Capital Group International Equity ETF (CGIE)

Filed: 31 Jan 25, 12:02pm

| Fund | Cost of $10,000 Investment | Costs paid as a percentage of a $10,000 investment |

| CGIE | $ 27 | 0.54 % * |

| Fund net assets (in thousands) | $ 266,570 |

| Total number of portfolio holdings | 70 |

| Portfolio turnover rate | 16 % |

ITEM 2 - Code of Ethics

Not applicable for filing of semi-annual reports to shareholders.

ITEM 3 - Audit Committee Financial Expert

Not applicable for filing of semi-annual reports to shareholders.

ITEM 4 - Principal Accountant Fees and Services

Not applicable for filing of semi-annual reports to shareholders.

ITEM 5 - Audit Committee of Listed Registrants

Not applicable for filing of semi-annual reports to shareholders.

ITEM 6 - Investments

The schedule of investments is included as part of the material filed under Item 7 of this Form.

ITEM 7 - Financial Statements and Financial Highlights for Open-End Management Investment Companies

Common stocks 96.39% | Shares | Value (000) | ||

Information technology 19.10% | ||||

Microsoft Corp. | 19,597 | $8,299 | ||

Apple, Inc. | 25,811 | 6,126 | ||

Broadcom, Inc. | 16,236 | 2,632 | ||

Accenture PLC, Class A | 7,161 | 2,595 | ||

Texas Instruments, Inc. | 10,899 | 2,191 | ||

Taiwan Semiconductor Manufacturing Co., Ltd. (ADR) | 5,790 | 1,069 | ||

Salesforce, Inc. | 3,032 | 1,000 | ||

Oracle Corp. | 5,315 | 982 | ||

Analog Devices, Inc. | 4,316 | 941 | ||

Amphenol Corp., Class A | 7,795 | 566 | ||

Intel Corp. | 15,008 | 361 | ||

KLA Corp. | 246 | 159 | ||

26,921 | ||||

Financials 17.26% | ||||

JPMorgan Chase & Co. | 14,677 | 3,665 | ||

PNC Financial Services Group, Inc. | 8,621 | 1,851 | ||

Fidelity National Information Services, Inc. | 19,801 | 1,689 | ||

Morgan Stanley | 11,662 | 1,535 | ||

Marsh & McLennan Companies, Inc. | 6,554 | 1,529 | ||

Visa, Inc., Class A | 4,518 | 1,424 | ||

Wells Fargo & Co. | 18,437 | 1,404 | ||

Chubb, Ltd. | 4,819 | 1,391 | ||

Truist Financial Corp. | 28,123 | 1,341 | ||

S&P Global, Inc. | 2,565 | 1,340 | ||

Capital One Financial Corp. | 6,622 | 1,272 | ||

Great-West Lifeco, Inc. | 32,664 | 1,176 | ||

Progressive Corp. | 3,008 | 809 | ||

BlackRock, Inc. | 761 | 778 | ||

Mastercard, Inc., Class A | 1,415 | 754 | ||

Blackstone, Inc. | 3,831 | 732 | ||

State Street Corp. | 5,849 | 576 | ||

East West Bancorp, Inc. | 4,839 | 531 | ||

Principal Financial Group, Inc. | 6,067 | 528 | ||

24,325 | ||||

Industrials 15.45% | ||||

RTX Corp. | 42,224 | 5,144 | ||

General Electric Co. | 21,269 | 3,874 | ||

Union Pacific Corp. | 10,820 | 2,647 | ||

Carrier Global Corp. | 23,467 | 1,816 | ||

Paychex, Inc. | 9,550 | 1,397 | ||

Honeywell International, Inc. | 4,909 | 1,143 | ||

Automatic Data Processing, Inc. | 3,317 | 1,018 | ||

FedEx Corp. | 2,525 | 764 | ||

Northrop Grumman Corp. | 1,521 | 745 | ||

General Dynamics Corp. | 2,537 | 721 | ||

BAE Systems PLC (ADR) | 11,091 | 693 | ||

Illinois Tool Works, Inc. | 2,068 | 574 | ||

TFI International, Inc. | 3,062 | 464 | ||

Equifax, Inc. | 1,704 | 446 | ||

Stanley Black & Decker, Inc. | 3,793 | 339 | ||

21,785 | ||||

Health care 14.40% | ||||

AbbVie, Inc. | 26,600 | 4,866 | ||

UnitedHealth Group, Inc. | 6,368 | 3,886 | ||

Abbott Laboratories | 21,575 | 2,562 | ||

Gilead Sciences, Inc. | 21,774 | 2,016 | ||

Eli Lilly and Co. | 1,756 | 1,397 | ||

Amgen, Inc. | 3,599 | 1,018 | ||

Medtronic PLC | 11,359 | 983 | ||

Bristol-Myers Squibb Co. | 15,771 | 934 | ||

CVS Health Corp. | 11,482 | 687 | ||

Capital Group Equity Exchange-Traded Funds | 1 |

Common stocks (continued) | Shares | Value (000) | ||

Health care (continued) | ||||

Thermo Fisher Scientific, Inc. | 1,218 | $645 | ||

Danaher Corp. | 2,281 | 547 | ||

GE HealthCare Technologies, Inc. | 6,087 | 507 | ||

AstraZeneca PLC (ADR) | 3,645 | 246 | ||

20,294 | ||||

Consumer staples 6.82% | ||||

Philip Morris International, Inc. | 13,330 | 1,774 | ||

Mondelez International, Inc., Class A | 25,614 | 1,664 | ||

Constellation Brands, Inc., Class A | 5,759 | 1,388 | ||

General Mills, Inc. | 17,444 | 1,156 | ||

Hershey Co. | 5,082 | 895 | ||

British American Tobacco PLC (ADR) | 23,543 | 893 | ||

Procter & Gamble Co. | 4,020 | 720 | ||

PepsiCo, Inc. | 4,351 | 711 | ||

Nestlé SA | 4,836 | 420 | ||

9,621 | ||||

Utilities 6.61% | ||||

Sempra | 20,484 | 1,919 | ||

CenterPoint Energy, Inc. | 58,451 | 1,907 | ||

Constellation Energy Corp. | 6,751 | 1,732 | ||

DTE Energy Co. | 13,117 | 1,650 | ||

Southern Co. (The) | 9,575 | 853 | ||

Edison International | 7,500 | 658 | ||

Public Service Enterprise Group, Inc. | 6,302 | 594 | ||

9,313 | ||||

Energy 4.65% | ||||

TC Energy Corp. | 26,378 | 1,286 | ||

TC Energy Corp. | 22,449 | 1,099 | ||

Exxon Mobil Corp. | 19,814 | 2,337 | ||

ConocoPhillips | 10,360 | 1,122 | ||

EOG Resources, Inc. | 5,395 | 719 | ||

6,563 | ||||

Consumer discretionary 4.22% | ||||

Home Depot, Inc. | 6,517 | 2,797 | ||

McDonald’s Corp. | 2,997 | 887 | ||

Starbucks Corp. | 8,445 | 865 | ||

Hasbro, Inc. | 10,863 | 708 | ||

D.R. Horton, Inc. | 4,087 | 690 | ||

5,947 | ||||

Materials 3.27% | ||||

Linde PLC | 5,643 | 2,601 | ||

International Paper Co. | 20,017 | 1,178 | ||

Air Products and Chemicals, Inc. | 2,478 | 829 | ||

4,608 | ||||

Communication services 2.37% | ||||

Meta Platforms, Inc., Class A | 4,376 | 2,513 | ||

Comcast Corp., Class A | 19,245 | 831 | ||

3,344 | ||||

Real estate 2.24% | ||||

Welltower, Inc. REIT | 8,608 | 1,190 | ||

Public Storage REIT | 2,062 | 718 | ||

Extra Space Storage, Inc. REIT | 3,746 | 640 | ||

Digital Realty Trust, Inc. REIT | 3,109 | 608 | ||

3,156 | ||||

Total common stocks (cost: $128,337,000) | 135,877 | |||

2 | Capital Group Equity Exchange-Traded Funds |

Short-term securities 3.47% | Shares | Value (000) | ||

Money market investments 3.47% | ||||

Capital Group Central Cash Fund 4.65%1,2 | 48,914 | $4,892 | ||

Total short-term securities (cost: $4,892,000) | 4,892 | |||

Total investment securities 99.86% (cost: $133,229,000) | 140,769 | |||

Other assets less liabilities 0.14% | 197 | |||

Net assets 100.00% | $140,966 | |||

Value at 6/25/20243 (000) | Additions (000) | Reductions (000) | Net realized gain (loss) (000) | Net unrealized appreciation (depreciation) (000) | Value at 11/30/2024 (000) | Dividend or interest income (000) | |

Short-term securities 3.47% | |||||||

Money market investments 3.47% | |||||||

Capital Group Central Cash Fund 4.65% 1 | $— | $8,567 | $3,675 | $— 4 | $— 4 | $4,892 | $62 |

1 | Rate represents the seven-day yield at 11/30/2024. |

2 | Part of the same "group of investment companies" as the fund as defined under the Investment Company Act of 1940, as amended. |

