UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSRS

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-01911 |

|

Schroder Capital Funds (Delaware) |

(Exact name of registrant as specified in charter) |

|

875 Third Avenue, 22nd Floor New York, NY | | 10022 |

(Address of principal executive offices) | | (Zip code) |

|

Schroder Capital Funds (Delaware) P.O. Box 8507 Boston, MA 02266 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | 1-800-464-3108 | |

|

Date of fiscal year end: | October 31, 2012 | |

|

Date of reporting period: | April 30, 2012 | |

| | | | | | | | |

Item 1. Reports to Stockholders.

April 30, 2012 Semi-Annual Report

Schroder North American Equity Fund

Schroder U.S. Opportunities Fund

Schroder U.S. Small and Mid Cap Opportunities Fund

Schroder Emerging Market Equity Fund

Schroder International Alpha Fund

Schroder International Multi-Cap Value Fund

Schroder Global Quality Fund

Schroder Total Return Fixed Income Fund

Schroder Absolute Return EMD and Currency Fund

Schroder Mutual Funds

Table of Contents

Letter to Shareholders | 1 |

| |

Management Discussion and Analysis | 3 |

| |

Schedules of Investments | |

| |

North American Equity Fund | 24 |

| |

U.S. Opportunities Fund | 33 |

| |

U.S. Small and Mid Cap Opportunities Fund | 36 |

| |

Emerging Market Equity Fund | 39 |

| |

International Alpha Fund | 43 |

| |

International Multi-Cap Value Fund | 46 |

| |

Global Quality Fund | 61 |

| |

Total Return Fixed Income Fund | 70 |

| |

Absolute Return EMD and Currency Fund | 78 |

| |

Statements of Assets and Liabilites | 82 |

| |

Statements of Operations | 84 |

| |

Statements of Changes in Net Assets | 86 |

| |

Financial Highlights | 90 |

| |

Notes to Financial Statements | 94 |

| |

Disclosure of Fund Expenses | 110 |

Proxy Voting (Unaudited)

A description of the Funds’ proxy voting policies and procedures is available upon request, without charge, by visiting the Securities and Exchange Commission’s (“SEC”) website at http://www.sec.gov, or by calling 1-800-464-3108 and requesting a copy of the applicable Fund’s Statement of Additional Information or on the Schroder Funds website at http://www.schroderfunds.com, by downloading the Funds’ Statement of Additional Information. Information regarding how the Funds voted proxies related to portfolio securities during the most recent 12-month period ended June 30 is available without charge, upon request by calling 1-800-464-3108 and on the SEC’s website at http://www.sec.gov.

Form N-Q (Unaudited)

The Funds file their complete schedules of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. The Funds’ Form N-Q is available on the SEC’s website at http://www.sec.gov, and may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

Schroder Mutual Funds

June 11, 2012

Dear Shareholder:

The beginning of the reporting period for the US equity market was relatively volatile, but proved the best performing region overall. Moderately positive economic indicators, better-than-expected employment and manufacturing data and some good corporate earnings buoyed investor sentiment as the fourth quarter of 2011 progressed. The coordinated action taken by the Fed and five other major central banks to ease the dollar funding pressure, coupled with further encouraging data in December (a rebound in US consumer confidence and continued growth in the US services sector), boosted US stocks and saw equity markets end the year as a whole in positive territory.

Throughout Europe, the news through the end of 2011 triggered vast swings in sentiment and was borne out in equity markets during the fourth quarter. November saw a decent pick up in sentiment that drove share price gains, pulling equity markets firmly into positive territory over the fourth quarter as a whole. The European Central Bank (ECB) cut interest rates by 25 basis points (bps) at the beginning of November, with a further quarter percentage point cut in December. Stronger composite Purchasing Managers Index (PMI) data in December from the previous month offered some indication that the slowdown in Europe had been less severe than feared, while inflation showed signs of subsiding. As European politicians struggled to reach an agreement on a credible, long-term solution to the ballooning sovereign debt crisis, banks welcomed the ECB’s liquidity boost (designed to help ease funding pressures) with its sale of three-year loans attracting strong demand. While the move averted an interbank lending freeze, much of the money has been parked back at the ECB’s overnight deposit facility (a record high of €452 billion in December).

At the same time, Japanese equities struggled to find momentum over the beginning of the reporting period. The end of 2011 saw the yen hit record high levels against the US dollar, prompting the Japanese government to intervene to push the currency lower. Japanese exporters struggled with the persistently strong yen, which was driven higher as risk-averse investors sought safe havens amid the continued turmoil in the eurozone and concerns about the global economic outlook.

Robust consumer data from the US and an easing of panic over eurozone debt lifted Asian equities in the fourth quarter but failed to rescue them from their first annual decline in three years. Signs of a slowdown in growth across the region were underscored by China’s decision to lift the reserve requirement ratio on banks, marking the end of a two-year tightening cycle. Meanwhile, manufacturing activity expanded in India and China in December. Emerging market equities, as measured by the MSCI Emerging Markets Index, produced positive returns over the fourth quarter of 2011; however, they underperformed developed equities, reflecting the ‘risk off’ environment in equity markets as a result of macroeconomic problems in the eurozone.

Equity markets made a very strong start to 2012, ending the first quarter with the S&P 500 recording a return of more than 12%, the seventh best start to a year since 1928 according to Bloomberg figures. High beta cyclical sectors led the way with technology and financial stocks outperforming strongly while the more defensive telecoms, consumer staples and utilities lagged. Such a mix helped account for the strong performance of the German and Japanese markets with the DAX and Topix up around 20%.

Despite the rally in equity markets, government bond yields remained low. Yields rose following the US Federal Reserve’s policy statement on March 13th, when the Fed indicated it was slightly less wary about the outlook for growth but remained well below the levels of a year ago.

The end of the reporting period saw US markets falling slightly, as concerns over the European debt crisis, a focus on Spain and weak US economic news over the month of April as a whole, affected investor sentiment. Towards the end of April, the Federal Open Market Committee (FOMC) kept its monetary policy settings unchanged in order to support a stronger economic recovery and ensure that inflation stays at a consistent rate. Longer-term inflation expectations have remained stable. The FOMC stated that Operation Twist—designed to put downward pressure on longer-term interest rates to stimulate the economy while keeping short-term rates high to prevent an outflow of reserves — is still on schedule to run through to mid-year.

Growing risk aversion was reflected in eurozone equity markets as we closed the reporting period. Positive sentiment following the ECB’s €1 trillion liquidity injection was swiftly replaced with growing unease about political and economic stability in the region, while concerns about global growth prospects added to the gloom. We saw a change in ‘sector leadership’, with those more economically sensitive stocks that led the first-quarter rally in 2012 pulling back and defensive areas of the market benefiting from the retrenchment by investors.

The north-south divergence continued with northern and core European countries outperforming while Spanish and Italian equities were among the weakest performers. As peripheral country concerns escalated, with particular focus on Spain’s fiscal issues, Italian and Spanish bond yields rose significantly. The euro softened against the US dollar by the end of April, although a relatively hawkish monetary policy stance from the ECB provided some support. Interest rates remained on hold as we closed out April.

1

Looking forward, the improvement in US economic activity over the past six months has led many to argue that we are now in a self sustaining recovery. Better payroll figures have raised the prospect of stronger employment feeding into stronger income and spending figures. In response, investors are questioning the sustainability of the low level of bond yields in the US government bond market. While recognizing that rates will eventually rise, we believe it is too early to see an acceleration in US growth and a subsequent sell off in the Treasury market. Despite the better than expected start to the year, we continue to expect a year of subdued activity with growth around 2% in 2012.

