Exhibit 99.1

Forward-looking statements

This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements are based on the current beliefs and expectations of JPMorgan Chase & Co.’s management and are subject to significant risks and uncertainties. Actual results may differ from those set forth in the forward-looking statements. Factors that could cause JPMorgan Chase & Co.’s actual results to differ materially from those described in the forward-looking statements can be found in JPMorgan Chase & Co.’s Annual Report on Form 10-K for the year ended December 31, 2010 (as revised by a Current Report on Form 8-K dated November 4, 2011), and Quarterly Reports on Form 10-Q for the quarters ended March 31, 2011 (as revised by a Current Report on Form 8-K dated November 4, 2011), June 30, 2011 (as revised by a Current Report on Form 8-K dated November 4, 2011), and September 30, 2011, which have been filed with the Securities and Exchange Commission and are available on JPMorgan Chase & Co.’s website (www.jpmorganchase.com) and on the Securities and Exchange Commission’s website (www.sec.gov). JPMorgan Chase & Co. does not undertake to update the forward-looking statements to reflect the impact of circumstances or events that may arise after the respective dates of the referenced forward-looking statements.

February 28, 2012 F I R M O V E R V I E W Doug Braunstein, Chief Financial Officer |

I. JPMorgan Chase overview Performance summary Customer focus Leveraging the franchise Global presence Loan growth and run-off portfolios Credit quality Deposit growth Net interest margin Expense and investments Agenda II. Specific risk questions from investors European exposure Mortgage settlement Private label litigation III. Firmwide capital LOB capital allocation Target returns Capital planning IV.Key firmwide themes V. Appendix 1 |

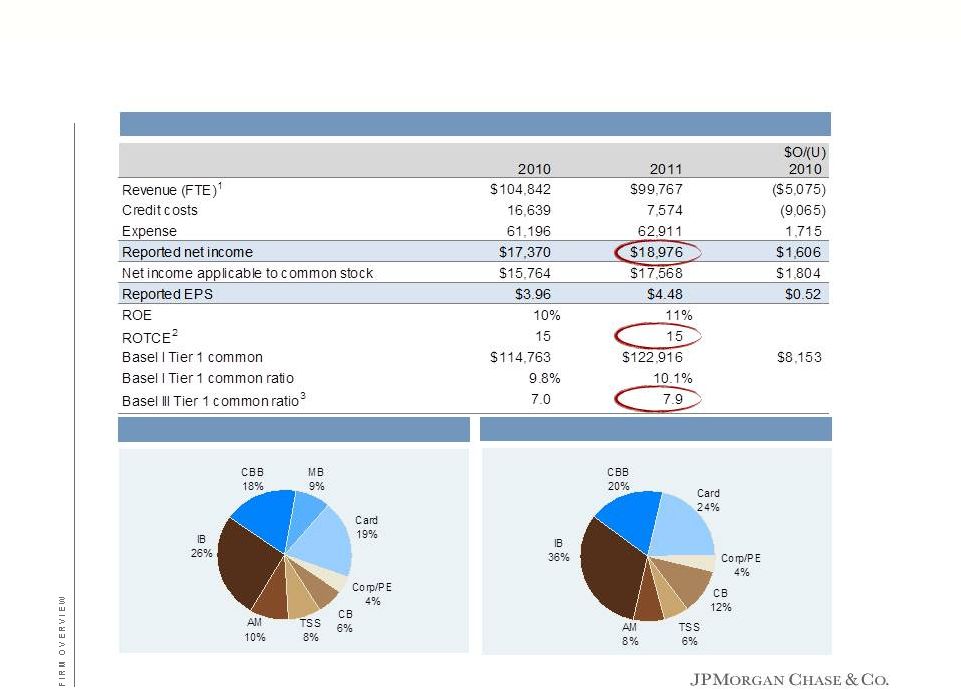

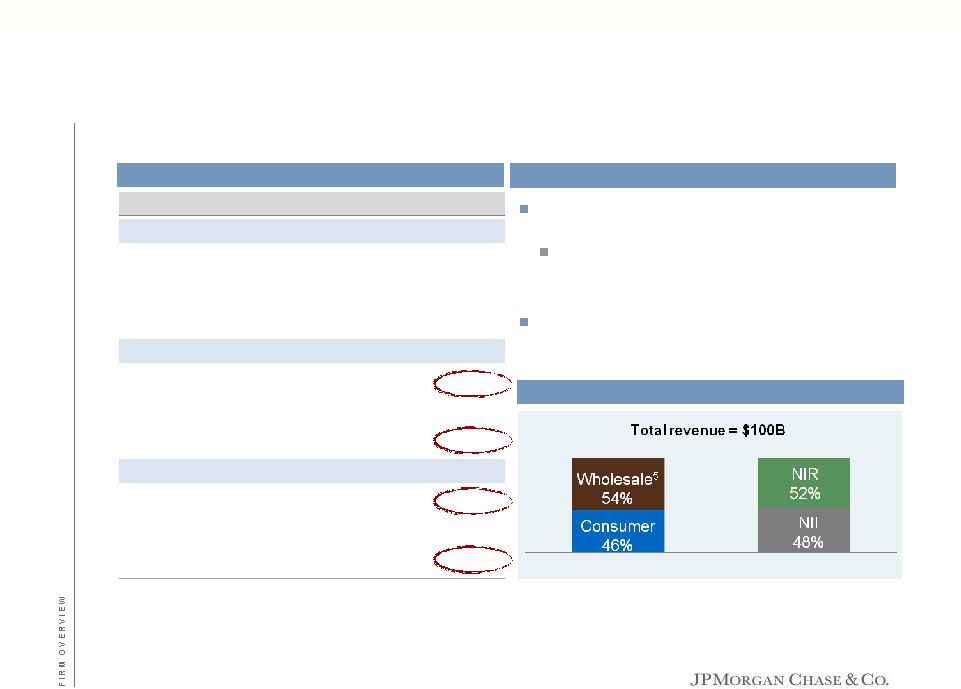

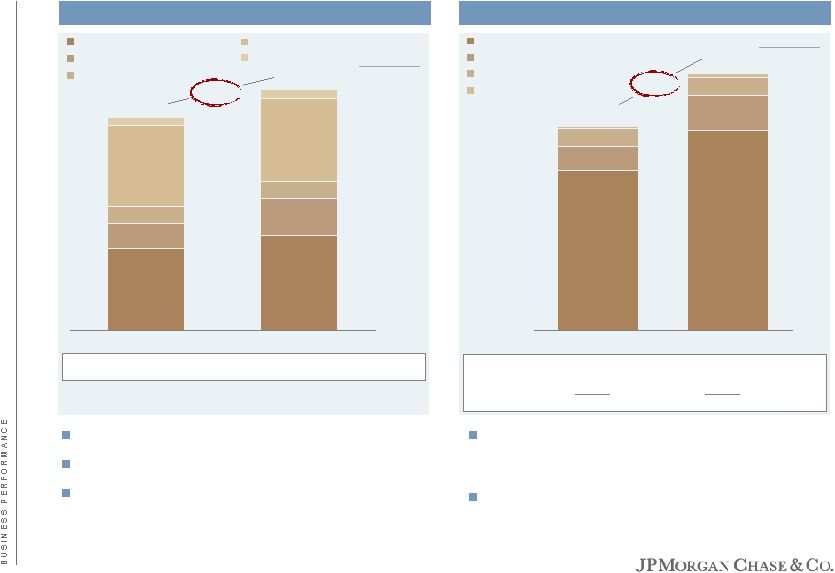

$mm, excluding EPS Performance summary JPMorgan Chase overview 1 See note 1 on slide 43 2 See note 4 on slide 43 3 Estimated 4 Excludes MB FY11 net loss of ($2.1B) or (11)% Total = $19.0B Net income – 2011 4 Total = $99.8B Firmwide revenue – 2011 2 |

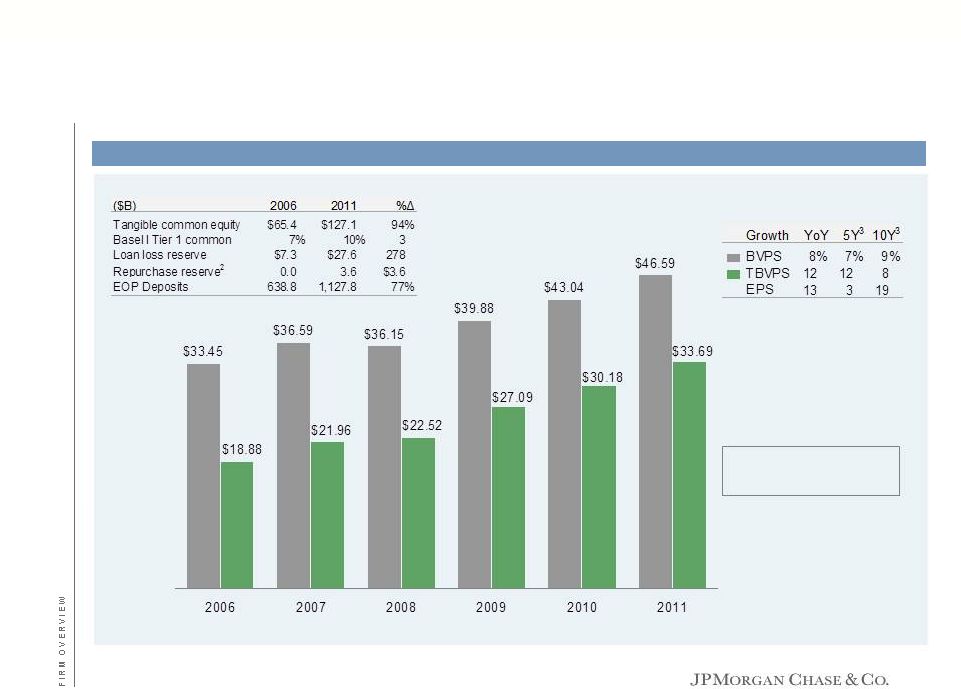

Book value per share: growing our fortress balance sheet JPMorgan Chase overview Shares outstanding (EOP) 3.7B 3.9B 3.9B 3.8B 3.4B 3.5B 1 Actual change 2 Excludes litigation reserve 3 CAGR Key metrics since 2006 3 2011 share repurchases: $9B 1 1 |

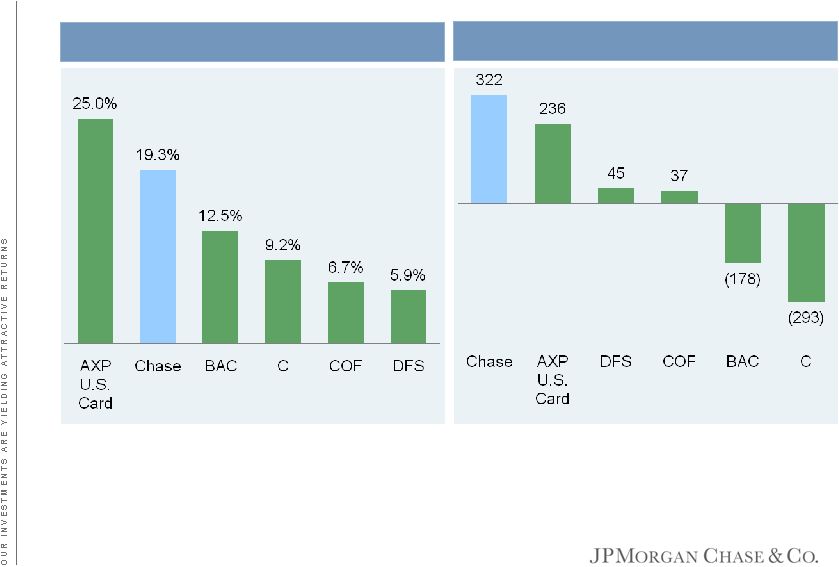

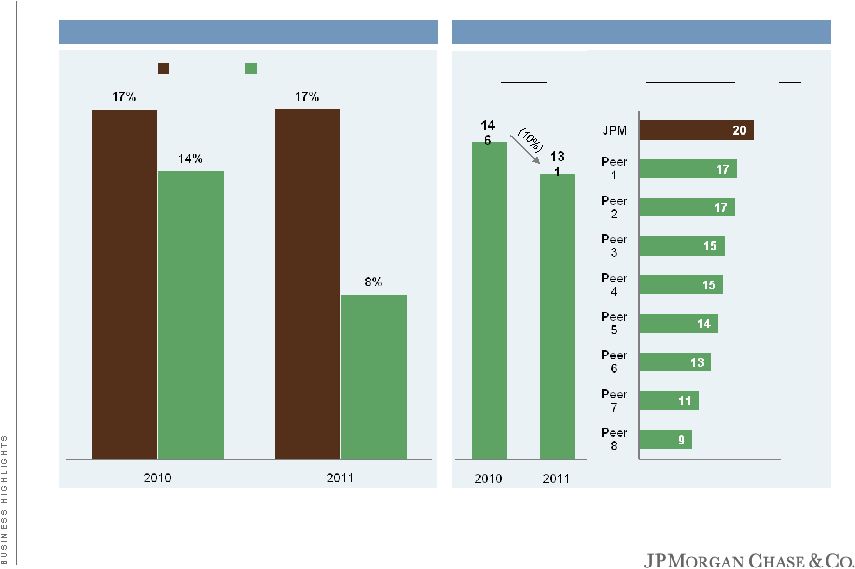

1 Peer group includes BAC, C, WFC, GS and MS 2 Based on Basel I RWA 3 (NII+NIR-NCOs)/Basel I RWA; excludes GS and MS 4 Presented on a managed basis. See note 1 on slide 43 5 Wholesale includes Corporate Note: Totals may not sum due to rounding Business returns JPMorgan Chase overview ROA does not capture the difference in business mix between JPM and its peers For instance, the IB includes large asset classes which have low yield but low risk, including the repo book We consider return on RWA and risk-adjusted return to be more relevant for JPM and comparisons to peers 4 Return analysis Comments 2011 revenue mix 4 2009 2010 2011 Return on assets 1 JPM 0.6% 0.9% 0.9% Peer avg. 0.6 0.6 0.6 Best-in-class 1.5 1.0 1.2 Return on RWA 1,2 JPM 1.0% 1.5% 1.6% Peer avg. 1.0 1.2 1.1 Best-in-class 3.2 1.9 1.6 Risk-adjusted return 1,3 JPM 6.5% 6.8% 7.3% Peer avg. 5.2 5.8 6.1 Best-in-class 6.7 6.8 7.3 |