3 | Commencement of operations. |

4 | Amount less than one thousand. |

Key to abbreviation(s) |

ADR = American Depositary Receipts |

REIT = Real Estate Investment Trust |

Capital Group Equity Exchange-Traded Funds | 3 |

Common stocks 98.88% | Shares | Value (000) | ||

Information technology 23.22% | ||||

Microsoft Corp. | 628,116 | $265,982 | ||

Apple, Inc. | 875,722 | 207,835 | ||

Broadcom, Inc. | 843,063 | 136,644 | ||

NVIDIA Corp. | 735,817 | 101,727 | ||

Accenture PLC, Class A | 215,170 | 77,971 | ||

Texas Instruments, Inc. | 276,522 | 55,589 | ||

Salesforce, Inc. | 129,942 | 42,880 | ||

Oracle Corp. | 132,529 | 24,497 | ||

ServiceNow, Inc.1 | 14,847 | 15,581 | ||

Taiwan Semiconductor Manufacturing Co., Ltd. (ADR) | 79,967 | 14,767 | ||

Seagate Technology Holdings PLC | 105,837 | 10,724 | ||

Palo Alto Networks, Inc.1 | 25,152 | 9,754 | ||

963,951 | ||||

Industrials 13.77% | ||||

RTX Corp. | 675,901 | 82,345 | ||

Automatic Data Processing, Inc. | 204,729 | 62,838 | ||

General Electric Co. | 299,695 | 54,593 | ||

Carrier Global Corp. | 630,560 | 48,786 | ||

GFL Environmental, Inc., subordinate voting shares | 900,858 | 42,430 | ||

Airbus SE, non-registered shares | 215,967 | 33,726 | ||

United Rentals, Inc. | 38,829 | 33,626 | ||

General Dynamics Corp. | 115,592 | 32,829 | ||

TFI International, Inc. | 213,084 | 32,321 | ||

Honeywell International, Inc. | 133,607 | 31,121 | ||

Ingersoll-Rand, Inc. | 292,208 | 30,439 | ||

Woodward, Inc. | 167,815 | 30,260 | ||

XPO, Inc.1 | 178,210 | 27,161 | ||

TransDigm Group, Inc. | 12,814 | 16,056 | ||

Union Pacific Corp. | 53,470 | 13,082 | ||

571,613 | ||||

Financials 13.18% | ||||

JPMorgan Chase & Co. | 286,438 | 71,529 | ||

Mastercard, Inc., Class A | 133,042 | 70,904 | ||

Fidelity National Information Services, Inc. | 680,182 | 58,020 | ||

BlackRock, Inc. | 45,227 | 46,258 | ||

PNC Financial Services Group, Inc. | 195,521 | 41,982 | ||

Capital One Financial Corp. | 206,911 | 39,729 | ||

S&P Global, Inc. | 71,659 | 37,443 | ||

Visa, Inc., Class A | 85,952 | 27,082 | ||

Marsh & McLennan Companies, Inc. | 99,521 | 23,211 | ||

Berkshire Hathaway, Inc., Class B1 | 46,462 | 22,442 | ||

Morgan Stanley | 155,440 | 20,458 | ||

Wells Fargo & Co. | 256,180 | 19,513 | ||

Chubb, Ltd. | 65,360 | 18,871 | ||

Arthur J. Gallagher & Co. | 46,270 | 14,447 | ||

State Street Corp. | 146,491 | 14,431 | ||

B3 SA - Brasil, Bolsa, Balcao | 6,917,695 | 10,725 | ||

First Citizens BancShares, Inc., Class A | 4,436 | 10,181 | ||

547,226 | ||||

Health care 13.02% | ||||

UnitedHealth Group, Inc. | 226,481 | 138,199 | ||

Eli Lilly and Co. | 84,961 | 67,574 | ||

AbbVie, Inc. | 346,897 | 63,458 | ||

GE HealthCare Technologies, Inc. | 691,292 | 57,529 | ||

Abbott Laboratories | 360,820 | 42,855 | ||

Thermo Fisher Scientific, Inc. | 79,098 | 41,893 | ||

Vertex Pharmaceuticals, Inc.1 | 88,919 | 41,626 | ||

Danaher Corp. | 136,102 | 32,622 | ||

4 | Capital Group Equity Exchange-Traded Funds |

Common stocks (continued) | Shares | Value (000) | ||

Health care (continued) | ||||

Revvity, Inc. | 265,155 | $30,795 | ||

Sanofi | 162,227 | 15,810 | ||

Insulet Corp.1 | 31,421 | 8,382 | ||

540,743 | ||||

Communication services 10.80% | ||||

Meta Platforms, Inc., Class A | 374,686 | 215,189 | ||

Alphabet, Inc., Class A | 648,810 | 109,617 | ||

Alphabet, Inc., Class C | 416,976 | 71,090 | ||

Netflix, Inc.1 | 38,724 | 34,341 | ||

Comcast Corp., Class A | 416,925 | 18,007 | ||

448,244 | ||||

Consumer discretionary 10.44% | ||||

Amazon.com, Inc.1 | 840,125 | 174,654 | ||

Wyndham Hotels & Resorts, Inc. | 534,713 | 52,498 | ||

Tesla, Inc.1 | 118,364 | 40,855 | ||

Royal Caribbean Cruises, Ltd. | 167,344 | 40,842 | ||

Restaurant Brands International, Inc. | 462,094 | 32,166 | ||

Home Depot, Inc. | 68,326 | 29,321 | ||

InterContinental Hotels Group PLC | 186,875 | 23,343 | ||

Tapestry, Inc. | 274,573 | 17,100 | ||

Hasbro, Inc. | 182,258 | 11,874 | ||

NIKE, Inc., Class B | 139,996 | 11,027 | ||

433,680 | ||||

Consumer staples 3.40% | ||||

British American Tobacco PLC | 1,743,967 | 66,419 | ||

Philip Morris International, Inc. | 222,726 | 29,636 | ||

Constellation Brands, Inc., Class A | 73,866 | 17,798 | ||

Mondelez International, Inc., Class A | 220,293 | 14,308 | ||

General Mills, Inc. | 199,503 | 13,219 | ||

141,380 | ||||

Materials 3.24% | ||||

Air Products and Chemicals, Inc. | 171,638 | 57,384 | ||

Freeport-McMoRan, Inc. | 495,832 | 21,916 | ||

Eastman Chemical Co. | 204,988 | 21,466 | ||

Linde PLC | 44,368 | 20,453 | ||

International Paper Co. | 223,412 | 13,143 | ||

134,362 | ||||

Energy 3.17% | ||||

Baker Hughes Co., Class A | 1,158,003 | 50,894 | ||

Canadian Natural Resources, Ltd. (CAD denominated) | 973,961 | 33,055 | ||

Exxon Mobil Corp. | 226,542 | 26,723 | ||

Chevron Corp. | 130,171 | 21,079 | ||

131,751 | ||||

Utilities 2.53% | ||||

PG&E Corp. | 1,912,387 | 41,365 | ||

Edison International | 269,691 | 23,665 | ||

CenterPoint Energy, Inc. | 694,025 | 22,639 | ||

Sempra | 187,402 | 17,554 | ||

105,223 | ||||

Real estate 2.11% | ||||

VICI Properties, Inc. REIT | 1,134,340 | 36,991 | ||

Equinix, Inc. REIT | 36,813 | 36,131 | ||

Welltower, Inc. REIT | 103,432 | 14,292 | ||

87,414 | ||||

Total common stocks (cost: $3,392,585,000) | 4,105,587 | |||

Capital Group Equity Exchange-Traded Funds | 5 |

Short-term securities 1.13% | Shares | Value (000) | ||

Money market investments 1.13% | ||||

Capital Group Central Cash Fund 4.65%2,3 | 468,252 | $46,830 | ||

Total short-term securities (cost: $46,827,000) | 46,830 | |||

Total investment securities 100.01% (cost: $3,439,412,000) | 4,152,417 | |||

Other assets less liabilities (0.01)% | (297 ) | |||

Net assets 100.00% | $4,152,120 | |||

Value at 6/1/2024 (000) | Additions (000) | Reductions (000) | Net realized gain (loss) (000) | Net unrealized appreciation (depreciation) (000) | Value at 11/30/2024 (000) | Dividend or interest income (000) | |

Short-term securities 1.13% | |||||||

Money market investments 1.13% | |||||||

Capital Group Central Cash Fund 4.65% 2 | $54,961 | $437,603 | $445,726 | $1 | $(9 ) | $46,830 | $1,718 |

1 | Security did not produce income during the last 12 months. |

2 | Rate represents the seven-day yield at 11/30/2024. |

3 | Part of the same "group of investment companies" as the fund as defined under the Investment Company Act of 1940, as amended. |

Key to abbreviation(s) |

ADR = American Depositary Receipts |

CAD = Canadian dollars |

REIT = Real Estate Investment Trust |

6 | Capital Group Equity Exchange-Traded Funds |

Common stocks 97.13% | Shares | Value (000) | ||

Industrials 19.97% | ||||

RTX Corp. | 243,184 | $29,627 | ||

Broadridge Financial Solutions, Inc. | 105,810 | 24,973 | ||

UL Solutions, Inc., Class A | 413,594 | 22,222 | ||

Carrier Global Corp. | 286,861 | 22,194 | ||

FedEx Corp. | 65,194 | 19,732 | ||

Airbus SE, non-registered shares | 117,467 | 18,344 | ||

Paychex, Inc. | 100,271 | 14,667 | ||

RELX PLC | 300,230 | 14,178 | ||

BAE Systems PLC | 860,141 | 13,452 | ||

Hitachi, Ltd. | 524,500 | 13,148 | ||

Trinity Industries, Inc. | 345,498 | 13,025 | ||

Mitsubishi Corp. | 753,500 | 12,717 | ||

Northrop Grumman Corp. | 25,267 | 12,372 | ||

Ryanair Holdings PLC (ADR) | 279,634 | 12,315 | ||

Canadian National Railway Co. (CAD denominated) | 104,736 | 11,695 | ||

ITOCHU Corp. | 215,400 | 10,629 | ||

Norfolk Southern Corp. | 35,225 | 9,717 | ||

275,007 | ||||

Financials 15.99% | ||||

Morgan Stanley | 198,086 | 26,070 | ||

Intact Financial Corp. | 132,476 | 25,231 | ||

DBS Group Holdings, Ltd. | 664,270 | 21,056 | ||

Banca Generali SpA | 440,006 | 20,647 | ||

London Stock Exchange Group PLC | 131,771 | 18,929 | ||

Truist Financial Corp. | 313,813 | 14,963 | ||

Webster Financial Corp. | 237,907 | 14,698 | ||

JPMorgan Chase & Co. | 55,959 | 13,974 | ||

East West Bancorp, Inc. | 126,758 | 13,903 | ||

AIA Group, Ltd. | 1,748,600 | 13,067 | ||

KB Financial Group, Inc. (ADR) | 186,054 | 12,825 | ||

CME Group, Inc., Class A | 43,944 | 10,459 | ||

Hong Kong Exchanges and Clearing, Ltd. | 150,100 | 5,590 | ||

UniCredit SpA | 133,045 | 5,123 | ||

Ping An Insurance (Group) Company of China, Ltd., Class H | 637,000 | 3,667 | ||

220,202 | ||||

Information technology 14.33% | ||||

Taiwan Semiconductor Manufacturing Co., Ltd. (ADR) | 275,184 | 50,815 | ||

Broadcom, Inc. | 299,331 | 48,516 | ||

SAP SE | 116,280 | 27,676 | ||

Accenture PLC, Class A | 63,222 | 22,910 | ||

KLA Corp. | 27,380 | 17,716 | ||

Fujitsu, Ltd. | 616,800 | 11,813 | ||

Texas Instruments, Inc. | 57,707 | 11,601 | ||

MediaTek, Inc. | 162,000 | 6,259 | ||

197,306 | ||||

Consumer staples 9.46% | ||||

Philip Morris International, Inc. | 281,599 | 37,470 | ||

Imperial Brands PLC | 572,361 | 18,742 | ||

Danone SA | 231,346 | 15,831 | ||

Carlsberg A/S, Class B | 146,597 | 15,118 | ||

British American Tobacco PLC | 363,298 | 13,836 | ||

Anheuser-Busch InBev SA/NV | 218,540 | 11,781 | ||

Nestlé SA | 125,090 | 10,864 | ||

Constellation Brands, Inc., Class A | 27,238 | 6,563 | ||

130,205 | ||||

Health care 7.95% | ||||

UnitedHealth Group, Inc. | 40,522 | 24,726 | ||

Eli Lilly and Co. | 22,731 | 18,079 | ||

Abbott Laboratories | 144,687 | 17,184 | ||

Bristol-Myers Squibb Co. | 247,914 | 14,681 | ||

Capital Group Equity Exchange-Traded Funds | 7 |

Common stocks (continued) | Shares | Value (000) | ||

Health care (continued) | ||||

AstraZeneca PLC | 91,554 | $12,384 | ||

Amgen, Inc. | 40,993 | 11,596 | ||

AbbVie, Inc. | 59,234 | 10,836 | ||

109,486 | ||||

Utilities 7.89% | ||||

CenterPoint Energy, Inc. | 883,564 | 28,822 | ||

Iberdrola, SA, non-registered shares | 1,383,735 | 19,755 | ||

Engie SA | 1,203,206 | 19,208 | ||

Edison International | 201,100 | 17,647 | ||

SSE PLC | 744,473 | 16,810 | ||

AES Corp. | 493,340 | 6,433 | ||

108,675 | ||||

Consumer discretionary 7.18% | ||||

Industria de Diseño Textil, SA | 388,282 | 21,442 | ||

Starbucks Corp. | 149,894 | 15,358 | ||

Tractor Supply Co. | 43,962 | 12,471 | ||

LVMH Moët Hennessy-Louis Vuitton SE | 17,840 | 11,186 | ||

YUM! Brands, Inc. | 79,718 | 11,076 | ||

Amadeus IT Group SA, Class A, non-registered shares | 141,004 | 9,912 | ||

Galaxy Entertainment Group, Ltd. | 1,984,000 | 8,809 | ||

Bridgestone Corp. | 240,200 | 8,586 | ||

98,840 | ||||

Real estate 6.03% | ||||

VICI Properties, Inc. REIT | 1,003,531 | 32,725 | ||

Welltower, Inc. REIT | 157,502 | 21,764 | ||

Rexford Industrial Realty, Inc. REIT | 294,495 | 12,392 | ||

Link REIT | 2,119,500 | 9,220 | ||

Longfor Group Holdings, Ltd. | 4,952,500 | 6,950 | ||

83,051 | ||||

Energy 3.83% | ||||

TotalEnergies SE | 285,134 | 16,588 | ||

BP PLC | 2,764,368 | 13,553 | ||

TC Energy Corp. | 236,668 | 11,538 | ||

ConocoPhillips | 55,908 | 6,057 | ||

Schlumberger NV | 111,653 | 4,906 | ||

52,642 | ||||

Communication services 3.47% | ||||

Koninklijke KPN NV | 4,672,012 | 18,151 | ||

T-Mobile US, Inc. | 58,384 | 14,417 | ||

WPP PLC | 701,328 | 7,681 | ||

América Móvil, SAB de CV, Class B (ADR) | 509,465 | 7,555 | ||

47,804 | ||||

Materials 1.03% | ||||

Vale SA (ADR), ordinary nominative shares | 724,911 | 7,148 | ||

Dow, Inc. | 160,057 | 7,076 | ||

14,224 | ||||

Total common stocks (cost: $1,246,358,000) | 1,337,442 | |||

8 | Capital Group Equity Exchange-Traded Funds |

Short-term securities 2.72% | Shares | Value (000) | ||

Money market investments 2.72% | ||||

Capital Group Central Cash Fund 4.65%1,2 | 374,995 | $37,503 | ||

Total short-term securities (cost: $37,500,000) | 37,503 | |||

Total investment securities 99.85% (cost: $1,283,858,000) | 1,374,945 | |||

Other assets less liabilities 0.15% | 2,024 | |||

Net assets 100.00% | $1,376,969 | |||

Value at 6/1/2024 (000) | Additions (000) | Reductions (000) | Net realized gain (loss) (000) | Net unrealized appreciation (depreciation) (000) | Value at 11/30/2024 (000) | Dividend or interest income (000) | |

