Exhibit 99.3

FELDMAN FINANCIAL ADVISORS, INC.

8804 MIRADOR PLACE

MCLEAN, VA 22102

202-467-6862

First Seacoast Bancorp

Dover, New Hampshire

Conversion Valuation Appraisal Report

Valued as of August 26, 2022

Prepared By

Feldman Financial Advisors, Inc.

McLean, Virginia

FELDMAN FINANCIAL ADVISORS, INC.

8804 MIRADOR PLACE

MCLEAN, VA 22102

202-467-6862

August 26, 2022

Boards of Directors

First Seacoast Bancorp, MHC

First Seacoast Bancorp

First Seacoast Bancorp, Inc.

First Seacoast Bank

633 Central Avenue

Dover, New Hampshire 03820

Members of the Boards of Directors:

At your request, we have completed and hereby provide an independent appraisal (the “Appraisal”) of the estimated pro forma market value of First Seacoast Bancorp (“FSB” or the “Company”) on a fully converted basis as of August 26, 2022 in conjunction with the Company’s conversion (the “Conversion”) from the two-tier mutual holding company structure to the fully stock holding company form of ownership and simultaneous offering for sale (the “Stock Offering”) of the shares of common stock currently held by First Seacoast Bancorp, MHC (the “MHC”). The Company is a federally-chartered mid-tier stock holding company that owns all of the outstanding shares of common stock of First Seacoast Bank (the “Bank”). The MHC currently owns approximately 55.2% of the outstanding shares of common stock of FSB. The Appraisal is furnished pursuant to the filing by the MHC and the Company of an application (the “Application”) concerning the Conversion and Stock Offering with the Board of Governors of the Federal Reserve System.

Pursuant to the Plan of Conversion and Reorganization (“Plan of Conversion”), the MHC will be merged into FSB and, as a result, the MHC will cease to exist. FSB, which owns 100% of the outstanding common stock of the Bank, will merge into a new Maryland-chartered corporation named First Seacoast Bancorp, Inc. (“New FSB”) and, as a result, FSB will cease to exist. As part of the Conversion, the 55.2% ownership interest of the MHC in FSB will be offered for sale in the Stock Offering. When the Conversion is completed, New FSB will own all of the outstanding common stock of the Bank and public stockholders will own all of the outstanding common stock of New FSB.

In conjunction with the Conversion, the shares of common stock are first being offered for sale in a subscription offering to eligible depositors and borrowers of the Bank and to tax-qualified employee benefit plans of the Bank. Shares not purchased in the subscription offering may be offered for sale to the general public in a community offering, with a preference given first to residents of specific counties served by the Bank and secondly to existing public stockholders of FSB. Any shares of common stock not purchased in the subscription or community offerings may be offered for sale to the public in a syndicated community offering.

FELDMAN FINANCIAL ADVISORS, INC.

Boards of Directors

August 26, 2022

Page Two

In addition to the shares being sold in the Stock Offering, the shares of common stock of FSB currently owned by public stockholders will be exchanged for shares of common stock of New FSB based on an exchange ratio, subject to any necessary adjustment, that will result in existing public stockholders owning approximately the same percentage of common stock as they owned of the common stock of FSB immediately before the completion of the Conversion.

Feldman Financial Advisors, Inc. (“Feldman Financial”) is a financial consulting and economic research firm that specializes in financial valuations and analyses of business enterprises and securities in the thrift, banking, and mortgage industries. The background of Feldman Financial is presented in Exhibit I. In preparing the Appraisal, we conducted an analysis of the Company that included discussions with the Company’s management, the Company’s legal counsel, Luse Gorman, PC, and the Company’s independent registered public accounting firm, Baker Newman & Noyes LLC. In addition, where appropriate, we considered information based on other available published sources that we believe are reliable; however, we cannot guarantee the accuracy and completeness of such information.

We also reviewed, among other factors, the economy in the Company’s primary market area and compared the Company’s financial condition and operating performance with that of selected publicly traded thrift institutions. We reviewed conditions in the securities markets in general and in the market for thrift institution common stocks in particular.

The Appraisal is based on the Company’s representation that the information contained in the Application and additional evidence furnished to us by the Company and its independent auditor are truthful, accurate, and complete. We did not independently verify the financial statements and other information provided by the Company and its independent auditor, nor did we independently value the assets or liabilities of the Company. The Appraisal considers the Company only as a going concern and should not be considered as an indication of the liquidation value of the Company.

It is our opinion that, as of August 26, 2022, the estimated pro forma market value of the Company on a fully converted basis – including (1) newly-issued shares representing the MHC’s current ownership interest in the Company and (2) exchange shares issued to existing public stockholders of the Company – was within a range (the “Valuation Range”) of $50,774,920 to $68,695,480 with a midpoint of $59,735,200. The Valuation Range was based upon a 15% decrease from the midpoint to determine the minimum and a 15% increase from the midpoint to establish the maximum. Based on an offering price of $10.00 per share, the Valuation Range reflects total pro forma outstanding shares ranging from 5,077,492 at the minimum to 6,869,548 at the maximum.

FELDMAN FINANCIAL ADVISORS, INC.

Boards of Directors

August 26, 2022

Page Three

In preparing the pro forma valuation analysis, we have taken into account the pro forma impact of the MHC’s unconsolidated net assets that will be consolidated with the Company and thus will slightly increase pro forma equity. After accounting for the impact of the MHC’s net assets of $100,000 as of June 30, 2022, the public stockholders’ aggregate ownership interest in FSB was reduced by 0.2%, or a difference of 0.0750 percentage points. Accordingly, for purposes of the Company’s pro forma valuation, the public stockholders’ pro forma ownership interest was reduced from 44.8312% to 44.7562% and the MHC’s pro forma ownership interest was increased from 55.1688% to 55.2438%.

Based on the Valuation Range and taking into account the pro forma ownership interest represented by the shares owned by the MHC, the midpoint of the offering range is $33,000,000 or equal to 3,300,000 shares at the offering price of $10.00 per share. The resulting offering range and offering shares, all based on the offering price of $10.00 per share, are as follows: $28,050,000 or 2,805,000 shares at the minimum and $37,950,000 or 3,795,000 shares at the maximum.

The federal conversion regulations provide that in a conversion of a mutual holding company, the minority stockholders are entitled to exchange the public shares for newly issued shares in the fully converted company. The Boards of Directors of the MHC, the Company, and the Bank have independently determined the exchange ratio, which has been designed to preserve the current aggregate percentage ownership in the Company (adjusted for the dilution caused by the consolidation of the MHC’s unconsolidated net assets into the Company and the resulting capital contribution).

The exchange ratio to be received by the existing minority stockholders of the Company will be determined at the end of the Stock Offering, based on the total number of shares sold in the subscription and community offerings and the final appraisal. Based on the valuation conclusion herein, the resulting offering value, and the $10.00 per share offering price, the indicated exchange ratio at the midpoint is 0.9833 shares of New FSB common stock for every one share of FSB common stock held by public stockholders. Furthermore, based on the offering range of value, the indicated exchange ratio is 0.8358 at the minimum and 1.1308 at the maximum. Feldman Financial expresses no opinion on the proposed exchange of newly issued shares of New FSB common stock for the shares of FSB common stock held by the public stockholders or on the proposed exchange ratio.

Our Appraisal is not intended, and must not be construed, to be a recommendation of any kind as to the advisability of purchasing shares of common stock in the Stock Offering. Moreover, because the Appraisal is necessarily based upon estimates and projections of a number of matters, all of which are subject to change from time to time, no assurance can be given that persons who purchase shares of stock in the Stock Offering will thereafter be able to sell such shares at prices related to the foregoing estimate of the Company’s pro forma market value.

FELDMAN FINANCIAL ADVISORS, INC.

Boards of Directors

August 26, 2022

Page Four

Feldman Financial is not a seller of securities within the meaning of any federal or state securities laws, and any report prepared by Feldman Financial shall not be used as an offer or solicitation with respect to the purchase or sale of any securities.

The Valuation Range reported herein will be updated as appropriate. These updates will consider, among other factors, any developments or changes in the Company’s operating performance, financial condition, or management policies, and current conditions in the securities markets for thrift institution common stocks. Should any such new developments or changes be material, in our opinion, to the valuation of the Company, appropriate adjustments to the estimated pro forma market value will be made. The reasons for any such adjustments will be explained in detail at that time.

| Respectfully submitted, |

| Feldman Financial Advisors, Inc. |

|

| Trent R. Feldman |

| President |

|

| Peter W. L. Williams |

| Principal |

FELDMAN FINANCIAL ADVISORS, INC.

