DEPRECIATION—Depreciation expenses for the period from September 21, 2022 to December 31, 2022 were $0.6 million.

NET INCOME—As a result of the above factors, we recorded net income of $0.6 million for the period from September 21, 2022 to December 31, 2022.

Period from January 1, 2022 to October 18, 2022 (Predecessor)

The average number of vessels in our fleet was 1.49 for the period from January 1, 2022 to October 18, 2022 (Predecessor).

REVENUES—Voyage revenues amounted to $12.8 million for the period January 1, 2022 to October 18, 2022 and $6.3 million for the period from March 12, 2021 (inception) to December 31, 2021. The increase in voyage revenues by $6.5 million or 103.2% was due to the increase in the average number of vessels along with an improvement in market charter rates. Total calendar days for our fleet were 431 for the period from January 1, 2022 to October 18, 2022 compared to 281 for the period March 12, 2021 (inception) to December 31, 2021. Of the total calendar days for the period January 1, 2022 to October 18, 2022, 369 or 85.6% were time charter days, while, our fleet operational utilization was 85.8%.

VOYAGE EXPENSES—Voyage expenses were $0.7 million for the period January 1, 2022 to October 18, 2022 compared to $0.4 million for the period March 12, 2021 (inception) to December 31, 2021. The increase in voyage expenses by $0.3 million or 75.0% was due to the increase in the size of our fleet by one drybulk carrier in May 2022. Voyage expenses for the period January 1, 2022 to October 18, 2022 mainly included commissions to third parties of $0.6 million, corresponding to 85.7% of total voyage expenses.

VESSEL OPERATING EXPENSES—Vessel operating expenses were $2.4 million for the period January 1, 2022 to October 18, 2022 compared to $1.5 million for the period from March 12, 2021 (inception) to December 31, 2021. The increase in operating expenses by $0.9 million or 60.0% was mainly due to the increase of our fleet by one drybulk carrier in May 2022.

DRY DOCKING COSTS—Dry docking costs were $0.8 million for the Period January 1, 2022 to October 18, 2022 compared to $0.1 million for the period from March 12, 2021 (inception) to December 31, 2021. During the period January 1, 2022 to October 18, 2022 our drybulk carrier, the Eco Bushfire, underwent drydocking services along with ballast water system treatment installation. The drydocking cost of $0.1 million for the period from March 12, 2021 (inception) to December 31, 2021 related to the preparation for the Eco Bushfire drydocking services.

MANAGEMENT FEES – RELATED PARTY—Management fees – related party were $0.2 million for the period January 1, 2022 to October 18, 2022 compared to $0.1 million for the period from March 12, 2021 (inception) to December 31, 2021. The increase of management fees by $0.1 million is due to the increase of our fleet by one drybulk carrier in May 2022.

DEPRECIATION—Depreciation expenses for the period January 1, 2022 to October 18, 2022 were $0.5 million. For the period March 12, 2021 (inception) to December 31, 2021 depreciation expenses were $0.4 million. The $0.1 million increase between the two periods is attribute to the increase in the average number of our vessels.

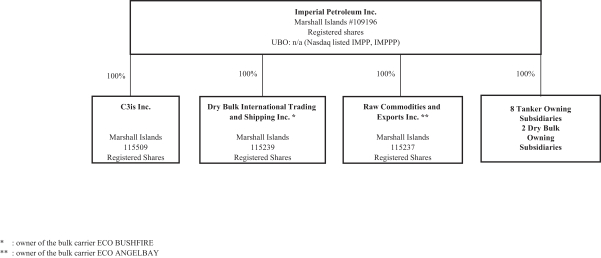

GAIN ON VESSEL SALE- During the period January 1, 2022 to October 18, 2022, we sold to Imperial Petroleum, and on September 21, 2022 delivered to Imperial Petroleum, the Eco Bushfire, for which an aggregate gain on the sale of vessel of $9.3 million was recognized.

NET INCOME—As a result of the above factors, we recorded net income of $17.5 million for the period January 1, 2022 to October 18, 2022. For the period from March 12, 2021 (inception) to December 31, 2021 net

69