Short-term securities 2.72% | |||||||

Money market investments 2.72% | |||||||

Capital Group Central Cash Fund 4.65% 1 | $13,229 | $168,542 | $144,262 | $(7 ) | $1 | $37,503 | $1,073 |

1 | Rate represents the seven-day yield at 11/30/2024. |

2 | Part of the same "group of investment companies" as the fund as defined under the Investment Company Act of 1940, as amended. |

Key to abbreviation(s) |

ADR = American Depositary Receipts |

CAD = Canadian dollars |

REIT = Real Estate Investment Trust |

Capital Group Equity Exchange-Traded Funds | 9 |

Common stocks 96.12% | Shares | Value (000) | ||

Industrials 20.61% | ||||

Carrier Global Corp. | 6,808,542 | $526,777 | ||

RTX Corp. | 4,113,429 | 501,139 | ||

General Electric Co. | 2,583,518 | 470,614 | ||

Union Pacific Corp. | 976,245 | 238,848 | ||

General Dynamics Corp. | 710,814 | 201,878 | ||

Illinois Tool Works, Inc. | 533,609 | 148,087 | ||

United Rentals, Inc. | 170,144 | 147,345 | ||

Boeing Co. (The)1 | 852,699 | 132,544 | ||

Uber Technologies, Inc.1 | 1,508,898 | 108,580 | ||

TFI International, Inc. | 432,852 | 65,655 | ||

2,541,467 | ||||

Information technology 15.61% | ||||

Microsoft Corp. | 1,332,240 | 564,150 | ||

Apple, Inc. | 2,074,389 | 492,315 | ||

Broadcom, Inc. | 1,654,069 | 268,091 | ||

Texas Instruments, Inc. | 1,332,443 | 267,861 | ||

Salesforce, Inc. | 533,479 | 176,043 | ||

Oracle Corp. | 569,563 | 105,278 | ||

Intel Corp. | 2,168,979 | 52,164 | ||

1,925,902 | ||||

Health care 13.44% | ||||

UnitedHealth Group, Inc. | 598,553 | 365,237 | ||

GE HealthCare Technologies, Inc. | 3,151,166 | 262,240 | ||

AbbVie, Inc. | 1,182,914 | 216,390 | ||

Abbott Laboratories | 1,689,744 | 200,691 | ||

Gilead Sciences, Inc. | 2,073,628 | 191,976 | ||

Amgen, Inc. | 588,609 | 166,500 | ||

Medtronic PLC | 1,691,556 | 146,387 | ||

Danaher Corp. | 453,025 | 108,586 | ||

1,658,007 | ||||

Consumer discretionary 11.16% | ||||

Royal Caribbean Cruises, Ltd. | 1,469,028 | 358,531 | ||

Las Vegas Sands Corp. | 5,403,348 | 286,702 | ||

McDonald’s Corp. | 670,192 | 198,383 | ||

D.R. Horton, Inc. | 1,117,090 | 188,542 | ||

TopBuild Corp.1 | 314,386 | 122,812 | ||

Hasbro, Inc. | 1,871,482 | 121,927 | ||

Amazon.com, Inc.1 | 480,235 | 99,836 | ||

1,376,733 | ||||

Financials 10.19% | ||||

American International Group, Inc. | 6,126,847 | 471,032 | ||

Capital One Financial Corp. | 1,691,584 | 324,801 | ||

JPMorgan Chase & Co. | 974,094 | 243,251 | ||

First Citizens BancShares, Inc., Class A | 94,940 | 217,887 | ||

1,256,971 | ||||

Consumer staples 7.47% | ||||

Philip Morris International, Inc. | 3,179,190 | 423,023 | ||

British American Tobacco PLC | 8,566,097 | 326,240 | ||

Coca-Cola Co. | 1,416,314 | 90,757 | ||

Mondelez International, Inc., Class A | 1,255,588 | 81,551 | ||

921,571 | ||||

10 | Capital Group Equity Exchange-Traded Funds |

Common stocks (continued) | Shares | Value (000) | ||

Materials 6.07% | ||||

International Paper Co. | 4,284,630 | $252,065 | ||

Linde PLC | 529,164 | 243,939 | ||

Celanese Corp. | 1,364,423 | 99,890 | ||

Freeport-McMoRan, Inc. | 2,190,049 | 96,800 | ||

Albemarle Corp. | 521,541 | 56,170 | ||

748,864 | ||||

Communication services 5.75% | ||||

Meta Platforms, Inc., Class A | 836,656 | 480,508 | ||

Alphabet, Inc., Class A | 1,356,507 | 229,182 | ||

709,690 | ||||

Energy 3.18% | ||||

TC Energy Corp. | 3,324,714 | 162,086 | ||

Canadian Natural Resources, Ltd. | 3,994,311 | 135,088 | ||

EOG Resources, Inc. | 712,523 | 94,951 | ||

392,125 | ||||

Utilities 2.64% | ||||

PG&E Corp. | 10,354,569 | 223,969 | ||

Edison International | 1,151,187 | 101,017 | ||

324,986 | ||||

Total common stocks (cost: $9,957,658,000) | 11,856,316 | |||

Short-term securities 3.82% | ||||

Money market investments 3.82% | ||||

Capital Group Central Cash Fund 4.65%2,3 | 4,714,155 | 471,463 | ||

Total short-term securities (cost: $471,442,000) | 471,463 | |||

Total investment securities 99.94% (cost: $10,429,100,000) | 12,327,779 | |||

Other assets less liabilities 0.06% | 7,274 | |||

Net assets 100.00% | $12,335,053 | |||

Value at 6/1/2024 (000) | Additions (000) | Reductions (000) | Net realized gain (loss) (000) | Net unrealized appreciation (depreciation) (000) | Value at 11/30/2024 (000) | Dividend or interest income (000) | |

Short-term securities 3.82% | |||||||

Money market investments 3.82% | |||||||

Capital Group Central Cash Fund 4.65% 2 | $226,589 | $1,801,169 | $1,556,280 | $13 | $(28 ) | $471,463 | $9,528 |

1 | Security did not produce income during the last 12 months. |

2 | Rate represents the seven-day yield at 11/30/2024. |

3 | Part of the same "group of investment companies" as the fund as defined under the Investment Company Act of 1940, as amended. |