TABLE OF CONTENTS

TAB | PAGE | |||||||

| INTRODUCTION | 1 | |||||||

| I. | CHAPTER ONE – BUSINESS OF FIRST SEACOAST BANCORP | |||||||

| General Overview | 4 | |||||||

| Financial Condition | 11 | |||||||

| Income and Expense Trends | 24 | |||||||

| Interest Rate Risk Management | 32 | |||||||

| Asset Quality | 36 | |||||||

| Office Facilities | 39 | |||||||

| Market Area | 41 | |||||||

| Summary Outlook | 55 | |||||||

| II. | CHAPTER TWO – COMPARISONS WITH PUBLICLY TRADED THRIFTS | |||||||

| General Overview | 57 | |||||||

| Selection Criteria | 58 | |||||||

| Recent Financial Comparisons | 62 | |||||||

| III. | CHAPTER THREE – MARKET VALUE ADJUSTMENTS | |||||||

| General Overview | 75 | |||||||

| Earnings Prospects | 76 | |||||||

| Financial Condition | 77 | |||||||

| Market Area | 78 | |||||||

| Management | 79 | |||||||

| Dividend Payments | 80 | |||||||

| Liquidity of the Issue | 81 | |||||||

| Subscription Interest | 82 | |||||||

| Recent Acquisition Activity | 83 | |||||||

| Effect of Banking Regulations and Regulatory Reform | 85 | |||||||

| Stock Market Conditions | 85 | |||||||

| Adjustments Conclusion | 92 | |||||||

| Valuation Approach | 93 | |||||||

| Valuation Conclusion | 96 | |||||||

| IV. | APPENDIX – EXHIBITS | |||||||

| I | Background of Feldman Financial Advisors, Inc. | I-1 | ||||||

| II-1 | Consolidated Balance Sheets | II-1 | ||||||

| II-2 | Consolidated Income Statements | II-2 | ||||||

| II-3 | Loan Portfolio Composition | II-3 | ||||||

| II-4 | Cash and Investments Composition | II-4 | ||||||

| II-5 | Deposit Account Composition | II-5 | ||||||

| II-6 | Borrowed Funds Activity | II-6 | ||||||

| II-7 | Office Properties | II-7 | ||||||

| III | Financial and Market Data for All Public Thrifts | III-1 | ||||||

| IV-1 | Effect of the MHC’s Assets on Minority Stock Ownership | IV-1 | ||||||

| IV-2 | Pro Forma Assumptions for the Stock Offering | IV-2 | ||||||

| IV-3 | Pro Forma Fully Converted Valuation Range | IV-3 | ||||||

| IV-4 | Pro Forma Fully Converted Analysis at the Midpoint Valuation | IV-5 | ||||||

| IV-5 | Comparative Valuation Ratio Differential | IV-6 | ||||||

i

FELDMAN FINANCIAL ADVISORS, INC.

LIST OF TABLES

TAB | PAGE | |||||||

| I. | CHAPTER ONE – BUSINESS OF FIRST SEACOAST BANCORP | |||||||

| Table 1 | Selected Financial Condition Data | 11 | ||||||

| Table 2 | Relative Balance Sheet Concentrations | 12 | ||||||

| Table 3 | Income Statement Summary | 25 | ||||||

| Table 4 | Income Statement Ratios | 26 | ||||||

| Table 5 | Yield and Cost Summary | 28 | ||||||

| Table 6 | Net Portfolio Value of Equity | 35 | ||||||

| Table 7 | Non-performing Asset Summary | 37 | ||||||

| Table 8 | Allowance for Loan Losses | 38 | ||||||

| Table 9 | Selected Demographic Data | 42 | ||||||

| Table 10 | Branch Office Deposit Data | 46 | ||||||

| Table 11 | Map of Branch Office Locations | 47 | ||||||

| Table 12 | Deposit Market Share in Strafford County, New Hampshire | 49 | ||||||

| Table 13 | Deposit Market Share in Rockingham County, New Hampshire | 50 | ||||||

| Table 14 | Residential Lending Share in Strafford County, New Hampshire | 52 | ||||||

| Table 15 | Residential Lending Share in Rockingham County, New Hampshire | 53 | ||||||

| Table 16 | Residential Lending Share in York County, Maine | 54 | ||||||

| II. | CHAPTER TWO – COMPARISONS WITH PUBLICLY TRADED THRIFTS | |||||||

| Table 17 | Comparative Group Operating Summary | 61 | ||||||

| Table 18 | Key Financial Comparisons | 63 | ||||||

| Table 19 | General Operating Characteristics | 70 | ||||||

| Table 20 | Summary Financial Performance Ratios | 71 | ||||||

| Table 21 | Income and Expense Analysis | 72 | ||||||

| Table 22 | Balance Sheet Composition | 73 | ||||||

| Table 23 | Growth Rates, Credit Risk, and Loan Composition | 74 | ||||||

| III. | CHAPTER THREE – MARKET VALUE ADJUSTMENTS | |||||||

| Table 24 | Comparative Market Area Data | 79 | ||||||

| Table 25 | Summary of Recent Northeast Acquisition Activity | 84 | ||||||

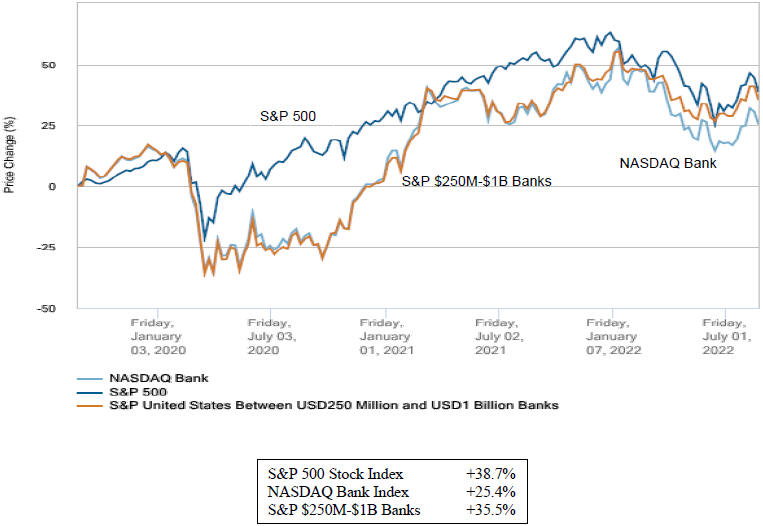

| Table 26 | Comparative Three-Year Stock Index Performance | 88 | ||||||

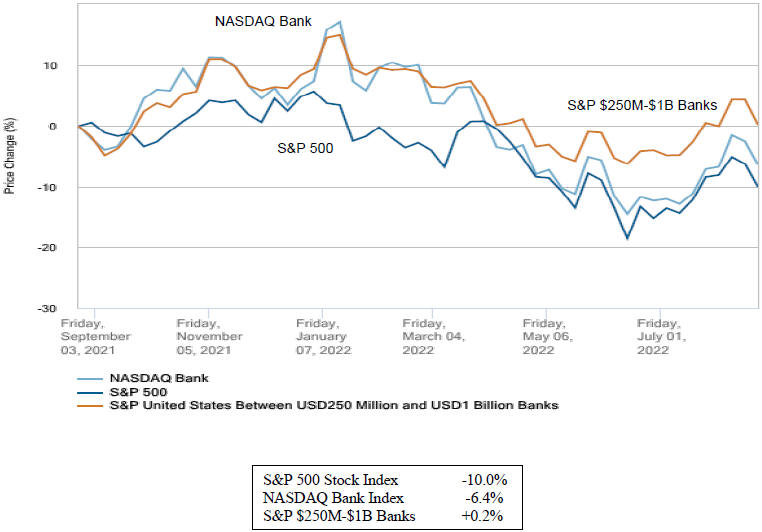

| Table 27 | Comparative One-Year Stock Index Performance | 89 | ||||||

| Table 28 | Summary of Recent Thrift Conversion Stock Offerings | 90 | ||||||

| Table 29 | Comparative Pro Forma Fully Converted Valuation Analysis | 98 | ||||||

ii

FELDMAN FINANCIAL ADVISORS, INC.

INTRODUCTION

At your request, we have completed and hereby provide an independent appraisal (the “Appraisal”) of the estimated pro forma market value of First Seacoast Bancorp (“FSB” or the “Company”) on a fully converted basis as of August 26, 2022 in conjunction with the Company’s conversion (the “Conversion”) from the two-tier mutual holding company structure to the fully stock holding company form of ownership and simultaneous offering (the “Stock Offering”) for sale the shares of common stock currently held by First Seacoast Bancorp, MHC (the “MHC”). The Company is a federally-chartered mid-tier stock holding company that owns all of the outstanding shares of common stock of First Seacoast Bank (the “Bank”). The MHC currently owns approximately 55.2% of the outstanding shares of common stock of FSB. The Appraisal is furnished pursuant to the filing by the MHC and the Company of an application (the “Application”) concerning the Conversion and Stock Offering with the Board of Governors of the Federal Reserve System (“Federal Reserve Board”).