Another issue which has dominated market sentiment lately has been the Euro crisis and the plight of Spain, which has been struggling to implement an austerity program and structural reform. In our view this is not over, as can be seen from our baseline forecast where we believe there is a high probability of a Greek exit from the eurozone in 2013. Investors are nervous again. We believe the rally in European risk assets at the start of the year is well and truly over. To make matters worse, it seems that the pick up in economic activity around the same time may also have been a temporary blip. We see the risk of recession intensifying which is making a further drive for austerity very difficult. This has been a battle ground in European politics for the last couple of years, though the beginning of the next reporting period may see even more debate, and possibly even some consequential change. Consensus growth forecasts for the current calendar year for the world economy are one percentage point lower than they were this time last year.

In conclusion, the world economy still faces a challenging 2012 with growth at subdued levels, but recent data points to stabilization in the manufacturing sector and policy makers have been more aggressive than expected in loosening monetary policy. As a result, we see a smaller recession than before in the Eurozone. Although tighter fiscal policy and banking sector de-leveraging remains a feature, Germany has proved to be more resilient than forecast while the ECB’s long-term repo operations liquidity measures are expected to have headed off the worse effects of the credit crunch.

Nonetheless, 2012 could prove to be a more difficult year. As it becomes apparent that Greece is missing it targets, the European and international authorities are likely to demand more austerity, which could force a Greek exit from the eurozone. The eurozone survives based on the view that much of the private sector exposure has been written off so far and firewalls are likely to be in place to prevent contagion to the rest of the periphery. However, the risk, of course, is that we are too optimistic and that a Greek exit would be a forerunner to a wider eurozone break up.

As we stated in the Funds’ Annual Report, in this type of environment, we believe that the investor who maintains a diversified portfolio — both across asset classes and geographic borders — should be able to weather the bumpy periods better than those who have high concentrations in one or two sectors or regions. We encourage you to consult with your financial advisor to ascertain whether your current mix of investments is suitable for your long-term objectives.

Again, we thank you for including Schroders in your financial plan and we look forward to our continued relationship.

| Sincerely, |

| |

| |

| /s/ Mark A. Hemenetz |

| |

| Mark A. Hemenetz, CFA |

| President |

The views expressed in the following report were those of each respective Fund’s portfolio management team as of the date specified, and may not reflect the views of the portfolio managers on the date this Annual Report is published or any time thereafter. These views are intended to assist shareholders of the Funds in understanding their investment in the Funds and do not constitute investment advice; investors should consult their own investment professionals as to their individual investment programs. Certain securities described in these reports may no longer be held by the Funds and therefore may no longer appear in the Schedules of Investments as of April 30, 2012.

2

Schroder North American Equity Fund

MANAGEMENT DISCUSSION AND ANALYSIS (As of May 31, 2012)

Performance

In the six months ended April 30, 2012, the Schroder North American Equity Fund (the “Fund”) rose 11.62% (Investor Shares) and 11.37% (Advisor Shares). For the same six-month period, the S&P 500 Index (the “Index”) rose 12.77%.

Market Background

Despite getting off to a rocky start in November after the downward revision of third-quarter GDP growth to an annual rate of 2% (from an earlier estimate of 2.5%) hit investor confidence, moderately positive economic indicators, better-than-expected employment and manufacturing data and some good corporate earnings buoyed sentiment through December. A rebound in US consumer confidence and continued growth in the US services sector added to investor confidence.

As we entered 2012, investors were seeing more reasons to be hopeful than pessimistic — on the back of improving economic data, and as concerns about eurozone sovereign debt began to ease following the European Central Bank’s (ECB’s) liquidity boost to the European banking system. The renewed optimism saw US equities continue to rally in the first three months of 2012, recording its strongest first quarter gains since 1998.

The US labor market added nearly three quarters of a million jobs in the first quarter 2012, boosting hopes for the global economic growth outlook. Indeed, figures towards the end of March showed the lowest number of initial jobless claims for nearly four years — highlighting the resilience of the economy.

The US Federal Reserve’s Open Markets Committee also extended its commitment to a near-zero benchmark interest rate through late 2014 (previously stating through mid-2013), further boosting risk appetite.

However, confidence began to deteriorate once more in April as concerns about economic and fiscal stability in peripheral European countries re-emerged. Despite losing steam towards the end of the period, positive sentiment drove US equity market gains overall.

Cyclical sectors benefited from growing risk appetite over the period. House-builders and building-related companies outperformed, along with banking stocks, retailers and oil-services names. Pockets of risk aversion also supported traditionally defensive stocks, such as tobacco companies.

Portfolio Review

Both the Fund and Index registered absolute gains over the period, although Fund returns lagged the benchmark.

Weaker stock selection among retailers, media and software names, along with the Fund’s larger relative exposure to minerals and mining stocks, accounted for the majority of the performance gap. Leading contributors included utilities and technology hardware stocks.

Outlook

The Fund remains well diversified, seeking a broad range of opportunities across the market. Multiple investment strategies are spread across a large number of small stock positions to capture broad themes and limit stock-specific risk while top down risks (such as those arising from region and sector positions) are carefully managed.

Within cyclical parts of the market, we prefer technology stocks, specifically semiconductors and hardware. Consumer discretionary remains an underweight within the Fund’s portfolio.

Within defensives, the Fund is overweight healthcare favoring service providers. The Fund continues to hold an underweight allocation to utilities.

Within resources, the Fund retains a preference for energy; we anticipate selectively favoring mining stocks that demonstrate very high levels of profitability.

In addition, the Fund’s strategy within financials remains focused on high quality companies.

3

PERFORMANCE INFORMATION

| | | | | | Annualized | |

| | One Year Ended | | Five Years Ended | | Since | |

| | April 30, 2012 | | April 30, 2012 (a) | | Inception | |

Schroder North American Equity Fund — | | | | | | | |

Investor Shares | | 3.75 | % | 1.33 | % | 6.19 | %(b) |

Advisor Shares | | 3.40 | % | 0.97 | % | 5.84 | %(c) |

Standard & Poor’s (S&P) 500 Index | | 4.76 | % | 1.01 | % | 5.76 | % |

(a) Average annual total return.

(b) The Investor Shares commenced operations on September 17, 2003.

(c) The Advisor Shares commenced operations on March 31, 2006. The performance information provided in the above table for periods prior to March 31, 2006 reflects the performance of the Investor Shares of the Fund, adjusted to reflect the distribution fees paid by Advisor Shares.

“Total Return” is calculated including reinvestment of all dividends and distributions. Results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. Results represent past performance and do not indicate future results. The value of an investment in the Fund and the return on investment both will fluctuate and redemption proceeds may be higher or lower than an investor’s original cost.

Top 5 Holdings

Security* | | % of Investments | |

Apple | | 4.0 | % |

ExxonMobil | | 3.1 | |

Microsoft | | 1.9 | |

International Business Machines | | 1.9 | |

Chevron | | 1.7 | |

* Excludes Short-Term Investment.

Sector Allocation

Sector | | % of Investments | |

Information Technology | | 18.2 | % |

Financials | | 13.5 | |

Healthcare | | 11.2 | |

Energy | | 10.8 | |

Consumer Staples | | 9.8 | |

Industrials | | 9.8 | |

Consumer Discretionary | | 8.6 | |

Utilities | | 3.2 | |

Materials | | 3.2 | |

Telecommunication Services | | 2.6 | |

Short-Term Investment | | 9.1 | |

4

Schroder U.S. Opportunities Fund

MANAGEMENT DISCUSSION AND ANALYSIS (As of May 31, 2012)

Performance

In the six months ended April 30, 2012, the Schroder U.S. Opportunities Fund (the “Fund”) rose 9.55% (Investor Shares) and 9.44% (Advisor Shares) compared to the Russell 2000 Index (the “Index”), a broad-based basket of stocks with characteristics similar to the Fund’s portfolio, which rose 11.02%.