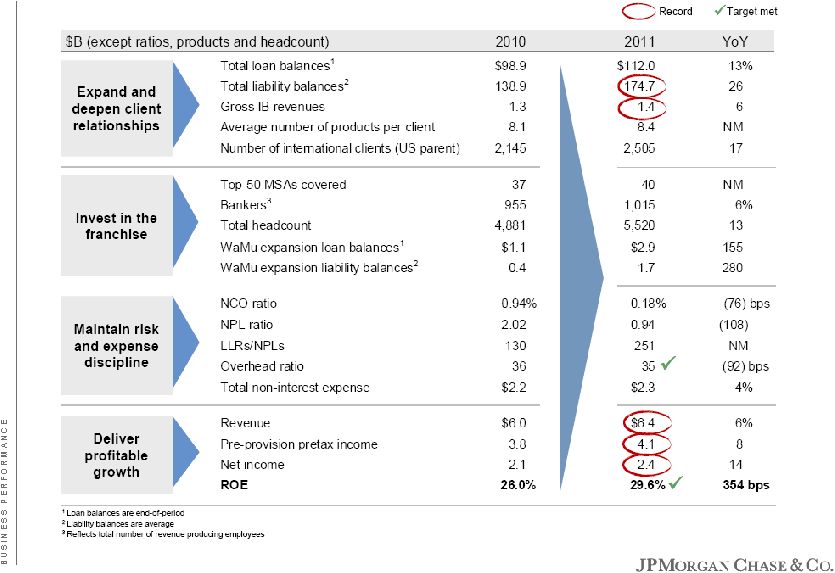

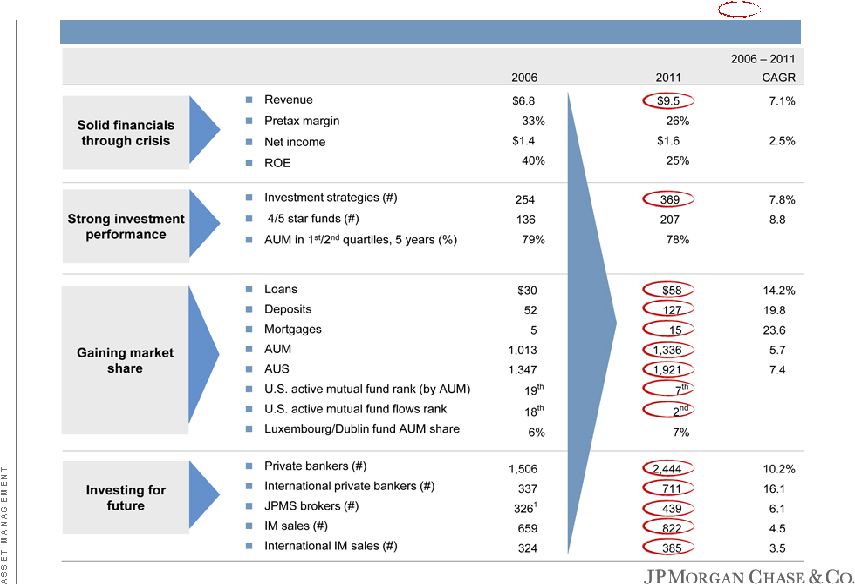

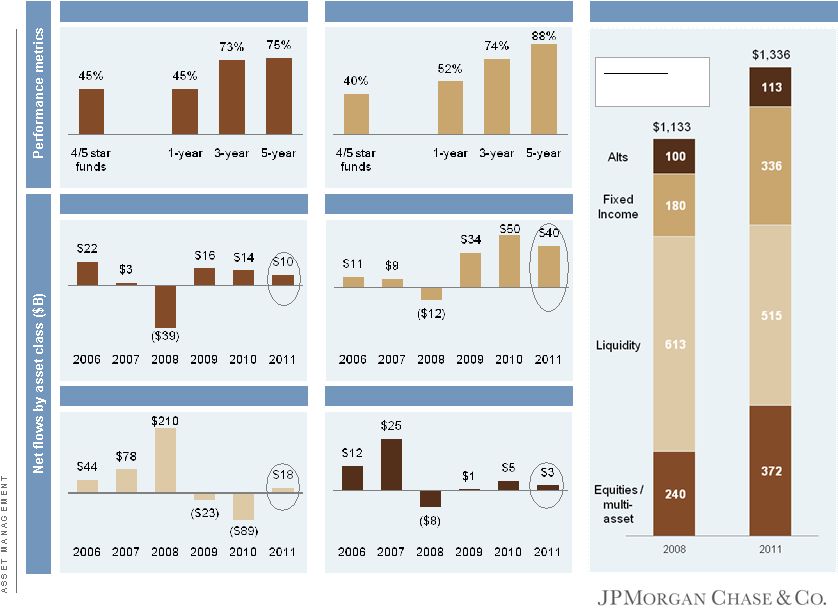

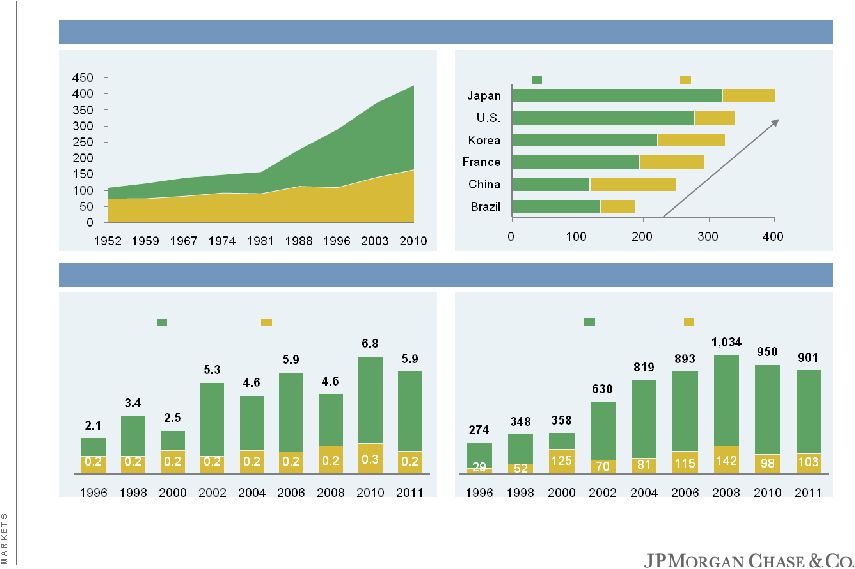

Building market leading franchises JPMorgan Chase overview 1 2006 IB financial data represents heritage JPM only. JPM’s Dealogic IB fees rank was #1 in 2011 and # 1 in 2006 for heritage JPM only 2 Includes deposits and deposits swept to on-balance sheet liabilities 3 Source: Inside Mortgage Finance, 4Q06 and 4Q11 for 2006 and 2011, respectively 4 Excludes Commercial Card 5 GPCC stands for General Purpose Credit Card; excludes WaMu and Commercial Card 6 2011 is through November 5 Select key stats ($B, except where noted) 2006 2011 2006-2011 CAGR IB fees ($mm) $5,537 $5,859 1.1% Fixed income markets ($mm) 8,736 15,337 11.9 Equity markets ($mm) 3,458 4,832 6.9 Average liability balances $73.6 $174.7 18.9% Average loans 53.6 104.2 14.2 IB revenue, gross 0.7 1.4 14.7 Overhead ratio 52% 35% Average liability balances $189.5 $318.8 11.0% Assets under custody ($T) 13.9 16.9 3.9 Average trade loan balances 1.5 27.8 79.6 Non-U.S. revenue (%) 40.8% 55.0% Assets under management $1,013.1 $1,336.2 5.7% Long-term flows 45.0 53.0 3.3 Number of Private Banking client advisors 1,506 2,883 13.9 Average total deposits $190.1 $360.7 13.7% Client investment assets, excluding deposits 80.6 137.9 11.3 End-of-period Business Banking loans 14,205 17,652 4.4 Number of branches 3,079 5,508 12.3 Mortgage loans originated $119.2 $145.6 4.1% Retail branch and direct to consumer originations 40.5 87.2 16.6 Number of branch salespeople 1,196 3,125 21.2 Mortgage loan origination market share 5.8% 11.5% Card Services sales volume 4 $256.8 $343.7 6.0% Card Services net revenue rate (% avg. loans) 10.4% 12.3% GPCC sales volume market share 5 15.7 19.3 Auto originations market share 3.1 4.3 Card AM IB CBB TSS CB MB 1 1 1 2 3 4 6 2 |

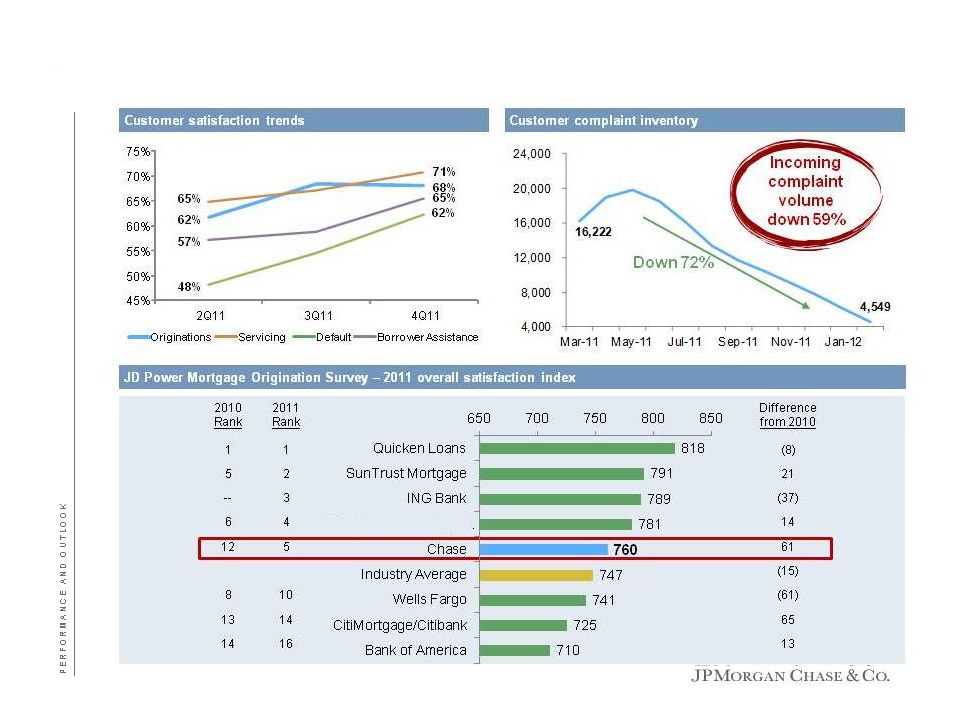

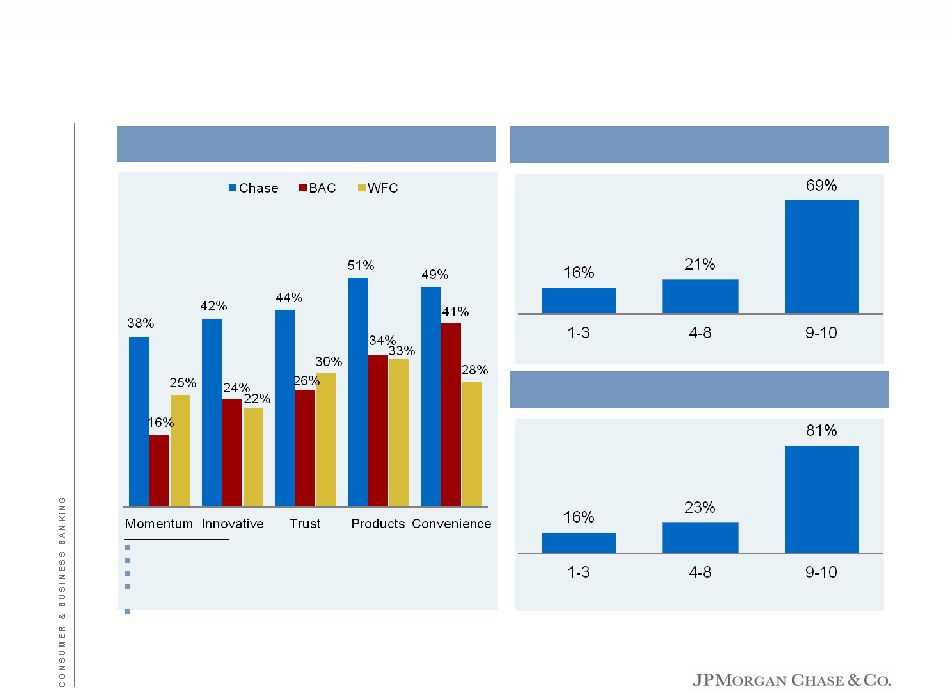

88% of the customers surveyed are satisfied with their relationship with Chase Highest client loyalty score – Ahead of WFC, USB, PNC and BAC Customer focus JPMorgan Chase overview 1 Greenwich Associates, 2011 2 2010 Chase Relationship Survey 3 Greenwich Associates, 2011 Twenty Two State Footprint Market Share Study 4 Client surveys conducted by the TS and WSS client service team 5 Survey of retail investors in the 10 largest European countries 6 Cogent Research Investor Brandscape, 2012 7 Cogent Advisor Touchpoints 2011: Trends and Best Practices for Creating a Connection with FAs 8 Chase Relationship Survey 9 Monthly Consumer Bank relationship survey (data from December 2011). Strongly agree equals a 9 or 10 on a 10-point scale 10 JD Power and Associates 2011 Credit Card Satisfaction Trends AM MB Card According to the JD Power overall satisfaction index rankings, Chase moved up to the 4 position, topping the industry average, ahead of WFC, USB, COF, C and BAC 10 Continuing focus on issue identification, elimination and prevention has yielded positive results with significant reduction in OCC/CFPB complaints CB TSS CBB Overall satisfaction with Chase (top 2-box scores) increased from 57% to 67% in 2011 8 For customers with top 2-box scores: 69% of households surveyed strongly agree that they are likely to use Chase to fulfill new financial need 9 81% of households surveyed strongly agree that they are likely to recommend Chase to others 9 Ranked #1 in client-oriented thinking by the 2012 Fund Brand 30 report 5 Significant increase in loyalty score – Ranked #7 in 2011, up from #21 in 2010 6 Ranked #1 for satisfaction with website, investment tools and resources for advisors 7 IB Selected as a Quality and Share Leader for 48 distinctions across 15 programs 1 , including Global Fixed Income, U.S. Large Corporate Finance and U.S. Equities Ranked #5 in the JD Power mortgage origination survey, up from #12 in 2010; topping the industry average and ahead of WFC, C and BAC Customer satisfaction for origination and servicing (top 2-box scores) of ~70% by the end of 2011 Customer complaint inventory declined by more than 60% since May 2011 Overall TS Service Delivery rated at near “best-in-class” levels with 89% of U.S. and 87% of EMEA clients rating service Excellent/Very Good 4 82% of WSS clients in 2011 indicated that they were satisfied with their current level of service WSS moved to #3 in 2011 from #7 in 2010 in Global Custodian Magazine’s 2011 Global Custody Survey 6 Customer satisfaction metrics 2 th 3 4 |

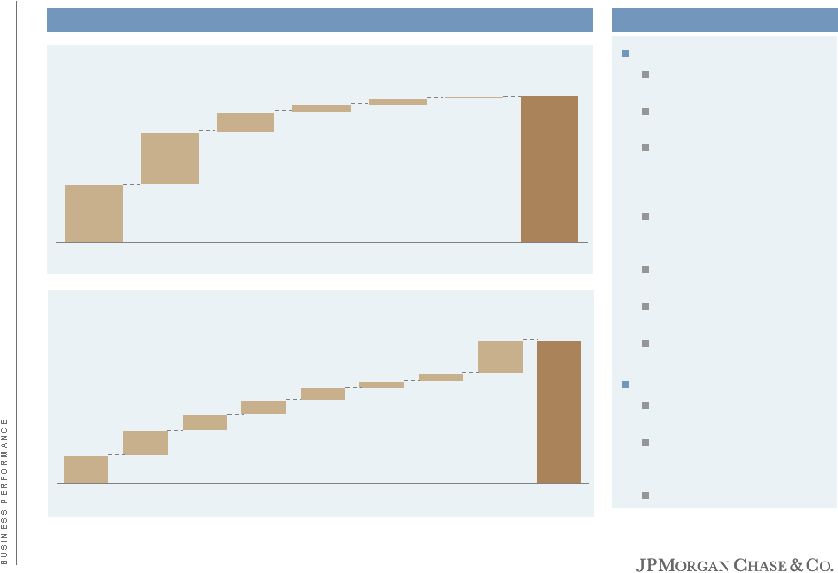

Major competitive advantage: leveraging the franchise JPMorgan Chase overview JPMorgan Chase & Co. 1 Calculated based on gross domestic IB revenue for SLF, M&A, Equity Underwriting, Bond Underwriting 75% of CB clients use Treasury Services products $2.3B of revenue in 2011 CBB clients use TS services ($215mm in 2011, up 10% YoY) Provide custodial and transfer agency services to AM Significant revenue generated from the CB client base Joint coverage of ~1,800 clients 25% of North American IB revenue in 2011 1 $1.4B of gross total IB revenue from CB clients in 2011 Robust client referral to and from AM 41 new PB clients through IB referrals Manage $90B of AUM for TSS clients $140mm in 2011 firmwide revenue IM products offered to CB clients $370mm in 2011 firmwide revenue Products offered to retail clients through the branch network $510mm in firmwide revenue ~45% of Chase branded cards sold through branches ~40% of Card Services revenue from new merchants is sourced through the branches ~20% of JPM IM U.S. Retail AUM comes from the branches >16mm branch transactions annually by CB clients Treasury & Securities Services Investment Bank Consumer & Business Banking Card Services & Auto Joint coverage of foreign multinational clients Presence in 40+ countries $200B+ of global exposure to GCB clients Mortgage Banking 6.1mm existing eligible Chase banking relationships with no mortgage relationship ~50% of retail mortgages originated through branches Referral source for Private Bank, Private Wealth Management and Chase Private Client CB clients accounting for 66% of total Global Commercial Card clients, driving nearly $15B in Card spend in 2011 Increased signings of new Paymentech accounts through branch referrals by 34% Sourced most new Middle Market Commercial Card customers through CB Generated >40% of Commercial Card revenue from wholesale clients 7 Leveraging the franchise Global Corporate Bank Commercial Bank Asset Management |

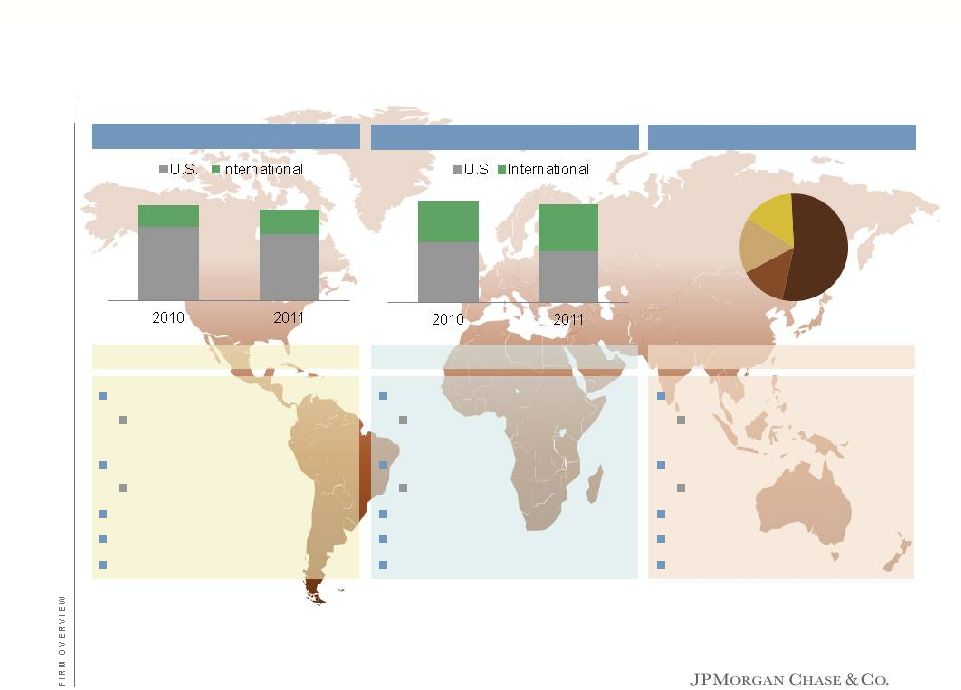

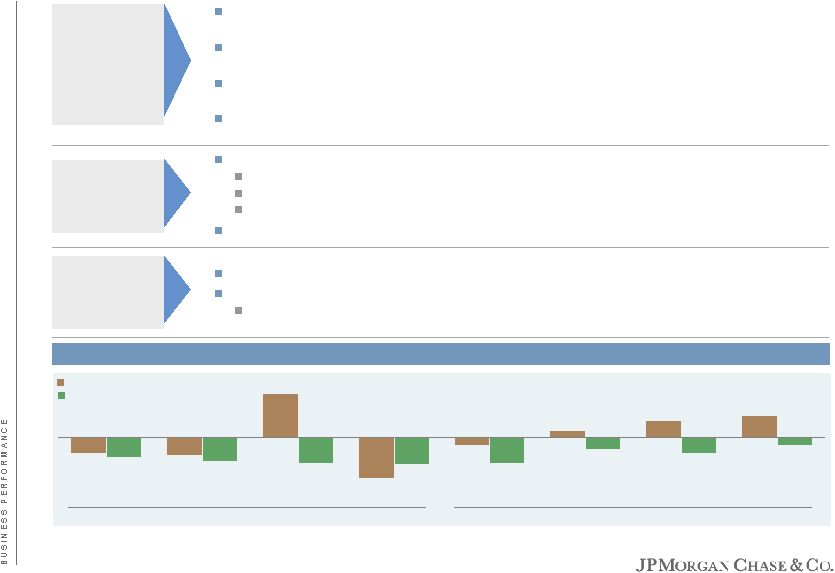

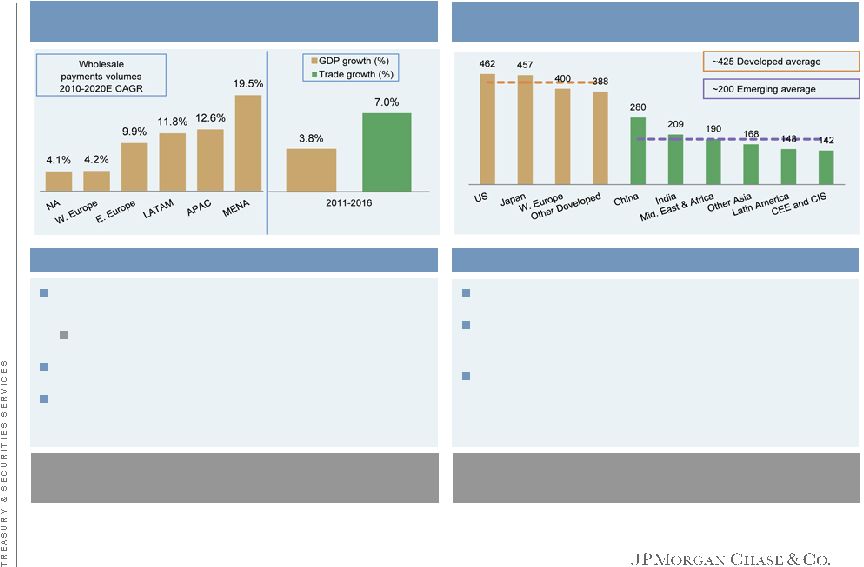

Global footprint and scorecard JPMorgan Chase overview LatAm/Caribbean (9%) 3 2011 revenue of $2.2B 2006 – 2011 CAGR: 11%; up 32% YoY Operate in 9 countries in the region 4 new offices opened in 2011 $5B in deposits 4 , down 15% YoY $25B in loans 5 , up 53% YoY $34B in AUM 2011 revenue of $6.0B 2006 – 2011 CAGR: 13%; down 2% YoY Operate in 16 countries in the region 2 new offices opened in 2011 $58B in deposits 4 , up 8% YoY $31B in loans 5 , up 51% YoY $105B in AUM 2011 revenue of $16.1B 2006 – 2011 CAGR: 7%; up 14% YoY Operate in 33 countries in the region 3 new offices opened in 2011 $169B in deposits 4 , up 18% YoY $37B in loans 5 , up 31% YoY $278B in AUM EMEA (64%) 3 Asia Pacific (24%) 3 22% 78% 26% 74% 41% 59% 48% 52% 1 On a managed basis 2 Primarily composed of CIO net gains 3 % of Wholesale revenue 4 Average deposits are based on the location from which the customer relationship is managed 5 End-of-period loans outstanding are based predominantly on the domicile of the borrower and exclude loans held-for-sale and loans carried at fair value Note: Wholesale international operations comprised of IB, AM, TSS, CB and CIO/Treasury. Totals may not sum due to rounding Wholesale revenue 1 – ($B) Firmwide revenue 1 – ($B) Int’l Wholesale revenue by LOB 1 8 $105 $100 $55 $53 Other 2 TSS IB AM 17% 54% 15% Total = $25B 14% |