Pursuant to the Plan of Conversion and Reorganization (“Plan of Conversion”), the MHC will be merged into FSB and, as a result, the MHC will cease to exist. FSB, which owns 100% of the outstanding common stock of the Bank, will merge into a new Maryland-chartered corporation named First Seacoast Bancorp, Inc. (“New FSB”) and, as a result, FSB will cease to exist. As part of the Conversion, the 55.2% ownership interest of the MHC in FSB will be offered for sale in the Stock Offering. When the Conversion is completed, New FSB will own all of the outstanding common stock of the Bank and public stockholders will own all of the outstanding common stock of New FSB.

In addition to the shares being sold in the Stock Offering, the shares of common stock of FSB currently owned by public stockholders will be exchanged for shares of common stock of New FSB based on an exchange ratio, subject to any necessary adjustment, that will result in existing public stockholders owning approximately the same percentage of common stock as they owned of the common stock of FSB immediately before the completion of the Conversion.

1

FELDMAN FINANCIAL ADVISORS, INC.

Feldman Financial Advisors, Inc. (“Feldman Financial”) is a financial consulting and economic research firm that specializes in financial valuations and analyses of business enterprises and securities in the thrift, banking, and mortgage industries. The background of Feldman Financial is presented in Exhibit I. In preparing the Appraisal, we conducted an analysis of the Company that included discussions with the Company’s management, the Company’s legal counsel, Luse Gorman, PC, and the Company’s independent registered public accounting firm, Baker Newman & Noyes LLC. In addition, where appropriate, we considered information based on other available published sources that we believe are reliable; however, we cannot guarantee the accuracy and completeness of such information.

We also reviewed, among other factors, the economy in the Company’s primary market area and compared the Company’s financial condition and operating performance with that of selected publicly traded thrift institutions. We reviewed conditions in the securities markets in general and in the market for thrift institution common stocks in particular.

The Appraisal is based on the Company’s representation that the information contained in the Application and additional evidence furnished to us by the Company and its independent auditor are truthful, accurate, and complete. We did not independently verify the financial statements and other information provided by the Company and its independent auditor, nor did we independently value the assets or liabilities of the Company. The Appraisal considers the Company only as a going concern and should not be considered as an indication of the liquidation value of the Company.

2

FELDMAN FINANCIAL ADVISORS, INC.

Our Appraisal is not intended, and must not be construed, to be a recommendation of any kind as to the advisability of purchasing shares of common stock in the Stock Offering. Moreover, because the Appraisal is necessarily based upon estimates and projections of a number of matters, all of which are subject to change from time to time, no assurance can be given that persons who purchase shares of stock in the Stock Offering will thereafter be able to sell such shares at prices related to the foregoing estimate of the Company’s pro forma market value. Feldman Financial is not a seller of securities within the meaning of any federal or state securities laws, and any report prepared by Feldman Financial shall not be used as an offer or solicitation with respect to the purchase or sale of any securities.

The Valuation Range reported herein will be updated as appropriate. These updates will consider, among other factors, any developments or changes in the Company’s operating performance, financial condition, or management policies, and current conditions in the securities markets for thrift institution common stocks. Should any such new developments or changes be material, in our opinion, to the valuation of the Company, appropriate adjustments to the estimated pro forma market value will be made. The reasons for any such adjustments will be explained in detail at that time.

3

FELDMAN FINANCIAL ADVISORS, INC.

I. BUSINESS OF FIRST SEACOAST BANCORP

General Overview

First Seacoast Bancorp is the publicly traded stock holding company of First Seacoast Bank. The Company was established in conjunction with the reorganization to the mutual holding company structure in July 2019. The Company raised gross proceeds of $26.8 million in the initial capital offering and became part of a two-tier mutual holding company structure. Established in 1890, the Bank is a federally-chartered stock savings bank headquartered in Dover, New Hampshire. In 2019, the Bank also completed a name change from Federal Savings Bank. The name change was intended to enhance brand and marketing visibility and associate the Bank by name with the New Hampshire and southern Maine Seacoast Region, which the Bank serves and considers to be its primary market area. Unless described otherwise herein, the operations of the Company refer to the consolidated operations of FSB with the Bank.

The Company’s business consists primarily of taking deposits from the general public and investing those deposits, together with funds generated from operations and borrowings from the Federal Home Loan Bank (“FHLB”), in one- to four-family residential real estate loans, commercial real estate and multi-family loans, commercial business loans, construction and land development loans, home equity loans and lines of credit, and consumer loans. In recent years, the Company has increased its focus on originating higher-yielding commercial real estate and commercial business loans, and intends to continue expanding its portfolio of non-residential loans.

FSB conducts its operations from four full-service banking offices in Strafford County, New Hampshire and one full-service banking office in Rockingham County, New Hampshire. The Company considers its primary lending market area to be Strafford and Rockingham counties in New Hampshire and York County in southern Maine. At June 30, 2022, the

4

FELDMAN FINANCIAL ADVISORS, INC.

Company had total assets of $510.2 million, total deposits of $387.9 million, and total equity of $51.9 million (10.17% of assets). The Company reported net income of $2.6 million for the year ended December 31, 2021 and net income of $572,000 for the six months ended June 30, 2022. The Bank’s deposits are insured up to applicable limits by the Federal Deposit Insurance Corporation (“FDIC”). The Bank is subject to regulation and examination by the Office of the Comptroller of the Currency, its primary federal regulator, and the FDIC, its deposit insurer. The Bank is also a member of the FHLB of Boston. The Company is subject to regulation by the Federal Reserve Board.

The Bank has served residents of the Seacoast Region of New Hampshire since 1890. Originally established as Dover Co-Operative Savings Fund and Loan Association, the Bank was subsequently known as Dover Co-Operative Bank and later became Dover Federal Savings and Loan Association. The Bank’s present main office at 633 Central Avenue in Dover was constructed in 1972. The Bank’s name was changed to Federal Savings Bank in 1983 to reflect a growing customer base in areas outside of Dover.

Historically, the Bank has operated as a conservative residential lender with a focus on managing growth and increasing its capital. The Bank’s assets expanded at a compound annual growth rate (“CAGR”) of 4.8% and increased from $165.3 million at December 31, 2000 to $387.1 million at December 31, 2018. While the Bank’s primary lending thrust has centered on the origination of residential mortgage loans, FSB has steadily expanded its balances of commercial real estate loans and commercial business loans. Following the initial offering in 2019, the Company has grown at a more accelerated pace in an attempt to redeploy and leverage the additional capital. Total assets have expanded at a CAGR of 8.2% or an increase of $123.1 million from $387.1 million at December 31, 2018 to $510.2 million at June 30, 2022.

5

FELDMAN FINANCIAL ADVISORS, INC.

The Company has continued its track record of maintaining excellent asset quality. The Company’s ratio of non-performing assets to total assets measured 0.12% at June 30, 2022. While the Company has enjoyed steady asset growth, improved capital ratios, and outstanding asset quality, its profitability has been rather undistinguished. From 2010 to 2018, the Bank reported consecutive years of positive earnings with an average return on assets (“ROA”) of 0.35%. Excluding non-recurring items, the Company reported a core ROA of 0.12%, 0.17%, and 0.46% for 2019, 2020, and 2021, respectively.

The Company’s earnings generally have been hampered by relatively high levels of non-interest expense and low levels of non-interest income. The recent increases in operating expenses have mostly reflected FSB’s investment in staffing, systems, and infrastructure to facilitate the implementation and management of its organic growth strategies. The Company believes that these expenditures and enhancements help position it to take advantage of growth opportunities given the attractive demographics of its primary market area. In addition, the Company also faces intensified competition from other financial institutions, including new entrants, because of the favorable market attributes and must also seek to defend its market share penetration from further encroachment.

The Seacoast Region benefits from an economy with high employment, rising home values, and a migration of individuals from out-of-state. The Company is optimistic about the growth of business and residential real estate activity in the current environment. Rising operating costs for employees, healthcare, technology, compliance, and other expenses, combined with a relatively low interest rate environment, remain as financial challenges for the Company.

6

FELDMAN FINANCIAL ADVISORS, INC.

The Company has continued to pursue a business strategy that is intended to improve long-term profitability and optimize its capital position. Among other initiatives, the business strategy emphasizes: (1) maintaining a conservative balance sheet; (2) investing in personnel, technology, and marketing; (3) enhancing asset quality; and (4) maintaining an effective risk management system. The Company’s long-term strategic objectives focus on (1) earnings growth, (2) capital planning, (3) asset growth, and (4) cost control and efficiency. The earnings growth objective is aimed primarily at achieving commercial real estate and residential mortgage loan growth along with wealth management and deposit fee income growth. The capital planning objective will be furthered through the completion of the planned Conversion and Stock Offering and emphasizes leveraging the capital base and enhancing long-term shareholder returns. The asset growth objective will be facilitated by realizing growth in commercial real estate, residential mortgage, commercial business, and consumer loan originations and expanding business development initiatives. The cost control and efficiency objective will be achieved partially by leveraging the operating infrastructure to generate increased revenue and asset growth to improve the efficiency ratio and also by expanding digital banking offerings.

