| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-260277-03 | ||

March 28, 2023

BENCHMARK 2023-B38

Mortgage Trust

Free Writing Prospectus

Structural and Collateral Term Sheet

$656,890,689

(Approximate Total Mortgage Pool Balance)

$562,421,000

(Approximate Offered Certificates)

| Deutsche Mortgage & Asset Receiving Corporation Depositor |

Commercial Mortgage Pass-Through Certificates

Series 2023-B38

| German American Capital Corporation |

| Goldman Sachs Mortgage Company |

| JPMorgan Chase Bank, National Association |

| Citi Real Estate Funding Inc. |

As Sponsors and Mortgage Loan Sellers

| Deutsche Bank Securities | J.P. Morgan | Citigroup | Goldman Sachs & Co. LLC |

Co-Lead Managers and Joint Bookrunners

| AmeriVet Securities | Drexel Hamilton |

Co-Managers

The depositor has filed a registration statement (including the prospectus) with the Securities and Exchange Commission (File No. 333-260277) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the Securities and Exchange Commission for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the Securities and Exchange Commission website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by emailing: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us. This free writing prospectus does not contain all information that is required to be included in the prospectus.

Benchmark 2023-B38 Mortgage Trust

Capitalized terms used but not defined herein have the meanings assigned to them in the Preliminary Prospectus expected to be dated March 27, 2023 relating to the offered certificates (hereinafter referred to as the “Preliminary Prospectus”).

| KEY FEATURES OF SECURITIZATION |

| Offering Terms: | |

| Co-Lead Managers and Joint Bookrunners: | Deutsche Bank Securities Inc., Goldman Sachs & Co. LLC, J.P. Morgan Securities LLC and Citigroup Global Markets Inc. |

| Co-Managers: | AmeriVet Securities, Inc. and Drexel Hamilton, LLC |

| Sponsors and Mortgage Loan Sellers: | German American Capital Corporation* (“GACC”) (18.8%), Goldman Sachs Mortgage Company (“GSMC”) (39.4%), JPMorgan Chase Bank, National Association (“JPMCB”) (22.1%) and Citi Real Estate Funding Inc. (“CREFI”) (19.8%) *An indirect wholly owned subsidiary of Deutsche Bank AG |

| Master Servicer: | Midland Loan Services, a Division of PNC Bank, National Association |

| Operating Advisor: | Park Bridge Lender Services LLC |

| Asset Representations Reviewer: | Park Bridge Lender Services LLC |

| General Special Servicer: | LNR Partners, LLC |

| Pacific Design Center Special Servicer: | Argentic Services Company LP |

| Certificate Administrator: | Computershare Trust Company, N.A. |

| Trustee: | Computershare Trust Company, N.A. |

| Rating Agencies: | Fitch Ratings, Inc. (“Fitch”), Kroll Bond Rating Agency, LLC (“KBRA”) and Moody’s Investors Service, Inc. (“Moody’s”). |

| Credit Risk Retention: | For a discussion on the manner in which the U.S. credit risk retention requirements are being satisfied by GACC, as retaining sponsor, see “Credit Risk Retention” in the Preliminary Prospectus. Note that this securitization transaction is not being structured to satisfy EU/UK risk retention and due diligence requirements. |

| Determination Date: | 11th day of each month, or if such 11th day is not a business day, the immediately following business day, commencing in May 2023. |

| Distribution Date: | 4th business day following the Determination Date in each month, commencing in May 2023. |

| Cut-off Date: | With respect to each mortgage loan, the later of the related payment date of such mortgage loan in April 2023 (or, in the case of any mortgage loan that has its first due date subsequent to April 2023, the date that would have been its due date in April 2023 under the terms of that mortgage loan if a monthly payment were scheduled to be due in that month) and the date of origination of such mortgage loan. Unless otherwise noted, all mortgage loan statistics are based on balances as of the Cut-off Date. |

| Closing Date: | On or about April 21, 2023 |

| Settlement Terms: | DTC, Euroclear and Clearstream, same day funds, with accrued interest. |

| ERISA Eligible: | All of the Offered Certificates are expected to be ERISA eligible. |

| SMMEA Eligible: | None of the Offered Certificates will be SMMEA eligible. |

| Day Count: | 30/360 |

| Tax Treatment: | REMIC |

| Rated Final Distribution Date: | April 2056 |

| Minimum Denominations: | $10,000 (for each class of offered principal balance certificates) and $100,000 (for each class of offered interest-only certificates) and in each case in multiples of $1 thereafter. |

| Clean-up Call: | 1% (with certain exceptions described under “Pooling and Servicing Agreement—Termination; Retirement of Certificates” in the Preliminary Prospectus) |

| Distribution of Collateral by Property Type |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 2 | ||

Benchmark 2023-B38 Mortgage Trust

| Overview of Mortgage Pool Characteristics | ||||

| Mortgage Loan Sellers | Number of Mortgage Loans | Number of Mortgaged Properties | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance |

| German American Capital Corporation | 5 | 10 | $83,378,471 | 12.7% |

| Goldman Sachs Mortgage Company | 6 | 6 | $198,750,000 | 30.3% |

| JPMorgan Chase Bank, National Association | 4 | 4 | $144,972,500 | 22.1% |

| Citi Real Estate Funding Inc. | 8 | 20 | $129,789,718 | 19.8% |

| Goldman Sachs Mortgage Company / German American Capital Corporation(1)(2) | 2 | 2 | $100,000,000 | 15.2% |

| Total: | 25 | 42 | $656,890,689 | 100.0% |

Collateral Facts | ||||

| Initial Outstanding Pool Balance: | $656,890,689 | |||

| Number of Mortgage Loans: | 25 | |||

| Number of Mortgaged Properties: | 42 | |||

| Average Mortgage Loan Cut-off Date Balance: | $26,275,628 | |||

| Weighted Average Mortgage Rate: | 6.26691% | |||

| Weighted Average Mortgage Loan Original Term to Maturity Date or ARD (months): | 99 | |||

| Weighted Average Mortgage Loan Remaining Term to Maturity Date or ARD (months): | 95 | |||

| Weighted Average Mortgage Loan Seasoning (months): | 4 | |||

| % of Mortgaged Properties Leased to a Single Tenant: | 16.3% | |||

Credit Statistics(3) | ||||

| Weighted Average Mortgage Loan U/W NCF DSCR: | 1.95x | |||

| Weighted Average Mortgage Loan Cut-off Date LTV(4): | 50.1% | |||

| Weighted Average Mortgage Loan Maturity Date or ARD LTV(4): | 49.1% | |||

| Weighted Average U/W NOI Debt Yield: | 13.5% | |||

Amortization Overview | ||||

| % Mortgage Loans with Amortization through Maturity Date or ARD: | 17.4% | |||

| % Mortgage Loans which pay Interest Only through Maturity or ARD Date: | 81.2% | |||

| % Mortgage Loans which pay Interest Only followed by Amortization through Maturity Date or ARD: | 1.5% | |||

| Weighted Average Remaining Amortization Term (months)(5): | 352 | |||

Loan Structural Features | ||||

| % Mortgage Loans with Upfront or Ongoing Tax Reserves: | 50.5% | |||

| % Mortgage Loans with Upfront or Ongoing Insurance Reserves: | 21.8% | |||

| % Mortgage Loans with Upfront or Ongoing Replacement Reserves(6): | 53.7% | |||

| % Mortgage Loans with Upfront or Ongoing TI/LC Reserves(7): | 72.9% | |||

| % Mortgage Loans with In Place Hard Lockboxes: | 91.3% | |||

| % Mortgage Loans with Cash Traps Triggered at DSCR Levels ≥ 1.15x: | 72.0% | |||

| % Mortgage Loans with Cash Traps Triggered at Debt Yield Levels ≥ 8.0%: | 41.7% | |||

| Prepayment Provisions(8) | ||||

| % Mortgage Loans with Defeasance Only After a Lockout Period and Prior to an Open Period: | 61.2% | |||

| % Mortgage Loans with Prepayment Only After a Lockout Period and Prior to an Open Period with Defeasance and/or a Yield Maintenance Charge: | 28.9% | |||

| % Mortgage Loans with Prepayment Only After a Lockout Period and Prior to an Open Period with a Yield Maintenance Charge: | 9.9% | |||

| (1) | Includes a $50.0 million non-control pari passu portion of the Green Acres mortgage loan, as to which GSMC is acting as mortgage loan seller of approximately $32.5 million and GACC is acting as the mortgage loan seller of approximately $17.5 million. |

| (2) | Includes a $50.0 million control pari passu portion of the Great Lakes Crossing Outlets mortgage loan, as to which GSMC is acting as mortgage loan seller of approximately $27.5 million and GACC is acting as the mortgage loan seller of approximately $22.5 million. |

| (3) | The LTV, DSCR and Debt Yield calculations include any related pari passu companion loan(s) and exclude any related subordinate companion loan(s) and/or mezzanine loan(s). |

| (4) | With respect to four mortgage loans (20.8%) (CX – 250 Water Street (8.1%), 100 Jefferson Road (4.6%), 9200 Calumet Industrial (4.5%) and Crowne Plaza Union Station (3.7%)), the Cut-off Date LTV and Maturity Date or ARD LTV have been calculated using a value other than the “As Is” appraised value. For additional information please see the footnotes to Annex A-1 in the Preliminary Prospectus. |

| (5) | Excludes mortgage loans which are interest only for the full loan term. |

| (6) | Includes FF&E reserves. |

| (7) | Represents the percent of the allocated Initial Outstanding Pool Balance of office, retail, industrial and mixed use properties only structured with TI/LC reserves. |

| (8) | Please see Annex A-1 of the Preliminary Prospectus for more information. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 3 | ||

Benchmark 2023-B38 Mortgage Trust

| STRUCTURE SUMMARY |

OFFERED CERTIFICATES

| Class(1) | Ratings (Moody’s/Fitch/KBRA) | Initial Certificate Balance or Notional Amount(2) | Initial Subordination | Weighted Average Life (years)(4) | Principal Window (months)(4) | Certificate Principal to Value Ratio(5) | Certificate Underwritten NOI Debt Yield(6) | |

| Class A-1 | Aaa(sf) / AAAsf / AAA(sf) | $6,484,000 | 30.000%(7) | 2.52 | 1 – 56 | 35.1% | 19.3% | |

| Class A-2 | Aaa(sf) / AAAsf / AAA(sf) | $201,433,000 | 30.000%(7) | 4.86 | 56 – 60 | 35.1% | 19.3% | |

| Class A-3 | Aaa(sf) / AAAsf / AAA(sf) | $50,784,000 | 30.000%(7) | 6.75 | 79 – 84 | 35.1% | 19.3% | |

| Class A-SB | Aaa(sf) / AAAsf / AAA(sf) | $4,164,000 | 30.000%(7) | 6.92 | 60 – 111 | 35.1% | 19.3% | |

| Class A-4 | Aaa(sf) / AAAsf / AAA(sf) | $173,967,000 | 30.000%(7) | 9.64 | 111 – 118 | 35.1% | 19.3% | |

| Class X-A(8) | Aa1(sf) / AAAsf / AAA(sf) | $507,037,000 | (9) | N/A | N/A | N/A | N/A | N/A |

| Class A-M | Aa1(sf) / AAAsf / AAA(sf) | $70,205,000 | 18.750% | 9.82 | 118 – 118 | 40.7% | 16.6% | |

| Class B | Aa3(sf) / AA-sf / AA-(sf) | $31,202,000 | 13.750% | 9.86 | 118 – 119 | 43.2% | 15.7% | |

| Class C | A3(sf) / A-sf / A-(sf) | $24,182,000 | 9.875% | 9.97 | 119 – 120 | 45.2% | 15.0% | |

