UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| |

(Mark One) |

☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended December 31, 2024 |

| OR |

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from ________________ to _______________ |

Commission File Number 001-41695

CORE LABORATORIES INC.

(Exact name of registrant as specified in its charter)

| | |

Delaware | | 98-1164194 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

6316 Windfern Road | | |

Houston, TX | | 77040 |

(Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number, including area code: (713) 328-2673

Securities registered pursuant to Section 12(b) of the Act:

| | | | |

Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

Common Stock (par value $0.01) | | CLB | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company, or emerging growth company. See definition of "large accelerated filer," "accelerated filer" and "smaller reporting company" and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | |

Large accelerated filer | ☒ | | Accelerated filer | ☐ | | Non-accelerated filer | ☐ | | Smaller reporting company | ☐ | | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes☐ No ☒

As of June 30, 2024, the aggregate market value of common stock held by non-affiliates of the registrant was approximately $938,376,082.

As of January 31, 2025, the number of shares of common stock of the registrant outstanding was 46,826,820.

DOCUMENTS INCORPORATED BY REFERENCE

The information required by Part III of this Report, to the extent not set forth herein, is incorporated herein by reference from the registrant’s definitive proxy statement relating to the Annual Meeting of Shareholders to be held in 2025, which definitive proxy statement shall be filed with the Securities and Exchange Commission within 120 days after the end of the fiscal year to which this Report relates.

CORE LABORATORIES INC.

FORM 10-K FOR THE FISCAL YEAR ENDED DECEMBER 31, 2024

TABLE OF CONTENTS

PART I

ITEM 1. BUSINESS

General

Core Laboratories Inc. is a Delaware corporation. We were established in 1936 and are one of the world’s leading providers of proprietary and patented reservoir description and production enhancement services and products to the oil and gas industry, primarily through client relationships with many of the world’s major, national and independent oil companies. These services and products can enable our clients to evaluate and improve reservoir performance and increase oil and gas recovery from their new and existing fields. We make measurements on reservoir rocks, reservoir fluids (crude oil, natural gas and water) and their derived products. In addition, we assist clients in evaluating subsurface targets associated with Carbon Capture and Sequestration (“CCS”) projects or initiatives. We have over 70 offices in more than 50 countries and have approximately 3,500 employees.

On May 1, 2023, Core Laboratories N.V. completed its previously announced redomestication transaction (the “Redomestication Transaction”), which through a series of steps, resulted in the merger of Core Laboratories N.V., a holding company in the Netherlands, with and into Core Laboratories Luxembourg S.A., a public limited liability company incorporated under the laws of Luxembourg, with Core Laboratories Luxembourg S.A. surviving, and subsequently the migration of Core Laboratories Luxembourg S.A. out of Luxembourg and its domestication as Core Laboratories Inc., a Delaware corporation. As a result of the Redomestication Transaction, all common shares in Core Laboratories N.V. were canceled and exchanged for common stock in Core Laboratories Luxembourg S.A. on a one-for-one basis. Former holders of Core Laboratories N.V. common shares now hold one share of common stock of Core Laboratories Inc. (formerly Core Laboratories Luxembourg S.A.) for each Core Laboratories N.V. common share owned immediately prior to the consummation of the Redomestication Transaction, and the business, assets, liabilities, directors and officers of Core Laboratories Inc. became the same as the business, assets, liabilities, directors and officers of Core Laboratories N.V. immediately prior to the Redomestication Transaction.

References to “Core Lab”, “the Company”, “we”, “our”, and similar phrases are used throughout this Annual Report on Form 10-K (this “Form 10-K”) and relate collectively to Core Laboratories Inc. and its consolidated affiliates.

Business Strategy

Our business strategy is to provide advanced technologies that improve reservoir performance by (i) continuing the development of proprietary technologies through client-driven research and development, (ii) expanding the services and products offered throughout our global network of offices and (iii) acquiring complementary technologies that add key technologies or market presence and enhance existing services and products.

Development of New Technologies, Services and Products

We conduct research and development to meet the needs of our clients who are continually seeking new services and technologies to lower their costs of finding, developing and producing oil and gas. While the aggregate number of wells being drilled per year fluctuates in response to market conditions, oil and gas producers have, on a proportional basis, increased expenditures on technology services to improve their understanding of the reservoir, increased production of oil and gas from their producing fields, and more recently, CCS projects. We intend to continue concentrating our efforts on services and technologies that help our clients reduce risk by evaluating geologic and engineering aspects of subsurface stratigraphic targets to improve reservoir performance and increase oil and gas recovery, as well as CCS projects and other projects directed at the global objective to reduce carbon emissions.

International Expansion of Services and Products

Another component of our business strategy is to broaden the spectrum of services and products offered to our clients on a global basis. We intend to continue using our worldwide network of offices to offer our services and products that have been developed internally or obtained through acquisitions. This global emphasis allows us to increase our revenue and enhance our profit through efficient utilization of our worldwide network.

Acquisitions

We continually review potential acquisitions to add key services and technologies, enhance market presence or complement existing business.

More information relating to any significant acquisitions is included in Note 3 - Acquisitions and Divestures of the Notes to the Consolidated Financial Statements.

Operations

We derive our revenue from services and product sales to clients primarily in the oil and gas and associated industries.