The Company believes that its community orientation is attractive to customers and distinguishes it from the larger banks that operate in the local market area. The Company continues to stress high quality, personal customer service through an honest, straightforward, and upfront marketing approach and has developed a loyal customer base. The Company relies on its experienced and committed staff to meet the needs of customers and effectively deliver banking products and services.

7

FELDMAN FINANCIAL ADVISORS, INC.

The core elements of the Company’s business strategy are outlined in more detail below:

| • | Grow the balance sheet, leverage existing infrastructure, and improve profitability and operating efficiency. Given the Company’s existing infrastructure and capabilities, FSB believes it is well-positioned to grow without a proportional increase in overhead expense or operating risk. In recent years, it has assembled an experienced management team and selectively hired lending, business development, and support staff. The Company’s operations also benefit from established marketing, sales, information technology, cybersecurity, and audit and compliance departments. Additionally, FSB continues to invest in digital banking technologies. |

| • | Grow the loan portfolio and increase commercial real estate and commercial business lending. The Company’s principal loan origination activity remains primarily one- to four-family residential mortgage loans. The Company continues to supplement these originations by focusing on originating higher-yielding commercial real estate loans (including owner-occupied and non-owner-occupied commercial real estate and multi-family loans), construction loans, commercial business loans, and home equity loans and lines of credit. The Company intends to remain a residential mortgage lender in its market area while maintaining its focus on the origination of commercial real estate loans and commercial business loans. The additional capital that FSB is raising in the Stock Offering will increase the Bank’s legal lending limit, which will enable it to originate larger loans for portfolio retention to new and existing customers and reduce the need to participate with other lenders to originate larger loans. |

| • | Maintain strong asset quality and manage credit risk. Strong asset quality is a key to the long-term financial success of any financial institution. FSB has been successful in maintaining strong asset quality in recent years. The Company’s ratio of non-performing assets to total assets was 0.20%, 0.17%, and 0.12% at December 31, 2020, December 31, 2021, and June 30, 2022, respectively. FSB attributes this historical credit quality to a conservative credit culture and an effective credit risk management environment. The Company believes that it has an experienced team of credit professionals, well-defined and implemented credit monitoring policies and procedures, and conservative loan underwriting criteria. |

| • | Increase core deposits and reduce reliance on higher cost borrowings. Deposits are the Company’s primary source of funds for lending and investment. Core deposits (which are defined as all deposits except for certificates of deposit), particularly non-interest-bearing demand deposits, represent a low-cost, stable source of funds. Core deposits amounted to 85.9% of the Company’s total deposits at June 30, 2022, which level has increased from 77.2% at December 31, 2018. The Company also relies on higher cost FHLB borrowings as a supplemental funding source. At June 30, 2022, the Company’s ratio of net loans to deposits was 98.5% and FHLB borrowings totaled $64.3 million. The Company intends to continue to focus on expanding core deposits by leveraging its business development activities and commercial lending and retail relationships. |

8

FELDMAN FINANCIAL ADVISORS, INC.

| • | Grow organically and through opportunistic expansion. The Company’s primary intention is to grow its balance sheet organically and utilize its capital to increase its lending and investment capacity. As a local independent financial institution, FSB believes that it will have opportunities to gain market share from customer fallout resulting from the recent consolidation of competing financial institutions in its market area into larger, out-of-market acquirers. In addition to organic growth, the Company may also consider expansion opportunities in its market area or in contiguous markets that it believes would enhance both its franchise value and stockholder returns. These opportunities chiefly include establishing loan production offices, establishing new, or de novo, branch offices and/or acquiring branch offices. However, the Company has no current plans or pending transactions regarding any expansion opportunities. |

While its equity level is solid at $51.9 million or 10.17% of total assets at June 30, 2022, FSB believes it must raise additional capital in order to facilitate its long-term growth objectives and loan generation activity, and provide a greater cushion in response to the risk profile associated with continued expansion and future economic conditions. Although the Company recorded positive earnings of $572,000 for the six months ended June 30, 2022, its equity capital declined by 14.2% or $8.6 million from $60.5 million at December 31, 2021, mainly due to unrealized holding losses on available-for-sale securities arising during the first half of the year.

The Company’s primary reasons for undertaking the Conversion and Stock Offering are to:

| • | Support the planned growth and strengthen the regulatory capital positions of the Company and the Bank with the additional capital raised in the Stock Offering. |

| • | Transition the organization to a fully stock holding company structure, which provides greater flexibility to access the capital markets as compared to the current mutual holding company structure. |

| • | Improve the liquidity of the Company’s shares of common stock by increasing the number of shares available for trading. |

| • | Facilitate the stock holding company’s ability to pay dividends to public stockholders by eliminating the mutual holding company structure, which entails a majority ownership stake that is held by a single entity. |

9

FELDMAN FINANCIAL ADVISORS, INC.

| • | Facilitate future mergers and acquisitions by increasing the Company’s flexibility to structure and finance the expansion of its operations as opportunities arise. |

The remainder of Chapter I examines in more detail the trends addressed in this section, including the impact of changes in the Company’s economic and competitive environment, and recent strategic initiatives. The discussion is supplemented by the exhibits in the Appendix. Exhibit II-1 summarizes the Company’s consolidated balance sheets as December 31, 2020 and 2021 and June 30, 2022. Exhibit II-2 presents the Company’s consolidated income statements for the years ended December 31, 2020 and 2021 and the six months ended June 30, 2021 and 2022.

10

FELDMAN FINANCIAL ADVISORS, INC.

Financial Condition

Table 1 presents selected data concerning the Company’s financial position as of December 31, 2020 and 2021 and June 30, 2022. Table 2 displays relative balance sheet concentrations for the Company as of similar year-end dates.

Table 1

Selected Financial Condition Data

As of December 31, 2020 and 2021 and June 30, 2022

(Dollars in Thousands)

| June 30, | December 31, | |||||||||||

| 2022 | 2021 | 2020 | ||||||||||

Total assets | $ | 510,246 | $ | 487,074 | $ | 443,062 | ||||||

Cash and cash equivalents (1) | 5,053 | 7,883 | 8,484 | |||||||||

Securities available-for-sale | 103,387 | 91,365 | 55,470 | |||||||||

Federal Home Loan Bank Stock | 2,684 | 1,688 | 1,796 | |||||||||

Total loans, net | 381,957 | 373,051 | 364,800 | |||||||||

Premises and equipment, net | 4,401 | 4,566 | 5,078 | |||||||||

Bank-owned life insurance | 4,502 | 4,461 | 4,356 | |||||||||

Total deposits | 387,868 | 393,243 | 327,381 | |||||||||

Borrowed funds | 64,250 | 29,462 | 52,322 | |||||||||

Total equity | 51,872 | 60,468 | 58,861 | |||||||||

| (1) | Includes interest-bearing time deposits with other banks. |

Source: First Seacoast Bancorp, financial statements.

Asset Composition

The Company’s total assets amounted to $510.2 million at June 30, 2022, reflecting an increase of 4.8% or $23.2 million during the six-month period from total assets of $487.1 million at December 31, 2021. In the prior year, the Company’s total assets increased by 9.9% or $44.0 million from $443.1 million at December 31, 2020 to $487.1 million at December 31, 2021. The recent increases in total assets were primarily attributable to increases in the holdings of loans

11

FELDMAN FINANCIAL ADVISORS, INC.

and investment securities funded by increases in total deposits and borrowings. Total loans increased by $17.5 million from $368.1 million at December 31, 2020 to $385.6 million at June 30, 2022, spurred by growth mainly in residential mortgage and commercial real estate loans and offset by a decline in commercial business loans due to the guaranteed forgiveness of Paycheck Protection Program (“PPP”) loans. Securities available-for-sale increased by $47.9 million from $55.5 million at December 31, 2020 to $103.4 million at June 30, 2022. Largely as a result of the increase in cash and investments, the ratio of net total loans to total assets declined from 82.3% at December 31, 2020 to 74.9% at June 30, 2022. Conversely, the aggregate balance of cash and investments increased from 14.8% at December 31, 2020 to 21.8% at June 30, 2022. Total deposits increased by $60.5 million from $327.4 million at December 31, 2020 to $387.9 million at June 30, 2020.

