File No. 333-267866

Per Class S Share | Per Class D Share | Per Class I Share | Total | |||||

| Public Offering Price(1) | Current NAV | Current NAV | Current NAV | Amount invested at NAV | ||||

| Sales Load(2) | None | None | None | |||||

| Proceeds to the Fund | Current NAV | Current NAV | Current NAV | Amount invested at NAV |

| (1) | J.P. Morgan Institutional Investments Inc. (the “Distributor”), an affiliate of the Adviser, acts as principal underwriter for the Fund’s Shares and serves in that capacity on a reasonable best efforts basis, subject to various conditions. The Distributor is not obligated to sell any specific number of shares, nor have arrangements been made to place shareholders’ funds in escrow, trust, or similar arrangement. Class S Shares, Class D Shares and Class I Shares are or will be continuously offered at a price per share equal to the NAV per share for such class. Each share class will initially be offered at $10 per share. Generally, the stated minimum investment by an investor in the Fund is $25,000 with respect to Class S Shares and Class D Shares and $1,000,000 with respect to Class I Shares. The stated minimum investment for Class I Shares may be reduced for certain investors as described under “Purchasing Shares.” The minimum additional investment in the Fund is $10,000. The Fund may, in its sole discretion, accept investments below these minimums. Investors subscribing through a given broker/dealer or registered investment adviser may have shares aggregated to meet these minimums, so long as initial investments are not less than $25,000 and incremental contributions are not less than $10,000. |

| (2) | No upfront sales load will be paid with respect to Class S Shares, Class D Shares or Class I Shares, however, if you buy Class S Shares or Class D Shares through certain financial intermediaries, they may directly charge you transaction or other fees, including upfront placement fees or brokerage commissions, in such amount as they may determine, provided that financial intermediaries limit such charges to a 1.5% cap on NAV for Class D Shares and a 3.5% cap on NAV for Class S Shares. Financial intermediaries will not charge such fees on Class I Shares. Your financial intermediary may impose additional charges when you purchase Shares of the Fund. Please consult your financial intermediary for additional information. |

| • | The Fund has no operating history. |

| • | Shares are not listed on any securities exchange, and it is not anticipated that a secondary market for Shares will develop. Shares are subject to limitations on transferability, and liquidity will be provided only through limited repurchase offers. Although the Fund may offer to repurchase Shares from time to time, Shares will not be redeemable at an investor’s option nor will they be exchangeable for shares of any other fund. As a result, an investor may not be able to sell or otherwise liquidate his or her Shares. The Adviser intends to recommend that, in normal market circumstances, the Fund’s Board of Trustees conduct quarterly repurchase offers of no more than 5% of the Fund’s net assets. |

| • | An investment in the Fund may not be suitable for investors who may need the money they invested in a specified timeframe. |

| • | Shares are subject to substantial restrictions on transferability and resale and may not be transferred or resold except as permitted under the Fund’s agreement and declaration of trust. |

| • | The amount of distributions that the Fund may pay, if any, is uncertain. |

| • | The Fund may pay distributions in significant part from sources that may not be available in the future and that are unrelated to the Fund’s performance, such as the sale of assets, borrowings, return of capital, offering proceeds or from temporary waivers or expense reimbursements borne by the Adviser or its affiliates that may be subject to reimbursement to the Adviser or its affiliates. |

Page | ||||

| 1 | ||||

| 26 | ||||

| 28 | ||||

| 28 | ||||

| 29 | ||||

| 33 | ||||

| 35 | ||||

| 35 | ||||

6 1 | ||||

| 70 | ||||

| 73 | ||||

| 76 | ||||

| 79 | ||||

| 80 | ||||

| 81 | ||||

| 85 | ||||

| 85 | ||||

| 86 | ||||

| 88 | ||||

| 89 | ||||

| 89 | ||||

| 90 | ||||

| 92 | ||||

| 95 | ||||

| 108 | ||||

| 108 | ||||

| 108 | ||||

| 109 | ||||

| 110 | ||||

| 111 | ||||

The Fund | The Fund is a newly organized Delaware statutory trust that is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as a non-diversified, closed-end management investment company with no operating history. The Fund will sell its Shares of beneficial interest (“Shares”) only to eligible investors that are both “accredited investors,” as defined in Section 501(a) of Regulation D under the Securities Act of 1933, as amended (the “Securities Act”), and “qualified clients” as defined in Rule205-3 under the Investment Advisers Act of 1940, as amended (the “Advisers Act”). |

The Fund has received an exemptive order from the Securities and Exchange Commission (the “SEC”) that permits the Fund to offer multiple classes of shares. The Fund will offer three separate classes of Shares designated as Class S, Class D and Class I Shares. Each class of Shares is subject to different fees and expenses. The Fund may offer additional classes of Shares in the future. |

The business operations of the Fund are managed and supervised under the direction of the Fund’s Board of Trustees (the “Board”), subject to the laws of the State of Delaware and the Fund’s Declaration of Trust. The Board is comprised of four trustees, a majority of whom are not “interested persons” (as defined in the 1940 Act) of the Fund (“Independent Trustees”). The Board has overall responsibility for the management and supervision of the business operations of the Fund. |

The Investment Adviser | J.P. Morgan Investment Management Inc., an investment adviser registered with the SEC under the Advisers Act, serves as the Fund’s investment adviser. |

Investment Objective and Strategy | The Fund’s investment objective is to seek to provide long-term capital appreciation. In pursuing its investment objective, the Fund intends to invest primarily in an actively managed portfolio of private equity and other private assets (collectively, “private market investments”). The Fund’s private market investments focus on private equity strategies including private equity and venture capital. The Fund’s investment exposure to these strategies is implemented via a variety of investment types that include: (i) investments in private equity funds managed by various unaffiliated asset managers (“Portfolio Funds”) acquired in privately negotiated |

transactions (a) from investors in these Portfolio Funds, and/or (b) in connection with a restructuring transaction of a Portfolio Fund(s) (“Secondary Investments”); (ii) indirect investments in the equity of private companies, alongside private equity funds and/or other private equity firms via special purpose vehicles (“Co-Investments”); and (iii) primary investments in newly formed Portfolio Funds (“Primary Investments”). The Fund expects to invest principally in Secondary Investments,Co-Investments and Primary Investments, although the allocation among those types of investments and other investments may vary from time to time. |

To manage portfolio liquidity, the Fund may also have exposure to privately placed debt securities and other yield-oriented investments, including without limitation 144A securities, syndicated and other floating rate senior secured loans issued in private placements by U.S. and foreign corporations, partnerships and other business entities, privately placed bank loans, restricted securities, and other securities and instruments issued in transactions exempt from the registration requirements of the Securities Act (“Private Credit Investments”). The Fund may invest in Private Credit Investments indirectly through investment vehicles, including but not limited to affiliated or unaffiliated mutual funds and ETFs. |

The Adviser manages the Fund’s asset allocation and private equity investment decisions with a view towards managing liquidity and maintaining a high level of investment in private markets. The Fund’s asset allocation and amount of private market investments may be based, in part, on anticipated future distributions from private market investments. The Adviser may also take other anticipated cash flows into account, such as those relating to new subscriptions into the Fund, the repurchase of Shares through periodic tenders by members of the Fund (“Shareholders”) and any distributions made to Shareholders. To forecast portfolio cash flows, the Adviser utilizes quantitative and qualitative factors, including historical private equity data, actual portfolio observations and qualitative forecasts by the Adviser. |

To manage the liquidity of its investment portfolio, the Fund also invests a portion of its assets in a portfolio of short-term debt securities, affiliated and unaffiliated money market securities, cash and/or cash equivalents (“Liquid Assets”). The Fund may invest in one or more money market funds advised by the Adviser or its affiliates (affiliated money market funds). The Adviser has contractually agreed to waive fees and/or reimburse expenses in an amount sufficient to offset the respective net advisory fees it collects from the affiliated money market funds on the Fund’s investment in such money market funds. To enhance the Fund’s liquidity, particularly in |

times of possible net outflows through the repurchase of Shares by periodic tender offers to Shareholders, the Fund may sell certain of its assets. The Fund seeks to hold an amount of Liquid Assets and other liquid investments consistent with prudent liquidity management. During normal market conditions, it is generally not expected that the Fund will hold more than 20% of its net assets in Liquid Assets for extended periods of time. For temporary defensive purposes, liquidity management or in connection with implementing changes in the asset allocation, the Fund may hold a substantially higher amount of Liquid Assets and other liquid investments. |