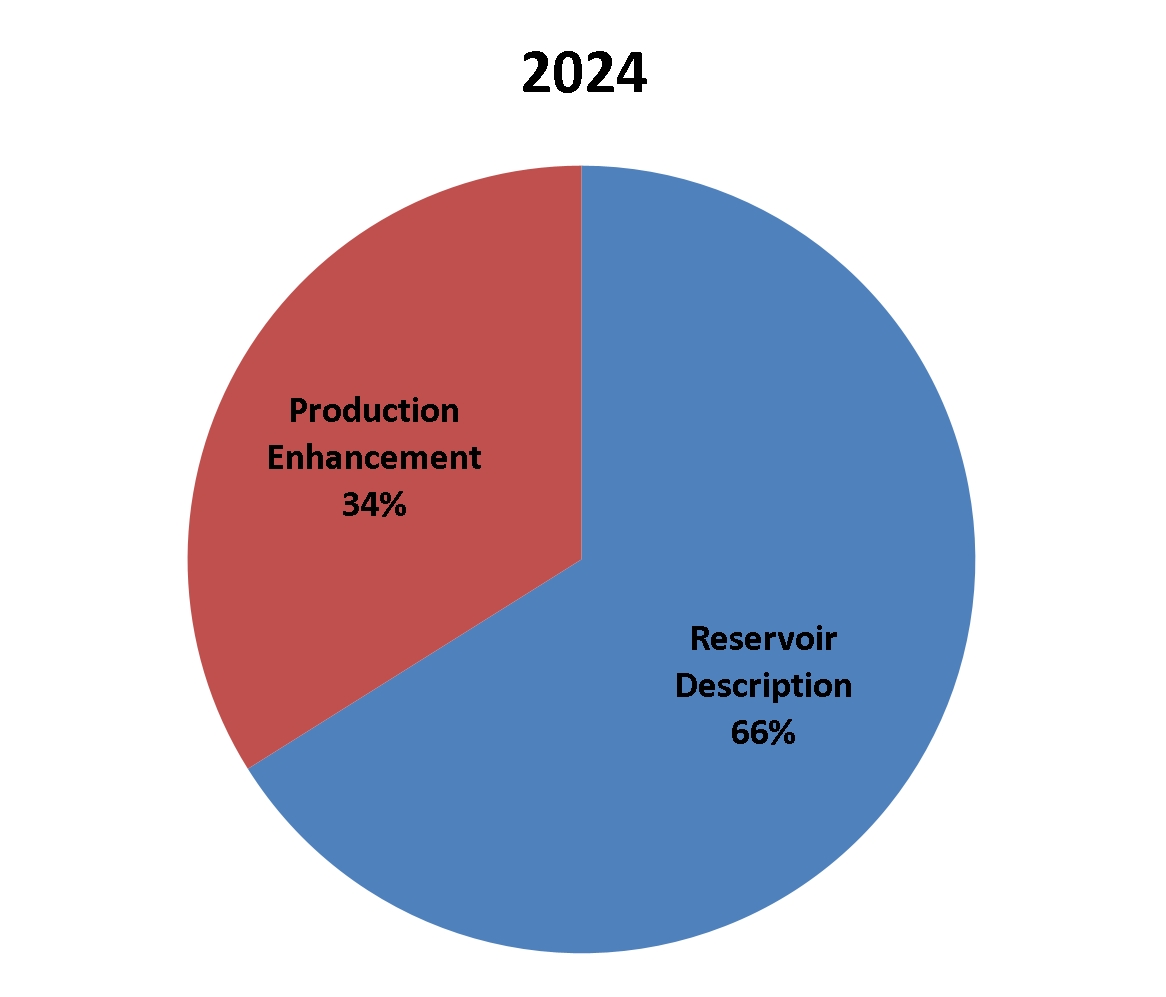

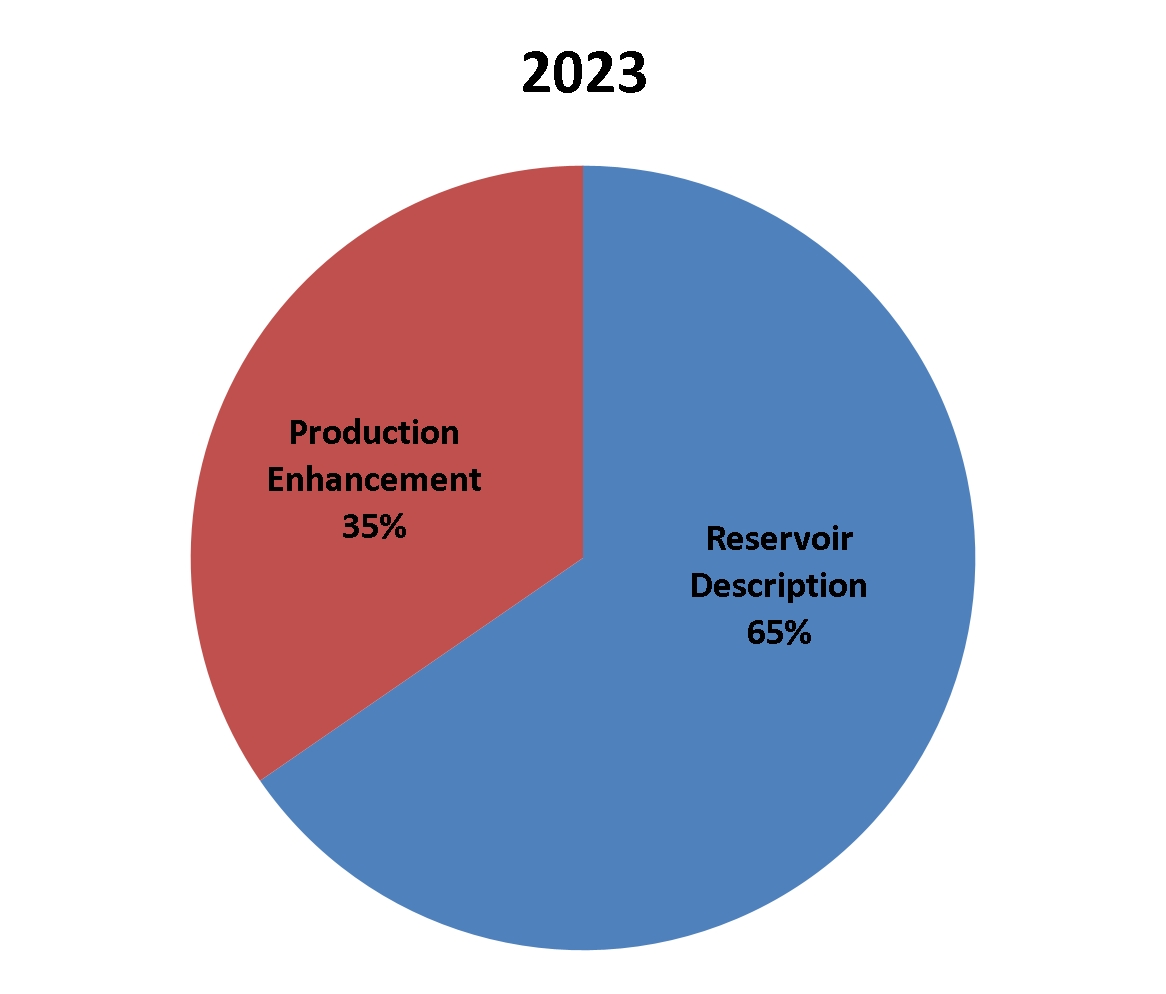

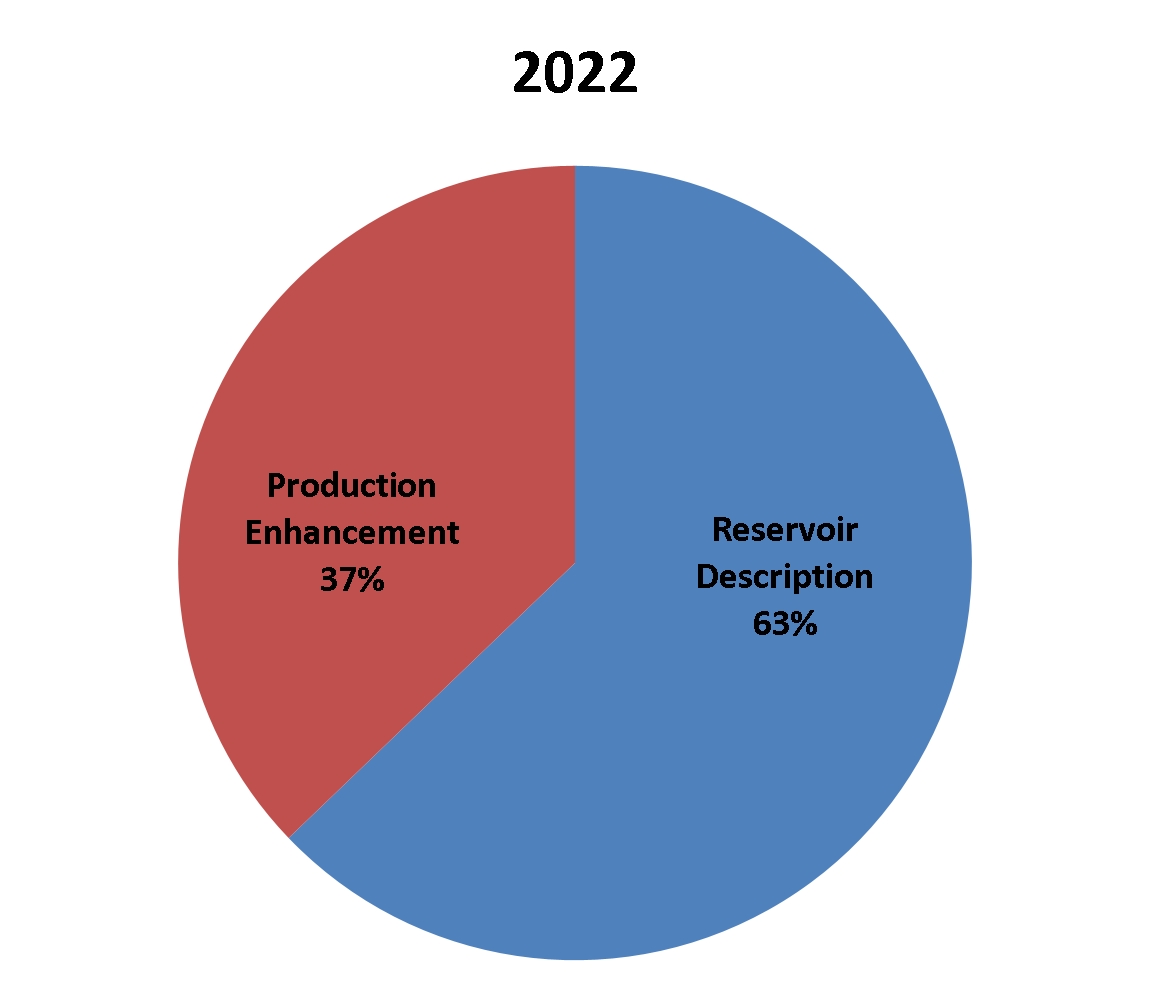

We operate our business in two segments. These complementary operating segments provide different services and products and utilize different technologies for evaluating and improving reservoir performance and increasing oil and gas recovery from new and existing fields. Disclosure relating to the operations and financial information of these operating segments is included in Note 21 - Segment Reporting and Other Disaggregated Information of the Notes to the Consolidated Financial Statements.

•Reservoir Description: Encompasses the characterization of petroleum reservoir rock, and reservoir fluids samples to increase production and improve recovery of crude oil and natural gas from our clients’ reservoirs. We provide laboratory-based analytical and field services to characterize properties of crude oil and crude oil-derived products to the oil and gas industry. Services associated with these fluids include determining the quality and measuring the quantity of the reservoir fluids and their derived products, such as gasoline, diesel and biofuels. We also provide proprietary and joint industry studies based on these types of analyses and manufacture associated laboratory equipment. In addition, we provide reservoir description capabilities that support various activities associated with energy transition projects, including services that support carbon capture, utilization and storage, geothermal projects, and the evaluation and appraisal of mining activities around lithium and other elements necessary for energy storage.

•Production Enhancement: Includes services and manufactured products associated with reservoir well completions, perforations, stimulation, production and well abandonment. We provide integrated diagnostic services to evaluate and monitor the effectiveness of well completions and to develop solutions aimed at increasing the effectiveness of enhanced oil recovery projects.

