Exhibit 99.1

| Cantel Medical Corp. (NYSE: CMN) Infection Prevention & Control Matters™ June 2012 FORWARD LOOKING STATEMENT This presentation contains forward-looking statements. All forward-looking statements involve risks and uncertainties, including, without limitation, the risks detailed in the Company’s filings and reports with the Securities and Exchange Commission. Such statements are only predictions, and actual events or results may differ materially from those projected. CROSSTEX |

| 2 Cantel Medical Corp. $385M NYSE Leader in Infection Prevention & Control1 Pure-play in a ~$45B Global Infection Prevention & Control Market (“IP&C”) Large, highly fragmented = growth opportunities 17 acquisitions since 2001 have re-shaped the company Recession-buffered with continued customer investment Reimbursement at risk for providers not meeting IP&C standards Growing, cash-generative core business with strong future upside and intermittent opportunistic spikes Leading share in every niche (endoscopy, water, dental disposables, and dialysis) 70% of consolidated sales are recurring1 5-year compound annual growth of 11% in sales and 24% in diluted EPS2 ~$66.6 million in EBITDAS (17%+ margin) and ~1.5x leverage on balance sheet1 9.34¢ / share annual dividend Thrive in regulated arenas with disposables & equipment w/ proprietary consumables 90+% of products are made in the USA to ensure ongoing compliance Three-prong approach to growth via acquisitions, new product development and sales & marketing capabilities Throughout economic downturn invested heavily, especially in endoscopy, which now has an 80-person direct U.S. sales team 1 Adjusted for acquisition of Byrne Medical, Inc., which closed on August 1, 2011. Q3’2012 reflects three quarters of Byrne Medical performance. Figures reflect LTM for quarter ended 4/30/2012 (Q3’2012), and adds in Byrne Medical performance for 4Q11E prior to closing of the acquisition to exhibit the data on a full-year basis. 2 FYE 7/31/2006 – 7/31/2011. |

| 3 Cantel Medical Corp. Three Synergistic Platforms Infection Prevention & Control Focus Healthcare & Life Sciences Orientation IP&C Device Management Endoscopy & Renal Dialysis Medivators/Byrne; Minntech Purification & Filtration Water Treatment & Therapeutic Filters Mar Cor Purification; Minntech Disposable Products Dental & Specialty Packaging Crosstex; Saf-T-Pak Chemistries (Disinfectants & Sterilants) Consumables and Service Leverage in Manufacturing, Regulatory and R&D |

| 4 Cantel Medical Corp. Snapshot: By Product, Customer, Channel Infection Prevention & Control Focus Healthcare & Life Sciences Orientation Renal / Dialysis Equipment, Sterilants, Consumables, Service Endoscopy Equipment, Disinfectants, Consumables, Service Dental Disposables Water Purification Equipment, Field Service, Consumables Specialty Packaging Packaging, Training PURIFICATION & FILTRATION IP&C DEVICE MGMT DISPOSABLES Therapeutic Filtration Hollow Fiber Filters Dialysis Chains Hospitals; GI Clinics/ASC’s Dental Offices Dialysis Clinics, Industrial Diverse Customer Set Hospitals, Biotech Firms Direct Sales Direct Sales Distributors Direct Sales & Distributors Direct Sales Distributors / OEM 1 6 4 8 1 1 Acquired2 89/11% 70/30% 100/0% 41/59% 100/0% 100/0% Consumable / Capital1 1 Consumables includes service. Splits represent rolling twelve months ended April 30, 2012. 2 Acquisition of Minntech Corporation in September 2001 is represented in Endoscopy, Renal/Dialysis, and Therapeutic Filtration. |