Under normal circumstances, the Fund invests at least 80% of its net assets (plus the amount of any borrowings for investment purposes) in private market investments. For purposes of this policy, private market investments include Secondary Investments; Co-Investments; Primary Investments; and Private Credit Investments. |

The Fund is permitted to borrow money or issue debt securities in an amount up to 33 1/3% of its total assets in accordance with the 1940 Act. The Fund may establish one or more credit lines to borrow money for a range of purposes, including to provide liquidity for capital calls by Portfolio Funds and Co-Investments, to satisfy tender requests, to manage timing issues in connection with the inflows of additional capital and to otherwise satisfy Fund obligations, or for investment purposes. There is no assurance, however, that the Fund will be able to enter into a credit line or that it will be able to timely repay any borrowings under such credit line, which may result in the Fund incurring leverage on its portfolio investments from time to time. The Fund’s use of leverage may increase or decrease from time to time in its discretion and the Fund may, in the future, determine not to use leverage. See “Risks—The Fund may be subject to leverage risk. |

The Fund may have exposure to companies and funds that are organized or headquartered or have substantial sales or operations outside of the United States, its territories, and possessions, including emerging market countries. The Fund may make investments directly or indirectly through one or more wholly-owned subsidiaries (each, a “Subsidiary” and collectively, the “Subsidiaries”). The Fund may form a Subsidiary in order to pursue its investment objective and strategies in a potentially tax-efficient manner or for the purpose of facilitating its use of permitted borrowings. Except as otherwise provided, references to the Fund’s investments also will refer to any Subsidiary’s investments. |

The Fund’s asset allocation and amount of private market investments may be based, in part, on anticipated future capital calls and distributions from such investments. This |

| There can be no assurance that the Fund’s investment objective will be achieved or that the Fund’s investment program will be successful. |

Principal Risk Factors | The following are certain principal risk factors that relate to the operations and terms of the Fund. These considerations, which do not purport to be a complete description of any of the particular risks referred to or a complete list of all risks involved in an investment in the Fund, should be carefully evaluated before determining whether to invest in the Fund. The Fund’s investment program is speculative and entails substantial risks. The following risks may be directly applicable to the Fund or may be indirectly applicable through the Fund’s private market investments. In considering participation in the Fund, prospective investors should be aware of certain principal risk factors, including the following: |

Risks of Investing in Private Market Investments |

Risks of Private Equity Strategies |

Less information may be available with respect to private company investments and such investments offer limited liquidity |

| operating results, may from time to time be parties to litigation, may be engaged in rapidly changing businesses with products subject to a substantial risk of obsolescence, and may require substantial additional capital to support their operations, finance expansion or maintain their competitive position. In addition, investments in private companies generally are in restricted securities that are not traded in public markets and subject to substantial holding periods. There can be no assurance that the Fund will be able to realize the value of such investments in a timely manner. |

Private equity investments are subject to general market risks |

Competition for access to private equity investment opportunities is limited |

In addition, certain provisions of the 1940 Act prohibit the Fund from engaging in transactions with the Adviser and its affiliates; however, unregistered funds also managed by the Adviser are not prohibited from the same transactions. The 1940 Act also imposes significant limits on co-investments with affiliates of the Fund. The Adviser will not cause the Fund to engage in investments alongside affiliates in private placement securities that involve the negotiation of certain terms of the private placement securities to be purchased (other than price-related terms) unless the Fund has received an order granting an exemption from Section 17 of the 1940 Act or unless such investments are not prohibited by Section 17(d) of the 1940 Act or interpretations of Section 17(d) as expressed in SEC no-action letters or other available guidance. Once the Adviser and the Fund receive an exemptive order from the SEC to engage in certain privately negotiated investments, the order will expand the Fund’s ability to co-invest alongside its affiliates. However, the exemptive order will contain certain conditions that may limit or restrict the Fund’s ability to participate in such negotiated investments or participate in such negotiated investments to a lesser extent. An inability to receive the desired allocation to potential investments may affect Fund’s ability to achieve the desired investment returns. |

The Fund is subject to the risks of its Portfolio Funds |

| Portfolio Fund interests are ordinarily valued based upon valuations provided by the manager or general partner of a Portfolio Fund (a “Portfolio Fund Manager”), which may be received on a delayed basis. Certain securities in which the Portfolio Funds invest may not have a readily ascertainable market price and are fair valued by the Portfolio Fund Managers. The Adviser will review and perform due diligence on the valuation procedures used by each Portfolio Fund Manager and monitor the returns provided by the Portfolio Funds. However, neither the Adviser nor the Board is able to confirm the accuracy of valuations provided by Portfolio Fund Managers. |

| The Fund will pay asset-based fees, and, in most cases, will be subject to performance-based fees in respect of its interests in Portfolio Funds. Such fees and performance-based compensation are in addition to the Advisory Fee and Incentive Fee. In addition, performance-based fees charged by Portfolio Fund Managers may create incentives for the Portfolio Fund Managers to make risky investments, and may be payable by the Fund to a Portfolio Fund Manager based on a Portfolio Fund’s positive returns even if the Fund’s overall returns are negative. Moreover, a Shareholder in the Fund will indirectly bear a proportionate share of the fees and expenses of the Portfolio Funds, in addition to its proportionate share of the expenses of the Fund. |

The Fund is subject to the risks associated with its Portfolio Funds’ underlying investments. |

The Fund may have limited Secondary Investment opportunities |

| Portfolio Funds by acquiring the interests in the Portfolio Funds from existing investors in such Portfolio Funds. In such instances, it is generally not expected that the Fund will have the opportunity to negotiate the terms of the interests being acquired, other than the purchase price, or other special rights or privileges. Moreover, there is no assurance that the Fund will be able to purchase interests at attractive discounts to net asset value, or at all. The overall performance of the Fund will depend in large part on the acquisition price paid by the Fund for its Secondary Investments, the structure of such acquisitions and the overall success of the Portfolio Fund. |

| There is significant competition for Secondary Investments. No assurance can be given that the Fund will be able to identify Secondary Investments that satisfy the Fund’s investment objective or, if the Fund is successful in identifying such Secondary Investments, that the Fund will be permitted to invest, or invest in the amounts desired, in such Secondary Investments. |

Regulatory Changes may adversely affect private equity funds |

In-kind distributions from Portfolio Funds may not be liquid |

The Fund’s Co-Investments may be subject to risks associated with the lead investor |

| negotiate the terms of such Co-Investments. The Fund’s ability to dispose of Co-Investments may be severely limited. |

The Fund may have limited Co-Investment opportunities Co-Investments. Furthermore, many competitors are not subject to the regulatory restrictions that the 1940 Act imposes on the Fund. As a result of this competition and regulatory restrictions, the Fund may not be able to pursue attractive Co-Investment opportunities from time to time. |

| The Fund will be subject to additional risks associated with different investments, including its investments in Liquid Assets. For information about those risks, see “Other Investment Risks” and “Other Risks” under the “Risks” section starting on page 39 of the Prospectus. |

General Risks of Investing in the Fund |

The Fund and the Portfolio Funds are subject to risks associated with market and economic downturns and movements non-U.S. jurisdictions in which its investments operate, including factors affecting interest rates, the availability of credit, currency exchange rates and trade barriers. These factors are outside the control of the Adviser and could adversely affect the liquidity and value of the Fund’s investments and reduce the ability of the Fund to make new investments. |