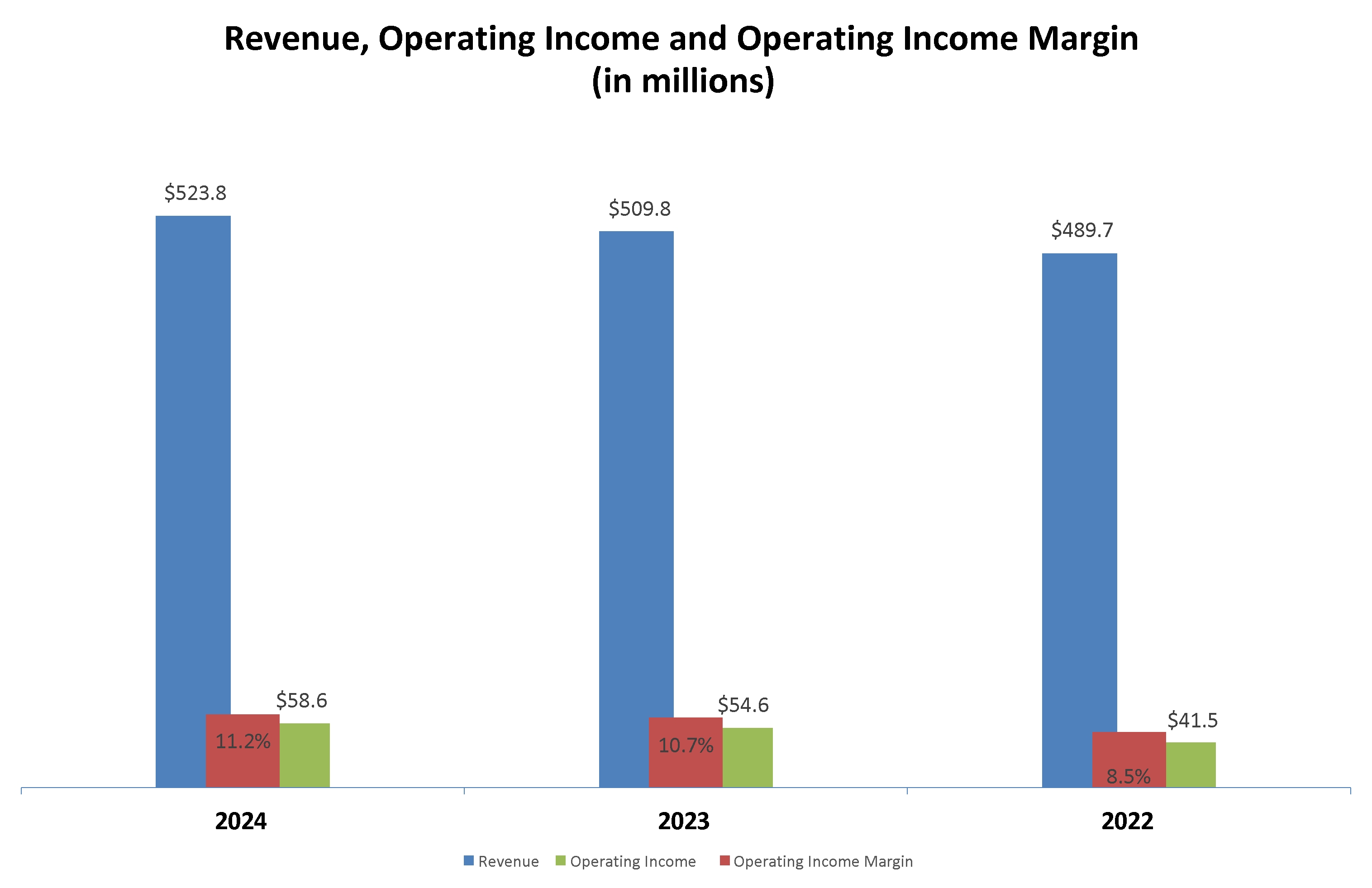

We offer our services worldwide through a global network of offices. Services accounted for 74%, 73% and 71% of our revenue for the years ended December 31, 2024, 2023 and 2022, respectively.

We manufacture products primarily in five facilities for distribution on a global basis. Product sales accounted for 26%, 27% and 29% of our revenue for the years ended December 31, 2024, 2023 and 2022, respectively.

Reservoir Description

Commercial oil and gas fields consist of porous and permeable reservoir rocks that contain crude oil, natural gas and formation water. Due to the density differences of the fluids, natural gas typically caps the field and overlies an oil layer, which overlies the water. We provide services that characterize the porous reservoir rock, all three reservoir fluids and their derived products. Services associated with these fluids include determining the quality and measuring the compositional, physical and volumetric properties of the complex reservoir hydrocarbons and their derived products, such as various fuels. Fluid analyses account for approximately two-thirds of Reservoir Description revenue. We also provide more advanced laboratory analyses which measure reservoir hydrocarbons at reservoir conditions to determine the changes in the hydrocarbon’s physical properties with changing pressure and temperature.

We analyze samples of reservoir rocks to determine lithologic, geochemical, and pore system properties. We measure rock properties, such as porosity, which determines reservoir storage capacity, and permeability, which defines the ability of the fluids to flow through the rock. These measurements are used to determine how much oil and gas are present in a reservoir and the rates at which the oil and gas can be produced. Conversely, the properties must also be known for injection projects such as CCS and water disposal. We also use our proprietary services and technologies to correlate the reservoir description data to wireline logs and other subsurface data.

The combined use of both the reservoir rock and fluid data are invaluable inputs for clients in determining the economic viability of hydrocarbon deposits and in identifying the most efficient methods to optimize the recovery, processing and refinement of these hydrocarbons. Early evaluations and key decisions about well performance and viability are important for optimizing a reservoir. This is accomplished by using proprietary and patented laboratory methods, including both traditional physical measurements and more recently introduced new technologies, such as Core Lab’s Non-Invasive Technologies for Reservoir OptimizationSM (“NITROSM”) services. NITROSM services include: Dual Energy Computed Tomography (“DECT”), Micro Computed Tomography, high and low frequency nuclear magnetic resonance, high-resolution gamma logging and continuous high energy x-ray fluorescence, along with pressure-volume-temperature (“PVT”), compositional analysis, and other Core Lab proprietary technologies.

Core Lab conducts a wide variety of physical laboratory tests to measure and evaluate fluid flow through the rock, often at in-situ reservoir temperatures and pressures. These are most commonly applied to conventional reservoirs. We have also developed unique analytical processes to understand the flow characteristics and saturation profiles of unconventional reservoir systems.

Core Lab has been at the forefront of digital transformation technologies for more than two decades. Core Lab’s extensive, proprietary databases and analog technologies, coupled with artificial intelligence (“AI”) and machine learning, help our clients improve efficiencies and lower operating costs throughout the upstream value chain. The analysis and integration of these critical datasets is enhanced because of Core Lab’s proprietary RAPIDTM database. Core Lab’s Digital Innovation Group works collaboratively with multiple international and national oil companies on projects that utilize Core Lab’s proprietary digital technologies and services. Core Lab’s proprietary Advanced Rock Typing technology combines Core Lab’s vast, comprehensive database of physical measurements and World Wide Rock CatalogTM with its proprietary image acquisition technology and innovative AI image recognition. Core Lab’s proprietary World Wide Rock CatalogTM provides a database and analog reference set for predicting properties when physical measurements are unavailable. These technologies provide clients with analog data sets in situations where the acquisition of new conventional core may not be possible or where only wellbore drill cuttings are available. High-resolution images of wellbore cuttings and sidewall cores are quickly and efficiently matched with analogs from Core Lab’s proprietary database of samples from around the world. Physically measured data sets from the matching analogs are delivered to our clients in time to make appraisal and development decisions.

Core Lab’s proprietary legacy portfolio of geological studies and rock and fluid property datasets on conventional reservoirs and seals, accessible through Core Lab’s database platform, RAPIDTM, are being leveraged in energy transition projects as well, and are proving invaluable to operators evaluating potential CCS sites.

Core Lab holds various patents, trade secrets, and proprietary designs for laboratory equipment required to analyze reservoir rocks as well as the properties and phase behavior of reservoir fluids and derived products. We manufacture a wide range of ambient and reservoir condition rock and fluid analysis laboratory equipment for our own use throughout our international laboratory network. Among these devices are complex, high-pressure, high-temperature, reservoir condition, multi-phase flow systems and full visualization Pressure-Volume-Temperature cells, along with the ancillary equipment required to support these laboratory programs. We also sell equipment of this type to universities, government institutes, and client company research labs.

While recognizing the need to optimize the full value chain of our clients, from producing well to retail sales of hydrocarbon products, a state-of-the-art IT platform, CONNECT: was launched to efficiently acquire and optimize workflows of field data, laboratory results, and other observations relevant to our client base. The system is designed for single data entry, and that data can be used for further analysis and, more importantly, be shared with our clients by process flow dashboards with key performance indicators. The system can also share real-time data on mobile devices, enabling our clients to make quick decisions.

We continue to add new modules to our suite of data management platforms that enhance customer experience and improve access to project results.

We conduct numerous large-scale, multi-company reservoir description projects, applying proprietary and state-of-the-art techniques from the earliest phases of a field development program until the last economic barrel of oil is recovered. We initiate and deliver a group of international and U.S. based consortium studies to evaluate both conventional and unconventional reservoirs. These projects, which often run more than a year, are of increasing importance to oil companies as the incremental barrel is often the lowest cost and most profitable barrel in the reservoir. Producing incremental barrels increases our clients’ cash flows which we believe will result in additional capital expenditures by our clients, and ultimately further opportunities for us. Core Lab retains rights of ownership to complete joint industry project studies, which can be resold at a later date.

Our databases, technology and analytical methods also allow us to assist our clients in other ways. Many of our clients have begun investing in and developing other sources of energy, including renewables. Some of these initiatives include deployment of technologies associated with the assessment of strata to establish strategies tied to subsurface gas storage and mining of elements such as lithium, which are critical components of batteries for energy storage. Measurement and analytical techniques are also used to assist our clients with reporting requirements associated with carbon sequestration.