Table 2

Relative Balance Sheet Concentrations

As of December 31, 2020 and 2021 and June 30, 2022

(Percent of Total Assets)

| June 30, | December 31, | |||||||||||

| 2022 | 2021 | 2020 | ||||||||||

Cash and investments (1) | 21.78 | % | 20.72 | % | 14.84 | % | ||||||

Total loans, net | 74.86 | 76.59 | 82.34 | |||||||||

Premises and equipment, net | 0.86 | 0.94 | 1.15 | |||||||||

Bank-owned life insurance | 0.88 | 0.92 | 0.98 | |||||||||

Other assets | 1.62 | 0.83 | 0.69 | |||||||||

|

|

|

|

|

| |||||||

Total assets | 100.00 | % | 100.00 | % | 100.00 | % | ||||||

|

|

|

|

|

| |||||||

Total deposits | 76.02 | % | 80.74 | % | 73.89 | % | ||||||

Borrowed funds | 12.59 | 6.05 | 11.81 | |||||||||

Other liabilities | 1.23 | 0.80 | 1.02 | |||||||||

|

|

|

|

|

| |||||||

Total liabilities | 89.83 | 87.59 | 86.71 | |||||||||

Total equity | 10.17 | 12.41 | 13.29 | |||||||||

|

|

|

|

|

| |||||||

Total liabilities and equity | 100.00 | % | 100.00 | % | 100.00 | % | ||||||

|

|

|

|

|

| |||||||

| (1) | Includes cash equivalents, securities available-for-sale, and FHLB stock. |

Source: First Seacoast Bancorp, financial statements.

12

FELDMAN FINANCIAL ADVISORS, INC.

Lending is the Company’s principal business activity, and its loan portfolio constitutes the largest portion of its assets and is the predominant source of its income. The largest segment of the Company’s loan portfolio comprises real estate mortgage loans, consisting primarily of residential mortgage loans, commercial real estate and multi-family mortgage loans, and acquisition, development and land loans. Substantially all of the Company’s collateralized real estate loans are secured by properties located in the Company’s primary lending area.

As presented in Exhibit II-3, the Company’s current loan portfolio is composed substantially of real estate loans. At June 30, 2022, real estate loans comprised $352.6 million or 91.9% of the gross loan portfolio and included residential loans (including one- to four-family mortgages and home equity loans and lines of credit) and non-residential real estate loans (generally consisting of loans secured by commercial and multi-family real estate and acquisition, development, and land loans). Non-real estate loans chiefly comprised commercial business loans and a limited amount of consumer loans. The Company intends to continue to emphasize residential and commercial real estate lending with a focus on full-service relationship banking in its primary market area.

During the six months ended June 30, 2022, FSB originated $50.7 million of loans. For the year ended December 31, 2021, the Company originated $130.4 million of loans, including $13.1 million of PPP loans. During the year ended December 31, 2020, the Company originated $150.8 million of loans, including $33.0 million of PPP loans. In recent years, the Company has also periodically purchased one- to four-family residential mortgage loans and consumer loans secured by manufactured housing properties. As of June 30, 2022, the portfolio of purchased loans had an outstanding principal balance of $31.5 million and was performing in accordance with original repayment terms.

13

FELDMAN FINANCIAL ADVISORS, INC.

At June 30, 2022, FSB had $240.2 million in one- to four-family residential loans, which represented 62.6% of its total loan portfolio. One- to four-family residential loans outstanding increased by 9.6% in 2021 and by 2.6% for the first half of 2022. The Company’s one- to four-family residential real estate loans have terms of up to 30 years and are generally underwritten according to Freddie Mac guidelines. At June 30, 2022, approximately 97.1% of the Company’s one- to four-family residential real estate loans were fixed-rate loans. The Company sells a portion of fixed-rate conforming loans that it originates on a servicing-retained basis. Secondary market investors that purchase the Company’s loans include Freddie Mac and the New Hampshire Housing Finance Authority. For the year ended December 31, 2020 and 2021, the Company sold $12.0 million and $6.2 million, respectively, of one- to four-family residential mortgage loans. Loan sales of one- to four-family residential loans amounted to $495,000 for the first half of 2022. The Company’s portfolio of loans serviced for others amounted to $37.7 million at June 30, 2022.

At June 30, 2022, approximately 2.9% of the Company’s residential mortgage loans were adjustable-rate loans. The Company’s adjustable-rate mortgage loans have initial re-pricing terms of one, three, or five years. Following the initial re-pricing term, such loans adjust annually for the balance of the loan term. Adjustable-rate mortgage loans are indexed to the one-year U.S. Treasury constant maturity rate, plus a margin. The Company typically retains its adjustable-rate residential mortgage loans in portfolio. The Company does not offer “interest only” mortgage loans on permanent residential mortgage loans, and also does not offer residential mortgage loans that provide for negative amortization or principal or contain any other subprime loan characteristics.

14

FELDMAN FINANCIAL ADVISORS, INC.

In past years, the Company has purchased one- to four-family jumbo residential mortgage loans to supplement its own origination efforts. The Company did not purchase any such loans during the six months ended June 30, 2022. During the years ended December 31, 2020 and 2021, the Company purchased $9.9 million and $14.1 million and $9.9 million, respectively, of one- to four-family jumbo residential mortgage loans secured by properties located in the greater Boston market. As of June 30, 2022, the portfolio of purchased residential real estate loans had an outstanding principal balance of $26.5 million and these loans were performing in accordance with their original repayment terms.

As of June 30, 2022, the Company had $86.0 million in commercial real estate and multi-family real estate loans, which represented 22.4% of its total loan portfolio. The Company’s commercial real estate lending activity is consistent with its strategy to diversify the loan portfolio and increase the overall portfolio yield. The Company’s commercial real estate loans are secured by a variety of properties in FSB’s primary market area, including retail spaces, distribution centers, office buildings, manufacturing and warehouse properties, convenience stores, and other local businesses. The Company’s multi-family real estate loans, which amounted to $8.7 million at June 30, 2022, are secured by properties consisting of five or more rental units in the Company’s market area, including apartment buildings and student housing.

The Company’s commercial real estate and multi-family loans are generally originated as 10-year balloon loans, which reprice after five years and are amortized over 20 years. Interest rates on such loans are generally indexed to the FHLB of Boston five-year regular advance rate, plus a margin. The maximum loan-to-value ratio of the Company’s commercial real estate loans is generally 80% of the lower of purchase price or appraised value of the properties securing the loan and generally requires a minimum debt-service coverage ratio of 1.2x. On a limited basis, the Company also purchases and participates in commercial real estate loans from other financial institutions. Such loans are subject to the same underwriting criteria and loan approval requirements applied to loans originated by the Company. At June 30, 2022, the Company had outstanding participation interests totaling $20.6 million.

15

FELDMAN FINANCIAL ADVISORS, INC.

At June 30, 2022, the Company had $17.1 million in acquisition, development and land loans, which represented 4.5% of its total loan portfolio. Acquisition, development and loan loans decreased from $23.1 million at year-end 2020 and $21.4 million at year-end 2021. These loans consist of residential construction loans, commercial real estate construction loans, and land loans. The Company originates loans to finance the construction or rehabilitation of owner-occupied one- to four-family residential properties to prospective homeowners primarily located in its market area. Upon completion of construction, such loans convert to permanent mortgage loans. At June 30, 2022, residential construction loan balances amounted to $8.1 million or 2.1% of the total loan portfolio, with an additional $16.7 million available for advance to borrowers. Residential construction loans are generally structured as interest-only for nine months, with a loan-to-value ratio generally not exceeding 80% of the appraised value on a completed basis or the cost of completion, whichever is less.

The Company also originates loans to finance the construction of commercial properties, primarily owner-occupied properties located in its market area. Upon completion of construction, such loans convert to permanent commercial mortgage loans. At June 30, 2022, commercial construction loan balances totaled $8.1 million or 2.1% of the total loan portfolio, with an additional $4.7 million available for advance to borrowers. Commercial real estate construction loans are generally structured as interest-only for up to 18 months, with a loan-to-value ratio of up to 80% of the appraised value on a completed basis or a loan-to-cost of completion ratio of up to 85%. The Company also originated loans to finance the acquisition and development of land. Land development loans are generally secured by vacant land in the process of improvement. At June 30, 2022, land development loan balances amounted to $888,000 or 0.2% of the total loan portfolio.

16

FELDMAN FINANCIAL ADVISORS, INC.

At June 30, 2022, the Company had $24.6 million in commercial business loans, which represented 6.4% of its total loan portfolio. Commercial business loans outstanding increased from $24.7 million at year-end 2019 to $45.3 million at year-end 2020, largely due to the origination of PPP loans. Subsequently, as a result of the PPP loan forgiveness program, the Company’s commercial business loans outstanding returned to a more normalized level in 2021 and the first half of 2022. During the year ended December 31, 2020 and 2021, the Company originated 286 and 134 PPP loans, respectively, with aggregate principal balances of $33.0 million and $13.1 million, respectively. The Company’s remaining PPP loans outstanding amounted to $139,000 as of June 30, 2022.

