UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-23788

ARK Venture Fund

(Exact name of registrant as specified in charter)

c/o ARK Investment Management LLC

200 Central Avenue, Suite 220

St. Petersburg, FL 33701

(Address of principal executive offices) (Zip code)

Corporation Service Company

251 Little Falls Drive

Wilmington, DE 19808

(Name and address of agent for service)

Registrant’s telephone number, including area code: (727) 810-8160

Date of fiscal year end: July 31

Date of reporting period: July 31, 2023

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Table of Contents

Item 1. Reports to Stockholders.

(a) The Report to Shareholders is attached herewith.

Table of Contents

Table of Contents | |

|

| | |

Table of Contents

Shareholder Letter (Unaudited) | | |

| | |

Dear Shareholder:

ARK Investment Management LLC (“ARK” or the “Adviser”), the investment adviser to the Fund, specializes in thematic investing in disruptive innovation. The Fund is an actively managed, closed-end interval fund that invests not only in public and private companies focused on technologically enabled innovation but also, selectively, in other venture capital funds. Importantly, we aim to democratize venture capital, enabling any investor with a minimum of $500 to invest in private and public companies that we believe are going to change the way the world works, without encountering qualification or accreditation thresholds. In addition, the Fund expects to offer liquidity equal to 5% of NAV (net asset value) on a quarterly basis.

The Fund seeks to include portfolio companies that we believe are leading and benefiting from five innovation platforms: artificial intelligence (AI), energy storage, robotics, multiomic sequencing, and blockchain technology. According to ARK's research, we believe that these five innovation platforms are converging to create unprecedented growth trajectories. AI is the most important catalyst, its velocity cascading through all other technologies.

Despite the growth potential of disruptive innovation, the 2022 bear market obscured many disruptive breakthroughs. But innovation continued apace. ChatGPT, a version of GPT-3 tuned for conversation dialogue, already scores above the national average on SAT questions, highlighting the power of AI. In the UK, a research hospital used an advanced version of gene-editing called base-editing to cure a 12-year-old girl with leukemia who had failed dozens of therapies. SpaceX launched 61 Falcon9 rockets, reusing the last one within 21 days, compared to 356 days for the first one. In our view, companies sacrificing short-term profitability to invest heavily in innovative technologies have exponential and highly profitable long-term growth opportunities.

In the face of market headwinds and media criticism, these breakthroughs are corroborating our original research and boosting our confidence that ARK’s strategies are on the right side of change. Disruption can surface in surprising forms and at unexpected times. Innovation solves problems and has historically gained share during turbulent times.

Thus far in 2023, sentiment appears to have shifted with the market agreeing that AI is reshaping industries. We believe it could be a long-term growth driver more impactful than the internet. During the second quarter of 2023, ChatGPT continued its momentum in capturing the imagination of businesses and consumers, unleashing excitement that sparked a rally in mega-cap technology stocks. Relatedly, in the public equity markets shares of NVIDIA soared in May after the company reported its fiscal first-quarter earnings and became a clear beneficiary of the boom in generative AI that ChatGPT unleashed. Seemingly, many investors assumed that benchmark-heavy incumbents that came of age during the internet revolution would benefit disproportionately from the AI revolution as well.

We view the private markets at the “tip of the spear” for disruptive innovation, in particular the investment opportunity for AI. MosaicML, a Fund portfolio company, is improving the efficiently or AI model training by up to 7x. To note, in June, Databricks announced that it will pay $1.3 billion to acquire MosaicML, representing an approximate 5x return on this name since its addition to the Fund as its first investment in September 2022. Anthropic is an AI startup co-founded by Dario Amodei, the former VP of Research at OpenAI. The company is conducting research and building AI products that put safety first. Claude, its first product, is a general-purpose large language model that leverages Anthropic’s research on Constitutional AI to “align” the model and prevent abuse. While some companies might train their own AI models on proprietary data, others are likely to leverage a combination of proprietary and third-party models.

Unfortunately, we believe most investors are “short” venture capital. According to ARK’s research, venture capital still is in early days for three reasons:

1. In 2022, the $99 billion invested in venture capital represented only 0.24% of the capitalization of global public equity markets. In our view, innovation is likely to disrupt many of the companies that make up the $105 trillion in global public equity market cap, ceding significant share to startups and venture capital.

2. According to our research, disruptive innovation is likely to scale exponentially during the next decade. Startups and venture capitalists are likely to capture a share of that value creation.

3. Because the tech and telecom bust in the early 2000s and the Global Financial Crisis in 2008-09 precipitated extensive regulations that have burdened public companies, startups are choosing to stay private longer than historically has been the case. Previously, many startups raised two to three rounds of venture capital and then went public at ~$100 million valuations. Today, startups like Stripe and SpaceX have raised many private rounds and have scaled to $100+ billion valuations. Facilitating liquidity for employees and other shareholders, secondary markets have created even more capacity for venture capital.

1

Table of Contents

Shareholder Letter (continued) (Unaudited) | |

|

| | |

The Fund’s investment mandate is similar to our flagship ETF, ARK Innovation ETF (ARKK), in that it seeks to invest in the five innovation platforms, but expands the opportunity set into the private markets. Like our public equity strategies, our top-down and bottom-up research is the lens through which we screen and select investments. We continue to believe our differentiated value proposition combined with our network of co-investors, public companies, founders, and academics offers access to the most promising private technology companies.

On the following pages, you will find information relating to your ARK Venture Fund investment. If you have any questions, I encourage you to contact our distribution partner Titan or ARK directly. You can find additional information, including our portfolio holdings, on the Fund’s website located at: www.ark-ventures.com

We appreciate the opportunity to help you meet your investment goals and thank you for enabling us to invest for you at the pace of innovation!

Sincerely,

Catherine D.Wood

Chief Investment Officer and Chief Executive Officer

ARK Investment Management LLC

2

Table of Contents

Management’s Discussion of Fund Performance (Unaudited) | | |

| | |

Market Review and Investment Strategy

In the fiscal year ended July 31, 2023, global equity markets appreciated as NVIDIA’s guidance for the second quarter shocked on the high side of expectations, thanks to provocative proofs of concepts from artificial intelligence (AI) generally and ChatGPT specifically. Increased demand for AI hardware is pointing toward a significant acceleration in software revenue growth. As companies develop AI-powered products and services, ARK estimates that software may generate up to $8 of revenue for every dollar spent on AI hardware by 2030. In what could be “winner take most” opportunities, we believe companies with large pools of proprietary data and broad-based distribution should be best positioned to capitalize on AI use cases and reap the potentially dramatic productivity gains associated with generative AI.

Recent economic data and comments from the US Federal Reserve (Fed) appear to have tempered investors’ previous expectations of interest rate declines. Now, interest rate futures are pricing in a slowdown or recession and one or two more rate hikes before interest rates start to decline. Should an economic slowdown evolve into a hard landing, the slope of interest rate declines could steepen.

Economic data was not as clear-cut. While the labor market seemed resilient, a number of leading indicators were warning of recession.

• With a strong correlation to Gross Domestic Product (GDP), the US Leading Economic Index (LEI) has dropped for 14 consecutive months and now is down 7.9% year-over-year.1 In 2022, GDP declined for two consecutive quarters, a technical recession. During the last two quarters, Gross Domestic Income (GDI)—which should equal GDP over time—has declined sequentially. The divergence in growth between GDP and GDI is begging the question about future revisions: will GDI be revised up or GDP down. Our view is the latter.

• Based on monthly surveys from the Federal Reserve District Banks of Dallas, New York, Philadelphia, Richmond, and Kansas, manufacturing activity is contracting at an accelerated rate. Corroborating this evidence, new orders in the national Purchasing Managers’ Index, an index of the prevailing direction of economic trends in the manufacturing and service sectors, are declining.

• According to the Senior Loan Officer Opinion Survey (SLOOS), the willingness of banks to lend is plummeting, often a leading indicator of recession. Borrowing and lending play pivotal roles during economic expansions. The demand for commercial and industrial (C&I) loans is consistent with previous recession levels, and the Bank of America Fund Manager Survey suggests that commercial real estate could be the epicenter of the next financial crisis.

• US consumer sentiment2 remains at levels last seen during the Global Financial Crisis in 2008-2009 and back-to-back recessions with double-digit inflation and interest rates during the early 1980s. Meanwhile, the personal saving rate has collapsed from 9.3% pre-COVID to 4.6%3 which, when coupled with historically low consumer sentiment, is pointing toward weakness in consumption growth. Adding to those concerns, the third largest category of non-housing debt, credit card balances have reached a record high level at ~$1 trillion.4 Because interest rates on credit cards nearly doubled to 20-21% during the past ten years, the burden of credit card debt has intensified. Additionally, student loan payments are slated to resume this October, further pressuring consumer purchasing power.