Market Background

The six month period had divergent sub-periods which could be characterized as “risk on/risk off”. The period began rather quietly (i.e., “risk off”) as returns for November and December were both close to flat. Once the calendar turned, the market rose sharply for the first three months of the year (“risk on”) with a return for the Index of 12.44%. Optimism about the US economy abounded until April, when concerns rose about the slow pace of recovery in the jobs market in tandem with renewed worrisome headlines from Europe. As a result, the market returned to a “risk off” posture and began to pull back in April -1.54%. This has been typical of the overall equity market for some time now, as macroeconomic news has played a powerful role in setting market tone and direction.

Portfolio Review

The Fund underperformed the Index during the six months ending April 30, 2012. The underperformance can be analyzed in two ways: a) market factors and b) sector and stock positions.

From the viewpoint of market factors, several factors hurt the Fund’s portfolio. Over the six-month reporting period, higher beta stocks outperformed lower beta issues. Our investment style leads us to overweight the lower beta segments of the Index and underweight high beta. Interestingly, capitalization was much less of a factor than it has been in some other periods. There was no clear pattern of returns across the capitalization deciles.

From a sector/stock perspective, the Fund suffered from poor stock selection in financials. Additionally, the Fund was hurt by its underweight of the sector (which is normal given our disinclination to invest in Real Estate Investment Trusts or REITs) as financials were one of the strongest performing sectors during this period. In fact, the underweight in REITs was a key part of the Fund’s performance lag as this sector outperformed the Index by over 525 basis points. The Fund’s underweight in banks also detracted as this sector outperformed the Index by over 650 basis points. At the stock level, a holding in Cash America International, a specialty finance company, detracted from relative returns. The company operates payday loan and pawnshop businesses, and higher than expected expenses hurt the stock. The other main source of performance lag was the Fund’s cash holding, which averaged almost 9% over the six months. While cash helped in April, it certainly detracted during the strong months of January through March. The Fund also underperformed in the energy sector with SM Energy its largest detractor. The company is an oil and gas exploration and production company, and the low price of natural gas hurt their overall earnings.

On the positive side, the Fund saw significant value from stocks in the technology (AboveNet), materials and processing (Cabot) and healthcare (Cooper) sectors. AboveNet announced that they were being acquired by a private company (Zayo Group); Cabot saw good demand for their products (particularly carbon black used in tires) and expanding margins; and Cooper benefitted from growing demand for contact lens and an approval of a new lens designed for individuals with astigmatism.

Outlook

We have expressed concerns over the past year about excessive optimism from Wall Street on earnings forecasts for companies in our space. While analysts have slowly lowered their 2012 earnings estimates, we continue to feel that the Street is overly optimistic about the pace of the recovery. Additionally, we worry that the artificially low interest rates, which are a result of current Federal Reserve policy, are having an impact on valuations. The environment as we see it is now driven by low rates (which artificially lower valuations) and too-high expectations for earnings. This creates a difficult market for stock pickers looking for under-valued and under-appreciated companies. On the economic forefront, we believe that the US is in the midst of a long, slow recovery; we are not in the “double dip” recession camp. We also see signs that the housing market is beginning to recover, although there still remains significant unsold inventory which needs to clear the market. We are concerned about slowdowns overseas, specifically in China and Germany, which is the driver of the European economy. The sovereign debt problems plaguing what some refer to as ‘peripheral Europe’ remain a significant overhang to markets globally.

5

PERFORMANCE INFORMATION

| | One Year Ended

April 30, 2012 | | Five Years Ended

April 30, 2012 (a) | | Ten Years Ended

April 30, 2012 (a) | |

Schroder U.S. Opportunities Fund (b) (c) — | | | | | | | |

Investor Shares | | (4.36 | )% | 3.32 | % | 8.28 | % |

Advisor Shares | | (4.60 | )% | 3.07 | % | 8.02 | %(d) |

Russell 2000 Index | | (4.25 | )% | 1.45 | % | 6.19 | % |

(a) Average annual total return.

(b) Effective May 1, 2006, the combined advisory and administrative fees of the Fund increased to 1.00% per annum. If the Fund had paid such higher fees during prior periods, the returns of the Fund would have been lower.

(c) The portfolio manager primarily responsible for making investment decisions for the Fund assumed this responsibility effective January 2, 2003. The performance results for periods prior to January 2, 2003 were achieved by the Fund under a different portfolio manager.

(d) The Advisor Shares commenced operations on May 15, 2006. The performance information provided in the above table for periods prior to May 15, 2006 reflects the performance of the Investor Shares of the Fund, adjusted to reflect the distribution fees paid by Advisor Shares.

“Total Return” is calculated including reinvestment of all dividends and distributions. Results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. Results represent past performance and do not indicate future results. The value of an investment in the Fund and the return on investment both will fluctuate and redemption proceeds may be higher or lower than an investor’s original cost.

Top 5 Holdings

Security* | | % of Investments | |

| | | |

NorthWestern | | 1.4 | % |

Brown & Brown | | 1.4 | |

Waste Connections | | 1.4 | |

Alterra Capital Holdings | | 1.3 | |

Cleco | | 1.3 | |

* Excludes Short-Term Investment.

Sector Allocation

Sector | | % of Investments | |

| | | |

Consumer Discretionary | | 18.1 | % |

Financial Services | | 15.8 | |

Producer Durables | | 14.8 | |

Technology | | 11.4 | |

Healthcare | | 10.5 | |

Materials & Processing | | 7.8 | |

Other Energy | | 6.0 | |

Utilities | | 4.6 | |

Consumer Staples | | 0.9 | |

Short-Term Investment | | 10.1 | |

6

Schroder U.S. Small and Mid Cap Opportunities Fund

MANAGEMENT DISCUSSION AND ANALYSIS (As of May 31, 2012)

Performance

In the six months ended April 30, 2012, the Schroder U.S. Small and Mid Cap Opportunities Fund (the “Fund”) rose 10.69% (Investor Shares) and 10.56% (Advisor Shares) compared to the Russell 2500 Index (the “Index”), a broad-based basket of stocks with characteristics similar to the Fund’s portfolio, which rose 12.03%.

Market Background

The six month period had divergent sub-periods which could be characterized as “risk on/risk off”. The period began rather quietly (i.e., “risk off”) as returns for November and December were both close to flat. Once the calendar turned, the market rose sharply for the first three months of the year (“risk on”) with the Russell 2500 returning 12.99%. Optimism about the US economy abounded until April, when concerns rose about the slow pace of recovery in the jobs market in tandem with renewed worrisome headlines from Europe. As a result, the market returned to a “risk off” posture and began to pull back in April -0.73%. This has been typical of the overall equity market for some time now, as macroeconomic news has played a powerful role in setting market tone and direction.

Portfolio Review

From a market factor point of view, beta was a driver of returns during this period and capitalization was much less so. During the flat months of November and December, the lower beta quintiles outperformed high beta. That changed in January when investors returned from their year-end holidays in a decidedly “risk on” mood. Higher beta stocks led in January and February and began to fade in March and April. As indicated above, there was no clear pattern to capitalization returns over the six-month period, with the 7th decile being the weakest and the 6th and the 9th being the strongest.

From an asset allocation viewpoint, the Fund’s biggest detractor was cash, which averaged 9.9% during the six-month reporting period. Clearly in the “risk off” months, cash was not a detractor, but strong equity returns during the “risk on” months handicapped performance. Two other allocation positions are noteworthy: the Fund’s overweight in technology detracted modestly as the sector lagged and the underweight in financials hurt as financials were the second strongest sector for the six-month reporting period.

Within the sectors, the Fund had negative contributions to relative return from stock selection on producer durables, healthcare and utilities. In the producer durables group, the Fund’s biggest detractors were Waste Connections and Republic Services. Both companies are in the trash hauling business and are encountering a deterioration in pricing stability across the industry. A stock that detracted in healthcare was CareFusion, which was hurt by disappointing margins and pricing pressure. In the telecommunication services sector, the Fund’s major detractor was NII Holdings, a telecommunications company with wireless business in Latin America. Execution difficulties in their 3G network and competition dragged down the stock.