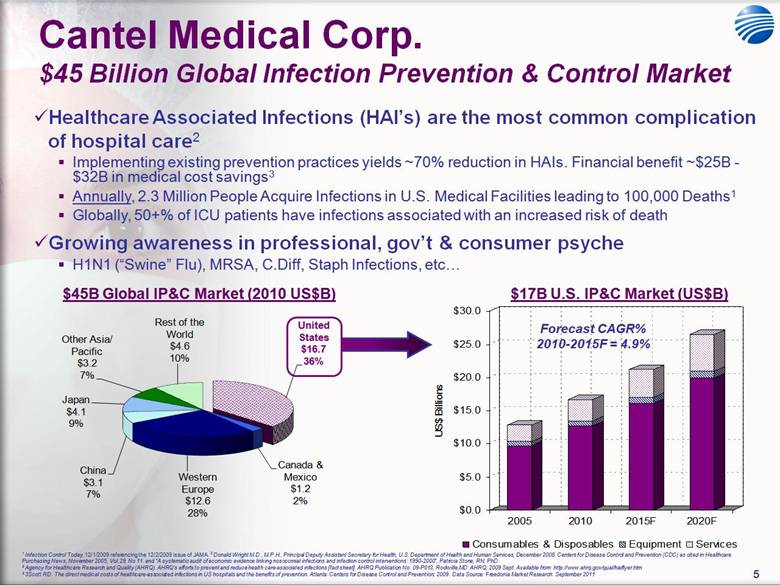

| 5 Cantel Medical Corp. $45 Billion Global Infection Prevention & Control Market Healthcare Associated Infections (HAI’s) are the most common complication of hospital care2 Implementing existing prevention practices yields ~70% reduction in HAIs. Financial benefit ~$25B - $32B in medical cost savings3 Annually, 2.3 Million People Acquire Infections in U.S. Medical Facilities leading to 100,000 Deaths1 Globally, 50+% of ICU patients have infections associated with an increased risk of death Growing awareness in professional, gov’t & consumer psyche H1N1 (“Swine” Flu), MRSA, C.Diff, Staph Infections, etc 1 Infection Control Today, 12/1/2009 referencing the 12/2/2009 issue of JAMA. 2 Donald Wright M.D., M.P.H., Principal Deputy Assistant Secretary for Health, U.S. Department of Health and Human Services, December 2008. Centers for Disease Control and Prevention (CDC) as cited in Healthcare Purchasing News, November 2005, Vol.29, No.11. and “A systematic audit of economic evidence linking nosocomial infections and infection control interventions: 1990-2000”, Patricia Stone, RN, PhD. 2 Agency for Healthcare Research and Quality (AHRQ). AHRQ’s efforts to prevent and reduce health care-associated infections [fact sheet]. AHRQ Publication No. 09-P013, Rockville,MD: AHRQ; 2009 Sept. Available from: http ://www.ahrq.gov/qual/haiflyer.htm 3 3Scott RD. The direct medical costs of healthcare-associated infections in US hospitals and the benefits of prevention. Atlanta: Centers for Disease Control and Prevention; 2009. Data Source: Freedonia Market Research. September 2011 $0.0 $5.0 $10.0 $15.0 $20.0 $25.0 $30.0 US$ Billions 2005 2010 2015F 2020F Consumables & Disposables Equipment Services $17B U.S. IP&C Market (US$B) $45B Global IP&C Market (2010 US$B) Forecast CAGR% 2010-2015F = 4.9% |

| 6 Cantel Medical Corp. Healthcare Reform Creates Greater Emphasis in IP&C Financial Penalties to Hospitals1 Preventable Readmissions – Estimated $30 billion cost to the system Beginning 2012, Medicare will stop paying hospitals for preventable readmissions tied to heart failure or pneumonia Beginning 2014, expand policy to cover four (4) more conditions Reduced Payment for Hospital Acquired Conditions – Infections & Errors Beginning 2012, Medicare will align actual payment to reported performance on patient satisfaction and care quality Beginning 2015, Dept. of Health & Human Services will start reporting each hospitals’ record for infections and medical errors pertaining to Medicare patients • Payments reduced by 1% for those with highest rate of infections & medical errors • No longer pay for treatment when a Medicaid patient is harmed during a hospital stay Despite Shrinking Budgets, Hospitals Maintain IP&C Funding2 2/3rds decreased or froze spending in 2009 and expect further cuts in 2010 However, virtually none cut patient safety infection control budgets in 2009, and spending growth is expected in the future 1 Healthcare Purchasing News, April 30, 2010. 2 HealthLeaders Media, April 6, 2010 – citation of LEK Hospital Purchasing Survey of January 2010 – Survey of 203 U.S. hospital CEOs, CFOs, COOs, materials managers, and purchasing directors. |