NON-OFFERED CERTIFICATES

| Class(1) | Ratings (Moody’s/Fitch/KBRA) | Initial Certificate Balance or Notional Amount (2) | Initial Subordination | Weighted Average Life (years)(4) | Principal Window (months)(4) | Certificate Principal to Value Ratio(5) | Certificate Underwritten NOI Debt Yield(6) | |

| Class X-D(8) | Baa3(sf) / BBB-sf / BBB-(sf) | $21,062,000 | (9) | N/A | N/A | N/A | N/A | N/A |

| Class X-F(8) | Ba1(sf) / BB-sf / BB(sf) | $12,481,000 | (9) | N/A | N/A | N/A | N/A | N/A |

| Class X-G(8) | B2(sf) / NR / B-(sf) | $10,140,000 | (9) | N/A | N/A | N/A | N/A | N/A |

| Class X-H(8) | NR / NR / NR | $17,942,153 | (9) | N/A | N/A | N/A | N/A | N/A |

| Class D | Baa2(sf) / BBBsf / BBB(sf) | $14,821,000 | 7.500% | 9.98 | 120 – 120 | 46.3% | 14.6% | |

| Class E | Baa3(sf) / BBB-sf / BBB-(sf) | $6,241,000 | 6.500% | 9.98 | 120 – 120 | 46.8% | 14.4% | |

| Class F | Ba1(sf) / BB-sf / BB(sf) | $12,481,000 | 4.500% | 9.98 | 120 – 120 | 47.8% | 14.1% | |

| Class G | B2(sf) / NR / B-(sf) | $10,140,000 | 2.875% | 9.98 | 120 – 120 | 48.7% | 13.9% | |

| Class H | NR / NR / NR | $17,942,153 | 0.000% | 9.98 | 120 – 120 | 50.1% | 13.5% | |

NON-OFFERED LOAN-SPECIFIC CERTIFICATES

| Class(1) | Ratings (Fitch) | Initial Certificate Balance(2) | Initial Subordination | Weighted Average Life (years)(4) | Principal Window (months)(4) | Certificate Principal to Value Ratio(10) | Certificate Underwritten NOI Debt Yield(11) | |

| Class PDC-A1(12) | BBsf | $10,000,000 | 3.774% | 9.82 | 118 – 118 | 49.8% | 13.2% | |

| Class PDC-A2(12) | BBsf | $9,000,000 | 0.377% | 9.82 | 118 – 118 | 51.5% | 12.8% | |

| Class PDC-HRR(12) | BBsf | $1,000,000 | 0.000% | 9.82 | 118 – 118 | 51.7% | 12.7% | |

NON-OFFERED VERTICAL RISK RETENTION INTEREST

| Non-Offered Vertical Risk Retention Interest | Ratings (Moody’s/Fitch/KBRA) | Initial Certificate Balance or Interest Balance | Initial Subordination | Weighted Average Life (years)(13) | Principal Window (months)(13) | Certificate Principal to Value Ratio | Certificate Underwritten NOI Debt Yield | |

| Class RR(14)(15) | NR / NR / NR | $12,658,410 | N/A | 7.85 | 1 – 120 | N/A | N/A | |

| RR Interest(14)(15) | NR / NR / NR | $20,186,125 | N/A | 7.85 | 1 – 120 | N/A | N/A | |

| (1) | The pass-through rates for the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4, Class A-M, Class B, Class C, Class D, Class E, Class F, Class G and Class H certificates (collectively, the “Pooled Principal Balance Certificates”) in each case, will be one of: (i) a fixed per annum rate, (ii) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which such Distribution Date occurs (the “WAC Rate”), (iii) a rate equal to the lesser of a specified pass-through rate and the WAC Rate or (iv) the WAC Rate less a specified rate, but in any case not less than 0.000%. The pass-through rates applicable to the Class PDC-A1, Class PDC-A2 and Class PDC-HRR certificates (collectively, the “Loan-Specific Certificates”), in each case, will be a per annum rate equal the net mortgage rate applicable to the trust subordinate companion loan related to the Pacific Design Center whole loan (the “Trust Subordinate Companion Loan”). |

| (2) | Approximate; subject to a variance of plus or minus 5%. The VRR Interest Balance of the VRR Interest is not included in the Certificate Balance or Notional Amount of any Class of Certificates set forth under "Offered Certificates" or "Non-Offered Certificates" in the table above. |

| (3) | The initial subordination levels are calculated based on the initial Certificate Balance. The approximate initial credit support percentage for each class of Pooled Principal Balance Certificates does not include the subordination provided by the Trust Subordinate Companion Loan. None of the Loan-Specific Certificates will provide credit support to any other class of certificates, except to the extent of the subordination of the Trust Subordinate Companion Loan (in which the Loan-Specific Certificates each represent an interest) to the Pacific Design Center mortgage loan. The initial credit support percentages of the Loan-Specific Certificates are based on the Pacific Design Center whole loan. The approximate initial credit support percentages shown in the table above do not take into account the VRR Interest. However, losses incurred on the mortgage loans will be allocated between the VRR Interest and the Pooled Principal Balance Certificates, pro rata in accordance with their respective percentage allocation entitlement. See “Credit Risk Retention” and “Description of the Certificates” in the Preliminary Prospectus. |

| (4) | The weighted average life and principal window during which distributions of principal would be received as set forth in the table with respect to each class of Pooled Principal Balance Certificates and the Loan-Specific Certificates are based on (i) modeling assumptions described in the Preliminary Prospectus and Loan-Specific PPM, as applicable, and (ii) assumptions that there are no prepayments, modifications or losses in respect of the mortgage loans and there are no extensions or forbearances of maturity dates or anticipated repayment dates of the mortgage loans (or, in the case of the Loan-Specific Certificates, the Trust Subordinate Companion Loan). |

| (5) | “Certificate Principal to Value Ratio” for any class of Pooled Principal Balance Certificates is calculated as the product of (a) the weighted average mortgage loan Cut-off Date LTV of the mortgage loans, multiplied by (b) a fraction, the numerator of which is the total initial Certificate Balance of the related class of Pooled Principal Balance Certificates and all other classes of Pooled Principal Balance Certificates, if any, that are senior to such class (and the VRR Interest Balance of any portion of the VRR Interest that is considered to be pari passu or senior to such class), and the denominator of which is the total initial Certificate Balance of all classes of Pooled Principal Balance Certificates and the initial VRR Interest Balance of the VRR Interest. The Certificate Principal to Value Ratios of the Class A-1, Class A-2, Class A-3, Class A-SB and Class A-4 certificates are calculated in the aggregate for those classes as if they were a single class. |

| (6) | “Certificate Underwritten NOI Debt Yield” for any class of Pooled Principal Balance Certificates is calculated as the product of (a) the weighted average Underwritten NOI Debt Yield for the mortgage loans, multiplied by (b) a fraction, the numerator of which is the total initial Certificate Balance of all classes of Pooled Principal Balance Certificates and the initial VRR Interest Balance of the VRR Interest and the denominator of which is the total initial Certificate Balance of such class of Pooled Principal Balance Certificates and all other classes of Pooled Principal Balance Certificates, if any, that are senior to such class (and the VRR Interest Balance of any portion of the VRR Interest that is considered to be pari passu or senior to such class). The Underwritten NOI Debt Yields of the Class A-1, Class A-2, Class A-3, Class A-SB and Class A-4 certificates are calculated in the aggregate for those classes as if they were a single class. |

| (7) | The initial subordination levels for the Class A-1, Class A-2, Class A-3, Class A-SB and Class A-4 certificates are represented in the aggregate. |

| (8) | As further described in the Preliminary Prospectus, the pass-through rate applicable to the Class X-A, Class X-D, Class X-F, Class X-G and Class X-H certificates (collectively, the “Class X Certificates” and, together with the Pooled Principal Balance Certificates and Class S Certificates, the “Non-VRR Certificates” and, together with the Class RR Certificates, the “Pooled Certificates”) for each Distribution Date will generally be equal to the excess of (i) the WAC Rate over (ii)(A) with respect to the Class X-A certificates, the weighted average of the pass-through rates of the Class A-1, Class |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 4 | ||

Benchmark 2023-B38 Mortgage Trust

| STRUCTURE SUMMARY |

A-2, Class A-3, Class A-SB, Class A-4 and Class A-M certificates (based on their respective Certificate Balances outstanding immediately prior to such Distribution Date), (B) with respect to the Class X-D certificates, the weighted average of the pass-through rates of the Class D and Class E certificates (based on their respective Certificate Balances outstanding immediately prior to such Distribution Date), (C) with respect to the Class X-F certificates, the pass-through rate of the Class F certificates, (D) with respect to the Class X-G certificates, the pass-through rate of the Class G certificates and (E) with respect to the Class X-H certificates, the pass-through rate of the Class H certificates.

| (9) | The Class X Certificates will not have Certificate Balances. None of the Class X Certificates will be entitled to distributions of principal. The interest accrual amounts on the Class X-A certificates will be calculated by reference to a notional amount equal to the aggregate Certificate Balances of the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4 and Class A-M certificates. The interest accrual amounts on the Class X-D certificates will be calculated by reference to a notional amount equal to the aggregate Certificate Balances of the Class D and Class E certificates. The interest accrual amounts on the Class X-F certificates will be calculated by reference to a notional amount equal to the Certificate Balance of the Class F certificates. The interest accrual amounts on the Class X-G certificates will be calculated by reference to a notional amount equal to the Certificate Balance of the Class G certificates. The interest accrual amounts on the Class X-H certificates will be calculated by reference to a notional amount equal to the Certificate Balance of the Class H certificates. The notional amount of each class of Class X Certificates is subject to change depending upon the final pricing of the Pooled Principal Balance Certificates, as follows: (1) if as a result of such pricing the pass-through rate of any class of Pooled Principal Balance Certificates whose Certificate Balance comprises such notional amount is equal to the WAC Rate, the Certificate Balance of such class of Pooled Principal Balance Certificates may not be part of, and will reduce accordingly, such notional amount of such class of Class X Certificates (or, if as a result of such pricing the pass-through rate of such class of Class X Certificates is equal to zero, such class of Class X Certificates may not be issued on the Closing Date), and/or (2) if as a result of such pricing the pass-through rate of any class of Pooled Principal Balance Certificates that does not comprise such notional amount of such class of Class X Certificates is less than the WAC Rate, such class of Pooled Principal Balance Certificates may become a part of, and increase accordingly, such notional amount of such class of Class X Certificates. |

| (10) | The “Certificate Principal to Value Ratio” for any class of Loan-Specific Certificates is (x) the sum of (i) the initial Certificate Balance of such class of Loan-Specific Certificates and all other classes of Loan-Specific Certificates, if any, that are senior to such class and (ii) the principal balance as of the Cut-off Date of the Pacific Design Center Senior Notes divided by (y) $512,500,000, which represents the appraised value (based on certain extraordinary assumptions as described under “Description of the Mortgage Pool—Appraised Value” in the Preliminary Prospectus) of the Pacific Design Center Mortgaged Property as of November 17, 2022. |

| (11) | The “Certificate Underwritten NOI Debt Yield” for any class of Loan-Specific Certificates means, (x) the Pacific Design Center Mortgage Loan Underwritten NOI of $33,781,880 divided by (y) the sum of (i) the initial Certificate Balance of such class of Loan-Specific Certificates and all other classes of Loan-Specific Certificates, if any, that are senior to such class and (ii) the principal balance as of the Cut-off Date of the Pacific Design Center Senior Notes. |