• In recent months, PIMCO and Brookfield have defaulted on commercial property mortgages across major US cities, a trend exacerbated by the combination of rapid interest rate increases and the lower occupancy rates associated with the shift to remote work environments. Recent trends have hit San Francisco particularly hard, the value of one commercial use building dropping from $300 million to $60 million, or 80%, in four years.5 Moreover, two of San Francisco’s largest hotels are vacating the city.

The movement in interest rates over this fiscal period was remarkable. The Federal Funds Target Rate has surged 22-fold in the last year, a faster pace than all previous tightening cycles—including the one in 1980-1981 that crushed inflation—creating significant strains at regional banking and in commercial real estate. Bank deposits have dropped 4.0% year-over-year, the largest decline since 1948. We believe additional rate hikes will exacerbate this fragile situation.

While the Fed is determined to squelch inflation by increasing interest rates, the bond market has been signaling that it could be making a major mistake. Since March 2021, the yield curve6 has flattened by 265 basis points, inverting from +159 to -106 basis points,7 the worst inversion since the early 1980s when the Fed was fighting entrenched double-digit inflation. This dynamic suggests that both real growth and inflation could surprise on the low side of expectations. In ARK’s view, the Fed is making decisions based on lagging indicators—employment and headline inflation—and ignoring leading indicators that are telegraphing recession and/or price deflation.

3

Table of Contents

Management’s Discussion of Fund Performance (continued) (Unaudited) | |

|

| | |

The Federal Reserve began increasing interest rates when the year-over-year Consumer Price Index (CPI)—a lagging economic indicator—reached 8.5% on a year-over-year basis in March 2022. Shortly thereafter, an inflationary surge influenced by geopolitical pressures and inventory hoarding peaked at 9.1% year-over-year. Since then, CPI inflation has dropped to 3.0%,8 thanks to various deflationary forces––good, bad, and cyclical. Tesla’s CEO Elon Musk9 and DoubleLine’s CEO Jeff Gundlach10 have echoed our concerns about the risk of deflation.

Innovation is a potential source of good deflation, as learning curves can cut costs and increase productivity. Yet, we believe many companies have catered to short-term-oriented, risk-averse shareholders, satisfying their demands for profits/dividends “now”. On balance, they have leveraged their balance sheets to buy back stock, bolster earnings, and increase dividends. In so doing, many have curtailed investments and could be ill-prepared for the potential disintermediation associated with disruptive innovation. Saddled with aging products and services, they could be forced to cut prices to clear unwanted inventories and service debt, causing bad deflation.

If we are correct in our assessment that growth, inflation, or both will surprise on the low side of expectations, scarce double-digit growth opportunities should be rewarded accordingly. The adoption of new technologies typically accelerates during tumultuous times as concerned businesses and consumers change their behavior much more rapidly than otherwise would be the case. As a result, stocks of innovation-oriented companies have historically performed better and emerge as new market leaders toward the end of a bear market. We believe the coronavirus crisis and Russia’s invasion of Ukraine have transformed the world significantly and permanently, suggesting that many innovation-driven strategies and stocks could be productive holdings during the next five to ten years.

ARK continues to research and discover companies that are causing or embracing disruptive innovation, and that are creating pockets of rapid growth in an otherwise uncertain growth environment.

Must be preceded or accompanied by a prospectus.

Communications Sector Risk. The Fund will be more affected by the performance of the communications sector than a fund with less exposure to such sector. Cyber Security Risk. As the use of Internet technology has become more prevalent in the course of business, funds have become more susceptible to potential operational risks through breaches in cyber security. Disruptive Innovation Risk. Companies that the Adviser believes are capitalizing on disruptive innovation and developing technologies to displace older technologies or create new markets may not in fact do so. Financial Technology Risk. Companies that are developing financial technologies that seek to disrupt or displace established financial institutions generally face competition from much larger and more established firms. Next Generation Internet Companies Risk. The risks described below apply, in particular, to the Fund’s investment in Next Generation Internet Companies. Foreign Securities Risk. The Fund’s investments in foreign securities can be riskier than U.S. securities investments. Investments in the securities of foreign issuers (including investments in ADRs and GDRs) are subject to the risks associated with investing in those foreign markets, such as heightened risks of inflation or nationalization. The prices of foreign securities and the prices of U.S. securities have, at times, moved in opposite directions. In addition, securities of foreign issuers may lose value due to political, economic and geographic events affecting a foreign issuer or market. During periods of social, political or economic instability in a country or region, the value of a foreign security traded on U.S. exchanges could be affected by, among other things, increasing price volatility, illiquidity, or the closure of the primary market on which the security (or the security underlying the ADR or GDR) is traded. You may lose money due to political, economic and geographic events affecting a foreign issuer or market. The Fund normally will not hedge any foreign currency exposure. Future Expected Genomic Business Risk. The Adviser may invest some of the Fund’s assets in Genomics Revolution Companies that do not currently derive a substantial portion of their current revenues from genomic-focused businesses and there is no assurance that any company will do so in the future, which may adversely affect the ability of the Fund to achieve its investment objective. Emerging Market Securities Risk. Investment in securities of emerging market issuers may present risks that are greater than or different from those associated with securities of developed market issuers due to less developed and liquid markets and such factors as increased economic, political, regulatory, or other uncertainties. Cryptocurrency Risk. Cryptocurrencies (also referred to as “virtual currencies” and “digital currencies”) are digital assets designed to act as a medium of exchange. Cryptocurrency is an emerging asset class. There are thousands of cryptocurrencies, the most well-known of which is bitcoin. The Fund may have exposure to cryptocurrencies, such as bitcoin indirectly through an investment in the Bitcoin Investment Trust (“GBTC”), a privately offered, open-end investment vehicle that invests in bitcoin. Health Care Sector Risk. The health care sector may be affected by government regulations and government health care programs, restrictions on government reimbursement for medical expenses, increases or decreases in the cost of medical products and services and product liability claims, among other factors. Leverage Risk. The use of leverage can create risks. Leverage can increase market exposure, increase volatility in the Fund, magnify investment risks, and cause losses to be realized more quickly. New Fund Risk. There can be no assurance that the Fund will grow to or maintain an economically viable size, in which case the Board may determine to liquidate the Fund if it determines that liquidation is in the best interest of shareholders. Non-Diversification Risk. The Fund is classified as a “non-diversified” investment company under the 1940 Act. Therefore, the Fund may invest a relatively higher percentage of its assets in a relatively smaller number of issuers or may invest a larger proportion of its assets in a single issuer. As a result, the gains and losses on a single investment may have a greater impact on the Fund’s NAV and may make the Fund more volatile than more diversified funds.

The ARK Venture Fund is a continuously-offered, non-diversified, registered closed-end fund with limited liquidity. You should not expect to be able to sell your Shares in the ARK Venture Fund other than through the Fund’s repurchase policy, regardless of how the Fund performs. The Fund’s Shares will not be listed on any securities exchange, and the Fund does not expect a secondary market in the Shares to develop.

Foreside Fund Services, LLC, distributor.

4

Table of Contents

Management’s Discussion of Fund Performance (continued) (Unaudited) | | |

Investment Results: ARK Venture Fund (ARKVX) | |

ARK Venture Fund (ARKVX) is a non-diversified closed-end management investment company registered under the Investment Company Act of 1940, as amended. The Fund’s investment objective is to seek long-term growth of capital. There can be no assurance that the Fund will achieve its investment objective. The Fund pursues this objective by investing its assets primarily in domestic and foreign equity securities of companies that are relevant to the Fund’s investment theme of disruptive innovation.