The Company’s commercial business loans include equipment loans, business acquisition loans, and lines of credit to businesses operating in the local market area. The Company’s commercial business loans are generally used by the borrowers for working capital purposes or for acquiring equipment, inventory, or furniture. These loans are generally secured by non-real estate business and personal assets, including equipment, inventory, accounts receivable, and marketable securities, although the Company may support this collateral with liens on real property such as buildings and other equipment. FSB generally requires its commercial business borrowers to maintain their primary deposit accounts with the Company, which help to improve the Company’s overall interest rate spread and profitability. The Company’s commercial business loans include term loans and revolving lines of credit and are made with either variable or fixed rates of interest. Variable interest rates are indexed to the prime rate as published in The Wall Street Journal, plus a margin. The Company also originates commercial business loans through specific loan programs overseen and partially guaranteed by the Small Business Administration (“SBA”). The aggregate SBA loans amounted to $1.4 million at June 30, 2022.

17

FELDMAN FINANCIAL ADVISORS, INC.

The Company had $9.2 million of home equity loans and lines of credit as of June 30, 2022, representing 2.4% of total loans. FSB offers home equity loans and lines of credit, which are multi-purpose loans used to finance various home or personal needs, where a one- to four-family primary or secondary residence serves as collateral. At June 30, 2022, the Company’s home equity lines of credit had an additional $21.1 million available to draw. Home equity loans are originated by the Company as fixed-rate term loans. Home equity lines of credit are tied to the prime rate as published in The Wall Street Journal and are offered for terms of up to 25 years, with a 10-year draw period and 15-year repayment period. Generally, the Company’s home equity loans and lines of credit are originated with loan-to-value ratios of up to 80%, inclusive of existing liens on the property.

At June 30, 2022, the Company’s consumer loans amounted to $6.2 million, representing 1.6% of total loans. The Company offers consumer loans to individuals who reside or work in its primary market area. Consumer lending has been a minor area of lending diversification for the Company. Consumer loans generally consist of installment loans extended directly to the borrower. Management believes that offering consumer loan products helps to expand and create stronger ties to its existing customer base by increasing the number of customer relationships and cross-marketing opportunities. FSB expects that growth of this segment of the consumer loan portfolio will be limited, with such loans extended primarily to existing customers of the Company. The Company also purchases consumer loans secured by manufactured housing properties. The Company purchased $1.5 million, $2.0 million, and $1.2 million of these loans during 2020, 2021, and the first half of 2022, respectively, which are secured by properties located in the greater Seacoast region. The Company expects that growth in this segment of its consumer loan portfolio will continue to increase in the future.

18

FELDMAN FINANCIAL ADVISORS, INC.

Exhibit II-4 presents a summary of the Company’s portfolio of cash, liquidity, and investments as of December 31, 2020 and 2021 and June 30, 2022. The Company’s primary investment objectives include the following: (1) provide and maintain liquidity to meet deposit withdrawal and loan funding needs; (2) help mitigate interest rate and market risk; (3) diversify the Company’s assets; and (4) generate a reasonable rate of return on funds within the context of the Company’s interest rate and credit risk objectives. FSB’s Board of Directors is responsible for annually adopting and reviewing the investment policy of the Company. FSB’s Asset/ Liability Management Committee (“ALCO”) is responsible for implementing the Company’s investment policy. Authority to make investments under the approved investment policy guidelines is delegated to the President and Chief Executive Officer, Chief Financial Officer, and Finance Officer. All of the Company’s investment securities are classified as available-for-sale.

At June 30, 2022, the Company’s cash and investments amounted to $111.1 million or 21.8% of total assets. Cash and cash equivalents along with certificates of deposit in other financial institutions amounted to $5.1 million or 4.6% of the Company’s total cash and investments as of June 30, 2022. The Company’s available-for-sale securities portfolio totaled $103.8 million at June 30, 2022 and was composed of municipal bonds, U.S. Government-sponsored enterprises (“GSEs”) obligations, residential mortgage-backed securities, U.S. Government agency pools guaranteed by the SBA, and corporate subordinated debt. Municipal bonds, which amounted to $53.3 million, represented the largest segment of the investment

19

FELDMAN FINANCIAL ADVISORS, INC.

portfolio at June 30, 2022. For the quarter ended June 30, 2022, the Company’s taxable and non-taxable debt securities had yields of 1.86% and 2.49%, respectively. The Company also owned $2.7 million of stock in the FHLB of Boston as of June 30, 2022. Due to a rise in interest rates during the first half of 2022, the Company’s securities available-for-sale changed from a position of $788,000 in net unrealized holding gains as of December 31, 2021 to $11.8 million in net unrealized holding losses as of June 30, 2022. Management has indicated that it has no current plans for sales of securities in the portfolio that would result in realizing the magnitude of losses currently reflected by the fair values of the portfolio, nor does it believe that the declines in fair values were related to changes in the underlying credit quality of the securities.

Liability Composition

Deposits are the Company’s primary external source of funds for lending and other investment purposes. The Company has also utilized used borrowings actively to supplement deposits as a funding source. Exhibit II-5 presents a summary of the Company’s deposit composition as of December 31, 2020 and 2021 and June 30, 2022. Total deposits amounted to $274.4 million or 76.0% of total assets and 84.6% of total liabilities at June 30, 2022. Total deposits decreased by 1.4% or $5.3 million from $393.2 million at December 31, 2021 to $387.9 million at June 30, 2022, after increasing by 20.1% or $65.8 million from $327.4 million at December 31, 2020 to $393.2 million at December 31, 2021. Recent deposit growth has largely been concentrated in the Company’s checking accounts and savings deposits, which increased by $43.9 million and $16.0 million from December 31, 2020 to June 30, 2022.

20

FELDMAN FINANCIAL ADVISORS, INC.

FSB relies on personalized customer service, longstanding relationships with customers, and the favorable image of the Company in its primary market area to attract and retain deposits. Deposit account terms vary according to the minimum balance required, the time period that funds must remain on deposit, and the interest rate, among other factors. In determining the terms of its deposit accounts, the Company considers the rates offered by its competition, its liquidity needs, profitability, and customer preferences and concerns. FSB generally reviews its deposit pricing on a monthly basis and continually reviews its deposit mix. The Company’s deposit pricing strategy has generally been to offer competitive rates, while generally not providing the highest rates in the market. The Company finds it more profitable to concentrate on specific special rate and term accounts, which allows it to increase certain deposits without impacting the Company’s overall liability costs for existing accounts. FSB also relies on customer service, convenience of its branch office locations, advertising, and existing customers to gather and develop deposit relationships.

The Company has placed a concerted emphasis on attracting core (non-certificate) deposit accounts, which tend to represent low cost and more stable funding sources. Core deposits composed 85.9% or $333.1 million of total deposits at June 30, 2022, which reflected increases from 76.8% of total deposits or $188.4 million at December 31, 2016. For the quarter ended, the Company’s weighted average cost of core deposits was 0.06%, the cost of certificate deposits was 0.50%, and the overall cost of total deposits was 0.12% (inclusive of non-interest bearing accounts).

Developing comprehensive banking relationships has been a key priority for FSB and is a focus of its commercial lending and business development officers. In recent years, the Company has introduced new business deposit products to appeal to its commercial borrowers. At June 30, 2022, the ratio of commercial deposits to commercial loans (including commercial real estate loans, commercial business loans, and acquisition, development, and land loans) was 89.8%.

21

FELDMAN FINANCIAL ADVISORS, INC.

As a member of the FHLB of Boston, the Company may obtain FHLB borrowings based upon the security of FHLB capital stock owned and certain of the Company’s real estate mortgage loans. Such advances may be made pursuant to several different credit programs, each of which has its own interest rate terms and range of maturities. The Company uses FHLB advances to provide short-term funding as a supplement to its deposits. As of June 30, 2022, the Company had $64.3 million in FHLB advances outstanding and $58.0 million in additional borrowing capacity from the FHLB of Boston. The Company could access additional FHLB advances if it purchased additional FHLB of Boston capital stock.

Equity Capital

The Company has historically maintained solid capital levels. As the Company has steadily expanded its asset base, the ratio of total equity to total assets has declined. The total equity to total assets ratio decreased from 13.94% at December 31, 2019 to 10.17% at June 30, 2022. Because of the Company’s consistently below-average level of profitability, its incremental equity accumulation has been slow. Furthermore, the increase in net unrealized holding losses resulted in a sharp decline in equity capital during the first half of 2022.