| (12) | The Loan-Specific Certificates will only be entitled to receive distributions from, and will only incur losses with respect to, the Trust Subordinate Companion Loan. The Trust Subordinate Companion Loan will be included as an asset of the issuing entity but will not be part of the mortgage pool backing the Pooled Certificates or the RR Interest. No class of Pooled Certificates or the RR Interest will have any interest in the Trust Subordinate Companion Loan. See “Description of the Mortgage Pool—The Whole Loans—The Serviced AB Whole Loan—Pacific Design Center Whole Loan” in the Preliminary Prospectus. |

| (13) | The weighted average life and principal window during which distributions of principal would be received as set forth in the foregoing table with respect to the VRR Interest (as defined below) are based on the assumptions set forth under “Yield and Maturity Considerations—Weighted Average Life” in the Preliminary Prospectus and on the assumptions that there are no prepayments, modifications or losses in respect of the mortgage loans and that there are no extensions or forbearances of maturity dates or anticipated repayment dates of the mortgage loans. |

| (14) | German American Capital Corporation, as the retaining sponsor, is expected to acquire from the depositor, on the Closing Date, an “eligible vertical interest” (as defined in Regulation RR) in the form of a single vertical security comprised of the Class RR certificates and the RR interest (collectively, the “VRR Interest”), representing approximately (but not less than) 5.00% of all amounts collected on the mortgage loans (net of expenses of the issuing entity) that are available for distribution on the Non-VRR Certificates and the VRR Interest. A portion of the VRR Interest will be retained by each of German American Capital Corporation or its “majority-owned affiliate”, JPMCB and Goldman Sachs Bank USA in accordance with the credit risk retention rules applicable to the pooled securitization transaction. See “Credit Risk Retention” in the Preliminary Prospectus. |

| (15) | Although it does not have a specified pass-through rate (other than for tax reporting purposes), the effective interest rate for the Class RR Certificates and the RR Interest will be the WAC rate. |

| Class A-2 Principal Paydown(1) |

| Class | Mortgage Loan Seller | Mortgage Loan | Property Type | Cut-off Date Balance | Remaining Term to Maturity (Mos.) | Cut-off Date LTV Ratio | U/W NCF DSCR | U/W NOI Debt Yield | |

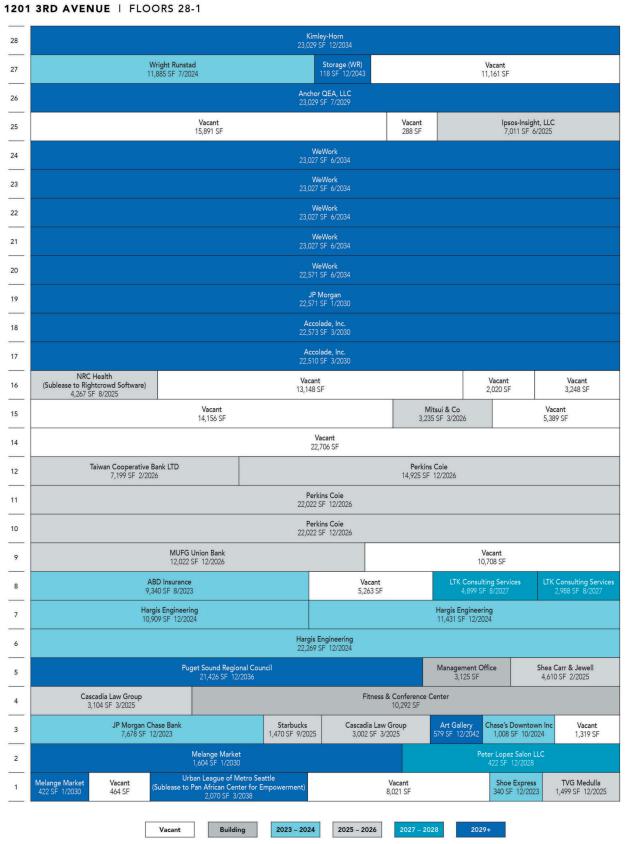

| A-2 | JPMCB | 1201 Third Avenue | Office | $60,000,000 | 59 | 30.5% | 2.76x | 17.7% | |

| A-2 | GSMC, GACC | Green Acres | Retail | $50,000,000 | 57 | 54.5% | 2.10x | 13.0% | |

| A-2 | GSMC | Scottsdale Fashion Square | Retail | $49,000,000 | 59 | 38.4% | 1.92x | 12.3% | |

| A-2 | CREFI | National Warehouse & Distribution Portfolio | Industrial | $35,000,000 | 60 | 56.7% | 1.54x | 13.0% | |

| A-2 | GACC | Sentinel Square II | Office | $10,000,000 | 56 | 62.3% | 1.47x | 9.1% | |

| A-2 | GACC | Centers of High Point | Mixed Use | $9,642,857 | 58 | 67.2% | 2.03x | 16.5% | |

| (1) | This table reflects the mortgage loans whose balloon payments will be applied to pay down the Class A-2 certificates, assuming (i) that none of the mortgage loans experience prepayments, defaults or losses, (ii) there are no extensions of maturity dates and (iii) each mortgage loan is paid in full on its stated maturity date. See “Yield and Maturity Considerations—Yield Considerations” in the Preliminary Prospectus. |

| Class A-3 Principal Paydown(1) |

| Class | Mortgage Loan Seller | Mortgage Loan | Property Type | Cut-off Date Balance | Remaining Term to Maturity (Mos.) | Cut-off Date LTV Ratio(2) | U/W NCF DSCR | U/W NOI Debt Yield | |

| A-3 | CREFI | 9200 Calumet Industrial | Industrial | $29,500,000 | 79 | 47.1% | 1.57x | 11.9% | |

| A-3 | GACC | Naugatuck Valley Shopping Center | Retail | $27,749,936 | 84 | 66.2% | 1.49x | 11.1% | |

| (1) | This table reflects the mortgage loans whose balloon payments will be applied to pay down the Class A-3 certificates, assuming (i) that none of the mortgage loans experience prepayments, defaults or losses, (ii) there are no extensions of maturity dates and (iii) each mortgage loan is paid in full on its stated maturity date. See “Yield and Maturity Considerations—Yield Considerations” in the Preliminary Prospectus. |

| (2) | With respect to the 9200 Calumet Industrial mortgage loan, the Cut-off Date LTV has been calculated using a value other than the “As Is” appraised value. For additional information please see the footnotes to Annex A-1 in the Preliminary Prospectus. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 5 | ||

Benchmark 2023-B38 Mortgage Trust

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

| Ten Largest Mortgage Loans | |||||||||

| Mortgage Loan | Mortgage Loan Seller | City, State | Property Type | Mortgage Loan Cut-off Date | % of Initial Outstanding Pool Balance | Cut-off Date Balance per NRA/Unit(1) | Cut-off Date LTV(1)(2) | U/W NCF DSCR after IO(1) | U/W NOI Debt Yield(1) |

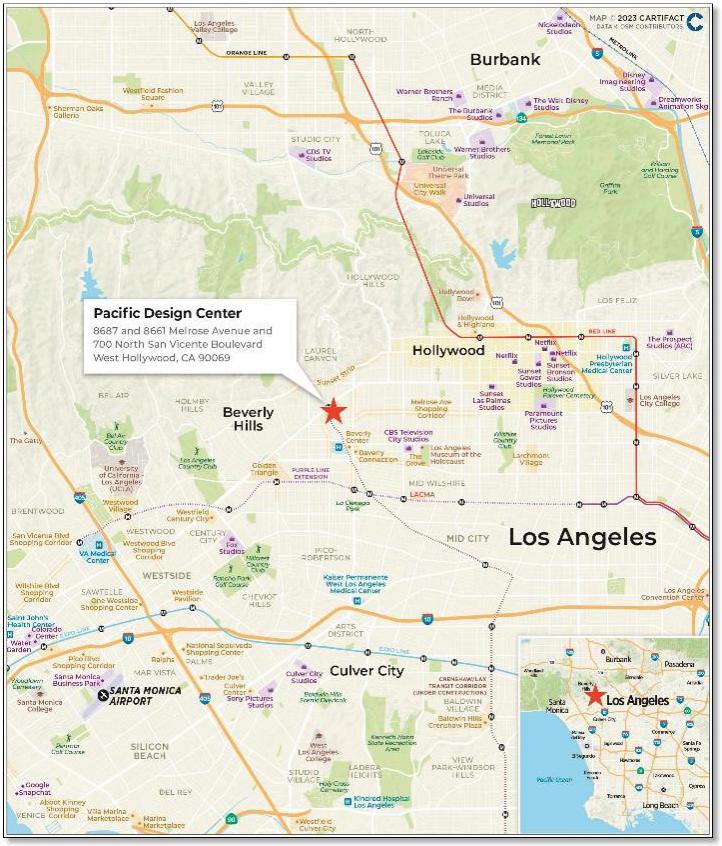

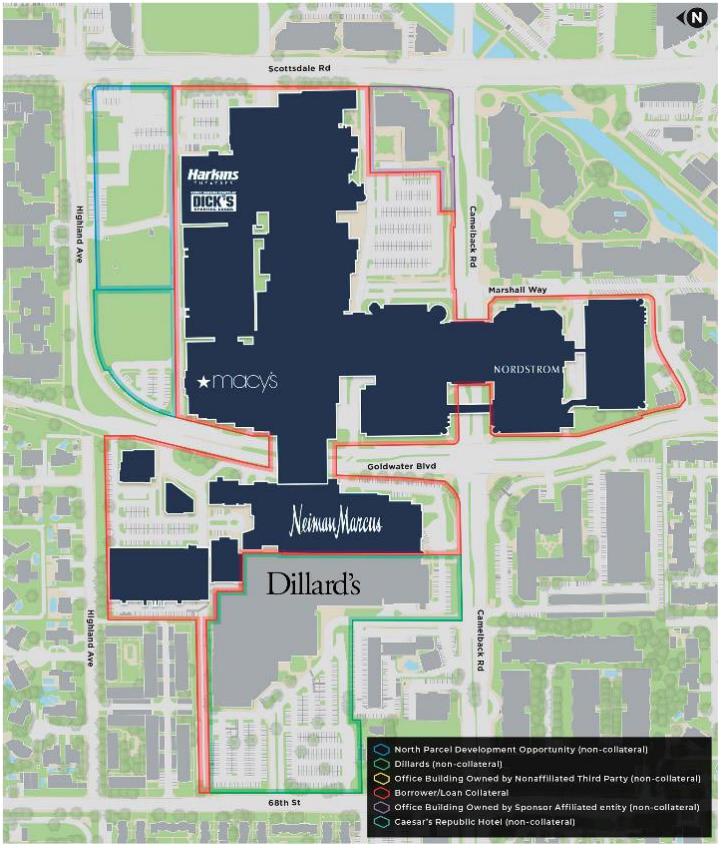

| Pacific Design Center | GSMC | West Hollywood, CA | Mixed Use | $65,600,000 | 9.99% | $233 | 47.8% | 2.17x | 13.8% |

| 1201 Third Avenue | JPMCB | Seattle, WA | Office | $60,000,000 | 9.1% | $150 | 30.5% | 2.76x | 17.7% |

