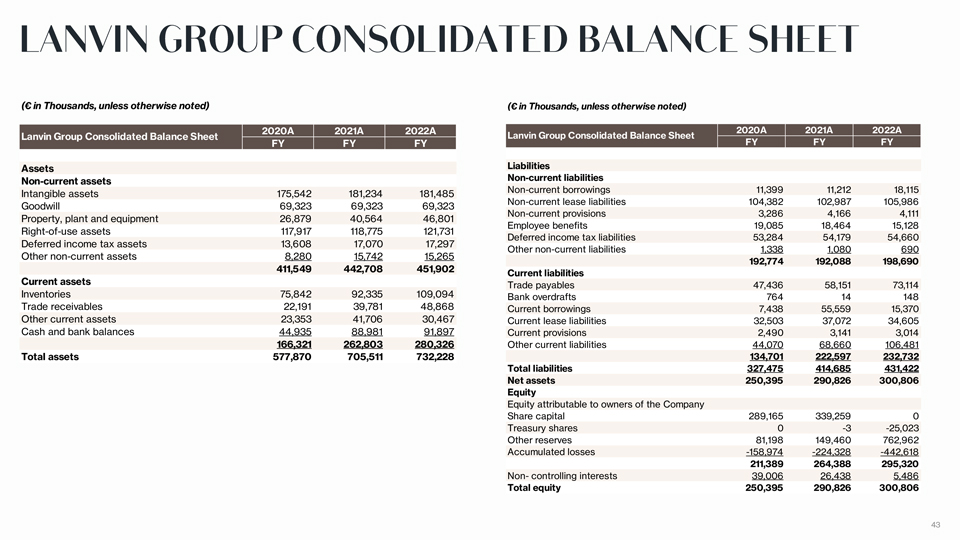

(€ in Thousands, unless otherwise noted) (€ in Thousands, unless otherwise noted) 2020A 2021A 2022A 2020A 2021A 2022A Lanvin Group Consolidated Balance Sheet Lanvin Group Consolidated Balance Sheet FY FY FY FY FY FY Assets Liabilities Non-current assets Non-current liabilities Intangible assets 175,542 181,234 181,485 Non-current borrowings 11,399 11,212 18,115 Goodwill 69,323 69,323 69,323 Non-current lease liabilities 104,382 102,987 105,986 Non-current provisions 3,286 4,166 4,111 Property, plant and equipment 26,879 40,564 46,801 Employee benefits 19,085 18,464 15,128 Right-of-use assets 117,917 118,775 121,731 Deferred income tax liabilities 53,284 54,179 54,660 Deferred income tax assets 13,608 17,070 17,297 Other non-current liabilities 1,338 1,080 690 Other non-current assets 8,280 15,742 15,265 192,774 192,088 198,690 411,549 442,708 451,902 Current liabilities Current assets Trade payables 47,436 58,151 73,114 Inventories 75,842 92,335 109,094 Bank overdrafts 764 14 148 Trade receivables 22,191 39,781 48,868 Current borrowings 7,438 55,559 15,370 Other current assets 23,353 41,706 30,467 Current lease liabilities 32,503 37,072 34,605 Cash and bank balances 44,935 88,981 91,897 Current provisions 2,490 3,141 3,014 166,321 262,803 280,326 Other current liabilities 44,070 68,660 106,481 Total assets 577,870 705,511 732,228 134,701 222,597 232,732 Total liabilities 327,475 414,685 431,422 Net assets 250,395 290,826 300,806 Equity Equity attributable to owners of the Company Share capital 289,165 339,259 0 Treasury shares 0 -3 -25,023 Other reserves 81,198 149,460 762,962 Accumulated losses -158,974 -224,328 -442,618 211,389 264,388 295,320 Non- controlling interests 39,006 26,438 5,486 Total equity 250,395 290,826 300,806 43