As filed with the U.S. Securities and Exchange Commission on November 7, 2023

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

AMPHITRITE DIGITAL INCORPORATED

(Exact name of registrant as specified in its charter)

U.S. Virgin Islands | | 4400 | | 66-1005420 |

(State or other jurisdiction of

incorporation or organization) | | (Primary Standard Industry

Classification Code Number) | | (I.R.S. Employee

Identification Number) |

Amphitrite Digital Incorporated

6501 Red Hook Plaza, Suite 201-465

St. Thomas, Virgin Islands, U.S., 00802

340-642-3895

(Address, including zip code, and telephone with area code, of registrant’s principal executive offices)

Cogency Global Inc.

10 East 40th Street, 10th Floor

New York, New York 10016

212-947-7200

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Brenda Hamilton, Esq. Hamilton & Associates Law Group P.A. 200 East Palmetto Park R. Ste 103 Boca Raton, FL 33432 Telephone: (561) 416-8956 Fax: (561) 416-2855 | Andrew M. Tucker, Esq. Nelson Mullins Riley &

Scarborough LLP 101 Constitution Avenue, NW Washington, DC 20001 Telephone: (202) 689-2800 | Alexander McClean, Esq. C. Christopher Murillo, Esq. Harter Secrest and Emery LLP 1600 Bausch & Lomb Place Rochester, NY 14604 Telephone: (585) 231-6500 Fax: (585) 232-2152 |

Approximate date of commencement of proposed sale to public: As soon as practicable after the effective date hereof.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large, accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | Large accelerated filer | ☐ | Accelerated filer | ☐ |

| | Non-accelerated filer | ☒ | Smaller reporting company | ☒ |

| | Emerging growth company | ☒ | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information contained herein is subject to completion or amendment. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission becomes effective. This prospectus is not an offer to sell, nor does it seek an offer to buy these securities in any state where the offer, solicitation, or sale is not permitted.

PRELIMINARY PROSPECTUS

| SUBJECT TO COMPLETION | DATED November [●], 2023 |

1,904,762 Shares of Common Stock

Amphitrite Digital Incorporated is offering 1,904,762 shares of Common Stock. This is our initial public offering (the “Offering”). We anticipate our public offering price to be between $4.25 and $6.25 per share of Common Stock. Prior to this Offering, there has been no public market for our Common Stock We have applied to list our Common Stock on the Nasdaq Capital Market, or Nasdaq, under the symbols “AMDI”, respectively. No assurance can be given that our application will be approved. If our Common Stock is not approved for listing on Nasdaq, we will not consummate this Offering. We are an “emerging growth company” as that term is used in the Jumpstart Our Business Startups Act of 2012, and we have elected to comply with certain reduced public company reporting requirements. See “PROSPECTUS SUMMARY — Emerging Growth Company Status.”

Investing in our securities involves a high degree of risk. See “RISK FACTORS” beginning on page 20 of this prospectus for a discussion of information that should be considered in connection with an investment in the Common Stock.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

| | | Per Share | | | Total | |

| Initial public offering price | | $ | | | | $ | | |

| Underwriting discounts and commissions(1) | | $ | | | | $ | | |

| Proceeds, before expenses, to us | | $ | | | | $ | | |

| (1) | See “UNDERWRITING” beginning on page 177 of this prospectus for a description of the compensation payable to the underwriters. |

We have granted the underwriters an option, exercisable within 45 days from the date of this prospectus, to purchase from us up to an additional 15% of the shares of Common Stock solely for the purpose of covering over-allotments, if any. If the underwriters exercise the option in full, the total underwriting discounts and commissions payable will be $920,000, and the total proceeds to us, before expenses, will be $10,580,000.

Delivery of the shares of common stock is expected to be made on or about [●], 2023.

Sole Book Running Manager

Maxim Group LLC

The date of this prospectus is [●], 2023

TABLE OF CONTENTS

You should rely only on the information contained in this prospectus. Neither we nor the underwriters have authorized any other person to provide you with information that is different from or adds to that contained in this prospectus. If anyone provides you with different or inconsistent information, you should not rely on it. We take no responsibility for and can provide no assurance as to the reliability of any other information that others may give you. We are offering to sell and seeking offers to buy our Common Stock only in jurisdictions where offers and sales are permitted. You should assume that the information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of our Common Stock. Our business, financial condition, results of operations and prospects may have changed since that date. We are not making an offer of any securities in any jurisdiction in which such offer is unlawful.

Through and including [●], 2023 (25 days after the date of this prospectus), all dealers that effect transactions in our common stock, whether or not participating in this Offering, may be required to deliver a prospectus. This delivery requirement is in addition to the dealer’s obligation to deliver a prospectus when acting as an underwriter and with respect to unsold allotments or subscriptions.

For investors outside the United States: Neither we nor any of the underwriters has done anything that would permit this Offering or possession or distribution of this prospectus or any free writing prospectus we may provide to you in connection with this Offering in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the Offering of the shares of our common stock and the distribution of this prospectus and any such free writing prospectus outside of the United States.

Numerical figures included in this prospectus have been subject to rounding adjustments. Accordingly, numerical figures shown as totals in various tables may not be arithmetic aggregations of the figures that precede them.

STATEMENT REGARDING INDUSTRY AND MARKET DATA

Any market or industry data contained in this prospectus is based on a variety of sources, including internal data and estimates, independent industry publications, government publications, reports by market research firms or other published independent sources. Industry publications and other published sources has been obtained from third-party sources believed to be reliable. Our internal data and estimates are based upon information obtained from trade and business organizations and other contacts in the markets in which we operate and our management’s understanding of industry conditions, and such information has not been verified by any independent sources. Accordingly, investors should not place undue reliance on such data and information.

TRADEMARKS

We have one pending trademark application with the USPTO for “Seas the Day Charters.” We have no other patents or trademarks. This prospectus contains references to trademarks and service marks belonging to other entities. Solely for convenience, trademarks and trade names referred to in this prospectus may appear without the ® or TM symbols, but such references are not intended to indicate, in any way, that the applicable licensor will not assert, to the fullest extent under applicable law, its rights to these trademarks and trade names. We do not intend our use or display of other companies’ trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

PROSPECTUS SUMMARY

This summary highlights selected information that is presented in greater detail elsewhere in this prospectus. Because it is a summary, it does not contain all of the information you should consider before investing in our common stock. You should read this entire prospectus carefully, including the sections titled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and our consolidated financial statements and the related notes included elsewhere in this prospectus, before making an investment decision. Unless the context otherwise requires, the terms “Company,” “we,” “us,” “our,” or similar terms refer to Amphitrite Digital Incorporated together with its consolidated subsidiaries.

Our Business

Our Mission

Our mission is to provide exceptional vacation or staycation tours, activities and attractions to our guests while staying committed to delivering industry leading unique, fun, and educationally memorable experiences. We believe that our boats, yachts and ships are increasingly versatile, allowing consumers to use them for a wide range of maritime based tours and activities that enhance the experience on the water with family and friends. Whether a day, a week, or a lifetime, we provide our guests the “Best Day of Their Vacation.” We believe that the performance, quality, value and multi-purpose features of our maritime vessels, combined with our operating processes and platforms, built from the foundation of best-in-class digital technology, position us to achieve our goal of becoming the market share leader in North America and the Caribbean in the expanding maritime tour activity and attractions market.

Company Overview

We provide award-winning in-destination tours, activities and attractions (“TAA”) in the continental United States and the United States Virgin Islands (“USVI”) using itineraries that feature up-close encounters with marine wildlife, nature, history and culture, and promote guest empowerment and interactivity. We have pioneered innovative ways to allow our guests to connect with exotic and remote places. Many of these maritime expeditions involve travel to top vacation destinations such as the USVI, Panama City Beach, Florida, and Chicago, Illinois. We have been the recipient of TripAdvisor’s 2022 and 2023 Travelers Choice Award, and we were voted the Best Day Sail operation by the Virgin Islands Daily News for 2021 and 2022. We own 14 luxury catamarans and power boats in the USVI, 12 catamaran yachts and power boats in Panama City, Florida, and offer a variety of maritime tours on Lake Michigan from Chicago on the Tall Ship Windy, a 148-foot, traditional four-masted topsail schooner ship designated as the official Tall Ship Ambassador for the City of Chicago.

We anticipate our acquisition of the Paradise Group of Companies (“PGC”) will be completed upon the consummation of this Offering. PGC currently manages and operates privately owned luxury yachts valued at over $55 million. PGC manages and operates 36 luxury yachts in the USVI and British Virgin Islands on behalf of yacht owners, including marketing weeklong, all-inclusive luxury yacht vacations, general yacht management and maintenance, term charter clearing agent services for an additional 12 yachts in the Virgin Islands, and yacht sales brokerage services.