The Company’s equity capital declined from $60.5 million or 12.41% of total assets at December 31, 2021 to $51.9 million or 10.17% of total assets at June 30, 2022. The reduction in equity during the first half of 2022 was due primarily to a reduction in accumulated other comprehensive income (“AOCI”) of $8.8 million related mainly to net changes in unrealized holding losses in the available-for-sale securities portfolio as a result of an increase in market interest rates during the period and common stock repurchases of $623,000, partially offset by the recognition of net income of $572,000 for the six months ended June 30, 2022.

22

FELDMAN FINANCIAL ADVISORS, INC.

The Bank’s capital level remains solid in comparison to minimum regulatory requirements. The Bank’s regulatory capital ratios of tier 1 leverage capital, common equity tier 1 risk-based capital, tier 1 risk-based capital, and total risk-based capital were 10.01%, 15.56%, 15.56%, and 16.70%, respectively, as of June 30, 2022. In comparison, the minimum regulatory requirements under federal banking agency guidelines were 4.00%, 4.50%, 6.00%, and 8.00%, and the threshold requirements for regulatory “well capitalized” levels were 5.00%, 6.50%, 8.00%, and 10.00%, respectively. Based on these regulatory capital ratios and requirements, the Bank was considered well capitalized for regulatory purposes as of June 30, 2022.

The Bank’s tier 1 capital amounted to $50.4 million as of June 30, 2022, as compared to the Bank’s equity capital of $42.7 million. The difference was primarily attributed to the net unrealized holding losses being excluded from tier 1 capital for regulatory purposes. Consistent with regulatory capital rules in effect, the Bank previously elected to opt out of the requirement to include most components of AOCI in regulatory capital. Therefore, the Bank’s AOCI in the amount of negative $8.1 million as of June 30, 2022 was added back to compute tier 1 capital for regulatory capital purposes.

The Company assesses its securities available-for-sale each quarter, or more often if a potential loss triggering event occurs, and considers the extent and duration of any unrealized losses and the financial condition and near-term prospects of the issuers. As of June 30, 2022, the Company did not intend to sell its investment securities available-for-sale and indicated it was unlikely that it would have had to sell them before recovery of their amortized cost, which may be at maturity. Furthermore, the Company believed that the unrealized holding losses at June 30, 2022 were primarily due to market interest rate fluctuations and not changes in credit quality.

23

FELDMAN FINANCIAL ADVISORS, INC.

Income and Expense Trends

Table 3 displays the main components of the Company’s earnings performance for the years ended December 31, 2020 and 2021 and the six months ended June 30, 2021 and 2022. Table 4 displays the Company’s principal income and expense ratios as a percent of average assets for the corresponding periods. Table 5 displays the Company’s weighted average yields on interest-earning assets and weighted average costs of interest-bearing liabilities for the years ended December 31, 2020 and 2021 and the six months ended June 30, 2021 and 2022.

General Overview

Over recent years, the Company has exhibited a record of low to moderate profitability. The Company’s average core ROA (excluding non-recurring items) for the past five years ended December 31, 2021 was approximately 0.27%, and reflected core ROA results of 0.30%, 0.29%, 0.12%, 0.17%, and 0.46% for 2017, 2018, 2019, 2020, and 2021, respectively. The Company reported an annualized core ROA of 0.21% for the six months ended June 30, 2022. Compared to its FDIC-insured institution peer group, the Company’s profitability trends can be characterized by above-average net interest margins, offset by relatively low levels of non-interest income and comparatively high operating expense ratios.

The Company’s earnings performance reflected a net loss of $79,000 in 2019 that resulted chiefly from a charitable foundation contribution expense of $758,000. The Company reported improved earnings of $1.1 million for 2020 and $2.6 million in 2021 as balance sheet growth drove increases in net interest income and securities gains augmented non-interest income. The Company’s net income amounted to $572,000 for the first half of 2022, representing an annualized ROA of 0.23% and an annualized return on average equity (“ROE”) of 2.02%.

24

FELDMAN FINANCIAL ADVISORS, INC.

Table 3

Income Statement Summary

For the Years Ended December 31, 2020 and 2021

And the Six Months Ended June 30, 2021 and 2022

(Dollars in Thousands)

| Six Months Ended | Year Ended | |||||||||||||||

| June 30, | December 31, | |||||||||||||||

| 2022 | 2021 | 2021 | 2020 | |||||||||||||

Interest income | $ | 7,922 | $ | 7,813 | $ | 15,495 | $ | 15,850 | ||||||||

Interest expense | 391 | 512 | 1,235 | 3,174 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Net interest income | 7,531 | 7,301 | 14,260 | 12,676 | ||||||||||||

Provision for loan losses | 60 | 85 | 205 | 480 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Net interest income after provision | 7,471 | 7,216 | 14,055 | 12,196 | ||||||||||||

Non-interest operating income | 788 | 844 | 1,714 | 1,636 | ||||||||||||

Securities gains, net | 52 | 535 | 535 | 410 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Non-interest income | 840 | 1,379 | 2,249 | 2,046 | ||||||||||||

Non-interest expense | 7,615 | 6,425 | 13,082 | 13,187 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Income before income tax expense | 696 | 2,170 | 3,222 | 1,055 | ||||||||||||

Income tax expense (benefit) | 124 | 429 | 601 | (24 | ) | |||||||||||

|

|

|

|

|

|

|

| |||||||||

Net income | $ | 572 | $ | 1,741 | $ | 2,621 | $ | 1,079 | ||||||||

|

|

|

|

|

|

|

| |||||||||

Source: First Seacoast Bancorp, financial statements.

Six Months Ended June 30, 2021 and 2022

Net income was $572,000 for the six months ended June 30, 2022, compared to $1.7 million for the six months ended June 30, 2021, a decrease of $1.2 million, or 67.1%. The decrease was due primarily to an increase in non-interest expense of $1.2 million and a decrease in non-interest income of $539,000 (including a decrease of $483,000 in net securities gains), offset by an increase in net interest income of $230,000. The Company’s annualized ROA decreased from 0.75% for the first half of 2021 to 0.23% for the first half of 2022.

25

FELDMAN FINANCIAL ADVISORS, INC.

Table 4

Income Statement Ratios

For the Years Ended December 31, 2020 and 2021

And the Six Months Ended June 30, 2021 and 2022

(Percent of Average Assets)

| Six Months Ended | Year Ended | |||||||||||||||

| June 30, | December 31, | |||||||||||||||

| 2022 | 2021 | 2021 | 2020 | |||||||||||||

Interest income | 3.17 | % | 3.35 | % | 3.23 | % | 3.50 | % | ||||||||

Interest expense | 0.16 | 0.21 | 0.26 | 0.70 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Net interest income | 3.02 | 3.13 | 2.97 | 2.80 | ||||||||||||

Provision for loan losses | 0.02 | 0.04 | 0.04 | 0.11 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Net interest income after provision | 2.99 | 3.10 | 2.93 | 2.70 | ||||||||||||

Non-interest operating income | 0.32 | 0.36 | 0.36 | 0.36 | ||||||||||||

Securities gains, net | 0.02 | 0.23 | 0.11 | 0.09 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Non-interest income | 0.34 | 0.59 | 0.47 | 0.45 | ||||||||||||

Non-interest expense | 3.05 | 2.76 | 2.73 | 2.91 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Income before income tax expense | 0.28 | 0.92 | 0.67 | 0.23 | ||||||||||||

Income tax expense | 0.05 | 0.18 | 0.13 | (0.01 | ) | |||||||||||

|

|

|

|

|

|

|

| |||||||||

Net income | 0.23 | 0.75 | 0.55 | 0.24 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Source: First Seacoast Bancorp, financial statements and offering prospectus.

Net interest income increased by $230,000 or 3.2% to $7.5 million for the six months ended June 30, 2022 from $7.3 million for the six months ended June 30, 2021. This increase was primarily due to a $31.2 million or 6.9% increase in the average balance of interest-earning assets, consisting primarily of increases in the average balances of loans and debt securities, offset by an increase of $8.8 million or 2.6%, in the average balance of interest-bearing liabilities (consisting primarily of an increase in the average balance of borrowings) during the six months ended June 30, 2022. The Company’s annualized net interest margin decreased to 3.10% for the

26

FELDMAN FINANCIAL ADVISORS, INC.

six months ended June 30, 2022 from 3.22% for the six months ended June 30, 2021 due primarily to a decrease in the average yield on loans (3.89% to 3.64%) offset by an increase in the average yield on debt securities (1.89% to 2.02%) and a decrease in the average cost of funds (0.25% to 0.18%). Based on management’s analysis of the allowance for loan losses, a $60,000 provision for loan losses was recorded for the six months ended June 30, 2022, compared to $85,000 for the six months ended June 30, 2021.