We did add value through stock selection overall, driven by the Fund’s holdings in technology, materials and processing and consumer staples. AboveNet was a big contributor in the technology area as they announced an agreement to be acquired by a private company (Zayo Group). The materials and processing sector returns were led by Airgas and Cabot. Airgas has had a series of strong earnings reports; and Cabot saw good demand for their products (particularly carbon black used in tires) and expanding margins. Consumer staples sector returns were led by Viterra, as the Canadian firm reached higher export levels of grain from its South Australian ports.

Outlook

We have expressed concerns over the past year about over-optimism from Wall Street on earnings forecasts for companies in our space. While analysts have slowly lowered 2012 earnings estimates, we continue to feel that the Street is overly optimistic about the pace of the recovery. Additionally we worry that the artificially low interest rates which are a result of current Federal Reserve policy are having an impact on valuations. The environment as we see it is now driven by low rates (which artificially lower valuations) and too-high expectations for earnings. This creates a difficult market for stock pickers looking for under-valued and under-appreciated companies. On the economic forefront, we believe that the US is in the midst of a long, slow recovery; we are not in the “double dip” recession camp. We also see signs that the housing market is beginning to recover, although there still remains significant unsold inventory which needs to clear the market. We are concerned about slowdowns overseas, specifically in China and Germany, which is the driver of the European economy. The sovereign debt problems plaguing what some refer to as ‘peripheral Europe’ remain a significant overhang to markets globally.

7

PERFORMANCE INFORMATION

| | | | | | Annualized | |

| | One Year Ended | | Five Years Ended | | Since | |

| | April 30, 2012 | | April 30, 2012 (a) | | Inception (b) | |

Schroder U.S. Small and Mid Cap Opportunities Fund — | | | | | | | |

Investor Shares | | (1.95 | )% | 4.22 | % | 5.66 | % |

Advisor Shares | | (2.15 | )% | 3.93 | % | 5.39 | % |

Russell 2500 Index | | (2.23 | )% | 2.35 | % | 3.69 | % |

(a) Average annual total return.

(b) From commencement of fund operations on March 31, 2006.

“Total Return” shown above is calculated including reinvestment of all dividends and distributions. Results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. Results represent past performance and do not indicate future results. The value of an investment in the Fund and the return on investment both will fluctuate and redemption proceeds may be higher or lower than an investor’s original cost.

Top 5 Holdings

Security* | | % of Investments | |

| | | |

Crown Holdings | | 2.1 | % |

Amdocs | | 2.0 | |

Energen | | 1.8 | |

PartnerRe | | 1.7 | |

Waste Connections | | 1.6 | |

* Excludes Short-Term Investment.

Sector Allocation

Sector | | % of Investments | |

| | | |

Consumer Discretionary | | 15.4 | % |

Financial Services | | 14.9 | |

Technology | | 14.3 | |

Healthcare | | 11.4 | |

Materials & Processing | | 9.8 | |

Producer Durables | | 7.7 | |

Utilities | | 6.5 | |

Other Energy | | 4.0 | |

Consumer Staples | | 2.1 | |

Auto & Transportation | | 1.7 | |

Telecommunication Services | | 0.5 | |

Short-Term Investment | | 11.7 | |

8

Schroder Emerging Market Equity Fund

MANAGEMENT DISCUSSION AND ANALYSIS (As of May 31, 2012)

Performance

In the six months ended April 30, 2012, the Schroder Emerging Market Equity Fund (the “Fund”) gained 7.60% (Investor Shares) and 7.56% (Advisor Shares), compared to the Morgan Stanley Capital International (“MSCI”) Emerging Markets Index (the “Index”), a broad-based basket of international stocks, which rose 3.93% during the same period.

Market Background

Global equity markets rose during the six-month reporting period, reflecting a strong improvement in global risk appetite in January and February 2012. The rally at the beginning of 2012 was supported by some encouraging US macro data releases and the avoidance of an immediate Greek sovereign debt default as the European Union (EU) and the International Monetary Fund (IMF) approved a second bail out for the country. The European Central Bank’s (ECB’s) Long Term Refinancing Operation (LTRO) also boosted sentiment in early 2012 as it helped to ease liquidity pressures faced by the European banking sector. However, global equity markets returned to worry mode in mid-March, reflecting some disappointing data releases in the eurozone and Asia and renewed concerns of a potential hard economic landing for China. The MSCI World Index produced a positive return over the period and outperformed the MSCI Emerging Markets Index, driven by strong returns from US equities.

The EMEA (Europe, Middle East and Africa) emerging markets outperformed broader emerging markets over the period, benefiting from strength in a number of the local currencies. Egypt outperformed its emerging market peers, aided by a very strong rally in January and February following the conclusion of largely peaceful parliamentary elections. However, concerns over the currency provided a headwind for the market, with Egypt’s foreign reserves reaching low levels in March. South Africa outperformed, aided by strength in some of the consumer-related names and rand appreciation versus the US dollar. However, a number of mining-related names performed poorly as gold prices weakened. Hungary outperformed, benefiting from the increased risk appetite environment (‘risk on’) in January and February and hopes that the government should be able to reach agreement with the IMF on the terms of a standby facility. Turkey outperformed, as market sentiment was boosted by the ‘risk on’ environment in early 2012, which helped to ease pressure on the currency. Turkish current account deficits narrowed in November and continued to moderate since then, having reached record highs earlier in 2011. However, inflation concerns provided a headwind for the Turkish market as the local Consumer Price Index (CPI) reached 10.6% year on year in January. Russia underperformed, largely reflecting a heavy sell-off in December following domestic unrest amid allegations of electoral fraud in parliamentary elections. However, market sentiment was supported by strength in Brent crude oil prices and a rally in the ruble. The Czech Republic underperformed, reflecting the defensive nature of the market and a weak growth environment. Poland underperformed, reflecting the market’s relatively low beta in an emerging markets context and stubbornly high inflation, which resulted in a hawkish policy stance at the central bank. Ongoing privatizations and the associated supply of new shares also provided a headwind for the Polish market.

Asian emerging markets performed broadly in line with wider emerging markets. Thailand outperformed, benefiting from strength in a number of the energy and banking names, and expectations that the impact of last year’s heavy flooding should be short-lived. On the policy front, the Thai central bank cut interest rates to 3.0% in January to support growth. The Philippines outperformed, aided by policy easing from its central bank. Inflation concerns also eased as the consumer price index fell to 2.6% year on year in March from 4.7% year on year in November. Malaysia outperformed, benefiting from its perceived lack of sensitivity to the problems in the eurozone and stronger-than-expected fourth quarter GDP growth of 5.2% year on year. China outperformed; fears of a hard landing eased as fourth quarter GDP growth increased to 8.9% year on year, while the central bank cut reserve requirement ratios in order to release liquidity to the banking system. South Korea outperformed, with some large-cap electronics names performing very strongly following market share gains. Interest rates remained on hold at 3.25%, as widely expected. Taiwan underperformed, reflecting some political uncertainty ahead of the parliamentary and presidential elections in January, while in April sentiment was hit by news that the government is considering the re-imposition of capital gains tax on some local share transactions. Indonesia underperformed, having outperformed strongly in 2011. Turning to policy, the central bank surprised the market by cutting interest rates to 5.75% in early February, despite the inflation risks posed by rising fuel prices. The growth environment also remained strong, with GDP up 6.5% year on year in the fourth quarter. India underperformed, reflecting weakness in the rupee while inflation, fiscal and political concerns also provided a headwind for the market. On the policy front, the central bank cut interest rates in April but indicated that the scope for further easing was likely to be very limited.