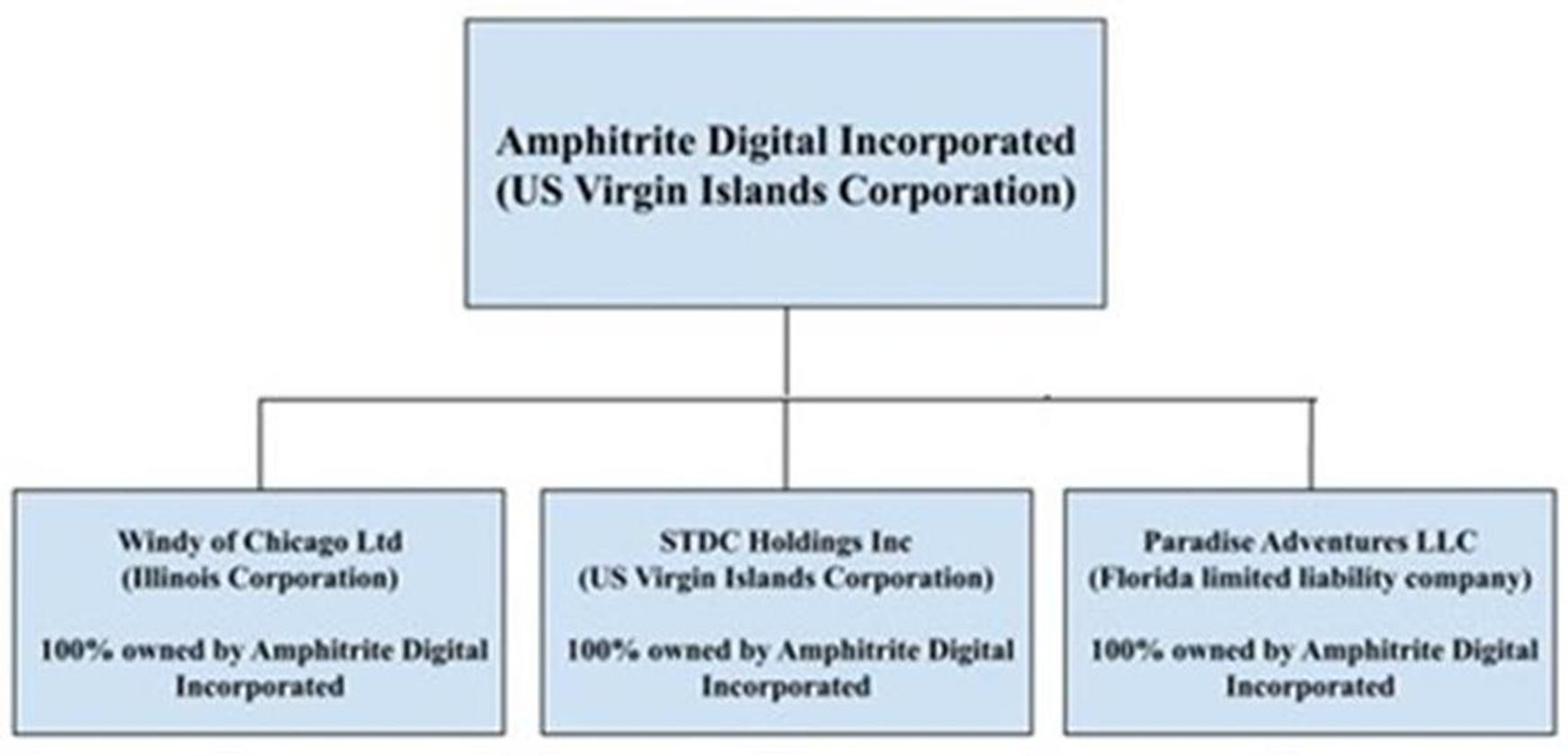

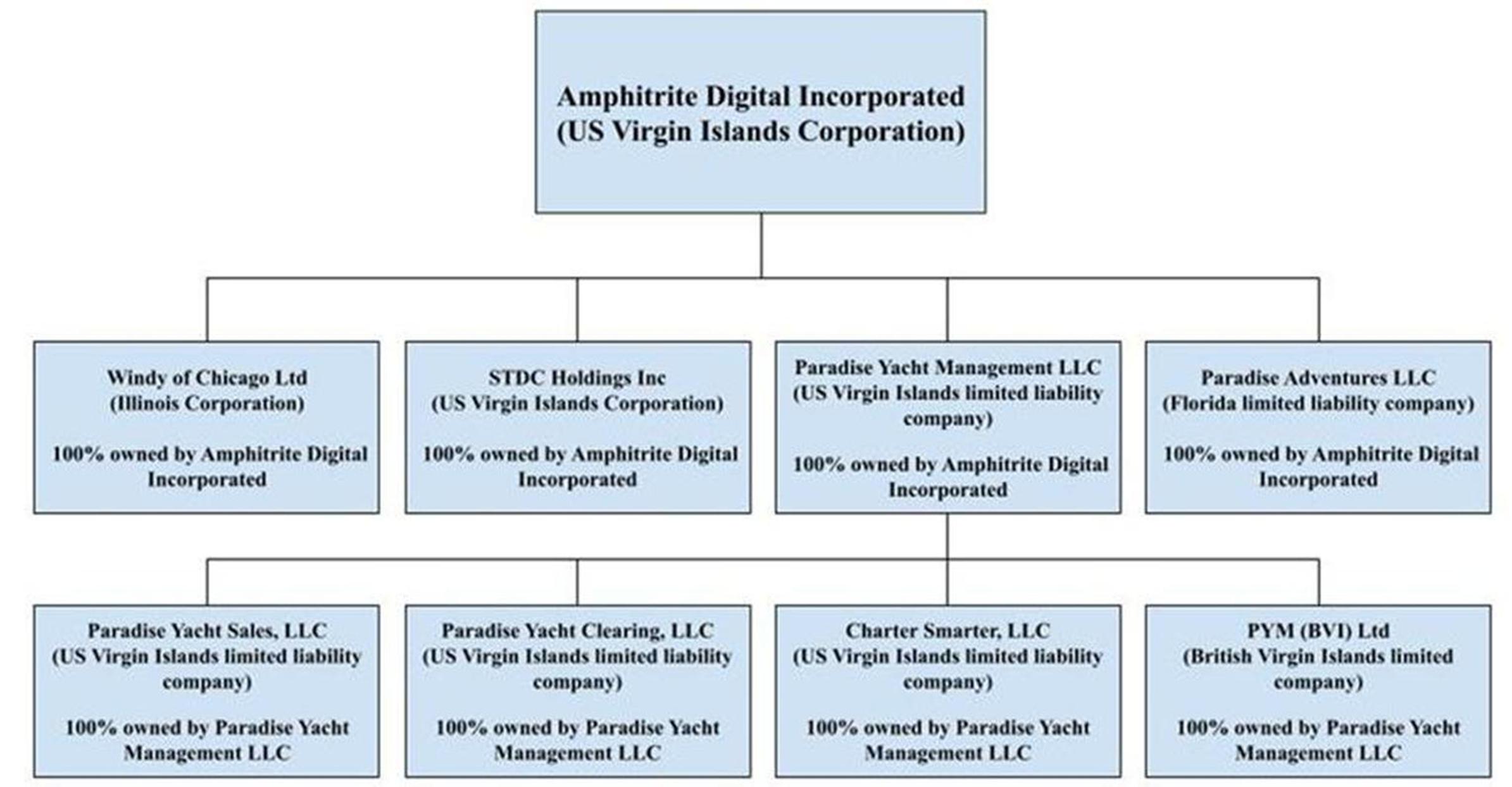

Our operating business units include: 1. Seas the Day Charters USVI and Magens Hideaway on St. Thomas, USVI, through our wholly owned subsidiary, STDC Holdings Incorporated (“STDC Holdings”), a USVI C-corporation, 2. Windy of Chicago, through our wholly owned subsidiary, Windy of Chicago Limited, a corporation formed in Illinois, and 3. Paradise Adventures Catamarans and Watersports in Panama City Beach, Florida, through our wholly owned subsidiary Paradise Adventures LLC, a Florida limited liability company. Additionally, upon the consummation of this Offering, it will include 4. The Paradise Group of Companies in the U.S. and British Virgin Islands, through our anticipated acquisition of PGC. PGC consists of five entities which have common ownership and control. PGC includes Paradise Yacht Management, LLC, formed in July 2015, and its wholly owned subsidiary PYM (BVI) Ltd, formed in May 2022; Paradise Yacht Sales, LLC, formed in November 2019; CharterSmarter, LLC, formed in August 2020; and Paradise Yacht Clearing, LLC, formed in August 2021, (collectively referred to as “PGC” or “Paradise Group of Companies”). Upon our acquisition of PGC upon the closing of this Offering, PGC will become a wholly owned business unit.