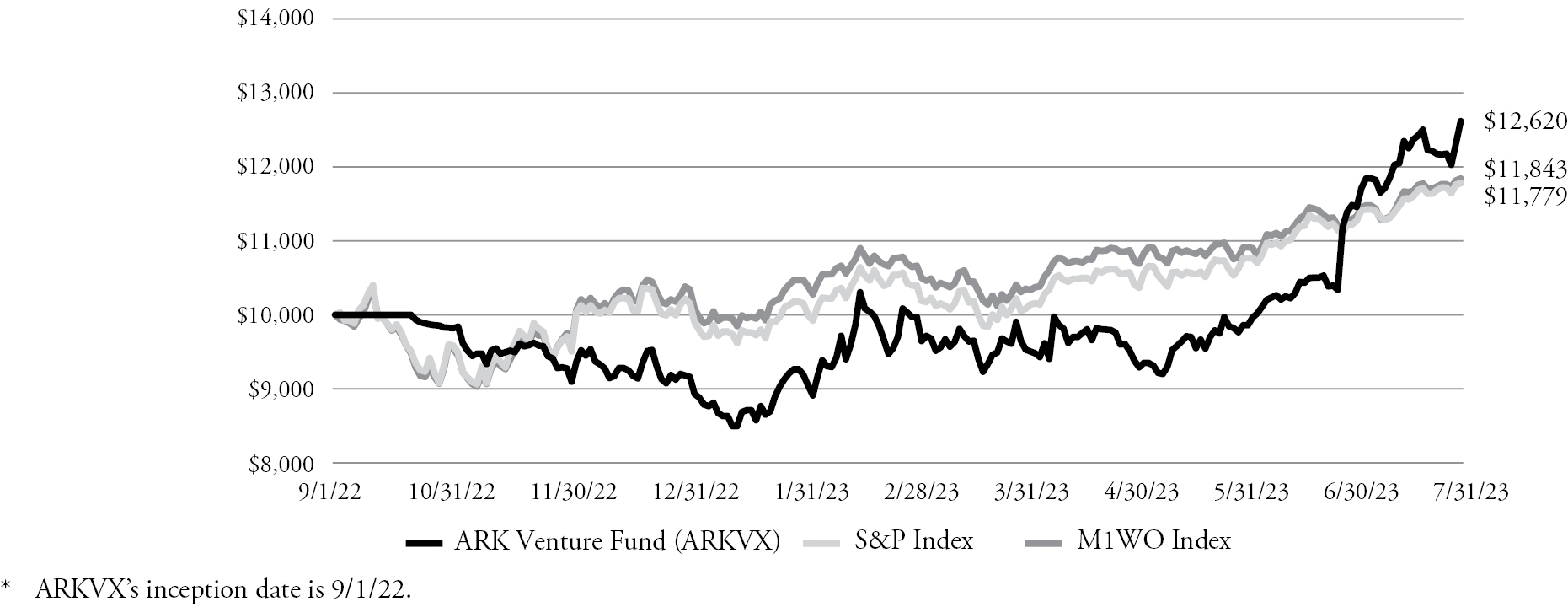

At July 31, 2023, ARKVX outperformed the S&P 500 Index and the MSCI World Net Index for the since-inception period.

Amongst ARKVX’s private holdings, the top positive contributors to performance were MosaicML, Critical Ideas, Inc. (Chipper Cash), Replit, Inc., Anthropic, PBC, and Freenome Holdings, Inc. The simple agreement to purchase future equity in MosaicML quintupled in value after the company agreed to be purchased by Databricks, Inc. for $1.3 billion. Databricks, Inc., one of the fastest growing SaaS enterprise software companies, aims to benefit from MosaicML’s cutting-edge machine learning tools and infrastructures that build, deploy, and manage advanced artificial intelligence models.

Amongst ARKVX’S private holdings, the top detractors to performance were X Holdings I, Inc., the parent company of X (formerly Twitter), Flexport, Inc., Discord Inc., and Epic Games, Inc. Shares of X were marked down shortly after the company went private due to lower revenue projections as advertisers paused their ad spend and concerns over the company’s negative cash burn. In June 2023, Linda Yaccarino succeeded Elon Musk as the CEO of the company. Linda brought extensive advertising experience from her previous role as the chairman of global advertising & partnerships for NBCUniversal. More recently, the company has seen advertisers come back to the platform but the advertising market remains pressured due to macro related headwinds. Management has also cut significant costs with a goal to generate positive cash flow by the end of the year. ARK believes that X is well-positioned to grow its influence as management continues to execute on Musk’s vision of an ‘Everything’ app.

Amongst ARKVX’S public holdings, the top positive contributors to performance were Exact Sciences Corp. (EXAS or Exact Sciences), NVIDIA Corp. (NVDA or NVIDIA), Coinbase Global, Inc. (COIN), DraftKings, Inc. (DKNG) and ROBLOX Corp. (RBLX). Shares of Exact Sciences contributed to performance after the company surpassed revenue and earnings expectations for the first quarter of 2023 and guided to positive free cash flow, which is the residual amount of cash that a business has earned from its operations, over a specific period of time, less maintenance, during 2023. In addition, Exact Sciences’ next-generation Cologuard screening test for colon cancer demonstrated better specificity and sensitivity than Exact Sciences’ existing product, so it will seek FDA approval of the new test by the end of this year. Shares of NVIDIA appreciated after the company announced much better than expected guidance for the second quarter of 2023, thanks to demand for data center products in response to breakthroughs in generative AI. As the primary provider of accelerated computing hardware for developing and running large language models, NVIDIA should be an early beneficiary of the boom in generative AI that ChatGPT unleashed late last year.

Amongst ARKVX’s public holdings, the top detractors to performance were Beam Therapeutics, Inc. (BEAM or Beam Therapeutics), Zoom Video Communications, Inc. (ZM or Zoom), Prime Medicine, Inc. (PRME), Moderna, Inc. (MRNA), and Intellia Therapeutics, Inc. (NTLA). Shares of Beam Therapeutics declined in a broad-based sell-off in gene-editing names in 2023 on no meaningful company specific news. Beam Therapeutics is focused on applying its novel base-editing method to rare disease indications. Shares of Zoom declined relatively recently after an analyst from Citibank focused on increased competition in the enterprise communications space and negative data points suggesting slower growth generally. We maintain conviction in Zoom’s potential to share most of the enterprise communications platform space with Microsoft Corp.

Cumulative Total Returns as of 7/31/23 |

| | Since

Inception*

(Cumulative) |

ARK Venture Fund (ARKVX) | 26.20% |

S&P 500 Index | 17.79% |

MSCI World Net Index | 18.43% |

5

Table of Contents

Management’s Discussion of Fund Performance (concluded) (Unaudited) | |

|

| | |

Growth of an Assumed $10,000 Investment Since Inception* Through 7/31/23 (At Net Asset Value)

Past performance does not guarantee future results. The performance data quoted represents past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when repurchased, may be worth more or less than the original cost. To obtain performance information current to the most recent month end, please visit www.ark-ventures.com. Performance reflects applicable fee waivers and/or expense limitations in effect during the periods shown and in their absence, performance would be reduced. As stated in the Fund’s current prospectus, as supplemented, the net expense ratio for the Fund is 2.90%. Additional information about fees and expense levels can be found in the Fund’s current prospectus. Returns are based on the dollar value of a single share of the Fund, calculated using the value of the underlying assets of the Fund minus its liabilities, divided by the number of shares outstanding. The NAV is typically calculated at 4:00 pm Eastern time on each business day the New York Stock Exchange is open for trading.

The returns for the Fund do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or upon sale of Fund shares.

This graph represents the growth of a hypothetical investment of $10,000. It assumes reinvestment of dividends and capital gains and reflects ongoing fund expenses, but does not reflect sales loads, redemption fees, or the effects of taxes on any capital gains and/or distributions.

6

Table of Contents

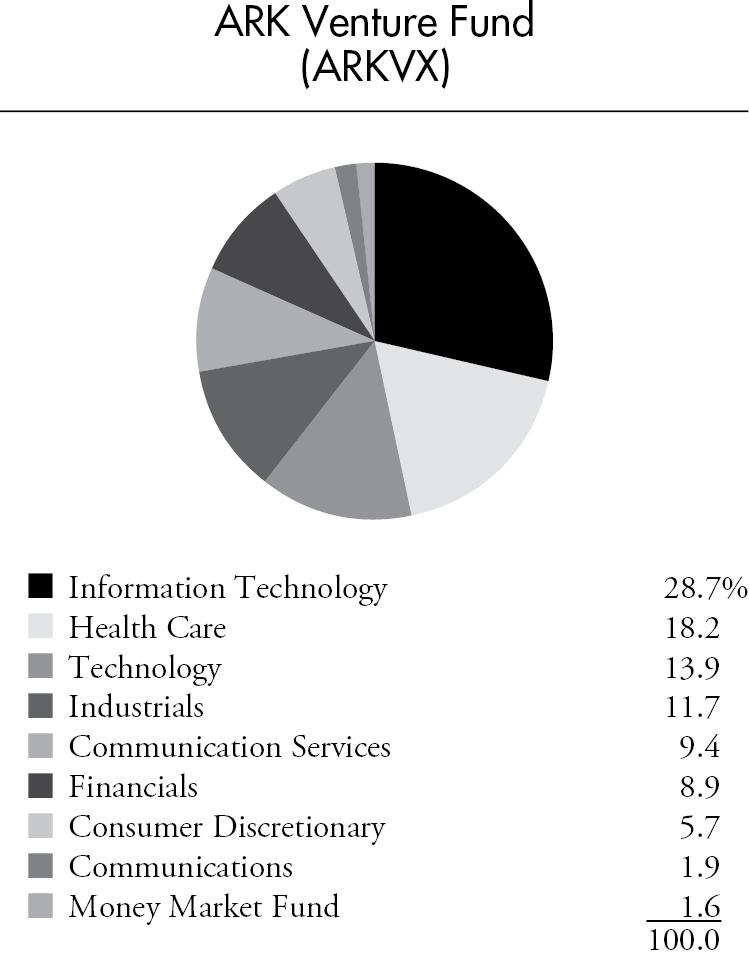

Sector Diversification (as a percentage of total investments) July 31, 2023 (Unaudited) | | |

