The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted

PRELIMINARY PROSPECTUS (Subject to Completion)

Dated May 31, 2023

Lucas GC Limited

3,070,000 Ordinary Shares

This is an initial public offering of, 3,070,000 ordinary shares of Lucas GC Limited, par value US$0.000005 per share, by Lucas GC Limited. We currently anticipate the initial public offering price of our ordinary shares will be between US$6.00 and US$7.00 per ordinary share.

Prior to this offering, there is no public market for our ordinary shares. We will apply to list the ordinary shares on the Nasdaq Global Market (the “Nasdaq”) under the symbol “LGCL.” At this time, Nasdaq has not yet approved our application to list our ordinary shares. There is no assurance that such application will be approved, and if our application is not approved by Nasdaq, this offering would not be completed.

Additionally, upon the completion of this offering, we will be a “controlled company” as defined under corporate governance rules of Nasdaq Stock Market, because HTL Lucky Holding Limited, which is wholly owned by our founder, chairman of the board of directors, or the Board, and chief executive officer, or CEO, Mr. Howard Lee, will beneficially own approximately 60.7% of our then-issued and outstanding ordinary shares and will be able to exercise approximately 60.7% of the total voting power of our issued and outstanding ordinary shares immediately after the consummation of this offering, assuming the underwriters do not exercise their option to purchase additional ordinary shares. For further information, see “Principal Shareholders.”

We are an “emerging growth company” and a “foreign private issuer” under applicable U.S. federal securities laws, and, as such are eligible for certain reduced public company reporting requirements for this prospectus and future filings. See the section titled “Prospectus Summary—Implications of Being an Emerging Growth Company” and “Prospectus Summary—Implications of Being a Foreign Private Issuer” for additional information.

