UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

OFFERING CIRCULAR

FORM 1-A

OFFERING STATEMENT UNDER THE SECURITIES ACT OF 1933 CURRENT REPORT

![]()

ROCKSTAR CAPITAL

GROUP LLC

Date: February 7, 2023

| Arkansas | 6500 | 88-4161726 |

(State or Other Jurisdiction of Incorporation) | (Primary Standard Classification Code) | (IRS Employer Identification No.) |

Brandon Rooks

Chief Executive Officer

10333 Windy Trail,

Bentonville, AR 72712

Telephone: 913-827-3517

(Address, including zip code, and telephone number,

including area code, of registrant’s principal executive offices)

Please send copies of all correspondence to:

Pino Nicholson PLLC

99 S. New York Ave.

Winter Park, FL 32789

Telephone: 407-425-7831

Email: ljp@PinoNicholsonLaw.com

(Name, address, including zip code, and telephone number,

including area code, of agent for service)

THIS OFFERING STATEMENT SHALL ONLY BE QUALIFIED UPON ORDER OF THE COMMISSION, UNLESS A SUBSEQUENT AMENDMENT IS FILED INDICATING THE INTENTION TO BECOME QUALIFIED BY OPERATION OF THE TERMS OF REGULATION A.

PART I - NOTIFICATION

Part I should be read in conjunction with the attached XML Document for Items 1-6

PART I – END

| 1 of 59 |

Offering Statement Initial Submission

File No. _______

PART II – OFFERING CIRCULAR

ROCKSTAR CAPITAL GROUP LLC

$75,000,000 OF PREFERRED SHARES

$1,000 PAR VALUE PER SHARE

This Offering involves the purchase of Preferred Shares (“Shares”) in Rockstar Capital Group LLC (the “Company”), which was formed for the purpose of raising capital to engage in the business of investing in all forms of real estate, primarily by issuing short-term loans (“Investment Activities”), providing working capital and project financing (“Project Financing”), and/or land financing (“Land Financing”) to affiliated and unaffiliated individuals and/or entities (“Borrowers”).

The Borrowers plan to acquire, permit, and develop land in the southeastern United States (the “Borrower Properties”) for the purpose of resale of permitted lots (“Permitted Real Estate Lots”) to regional or national homebuilders, hedge funds, or other arm’s length buyers. In addition, the Company may invest in properties that the Company’s Manager considers to be desirable to acquire or develop, and therefore suitable for investment, either directly, or indirectly through partnerships or strategic relationships with arm’s length and affiliated real estate developers and builders (“Qualified Properties”).

Purchasers of the Preferred Shares will become owners of the Shares (“Investors”) upon execution of the Subscription Agreement, submission of the Investor Qualification Questionnaire, delivery of the investment funds (“Capital Contribution”), and acceptance by the Manager, which is Rockstar Capital Group Management Corporation.

The Offering commenced on February 7, 2023 and will terminate upon the earlier of: (i) the completion of the sale of all of the Shares, or (ii) at the discretion of the Manager. The Offering may be extended by the Company in its sole discretion (the "Offering Period"). The Company is offering a minimum of ten (10) Shares and a maximum of seventy-five thousand (75,000) Shares. Each Share is priced at One Thousand ($1,000) Dollars and a minimum purchase of ten (10) Shares is required, although the minimum number of Shares may be offered in fractions at the discretion of the Manager. The executive management of the Company may purchase less. Any number of additional Shares may be purchased.

| Price to Public | |

| Per Unit | $1,000 |

| Total Minimum | $10,000 |

| Total Maximum | $75,000,000 |

These Shares are offered to both “accredited” and “non-accredited” investors as described in Section 1 “Suitability Standards.” However, non-accredited investors are restrained by the purchasing limits set by the SEC, which are as follows:

| 1. | Non-accredited investors may not purchase more than ten (10%) percent of the greater of annual income or net worth (for natural persons); or |

| 2. | Non-accredited investors may not purchase more than ten (10%) percent of the greater of annual revenue, or net assets at fiscal year-end (for non-natural persons). |

There is the possibility of conflicts of interest arising between the Investors and the Manager that are described in the “Conflicts of Interest” section further below in this Offering circular. This Offering of Shares involves substantial risks that are described in “Risk Factors and Disclosures”. There is the possibility that the proceeds of this Offering will be insufficient to meet the requirements described in “Investment Objectives, Policies, Preferred Return.” Before purchasing any of the Shares offered through this Memorandum, consult with an attorney or a financial advisor to determine if this investment is suitable for you.

| Per Share(1) | Minimum Offering Amount | Maximum Offering Amount | ||||||||||

| Price to public | $ | 1000.00 | $ | N/A | $ | 75,000,000.00 | ||||||

| Commissions(1) | $ | (0.00 | ) | $ | N/A | $ | (0.00 | ) | ||||

| Proceeds, net of Commissions, before expenses, to the Company | $ | 1000.00 | $ | N/A | $ | 75,000,000.00 | ||||||

| Proceeds to other persons | $ | N/A | $ | N/A | $ | N/A | ||||||

| 2 of 59 |

INVESTMENT IN SHARES OF THE COMPANY INVOLVES SIGNIFICANT RISK, AND YOU MAY BE REQUIRED TO HOLD YOUR INVESTMENT FOR AN INDEFINITE PERIOD OF TIME. YOU SHOULD PURCHASE THIS SECURITY ONLY IF YOU CAN AFFORD A COMPLETE LOSS OF YOUR INVESTMENT. SEE “RISK FACTORS” BEGINNING ON PAGE 18 OF THIS OFFERING CIRCULAR.

THE UNITED STATES SECURITIES AND EXCHANGE COMMISSION DOES NOT PASS UPON THE MERITS OF OR GIVE ITS APPROVAL TO ANY SECURITIES OFFERED OR THE TERMS OF THE OFFERING, NOR DOES IT PASS UPON THE ACCURACY OR COMPLETENESS OF ANY OFFERING CIRCULAR OR OTHER SOLICITATION MATERIALS. THESE SECURITIES ARE OFFERED PURSUANT TO AN EXEMPTION FROM REGISTRATION WITH THE COMMISSION; HOWEVER, THE COMMISSION HAS NOT MADE AN INDEPENDENT DETERMINATION THAT THE SECURITIES OFFERED HEREUNDER ARE EXEMPT FROM REGISTRATION.

GENERALLY, NO SALE MAY BE MADE TO YOU IN THIS OFFERING IF THE AGGREGATE PURCHASE PRICE YOU PAY IS MORE THAN 10 PERCENT OF THE GREATER OF YOUR ANNUAL INCOME OR NET WORTH. DIFFERENT RULES APPLY TO ACCREDITED INVESTORS AND NON-NATURAL PERSONS. BEFORE MAKING ANY REPRESENTATION THAT YOUR INVESTMENT DOES NOT EXCEED APPLICABLE THRESHOLDS, THE COMPANY ENCOURAGES YOU TO REVIEW RULES 251(d)(2)(i)(C) OF REGULATION A. FOR GENERAL INFORMATION ON INVESTING, THE COMPANY ENCOURAGES YOU TO REFER TO WWW.INVESTOR.GOV.

The Company is following the “Offering Circular” format of disclosure under Regulation A.

The date of this Offering Circular is February __, 2023.

| 3 of 59 |

IMPORTANT NOTICES TO INVESTORS

INVESTMENT IN REAL ESTATE FINANCING INVOLVES A HIGH DEGREE OF RISK, AND INVESTORS SHOULD NOT INVEST ANY FUNDS IN THIS OFFERING UNLESS THEY CAN AFFORD TO LOSE THEIR ENTIRE INVESTMENT. IN MAKING AN INVESTMENT DECISION, INVESTORS MUST RELY ON THEIR OWN EXAMINATION OF THE ISSUER AND THE TERMS OF THE OFFERING, INCLUDING THE MERITS AND RISKS INVOLVED.