| 7 Cantel Medical Corp. Well-Balanced Portfolio with Emphasis on Endoscopy All Other $16.89 4% Endoscopy $143.40 37% Dialysis $35.91 9% Healthcare Disposables $75.97 20% Endoscopy (BMI 1 qtrs preacquisition) $10.75 3% Water Purification & Filtration $101.65 27% Latest Twelve Months Ended April 30, 20121 1 Q3’2012 reflects three quarters of Byrne Medical performance. LTM figures add in Byrne Medical performance for 4Q11E prior to closing of the acquisition to exhibit the data on a full-year basis. “All Other” includes Therapeutic Filtration Products. Specialty Packaging Products, and Chemistries. 2 Before allocation of corporate expenses of ~$10.5M. 3 Earnings Before Interest, Taxes, Depreciation, Amortization, Stock Compensation Expense and (Gain)/Loss on Disposal of Fixed Asset. 4 EBIT for Byrne Medical reported in 8-K/A after full impact of purchase accounting and personal expenses. As in Net Sales, adjusted figures reflect full-year impact from Byrne Medical. The effect of rounding may create minor data variances. Dialysis $8.86 15% Water Purification & Filtration $10.66 19% Endoscopy (BMI 1 qtr preacquisition) $2.14 4% Endoscopy $24.38 43% All Other ($0.42) (1%) Healthcare Disposables $11.75 21% Net Sales $373.8M $385M adjusted for acquisition of Byrne Medical (8/1/11)1 Operating Income $55.2M2 $57M2,4 adjusted for acquisition of Byrne Medical (8/1/11)1 Reported EBITDAS = $63.9M3 $66.6M adjusted for acquisition of Byrne Medical (8/1/11)1 $27M 46% of total $154M 40% of total |

| 8 Cantel Medical Corp. Significant Upside Growth Opportunities Acquisitions: 3 recent acquisitions, one in each core segment Byrne Medical has leadership position to drive a large, global market conversion to profitable disposable endoscopy components Continue solid integration and advancement on the acquisitions of Gambro Water and ConFirm Monitoring Proven ability to integrate, leverage and grow acquired businesses Robust pipeline of opportunities in disposables, endoscopy, and water purification Add to international and/or hospital channels New Markets – Alternative Channels Dedicated focus on corporate and government pandemic flu preparation (“Contagion”) One of only a few large U.S. manufacturers of FDA-cleared face masks Sponsored research study published demonstrating effectiveness of surgical facemasks vs. N-95 respirators (American Journal of Infection Control) Research evidencing reduced spread of disease using face masks as “source control” Specialized commercial / consumer markets for contract sterilization, fogging and residual protection technology Greater focus on promoting profitable and proprietary product lines internationally |

| 9 Cantel Medical Corp. Significant Upside Growth Opportunities Substantial Sales & Marketing investments in core FY’09-FY’11 Substantial increase in R&D spending in FY’11 High-Margin Liquid Chemical Germicides (LCG) New chemistry development capabilities began mid-FY’10, accelerating in FY’11, to yield multiple New Product Introductions (NPI) in FY’12+ New General Manager and senior marketing executive added Expanded uses of existing chemistry products across all business segments Novel developments in fogging equipment and Revox sterilization services launched Antimicrobial coating and residual protection technology Odor eradication products Equipment and Disposables Endoscope reprocessors: broader portfolio, higher technology now with proprietary, “single-shot” chemistry launched worldwide Next generation water treatment equipment with focus on heat disinfection Unique disposables: Sure-Check® sterilization pouch & Secure-Fit™ face mask High value therapeutic filter developments underway Strong pipeline of future Byrne Medical products to be launched |

| 10 Byrne Acquisition – Aug 1, 2011 Endoscopy: Facilitate Accelerated Global Growth Minntech subsidiary acquired the assets of Byrne Medical, Inc. for $89.4M in cash and $10.0M in stock, plus $10.0M potential earnout Pre-acquisition revenues of ~$38.6M and EBIT of $10.9M1 Complementary: Further bolster our infection control presence and leadership in the gastroenterology suite Technology: precision performance disposables to reduce infection risk and complexities of sterilizing water bottles, tube sets, and valves IP protected product portfolio Market: sizeable, underpenetrated, global opportunity Early stages of shift to disposable being driven by Byrne Medical Customers: broaden reach from post-procedure cleaning (Medivators) into the treatment itself (Byrne Medical) Move closer to physician and operating nurses with preference items Sales Force: combined, the Endoscopy group now has over 80 field sales consultants and clinical specialists Exclusively focused on infection control in GI endoscopy Manufacturing: high-end engineering, design, production Utilize Byrne Medical facilities to create “Center of Excellence” for precision designed and manufactured disposable products Talent: Hired entire Byrne Medical team and refocused founder on product development and sales strategy. Smooth customer and employee transition SmartCap EndoGator A/W/S Valves 1 EBIT after backing out the impact of purchase accounting and non-operating expenses. EBIT of $7.3M reported in 8-K/A accounts for full effect of these adjustments. |