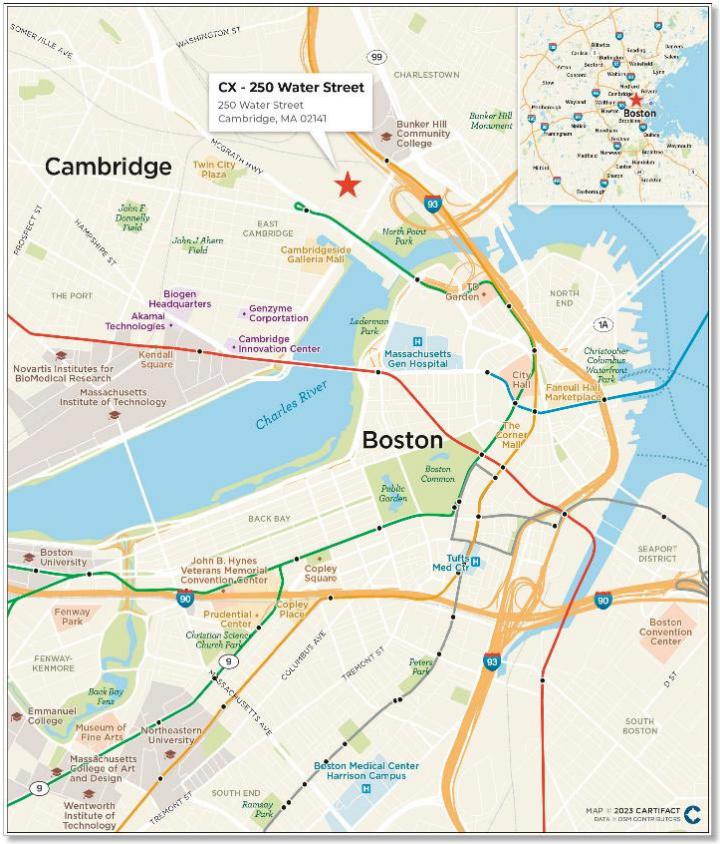

| CX - 250 Water Street | GSMC | Cambridge, MA | Mixed Use | $53,150,000 | 8.1% | $1,110 | 48.8% | 1.66x | 9.3% |

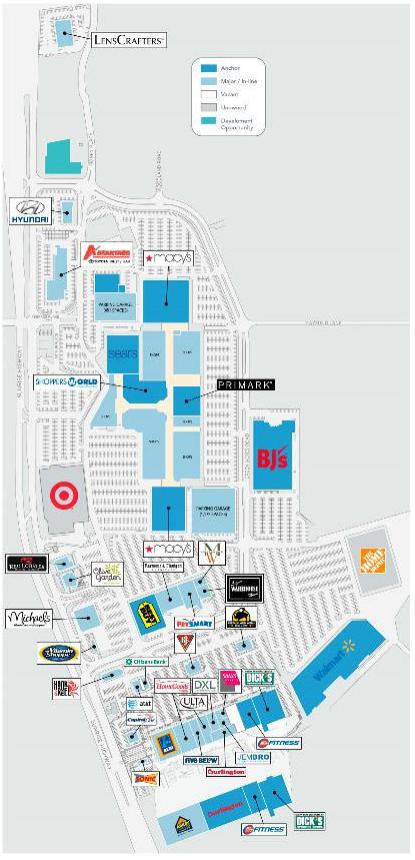

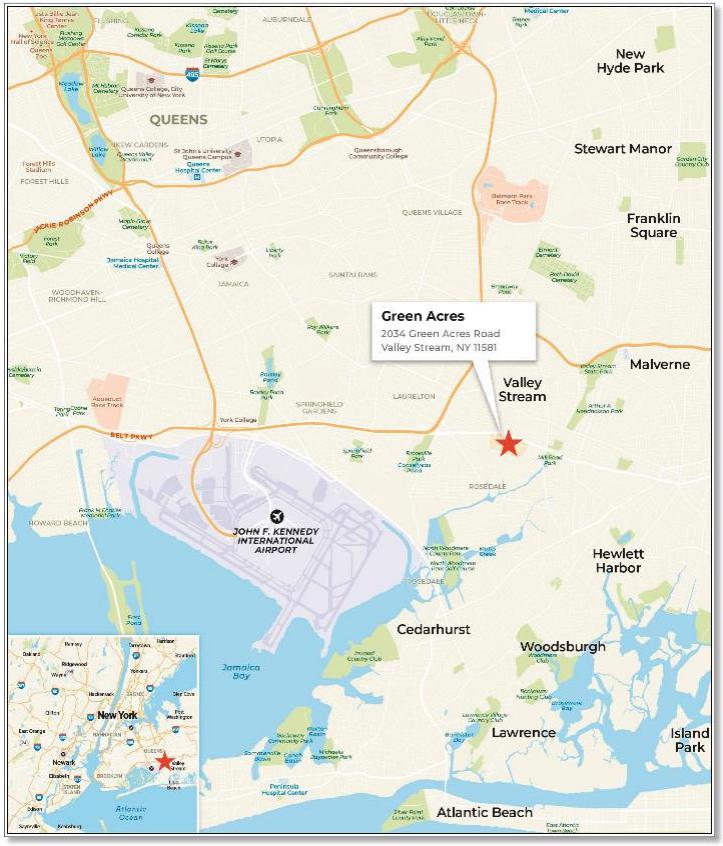

| Green Acres | GSMC, GACC | Valley Stream, NY | Retail | $50,000,000 | 7.6% | $178 | 54.5% | 2.10x | 13.0% |

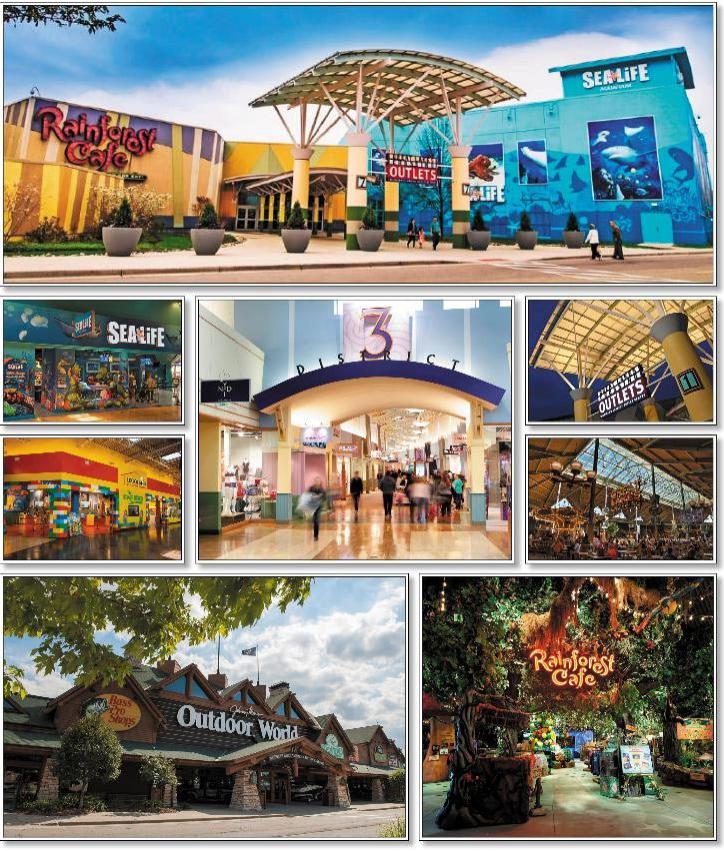

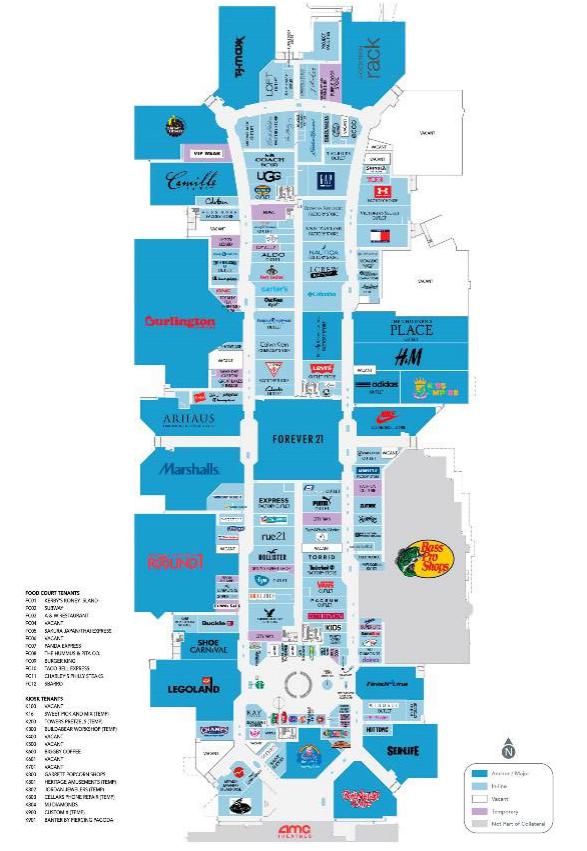

| Great Lakes Crossing Outlets | GSMC, GACC | Auburn Hills, MI | Retail | $50,000,000 | 7.6% | $160 | 45.0% | 2.50x | 17.5% |

| Scottsdale Fashion Square | GSMC | Scottsdale, AZ | Retail | $49,000,000 | 7.5% | $450 | 38.4% | 1.92x | 12.3% |

| National Warehouse & Distribution Portfolio | CREFI | Various | Industrial | $35,000,000 | 5.3% | $40 | 56.7% | 1.54x | 13.0% |

| 100 Jefferson Road | JPMCB | Parsippany, NJ | Industrial | $30,000,000 | 4.6% | $174 | 56.4% | 1.42x | 10.7% |

| 9200 Calumet Industrial | CREFI | Munster, IN | Industrial | $29,500,000 | 4.5% | $32 | 47.1% | 1.57x | 11.9% |

| Naugatuck Valley Shopping Center | GACC | Waterbury, CT | Retail | $27,749,936 | 4.2% | $72 | 66.2% | 1.49x | 11.1% |

| Total/Weighted Average | $449,999,936 | 68.5% | 47.4% | 2.01x | 13.4% | ||||

| (1) | The Cut-off Date Balance per NRA/Unit, Cut-off Date LTV, U/W NCF DSCR after IO and U/W NOI Debt Yield calculations include any related pari passu companion loan(s) and exclude any related subordinate companion loan(s) and/or mezzanine loan(s). |

| (2) | With respect to the CX – 250 Water Street, 100 Jefferson Road and 9200 Calumet Industrial mortgage loans, the Cut-off Date LTV has been calculated using a value other than the “As Is” appraised value. For additional information please see the footnotes to Annex A-1 in the Preliminary Prospectus. |

| Subordinate Debt Summary | ||||||||||

| Mortgage Loan | Mortgage Loan Cut-off Date Balance |

Pari Passu Companion Loans Cut-off Date Balance | Subordinate Debt Cut-off Date Balance | Mezzanine Debt Cut-off Date Balance | Trust U/W NCF DSCR(1) | Total Debt U/W NCF DSCR(2) | Trust Cut-off Date LTV(1)(3) | Total Debt Cut-off Date LTV(2)(3) | Trust U/W NOI Debt Yield(1) | Total Debt U/W NOI Debt Yield(2) |

| Pacific Design Center | $65,600,000 | $179,400,000 | $20,000,000 | $0 | 2.17x | 1.79x | 47.8% | 51.7% | 13.8% | 12.7% |

| 9200 Calumet Industrial | $29,500,000 | $0 | $0 | $8,500,000 | 1.57x | 1.14x | 47.1% | 60.7% | 11.9% | 9.2% |

| (1) | The Trust U/W NCF DSCR, Trust Cut-off Date LTV and Trust U/W NOI Debt Yield calculations include any related pari passu companion loan(s) and exclude any related subordinate companion loan(s) and/or mezzanine loan(s). |

| (2) | Total Debt U/W NCF DSCR, Total Debt Cut-off Date LTV and Total Debt U/W NOI Debt Yield calculations include any related pari passu companion loan(s), related subordinate companion loan(s) and/or related mezzanine loan(s). |

| (3) | With respect to the 9200 Calumet Industrial mortgage loan, the Trust Cut-off Date LTV and Total Debt Cut-off Date LTV have been calculated using a value other than the “As Is” appraised value. For additional information please see the footnotes to Annex A-1 in the Preliminary Prospectus. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 6 | ||

