of Investments. |

| b) | Direct Investments – The Fund's Direct Investments will typically be in the form of co-investments, which involve the Fund acquiring an interest in a single operating company alongside an investment by a private equity firm or other entity and are generally structured such that the co-investors are passive. |

| 17 |

| c) | Secondary Investments– Secondary Investments ("secondaries") refer to investments in which one investor acquires another investor's existing interest in a private equity investment through a negotiated transaction in which the private equity manager managing the investment remains the same. In making Secondary Investments, the buyer acquires exposure to one or more existing assets of a private equity fund by either acquiring an interest in a fund created to hold the acquired assets or by acquiring the interests of an existing limited partner of the private equity fund and agreeing to take on future funding obligations in exchange for future returns and distributions. A Secondary Investment that involves acquiring an investor's interests in a private equity fund may be acquired at a discount to an Investment Fund's net asset value. As a result, Secondary Investments acquired at a discount may result in unrealized gains to the Fund at the time the Fund next calculates its monthly net asset value. Because Secondary Investments are generally made after an Investment Fund has deployed capital into portfolio companies, these investments are viewed as more mature and may not exhibit the initial decline in net asset value associated with Primary Investments and may reduce the impact of the J-curve associated with private equity primary fund investing. However, there can be no assurance that any or all Secondary Investments made by the Fund will exhibit this pattern of investment returns, and realization of later gains is dependent upon the performance of each Investment Fund’s portfolio companies. |

| The market for certain Secondary Investments may be very limited, and the strategies and Investment Funds to which the Fund wishes to allocate capital may not be available for Secondary Investment at any given time. Secondary Investments may be heavily negotiated and may incur additional transaction costs for the Fund. There is a risk that investors exiting an Investment Fund through a secondary transaction may possess superior knowledge regarding the value of their holdings and the portfolio companies of the Investment Fund and the Fund may pay more for a Secondary Investment than it would have if it were also privy to such information. |

| d) | Primary Investments– Primary Investments ("primaries") refer to interests in newly established Investment Funds. Primary Investments are made during the Investment Fund's fundraising period in the form of capital commitments, which are then periodically called by the fund to finance underlying investments in operating companies during a predefined period. A fund's capital account will typically exhibit a "J-curve," undergoing a modest decline in the early portion of its life cycle as expenses outweigh investment gains, with the trend typically reversing in the later portion of its life cycle as underlying investments mature and are eventually realized. There can be no assurance that any or all Primary Investments made by the Fund will exhibit this pattern of investment returns and the realization of investment gains is dependent upon the performance and disposition of each underlying investment. Primary Investments typically range in duration from ten to twelve years, while underlying investments generally range in duration from three to seven years. |

| Seasoned primaries are primary fund investments made after an Investment Fund has already invested a certain percentage of its capital commitments (e.g., 25%, at the time of closing). Since the Investment Fund contains investments at the time the Fund invests, the Fund is able to accelerate its capital deployment compared to a typical primary fund investment and the Sub-Advisers are able to assess the attractiveness of the investments in the Investment Fund before making a capital commitment thereby reducing the blind-pool risk associated with a typical primary fund investment that has not made any investments. | |

| Typically, private equity fund sponsors will not launch new funds that have the same focus more frequently than every two to four years. Private equity managers pursuing multiple strategies may offer multiple primary new funds each year, but may not offer new funds within a given geography or that pursue a certain strategy in any particular year. Many new funds offered by top-tier private equity firms may be inaccessible due to high demand and, accordingly, may be unavailable for Primary Investments at any given time. As a result, having well-established relationships with fund sponsors is critically important for primary investors. |

| 4. | Principal Risks: |

| 18 |

| 5. | Federal Income Taxes: |

| a) | The Fund intends to continue to qualify as a Regulated Investment Company ("RIC") under Subchapter M of the Internal Revenue Code ("IRC") by distributing substantially all of its taxable net investment income and net realized capital gains to its shareholders each year. The Fund has distributed substantially all of its income and capital gains in prior years, if applicable, and intends to distribute substantially all of its income and capital gains during the calendar year. Accordingly, no provision for federal income or excise taxes has been made in the accompanying financial statements. Distributions from short-term capital gains are treated as ordinary income distributions for federal income tax purposes. |

| b) | Net Investment Income (Loss), Net Realized Gains (Losses) and Distributions – Net investment income (loss) and net realized gains (losses) may differ from financial statements and tax purposes primarily because of adjustments related to certain derivatives and partnerships. The character of distributions made during the year from net investment income or net realized gain may differ from their ultimate characterization for federal income tax purposes. Also, due to the timing of the dividend distributions, the fiscal year in which amounts are distributed may differ from the year the income or realized gains (losses) were recorded by the Fund. |