In the preceding twelve months ended September 30, 2023, more than 77,000 guests have experienced one of our maritime tours or yacht charters. 5.24 million unique users visited our websites and social media sites to plan their activities. 98% of guest reviews of Amphitrite’s business unit services are positive reviews; 3-star (average) to 5-star (exceptional) reviews. From July 30, 2019 through September 30, 2023 on a cumulative basis, our operating units have received more than 10,100 reviews on major consumer review sites; Google Reviews, TripAdvisor, and Facebook. Of those reviews on a 5-star scale, 95% were 5-star reviews, 2% were 4-star, 1% were 3-star and 2% were 2 or 1-star reviews.

Our principal executive office is located at 6100 Red Hook Qtrs, B1-2, St. Thomas, Virgin Islands 00802. Our telephone number is 312-386-5906. Our customers book our tours through (i) our websites at www.amphitritedigital.com, www.tallshipwindy.com, www.seasthedayusvi.com, www.paradiseadventurespcb.com, www.magenshideaway.com, upon our anticipated acquisition of PGC www.paradiseyachtmanagement.com, and www.chartersmarter.com, (ii) strategic relationships with online travel agents (“OTAs”) to provide optimal guest experiences, revenue generation and operational efficiencies. Our websites are not part of this prospectus.

On July 31, 2022, we completed an SEC Regulation Crowdfunding and sold an aggregate of 650,034 shares of our Common Stock for proceeds of $650,034.

Corporate Structure

Our operations are conducted by our wholly owned subsidiaries. Our corporate structure as of September 30, 2023 is illustrated below:

Our corporate structure after giving effect to the PGC acquisition anticipated to close upon the consummation of this Offering is illustrated below. Upon closing of the PGC acquisition, PYM (BVI) Ltd,, Paradise Yacht Sales LLC, CharterSmarter LLC, and Paradise Yacht Clearing LLC will be wholly owned subsidiaries of Paradise Yacht Management LLC, which in turn will be a wholly owned subsidiary of the Company.

Reorganization and Acquisitions

Our predecessor, Ham and Cheese Events LLC (“HAM”), the Seas the Day business unit (“Seas the Day BU”) commenced operations in April of 2019. HAM, a Texas limited liability company, was formed in March 2012 and controlled by Hope and Scott Stawski, our President and Chairman, respectively. We were formed on April 1, 2022 by Hope and Scott Stawski and Patrick Mullet, our Vice President of Operations. As part of our formation, we formed and acquired two entities:

| ● | On April 1, 2022, we acquired Windy of Chicago Limited, a limited liability company formed in Illinois on March 30, 1995, which owns and operates Tall Ship Windy in Chicago, a 148-foot, traditional four-masted topsail schooner ship, in exchange for a $100,000 loan with interest at the rate of four percent per annum to be paid on or before April 1, 2023, as provided for in a secured promissory note secured by our assets. As of September 30, 2023, we have paid the promissory note in full. |

| | ● | On April 19, 2022, we formed STDC Holdings Incorporated (“STDC Holdings”), a USVI C-corporation, as a wholly owned operating unit to acquire the Seas the Day BU, which includes the boat charter business in the USVI, and does business as Seas the Day Charters USVI, in exchange for the assumption of $1,948,901 of HAM’s debt and payment of $551,098.06 with interest at the rate of four percent per annum to be paid on or before April 1, 2028, as provided for in a secured promissory note secured by our assets. Upon the occurrence and during the continuance of any event of default, all outstanding principal of the secured promissory note shall bear interest at the rate of ten percent per annum. As of September 30, 2023, we have paid $205,100 toward the promissory note, leaving a balance of $345,998, including accrued and unpaid interest. |

In 2023, we expanded our operations with the acquisition of an additional wholly owned subsidiary and anticipate acquiring another wholly owned subsidiary upon the consummation of this Offering:

| | ● | On January 18, 2023, we acquired Paradise Adventures LLC, a Florida limited liability company formed on September 18, 2012, that operates a boat charter and watersports business at the Bluegreen’s Bayside Resort and Spa in Panama City Beach, Florida, and is equipped with a fleet of 12 charter vessels as well as water sports equipment, in exchange for approximately $3,200,000 subject to (a) a cash payment of $755,134 paid upon the closing of the transaction, (b) a promissory note in the amount of $2,075,999 with a simple interest at the rate of 0% percent per annum to be paid at the effective date of this registration statement, (c) a payoff of vessel liens in the amount of $408,040.06, (d) a payment of escrow deposit in the amount of $64,000 and (e) a stock assignment of 300,000 shares of common stock of the Company as provided for in the Assignment and Transfer of Stock Certificate. As of September 30, 2023, the Company has pre-paid $500,000 toward the promissory note leaving a balance of $1,575,999. |

| | ● | On October 18, 2022, we entered into a non-binding Letter of Intent to acquire the Paradise Group of Companies in the U.S. and British Virgin Islands, through our anticipated acquisition of PGC, which consist of five entities which have common ownership and control. PGC includes Paradise Yacht Management, LLC, formed in July 2015, and its wholly owned subsidiary PYM (BVI) Ltd, formed in May 2022; Paradise Yacht Sales, LLC, formed in November 2019; CharterSmarter, LLC, formed in August 2020; and Paradise Yacht Clearing, LLC, formed in August 2021, (collectively referred to as “PGC” or “Paradise Group of Companies”). Upon our acquisition of PGC upon the closing of this Offering, PGC will become a wholly owned business unit. On March 24, 2023 we entered into a Purchase Agreement to acquire said companies, which collectively provide luxury yacht management services and all-inclusive luxury yacht vacations for guests aboard luxury sailing and motor yachts in the Caribbean with a fleet of 36 managed yachts. In addition, PGC also provide ancillary yacht management services which include term charter broker sales activity, term charter clearing agent activity for an additional 12 yachts, yacht sales brokerage services, and yacht maintenance services. On June 6, 2023, we entered into a First Amendment to the Purchase Agreement which extended the closing date to on or before July 31, 2023. On July 31, 2023, we entered into a Second Amendment to the Purchase Agreement which extended the closing date to on or before September 15, 2023 and eliminated “Contingent Consideration” for financial performance for post-acquisition financial periods agreed upon in the initial Purchase Agreement. The purchase price was adjusted to $6,280,000 as the “Base Price” with $3,140,000 to be paid in cash at closing and the remaining balance paid by the issuance of 887,006 shares of the Company’s common stock at a value of $3.54 per share at the date and time of the closing of the transaction or by delivery of a promissory note in the amount of $3,140,000, or for any portion of the balance for which Paradise Yacht Management LLC does not exercise an option to receive the Company’s common stock. On September 15th, 2023, we entered into a Third Amendment to the Purchase Agreement which extended the closing date to on or before October 31, 2023. On November 1, 2023, we entered into a Fourth Amendment to the Purchase Agreement which extended the closing date to on or before December 15th, 2023. We anticipate our acquisition of Paradise Yacht Management LLC to be completed upon the consummation of this Offering. |

Market Opportunity

The TAA market, commonly referred to as in-destination travel, includes tours, activities, attractions & events. This sector of the travel industry is the third largest sector by spending and represents the activities travelers partake ‘in destination’ when they arrive at their location. According to Verified Market Research’s January 2021 Global In-Destination Travel Market Research report, the global in-destination portion of the travel market will reach about $297.6 billion in 2026 from 133.6 US$ Million in 2022, with a CAGR of 17.3%. The North American TAA market is estimated to reach $90 billion according to the same report. The market for activities is highly fragmented with most providers offering a limited range of services at few locations with limited use of technology. We believe an opportunity exists for a well-funded provider to become brand trusted in multiple destinations.