NO PERSON HAS BEEN AUTHORIZED TO GIVE ANY INFORMATION OR TO MAKE ANY REPRESENTATIONS IN CONNECTION WITH THE OFFER MADE BY THIS OFFERING CIRCULAR, NOR HAS ANY PERSON BEEN AUTHORIZED TO GIVE ANY INFORMATION OR MAKE ANY REPRESENTATION OTHER THAN THOSE CONTAINED IN THIS OFFERING CIRCULAR, AND IF GIVEN OR MADE, SUCH INFORMATION OR REPRESENTATIONS MUST NOT BE RELIED UPON. THIS OFFERING CIRCULAR DOES NOT CONSTITUTE AN OFFER TO SELL OR SOLICITATION OF AN OFFER TO BUY IN ANY JURISDICTION IN WHICH SUCH OFFER OR SOLICITATION WOULD BE UNLAWFUL OR ANY PERSON TO WHO IT IS UNLAWFUL TO MAKE SUCH OFFER OR SOLICITATION. NEITHER THE DELIVERY OF THIS OFFERING CIRCULAR NOR ANY SALE MADE HEREUNDER SHALL, UNDER ANY CIRCUMSTANCES, CREATE AN IMPLICATION THAT THERE HAS BEEN NO CHANGE IN THE AFFAIRS OF THE ISSUER SINCE THE DATE HEREOF.

THIS OFFERING CIRCULAR MAY NOT BE REPRODUCED IN WHOLE OR IN PART. THE USE OF THIS OFFERING CIRCULAR FOR ANY PURPOSE OTHER THAN AN INVESTMENT IN SECURITIES DESCRIBED HEREIN IS NOT AUTHORIZED AND IS PROHIBITED.

THE OFFERING PRICE OF THE SECURITIES IN WHICH THIS OFFERING CIRCULAR RELATES HAS BEEN DETERMINED BY THE ISSUER AND DOES NOT NECESSARILY BEAR ANY SPECIFIC RELATION TO THE ASSETS, BOOK VALUE OR POTENTIAL EARNINGS OF THE ISSUER OR ANY OTHER RECOGNIZED CRITERIA OF VALUE.

IN MAKING AN INVESTMENT DECISION, INVESTORS MUST RELY ON THEIR OWN EXAMINATION OF THE ISSUER AND THE TERMS OF THE OFFERING, INCLUDING THE MERITS AND RISKS INVOLVED. THESE SECURITIES HAVE NOT BEEN RECOMMENDED BY ANY FEDERAL OR STATE SECURITIES COMMISSION OR REGULATORY AUTHORITY. FURTHERMORE, THE FOREGOING AUTHORITIES HAVE NOT CONFIRMED THE ACCURACY OR DETERMINED THE ADEQUACY OF THIS OFFERING CIRCULAR. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE. THESE SECURITIES ARE SUBJECT TO RESTRICTIONS ON TRANSFERABILITY AND RESALE AND MAY NOT BE TRANSFERRED OR RESOLD EXCEPT AS PERMITTED UNDER THE APPLICABLE STATE SECURITIES LAWS, PURSUANT TO REGISTRATION OR EXEMPTION THEREFROM. INVESTORS SHOULD BE AWARE THAT THEY WILL BE REQUIRED TO BEAR THE FINANCIAL RISKS OF THIS INVESTMENT FOR AN INDEFINITE PERIOD OF TIME.

THE SECURITIES OFFERED HEREBY HAVE NOT BEEN REGISTERED UNDER THE SECURITIES ACT OF 1933, AS AMENDED, OR THE SECURITIES LAWS OF CERTAIN STATES AND ARE BEING OFFERED AND SOLD IN RELIANCE ON EXEMPTIONS FROM THE REGISTRATION REQUIREMENTS OF SAID ACT AND SUCH LAWS. THE SECURITIES HAVE NOT BEEN APPROVED OR DISAPPROVED BY THE SECURITIES AND EXCHANGE COMMISSION, ANY STATE SECURITIES COMMISSION OR OTHER REGULATORY AUTHORITY, NOR HAVE ANY OF THE FOREGOING AUTHORITIES PASSED UPON OR ENDORSED THE MERITS OF THIS OFFERING OR THE ACCURACY OR ADEQUACY OF THE OFFERING CIRCULAR. ANY REPRESENTATION TO THE CONTRARY IS UNLAWFUL.

THE COMPANY WILL BE PERMITTED TO MAKE A DETERMINATION THAT THE PURCHASERS OF SHARES IN THIS OFFERING ARE “QUALIFIED PURCHASERS” IN RELIANCE ON THE INFORMATION AND REPRESENTATIONS PROVIDED BY THE PURCHASERS REGARDING THE PURCHASERS’ FINANCIAL SITUATION. BEFORE MAKING ANY REPRESENTATION THAT YOUR INVESTMENT DOES NOT EXCEED APPLICABLE THRESHOLDS, THE COMPANY ENCOURAGES YOU TO REVIEW RULE 251(D)(2)(I)(C) OF REGULATION A. FOR GENERAL INFORMATION ON INVESTING, THE COMPANY ENCOURAGES YOU TO REFER TO WWW.INVESTOR.GOV.

| 4 of 59 |

STATE LAW EXEMPTION AND INVESTOR SUITABILITY REQUIREMENTS

The Shares are being offered and sold only to “qualified purchasers” (as defined in Regulation A under the Securities Act). As a Tier 2 Offering pursuant to Regulation A under the Securities Act, this Offering will be exempt from state law “blue sky” review, subject to meeting certain state filing requirements and complying with certain anti-fraud provisions, to the extent that the Shares offered hereby are offered and sold only to “qualified purchasers” or at a time when the Shares are listed on a national securities exchange. “Qualified purchasers” include: (i) “accredited investors” under Rule 501(a) of Regulation D and (ii) all other investors so long as their investment in the Shares does not represent more than 10% of the greater of their annual income or net worth (for natural persons), or 10% of the greater of annual revenue or net assets at fiscal year-end (for non-natural persons). Accordingly, the Company reserves the right to reject any investor’s subscription in whole or in part for any reason, including if the Company determines in its sole and absolute discretion such investor is not a “qualified purchaser” for purposes of Regulation A.

To determine whether a potential investor is an “accredited investor” for purposes of satisfying one of the tests in the “qualified purchaser” definition, the investor must be a natural person who has:

| 1. | an individual net worth, or joint net worth with the person’s spouse, that exceeds $1,000,000 at the time of the purchase, excluding the value of the primary residence of such person; or |

| 2. | earned income exceeding $200,000 in each of the two most recent years or joint income with a spouse exceeding $300,000 for those years and a reasonable expectation of the same income level in the current year. |

If the investor is not a natural person, different standards apply. See Rule 501 of Regulation D for more details.

| 5 of 59 |

TABLE OF CONTENTS

| IMPORTANT NOTICES TO INVESTORS | 4 |

| STATE LAW EXEMPTION AND INVESTOR SUITABILITY REQUIREMENTS | 5 |

| TABLE OF CONTENTS | 6 |

| CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS | 7 |

| OFFERING CIRCULAR SUMMARY | 12 |

| THE OFFERING | 16 |

| RISK FACTORS | 18 |

| LEGAL, TAX AND REGULATORY RISKS | 23 |

| RISK RELATED TO CONFLICTS OF INTEREST | 25 |

| PLAN OF DISTRIBUTION | 26 |

| USE OF PROCEEDS | 28 |

| DESCRIPTION OF BUSINESS | 29 |

| COMPANY STRUCTURE GRAPHIC | 30 |

| MANAGEMENT’S ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 34 |

| PLAN OF OPERATIONS | 35 |

| DIRECTORS, EXECUTIVE OFFICERS AND SIGNIFICANT EMPLOYEES | 39 |

| COMPENSATION OF MANAGEMENT AND DIRECTORS | 45 |

| PRINCIPAL SHAREHOLDERS AND OTHER COMPANY SHAREHOLDERS | 46 |

| CERTAIN RELATIONSHIPS AND RELATED PARTY TRANSACTIONS | 47 |

| SHAREHOLDERS’ RIGHTS UNDER THE COMPANY’S OPERATING AGREEMENT | 49 |

| FEDERAL INCOME TAX CONSEQUENCES OF AN INVESTMENT IN THE COMPANY | 54 |

| LEGAL MATTERS | 56 |

| EXPERTS | 57 |

| ADDITIONAL INFORMATION | 58 |

| PART FS - AUDITED FINANCIAL STATEMENTS | F-1 |

The following Table of Contents has been designed to help you find important information contained in this Offering Circular.