The Fund has no operating history non-diversified, closed-end management investment company with no operating history. While members of the Adviser’s Private Equity Group who will be active in managing the Fund’s investments have substantial experience in private market investments, the Fund was recently formed, does not yet have any operating history and has not made any investments. |

The Fund is subject to conflicts of interest |

for which the Fund compensates them. As a result, the Adviser and/or its affiliates have an incentive to enter into arrangements with the Fund, and face conflicts of interest when balancing that incentive against the best interests of the Fund. The Adviser and/or its affiliates also face conflicts of interest in their service as investment adviser to other clients, and, from time to time, make investment decisions that differ from and/or negatively impact those made by the Adviser on behalf of the Fund. In addition, affiliates of the Adviser provide a broad range of services and products to their clients and are major participants in the global currency, equity, commodity, fixed-income and other markets. In certain circumstances, by providing services and products to their clients, these affiliates’ activities will disadvantage or restrict the Fund and/or benefit these affiliates and may result in the Fund forgoing certain investments that it would otherwise make. The Adviser may also acquire material non-public information which would negatively affect the Adviser’s ability to transact in securities for the Fund. See “Potential Conflicts of Interest” below. |

The Board may change the Fund’s investment objective and strategies without Shareholder approval |

The Fund is actively managed and subject to management risk Co-Investments and other portfolio investments representing various strategies, geographic regions, asset classes and sectors may vary significantly over time based on the Adviser’s analysis and judgment. It is possible that the Fund will focus on an investment that performs poorly or underperforms other investments under various market conditions. |

The Fund’s performance will depend on the Adviser and key personnel |

internal management capacity or employees and depends on the experience, diligence, skill and network of business contacts of the investment professionals the Adviser and the Private Equity Group currently employ, or may subsequently retain, to identify, evaluate, negotiate, structure, close, monitor and manage the Fund’s investments. In addition, the Fund cannot assure investors that the Adviser will remain the Fund’s investment adviser. The Fund may not be able to find a suitable replacement within that time, resulting in a disruption in its operations that could adversely affect its financial condition, business and results of operations. This could have a material adverse effect on the Fund’s financial conditions, results of operations and cash flow. |

The Adviser’s due diligence process may entail evaluation of important and complex issues and may require outside consultants |

Investments in the Fund will be primarily illiquid closed-end fund, should be considered illiquid. The Shares are appropriate only for investors who are comfortable with investment in less liquid or illiquid portfolio investments within an illiquid fund. Unlikeopen-end funds (commonly known as mutual funds), which generally permit redemptions on a daily basis, the Shares will not be redeemable at a Shareholder’s option. Unlike stocks of listedclosed-end funds, the Shares are not listed, and are not expected to be listed, for |

trading on any securities exchange, and the Fund does not expect any secondary market to develop for the Shares in the foreseeable future. |

There can be no assurance that the Fund will conduct repurchase offers in a particular period |

It is possible that the Fund may be unable to repurchase all of the Shares that a Shareholder tenders due to the illiquidity of the Fund’s investments or if the Shareholders request the Fund to repurchase more Shares than the Fund is then offering to repurchase. In addition, substantial requests for the Fund to repurchase Shares could require the Fund to liquidate certain of its investments more rapidly than otherwise desirable in order to raise cash to fund the repurchases and achieve a market position appropriately reflecting a smaller asset base. This could have a material adverse effect on the value of the Shares. |

There will be a substantial period of time between the date as of which Shareholders must submit a request to have their Shares repurchased and the date they can expect to receive payment for their Shares from the Fund. Shareholders whose Shares are accepted for repurchase bear the risk that the Fund’s net asset value may fluctuate significantly between the time that they submit their repurchase requests and the date as of which such Shares are valued for purposes of such repurchase. Shareholders will have to decide whether to request that the Fund repurchase their Shares without the benefit of having current information regarding the value of Shares on a date proximate to the date on which Shares are valued by the Fund for purposes of effecting such repurchases. See “Repurchase of Shares.” |

The Fund may repurchase Shares through distributions in-kind |

repurchase. See “Repurchases of Shares—Periodic Repurchases.” However, there can be no assurance that the Fund will have sufficient cash to pay for Shares that are being repurchased or that it will be able to liquidate investments at favorable prices to pay for repurchased Shares. The Fund has the right to distribute securities as payment for repurchased Shares in unusual circumstances, including if making a cash payment would result in a material adverse effect on the Fund. In the event that the Fund makes such a distribution of securities, there can be no assurance that any Shareholder would be able to readily dispose of such securities or dispose of them at the value determined by the Adviser. |

The Fund will have access to confidential information |

Shares are not freely transferable |

The Fund is classified as non-diversified for purposes of the 1940 Act “non-diversified” investment company for purposes of the 1940 Act, which means it is not subject to percentage limitations under the 1940 Act on assets that may be invested in the securities of any one issuer. Having a larger percentage of assets in a smaller number of issuers makes anon-diversified fund, like the Fund, more susceptible to the risk that one single event or occurrence can have a significant adverse impact upon the Fund. However, the Fund will be subject to the diversification requirements applicable to regulated investment companies under Subchapter M of the Internal Revenue Code of 1986, as amended (the “Code”). |

The Fund’s investments may be difficult to value |

prices provided by dealers to value securities at their market value. Because the secondary markets for certain investments may be limited, such instruments may be difficult to value. |

A substantial portion of the Fund’s assets are expected to consist of Portfolio Funds and Co-Investments for which there are no readily available market quotations. The information available in the marketplace for such companies, their securities and the status of their businesses and financial conditions is often extremely limited, outdated and difficult to confirm. Such securities are valued by the Fund at fair value as determined pursuant to policies and procedures approved by the Board. |

The value at which the Fund’s investments can be liquidated may differ, sometimes significantly, from the valuations assigned by the Fund. In addition, the timing of liquidations may also affect the values obtained on liquidation. The Fund will invest a significant amount of its assets in private market investments for which no public market exists. There can be no guarantee that the Fund’s investments could ultimately be realized at the Fund’s valuation of such investments. |

The Fund’s net asset value is a critical component in several operational matters including computation of the Advisory Fee, the Incentive Fee and the Distribution and Servicing Fee, and determination of the price at which the Shares will be offered and at which a repurchase offer will be made. Consequently, variance in the valuation of the Fund’s investments will impact, positively or negatively, the fees and expenses Shareholders will pay, the price a Shareholder will receive in connection with a repurchase offer and the number of Shares an investor will receive upon investing in the Fund. |

The Fund cannot guarantee the amount or frequency of distributions . The Fund expects to pay distributions out of assets legally available for distribution from time to time, at the sole discretion of the Board, and otherwise in a manner to comply with the distribution requirements necessary for the Fund to qualify to be treated as a RIC. See “Distributions.” Nevertheless, the Fund cannot assure Shareholders that the Fund will achieve investment results that will allow the Fund to make a specified level of cash distributions oryear-to-year |

Additional subscriptions will dilute the voting interest of existing Shareholders |

of existing Shareholders in the Fund investments prior to such purchases, which could have an adverse impact on the existing Shareholders’ interests in the Fund if subsequent Fund investments underperform the prior investments. |

The Fund and certain service providers may have access to Shareholders’ personal information sub-delegates and certain third parties in any country in which such person conducts business. Subject to applicable law, Shareholders may have rights in respect of their personal data, including a right to access and rectification of their personal data and may in some circumstances have a right to object to the processing of their personal data. |

The Adviser and its affiliates manage funds and accounts with similar strategies and objectives to the Fund |

The Fund is subject to inflation risk |

Recent inflationary pressures have increased the costs of labor, energy and raw materials, have adversely affected consumer spending and economic growth, and may adversely affect portfolio companies’ operations. If portfolio companies are unable to pass increases in their costs of operations along to their customers, it could adversely affect their operating results and impact their ability to pay interest and principal on |

their loans, particularly as interest rates rise in response to inflation. In addition, any projected future decreases in portfolio companies’ operating results due to inflation could adversely impact the fair value of those investments. Any decreases in the fair value of those investments could result in future realized or unrealized losses and therefore reduce the Fund’s net asset value. |