Production Enhancement

Core Lab's Production Enhancement group provides products and diagnostic services to help optimize well completions, reservoir operations and field development strategies, in order to increase recoverable reserves in the most efficient way. These product offerings include perforating technologies to establish communication between the wellbore and the reservoir.

Diagnostic services are used to assess well completions and field floods. Two commonly used production enhancement methods are (i) hydraulic fracturing of the reservoir rock to improve flow and (ii) flooding a reservoir with water, carbon dioxide, nitrogen or hydrocarbon gases to drive more oil and gas to the producing wellbores. Many oilfields today are hydraulically fractured and/or flooded to maximize oil and gas recovery. Although Core Lab is not a hydraulic fracturing company, Core Lab does provide services that are used by operators to develop and optimize hydraulic fracturing and field flood projects and to evaluate the success of those projects. These services, products and expertise play a key role in the success of stimulation and enhanced oil recovery programs.

The hydraulic fracturing of a producing formation is achieved by pumping a fluid slurry containing a proppant material into the reservoir zone at extremely high pressures. This fractures the rock and the proppant material “props” or holds the fracture open after the pressure pumping is complete, so that reservoir fluids can flow through a highly conductive fracture network into the production wellbore. Data on rock type and strength generated in the Reservoir Description operating segment are critical for determining the proper design of the hydraulic fracturing treatment. In addition, further testing indicates whether the fluid slurry is compatible with the reservoir rock so that damage does not occur that would otherwise restrict production. Core Lab also provides testing of various propping agents and software to help select the best propping agent based on net present value calculations of client investments. Clients leverage our diagnostic services and the associated proprietary and patented technologies in the Permian, Eagle Ford, Wolfcamp, Bakken, Haynesville and other plays to assist them in the following areas;

•Chemical frac water tracing services are used to aid operators in determining the efficiency of the fracturing fluids used to optimize hydraulic fracture stimulation of long, multi-stage horizontal wells in oil- and gas-shale plays in unconventional reservoirs. This technology also enables clients to evaluate load recovery, gas breakthrough, fluid leak-off and breaker efficiency, all of which are important factors for optimizing oil and/or natural gas production after the formation is hydraulically fractured.

•Well diagnostic data sets are used to determine if and how effectively each frac stage is flowing and cleanup efficiency of the stimulation fluid, to determine whether horizontal wells are unobstructed and flowing through the entire length of a horizontal well. Clients use this data to confirm optimum cluster efficiency, stage spacing, stimulated reservoir volume, and to increase ultimate recovery. By applying this technology, clients can identify and remediate well obstructions that can negatively impact well performance, reserve calculations and reserve-based lending. Additionally, hydrocarbon production can be quantified from discrete segments in multi-stage horizontal well completions in unconventional tight-oil or gas plays. Frac stages with ineffective flows may warrant further stimulation or remedial actions, while guiding improvements in future frac designs and flowback procedures.

•The diagnostic services are also used as a completion monitoring system, to determine flow rates from reservoir zones after they have been hydraulically fractured. This provides clients with a baseline of early production information that can be compared to subsequent data later in the life of the well to see how hydrocarbon production from different reservoir layers or different quality rock varies over time.

•To help optimize the placement of unconventional horizontal wells, our diagnostic services are used to monitor offset well interference by sampling offset well oil, gas and water production. The amount of tracer detected in offset wells is used to help clients optimize both horizontal and vertical well spacing and the optimum amount of fracturing fluids for each stage.

•Dynamic flow tests of the reservoir fluids through reservoir rock are conducted, at actual reservoir pressure and temperature, to realistically simulate the flooding of a producing zone and assist in designing the enhanced hydrocarbon recovery projects. After a field flood is initiated, Core Lab is often involved in monitoring the progress of the flood to ensure the sweep efficiency during field flood is optimized and maximum incremental production is achieved.

•Our tracer technologies and proprietary logging tools are also used in the evaluation of gravel pack effectiveness in unconsolidated reservoirs. Patented technologies are used to measure density changes in the gravel pack annulus to verify the competency of the gravel pack.

In addition to Core Lab’s many patented reservoir diagnostic technologies, Production Enhancement has established itself as a global leader in the manufacturing and distribution of high-performance perforating products. Core Lab’s manufacturing operations in the United States and Canada continue to meet the global demand for our perforating systems while gaining in efficiency and productivity. Core Lab’s unique understanding of complex reservoirs supports our ability to supply perforating systems engineered to maximize well productivity by reducing, eliminating and overcoming formation damage caused during the drilling and completion of oil and gas wells. This “systems” approach to the perforation of an oil or gas well has resulted in numerous patented products which are aimed at assisting clients with the following:

•Perforating charges which provide a deeper and cleaner perforating tunnel into the oil and gas reservoir. This allows greater flow of hydrocarbons to the wellbore and helps to maximize hydrocarbon recovery from the reservoir.

•Perforating charges designed specifically for optimizing fracture stimulation well completions by providing low standard deviation perforation hole size, which minimizes tortuosity effects. This not only results in better well stimulations and improved, cleaner perforation tunnels, but also less surface horsepower and less time to stimulate the well, which translates into lower costs.

•Perforating technology which creates a uniform hole size through two strings of casing, utilized in mechanically isolated re-stimulation programs where the internal string is used to isolate older, depleted stages in previously under-stimulated wells.

•Oriented perforating systems which deliver consistent-hole-size charges that can be aligned in a specific orientation in order to achieve uniform breakdown across each stage. These systems offer: 1) extreme limited entry perforating capability, 2) precisely aligned perforations, and 3) minimized connections and completion string length.

•Proprietary plug and abandonment perforating systems, used in partial or full well abandonment projects, that allow for reduced rig time and efficient recovery of the interior casing, while eliminating risks and creating opportunities for production from untapped and still producing reservoir sections.

•The patented X-SPAN® and GTX-SPAN® casing patches which have temperature ratings to as much as 600°F. These systems are capable of performing in high temperature as well as high pressure oil and gas environments and are used to seal non-productive reservoir zones from the producing wellbore.

Additionally, Core Lab’s Production Enhancement operating segment offers services to assist clients in determining the best energetic solutions for a specific rock type, to maximize productivity of an operator’s reservoir through our Reservoir Optimized Completions Lab (“ROC LabTM”). The ROC LabTM features an industry-leading, Ultra High Pressure/High Temperature perforation test vessel. The test vessel is paired with a proprietary flow system that uses highly specialized, internally developed and manufactured pumps and flow controllers. Combined, these technologies create a proprietary flow loop capable of dynamically displacing oil, brine and gas through rock samples that have been perforated with preselected energetics. Core Lab leverages its multi-decade expertise in conducting multi-phase fluid flow tests through porous medium to optimize this technological investment.

Core Lab’s proprietary downhole energetic solutions and instrumentation are designed to systemize, simplify, automate, and de-risk the deployment of perforating systems, which are utilized by international oil and gas operators for well completions. These technologies provide a unique range of perforating tools and equipment, which have been developed to provide a number of advantages over existing technology. Core Lab’s Production Enhancement team has experienced technical services personnel to support clients through our global network of offices for the everyday use of our perforating systems and the rapid introduction of new products. Our personnel are capable of providing client training and on-site services in the completion of oil and gas wells.

Marketing and Sales

We market and sell our services and products through a combination of sales representatives, technical seminars, trade shows and print advertising. Direct sales and marketing are carried out by our sales force, technical experts and operating managers, as well as by sales representatives and distributors in various markets where we do not have offices. Our Business Development group manages a Large Account Management Program to better serve our largest and most active clients by meeting with key personnel within their organizations to ensure the quality of our services and products are meeting their expectations and address any issues or needs in a timely manner.

Research and Development

The market for our services and products is characterized by changing technology and frequent product introduction. As a result, our success is dependent upon our ability to develop or acquire new services and products on a cost-effective basis and to introduce them into the marketplace in a timely manner. Many of our acquisitions have allowed us to obtain the benefits of the acquired company’s research and development projects without incurring significant costs if we had attempted to develop the services and products ourselves. We incur costs as part of internal research and development, and these costs are charged to expense as incurred and reflected in the operational results of the associated operating segment. We intend to continue committing financial resources and effort to the development and acquisition of new services and products. Over the years, we have made a number of technological advances, including the development of key technologies utilized in our operations.

Substantially all of our new technologies are the result of requests and guidance from our clients, particularly major oil companies.

Patents and Trademarks

We believe our trade secrets, patents, technology, trademarks and other intellectual property rights are an important factor in maintaining our technological advantage, although no single one of these is considered essential to our success. Typically, we will seek to protect our intellectual property in all jurisdictions where we believe the cost of such protection is warranted. While we have patented some of our key technologies, we do not patent all of our proprietary technology even where regarded as patentable. We protect our intellectual property, including through the use of appropriate confidentiality agreements, legal enforcement proceedings and by other means.

International Operations

We operate facilities in more than 50 countries. Our non-U.S. operations accounted for 66%, 65% and 66% of our revenue during the years ended December 31, 2024, 2023 and 2022, respectively. We attribute service revenue to the country in which the service was performed rather than where the reservoir or project is located, while we attribute product sales revenue to the country where the product was shipped as we feel this gives a clearer view of our operations. We do, however, have significant levels of service revenue performed and recorded in the U.S. that are sourced from projects on non-U.S. oilfields.