The Company encourages you to read the entire Offering Circular. |

| 6 of 59 |

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

Some of the statements under “Offering Circular Summary,” “Risk Factors,” “Description of Business”, “Plan of Operations,” and elsewhere in this Offering Circular constitute forward-looking statements. Forward-looking statements relate to expectations, beliefs, projections, future plans and strategies, anticipated events or trends and similar expressions concerning matters that are not historical facts. In some cases, you can identify forward-looking statements by terms such as “anticipate,” “believe,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “potential,” “should,” “will” and “would” or the negatives of these terms or other comparable terminology. In this Offering Circular, unless the context indicates otherwise, references to “we”, “our”, and “the Company” refer to ROCKSTAR CAPITAL GROUP LLC.

The forward-looking statements are based on the Company’s beliefs, assumptions and expectations of its future performance, taking into account all information currently available to the Company. These beliefs, assumptions and expectations can change as a result of many possible events or factors, not all of which are known to the Company or are within its control. If a change occurs, its business, financial condition, liquidity and results of operations may vary materially from those expressed in its forward-looking statements. You should carefully consider these risks before you make an investment decision with respect to the Shares, along with the following factors that could cause actual results to vary from the Company’s forward-looking statements:

| · | Although this is technically a blind pool Offering, since the Company will not identify all specific loans to service with the Net Proceeds of this Offering, the Manager represents that he has been working with the same core group of Affiliates for an extended period of time to provide financing for land and/or development projects, and further affirms that it has already identified prepared several projects ready to finance with the proceeds from this Offering. |

| · | The Company commenced operations on October 5, 2022 and is an affiliate of Rockstar Capital Development Group, Rockstar Capital II, LLC, Rockstar Capital Development Group II, LLC, Rockstar Capital Development Group III, LLC, and all GPs and LPs associated with the aforementioned entities. |

| · | The Company has made no investments to date. |

| · | Traditionally, the real estate loan industry is cyclical in nature, causing it to experience dramatic swings in value. Real estate has generally appreciated in value over time, allowing borrowers to repay back their loans, but the Company cannot assure that such appreciation will continue to occur, especially given then present rise of interest rates across the U.S. economy. |

| · | The Shares are non-voting. As such, Investors do not have a right to participate in the management of the Company’s affairs. Investors cannot propose changes to the Manager or to the Operating Agreement. The Manager will make all decisions with respect to the management of the Company. Investors will have no right or power to take part in the management of the Company. Therefore, they will be relying entirely on the Manager for management of the Company and the operation of its business. The Manager may not be removed under the Operating Agreement. |

| · | The Manager will have an exclusive role in determining what is in the best interests of the Company. Since no individual other than the Manager has any direct control over management of the Company, it does not have the benefit of independent consideration of issues affecting its operations. Therefore, the Manager will determine the propriety of its own actions, which could result in a conflict of interest and a risk to the viability and success of the Company when they are faced with any significant decisions relating to the affairs of the Company. |

| · | The Company may need to raise additional capital to address liquidity needs caused by shortfalls in revenue or unanticipated expenses. There can be no assurance that additional financing will be available when needed on terms favorable to the Company or at all. The Manager reserves the right to add capital from its own individual accounts to make up for such shortfall if it so desires. |

| · | Although the Company does not exercise direct control in the management of the properties to which the Company issues loans, the Company does exercise due diligence in ensuring that only properties that can be permitted and developed are loaned to. However, Borrower properties are not always directly owned by the Borrower, and so this lack of complete legal control represents an inherent risk. |

| · | Investors will not have any interest in, and their investment will not be secured by any Company Loans. Any returns on that investment will depend solely on the results of operations of the Company Loans. |

| 7 of 59 |

| · | An Investor’s return on an investment will depend on the successful development or acquisition, results of operations, and/or profitable disposition of Company Properties. |

| · | The Company intends to establish an operating reserve account with a portion of the proceeds raised from this Offering to pay anticipated operating, administrative and other expenses that shall be incurred as part of this Offering. If future expenses increase by unanticipated amounts, the Company may not have sufficient reserves to pay these obligations. The Company does not currently have any commitment or arrangement in place to obtain additional Funding, and there are no assurances that additional Funding can be obtained, if necessary, or that such additional Funding, if obtained, will be adequate for its financial needs. |

| · | The real estate market is affected by many factors, such as general economic conditions, the availability of financing, interest rates and other factors, including the supply and demand for real estate investments, all of which are beyond the control of the Company all of which could materially affect the Company and the Shares. There are no assurances that the Company can successfully achieve its investment goals and therefore, Investors may have to hold their Shares for an indefinite period of time, or have their Shares sold or redeemed prior to the Investment Period. The Manager affirms that it does not anticipate nor expect Investors to receive less than their Capital Contribution in the event of a default, but acknowledges that it is a possibility in the event that substantial loan defaults occur. |

| · | Environmentally hazardous property. Under various federal, state and local environmental laws, ordinances and regulations, a current or previous owner or operator of real property may be liable for the cost of removal or remediation of hazardous or toxic substances on, under or in such property. Such laws often impose liability whether or not the owner or operator knew of, or was responsible for, the presence of such hazardous or toxic substances. Environmental laws also may impose restrictions on the manner in which property may be used or businesses may be operated, and these restrictions may require expenditures. Environmental laws provide for sanctions in the event of noncompliance and may be enforced by governmental agencies or, in certain circumstances, by private parties. |

| · | There will be competing demands on the Manager, Employees, and Borrowers and they will not devote all of their attention to the Company, which could have a material adverse effect on the Company’s business and financial condition. The officers of the Manager will experience conflicts of interest in managing the Company, because they also have management responsibilities for other companies, including companies that conduct the same Investment Activities as the Company. For these reasons, all of these individuals share their management time and services among those companies, and the Company, and will not devote all of their attention to the Company. |

| · | Investors may not be able to withdraw Shares from the Company whenever they desire, particularly if that falls outside the investment period outlined by the Manager. Although the Manager will strive to honor requested redemptions, such redemptions are ultimately in the Manager’s sole and absolute discretion, and if the Manager believes that the Company is in need of capital reserves during the period when an Investor makes such a withdrawal request, the Manager is within its rights to make such a denial. Consequently, Investors may not be able to liquidate their Interests prior to the termination of the Company and must be prepared to bear the risks of owning Shares for an extended period of time. |

| · | There is no present public trading market for the Shares and the price at which the Shares are being offered bears no relationship to conventional criteria such as book value or earnings per share. |

| · | Although the Manager has been working with the same core team of Affiliates and Strategic Partners for an extended period of time, there is still the possibility that Company employees may change from time to time. Turnover may result in negative consequences to the Company’s Investment Activities. |

| · | The Manager will endeavor to communicate in advance any perceived exceeded risk based on the Manager’s anticipation of not meeting the required interest payouts, accrual, and/or withdrawal of Capital Contributions. The Manager will not communicate normal operational challenges including but not limited to construction delays, termination or reprimanding of Employees, and lawsuits as part of the Investment Activities. |

| · | The Company’s assessment of the merits of any identified projects under consideration may be inaccurate, which may negatively affect its results of operations. |

| · | Timing of development in real estate financing related projects is inherently uncertain and any delays in the development or acquisitions of Company Properties will adversely affect an investment. |

| 8 of 59 |

| · | There is a risk that no market for the Shares will ever exist and as a result, the investment in the Company is illiquid in the event a Investor desires to liquidate their interest. If an Investor attempts to sell its Shares prior to the dissolution of the Company, there is no certainty that they can be sold for full market value or that the Shares may be sold at any price. |

| · | There is an investment risk of losing the whole investment. There can be no assurance that the Company will be able to achieve its investment objectives or that Investors will receive any return of their capital. Investment results may vary substantially over time and as a result, Investors should understand the results of a particular period will not necessarily be indicative of results in future periods. |

| · | The revenue and profit potential of the company are uncertain. If the Company meets its revenue expectations, there is no guarantee that the Company will be profitable or that costs will not exceed revenue. |

| · | The Company may not generate sufficient income to fund the Preferred Return and there is a risk that the Company may never pay such Preferred Return. Additionally, the Company may use other sources including borrowings and sales of assets. If it pays interest on the Shares from sources other than its cash flow from operations, it will have less funds available for investments and your overall return may be reduced. |