Benchmark 2023-B38 Mortgage Trust

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

| Companion Loan Summary |

| Loan No. | Mortgage Loan | Note(s) | Original Balance | Cut-off Date Balance | Holder of Note(1) | Lead Servicer for Whole Loan (Y/N) | Master Servicer Under Lead Securitization | Special Servicer Under Lead Securitization |

| 1 | Pacific Design Center | A-1 | $65,600,000 | $65,600,000 | Benchmark 2023-B38 | Yes | ||

| A-2 | $34,400,000 | $34,400,000 | GSBI | No | ||||

| A-3 | $30,000,000 | $30,000,000 | GSBI | No | ||||

| A-4 | $40,000,000 | $40,000,000 | Argentic | No | ||||

| A-5 | $15,000,000 | $15,000,000 | Argentic | No | ||||

| A-6 | $10,000,000 | $10,000,000 | Argentic | No | ||||

| A-7 | $10,000,000 | $10,000,000 | Argentic | No | ||||

| A-8 | $25,000,000 | $25,000,000 | BMO | No | ||||

| A-9 | $15,000,000 | $15,000,000 | BMO | No | ||||

| B | $20,000,000 | $20,000,000 | Benchmark 2023-B38 (Loan Specific Certificates) | Yes | Midland | Argentic | ||

| 2 | 1201 Third Avenue | A-1-1 | $30,000,000 | $30,000,000 | BANK5 2023-5YR1(2) | No(3) | Wells Fargo(3) | CWCapital(3) |

| A-1-2 | $20,000,000 | $20,000,000 | MSBNA | No | ||||

| A-1-3 | $10,000,000 | $10,000,000 | MSBNA | No | ||||

| A-2 | $42,000,000 | $42,000,000 | MSBNA | Yes(3) | ||||

| A-3 | $40,000,000 | $40,000,000 | Benchmark 2023-B38 | No | ||||

| A-4-1 | $20,000,000 | $20,000,000 | Benchmark 2023-B38 | No | ||||

| A-4-2 | $8,000,000 | $8,000,000 | JPMCB | No | ||||

| 3 | CX - 250 Water Street | A-1 | $56,250,000 | $56,250,000 | BOA | Yes(4) | ||

| A-2 | $53,125,000 | $53,125,000 | BOA | No | ||||

| A-3 | $50,000,000 | $50,000,000 | BOA | No | ||||

| A-4 | $34,375,000 | $34,375,000 | BANK 2023-BNK45 | No(4) | Wells Fargo(4) | LNR(4) | ||

| A-5 | $46,875,000 | $46,875,000 | BOA | No | ||||

| A-6 | $6,250,000 | $6,250,000 | BOA | No | ||||

| A-7 | $3,125,000 | $3,125,000 | BOA | No | ||||

| A-8 | $15,750,000 | $15,750,000 | BOA | No | ||||

| A-9 | $33,750,000 | $33,750,000 | WFB | No | ||||

| A-10 | $31,875,000 | $31,875,000 | WFB | No | ||||

| A-11 | $30,000,000 | $30,000,000 | WFB | No | ||||

| A-12 | $20,625,000 | $20,625,000 | BANK 2023-BNK45 | No(4) | Wells Fargo(4) | LNR(4) | ||

| A-13 | $28,125,000 | $28,125,000 | WFB | No | ||||

| A-14 | $3,750,000 | $3,750,000 | WFB | No | ||||

| A-15 | $1,875,000 | $1,875,000 | WFB | No | ||||

| A-16 | $9,450,000 | $9,450,000 | WFB | No | ||||

| A-17 | $30,000,000 | $30,000,000 | Benchmark 2023-B38 | No | ||||

| A-18 | $23,150,000 | $23,150,000 | Benchmark 2023-B38 | No | ||||

| A-19 | $25,000,000 | $25,000,000 | 3650 | No | ||||

| A-20 | $28,150,000 | $28,150,000 | 3650 | No | ||||

| 4 | Green Acres | A-1 | $36,000,000 | $36,000,000 | GSBI | Yes(5) | ||

| A-2 | $31,500,000 | $31,500,000 | FIVE 2023-V1 | No | ||||

| A-3 | $32,500,000 | $32,500,000 | Benchmark 2023-B38 | No | ||||

| A-4 | $24,000,000 | $24,000,000 | BMO | No | ||||

| A-5 | $21,500,000 | $21,500,000 | BMO | No | ||||

| A-6 | $20,000,000 | $20,000,000 | BMO 2023-C4 | No(5) | Midland(5) | LNR(5) | ||

| A-7 | $18,500,000 | $18,500,000 | FIVE 2023-V1 | No | ||||

| A-8 | $6,000,000 | $6,000,000 | BMO 2023-C4 | No(5) | Midland(5) | LNR(5) | ||

| A-9 | $50,000,000 | $50,000,000 | MS | No | ||||

| A-10 | $20,000,000 | $20,000,000 | MS | No | ||||

| A-11 | $10,000,000 | $10,000,000 | MS | No | ||||

| A-12 | $10,000,000 | $10,000,000 | MS | No | ||||

| A-13-1 | $25,000,000 | $25,000,000 | DBRI | No | ||||

| A-13-2 | $5,000,000 | $5,000,000 | DBRI | No | ||||

| A-14 | $25,000,000 | $25,000,000 | FIVE 2023-V1 | No | ||||

| A-15-1 | $17,500,000 | $17,500,000 | Benchmark 2023-B38 | No | ||||

| A-15-2 | $2,500,000 | $2,500,000 | DBRI | No | ||||

| A-16 | $15,000,000 | $15,000,000 | DBRI | No |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 7 | ||

Benchmark 2023-B38 Mortgage Trust

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

| Loan No. | Mortgage Loan | Note(s) | Original Balance | Cut-off Date Balance | Holder of Note | Lead Servicer for Whole Loan (Y/N) | Master Servicer Under Lead Securitization | Special Servicer Under Lead Securitization |

| 5 | Great Lakes | A-1-1 | $27,500,000 | $27,500,000 | Benchmark 2023-B38 | Yes | Midland | LNR |

| Crossing Outlets | A-1-2 | $17,500,000 | $17,500,000 | GSBI | No | |||

| A-1-3 | $17,500,000 | $17,500,000 | GSBI | No | ||||

| A-1-4 | $17,500,000 | $17,500,000 | GSBI | No | ||||

| A-2-1-A | $12,500,000 | $12,500,000 | DBRI | No | ||||

| A-2-1-B | $7,500,000 | $7,500,000 | Benchmark 2023-B38 | No | ||||

| A-2-2 | $15,000,000 | $15,000,000 | Benchmark 2023-B38 | No | ||||

| A-2-3 | $15,000,000 | $15,000,000 | DBRI | No | ||||

| A-3-1 | $25,750,000 | $25,750,000 | BMO 2023-C4 | No | ||||

| A-3-2 | $14,250,000 | $14,250,000 | BMO | No | ||||

| A-3-3 | $10,000,000 | $10,000,000 | BMO | No | ||||

| 6 | Scottsdale Fashion | A-1-S1 | $250,000,000 | $250,000,000 | SCOTT 2023-SFS | Yes | Berkadia | KeyBank |

| A-2-S1 | $250,000,000 | $250,000,000 | SCOTT 2023-SFS | No | ||||

| A-1-C1 | $25,000,000 | $25,000,000 | Benchmark 2023-B38 | No | ||||

| A-1-C2 | $24,000,000 | $24,000,000 | Benchmark 2023-B38 | No | ||||

| A-1-C3 | $26,000,000 | $26,000,000 | GSBI | No | ||||

| A-1-C4 | $25,000,000 | $25,000,000 | GSBI | No | ||||

| A-2-C1 | $40,000,000 | $40,000,000 | DBNY | No | ||||

| A-2-C2 | $30,000,000 | $30,000,000 | DBNY | No | ||||

| A-2-C3-1 | $25,000,000 | $25,000,000 | DBNY | No | ||||

| A-2-C3-2 | $5,000,000 | $5,000,000 | DBNY | No | ||||

| 7 | National Warehouse & Distribution Portfolio | A-1 | $50,000,000 | $50,000,000 | BANK5 2023-5YR1 | Yes | Wells Fargo | CWCapital |

| A-2 | $30,000,000 | $30,000,000 | BANK5 2023-5YR1 | No | ||||

| A-3 | $30,000,000 | $30,000,000 | Benchmark 2023-B38 | No | ||||

| A-4-1 | $5,000,000 | $5,000,000 | Benchmark 2023-B38 | No | ||||

| A-4-2 | $22,000,000 | $22,000,000 | CREFI | No | ||||

| A-5 | $20,000,000 | $20,000,000 | BANK5 2023-5YR1 | No | ||||

| 8 | 100 Jefferson Road | A-1 | $30,000,000 | $30,000,000 | Benchmark 2023-B38 | No(6) | Midland(6) | LNR(6) |

| A-2 | $29,500,000 | $29,500,000 | AREF2 or an affiliate | Yes(6) | ||||

| A-3 | $29,500,000 | $29,500,000 | AREF2 or an affiliate | No | ||||

| A-4 | $8,500,000 | $8,500,000 | AREF2 or an affiliate | No | ||||

| 11 | One Campus Martius | A-1 | $50,000,000 | $50,000,000 | Benchmark 2022-B36 | Yes | Midland | Midland |

| A-2 | $30,000,000 | $30,000,000 | Benchmark 2022-B37 | No | ||||

| A-3 | $25,000,000 | $25,000,000 | Benchmark 2023-B38 | No | ||||

| A-4-A | $2,500,000 | $2,500,000 | Benchmark 2023-B38 | No | ||||

| A-4-B | $13,300,000 | $13,300,000 | JPMCB | No | ||||

| A-5 | $10,000,000 | $10,000,000 | JPMCB | No | ||||

| A-6 | $46,200,000 | $46,200,000 | BANK 2022-BNK43 | No | ||||

| A-7 | $25,000,000 | $25,000,000 | BANK 2022-BNK44 | No | ||||

| A-8 | $16,000,000 | $16,000,000 | BANK 2022-BNK44 | No | ||||

| 16 | Riverport Tower | A-1 | $6,600,000 | $6,600,000 | Benchmark 2022-B37 | No | ||

| A-2 | $15,000,000 | $15,000,000 | Benchmark 2023-B38 | Yes | Midland | LNR | ||

| 20 | Sentinel Square II | A-1-1 | $30,000,000 | $30,000,000 | GACC | No | ||

| A-1-2 | $10,000,000 | $10,000,000 | Benchmark 2023-B38 | No | ||||

| A-2 | $25,000,000 | $25,000,000 | FIVE 2023-V1 | Yes | Midland | Greystone | ||