| | |

7

Table of Contents

ARK Venture Fund’s Private Investments | |

|

July 31, 2023 (Unaudited) | |

| Anthropic | Anthropic, PBC is an AI startup conducting research and building AI products that put safety at the frontier. |

| Freenome | Freenome Holdings, Inc. combines deep learning and novel biomolecular techniques to detect early-stage cancers from a routine, non-invasive blood draw. |

| Discord | Discord Inc. is a casual communications platform that enables its individual users and groups/organizations to communicate via text, audio, and video. |

| Replit | Replit, Inc. is a modern browser-based coding platform with an embedded AI coding assistant. |

| Databricks | Databricks, Inc. is a software platform that helps its customers unify their analytics across the business, data science, and data engineering. |

| X | Founded in 2006, X Holdings I, Inc., formerly Twitter, is the first mobile-first social network. |

| Chipper Cash | Critical Ideas, Inc. (Chipper Cash) is a fintech company offering financial products to consumers and businesses across Africa. |

| Flexport | Flexport, Inc. is a tech-enabled platform that helps customers manage their supply chain. |

| Epic Games | Epic Games, Inc. is a video game and software company that develops and publishes its own video games and offers its game engine technology to other developers. |

| Mythical Games | Mythical, Inc. provides a suite of tools to enable video game publishers/developers to launch blockchain-based games. |

| Axiom Space | Axiom Space, Inc. operates missions to the International Space Station (ISS) for customers. |

| Zipline | Drone delivery company Zipline International Inc. operates in Africa, the US, and Japan, providing instant delivery service. |

| Humata AI | Tilda Technologies Inc. (Humata AI) is an early-stage AI startup that enables users to extract knowledge from files. |

| Blockdaemon | Blockdaemon Inc. is a cryptocurrency infrastructure provider. |

| Hammerspace | Hammerspace, Inc. offers a global data environment for distributed teams of developers to access and handle data as if it were locally stored. |

8

Table of Contents

Consolidated Schedule of Investments

ARK Venture Fund | | |

July 31, 2023 | | |

| | Shares/

Principal/

Units | | Cost | | Value |

COMMON STOCKS IN PUBLIC COMPANIES – 49.9% |

AEROSPACE & DEFENSE – 1.9% | | | | | | | | |

Rocket Lab USA, Inc.* | | 64,239 | | $ | 255,639 | | $ | 473,441 |

AUTOMOBILES – 4.0% | | | | | | | | |

Tesla, Inc.* | | 3,745 | | | 523,726 | | | 1,001,525 |

BIOTECHNOLOGY – 9.2% | | | | | | | | |

Beam Therapeutics, Inc.* | | 12,504 | | | 418,738 | | | 385,998 |

CRISPR Therapeutics AG (Switzerland)* | | 6,733 | | | 314,502 | | | 386,003 |

Exact Sciences Corp.* | | 3,407 | | | 143,834 | | | 332,319 |

Ginkgo Bioworks Holdings, Inc.* | | 100,932 | | | 227,824 | | | 253,339 |

Intellia Therapeutics, Inc.* | | 5,593 | | | 228,403 | | | 236,752 |

Prime Medicine, Inc.* | | 30,516 | | | 469,380 | | | 459,876 |

Recursion Pharmaceuticals, Inc., Class A* | | 17,480 | | | 225,282 | | | 246,818 |

| | | | | 2,027,963 | | | 2,301,105 |

CAPITAL MARKETS – 6.6% |

Coinbase Global, Inc., Class A* | | 11,848 | | | 530,069 | | | 1,168,331 |

Robinhood Markets, Inc., Class A* | | 37,381 | | | 357,465 | | | 480,720 |

| | | | | 887,534 | | | 1,649,051 |

ENTERTAINMENT – 4.3% | | | | | | | | |

ROBLOX Corp., Class A* | | 10,826 | | | 346,002 | | | 424,921 |

Roku, Inc.* | | 6,664 | | | 344,371 | | | 641,543 |

| | | | | 690,373 | | | 1,066,464 |

FINANCIAL SERVICES – 2.1% |

Block, Inc.* | | 6,577 | | | 410,882 | | | 529,646 |

HEALTHCARE PRODUCTS – 1.2% |

Quantum-SI, Inc.* | | 74,812 | | | 231,371 | | | 291,019 |

HOTELS, RESTAURANTS & LEISURE – 1.6% |

DraftKings, Inc., Class A* | | 12,490 | | | 166,585 | | | 396,932 |

INTERACTIVE MEDIA & SERVICES – 1.8% |

Pinterest, Inc., Class A* | | 15,654 | | | 423,428 | | | 453,810 |

IT SERVICES – 3.4% | | | | | | | | |

Shopify, Inc., Class A (Canada)* | | 5,085 | | | 163,678 | | | 343,645 |

Twilio, Inc., Class A* | | 7,408 | | | 364,390 | | | 489,150 |

| | | | | 528,068 | | | 832,795 |

LIFE SCIENCES TOOLS & SERVICES – 1.7% |

10X Genomics, Inc., Class A* | | 6,837 | | | 264,069 | | | 430,594 |

PHARMACEUTICALS – 1.4% | | | | | | | | |

Moderna, Inc.* | | 2,884 | | | 342,900 | | | 339,332 |

SEMICONDUCTORS & SEMICONDUCTOR EQUIPMENT – 3.4% |

NVIDIA Corp. | | 781 | | | 102,210 | | | 364,953 |

Teradyne, Inc. | | 4,189 | | | 452,908 | | | 473,106 |

| | | | | 555,118 | | | 838,059 |

| | Shares/

Principal/

Units | | Cost | | Value |

SOFTWARE – 7.3% |

Palantir Technologies, Inc., Class A* | | 21,128 | | $ | 340,833 | | $ | 419,179 |

UiPath, Inc., Class A* | | 26,738 | | | 369,262 | | | 483,423 |

Unity Software, Inc.* | | 10,829 | | | 330,683 | | | 496,401 |

Zoom Video Communications, Inc., Class A* | | 5,539 | | | 408,668 | | | 406,286 |

| | | | | 1,449,446 | | | 1,805,289 |

TOTAL COMMON STOCKS IN PUBLIC COMPANIES | | | | | 8,757,102 | | | 12,409,062 |

| | Acquisition

Date | | Shares/

Principal/

Units | | Cost | | Value |

COMMON STOCKS IN PRIVATE COMPANIES – 10.5% |

DIVERSIFIED FINANCIAL SERVICES – 4.1% |

Blockdaemon, Inc.*(a)(b) | | 6/27/23 | | 217,865 | | 1,020,000 | | 1,020,000 |

ENTERTAINMENT – 1.0% |

Discord Inc.*(a)(b) | | 11/14/22 | | 960 | | 360,000 | | 254,419 |

INTERNET – 2.2% |

X Holdings I, Inc.

(Twitter)*(a)(b) | | 10/28/22 | | 10,000 | | 1,000,000 | | 553,190 |

SOFTWARE – 3.2% |

Databricks, Inc.(a)(b)(d) | | 9/23/22 | | 26,371 | | 400,000 | | 2,000,000 |

Epic Games, Inc.*(a)(b)(c) | | 9/23/22 | | 1,631 | | 1,022,829 | | 804,701 |

| | | | | | | 1,422,829 | | 2,804,701 |

TOTAL COMMON STOCKS IN PRIVATE COMPANIES | | | | 3,802,829 | | 4,632,310 |

PREFERRED STOCKS IN PRIVATE COMPANIES – 26.2% |

AEROSPACE & DEFENSE – 2.2% |

Axiom Space, Inc, Series C*(a)(b) | | 4/12/23 | | 2,960 | | 500,033 | | 539,815 |

COMPUTERS – 2.0% |

Hammerspace, Inc., Series A-1*(a)(b) | | 7/26/23 | | 511,456 | | 499,999 | | 499,999 |

HEALTHCARE PRODUCTS – 4.6% |

Freenome Holdings, Inc.,

Series E*(a)(b) | | 9/23/22 | | 85,711 | | 999,990 | | 1,147,671 |

SOFTWARE – 11.9% |

Anthropic, Inc.,

Series C-1*(a)(b) | | 3/31/23 | | 89,078 | | 1,049,998 | | 1,216,806 |

Mythical, Inc.,

Series C-1*(a)(b) | | 4/11/23 | | 60,415 | | 500,001 | | 548,568 |

Replit, Inc.,

Series B-1*(a)(b) | | 1/23/23 | | 25,385 | | 1,000,000 | | 1,202,487 |

| | | | | | 2,549,999 | | 2,967,861 |

See accompanying Notes to Consolidated Financial Statements.