| ● | Fragmentation. The tour activity operator industry is fragmented, with few large, multi-geographic players. This fragmentation results in a lack of efficiency and economy of scale. According to an October 2022 Phocuswright Research report titled ‘The outlook for travel experiences’, “More than eight in 10 operators generate less than $200,000 in annual gross sales.” According to an October 2022 Phocuswright Research publication titled ‘Move to digital gains momentum in tours and activities sector’ not only is the average TAA operator small, with the industry average being $250,000 in revenue, but TAA operators also do not tend to have longevity. 45% of current TAA businesses are less than 7 years old. |

| ● | Technology Adoption. The digital technology revolution has not reached the in-destination tour activity operator industry. Fragmentation and TAA operators with low revenue bases are some of the causes of a low technology adoption rate in the industry. As stated in a September 2018 article published in Skift by Dan Peltier and Andrew Sheivachman, “Nearly every travel sector has leveraged the internet to modernize and give consumers a more convenient booking experience during the past two decades. Tours and activities are a notable exception largely because of global fragmentation.” |

| ● | Value Chain Optimization. Tech-savvy consumers demand digitally enabled ease of use in all rungs of the value chain. For consumers looking for in-destination tours and activities, this includes consumer ease in researching in-destination activities and extends to the booking process and culminates in the activity itself. However, existing TAA operators have not embraced digital technology and the resulting improvements in business processes. According to Skift Research, published in March 2022, titled ‘Tours and Activities Go From Hardest Hit to In Hot Demand This Year: New Survey’, “Not all operators of tours, attractions, and experiences have adapted the latest technologies, which may mean they are leaving some money on the table as consumers switch from walk-up bookings to digital channels.” This digital enablement also extends to the actual tour and activity experience including digital guides, social media value-adds, and on activity virtual enhancement as examples. |

Amphitrite Digital believes we have effectively addressed these opportunities using digital technology for our TAA business operations, including advertising and marketing, guest service, and repair and maintenance resulting in efficiencies not usually seen in this sector.

Our Solutions and Competitive Strengths

We believe our strength is our ability to re-imagine and re-map the traditional TAA operator to a futuristic, digitally enabled operating model. We believe our integrated, digitally enabled operating model allows us to exceed consumer expectations while providing a foundation for both organic growth and the continuation of an acquisition roll-up strategy. Directly addressing the market opportunities of the TAA industry, we believe the following competitive strengths support our core mission:

| ● | Digitally Enabled Business Operating Model. The foundation of our competitive strength is the utilization of digital technology in all aspects of our operations. We refer to this digital foundation as “The Helm.” The Helm is both an operating business model philosophy and an online and app portal, allowing our employees, contractors and associates, including sales affiliates, marketing and advertising companies and key suppliers, to access information and key technology to enhance our performance. We strive to bring this digital technology to the TAA industry, which is characterized by a low technology adoption rate. Our digital operating platform, through our agreements and licenses, is primarily comprised of the following technology service providers. |

We believe our digital enabled business operating model allows us to use technology to more effectively market and book tours, manage resources and improve our operating efficiencies than our competitors. The utilization and integration of this digital technology for specific operating processes critical to the TAA industry we believe gives us competitive advantages. Some examples of areas we ‘digitally enable’ to our competitive advantage include:

Advertising and Marketing. We believe the traditional maritime TAA operator does not use advanced guest acquisition programs that are informed by inventory and revenue management analytics and objectives. We also believe the typical TAA operator does little to no direct digital advertising and instead relies on the online travel agencies (OTAs) for bookings and traditional location-based marketing such as rack-cards driven by discounts. In contrast, we use advanced analytics technology to determine utilization and revenue management metrics at various pivots; vessels, and tour days & time. We then use our advertising campaign management technology to acquire guests that positively affect the underperforming areas of utilization which we have identified; for example a specific tour day & time. In turn this helps us increase our utilization metrics in a targeted manner while using a guest acquisition program which we believe is less expensive than the traditional TAA guest acquisition model. Our direct and online guest acquisition programs achieve a cost of sale of 11.95% compared to the traditional TAA operator relying on OTA bookings paying an estimated 15% to 30% commissions according to Phocuswright in their research report titled, ‘The Outlook for Travel Experiences 2019-2025’.

Customer Service. We believe the traditional TAA operator has limited customer service initiatives due to lack of technology. In our experience, a phone number for the TAA operator is often a cell phone of the owner or operator. Emails, phone calls and text by consumers both before and after the tour will have significant variances in the method and quality of handling. In our experience most TAA operators do not use customer relationship management (CRM) technology to assist with managing a customer’s overall experience. We use digital technology to enable our guest service efforts. We use 8X8 VOIP technology to forward phone calls to a live guest services coordinator, who is available 24/7 including an in-destination/local guest services coordinator during normal tour operating hours. We use advanced reservation management tools provided by Fareharbor to manage reservations real-time by computer or phone app. Saleforce.com has been selected as our CRM enabler to provide a single and central view on the data on our affiliates, concierge partners and guests. This technology is used for guest messaging: inbound and outbound. Our guest management communications is integrated into our campaign management systems for post-tour communication. These guest services technology enablers and processes provide us a competitive advantage over the typical TAA operator that does not provide guest services at this enhanced level. We believe it has contributed to our number of positive reviews, our rankings on Tripadvisor compared to our competitors and our other guest services awards and accolades.

Repair, Maintenance and Resource Management. For maritime TAA operators, managing the resources (vessels) is vital. As an example, vessel utilization rate and specifically available utilization rate is a key performance indicator. Available utilization rate expresses the ratio of calendar days a vessel is available for tours/charter versus unavailable. Our objective is 93.3% available utilization; this equates to 28 days out of 30 days to generate revenue. We believe the typical maritime TAA operator is reactive driven to events like repair and maintenance that negatively affect available utilization rate. Amphitrite uses digital technology including MaxPanda and ServiceFusion to schedule preventative maintenance twice a month (1 day each 15 days of service) and to log, schedule and complete unexpected repairs during scheduled maintenance days or during time periods where the vessel is not scheduled for a tour; i.e. evenings. Equipment content (schematics, parts lists, etc.) is stored digitally on “The Helm” for easy access by captains and crew and repair personnel via their cell phone. This digital repair and maintenance technology also informs our marketing and advertising technology on vessel utilization which influences where we purchase advertising. These and other digital enablers, allow us to manage resources at a higher available utilization rate, as one example, than we believe other maritime TAA operators achieve.

Improve Overall Operations. One of the key performance indicators for operating efficiency is the cost of goods/services sold. Cost of labor, cost of the captain and crew labor for each tour or charter, is a key component of costs of services sold. We believe the typical maritime TAA operator relies primarily on 1099 contractors that are hired seasonally. This is the industry standard which we believe is driven by the inability of TAA operators to both produce valid revenue and utilization projections and to influence guest count or revenue projections using digital marketing channels to achieve a comfort level for an employee hire commitment. In contrast, we strive to utilize full-time, year-round employees for captains and crew which we believe results in several operating efficiencies including cost of services: cost of labor. We can hire full-time captains and crew as we have the technology for proper utilization projections, and we can positively influence utilization when needed to match our labor plan. In addition, other technology enablers assist with providing captains and crew flexible workday arrangements to meet their needs while still benefiting from a full-time employment arrangement.

We believe the three areas above are examples and representative of the competitive advantage created by our digitally enabled business operating model. Other competitive strengths include:

| | ● | Highly Effective Marketing Program. We have a digitally enabled advertising and marketing program that emphasizes online and direct sales and is complementary to our OTA sales channel. To achieve our online and direct sales objective, we use advanced campaign management technology. Campaign management technology such as MarinOne, DiiB and tools by Google, Microsoft and Meta utilize automated routines, integrated data feeds, targeting and segmentation, real-time AI driven learning and programmatic advertising in the design, development, implementation and analysis of guest acquisition programs. Amphitrite utilizes these digitally enabled advertising and marketing programs to acquire guests at a significantly lower cost than the industry average. Our marketing programs resulted in a return on advertising spending (“ROAS”) of 621% for the nine months ended September 30, 2023 for our operating business units of Seas the Day Charters USVI, Windy of Chicago, and Paradise Adventures LLC. For this ROAS calculation, we spent $746,851 on online advertising guest acquisition programs, primarily online search and display advertising buys on Google, Microsoft Audience Network and Meta, to achieve $4,637,947 in online and direct ticket sales. Website and social media traffic for this time period, measured by unique users, was 4.12 million, an increase of 383% year over year for our company-owned websites at tallshipwindy.com, seasthedayusvi.com, and paradiseadventurespcb.com. Our ROAS of 621% for this time period converts to a cost of online and direct revenue of 16.1%. As we believe the typical maritime TAA operator relies primarily on OTAs for guest acquisition paying between 15% and 30% commission, we believe our highly effective marketing programs described above provide us with a competitive advantage in the TAA industry. |

| ● | Unique Maritime Charter and Activity Products and Guest Experience. Since our start in 2018, our wholly owned operations have grown from 1 yacht in St. Thomas, USVI, to 63 owned or managed boats, yachts and ships in the United States and the Caribbean. |