Distributor | J.P. Morgan Institutional Investments Inc., an affiliate of the Fund and the Adviser, acts as distributor for the Shares (the “Distributor”) and serves in that capacity on a reasonable best efforts basis, subject to various conditions. |

The Distributor may retain additional selling agents or other financial intermediaries to place Shares in the Fund. Such selling agents or other financial intermediaries may impose terms and conditions on Shareholder accounts and investments in the Fund that are in addition to the terms and conditions set forth in this Prospectus. |

Share Classes; Minimum Investments | The Fund has received an exemptive order from the SEC that permits the Fund to offer multiple classes of shares. The Fund will offer three separate classes of Shares designated as Class S, Class D and Class I Shares. Each class of Shares has differing characteristics, particularly in terms of the sales charges that Shareholders in that class may bear, and the Distribution and Servicing Fee (as defined herein) that each class may be charged. The Fund may offer additional classes of Shares in the future. |

The minimum initial investment in the Fund by any investor is $25,000 with respect to Class S Shares and Class D Shares, and $1,000,000 with respect to Class I Shares. The minimum additional investment in the Fund by any investor is $10,000, except for additional purchases pursuant to the dividend reinvestment plan. Investors subscribing through a given broker/dealer or registered investment adviser may have shares aggregated to meet these minimums, so long as initial investments are not less than $25,000 and incremental contributions are not less than $10,000. |

The stated minimum investment for Class I Shares may be reduced for certain investors as described under “Purchasing Shares.” In addition, the Board reserves the right to accept lesser amounts below these minimums for Trustees of the Fund and employees of JPMorgan Chase Bank, N.A. and its affiliates (“JPM Employees”) and vehicles controlled by such employees. |

Shares are not listed on any securities exchange, and it is not anticipated that a secondary market for Shares will develop. Shares are subject to limitations on transferability, and |

| liquidity will be provided only through limited repurchase offers. |

The minimum initial and additional investments may be reduced by either the Fund or the Distributor in the discretion of each for certain investors based on consideration of various factors, including the investor’s overall relationship with the Adviser or Distributor, the investor’s holdings in other funds affiliated with the Adviser or Distributor, and such other matters as the Adviser or Distributor may consider relevant at the time, though Shares will only be sold to investors that satisfy the Fund’s eligibility requirements. The minimum initial and additional investments may also be reduced by either the Fund or the Distributor in the discretion of each for clients of certain registered investment advisers and other financial intermediaries based on consideration of various factors, including the registered investment adviser or other financial intermediary’s overall relationship with the Adviser or Distributor, the type of distribution channels offered by the intermediary and such other factors as the Adviser or Distributor may consider relevant at the time. |

In addition, the Fund may, in the discretion of the Adviser or Distributor, aggregate the accounts of clients of registered investment advisers and other financial intermediaries whose clients invest in the Fund for purposes of determining satisfaction of minimum investment amounts. At the discretion of the Adviser or the Distributor, the Fund may also aggregate the accounts of clients of certain registered investment advisers and other financial intermediaries across Share classes for purposes of determining satisfaction of minimum investment amounts for a specific Share class. The aggregation of accounts of clients of registered investment advisers and other financial intermediaries for purposes of determining satisfaction of minimum investment amounts for the Fund or for a specific Share class may be based on consideration of various factors, including the registered investment adviser or other financial intermediary’s overall relationship with the Adviser or Distributor, the type of distribution channels offered by the intermediary and such other factors as the Adviser or Distributor may consider relevant at the time. |

Eligible Investors | Although the Shares will be registered under the Securities Act, each prospective investor in the Fund will be required to certify that it is a “qualified client” within the meaning of Rule 205-3 under the Advisers Act and an “accredited investor” within the meaning of Rule 501 under the Securities Act. |

Shares are being offered to investors that are U.S. persons for U.S. federal income tax purposes. In addition, the Fund may offer Shares to non-U.S. persons subject to appropriate |

diligence by the Adviser and in compliance with applicable law. The qualifications required to invest in the Fund will appear in subscription documents that must be completed by each prospective investor. |

Each prospective investor in the Fund should obtain the advice of his, her or its own legal, accounting, tax and other advisers in reviewing documents pertaining to an investment in the Fund, including, but not limited to, this Prospectus, the SAI and the Declaration of Trust before deciding to invest in the Fund. |

Purchasing Shares | Shares will generally be offered for purchase as of the first business day of each calendar month at the NAV per Share on that date. Fractions of Shares will be issued to one one-hundredth of a Share. |

Although no upfront sales load will be paid with respect to Class S Shares, Class D Shares or Class I Shares, if you buy Class S Shares or Class D Shares through certain financial intermediaries, they may directly charge you transaction or other fees, including upfront placement fees or brokerage commissions, in such amount as they may determine, provided that financial intermediaries limit such charges to a 1.5% cap on NAV for Class D Shares and a 3.5% cap on NAV for Class S Shares. |

Subscriptions are generally subject to the receipt of cleared funds on or prior to the acceptance date set by the Fund and notified to prospective investors. An investor who misses the acceptance date will have the effectiveness of his, her or its investment in the Fund delayed until the following month. |

Pending any closing, funds received from prospective investors will be placed in an account with SS&C GIDS, Inc., the Fund’s transfer agent (the “Transfer Agent”). On the date of any closing, the balance in the account with respect to each investor whose investment is accepted will be invested in the Fund on behalf of such investor. Any interest earned with respect to such account will be paid to the Fund and allocated pro rata among investors. Prospective investors whose subscriptions to purchase Shares are accepted by the Fund will become shareholders by being admitted as Shareholders. |

A prospective investor must submit a completed subscription document on or prior to the acceptance date set by the Fund and notified to prospective investors. An existing Shareholder generally may subscribe for additional Shares by completing an additional subscription agreement by the acceptance date and funding such amount by the deadline. The Fund reserves the right to accept or reject, in its sole discretion, any request to purchase Shares at any time. The Fund also reserves the |

| right to suspend or terminate offerings of Shares at any time. Unless otherwise required by applicable law, any amount received in advance of a purchase ultimately rejected by the Fund will be returned promptly to the prospective investor without the deduction of any fees or expenses. Prospective investors whose purchases are rejected by the Fund will receive a pro rata share of any interest earned on the amounts placed in escrow prior to acceptance, if applicable. |

| Prospective investors who purchase Shares through financial intermediaries will be subject to the procedures of those intermediaries through which they purchase Shares, which may include charges, investment minimums, cutoff times and other restrictions in addition to, or different from, those listed herein. Prospective investors purchasing shares of the Fund through financial intermediaries should acquaint themselves with their financial intermediary’s procedures and should read this Prospectus in conjunction with any materials and information provided by their financial intermediary. |

Distributions | The Fund intends to make distributions in one or more payments on an annual basis in aggregate amounts representing substantially all of the Fund’s investment company taxable income (including realized short-term capital gains), if any, earned during the year. Distributions may also include net capital gains, if any. |

Because the Fund intends to qualify annually as a regulated investment company (a “RIC”) under the Code, the Fund intends to distribute at least 90% of its annual net taxable income to its Shareholders. Nevertheless, there can be no assurance that the Fund will pay distributions to Shareholders at any particular rate. Each year, a statement on Internal Revenue Service (“IRS”) Form 1099-DIV identifying the amount and character (e.g., as ordinary income, qualified dividend income or long-term capital gain) of the Fund’s distributions will be reported to Shareholders by their financial intermediary. See “Taxes, RIC Status” below and “Material U.S. Federal Income Tax Considerations.” |

| The Fund cannot guarantee that it will make distributions. The Fund may finance its cash distributions to Shareholders from any sources of funds available to the Fund, including offering proceeds, borrowings, net investment income from operations, capital gains proceeds from the sale of assets (including fund investments), non-capital gains proceeds from the sale of assets (including fund investments), dividends or other distributions paid to the Fund on account of preferred and common equity investments by the Fund in Portfolio Funds and/or Co-Investments and expense reimbursements from the Adviser. The Fund has not established limits on the amount of funds the Fund may use from available sources to make distributions. The repayment of any amounts owed to the |

| Adviser or its affiliates will reduce future distributions to which you would otherwise be entitled. |