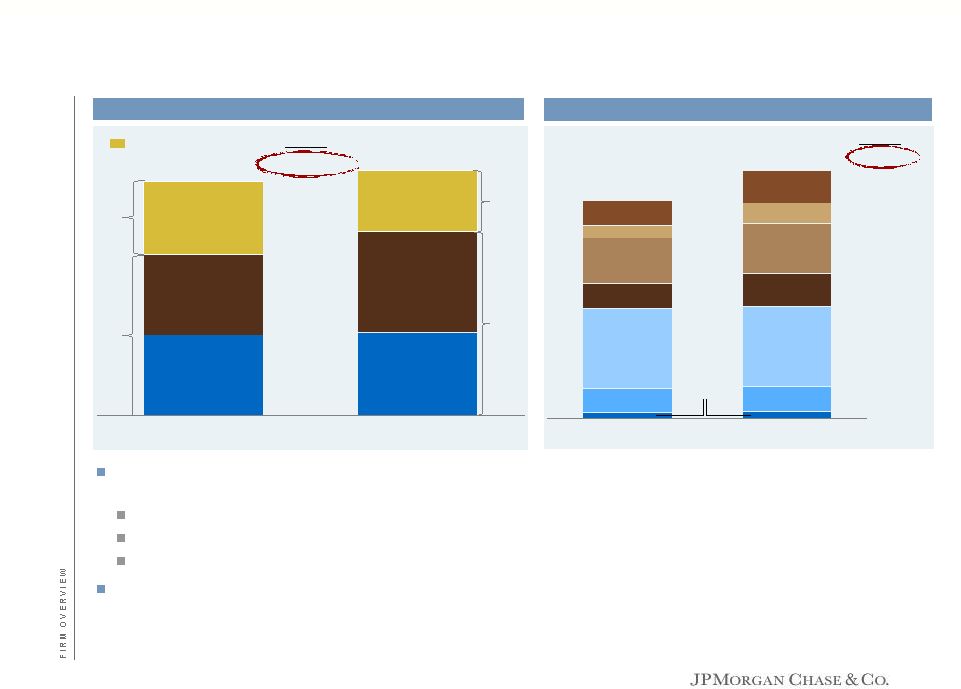

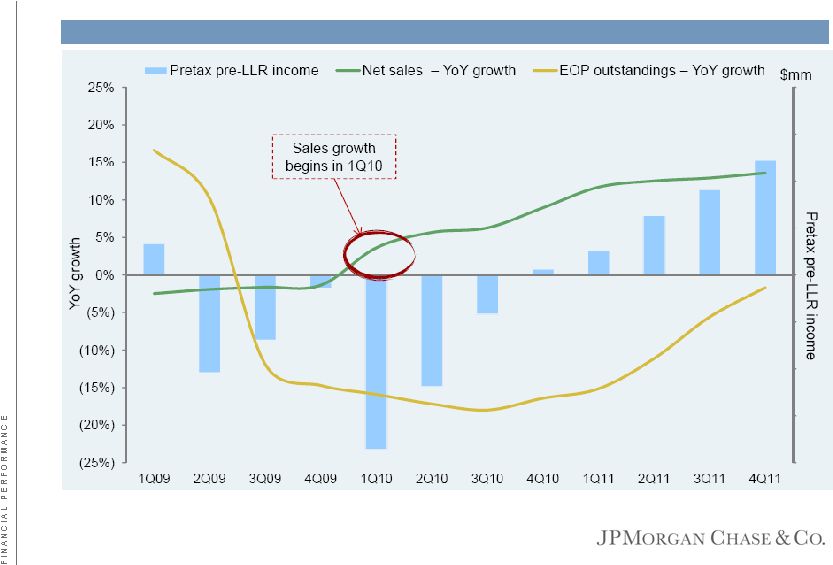

Loan growth JPMorgan Chase overview Total loans increased 4% YoY driven by core loan growth of 14% across all businesses, including Wholesale loan growth of 25% CB achieved six consecutive quarters of loan growth through the end of 2011; Middle Market loans up 17% YoY TSS trade loans up 73% Business Banking loans up 5%; 24% increase in new origination volume in 2011 Run-off portfolios decreased 16% YoY driven by runoff of Mortgage Banking loans Note: Wholesale includes IB, CB, TSS, AM and Corporate; Consumer includes CBB, MB and Card 1 Other includes Card run-off portfolio, including certain legacy WaMu loans, legacy balance transfer programs and terminated partner portfolios (e.g. Kohl’s ), and CBB run-off portfolio, including discontinued products 2 MB run-off portfolio includes WaMu purchased credit-impaired loans, discontinued products, and certain prime loans with estimated current LTVs greater than 80% as of January 2010 3 AM includes loans originated by AM that are held in Corporate and other loans held in Corporate Note: Totals may not sum due to rounding 2010 2011 $693 $724 (16)% 14% Growth Total loans: 4% Consumer Wholesale Run-off (MB and Other) 1,2 Consumer Wholesale Core $477 Core $543 $216 $180 2010 2011 $477 $543 Card MB CB CB IB IB TSS TSS AM 3 AM 3 MB Growth 14% Card 30% 58% 13% 25% 2% 3% 14% Core loans by line of business ($B) Run-off portfolios Run-off (MB and Other) 1,2 CBB 9 Total end-of-period loans ($B) |

Impact of our run-off portfolios: a simulation JPMorgan Chase overview Simulation assumes provision for credit losses equals net charge-offs; other reserve actions not simulated NII will decline as portfolios run off; reduction of higher yield loans puts pressure on firmwide NIM NII for run-off portfolios expected to decline by $1B +/- in 2012, including $500mm +/- related to MB However, runoff will benefit firmwide ROTCE as expense and credit losses also decline, and approximately $2B of capital per year could be liberated and redeployed, including $1B +/- related to MB Pro-forma impact on ROTCE 6 ($B) Comments 15.3% 16.0% 0.7% NI $19 $0.5 $20 TCE 7 124 (2.0) 122 8 10 2011 2012 2013 2014 MB $173 $152 $128 $110 Other 2 22 16 12 10 Total average loans $196 $167 $140 $120 Total run-off portfolios Net interest income $6.3 $5.1 $4.1 $3.2 Noninterest expense 2.0 1.6 1.3 1.1 NCOs 5.8 4.2 2.8 1.6 Net income 4 ($0.9) ($0.4) ($0.1) $0.3 Capital $12 $10 $8 $7 Net interest margin 3.2% 3.1% 2.9% 2.7% 5 5 5 1 3 Run-off portfolios simulation ($B) 1 2 3 4 5 6 MB run-off portfolio includes WaMu purchased credit-impaired loans, discontinued products, and certain prime loans with estimated current LTVs greater than 80% as of January 2010 Other includes Card run-off portfolio, including certain legacy WaMu loans, legacy balance transfer programs and terminated partner portfolios, and CBB run-off portfolio, including discontinued products Assumes provision for credit losses equals net charge-offs associated with NCI portfolio. Assumes no reserve actions associated with run-off PCI portfolio. All amounts presented in the simulated periods are estimates within a range of possible outcomes. Actual results could differ significantly from these estimates Assumes 38% tax rate Simulated results based on current run-off portfolios trends Run-off portfolios impact represents the incremental ROTCE impact of changes to net income and allocated capital in the first year of the simulation Average tangible common equity Adjusted for difference between 2011 actual and 2012 simulated amounts Note: Totals may not sum due to rounding 7 8 |

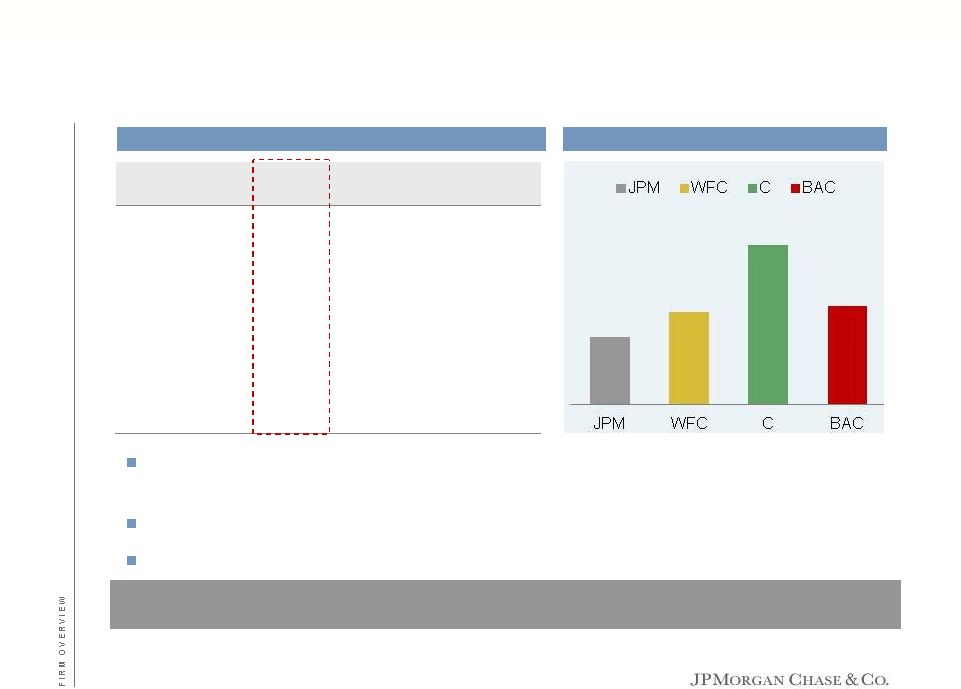

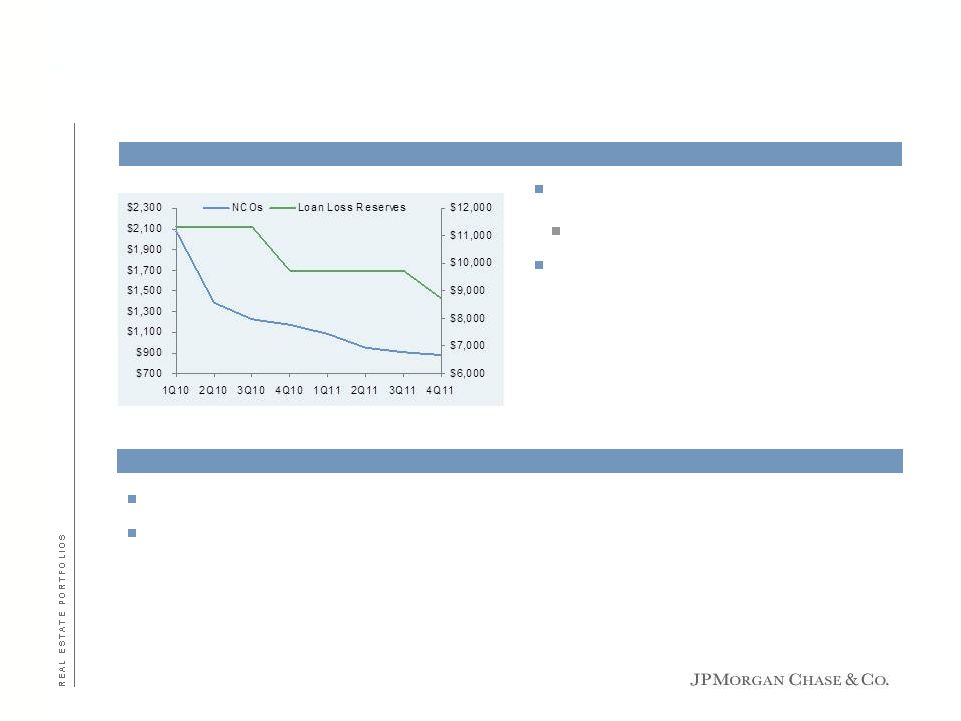

Expect reserve levels to adjust to normalized levels of ~$15B as underlying credit improves and we recognize the impact of certain portfolio runoff Credit quality: strengthened coverage and reserve position JPMorgan Chase overview The Firm’s net charge-offs and nonperforming loans are down 48% and 44% from peak levels, while loan loss reserves decreased 28% from peak and 13% since 2009 LLRs/NPLs ratio is 281%, up from 184% in 2009 1 LLRs/NCOs 2 coverage is 237%, up from 128% in 2009 3 0.6 1.0 0.6 0.4 1 Loan loss reserve includes $5.7B and $1.6B of PCI reserves in 2011 and 2009, respectively 2 Reflects 4Q11 NCOs annualized 3 Reflects 4Q09 NCOs annualized; excludes NCOs for securitized credit card receivables for which there was no associated LLR 1 11 JPM WFC C BAC EOP loans $723.7 $769.6 $647.2 $940.0 NCOs 12.2 11.3 20.0 20.8 NPLs 10.0 21.3 11.2 25.1 LLR 27.6 19.4 30.1 33.8 LLRs/NCOs 2 237% 183% 183% 208% Peer group credit statistics – 2011 ($B) YoY change in LLRs to change in NCOs |

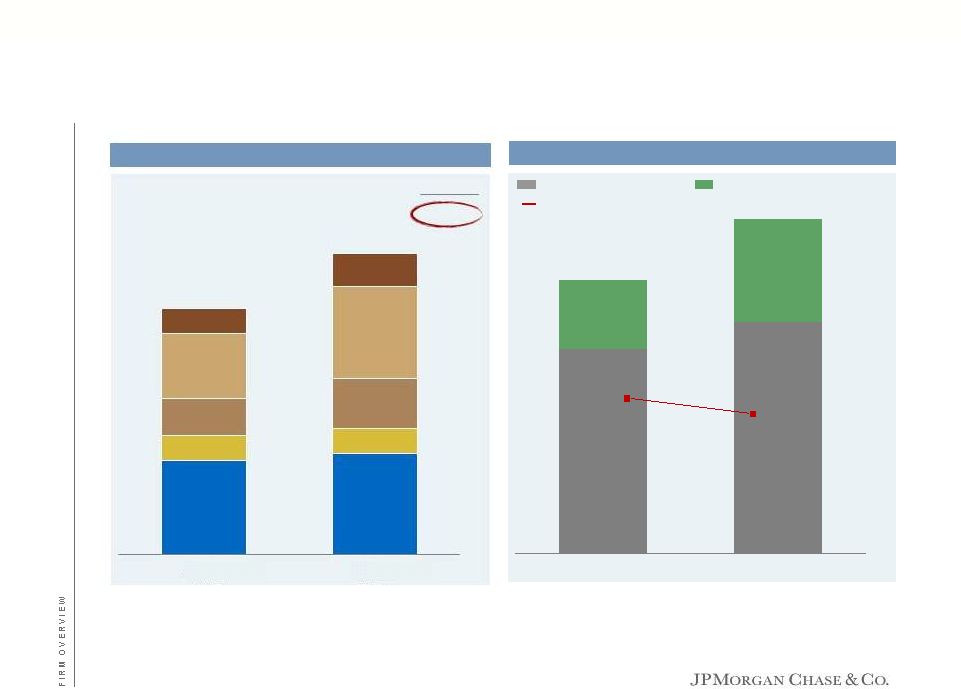

4Q10 4Q11 Deposit growth JPMorgan Chase overview 40% 39% 7% 0.50% 36% Interest-bearing deposits Noninterest-bearing deposits $895 $1,097 0.50% 0.43% $895 $1,097 1 Other includes IB, MB, Card and Corporate Note: Totals may not sum due to rounding Growth (3)% 23% Avg. yield 12 AM TSS CB Other¹ CBB AM TSS CB Other¹ CBB Avg. deposits by line of business ($B) Avg. interest-bearing vs. noninterest-bearing deposits ($B) 4Q10 4Q11 |

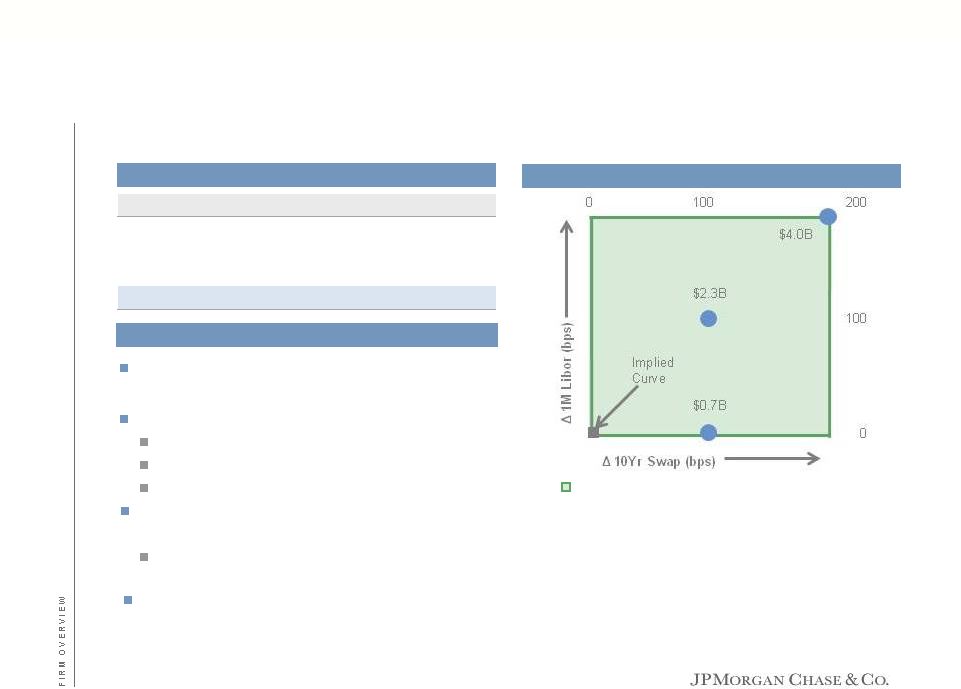

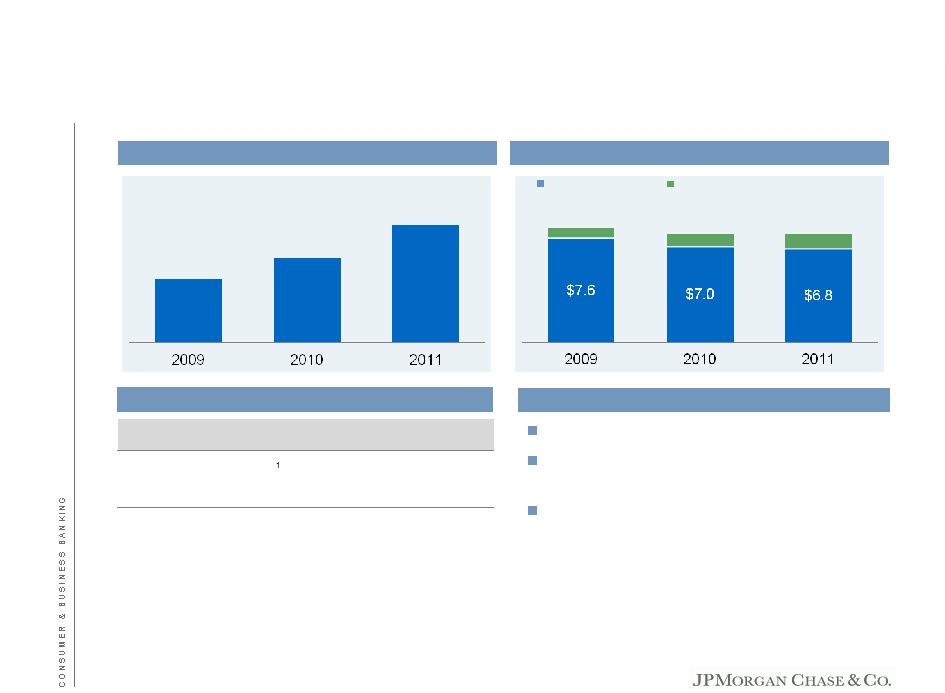

Net interest margin and net interest income rate sensitivity JPMorgan Chase overview Net interest income has been impacted by the runoff of higher yield loan portfolios and portfolio mix Net interest margin decreased by 32bps in 2011 due to Runoff Changes in portfolio mix Impact of lower rates Spread compression will negatively impact CBB net income by $400mm+/- Potential increases in NII relative to the implied curve 2010 2011 Net interest income $51.4 $48.2 Interest-earning assets 3.83% 3.51% Interest-bearing liabilities 0.84 0.86 Net interest margin (NIM %) 3.06% 2.74% 13 YoY net interest margin ($B) Comments Potential net interest income increases 1 Continued pressure on NIM in 2012 as market and mix conditions continue Portfolio runoff will negatively impact NII in REP by $500mm+/- 1 As of 12/31/2011. Reflects risk exposure to pretax NII of the Firm's non-market-based business activities (see 3Q11 form 10-Q disclosure for further discussion on interest rate exposure). Implied curve represents the market expectation of rates over the next 12 months |