| A-3 | $25,000,000 | $25,000,000 | FIVE 2023-V1 | No | ||||

| A-4 | $14,000,000 | $14,000,000 | FIVE 2023-V1 | No | ||||

| 21 | Centers of High Point | A-1 | $20,000,000 | $20,000,000 | FIVE 2023-V1 | Yes | Midland | Greystone |

| A-2 | $9,642,857 | $9,642,857 | Benchmark 2023-B38 | No |

| (1) | The identification of a securitization trust means we have identified another securitization trust that has closed or as to which a preliminary prospectus (or preliminary offering circular) or final prospectus (or final offering circular) has printed that has or is expected to include the identified Mortgage Note(s). |

| (2) | The BANK5 2023-5YR1 securitization transaction is expected to close on April 19, 2023. |

| (3) | The 1201 Third Avenue Whole Loan is expected to be initially serviced under the BANK5 2023-5YR1 PSA. From and after the securitization of the related controlling note, the 1201 Third Avenue Whole Loan will be serviced under the related pooling and servicing agreement for such securitization. |

| (4) | The CX – 250 Water Street Whole Loan is initially serviced under the BANK 2023-BNK45 PSA. From and after the securitization of the related controlling note, the CX – 250 Water Street Whole Loan will be serviced under the related pooling and servicing agreement for such securitization. |

| (5) | The Green Acres Whole Loan is initially serviced under the BMO 2023-C4 PSA. From and after the securitization of the related controlling note, the Green Acres Whole Loan will be serviced under the related pooling and servicing agreement for such securitization. |

| (6) | Prior to the related servicing shift securitization date, the 100 Jefferson Road whole loan will be serviced under the pooling and servicing agreement for this transaction, provided, however, if one or more non-controlling companion loans is securitized in a transaction before the closing date of the BMARK 2023-B38 transaction, the 100 Jefferson Road whole loan will be a non-serviced whole loan and will be serviced under the servicing agreement for such earlier securitization. From and after the related servicing shift securitization date, the related servicing shift whole loan will be serviced under the related servicing shift pooling and servicing agreement entered into in connection with the securitization of the controlling companion loan. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 8 | ||

Benchmark 2023-B38 Mortgage Trust

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

| Distribution of Cut-off Date Balances(1) | |||||||||||||

| Range of Cut-off Date Balances | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Pool | Weighted Averages | |||||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR | Cut-off Date LTV(2) | Maturity Date or ARD LTV(2) | |||||||||

| $3,888,468 | - | $9,999,999 | 5 | $37,607,575 | 5.7% | 6.6452% | 103 | 1.85x | 58.9% | 56.3% | |||

| $10,000,000 | - | $19,999,999 | 7 | $90,325,000 | 13.8% | 6.5456% | 110 | 1.88x | 52.8% | 51.9% | |||

| $20,000,000 | - | $29,999,999 | 5 | $136,208,114 | 20.7% | 6.4330% | 101 | 1.64x | 57.6% | 54.8% | |||

| $30,000,000 | - | $39,999,999 | 2 | $65,000,000 | 9.9% | 7.0177% | 88 | 1.48x | 56.6% | 54.9% | |||

| $40,000,000 | - | $65,600,000 | 6 | $327,750,000 | 49.9% | 5.9288% | 89 | 2.20x | 44.0% | 44.0% | |||

| Total/Weighted Average | 25 | $656,890,689 | 100.0% | 6.2669% | 95 | 1.95x | 50.1% | 49.1% | |||||

| Distribution of Mortgage Rates(1) | |||||||||||||

| Range of Mortgage Rates | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Pool | Weighted Averages | |||||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR | Cut-off Date LTV(2) | Maturity Date or ARD LTV(2) | |||||||||

| 5.1500% | - | 5.9999% | 6 | $271,499,936 | 41.3% | 5.6829% | 90 | 2.12x | 47.9% | 46.9% | |||

| 6.0000% | - | 6.4999% | 5 | $106,276,250 | 16.2% | 6.1646% | 83 | 1.77x | 48.9% | 48.9% | |||

| 6.5000% | - | 6.9999% | 8 | $164,240,357 | 25.0% | 6.6454% | 102 | 2.00x | 55.3% | 54.2% | |||

| 7.0000% | - | 7.2800% | 6 | $114,874,146 | 17.5% | 7.2007% | 109 | 1.65x | 49.2% | 47.0% | |||

| Total/Weighted Average | 25 | $656,890,689 | 100.0% | 6.2669% | 95 | 1.95x | 50.1% | 49.1% | |||||

| Property Type Distribution(1)(3) | |||||||||||

| Property Type | Number of Mortgaged Properties | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Number of NRA/Units/Rooms | Weighted Averages | ||||||

Cut-off Date NRA/Units/Rooms | Mortgage Rate | Stated Remaining Term (Mos.) | Occupancy | U/W NCF DSCR | Cut-off Date LTV(2) | Maturity Date or ARD LTV(2) | |||||

| Retail | 19 | $258,012,154 | 39.3% | 5,792,203 | $206 | 6.2317% | 91 | 95.9% | 1.98x | 51.3% | 50.2% |

| Anchored | 6 | $88,335,904 | 13.4% | 885,000 | $117 | 6.1749% | 107 | 97.8% | 1.67x | 59.9% | 56.7% |

| Regional Mall | 1 | $50,000,000 | 7.6% | 2,081,286 | $178 | 5.8990% | 57 | 97.7% | 2.10x | 54.5% | 54.5% |

| Outlet Center | 1 | $50,000,000 | 7.6% | 1,128,332 | $160 | 6.5210% | 118 | 89.6% | 2.50x | 45.0% | 45.0% |

| Super Regional Mall | 1 | $49,000,000 | 7.5% | 1,555,459 | $450 | 6.2143% | 59 | 96.0% | 1.92x | 38.4% | 38.4% |

| Single Tenant | 8 | $19,213,750 | 2.9% | 110,786 | $199 | 6.6406% | 118 | 100.0% | 1.88x | 52.0% | 52.0% |

| Unanchored | 2 | $1,462,500 | 0.2% | 31,340 | $50 | 6.3600% | 118 | 78.7% | 1.61x | 63.0% | 63.0% |

| Mixed Use | 9 | $143,892,857 | 21.9% | 2,301,437 | $523 | 5.9461% | 114 | 89.5% | 1.94x | 49.1% | 48.4% |

| Office/Showroom/Lab | 1 | $65,600,000 | 9.99% | 1,053,217 | $233 | 5.9411% | 118 | 78.3% | 2.17x | 47.8% | 47.8% |

| Lab/Office | 1 | $53,150,000 | 8.1% | 479,004 | $1,110 | 5.5095% | 118 | 98.7% | 1.66x | 48.8% | 48.8% |

| Parking Garage/Retail | 1 | $15,500,000 | 2.4% | 287,000 | $54 | 7.1200% | 120 | 100.0% | 1.83x | 44.6% | 39.1% |

| Industrial/Retail | 6 | $9,642,857 | 1.5% | 482,216 | $20 | 6.5000% | 58 | 98.1% | 2.03x | 67.2% | 65.4% |

| Office | 4 | $112,500,000 | 17.1% | 3,087,841 | $161 | 5.7647% | 78 | 84.9% | 2.31x | 44.3% | 44.3% |

| CBD | 3 | $97,500,000 | 14.8% | 2,769,950 | $176 | 5.7554% | 73 | 84.0% | 2.34x | 42.1% | 42.1% |

| Suburban | 1 | $15,000,000 | 2.3% | 317,891 | $68 | 5.8250% | 111 | 90.8% | 2.12x | 58.2% | 58.2% |

| Industrial | 7 | $94,500,000 | 14.4% | 5,418,336 | $70 | 7.0996% | 85 | 100.0% | 1.51x | 53.6% | 52.5% |

| Warehouse/Distribution | 6 | $88,900,000 | 13.5% | 5,158,336 | $73 | 7.1178% | 87 | 100.0% | 1.51x | 53.4% | 52.4% |

| Flex | 1 | $5,600,000 | 0.9% | 260,000 | $22 | 6.8100% | 60 | 100.0% | 1.54x | 56.7% | 53.6% |

| Hospitality | 3 | $47,985,678 | 7.3% | 519 | $102,223 | 6.9559% | 120 | 70.3% | 1.84x | 53.8% | 49.7% |

| Full Service | 1 | $23,985,678 | 3.7% | 273 | $87,860 | 7.1520% | 119 | 55.7% | 1.68x | 47.5% | 41.6% |

| Select Service | 1 | $16,000,000 | 2.4% | 110 | $145,455 | 6.7200% | 120 | 85.7% | 2.01x | 64.0% | 64.0% |

| Extended Stay | 1 | $8,000,000 | 1.2% | 136 | $58,824 | 6.8400% | 120 | 83.3% | 1.95x | 52.3% | 45.4% |

| Total/Weighted Average | 42 | $656,890,689 | 100.0% | 6.2669% | 95 | 91.3% | 1.95x | 50.1% | 49.1% | ||

| Geographic Distribution(1)(3) | ||||||||||||

| State/Location | Number of Properties | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR | Cut-off Date LTV(2) | Maturity Date or ARD LTV(2) | ||||||||

| California | 4 | $93,452,707 | 14.2% | 6.1282% | 110 | 1.99x | 48.9% | 48.4% | ||||

| Southern | 4 | $93,452,707 | 14.2% | 6.1282% | 110 | 1.99x | 48.9% | 48.4% | ||||

| Michigan | 4 | $83,805,000 | 12.8% | 6.3445% | 116 | 2.18x | 51.3% | 51.3% | ||||

| Washington | 1 | $60,000,000 | 9.1% | 5.5850% | 59 | 2.76x | 30.5% | 30.5% | ||||

| Indiana | 2 | $53,485,678 | 8.1% | 7.2226% | 97 | 1.62x | 47.3% | 44.6% | ||||

| Massachusetts | 1 | $53,150,000 | 8.1% | 5.5095% | 118 | 1.66x | 48.8% | 48.8% | ||||

| New York | 1 | $50,000,000 | 7.6% | 5.8990% | 57 | 2.10x | 54.5% | 54.5% | ||||

| Arizona | 1 | $49,000,000 | 7.5% | 6.2143% | 59 | 1.92x | 38.4% | 38.4% | ||||

| Missouri | 2 | $42,472,500 | 6.5% | 6.3295% | 115 | 1.86x | 63.7% | 63.7% | ||||

| New Jersey | 3 | $39,650,000 | 6.0% | 7.1085% | 120 | 1.56x | 55.4% | 55.4% | ||||

| Other | 23 | $131,874,804 | 20.1% | 6.4297% | 93 | 1.74x | 57.7% | 53.9% | ||||

| Total/Weighted Average | 42 | $656,890,689 | 100.0% | 6.2669% | 95 | 1.95x | 50.1% | 49.1% | ||||

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 9 | ||

Benchmark 2023-B38 Mortgage Trust

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

| Distribution of Cut-off Date LTVs(1)(2) | |||||||||||||

| Range of Cut-off Date LTVs | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance |

Weighted Averages | |||||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR | Cut-off Date LTV | Maturity Date or ARD LTV | |||||||||

| 30.5% | - | 39.9% | 2 | $109,000,000 | 16.6% | 5.8679% | 59 | 2.38x | 34.1% | 34.1% | |||

| 40.0% | - | 49.9% | 8 | $261,435,678 | 39.8% | 6.3615% | 114 | 1.97x | 46.9% | 46.0% | |||

| 50.0% | - | 59.9% | 8 | $160,013,468 | 24.4% | 6.5118% | 86 | 1.80x | 55.3% | 54.1% | |||

| 60.0% | - | 67.2% | 7 | $126,441,543 | 19.2% | 6.1054% | 100 | 1.71x | 64.3% | 62.2% | |||

| Total/Weighted Average | 25 | $656,890,689 | 100.0% | 6.2669% | 95 | 1.95x | 50.1% | 49.1% | |||||

| Distribution of Maturity Date or ARD LTVs(1)(2) | |||||||||||||

| Range of Maturity Date or ARD LTVs | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | |||||||||

| Mortgage Rate | Stated Remaining Term (Mos.)(2) | U/W NCF DSCR | Cut-off Date LTV | Maturity Date or ARD LTV | |||||||||

| 30.5% | - | 39.9% | 3 | $124,500,000 | 19.0% | 6.0238% | 67 | 2.31x | 35.4% | 34.7% | |||

| 40.0% | - | 49.9% | 9 | $257,824,146 | 39.2% | 6.3438% | 114 | 1.97x | 47.3% | 46.4% | |||

| 50.0% | - | 59.9% | 7 | $175,874,936 | 26.8% | 6.2661% | 83 | 1.76x | 57.1% | 55.1% | |||

| 60.0% | - | 66.7% | 6 | $98,691,607 | 15.0% | 6.3741% | 104 | 1.77x | 63.7% | 63.5% | |||

| Total/Weighted Average | 25 | $656,890,689 | 100.0% | 6.2669% | 95 | 1.95x | 50.1% | 49.1% | |||||

| Distribution of Underwritten NCF Debt Service Coverages(1) | |||||||||||||

| Range of Underwritten NCF Debt Service Coverages | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | |||||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR | Cut-off Date LTV(2) | Maturity Date or ARD LTV(2) | |||||||||

| 1.34x | - | 1.49x | 4 | $71,638,404 | 10.9% | 6.2721% | 97 | 1.45x | 61.0% | 57.2% | |||

| 1.50x | - | 1.99x | 12 | $299,009,428 | 45.5% | 6.4423% | 97 | 1.71x | 50.6% | 49.3% | |||

| 2.00x | - | 2.49x | 7 | $176,242,857 | 26.8% | 6.1273% | 97 | 2.12x | 53.0% | 52.9% | |||

| 2.50x | - | 2.76x | 2 | $110,000,000 | 16.7% | 6.0105% | 86 | 2.64x | 37.1% | 37.1% | |||

| Total/Weighted Average | 25 | $656,890,689 | 100.0% | 6.2669% | 95 | 1.95x | 50.1% | 49.1% | |||||

| Original Terms to Maturity or ARD(1) | |||||||||||||

| Original Terms to Maturity or ARD | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | |||||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR | Cut-off Date LTV(2) | Maturity Date or ARD LTV(2) | |||||||||

| 60 | - | 60 | 6 | $213,642,857 | 32.5% | 6.0666% | 59 | 2.12x | 45.4% | 44.8% | |||

| 84 | - | 84 | 1 | $29,500,000 | 4.5% | 7.2800% | 79 | 1.57x | 47.1% | 47.1% | |||

| 120 | - | 120 | 18 | $413,747,832 | 63.0% | 6.2981% | 115 | 1.89x | 52.8% | 51.5% | |||

| Total/Weighted Average | 25 | $656,890,689 | 100.0% | 6.2669% | 95 | 1.95x | 50.1% | 49.1% | |||||

| Distribution of Remaining Terms to Maturity or ARD(1) | |||||||||||||

| Range of Remaining Terms to Maturity or ARD | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | |||||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR | Cut-off Date LTV(2) | Maturity Date or ARD LTV(2) | |||||||||

| 56 | - | 60 | 6 | $213,642,857 | 32.5% | 6.0666% | 59 | 2.12x | 45.4% | 44.8% | |||

| 79 | - | 84 | 2 | $57,249,936 | 8.7% | 6.2476% | 81 | 1.53x | 56.4% | 52.0% | |||

| 111 | - | 120 | 17 | $385,997,896 | 58.8% | 6.3807% | 118 | 1.91x | 51.8% | 51.0% | |||

| Total/Weighted Average | 25 | $656,890,689 | 100.0% | 6.2669% | 95 | 1.95x | 50.1% | 49.1% | |||||

Distribution of Underwritten NOI Debt Yields(1) | |||||||||||||

| Range of Underwritten NOI Debt Yields | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | |||||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR | Cut-off Date LTV(2) | Maturity Date or ARD LTV(2) | |||||||||

| 9.1% | - | 10.4% | 2 | $63,150,000 | 9.6% | 5.5951% | 108 | 1.63x | 50.9% | 50.9% | |||

| 10.5% | - | 12.4% | 10 | $225,012,154 | 34.3% | 6.4322% | 95 | 1.66x | 53.6% | 52.3% | |||

| 12.5% | - | 14.4% | 4 | $158,600,000 | 24.1% | 6.1543% | 86 | 2.00x | 52.1% | 51.4% | |||

| 14.5% | - | 17.7% | 9 | $210,128,535 | 32.0% | 6.3768% | 98 | 2.31x | 44.7% | 43.3% | |||

| Total/Weighted Average | 25 | $656,890,689 | 100.0% | 6.2669% | 95 | 1.95x | 50.1% | 49.1% | |||||

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 10 | ||

Benchmark 2023-B38 Mortgage Trust

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

| Amortization Types(1) | |||||||||||

| Amortization Type | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | |||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR | Cut-off Date LTV(2) | Maturity Date or ARD LTV(2) | |||||||

| Interest Only | 17 | $479,973,750 | 73.1% | 6.2819% | 94 | 2.06x | 48.8% | 48.8% | |||

| Amortizing Balloon | 6 | $114,124,082 | 17.4% | 6.5368% | 92 | 1.62x | 55.1% | 49.3% | |||

| Interest Only - ARD | 1 | $53,150,000 | 8.1% | 5.5095% | 118 | 1.66x | 48.8% | 48.8% | |||

| Interest Only, Amortizing Balloon | 1 | $9,642,857 | 1.5% | 6.5000% | 58 | 2.03x | 67.2% | 65.4% | |||

| Total/Weighted Average | 25 | $656,890,689 | 100.0% | 6.2669% | 95 | 1.95x | 50.1% | 49.1% | |||

| (1) | The U/W NCF DSCR, Cut-off Date LTV, Maturity Date or ARD LTV, Underwritten NOI Debt Yield and Cut-off Date Balance per # of NRA/Units/Rooms calculations include any related pari passu companion loan(s) and exclude any related subordinate companion loan(s) and/or mezzanine loan(s). |

| (2) | With respect to four mortgage loans (20.8%) (CX – 250 Water Street (8.1%), 100 Jefferson Road (4.6%), 9200 Calumet Industrial (4.5%) and Crowne Plaza Union Station (3.7%)), the Cut-off Date LTV and Maturity Date or ARD LTV have been calculated using a value other than the “As Is” appraised value. For additional information please see the footnotes to Annex A-1 in the Preliminary Prospectus. |

| (3) | Reflects allocated loan amount for properties securing multi-property Mortgage Loans. |

| Previously Securitized Mortgaged Properties(1) | ||||||

| Mortgaged Property | Cut-off Date Balance | % of Initial Outstanding Pool Balance | City, State | Property Type | Previous Securitization | |

| Pacific Design Center | $65,600,000 | 9.99% | West Hollywood, CA | Mixed Use | WFCMT 2014-LC16, COMM 2014-CCRE18 | |

| Green Acres | $50,000,000 | 7.6% | Valley Stream, NY | Retail | COMM 2013-GAM | |

| Great Lakes Crossing Outlets | $50,000,000 | 7.6% | Auburn Hills, MI | Retail | GSMS 2013-G1 | |

| 100 Jefferson Road | $30,000,000 | 4.6% | Parsippany, NJ | Industrial | GPMT 2019-FL2 | |

| Naugatuck Valley Shopping Center | $27,749,936 | 4.2% | Waterbury, CT | Retail | WFCG 2015-BXRP | |

| One Campus Martius | $27,500,000 | 4.2% | Detroit, MI | Office | TRTX 2022-FL5 | |

| Crowne Plaza Union Station | $23,985,678 | 3.7% | Indianapolis, IN | Hospitality | COMM 2012-CR5 | |

| Sentinel Square II | $10,000,000 | 1.5% | Washington, DC | Office | BMARK 2018-B1, BMARK 2018-B2 | |

| TownePlace Suites BWI Airport | $8,000,000 | 1.2% | Linthicum, MD | Hospitality | JPMBB 2013-C12 | |

| 68-78 River Road | $8,000,000 | 1.2% | Summit, NJ | Retail | UBSBB 2013-C6 | |

| Sylvan Heights | $3,888,468 | 0.6% | Arlington, TX | Retail | WFRBS 2012-C10 | |

| (1) | The table above includes mortgaged properties securing mortgage loans for which the most recent prior financing of all or a significant portion of each such mortgaged property was included in a securitization. Information under “Previous Securitization” represents the most recent such securitization with respect to each of those mortgaged properties. The information in the above table is based solely on information provided by the related borrower or obtained through searches of a third-party database and has not otherwise been confirmed by the related mortgage loan seller. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 11 | ||

Benchmark 2023-B38 Mortgage Trust

| STRUCTURE OVERVIEW |

| Allocation between VRR Interest and the Non-VRR Certificates: | The aggregate amount available for distribution to holders of the Non-VRR Certificates and the VRR Interest on each Distribution Date will be: (i) the gross amount of interest, principal, yield maintenance charges and prepayment premiums collected with respect to the Mortgage Loans in the applicable one-month collection period (other than any excess interest accrued after the related anticipated repayment date on any mortgage loan with an anticipated repayment date), net of specified expenses of the issuing entity, including fees payable therefrom to, and losses, liabilities, costs and expenses reimbursable or indemnifiable therefrom to, the Master Servicer, the Special Servicer, the Certificate Administrator, the Trustee, the Operating Advisor, the Asset Representations Reviewer and CREFC®; and (ii) allocated to amounts available for distribution to the owners of the VRR Interest, on the one hand, and amounts available for distribution to the holders of the Non-VRR Certificates, on the other hand. On each Distribution Date, the portion of such pooled aggregate available funds allocable to: (a) the VRR Interest will be the product of such pooled aggregate available funds multiplied by a fraction, expressed as a percentage, the numerator of which is the initial VRR Interest Balance of the VRR Interest, and the denominator of which is the sum of the aggregate initial Certificate Balance of all classes of Pooled Principal Balance Certificates and the initial VRR Interest Balance of the VRR Interest (the “VRR Percentage”); and (b) the Non-VRR Certificates will at all times be the product of such pooled aggregate available funds multiplied by the difference between 100% and the VRR Percentage (such difference, the “Non-VRR Percentage”). See “Credit Risk Retention” and “Description of the Certificates” in the Preliminary Prospectus. |