Dividend Reinvestment Plan | The Fund will operate under a dividend reinvestment plan (the “DRIP”) administered by SS&C GIDS, Inc. Pursuant to the DRIP, the Fund’s income dividends or capital gains or other distributions, net of any applicable U.S. withholding tax, are reinvested in the same class of Shares of the Fund. |

Shareholders automatically participate in the DRIP, unless and until an election is made to withdraw from the DRIP on behalf of such participating Shareholder. A Shareholder who does not wish to have distributions automatically reinvested may terminate participation in the DRIP at any time by written instructions to that effect to SS&C GIDS, Inc. Shareholders who elect not to participate in the DRIP will receive all distributions in cash paid to the Shareholder of record (or, if the Shares are held in street or other nominee name, then to such nominee). Such written instructions must be received by SS&C GIDS, Inc. 30 days prior to the record date of the distribution or the Shareholder will receive such distribution in Shares through the DRIP. Under the DRIP, the Fund’s distributions to Shareholders are reinvested in full and fractional Shares. |

No Redemption; Restrictions on Transfer | No Shareholder will have the right to require the Fund to redeem Shares. With very limited exceptions, Shares are not transferable, and liquidity for investments in Shares may be provided only through periodic offers by the Fund to repurchase Shares from Shareholders. See “Repurchase of Shares.” |

Repurchase of Shares | To provide a limited degree of liquidity to Shareholders, at the sole discretion of the Board, the Fund may from time to time offer to repurchase Shares pursuant to written tenders by Shareholders. |

| The Adviser anticipates recommending to the Board that, under normal market circumstances, the Fund conduct repurchase offers of no more than 5% of the Fund’s net assets on a quarterly basis. The Adviser currently expects to recommend to the Board that the Fund conducts its first repurchase offer following the second full quarter of Fund operations (or such earlier or later date as the Board may determine). |

| Any repurchases of Shares will be made at such times and on such terms as may be determined by the Board from time to time in its sole discretion. In determining whether the Fund should offer to repurchase Shares from Shareholders of the Fund pursuant to repurchase requests, the Board may consider, |

| among other things, the recommendation of the Adviser as well as a variety of other operational, business and economic factors. The Fund may repurchase less than the full amount that Shareholders request to be repurchased. |

| Under certain circumstances, the Fund may offer to repurchase Shares at a discount to their prevailing net asset value. The Board may under certain circumstances elect to postpone, suspend or terminate an offer to repurchase Shares. |

| A Shareholder who tenders some but not all of its Shares for repurchase will be required to maintain a minimum account balance of $10,000. Such minimum ownership requirement may be waived by the Board, in its sole discretion. If such requirement is not waived by the Board, the Fund may redeem all of the Shareholder’s Shares. To the extent a Shareholder seeks to tender all of the Shares they own and the Fund repurchases less than the full amount of Shares that the Shareholder requests to have repurchased, the Shareholder may maintain a balance of Shares of less than $10,000 following such Share repurchase. |

A 2.00% early repurchase fee may be charged by the Fund with respect to any repurchase of Shares from a Shareholder at any time prior to the day immediately preceding the one-year anniversary of the Shareholder’s purchase of the Shares. Shares tendered for repurchase will be treated as having been repurchased on a “firstin-first out” basis. An early repurchase fee payable by a Shareholder may be waived by the Fund in circumstances where the Board determines that doing so is in the best interests of the Fund. See “Repurchase of Shares.” |

Fees and Expenses | The Fund will bear its own operating expenses (including, without limitation, its ongoing offering expenses). A more detailed discussion of the Fund’s expenses can be found below under “Advisory Fee,” “Incentive Fee,” “Administrator” and “Distribution and Servicing Fee for Class S and Class D Shares.” |

The Fund will bear certain of its organizational and initial offering costs in connection with this offering. The Fund’s initial offering costs, whether borne by the Adviser or the Fund, are being capitalized and amortized over a 12-month period. The Fund’s organizational costs are expensed as incurred. |

Advisory Fee | In consideration of the advisory services provided by the Adviser, the Fund pays the Adviser a quarterly advisory fee at an annual rate of 1.00% based on the value of the Fund’s net assets calculated and accrued monthly as of the last business day of each month (the “Advisory Fee”). The Adviser has contractually agreed to reduce its Advisory Fee to an annual rate of 0.25% through June 30, 2024. |

For purposes of determining the Advisory Fee payable to the Adviser, the value of the Fund’s net assets will be calculated prior to the inclusion of the Advisory Fee and Incentive Fee, if any, payable to the Adviser or to any purchases or repurchases of Shares of the Fund or any distributions by the Fund. The Advisory Fee will be payable in arrears within 5 business days after the completion of the net asset value computation for the quarter. The Advisory Fee is paid to the Adviser out of the Fund’s assets, and therefore decreases the net profits or increases the net losses of the Fund. |

The services of all investment professionals and staff of the Adviser, when and to the extent engaged in providing investment advisory and management services, and the compensation and routine overhead expenses of such personnel allocable to such services, are provided and paid for by the Adviser. The Fund bears all other costs and expenses of its operations and transactions as set forth in its Investment Advisory and Management Agreement with the Adviser (the “Investment Advisory and Management Agreement”). |

In addition to the fees and expenses to be paid by the Fund under the Investment Advisory and Management Agreement, the Adviser and its affiliates will be entitled to reimbursement by the Fund of the Adviser’s and its affiliates’ cost of providing the Fund with certain non-advisory services. If persons associated with the Adviser or any of its affiliates, including persons who are officers of the Fund, provide accounting, legal, clerical, compliance or administrative and similar oversight services to the Fund at the request of the Fund, the Fund will reimburse the Adviser and its affiliates for their costs in providing such accounting, legal, clerical, compliance or administrative and similar oversight services to the Fund (which costs may include an allocation of overhead including rent and the allocable portion of the salaries and benefits of the relevant persons and their respective staffs, including travel expenses), using a methodology for determining costs approved by the Board. |

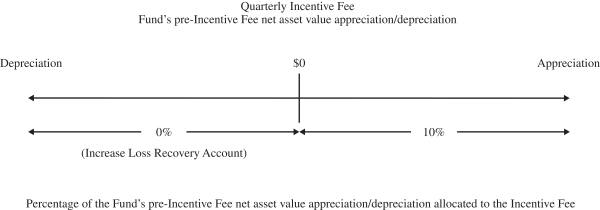

Incentive Fee | At the end of each calendar quarter of the Fund (and at certain other times), the Adviser (or, to the extent permitted by applicable law, an affiliate of the Adviser) will be entitled to receive an Incentive Fee equal to 10% of the excess, if any, of (i) the net profits of the Fund for the relevant period over (ii) the then balance, if any, of the Loss Recovery Account (as defined below). For the purposes of the Incentive Fee and Loss Recovery Account, the term “net profits” shall mean the amount by which (i) the sum of (A) the net asset value of the Fund as of the end of such quarter, (B) the aggregate repurchase price of all shares repurchased by the Fund during such quarter and (C) the amount of dividends and other distributions paid in respect of the Fund during such quarter |

and not reinvested in additional shares through the DRIP exceeds (ii) the sum of (X) the net asset value of the Fund as of the beginning of such quarter and (Y) the aggregate issue price of shares of the Fund issued during such quarter (excluding any shares of such class issued in connection with the reinvestment through the DRIP of dividends paid, or other distributions made, by the Fund through the DRIP). |