| · | As Rockstar Capital Group Management Corporation (the “Manager”) will exercise complete control over the Company, it will have the ability to make decisions regarding (i) changes to share classes without Member notice or consent, (ii) making changes to the Company’s Operating Agreement as to the issuance of additional Shares, including to itself, (iii) employment decisions, including compensation arrangements; and (iv) the decision to enter into material transactions with related parties. |

| · | The Company’s Operating Agreement, Qualification Profile, and Subscription Agreement, all provide mandatory binding arbitration provisions that, unlike in judicial proceedings, are subject to determination by an arbitrator, not a judge, who is not necessarily governed by the same standards. In light of that, there is a risk that an arbitrator will not view the contract or the law in the same way a judge would and may grant a remedy or award relief that the arbitrator deems just and equitable and within the scope of the agreement of the parties or based on simple notions of equity, rather than the facts or the relevant law. Furthermore, there is a risk that an arbitrator may interpret the relevant agreements or facts without regard to legal precedent. That risk is exacerbated by the fact that it is more difficult to overturn or vacate an arbitration award, because the law supports confirmation of an arbitration decision which is not otherwise arbitrary or capricious; therefore, investors should consider the difficulty of reversing an arbitration award, once made. |

| · | The Company’s long-term growth depends upon its ability to retain and grow its investor base by successfully identifying and financing projects with attractive returns on investment. If the Company is unable to find such projects or if Company Loans do not produce the expected returns, it may be unable to retain or grow its investor base, and its operations and business could be adversely affected. |

| · | There has been no public market for the securities of the Company. The Shares will not be listed on any securities exchange. There will be no active market for the Shares. |

| · | There is a risk that an audit of the Company’s records could trigger an audit of the individual Investor’s tax records. |

| · | The incapacitation of key operational and management personnel could adversely affect the Company. |

| · | The Manager may invest a significant amount of the proceeds raised on behalf of the Company in ways that Investors may not agree or that do not yield maximum favorable return due to market cycles |

| · | The acquisition, entitlement, and permitting of real estate entails various risks, including the risk that investments may not perform as expected. The prices paid, or to be paid, for any Borrower Property are based upon a series of market judgments, some of which may prove to be inaccurate. These risks could adversely affect the Borrower’s financial condition, results of operations, cash flow and ultimate ability to service or repay the Financing which are the basis of Investors’ Preferred Return. |

| · | The success of the Investment Activities will depend largely on adapting to trends in the real estate industry, including competitive pressures, increased consolidation, industry overbuilding and changing demographics, the introduction of new concepts and products, availability of labor, changing tenant pricing levels and general economic conditions. Failures in adapting to the foregoing may affect the Company’s financial performance and thus the profits it receives. |

| 9 of 59 |

| · | The Company’s geographic focus consists of the sizable area of the United States, with a particular focus on the Southeast, Southwest, and Midwest regions of the United States, although the Company retains the right to invest outside this area if the opportunity arises. The Company’s overall performance is therefore largely dependent on real estate economic conditions in these geographic areas. Since there are no diversification requirements with regard to the Company’s investment activities the Company’s investment portfolio may include a small number of large positions, and at times, in a limited number of geographic markets. While such a portfolio concentration may enhance Company profits, if any large position has a material loss, then returns to Investors may be lower than if the Company had invested in a more diversified and widespread portfolio of smaller positions. Such concentration may increase the volatility of the Company’s returns and may also expose the Company to significant risk of economic downturns in this sector to a greater extent than if its portfolio was further diversified. Although the Manager will strive to ensure the Company meets its financial objectives, those objectives may at one time or another require deployment of capital in a limited number of opportunities, thus limiting diversification by practical necessity. As a result, economic downturns in the real estate sector could have an adverse effect on the financial condition, results of operations and cash flow of the Company. |

| · | The SEC heavily regulates the manner in which “investment companies,” “investment advisors,” and “broker-dealers” are permitted to conduct their business activities. The Company firmly believes the Company has conducted business in a manner that does not result in the Company or its affiliates being characterized as an investment company, an investment advisor or a broker-dealer, as the Company does not believe that the Company engages in any of the activities described under Section 3(a)(1) of the Investment Company Act of 1940 or Section 202(a)(11) or the Investment Advisor’s Act of 1940 or any similar provisions under state law, or in the business of (i) effecting transactions in securities for the account of others as described under Section 3(a)(4)(A) of the Exchange Act or any similar provisions under state law or (ii) buying and selling securities for our own account, through a broker or otherwise as described under Section 3(a)(5)(A) of the Exchange Act or any similar provisions under state law. The Company intends to continue to conduct our business in such manner. If, however, the Company (or any of the Company’s affiliates) are deemed to be an investment company, an investment advisor, or a broker-dealer, the Company may be required to institute burdensome compliance requirements and our activities may be restricted, which would affect the Company’s operations to a material degree. |

| · | Any Investor’s ability to bring legal action against the Manager for these actions is limited. |

| · | This Offering Circular, as well as other documents connected herewith, may contain “forward-looking statements,” such as statements related to financial condition and prospects, lending risks, plans for future business development and marketing activities, capital spending and financing sources, capital structure, the effects of regulation and competition, and the prospective business of the Company. Where used in this Offering Circular, the words “anticipate,” “believe,” “estimate,” “expect,” “intend,” as well as other or similar words and expressions, as they relate to the Company, identify forward-looking statements. All forward-looking statements, by their nature, are subject to risks and uncertainties. Results may differ materially from those set forth in the forward-looking statements. The Company’s ability to achieve financial objectives could be adversely affected by the factors discussed in detail in throughout the Offering Circular as well as the following: |

| a. | Changes in the securities and real estate markets; |

| b. | The strength of the United States economy in general and the strength of the local economies in which we conduct operations; |

| c. | Changes in monetary and fiscal policies of the U.S. Government; |

| d. | Inflation, interest rate, market and monetary fluctuations; |

| e. | Legislative or regulatory changes; |

| f. | The accuracy of the Company’s estimates and assumptions; |

| g. | The loss of key personnel; |

| h. | The Company’s need and ability to incur additional debt or equity financing; |

| i. | The effects of harsh weather conditions, including hurricanes; |

| 10 of 59 |

| j. | The Company’s ability to comply with the extensive laws and regulations to which it is subject; |

| k. | Increased competition and its effect on pricing; |

| l. | Technological changes; |

| m. | The effects of security breaches and computer viruses that may affect Company computer systems; |

| n. | Changes in consumer spending and saving habits; |

| o. | Changes in accounting principles, policies, practices or guidelines; |

| p. | Our ability to manage the risks involved in the foregoing. |

| 11 of 59 |

OFFERING CIRCULAR SUMMARY

This summary highlights selected information contained elsewhere in this Offering Circular. This summary is not complete and does not contain all the information that you should consider before investing in Shares. You should carefully read the entire Offering Circular including the risks associated with an investment in the specific securities you are offered, which are discussed under the “Risk Factors” section of this Offering Circular, before making an investment decision. Some of the statements in this Offering Circular are forward-looking statements. See the section of this Offering Circular entitled “Cautionary Statement Regarding Forward-Looking Statements.” In this Offering Circular, unless the context indicates otherwise, references to “we”, “our”, and “the Company” refer to Rockstar Capital Group LLC.

Overview

The Company is an Arkansas Limited Liability Company formed on October 5, 2022 for the purpose of raising capital to engage in the business of investing in all forms of real estate, primarily by providing financing to affiliated and unaffiliated Borrowers (“Investment Activities”).

The Company intends to raise capital to engage in the business of investing in all forms of real estate, primarily by issuing short-term loans (“Investment Activities”), providing working capital and project financing (“Project Financing”), and/or land financing (“Land Financing”) to affiliated and unaffiliated individuals and/or entities (“Borrowers”).

The Borrowers plan to acquire, permit, and develop land in the southeastern United States (the “Borrower Properties”) for the purpose of resale of permitted lots (“Permitted Real Estate Lots”) to regional or national homebuilders, hedge funds, or other arm’s length buyers. In addition, the Company may invest in properties that the Company’s Manager considers to be desirable to acquire or develop, and therefore suitable for investment, either directly, or indirectly through partnerships or strategic relationships with arm’s length and affiliated real estate developers and builders (“Qualified Properties”).

