Following the date of the Business Combination Agreement, we and our sponsor will use commercially reasonable efforts to enter into additional Non-Redemption Agreements with our public shareholders, pursuant to which our sponsor will be required to forfeit for no consideration 2,000,000 of Class B ordinary shares held by our sponsor. To the extent the aggregate amount of our Class B ordinary shares to be forfeited by our sponsor pursuant to such additional Non-Redemption Agreements is less than 2,000,000, our sponsor will forfeit an additional amount of our Class B ordinary shares on the Closing Date and immediately prior to the First Merger Effective Time, such that our sponsor will forfeit an aggregate of 2,000,000 Class B ordinary shares pursuant to such additional Non-Redemption Agreements and the Sponsor Support Agreement.

In addition, on the terms and subject to the conditions of the Sponsor Support Agreement, following the closing of the Business Combination until 30 days following the expiration of the statute of limitations for the applicable taxes (or if an audit is commenced during this period, until the completion of the audit), subject to the occurrence of certain triggering events, Webull agreed to indemnify our sponsor and each other SPAC Insiders for any U.S. federal (and applicable U.S. state and U.S. local) income taxes, together with any interests and penalties (the “Indemnifiable Amounts”) payable by our sponsor or the other SPAC Insiders, as applicable, solely arising from or attributable to the failure of the Mergers to qualify as a reorganization within the meaning of Section 368(a) of the Internal Revenue Code of 1986, as amended (the “Code”) or as an exchange described in Section 351 of the Code, provided, however, that Webull shall not have any liability in respect of any Indemnifiable Amounts to the extent that the aggregate amount of such Indemnifiable Amounts exceeds $5,000,000.

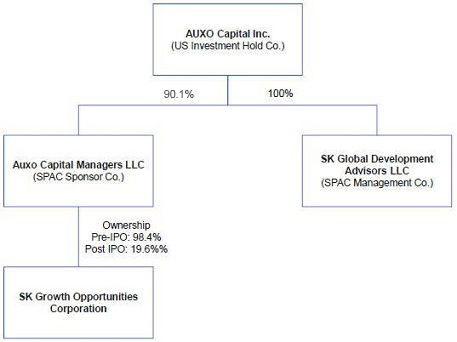

The foregoing description of the Sponsor Support Agreement does not purport to be complete and is qualified in its entirety by the terms and conditions of the Sponsor Support Agreement, a copy of which is filed with our Current Report on Form 8-K filed with the SEC on February 28, 2024 which is incorporated by reference herein.

Going Concern Consideration

As of December 31, 2023, the company had $163,718 in cash and working capital deficit of approximately $6.6 million.

Our liquidity needs prior to the consummation of the initial public offering were satisfied through the payment of $25,000 from our sponsor to purchase founder shares, and loan proceeds from our sponsor of $300,000 under a promissory note, dated December 9, 2021 that was later amended on May 5, 2022 (the “Note”). We repaid the Note in full upon closing of the initial public offering. Subsequent to the consummation of the initial public offering, our liquidity has been satisfied through the net proceeds from the consummation of the initial public offering, the overfunding loans and the private placement held outside of the trust account. In addition, in order to finance transaction costs in connection with a business combination, our sponsor, members of our founding team or any of their affiliates may provide us with working capital loans as may be required (of which up to $1.5 million may be converted at the lender’s option into warrants).

We have incurred and expect to continue to incur significant costs in pursuit of our acquisition plans. In connection with our assessment of going concern considerations in accordance with FASB ASC Topic 205-40, “Presentation of Financial Statements-Going Concern,” we have until September 30, 2024 (or March 31, 2025 as may be approved as described in this Report) to consummate a business combination. It is uncertain that we will be able to consummate a business combination by this time, and if a business combination is not consummated by this date, then there will be a mandatory liquidation and subsequent dissolution of our company.

Our management has determined that the liquidity condition and mandatory liquidation, should a business combination not occur, and potential subsequent dissolution raises substantial doubt about our ability to continue as a going concern for a period of time within one year after the date that the financial statements are issued. Our management plans to address this uncertainty through the initial business combination as discussed above. There is no assurance that our plans to consummate the initial business combination will be successful or successful by September 30, 2024 (or March 31, 2025 as may be approved as described in this Report). The financial statements do not include any adjustments that might result from the outcome of this uncertainty.

Risks and Uncertainties

United States and global markets are experiencing volatility and disruption following the geopolitical instability resulting from the ongoing Russia-Ukraine conflict and the recent escalation of the Israel-Hamas conflict. In response to the ongoing Russia-Ukraine conflict, the North Atlantic Treaty Organization (“NATO”) deployed additional military forces to eastern Europe, and the United States, the United Kingdom, the European Union and other countries have announced various sanctions and restrictive actions against Russia, Belarus and related individuals and entities, including the removal of certain financial institutions from the Society for Worldwide Interbank Financial Telecommunication (SWIFT) payment system. Certain countries, including the United States, have also provided and may continue to provide military aid or other assistance to Ukraine and to Israel, increasing geopolitical tensions among a number of nations. The Russia-Ukraine conflict and the escalation of the Israel-Hamas conflict and the resulting measures that have

75