The Fund will maintain a memorandum account (the “Loss Recovery Account”), which will have an initial balance of zero and will be (i) increased upon the close of each calendar quarter of the Fund by the amount of the net losses of the Fund for the quarter, before giving effect to any repurchases or distributions for such quarter, and (ii) decreased (but not below zero) upon the close of each calendar quarter by the amount of the net profits of the Fund for the quarter. For purposes of the Loss Recovery Account, the term “net losses” shall mean the amount by which (i) the sum of (A) the net asset value of the Fund as of the beginning of such quarter and (B) the aggregate issue price of shares of the Fund issued during such quarter (excluding any Shares of such Class issued in connection with the reinvestment of dividends paid, or other distributions made, by the Fund through the DRIP) exceeds (ii) the sum of (X) the net asset value of the Fund as of the end of such quarter, (Y) the aggregate repurchase price of all shares repurchased by the Fund during such quarter and (Z) the amount of dividends and other distributions paid in respect of the Fund during such quarter and not reinvested in additional shares through the DRIP. Shareholders will benefit from the Loss Recovery Account in proportion to their holdings of Shares. For purposes of the “net losses” calculation, the net asset value shall include unrealized appreciation or depreciation of investments and realized income and gains or losses and expenses (including offering and organizational expenses). Incentive Fees are accrued monthly and paid quarterly. |

shareholder servicing fees. Accordingly, the Fund has adopted a distribution and servicing plan for its Class S Shares and Class D Shares (the “Distribution and Servicing Plan”) and pays the Distribution and Servicing Fee with respect to its Class S and Class D Shares. The Distribution and Servicing Plan operates in a manner consistent with Rule 12b-1 under the 1940 Act. |

Class S Shares and Class D Shares pay a Distribution and Servicing Fee to the Distributor at an annual rate of 0.70% and 0.25%, respectively, based on the aggregate net assets of the Fund attributable to such class. For purposes of determining the Distribution and Servicing Fee, net asset value will be calculated prior to any reduction for any fees and expenses, including, without limitation, the Distribution and Servicing Fee payable. |

Class I Shares are not subject to a Distribution and Servicing Fee. |

The Adviser, or its affiliates, may pay additional compensation out of its own resources (i.e., not Fund assets) to certain selling agents or financial intermediaries in connection with the sale of the Shares. The additional compensation may differ among brokers or dealers in amount or in the amount of calculation. Payments of additional compensation may be fixed dollar amounts or, based on the aggregate value of outstanding Shares held by Shareholders introduced by the broker or dealer, or determined in some other manner. The receipt of the additional compensation by a selling broker or dealer may create potential conflicts of interest between an investor and its broker or dealer who is recommending the Fund over other potential investments. |

Administrator | The Fund has retained State Street Bank and Trust Company (the “Administrator”) to provide it with certain administrative services, including fund administration and fund accounting. The Fund compensates the Administrator for these services and reimburses the Administrator for certain out-of-pocket expenses (the “Administration Fee”). The Administration Fee is paid to the Administrator out of the assets of the Fund and therefore decreases the net profits or increases the net losses of the Fund. See “Administration and Accounting Services.” |

Transfer Restrictions | A Shareholder may assign, transfer, sell, encumber, pledge or otherwise dispose of (each, a “transfer”) Shares only (i) by operation of law pursuant to the death, divorce, insolvency, bankruptcy, or adjudicated incompetence of the Shareholder; or (ii) under other limited circumstances, with the consent of the Board (which may be withheld in its sole discretion and is expected to be granted, if at all, only under extenuating circumstances). |

Notice of a proposed transfer of Shares must be accompanied by properly completed transfer information documents in respect of the proposed transferee and must include evidence satisfactory to the Board that the proposed transferee, at the time of the transfer, meets any requirements imposed by the Fund with respect to investor eligibility and suitability. Each transferring Shareholder and transferee may be charged reasonable expenses, including attorneys’ and accountants’ fees, incurred by the Fund in connection with the transfer. |

Unlisted Closed-End Structure; Limited Liquidity | Shares are not listed on any securities exchange, and it is not anticipated that a secondary market for Shares will develop. In addition, Shares are subject to limitations on transferability and liquidity will be provided only through limited repurchase offers described below. An investment in the Fund is suitable only for Shareholders who can bear the risks associated with the limited liquidity of the Shares and should be viewed as a long-term investment. See “General Risks of Investing in the Fund—Closed-End Fund Structure; Liquidity Limited to Periodic Repurchases of Shares.” |

Taxes; RIC Status | The Fund intends to elect to be treated as a RIC for U.S. federal income tax purposes, and it further intends to elect to be treated, and expects each year to qualify as a RIC for U.S. federal income tax purposes. As such, the Fund generally will not be subject to U.S. federal corporate income tax, provided that it distributes all of its net taxable income and gains each year. It is anticipated that the Fund will principally recognize capital gains and dividends and therefore dividends paid to Shareholders in respect of such income generally will be taxable to Shareholders at the reduced rates of U.S. federal income tax that are applicable to individuals for “qualified dividends” and long-term capital gains. |

In addition, because the Fund intends to qualify as a RIC, it is expected to have certain attributes that are not generally found in traditional unregistered private equity fund of funds. These include providing simpler tax reports to Shareholders on Form 1099-DIV and the avoidance of unrelated business taxable income for benefit plan investors and other investors that are exempt from payments of U.S. federal income tax. |

For a discussion of certain tax risks and considerations relating to an investment in the Fund, see “Material U.S. Federal Income Tax Considerations.” |

Prospective investors should consult their own tax advisers with respect to the specific U.S. federal, state, local, U.S. and non-U.S. tax consequences, including applicable tax reporting requirements. |

Tax Reports | The Fund will distribute to its Shareholders, after the end of each calendar year, IRS Forms 1099-DIV detailing the amounts includible in such Shareholder’s taxable income for such year as ordinary income, qualified dividend income and long-term capital gains. Dividends and other taxable distributions are taxable to the Fund’s Shareholders even if they are reinvested in additional Shares pursuant to the DRIP. |

Reports to Shareholders | The Fund will provide Shareholders with an audited annual report and an unaudited semi-annual report within 60 days after the close of the reporting period for which the report is being made, or as otherwise required by 1940 Act. Shareholders will also receive quarterly commentary regarding the Fund’s operations and investments. |

The Fund will furnish as soon as practicable after the end of each taxable year information on Form 1099-DIV to assist Shareholders in preparing their tax returns. Your financial intermediary will report this information to you. |

Fiscal and Tax Year | The Fund’s fiscal year is the 12-month period ending on March 31. The Fund’s taxable year is the12-month period ending on September 30. |

Term | The Fund’s term is perpetual unless the Fund is otherwise terminated under the terms of the Declaration of Trust. |

Custodian and Transfer Agent | State Street Bank and Trust Company serves as the Fund’s custodian, and SS&C GIDS, Inc. serves as the Fund’s transfer agent. |

ERISA | Investors subject to the Employee Retirement Income Security Act of 1974, as amended (“ERISA”) or section 4975 of the Code, including employee benefit plans and individual retirement accounts, may purchase Shares. Because the Fund is registered as an investment company under the 1940 Act, the underlying assets of the Fund will not be considered to be “plan assets” subject to the fiduciary responsibility and prohibited transaction rules of ERISA. Thus, it is not intended that the Adviser will be a “fiduciary” within the meaning of ERISA with respect to the assets of any “benefit plan investor” within the meaning of ERISA that becomes a Shareholder, solely as a result of the Shareholder’s investment in the Fund. |

Shareholder Transaction Expenses (fees paid directly from your investment) | Class S Shares | Class D Shares | Class I Shares | |||||||||

Maximum Sales Load (as a percentage of purchase amount) (1) | — | — | — | |||||||||

Maximum Early Repurchase Fee (as a percentage of repurchased amount) (2) | 2.00 | % | 2.00 | % | 2.00 | % | ||||||

Estimated Annual Operating Expenses (as a percentage of net assets attributable to Shares) | Class S Shares | Class D Shares | Class I Shares | |||||||||