Non-interest income decreased $539,000 or 39.1% to $840,000 for the six months ended June 30, 2022, compared to $1.4 million for the six months ended June 30, 2021. The decrease in non-interest income during the first half of 2022 was due primarily to a $483,000 decrease in net securities gains, an $86,000 decrease in gain on sale of loans, and a $27,000 decrease in customer service fees, offset by a $58,000 increase in investment services fees. The annualized ratio of non-interest income to average assets declined from 0.59% for the first half of 2021 to 0.34% for the first half of 2022. Excluding net securities gains, the ratio of non-interest operating income to average assets declined from 0.36% to 0.32% over the corresponding six-month periods.

Investment services fees increased from $118,000 for the first half of 2021 to $176,000 for the first half of 2022. The Company offers investment management services through FSB Wealth Management, which operates as a division of the Bank. FSB Wealth Management provides customers with access to investment products that include retirement planning, portfolio management, investment and insurance strategies, business retirement plans, and college planning. These investments and services are offered through a third-party registered broker-dealer and investment advisor. FSB Wealth Management receives fees from advisory services and commissions on individual investment and insurance products purchased by clients.

27

FELDMAN FINANCIAL ADVISORS, INC.

Table 5

Yield and Cost Summary

For the Years Ended December 31, 2020 and 2021

And the Six Months Ended June 30, 2021 and 2022

| Six Months Ended | Year Ended | |||||||||||||||

| June 30, | December 31, | |||||||||||||||

| 2022 | 2021 | 2021 | 2020 | |||||||||||||

Weighted Average Yields | ||||||||||||||||

Loans | 3.64 | 3.89 | % | 3.79 | % | 3.95 | % | |||||||||

Taxable debt securities | 1.70 | 1.01 | 1.27 | 1.60 | ||||||||||||

Non-taxable debt securities | 2.37 | 2.39 | 2.31 | 2.52 | ||||||||||||

Interest-bearing deposits | 0.66 | 0.33 | 0.28 | 0.43 | ||||||||||||

Federal Home Loan Bank stock | 2.06 | 0.21 | 1.17 | 4.18 | ||||||||||||

Total interest-earning assets | 3.26 | 3.44 | 3.31 | 3.60 | ||||||||||||

Weighted Average Costs | ||||||||||||||||

NOW and demand deposits | 0.09 | 0.13 | 0.12 | 0.23 | ||||||||||||

Money market deposits | 0.11 | 0.15 | 0.14 | 0.59 | ||||||||||||

Savings deposits | 0.04 | 0.06 | 0.06 | 0.10 | ||||||||||||

Certificates of deposit | 0.52 | 0.64 | 0.56 | 1.49 | ||||||||||||

Total interest-bearing deposits | 0.17 | 0.23 | 0.20 | 0.58 | ||||||||||||

Borrowings | 0.61 | 0.84 | 1.57 | 2.33 | ||||||||||||

Total interest-bearing liabilities | 0.23 | 0.31 | 0.37 | 0.95 | ||||||||||||

Net interest rate spread (1) | 3.03 | 3.13 | 2.94 | 2.65 | ||||||||||||

Net interest margin (2) | 3.10 | 3.22 | 3.04 | 2.88 | ||||||||||||

| (1) | Weighted average yield on interest-earning assets less the weighted average cost of interest-bearing liabilities. |

| (2) | Net interest income divided by average total interest-earning assets. |

Source: First Seacoast Bancorp, offering prospectus.

In August 2021, the Company entered into a definitive agreement with an investment advisory and wealth management firm to purchase certain of its client accounts and client relationships for a purchase price of $347,000. As of June 30, 2022, approximately $23.4 million of purchased client accounts are included in the Company’s total assets under management. The Company’s assets under management totaled $85.6 million, $88.0 million, and $58.4 million at June 30, 2022, December 31, 2021, and December 31, 2020, respectively. The client accounts purchased are recorded as a customer list intangible asset. The Company is amortizing the customer list intangible on a straight-line basis over a 10-year period. As of June 30, 2022, the unamortized balance of the customer list intangible was $316,000.

28

FELDMAN FINANCIAL ADVISORS, INC.

Non-interest expense increased by $1.2 million or 18.5% to $7.6 million for the six months ended June 30, 2022, compared to $6.4 million for the six months ended June 30, 2021. The increase in non-interest expense was due primarily to a $926,000 or 24.7% increase in salaries and employee benefits expense. The increase in salaries and benefits expense during the six months ended June 30, 2022 was due to filling certain open positions and associated recruitment fees, normal salary increases, and the recognition of compensation expense associated with the restricted stock awards granted in 2021. The annualized ratio of non-interest expense to average assets declined from 2.76% for the six months ended June 30, 2021 to 3.05% for the six months ended June 30, 2022.

The Company participates in the Pentegra Defined Benefit Plan for Financial Institutions, a multiple-employer pension plan. Total pension plan expense for the six months ended June 30, 2022 and the year ended December 31, 2021 was $100,000 and $200,000, respectively. The Company has provided notice of its intent to withdraw as a participant from the pension plan as of September 30, 2022. Based on an estimate provided in August 2022 by the plan administrator, the estimated total cost (pre-tax) to withdraw is $2.5 million. The Company intends to accrue for this amount during the quarter ending September 30, 2022. Because the cost of withdrawal will primarily depend on the value of the plan’s assets and applicable interest rates at the time of withdrawal, the actual withdrawal cost will not be known until the ultimate withdrawal date, which the Company anticipates would occur during the first quarter of 2022. The actual withdrawal cost may differ materially from the estimated cost provided by the plan administrator.

29

FELDMAN FINANCIAL ADVISORS, INC.

Years Ended December 31, 2020 and 2021

Net income was $2.6 million for the year ended December 31, 2021, compared to net income of $1.1 million for the year ended December 31, 2020, an increase of $1.5 million or 142.9%. The increase was related primarily to a $1.6 million or 12.5% increase in net interest income, a $275,000 or 57.3% decrease in the provision for loan losses, a $203,000 or 9.9% increase in non-interest income, and a $105,000 or 0.8% decrease in non-interest expense. The Company’s ROA improved from 0.24% in 2020 to 0.55% for 2021.

Net interest income increased $1.6 million or 12.5% to $14.3 million for the year ended December 31, 2021 from $12.7 million for the year ended December 31, 2020. This increase was due to a $27.8 million or 6.3% increase in the balance of average interest-earning assets and a 58 basis point or 61.2% decrease in the weighted average rate of average interest-bearing liabilities during the year ended December 31, 2021. The Company’s net interest margin increased to 3.04% for the year ended December 31, 2021 from 2.88% for the year ended December 31, 2020.

The Company decreased its provision for loan losses from $480,000 for the year ended December 31, 2020 to $205,000 for the year ended December 31, 2021. The decrease in the provision for loan losses for the year ended December 31, 2021 was primarily due to adjustments to qualitative factors reflecting improved economic conditions compared to economic uncertainties as a result of the coronavirus pandemic during 2020.

Non-interest income increased $203,000 or 9.9% to $2.2 million in the year ended December 31, 2021, compared to $2.0 million for the year ended December 31, 2020. The increase in non-interest income during the year ended December 31, 2021 was due primarily to a $125,000 or 30.5% increase in net securities gains, a $166,000 increase in loan servicing fee

30

FELDMAN FINANCIAL ADVISORS, INC.

income, a $49,000 or 24.7% increase in investment services fees, and a $28,000 or 2.9% increase in customer service fees, offset by a decrease of $193,000 or 59.8% in gain on sale of loans. The ratio of non-interest income to average assets increased from 0.45% in 2020 to 0.47% for 2021. Excluding net securities gains, the ratio of non-interest operating income to average assets was unchanged at 0.36% for both yearly periods.

Non-interest expense decreased by $105,000 or 0.8% to $13.1 million for the year ended December 31, 2021 from $13.2 million for the year ended December 31, 2020. The decrease in non-interest expense was due primarily to a $236,000 or 2.9% decrease in salaries and employee benefits, a $57,000 or 6.4% decrease in professional fees and assessments, a $34,000 or 5.1% decrease in occupancy expense, and a $28,000 or 4.9% decrease in equipment expense, offset by a $241,000 or 20.7% increase in data processing during the year ended December 31, 2021.

The decrease in salaries and employee benefits was due to the elimination of certain positions and early retirements during 2020, offset by normal salary increases. The increase in data processing was due primarily to continued investment in cybersecurity initiatives and enhancements to the Company’s customer-based technologies. The overall ratio of non-interest expense to average assets declined from 2.91% for the year ended December 31, 2020 to 2.73% for the year ended December 31, 2021. The Company’s efficiency ratio improved from 92.1% in 2020 to 81.9% in 2021. (The efficiency ratio represents non-interest operating expense divided by the sum of net interest income and non-interest income exclusive of securities gains.)

31

FELDMAN FINANCIAL ADVISORS, INC.

Interest Rate Risk Management