| 11 Medivators Plus Byrne Medical Endoscopy Segment: Complementary Businesses Intercept Wipes Veriscan Scope Buddy Intercept CER/DSD/ Advantage Rapicide Rapicide PA IN THE PROCEDURE ROOM Byrne Medical Products Treatment Room Physicians & Nurses Medivators Endoscope Reprocessing Products Principally in Post-Procedure, Reprocessing Area Sterile Processing Department / Nurses A/W/S Valves SmartCap / EndoGator REPROCESSING AREA (Post-Procedure) |

| 12 Gambro Acquisition in FY’11 Water Treatment Mar Cor Purification subsidiary acquired Gambro’s U.S. water treatment business (Oct 6, 2010) for $23.7M in cash. Pre-acquisition revenues of ~$14.0M. Strategic value akin to success of Mar Cor’s acquisition of GE’s Dialysis Water Business in March 2007. Technology: Industry Shift to Heat Disinfection and Growing Investment in Home Hemodialysis Acquired FDA-cleared heat disinfection central and portable systems to broaden the addressable customer base Installed Customer Base: Brought over 1,200 U.S. dialysis clinics and numerous hospitals to add consumables and service sales opportunities Manufacturing Scale: Relocate production from Sweden to our Minnesota facility and create tangible benefit through factory overhead absorption Customer Supply Agreement: Unique supply contract position with a leading U.S. dialysis chain. Master data transitioned and we’re shipping orders Talent: Hired all of Gambro’s U.S. aligned water personnel with expertise in dialysis and heat disinfection. Smooth customer transition |

| 13 ConFirm Acquisition in FY’11 Healthcare Disposables Crosstex Int’l subsidiary acquired ConFirm Monitoring Systems’ sterility assurance business (Feb 14, 2011) for $7.5M in cash1. Pre-acquisition revenues of ~$4.0M. Product line extension to Crosstex’ key sterilization product category Position: #1 player in dental biological monitoring services in North America Industry guidelines call for weekly sterilizer testing. Canada now has two provinces shifting to daily testing Installed Customer Base: Key, long-term, private label distributor and dental school relationships as well as a solid branded business Direct contact with dentists daily Talent: Retained all of ConFirm’s aligned personnel with expertise in sterility assurance. Smooth customer transition. 1 Upfront cash purchase price. Up to an additional $1M of contingent cash consideration is possible based on achievement of sales levels for the twelve month period ending Jan 31, 2012. |

| 14 Cantel Medical Corp. Formula: Acquire, Improve Businesses, Repeat CAGR% ’03-9M’12 17% 22% FY’11 and LTM PF12 are adjusted for the acquisition of Byrne Medical on August 1, 2011. $400 $375 $350 $325 $300 $275 $250 $225 $200 $175 $150 $125 $100 $75 $50 $25 $0 Phase I: Build Position; Grow EBITDAS [CAGR% 33%]; Improve Margin; Reduce Debt; Reload Phase II: Grow EBITDAS [CAGR% 20%]; Further Improve Margin; Reduce Debt, Reload Fy’03 Fy’04 Fy’05 Fy’06 Fy’07 Fy’08 Fy’09 Fy’10 PF FY’11* PF LTM* Net Sales $94.0 $123.0 $137.2 $192.2 $219.0 $249.4 $260.1 $274.0 $274.0 $360.2 $384.6 EBITDAS $11.3 $14.0 $19.2 $26.5 $28.6 $31.8 $42.1 $47.5 $59.4 $66.6 Net Debt/(Cash) $3.7 $7.1 ($17.6) $8.1 $41.1 $40.0 $19.9 ($1.6) $103.6 $75.5 EBITDAS Margin 12.0% 11.4% 14.0% 13.8% 13.0% 12.8% 16.2% 17.3% 16.5% 17.3% |