| �� | In the USVI, we own and operate Seas the Day Charters USVI, a luxury day charter and tour operator in St. Thomas and St. John. Seas the Day Charters USVI owns and operates 6 luxury catamaran yachts, 5 luxury power yachts and 3 runabout power boats, Offering a variety of day sail activities, including private charters, beach and snorkeling excursions, and island-hopping adventures. |

| | ○ | In the Caribbean, we expect to manage and operate the Paradise Group of Companies, the leading multi-day luxury yacht charter operation in the Leeward Islands. We anticipate our acquisition of the Paradise Group of Companies to be completed upon the consummation of this Offering. Operating out of the USVI and the British Virgin Islands, the Paradise Group of Companies manages and markets 36 privately owned luxury yachts with a market value of over $55 million and provides yacht clearing agent services for an additional 12 yachts. The Paradise Group of Companies specializes in week-long, luxury ‘crewed’ yacht charters with destinations throughout the Leeward Islands. |

| ○ | In Florida, we own and operate Paradise Adventures Catamarans and Watersports from the Bluegreen’s Bayside Resort and Spa in Panama City Beach, Florida. The Paradise Adventures fleet of all company-owned vessels includes 2 catamarans, 1 monohull luxury sailing yacht, 2 powerboats, 7 pontoon boats and 1 work barge for a variety of excursions, including sightseeing, dolphin tours, snorkeling, watersports and private parties. |

| ○ | On Lake Michigan, we own and operate Windy of Chicago Ltd, which owns and operates Tall Ship Windy. Tall Ship Windy is the Official Tall Ship Ambassador for the City of Chicago; designated and commended by Mayor Richard Daly and the Chicago City Council in 2006. The Tall Ship Windy sails daily from Navy Pier in Chicago from May through September and offers skyline sails, sunset sails, fireworks sails, as well as a premium location for weddings, private parties and full ship charters for corporate events. |

| ○ | In St. Thomas, USVI, we sublease Magens Hideaway, a luxury villa and bed and breakfast Offering land and sea vacations and activities to its guests. Magens Hideaway comprises three buildings surrounding a quietly bubbling fountain and tropical garden views in the traditional Caribbean Danish architectural style. Accommodating 14 guests, the luxury property sits atop Peterborg peninsula on St. Thomas and overlooks Magens Bay on the south side and the British Virgin Islands on its north side. |

| | ● | Company-owned Marketing and Distribution Channels. Our key marketing philosophy is to own the predominance of our guest acquisition and retention channels. Our primary marketing objective is to utilize our digitally enabled advertising and marketing to drive sales through our company-owned websites (tallshipwindy.com, seasthedayusvi.com, paradiseadventurespcb.com, paradiseyachtmanagement.com, chartersmarter.com, and magenshideaway.com) and direct bookings, as this channel powered by our digitally-enabled online advertising has the lowest cost of sale at 16.1% for the nine months ended September 30, 2023. |

| | ○ | We have made substantial progress with fully automating the charter and activity booking process by utilizing best of class digital reservation technologies, API linkages, transparent pricing strategies, effective automated customer service tools, and improved multi-channel communication. The company has completed and implemented fully automated, self-service websites and reservation platforms for the business units of Seas the Day Charters USVI, Windy of Chicago and Paradise Adventures. The company completed and implemented a fully automated, self-service reservation website and platform for the Paradise Group of Companies on September 1, 2023; www.chartersmarter.com. |

| | ○ | Company-owned websites, direct ticket sales and other non-OTA channels represented 69% of our revenue in the nine months ended September 30, 2023. We will strive to grow revenue by emphasizing online and direct bookings at a cost of sale lower than the OTA channel provides. We believe OTA channels typically charge between a 15% to a 30% commission, the continued movement of sales to company-owned online and direct sales channels at an 16.1% cost of sale is a competitive advantage. |

| | ○ | Recognizing that OTAs will continue to play an important role in the sector, we continue to develop strategic relationships with certain OTAs, including Expedia, TripAdvisor, TripShock and GetYourGuide, which represented 31% of our revenue in the nine months ended September 30, 2023. Our primary OTA provider, Viator, represented 26% of revenue for the nine months ended September 30, 2023. Viator through its online travel agency websites including TripAdvisor.com and Viator.com promotes and sells the company’s tours. We anticipate that strategic partnerships with global and regional OTAs will continue to augment our primary direct channel. |

| ● | Highly Experienced Management Team. Our management team consists of highly skilled technology, marketing and hospitality professionals. See “Management” beginning on page 144 of this prospectus for a detailed discussion of our management team. |

| ○ | Scott Stawski, our co-Founder and Executive Chairman of the Board of Directors is a recognized digital technology thought leader. He has served in various executive roles at leading technology companies including DXC Technology (NYSE: DXC) and its predecessor company Hewlett Packard. Mr. Stawski authored Inflection Point – How the Convergence of Cloud, Mobility, Apps and Data Will Shape the Future of Business, which was published and distributed globally by Pearson FT Press in 2015. In 2019, McGraw-Hill published his second book, The Power of Mandate – How Visionary Leaders Keep Their Organization Focused on What Matters Most. |

| | ○ | Rob Chapple, our Chief Executive Officer and Director has over 25 years of experience in leading marketing and business operations in various industries. Since January 2020, Mr. Chapple served as the co-founder and chief customer officer of New York-based Esellas, a revenue performance management company. Prior to that, from 2017 to 2019, Mr. Chapple served as the chief revenue officer for Civis Analytics, a Google Eric Schmidt backed venture, where he helped create new data analytics product strategies and go to market initiatives. Mr. Chapple held various global management roles from 2001 until 2017 with Hewlett Packard Enterprise Services and its predecessor EDS. |

| ○ | Hope Stawski, our co-Founder, President and Director is an accomplished hospitality executive with many years in management positions at ARAMARK, Hyatt-Regency and other leading hospitality companies. Hope Stawski leads the guest services and day-to-day charter operations of the company and has proven invaluable in developing our award-winning guest experience program. She is also deeply involved in all aspects of recruitment, merchandising and special events. |

| ○ | Patrick Mullett, our co-Founder, Vice President of Operations and Director, is a seasoned hospitality executive, most recently VP of Operations for Margaritaville Caribbean Group, responsible for the opening and management of Jimmy Buffett’s Margaritaville restaurants in the Caribbean. Pat Mullett is responsible for the daily operations in the Caribbean. |

| ○ | Amphitrite Digital has an independent Board of Directors consisting of financial, merger and acquisition, technology, hospitality and safety experts who are a source of valuable counsel and oversight to the company. |

Growth Strategy

The in-destination tour activities and attractions industry is highly fragmented with a low technology adoption rate. According to a November 2023 Phocuswright Conference article titled, ‘The Future of Experiences: Tours, Activities, Attractions’, “Tours, activities and attractions (TAA) is perhaps the most diverse and fragmented sector in the global tourism industry. It is also the least understood and studied.” According to a Tourwriter article titled, ‘The travel industry is resilient,’ the industry has proven to be highly resilient and has rapidly rebounded after global crises. According to an October 2022 Phocuswright Research titled, ‘The outlook for travel experiences’, “Gross industry revenue will surpass 2019 by 2024, when global gross bookings will reach $260 billion.”

With increasing global and North American consumer spending on tours, activities and attractions, and the increased need for a digitally optimized business operating model in the TAA industry, the company believes that the market opportunity in this space will be best captured by TAA operators who embrace digital technology as an enabler to their major business processes. Key elements of our growth strategy include:

| ● | Customer Segment Targets. Our marketing objective is to focus on obtaining guests using our digitally enabled operations without discounting. The customer segments we actively target include: |

| ○ | Consumer Vacationers: Individuals and families planning and conducting vacations in the geographies we serve; |

| ○ | Consumer Staycationers: Individuals and families residing in the geographies we serve; and |

| ○ | Businesses and Business Groups. Businesses and business groups desiring to have corporate events in the growing geographies we serve. |

| ● | Organic Growth in Existing Geographies. We plan to grow our operations solely in North America and the Caribbean over the next 5 years. We believe a 15% market share for maritime tours and activities in each geography entered achieves the economies of scale and operational efficiency to maximize profitability. In each geography entered, we will continue to use our competitive strength in digitally enabled guest acquisition to achieve this target. In the near term, we will continue to work on organic growth to achieve our market share goals in Chicago, Panama City Beach, Florida and the Virgin Islands. |

| ● | Acquisition / Roll-up Strategy. The TAA industry is fragmented, and current operators have a low technology adoption. According to an October 2022 Phocuswright Research titled, ‘The outlook for travel experiences’ discussed above, “Tour and attraction operators, which have historically lagged in digital adoption, may cede ground in online market share to faster- moving OTAs.” These challenges present an opportunity for us to pursue an acquisition roll-up strategy. We have successfully acquired TAA operators in Chicago, Florida and the Caribbean. The company has an active acquisition pipeline and it is the company’s intent to complete further acquisitions in the next twelve months. |