Core net interest margin 1 JPMorgan Chase overview 1 See note 6 on slide 43 2 IB’s market-based activities are defined as total IB net interest income less net interest income earned on IB loans 3 Net interest income presented as an average 2009 quarter (i.e. total year divided by 4); all others are yearly rates Core NIM is a measure that is more comparable to the NIM of financial institutions focused primarily on loan and deposit-related activities Given mark-to-market and P&L geography of hedging in the IB, NIM is not a good indicator of IB profitability Core net interest income walk – 4Q11 ($B) Core net interest income Net interest income trend Avg. earning assets NII Yield Firm reported $1,808 $12 2.7% IB reported 1.5 Less IB loans 1.8 IB market-based activities $502 $2 1.4% Core $1,306 $11 3.2% 14 567 65 2 0.3 |

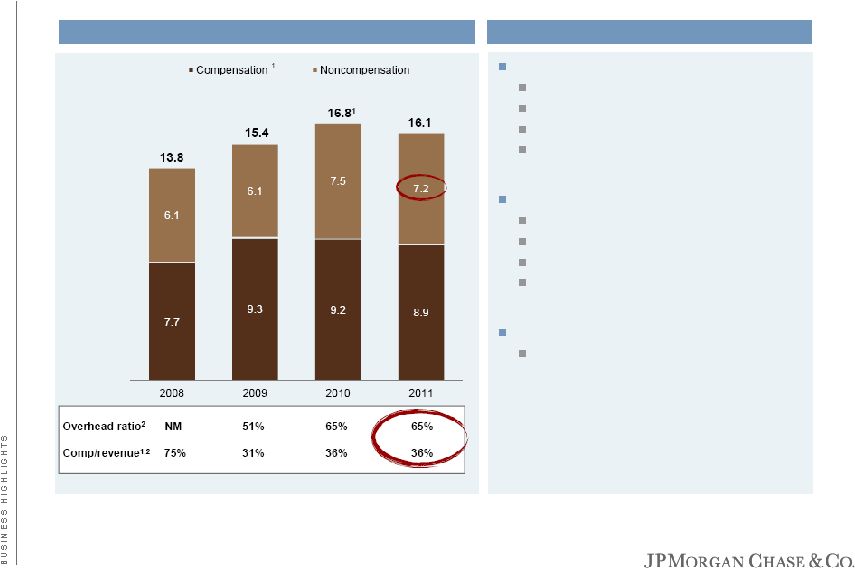

1 Excludes Investment Bank compensation expense, Corporate litigation expense, and foreclosure-related matters. Investment Bank compensation expense totaled $9.7B in FY2010 and $8.9B in FY2011. Corporate litigation expense totaled $5.7B in FY2010 and $3.2B in FY2011. Foreclosure-related matters totaled $350mm in FY2010 and $1.7B in FY2011 2 Specific transaction related noninterest expense, which is directly related to generating the associated revenue (e.g., storage and transportation costs) 3 Presented on a managed basis. See note 1 on page 43 Note: Totals may not sum due to rounding Firmwide expense has been trending higher JPMorgan Chase overview $45.4B $49.2B $960mm Mortgage servicing $640mm FDIC $600mm Card marketing $450mm Commodities 2 Significant Drivers Expect total adjusted firmwide noninterest expense to remain relatively flat in 2012 Moderating expense in growth initiatives Targeted branch build GCB build-out almost complete More efficiency in marketing expense Default-related expense likely to decline in 2H12 LOBs continue to focus on efficiencies $1.2B Other Headcount OH ratio 3 239,831 58% 260,157 63% 2010 2011 Primarily headcount growth CPC Branch build Business Banking – WaMu expansion CB expansion GCB International expansion AM banker build-out MB production 15 Adjusted firmwide noninterest expense 1 |

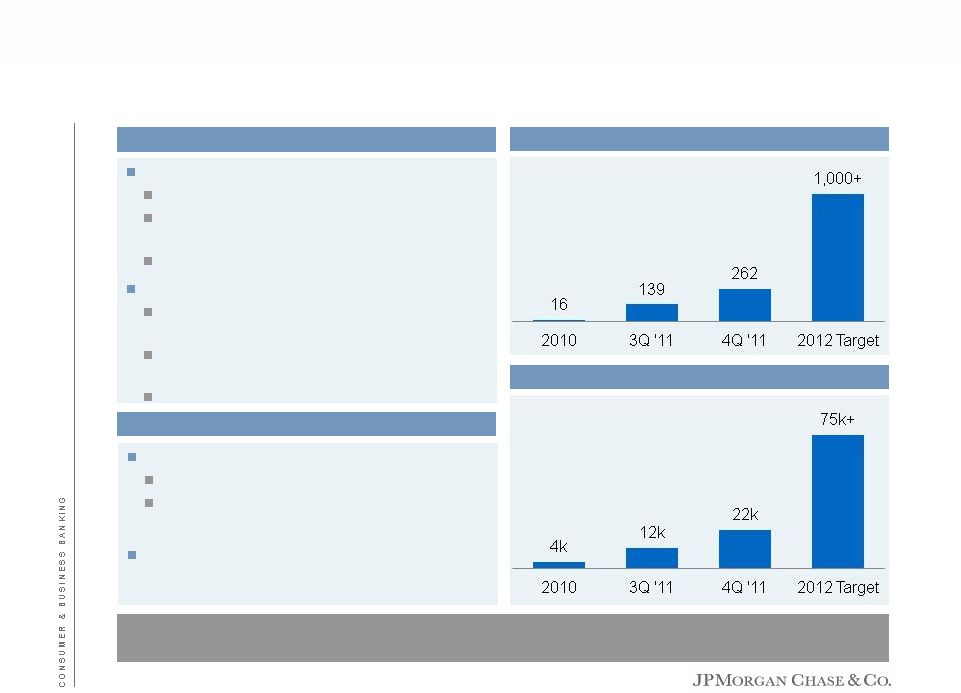

2011 expense and NI impact of cumulative spend from select investments ($mm, except where noted) Overview of select investments JPMorgan Chase overview Build out branches and product capabilities Uplift primarily from Markets, Credit and TS products ~525 new branches built since 2009 Avg. branch achieves payback & 30% ROE by year 8+/- 1,200 new RMs & business bankers hired since 2009 Significant growth opportunities in h-WaMu markets Build out int’l platform to facilitate clients’ regional strategies Successful launch of int’l platform in 2011; steady state 2014/15 Expand CB coverage into new markets Broke even in 2011; continue to add 200+ clients a year 262 CPC locations as of 2011; plan to add 750 in 2012 22K clients as of 2011; plan to reach 75K clients by 2012 ¹ Reflects NI contribution from 2002-2011 branch builds ² Excl. expense related to existing portfolios and litigation ³ Excl. the impact of deferred loan origination cost (FAS 91) 1 3 16 LOB/Investment 2011 Expense Comments ~$60 Middle Market expansion ~70 ~200 600 ~300 400 ~400 600 ~150 600 ~50 ~175 ~500 350 ~$1,900 NI impact of cumulative spend IB International Prime Brokerage $175 +/- IB/TSS International expansion/ Global Corporate Bank +/- CB 450 +/- CBB Branch builds 2011 expense associated with 2009-2011 branch builds +/- Business Banking 2011 expense associated with 2009-2011 new hires +/- Chase Private Client 600 +/- AM PB banker/ IM expansion +/- MB Mortgage capacity & productivity 2 450 +/- Card Incremental customer acquisition marketing +/- 317 PB bankers hired since 2010; 729 IM sales, investors & support hires since 2009 (expense incl tech & other support) Expect to reach target net income by 2015 Added 700 loan officers in 2011; plan to add 1,000 in 2012 to grow retail capacity Improve productivity through origination & servicing investments Total spend in 2011 expected to generate 9mm+/- accounts and $45B+/- in sales volume in 2012 Run-rate NI by year 3 |

Agenda Page 17 Specific risk questions from investors 17 Firmwide capital 21 Key firmwide themes 29 Appendix 31 |

Lending exposure includes both funded loans and undrawn commitments Lending exposure ~72% to corporates AFS securities exposure – 73% government guaranteed Trading exposure ~ 42% to sovereigns Includes $2.4B of debt and equity securities Predominantly client-driven net derivative receivables of $15.3B, offset by collateral of $6.8B (98%+ held in cash) Credit derivatives counterparties primarily outside Euro 5 and are investment-grade or well-supported by collateral arrangements Mark-to-market of large counterparty gross long and short positions largely offset and are all collateralized daily ~ 79% of portfolio hedges are against sovereign exposure Substantially all hedges are with investment grade counterparties outside the Euro 5 and are collateralized Non-sovereign net exposure – 82% to corporate clients and remaining 18% to the banking sector European exposure Specific risk questions from investors As of February 16, 2012 ($B) 18 Exposure 1 Securities & Trading Lending AFS Trading Derivative collateral Portfolio hedging Net exposure Spain $3.4 $0. 8 $5. 3 ($3.3) ($0.5) $5.7 Sovereign - 0.5 (0.3) - (0.1 ) 0.1 Non -sovereign 3.4 0.3 5.6 (3.3 ) (0.4) 5.6 Italy 3.4 0.1 10.3 (2.2 ) ( 4.3) 7.3 Sovereign - - 7.7 (1.1 ) (3.6) 3.0 Non -sovereign 3.4 0.1 2. 6 (1.1 ) (0.7 ) 4.3 Other (Ireland, Portugal & Greece) 1.4 0. 6 2.3 (1.3) (1.0 ) 2.0 Sovereign - 0.6 0.1 - ( 0.8) (0.1) Non-sovereign 1.4 - 2.2 (1.3) (0.2 ) 2.1 Total firmwide exposure $8.2 $1.5 $17.9 ($6 .8) ($5.8 ) $15.0 1 Exposure is a risk management view. Lending is net of liquid collateral. Trading includes net inventory, derivative netting under legally enforceable trading agreements, net CDS underlying exposure from market-making flows, unsecured net derivative receivables and under collateralized securities financing counterparty exposure |

Department of Justice and Attorneys General mortgage settlement summary Specific risk questions from investors $25B global settlement announced between the five major servicers and the Federal Government including the Department of Justice, Department of Housing and Urban Development, and the State Attorneys General For Chase the settlement amount will be ~$5.3B and will consist of ~$1.1B in cash payments ~$0.5B toward a refinance program – Will offer interest rate reductions for certain homeowners with Chase-owned mortgages Up to ~$3.7B of additional relief for homeowners – Menu of options from which the bank can choose to assist homeowners, including modifications with first and second lien principal reductions New servicing standards, which establish a new level of transparency and clarity for servicer activities Limits the Firm’s liability related to MERS-related conduct, such as recording of assignments and standing in foreclosures Only New York, Delaware and Massachusetts may maintain suits for MERS-related conduct. The settlement limits monetary remedies those states can seek against Chase, and precludes them from seeking to vacate past foreclosures for MERS-related conduct Given our current reserve position, the settlement is not expected to have a material impact on earnings 19 |

Private label securitization Specific risk questions from investors 1 The Firm believes that WaMu bank-related repurchase liabilities are the responsibility of the FDIC (the FDIC disagrees) and any securities liabilities reside with the WaMu subsidiaries 2 Excludes class action deals with standing defects, deals where the Firm was sued solely as an underwriter (and was not an issuer), monoline claims and trustee claims 3 Certain analysts include estimates for private label litigation in their private label repurchase exposure estimates. Certain analysts exclude WaMu related liabilities from JPM repurchase estimates Original balances in litigation for Chase (excl. WaMu) 1 of ~$50B 2 A group of investors claiming to have a quorum in trusts with an original principal balance (excl. WaMu) of ~$175B asked various trustees to, among other things, investigate servicing and repurchase claims Both securities and repurchase claims are likely to be litigated Substantial impediments to repurchase and servicing claims Trustees generally do not act unless instructed by a quorum and indemnified Many loans were originated or are serviced by others WaMu repurchase liabilities reside with the FDIC 1 We intend to honor our obligations, but claims are fact intensive, generally requiring loan-by-loan analysis – There is no repurchase absent proof that a breach “materially and adversely” affected value of loan Securities litigation claimants also face significant hurdles There is significant overlap between repurchase and securities exposure: we do not intend to pay twice for the same exposure Median analyst estimate of exposure across the entire private label securitization portfolio, including balances not in litigation, is $6.5B 3 Litigation could take years, but we have built significant litigation reserves 20 |

Agenda Page 21 Firmwide capital 21 Specific risk questions from investors 17 Key firmwide themes 29 Appendix 31 |

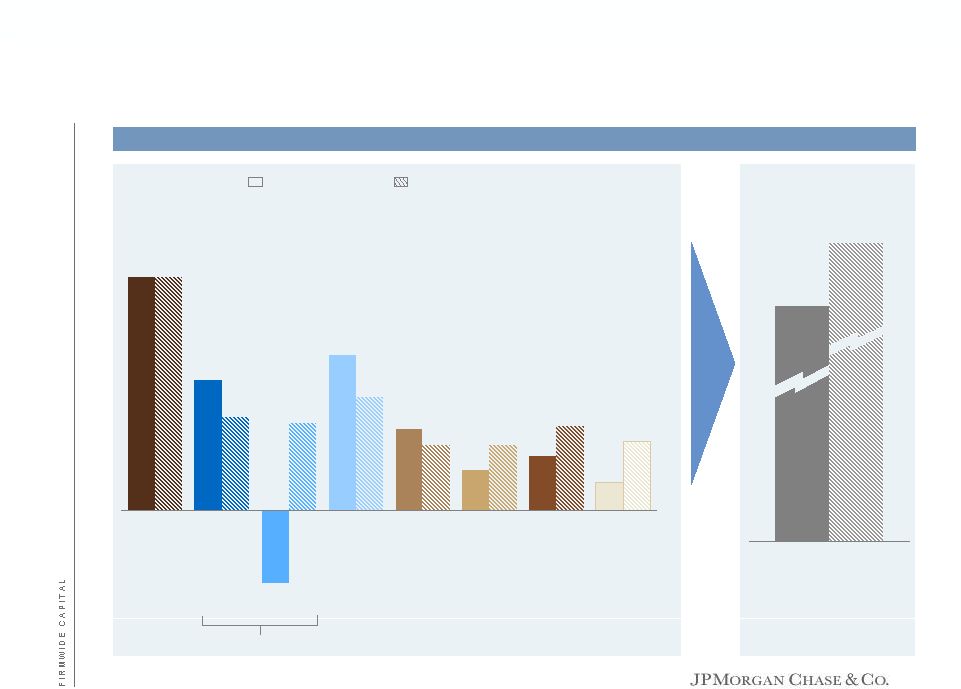

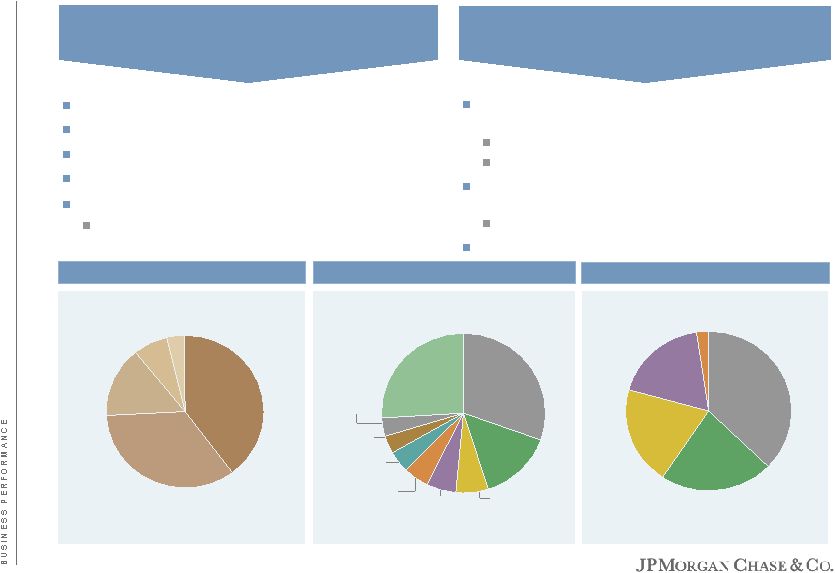

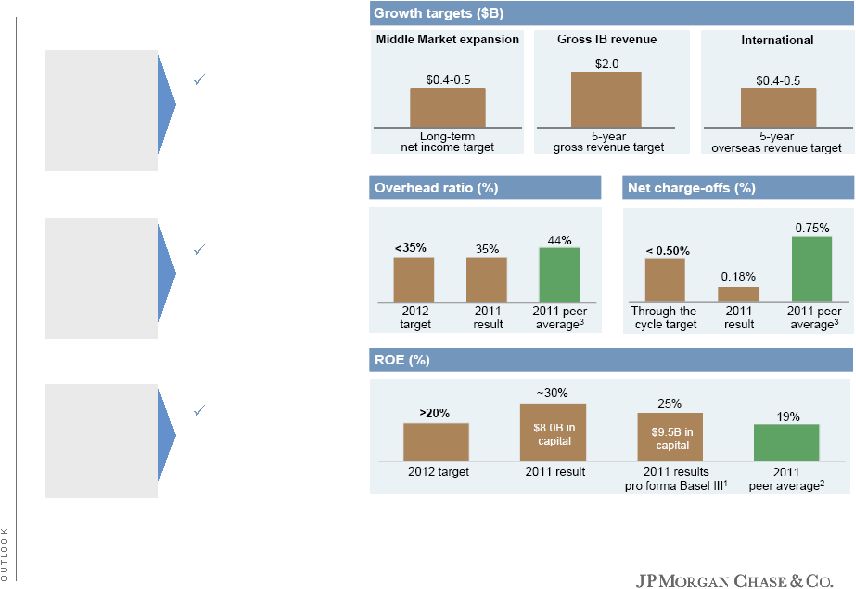

1 TSS and AM pretax margin targets remain unchanged at 35% +/- through the cycle 2 IRR of 20% +/- 3 1/1/12 for illustrative purposes only 4 Reflects capital held against Corporate goodwill Common equity and target ROEs ($B) Common equity and performance targets Firmwide capital $0.5-$1B +/- of net income 22 $0.5-$1B +/- of net income 2011 1/1/2012 Investment Bank $40.0 $40.0 17% 17% +/- 9.5% +/- Consumer & Business Banking 9.5 9.0 40 30 +/- 8.5 +/- Mortgage Banking 15.5 17.5 (14) 15 +/- 8.5 +/- Card Services & Auto 16.0 16.5 28 20 +/- 8.5 +/- Commercial Banking 8.0 9.5 30 20 + 8.5 +/- Treasury & Securities Svcs. 1 7.0 7.5 17 25 +/- 9.0 +/- Asset Management 1 6.5 7.0 25 35 +/- 8.5 +/- Private Equity 3.6 4.8 11 20 +/- 2 9.5 +/- Corporate (CIO/Treasury/Corp) 13.1 18.3 3 Subtotal $119.2 $130.1 Unallocated Capital 3 $14.5 $3.6 Corporate Goodwill 4 42.1 42.1 Total Firm ROE $175.8 $175.8 Total Firm ROTCE Common equity 2011 ROE Targets Through-the- cycle ROE Basel III Tier 1 common 11% 15% 9.5% +/- 16% +/- |