Latin American emerging markets underperformed their emerging market peers over the reporting period due to weakness in the Brazilian Real. However, Colombia outperformed, aided by strength in the peso. At the stock level, energy-related names ranked among the best performers as Brent crude oil prices rose. On the policy front Colombia’s central bank continued to raise interest rates, as widely expected, with the overnight rate reaching 5.25% in late February. Peru outperformed, aided by strength in some financial stocks. However, some mining names struggled to make headway following protests against high-profile projects. Mexico outperformed, benefiting from some encouraging US macroeconomic data releases and the market’s perceived lack of sensitivity to the fiscal problems in the eurozone. Hopes of monetary policy easing also supported sentiment, although interest rates remained on hold at 4.5%. Chile outperformed, aided by a rally in copper prices and strength in the peso. On the policy front, the central bank reduced interest rates to 5.0% in early January. Brazil underperformed due to weakness in the Real as the carry trade reversed while the central

9

bank cut interest rates aggressively (from 11.5% at the start of the period to 9% in April). In other developments, the government introduced further policy measures to deter short-term speculative inflows of foreign capital.

Portfolio Review

Fund performance was ahead of the Index for both Investor Shares and Advisor Shares over the six-month period. Emerging markets rose during the six months to end April 2012, although returns were behind those of developed markets. Both country allocation and stock selection added value over the period.

In terms of our country positioning, the main positive impacts came from our overweight position in Thailand, which outperformed, and the underweight position in India, which underperformed. Recent data releases from Thailand continue to indicate that the economy is recovering quickly from last year’s flooding and consequently the central bank has been upgrading its growth forecasts for 2012. Indian equities performed poorly due to a combination of currency, inflation and fiscal deficit concerns, while strong oil prices provided a further headwind due to India’s reliance on energy imports. More recently, March’s state elections saw the governing Congress Party perform poorly, reducing the likelihood of meaningful corporate reform. The positive impact of our Thai overweight and Indian underweight more than offset the unfavourable impact of our underweight positions in Mexico and South Africa. Mexico outperformed due to easing inflation concerns, hopes of domestic policy easing and the better tone of US economic data at the start of 2012, while the South African market benefited from strong performance from some of the consumer and banking sector names in the local index and its perceived lack of sensitivity to the debt and fiscal crisis in the eurozone.

Stock selection was favourable over the period and provided the main driver of the Fund’s outperformance versus the benchmark. Selection was particularly strong in Korea (overweight Samsung Electronics, overweight Hyundai Motor), Brazil (overweight Cemig, overweight Ultrapar Participacoes), Taiwan (overweight Taiwan Semiconductor Manufacturing), Thailand (overweight CP ALL), Indonesia (overweight Semen Gresik Persero) and China (overweight Tencent Holdings). These positive stock selection effects more than offset the negative impact of our selection decisions in Egypt (overweight Centamin) and Poland (overweight KGHM Polska Miedz earlier in the period).

Outlook

Global stock markets continued to consolidate and fall recently following renewed concerns over the sustainability of the recovery in the developed world. The deterioration of the situation in the eurozone has resulted in elevated political uncertainty in several countries and the US has offered little respite to investors with growth momentum showing signs of decelerating. The more positive medium-to longer-term outlook for global emerging markets (GEMs) continues to be tempered in the short term by challenges stemming chiefly from the developed world.

The positive effects of LTRO on investor sentiment have dissipated and a combination of austerity fatigue and disappointing data releases has resurrected sovereign debt concerns in the eurozone. The result has been political upheaval in many countries. Greek elections have been inconclusive and threatened to disqualify Greece for additional bailout funding, although the immediate risks of a default have been somewhat diminished by additional support from the European Financial Stability Facility (EFSF). Elevated political uncertainty has not been confined to the eurozone periphery. Francois Hollande became the first socialist President in France for 17 years; his pro-growth campaign has raised question marks over policy coordination with Angela Merkel in Germany, who continues to maintain a pro-austerity stance. The Dutch similarly succumbed to popular anti-austerity sentiment and the government collapsed. The vulnerable position of Spain continues to be apparent with 10-year sovereign bond yields rising to around 6% and news that the economy has fallen back into recession. Recent data releases from the US have been largely disappointing, although it remains subject to debate whether the recovery is sufficiently fragile to warrant further quantitative easing. The Schroders Economics team’s growth forecasts remain unchanged with global, US and eurozone GDP growth over 2012 of 2.3%, 2.1% and -0.8% respectively.

We see signs that the positive market impact of ‘sticking plasters’ or quantitative easing measures in the developed world look to be diminishing and, we believe, until a coordinated, credible policy response is forthcoming, the short-term outlook for GEMs remains vulnerable to swings in investor risk sentiment. Robust economic fundamentals continue to support a two-speed world with consensus emerging economic GDP growth estimated to be 5.1% over 2012. Valuations continue to look attractive, with GEMs trading on a price-to-earnings ratio of 10 times, and forecast earnings growth is 13%. With commodity price and inflationary pressure typically moderating, several GEMs continue to pursue expansionary monetary policy which historically has boosted stock market returns. Concerns over a ‘hard landing’ in China have not abated with first quarter GDP slowing to 8.1% year on year, although more recent data releases point to some stabilization in growth. However, while the outlook for GEMs is supported by robust growth and attractive valuation levels, GEMs will likely continue to be hampered in the near term by negative sentiment from the developed world.

10

PERFORMANCE INFORMATION

| | | | | | Annualized | |

| | One Year Ended | | Five Years Ended | | Since | |

| | April 30, 2012 | | April 30, 2012 (a) | | Inception (b) | |

| | | | | | | |

Schroder Emerging Market Equity Fund — | | | | | | | |

Investor Shares | | (11.19 | )% | 4.39 | % | 7.43 | % |

Advisor Shares | | (11.36 | )% | 4.21 | % | 7.22 | % |

MSCI Emerging Markets Index | | (12.61 | )% | 3.48 | % | 6.86 | % |

(a) Average annual total return.

(b) From commencement of fund operations on March 31, 2006.

“Total Return” shown above is calculated including reinvestment of all dividends and distributions. Results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for certain periods reflect fee waivers and/or reimbursements in effect for that period absent fee waivers and reimbursements, performance would have been lower. Results represent past performance and do not indicate future results. The value of an investment in the Fund and the return on investment both will fluctuate and redemption proceeds may be higher or lower than an investor’s original cost.

Top 5 Holdings

Security* | | % of Investments | |

| | | |

Samsung Electronics | | 6.4 | % |

Hyundai Motor | | 3.4 | |

China Mobile | | 3.1 | |

Gazprom ADR | | 2.7 | |

Taiwan Semiconductor Manufacturing | | 2.5 | |

* Excludes Short-Term Investment.

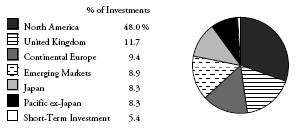

Geographic Allocation

11

Schroder International Alpha Fund

MANAGEMENT DISCUSSION AND ANALYSIS (As of May 31, 2012)

Performance

In the six months ended April 30, 2012, the Schroder International Alpha Fund (the “Fund”) gained 6.23% (Investor Shares) and 6.00% (Advisor Shares) compared to the Morgan Stanley Capital International EAFE Index (the “Index”), a broad-based basket of international stocks, which rose 2.44%.

Market Background

Markets regained their risk appetite over much of the last six months, however, this appetite stalled in April. Events in the eurozone have dominated throughout the period. While sentiment was momentarily improved by events such as the European Union (EU) summit in December and a second bailout for Greece, this did not last long, as investors became skeptical. Doubt arose over the efficacy of the summit and fears resurfaced that Greece would default. A resurgence of fragile data in the “post- Long-Term Refinancing Operations (LTRO)” environment, and uncertain outcomes in French and Greek elections, put pressure on investors to take profits in stocks after the strong rally that started in November last year. The successful presidential bid by Mr. Hollande raised fears that progress in Europe may be jeopardized Focus turned to Spain in the first quarter of 2012 as the country re-entered recession and the risk of contagion seemed more likely. At the end of the six-month period, the argument of “austerity versus growth” was at the forefront of the European discussion. Jitters about the impact of rising oil price surfaced sporadically throughout the beginning of the year, but failed to seriously hurt the positive rally seen up until April. Emerging markets mostly had a strong run as data from China generally pointed to the avoidance of a hard landing. Moderate but steadily improving US data towards the end of the period remained a bright spot in the developed world and although we think a short-term set back in momentum is still possible, markets remain cautiously optimistic.