9

Table of Contents

Consolidated Schedule of Investments (continued)

ARK Venture Fund | |

|

July 31, 2023 | | |

| | Acquisition

Date | | Shares/

Principal/

Units | | Cost | | Value |

TRANSPORTATION – 5.5% |

Flexport, Inc., Series A*(a)(b) | | 9/23/22 | | 49 | | $ | 670 | | $ | 449 |

Flexport, Inc., Series B-1*(a)(b) | | 9/23/22 | | 4,940 | | | 67,524 | | | 45,251 |

Flexport, Inc., Series C*(a)(b) | | 9/23/22 | | 24,640 | | | 336,798 | | | 225,702 |

Zipline International, Inc., Series F*(a)(b) | | 5/30/23 | | 24,877 | | | 999,983 | | | 1,104,041 |

| | | | | | | | 1,404,975 | | | 1,375,443 |

TOTAL PREFERRED STOCKS IN PRIVATE COMPANIES | | | | | 5,954,996 | | | 6,530,789 |

SIMPLE AGREEMENT TO PURCHASE EQUITY IN PRIVATE COMPANIES – 11.0% |

COMMERCIAL SERVICES – 2.0% |

Critical Ideas, Inc. (Chipper Cash)*(a)(b) | | 9/23/22 | | 400,000 | | | 400,000 | | | 490,120 |

SOFTWARE – 9.0% |

Tilda Technologies, Inc. (Humata AI)*(a)(b) | | 6/27/23 | | 250,000 | | | 250,000 | | | 250,000 |

TOTAL SIMPLE AGREEMENT TO PURCHASE EQUITY IN PRIVATE COMPANIES | | | 650,000 | | | 740,120 |

| | Shares/

Principal/

Units | | Cost | | Value |

MONEY MARKET FUND – 1.6% |

Goldman Sachs Financial Square Treasury Obligations Fund, 5.15%(e) | | 396,025 | | 396,025 | | | 396,025 |

TOTAL INVESTMENTS – 99.2% | | | | 19,560,952 | | | 24,708,306 |

Other Assets in Excess of Liabilities – 0.8% | | | | | | | 210,231 |

Net Assets – 100.0% | | | | | | $ | 24,918,537 |

Fair Value Measurements

The Fund discloses the fair value of its investments in a hierarchy that distinguishes between: (i) market participant assumptions developed based on market data obtained from sources independent of the Fund (observable inputs) and (ii) the Fund’s own assumptions about market participant assumptions developed based on the best information available under the circumstances (unobservable inputs). The three levels defined by the hierarchy are as follows:

• Level 1 – Quoted prices in active markets for identical assets.

• Level 2 – Other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.).

• Level 3 – significant unobservable inputs, including the Fund’s own assumptions in determining the fair value of investments.

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

The following is a summary of the Fund’s investments as of July 31, 2023:

Investment in Securities | | Level 1 | | Level 2 | | Level 3 | | Total |

Common Stocks in Public Companies‡ | | $12,409,062 | | $ — | | $ — | | $12,409,062 |

Preferred Stocks in Private Companies‡ | | — | | — | | 6,530,789 | | 6,530,789 |

Simple Agreement to Purchase Equity in Private Companies‡ | | — | | — | | 740,120 | | 740,120 |

Common Stocks in Private Companies‡ | | — | | — | | 4,632,310 | | 4,632,310 |

Money Market Fund | | 396,025 | | — | | — | | 396,025 |

Total | | $12,805,087 | | $ — | | $11,903,219 | | $24,708,306 |

See accompanying Notes to Consolidated Financial Statements.

10

Table of Contents

Consolidated Schedule of Investments (concluded)

ARK Venture Fund | | |

July 31, 2023 | | |

A reconciliation of assets in which Level 3 inputs are used in determining fair value is presented below:

| | Common Stocks In

Private Companies | | Preferred Stocks In

Private Companies | | Simple Agreement To

Purchase Equity In

Private Companies | | Total |

Balance at September 1, 2022* | | $ | — | | $ | — | | $ | — | | | $ | — |

Purchases | | | 3,402,829 | | | 4,954,996 | | | 2,050,000 | | | | 10,407,825 |

Sales | | | — | | | — | | | — | | | | — |

Transfer into Level 3 | | | — | | | — | | | — | | | | — |

Transfer out of Level 3 | | | — | | | — | | | — | | | | — |

Conversions | | | 400,000 | | | 1,000,000 | | | (1,400,000 | ) | | | — |

Net Realized Gain (Loss) | | | — | | | — | | | — | | | | — |

Net Change in Unrealized Appreciation (Depreciation) | | | 829,481 | | | 575,793 | | | 90,120 | | | | 1,495,394 |

Balance at July 31, 2023 | | $ | 4,632,310 | | $ | 6,530,789 | | $ | 740,120 | | | $ | 11,903,219 |

Net Change in Unrealized Appreciation (Depreciation) on Level 3 securities still held as of July 31, 2023 | | | 829,481 | | | 575,793 | | | 90,120 | | | | 1,495,394 |

The following table presents additional information about valuation techniques and inputs used for investments that are measured at fair value and categorized within Level 3 as of July 31, 2023:

Asset Type | Fair Value at

July 31, 2023 | Valuation Approach | Significant

Unobservable Inputs | Impact to

value

if Input

Increases* | Range | Weighted

Average |

Preferred Stocks in Private Companies | $6,530,789 | Market Approach | Precedent Transactions

Market Movement | Increase

Increase | N/A

0.7% – 21.69% | N/A

13.76% |

Simple Agreement to Purchase Equity in

Private Companies | 740,120 | Market Approach | Precedent Transactions

Market Movement | Increase

Increase | N/A

22.53% | N/A

22.53% |

Common Stocks in Private Companies | 4,632,310 | Market Approach | Precedent Transactions

Market Movement | Increase

Increase | N/A

3.18% – 21.68% | N/A

9.65% |

See accompanying Notes to Consolidated Financial Statements.

11

Table of Contents

Consolidated Statement of Assets and Liabilities

ARK Venture Fund |

|

July 31, 2023 | |

ASSETS: | |

Investments at market value (Note 2) | $24,708,306 |

Cash | 231,371 |

Receivables: | |

Capital shares sold | 211,295 |

Reimbursement from Adviser | 202,066 |

Investment securities sold | 71,584 |

Dividends | 5,531 |

Total Assets | 25,430,153 |

LIABILITIES: | |

Payables: | |

Investment securities purchased | 254,572 |

Management fees (Note 3) | 52,134 |

Audit and tax fees | 82,000 |

Fund accounting, custody & administration fees | 47,534 |

Transfer agent fees | 18,000 |

Trustee fees | 7,083 |

Shareholder servicing fee | 2,844 |

Other expenses | 47,449 |

Total Liabilities | 511,616 |

NET ASSETS | $24,918,537 |

NET ASSETS CONSIST OF: | |

Paid-in capital | $19,556,182 |

Total distributable earnings | 5,362,355 |

NET ASSETS | $24,918,537 |

Shares outstanding no par value (unlimited shares authorized) | 987,432 |

Net asset value, per share | $ 25.24 |

Investments at cost | $19,560,952 |

See accompanying Notes to Consolidated Financial Statements.

12

Table of Contents

Consolidated Statement of Operations

ARK Venture Fund | |

For the Period Ended July 31, 2023(1) | |

INVESTMENT INCOME: | | |

Dividend income | $ 60,508 | |

Total Income | 60,508 | |

EXPENSES: | | |

Management fees (Note 3) | 315,517 | |

Legal fees | 222,521 | |

Fund accounting, custody & administration fees | 113,036 | |

Audit and tax fees | 82,000 | |

Trustee fees | 70,833 | |

Shareholder servicing fees | 44,919 | |

Registration fees | 41,231 | |

Transfer agent fees | 40,812 | |

Printing & postage | 32,003 | |

Professional fees | 31,000 | |

Credit facility fees | 56,646 | |

Other expenses | 29,853 | |

Total Expenses | 1,080,371 | |

Less expense waivers and reimbursements (Note 3) | (747,644 | ) |

Net Expenses | 332,727 | |

Net Investment Loss | (272,219 | ) |

NET REALIZED AND UNREALIZED GAIN ON INVESTMENTS: | | |

Net realized gain on investments | 487,220 | |

Change in unrealized appreciation on investments | 5,147,354 | |

Net realized and unrealized gain on investments | 5,634,574 | |

Net Increase in Net Assets Resulting From Operations | $5,362,355 | |

(1) For the period September 1, 2022 (commencement of operations) to July 31, 2023.

See accompanying Notes to Consolidated Financial Statements.