$6.8 $3.8 ($2.1) $4.5 $2.4 $1.2 $1.6 $0.8 LOB performance at targets Firmwide capital $24+/- 1 Net income projections based on performance target and steady state assumptions $19.0 2011 Net income Net income at performance targets 1 IB CBB MB Card CB TSS AM Corporate/PE RFS JPM 23 Net income by LOB ($B) |

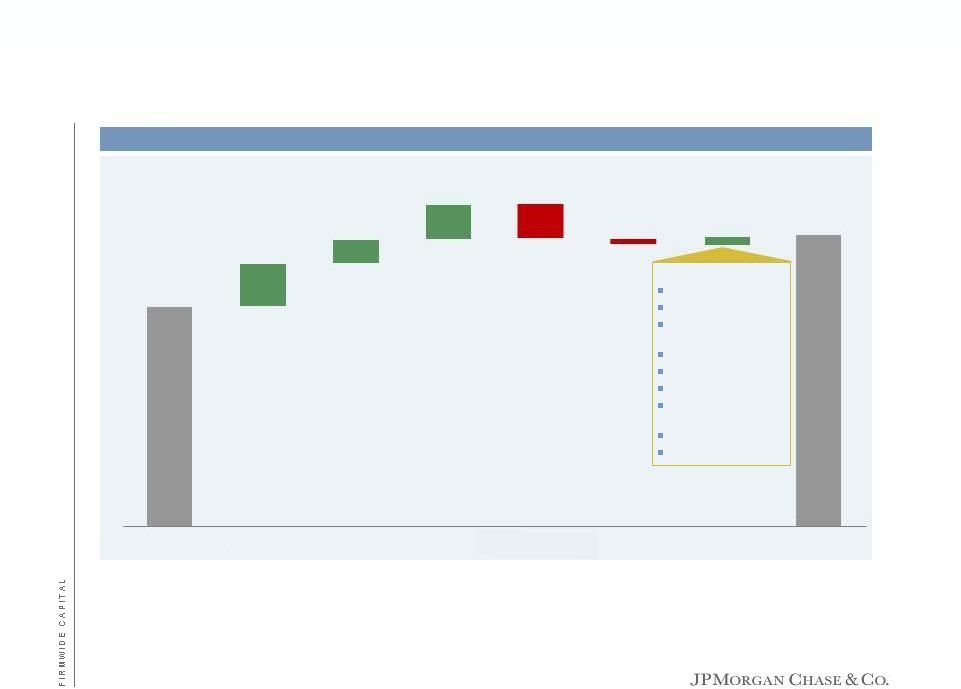

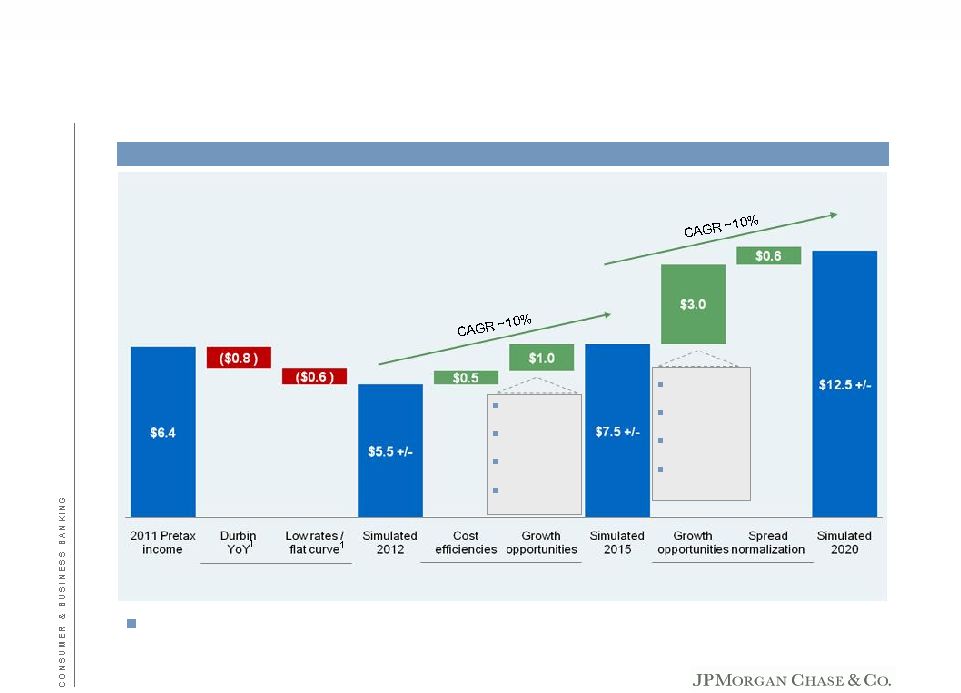

1 Includes servicing and default related costs, foreclosed asset expense, repurchase losses, MSR valuation adjustments offset by normalized production revenue, and normalized repurchases; excludes elevated credit costs 2 Corporate litigation expense for 2011 (after-tax) 3 Based on disclosed through-the-cycle net charge-off rates for IB, Card (excl. WaMu and Commercial Card), CB, Home Equity and Prime excl. Option ARM; applied to 2011 average retained loan balances. Card through-the-cycle charge-off rate applied to Card average balances, excl. WaMu and Commercial Card . Also excludes MB WaMu PCI portfolio and discontinued products 4 Loan loss reserve release for FY 2011 5 Durbin Amendment annualized 2012 net income impact of $600mm+/- less the impact of Durbin included in FY11 results. Excludes the potential incremental impact from Dodd Frank on the IB Note: Assumes tax rate of 38% Earnings walk Firmwide capital 24 Net income build ($B) FY11 NI excl. DVA Mortgage - related Matters 1 Corporate Litigation 2 Normalization of NCOs 3 Reserve Release 4 Durbin 5 Growth NI at performance targets $18.1 $24+/- $3.5 $2.0 ($2.9) ($0.5) $0.8+/- $3.0 Growth initiatives CPC Branch build Business Banking - WaMu expansion CB expansion Commodities GCB International expansion AM banker build-out MB production |

Capital planning Firmwide capital Submitted Capital Plan on January 9, 2012 Follow-up meetings with Fed currently under way Expect response by March 15, 2012 Severe Fed stress scenario, evaluated under Basel I GDP decline of 8% Peak unemployment of 13% HPI decline of 20% from current level Equity markets decline of 52% from 3Q11 Severe global market shock, including specific European stresses Baseline evaluated under Basel III Capital Plan expected to show steady progress toward the fully phased in requirement of Basel III Tier 1 common ratio of 9.5% by 2019 Hierarchy of capital deployment, after dividends Organic growth Acquisitions Share repurchases Increase dividend to 30% payout ratio of normalized earnings over time 25 Dividends Capital hierarchy CCAR |

Fed CCAR requires share repurchases to be consistent with baseline distributions Assuming analyst estimated dividends, and share repurchases generally consistent with 2011, Basel I Tier 1 common remains at ~8% in 2012 and 2013 Results in over $35B of excess capital above the 5% minimum Indicative stress analysis – Based on analyst estimates Firmwide capital Key assumptions Analyst estimates for net income and dividends Actual year end 2011 Basel I RWA held constant Repurchases to neutralize employee issuance ($B) 2011 2012 2013 Base net income $19.0 $18.2 $20.3 Stressed net income 1.5 12.8 Actual Basel I RWA ($T) $1.22 1.22 1.22 10.1% 11.1% 8.8% 9.3% 2011 2012 2013 12.2% Basel I Tier 1 common Stressed Basel I Tier 1 common 5% 2012-2013 net income reflects the average of 8 analyst estimates. Stressed net income reflects analyst Baseline NI multiplied by (JPM Fed Stress NI/JPM Baseline NI). 2012 and 2013 RWA levels held constant from year end 2011 Analyses assume analyst average dividend/share of $1.22 in 2012 and $1.51 in 2013 Stressed Basel I Tier 1 common remains well above 5% threshold 26 Key assumptions 1 Indicative stressed capital 2 Comments on stress results 1 2 Note: Fed stress case assumes backward looking market stress, which changes pro-forma Tier 1 common at the end of 2011. 2011 stressed Tier 1 common is used as a starting point for the stressed case in this analysis See note 3 on slide 43 for discussion of Basel estimates |

Basel III RWA and Tier 1 common Firmwide capital 1 Basel III market risk RWA reflects the new capital requirements related to trading assets and securitizations, which include incremental capital requirements for stress VaR, correlation trading, and re-securitization positions 2 Primarily reflects securitization-related exposures required to be risk weighted at 1250% based on Basel III rules 3 Capital charge for potential mark-to-market losses associated with a deterioration in the credit worthiness of a counterparty 4 Applied to MSR, DTA, and investments in unconsolidated financial institutions 5 Other includes Basel I to II transition, reclassification of trading book positions, and counterparty credit Note: Analysis reflects current interpretation of Basel III guidelines and balance sheet assumptions See note 3 on slide 43 for discussion of Basel estimates 2011 Basel I Tier 1 common $123 AOCI for AFS securities; pension and other postretirement plans 0.9 Deduction for net defined benefit pension asset (1.4) Other (0.5) Basel I to Basel III incremental Tier 1 common (1.0) Estimated Basel III Tier 1 common $122 2011 RWA Basel I $1.22 Market risk impact 1 80 Risk weight 50/50 deductions at 1250% 2 80 CVA 3 65 250% risk weight 4 35 Other 5 65 Basel I to Basel III incremental RWA ($B) $325 Estimated RWA Basel III $1.55 2012 2013 Estimated beginning balance $1.55 $1.48 Data / Model enhancement (30) (30) Portfolio runoff (45) (35) BAU portfolio changes 10 20 Reduction in RWA ($B) (65) (45) Estimated ending balance $1.48 $1.44 27 Basel I to Basel III incremental RWA ($T) Potential Basel III RWA reductions ($T) Basel I to Basel III capital reconciliation ($B) |

Baseline scenarios – Alternative Basel III trajectories Firmwide capital 1 2012-2013 net income reflects the average of 8 analyst estimates 2 Net of preferred dividends of $629mm, and includes estimated impact of employee issuance. The Firm expects to utilize its repurchase capacity to, at a minimum, essentially repurchase the same amount of shares that it issues for employee stock-based incentive awards 3 Reported estimates 4 Achieve a Tier 1 common ratio of 9.5% by the end of 2018 5 Achieve a Tier 1 common ratio of 9.5% by the end of 2013 Note: See note 3 on slide 43 for discussion of Basel estimates 3 3 2011 2012E 2013E Net income¹ $19.0 $18.2 $20.3 Potential RWA ($T) $1.55 $1.48 $1.44 Tier 1 common - pre-capital distribution 2 $122 $141 $163 Tier 1 common ratio - pre-capital distribution 2 7.9% 9.5% 11.3% 28 Capital adequacy – Based on analyst estimates ($B) Straight line 4 Accelerated 5 2012E 2013E Tier 1 common ratio target 2 8.1% 8.3% Annual capital distribution capacity 2 $21 $22 2012E 2013E Tier 1 common ratio target 2 8.7% 9.5% Annual capital distribution capacity 2 $13 $14 |

Agenda Page 29 Key firmwide themes 29 Specific risk questions from investors 17 Firmwide capital 21 Appendix 31 |

Key firmwide themes Consistent focus on customer experience and innovation Continued focus on cross-LOB opportunities GCB at the core of IB/TSS/CB collaboration Organizing Consumer businesses Positioning LOBs for continued growth in market share Significant opportunity for net income growth Enhancing our ongoing focus on expense discipline Adapting to the new regulatory environment and capital rules Fortress balance sheet affords us the opportunity to Serve as a source of strength for our clients Continue to invest in organic growth Return excess capital to our shareholders 30 |

Agenda Page 31 Appendix 31 Specific risk questions from investors 17 Firmwide capital 21 Key firmwide themes 29 |

Managed financial results 2009 2010 2011 Investment Bank $6,899 $6,639 $6,789 Retail Financial Services (335) 1,728 1,678 Card Services (1,793) 2,872 4,544 Commercial Banking 1,271 2,084 2,367 Treasury & Securities Services 1,226 1,079 1,204 Asset Management 1,430 1,710 1,592 Corporate/Private Equity 3,030 1,258 802 Total firm net income $11,728 $17,370 $18,976 Firmwide results ($mm) Net income by lines of business ($mm) 1 See note 1 on slide 43 2 Net income used to calculate the ratios for 2009 excludes the one-time, non-cash negative adjustment of $1.1B resulting from the repayment of TARP preferred capital, which is a non-GAAP financial measure. Including this, ROE was 6% 3 See note 4 on slide 43 32 2009 2010 2011 Revenue (FTE) 1 $108,647 $104,842 $ 99,767 Credit Costs 1 38,458 16,639 7,574 Expense 52,352 61,196 62,911 Reported net income $11,728 $17,370 $ 18,976 Reported EPS $2.2 6 $3.96 $4.48 ROE 2 7% 10% 11% ROTCE 2,3 11 15 15 |

Investment Bank Leadership positions Global IB Fee market leader, #1 ranking for the past three years 5 Ranked #1 in disclosed 2011 Markets revenue among the top 10 competitors, both including and excluding DVA, up from #2 in 2010 Selected by Greenwich Associates as a Quality and Share Leader for 48 distinctions across 15 programs, including Global Fixed Income, U.S. Large Corporate Finance and U.S. Equities, 2011 Named U.S. Municipal Bond House of the Year by IFR, 2011 Ranked #1 2011 Overall, Risk’s Institutional Investor rankings $mm 2009 2010 2011 Revenue $28,109 $26,217 $26,274 IB Fees 7,169 6,186 5,859 Fixed Income Markets 17,564 15,025 15,337 Equity Markets 4,393 4,763 4,832 Credit Portfolio (1,017) 243 246 Expense 15,401 17,265 16,116 Credit Costs 2,279 (1,200) (286) Net Income $6,899 $6,639 $6,789 Key Statistics ($B) Overhead Ratio 55% 66% 61% Comp/Revenue 1 33 37 34 EOP Loans $49.1 $56.9 $71.1 Allow. for Loan Losses 3.8 1.9 1.4 Net Charge-off Rate 3.04% 1.35% 0.28% ALL / EOP Loans 2 8.25 3.51 2.11 ROE 3 21 17 17 VAR ($mm) 4 $164 $87 $76 EOP Equity 33.0 40.0 40.0 33 The compensation expense as a percentage of total net revenue ratio includes the impact of the U.K. Bank Payroll Tax on certain compensation awarded from December 9, 2009 to April 5, 2010 to relevant banking employees. For comparability to prior periods, IB excludes the impact of the U.K. Bank Payroll Tax expense, which results in a compensation expense as a percentage of total net revenue for 2010 of 35%, which is a non-GAAP financial measure Loans held-for-sale and loans at fair value were excluded when calculating the loan loss coverage ratio and net charge-off rate Calculated based on average equity Average Trading and Credit portfolio VAR at 95% confidence level Dealogic based on revenue 1 2 3 4 5 |

Retail Financial Services $mm 34 % % % % % % 1 Calculated based on average equity; average equity for 2011, 2010 and 2009 was $25.0B $24.6B, and $22.5B, respectively 2 Calculated based on average equity; average equity for 2011, 2010 and 2009 was $14.5B, $14.9B, and $12.7B, respectively 2009 2010 2011 Net Interest Income $18,383 $17,220 $16,133 Noninterest Income 11,414 11,227 10,405 Revenue 29,797 28,447 26,538 Expense 15,512 16,483 19,458 Pre-Provision Pretax $14,285 $11,964 $7,080 Credit Costs 14,754 8,919 3,999 Net Income ($335) $1,728 $1,678 EOP Equity ($B) $22 $25 $25 ROE 1 (1) 7 7 Memo: RFS Net income excl. Real Estate Portfolios $5,114 $4,221 $1,984 ROE excl. Real Estate Portfolios 40 28 14 |

Retail Financial Services Consumer & Business Banking $mm Leadership positions Attractive footprint Tri-state Midwest California Top deposit shares in #1 New York #1 Chicago #1 Phoenix #1 Dallas/Ft. Worth #1 Houston Northwest Florida Southwest # 1 Columbus, OH #2 Seattle #3 Los Angeles #3 San Francisco #3 Miami 2009 2010 2011 Net Interest Income $10,864 $10,884 $10,809 Noninterest Income 7,204 6,844 7,201 Revenue $18,068 $17,728 $18,010 Expense 10,421 10,717 11,202 Pre-Provision Pretax $7,647 $7,011 $6,808 Credit Costs 1,176 630 419 Net Income $3,915 $3,652 $3,816 Key Drivers ($B) Average Total Deposits $345.0 $340.8 $360.7 Deposit Margin 2.92% 3.00% 2.82% Checking Accounts (mm) 25.7 27.3 26.6 # of Branches 5,154 5,268 5,508 Business Banking Originations $2.3 $4.7 $5.8 Client Investment Assets $120.5 $133.1 $137.9 # of Active Mobile Customers (mm) 1.2 5.3 8.4 35 |

Retail Financial Services Mortgage Production and Servicing Leadership positions #3 in Mortgage Originations with 11.5% market share² #3 in Mortgage Servicing with 11.4% market share² $mm 1 Headcount for total Mortgage Banking 2 Source: Inside Mortgage Finance, 4Q11 2009 2010 2011 Production Production-related Revenue excl. Repurchase Losses $3,194 $4,309 $4,235 Production Expense 1,575 1,613 1,895 Income excl. repurchase losses $1,619 $2,696 $2,340 Repurchase Losses (1,612) (2,912) (1,347) Income/(loss) before income tax expense/(benefit) $7 ($216) $993 Servicing Servicing-related Revenue $5,182 $5,008 $4,524 MSR Asset Amoritization (3,279) (2,384) (1,904) Servicing Expense 1,684 2,584 4,845 Income/(loss), excl. MSR risk management 219 40 (2,225) MSR Risk Management 1,724 1,151 (1,572) Income/(loss) before income tax expense/(benefit) $1,943 $1,191 ($3,797) Net income/(loss) $1,199 $569 ($1,832) Key Drivers ($B) Mortgage Loan Originations $150.7 $155.6 $145.6 Retail Channel Originations 53.9 68.8 87.2 Mortgage Application Volume 206.6 214.8 204.7 3rd Party Mtg Loans Svc'd (EOP) 1,082.1 967.5 902.2 Headcount 1 32,393 39,440 49,189 36 |