| 19 |

| c) | Distributions and Components of Distributable Earnings - The Fund's tax year end is September 30 and the tax character of the current year distributions and current components of accumulated earnings (deficit) will be determined at the end of the current tax year. As of the Fund's tax year end September 30, 2023, the Fund did not make a distribution. |

| As of the Fund's tax year end of September 30, 2023, the components of total accumulated earnings (deficit) for the Fund on a tax basis are as follows: | |

| Undistributed Ordinary Income | Other Temporary Differences | Unrealized Appreciation (Depreciation) on Investments | Total Accumulated Earnings (Deficit) | |||

| $ 93,277 | $ (5,840) | $ — | $ 87,437 |

| d) | Capital Loss Carryforward – Under the Regulated Investment Company Modernization Act of 2010, funds are permitted to carry forward capital losses for an unlimited period of time. The Fund commenced operations after its fiscal year end, but before the Fund's tax year end of September 30, 2023. At September 30, 2023, the Fund had no capital loss carryover. |

| e) | Tax Basis of Investments – The aggregate cost of investments for federal income tax purposes at March 31, 2024 was substantially the same for book purposes. The net unrealized appreciation/(depreciation) on investments, which consists of gross unrealized appreciation and depreciation, is disclosed below: |

| Tax Cost | Gross Unrealized Appreciation | Gross Unrealized (Depreciation) | Net Unrealized Appreciation (Depreciation) | |||

| $ 6,401,839 | $ 794,024 | $ (17,152) | $ 776,872 |

| 6. | Expenses: |

| a) | Investment Management Agreement – HFMC serves as the Fund’s investment manager. The Fund has entered into an Investment Management Agreement with HFMC. HFMC is an indirect subsidiary of The Hartford Financial Services Group, Inc. ("The Hartford"). HFMC has overall investment supervisory responsibility for the Fund. In addition, HFMC provides administrative personnel, services, equipment, facilities and office space for proper operation of the Fund. HFMC has contracted with Schroder Investment Management North America Inc. ("SIMNA") under a sub-advisory agreement and SIMNA has contracted with Schroders Capital Management (US), Inc. (“Schroders Capital” and, collectively with SIMNA, the "Sub-Advisers") under a sub-sub-advisory agreement. The Fund pays a fee to HFMC. HFMC pays a sub-advisory fee to SIMNA out of its management fee. SIMNA pays the sub-sub-advisory fees to Schroders Capital. |

| The Fund pays a monthly management fee in arrears to HFMC at the annual rate of 1.50% of the average month end value of the Fund's net assets (a portion of which will be waived for the first twelve months following the Fund's commencement of operations). HFMC, not the Fund, pays the sub-advisory fees to SIMNA at the annual rate of 1.00% of the average month end value of the Fund’s net assets (a portion of which will be waived for the first twelve months following the Fund’s commencement of operations). SIMNA, not the Fund or HFMC, pays the sub-sub-advisory fees to Schroders Capital. The sub-sub-advisory fee paid by SIMNA to Schroders Capital is determined at the end of each month based on the internal Schroders Group Transfer Pricing Policy then in effect. HFMC has contractually agreed to waive the Fund’s management fee in the amount of 1.25% for the first twelve months following the Fund’s commencement of operations. For the period ended, March 31, 2024, the Fund has reimbursed the Investment Manager for operating expenses as reflected on the Consolidated Statement of Assets and Liabilities. |

| b) | Accounting Services Agreement – HFMC provides the Fund with accounting services pursuant to a fund accounting agreement by and between the Fund and HFMC. HFMC has delegated certain accounting and administrative service functions to State Street Bank and Trust Company ("State Street"). In consideration of services rendered and expenses assumed pursuant to the fund accounting agreement, the Fund pays HFMC a fee. The fund accounting fee for the Fund shall equal the sum of (i) the sub-accounting fee payable by HFMC with respect to the Fund; (ii) the fee payable for tax preparation services for the Fund; and (iii) the amount of expenses that HFMC allocates for providing the fund accounting services to the Fund; plus a target profit margin. |

| c) | Operating Expenses – Allocable expenses incurred by the Fund are allocated to each class within the Fund, in proportion of the average monthly net assets of the Fund and classes, except where allocation of certain expenses is more fairly made directly to the Fund or to specific classes within the Fund. Closing costs associated with the purchase of Direct Investments, Secondary Investments and Primary Investments are included in the cost of the investment. Professional fees relating to investments, including expenses of consultants, investment bankers, attorneys, accountants, and other experts is included in Legal Fees on the Consolidated Statement of Operations. As of March 31, 2024, HFMC has contractually agreed to reimburse expenses to limit total net operating expenses (excluding management fees, Rule 12b-1 distribution and service fees, sub-transfer agency fees payable by Hartford Administrative Services Company (“HASCO”) |