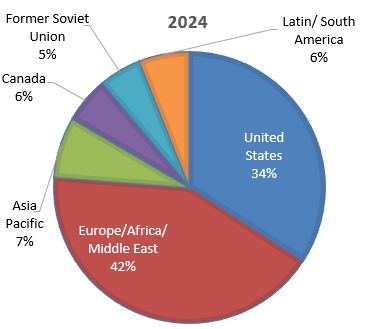

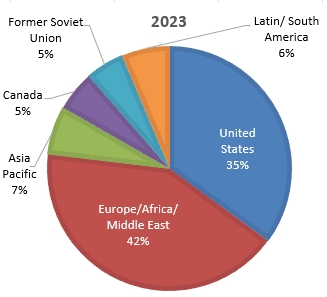

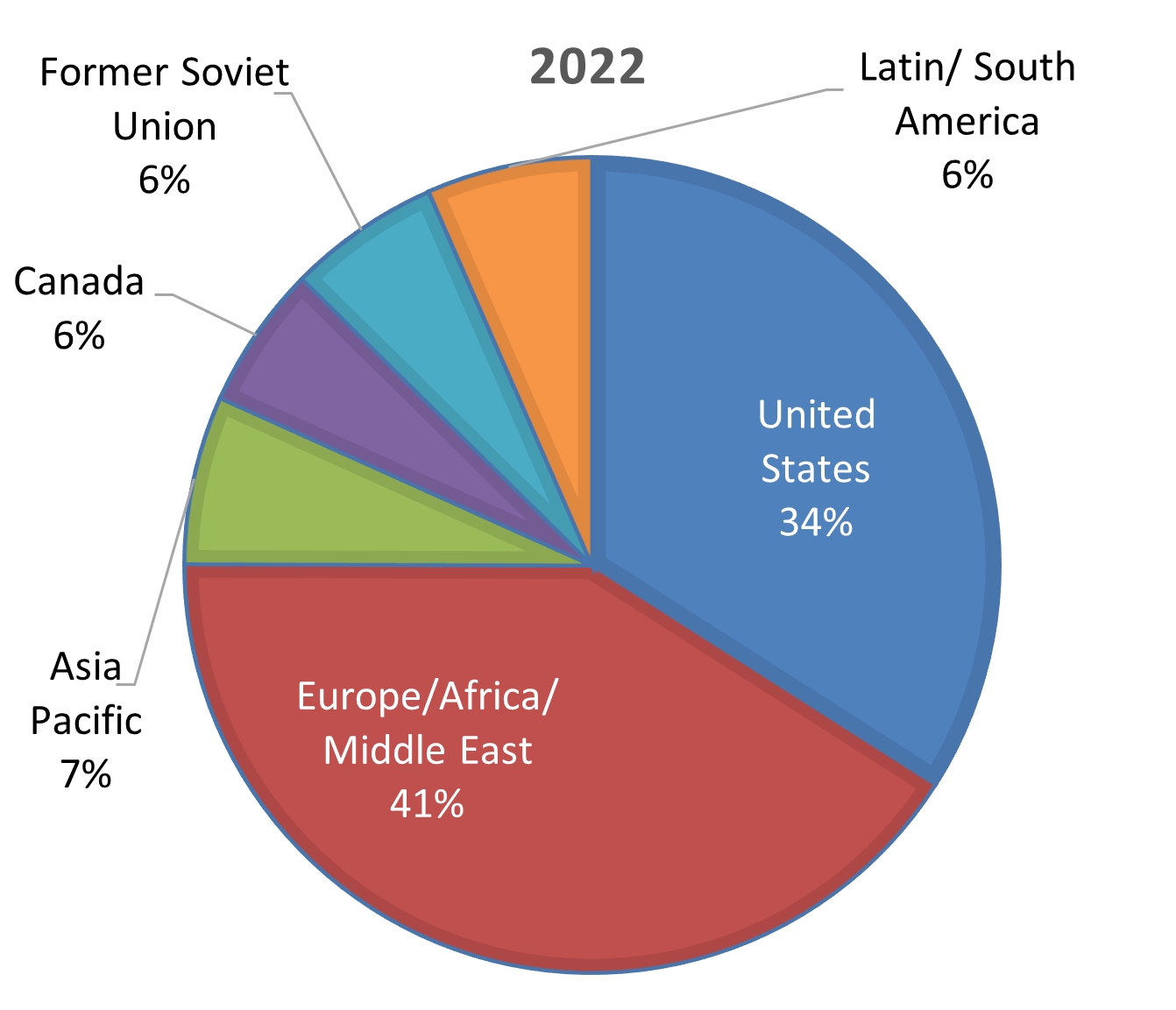

The following graphs and table summarize our reported revenue by geographic region for the years ended December 31, 2024, 2023 and 2022 (in thousands):

| | | | | | | | | | | | | | | | | | | | | |

| United States | | Europe/Africa/

Middle East | | Asia Pacific | | Canada | | Former Soviet

Union | | Latin/ South America | | Consolidated | |

2024 | $ | 178,895 | | $ | 220,360 | | $ | 37,796 | | $ | 28,637 | | $ | 26,723 | | $ | 31,437 | | $ | 523,848 | |

2023 | $ | 178,549 | | $ | 213,339 | | $ | 32,770 | | $ | 26,898 | | $ | 26,118 | | $ | 32,116 | | $ | 509,790 | |

2022 | $ | 166,701 | | $ | 200,863 | | $ | 32,688 | | $ | 27,797 | | $ | 29,514 | | $ | 32,172 | | $ | 489,735 | |

While we are subject to fluctuations and changes in currency exchange rates relating to our international operations, we attempt to limit our exposure to foreign currency fluctuations by limiting the amount in which our foreign contracts are denominated in a currency other than the U.S. dollar. However, the ultimate decision as to the proportion of the foreign currency component within a contract usually resides with our clients. Consequently, we are not always able to eliminate our foreign currency exposure. We have not historically engaged in and are not currently engaged in any significant currency hedging or trading transactions designed to compensate for adverse currency fluctuations.

Environment and Climate

Governmental Laws and Regulations

We are subject to stringent governmental laws and regulations, both in the United States and other countries, pertaining to protection of the environment.

We have developed policies and procedures associated with the management, handling, recycling or disposal of chemicals and gases and other materials and wastes resulting from our operations. In areas where environmental regulations do not exist, we have established other policies and procedures in efforts to preserve the environment.

Additionally, our analytical and manufacturing processes involve the handling and use of numerous chemicals and gases as well as the generation of wastes. Spills or other unauthorized releases of these chemicals, gases, and wastes at our facilities, whether by us or prior owners or operators, or at offsite locations where we transport them for recycling or disposal, could subject us to environmental liability, either from the applicable government agency or private landowners or other third parties. This could also include costs of cleaning up chemicals and wastes released into the environment and for damages to persons, properties or natural resources. As a result of such actions, we could be required to remove previously disposed wastes (including wastes disposed of or released by prior owners or operators), remediate environmental contamination (including contaminated groundwater), and undertake measures to prevent future contamination. Other countries where we operate have similar legal regimes. We may also be subject to claims alleging personal injury or property damage as a result of alleged exposure to hazardous substances as well as damage to natural resources. We may not be able to recover some or any of these remedial or corrective costs from insurance.

Environmental laws and regulations, and their interpretation, frequently change, and have tended to become more stringent over time. Our costs for compliance may not be fully recoverable from our clients and, thus, could reduce net income. New, modified or stricter enforcement of environmental laws and regulations could be adopted or implemented that significantly increase our compliance costs, pollution mitigation costs, or the cost of any remediation of environmental contamination that may become necessary, and these costs could have a material adverse effect on our business, financial condition, results of operation, or cash flows.

Historically, our environmental compliance costs have not had a material adverse effect on our results of operations; however, there can be no assurance that such costs will not be material in the future or that such future compliance will not have a material adverse effect on our business or results of operations.

In addition, we depend on the demand for our products and services from the oil and gas industry and, therefore, are affected by changing taxes (including subsidies), price controls, tariffs, and trade restrictions, and other laws and regulations relating to the oil and gas industry in general, including those specifically directed to hydraulic fracturing, onshore production, air pollution, and climate change.

Likewise, governmental, scientific, and public concern over the threat of climate change arising from greenhouse gas (“GHG”) emissions, including public and private incentive programs for alternative and renewable energy sources, may result in a change in consumer preferences for energy sources and therefore a decreased demand for our customers’ products. Sustained deviations from normal weather patterns, such as cooler or warmer summers and winters, can have a significant impact on demand as consumption of energy, particularly natural gas, is seasonal.

See Item 1A. Risk Factors, “Risk factors associated with health, safety and the environment” for further discussion on environmental matters.

Climate Related Initiatives

We are committed to reducing our physical risks and environmental footprint associated with climate change while improving our performance and sustainability in line with the global transition toward lower carbon sources of energy. Core Lab has disclosed its environmental impact through the Carbon Disclosure Project (a non-profit that runs the world’s leading environmental disclosure platform, “CDP”) annual survey since 2014.

Core Lab’s eighty-plus years of expertise evaluating both subsurface geology and fluid flow through natural, porous media and our reputation for reliable and efficient reservoir optimization services provides us with opportunities to play a positive role in supporting emerging energy transition initiatives.