Capital Group Equity Exchange-Traded Funds | 11 |

Common stocks 96.23% | Shares | Value (000) | ||

Industrials 20.14% | ||||

Safran SA | 6,301 | $1,470 | ||

Rolls-Royce Holdings PLC1 | 129,021 | 919 | ||

GE Vernova, Inc.1 | 2,736 | 914 | ||

FedEx Corp. | 2,952 | 894 | ||

HEICO Corp. | 2,984 | 816 | ||

General Electric Co. | 4,392 | 800 | ||

Northrop Grumman Corp. | 1,523 | 746 | ||

Ingersoll-Rand, Inc. | 6,964 | 726 | ||

ABB, Ltd. | 12,528 | 715 | ||

Airbus SE, non-registered shares | 4,254 | 664 | ||

AMETEK, Inc. | 3,376 | 656 | ||

Armstrong World Industries, Inc. | 3,693 | 590 | ||

Epiroc AB, Class A | 32,234 | 588 | ||

SMC Corp. | 1,100 | 467 | ||

Recruit Holdings Co., Ltd. | 6,300 | 437 | ||

DSV A/S | 2,013 | 431 | ||

Saia, Inc.1 | 733 | 417 | ||

CSX Corp. | 11,164 | 408 | ||

ITOCHU Corp. | 7,900 | 390 | ||

United Airlines Holdings, Inc.1 | 3,863 | 374 | ||

Honeywell International, Inc. | 1,560 | 363 | ||

RTX Corp. | 2,848 | 347 | ||

Axon Enterprise, Inc.1 | 496 | 321 | ||

Ryanair Holdings PLC (ADR) | 7,112 | 313 | ||

RELX PLC | 6,259 | 296 | ||

15,062 | ||||

Information technology 17.40% | ||||

Broadcom, Inc. | 12,602 | 2,042 | ||

Microsoft Corp. | 4,364 | 1,848 | ||

Apple, Inc. | 7,646 | 1,815 | ||

SAP SE | 5,168 | 1,230 | ||

Taiwan Semiconductor Manufacturing Co., Ltd. (ADR) | 5,729 | 1,058 | ||

KLA Corp. | 1,215 | 786 | ||

Fujitsu, Ltd. | 36,300 | 695 | ||

Keyence Corp. | 1,500 | 649 | ||

Accenture PLC, Class A | 1,542 | 559 | ||

Analog Devices, Inc. | 2,107 | 459 | ||

ServiceNow, Inc.1 | 405 | 425 | ||

TDK Corp. | 29,000 | 374 | ||

Capgemini SE | 2,320 | 373 | ||

Atlassian Corp., Class A1 | 1,239 | 326 | ||

Globant SA1 | 1,272 | 290 | ||

ASML Holding NV | 122 | 85 | ||

13,014 | ||||

Financials 13.48% | ||||

JPMorgan Chase & Co. | 4,625 | 1,155 | ||

Visa, Inc., Class A | 3,200 | 1,008 | ||

London Stock Exchange Group PLC | 5,831 | 837 | ||

Marsh & McLennan Companies, Inc. | 3,129 | 730 | ||

DBS Group Holdings, Ltd. | 21,200 | 672 | ||

Mastercard, Inc., Class A | 1,252 | 667 | ||

S&P Global, Inc. | 1,249 | 653 | ||

AIA Group, Ltd. | 86,800 | 649 | ||

Aon PLC, Class A | 1,311 | 513 | ||

Wells Fargo & Co. | 6,693 | 510 | ||

Hong Kong Exchanges and Clearing, Ltd. | 12,000 | 447 | ||

Arthur J. Gallagher & Co. | 1,345 | 420 | ||

Partners Group Holding AG | 285 | 414 | ||

Skandinaviska Enskilda Banken AB, Class A | 29,128 | 405 | ||

12 | Capital Group Equity Exchange-Traded Funds |

Common stocks (continued) | Shares | Value (000) | ||

Financials (continued) | ||||

NatWest Group PLC | 73,376 | $377 | ||

CME Group, Inc., Class A | 1,387 | 330 | ||

DNB Bank ASA | 14,194 | 297 | ||

10,084 | ||||

Health care 12.29% | ||||

Novo Nordisk AS, Class B | 15,458 | 1,661 | ||

AstraZeneca PLC | 10,492 | 1,419 | ||

UnitedHealth Group, Inc. | 1,793 | 1,094 | ||

Abbott Laboratories | 8,390 | 997 | ||

EssilorLuxottica SA | 3,712 | 903 | ||

Danaher Corp. | 3,054 | 732 | ||

Regeneron Pharmaceuticals, Inc.1 | 859 | 645 | ||

AbbVie, Inc. | 3,215 | 588 | ||

Bristol-Myers Squibb Co. | 7,532 | 446 | ||

BeiGene, Ltd. (ADR)1 | 1,815 | 390 | ||

Daiichi Sankyo Co., Ltd. | 10,000 | 317 | ||

9,192 | ||||

Consumer discretionary 7.92% | ||||

Hilton Worldwide Holdings, Inc. | 4,759 | 1,206 | ||

Industria de Diseño Textil, SA | 16,640 | 919 | ||

Royal Caribbean Cruises, Ltd. | 3,281 | 801 | ||

Amadeus IT Group SA, Class A, non-registered shares | 11,160 | 784 | ||

MercadoLibre, Inc.1 | 281 | 558 | ||

Amazon.com, Inc.1 | 2,384 | 496 | ||

LVMH Moët Hennessy-Louis Vuitton SE | 657 | 412 | ||

Tractor Supply Co. | 1,326 | 376 | ||

Hermès International | 168 | 367 | ||

5,919 | ||||

Consumer staples 6.89% | ||||

Philip Morris International, Inc. | 6,738 | 897 | ||

L’Oréal SA, non-registered shares | 1,704 | 593 | ||

Anheuser-Busch InBev SA/NV | 10,945 | 590 | ||

Nestlé SA | 5,537 | 481 | ||

Carlsberg A/S, Class B | 4,105 | 423 | ||

Costco Wholesale Corp. | 415 | 403 | ||

Danone SA | 5,691 | 389 | ||

Constellation Brands, Inc., Class A | 1,490 | 359 | ||

Imperial Brands PLC | 10,664 | 349 | ||

Keurig Dr Pepper, Inc. | 10,683 | 349 | ||

General Mills, Inc. | 4,765 | 316 | ||

5,149 | ||||

Communication services 6.82% | ||||

Alphabet, Inc., Class A | 9,613 | 1,624 | ||

Comcast Corp., Class A | 14,898 | 643 | ||

Meta Platforms, Inc., Class A | 1,038 | 596 | ||

Charter Communications, Inc., Class A1 | 1,362 | 541 | ||

Electronic Arts, Inc. | 3,081 | 504 | ||

Nintendo Co., Ltd. | 7,800 | 459 | ||

Koninklijke KPN NV | 114,403 | 445 | ||

América Móvil, SAB de CV, Class B (ADR) | 19,269 | 286 | ||

5,098 | ||||

Capital Group Equity Exchange-Traded Funds | 13 |

Common stocks (continued) | Shares | Value (000) | ||

Materials 4.15% | ||||

Shin-Etsu Chemical Co., Ltd. | 18,400 | $683 | ||

Air Liquide SA | 3,587 | 597 | ||

Freeport-McMoRan, Inc. | 11,411 | 504 | ||

Givaudan SA | 112 | 494 | ||

Sika AG | 1,612 | 417 | ||

Linde PLC | 887 | 409 | ||

3,104 | ||||

Energy 3.92% | ||||

TotalEnergies SE | 18,202 | 1,059 | ||

TC Energy Corp. | 15,854 | 773 | ||

BP PLC | 118,096 | 579 | ||

Chevron Corp. | 3,209 | 519 | ||

2,930 | ||||

Utilities 2.65% | ||||

Engie SA | 39,534 | 631 | ||

Edison International | 5,756 | 505 | ||

CenterPoint Energy, Inc. | 13,937 | 455 | ||

Constellation Energy Corp. | 1,531 | 393 | ||

1,984 | ||||

Real estate 0.57% | ||||

Equinix, Inc. REIT | 436 | 428 | ||

Total common stocks (cost: $68,854,000) | 71,964 | |||

Short-term securities 3.66% | ||||

Money market investments 3.66% | ||||

Capital Group Central Cash Fund 4.65%2,3 | 27,354 | 2,736 | ||

Total short-term securities (cost: $2,736,000) | 2,736 | |||

Total investment securities 99.89% (cost: $71,590,000) | 74,700 | |||

Other assets less liabilities 0.11% | 82 | |||

Net assets 100.00% | $74,782 | |||

Value at 6/25/20244 (000) | Additions (000) | Reductions (000) | Net realized gain (loss) (000) | Net unrealized appreciation (depreciation) (000) | Value at 11/30/2024 (000) | Dividend or interest income (000) | |

Short-term securities 3.66% | |||||||

Money market investments 3.66% | |||||||

Capital Group Central Cash Fund 4.65% 2 | $— | $7,229 | $4,493 | $— 5 | $— 5 | $2,736 | $47 |

1 | Security did not produce income during the last 12 months. |

2 | Rate represents the seven-day yield at 11/30/2024. |

3 | Part of the same "group of investment companies" as the fund as defined under the Investment Company Act of 1940, as amended. |

4 | Commencement of operations. |

5 | Amount less than one thousand. |

Key to abbreviation(s) |

ADR = American Depositary Receipts |

REIT = Real Estate Investment Trust |

14 | Capital Group Equity Exchange-Traded Funds |

Common stocks 95.91% | Shares | Value (000) | ||

Information technology 26.04% | ||||

Microsoft Corp. | 625,570 | $264,904 | ||

Taiwan Semiconductor Manufacturing Co., Ltd. (ADR) | 1,348,710 | 249,053 | ||

NVIDIA Corp. | 1,458,400 | 201,624 | ||

Broadcom, Inc. | 572,125 | 92,730 | ||

ASML Holding NV | 126,835 | 88,377 | ||

Apple, Inc. | 305,442 | 72,490 | ||

Synopsys, Inc.1 | 119,932 | 66,981 | ||

Shopify, Inc., Class A, subordinate voting shares1 | 399,795 | 46,216 | ||

Applied Materials, Inc. | 195,951 | 34,235 | ||

Arista Networks, Inc.1 | 78,531 | 31,869 | ||

Keyence Corp. | 70,300 | 30,405 | ||

EPAM Systems, Inc.1 | 109,860 | 26,797 | ||

NEC Corp. | 282,500 | 24,061 | ||

Capgemini SE | 70,671 | 11,361 | ||

1,241,103 | ||||

Industrials 16.04% | ||||

Safran SA | 556,420 | 129,843 | ||

Comfort Systems USA, Inc. | 171,600 | 84,645 | ||

Ingersoll-Rand, Inc. | 563,052 | 58,653 | ||

Schneider Electric SE | 222,058 | 57,223 | ||

Caterpillar, Inc. | 134,347 | 54,560 | ||

ITOCHU Corp. | 1,087,100 | 53,643 | ||

Copart, Inc.1 | 820,519 | 52,013 | ||

TransDigm Group, Inc. | 35,152 | 44,044 | ||

Airbus SE, non-registered shares | 263,826 | 41,200 | ||

ASSA ABLOY AB, Class B | 1,198,359 | 36,849 | ||

Johnson Controls International PLC | 417,398 | 35,003 | ||

Ryanair Holdings PLC (ADR) | 756,837 | 33,331 | ||

Carrier Global Corp. | 336,961 | 26,071 | ||

Techtronic Industries Co., Ltd. | 1,695,500 | 23,881 | ||

GT Capital Holdings, Inc. | 1,946,380 | 21,743 | ||

Alliance Global Group, Inc. | 79,922,900 | 11,968 | ||

764,670 | ||||

Health care 14.79% | ||||

Novo Nordisk AS, Class B | 1,246,757 | 133,968 | ||

Eli Lilly and Co. | 124,497 | 99,019 | ||

UnitedHealth Group, Inc. | 136,517 | 83,303 | ||

Vertex Pharmaceuticals, Inc.1 | 148,556 | 69,544 | ||

Thermo Fisher Scientific, Inc. | 129,481 | 68,577 | ||

AstraZeneca PLC | 395,174 | 53,451 | ||

Regeneron Pharmaceuticals, Inc.1 | 58,630 | 43,985 | ||

Pfizer, Inc. | 1,133,399 | 29,706 | ||

Sanofi | 302,635 | 29,495 | ||

Cigna Group (The) | 80,580 | 27,220 | ||

Centene Corp.1 | 423,119 | 25,387 | ||

Argenx SE (ADR)1 | 37,259 | 22,972 | ||

Alnylam Pharmaceuticals, Inc.1 | 71,396 | 18,068 | ||

704,695 | ||||

Consumer discretionary 13.92% | ||||

Chipotle Mexican Grill, Inc.1 | 1,415,025 | 87,052 | ||

LVMH Moët Hennessy-Louis Vuitton SE | 131,343 | 82,358 | ||

Amazon.com, Inc.1 | 344,560 | 71,631 | ||

Booking Holdings, Inc. | 13,108 | 68,188 | ||

Prosus NV, Class N | 1,546,162 | 63,079 | ||

Renault SA | 1,032,206 | 44,274 | ||

Trip.com Group, Ltd. (ADR)1 | 679,757 | 43,946 | ||

InterContinental Hotels Group PLC | 312,725 | 39,063 | ||

MGM China Holdings, Ltd. | 27,038,188 | 33,913 | ||

MercadoLibre, Inc.1 | 16,946 | 33,641 | ||

Home Depot, Inc. | 67,991 | 29,177 | ||

Capital Group Equity Exchange-Traded Funds | 15 |

Common stocks (continued) | Shares | Value (000) | ||

Consumer discretionary (continued) | ||||

Starbucks Corp. | 231,456 | $23,715 | ||

Evolution AB | 249,960 | 21,849 | ||

lululemon athletica, Inc.1 | 66,740 | 21,401 | ||

663,287 | ||||

Financials 12.40% | ||||

3i Group PLC | 1,795,419 | 84,878 | ||

Fiserv, Inc.1 | 377,998 | 83,523 | ||

Aon PLC, Class A | 174,012 | 68,133 | ||

AXA SA | 1,914,877 | 66,834 | ||

Visa, Inc., Class A | 166,168 | 52,356 | ||

Blackstone, Inc. | 244,572 | 46,735 | ||

Tradeweb Markets, Inc., Class A | 280,361 | 37,989 | ||

Citigroup, Inc. | 535,785 | 37,971 | ||

Axis Bank, Ltd. | 2,762,409 | 37,149 | ||

Société Générale | 1,029,061 | 27,330 | ||

Prudential PLC | 3,266,770 | 26,724 | ||

Banco Bilbao Vizcaya Argentaria, SA | 2,243,130 | 21,213 | ||

590,835 | ||||

Communication services 4.82% | ||||

Alphabet, Inc., Class A | 734,427 | 124,081 | ||

Meta Platforms, Inc., Class A | 149,942 | 86,115 | ||

Publicis Groupe SA | 181,311 | 19,706 | ||

229,902 | ||||

Energy 3.22% | ||||

Canadian Natural Resources, Ltd. (CAD denominated) | 2,453,146 | 83,258 | ||

Schlumberger NV | 998,929 | 43,893 | ||

Reliance Industries, Ltd. | 1,708,009 | 26,120 | ||

153,271 | ||||

Consumer staples 2.57% | ||||

Monster Beverage Corp.1 | 671,560 | 37,023 | ||

Philip Morris International, Inc. | 232,364 | 30,918 | ||

British American Tobacco PLC | 772,323 | 29,414 | ||

Nestlé SA | 292,072 | 25,367 | ||

122,722 | ||||

Materials 2.11% | ||||

Linde PLC | 188,359 | 86,832 | ||

First Quantum Minerals, Ltd.1 | 1,013,298 | 13,844 | ||

100,676 | ||||

Total common stocks (cost: $3,838,354,000) | 4,571,161 | |||

Preferred securities 0.89% | ||||

Information technology 0.89% | ||||

Samsung Electronics Co., Ltd., nonvoting preferred shares | 1,279,702 | 42,380 | ||