2009 2010 2011 Revenue $6,520 $5,547 $4,592 Expense 1,847 1,627 1,521 Pre-Provision Pretax 4,673 3,920 3,071 Net Charge-Offs 8,343 6,450 3,805 Change in Allowance 5,220 1,781 (230) Credit Costs 13,563 8,231 3,575 Net Income ($5,449) ($2,493) ($306) Memo: ALL/ EOP Loans 1 6.55% 6.47% 6.58% Key Drivers 1 ($B) Average Home Equity Loans Owned 2 $136.0 $120.3 $106.4 Average Mortgage Loans Owned 2 133.7 117.6 102.8 Retail Financial Services Real Estate Portfolios Excludes the impact of purchased credit-impaired loans acquired as part of the WaMu transaction. An allowance for loan losses of $5.7B, $4.9B and $1.6B was recorded for these loans at year end 2011, 2010 and 2009, respectively Includes purchased credit-impaired loans acquired as part of the WaMu transaction 37 $mm 1 2 |

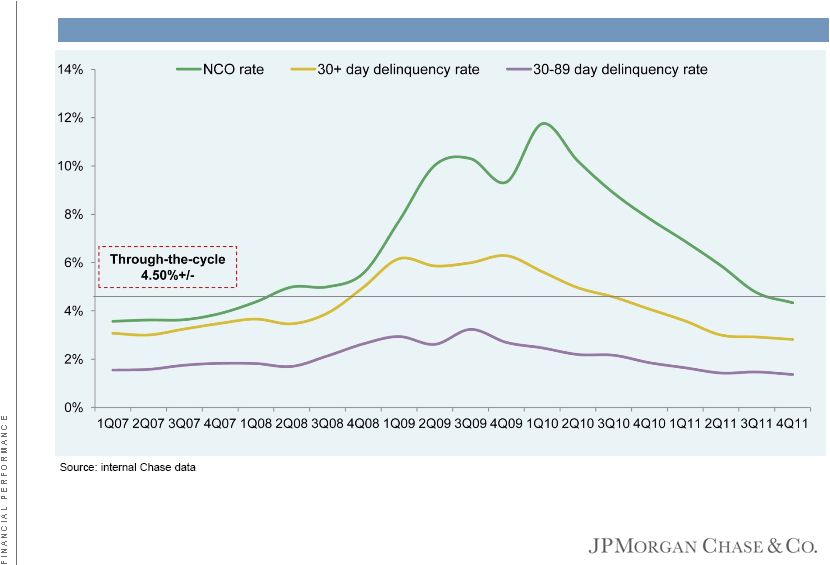

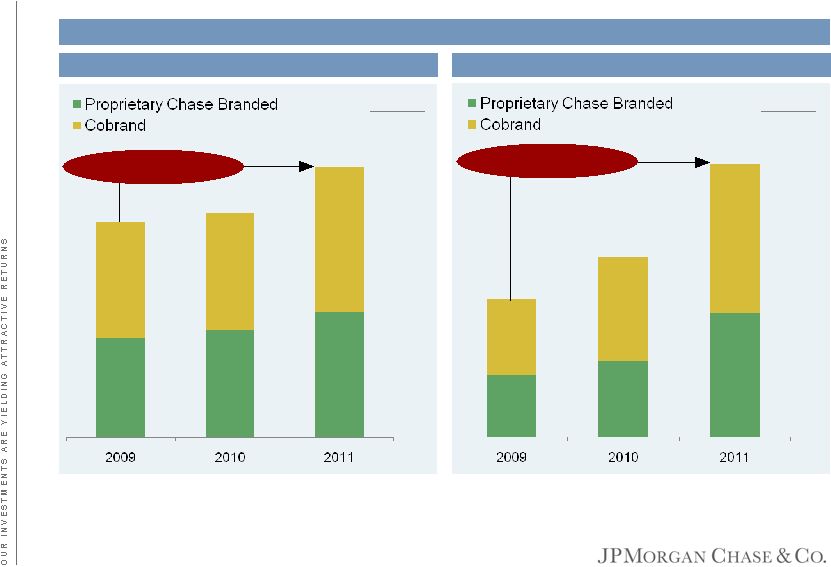

Card Services & Auto Leadership positions Chase is #1 Visa credit card issuer 20.8% market share of General Purpose Credit Card outstandings 4 19.3% market share of General Purpose Credit Card sales volume 4 #1 co-brand card issuer in the U.S. 5 #1 merchant acquirer in e-commerce payment processing 5 1 2009 on a managed basis. See note 1 on slide 43 2 Calculated based on average equity; 2011, 2010 and 2009 average equity was $16.0B, $18.4B and $17.5B, respectively 3 Statistics include loans held for sale 4 Excludes WaMu and Commercial Card 5 Based on internal JPM estimates 2009 1 2010 2011 Card Services & Auto Revenue $23,199 $20,472 $19,141 Credit Costs 19,648 8,570 3,621 Expense 6,617 7,178 8,045 Net Income ($1,793) $2,872 $4,544 ROE 2 (10)% 16% 28% EOP Equity ($B) $17.5 $18.4 $16.0 Card Services — Key Drivers excl. Commercial Card 3 ($B) Avg Outstandings $172.4 $144.4 $126.8 Sales volume $294.1 $313.0 $343.7 New Accts Opened (mm) 10.2 11.3 8.8 Net Revenue Rate 11.78% 11.89% 12.31% Net Charge-off Rate 9.33 9.72 5.46 30+ Day Delinquency Rate 6.28 4.07 2.82 Merchant Services — Key Drivers (B) Bank card volume $409.7 $469.3 $553.7 # of total transactions 18.0 20.5 24.4 Auto — Key Drivers ($B) Avg Outstandings - Auto $43.6 $47.6 $47.0 Avg Outstandings - Student 16.1 15.9 $14.0 Auto Originations 23.7 23.0 $21.0 38 $mm |

Includes deposits and deposits swept to on-balance sheet liabilities Loans held-for-sale and loans at fair value were excluded when calculating the loan loss coverage ratio and net charge-off rate Calculated based on average equity Reflect CB-equivalent segments at BAC, KEY, PNC and USB Based on CB-equivalent segments or wholesale portfolios at BAC, CMA, FITB, KEY, PNC, USB and WFC Thomson Reuters FY11 FDIC 9/30/11 Commercial Banking Leadership positions Highest ROE in peer group 4 Lowest overhead ratio in peer group 5 Continued to outperform peers in credit quality with the lowest net charge-off ratio and nonperforming loan ratio in peer group 5 Top 3 Middle Market syndicated lender in the U.S. 6 #1 multi-family lender in the U.S. 7 2009 2010 2011 Revenue $5,720 $6,040 $6,418 Middle Market 3,055 3,060 3,145 Corp. Client Banking 1,102 1,154 1,261 Comm. Term Lending 875 1,023 1,168 Real Estate 461 460 416 Other 227 343 428 Expense 2,176 2,199 2,278 Credit Costs 1,454 297 208 Net Income $1,271 $2,084 $2,367 Key Statistics ($B) Avg Loans $106.7 $97.0 $104.2 EOP Loans 97.4 98.9 112.0 Avg Liability Balances 1 113.2 138.9 174.7 Gross IB Fees ($mm) 1,163 1,335 1,421 Allow. for Loan Losses 3.0 2.6 2.6 NPLs 2.8 2.0 1.1 Net Charge-Off Rate 2 1.02% 0.94% 0.18% ALL/Loans 2 3.12 2.61 2.34 ROE 3 16 26 30 Overhead Ratio 38 36 35 EOP Equity $8.0 $8.0 $8.0 39 $mm 1 2 3 4 5 6 7 |

Treasury & Securities Services 2009 2010 2011 Revenue $7,344 $7,381 $7,702 Treasury Services 3,702 3,698 3,841 Worldwide Securities Svcs. 3,642 3,683 3,861 Expense 5,278 5,604 5,863 Credit Costs 55 (47) 1 Net Income $1,226 $1,079 $1,204 Key Statistics Avg Liability Balances ($B) 1 $248.1 $248.5 $318.8 Assets Under Custody ($T) 14.9 16.1 16.9 Pretax Margin 26% 23% 24% ROE 2 25 17 17 TSS Firmwide Revenue $10,231 $10,260 $10,237 TS Firmwide Revenue 6,589 6,577 6,376 TSS Firmwide Avg Liab Bal ($B) 1 361.2 387.3 493.5 EOP Equity ($B) 5.0 6.5 7.0 Includes deposits and deposits swept to on-balance sheet liabilities Calculated based on average equity Source: Federal Reserve, Clearing House for Interbank Payments (CHIPS), and Ernst & Young Source: Greenwich Associates, 2011 Source: JPM and peer 4Q11 company filings Source: Various global exchanges, as of November 2011 Source: Nilson Leadership positions #1 global clearer of U.S. dollars and #1 Automated Clearing House for originations 3 #1 (tied) share leader in U.S. Large Corporate Treasury Management Market Penetration providers 4 #2 provider of custody services leveraging significant scale and global footprint with $16.9T in AUC 5 #2 in number of sponsored American Depository Receipt (ADR) shares 6 #1 Visa / MasterCard Commercial, Purchasing and Prepaid card issuer in the U.S. 7 40 1 2 3 4 5 6 7 $mm |

Asset Management Leadership positions #1 Institutional Money Market Fund Manager Worldwide 2 #1 Ultra-High-Net-Worth Private Bank Globally 3 #2 in U.S. Total Net Mutual Fund flows 4 2011 Asset Manager of the Year for Asia and Hong Kong 5 Leading Pan-European Fund Management Firm 6 Best brand in Private Banking 7 Best Private Bank for Customer Service 7 1 Calculated based on average equity 2 Source: iMoney, 2011 3 Source: EuroMoney, 2012 4 Source: Strategic Insight, 2011 5 Source: The Asset Magazine, 2011 6 Source: Thomson Reuters, 2011 7 Source: Financial Times, 2011 2009 2010 2011 Revenue $7,965 $8,984 $9,543 Private Banking 4,320 4,860 $5,116 Institutional 2,065 2,180 2,273 Retail 1,580 1,944 2,154 Expense 5,473 6,112 7,002 Credit Costs 188 86 67 Net Income $1,430 $1,710 $1,592 Key Statistics ($B) Assets Under Management $1,249 $1,298 $1,336 Assets Under Supervision 1,701 1,840 1,921 Average Loans 35.0 38.9 50.3 EOP Loans 37.8 44.1 57.6 Average Deposits 77.0 86.1 106.4 Pretax Margin 29% 31% 26% ROE 1 20 26 25 EOP Equity $7.0 $6.5 $6.5 41 $mm |

Corporate/Private Equity $8.7 $7.7 $7.3 5.7% 6.9% 6.3% $5.0 $6.0 $7.0 $8.0 $9.0 2009 2010 2011 0.0% 2.0% 4.0% 6.0% 8.0% Portfolio as % of equity ex. goodwill EOP carrying value 1 Includes merger-related items 2009 2010 2011 Private Equity ($78) $588 $391 Corporate 1 3,108 670 411 Net Income $3,030 $1,258 $802 42 Net income ($mm) Private Equity portfolio ($B) |

Notes on non-GAAP & other financial measures 43 Notes on non-GAAP financial measures 1. In addition to analyzing the Firm’s results on a reported basis, management reviews the Firm’s results and the results of the lines of business on a “managed” basis, which is a non-GAAP financial measure. The Firm’s definition of managed basis starts with the reported U.S. GAAP results and includes certain reclassifications to present total net revenue for the Firm (and each of the business segments) on a FTE basis. Accordingly, revenue from tax-exempt securities and investments that receive tax credits is presented in the managed results on a basis comparable to taxable securities and investments. This non-GAAP financial measure allows management to assess the comparability of revenue arising from both taxable and tax-exempt sources. The corresponding income tax impact related to tax-exempt items is recorded within income tax expense. These adjustments have no impact on net income as reported by the Firm as a whole or by the lines of business. Prior to January 1, 2010, the Firm’s managed basis presentation also included certain reclassification adjustments that assumed credit card loans securitized by Card Services & Auto remained on the balance sheet. Effective January 1, 2010 the Firm adopted accounting guidance that required the Firm to consolidate its Firm-sponsored credit card securitization trusts. The income, expense and credit costs associated with these securitization activities are recorded in the 2011 Consolidated Statements of Income in the same classifications that were previously used to report such items on a managed basis. As a result of the consolidation of the credit card securitization trusts, reported and managed basis relating to credit card securitizations are equivalent for periods beginning January 1, 2010. The presentation of Card Services & Auto’s results prior to January 1, 2010 on a managed basis assumed that credit card loans that had been securitized and sold in accordance with U.S. GAAP remained on the Consolidated Balance Sheets, and that the earnings on the securitized loans were classified in the same manner as the earnings on retained loans recorded on the Consolidated Balance Sheets. JPMorgan Chase used the concept of managed basis to evaluate the credit performance and overall financial performance of the entire managed credit card portfolio. Operations were funded and decisions were made about allocating resources, such as employees and capital, based on managed financial information. In addition, the same underwriting standards and ongoing risk monitoring are used for both loans on the Consolidated Balance Sheets and securitized loans. Although securitizations result in the sale of credit card receivables to a trust, JPMorgan Chase retains the ongoing customer relationships, as the customers may continue to use their credit cards; accordingly, the customer’s credit performance affects both the securitized loans and the loans retained on the Consolidated Balance Sheets. JPMorgan Chase believed that this managed-basis information was useful to investors, as it enabled them to understand both the credit risks associated with the loans reported on the Consolidated Balance Sheets and the Firm’s retained interests in securitized loans. 2. The ratio of the allowance for loan losses to end-of-period loans excludes the following: loans accounted for at fair value and loans held-for-sale; purchased credit-impaired (“PCI”) loans; and the allowance for loan losses related to PCI loans. Additionally, Real Estate Portfolios net charge-offs exclude the impact of PCI loans. The allowance for loan losses related to the purchased credit-impaired portfolio totaled $5.7 billion, $4.9 billion and $1.6 billion at December 31, 2011, 2010 and 2009, respectively 3. The Basel I Tier 1 common ratio is Tier 1 common divided by risk-weighted assets. Tier 1 common is defined as Tier 1 capital less elements of Tier 1 capital not in the form of common equity, such as perpetual preferred stock, noncontrolling interests in subsidiaries and trust preferred capital debt securities. Tier 1 common, a non-GAAP financial measure, is used by banking regulators, investors and analysts to assess and compare the quality and composition of the Firm’s capital with the capital of other financial services companies. The Firm uses Tier 1 common along with other capital measures to assess and monitor its capital position. On December 16, 2010, the Basel Committee issued the final version of the Basel Capital Accord, commonly referred to as “Basel III.” The Firm’s estimate of its Tier 1 common ratio under Basel III is a non-GAAP financial measure and reflects the Firm’s current understanding of the Basel III rules and the application of such rules to its businesses as currently conducted, and therefore excludes the impact of any changes the Firm may make in the future to its businesses as a result of implementing the Basel III rules. The Firm’s understanding of the Basel III rules is based on information currently published by the Basel Committee and U.S. federal banking agencies. Management considers this estimate as a key measure to assess the Firm’s capital position in conjunction with its capital ratios under Basel I requirements, in order to enable management, investors and analysts to compare the Firm’s capital under the Basel III capital standards with similar estimates provided by other financial services companies. 4. Tangible common equity (“TCE”), a non-GAAP financial measure, represents common stockholders’ equity (i.e., total stockholders’ equity less preferred stock) less goodwill and identifiable intangible assets (other than MSRs), net of related deferred tax liabilities. ROTCE, a non-GAAP financial ratio, measures the Firm’s earnings as a percentage of TCE. In management’s view, these measures are meaningful to the Firm, as well as analysts and investors in assessing the Firm’s use of equity, and in facilitating comparisons with competitors. 5. In Card Services, supplemental information is provided for Chase, excluding Washington Mutual and Commercial Card portfolios, to provide more meaningful measures that enable comparability with prior periods. The net charge-off rate and 30+ delinquency rate presented include loans held-for-sale. 6 In addition to reviewing JPMorgan Chase's net interest yield on a managed basis, management also reviews core net interest income to assess the performance of its core lending, investing (including asset /liability management), and deposit-raising activities, excluding the impact of IB's market-based activities. IB’s market-based activities is defined as total IB net interest income less net interest income earned on IB loans. The chart presents an analysis of managed core net interest income and core net interest margin. These are non-GAAP financial measures due to the exclusion of IB's market-based net interest income and the related assets. Management believes the exclusion of IB's market-based activities, provides investors and analysts a more meaningful measure to analyze non-market related business trends of the Firm and can be used as a comparable measure to other financial institutions primarily focused on core lending, investing and deposit-raising activities. Additional notes on financial measures 7. Pretax margin represents income before income tax expense divided by total net revenue, which is, in management’s view, a comprehensive measure of pretax performance derived by measuring earnings after all costs are taken into consideration. It is, therefore, another basis that management uses to evaluate the performance of TSS and AM against the performance of their respective competitors. |

February 28, 2012 M O R T G A G E B A N K I N G Frank Bisignano, Mortgage Banking CEO and Chief Administrative Officer |

Agenda Page 1 Performance and outlook 1 Mortgage Production 10 Mortgage Servicing 19 Real Estate Portfolios 27 Appendix 32 |

Uncertainty continues Private label litigation; GSE/FHA/VA/PLS repurchases and other Volume of unsold homes; shadow inventory Role of private capital in mortgage market liquidity The OCC and the Fed issued Consent Orders in April 2011 to large mortgage servicers Servicer plans were approved by the OCC and the Fed Communication with borrowers began in October Modification and refinance programs continue to be expanded Significant proprietary modification and short sale programs exist with each servicer Servicing practices largely remediated 2011 – A year of repositioning $25B settlement covers 5 servicers ~$5B – Cash ~$3B – Refi Program for “underwater” homeowners ~$17B – Additional consumer relief Required to adhere to certain enhanced mortgage servicing standards 1 Ever 30 days delinquent measured 6 months from origination for the JPMC serviced portfolio; excludes HARP Recent underwriting practices have demonstrated strong performance Early delinquency rates 1 peaked in 2005-2008 vintages at 1.5% for Prime/Home Equity loans; over 4% for government insured 2009+ vintages averaging less than 0.5% across product types 2 |

2011 – Positioning for success at Chase Chase now #2 in originations – 3Q/4Q11 Increased the number of loans originated from the branches by over 40% Enhanced customer experience JD Power Customer Satisfaction rank up to 5 th , from 12 th Community relationships improved Reconstituted management team and organizational structure Recruited key leadership by leveraging talent inside the firm and from strategic external hires Formed Borrower Assistance Increased loan officers 23% in 2011 Leveraged firmwide expertise and best practices across LOBs – Investment Bank, CIO, and other Consumer businesses Consolidated three servicing platforms into one Re-engineered servicing processes to improve efficiency Increased number of modifications per month by 38% and short sales by 43% Charge-offs decreased Repurchase losses lower Strong retail channel volumes and margins Control governance structure revamped; risk management oversight enhanced Consent Orders servicing improvements Brought full power of the firm to fix our mortgage business Delivered on technology and process improvements Improved volumes, market share, and customer satisfaction Improved risk and control environment Improving financial performance 3 |