| 15 Cantel Medical Corp. Fragmented Nature of Infection Prevention & Control 1 2 3 4 5 Disinfectants & Cleaners Disposables Masks / Headwear Air & Water Quality Protective Apparel Brushes Disposable kits / trays Face shields Air filtration systems Aprons / bibs / arm protectors Dispensers Disposable medical products Masks Germicidal air cleaners Gloves Enzymatic cleaners Disposable surgical products Nurse/MD/Surg/Lab Hats Negative pressure isolation Lab gowns Medical device disinfectants Protection goggles Smoke evacuators Overshoes / coated boots Surface disinfectants Respirators Toxic gas detection systems Shirt jackets Wipes Wrap around lenses Water purification systems Surgical gowns 6 7 8 9 10 Sterilization Drapes & Barrier Products Hand Hygiene Wound Care & Closures Needles / Sharps / Transport Autoclaves Antimicrobial linens Automated hand washers Adhesives / adhesive removers Antimicrobial catheters Chemical sterilizers Fluid control drapes Hand cleaners / soaps Antimicrobial dressings Blood pressure cuff covers EtO sterilizers General purpose drapes Hand sanitizers (waterless) Dressings Catheter securement devices Low temperature sterilizers Surgical drapes Drains / suction Dispenser boxes Medical device drying cabinets Hydrogel adhesive dressings Needle protection devices Medical device reprocessing Silver bandages / dressings Safety I.V. catheters Steam sterilizing units Surgical site skin prep Specimen transport bags Sterilization containers Sterilization packaging Washers / decontaminators Sterilization Services 11 12 13 14 15 Quality Control & Testers Fluid / Temperature/ Positioning Medical Waste & Cleaning Equipment Environmental Surveillance / Software / Education Biological indicators Filtration systems Antimicrobial casters Antimicrobial paint Alert systems Chemical integrators Fluid control systems Cleaning carts Containment systems Handwashing EtO monitors Fluid warming systems Decontamination equip Washable keyboards Surveillance software Glutaraldehyde monitors Forced air warming Infectious waste bags Pest management Training Respirator fit testers Patient positioning Microfiber mops Rapid MRSA diagnostics Sterility assurance products Pressure mgmt systems Room decontaminators Temperature mgmt kits Sharps containers Solidifiers / Spill Kits Suction canister systems Waste management systems Indicates Cantel product offering Key strategic priorities |

| 16 Cantel Medical Corp. Historical P&L Reveals Success of Acquisition Program 1 Reflects continuing operations and excludes any historical impact of Carsen Endoscopy & Surgical business. 2 Earnings before Interest, Taxes, Depreciation, Amortization, and Stock Compensation Expense. 3 Equivalent to “Income from Continuing Operations”. 4 Compound Annual Growth Rate. 5 Retroactively applies the 3:2 stock split effective in February 2012. 6 Adjustments exclude $0.04 in FY’09 and $0.08 in FY’10 due to H1N1 pandemic benefit. CAGR% 4 2007 2008 2009 2010 2011 06-'11 9M'12 LTM $219.0 $249.4 $260.1 $274.0 $321.7 11% $287.8 $373.8 $79.0 $87.6 $99.5 $111.0 $122.8 12% $121.4 $153.3 Gross Margin % 36.1% 35.1% 38.3% 40.5% 38.2% 42.2% 41.0% $28.6 $31.8 $42.1 $47.5 $47.1 12% $52.8 $63.9 $16.8 $18.0 $27.5 $32.7 $31.3 15% $37.7 $44.7 $8.1 $8.7 $15.6 $19.9 $20.4 25% $21.7 $26.4 $0.33 $0.35 $0.63 $0.78 $0.79 24% $0.80 $0.98 $0.33 $0.35 $0.59 $0.70 $0.79 24% (non-GAAP metric) Diluted EPS5 US Dollars Millions, except per share amounts Net Sales Net Income Gross Profit Op. Profit3 Adj. Dil. EPS 5,6 Fiscal Years Ended July 311 Continuing Operations EBITDAS2 |

| 17 Cantel Medical Corp. Capacity for Continued Investment 2006 2007 2008 2009 2010 2011 Q3'12 $238.2 $263.7 $279.2 $277.9 $280.7 $321.4 $430.3 2.1:1 2.1:1 2.2:1 2.3:1 2.3:1 2.6:1 2.5:1 $140.8 $155.1 $168.7 $187.1 $209.4 $234.3 $266.4 0.27 0.37 0.35 0.23 0.10 0.10 0.38 1.4x 2.0x 1.8x 1.0x 0.4x 0.5x 1.5x 2,3 24.4 24.2 24.7 24.9 25.5 26.0 27.3 Funded Debt to Equity Gross Debt / LTM EBITDAS1 Fiscal Year Ended July 31 US Dollars and shares in millions # of Diluted Shares4 Total Assets Current Ratio2 Equity 1 Earnings before Interest, Taxes, Depreciation, Amortization, and Stock Compensation Expense. 2 Impact of $96M in senior debt used to acquired Byrne Medical on August 1, 2011.. 3 EBITDAS calculated using LTM actual results plus one quarter of Byrne results prior to acquisition closing on Aug 1, 2011. 4 Retroactively reflects 3:2 stock split effective February 1, 2012. |