IMPLICATIONS OF BEING AN EMERGING GROWTH COMPANY

AND A SMALLER REPORTING COMPANY

We qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, as amended, or the JOBS Act. As an emerging growth company, we may take advantage of specified reduced disclosure and other requirements that are otherwise applicable generally to public companies. These provisions include:

| | ● | only two years of audited financial statements in addition to any required unaudited interim financial statements with correspondingly reduced “Management’s Discussion and Analysis of Financial Condition and Results of Operations” disclosure; |

| | | |

| | ● | reduced disclosure about our executive compensation arrangements; |

| | | |

| | ● | no non-binding advisory votes on executive compensation or golden parachute arrangements; and |

| | | |

| | ● | exemption from the auditor attestation requirement in the assessment of our internal control over financial reporting. |

We may take advantage of these exemptions for up to five years or such earlier time that we are no longer an emerging growth company. We would cease to be an emerging growth company on the date that is the earliest of (i) the last day of the fiscal year in which we have total annual gross revenues of $1.235 billion or more; (ii) the last day of our fiscal year following the fifth anniversary of the date of the completion of this Offering; (iii) the date on which we have issued more than $1 billion in nonconvertible debt during the previous three years; or (iv) the date on which we are deemed to be a large accelerated filer under the rules of the SEC. We may choose to take advantage of some but not all of these exemptions. We have taken advantage of reduced reporting requirements in this prospectus. Accordingly, the information contained herein may be different from the information you receive from other public companies in which you hold stock. Additionally, the JOBS Act provides that an emerging growth company can take advantage of an extended transition period for complying with new or revised accounting standards. This allows an emerging growth company to delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. We have elected to avail ourselves of this exemption and, therefore, while we are an emerging growth company, we will not be subject to new or revised accounting standards at the same time that they become applicable to other public companies that are not emerging growth companies.

We are also a “smaller reporting company” as defined in the Securities Exchange Act of 1934, as amended (the “Exchange Act”). We may continue to be a smaller reporting company even after we are no longer an emerging growth company. We may take advantage of certain of the scaled disclosures available to smaller reporting companies until the fiscal year following the determination that our voting and non-voting common stock held by non-affiliates is greater than $250 million measured on the last business day of our second fiscal quarter, or our annual revenues are less than $100 million during the most recently completed fiscal year and our voting and non-voting common stock held by non-affiliates is more than $700 million measured on the last business day of our second fiscal quarter.

SUMMARY RISK FACTORS

| | ● | Scott Stawski, our co-Founder, Executive Chairman and Chief Revenue Officer, and Hope Stawski, our co-Founder and President, are husband and wife collectively hold approximately 57.8% of our Common Stock as of September 30, 2023 and will collectively hold 49.7% of our Common Stock post this Offering, giving them the ability to influence the outcome of director elections and other matters requiring stockholder approval. |

| | ● | We depend on our executive officers, particularly Scott and Hope Stawski, our co-Founder, Executive Chairman, and Chief Revenue Officer and co-Founder and President, Rob Chapple, our CEO and other key employees, and the loss of one or more of these employees could materially adversely affect our business. |

| ● | Our Articles of Incorporation provide that we will indemnify our directors and officers to the fullest extent permitted by law. |

| ● | Our management will have broad discretion over the use of the proceeds we receive in this Offering and might not apply the proceeds in ways that increase the value of your investment. |

| ● | Financial Industry Regulatory Authority (“FINRA”) sales practice requirements may limit a stockholder’s ability to buy and sell our stock. |

| | ● | Future sales of our Common Stock, warrants, or securities convertible into our Common Stock may depress our stock price. |

| | ● | We may, in the future, issue additional securities, which would reduce investors’ percentage of ownership and dilute the value of your investment in our Common Stock. |

| | ● | No active trading market for our Common Stock currently exists, and an active trading market may not develop or be sustained following this Offering. |

| | ● | The prices of our securities may be volatile, which could subject us to securities class action litigation and prevent you from being able to sell your shares at or above the Offering price. |

| | ● | If you purchase shares in this Offering, you will suffer immediate dilution of your investment. |

| | ● | We have not and do not expect to declare any cash dividends to our stockholders in the foreseeable future. |

| | ● | Once listed on Nasdaq, our failure to meet the continued listing requirements of Nasdaq could result in a delisting of our Common Stock. |

| | ● | An active, liquid and orderly trading market for our Common Stock may not develop, the price of our stock may be volatile, and you could lose all or part of your investment. |

| | ● | We are an “emerging growth company,” and we cannot be certain if the reduced reporting and disclosure requirements applicable to emerging growth companies will make our Common Stock less attractive to investors. |

| | ● | If we are unable to establish appropriate internal financial reporting controls and procedures, it could cause us to fail to meet our reporting obligations, resulting in the restatement of our financial statements, harm our operating results, subject us to regulatory scrutiny and sanction, cause investors to lose confidence in our reported financial information and have a negative effect on the market price for shares of our Common Stock. |

| | ● | We will incur increased costs and demands upon management as a result of complying with the laws and regulations affecting public companies, which could adversely affect our operating results. |

| | ● | The financial and operational projections that we may make from time to time are subject to inherent risks. |

| | ● | If securities or industry analysts do not publish research or publish unfavorable or inaccurate research about our business, the market price and trading volume of our Common Stock could decline. |

| ● | Instances of foodborne illness and outbreaks of disease, as well as negative publicity relating thereto, could result in reduced demand for our menu offerings and negatively impact our business. |

| ● | We may not be able to achieve our financial and climate-related performance goals. |

| ● | The potential unavailability of insurance coverage, an inability to obtain insurance coverage at commercially reasonable rates or our failure to have coverage in sufficient amounts to cover our incurred losses may adversely affect our financial condition or results of operations. |

| ● | Litigation, enforcement actions, fines or penalties could adversely impact our financial condition or results of operations and/or damage our reputation. |

CORPORATE INFORMATION

We are incorporated under the laws of the United States Virgin Islands on April 1, 2022. Our principal executive office is located at 6100 Red Hook Qtrs, B1-2, St. Thomas, Virgin Islands 00802. Our phone number is 312-386-5906. Our website address is www.amphitritedigital.com. We do not incorporate the information on or accessible through our website as part of this prospectus. We have included our website address in this prospectus solely as an inactive textual reference.

THE OFFERING

The following summary of the Offering contains basic information about the Offering and our securities and is not intended to be complete. It does not contain all the information that is important to you. For a more complete understanding of our securities, please refer to the section of this prospectus entitled “DESCRIPTION OF SECURITIES.”

| Common Stock offered by us | | We are offering 1,904,762 shares of Common Stock. |

| | | |

| Public Offering Price | | The assumed public offering price is between $4.25 and $6.25 per share of Common Stock. |

| | | |

| Common Stock outstanding before this Offering(1) | | 11,685,279 shares of Common Stock |

| | | |

| Common Stock outstanding after this Offering(1) | | 13,590,041 shares of Common Stock or 13,875,755 shares if the underwriters exercise their over-allotment option in full, and assuming in each case, no exercise of the Underwriters’ Warrants. |

| | | |

| Over-allotment option | | The underwriters have an option for a period of 45 days to purchase from us up to an additional 15% of the shares of Common Stock sold in this public Offering solely for the purpose of covering over-allotments, if any. |

| | | |

| Use of Proceeds | | We expect to receive approximately $8,500,000 net proceeds from this Offering (approximately $9,880,000 if the underwriters exercise their over-allotment option in full), assuming an Offering price of $5.25 per share of Common Stock, the midpoint of the price range set forth on the cover page of this prospectus, after deducting estimated underwriting discounts and commissions and estimated Offering expenses payable by us. We plan to use the proceeds of the Offering for a pending acquisition, debt retirement for a prior acquisition, technology development, marketing program expansion, executive and management recruitment, future acquisitions, and general working capital. Please see “USE OF PROCEEDS” on page 54 of this prospectus for a more complete description of the intended use of proceeds from this Offering. |

| Underwriters’ Warrants(2) | | Upon the closing of this Offering, we have agreed to sell to the representative of the underwriters of this Offering, or its permitted designees, for nominal consideration, warrants to purchase 8% of the shares of Common Stock sold in this Offering as additional consideration to the underwriters in this Offering. The Underwriters’ Warrants will have an exercise price equal to 100% of the public Offering price in this Offering and shall be exercisable commencing six (6) months after the effective date of the registration statement related to this Offering, and will expire five years after the commencement of sales of this Offering. The Underwriters’ Warrants will contain customary anti-dilution, “cashless” exercise and registration rights provisions. For additional information regarding our arrangement with the underwriters, please see “UNDERWRITING.” |