2011 – Focused on more profitable Retail channel Overall market share increase driven by Retail originations – Now represent ~2/3 of our volume While growth has been driven by the Retail channel, we continue to believe the Correspondent channel is attractive with the appropriate risk/return profile Note: Retail channel includes branch and direct to consumer originations Source: Inside Mortgage Finance – Originations are firmwide 4 |

2011 – Positioning for success at Chase 5 BB&T |

2011 Results Total origination market size $1,840.0 $1,630.0 $1,350.0 Chase mortgage loan originations 150.7 155.6 145.6 Chase Retail channel originations $53.9 $68.8 $87.2 Chase Correspondent channel originations 93.2 85.5 57.9 3rd Party mtg loans svc'd (EOP) 1,082.1 967.5 902.2 MSR net carrying value (EOP) 15.5 13.6 7.2 MSR revenue multiple 3.3x 3.2x 1.8x Headcount 32,393 39,440 49,189 2009 2010 2011 Production pre-tax $7 ($216) $993 Servicing pre-tax 1,943 1,191 (3,797) Real Estate Portfolio pre-tax (8,890) (4,311) (504) Total net income ($4,250) ($1,924) ($2,138) 6 P&L ($mm) Key drivers ($B, unless otherwise noted) |

Ongoing Legacy Total Normalized Production Pre-tax income $2,270 ($1,277) $993 $1,500 +/- Servicing Servicing operating pre-tax 203 (2,428) (2,225) MSR risk management 154 (1,726) (1,572) Total pre-tax income $357 ($4,154) ($3,797) $1,000 +/- Real Estate Portfolios 1 Pre-tax pre-provision 549 2,522 3,071 Credit costs 109 3,466 3,575 Total pre-tax income $440 ($944) ($504) $500-1,000 Total Mortgage Banking pre-tax income $3,067 ($6,375) ($3,308) $3,000-3,500 Mortgage Banking net income $1,982 ($4,120) ($2,138) $1,800-2,100 Normalized ROE 15% 2011 2011 Ongoing vs. legacy view – Ongoing business profitable Production: legacy repurchase losses will normalize over time Servicing: MSR yield will improve in 2012 based on refinement of MSR valuation model in 4Q11 Weighted average option adjusted spread of 7.8% at year end 2011 vs. 3.9% at year end 2010 Real Estate Portfolios: legacy portfolio will improve with credit and ultimately turn positive Normalized earnings should produce 15% ROE through the cycle 1 Legacy Real Estate Portfolio is defined as WaMu purchased credit-impaired, discontinued products, broker originated loans, limited documentation loans, and certain loans with ECLTVs greater than 80%. Ongoing portfolio end-of-period loan balance is $36B and legacy portfolio end-of-period loan balance is $162B 7 Mortgage Banking ($mm) Key drivers |

2011 included significant negatives 1 RFS only. Excludes EMC 2 Excludes non-recurring foreclosure-related matters 3 Includes refinements to the valuation model and related inputs comprising updates to the prepayment model, revised fee and cost to service assumptions and an increase in the option adjusted spread (“OAS”) to reflect higher return and capital requirements 2011 servicing and default expense of $3.2B will normalize to $1.25B over time 2011 results include $3.4B of non-recurring costs Significant items - pretax 2010 2011 Normalized Production Repurchase losses 1 (2,912) (1,347) (150) Servicing Servicing and default expense 2 ($2,234) ($3,195) ($1,250) Core servicing expense (837) (1,031) Default servicing expense (1,397) (2,164) Non-recurring ($350) ($3,377) Foreclosure related matters (350) (1,650) MSR valuation updates 3 NM (1,727) Real Estate Portfolios Foreclosed asset expense (896) (649) (200) Subtotal ($6,392) ($8,568) ($1,600) ($mm) 8 |

Capitalize on ‘One Chase’ brand Continue to improve customer experience Continue root cause analysis to eliminate customer complaints Strengthen controls, minimize breakages and defects Enhance compliance, risk and control infrastructure Deliver against Consent Orders and DOJ/AG requirements Attract and retain talent to focus on most critical areas Develop and motivate high performers Improve loan officer retention Build a culture of quality and control 2012: business growth and winning Expand and strengthen the production franchise Accelerate growth, particularly in retail channel and purchase lending Re-engineer origination and servicing processes and enhance operating efficiency Price for appropriate returns given increasing capital requirements Leverage technology to enhance customer experience and improve operating efficiencies and controls 9 |

Agenda Page 10 Mortgage Production 10 Performance and outlook 1 Mortgage Servicing 19 Real Estate Portfolios 27 Appendix 32 |

Blank slide Best-in-class customer experience – Mortgage Manager video This page is intentionally left blank 11 |

Blank slide Strengthen the production franchise Retail origination model leverages Chase brand and customer delivery platform Branches, online, and mobile Core product for branch cross-sell opportunities Fee based counter-cyclical earnings stream complements traditional spread businesses Attractive returns over the cycle Why we like the business Improve purchase market share to 10%-12% An increase of ~50% from 2011 Retail sales force growth ~25% in 2012 Best-in-class customer experience Roll out Mortgage Manager New retail origination platform Improve productivity Enhance underwriting and process quality Areas of focus 12 |

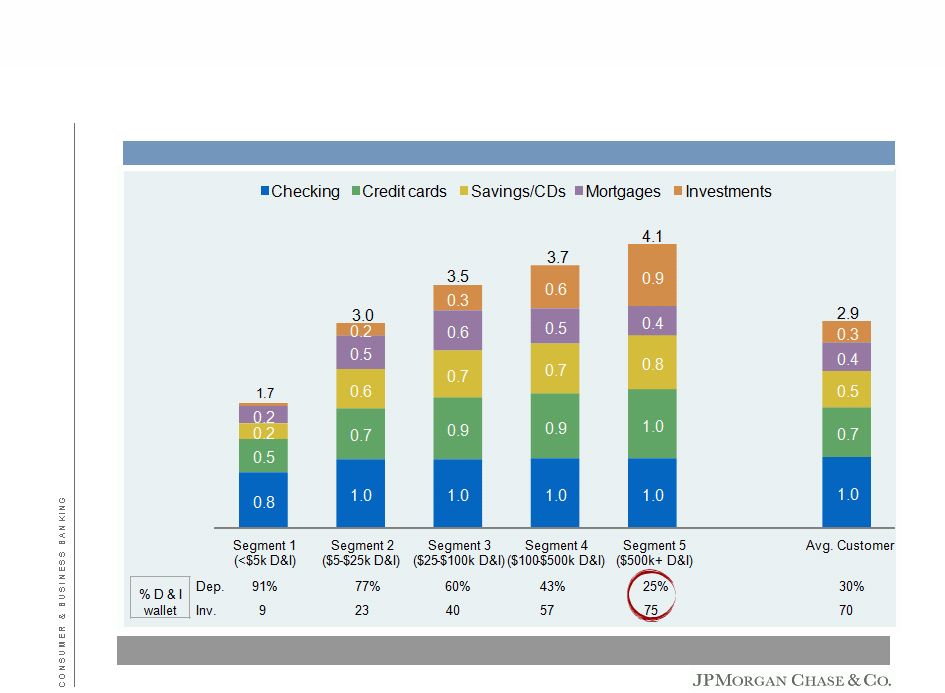

Core product for branch cross-sell opportunities Relationship impact after acquiring a Chase mortgage Excludes any additional value attributed to cross-sell (e.g. credit card, investments) Households with a mortgage are generally more affluent and offer more cross-sell value than those without a mortgage Mortgage increases the value of the overall customer relationship 2 Mass Affluent has a deposit and investment wallet of $100k-$500k, affluent has $500k-$5mm, and high net worth has greater than $5mm 1 Higher share of wallet and lower attrition of balances 13 Incremental value 1 of adding mortgage to a banking relationship % of HH that are high net worth, mass affluent or affluent 2 |

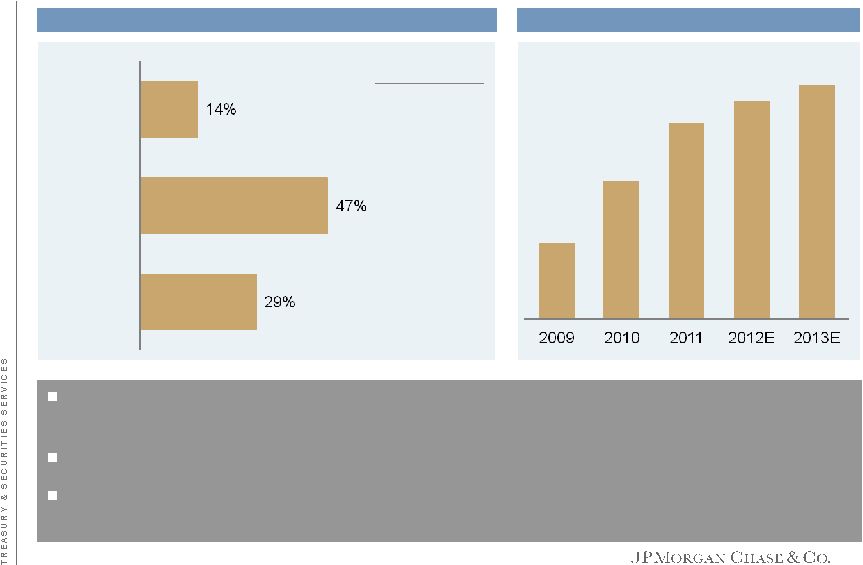

Blank slide Mortgage production – Purchase market share opportunity Source: Inside Mortgage Finance Lowest rates in history and HARP led to recent robust refinance market We expect market mix to be weighted to purchase in a more normal rate environment Focus on growing share in purchase to capitalize on market growth Well positioned to take share in purchase market 5.7mm existing Chase mortgage households 6.1mm existing eligible Chase banking relationships with no mortgage relationship 75k real estate agent relationships in business banking Strong recruiting of purchase-focused loan officers Increasing lead in customer satisfaction versus top competitors Purchase Refi $2.5T $1.6T Average mortgage market size and purchase/refinance mix Comments Chase mortgage originations market share 14 |

Blank slide Mortgage production – Retail model differentiation Opportunity to increase sales force to match competitors Added +/- 700 loan officers in 2011 Additional +/- 1,000 loan officers in 2012 is additional run rate annual pretax earnings of $100mm+ Sources: Company filings and investor presentations Chase loan officer productivity exceeds major competitors Loan officers substantially located at branches Marketing investment drives leads to branches and call center 15 2011 Retail fundings / loan officer / month Number of loan officers (EOP) Commentary Commentary |

Blank slide Mortgage origination economics Business drivers Sales force size/productivity Marketing effectiveness Customer experience Operational efficiency and capacity flexibility Underwriting and process quality Repurchase expense Market risk exposure to MBS rates Competitor capacity/margin positioning Purchase market does not recover Regulatory and GSE changes Risks Market volume $1.5T +/- Market share 15% +/- Chase volume $225B +/- Chase pretax margin / $ volume 65bps +/- Chase pretax income $1.5B +/- Execution of business drivers creates attractive returns over the cycle High returns in peak refinance years Lower returns in “normal” years Normalized target income 16 |

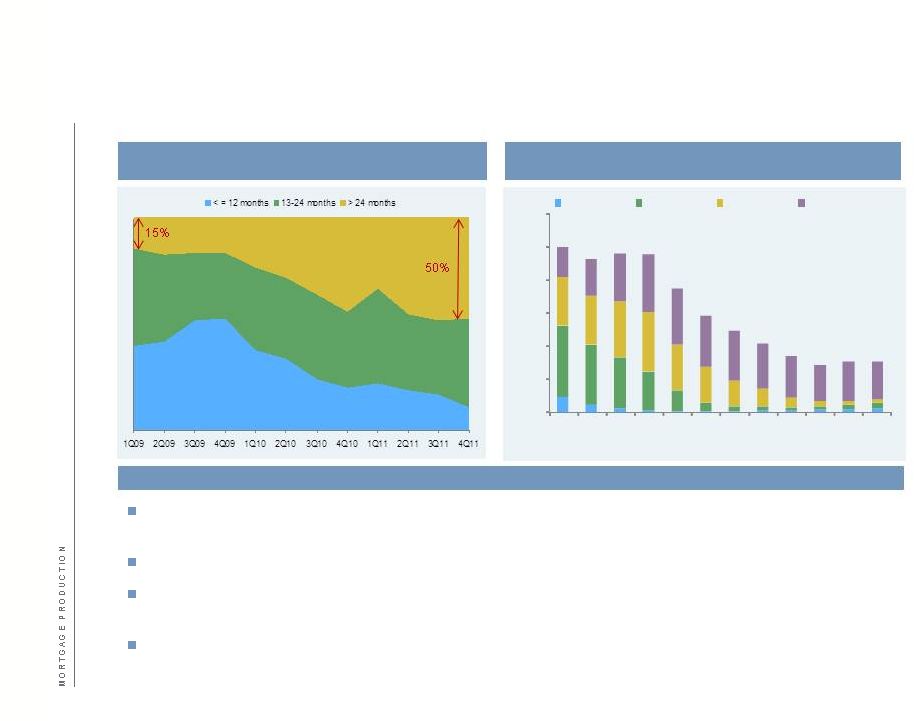

Repurchase update FY11 realized losses of $1.1B with reserves of $3.2B Realized losses trended higher in 2H11 as GSE demands accelerated GSEs have improved cycle times (reduced time between file request and demand) ~90% of demands continue to come from 2005-2008 vintages While 2012 realized losses are expected to remain elevated, reserves will come down at some point Newly delinquent loans have longer payment history, reducing likelihood of origination defect Outlook of +/- $350mm realized losses per quarter Realized losses and reserve Commentary 4Q10 1Q11 2Q11 3Q11 4Q11 FY10 FY11 Realized losses ($mm) $349 $215 $215 $314 $390 $1,360 $1,134 Reserve ($B, EOP) $3.0 $3.2 $3.2 $3.2 $3.2 $3.0 $3.2 17 |

Repurchase update Loans going delinquent after 24 months of payment history are typically at a lower risk of repurchase due to rep and warrant defect ~50% of demands received in 2H11 have made more than 24 months of payments – Up from ~15% in 2009 Cure rates (ability to remedy purported defect) have been 10-15 points higher on loans with greater than 24 months pay history New delinquencies have decreased significantly from 2009 peak; majority of newly delinquent loans in 2011 had more than 36 months of pay history 4,968 4,611 4,786 4,742 3,719 2,909 2,457 2,053 1,694 1,426 1,527 1,520 - 1,000 2,000 3,000 4,000 5,000 6,000 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 <= 12 months 13 - 24 months 25 - 36 months >36 months 18 GSE new demands by pay history (2005-2008 Vintages, hChase UPB, $mm) GSE new loans to 90 days past due by burnout (2005-2011 vintages, hChase, UPB $mm) Commentary |

Agenda Page 19 Mortgage Servicing 19 Performance and outlook 1 Mortgage Production 10 Real Estate Portfolios 27 Appendix 32 |

Blank slide Improving servicing profitability Achieve short term run-rate savings Delinquent accounts decrease Modification inventory reduced through borrower assistance initiatives Normalize servicing expense over time Regulatory environment, including Consent Orders and DOJ/AG related items Improve customer satisfaction Deployment of NICE analytics for early escalation of customer issues Why we like the business Areas of focus Mortgage increases the value of the overall customer relationship Chase, as the 3 rd largest servicer has the advantage of scale Macroeconomic fundamentals are improving, resulting in reduced default rates, and improving cost structure With appropriate operations and risk management, the MSR asset will deliver consistent attractive returns (15% ROE) 20 |

Prevented twice as many foreclosures as have been acted upon Offered over 1.2 million modifications and completed 452,000 since 2009 Foreclosure alternatives (short sales, Deed in Lieu) increased 22% over the prior year 82 Chase Home Ownership Centers (CHOCs) 15,000 borrower assistance and default servicing support staff Refinanced more than 1 million mortgages since 2010 Met with over 273,000 struggling customers Doing more to prevent foreclosures Foreclosure process update Average delinquency at foreclosure is over 17 months Recent foreclosure sales showed the following customer/loan characteristics: 54% non-owner occupied or vacant – Of which 80% were vacant at time of sale 46% were owner-occupied Key facts about foreclosures 21 |

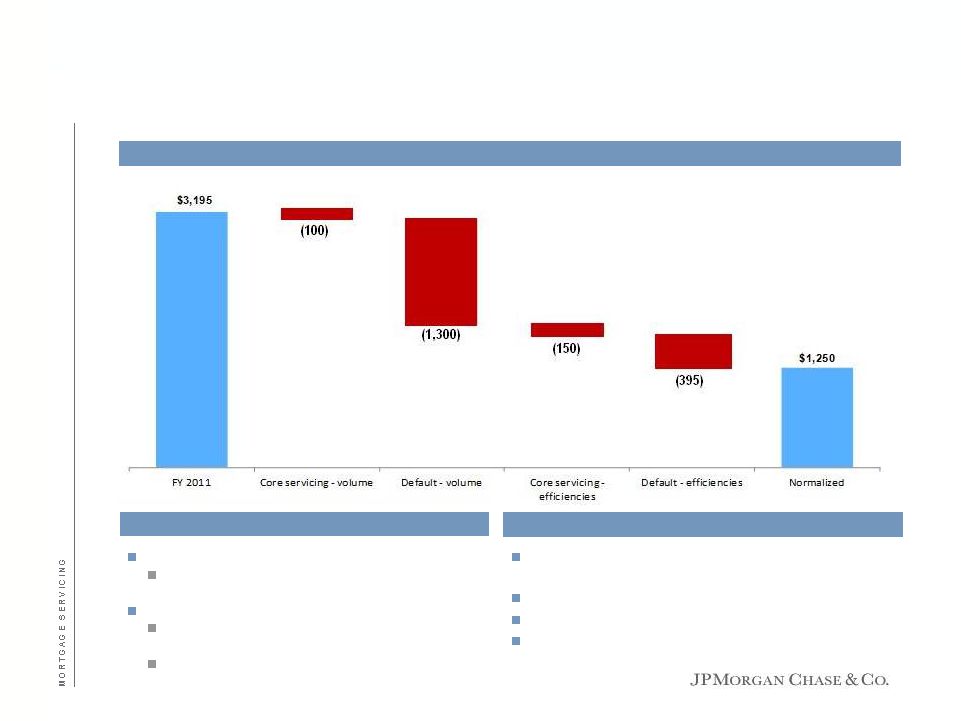

22 Short term run-rate savings in 2012 – Driven by both volume declines and efficiency |

Achieve short term run-rate savings – More than $1B by 4Q12 Consolidated site strategy Improved productivity through employee retention Non-compensation expense improvement primarily due to non-recurring costs and lower operational losses Loan portfolio declines by 5-10% 30+ delinquencies decline approximately 25% Modification pipeline reduced Volume Efficiencies 23 4Q11 Annualized Core servicing volume Default volume Core servicing - efficiencies Default - efficiencies 4Q12 Annualized Servicing and default expense ($mm) |

Normalizing servicing expenses over time Volume Efficiencies Process improvements and technology enhancements in core servicing and default Consolidated site strategy Improved productivity through employee retention Lower legal costs and operational losses Core servicing Loan portfolio declines by 10-15% to steady state of ~7.5mm units Default 30+ delinquencies decline by 70-75% to steady state of ~200k units Modification pipeline materially reduced Servicing and default expense ($mm) 24 |