Purchasers of the Preferred Shares will become owners of the Shares (“Investors”) upon execution of the Subscription Agreement, submission of the Investor Qualification Questionnaire, delivery of the investment funds (“Capital Contribution”), and acceptance by the Manager, which is Rockstar Capital Group Management Corporation.

The Offering commenced on February 7, 2023 and will terminate upon the earlier of: (i) the completion of the sale of all of the Shares, or (ii) at the discretion of the Manager. The Offering may be extended by the Company in its sole discretion (the "Offering Period"). The Company is offering a minimum of ten (10) Shares and a maximum of seventy-five thousand (75,000) Shares. Each Unit is priced at One Thousand ($1,000) Dollars and a minimum purchase of ten (10) Shares is required, although the minimum number of Shares may be offered in fractions at the discretion of the Manager. The executive management of the Company may purchase less. Any number of additional Shares may be purchased.

This is an initial Offering by the Company on a “best efforts” basis for its Class A Non-Voting Preferred Shares. Company management (“Management”) will be making the investment decision about which loans to provide and to which borrowers such loans will go. The Manager is an Arkansas corporation, and an affiliate of the Company.

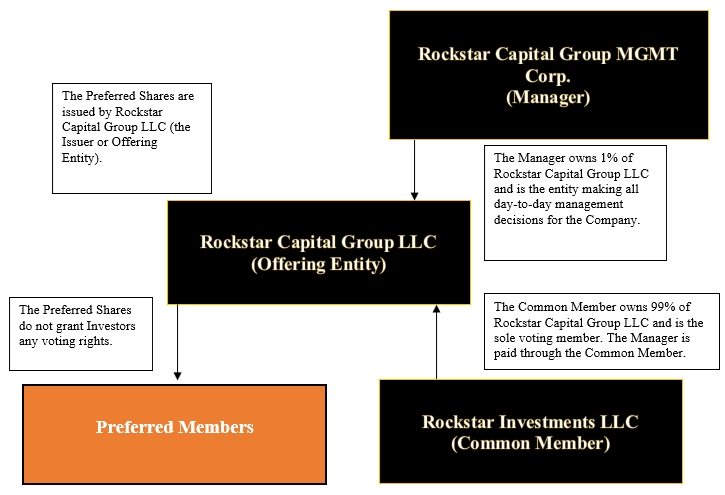

Substantially all of the Company’s assets will be directly held by the Company, and substantially all of its operations will be conducted by the Manager. Under this structure, the Common Member shall be Rockstar Investments LLC, an affiliate of the Manager. Only Rockstar Investments LLC shall have any voting rights as it relates to the Company.

The proceeds from the Offering may be used to (i) pay fees and expenses relating to the organization of the Company and the sale of Shares, (ii) invest in loans to made to Borrowers for various qualified properties and (iii) establish working capital reserves for the Company to fund operating and other expenses of the Company. The Company expects to use the Offering proceeds to pay such amounts at such time and in such order as the Management deems, in its sole and absolute discretion, to be in the best interest of the Company.

The expenses of this Offering, including the preparation of this Offering Circular and the filing of this Offering Statement, are being paid for on behalf of the Company by the Sponsor, and will be repaid to Sponsor from the Company’s working capital reserves, the timing of which shall be as Management deems, in its sole and absolute discretion, to be in the best interest of the Company.

Classes of Shares Offered: Class A Non-Voting Preferred Shares

The Company has established one non-voting class of Shares, known as Class A Preferred Non-Voting Shares (“Class A Shares”) each with $1,000 par value per Unit (“Shares”) and seeks to raise $75,000,000 through the sale of 75,000 Shares. Shares will have the right to Interest Payments and Special Preferred Return. See “MEMBER RIGHTS UNDER THE COMPANY’S OPERATING AGREEMENT.”

| 12 of 59 |

No Preferred Return to holders of Shares are assured, nor are any returns on, or of, a purchaser’s investment guaranteed. Preferred Return are subject to the Company’s ability to generate positive cash flow from operations. All Preferred Returns are further subject to the discretion of the Manager. It is possible that the Company may have cash available for Preferred Return, but the Manager could determine that the reservation, and not distribution, of such cash by the Company would be in its best interest.

Class A Non-Voting Shares

The Company is issuing a maximum of seventy-five thousand (75,000) Non-Voting Preferred Shares at a price of one thousand ($1,000) dollars per share, with a minimum purchase requirement of ten (10) shares or ten thousand ($10,000) dollars. The Class A Preferred Shares grant Investors the right to a non-cumulative, non-compounding Preferred Return of ten (10%) percent annually, anticipated to be paid quarterly.

If the Manager misses making a payment in a particular period, that interest will still accrue for that period such that Investors attains the ten (10%) percent annualized Preferred Return. Investors in the Class A Shares are also entitled to participate in a profit-sharing plan with the Company. This profit-sharing plan allows Investors to share in company profits—outside of those earmarked to pay the Preferred Return to Class A Members—and receive sixty (60%) percent of all such Company profits. The Manager will receive forty (40%) percent of such Company profits under the profit-sharing plan. Distributions of Member returns will be as follows:

| 1. | First, a distribution in an amount equal to ten (10%) percent of the Preferred Member's Capital Contribution ("Preferred Return") which shall be reflected as a return of capital on an annual Schedule K-1 (Form 1065) which will reduce the basis of the Members' Capital Account for tax purposes for that year. |

| 2. | Second, to pay any accrued, unpaid expenses owed by the Company, to its subsidiaries, or their affiliates. |

| 3. | Third, to pay the Manager the Asset Management Fee. |

| 4. | Fourth, to the Manager or its affiliates to repay any advances made to the Company, or its subsidiary with accrued interest as outlined in Section 5 on such advances; then |

| 5. | Fifth, a distribution, which may be made quarterly or at any other time to the extent available, to Members as Profit Participation, based upon the Net Distributable Cash Flow, payable sixty (60%) percent to the Preferred Members and forty (40%) percent to the Manager. |

| 6. | Distributions paid to Rockstar Investments LLC (the “Common Member”). |

Liquidation

In the event of the Company liquidating its assets, the priority of distributions (“Liquidation Distributions”) shall be performed in the

following manner:

| 1. | First, to creditors of the Company, including Preferred Members who may be creditors, to the extent otherwise permitted by law, in satisfaction of all debts, liabilities, obligations and expenses of the Company, including, without limitation, the expenses incurred in connection with the liquidation of the Company; and |

| 2. | Second, to the Preferred Members to the extent of and in proportion to their invested capital until the aggregate amount paid to such Preferred Shareholders is sufficient to provide for a complete return of such Preferred Members’ invested capital; |

| 3. | Third, to the Preferred Members to the extent of and in proportion to their respective unpaid Preferred Return until such Preferred Member’s unpaid Preferred Return has been paid in full; and |

| 4. | Fourth, to the Manager. |

| 13 of 59 |

Services Performed by, and Compensation Paid to Affiliates

The Manager and its Affiliates will be engaged by the Company to perform various services for day-to-day management of the Company including the identification of Borrowers, investment of its assets, and any other actions in furtherance of the Investment Activities. The Company and its Affiliates may receive compensation and profits for such services as described in this section. None of the agreements for such services are the result of arm’s-length negotiations. The Company believes, however, that the terms of such arrangements are reasonable and are comparable to those that could be obtained from unaffiliated entities. The timing and nature of the compensation could create a conflict between the interests of the Manager, its Affiliates, and those of Investors. Services performed by Company Affiliates include the following:

Asset Management Fees. The Company shall pay to the Manager (or another party at the election of the Manager), an annual Asset Management Fee of one and one half (1.5%) percent of all Capital Contributions to the Company.

Acquisition and Disposition of Projects. The Company may pay fees to Affiliates of the Manager that are licensed real estate brokers and other parties upon the acquisition or disposition of an investment project, not to exceed three (3.0%) percent of the purchase price or sales price, or at market rates, whichever is higher. The payment of the above fees shall be offset and reduced by any fees received from a co-broker or third party in connection with a transaction described above.

Company Expenses. Company expenses such as Marketing expenses may be paid with the Company’s funds.

Referral Fees. The Company reserves the right to contract with and compensate third parties who bring Prospective Investors to the attention of the Manager’s Executive Team. If the Manager elects this option, all such third parties shall be disclosed to Investors through the filing of a Form 1-U amendment.