Total preferred securities (cost: $56,237,000) | 42,380 | |||

16 | Capital Group Equity Exchange-Traded Funds |

Short-term securities 3.09% | Shares | Value (000) | ||

Money market investments 3.09% | ||||

Capital Group Central Cash Fund 4.65%2,3 | 1,473,189 | $147,333 | ||

Total short-term securities (cost: $147,333,000) | 147,333 | |||

Total investment securities 99.89% (cost: $4,041,924,000) | 4,760,874 | |||

Other assets less liabilities 0.11% | 5,441 | |||

Net assets 100.00% | $4,766,315 | |||

Value at 6/1/2024 (000) | Additions (000) | Reductions (000) | Net realized gain (loss) (000) | Net unrealized appreciation (depreciation) (000) | Value at 11/30/2024 (000) | Dividend or interest income (000) | |

Short-term securities 3.09% | |||||||

Money market investments 3.09% | |||||||

Capital Group Central Cash Fund 4.65% 2 | $64,195 | $500,258 | $417,094 | $(11 ) | $(15 ) | $147,333 | $1,705 |

1 | Security did not produce income during the last 12 months. |

2 | Rate represents the seven-day yield at 11/30/2024. |

3 | Part of the same "group of investment companies" as the fund as defined under the Investment Company Act of 1940, as amended. |

Key to abbreviation(s) |

ADR = American Depositary Receipts |

CAD = Canadian dollars |

Capital Group Equity Exchange-Traded Funds | 17 |

Common stocks 97.98% | Shares | Value (000) | ||

Information technology 23.85% | ||||

Microsoft Corp. | 969,171 | $410,405 | ||

NVIDIA Corp. | 2,290,528 | 316,666 | ||

Broadcom, Inc. | 1,545,185 | 250,444 | ||

Shopify, Inc., Class A, subordinate voting shares1 | 1,468,824 | 169,796 | ||

Apple, Inc. | 703,212 | 166,893 | ||

Salesforce, Inc. | 433,090 | 142,915 | ||

MicroStrategy, Inc., Class A1,2 | 353,691 | 137,045 | ||

Cloudflare, Inc., Class A1 | 980,135 | 97,847 | ||

Taiwan Semiconductor Manufacturing Co., Ltd. (ADR) | 437,114 | 80,718 | ||

Synopsys, Inc.1 | 99,292 | 55,454 | ||

Motorola Solutions, Inc. | 102,606 | 51,272 | ||

Constellation Software, Inc. | 14,493 | 49,003 | ||

Atlassian Corp., Class A1 | 149,979 | 39,532 | ||

Adobe, Inc.1 | 63,508 | 32,766 | ||

Micron Technology, Inc. | 307,813 | 30,150 | ||

ASML Holding NV (ADR) | 36,994 | 25,400 | ||

Applied Materials, Inc. | 142,844 | 24,956 | ||

Unity Software, Inc.1 | 1,012,905 | 24,421 | ||

Dell Technologies, Inc., Class C | 191,152 | 24,389 | ||

2,130,072 | ||||

Communication services 18.92% | ||||

Meta Platforms, Inc., Class A | 1,311,747 | 753,362 | ||

Netflix, Inc.1 | 532,024 | 471,804 | ||

Alphabet, Inc., Class C | 1,272,816 | 217,002 | ||

Alphabet, Inc., Class A | 755,948 | 127,718 | ||

Charter Communications, Inc., Class A1 | 190,220 | 75,511 | ||

Snap, Inc., Class A, nonvoting shares1 | 3,758,304 | 44,386 | ||

1,689,783 | ||||

Consumer discretionary 14.18% | ||||

Tesla, Inc.1 | 1,399,588 | 483,082 | ||

Amazon.com, Inc.1 | 758,491 | 157,683 | ||

Royal Caribbean Cruises, Ltd. | 461,668 | 112,675 | ||

DoorDash, Inc., Class A1 | 587,740 | 106,075 | ||

Home Depot, Inc. | 143,669 | 61,653 | ||

Tractor Supply Co. | 163,588 | 46,405 | ||

Airbnb, Inc., Class A1 | 309,868 | 42,176 | ||

Chipotle Mexican Grill, Inc.1 | 633,254 | 38,958 | ||

Aramark | 893,448 | 36,354 | ||

Norwegian Cruise Line Holdings, Ltd.1 | 1,333,005 | 35,844 | ||

Amadeus IT Group SA, Class A, non-registered shares | 504,906 | 35,491 | ||

Hermès International | 15,964 | 34,887 | ||

D.R. Horton, Inc. | 198,974 | 33,583 | ||

Evolution AB | 238,067 | 20,810 | ||

Booking Holdings, Inc. | 3,951 | 20,553 | ||

1,266,229 | ||||

Health care 12.89% | ||||

Intuitive Surgical, Inc.1 | 396,826 | 215,080 | ||

UnitedHealth Group, Inc. | 273,865 | 167,112 | ||

Vertex Pharmaceuticals, Inc.1 | 280,249 | 131,193 | ||

Regeneron Pharmaceuticals, Inc.1 | 165,821 | 124,402 | ||

Eli Lilly and Co. | 141,634 | 112,649 | ||

Alnylam Pharmaceuticals, Inc.1 | 422,775 | 106,992 | ||

Boston Scientific Corp.1 | 644,632 | 58,442 | ||

Thermo Fisher Scientific, Inc. | 108,501 | 57,465 | ||

HCA Healthcare, Inc. | 129,205 | 42,279 | ||

Abbott Laboratories | 277,308 | 32,936 | ||

Danaher Corp. | 116,416 | 27,904 | ||

Novo Nordisk AS, Class B | 218,831 | 23,514 | ||

18 | Capital Group Equity Exchange-Traded Funds |

Common stocks (continued) | Shares | Value (000) | ||

Health care (continued) | ||||

Mettler-Toledo International, Inc.1 | 17,756 | $22,216 | ||

Sarepta Therapeutics, Inc.1 | 153,992 | 20,533 | ||

NovoCure, Ltd.1 | 424,274 | 8,503 | ||

1,151,220 | ||||

Industrials 11.53% | ||||

TransDigm Group, Inc. | 80,019 | 100,261 | ||

General Electric Co. | 517,005 | 94,178 | ||

Carrier Global Corp. | 1,174,412 | 90,864 | ||

Uber Technologies, Inc.1 | 1,179,652 | 84,888 | ||

GE Vernova, Inc.1 | 216,678 | 72,396 | ||

Ingersoll-Rand, Inc. | 561,058 | 58,445 | ||

Caterpillar, Inc. | 115,967 | 47,095 | ||

Quanta Services, Inc. | 134,067 | 46,189 | ||

United Airlines Holdings, Inc.1 | 473,182 | 45,818 | ||

Eaton Corp. PLC | 110,362 | 41,432 | ||

Ryanair Holdings PLC (ADR) | 885,023 | 38,976 | ||

United Rentals, Inc. | 44,249 | 38,320 | ||

Equifax, Inc. | 144,444 | 37,781 | ||

FTAI Aviation, Ltd. | 204,275 | 34,486 | ||

Dayforce, Inc.1 | 414,336 | 33,143 | ||

Old Dominion Freight Line, Inc. | 147,039 | 33,104 | ||

Airbus SE, non-registered shares | 207,994 | 32,481 | ||

Genpact, Ltd. | 695,380 | 32,099 | ||

MTU Aero Engines AG | 82,293 | 28,061 | ||

Boeing Co. (The)1 | 144,451 | 22,454 | ||

Southwest Airlines Co. | 526,271 | 17,030 | ||

1,029,501 | ||||

Financials 8.75% | ||||

Visa, Inc., Class A | 667,252 | 210,238 | ||

KKR & Co., Inc. | 620,415 | 101,047 | ||

Fiserv, Inc.1 | 442,304 | 97,731 | ||

Bank of America Corp. | 2,017,829 | 95,867 | ||

Mastercard, Inc., Class A | 153,947 | 82,044 | ||

Apollo Asset Management, Inc. | 316,984 | 55,482 | ||

Toast, Inc., Class A1 | 1,193,318 | 51,957 | ||

Blackstone, Inc. | 190,531 | 36,409 | ||

Affirm Holdings, Inc., Class A1 | 403,398 | 28,242 | ||

Block, Inc., Class A1 | 254,718 | 22,555 | ||

781,572 | ||||

Energy 3.09% | ||||

Halliburton Co. | 2,366,464 | 75,395 | ||

Schlumberger NV | 1,334,930 | 58,657 | ||

EOG Resources, Inc. | 348,371 | 46,424 | ||

Canadian Natural Resources, Ltd. (CAD denominated) | 1,235,522 | 41,933 | ||

Cenovus Energy, Inc. | 1,865,370 | 29,549 | ||

Tourmaline Oil Corp. | 504,585 | 23,814 | ||

275,772 | ||||

Consumer staples 1.79% | ||||

Performance Food Group Co.1 | 788,316 | 69,561 | ||

Costco Wholesale Corp. | 61,140 | 59,421 | ||

Target Corp. | 231,993 | 30,695 | ||

159,677 | ||||

Materials 1.37% | ||||

Wheaton Precious Metals Corp. | 656,988 | 40,950 | ||

ATI, Inc.1 | 532,636 | 32,049 | ||

Albemarle Corp.2 | 249,499 | 26,871 | ||

Grupo México, SAB de CV, Series B | 4,660,346 | 22,492 | ||

122,362 | ||||

Capital Group Equity Exchange-Traded Funds | 19 |

Common stocks (continued) | Shares | Value (000) | ||

Utilities 0.91% | ||||

PG&E Corp. | 2,281,566 | $49,350 | ||

Constellation Energy Corp. | 126,212 | 32,381 | ||

81,731 | ||||

Real estate 0.70% | ||||

CoStar Group, Inc.1 | 464,822 | 37,808 | ||

Zillow Group, Inc., Class C, nonvoting shares1 | 292,997 | 24,820 | ||

62,628 | ||||

Total common stocks (cost: $6,466,246,000) | 8,750,547 | |||

Rights & warrants 0.00% | ||||

Information technology 0.00% | ||||

Constellation Software, Inc., warrants, expire 3/31/20401,3 | 4,185 | — 4 | ||

Short-term securities 1.96% | ||||

Money market investments 1.70% | ||||

Capital Group Central Cash Fund 4.65%5,6 | 1,520,162 | 152,031 | ||

Money market investments purchased with collateral from securities on loan 0.26% | ||||

Capital Group Central Cash Fund 4.65%5,6,7 | 10,000,000 | 10,000 | ||

State Street Institutional U.S. Government Money Market Fund, Institutional Class 4.56%5,7 | 13,131,957 | 13,132 | ||

23,132 | ||||

Total short-term securities (cost: $175,151,000) | 175,163 | |||

Total investment securities 99.94% (cost: $6,641,397,000) | 8,925,710 | |||

Other assets less liabilities 0.06% | 5,043 | |||

Net assets 100.00% | $8,930,753 | |||

Value at 6/1/2024 (000) | Additions (000) | Reductions (000) | Net realized gain (loss) (000) | Net unrealized appreciation (depreciation) (000) | Value at 11/30/2024 (000) | Dividend or interest income (000) | |

Short-term securities 1.81% | |||||||

Money market investments 1.70% | |||||||

Capital Group Central Cash Fund 4.65% 5 | $114,011 | $587,810 | $549,789 | $6 | $(7 ) | $152,031 | $2,319 |

Money market investments purchased with collateral from securities on loan 0.11% | |||||||