Core Lab offers technologically advanced services that provide scientific data important to the design of client projects that involve injecting carbon dioxide (“CO2”) into geologic formations for permanent storage or to improve recovery of hydrocarbons. Within Core Lab’s CCS Consortium and through our laboratories, we study how CO2 interacts with fluids in the reservoir as well as how CO2 mobilizes residual oil in collaboration with the reservoir.

Physical Risk Analysis

In 2020, Core Lab conducted a physical risk assessment with the aid of a third-party sustainability data company for 100 of our locations to understand the exposure of our facilities and capital assets to climate change physical impacts under future

climate change scenarios. Physical risks evaluated were water stress, flooding, heatwave, cold wave, hurricane, wildfire, and sea level rise using three climate scenarios over time periods of 2020 (baseline), 2030 and 2050. Overall, the assessment indicated that we face moderate physical risk with our greatest exposure to water stress and cold wave. Our overall exposure has remained consistent throughout the scenarios, although exposure to a cold wave shows a decline through the scenarios. These physical risks could result in loss of revenue, increase in our costs, including insurance premiums, or affect the availability of insurance against such risks.

We do not have locations in a natural, rural environment. Before opening a new location, potential impacts to the environment and community are considered by executive management. In the event we close a particular location, we try to ensure that the land and building are properly returned to a suitable condition. We also take steps designed to ensure that any potential environmental conditions have been remediated as required by local regulation and standards.

GHG Emissions

Core Laboratories maintains a sustainability management system that tracks our consumption of non-renewable resources. We have also engaged a third-party sustainability data company to quantify the impact of emissions categorized as:

•Scope 1 (direct GHG emissions that occur from sources that we control or own),

•Scope 2 (indirect GHG emissions associated with the purchase of electricity, steam, heat, or cooling) or

•Scope 3 (indirect emissions that occur upstream or downstream in our value chain)

This system assists us in setting science-based targets for our Scope 1 and Scope 2 emissions. Science-based targets aim to help companies work towards limiting the increase in global average temperatures to below 2°C, a limit agreed upon by leading climate scientists and governments to ensure long-term sustainability and profitability. These tools focus our efforts on reducing our environmental footprint and provide the data needed to create other climate targets and goals.

Our operational footprint is primarily from our office buildings and laboratories and their related electricity consumption (Scope 2 emission) and use of natural gas and diesel for heating, backup generation and refrigeration processes (Scope 1 emission). In our efforts to reduce GHG emissions, we choose alternative sources of electricity, such as renewable sources or low-carbon emission natural gas when there are options available and feasible. We also consume fuel to operate field vehicles (Scope 1 emission), however, this is primarily limited to our staff working in the field and is not a significant emission component of our total operations. Most of the value chain emissions (Scope 3 emissions) occur upstream from our operations and are associated with employee commuting, purchased goods and services, activities associated with fuel and energy, and upstream transportation and distribution. Downstream emissions are primarily associated with transportation and distribution.

See Item 1A. Risk Factors, “Risk factors associated with health, safety and the environment” for further discussion on environmental matters.

Occupational Safety and Health Regulations

Our operations in the United States and foreign countries are subject to stringent occupational safety and health laws and regulations, which are intended to protect worker health and safety, including the federal Occupational Safety and Health Act, which establishes requirements to protect the health and safety of workers. The U.S. Occupational Safety and Health Administration (“OSHA”) hazard communication standard, the Environmental Protection Agency (“EPA”) community right-to-know regulations under Title III of the federal Superfund Amendment and Reauthorization Act and comparable state statutes require maintenance of information about hazardous materials used or produced in operations and provision of this information to employees, state and local government authorities and citizens. The federal Bureau of Alcohol, Tobacco, Firearms and Explosives (“ATF”) establishes requirements for the safe use and storage of explosives. Substantial fines and penalties can be imposed and orders or injunctions limiting or prohibiting certain operations may be issued in connection with any failure to comply with these laws and regulations. Foreign countries in which we conduct operations may also have analogous controls that regulate our worker safety-related activities, which controls may impose additional, or more stringent requirements.

As discussed above, our processes involve the handling and use of numerous chemicals and gases as well as the generation of waste which could cause harm to our employees. Such work is performed in an industrial or laboratory setting, or at our clients’ worksite which would also require travel. These types of conditions are susceptible to workplace accidents.

See Item 1A. Risk Factors, “Risk factors associated with health, safety and the environment” for further discussion on environmental matters.

Competition

The business in which we engage is competitive. Some of our competitors are divisions or subsidiaries of companies that are larger and have greater financial and other resources than we have. While no one company competes with us in all of our service and product lines, we face competition in these lines, primarily from independent regional companies and internal divisions of major integrated oil and gas companies. We compete in different service and product lines to various degrees on the basis of price, technical performance, availability, quality and technical support. Our ability to compete successfully depends on elements both within and outside of our control, including successful and timely development of new services and products, performance and quality, client service, pricing, industry trends and general economic trends.

Reliance on the Oil and Gas Industry

Our business and operations are substantially dependent upon the condition of the global oil and gas industry. Future downturns in the oil and gas industry, or in the oilfield services business as well as the adoption and implementation of legislation, executive orders, and other regulatory initiatives that seek to combat climate change by restricting fossil fuel activities, limiting GHG emissions, certain methods of extraction of oil and gas, or the locations in which such activities may be conducted, may have a material adverse effect on our financial position, results of operations or cash flows. This risk factor is perhaps amplified given recent pronouncements and actions taken by the executive and/or legislative branches of the U.S. government in an uncertain and shifting political environment.

The oil and gas industry is highly cyclical and has been subject to significant economic downturns at various times as a result of numerous factors affecting the supply of and demand for oil and natural gas, including the level of capital expenditures of the oil and gas industry, the level of drilling activity, the level of production activity, market prices of oil and gas, economic conditions existing in the world, interest rates and the cost of capital, environmental regulations, tax policies, the impact of certain geopolitical conflicts, political requirements of national governments, coordination by the Organization of Petroleum Exporting Countries and other oil producing nations (“OPEC+”), cost of producing oil and natural gas, and technological advances.

The success of our business has been underpinned by developing industry leading technologies used in evaluating and improving reservoir performance, increasing oil and gas recovery from new and existing fields, as well as evaluating potential CCS sites in the subsurface both onshore and offshore. Many of these technologies have been developed to meet the needs of our clients, which continue to evolve with demands in both traditional energy sources and with energy transition. As energy transition continues to evolve, our business may become more dependent on the continued innovation and adoption of our industry leading technologies.

Human Capital

We are primarily a service provider in the oilfield services industry, so our workforce includes employees who are highly skilled professionals, including engineers and geologists, and other technical personnel, in addition to our administrative employees. As of December 31, 2024, we had approximately 3,500 employees. We do not have any material collective bargaining agreements and consider relations with our employees to be good.

Our Core Values: (1) Safety Awareness, (2) Honesty & Integrity, (3) Customer Focus, (4) Building Trust and (5) Employee Development, define us as a company and are the framework that unite us on the path toward achieving our goals and propelling Core Lab forward. These values represent and establish the foundation by which we treat each other, conduct our business and simply define “how we do things around here.” By embedding our Core Values into our operating strategies, we ensure that our company culture and mission also drive our Environmental, Social and Governance (“ESG”) sustainability efforts. We keep our employees informed of major business developments through CoreConnect, a communication initiative to drive connection and engagement between employees and executive leadership, and through contact by extended leadership teams, periodic emails, quarterly newsletters, quarterly reports, and annual events.

Core Lab values its employees and is committed to providing resources that engage employees, enhance their work experience, and develop them for the future. To assist in this pledge, Core Lab has created its talent management strategy based on the employee life cycle. Our total rewards approach is aligned to our business strategy and country-specific market influences. We offer competitive compensation and benefit programs in each country where we operate. Our approach not only encompasses competitive compensation and benefits, but also personal and professional growth opportunities within a global performance culture.

We develop our employees through performance management and talent assessment processes, competency-based development plans and training both in leadership and functional areas while also offering educational assistance programs.

Our annual performance management cycle is an ongoing process that enables managers and employees to collaborate throughout the year to set performance goals and development objectives that align to business objectives. These processes are designed to help employees understand where they add value to the organization, provide focus on and discussion around career aspirations, and reward employees for high performance.

We aspire to create an inclusive work culture where differences are valued. We recognize the unique perspectives and thoughts that our employees bring to our environment which stimulates innovation and generates out-of-the-box solutions that benefit our Company, clients and industry. We promote a culture-centric focus on the health and safety of our employees and the environment with a proactive approach towards identifying and managing risks through recognition, evaluation, and education. We empower our employees by fostering a sense of responsibility for managing their own work environment through open communication, and a management-supported “zero accident” culture.

Web Site Access to Our Periodic SEC Reports

Our primary internet address is https://www.corelab.com. We file or furnish Quarterly Reports on Form 10-Q, Annual Reports on Form 10-K, Current Reports on Form 8-K, and any amendments to those reports with the U.S. Securities and Exchange Commission (“SEC”). These reports are available free of charge through our web site as soon as reasonably practicable after they are filed or furnished electronically with the SEC. We may from time to time provide important disclosures to investors by posting them in the investor relations section of our web site, as allowed by SEC rules.

The SEC maintains an internet website at https://www.sec.gov that contains reports, proxy and information statements, and other information regarding our company that we file electronically with the SEC. References to the Company’s website in this Form 10-K are provided as a convenience and do not constitute, and should not be deemed, an incorporation by reference of the information contained on, or available through, the website, and such information should not be considered part of this Form 10-K.