13

Table of Contents

Consolidated Statement of Changes in Net Assets

ARK Venture Fund | |

|

For the Period Ended July 31, 2023(1) | | |

OPERATIONS: | | |

Net investment loss | $ (272,219 | ) |

Net realized gain on investments | 487,220 | |

Net change in unrealized appreciation on investments | 5,147,354 | |

Net increase in net assets resulting from operations | 5,362,355 | |

SHAREHOLDER TRANSACTIONS: | | |

Proceeds from shares sold | 21,096,499 | |

Cost of shares repurchased | (1,640,317 | ) |

Net increase in net assets resulting from shareholder transactions | 19,456,182 | |

Increase in net assets | 24,818,537 | |

NET ASSETS: | | |

Beginning of period | 100,000 | |

End of period | $24,918,537 | |

CHANGES IN SHARES OUTSTANDING: | | |

Shares outstanding, beginning of period | 5,000 | |

Shares sold | 1,057,356 | |

Shares redeemed | (74,924 | ) |

Shares outstanding, end of period | 987,432 | |

(1) For the period September 1, 2022 (commencement of operations) to July 31, 2023.

See accompanying Notes to Consolidated Financial Statements.

14

Table of Contents

Consolidated Statement of Cash Flows

ARK Venture Fund | | |

For the Period Ended July 31, 2023(1) | | |

Cash flows used in operating activities: | | |

Net increase in net assets resulting from operations | $ 5,362,355 | |

Adjustments to reconcile net increase in net assets from operations to net cash provided by/(used in) operating activities: | | |

Payments for purchases of investments | (21,824,153 | ) |

Proceeds from sales of investments | 3,146,446 | |

Payments for net purchases of short-term investment securities | (396,025 | ) |

Net realized gain on investments | (487,220 | ) |

Net change in unrealized appreciation on investments | (5,147,354 | ) |

(Increase) decrease in assets: | | |

Proceeds from shares sold | (211,295 | ) |

Reimbursement from Adviser | (202,066 | ) |

Investments securities sold | (71,584 | ) |

Receivable for dividends | (5,531 | ) |

Increase in liabilities: | | |

Management fees | 52,134 | |

Investment securities purchased | 254,572 | |

Audit and tax fees | 82,000 | |

Fund accounting, custody & administration fees | 47,534 | |

Transfer agent fees | 18,000 | |

Trustee fees | 7,083 | |

Shareholder servicing fee | 2,844 | |

Other accrued expenses | 47,449 | |

Net cash used in operating activities | $(19,324,811 | ) |

Cash flows provided by financing activites: | | |

Proceeds from shares sold | $ 21,096,499 | |

Cost of shares repurchased | (1,640,317 | ) |

Net cash provided by financing activities | $ 19,456,182 | |

Net increase in cash | $ 131,371 | |

Cash: | | |

Beginning of period | $ 100,000 | |

End of period | $ 231,371 | |

(1) Represents the period September 1, 2022 (commencement of operations) to July 31, 2023.

See accompanying Notes to Consolidated Financial Statements.

15

Table of Contents

Consolidated Financial Highlights ARK Venture Fund For a share outstanding throughout the period presented. | |

|

| Period Ended

July 31, 2023(1) |

Per Share Data: | |

Net asset value, beginning of period | $ 20.00 |

Net investment loss(2) | (0.43) |

Net realized and unrealized gain on investments | 5.67 |

Total gain from investment operations | 5.24 |

Net asset value, end of period | $ 25.24 |

Total Return at Net Asset Value(3) | 26.20% |

Ratios/Supplemental Data: | |

Net assets, end of period (000’s omitted) | $24,919 |

Ratio to average net assets of: | |

Expenses, prior to expense waivers and reimbursements | 9.33%(4)(5) |

Expenses, net of expense waivers and reimbursements | 2.90%(4)(5) |

Net investment loss | (2.37)%(4)(5) |

Portfolio turnover rate(6) | 27% |

See accompanying Notes to Consolidated Financial Statements.

16

Table of Contents

Notes to Consolidated Financial Statements July 31, 2023 | | |

1. Organization

ARK Venture Fund (the “Fund”) is a non-diversified closed-end management investment company registered under the Investment Company Act of 1940, as amended (“1940 Act”). The Fund was organized as a Delaware statutory trust on January 11, 2022 and commenced operations on September 1, 2022. Prior to September 1, 2022, the Fund had been inactive except for matters relating to the Fund’s organization and accepting initial seed capital. The Fund operates as an “interval fund” and continuously offers its shares of beneficial interest (“Shares”). To provide liquidity, the Fund expects to make quarterly repurchase offers of 5% of the Fund’s outstanding Shares at net asset value pursuant to Rule 23c-3 of the 1940 Act.

The Fund’s investment objective is to seek long-term growth of capital. There can be no assurance that the Fund will achieve its investment objective. The Fund pursues this objective by investing its assets primarily in domestic and foreign equity securities of companies that are relevant to the Fund’s investment theme of disruptive innovation. The Fund may invest, without limit, in privately placed or restricted securities, illiquid securities and securities in which no secondary market is readily available, including those of private companies and publicly traded securities. The Fund may also borrow money for investment purposes.

ARK Investment Management LLC serves as the Fund’s investment adviser (the “Adviser”) under an Investment Advisory Agreement (“Advisory Agreement”).

The Fund had no operations from its initial registration until the Fund’s respective commencement of operations date other than matters relating to its organization and registration and the sale and issuance to ARK Investment Management LLC of 5,000 Shares at an aggregate purchase price of $100,000 in the Fund.

The Fund’s fiscal and tax reporting year ends July 31.

2. Significant Accounting Policies

These consolidated financial statements are prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”), which require management to make estimates and assumptions that affect the reported amount of assets and liabilities, the disclosure of contingent liabilities at the date of the consolidated financial statements, and the reported amount of increase and decrease in net assets from operations during the fiscal period. Actual amounts could differ from these estimates. The Fund is an investment company and follows the investment company accounting standards and reporting guidance under Financial Accounting Standards Board (FASB) Accounting Standard Codification (“ASC”) Topic 946, “Financial Services — Investment Companies”. Rules and interpretive releases of the Securities and Exchange Commission (“SEC”) under authority of federal laws are also sources of authoritative guidance for SEC registrants. The following summarizes the significant accounting policies of the Fund:

Investment Valuation

The values of the Fund’s securities that are traded on a securities market are based on such securities’ closing prices on the principal market on which the securities are traded. Such valuations would typically be categorized as Level 1 in the fair value hierarchy. If a security’s market price is not readily available (as is generally the case with private companies) or does not otherwise accurately reflect the market value of such security, the security will be fair valued by the Adviser which was selected by the Board of Trustees of the Fund (“Board of Trustees”) as valuation designee, to provide such fair values in accordance with the Adviser’s valuation policies and procedures that were reviewed by, and subject to the oversight of, the Board of Trustees. The Fund may use fair value pricing in a variety of circumstances, including but not limited to, situations when the value of the Fund’s security has been materially affected by events occurring after the close of the market on which such security is principally traded (such as a corporate action or other news that may materially affect the price of such security) or trading in such security has been suspended or halted. Such valuations would typically be categorized as Level 2 or Level 3 in the fair value hierarchy. For direct investments in portfolio companies, management primarily uses the market approach to estimate the fair value of private companies. The market approach utilizes prices and other relevant information generated by market transactions, type of security, size of the position, degree of liquidity, restrictions on the disposition, latest round of financing data, current financial position and operating results, among other factors. Because of the uncertainty and judgement involved in the valuation of the portfolio company securities, which do not have a readily available market, the estimated fair value of such securities may be different from values that would have been used had a readily available market existed for such securities. Fair value pricing involves subjective judgments and it is possible that a fair value determination for a security could be materially different than the value that could be realized upon the sale of such security.

Investments in money market fund are valued at their NAV as of the close of each business day.

17

Table of Contents

Notes to Consolidated Financial Statements (continued) July 31, 2023 | |

|

Investment Transactions

Investment transactions are accounted for on the trade date. Realized gains and losses on sales of investment securities are calculated using the identified cost method. Dividend income is recognized on the ex-dividend date, except for certain foreign dividends that may be recorded as soon as such information becomes available. Interest income and expenses are recognized on the accrual basis.

Dividend Distributions

Distributions to shareholders are recorded on the ex-dividend date and are determined in accordance with federal income tax regulations, which may differ from U.S. GAAP. The Fund distributes all or substantially all of its net investment income to shareholders in the form of dividends. Net realized capital gains are distributed to shareholders as capital gain distributions. Net investment income, if any, and net capital gains, if any, are typically distributed to shareholders at least annually. Dividends may be declared and paid more frequently to comply with the distribution requirements of the Internal Revenue Code.

Currency Translation

Assets and liabilities, including investment securities, denominated in currencies other than U.S. dollars are translated into U.S. dollars at the exchange rates supplied by one or more pricing vendors on the valuation date. Purchases and sales of investment securities and income and expenses are translated into U.S. dollars at the exchange rates on the dates of such transactions.