Capital Group Central Cash Fund 4.65% 5,7 | — | 10,000 8 | — | — | — | 10,000 | — 9 |

Total short-term securities | 162,031 | ||||||

Total 1.81% | $6 | $(7 ) | $162,031 | $2,319 | |||

20 | Capital Group Equity Exchange-Traded Funds |

1 | Security did not produce income during the last 12 months. |

2 | All or a portion of this security was on loan. The total value of all such securities was $25,173,000, which represented 0.28% of the net assets of the fund. Refer to Note 5 for more information on securities lending. |

3 | Value determined using significant unobservable inputs. |

4 | Amount less than one thousand. |

5 | Rate represents the seven-day yield at 11/30/2024. |

6 | Part of the same "group of investment companies" as the fund as defined under the Investment Company Act of 1940, as amended. |

7 | Security purchased with cash collateral from securities on loan. Refer to Note 5 for more information on securities lending. |

8 | Represents net activity. Refer to Note 5 for more information on securities lending. |

9 | Dividend income is included with securities lending income in the fund’s statement of operations and is not shown in this table. |

Key to abbreviation(s) |

ADR = American Depositary Receipts |

CAD = Canadian dollars |

Capital Group Equity Exchange-Traded Funds | 21 |

Common stocks 96.23% | Shares | Value (000) | ||

Financials 20.17% | ||||

Zurich Insurance Group AG | 1,503 | $953 | ||

AXA SA | 22,365 | 781 | ||

HSBC Holdings PLC | 56,144 | 524 | ||

KB Financial Group, Inc. | 7,311 | 504 | ||

Tryg A/S | 19,510 | 450 | ||

Tokio Marine Holdings, Inc. | 11,100 | 413 | ||

Deutsche Bank AG | 24,119 | 410 | ||

Société Générale | 15,280 | 406 | ||

UniCredit SpA | 10,186 | 392 | ||

Ping An Insurance (Group) Company of China, Ltd., Class H | 64,500 | 371 | ||

Euronext NV | 3,199 | 358 | ||

NatWest Group PLC | 67,052 | 344 | ||

London Stock Exchange Group PLC | 2,322 | 334 | ||

Bank Hapoalim BM | 28,925 | 332 | ||

HDFC Bank, Ltd. | 14,565 | 310 | ||

Skandinaviska Enskilda Banken AB, Class A | 21,822 | 304 | ||

Royal Bank of Canada | 2,382 | 300 | ||

Hana Financial Group, Inc. | 6,523 | 292 | ||

Banco Bilbao Vizcaya Argentaria, SA | 30,839 | 292 | ||

Resona Holdings, Inc. | 33,700 | 281 | ||

Kotak Mahindra Bank, Ltd. | 13,397 | 280 | ||

Edenred SA | 8,299 | 275 | ||

CaixaBank, SA, non-registered shares | 47,242 | 257 | ||

Prudential PLC | 30,957 | 253 | ||

DBS Group Holdings, Ltd. | 7,300 | 231 | ||

AIA Group, Ltd. | 29,600 | 221 | ||

Aon PLC, Class A | 554 | 217 | ||

PICC Property and Casualty Co., Ltd., Class H | 138,000 | 209 | ||

Mizuho Financial Group, Inc. | 7,200 | 182 | ||

DNB Bank ASA | 8,147 | 170 | ||

Grupo Financiero Banorte, SAB de CV, Series O | 17,628 | 117 | ||

Hong Kong Exchanges and Clearing, Ltd. | 3,000 | 112 | ||

Discovery, Ltd. | 9,134 | 98 | ||

10,973 | ||||

Industrials 14.98% | ||||

BAE Systems PLC | 63,666 | 996 | ||

Airbus SE, non-registered shares | 4,748 | 741 | ||

ABB, Ltd. | 9,048 | 517 | ||

SMC Corp. | 1,100 | 467 | ||

Safran SA | 1,839 | 429 | ||

Rheinmetall AG, non-registered shares | 579 | 381 | ||

Mitsui & Co., Ltd. | 16,100 | 337 | ||

Siemens AG | 1,651 | 320 | ||

RELX PLC | 6,716 | 317 | ||

Ryanair Holdings PLC (ADR) | 7,080 | 312 | ||

Diploma PLC | 5,347 | 304 | ||

Canadian National Railway Co. (CAD denominated) | 2,687 | 300 | ||

Epiroc AB, Class A | 14,665 | 268 | ||

Volvo AB, Class B | 9,975 | 249 | ||

Thales SA | 1,651 | 247 | ||

ASSA ABLOY AB, Class B | 7,599 | 234 | ||

Copa Holdings, SA, Class A | 2,438 | 228 | ||

CCR SA, ordinary nominative shares | 121,058 | 224 | ||

ITOCHU Corp. | 4,100 | 202 | ||

DSV A/S | 825 | 176 | ||

Hitachi, Ltd. | 7,000 | 175 | ||

Pluxee NV1 | 6,924 | 149 | ||

TFI International, Inc. (CAD denominated) | 952 | 145 | ||

Alliance Global Group, Inc. | 853,900 | 128 | ||

22 | Capital Group Equity Exchange-Traded Funds |

Common stocks (continued) | Shares | Value (000) | ||

Industrials (continued) | ||||

Grupo Aeroportuario del Pacífico, SAB de CV, Class B | 6,231 | $115 | ||

Wizz Air Holdings PLC1 | 6,247 | 103 | ||

Bombardier, Inc., Class B1 | 1,277 | 88 | ||

8,152 | ||||

Information technology 13.67% | ||||

Taiwan Semiconductor Manufacturing Co., Ltd. (ADR) | 12,242 | 2,261 | ||

MediaTek, Inc. | 25,000 | 966 | ||

ASML Holding NV | 1,302 | 907 | ||

Broadcom, Inc. | 4,001 | 648 | ||

SAP SE | 2,113 | 503 | ||

Samsung Electronics Co., Ltd. | 12,684 | 493 | ||

Sage Group PLC (The) | 19,285 | 322 | ||

Capgemini SE | 1,848 | 297 | ||

Keyence Corp. | 600 | 260 | ||

E Ink Holdings, Inc. | 28,000 | 242 | ||

Fujitsu, Ltd. | 8,400 | 161 | ||

ASM International NV | 285 | 154 | ||

Tokyo Electron, Ltd. | 800 | 125 | ||

ASMPT, Ltd. | 9,800 | 97 | ||

7,436 | ||||

Consumer discretionary 10.72% | ||||

Industria de Diseño Textil, SA | 16,769 | 926 | ||

Trip.com Group, Ltd. (ADR)1 | 8,441 | 546 | ||

Renault SA | 12,018 | 515 | ||

Prosus NV, Class N | 9,210 | 376 | ||

Evolution AB | 3,705 | 324 | ||

Restaurant Brands International, Inc. (CAD denominated) | 4,504 | 314 | ||

MGM China Holdings, Ltd. | 232,400 | 292 | ||

Suzuki Motor Corp. | 26,600 | 282 | ||

LVMH Moët Hennessy-Louis Vuitton SE | 445 | 279 | ||

InterContinental Hotels Group PLC | 1,836 | 229 | ||

B&M European Value Retail SA | 47,421 | 210 | ||

Stellantis NV | 15,666 | 208 | ||

Wynn Macau, Ltd. | 274,400 | 206 | ||

Midea Group Co., Ltd., Class A | 19,600 | 190 | ||

Hyundai Motor Co. | 1,179 | 185 | ||

Bajaj Auto, Ltd. | 1,647 | 176 | ||

Paltac Corp. | 5,500 | 158 | ||

Entain PLC | 14,919 | 153 | ||

H World Group, Ltd. (ADR) | 4,661 | 150 | ||

Galaxy Entertainment Group, Ltd. | 26,000 | 115 | ||

5,834 | ||||

Consumer staples 10.27% | ||||

British American Tobacco PLC | 24,965 | 951 | ||

Philip Morris International, Inc. | 6,872 | 914 | ||

Imperial Brands PLC | 15,980 | 523 | ||

Nestlé SA | 5,887 | 511 | ||

Carlsberg A/S, Class B | 3,660 | 378 | ||

Arca Continental, SAB de CV | 37,300 | 315 | ||

Carrefour SA, non-registered shares | 18,923 | 288 | ||

ITC, Ltd. | 49,262 | 278 | ||

Pernod Ricard SA | 2,397 | 269 | ||

KT&G Corp. | 2,931 | 256 | ||

L’Oréal SA, non-registered shares | 619 | 215 | ||

Tsingtao Brewery Co., Ltd., Class H | 34,000 | 213 | ||

Anheuser-Busch InBev SA/NV | 3,753 | 202 | ||

Asahi Group Holdings, Ltd. | 14,300 | 156 | ||

Ocado Group PLC1 | 30,297 | 122 | ||

5,591 | ||||

Capital Group Equity Exchange-Traded Funds | 23 |

Common stocks (continued) | Shares | Value (000) | ||

Health care 7.30% | ||||

AstraZeneca PLC | 9,301 | $1,258 | ||

Novo Nordisk AS, Class B | 11,687 | 1,256 | ||

Sanofi | 6,636 | 647 | ||

EssilorLuxottica SA | 2,464 | 599 | ||

Grifols, SA, Class B (ADR)1 | 15,603 | 109 | ||

Bayer AG | 5,098 | 105 | ||

3,974 | ||||

Communication services 5.63% | ||||

Tencent Holdings, Ltd. | 17,200 | 880 | ||

Koninklijke KPN NV | 196,904 | 765 | ||

Telefónica, SA, non-registered shares | 58,334 | 265 | ||

Indus Towers, Ltd.1 | 53,869 | 223 | ||

América Móvil, SAB de CV, Class B (ADR) | 14,854 | 220 | ||

BT Group PLC | 101,287 | 206 | ||

MTN Group, Ltd. | 32,249 | 144 | ||

KANZHUN, Ltd., Class A (ADR) | 9,800 | 132 | ||

Vodafone Group PLC | 133,008 | 120 | ||

NetEase, Inc. | 6,400 | 110 | ||

3,065 | ||||

Energy 4.77% | ||||

TotalEnergies SE | 19,802 | 1,152 | ||

Canadian Natural Resources, Ltd. (CAD denominated) | 12,814 | 435 | ||

BP PLC | 74,774 | 367 | ||

Cameco Corp. | 5,950 | 356 | ||

TC Energy Corp. | 3,257 | 159 | ||

Schlumberger NV | 2,924 | 128 | ||

2,597 | ||||

Materials 4.65% | ||||

Linde PLC | 877 | 404 | ||

Glencore PLC1 | 67,930 | 329 | ||

Rio Tinto PLC | 4,932 | 311 | ||

Barrick Gold Corp. | 17,157 | 300 | ||

Fortescue, Ltd. | 19,313 | 239 | ||

Holcim, Ltd. | 2,199 | 224 | ||

Vale SA (ADR), ordinary nominative shares | 22,260 | 220 | ||

Air Liquide SA | 1,317 | 219 | ||

Nutrien, Ltd. | 3,299 | 154 | ||

Freeport-McMoRan, Inc. | 2,891 | 128 | ||

2,528 | ||||

Real estate 2.05% | ||||

Embassy Office Parks REIT | 69,942 | 307 | ||

CK Asset Holdings, Ltd. | 67,500 | 276 | ||

Mitsubishi Estate Co., Ltd. | 16,000 | 227 | ||

Prologis Property Mexico, SA de CV, REIT | 40,218 | 119 | ||

Link REIT | 25,600 | 111 | ||

Longfor Group Holdings, Ltd. | 55,500 | 78 | ||

1,118 | ||||

Utilities 2.02% | ||||

Engie SA | 23,531 | 375 | ||

Brookfield Infrastructure Partners, LP | 8,145 | 288 | ||

SSE PLC | 10,185 | 230 | ||

Iberdrola, SA, non-registered shares | 14,273 | 204 | ||

1,097 | ||||

Total common stocks (cost: $53,063,000) | 52,365 | |||

24 | Capital Group Equity Exchange-Traded Funds |

Short-term securities 3.56% | Shares | Value (000) | ||

Money market investments 3.56% | ||||

Capital Group Central Cash Fund 4.65%2,3 | 19,375 | $1,938 | ||

Total short-term securities (cost: $1,938,000) | 1,938 | |||

Total investment securities 99.79% (cost: $55,001,000) | 54,303 | |||

Other assets less liabilities 0.21% | 113 | |||

Net assets 100.00% | $54,416 | |||

Value at 6/25/20244 (000) | Additions (000) | Reductions (000) | Net realized gain (loss) (000) | Net unrealized appreciation (depreciation) (000) | Value at 11/30/2024 (000) | Dividend or interest income (000) | |