ITEM 1A. RISK FACTORS

Our forward-looking statements are based on assumptions that we believe to be reasonable but that may not prove to be accurate. All of our forward-looking information is, therefore, subject to risks and uncertainties that could cause actual results to differ materially from the results expected. All known, material risks and uncertainties are discussed below.

Risk factors associated with the industry in which we operate

Any cost reduction initiatives that Core Lab undertakes may not deliver the results it expects, and these actions may adversely affect its business.

As business conditions change, the Company may need to implement cost-cutting measures that may adversely affect its business. These cost-cutting measures may include reductions in the quarterly dividend, base salaries of senior executives and employees, annual capital expenditures, implementation of temporary employee furloughs, and workforce reductions, among other reductions of corporate and operating costs.

In addition, these initiatives could result in disruptions to Core Lab’s operations. Any cost-cutting measures could also negatively impact Core Lab’s business by delaying the introduction of new products or technologies, interrupting service of additional products, or impacting employee retention. There can be no assurance that additional costs will not offset any such reductions of its operations. If Core Lab’s operating costs are higher than expected, or if it does not maintain adequate control of its costs and expenses, Core Lab’s results of operations will suffer. If Core Lab is unable to mitigate these or other potential risks related to its cost cutting initiatives, it may disrupt Core Lab’s business or could have a material adverse effect on its financial condition and results of operations.

Downturns in the oil and gas industry, or in the oilfield services business, may have a material adverse effect on our financial condition or results of operations.

The oil and gas industry is highly cyclical and demand for the majority of our oilfield services and products is substantially dependent on the level of expenditures by the oil and gas industry for the exploration, development and production of crude oil and natural gas reserves, which are sensitive to oil and natural gas prices and generally dependent on the industry's view of future oil and gas prices. There are numerous factors affecting the supply of and demand for our services and products, which are summarized as:

▪general and economic business conditions, including market prices of oil and gas and expectations about future prices;

▪global or domestic health crises;

▪the adoption of legal requirements or taxation;

▪changes in existing laws, regulations or other governmental actions;

▪cost of producing and the ability to deliver oil and natural gas;

▪the level of drilling and production activity;

▪financial condition of our client base and their ability to fund capital expenditures;

▪coordination by the OPEC+;

▪civil unrest or political uncertainty in oil producing or consuming countries and other geopolitical conflict, including the ongoing conflict in the Middle East and between Russia and Ukraine;

▪level of consumption of oil, gas and petrochemicals by consumers;

▪availability of services and materials for our clients to grow their capital expenditures and to deliver product to market; and

▪availability of materials and equipment from key suppliers.

The oil and gas industry has historically experienced periodic downturns, which have been characterized by diminished demand for our oilfield services and products and downward pressure on the prices we charge. A significant downturn in the oil and gas industry could result in a reduction in demand for oilfield services and could adversely affect our operating results.

Changes in macro-economic factors impacting the oil and gas industry may negatively affect our ability to accurately predict client demand, which could cause us to hold excess or obsolete inventory and experience a reduction in gross margins and financial results.

We cannot accurately predict which or what level of our services and products our clients will need in the future. Orders are placed with our suppliers based on forecasts of client demand and, in some instances, we may establish buffer inventories to accommodate anticipated demand. Our forecasts of client demand are based on multiple assumptions, each of which may introduce errors into the estimates. In addition, many of our suppliers require a longer lead time to provide products than our clients’ demand for delivery of our finished products. If we overestimate client demand, we may allocate resources to the purchase of materials or manufactured products that we may not be able to sell when we expect to, if at all. As a result, we could hold excess or obsolete inventory, which would reduce gross margin and adversely affect financial results. Conversely, if we underestimate client demand or if insufficient manufacturing capacity is available, we could miss revenue opportunities and potentially lose market share and damage our client relationships. In addition, any future significant cancellations or deferrals of service contracts or product orders could materially and adversely affect profit margins, increase product obsolescence and restrict our ability to fund our operations.

Risk factors associated with our international presence

We depend on the results of our international operations, which expose us to risks inherent in doing business abroad.

We conduct our business in over 50 countries. Our operations, and those of our clients, are subject to the various laws, regulations and other legal requirements of those respective countries as well as various risks peculiar to each country, which may include, but are not limited to:

▪global economic conditions;

▪political actions and requirements of national governments including trade restrictions, embargoes, seizure, detention, nationalization and expropriation of assets;

▪interpretation of tax statutes and requirements of taxing authorities worldwide, including the United States, routine examination by taxing authorities and assessment of additional taxes, penalties and/or interest;

▪trade and economic sanctions, tariffs or other restrictions imposed by the European Union, the United Kingdom, the United States or other countries;

▪fluctuations and changes in currency exchange rates (see section below);

▪the impact of inflation;

▪difficulty in repatriating foreign currency received in excess of the local currency requirements;

▪current conditions in oil producing countries such as Venezuela, Nigeria, Libya, Iran and Iraq considering their potential impact on the world markets; and

▪geopolitical conflicts in the countries or regions we operate in, including the Russia-Ukraine and Middle East conflicts.

Historically, economic downturns and political events have resulted in lower demand for our services and products in certain markets. The continuing instability in the Middle East, North Africa, South America and Ukraine, and the potential for activity from terrorist groups that the U.S. government has cautioned against have further heightened our exposure to international risks. The global economy is highly influenced by public confidence in the geopolitical environment, and the situations in the affected countries and regions, as mentioned above, continue to be highly fluid; therefore, we expect to experience heightened international risks.

From time to time, certain geopolitical conflicts may lead to imposition of economic sanctions and associated export controls applicable to our operations. These sanctions may be imposed against certain countries, companies and individuals that may restrict or prohibit transactions involving the countries, companies and individuals identified, which may also further restrict or prohibit us in conducting sales and maintaining operations in any of these jurisdictions.

Our operations may be adversely affected by sanctions, export controls, and similar measures targeting Russia and other countries and territories as well as other responses to Russia’s military conflict in Ukraine.

The geopolitical conflict between Russia and Ukraine has resulted in the U.S. government, European Union, the United Kingdom and other countries imposing broad-ranging and coordinated economic sanctions and export control measures against Russia, Belarus, the Crimea Region of Ukraine, the so-called Donetsk People’s Republic and the so-called Luhansk People’s Republic, including, among others:

•a prohibition on doing business with certain Russian companies, large financial institutions, officials and oligarchs;

•a prohibition on commercial activities in the so-called Donetsk People’s Republic and the so-called Luhansk People’s Republic;

•a commitment by certain countries and the European Union to remove selected Russian banks from the Society for Worldwide Interbank Financial Telecommunications (“SWIFT”), the electronic banking network that connects banks globally;

•a ban on imports of Russian crude oil, certain refined petroleum products, and liquefied propane gas originating in or exported from Russia to the European Union, subject to limited exceptions;

•a ban on imports of Russian crude oil, liquefied natural gas and coal to the United States;

•a ban on new investment in the Russian energy sector;

•a prohibition by the U.S. on exporting, selling, or supplying certain categories of services, including engineering services and petroleum services, to persons located in Russia; and

•enhanced export controls and trade sanctions targeting Russia’s importation of certain goods and technology, including restrictive measures on the export and re-export of dual-use goods, stricter licensing policy with respect to issuing export licenses, and increased use of “end-use” controls to block or impose licensing requirements on exports.

Due to the international scope of our operations, the Company is subject to various laws and regulations, including regulations issued by the U.S. Department of Treasury, the U.S. Department of State, the Bureau of Industry and Security and Office of Foreign Asset Control, as well as the counterparts of these agencies in foreign countries. The Company actively monitors changes in these regulations as they pertain to the goods and services we provide and their impact on our business, including our business partners and customers.

As the conflict in Ukraine continues, these sanctions may change and be expanded, which could further hinder the Company’s ability to do business in Russia or with certain Russian entities, which could have an adverse impact on the Company’s financial condition and results of operations. Furthermore, in retaliation against new international sanctions and as part of measures to stabilize and support the volatile Russian financial and currency markets, Russian authorities imposed

significant currency control measures aimed at restricting the outflow of foreign currency and capital from Russia, imposed various restrictions on transacting with non-Russian parties, banned exports of various products and other economic and financial restrictions.

The Company routinely screens existing business partners globally against Specially Designated National / Restricted Persons lists. All new engagements with business partners are screened prior to the beginning of any business relationship. Individuals or entities that become subject to applicable sanctions are immediately blocked from further commercial activity with the Company until confirmed by the Company’s legal counsel whether permissible to proceed pursuant to a general or special license or other exemption, or a change in facts.

Furthermore, while we have policies, procedures and internal controls in place designed to ensure compliance with applicable sanctions and trade restrictions, and though the current effects from the Russia-Ukraine conflict have, thus far, not resulted in a material adverse impact to the Company’s financial condition or results of operations, our employees, contractors, and agents may take actions in violation of such policies and applicable law and we could be held ultimately responsible. We rely on our employees to adhere to the policies, procedures and internal controls we have established to maintain compliance with evolving sanctions and export controls. To that end, we have implemented training programs, both in person and online, to educate our employees on applicable sanctions and export controls laws. If we are held responsible for a violation of U.S. or other countries’ sanctions laws, we may be subject to various penalties, any of which could have a material adverse effect on our business, financial condition or results of operations.