| 20 |

| to the extent that such sub-transfer agency fees are a component of the transfer agency fee payable by the Fund to HASCO, acquired fund fees and expenses, interest expenses, and certain extraordinary expenses) to no more than 0.75% of the Fund’s average monthly net assets. This contractual arrangement will remain in effect at least until September 30, 2024 unless the Fund’s Board of Trustees approves its earlier termination. | |

| d) | Sales Charges and Distribution and Service Plan for Class A Shares – Hartford Funds Distributors, LLC ("HFD"), an indirect subsidiary of The Hartford, is the principal underwriter and distributor of the Fund. The Distributor will also act as agent for the Fund in connection with repurchases of Shares. |

| For the period ended March 31, 2024, HFD did not receive sales charges for the Fund. | |

| The Board has approved the adoption by the Fund of a distribution plan (the "Plan") pursuant to Rule 12b-1 under the 1940 Act for Class A Shares. Under the Plan, Class A Shares of the Fund bear distribution and/or service fees paid to HFD, some of which may be paid to select broker-dealers. Total compensation under the Plan may not exceed the maximum cap imposed by FINRA with respect to asset-based sales charges. Distribution fees paid to HFD may be spent on any activities or expenses primarily intended to result in the sale of the Fund’s Shares. Under the Plan, the Fund pays HFD the entire fee, regardless of HFD's expenditures. Even if HFD's actual expenditures exceed the fee payable to HFD at any given time, the Fund will not be obligated to pay more than that fee. If HFD's actual expenditures are less than the fee payable to HFD at any given time, HFD may realize a profit from the arrangement. Pursuant to the Class A Plan, the Fund may pay HFD a fee of up to 0.70% of the average monthly net assets attributable to Class A Shares for distribution financing activities, and up to 0.25% may be used for shareholder account servicing activities. | |

| No market currently exists for the Fund's Shares. The Fund's Shares are not listed and the Fund does not currently intend to list its Shares for trading on any securities exchange, and the Fund does not anticipate that any secondary market will develop for its Shares. Neither HFMC nor HFD intends to make a market in the Fund's Shares. |

| e) | HASCO, an indirect subsidiary of The Hartford, provides transfer agent services to the Fund. The Fund pays HASCO a transfer agency fee payable monthly based on the costs of providing or overseeing transfer agency services provided to each share class of the Fund plus a target profit margin. Such fee is intended to compensate HASCO for: (i) fees payable by HASCO to UMB Fund Services, Inc. ("UMBFS") (and any other designated sub-agent) according to the agreed-upon fee schedule under the sub-transfer agency agreement between HASCO and UMBFS (or between HASCO and any other designated sub-agent, as applicable); (ii) sub-transfer agency fees payable by HASCO to financial intermediaries, according to the agreed-upon terms between HASCO and the financial intermediaries, provided that such payments are within certain limits approved by the Board of Trustees; (iii) certain expenses that HASCO’s parent company, Hartford Funds Management Group, Inc., allocates to HASCO that relate to HASCO’s transfer agency services provided to the Fund; and (iv) a target profit margin. |

| Pursuant to a sub-transfer agency agreement between HASCO and UMBFS, HASCO has delegated certain transfer agent, dividend disbursing agent and shareholder servicing agent functions to UMBFS. The Fund does not pay any fee directly to UMBFS; rather, HASCO makes all such payments to UMBFS. The accrued amount shown in the Statement of Operations reflects the amounts charged by HASCO. These fees are accrued and paid monthly. | |

| For the period ended March 31, 2024, the effective rate of compensation paid to HASCO for transfer agency services as a percentage of each Class average monthly net assets is as follows: | |

| Class A | Class I | Class SDR | ||

| 0.60% | 0.60% | 0.46% |

| 7. | Affiliate Holdings: |

| As of March 31, 2024, affiliates of The Hartford had ownership of shares in the Fund as follows: | |

| Percentage of a Class: | |||||

| Class A | Class I | Class SDR | |||

| 100% | 100% | 44% | |||

| 21 |

| 8. | Beneficial Fund Ownership: |

| As of March 31, 2024, to the knowledge of the Fund, the shareholders listed below beneficially held more than 25% of the shares outstanding of the Fund. | |