DOJ and State AG settlement Impact to Chase ~$5.3B: ~$1.1B cash payment, ~$0.5B refinance program and up to ~$3.7B of additional consumer relief (primarily through modification programs) Limits the firm’s liability related to Servicing activities, including past foreclosure, loss mitigation and bankruptcy practices Origination activities, including federal False Claims Act violations and federal consumer statute claims MERS-related conduct, such as recording of assignments and standing in foreclosures Only New York, Delaware, and Massachusetts may maintain suits for MERS-related conduct. The settlement limits monetary remedies those states can seek against Chase, and precludes them from seeking to vacate past foreclosures for MERS-related conduct Does not release the firm from liability related to securitizations and whole loan sales, GSE/FHA/VA/PLS repurchase demands, pension fund claims, fair lending claims, and criminal actions. It also does not preclude suits against MERS as an entity or suits against Chase by county recorders for lost fees Financial impact overview Estimated impact was covered in prior periods Modification programs Modest impact on charge-off timing as a result of principal forgiveness – No change to loss guidance Refinance program Impact of reducing borrower rates is expected to drive an immaterial decrease in net interest margin – Offset in reserves 25 |

Mortgage servicing economics Average UPB $1.0T +/- Servicing & Other Revenue 45bps +/- Amortization 22bps +/- Servicing & Default Costs 13bps +/- Pretax $1.0B +/- Business drivers Macroeconomics (unemployment, HPI, interest rates) Size and average life of servicing book Management of operational risk and efficiency of platforms Market risk management – MSR hedging Default costs expected to remain high for the medium term to handle modification and foreclosure volumes Market risk management Regulatory and GSE changes Risks Normalized target income With appropriate operations and risk management and market recovery, the size and mix of our serviced portfolio will deliver solid profitability 26 |

Agenda Page 27 Real Estate Portfolios 27 Performance and outlook 1 Mortgage Production 10 Mortgage Servicing 19 Appendix 32 |

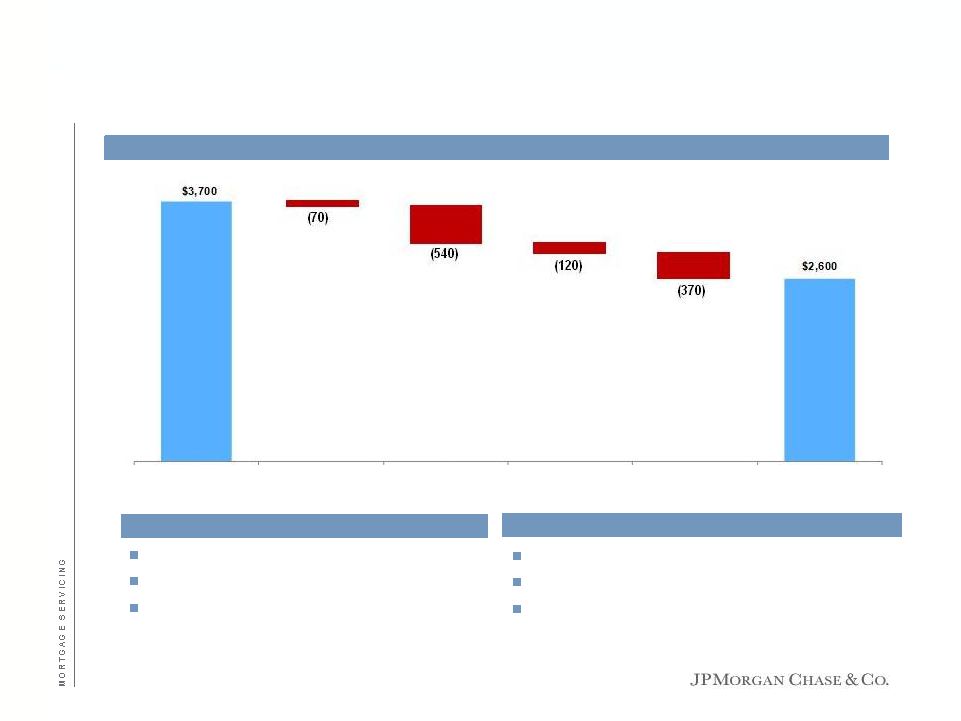

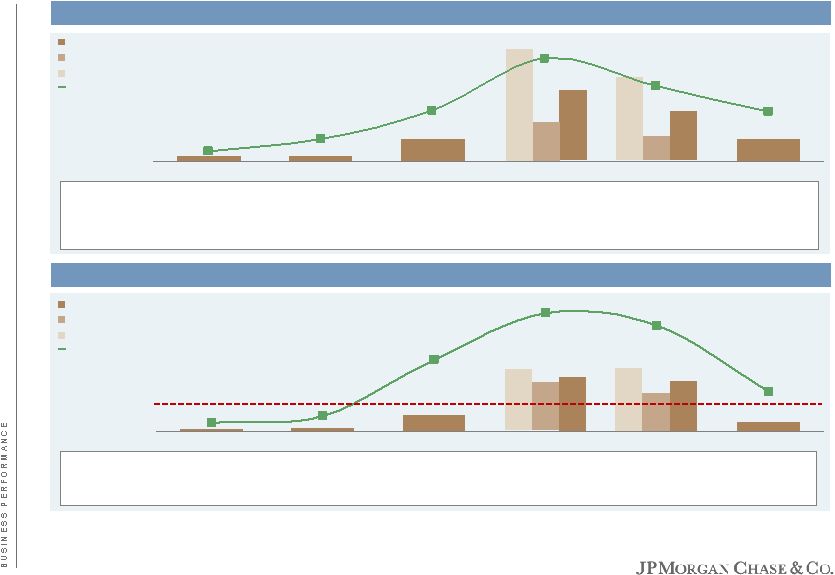

Real Estate Portfolios simulation Future reserve actions not simulated Although NII will decline as portfolio runs down, expense and credit losses will also decline As a result, the net losses today will become a modest positive contribution to earnings over time As portfolio runs off, ~$1B of capital per year could be freed up and re-deployed – Timing is impacted by pro- cyclicality of capital rules Real Estate Portfolios — simulated ending loan balance run-off and net income ($mm) Commentary 2009 2010 2011 2012 2013 2014 Ending Balances ($B) $252 $223 $198 $178 $158 $144 Ongoing ($B) 37 36 37 $39 42 Legacy ($B) 186 162 141 $119 102 Revenue $6,520 $5,547 $4,592 $4,100 $3,400 $2,900 Net charge-offs 8,343 6,450 3,805 3,000-4,000 2,000-3,500 1,000-1,500 Change in reserves 5,220 1,781 (230) Expense 1,847 1,627 1,521 1,300 1,200 1,000 Pre-tax net income / (loss) ($8,890) ($4,311) ($504) ($1,200)-($200) ($1,300)-$200 $400-$900 28 |

Non credit-impaired Purchased credit-impaired Total loans Home Equity $78 $25 $103 Prime Mortgage $37 16 53 Option ARM $7 26 33 Subprime Mortgage $10 7 17 Total REP Loans 1 $132 $74 $206 Fair Value Mark 2 NA 9 9 Total Mortgage Banking Portfolio $132 $65 $197 Loan loss reserve (LLR) $8.7 $5.7 $14.4 LLR as % of loans / LLR + FVM as % of UPB PCI 6.6% 19.7% NA Real Estate Portfolios EOP loans as of 12/31/11 ($B) Real Estate Portfolios 6.6% reserve ratio on non credit-impaired portfolio Purchased credit-impaired portfolio is appropriately reserved for best estimate of remaining lifetime losses 1 Credit-impaired represents Unpaid Principal Balance (UPB), not book value 2 Fair Value Mark (FVM) remaining is the original mark reduced by liquidation losses realized Note: Table above excludes prime mortgage loans and student loans classified as held-for-sale Commentary 29 |

Non-credit-impaired Credit Total Mortgage Banking reserves of $8.7B (excluding WaMu purchased credit-impaired) 4Q11 net charge-offs annualized of $3.5B Loss guidance: Mortgage Banking quarterly net charge-offs expected to be $900mm+/- 1 4Q10 net charge-offs exclude the one-time impact of the $632mm adjustment related to the timing of when the Firm recognizes charge-offs on delinquent loans Current reserve and mark reflect ~$35B of lifetime losses, of which $21B has been realized to-date Further 8% HPI decline from current levels would result in a $1.5B impairment Net charge-offs 1 vs. Loan loss reserve ($mm), excl PCI 30 Purchase credit-impaired |

Key themes addressed throughout the day Production business positioned for success Continuing to improve the customer experience Servicing – Building efficiencies for the future Real Estate Portfolios – Returning to profitability and returning capital Significant legacy issues behind us: Consent Orders and DOJ/AG Settlement Attractive earnings potential with 15% ROE through the cycle Our goal is to be the most efficient, profitable, and customer-centric mortgage business 31 |

Agenda Page 32 Appendix 32 Performance and outlook 1 Mortgage Production 10 Mortgage Servicing 19 Real Estate Portfolios 27 |

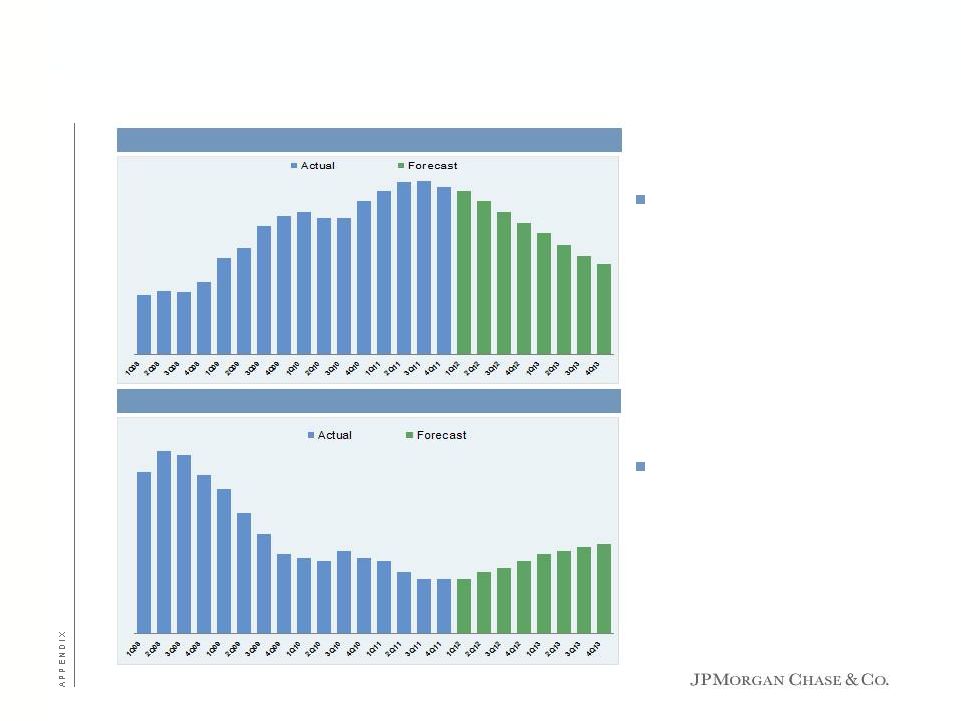

Foreclosure and REO trends – Total serviced Foreclosure inventory will continue to decline as inflows of new delinquencies decline and outflows of foreclosure and short sales increase REO inventory forecast to increase as volume of foreclosure sales increase 33 Units in REO Units in process of foreclosure |

Home Equity – Performance of 2 nd lien relative to 1 st lien UPB as of 12/31/11 ($B), non-credit-impaired portfolio 2nd Lien status Note: Current Mortgage defined as Current (excludes 1-29), while Current Home Equity is Current or 1-29 bucket to align with OCC definition 1st liens $21.8 2nd liens 56.0 Total $77.8 Delinquent 1st and 2nd 1.1 Current 2nd / delinquent or modified 1st 3.7 Total $56.0 Current 1st / current 2nd $50.8 Current 1st / delinquent 2nd 0.3 34 |

High Risk 2nd liens 1st Lien status UPB Estimated lifetime loss rates >100+% CLTV Modified $1.8 ~40% 65% <150+ DPD 1.4 ~50% 40% 150+ DPD 0.5 ~95% 53% Total $3.7 55% +/- 53% High risk 2nds – Performing 2nds behind troubled borrowers Excluding purchased credit-impaired loans Performing 1st and 2nd liens CLTV UPB Estimated lifetime loss rates <=80% $24.5 ~ 1% 80-100% 12.2 4-5 % 100+% 14.1 12-15 Total $50.8 6% +/ Performing 1 st and 2 nd Liens Delinquent 2nds High Risk 2nds High Risk 2nds – 1 st < 150+ DPD High Risk 2nds – 1 st 150+ DPD High Risk 2nds – Modified/Trial 1 st Note: grossed up based on 35% match rate 2 nd Lien Home Equity UPB ($B) - Dec11 High Risk 2 nd Liens ($B) - Dec11 We have considered the status of 1st lien and equity position of borrowers in our reserves Note: ECLTV for Home Equity 2 nd Liens and ELTV for 1 st Lien Home Equity (Change made in 3Q11). ECLTV = estimated combined loan to value considering all available lien positions related to the property which we own or service Current ECLTVs are calculated using original appraised value adjusted using the latest HPI published by Moody's Economy.com Missing ECLTV & Missing FICO allocated based on Non Missing Current Mortgage defined as Current (excludes 1-29), while current Home Equity is Current or 1-29 bucket to align with OCC definition Note: grossed up based on 35% match rate 35 |

February 28, 2012 Todd Maclin, Chief Executive Officer Consumer & Business Banking C O N S U M E R & B U S I N E S S B A N K I N G |

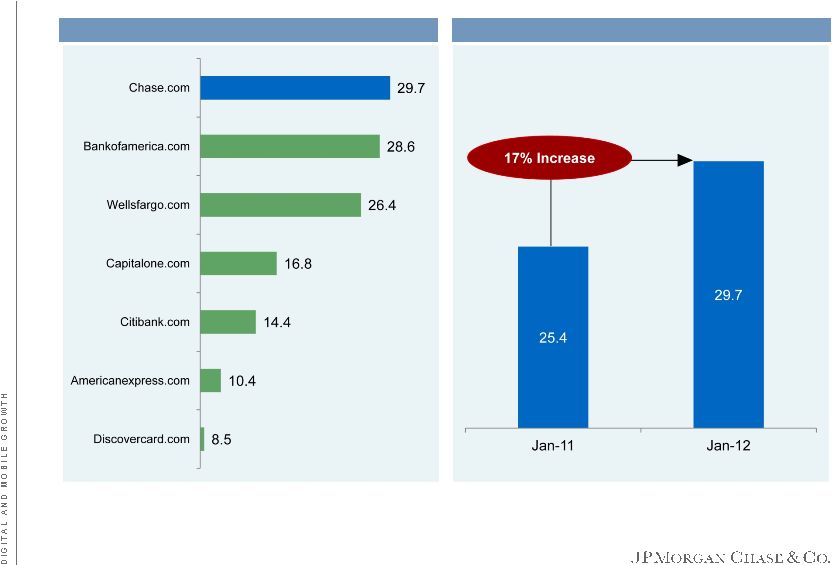

Consumer & Business Banking is a strong franchise today Great business with a focus on growth 1 Strong profitability, despite the environment – 2011 net income of $3.8B and ROE of 40% Low volatility in earnings Significant opportunities to lower cost to serve and increase revenues – 3-5 year horizon Brand strength, driven by excellent products, services and convenient channels #3 in U.S 1 : over 5,500 branches and over 17,200 ATMs across 23 states serving 23mm households Over 17mm active online customers Over 8mm active online mobile customers, over 50% YoY growth Significant presence and leadership in key deposit markets Competitive position of strength: our customers, our people and our financial capacity Investment consistency: we are growing and deepening relationships Over 27,000 personal and business bankers and 3,200 financial advisors Branch and ATM build-out to capture growth at low risk ROIs Significant mobile and internet investment Technology to lower cost-to-serve and delight customers Across “One Chase,” ~51mm households and ~63mm customers to target more aggressively – Chase.com #1 most visited banking portal in the US 2 Note: all data as of December 31, 2011 1 Based on FDIC data for retail deposits as of June 2011; deposits adjusted to exclude large branches (+$1B) assumed to contain non-retail deposits 2 January 2012 compete.com rankings |

Near-term headwinds will slow – Our focus on strong underlying growth will pay off Near-term headwinds Medium-term uplift Longer-term growth $0.5: ’02-’11 New builds ($0.3): ’12+ New builds $0.3: Business Banking $0.4: Chase Private Client $0.5: ’02-’11 New builds $1.0: ’12+ New builds $0.7: Business Banking $0.6: Chase Private Client 1 Consistent with 2012 outlook provided in 4Q11 earnings materials 4% underlying annual growth (net of investment) assumed 2 Simulated pretax income ($B) |

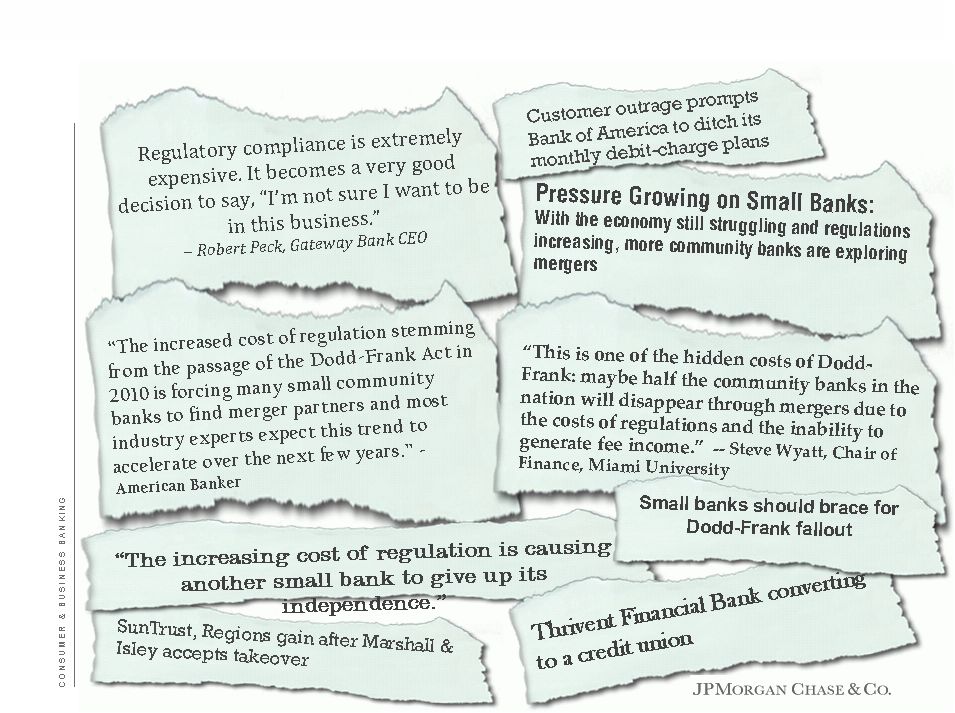

h-Chase Chase incl. WaMu Revenue '05-'09 CAGR '09-'11 CAGR YoY '11-12 Net interest income 8% 0% Noninterest revenue 11 0 Debit 23 11 NSF-OD 15 (20) Investment revenue 5 9 Service fees and other 3 14 Total revenue 9% 0% # of checking accounts 12% 2% # of debit transactions 20% 17% Regulatory reform cost the industry ~$20B 1 In addition, low rates cost the industry ~$4B 2 These revenues will not be replaced in the short term Regulatory reform forces industry to significantly change business models Regulatory reform has permanently altered the economics in CBB 3 1 Source: Boston Consulting Group 2 Source: Bernstein and Morgan Stanley research Historical growth |