| 18 Cantel Medical Corp. Experienced Executive Team Andrew A. Krakauer President & CEO Former President of Ohmeda Medical (Division of Instrumentarium/GE) Over 20 years of healthcare experience Joined Cantel in 2004 as COO Craig A. Sheldon SVP, Chief Financial Officer & Treasurer Formerly with Ernst & Young LLP Certified Public Accountant Joined Cantel in 1994 Eric W. Nodiff SVP, General Counsel Former Partner at Dornbush Schaeffer Strongin & Venaglia, LLP Outside counsel to Cantel for 18 years Joined in-house in 2005 Seth M. Yellin VP, Corporate Development Formerly with Citadel Asset Management and UBS Investment Bank Joined Cantel in 2012 Don Byrne President & CEO, Medivators (Byrne) Over 20 Years in Healthcare Curtis Weitnauer President & CEO, Mar Cor Over 20 Years in Water Treatment Gary Steinberg President & CEO, Crosstex Over 20 Years in Dental Products Paul Helms EVP, Operations 30+ Years Healthcare Javier Henao EVP, International 30+ Years Healthcare |

| 19 Cantel Medical Corp. Strategic Objectives Remain Focused within Infection Prevention & Control Near-term build a profitable $500 Million Specialty Business...setting the strategy for $1 Billion Achieve accelerated growth and profits from the three recent acquisitions Invest in higher technology, higher margin and higher growth organic programs with near-to-mid-term payoff High-value, unique IP&C disposables (e.g. Byrne Medical) Orientation around Liquid Chemical Germicides (LCG’s) Capital Equipment / Proprietary Consumable combination solutions Focus on channel expansion including flu preparation, hospital and international markets Substantial increased sales and marketing investments in base business Continue aggressive and proven acquisition program to leverage existing assets and channels Continue focus on operational excellence |

| 20 Cantel Medical Corp. Cantel Medical Corp. Strategic Evolution FY’04 – FY’08: Acquire and Define Infection Prevention & Control (IPC) Portfolio FY’09 – FY’10: Substantial Operational and P&L Improvement, while Investing in Sales & Marketing FY’11: Leverage Sales & Marketing and Drive R&D Investments. Close 1-2 Key Acquisitions EPS Range: $0.21-$0.35 EPS Range: $0.63-$0.78 (including H1N1 spike) $0.59-$0.70 (base business) FY’12+: Capitalize on all Strategic Investments (S&M, R&D, NPIs, Acquisitions) EPS Range: Significant Growth LTM Q3’12: • Reported: $0.98 • Pro Forma:$1.001 EPS: $0.79 (inclusive of $0.03 of 1x acquisition expenses) All EPS figures ar e adjusted retroactively for the 3:2 stock split effectuated on February 1, 2012. 1 Pro Forma LTM EPS add in one quarter of Byrne Medical performance prior to closing of the acquisition to exhibit the data on a full-year basis. |

| 21 Cantel Medical Corp. Summary Growing ~$45B Global Market in Infection Prevention & Control Pure-play focus Fragmented nature creates opportunities for further growth and expansion $385M NYSE Specialty Infection Prevention & Control Leader1 Strong, recession-buffered core business with high future growth prospects 70% recurring revenue and $66.6M in trailing EBITDAS1 Successfully acquired 17 businesses since 2001 Substantial investments in new product development and increased sales and marketing capabilities Pristine record with the FDA, EPA and global regulatory bodies 90+% of products are made in the USA Strong cash flow and balance sheet (~1.5x leverage ratio)1 9.34¢ / share annual dividend Included in the S&P SmallCap 600 Index 1 Adjusted for acquisition of Byrne Medical, Inc., which closed on August 1, 2011. Q3’2012 reflects three quarters of Byrne Medical performance. Figures reflect LTM for quarter ended 4/30/2012 (Q3’2012), and adds in Byrne Medical performance for 4Q11E prior to closing of the acquisition to exhibit the data on a full-year basis. |

| Cantel Medical Corp. (NYSE: CMN) Infection Prevention & Control Matters™ CROSSTEX |