The effects of changes in exchange rates on investment securities are included with the net realized gain or loss and net unrealized appreciation or depreciation on investments in the Fund’s consolidated statement of operations. The realized gain or loss and unrealized appreciation or depreciation resulting from all other transactions denominated in currencies other than U.S. dollars are disclosed separately.

Wholly-owned Subsidiary

The Fund seeks to gain exposure to private companies through ARK Venture Private Holdings LLC, a wholly-owned subsidiary of the Fund (the “Subsidiary”). The Subsidiary is a Delaware limited liability company and the Fund is its sole member. All intercompany transactions and balances have been eliminated in consolidation.

3. Management and Other Agreements

Management

Under the terms of the Advisory Agreement, the Adviser serves as the adviser to the Fund, subject to the general oversight of the Board of Trustees and is responsible for the day-to-day investment management of the Fund. The Fund pays the Adviser a fee calculated daily and payable monthly at an annual rate (stated as a percentage of the average daily net assets of the Fund) of 2.75% (“Management Fee”) in return for providing investment management services.

Organizational and Offering Cost

The Adviser incurred the Fund’s organizational and initial offering costs associated with the Fund’s continuous offering of Shares of $885,178. Pursuant to an expense reimbursement agreement between the Fund and the Adviser, the Fund will be obligated to reimburse the Adviser for any such payments within two years of the Adviser incurring such expenses subject to the limitation that a reimbursement (an “Adviser Reimbursement”) will be made only if and to the extent that: (i) the Fund’s net assets exceed $50,000,000; and (ii) the Adviser Recoupment does not cause the Fund’s net assets to fall below $50,000,000. As of the date of this Report, the Fund’s net assets did not exceed $50,000,000 and therefore the Fund is currently not obligated to reimburse the Adviser for any such payments.

Administrator, Custodian, Transfer Agent and Accounting Agent

The Bank of New York Mellon is the administrator for the Fund, the custodian of the Fund’s assets and also provides transfer agency, fund accounting and various administrative services to the Fund (in each capacity, “Administrator,” “Custodian,” “Transfer Agent” or “Accounting Agent”). The Bank of New York Mellon is a subsidiary of The Bank of New York Mellon Corporation, a financial holding company.

18

Table of Contents

Notes to Consolidated Financial Statements (continued) July 31, 2023 | | |

Distribution

The Fund’s Shares are continuously offered and distributed primarily by Foreside Fund Services, LLC (“Distributor”) and its associated persons through the Titan Platform which is owned by Titan Global Capital Management Inc (“Titan”). The Fund pays to the Distributor a shareholder servicing fee, payable monthly in arrears, at an annual rate of 0.15% of the average daily net assets of the Fund. The Distributor may pay Titan, its broker-dealer and investment adviser subsidiaries and other intermediaries up to the full amount of the shareholder servicing fee. Prior to April 1, 2023, the Fund paid to the Distributor a distribution and/or shareholder servicing fee, payable monthly in arrears, at an annual rate of 0.65% of the average daily net assets of the Fund.

Board of Trustees

Pursuant to the Declaration of Trust and bylaws, the Fund’s business and affairs are managed by the Adviser and subject to the oversight of the Board of Trustees, which has overall responsibility for monitoring and overseeing the Fund’s management and operations. The Board consists of four members, three of whom are considered Independent Trustees. The Trustees are elected by shareholders and are subject to removal or replacement in accordance with Delaware law and the Declaration of Trust. The Trustees serving on the Board were elected by the initial shareholder of the Fund. The Statement of Additional Information provides additional information about the Trustees.

Each Independent Trustee receives an annual retainer fee of $25,000 for services provided as a Trustee of the Fund, plus out-of-pocket expenses related to attendance at Board and Committee Meetings. The Chairs of the Board, Audit and Nominating Committees each also receive an additional annual retainer fee of $5,000, $2,500 and $2,500, respectively, for their service as such.

Line of Credit

On November 15, 2022, the Fund entered into a Credit Facility Agreement (“Facility”) with PNC Bank, National Association. The maximum amount of the borrowing under this Facility is the lesser of $15,000,000 or the sum of (i) 50% of the Fund’s Level 1 securities plus (ii) 100% of the Fund’s unrestricted cash. The purpose of the Facility is primarily to finance, temporarily, the repurchase of Shares of the Fund. The unused balance of the Facility bears commitment fees at an annual interest rate of 0.25%. For the period ended July 31, 2023, the Fund incurred fees on the Facility of $56,646, which includes commitment fees and origination fees as presented within the Consolidated Statement of Operations. The Fund did not borrow under the line of credit agreement during the period ended July 31, 2023.

Expense Limitation Agreement

In March 2023, the Adviser and the Fund entered into an Expense Limitation Agreement under which the Adviser has agreed contractually through November 28, 2024 to waive its Management Fee and/or reimburse the Fund’s operating expenses on a monthly basis to the extent that the Fund’s total annualized fund operating expenses (excluding expenses directly related to the costs of making investments, taxes, brokerage costs, acquired fund fees and expenses, expenses of litigation, indemnification, and shareholder meetings, organizational expenses, offering costs and extraordinary expenses) exceed 2.90% of the Fund’s average daily net assets (“Expense Limit”). The Expense Limitation Agreement went into effect starting April 1, 2023. Pursuant to the Expense Limitation Agreement, the Adviser may receive recoupment of any fees waived and/or excess expense payments paid by it pursuant to the Expense Limitation Agreement within three years of such waiver and/or payment, if such recoupment can be achieved within the Expense Limit or the expense limit that was in effect at the time of the waiver and/or payment, whichever is lower, and such recoupment has been approved by the Board. The Expense Limitation Agreement will remain in effect until at least November 28, 2024, unless and until the Board approves its earlier termination. For the period ended July 31, 2023, the Adviser reimbursed the Fund $747,644 inclusive of the $448,000 voluntary reimbursement discussed below.

Voluntary Reimbursement

On March 31, 2023, the Adviser agreed to voluntarily reimburse the Fund $448,000, which had the effect of lowering the Fund’s net expense ratio from commencement of operations through March 31, 2023, the period before the Expense Limit went into effect, to 2.90% of the Fund’s average daily net assets.

4. Shares of Beneficial Interest

The Fund offers an unlimited number of Shares on a continuous basis. The minimum initial investment by a shareholder for the Shares is $500, while subsequent investments may be made in any amount. The Fund reserves the right to waive the investment minimum. Shares are being offered through the Distributor at an offering price equal to the Fund’s then current NAV per Share.

19

Table of Contents

Notes to Consolidated Financial Statements (continued) July 31, 2023 | |

|

Since meeting the minimum offering requirement and commencing its continuous public offering through July 31, 2023, the Fund raised $1,000,000 of additional seed capital contributed by the Adviser in September 2022 and $2,100,000 in a private placement to feeder vehicles advised by the Adviser created to hold the Fund’s Shares. As of July 31, 2023, the Adviser and feeder vehicles owned 55,454 and 102,338 Shares of the Fund, respectively.

5. Investment Transactions

The cost of purchases and the proceeds from sales of investment securities, excluding short-term obligations, for the period ended July 31, 2023 were $21,824,153 and $3,146,446, respectively.

6. Federal Income Tax

The Fund intends to qualify as a “regulated investment company” under Subchapter M of the Internal Revenue Code of 1986, as amended. If so qualified, the Fund will not be subject to federal income tax to the extent it distributes substantially all of its net investment income and net capital gains to its shareholders. U.S. GAAP provides guidance for how uncertain tax positions should be recognized, measured, presented and disclosed in the consolidated financial statements, and requires the evaluation of tax positions taken or expected to be taken in the course of preparing the Fund’s tax returns to determine whether the tax positions are “more-likely-than-not” to be sustained by the applicable tax authority. Tax positions not deemed to meet the more-likely-than-not threshold would be recorded as a tax benefit or expense in the current year. Interest and penalties related to income taxes would be recorded as income tax expense. The management of the Fund is required to analyze all open tax years, including the year of inception, as defined by IRS statute of limitations, for all major jurisdictions, including federal tax authorities and certain state tax authorities.

As of July 31, 2023, the approximate cost of investments and net unrealized appreciation (depreciation) for federal income tax purposes was as follows:

Fund | Cost | Gross

Unrealized

Appreciation | Gross

Unrealized

Depreciation | Net

Unrealized

Appreciation |

ARK Venture Fund | $19,634,691 | $6,090,364 | $(1,016,749) | $5,073,615 |

The differences between book-basis and tax-basis components of net assets are primarily attributable to passive foreign investment companies, corporate actions and differences in the tax treatment of partnership investments. These adjustments have no impact on net asset values.