Advisory Fee (3)(7) | 1.00 | % | 1.00 | % | 1.00 | % | ||||||

Incentive Fee (4) | — | % | — | % | — | % | ||||||

Other Expenses (5) | 1.95 | % | 1.95 | % | 1.95 | % | ||||||

Distribution and Servicing Fee | 0.70 | % | 0.25 | % | None | |||||||

Acquired Fund Fees and Expenses (6) | 1.33 | % | 1.33 | % | 1.33 | % | ||||||

Total Annual Expenses | 4.98 | % | 4.53 | % | 4.28 | % | ||||||

Fee Waiver and/or Expense Reimbursement (7)(8) | (2.40 | )% | (2.40 | )% | (2.40 | )% | ||||||

Total Annual Expenses (After Fee Waiver and/or Expense Reimbursement) | 2.58 | % | 2.13 | % | 1.88 | % | ||||||

| (1) | No upfront sales load will be paid with respect to Class S Shares, Class D Shares or Class I Shares, however, if you buy Class S Shares or Class D Shares through certain financial intermediaries, they may directly charge you transaction or other fees, including upfront placement fees or brokerage commissions, in such amount as they may determine, provided that selling agents limit such charges to a 1.5% cap on NAV for Class D Shares and a 3.5% cap on NAV for Class S Shares. Financial intermediaries will not charge such fees on Class I Shares. Please consult your financial intermediary for additional information. |

| (2) | A 2.00% Early Repurchase Fee payable to the Fund may be charged with respect to the repurchase of Shares at any time prior to the day immediately preceding the one-year anniversary of a Shareholder’s purchase of the Shares (on a “first in—first out” basis). An Early Repurchase Fee payable by a Shareholder may be waived in circumstances where the Board determines that doing so is in the best interests of the Fund and in a manner that will not discriminate unfairly against any Shareholder. The Early Repurchase Fee will be retained by the Fund for the benefit of the remaining Shareholders. |

| (3) | The Fund pays the Adviser a quarterly Advisory Fee at an annual rate of 1.00% based on value of the Fund’s net assets, calculated and accrued monthly as of the last business day of each month. For purposes of determining the Advisory Fee payable to the Adviser, the value of the Fund’s net assets will be calculated prior to the inclusion of the Advisory Fee and Incentive Fee, if any, payable to the Adviser or to any purchases or repurchases of Shares of the Fund or any distributions by the Fund. The Adviser has contractually agreed to reduce its Advisory Fee to an annual rate of 0.25% through June 30, 2024 (the “Fee Reduction Agreement”). Unless otherwise extended by agreement between the Fund and the Adviser, the Advisory Fee payable by the Fund as of July 1, 2024 will be at the annual rate of 1.00%. The reduction of the Advisory Fee under the Fee Reduction Agreement is not subject to recoupment by the Adviser under the Expense Limitation Agreement, described below. |

(4) | At the end of each calendar quarter of the Fund (and at certain other times), the Adviser (or, to the extent permitted by applicable law, an affiliate of the Adviser) will be entitled to receive an Incentive Fee equal to 10% of the excess, if any, of (i) the net profits of the Fund for the relevant period over (ii) the then balance, if any, of the Loss Recovery Account. For the purposes of the Incentive Fee, the term “net profits” shall mean the amount by which (i) the sum of (A) the net asset value of the Fund as of the end of such quarter, (B) the aggregate repurchase price of all shares repurchased by the Fund during such quarter and (C) the amount of dividends and other distributions paid in respect of the Fund during such quarter and not reinvested in additional shares through the DRIP exceeds (ii) the sum of (X) the net asset value of the Fund as of the beginning of such quarter and (Y) the aggregate issue price of shares of the Fund issued during such quarter (excluding any Shares of such Class issued in connection with the reinvestment through the DRIP of dividends paid, or other distributions made, by the Fund through the DRIP). Incentive Fees are accrued monthly and paid quarterly. Because the Incentive Fee is speculative, no Incentive Fee is presented for the initial year of operations. See “Management and Incentive Fees.” |

| (5) | The Other Expenses include, among other things, professional fees and other expenses that the Fund will bear, including initial and ongoing offering costs and fees and expenses of the Administrator, transfer agent and custodian. The Other Expenses are based on estimated amounts for the Fund’s current fiscal year. |

| (6) | The Acquired Fund Fees and Expenses include the fees and expenses of the Portfolio Funds in which the Fund intends to invest. Some or all of the Portfolio Funds in which the Fund intends to invest generally charge asset-based management fees. The managers of the Portfolio Funds may also receive performance-based compensation if the Portfolio Funds achieve certain profit levels, generally in the form of “carried interest” allocations of profits from the Portfolio Funds, which effectively will reduce the investment returns of the Portfolio Funds. The Portfolio Funds in which the Fund intends to invest generally charge a management fee of 1.50% to 2.50%, and generally charge between 20% and 30% of net profits as a carried interest allocation, subject to a clawback. The “Acquired Fund Fees and Expenses” disclosed above are based on historic returns of the types of Portfolio Funds in which the Fund anticipates investing, which may change substantially over time and, therefore, significantly affect “Acquired Fund Fees and Expenses.” The Acquired Fund Fees and Expenses are based on estimated amounts for the Fund’s current fiscal year. |

| (7) | Pursuant to an expense limitation agreement (the “Expense Limitation Agreement”) with the Fund, the Adviser has agreed to waive fees that it would otherwise be paid, and/or to assume expenses of the Fund, if required to ensure certain annual operating expenses (excluding the Advisory Fee, Incentive Fee, any Distribution and Servicing Fee, interest, taxes, brokerage commissions, acquired fund fees and expenses, dividend and interest expenses relating to short sales, borrowing costs, merger or reorganization expenses, shareholder meetings expenses, litigation expenses, expenses associated with the acquisition and disposition of investments (including interest and structuring costs for borrowings and line(s) of credit) and extraordinary expenses, if any; collectively, the “Excluded Expenses”) do not exceed 0.30% per annum (excluding Excluded Expenses) of the Fund’s average monthly net assets of each class of Shares. With respect to each class of Shares, the Fund agrees to repay the Adviser any fees waived or expenses assumed under the Expense Limitation Agreement for such class of Shares, provided the repayments do not cause the Fund’s annual operating expenses (excluding Excluded Expenses) for that class of Shares to exceed the expense limitation in place at the time the fees were waived and/or the expenses were reimbursed, or the expense limitation in place at the time the Fund repays the Adviser, whichever is lower. Any such repayments must be made within thirty-six months after the month in which the Adviser incurred the expense. The Expense Limitation Agreement will have a term ending one from the date the Fund commences operations, and the Adviser may extend the term for a period of one year on an annual basis. The Adviser may not terminate the Expense Limitation Agreement during its initial one-year term. |

| (8) | The Fund may invest in one or more money market funds advised by the Adviser or its affiliates (affiliated money market funds). The Adviser has contractually agreed to waive fees and/or reimburse expenses in an amount sufficient to offset the respective net advisory fees it collects from the affiliated money market funds on the Fund’s investment in such money market funds. |

1 Year | 3 Years | 5 Years | 10 Years | |||||||||||||

You would pay the following expenses on a $1,000 Class S Shares investment, assuming a 5% annual return: | $31 | $118 | $210 | $462 | ||||||||||||

You would pay the following expenses on a $1,000 Class D Shares investment, assuming a 5% annual return: | $27 | $105 | $189 | $423 | ||||||||||||

You would pay the following expenses on a $1,000 Class I Shares investment, assuming a 5% annual return: | $24 | $98 | $178 | $400 | ||||||||||||

1 Year | 3 Years | 5 Years | 10 Years | |||||||||||||

You would pay the following expenses on a $25,000 Class S Shares investment, assuming a 5% annual return: | $ | 769 | $ | 2,946 | $ | 5,242 | $ | 11,544 | ||||||||

You would pay the following expenses on a $25,000 Class D Shares investment, assuming a 5% annual return: | $ | 665 | $ | 2,635 | $ | 4,730 | $ | 10,563 | ||||||||