| Shareholder | Percentage of Ownership | |

| Schroder US Holdings, Inc | 50% | |

| Hartford Funds Management Company, LLC | 50% |

| 9. | Investment Transactions: |

| For the period ended March 31, 2024, the cost of purchases and proceeds from sales of investment securities (excluding short-term investments) were as follows: | |

| Cost of Purchases Excluding U.S. Government Obligations | Total Cost of Purchases | Total Sales Proceeds | ||

| $6,401,839 | $6,401,839 | $— |

| 10. | Commitments and Contingencies: |

| 11. | Capital Share Transactions: |

| The Fund offers 3 classes of shares, Class A, Class I, and Class SDR shares on a continuous basis at the NAV per shares. The minimum initial investment for Class A and Class I Shares of the Fund is $25,000, and the minimum subsequent investment for Class A and Class I Shares of the Fund is $10,000. The minimum initial investment for Class SDR Shares of the Fund is $5,000,000, while subsequent investments may be made in any amount. These minimums may be waived for certain investors. Class A Shares are subject to a sales charge of up to 3.50%. Class I Shares and Class SDR Shares of the Fund are not subject to sales charges. Under the Plan, the Fund may charge a distribution and service (12b-1) fee up to a rate of 0.70% of the NAV as of the end of each month of the Fund attributable to Class A shares. | |

| The Shares have no history of public trading, nor is it intended that the Shares will be listed on a public exchange. No secondary market is expected to develop for the Fund's Shares. To provide a limited degree of liquidity to shareholders, the Fund may from time to time offer to repurchase Shares pursuant to written tenders by shareholders. No shareholder has the right to require the Fund to redeem his, her or its Shares. | |

| Beginning no later than the fifth full calendar quarter following the date the Fund commences operations, HFMC intends to recommend to the Board (subject to its discretion) that the Fund offer to repurchase Shares from shareholders on a quarterly basis. Such repurchases are expected to be offered at the Fund’s net asset value per share as of March 31, June 30, September 30 and December 31 (each, a "Valuation Date"), as applicable. Each repurchase offer will generally commence approximately 75 days prior to the applicable Valuation Date and will remain open for a minimum of 20 business days following the commencement of the offer. It is also expected that HFMC will recommend to the Board, subject to the Board’s discretion, that any such tender offer would be for an amount that is not more than 5% of the Fund's net asset value. There can be no assurance that the Board will accept HFMC's recommendation. | |

| Any repurchase of Shares from a shareholder that were held for less than one year (on a first-in, first-out basis) will be subject to an "Early Repurchase Fee" equal to 2% of the net asset value of any Shares repurchased by the Fund that were held for less than one year. If an Early Repurchase Fee is charged to a shareholder, the amount of such fee will be retained by the Fund. | |

| The following information is for the period ended March 31, 2024: | |

| For the Period Ended March 31, 2024(1) | |||||

| Shares | Amount | ||||

| Class A | |||||

| Shares Sold | 100,000 | $ 1,000,000 | |||

| Shares Issued for Reinvested Dividends | 963 | 9,760 | |||

| Net Increase (Decrease) | 100,963 | 1,009,760 | |||

| 22 |

| For the Period Ended March 31, 2024(1) | |||||

| Shares | Amount | ||||

| Class I | |||||

| Shares Sold | 100,000 | $ 1,000,000 | |||

| Shares Issued for Reinvested Dividends | 1,253 | 12,701 | |||

| Net Increase (Decrease) | 101,253 | 1,012,701 | |||

| Class SDR | |||||

| Shares Sold | 1,791,444 | $ 18,000,000 | |||

| Shares Issued for Reinvested Dividends | 22,450 | 227,539 | |||

| Net Increase (Decrease) | 1,813,894 | 18,227,539 | |||

| Total Net Increase (Decrease) | 2,016,110 | $ 20,250,000 | |||

| (1) | Commenced operations on July 31, 2023. |

| 12. | Indemnifications: |

| Under the Fund’s organizational documents, the Fund shall indemnify its officers and trustees to the full extent required or permitted under applicable laws of the State of Delaware and federal securities laws. In addition, the Fund, may enter into contracts that contain a variety of indemnifications. The Fund’s maximum exposure under these arrangements is unknown. However, as of the date of these financial statements, the Fund has not had prior claims or losses pursuant to these contracts and expects the risk of loss to be remote. |

| 13. | Subsequent Events: |

| In connection with the preparation of the financial statements of the Fund as of and for the period ended March 31, 2024, events and transactions subsequent to March 31, 2024, through the date the financial statements were issued have been evaluated by the Fund's management for possible adjustment and/or disclosure. | |

| Subsequent to March 31, 2024, the Fund purchased 4 Investment Funds and provided $4,494,672 as capital contributions to its private equity investments. |