Short-term securities 3.56% | |||||||

Money market investments 3.56% | |||||||

Capital Group Central Cash Fund 4.65% 2 | $— | $11,411 | $9,473 | $— 5 | $— 5 | $1,938 | $30 |

1 | Security did not produce income during the last 12 months. |

2 | Rate represents the seven-day yield at 11/30/2024. |

3 | Part of the same "group of investment companies" as the fund as defined under the Investment Company Act of 1940, as amended. |

4 | Commencement of operations. |

5 | Amount less than one thousand. |

Key to abbreviation(s) |

ADR = American Depositary Receipts |

CAD = Canadian dollars |

REIT = Real Estate Investment Trust |

Capital Group Equity Exchange-Traded Funds | 25 |

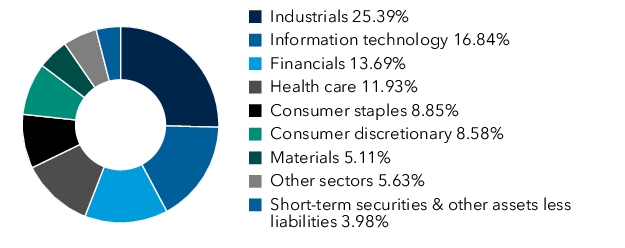

Common stocks 96.02% | Shares | Value (000) | ||

Industrials 25.39% | ||||

Safran SA | 37,967 | $8,860 | ||

ABB, Ltd. | 93,926 | 5,363 | ||

Rolls-Royce Holdings PLC1 | 725,448 | 5,165 | ||

ITOCHU Corp. | 102,800 | 5,073 | ||

Airbus SE, non-registered shares | 29,092 | 4,543 | ||

RELX PLC | 89,382 | 4,221 | ||

Epiroc AB, Class A | 218,947 | 3,995 | ||

Canadian National Railway Co. | 35,364 | 3,950 | ||

Hitachi, Ltd. | 149,600 | 3,750 | ||

DSV A/S | 17,004 | 3,636 | ||

Mitsubishi Corp. | 208,400 | 3,517 | ||

SMC Corp. | 7,700 | 3,270 | ||

Recruit Holdings Co., Ltd. | 46,900 | 3,255 | ||

BAE Systems PLC | 168,958 | 2,642 | ||

TFI International, Inc. (CAD denominated) | 17,247 | 2,626 | ||

MTU Aero Engines AG | 6,941 | 2,367 | ||

Marubeni Corp. | 96,500 | 1,453 | ||

67,686 | ||||

Information technology 16.84% | ||||

SAP SE | 42,329 | 10,075 | ||

Taiwan Semiconductor Manufacturing Co., Ltd. (ADR) | 34,680 | 6,404 | ||

ASML Holding NV | 8,334 | 5,807 | ||

Keyence Corp. | 9,600 | 4,152 | ||

OBIC Co., Ltd. | 115,900 | 3,799 | ||

Capgemini SE | 21,288 | 3,422 | ||

Nomura Research Institute, Ltd. | 101,400 | 3,104 | ||

Halma PLC | 87,562 | 3,022 | ||

Tokyo Electron, Ltd. | 17,100 | 2,664 | ||

TDK Corp. | 189,200 | 2,439 | ||

44,888 | ||||

Financials 13.69% | ||||

London Stock Exchange Group PLC | 52,886 | 7,597 | ||

DBS Group Holdings, Ltd. | 151,300 | 4,796 | ||

Skandinaviska Enskilda Banken AB, Class A | 244,079 | 3,395 | ||

DNB Bank ASA | 151,850 | 3,175 | ||

NatWest Group PLC | 596,735 | 3,063 | ||

Euronext NV | 25,023 | 2,799 | ||

Hong Kong Exchanges and Clearing, Ltd. | 71,300 | 2,655 | ||

Deutsche Bank AG | 145,347 | 2,473 | ||

AIA Group, Ltd. | 329,400 | 2,462 | ||

Partners Group Holding AG | 1,551 | 2,254 | ||

Resona Holdings, Inc. | 218,900 | 1,829 | ||

36,498 | ||||

Health care 11.93% | ||||

Novo Nordisk AS, Class B | 85,687 | 9,207 | ||

AstraZeneca PLC | 49,411 | 6,683 | ||

EssilorLuxottica SA | 21,809 | 5,304 | ||

Daiichi Sankyo Co., Ltd. | 124,400 | 3,948 | ||

HOYA Corp. | 16,100 | 2,072 | ||

Chugai Pharmaceutical Co., Ltd. | 39,200 | 1,729 | ||

BeiGene, Ltd. (ADR)1 | 7,044 | 1,515 | ||

Innovent Biologics, Inc.1 | 268,500 | 1,330 | ||

31,788 | ||||

Consumer staples 8.85% | ||||

L’Oréal SA, non-registered shares | 11,716 | 4,075 | ||

Imperial Brands PLC | 112,285 | 3,677 | ||

Nestlé SA | 41,491 | 3,603 | ||

Anheuser-Busch InBev SA/NV | 61,146 | 3,296 | ||

Danone SA | 36,709 | 2,512 | ||

26 | Capital Group Equity Exchange-Traded Funds |

Common stocks (continued) | Shares | Value (000) | ||

Consumer staples (continued) | ||||

British American Tobacco PLC | 65,368 | $2,490 | ||

Carlsberg A/S, Class B | 20,084 | 2,071 | ||

Uni-Charm Corp. | 72,000 | 1,872 | ||

23,596 | ||||

Consumer discretionary 8.58% | ||||

Amadeus IT Group SA, Class A, non-registered shares | 73,420 | 5,161 | ||

Industria de Diseño Textil, SA | 83,355 | 4,603 | ||

MercadoLibre, Inc.1 | 1,831 | 3,635 | ||

LVMH Moët Hennessy-Louis Vuitton SE | 5,353 | 3,357 | ||

Ferrari NV | 5,429 | 2,365 | ||

Hermès International | 966 | 2,111 | ||

Evolution AB | 18,693 | 1,634 | ||

22,866 | ||||

Materials 5.11% | ||||

Sika AG | 16,422 | 4,254 | ||

Givaudan SA | 874 | 3,852 | ||

Air Liquide SA | 19,682 | 3,276 | ||

Shin-Etsu Chemical Co., Ltd. | 60,500 | 2,245 | ||

13,627 | ||||

Energy 3.14% | ||||

TotalEnergies SE | 105,748 | 6,152 | ||

BP PLC | 451,990 | 2,216 | ||

8,368 | ||||

Utilities 1.28% | ||||

Engie SA | 214,094 | 3,418 | ||

Communication services 1.21% | ||||

Tencent Holdings, Ltd. | 63,000 | 3,222 | ||

Total common stocks (cost: $245,816,000) | 255,957 | |||

Short-term securities 3.85% | ||||

Money market investments 3.85% | ||||

Capital Group Central Cash Fund 4.65%2,3 | 102,546 | 10,256 | ||

Total short-term securities (cost: $10,255,000) | 10,256 | |||

Total investment securities 99.87% (cost: $256,071,000) | 266,213 | |||

Other assets less liabilities 0.13% | 357 | |||

Net assets 100.00% | $266,570 | |||

Value at 6/1/2024 (000) | Additions (000) | Reductions (000) | Net realized gain (loss) (000) | Net unrealized appreciation (depreciation) (000) | Value at 11/30/2024 (000) | Dividend or interest income (000) | |

Short-term securities 3.85% | |||||||

Money market investments 3.85% | |||||||

Capital Group Central Cash Fund 4.65% 2 | $6,033 | $18,515 | $14,291 | $(1 ) | $— 4 | $10,256 | $229 |

Capital Group Equity Exchange-Traded Funds | 27 |

1 | Security did not produce income during the last 12 months. |

2 | Rate represents the seven-day yield at 11/30/2024. |

3 | Part of the same "group of investment companies" as the fund as defined under the Investment Company Act of 1940, as amended. |