Portfolio Review

By region, the main drivers of outperformance were Continental Europe and the UK, while Pacific ex Japan was the only significant detractor. In Continental Europe, the Fund’s underweight position to telecoms drove performance. The region’s industrials (GEA Group and Safran) also contributed strongly. The top performing stock in Continental Europe was Anheuser-Busch InBev. The world’s largest brewer reported strong results throughout the period with strong fourth quarter revenue growth, continued margin expansion and a 4.6% growth in annual revenue. Favorable weather conditions and the roll out of its Bud Light Platinum product helped performance throughout March.

In the UK, energy led relative returns. AMEC shares have had a strong run, benefitting from February’s surge in oil prices on the back of renewed hopes for global growth and political tension in the Middle East. AMEC raised its dividend, launched a £400 million share buyback scheme and announced that it expects to deliver double-digit underlying revenue growth this year.

Pacific ex-Japan materials weighed heavily on performance. Mining stocks have had a particularly tough six months, with production affected by adverse weather conditions in the region. Both stocks (Newcrest Mining, Atlas Iron) in the region’s materials underperformed. Newcrest Mining announced shortfalls in production over the period due to heavy rainfall at key sites. The company also suffered from weakness in the gold price towards the end of the first quarter this year. We believe April’s poor production numbers will be the last major production disappointment and continue to see good upside.

From the Fund’s total portfolio sector perspective, financials (Sberbank, Kasikornbank) and information technology (Samsung Electronics) contributed the most to performance. Sberbank has continued to do well since rebounding on the back of returning risk appetite in October. Annual net income was up 75% in January compared to the equivalent profit the year before. Samsung Electronics has enjoyed continued strong performance thanks to its impressive smartphone sales, becoming the largest seller of smartphones in the world. In April, the company’s earnings surprised on the upside, driven by strong handset sales and reduced seasonal marketing costs.

Outlook

The new-year rally ended in April as focus returned to Europe’s sovereign woes. Peripheral European countries’ bond yields have risen again and the regional debate on austerity versus growth has come under increasing pressure. Spain is a center of attention, with yields on its 10-year bonds once again breaching 6% — the point generally seen as the threshold for what is sustainable. While the Spanish government is stable and has the ability to reform, the market doubts the underlying political support for austerity measures. Indeed, with Spain officially back in recession and civil unrest brewing on the streets, the difficulty of fiscal tightening is starkly illustrated.

The “austerity versus growth” debate is at the heart of Europe at this point. In Holland, the prime minister offered to resign over disagreements with coalition partners on the austerity mandate. In France, the win for Mr. Hollande, who wants to amend the European fiscal pact to incorporate higher growth bias, could undermine the country’s drive for austerity and upset the political progress made in Europe in the past six months. His plans for spending increases of 20 billion euros and tax increases of 44.7 billion euros contrast with the tone for addressing structural issues and imbalances in the region via sharp austerity programs. The French parliamentary elections in June lead us to believe that he will not tone down his message until after June, in an effort to continue to win support from left wing parties. On-going elections in Greece, where public opposition to spending cuts is fierce, and a political stalemate are another source of volatility. Developments could lead to the country breaching the terms of its bailout and an exit from

12

the eurozone is possible. If this were to happen, we believe containing the fallout is now more manageable than if such an event had occurred six months ago but the risk of contagion remains real.

Previously, the two waves of European Central Bank LTRO funding have given Europe breathing space but they do not solve the underlying problems— as recent developments have shown. We believe extensive restructuring is needed which will be a very challenging task. We therefore see potential for further volatility in the short-term, although we believe the worst of outcomes for the region now looks unlikely. Ultimately, we believe the region will need to move towards closer fiscal union in order to truly address its problems.

Although China GDP for the first quarter of 2012 disappointed some in the market at 8.1%, we believe this level of growth is healthy and its slowdown in growth is coming to an end. Economic data from China has broadly been encouraging and continues to support our view that the world’s second largest economy is on track for a soft landing. Official Chinese manufacturing PMI rose to 53.3 and industrial production, retail sales, new loans and export growth also picked up in March. The growth rate remains healthy and efforts to continue to promote domestic growth and selected capital spending while maintaining a cautious approach to the property sector are still on target. As expected in a political transitional year some “last minute” political positioning is taking place as evidenced by the Bo Xi Lai scandal.

We are cognizant of the risk of “mini cycles” — short-term deviations from long-term global trends which may impact economic growth. Rising oil prices currently represent one of the biggest sources of risk. The impact of sanctions and the risk of a military strike against Iran’s nuclear facilities might support higher prices, although fear of a slowdown in China might counterbalance this trend to some extent.

Given the improvement that we are seeing in parts of the US economy and our belief that growth in China will be stable to up during the rest of the year, in our view the two largest world economies will help support growth globally. The current “air pocket” and potential for volatility in the near term we feel should therefore be used to accumulate equities globally as they come under short-term pressure linked to fear and lack of political visibility.

We continue to pursue reasonably valued growth in companies which, irrespective of these short-term market uncertainties, are benefiting from much longer-term global trends. With a good portfolio balance between growth defensives and more cyclical industries, the Fund’s trading activity is likely to focus on stock-specific situations where we feel there is expectation for growth and valuation upside.

13

PERFORMANCE INFORMATION

| | One Year Ended

April 30, 2012 | | Five Years Ended

April 30, 2012 (a) | | Ten Years Ended

April 30, 2012 (a) | |

Schroder International Alpha Fund (b) — | | | | | | | |

Investor Shares | | (14.35 | )% | (2.10 | )% | 5.54 | % |

Advisor Shares | | (14.58 | )% | (2.35 | )% | 5.29 | %(c) |

MSCI EAFE Index | | (12.82 | )% | (4.72 | )% | 5.42 | % |

(a) Average annual total return.

(b) Effective March 21, 2012, the advisory fee of the Fund decreased to 0.80% per annum. If the Fund had paid such lower fees during prior periods, the returns of the Fund would have been higher.

(c) The Advisor Shares commenced operations on May 15, 2006. The performance information provided in the above table for periods prior to May 15, 2006 reflects the performance of the Investor Shares of the Fund, adjusted to reflect the distribution fees paid by Advisor Shares.

“Total Return” shown above is calculated including reinvestment of all dividends and distributions. Results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. Results represent past performance and do not indicate future results. The value of an investment in the Fund and the return on investment both will fluctuate and redemption proceeds may be higher or lower than an investor’s original cost.

Top 5 Holdings

Security* | | % of Investments | |

| | | |

Nestle | | 2.9 | % |

Roche Holding | | 2.8 | |

HSBC Holdings | | 2.4 | |

Safran | | 2.3 | |

Anheuser-Busch InBev | | 2.2 | |

* Excludes Short-Term Investment.

Geographic Allocation

14

Schroder International Multi-Cap Value Fund

MANAGEMENT DISCUSSION AND ANALYSIS (As of May 31, 2012)

Performance

In the six months ended April 30, 2012, the Schroder International Multi-Cap Value Fund (the “Fund”) gained 3.98% (Investor Shares) and 4.02% (Advisor Shares) compared to the Morgan Stanley Capital International EAFE Index (the “Index”), a broad-based basket of international stocks, which rose 2.44% during this same period.

Market Background

International equities rallied strongly towards the end of 2011 driven by economically sensitive industries as expectations for global growth continued to improve following a mid-year pause. The late flurry capped a year characterised more by marked sharp swings in sentiment as investors assessed the significance of economic data and the sovereign debt crises in Europe. The dominance of top-down themes was manifested in the relatively high level of correlation between stocks and the often significant rotation in the performance of cyclical and defensive sectors depending upon market direction.