| Principal Payments: | Payments in respect of the Non-VRR Percentage of principal on the Non-VRR Certificates will be distributed, first, to the Class A-SB certificates, until the Certificate Balance of such class is reduced to the planned principal balance for the related Distribution Date set forth on Annex G to the Preliminary Prospectus, then, to the Class A-1, Class A-2, Class A-3, Class A-4, Class A-SB, Class A-M, Class B, Class C, Class D, Class E, Class F, Class G and Class H certificates, in that order, until the Certificate Balance of each such class is reduced to zero. Notwithstanding the foregoing, if the total Certificate Balance of the Class A-M, Class B, Class C, Class D, Class E, Class F, Class G and Class H certificates have been reduced to zero as a result of loss allocation, payments in respect of principal of the certificates will be distributed, first, to the Class A-1, Class A-2, Class A-3, Class A-SB and Class A-4 certificates, on a pro rata basis, based on the Certificate Balance of each such class, then, to the extent of any recoveries on realized losses, to the Class A-M, Class B, Class C, Class D, Class E, Class F, Class G and Class H certificates, in that order, in each case until the Certificate Balance of each such class is reduced to zero (or previously allocated realized losses have been fully reimbursed). Each class of Class X Certificates will not be entitled to receive distributions of principal; however, (i) the notional amount of the Class X-A certificates will be reduced by the aggregate amount of principal distributions and realized losses allocated to the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4 and Class A-M certificates; (ii) the notional amount of the Class X-D certificates will be reduced by the aggregate amount of principal distributions and realized losses allocated to the Class D and Class E certificates; (iii) the notional amount of the Class X-F certificates will be reduced by the amount of principal distributions and realized losses allocated to the Class F certificates; (iv) the notional amount of the Class X-G certificates will be reduced by the amount of principal distributions and realized losses allocated to the Class G certificates; and (v) the notional amount of the Class X-H certificates will be reduced by the amount of principal distributions and realized losses allocated to the Class H certificates. The holders of the Loan-Specific Certificates will only be entitled to distributions from amounts paid or advanced on and allocated to the Trust Subordinate Companion Loan in accordance with the PSA and co-lender agreement relating to the Pacific Design Center Whole Loan and no class of Pooled Certificates or the RR Interest will be entitled to distributions paid or advanced on and allocable to the Trust Subordinate Companion Loan. |

Interest Payments: | On each Distribution Date, interest accrued for each class of Non-VRR Certificates at the applicable pass-through rate will be distributed in the following order of priority, to the extent of the Non-VRR Percentage of the pooled aggregate available funds (exclusive of any portion thereof that represents the Non-VRR Percentage of any yield maintenance charges and prepayment premiums): first, to the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4, Class X-A, Class X-D, Class X-F, Class X-G and Class X-H certificates, on a pro rata basis, based on the accrued and unpaid interest on each such class and then, to the Class A-M, Class B, Class C, Class D, Class E, Class F, Class G and Class H certificates, in that order, in each case until the interest payable to each such class is paid in full.

|

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 12 | ||

Benchmark 2023-B38 Mortgage Trust

| STRUCTURE OVERVIEW |

The pass-through rates applicable to the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4, Class A-M, Class B, Class C, Class D, Class E, Class F, Class G and Class H certificates for each Distribution Date will equal one of: (i) a fixed per annum rate, (ii) the WAC Rate, (iii) a rate equal to the lesser of a specified pass-through rate and the WAC Rate or (iv) the WAC Rate less a specified rate, but in any case not less than 0.000%. As further described in the Preliminary Prospectus, the pass-through rates applicable to the Class X Certificates for each Distribution Date will generally be equal to the excess of (i) the WAC Rate over (ii) (A) with respect to the Class X-A certificates, the weighted average of the pass-through rates of the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4, and Class A-M certificates (weighted based on their respective Certificate Balances outstanding immediately prior to that Distribution Date), (B) with respect to the Class X-D certificates, the weighted average of the pass-through rates of the Class D and Class E certificates (weighted based on their respective Certificate Balances outstanding immediately prior to that Distribution Date), (C) with respect to the Class X-F certificates, the pass-through rate of the Class F certificates, (D) with respect to the Class X-G certificates, the pass-through rate of the Class G certificates and (E) with respect to the Class X-H certificates, the pass-through rate of the Class H certificates. No class of Pooled Certificates or the RR Interest will be entitled to distributions paid or advanced on and allocable to the Trust Subordinate Companion Loan. The holders of the Loan-Specific Certificates will only be entitled to distributions from amounts paid or advanced on and allocated to the Trust Subordinate Companion Loan in accordance with the PSA and co-lender agreement relating to the Pacific Design Center Whole Loan. | |

| Prepayment Interest Shortfalls: | Prepayment interest shortfalls will be allocated pro rata based on interest entitlements, in reduction of the interest otherwise payable with respect to each of the interest-bearing classes of certificates. |

| Loss Allocation: | The Non-VRR Percentage of losses on the Mortgage Loans will be allocated to each class of Non-VRR Certificates entitled to principal in reverse alphabetical order starting with the Class H certificates through and including the Class A-M certificates and then to the Class A-1, Class A-2, Class A-3, Class A-SB and Class A-4 certificates on a pro rata basis based on the Certificate Balance of each such class. The notional amount of any class of Class X Certificates will be reduced by the aggregate amount of realized losses allocated to the class(es) of certificates that are component(s) of the notional amount of such class of Class X Certificates. Losses realized on the Trust Subordinate Companion Loan will be allocated each class of Loan-Specific Certificates in the following order, in each case until the related certificate balance is reduced to zero: first, to the Class PDC-HRR certificates, then to the Class PDC-A2 certificates, and then, to the Class PDC-A1 certificates. |

Prepayment Premiums:

| A percentage of the Non-VRR Percentage of all prepayment premiums (either fixed prepayment premiums or yield maintenance amounts) collected on the Mortgage Loans will be allocated to each of the Class A-1, Class A-2, Class A-3, Class A-SB, Class A-4, Class A-M, Class B, Class C, Class D and Class E certificates (the “YM P&I Certificates”) then entitled to principal distributions, which percentage will be equal to the product of (a) a fraction, not greater than one, the numerator of which is the amount of principal distributed to such class on such Distribution Date and the denominator of which is the total amount of principal distributed to the holders of each class of Principal Balance Certificates on such Distribution Date and (b) the Base Interest Fraction for the related principal prepayment and such class of certificates. The VRR Percentage of all prepayment premiums (either fixed prepayment premiums or yield maintenance amounts) will be distributed to the VRR Interest. The “Base Interest Fraction” for any principal prepayment on any Mortgage Loan and for: (A) any of the Class A-1 through Class E certificates with a Pass-Through Rate equal to either the WAC Rate or the WAC Rate less a specified rate, will be a fraction (not greater than one) (a) whose numerator is the greater of zero and the amount, if any, by which (i) the Pass-Through Rate on such class of certificates exceeds (ii) the yield rate (as provided by the master servicer) used in calculating the prepayment premium or yield maintenance charge, as applicable, with respect to such principal prepayment and (b) whose denominator is the amount, if any, by which (i) the Net Mortgage Rate on such Mortgage Loan during the related interest accrual period exceeds (ii) the yield rate (as provided by the master servicer) used in calculating the prepayment premium or yield maintenance charge, as applicable, with respect to such principal prepayment; provided, however, that if such yield rate is greater than or equal to the |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 13 | ||

Benchmark 2023-B38 Mortgage Trust

| STRUCTURE OVERVIEW |

| Net Mortgage Rate on such Mortgage Loan during the related interest accrual period, then the respective Base Interest Fraction will be zero; provided, further, that if such yield rate is greater than or equal to the Net Mortgage Rate on such Mortgage Loan during the related interest accrual period, but less than the Pass-Through Rate described in clause (a)(i) above, then the respective Base Interest Fraction will be one; and (B) any of the Class A-1 through Class E certificates with a Pass-Through Rate equal to a fixed per annum rate, will be a fraction (not greater than one) (a) whose numerator is the greater of zero and the amount, if any, by which (i) the Pass-Through Rate on such class of certificates exceeds (ii) the yield rate (as provided by the master servicer) used in calculating the prepayment premium or yield maintenance charge, as applicable, with respect to such principal prepayment and (b) whose denominator is the amount, if any, by which (i) the Mortgage Rate on such Mortgage Loan (without regard to any increase in the interest rate of any ARD Loan after the related Anticipated Repayment Date, and net of the Administrative Cost Rate) during the related interest accrual period multiplied by 365/360 exceeds (ii) the yield rate (as provided by the master servicer) used in calculating the prepayment premium or yield maintenance charge, as applicable, with respect to such principal prepayment; provided, however, that if such yield rate is greater than or equal to the amount set forth in clause (b)(i) above, then the respective Base Interest Fraction will be zero; provided, further, that if such yield rate is greater than or equal to the amount set forth in clause (b)(i) above, but less than the Pass-Through Rate described in clause (a)(i) above, then the respective Base Interest Fraction will be one. The remaining percentage of the Non-VRR Percentage of prepayment premiums will be allocated to the Class X-A and Class X-D certificates. In general, this formula provides for an increase in the percentage of prepayment premiums allocated to the YM P&I Certificates then entitled to principal distributions relative to the Class X-A and Class X-D certificates as Discount Rates decrease and a decrease in the percentage allocated to such classes as Discount Rates rise. |

| Whole Loans: | The mortgaged properties identified on Annex A-1 to the Preliminary Prospectus as Pacific Design Center, 1201 Third Avenue, CX – 250 Water Street, Green Acres, Great Lakes Crossing Outlets, Scottsdale Fashion Square, National Warehouse & Distribution Portfolio, 100 Jefferson Road, One Campus Martius, Riverport Tower, Sentinel Square II and Centers of High Point each secure both a mortgage loan to be included in the trust fund and one or more other companion loans that will not be included in the trust fund, each of which will be pari passu or subordinate in right of payment with the mortgage loan included in the trust fund. We refer to each such group of related loans as a “whole loan”. As of the Closing Date, the pari passu companion loans and the subordinate companion loans are expected to be held by the party identified in “—Companion Loan Summary” above and the table titled “Whole Loan Control Notes and Non-Control Notes” in “Description of the Mortgage Pool—The Whole Loans—General” in the Preliminary Prospectus. |

| Control Rights and Directing Holder: | With respect to any Serviced Mortgage Loan and any related Serviced Companion Loan, the Directing Holder will generally be entitled to direct the Special Servicer to take, or refrain from taking certain actions with respect to each Serviced Mortgage Loan and any related Serviced Companion Loans. Furthermore, the Directing Holder will also have the right to receive notice and consent to certain material actions that the Master Servicer and the Special Servicer proposes to take with respect to each Serviced Mortgage Loan and any related Serviced Companion Loans. The “Directing Holder” means, (i) with respect to each Serviced Mortgage Loan (other than the Pacific Design Center Mortgage Loan and any Servicing Shift Mortgage Loan) or Serviced Whole Loan (other than the Pacific Design Center Whole Loan and any Servicing Shift Whole Loan), the certificateholder (or its representative) selected by more than 50% of the Controlling Class, by Certificate Balance, as determined by the certificate registrar from time to time (the “Trust Directing Holder”); (ii) with respect to the Pacific Design Center Whole Loan, (a) for so long as no Pacific Design Center control appraisal period exists, the certificateholder (or its representative) selected by more than 50% of the controlling class of the Loan-Specific Certificates by Certificate Balance, as determined by the certificate registrar from time to time (the “Pacific Design Center Controlling Class Representative”) and (b) for so long as an Pacific Design Center control appraisal period exists, the Trust Directing Holder and (iii) with respect to any Servicing Shift Mortgage Loan or Servicing Shift Whole Loan, the related Loan-Specific Directing Holder identified in the Preliminary Prospectus (which is expected to be the holder of the related controlling pari passu companion loan) prior to the related Servicing Shift Securitization Date. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 14 | ||

Benchmark 2023-B38 Mortgage Trust

| STRUCTURE OVERVIEW |