| 23 |

| 24 |

| NAME, YEAR OF BIRTH AND ADDRESS(1) | POSITION HELD WITH THE FUND | TERM OF OFFICE(2) AND LENGTH OF TIME SERVED | PRINCIPAL OCCUPATION(S) DURING PAST 5 YEARS | NUMBER OF PORTFOLIOS IN FUND COMPLEX(3) OVERSEEN BY TRUSTEE | OTHER DIRECTORSHIPS FOR PUBLIC COMPANIES AND OTHER REGISTERED INVESTMENT COMPANIES HELD BY TRUSTEE | |||||

| NON-INTERESTED TRUSTEES | ||||||||||

| HILARY E. ACKERMANN (1956) | Trustee | Since 2022 | Ms. Ackermann served as Chief Risk Officer at Goldman Sachs Bank USA from October 2008 to November 2011. | 84 | Ms. Ackermann served as a Director of Dynegy, Inc. from October 2012 until its acquisition by Vistra Energy Corporation (“Vistra”) in 2018, and since that time she has served as a Director of Vistra. Ms. Ackermann served as a Director of Credit Suisse Holdings (USA), Inc. from January 2017 to December 2022. | |||||

| ROBIN C. BEERY (1967) | Trustee | Since 2022 | Ms. Beery has served as a consultant to ArrowMark Partners (an alternative asset manager) since March of 2015 and since November 2018 has been employed by ArrowMark Partners as a Senior Advisor. Previously, she was Executive Vice President, Head of Distribution, for Janus Capital Group, and Chief Executive Officer and President of the Janus Mutual Funds (a global asset manager) from September 2009 to August 2014. | 84 | Ms. Beery serves as an independent Director of UMB Financial Corporation (January 2015 to present), has chaired the Compensation Committee since April 2017, and has been a member of the Compensation Committee and the Risk Committee since January 2015. | |||||

| DERRICK D. CEPHAS (1952) | Trustee | Since 2022 | Mr. Cephas currently serves as Of Counsel to Squire Patton Boggs LLP, an international law firm with 45 offices in 20 countries. Until his retirement in October 2020, Mr. Cephas was a Partner of Weil, Gotshal & Manges LLP, an international law firm headquartered in New York, where he served as the Head of the Financial Institutions Practice (April 2011 to October 2020). | 84 | Mr. Cephas currently serves as a Director of Claros Mortgage Trust, Inc., a real estate investment trust and is a member of the Compensation Committee and Nominating and Governance Committee. | |||||

| CHRISTINE R. DETRICK (1958) | Trustee and Chair of the Board | Since 2022 | From 2002 until 2012, Ms. Detrick was a Senior Partner, Leader of the Financial Services Practice, and a Senior Advisor at Bain & Company (“Bain”). Before joining Bain, she served in various senior management roles for other financial services firms and was a consultant at McKinsey and Company. | 84 | Ms. Detrick currently serves as a Director of Charles River Associates (May 2020 to present); currently serves as a Director of Capital One Financial Corporation (since November 2021); and currently serves as a Director and Chair of Altus Power, Inc. (since December 2021). | |||||

| 25 |

| NAME, YEAR OF BIRTH AND ADDRESS(1) | POSITION HELD WITH THE FUND | TERM OF OFFICE(2) AND LENGTH OF TIME SERVED | PRINCIPAL OCCUPATION(S) DURING PAST 5 YEARS | NUMBER OF PORTFOLIOS IN FUND COMPLEX(3) OVERSEEN BY TRUSTEE | OTHER DIRECTORSHIPS FOR PUBLIC COMPANIES AND OTHER REGISTERED INVESTMENT COMPANIES HELD BY TRUSTEE | |||||

| JOHN J. GAUTHIER (1961) | Trustee | Since 2022 | Mr. Gauthier currently is the Principal Owner of JJG Advisory, LLC, an investment consulting firm, and Co-Founder and Principal Owner of Talcott Capital Partners (a placement agent for investment managers serving insurance companies). From 2008 to 2018, Mr. Gauthier served as a Senior Vice President (2008-2010), Executive Vice President (2010-2012), and President (2012-2018) of Allied World Assurance, LTD, AG (a global provider of property, casualty and specialty insurance and reinsurance solutions). | 84 | Mr. Gauthier serves as a Director of Reinsurance Group of America, Inc. (from 2018 to present); currently serves as a Director of Hamilton Insurance Group, Ltd, (October 2023 to present); and chairs the Investment Committee and is a member of the Audit and Risk Committees. | |||||