At July 31, 2023, the components of distributable earnings (loss) on a tax basis were as follows:

Fund | Undistributed

Income | Undistributed

Long-term

Capital Gains | Accumulated

Capital

Gains/(Losses) | Net Unrealized

Appreciation | Total

Earnings |

ARK Venture Fund | $288,740 | $ — | $ — | $5,073,615 | $5,362,355 |

7. Repurchase Offers

The Fund is an “interval fund,” a type of fund which, to provide some liquidity to Shareholders, intends to make quarterly offers to repurchase between 5% and 25% of its outstanding Shares at NAV, pursuant to Rule 23c-3 under the 1940 Act, unless such offer is suspended or postponed in accordance with regulatory requirements (as discussed below). In connection with any given repurchase offer, the Fund expects to make quarterly repurchase offers of 5% of the Fund’s outstanding Shares at net asset value. Quarterly repurchases occur in the months of March, June, September and December and the Fund made its initial repurchase offer in March 2023. The offer to purchase Shares is a fundamental policy that may not be changed without the vote of the holders of a majority of the Fund’s outstanding voting securities (as defined in the 1940 Act). Written notification of each quarterly repurchase offer (the “Repurchase Offer Notice”) is sent to Shareholders at least 21 and not more than 42 calendar days before the repurchase request deadline (i.e., the date by which Shareholders can tender their Shares in response to a repurchase offer) (the “Repurchase Request Deadline”). The Fund expects to determine the NAV applicable to repurchases on the Repurchase Request Deadline, but it will in any case be calculated no later than the 14th calendar day (or the next business day if the 14th calendar day is not a business day) after the Repurchase Request Deadline (the “Repurchase Pricing Date”). The Fund expects to distribute payment to Shareholders between one and three business days after the Repurchase Pricing Date but it will in any case distribute such payment no later than seven calendar days after such date. The Fund’s Shares are not listed on any securities exchange, and the Fund anticipates that no secondary market will develop for its Shares. Accordingly, you may not be able to sell Shares when and/or in the amount that you desire. Thus, the Shares are appropriate only as a long-term investment. In addition, the Fund’s repurchase offers may subject the Fund and Shareholders to special risks.

20

Table of Contents

Notes to Consolidated Financial Statements (continued) July 31, 2023 | | |

During the period ended July 31, 2023, the Fund completed two quarterly repurchase offers. In these offers, the Fund offered to repurchase up to 5% of the number of its outstanding shares as of the Repurchase Pricing Dates. The results of those repurchase offers were as follows:

| Repurchase

Offer #1 | Repurchase

Offer #2 |

Repurchase Offer Notice | March 9, 2023 | May 26, 2023 |

Repurchase Request Deadline | March 31, 2023 | June 30, 2023 |

Repurchase Pricing Date | March 31, 2023 | June 30, 2023 |

Repurchase Offer Amount | 5.00% | 5.00% |

% of Shares Repurchased | 4.30% | 4.70% |

Shares Repurchased | 33,093 | 41,831 |

8. Indemnification Obligations

The Fund has a variety of indemnification obligations under contracts with their service providers. The Fund’s maximum exposure under these arrangements is unknown. However, the Fund has not had prior claims or losses pursuant to these contracts and expects the risk of loss to be remote.

9. Investment Risks

The Fund’s prospectus contains additional information regarding the risks associated with an investment in the Fund.

Privately Held Company Risk: The Fund invests in privately held companies. Investments in privately held companies involve a number of significant risks, including the following: these companies may have limited financial resources and may be unable to meet their obligations, which may be accompanied by a deterioration in the value of any collateral; they typically have shorter operating histories, narrower product lines and smaller market shares than larger businesses, which tend to render them more vulnerable to competitors’ actions and market conditions, as well as general economic downturns; they typically depend on the management talents and efforts of a small group of persons; there is generally little public information about these companies and these companies and their financial information are not subject to the Securities Exchange Act and other regulations that govern public companies, and there may be an inability to uncover all material information about these companies; they generally have less predictable operating results and may require substantial additional capital to support their operations, finance expansion or maintain their competitive position; changes in laws and regulations, as well as their interpretations, may adversely affect their business, financial structure or prospects; and; they may have difficulty accessing the capital markets to meet future capital needs.

Valuation Risk: Because the Fund may invest a significant portion of its assets in non-publicly traded securities, there will be uncertainty regarding the value of the Fund’s investments, which could adversely affect the determination of the Fund’s net asset value. Accordingly, the Fund should be considered a speculative investment that entails substantial risks, and a prospective investor should invest in the Fund only if they can sustain a complete loss of their investment.

Market Risk: The value of the Fund’s assets will fluctuate as the markets in which the Fund invests fluctuate. The value of the Fund’s investments may decline, sometimes rapidly and unpredictably, simply because of economic changes or other events, such as inflation (or expectations for inflation), deflation (or expectations for deflation), interest rates, global demand for particular products or resources, market instability, debt crises and downgrades, embargoes, tariffs, sanctions and other trade barriers, regulatory events, other governmental trade or market control programs and related geopolitical events. In addition, the value of the Fund’s investments may be negatively affected by the occurrence of global events such as war, terrorism, environmental disasters, natural disasters or events, exchange trading suspensions and closures (including exchanges of the Fund’s underlying securities), infectious disease outbreaks or pandemics.

For example, the outbreak of COVID-19 has negatively affected economies, markets and individual companies throughout the world, including those in which the Fund invests. The effects of this, or any future, pandemic to public health and business and market conditions, including exchange trading suspensions and closures, may have a significant negative impact on the performance of the Fund’s investments, increase the Fund’s volatility, negatively impact the Fund’s arbitrage and pricing mechanisms, exacerbate pre-existing political, social and economic risks to the Fund and negatively impact broad segments of businesses and populations. The Fund’s operations may be interrupted as a result, which may contribute to the negative impact on investment performance. In addition, governments, their regulatory agencies, or self-regulatory organizations have taken or may take actions in response to a pandemic that affect the instruments in which the Fund invests, or the issuers of such instruments, in ways that could have a significant negative impact on the Fund’s investment performance. The ultimate impact of any pandemic and the extent to which the associated conditions and governmental responses impact the Fund will also depend on future developments, which are highly uncertain, difficult to accurately predict and subject to frequent changes.

21

Table of Contents

Notes to Consolidated Financial Statements (concluded) July 31, 2023 | |

|

In February 2022, Russia began engaging in military actions in the sovereign territory of Ukraine. The current political and financial uncertainty surrounding Russia and Ukraine may increase market volatility and the economic risk of investing in securities in these countries and may also cause uncertainty for the global economy and broader financial markets. The ultimate fallout and long-term impact from these events are not known.

Concentration Risk: The Fund’s assets will be concentrated in securities of issuers having their principal business activities in groups of industries in the technology sector. To the extent that the Fund continues to be concentrated in groups of industries in the technology sector, the Fund will be subject to the risk that economic, political, business or other conditions that have a negative effect on such industry groups will negatively impact the Fund to a greater extent than if the Fund’s assets were invested in a wider variety of sectors or industries.

10. New Accounting Pronouncement

In June 2022, the FASB issued Accounting Standards Update (“ASU”) No. 2022-03, Fair Value Measurement (Topic 820): Fair Value Measurement of Equity Securities Subject to Contractual Sale Restrictions. The amendments in this update clarify that a contractual restriction on the sale of an equity security is not considered part of the unit of account of the equity security and, therefore, is not considered in measuring fair value. The amendments also introduce new disclosure requirements related to such equity securities. The ASU is effective for fiscal years beginning after December 15, 2023 and interim periods within those fiscal years. Early adoption is permitted. Management is currently evaluating the impact of this ASU on the Fund’s consolidated financial statements.

11. Subsequent Events

Subsequent events occurring after the date of this Report have been evaluated for potential impact to this Report through the date the Report was issued, and it has been determined that no events have occurred that require disclosure.

22

Table of Contents

Report of Independent Registered Public Accounting Firm

To the Board of Trustees and Shareholders of ARK Venture Fund

Opinion on the Financial Statements

We have audited the accompanying consolidated statement of assets and liabilities of ARK Venture Fund (the “Fund”), including the consolidated schedule of investments, as of July 31, 2023, and the related consolidated statements of operations, changes in net assets, and cash flows and the consolidated financial highlights for the period from September 1, 2022 (commencement of operations) to July 31, 2023 and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the consolidated financial position of the Fund at July 31, 2023, the consolidated results of its operations, changes in its net assets, and cash flows, and its consolidated financial highlights for the period from September 1, 2022 (commencement of operations) to July 31, 2023, in conformity with U.S. generally accepted accounting principles.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audit. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audit in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform, an audit of the Fund’s internal control over financial reporting. As part of our audit, we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audit included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of July 31, 2023, by correspondence with the custodian, brokers and others; when replies were not received from brokers or others, we performed other auditing procedures. Our audit also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audit provides a reasonable basis for our opinion.

/s/ Ernst & Young LLP

We have served as the auditor of one or more of the ARK Invest investment companies since 2022.

New York, New York

September 29, 2023

23

Table of Contents

Supplemental Information (Unaudited) | |

|