| | | |

| Risk Factors | | Investing in our securities is highly speculative and involves a high degree of risk. You should carefully consider the information set forth in this prospectus and, in particular, the specific factors set forth in the “RISK FACTORS” section beginning on page 20 of this prospectus before deciding whether or not to invest in our securities. |

| Proposed Nasdaq Ticker Symbol | | We have applied to list our Common Stock on the Nasdaq Capital Market, or Nasdaq, under the symbol “AMDI.” No assurance can be given that our application will be approved. If our Common Stock is not approved for listing on Nasdaq, we will not consummate this Offering. |

| | | |

| Lockups | | We and our directors, officers, and holders of 1% of our outstanding securities have agreed with the underwriters not to offer for sale, issue, sell, contract to sell, pledge or otherwise dispose of any of the Common Stock for a period of 180 days from the effectiveness of this registration statement., in the case of our company and our officers and directors. See “UNDERWRITING” on page 177. |

| (1) | The number of shares of Common Stock outstanding after this Offering, as set forth in the table above, is based on 11,685,279 shares of the Common Stock outstanding as of the date of this prospectus, which excludes, as of that date, (i) outstanding options to purchase 1,821,736 shares of the Common Stock granted but unvested as of the date of this Offering pursuant to our Incentive Plans adopted on April 1, 2022 (the “Plan”) (ii) options to purchase 1,927,431 shares of our Common Stock available for future issuance under the Plan and (iii) Underwriters’ Warrants will not be exercisable for six (6) months from the effective date of this Registration Statement and will expire five (5) years from such date entitling the underwriters to purchase 8% of the number of shares of the Common Stock sold in this Offering, at an exercise price equal to 100% of the public offering price. For additional information regarding our arrangement with the underwriters, please see “UNDERWRITING.” |

| (2) | The actual shares of Common Stock and Underwriters’ Warrants that we will offer and that will be outstanding after this Offering will be determined based on the actual public offering price. |

SUMMARY CONSOLIDATED FINANCIAL DATA

The following summary financial data have been derived from the Company’s (i) unaudited consolidated financial statements included elsewhere in this prospectus as of September 30, 2023 and for nine months ended September 30, 2023 and 2022 and (ii) audited financial statements as of and for the years ended December 31, 2022 and 2021 that are included elsewhere in this prospectus. The financial statements have been prepared and presented in accordance with U.S. GAAP. The results for the nine months ended September 30, 2023 are not necessarily indicative of the results expected for a full year or for future periods. In the opinion of the Company’s management, the unaudited consolidated financial statements for interim periods include all adjustments consisting of normal recurring adjustments necessary for a fair statement of the results for such interim periods. This summary financial information should be read in conjunction with the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations”, “Unaudited Pro Forma Consolidated Financial Information” and the Company’s audited consolidated financial statements and the related notes included elsewhere in this prospectus.

| | | For the

Nine Months Ended

September 30, | | | For the

Year Ended

December 31, | |

| (in USD dollars) | | 2023 | | | 2022 | | | 2022 | | | 2021 | |

| | | (unaudited) | | | (audited) | |

| Consolidated Statements of Operations Data: | | | | | | | | | | | | |

| Revenue | | $ | 6,993,366 | | | $ | 4,508,743 | | | $ | 4,591,690 | | | $ | 2,059,001 | |

| Cost of revenue | | $ | 4,187,746 | | | $ | 2,450,688 | | | $ | 3,791,356 | | | $ | 1,633,373 | |

| Operating loss | | $ | (2,702,803 | ) | | $ | (1,272,960 | ) | | $ | (2,594,886 | ) | | $ | 100,901 | |

| Net loss | | $ | (4,342,250 | ) | | $ | (1,647,792 | ) | | $ | (3,010,701 | ) | | $ | 72,624 | |

| | | As of

September 30, | | | As of

December 31, | |

| (in USD dollars) | | 2023 | | | 2022 | | | 2021 | |

| | | (unaudited) | | | (audited) | |

| Consolidated Balance Sheet Data: | | | | | | | | | | | | |

| Cash (includes restricted cash) | | $ | 62,000 | | | $ | 134,868 | | | $ | 1,027 | |

| Total Assets | | $ | 8,810,419 | | | $ | 4,904,395 | | | $ | 1,681,162 | |

| Total Liabilities | | $ | 10,631,529 | | | $ | 6,222,817 | | | $ | 1,864,218 | |

| Working Capital (deficit)(1) | | $ | (5,862,772 | ) | | $ | (1,616,875 | ) | | $ | (487,248 | ) |

| (1) | Working capital deficit is defined as the difference between current assets and current liabilities including acquisition debt to be paid with use of proceeds from this Offering. |

Certain Non-GAAP Financial Measures

Amphitrite uses Adjusted EBITDA to identify and target operational results which is beneficial to management and investors in evaluating operational effectiveness. Adjusted EBITDA is a supplemental measure of the Company’s performance that is not required by, or presented in accordance with, U.S. GAAP. Adjusted EBITDA is not a measurement of Amphitrite’s financial performance under U.S. GAAP and should not be considered as an alternative to net income (loss) or any other performance measure derived in accordance with U.S. GAAP. Amphitrite’s calculation of this non-GAAP financial measure may differ from similarly titled non-GAAP measures, if any, reported by other companies. This non-GAAP financial measure should not be considered in isolation from, or as a substitute for, financial information prepared in accordance with U.S. GAAP.

Non-GAAP financial measures have limitations in their usefulness to investors because they have no standardized meaning prescribed by GAAP and are not prepared under any comprehensive set of accounting rules or principles. In addition, non-GAAP financial measures may be calculated differently from, and therefore may not be directly comparable to, similarly titled measures used by other companies.

Amphitrite presents Adjusted EBITDA because it considers this measure to be an important supplemental measure of its performance and believes it is frequently used by securities analysts, investors, and other interested parties in the evaluation of companies in its industry. Management believes that investors’ understanding of the Company’s performance is enhanced by including this non-GAAP financial measure as a reasonable basis for comparing its ongoing results of operations.

Amphitrite calculates Adjusted EBITDA as net income (loss) adjusted for depreciation and amortization, interest expense, income tax expense, share-based compensation expenses, legal settlements, non-recurring expenses related to acquisitions, and transaction expenses related to this offering.

The following table presents a reconciliation of Adjusted EBITDA to loss for each of the periods indicated.

| | | Nine Months Ended

September 30, | | | Year End

December 31, | |

| (in USD dollars) | | 2023 | | | 2022 | | | 2022 | | | 2021 | |

| Net loss | | $ | (4,342,250 | ) | | $ | (1,647,792 | ) | | $ | (3,010,701 | ) | | $ | 72,624 | |

| Addback: | | | | | | | | | | | | | | | | |

| Depreciation and amortization | | | 742,392 | | | | 410,637 | | | | 587,922 | | | | 230,448 | |

| Interest expense | | | 1,634,266 | | | | 145,665 | | | | 190,249 | | | | 44,555 | |

| Income tax expense (benefit) | | | | | | | | | | | | | | | | |

| Settlements(1) | | | | | | | 250,000 | | | | 250,000 | | | | | |

| Share-based compensation expense(2) | | | 1,720,244 | | | | 1,242,500 | | | | 1,654,546 | | | | | |

| Non-recurring expenses related to acquisitions(3) | | | 836,898 | | | | 467,881 | | | | 562,348 | | | | | |

| Transaction costs(4) | | | 425,000 | | | | 115,000 | | | | 220,000 | | | | | |

| Adjusted EBITDA | | $ | 1,016,550 | | | $ | 983,891 | | | $ | 454,364 | | | $ | 347,627 | |

| (1) | Represents an adjustment for a non-recurring legal settlement for $250,000. |

| (2) | Represents non-cash expenses related to equity-based compensation programs used primarily for employee retention incentives related to acquisitions, which vary from period to period depending on various factors including the timing, number, and the valuation of awards. |

| (3) | Represents non-recurring expenses related to the acquisition of Paradise Adventures LLC in January 2023, the pending acquisition of the Paradise Group of Companies to close with this Offering and the acquisition of Windy of Chicago Ltd in January 2022. |

| (4) | Represents costs related to a public company transaction, including accounting, legal, and listing costs. |

SUMMARY UNAUDITED PRO FORMA CONSOLIDATED FINANCIAL INFORMATION

The summary unaudited pro forma consolidated financial data of the Company presented below has been derived from our unaudited pro forma consolidated financial statements included elsewhere in this prospectus. The summary unaudited pro forma consolidated financial data give effect to the acquisition of Paradise Adventures LLC on January 18, 2023, the pending acquisition of the Paradise Group of Companies to occur with the use of proceeds described in “Our Organizational Structure” and “Use of Proceeds,” and the financial impact of this Offering.