Third Parties. Third parties may profit while working with the Company to facilitate Investment Activities.

Employees. The Company may employ employees to assist in the Company’s Investment Activities.

Conflicts of Interest

There are conflicts of interest between and among the Company, Manager, the Sponsor, and other Company Affiliates. The Manager may provide services to other affiliate companies in addition to the Company. All of the agreements and arrangements between and among Company Affiliates and the Company, including those related to compensation, are not the result of arm’s-length negotiations. The Company will try to balance the interests of Company Affiliates with the interests of the Company. However, to the extent that the Company takes actions that are more favorable to Company Affiliates than the Company, these actions could have a negative impact on the Company’s financial performance and, consequently, on the Preferred Return to holders of Shares and the value of those securities. The Company has not adopted, and does not intend to adopt in the future, either a conflicts of interest policy or a conflicts resolution policy.

Some of the conflict of interest risks are listed here.

· Manager or Company May be Involved in Similar Investments. The Manager, the Company, or their affiliates, may act as managers in other limited liability companies engaged in making similar investments.

· Manager or Company May Have Interests in Similar Properties. The Manager, the Company, or their affiliates, own or may come to own an interest in properties that may compete with Borrower’s Properties.

· Manager or Company May Act on Behalf of Others. The Manager or the Company, or their affiliates, who may act as managers for the Company, may act in such capacities for other companies, partnerships or entities that may compete with the Loans.

· Manager or Company May Raise Capital for Others. The Manager or the Company, or their affiliates, who will raise investment Funds, may act in the same capacity for other companies, partnerships or entities that may compete with the Loans.

· Manager’s or Company’s Compensation May be a Conflict. The compensation plan for the Manager or the Company may create a conflict between the interests of the Manager, the Company, and the interests of the Company.

· Manager or Company Allocating Time and Resources to Affiliated Entities. The Manager or the Company may have a conflict in allocating their time and resources between the Company and other business activities they are involved with.

| 14 of 59 |

· Principals of Manager and Company May Provide for Affiliated Partnerships. The principals of the Manager and the Company are comprised of individuals who may be principals of other affiliated or non-affiliated organizations organized to promote other real estate investments.

· Principals of Manager and Company. The Manager and the Company are comprised of individuals who may be principals of other affiliated or non-affiliated entities. One or more principals of the Manager and Company may provide additional or subsequent private offerings or terms of offer different than herein.

Competitive Strengths

The Company’s competitive strengths stem from the Management’s experience and understanding of the intricacies of the real estate borrowing sector. The Manager has twenty-two (22) years of experience in private lending and development is able to leverage that knowledge and experience in underwriting the loans to be provided by the Company.

Additionally, the Manager has already established an ecosystem of Rockstar-branded as well as other Affiliates in which the Company will operate, thus greatly reducing start-up risks. Much of the land that the Company is seeking funds for is already owned by Affiliates of the Manager, who simply require working capital to cover the soft costs of permitting the land. The Company will issue these loans with the proceeds of this Offering, and it will allow Investors to share in the upside from the interest charged on these transactions.

On the development side, the Manager has already established and worked with many Build-to-Rent (“BFR”) developers as well as traditional national homebuilders, creating a strategic pipeline of opportunities that seamlessly feed into one another.

Corporate Information

The Company’s executive offices are located at 23 Tamworth Circle, Bella Vista, AR 72715. The Company’s telephone number is 913-827-3517.

Reporting Requirements Under Tier 2 of Regulation A

Following this Tier 2 Regulation A Offering, the Company has, and will continue to be required to comply with certain ongoing disclosure requirements under Regulation A. The Company has, and will be required to file (i) an annual report with the SEC on Form 1-K, (ii) a semi-annual report with the SEC on Form 1-SA, (iii) current reports with the SEC on Form 1-U, and (iv) a notice under cover of Form 1-Z. The necessity to file current reports will be triggered by certain corporate events. Parts I and II of Form 1-Z will be filed by the Company if and when it decides to and is no longer obligated to file and provide annual reports pursuant to the requirements of Regulation A.

| 15 of 59 |

THE OFFERING

| Issuer: | Rockstar Capital Group LLC |

| Securities Offered: | Class A Non-Voting Preferred Shares |

| Par Value: | $1,000.00 per Unit. |

| Minimum Purchase: | Class A – Ten (10) Shares or Ten Thousand ($10,000) Dollars |

| Minimum Offering Amount: | N/A |

| Maximum Offering Amount: | 75,000 Shares ($75,000,000) |

| Escrow: | None. |

ERISA: |

Investment in the Company is generally open to institutions, including pensions and other Funds subject to ERISA. The Company may require certain representations or assurances from investors subject to ERISA to determine compliance with ERISA provisions. |

| Offering Price: | $1,000 per Preferred Share (“Offering Price”) |

| Offering Period: | To begin as soon as practicable after the Offering statement, of which this Offering Circular forms a part as soon as the Offering has been requalified by the SEC and will terminate December 31, 2023 (“Offering Period”). |

| The Offering Period may be extended, or the Offering terminated at any time by the Company in its sole discretion. | |

| Preferred Return: | No Preferred Return to holders of Shares are assured, nor are any returns on, or of, a purchaser’s investment guaranteed. Preferred Return are subject to the Company’s ability to generate positive cash flow from operations. All Preferred Return are further subject to the discretion of the Manager. It is possible that the Company may have cash available for Preferred Return, but the Manager could determine that the reservation, and not distribution, of such cash by the Company would be in its best interest. |

| Voting Rights: | None |

| Dilution: | Not applicable |

| Liquidation Rights: | None |

| Conversion Rights: | None |

| Pre-emptive Rights: | None |

| Sinking Fund Provision: | None |

| Liability for Further Calls: | None |

| Gross Proceeds: | The proceeds from this Offering prior to the payment of any commission, Offering expenses, Manager operating expenses, legal fees, fund management, supervisory and accounting services, and other working capital reserves (“Gross Proceeds”). |

| Net Proceeds: | Gross Proceeds, less organization and Offering expenses, Manager operating expenses (“Net Proceeds”). |

| Net Proceeds Allocation: | Based on raising the Maximum Offering Amount, the Company intends to initially allocate ninety-five (95%) percent of Net Proceeds to the financing of Borrower loans, and five (5%) percent of Net Proceeds to legal fees, fund management, supervisory and accounting services, and other working capital reserves. Management may change this allocation at any time based on the actual Net Proceeds of the Offering and Management’s sole determination of what is in the best interests of the Company. |

| 16 of 59 |

| Risk Factors: | Investing in the Shares involves a high degree of risk. See “Risk Factors” beginning on page 18 of this Offering Circular. |

| Liquidity: | There is no public market for the Shares. |

Withdrawals: |

Holders of Class A Shares shall be able, after a twelve (12) month period from the date their initial Capital Contribution is received by the Company, and upon the submission of a written request to the Manager, receive their initial Capital Contribution within one (1) month of the Manager receiving their written request. The Manager shall strive to honor all such requests but may refuse to do so if it is not in the Company’s best interest or if the Company does not have sufficient cash to cover these Withdrawals. All Withdrawal requests are in the sole and absolute discretion of the Manager. |

Rollover of Shares: |

Investors may select automatic rollover of Preferred Return. In case interest on Preferred Return is rolled over as per the request of the Investors, Company will still send an IRS Form 1099 for tax reasons. The Company may redeem an Investor’s capital at any time. |

Closing: |

The Company may close the Offering at any time and may suspend the Offering on a temporary basis from time to time as it deems necessary. |

| 17 of 59 |

RISK FACTORS

An investment in Shares of the Company involves a high degree of risk. You should carefully consider the following risk factors, together with the other information contained in this Offering Circular, before purchasing securities offered by the Company. Any of the following factors could harm the Company’s business and future results of operations and could result in a partial or complete loss of your investment. This could cause the value of Shares to decline significantly, and you could lose part or all of your investment. Some statements in this Offering Circular, including statements in the following risk factors, constitute forward-looking statements. Please refer to the section entitled “Cautionary Statement Regarding Forward-Looking Statements.”

RISKS RELATED TO THE OFFERING

This Offering is being made pursuant to the rules and regulations under Regulation A of the Securities Act.

The legal and compliance requirements of these rules and regulations, including ongoing reporting requirements related thereto, are relatively untested.