By the end of the year, however, cyclical industries were in the ascendency, driven by resources and industrials in particular, while more defensive areas of the market, such as utilities and healthcare, were the clear laggards. This was driven by a positive reception to the U.S. Federal Reserve Bank’s announcement of a further round of Quantitative Easing (dubbed “QE2”) prior to the beginning of the reporting period as well as an unexpected fiscal stimulus and generally supportive economic data. Weakness in the U.S. dollar on the back of QE2 helped to buoy the U.S. equity market, while renewed concerns about European sovereign debt weighed on European stocks, banks in particular.

International equity markets entered 2012 on an equally positive note, buoyed by expectations of strengthening economic growth, ample liquidity and receding concerns about sovereign debt risk in Europe. The six-month period as a whole was characterised by some reasonably significant swings in investor focus, with higher risk, deep value stocks — predominantly low-quality European banks — performing particularly well in early January, only to give much of this performance back in March. This echoed a more general preference for market sensitivity (beta) at the beginning of the year, which was replaced by a focus on higher-quality stocks towards the end of the period.

Macro-economic events strongly influenced sentiment during the period, when investors were forced to confront a raft of bad news. Continuing political tensions across the Middle East led to persistently high oil prices. Meanwhile, the threat of rising global inflation — fuelled by rising food and energy prices — resulted in expectations of earlier-than-anticipated tightening of monetary policy in the US and Europe (a process which is already underway in parts of Asia). This was borne out in Europe, after the European Central Bank (ECB) chose to raise interest rates by a quarter of a percentage point, to 1.25%, in April.

Portfolio Review

The Fund ended the period ahead of the market. Performance was chiefly driven by positive stock selection in the energy and materials sectors, as well as among defensive names in the utilities, consumer staples and healthcare sectors. The Fund’s holdings within the telecoms and industrials sectors detracted from relative gains over the period.

Despite ongoing turmoil in Japan, regional stock selection was, by far, the leading contributor to the Fund’s performance. Avoiding underperforming Japanese utilities stocks (which continue to underperform in the wake of the Tohoku earthquake) boosted relative gains. Elsewhere, the Fund’s emerging markets allocation added value, despite weaker performance by emerging Asian stocks.

Outlook

Looking forward, we expect the Fund’s largest sector overweight to remain in telecoms, where we continue to be attracted to their high dividend yields and relative stability. Within the cyclical parts of the market, we expect technology stocks provide more value compared to consumer discretionary and industrials.

In the short term, we remain broadly neutral with respect to the resources sector as we expect continued strong performance to be matched by perceived improvements in fundamentals as demonstrated by strong earnings during end of this reporting season.

Within financials, we continue to retain a preference for insurers over banks. Given our expectations of continued high level of intrasector volatility within financials globally, we still believe that this sector will provide plenty of opportunities to benefit from stock selection during 2012.

The Fund’s regional allocations will remain broadly unchanged, but we expect to increase the Fund’s exposure to Japan — with valuations looking increasingly attractive. Within emerging markets, we expect to increase our allocation to Asian economies.

15

PERFORMANCE INFORMATION

| | | | | | Annualized | |

| | One Year Ended | | Five Years Ended | | Since | |

| | April 30, 2012 | | April 30, 2012 (a) | | Inception (b) | |

Schroder International Multi-Cap Value Fund (c) — | | | | | | | |

Investor Shares | | (12.22 | )% | (1.28 | )% | 3.12 | % |

Advisor Shares | | (12.30 | )% | (1.47 | )% | 2.93 | % |

MSCI EAFE Index | | (12.82 | )% | (4.72 | )% | (1.02 | )% |

(a) Average annual total return.

(b) From commencement of fund operations on August 30, 2006.

(c) Effective March 21, 2012, the advisory fee of the Fund decreased to 0.80% per annum. If the Fund had paid such lower fees during prior periods, the returns would have been higher.

“Total Return” shown above is calculated including reinvestment of all dividends and distributions. Results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for certain periods reflect fee waivers and/or reimbursements in effect for that period; absent fee waivers and reimbursements, performance would have been lower. Results represent past performance and do not indicate future results. The value of an investment in the Fund and the return on investment both will fluctuate and redemption proceeds may be higher or lower than an investor’s original cost.

Top 5 Holdings

Security* | | % of Investments | |

| | | |

Sanofi | | 0.8 | % |

AstraZeneca | | 0.8 | |

Roche Holding | | 0.7 | |

GlaxoSmithKline | | 0.7 | |

Reckitt Benckiser Group | | 0.7 | |

* Excludes Short-Term Investment.

Geographic Allocation

16

Schroder Global Quality Fund

MANAGEMENT DISCUSSION AND ANALYSIS (As of May 31, 2012)

Performance

For the six months ended April 30, 2012, the Schroder Global Quality Fund (the “Fund”) returned 7.93% compared to the Morgan Stanley Capital International World Index (the “Index”), a broad-based basket of global stocks, which returned 7.54% during this same period.

Market Background

Following a particularly volatile third quarter in 2011 — driven by escalating concerns about the eurozone debt crisis and fears of a double-dip recession — global equity markets were calmer in the final months of 2011.

As we entered the New Year, optimism prevailed, with investors encouraged by the European Central Bank’s (ECB’s) provision of liquidity to the European banking system via two long-term funding operations, along with more supportive US economic data. However, confidence deteriorated again in April, and equity markets lost ground as risk appetite waned. Concerns about Spain’s lack of progress in reducing its budget deficit provided a reminder that Europe’s sovereign debt issues are far from resolved.

Spain’s woes dominated headlines — officially re-entering recession, suffering an S&P downgrade, and seeing 10-year government bonds yields breach the all-important 6% threshold — while uncertainty surrounding the French presidential elections did little to improve sentiment. Despite losing steam towards the end of the reporting period, positive sentiment drove equity market gains overall.

Sector performance was mixed over the period; information technology was the standout performer, while defensive healthcare and consumer staples stocks benefited from risk aversion at the beginning and end of the period. Bouts of optimism also supported more cyclical areas of the market including consumer discretionary and industrials. From a regional perspective, the UK, Asia Pacific and Japan led the gains while continued turmoil in Europe saw continental European stocks lose ground.

Portfolio Review

The Fund outperformed the wider market over the period. Strong stock selection across a broad range of sectors drove the relative gains. Leading contributions came from the Fund’s holdings in the financials, industrials and energy sectors.

Within the more defensive areas, the Fund’s holdings in utilities and consumer staples added value. Detractors included healthcare stocks, while not owning outperforming consumer discretionary names dragged on Fund performance. Information technology also impacted relative returns, largely due to the continued success of Apple.

Regionally, UK and Pacific ex Japan holdings contributed to Fund performance, while its exposure to emerging markets stocks also boosted returns. In addition, the Fund benefited from its underweight allocation to continental European stocks. The US was the weakest performer on a relative basis.

Within defensives, the largest sector overweight remains healthcare. After increasing exposure to consumer staples following underperformance in the first quarter of 2012, we are now trimming and taking profits in some of the stronger performing holdings in the Fund’s portfolio (Coca-Cola, Colgate-Palmolive and Philip Morris International).

The Fund remains overweight resources, which the market continues to de-rate on the back of perceived concerns about weaker demand and the potential impact on prices for companies in this sector.

Technology remains the favored ‘cyclical’ sector, where the Fund has exposure to both software and semi-conductors. Industrials remain an underweight and need to continue to grow into their ratings.

Within financials, the Fund retains a preference for US financials, including the investment banks, and also the higher quality UK financials (HSBC Holdings and Prudential).

Outlook

Within defensives, we expect the Fund to remain overweight healthcare, as we look to continue trimming consumer staples in the early part of the next reporting period as investors focus on the “lose less money” trade.