| ANDREW A. JOHNSON (1962) | Trustee | Since 2022 | Mr. Johnson currently serves as a Diversity and Inclusion Advisor at Neuberger Berman, a private, global investment management firm. Prior to his current role, Mr. Johnson served as Chief Investment Officer and Head of Global Investment Grade Fixed Income at Neuberger Berman (January 2009 to December 2018). | 84 | Mr. Johnson currently serves as a Director of AGNC Investment Corp., a real estate investment trust. | |||||

| PAUL L. ROSENBERG (1953) | Trustee | Since 2022 | Mr. Rosenberg is a Partner of The Bridgespan Group, a global nonprofit consulting firm that is a social impact advisor to nonprofits, non-governmental organizations, philanthropists and institutional investors (October 2007 to present). | 84 | None | |||||

| DAVID SUNG (1953) | Trustee | Since 2022 | Mr. Sung was a Partner at Ernst & Young LLP from October 1995 to July 2014. | 84 | Mr. Sung serves as a Trustee of Ironwood Institutional Multi-Strategy Fund, LLC and Ironwood Multi-Strategy Fund, LLC (October 2015 to present). | |||||

| OFFICERS AND INTERESTED TRUSTEE | ||||||||||

| JAMES E. DAVEY(4) (1964) | Trustee, President and Chief Executive Officer | Trustee since 2022; President and Chief Executive Officer since 2022 | Mr. Davey serves as Executive Vice President of The Hartford Financial Services Group, Inc. Mr. Davey has served in various positions within The Hartford and its subsidiaries and joined The Hartford in 2002. Additionally, Mr. Davey serves as Director, Chairman, President, and Senior Managing Director for Hartford Funds Management Group, Inc. ("HFMG"). Mr. Davey also serves as President, Manager, Chairman of the Board, and Senior Managing Director for Hartford Funds Management Company, LLC (“HFMC”); Manager, Chairman of the Board, and President of Lattice Strategies LLC (“Lattice”); Chairman of the Board, Manager, and Senior Managing Director of Hartford Funds Distributors, LLC (“HFD”); and Chairman of the Board, President and Senior Managing Director of Hartford Administrative Services Company (“HASCO”), each of which is an affiliate of HFMG. | 84 | None | |||||

| AMY N. FURLONG (1979) | Vice President | Since 2022 | Ms. Furlong serves as Vice President and Assistant Treasurer of HFMC (since September 2019). From 2018 through March 15, 2021, Ms. Furlong served as the Treasurer of the Trust and resumed her position as Treasurer from January 9, 2023 through September 10, 2023. Ms. Furlong has served in various positions within The Hartford and its subsidiaries in connection with the operation of the Hartford Funds. Ms. Furlong joined The Hartford in 2004. | N/A | N/A | |||||

| 26 |

| NAME, YEAR OF BIRTH AND ADDRESS(1) | POSITION HELD WITH THE FUND | TERM OF OFFICE(2) AND LENGTH OF TIME SERVED | PRINCIPAL OCCUPATION(S) DURING PAST 5 YEARS | NUMBER OF PORTFOLIOS IN FUND COMPLEX(3) OVERSEEN BY TRUSTEE | OTHER DIRECTORSHIPS FOR PUBLIC COMPANIES AND OTHER REGISTERED INVESTMENT COMPANIES HELD BY TRUSTEE | |||||

| WALTER F. GARGER (1965) | Vice President and Chief Legal Officer | Since 2022 | Mr. Garger serves as Secretary, Managing Director and General Counsel of HFMG, HFMC, HFD, and HASCO (since 2013). Mr. Garger also serves as Secretary and General Counsel of Lattice (since July 2016). Mr. Garger has served in various positions within The Hartford and its subsidiaries in connection with the operation of the Hartford Funds. Mr. Garger joined The Hartford in 1995. | N/A | N/A | |||||

| THEODORE J. LUCAS (1966) | Vice President | Since 2022 | Mr. Lucas serves as Executive Vice President of HFMG (since July 2016) and as Executive Vice President of Lattice (since June 2017). Previously, Mr. Lucas served as Managing Partner of Lattice (2003 to 2016). | N/A | N/A | |||||

| JOSEPH G. MELCHER (1973) | Vice President, Chief Compliance Officer and AML Compliance Officer | Vice President and Chief Compliance Officer since 2022; AML Compliance Officer since 2022 | Mr. Melcher serves as Executive Vice President of HFMG and HASCO (since December 2013). Mr. Melcher also serves as Executive Vice President (since December 2013) and Chief Compliance Officer (since December 2012) of HFMC, serves as Executive Vice President and Chief Compliance Officer of Lattice (since July 2016), serves as Executive Vice President of HFD (since December 2013), and has served as President and Chief Executive Officer of HFD (from April 2018 to June 2019). | N/A | N/A | |||||