Arbitrary Determination of the Offering Price.

The Offering Price has been arbitrarily determined by the Company and may not bear any relationship to assets acquired or to be acquired or the book value of the Company or any other established criteria or quantifiable indicia for valuing a business. Neither the Company nor Sponsor represents that the Shares have or will have a market value equal to their Offering Price or that the Shares could be resold (if at all) at their original Offering Price.

No market currently exists for the Shares.

There is a risk that no market for the Shares will ever exist and as a result, an investment in the Company would be illiquid in the event investors were to desire to liquidate their Unit interests. If investors were to attempt to sell their Shares prior to the dissolution of the Company through secondary market sales or otherwise, they might have to sell them at a discount to their fair value as there is no certainty that they can be sold for full market value or that the Shares may be sold at any price.

RISKS RELATED TO THE COMPANY’S BUSINESS PLAN

General Risk of Investment in the Company.

The economic success of the Company will depend upon the results of operations of the Company loans issued to Borrowers. The results of operations are subject to those risks typically associated with the business of hard money lending, including the accuracy of underwriting said loans, and ensuring that Borrowers are able to repay the loans in a timely manner to ensure the Company can continue its operations. Although the experience of the Company’s Executive Team weights favorably, the Company makes no assurances that the Borrowers will successfully pay back their Company-issued loans in a timely manner. The traditional risks associated with any entity operating in the business of borrowing are all present here, which Investors should be mindful of. In addition, even if adverse operating results do not result in loan defaults, they will likely reduce the ability of the Company to make Preferred Return to Members.

Shares Have No Voting Rights.

Management will have sole power and authority over the business and management of the Company. Investors will not have the right to vote on any matters, and, therefore, Investors will not have an active role in the Company’s management and will be unable to implement a change in the Management team or the Management team’s decisions.

Preferred Return on the Shares are Not Guaranteed.

Although Preferred Return on the Shares are cumulative (but non-compounding), the Company’s Manager must approve the actual payment of the distributions. The Manager can elect at any time or from time to time, and for an indefinite duration, not to pay any or all accrued distributions. The Manager could do so for any reason, and may be prohibited from doing so in the following instances:

• poor historical or projected cash flows;

• the need to make payments on the Company’s indebtedness;

• concluding that payment of distributions on the Shares would cause the Company to breach the terms of any indebtedness or other instrument or agreement; or

• determining that the payment of distributions would violate applicable law regarding unlawful distributions.

| 18 of 59 |

Adverse economic conditions may negatively affect the Company’s results of operations and, as a result, its ability to make distributions to Investors or to realize appreciation in the value of Company loans.

The Company’s operating results may be adversely affected by market and economic challenges, which may negatively affect its returns and profitability and, as a result, its ability to make distributions to Investors and the value of an investment in the Company. These market and economic challenges include, but are not limited to, any future downturn in the U.S. economy and the related uncertainty in the financial and credit markets.

The length and severity of any economic slow-down or downturn cannot be predicted. The Company’s operations and, as a result, its ability to make distributions to holders of the Shares could be materially and adversely affected to the extent that an economic slow-down or downturn is prolonged or becomes severe.

The Company is a Blind Pool Investment without Operational Track Record prior to the Date of this Offering.

The Company has yet to identify all specific loans to finance with the Net Proceeds of this Offering and has no prior track record. However, the Manager affirms that it has a significant number of Borrower projects which are ready to be financed at present, but due to the fact that unexpected loan opportunities may arise, the Company cannot guarantee that it will only finance such already prospected projects. As a result, this Offering will generally operate as a Blind Pool Offering.

Investment Risk.

There can be no assurance that the Company will be able to achieve its investment objectives or that investors will receive any Preferred Return or any return of their capital. Investment results may vary substantially over time, and as a result, investors should understand that the results of a particular period will not necessarily be indicative of results in future periods.

Dependence Upon Key Management Personnel.

The Company will depend upon the efforts, experience, diligence, skill and network of business contacts of the Management team; therefore, the Company’s success will depend on their continued service. The departure of any of the Company’s key Management personnel could have a material adverse effect on performance. If any of the Company’s key personnel were to cease their employment, the Company’s operating results could suffer.

The Company believes its future success depends upon Management’s ability to hire and retain highly skilled managerial, operational and marketing personnel. Competition for such personnel is intense, and the Company cannot assure that it will be successful in attracting and retaining such skilled personnel. If the Company loses or is unable to obtain the services of key personnel, the Company’s ability to implement its investment strategies could be delayed or hindered, and the value of an investment in the Company may decline.

Reliance on Management.

The Company’s ability to achieve its investment objectives is largely dependent upon the performance of Management and the Sponsor, in selecting additional assets for the Company to acquire, securing financing arrangements, and financing the Company loans. The investors generally have no opportunity to evaluate the terms of transactions or other economic or financial data concerning any investments and must rely entirely on the ability of the Manager. The Manager may not be successful in identifying suitable investments on financially attractive terms, and the Company may not be successful in achieving its investment objectives.

There will be competing demands on the officers of the Manager, and they will not devote all of their attention to the Company, which could have a material adverse effect on the Company’s business and financial condition.

The officers of the Manager will experience conflicts of interest in managing the Company, because they also have management responsibilities for other companies, including companies that invest in the same types of assets as prospective Borrowers. For these reasons, all of these individuals share their management time and services among those companies, and the Company, and will not devote all of their attention to the Company.

| 19 of 59 |

RISKS RELATED TO INVESTMENTS IN REAL ESTATE LENDING

Legal Structure.

The Company shall provide Project Financing or Land Financing advances to the Borrower for Borrower Projects for which the Borrower does not have fee simple title. As such, Borrower Properties are typically controlled by, but not owned by the Borrower. As such, the Company’s source of Project Financing or Land Financing repayment is based on the Borrower’s perfection of its contractual rights under agreements to purchase the Borrower Property and subsequently sell it.

Risk of Borrower Inability to Obtain Financing.

The financial projections contained in this Memorandum assume that the Borrower will obtain other third-party financing. There is no guarantee that the Borrower will be able to obtain such financing.

Borrower Intends to Use Leverage.

The Company’s objectives are based on the Borrower’s use of leverage in the acquisition, development, construction, and operation of the Property. If the Borrower does obtain outside financing, the use of leverage increases the risk of an investment in the Shares, as it is possible that the Borrower’s income from the Property, in any month, will be inadequate to make the Company’s Project Financing or Land Financing debt-service after servicing other Borrower financing obligations. A result of being unable to make the required financing payments could be that the lender could complete a foreclosure on the Borrower and all of the investment in the Shares will be lost. There is also the risk that at the time of the refinancing or sale of the Property, the proceeds will not be greater than the amount needed to pay off the remaining balance of the Borrower’s other financing and, as a result, no cash will be available for repayment of the outstanding balance of the Project Financing, Land Financing, or any distribution to the Members.

The revenue is dependent upon a limited number of Homebuilders.

The Borrower Property will have one, or a small number of Homebuilders contracting to purchase Permitted Real Estate Lots. Although these Homebuilders are by and large members of the Top 25 National Builders in the country, and thus have outsize purchasing power, there is still a limited number of them, and Company revenues will be dependent upon effectuating successful land sales to these Homebuilders. There is a risk that these Homebuilders will not be able to fulfill their contractual obligations, and there is no guarantee that they will. If the Borrower is unable to receive payment from the Homebuilder for Permitted Real Estate Lots there is a risk that Project Financing or Land Financing, may not be paid. There is a risk of the Company being unable to pay its recurring operating expenses as a result, at the extreme, as the Company has no recourse to foreclosure on the Borrower Property and the Preferred Returns and Profit Participation distributions will not be able to be made.

Financial projections.

All financial projections are prepared on the basis of assumptions and hypotheses. Future operating results are impossible to predict and no representation of any kind is made with respect to future accuracy or completeness of the forecast of projections as to income, expenses, costs, or other items. No representations or warranties of any kind are intended or should be inferred with respect to economic return which may accrue to a Member. An investment in the Company should be made only after adequate personal investigation of the merits of the Company and the Offering.

Licensing Requirements.

The conversion of a Borrower Property into Permitted Real Estate Lots requires state, county, or local regulatory authority approval. While the Manager believes that Project Financing or Land Financing due diligence would provide assurance that the Borrower should be able to obtain such approvals, there can be no assurances that these approvals will either be obtained or be obtained on a timely basis.