We expect the Fund to remain overweight resources stocks, which continue to de-rate on concerns about weaker demand and over- investment. Fertilizer stocks look attractive and should have different demand drivers to mining and oil companies as we move into the second half of 2012. In the short term, the Fund’s regional allocations should remain broadly unchanged: we expect that the Fund will continue to be underweight Continental Europe in order to increase positions in emerging markets, predominantly in Asia.

17

PERFORMANCE INFORMATION

| | | | Annualized | |

| | One Year Ended | | Since | |

| | April 30, 2012 | | Inception (a) | |

Schroder Global Quality Fund — | | | | | |

Institutional Class Shares | | (3.43 | )% | 5.97 | % |

MSCI World Index | | (4.63 | )% | 4.15 | % |

(a) From commencement of fund operations on November 9, 2010.

“Total Return” shown above is calculated including reinvestment of all dividends and distributions. Results do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Returns for the period reflect fee waivers and/or reimbursements in effect; absent fee waivers and reimbursements, performance would have been lower. Results represent past performance and do not indicate future results. The value of an investment in the Fund and the return on investment both will fluctuate and redemption proceeds may be higher or lower than an investor’s original cost.

Top 5 Holdings

Security* | | % of Investments | |

| | | |

AstraZeneca | | 0.7 | % |

Eli Lilly | | 0.7 | |

Unilever | | 0.7 | |

Apple | | 0.7 | |

Roche Holding | | 0.7 | |

* Excludes Short-Term Investment.

Geographic Allocation

18

Schroder Total Return Fixed Income Fund

MANAGEMENT DISCUSSION AND ANALYSIS (As of May 31, 2012)

Performance

During the six months ended April 30, 2012, the Schroder Total Return Fixed Income Fund (the “Fund”) returned 3.20% (Investor Shares) and 3.07% (Advisor Shares), compared to the Barclays Capital U.S. Aggregate Bond Index (the “Index”), a broad-based basket of U.S. debt securities, which rose 2.44%.

Market Background

The bond market registered a positive return over the six-month reporting period, overcoming the severe market volatility of third quarter 2011. Economic data surprised to the upside as consumer sentiment and spending were supported by better job creation, pushing the unemployment rate down to 8.2% and GDP to 2.2%. Moreover, the massive infusion of liquidity from the European Central Bank’s Long Term Repo Operation (LTRO) effectively removed the near term risk of bank funding difficulties in Europe, and provided increased demand for higher yielding European sovereign bonds. While uncertain fiscal policy clouded the optimism in the market, monetary policy in the US remained highly supportive. Despite some discussion of being flexible in the event of much stronger growth, short term rates remained close to zero. First quarter 2012 corporate earnings were also better than expected and proved to be a catalyst for investors to take on a slightly higher risk tolerance than late 2011. Overall, the combination of punitive yields on cash and the removal of near term economic and financial risks propelled equity and bond prices higher.

Treasury yields were little changed during the reporting period, with 10 year Treasuries declining only 0.20%, to 1.91%. After initially moving higher in the beginning of the six-month period, on the optimism of better prospects for the US, yields trended lower in April on the back of concerns about Greece. The persistent low level of interest rates reflected a combination of the Federal Reserve accommodation, higher oil prices not yet threatening inflation, and the Fed’s policy commitment anchoring the entire yield curve.

The 2.44% return for the Index during the reporting period was primarily due to the dramatic narrowing of bond spreads relative to US Treasury yields. Returns on investment grade corporate bonds were much higher than government bonds as investors were compensated for taking on more credit risk in the market. Within corporates, financials produced the best performance, followed by utility bonds then industrials. Lower rated bonds outperformed higher rated securities. The triple-B rated sector was the top performing credit quality tier, returning 4.56%, or more than 2% higher than comparable Treasury securities during this period. High yield corporate bonds did even better, returning 6.90%, with a similar pattern of the lowest quality tiers providing the best performance. Although corporate fundamentals remained strong, they are starting to show signs of peaking. Default risk remains benign and is expected to stay reasonably low over the next 12 months. Supply demand conditions remained firm, especially in high yield, as new issuances were easily absorbed by investors.

The securitized sectors also did well with agency residential mortgage-backed securities (MBS) returning 4.3% and the smaller commercial mortgage-backed securities (CMBS), sector returning 5.7%. Asset-backed securities (ABS) likewise outperformed Treasuries, with auto and credit card receivable securities providing added income versus cash alternatives.

Portfolio Review

The Fund outperformed the Index primarily due to the overweighting of corporate bonds, both investment grade and high yield, and MBS in lieu of US Treasury and agency securities. Credit exposure was concentrated in triple-B and double-B rated issuers, allowing the Fund to have a positive sensitivity to narrowing credit spreads. Fund strategy emphasized industrial securities, especially consumer cyclicals, basic industries and transportation securities. Duration strategy also positively contributed to performance.

Fund positioning followed the template put in place during the third quarter of 2011. Recognizing that regulatory changes and government intervention would keep markets volatile, we were cautious in our risk budgeting and flexible with sector rotation. We maintained a relatively low risk profile in the Fund while continuing to express our long term positive views for corporate and MBS based on our fundamental economic and credit research. The Fund began the period with a substantial overweight to investment grade corporate and high yield credit. This was gradually reduced on the back of good performance into March and our concerns about potential risk flares in Europe. In late March, the Fund again slightly increased the allocation to corporate credit. High yield exposure was reduced from 8% to 5%.

The Fund’s MBS allocation followed a similar trajectory, although the overweight was more modest than the corporate allocation. We preferred overweighting Ginnie Mae lower coupon MBS to minimize volatility from potential regulatory changes in government mortgage programs as well as possibly higher prepayment rates. Collateralized Mortgage Obligations and agency hybrid adjustable-rate mortgage (ARM) holdings also added to returns. The Fund also invested in a selection of Canadian covered bonds. These AAA rated securities provided high income and performed well as alternatives to low yielding cash investments. ABS and CMBS exposures were in line with the benchmark.

19

The Fund’s duration was longer than the Index until the very end of April. Despite low overall interest rates, Treasury yields and credit risk have had a very high and robust negative correlation with each other since mid-2011. Having a duration longer than the Index effectively acted as a partial hedge to dampen overall portfolio volatility. The long duration was further supported by the Fed’s articulation of extended zero-percent interest rate policy and inflation having peaked on a year-over-year basis.

Outlook

The similarities between this year, 2012, so far, and 2011 are notable. Both began with sizable narrowing of non-Treasury spreads that followed significant liquidity provisions (LTRO in Europe and quantitative easing (QE) by the Fed), better than expected economic data and an easing of investor concerns. Returns across all fixed income sectors have subsequently been fairly strong; with the best returns coming from those sectors that experienced the most volatility the prior year—lower quality investment grade and high yield corporates.

We believe the balance of the year and perhaps the early stages of 2013 are likely to remain volatile as investors continue to grapple with the fragile economic condition and potentially disruptive fiscal budget negotiations. Europe remains a long way from being settled and is another source of pronounced uncertainty. However, market positions do not appear to be as extreme on the risk front as they were in August and May 2011. Most important is wider recognition of the low growth state of the US economy, tame inflation and the structural impediments to swifter expansion. In this respect, while we expect continued bouts of risk on/risk off market volatility; this should create ample opportunities to generate return.

We expect to continue to overweight bond sectors which present the best combination of strong fundamental underpinnings and higher spreads as compensation for uncertainty and price volatility. In particular, MBS and covered bonds should continue to offer good risk/return characteristics. Corporate bonds appear to be fairly valued and we expect to use periods of market strength to reduce credit exposure, but will look to a period of more pronounced weakness, as a possible opportunity to add to credit exposure. Duration exposure will likely remain fairly close to the Index. As always, we continue to be very cognizant of the need to be nimble in our investment strategy, consistent with the Fund’s objective of seeking a high level of total return.

20

PERFORMANCE INFORMATION

| | One Year Ended