Should future sanctions require us to cease or wind down our Russian operations, our assets located there may be impacted and could become subject to impairment. As of December 31, 2024, the Company’s fixed assets and total assets in Russia were $4.5 million and $11.7 million, respectively. Total assets located in Russia represent approximately 2% of the Company’s total assets. Additionally, the Company leases its operating facilities in Russia, and as of December 31, 2024, the contractual obligation to exit these leased facilities is approximately $0.4 million. For the year ended December 31, 2024, revenue attributable to our operations in Russia was $23.0 million, representing approximately 4% of the Company’s total revenue. If we discontinue our operations in Russia as a result of expanded sanctions, we could incur employee severance and other associated exit costs of approximately $2.5 million, as required under local laws.

During the year ended December 31, 2024, revenue attributable to the Company’s Ukraine operations and assets located in Ukraine, were immaterial to the Company’s total revenue and total assets.

We are actively monitoring the situation in Ukraine and assessing its impact on our operations in the region, including our business partners and customers. We have not experienced any material interruptions in our infrastructure, supplies or networks needed to support our operations. However, the situation is continuously evolving and the United States, the European Union, the United Kingdom and other countries may implement additional sanctions, export controls or other measures against Russia, Belarus and other countries, regions, officials, individuals or industries in the respective territories. We have no way to predict the progress or outcome of the conflict in Ukraine or its impacts in Ukraine, Russia or Belarus as the conflict, and any resulting government responses, are fluid and beyond our control. Our operations, financial results and cash flows, including our ability to repatriate cash, may be adversely affected due to the conflict and will depend on various factors, including the extent and duration of the conflict, its effects on regional and global economic and geopolitical conditions, and the effect of more expansive or stringent laws, sanctions or trade control restrictions, whether adopted by Western nations or the Russian Federation, on our business, the global economy and global supply chains.

The Russia-Ukraine conflict may also heighten many other risks, any of which could materially and adversely affect our business and results of operations. Such risks include, but are not limited to, adverse effects on global macroeconomic conditions, including increased inflation; increased volatility in the price and demand of oil and natural gas; increased exposure to cyber-attacks; limitations in our ability to implement and execute our business strategy; risks to employees and contractors that we have in the region; disruptions in global supply chains; exposure to foreign currency fluctuations; potential nationalizations and assets seizures in Russia; constraints or disruption in the capital markets and our sources of liquidity; our potential inability to service our remaining performance obligations; and potential contractual breaches and litigation.

Our results of operations may be significantly affected by foreign currency exchange rate risk.

We are exposed to risks due to fluctuations in currency exchange rates. By the nature of our business, we derive a substantial amount of our revenue from our international operations, where certain of our customer contracts are in foreign currencies that subject us to risks relating to fluctuations in currency exchange rates.

Our results of operations may be adversely affected because our efforts to comply with applicable anti-corruption laws such as the United States’ Foreign Corrupt Practices Act (the “FCPA”) and the United Kingdom’s Anti-Bribery Act (the

“ABA”) could restrict our ability to do business in foreign markets relative to our competitors who are not subject to these laws.

We operate in many parts of the world that have experienced governmental corruption to some degree and, in certain circumstances, strict compliance with anti-bribery laws may conflict with local customs and practices. We may be subject to competitive disadvantages to the extent that our competitors are able to secure business, licenses or other preferential treatment by making payments to government officials and others in positions of influence or through other methods that we are prohibited from using.

We are subject to the regulations imposed by the FCPA and the ABA, which generally prohibits us and our intermediaries from making improper payments to foreign officials for the purpose of obtaining or keeping business. In particular, we may be held liable for actions taken by our strategic or local partners even though our partners are not subject to these laws. Any such violations could result in substantial civil and/or criminal penalties and might adversely affect our business, results of operations or financial condition. In addition, our ability to continue to work in these parts of the world discussed above could be adversely affected if we were found to have violated certain laws, including the FCPA and the ABA.

Risk factors associated with technology advancement

If we are not able to develop or acquire new services or products or our services and products become technologically obsolete, our results of operations may be adversely affected.

The market for our services and products is characterized by changing technology and product introduction. As a result, our success is dependent upon our ability to develop or acquire new services and products on a cost-effective basis and to introduce them into the marketplace in a timely manner. While we intend to continue committing substantial financial resources and effort to the development or acquisition of new services and products, we may not be able to successfully differentiate our services and products from those of our competitors. Our clients may not consider our proposed services and products to be of value to them; or if the proposed services and products are of a competitive nature, our clients may not view them as superior to our competitors’ services and products. In addition, we may not be able to adapt to evolving markets and technologies, develop or acquire new services or products, or achieve and maintain technological advantages.

If we are unable to continue developing or acquiring competitive services and products in a timely manner in response to changes in technology, our business and operating results may be materially and adversely affected. In addition, continuing development or acquisition of new products inherently carries the risk of inventory obsolescence with respect to our older products.

If we are unable to obtain patents, licenses and other intellectual property rights covering our services and products, our operating results may be adversely affected.

Our success depends, in part, on our ability to obtain patents, licenses and other intellectual property rights covering our services and products. To that end, we have obtained certain patents and intend to continue to seek patents on some of our inventions, services and products. While we have patented some of our key technologies, we do not patent all of our proprietary technology, even when regarded as patentable. The process of seeking patent protection can be long and expensive. There can be no assurance that patents will be issued from currently pending or future applications or that, if patents are issued, they will be of sufficient scope or strength to provide meaningful protection or any commercial advantage to us. In addition, effective copyright and trade secret protection may be unavailable or limited in certain countries. Litigation, which could demand significant financial and management resources, may be necessary to enforce our patents or other intellectual property rights. Also, there can be no assurance that we can obtain licenses or other rights to necessary intellectual property on acceptable terms.

We are subject to cyber security risks. A cyber incident could occur and result in information theft, data corruption, operational disruption and/or financial loss.

The frequency and magnitude of cybersecurity attacks is increasing and threat actors have become more sophisticated. Cybersecurity attacks are similarly evolving and include without limitation use of malicious software, surveillance, credential stuffing, spear phishing, social engineering, use of deepfakes (i.e., highly realistic synthetic media generated by artificial intelligence), attempts to gain unauthorized access to data, and other electronic security breaches that could lead to disruptions in critical systems, unauthorized release of confidential or otherwise protected information and corruption of data. We may be unable to anticipate, detect or prevent future attacks, particularly as the vectors used by threat actors change frequently or are not readily identifiable until deployed. We may also be unable to investigate or remediate cybersecurity incidents as threat

actors are increasingly using techniques designed to circumvent controls, avoid detection, and delete or obfuscate forensic evidence.

Our technologies, systems and networks, and those of our vendors, suppliers and other business partners, may become the target of cyberattacks or information security breaches that could result in the unauthorized release, gathering, monitoring, misuse, loss or destruction of proprietary information, personal information and other data, or other disruption of our business operations. In addition, certain cyber incidents, such as unauthorized surveillance, may remain undetected for an extended period. Our systems and insurance coverage (if any) for protecting against cyber security risks, including cyberattacks, may not be sufficient and may not protect against or cover all of the losses (including potential reputational loss) we may experience. As cyber incidents continue to evolve, particularly with the advent of artificial intelligence, we may be required to expend additional resources to modify or enhance our cybersecurity measures or to investigate and remediate the effects of cyber incidents.

We utilize technologies, controls and procedures, as well as internal staff and external service providers to protect our systems and data, to identify and remediate vulnerabilities and to monitor and respond to threats. However, there can be no assurance that such measures will be sufficient to prevent security breaches from occurring. No security measure is infallible. If we or the third parties with whom we interact were to experience a successful attack, the potential consequences to our business, workforce and the communities in which we operate could be significant, including financial losses, regulatory fines, loss of business, an inability to settle transactions or maintain operations, litigation costs, remediation costs, disruptions related to investigation, and significant damage to our reputation. If our systems for protecting against cyber-attacks prove not to be sufficient, we could be adversely affected by loss or damage of intellectual property, proprietary information, client data, employee data, financial data, our reputation, interruption of business operations, or additional costs to prevent, respond to, or mitigate cyber-attacks. These risks could have a material adverse effect on our business, reputation, results of operations, and financial condition.

Risk factors associated with our supply chain, resources, liquidity and capital management

We are subject to the risk of supplier concentration.

Certain of our product lines depend on a limited number of third party suppliers and vendors available in the marketplace. As a result of this concentration in some of our supply chains, our business and operations could be negatively affected if our key suppliers were to experience significant disruptions affecting the price, quality, availability or timely delivery of their products. For example, we have a limited number of vendors for our manufactured product lines. The partial or complete loss of any one of our key suppliers, or a significant adverse change in the relationship with any of these suppliers, through consolidation or otherwise, would limit our ability to manufacture and sell certain of our products.

There are risks relating to our acquisition strategy. If we are unable to successfully integrate and manage businesses that we have acquired and any businesses acquired in the future, our results of operations and financial condition could be adversely affected.

One of our key business strategies is to acquire technologies, operations and assets that are complementary to our existing business. There are financial, operational and legal risks inherent in any acquisition strategy, including:

▪increased financial leverage;

▪ability to obtain additional financing;

▪increased interest expense; and

▪difficulties involved in combining disparate company cultures and facilities.