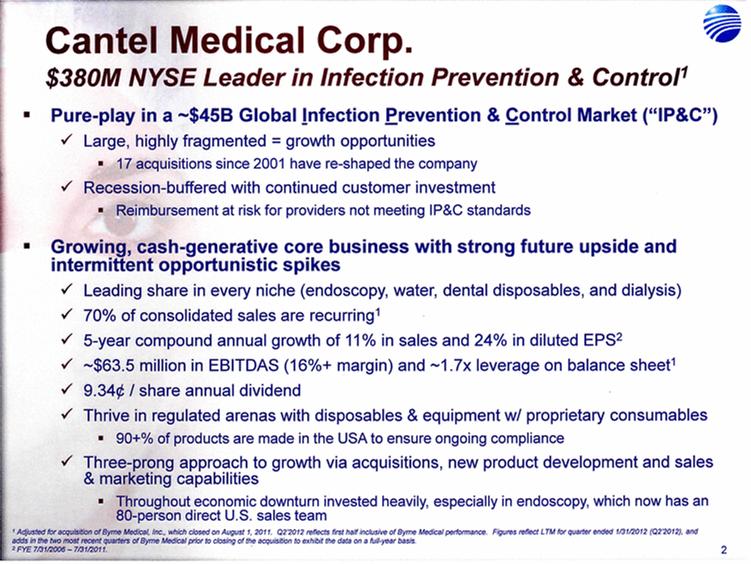

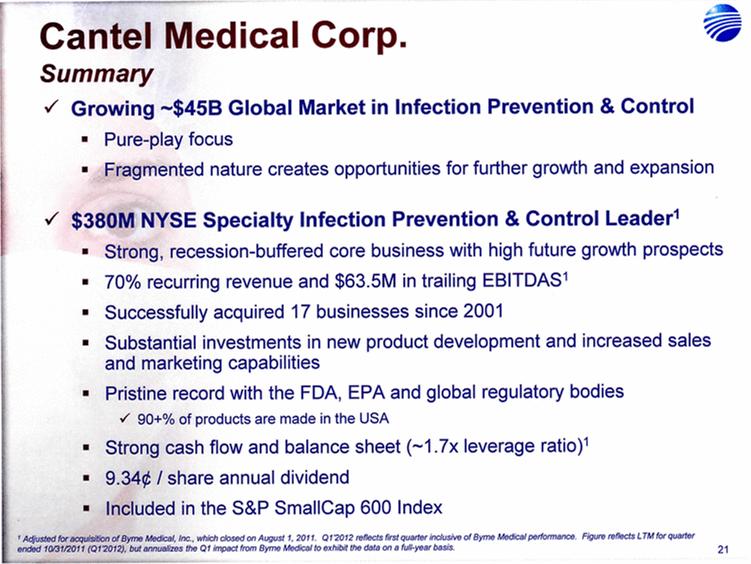

| 5 Cantel Medical Corp. $45 Billion Global Infection Prevention & Control Market Healthcare Associated Infections (HAI’s) are the most common complication of hospital care2 Implementing existing prevention practices yields ~70% reduction in HAIs. Financial benefit ~$25B - $32B in medical cost savings3 Annually, 2.3 Million People Acquire Infections in U.S. Medical Facilities leading to 100,000 Deaths1 Globally, 50+% of ICU patients have infections associated with an increased risk of death Growing awareness in professional, gov’t & consumer psyche H1N1 (“Swine” Flu), MRSA, C.Diff, Staph Infections, etc... 1 Infection Control Today, 12/1/2009 referencing the 12/2/2009 issue of JAMA. 2 Donald Wright M.D., M.P.H., Principal Deputy Assistant Secretary for Health, U.S. Department of Health and Human Services, December 2008. Centers for Disease Control and Prevention (CDC) as cited in Healthcare Purchasing News, November 2005, Vol.29, No.11. and “A systematic audit of economic evidence linking nosocomial infections and infection control interventions: 1990-2000”, Patricia Stone, RN, PhD. 2 Agency for Healthcare Research and Quality (AHRQ). AHRQ’s efforts to prevent and reduce health care-associated infections [fact sheet]. AHRQ Publication No. 09-P013, Rockville,MD: AHRQ; 2009 Sept. Available from: http://www.ahrq.gov/qual/haiflyer.htm 3 3Scott RD. The direct medical costs of healthcare-associated infections in US hospitals and the benefits of prevention. Atlanta: Centers for Disease Control and Prevention; 2009. Data Source: Freedonia Market Research. September 2011 $17B U.S. IP&C Market (US$B) $45B Global IP&C Market (2010 US$B) Forecast CAGR% 2010-2015F = 4.9% $0.0 $5.0 $10.0 $15.0 $20.0 $25.0 $30.0 US$ Billions 2005 2010 2015F 2020F Consumables & Disposables Equipment Services United States $16.7 36% Canada & Mexico $1.2 3% Western Europe $12.6 28% China $3.1 7% Japan $4.1 9% Other Asia/ Pacific $3.2 7% Rest of the World $4.6 10% |