| VERNON J. MEYER (1964) | Vice President | Since 2022 | Mr. Meyer serves as Managing Director and Chief Investment Officer of HFMC and Managing Director of HFMG (since 2013). Mr. Meyer also serves as Senior Vice President-Investments of Lattice (since March 2019). Mr. Meyer has served in various positions within The Hartford and its subsidiaries in connection with the operation of the Hartford Funds. Mr. Meyer joined The Hartford in 2004. | N/A | N/A | |||||

| ALICE A. PELLEGRINO (1960) | Vice President and Assistant Secretary | Since 2022 | Ms. Pellegrino is Deputy General Counsel for HFMG (since April 2022) and currently serves as Vice President of HFMG (since December 2013). Ms. Pellegrino also serves as Vice President and Assistant Secretary of Lattice (since June 2017). Ms. Pellegrino has served in various positions within The Hartford and its subsidiaries in connection with the operation of the Hartford Funds. Ms. Pellegrino joined The Hartford in 2007. | N/A | N/A | |||||

| ANKIT PURI (1984) | Vice President and Treasurer | Effective September 11, 2023 | Effective September 11, 2023, Mr. Puri serves as Vice President and Treasurer of the Company. Prior to joining HFMC in 2023, Mr. Puri was a Fund Accounting Director, Investment Management Services, at SEI Investments (July 2021 through August 2023), an Associate Director, Fund Accounting Policy at The Vanguard Group (September 2020 to June 2021), and served in various positions at Ernst & Young LLP (October 2014 through September 2020). | N/A | N/A | |||||

| THOMAS R. PHILLIPS (1960) | Vice President and Secretary | Since 2022 | Mr. Phillips is Deputy General Counsel for HFMG and currently serves as a Senior Vice President (since June 2021) and Assistant Secretary (since June 2017) for HFMG. Mr. Phillips also serves as Vice President of HFMC (since June 2021). Prior to joining HFMG in 2017, Mr. Phillips was a Director and Chief Legal Officer of Saturna Capital Corporation from 2014–2016. Prior to that, Mr. Phillips was a Partner and Deputy General Counsel of Lord, Abbett & Co. LLC. | N/A | N/A |

| (1) | The address for each Trustee is c/o Hartford Funds 690 Lee Road, Wayne, PA 19087. |

| (2) | Term of Office: Each Trustee holds an indefinite term until his or her retirement, resignation, removal, or death. Trustees generally must retire no later than December 31 of the year in which the Trustee turns 75 years of age, or the Trustee’s resignation, removal, or death prior to the Trustee’s retirement. Each Fund officer generally serves until his or her resignation, removal or death. |

| (3) | The portfolios of the “Fund Complex” include the Fund and the operational series of The Hartford Mutual Funds, Inc., The Hartford Mutual Funds II, Inc., Hartford Series Fund, Inc., Lattice Strategies Trust, and Hartford Funds Exchange-Traded Trust. |

| (4) | “Interested person,” as defined in the 1940 Act, of the Fund because of the person’s affiliation with, or equity ownership of, Hartford Funds Management Company, LLC (“HFMC” or the “Adviser”), Hartford Funds Distributors, LLC (“HFD”) or affiliated companies. |

| 27 |

| 28 |

| a) | management; |

| b) | use; and |

| c) | protection; |

| a) | service your Transactions with us; and |

| b) | support our business functions. |

| a) | You; |

| b) | your Transactions with us; and |

| c) | third parties such as a consumer-reporting agency. |

| a) | your name; |

| b) | your address; |

| c) | your income; |

| d) | your payment; or |

| e) | your credit history; |

| a) | our insurance companies; |

| b) | our employee agents; |

| c) | our brokerage firms; and |

| d) | our administrators. |

| a) | market our products; or |

| b) | market our services; |

| a) | independent agents; |

| b) | brokerage firms; |

| c) | insurance companies; |

| d) | administrators; and |

| e) | service providers; |

| a) | taking surveys; |

| b) | marketing our products or services; or |

| c) | offering financial products or services under a joint agreement |

| a) | cookies; |

| b) | pixel tagging; or |

| c) | other technologies; |

| a) | “opt-out;” or |

| b) | “opt-in;” |

| a) | your authorization; or |

| b) | as otherwise allowed or required by law. |

| a) | underwriting policies; |

| b) | paying claims; |

| c) | developing new products; or |

| d) | advising customers of our products and services. |

| a) | the confidentiality; and |

| b) | the integrity of; |

| a) | secured files; |

| b) | user authentication; |

| c) | encryption; |

| d) | firewall technology; and |

| e) | the use of detection software. |

| a) | identify information to be protected; |

| b) | provide an adequate level of protection for that data; and |

| c) | grant access to protected data only to those people who must use |

| a) | credit history; |

| b) | income; |

| c) | financial benefits; or |

| d) | policy or claim information. |

| a) | your medical records; or |

| b) | information about your illness, disability or injury. |

| a) | Personal Financial Information; and |

| b) | Personal Health Information. |

| a) | your Application; |

| b) | your request for us to pay a claim; and |

| c) | your request for us to take an action on your account. |

| a) | asking about; |

| b) | applying for; or |

| c) | obtaining; |

(b) Not applicable.