The summary unaudited pro forma condensed combined statement of operations for the nine months ended September 30, 2023, and for the year ended December 31, 2022, gives effect to the of acquisition of Paradise Adventures LLC on January 18, 2023 as if it had occurred on January 1, 2022. The summary unaudited pro forma condensed combined balance sheet as of September 30, 2023, gives effect to the acquisition of the Paradise Group of Companies, to occur with the Use of Proceeds from this Offering, as if it had occurred on September 30, 2023. The summary unaudited pro forma condensed combined statement of operations for the nine months ended September 30, 2023, and for the year ended December 31, 2022, gives effect to the of acquisition of the Paradise Group of Companies, to occur with the Use of Proceeds from this Offering, as if it had occurred on January 1, 2022. The summary unaudited pro forma condensed combined balance sheet as of September 30, 2023, gives effect to the financial impact of this Offering, as if it had occurred on September 30, 2023. The summary unaudited pro forma condensed combined statement of operations for the nine months ended September 30, 2023, and for the year ended December 31, 2022, gives effect to the financial impact of this Offering, as if it had occurred on January 1, 2022.

The unaudited pro forma consolidated statement of operations for the year ended December 31, 2022 combines figures derived from the separate audited consolidated statement of operations of our Company, Paradise Adventures LLC and The Paradise Group of Companies’ audited consolidated statement of operations for the year ended December 31, 2022. The unaudited pro forma consolidated financial information includes various estimates which are subject to material change and may not be indicative of what our operations or financial position would have been had this Offering and related transactions taken place on the dates indicated, or that may be expected to occur in the future.

Our historical results presented herein are not necessarily indicative or predictive of results in any future period. In our opinion, any unaudited financial and non-GAAP measurements presented herein represent a fair presentation of such financial data. We recommend reading the following information in conjunction with “Capitalization,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” “Business” and our consolidated financial statements and related footnotes included in this prospectus. Refer to “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Non-GAAP Financial Measures” for further discussion of the use of the below non-GAAP financial measures.

This summary pro forma financial information should be read in conjunction with the section entitled “Unaudited Pro Forma Consolidated Financial Information” and the related notes included elsewhere in this prospectus.

| (in USD dollars) | | As of

September 30,

2023 | |

| Unaudited Pro Forma Consolidated Balance Sheet Data: | | | | |

| Cash | | $ | 5,459,691 | |

| Total Assets | | $ | 20,448,923 | |

| Total Liabilities | | $ | 9,237,193 | |

| Total shareholders’ equity | | $ | 11,211,730 | |

| | | For the

Nine Months Ended

September 30, | | | For the

Year Ended

December 31, | |

| (in USD dollars) | | 2023 | | | 2022 | |

| | | (unaudited) | | | | |

| Unaudited Pro Forma Consolidated Statements of Operations Data: | | | | | | | | |

| Revenue | | $ | 13,798,594 | | | $ | 17,159,436 | |

| Cost of revenue, including vessel depreciation expense | | $ | 9,272,635 | | | $ | 13,394,526 | |

| Operating profit (loss) | | $ | (2,648,186 | ) | | $ | (2,808,502 | ) |

| Net profit (loss) | | $ | (2,710,983 | ) | | $ | (2,904,581 | ) |

| Weighted average shares outstanding – basic and diluted | | $ | 12,943,158 | | | $ | 10,419,532 | |

| Net profit (loss) per share – basic and diluted | | $ | (0.21 | ) | | $ | (0.28 | ) |

RISK FACTORS

An investment in our securities involves a high degree of risk. In addition to the other information contained in this prospectus, the following risks have the potential to impact our business and operations. These risk factors are not exhaustive, and all investors are encouraged to perform their own investigation with respect to our business, financial condition and prospects. The occurrence of any of the following risks or additional risks and uncertainties not presently known to us or that we currently believe are immaterial could have a material adverse effect on our business, financial condition, results of operations and future growth prospects. The trading price of our securities could decline due to any of these risks, and, as a result, you may lose all or part of your investment.

Macroeconomic, Business, Market and Operational Risks

Adverse economic or other conditions could reduce the demand for maritime vessels and passenger spending, adversely impacting our operating results, cash flows and financial condition including impairing the value of our goodwill, ships, trademarks and other assets and potentially affecting other critical accounting estimates where the impact may be material to our operating results.

Demand for maritime vessels is affected by international, national, and local economic conditions. Weak or uncertain economic conditions may impact consumer confidence and pose a risk as vacationers postpone or reduce discretionary spending. This, in turn, may result in cruise booking slowdowns, decreased cruise prices and lower onboard revenues. Given the global nature of our business, we are exposed to many different economies, and our business could be negatively impacted by challenging conditions in any of the markets in which we operate, and/or related reactions by our competitors in such markets.

Our operating costs could increase due to market forces and economic or geopolitical factors beyond our control.

Our operating costs, including fuel, food, payroll and benefits, airfare, taxes, insurance, and security costs, can be and have been subject to increases due to market forces and economic or geopolitical conditions or other factors beyond our control, including global inflationary pressures, which have increased our operating costs. Increases in these operating costs have affected, and may continue to adversely affect, our future profitability.

In particular, increases in fuel prices have and could continue to materially and adversely affect our business as fuel prices impact not only our fuel costs, but also some of our other expenses, such as crew travel, freight, and commodity prices. Mandatory fuel restrictions may also create uncertainty related to the price and availability of certain fuel types potentially impacting operating costs.

Price increases for commercial airline services for our guests or major changes or reduction in commercial airline services and/or availability could adversely impact the demand for cruises and undermine our ability to provide reasonably priced vacation packages to our guests.

Many of our guests depend on scheduled commercial airline services to transport them to or from the ports where our maritime tours embark or disembark. Increases in the price of airfare would increase the overall price of the vacation to our guests, which may adversely impact demand for our tours and excursions. In addition, changes in the availability and/or regulations governing commercial airline services could adversely affect our guests’ ability to obtain air travel, as well as our ability to transfer our guests to or from our cruise ships, which could adversely affect our results of operations.

Terrorist attacks, war, and other similar events could have a material adverse impact on our business and results of operations.

We are susceptible to a wide range of adverse events, including terrorist attacks, war, conflicts, civil unrest and other hostilities. The occurrence of these events or an escalation in the frequency or severity of them, and the resulting political instability, travel restrictions and advisories and concerns over safety and security aspects of traveling or the fear of any of the foregoing, have had, and could have in the future, a significant adverse impact on demand and pricing in the travel and vacation industry. These events could also result in additional security measures taken by local authorities which have, and may in the future, impact access to ports and/or destinations. In addition, such events have led, and could lead, to disruptions, instability and volatility in global markets, supply chains and industries, increased operating costs, such as fuel and food, and disruptions affecting fleet modernization efforts, any of which could materially and adversely impact our business and results of operations. Further, such events could have the effect of heightening the other risks we have described in this report, any of which also could materially and adversely affect our business and results of operations.

Events and conditions around the world, including war and other military actions, such as the invasion of Ukraine, and, more recently, the Israel-Hamas war, have heightened inflation and other general concerns impacting the ability or desire of people to travel, have led, and may in the future lead, to a decline in demand for travel, impacting our operating costs and profitability.

We have been, and may continue to be, impacted by the public’s concerns regarding the health, safety and security of travel, including government travel advisories and travel restrictions, political instability and civil unrest, terrorist attacks, war and military action, most recently the Israel-Hamas war, including its spread into a broader regional conflict and escalating geopolitical tensions as a result thereof, the invasion of Ukraine, and other general concerns. The Israel-Hamas war and the conflict between Russia and Ukraine and its resulting impacts, including supply chain disruptions, increased fuel prices and international sanctions and other measures that have been imposed, have adversely affected, and may continue to adversely affect, our business. These factors may also have the effect of heightening many other risks to our business, any of which could materially and adversely affect our business and results of operations. Additionally, we have been, and may continue to be, impacted by heightened regulations around customs and border control, travel bans to and from certain geographical areas, voluntary changes to our itineraries in light of geopolitical events, government policies increasing the difficulty of travel and limitations on issuing international travel visas. We have been, and may continue to be, impacted by inflation and supply chain disruptions and may also be impacted by adverse changes in the perceived or actual economic climate, such as global or regional recessions, higher unemployment and underemployment rates and declines in income levels.