You would pay the following expenses on a $25,000 Class I Shares investment, assuming a 5% annual return: | $ | 607 | $ | 2,462 | $ | 4,442 | $ | 10,000 | ||||||||

| • | Private Equity Investment Risks . Private equity transactions may result in new enterprises that are subject to extreme volatility, require time for maturity and may require additional capital. In addition, they frequently rely on borrowing significant amounts of capital, which can increase profit potential but at the same time increase the risk of loss. Leveraged companies may be subject to restrictive financial and operating covenants. The leverage may impair the ability of these companies to finance their future operations and capital needs. Also, their flexibility to respond to changing business and economic conditions and to business opportunities may be limited. A leveraged company’s income and net assets will tend to increase or decrease at a greater rate than if borrowed money was not used. Although these investments may offer the opportunity for significant gains, such buyout and growth investments involve a high degree of business and financial risk that can result in substantial losses, which risks generally are greater than the risks of investing in public companies that may not be as leveraged. |

| • | Venture Capital Risks . Venture capital investments are in private companies that have limited operating history, are attempting to develop or commercialize unproven technologies or to implement novel business plans or are not otherwise developed sufficiently to be self-sustaining financially or to become public. Although these investments may offer the opportunity for significant gains, such investments involve a high degree of business and financial risk that can result in substantial losses, which risks generally are greater than the risks of investing in public or private companies that may be at a later stage of development. |

| • | the likelihood of greater volatility of NAV of the Shares than a comparable portfolio without leverage; |

| • | the risk that fluctuations in interest rates or dividend rates on any leverage that the Fund must pay will reduce the return to Shareholders; |

| • | the effect of leverage in a declining market, which is likely to cause a greater decline in the NAV of the Shares than if the Fund were not leveraged; and |

| • | leverage may increase operating costs, which may reduce total return. |

| • | Quarterly and audited annual financial statements of Portfolio Funds and individual statements provided by a Portfolio Fund. The Adviser is not required to adjust fair valuations (inclusive of accrual based performance fees) provided by Portfolio Funds. |

| • | Where an accrual based performance fee has not been incorporated in the fair valuation provided by the Portfolio Fund Manager, a separate fair value analysis may be obtained from the Portfolio Fund Manager or prepared by the Adviser. The Portfolio Fund’s performance fee is then deducted from the valuation. |

| • | Where financial statements of a Portfolio Fund are prepared on a basis other than US GAAP, the Adviser may assess if the valuation methodology employed is equivalent to US GAAP, or if an adjustment is necessary. In the case of non-US GAAP financial statements (such as IFRS, UK GAAP, Irish GAAP or French GAAP), the Adviser may review the valuation policies and procedures of a Portfolio Fund with the Portfolio Fund Manager to allow the Adviser to conclude whether a Portfolio Fund valuation is US GAAP equivalent, and therefore whether no adjustment is required. Where Portfolio Fund financial statements are prepared on a basis inconsistent with US GAAP, the Adviser may review separately negotiated fair value statements or determine a fair valuation through discussion with the applicable Portfolio Fund Manager. |

| • | Where the Portfolio Fund’s measurement date is at a non-quarter end, net asset value may be adjusted for cash flows through the applicable reporting date. Where distributions are in excess of the Portfolio Fund’s valuation, the valuation will not be reduced below zero. The valuation may be adjusted to reflect the residual value in the Portfolio Fund, depending on materiality. |

| • | In addition, the Adviser expects to engage in the following processes as it deems necessary: |

| o | Representation in certain cases on the advisory board and/or valuation committee of the Portfolio Fund. |

| o | Attendance of the Portfolio Fund Manager annual meetings. |

| o | Ongoing dialogue with the Portfolio Fund Manager, including performance reviews of the Portfolio Fund’s underlying portfolio companies. |

| • | which share classes are available to you; |

| • | how much you intend to invest; |

| • | how long you expect to own the shares; and |

| • | total costs and expenses associated with a particular share class. |

Share Class | Amount Authorized | Amount Outstanding | ||

Class S Shares | Unlimited | 0 | ||

Class D Shares | Unlimited | 0 | ||

Class I Shares | Unlimited | 10,000 |

| • | an individual who is a citizen or resident of the United States; |

| • | a corporation, or other entity treated as a corporation for U.S. federal income tax purposes, created or organized in or under the laws of the United States or any state thereof or the District of Columbia; |

| • | a trust, if a court within the United States has primary supervision over its administration and one or more U.S. persons (as defined in the Code) have the authority to control all of its substantial decisions, or if the trust has a valid election in effect under applicable U.S. Treasury regulations to be treated as a domestic trust for U.S. federal income tax purposes; or |

| • | an estate, the income of which is subject to U.S. federal income taxation regardless of its source. |

| • | Elect to be treated and qualify as a registered management company under the 1940 Act at all times during each taxable year; |

| • | derive in each taxable year at least 90% of its gross income from (a) dividends, interest, payments with respect to certain securities loans, gains from the sale of stock, securities, or foreign currencies (including certain deemed inclusions) derived with respect to the Fund’s business of investing in such stock, securities, foreign currencies or other income, or (b) net income derived from an interest in a qualified publicly traded partnership (“QPTP”) (collectively, the “90% Gross Income Test”); and |

| • | diversify its holdings so that at the end of each quarter of the taxable year: |

| o | at least 50% of the value of its assets consists of cash, cash equivalents, U.S. government securities, securities of other RICs and other securities that, with respect to any issuer, do not represent more than 5% of the value of the Fund’s assets or more than 10% of the outstanding voting securities of that issuer; and |

| o | no more than 25% of the value of its assets is invested in the securities, other than U.S. government securities or securities of other RICs, of (i) one issuer, (ii) or of two or more issuers that are controlled, as determined under the Code, by the Fund and that are engaged in the same or similar or related trades or businesses or (iii) securities of one or more QPTPs (collectively, the “Diversification Tests”). |

| • | results in a “complete termination” of such U.S. Shareholder’s ownership of Shares in the Fund; |

| • | results in a “substantially disproportionate” redemption with respect to such U.S. Shareholder; or |

| • | is “not essentially equivalent to a dividend” with respect to the U.S. Shareholder. |

JPMORGAN PRIVATE MARKETS FUND

Class S Shares

Class D Shares

Class I Shares

June 16, 2023

JPMorgan Private Markets Fund (the “Fund”) is a non-diversified, closed-end management investment company with no operating history. This Statement of Additional Information (“SAI”) relating to the Shares does not constitute a prospectus, but should be read in conjunction with the Prospectus relating thereto dated June 16, 2023. This SAI, which is not a prospectus, does not include all information that a prospective investor should consider before purchasing Shares, and investors should obtain and read the Prospectus prior to purchasing such Shares. A copy of the Prospectus may be obtained without charge by calling 212-648-2293, by writing to the Fund at 277 Park Avenue, New York, New York 10172 or by visiting www.jpmorganfunds.com. You may also obtain a copy of the Prospectus on the SEC’s website at http://www.sec.gov. Capitalized terms used but not defined in this SAI have the meanings ascribed to them in the Prospectus.

References to the Investment Company Act of 1940, as amended (the “1940 Act”), or other applicable law, will include any rules promulgated thereunder and any guidance, interpretations or modifications by the U.S. Securities and Exchange Commission (the “SEC”), SEC staff or other authority with appropriate jurisdiction, including court interpretations, and exemptive, no-action or other relief or permission from the SEC, SEC staff or other authority.

TABLE OF CONTENTS

| Page | ||||

| 1 | ||||

| 5 | ||||

| 20 | ||||

| 27 | ||||

| 28 | ||||

| 30 | ||||

| 30 | ||||

| A-1 | ||||

i

ADDITIONAL INVESTMENT POLICIES

The investment objective and the principal investment strategies of the Fund, as well as the principal risks associated with such investment strategies, are set forth in the Prospectus. The following disclosure supplements the disclosure set forth under the captions “Investment Objective and Strategy” and “Risks” in the Prospectus and does not, by itself, present a complete or accurate explanation of the matters discussed. Prospective investors also should refer to “Investment Objective and Strategy” and “Risks” in the Prospectus for a complete presentation of the matters disclosed below.

Fundamental Policies