Item 2. Code of Ethics.

The registrant, as of the end of the period covered by this report, has adopted a code of ethics that applies to the registrant’s principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions, regardless of whether these individuals are employed by the registrant or a third party. There have been no amendments, during the period covered by this report, to a provision of the code of ethics that applies to the registrant’s principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions, regardless of whether these individuals are employed by the registrant or a third party, and that relates to any element of the code of ethics description. The registrant has not granted any waivers, including an implicit waiver, from a provision of the code of ethics that applies to the registrant’s principal executive officer, principal financial officer, principal accounting officer or controller, or persons performing similar functions, regardless of whether these individuals are employed by the registrant or a third party, that relates to one or more of the items set forth in paragraph (b) of this item’s instructions. A copy of the code of ethics is filed herewith.

Item 3. Audit Committee Financial Expert.

The Board of Trustees of the registrant (the “Board”) has designated David Sung as an Audit Committee Financial Expert. Mr. Sung is considered by the Board to be an independent director.

Item 4. Principal Accountant Fees and Services.

| (a) | Audit Fees: The aggregate fees billed for the Fund’s first fiscal year ended March 31, 2024 for professional services rendered by the principal accountant for the audit of the registrant’s annual financial statements or services that are normally provided by the accountant in connection with statutory and regulatory filings or engagements for that fiscal year were: |

$127,200 for the fiscal year ended March 31, 2024.

| (b) | Audit Related Fees: The aggregate fees billed for the Fund’s first fiscal year ended March 31, 2024 for assurance and related services by the principal accountant that are reasonably related to the performance of the audit of the registrant’s financial statements and are not reported under paragraph (a) of this Item were: |

$0 for the fiscal year ended March 31, 2024.

| (c) | Tax Fees: The aggregate fees billed for the Fund’s first fiscal year ended March 31, 2024 for professional services rendered by the principal accountant for tax compliance, tax advice, and tax planning were: |

$3,250 for the fiscal year ended March 31, 2024. Tax-related services are principally in connection with, but not limited to, general tax services, excise tax and Passive Foreign Investment Company (PFIC) analysis.

| (d) | All Other Fees: The aggregate fees billed for the Fund’s first fiscal year ended March 31, 2024 for products and services provided by the principal accountant, other than the services reported in paragraphs (a) through (c) of this Item were: |

$385 for the fiscal year ended March 31, 2024. These fees were principally in connection with, but not limited to, general audit related products and services and an accounting research tool subscription.

| (e) | (1) The Pre-Approval Policies and Procedures (the “Policy”) adopted by the Audit Committee of the registrant (also, the “Fund”) sets forth the procedures pursuant to which services performed by the independent registered public accounting firm for the registrant may be pre-approved. The following summarizes the pre-approval requirements under the Policy. |

| 1. | The Audit Committee must pre-approve all audit services and non-audit services that the independent registered public accounting firm provides to the Fund. |

| 2. | The Audit Committee must pre-approve any engagement of the independent registered public accounting firm to provide non-audit services to any Service Affiliate (which is defined to include any entity controlling, controlled by, or under common control with the investment adviser that provides ongoing services to the Fund) during the period of the independent registered public accounting firm’s engagement to provide audit services to the Fund, if the non-audit services to the Service Affiliate directly impact the Fund’s operations and financial reporting. |

| 3. | The Audit Committee shall pre-approve certain non-audit services to the Fund and its Service Affiliates pursuant to procedures set forth in the Policy. |

| 4. | The Audit Committee, from time to time, may designate one or more of its members who are Independent Directors (each a “Designated Member”) to consider, on the Audit Committee’s behalf, any non-audit services, whether to the Fund or to any Service Affiliate, that have not been pre-approved by the Audit Committee. The Designated Member also shall review, on the Audit Committee’s behalf, any proposed material change in the nature or extent of any non-audit services previously approved. In considering any requested non-audit services or proposed material change in such services, the Designated Member shall not authorize services which would exceed $50,000 in fees for such services. |