Lack of capital.

There is a risk that the amount of capital to be raised by the Company will be insufficient to meet the investment objectives of the Company. If there is a shortage of capital, the Manager will use best efforts to obtain funds from a third party or advance the funds directly or through an affiliate. Obtaining funds from a third party or an advance directly or through an affiliate may require an increase in the amount of financing the Company will be obligated to repay. In addition, there is no certainty that such funds will be available at a reasonable cost, if available at all.

| 20 of 59 |

Risks of having no control in management.

Under the Operating Agreement, Members do not have a right to participate in the management of the Company’s affairs. Members cannot propose changes to the Manager or to the Operating Agreement. Under the Operating Agreement, it may also be difficult for Members to enforce claims against the Manager, which means that Members may not be able to recover any losses they may suffer through their ownership of Shares arising from acts of the Manager that harm the Company’s business.

The Manager and its management must discharge their duties with reasonable care, in good faith and in the best interest of the Company. Despite this obligation, the Operating Agreement limits management’s liability to the Company and all Members. The Manager is not liable for monetary damages unless it involves receipt of an improper personal financial benefit, a willful failure to deal fairly with the Company on matters where there is a material conflict of interest, a knowing violation of law, or willful misconduct. Any Member’s ability to bring legal action against the Manager for these actions is also limited. Members may only bring a legal action on behalf of the Company if the Company has refused to bring the action or an effort to cause the Manager to bring the action is not successful.

Limited Operating Reserves.

The Company intends to establish an operating reserve account with a portion of the proceeds raised from this Offering to pay anticipated operating, administrative and other expenses that shall be incurred following the Closing Date of this Offering. If future expenses increase by unanticipated amounts, the Company may not have sufficient reserves to pay these obligations. The Company does not currently have any commitment or arrangement in place to obtain additional funding, and there are no assurances that additional funding can be obtained, if necessary, or that such additional funding, if obtained, will be adequate for its financial needs.

General economic conditions may affect the value and the timing of the sale of Borrower Property or the ability to refinance the Borrower Property.

The real estate market is affected by many factors, such as general economic conditions, the availability of financing, interest rates and other factors, including the supply and demand for real estate investments, all of which are beyond the control of the Borrower. The Company cannot predict whether the Borrower will be able to sell the Borrower Property for a price or on terms which are acceptable. Further, the Company cannot predict the Borrower’s ability to obtain adequate funding from a third-party lender to refinance the Borrower Property. There are no assurances that the Company can successfully achieve its investment goals and therefore, Members may have to hold their Shares for an indefinite period of time, or have their Shares sold or redeemed for less than the Preferred Members’ Capital Contribution.

Environmentally hazardous property.

Under various federal, state and local environmental laws, ordinances and regulations, a current or previous owner or operator of real property may be liable for the cost of removal or remediation of hazardous or toxic substances on, under or in such property. Such laws often impose liability whether or not the owner or operator knew of, or was responsible for, the presence of such hazardous or toxic substances. Environmental laws also may impose restrictions on the manner in which property may be used or businesses may be operated, and these restrictions may require expenditures. Environmental laws provide for sanctions in the event of noncompliance and may be enforced by governmental agencies or, in certain circumstances, by private parties. In connection with the ownership of the Property, the Borrower may be potentially liable for such costs. The cost of defending against claims of liability, complying with environmental regulatory requirements or remediating any contaminated property could materially adversely affect the value of the Property and the Shares.

Real estate investments are long-term investments and may be difficult to sell in response to changing economic conditions.

Virtually all real property investments are subject to certain inherent risks. Real estate investments are generally long-term investments which cannot be quickly converted to cash. Real property investments are also subject to adverse changes in general economic conditions or local conditions which may reduce the demand for commercial property.

Project Financing and Land Financing issued to Borrower may be subject to other unsecured loans and subordinate to Secured Lender advances.

The Company advances Project Financing or Land Financing to the Borrower to fund the Borrower’s conversion of Borrower Properties into Permitted Real Estate Lots. The Borrower’s ability to repay Project Financing or Land Financing may be adversely affected by other Borrower secured first mortgage debt obligations, and other pari passu unsecured loans entered into by the Borrower.

| 21 of 59 |

Risks of Borrower Exceeding Budgets.

There is a risk that budgets could be exceeded resulting in the need for additional financing or equity contributions from the Borrower, and that in the absence thereof the Borrower would not be able to repay Project Financing or Land Financing.

Adverse Trends in the Single-Family Housing Industry May Impact the Project.

The success of the Project will depend largely on the ability of the Borrower to adapt to trends in the single family housing industry, including competitive pressures, increased consolidation, industry overbuilding and changing demographics, the introduction of new concepts and products, availability of labor, changing tenant pricing levels and general economic conditions. Failures in adapting to the foregoing may affect the Borrower’s financial performance and thus the Company’s it has available to service or repay the Project Financing or Land Financing.

Geographic Concentration and Sector Risk.

The Company’s geographic focus is not specifically limited, but the Manager does affirm that the Company intends to operate primarily within the Southeast, Southwest, and Midwest regions of the U.S. Its sector focus is to provide Project Financing and Land Financing, enter into strategic relationships with real estate developers and builders. The Company’s overall performance is therefore largely dependent on real estate economic conditions in these geographic areas and real estate sectors. Since there are no diversification requirements with regard to the Company’s investment activities the Company’s investment portfolio may include a small number of large positions, and at times, may include only one or two Borrower Properties in one or two geographic markets.

While such a portfolio concentration may enhance total returns to Investors, if any large position has a material loss, then returns to Investors may be lower than if the Company had invested in a more diversified and widespread portfolio of smaller positions. The Company’s investments will consist entirely of investments related to Investment Properties. Such concentration may increase the volatility of the Company’s returns and may also expose the Company to significant risk of economic downturns in this sector to a greater extent than if its portfolio also included other property types. As a result, economic downturns in the real estate sector could have an adverse effect on the financial condition, results of operations and cash flow of the Company.

Competition in the Market

The real estate borrowing industry is highly competitive on both a national and regional level. The Company faces competition from REITs, other hard-money providers, other public and private real estate companies, private real estate investors, and banks. Competition may prevent the Company from providing loans to Borrowers of desirable Qualified Properties, who can then either refinance and/or sell the property(ies) financed with the Company loans in order to make prompt repayment and keep up with the loan’s APR. If the Company offers lower interest rates to remain competitive, Investors may experience a lower return on investment and be less inclined to invest in the Company’s next project which may decrease its profitability. Increased competition for Borrowers may also preclude the Company from acquiring Borrowers that would generate the most attractive returns to Investors or may reduce the number of Borrowers the Company could acquire, which could have an adverse effect on its business.

Availability of Future Financing and Market Conditions.

Market fluctuations in real estate financing may affect the availability and cost of funds needed to successfully operate in the private lending space. Rising interest rates require Offerings to provide greater returns to be attractive to investors, and many Sponsors of such Offerings may require additional third-party financing for operation in the real estate industry, which is a highly capital intensive area.

Development or Construction Difficulties or Delays.

Some Company loans will be to Borrowers who will require development and construction, and the Company has no ability to complete the development and construction, which will be outside the Company’s control or even the control of the entity supervising the construction. These factors include, but are not limited to:

| · | difficulties or delays in obtaining building, occupancy, licensing and other required governmental permits and approvals; |

| · | unforeseen engineering, environmental or geological problems; |

| · | failure of third-party contractors and subcontractors to perform under their contracts; |

| · | shortages of labor or materials that could delay construction or make it more expensive than budgeted; |

| · | adverse weather conditions that could cause delays; |

| · | unionization or work stoppages; |

| · | force majeure events or other acts of God; |

| · | increased costs resulting from changes in general economic conditions or increases in the costs of materials; and |

| · | increased costs as a result of addressing changes in laws and regulations or how existing laws and regulations are applied. |

| 22 of 59 |

LEGAL, TAX AND REGULATORY RISKS

Legal, tax and regulatory changes could occur during the lifetime of the Company that may adversely impact the Company’s and Company Affiliates’ taxation status and any distributions from the Company, and Preferred Return to Shareholders.

Risk of Arbitration.