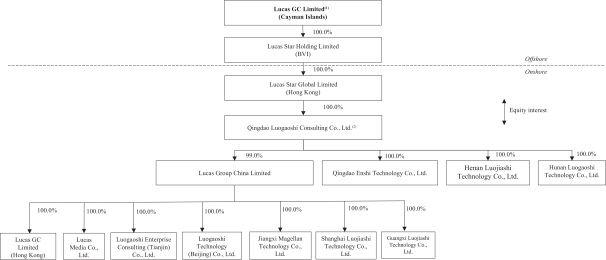

We are not a Chinese operating company but a Cayman Islands holding company with operations mainly conducted by our subsidiaries based in China. Investors in our securities are purchasing equity interest in Lucas GC Limited, a holding company incorporated in the Cayman Islands with business operations in China and therefore, investors may never hold equity interests in our Chinese operating entities. The “Company” or “our Company” refers to Lucas GC Limited, a Cayman Islands exempted company, and “we,” “us,” and “our” refer to Lucas GC Limited and its subsidiaries. We primarily conduct our business through Qingdao Luogaoshi Consulting Co., Ltd., a wholly owned subsidiary of Lucas GC Limited (the “WFOE”), and its subsidiaries based in the PRC. This operating structure may involve unique risks to investors. Under relevant PRC laws and regulations, foreign investors are permitted to own 100% of the equity interests in a PRC-incorporated company engaged in the business of providing services for professionals. However, the PRC government may implement changes to the existing laws and regulations in the future, which may result in the prohibition or restriction of foreign investors from owning equity interests in our PRC operating subsidiaries. There are significant legal and operational risks associated with being based in or having the substantial majority of operations in China, including those changes in the legal, political and economic policies of the Chinese government, the relations between China and the United States, or Chinese or U.S. regulations, all of which may materially and adversely affect our business, financial condition and results of operations. Any such changes could significantly limit or completely hinder our ability to offer or continue to offer our securities to investors, and could cause the value of our securities to significantly decline or become worthless. The PRC government has significant authority to exert influence on the ability of a company with operations in China to conduct business. The PRC government has initiated a series of regulatory actions and has made a number of public statements on the regulation of business operations in China with little advance notice, including cracking down on illegal activities in the securities market, enhancing supervision over China-based companies listed overseas, adopting new measures to extend the scope of cybersecurity reviews, and expanding efforts in anti-monopoly enforcement and data privacy protection. As of the date of this prospectus, as advised by our PRC legal adviser, Beijing Dentons Law offices, LLP, we do not believe that we are subject to (i) the cybersecurity review with the Cyberspace Administration of China, or CAC, as we do not qualify as a critical information infrastructure operator or an Internet platform operator that holds personal information of more than a million users, and our business does not involve data possessing that affects or may affect national security, implicates cybersecurity, or involves any type of restricted industry, pursuant to the 2022 Cybersecurity Review Measures (as defined elsewhere in this prospectus); or (ii) merger control review by China’s anti-monopoly enforcement agency due to the fact that we do not engage in monopolistic behaviors that are subject to these statements or regulatory actions. However, since these statements and regulatory actions are new, it is highly uncertain how soon legislative or administrative regulation making bodies will respond and what existing or new laws or regulations or detailed implementations and interpretations will be modified or promulgated, and, if any, the potential impact such modified or new laws and regulations will have on our daily business operation, ability to accept foreign investments and listing of our securities on a U.S. or other foreign exchange. On February 17, 2023, the China Securities Regulatory Commission, or the CSRC, issued the Trial Administrative Measures of Overseas Securities Offering and Listing by Domestic Companies, or the Trial Measures, which became effective on March 31, 2023. The Trial Measures regulate both direct and indirect overseas offering and listing by PRC domestic companies by adopting a filing-based regulatory regime. Pursuant to the Trial Measures, (i) an overseas offering and listing by a domestic company, whether directly or indirectly, shall be filed with the CSRC; and (ii) the issuer or its affiliated domestic company, as the case may be, shall file with the CSRC for its initial public offering, follow-on offering, issuance of convertible bonds, offshore relisting after go-private transactions and other equivalent offing activities in an overseas market. In addition, after a domestic company has offered and listed securities in an overseas market, it is required to file a report to the CSRC after the occurrence and public disclosure of certain material corporate events, including but not limited to, change of control and voluntary or mandatory delisting. As advised by our PRC legal adviser, Beijing Dentons Law Offices, LLP, under the applicable laws of PRC, we shall complete the relevant filing procedures with the CSRC before the completion of this offering and our listing on the Nasdaq. As of the date of the prospectus, we have been in the process of filing with the CSRC in connection with this offering and our listing on the Nasdaq. We may also be required to file with the CSRC in connection with any of our future offering and listing in an overseas market, including follow-on offerings, issuance of convertible bonds, offshore relisting after going-private transactions, and other equivalent offering activities. If we fail to complete such filing procedures for this offering and our listing on the Nasdaq as well as any future offshore offering or listing in an overseas market, including our follow-on offerings, issuance of convertible bonds, offshore relisting after going-private transactions, and other equivalent offering activities, we may face sanctions by the CSRC or other PRC regulatory authorities, which may include fines and penalties on us, restrictions on or delays to our financing transactions offshore, or other actions that could have a material and adverse effect on our business, financial condition, results of operations, reputation and prospects, as well as the trading price of our ordinary shares. For more details, please see “Risk Factors—Risks Relating to Our Business and Industry—We are subject to a variety of laws and regulations regarding cybersecurity and data protection, and any failure to comply with applicable laws and regulations, including improper use or appropriation of personal information provided directly or indirectly by our customers or end users, could have a material adverse effect on our business, financial condition and results of operations” and “Risk Factors—Risks Relating to Doing Business in China—Under the PRC laws, the approval of and the filing with the CSRC or other PRC government authorities may be required in connection with this offering and our listing on the Nasdaq as well as any of our future offering and listing in an overseas market, and, if required, we cannot predict whether or for how long we will be able to obtain such approval or complete such filing.”

The PRC government has significant oversight and discretion over the conduct of our business and may intervene with or influence our operations as the government deems appropriate to further regulatory, political and societal goals. The PRC government has published new policies that significantly affected certain industries such as the education and internet industries, and we cannot rule out the possibility that it will in the future release regulations or policies regarding our industry that could adversely affect our business, financial condition and results of operations. Furthermore, the PRC government has indicated an intent to exert more oversight and control over overseas securities offerings and other capital markets activities and foreign investment in China-based companies like us. Any such action, once taken by the PRC government, could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or in extreme cases, become worthless. For additional information, see “Risk Factors—Risks Relating to Doing Business in China—Uncertainties with respect to the PRC legal system, including uncertainties regarding the interpretation and enforcement of laws, and sudden or unexpected changes of PRC laws and regulations with little advance notice could adversely affect us and limit the legal protections available to you and us, and the Chinese government may exert more oversight and control over offerings that are conducted overseas, which changes could materially hinder our ability to offer or continue to offer our securities, and cause the value of our securities to significantly decline or become worthless.

As of the date of this prospectus, we have two subsidiaries in Hong Kong, including (i) Lucas Star Global Limited, a wholly owned subsidiary of Lucas Star Holding Limited, which is a wholly owned subsidiary of Lucas GC Limited; and (ii) Lucas GC Limited (Hong Kong), a wholly owned subsidiary of Lucas Group China Limited. Hong Kong is currently a separate jurisdiction from mainland China. The Basic Law of the Hong Kong Special Administrative Region, or the Basic Law, is a national law of the PRC and the constitutional document for Hong Kong, national laws and regulations of the PRC shall not