4 | Amount less than one thousand. |

Key to abbreviation(s) |

ADR = American Depositary Receipts |

CAD = Canadian dollars |

28 | Capital Group Equity Exchange-Traded Funds |

Common stocks 96.35% | Shares | Value (000) | ||

Industrials 20.61% | ||||

Recruit Holdings Co., Ltd. | 1,822,700 | $126,495 | ||

Airbus SE, non-registered shares | 632,101 | 98,711 | ||

Siemens AG | 300,907 | 58,327 | ||

Techtronic Industries Co., Ltd. | 3,937,500 | 55,459 | ||

Melrose Industries PLC | 6,272,268 | 45,921 | ||

MTU Aero Engines AG | 118,282 | 40,332 | ||

Rolls-Royce Holdings PLC1 | 4,671,124 | 33,258 | ||

Safran SA | 141,794 | 33,088 | ||

Ashtead Group PLC | 396,407 | 31,781 | ||

Volvo AB, Class B | 1,178,824 | 29,397 | ||

Diploma PLC | 489,992 | 27,855 | ||

Kingspan Group PLC | 277,363 | 20,900 | ||

Daikin Industries, Ltd. | 164,100 | 19,844 | ||

International Container Terminal Services, Inc. | 2,567,260 | 16,200 | ||

SMC Corp. | 34,700 | 14,734 | ||

652,302 | ||||

Information technology 14.73% | ||||

Shopify, Inc., Class A, subordinate voting shares1 | 818,641 | 94,635 | ||

Taiwan Semiconductor Manufacturing Co., Ltd. | 2,971,000 | 91,097 | ||

SAP SE | 333,904 | 79,473 | ||

ASML Holding NV | 66,074 | 46,039 | ||

SK hynix, Inc. | 379,867 | 43,540 | ||

Samsung Electronics Co., Ltd. | 969,860 | 37,681 | ||

Constellation Software, Inc. | 6,633 | 22,427 | ||

Fujitsu, Ltd. | 980,000 | 18,770 | ||

Renesas Electronics Corp. | 1,280,100 | 16,797 | ||

Keyence Corp. | 36,400 | 15,743 | ||

466,202 | ||||

Health care 11.99% | ||||

Daiichi Sankyo Co., Ltd. | 4,376,700 | 138,900 | ||

Novo Nordisk AS, Class B | 1,267,459 | 136,193 | ||

UCB SA | 171,916 | 33,722 | ||

Sanofi | 256,919 | 25,039 | ||

Eurofins Scientific SE, non-registered shares | 337,925 | 16,733 | ||

AstraZeneca PLC | 120,364 | 16,281 | ||

Grifols, SA, Class A, non-registered shares1 | 1,371,082 | 12,502 | ||

379,370 | ||||

Consumer discretionary 11.13% | ||||

MercadoLibre, Inc.1 | 39,944 | 79,296 | ||

adidas AG | 229,780 | 54,253 | ||

Flutter Entertainment PLC1 | 143,611 | 39,683 | ||

Ferrari NV | 75,044 | 32,697 | ||

LVMH Moët Hennessy-Louis Vuitton SE | 50,960 | 31,954 | ||

Meituan, Class B1 | 1,442,500 | 31,273 | ||

Maruti Suzuki India, Ltd. | 233,080 | 30,548 | ||

Evolution AB | 291,789 | 25,505 | ||

Compagnie Financière Richemont SA, Class A | 115,794 | 16,134 | ||

Entain PLC | 1,047,065 | 10,751 | ||

352,094 | ||||

Financials 10.55% | ||||

Nu Holdings, Ltd., Class A1 | 6,982,006 | 87,485 | ||

Banco Bilbao Vizcaya Argentaria, SA | 5,668,892 | 53,611 | ||

NatWest Group PLC | 8,105,386 | 41,603 | ||

Aegon, Ltd. | 6,048,092 | 39,057 | ||

ING Groep NV | 2,097,816 | 32,543 | ||

Kotak Mahindra Bank, Ltd. | 1,380,816 | 28,847 | ||

Standard Chartered PLC | 2,042,760 | 25,318 | ||

AIA Group, Ltd. | 3,381,000 | 25,266 | ||

333,730 | ||||

Capital Group Equity Exchange-Traded Funds | 29 |

Common stocks (continued) | Shares | Value (000) | ||

Materials 10.32% | ||||

Glencore PLC1 | 18,393,147 | $89,075 | ||

First Quantum Minerals, Ltd.1 | 6,459,388 | 88,253 | ||

Ivanhoe Mines, Ltd., Class A1 | 4,341,841 | 58,454 | ||

Shin-Etsu Chemical Co., Ltd. | 985,100 | 36,563 | ||

Anglo American PLC | 923,840 | 29,680 | ||

Rio Tinto PLC | 391,561 | 24,637 | ||

326,662 | ||||

Communication services 6.67% | ||||

Bharti Airtel, Ltd. | 3,862,524 | 74,381 | ||

Tencent Holdings, Ltd. | 1,061,300 | 54,283 | ||

Sea, Ltd., Class A (ADR)1 | 301,060 | 34,261 | ||

Universal Music Group NV | 1,373,883 | 33,165 | ||

Kuaishou Technology, Class B1 | 2,395,200 | 14,836 | ||

210,926 | ||||

Energy 5.25% | ||||

Reliance Industries, Ltd. | 6,276,704 | 95,989 | ||

Canadian Natural Resources, Ltd. (CAD denominated) | 1,170,347 | 39,721 | ||

Cenovus Energy, Inc. | 1,920,942 | 30,430 | ||

166,140 | ||||

Consumer staples 4.57% | ||||

JBS SA | 6,437,672 | 40,226 | ||

Danone SA | 582,128 | 39,835 | ||

Ajinomoto Co., Inc. | 691,000 | 29,009 | ||

Kweichow Moutai Co., Ltd., Class A | 91,000 | 19,195 | ||

Treasury Wine Estates, Ltd. | 2,217,344 | 16,390 | ||

144,655 | ||||

Real estate 0.53% | ||||

ESR Group, Ltd. | 11,434,400 | 16,811 | ||

Total common stocks (cost: $2,648,136,000) | 3,048,892 | |||

Short-term securities 3.37% | ||||

Money market investments 3.37% | ||||

Capital Group Central Cash Fund 4.65%2,3 | 1,065,347 | 106,545 | ||

Total short-term securities (cost: $106,534,000) | 106,545 | |||

Total investment securities 99.72% (cost: $2,754,670,000) | 3,155,437 | |||

Other assets less liabilities 0.28% | 8,866 | |||

Net assets 100.00% | $3,164,303 | |||

Value at 6/1/2024 (000) | Additions (000) | Reductions (000) | Net realized gain (loss) (000) | Net unrealized appreciation (depreciation) (000) | Value at 11/30/2024 (000) | Dividend or interest income (000) | |

Short-term securities 3.37% | |||||||

Money market investments 3.37% | |||||||

Capital Group Central Cash Fund 4.65% 2 | $38,033 | $394,829 | $326,314 | $(6 ) | $3 | $106,545 | $2,165 |

30 | Capital Group Equity Exchange-Traded Funds |

1 | Security did not produce income during the last 12 months. |

2 | Rate represents the seven-day yield at 11/30/2024. |

3 | Part of the same "group of investment companies" as the fund as defined under the Investment Company Act of 1940, as amended. |

Key to abbreviation(s) |

ADR = American Depositary Receipts |

CAD = Canadian dollars |

Capital Group Equity Exchange-Traded Funds | 31 |

Common stocks 94.67% | Shares | Value (000) | ||

Financials 18.34% | ||||

Nu Holdings, Ltd., Class A1 | 89,676 | $1,124 | ||

Banco Bilbao Vizcaya Argentaria, SA | 117,023 | 1,107 | ||

Mastercard, Inc., Class A | 2,047 | 1,091 | ||

AIA Group, Ltd. | 143,000 | 1,069 | ||

PB Fintech, Ltd.1 | 41,464 | 929 | ||

Capitec Bank Holdings, Ltd. | 4,899 | 886 | ||

Bank Mandiri (Persero) Tbk PT | 2,132,500 | 828 | ||

HDFC Bank, Ltd. | 36,211 | 770 | ||

Bank Central Asia Tbk PT | 1,072,500 | 677 | ||

Kotak Mahindra Bank, Ltd. | 28,064 | 586 | ||

Axis Bank, Ltd. | 37,659 | 506 | ||

Ping An Insurance (Group) Company of China, Ltd., Class H | 76,000 | 438 | ||

Visa, Inc., Class A | 1,325 | 418 | ||

Shriram Finance, Ltd. | 11,342 | 405 | ||

Eurobank Ergasias Services and Holdings SA | 180,923 | 383 | ||

XP, Inc., Class A | 28,097 | 380 | ||

S&P Global, Inc. | 646 | 338 | ||

Bank of the Philippine Islands | 146,810 | 322 | ||

Discovery, Ltd. | 30,081 | 321 | ||

Cholamandalam Investment and Finance Co., Ltd. | 21,589 | 315 | ||

ICICI Bank, Ltd. (ADR) | 8,549 | 261 | ||

UniCredit SpA | 6,761 | 260 | ||

Bajaj Finserv, Ltd. | 13,702 | 256 | ||

B3 SA - Brasil, Bolsa, Balcao | 163,039 | 253 | ||

Grupo Financiero Banorte, SAB de CV, Series O | 35,057 | 233 | ||

Canara Bank | 192,289 | 232 | ||

Bajaj Finance, Ltd. | 2,961 | 230 | ||

Hong Kong Exchanges and Clearing, Ltd. | 5,400 | 201 | ||

National Bank of Greece SA | 27,713 | 196 | ||

HSBC Holdings PLC | 20,902 | 195 | ||

DBS Group Holdings, Ltd. | 5,700 | 181 | ||

Aon PLC, Class A | 457 | 179 | ||

PICC Property and Casualty Co., Ltd., Class H | 116,000 | 176 | ||

China Merchants Bank Co., Ltd., Class H | 36,500 | 165 | ||

BSE, Ltd. | 2,791 | 154 | ||

BDO Unibank, Inc. | 58,530 | 154 | ||

Moody’s Corp. | 272 | 136 | ||

Commercial International Bank - Egypt (CIB) SAE (GDR) | 82,694 | 126 | ||

Banco BTG Pactual SA, units | 24,055 | 122 | ||

16,603 | ||||

Information technology 16.03% | ||||

Taiwan Semiconductor Manufacturing Co., Ltd. (ADR) | 20,118 | 3,715 | ||

Microsoft Corp. | 5,980 | 2,532 | ||

NVIDIA Corp. | 11,550 | 1,597 | ||

Broadcom, Inc. | 8,507 | 1,379 | ||

Keyence Corp. | 1,600 | 692 | ||

SAP SE | 2,709 | 645 | ||

Synopsys, Inc.1 | 979 | 547 | ||

SK hynix, Inc. | 4,285 | 491 | ||

Samsung Electronics Co., Ltd. | 9,988 | 388 | ||

Apple, Inc. | 1,584 | 376 | ||

Capgemini SE | 2,165 | 348 | ||

E Ink Holdings, Inc. | 38,000 | 329 | ||

ASM International NV | 543 | 294 | ||

Tokyo Electron, Ltd. | 1,400 | 218 | ||

eMemory Technology, Inc. | 2,000 | 180 | ||

Applied Materials, Inc. | 884 | 154 | ||

Coforge, Ltd. | 1,417 | 146 | ||

Globant SA1 | 575 | 131 | ||

32 | Capital Group Equity Exchange-Traded Funds |

Common stocks (continued) | Shares | Value (000) | ||

Information technology (continued) | ||||

Atlassian Corp., Class A1 | 449 | $118 | ||

MediaTek, Inc. | 3,000 | 116 | ||

ASML Holding NV | 157 | 109 | ||

14,505 | ||||

Consumer discretionary 12.71% | ||||

MercadoLibre, Inc.1 | 1,032 | 2,049 | ||

Trip.com Group, Ltd. (ADR)1 | 17,388 | 1,124 | ||

LVMH Moët Hennessy-Louis Vuitton SE | 1,736 | 1,089 | ||

Meituan, Class B1 | 41,800 | 906 | ||

Midea Group Co., Ltd., Class A | 60,900 | 590 | ||

Eicher Motors, Ltd. | 9,732 | 556 | ||

Galaxy Entertainment Group, Ltd. | 102,000 | 453 | ||

H World Group, Ltd. (ADR) | 13,072 | 421 | ||

BYD Co., Ltd., Class H | 7,500 | 244 | ||

BYD Co., Ltd., Class A | 3,200 | 122 | ||

adidas AG | 1,509 | 356 | ||

TVS Motor Co., Ltd. | 10,787 | 311 | ||

Compagnie Financière Richemont SA, Class A | 2,058 | 287 | ||

Jumbo SA | 10,734 | 280 | ||

Titan Co., Ltd. | 6,950 | 267 | ||

Hyundai Motor India, Ltd.1 | 9,607 | 218 | ||

Shenzhou International Group Holdings, Ltd. | 28,200 | 216 | ||

Hilton Worldwide Holdings, Inc. | 811 | 206 | ||

Sands China, Ltd.1 | 80,400 | 205 | ||

Ferrari NV | 470 | 205 | ||

Naspers, Ltd., Class N | 874 | 197 | ||

lululemon athletica, Inc.1 | 532 | 171 | ||

Zomato, Ltd.1 | 49,458 | 164 | ||

Maruti Suzuki India, Ltd. | 1,223 | 160 | ||

YUM! Brands, Inc. | 1,144 | 159 | ||

Amadeus IT Group SA, Class A, non-registered shares | 2,105 | 148 | ||

Industria de Diseño Textil, SA | 2,064 | 114 | ||

Alibaba Group Holding, Ltd. (ADR) | 1,155 | 101 | ||

Suzuki Motor Corp. | 9,100 | 96 | ||

Li Ning Co., Ltd. | 44,000 | 90 | ||

11,505 | ||||

Industrials 10.79% | ||||

Airbus SE, non-registered shares | 9,043 | 1,412 | ||

Safran SA | 4,154 | 969 | ||

Shenzhen Inovance Technology Co., Ltd., Class A | 68,700 | 573 | ||

Techtronic Industries Co., Ltd. | 39,000 | 549 | ||

Carrier Global Corp. | 6,023 | 466 | ||

Rumo SA | 142,922 | 465 | ||

Airports of Thailand PCL, foreign registered shares | 260,400 | 461 | ||

Copa Holdings, SA, Class A | 4,921 | 459 | ||

Rolls-Royce Holdings PLC1 | 61,620 | 439 | ||

International Container Terminal Services, Inc. | 52,830 | 333 | ||

General Electric Co. | 1,636 | 298 | ||

Contemporary Amperex Technology Co., Ltd., Class A | 8,100 | 293 | ||

Larsen & Toubro, Ltd. | 6,377 | 281 | ||

Caterpillar, Inc. | 682 | 277 | ||

Grupo Aeroportuario del Pacífico, SAB de CV, Class B | 14,707 | 271 | ||

Schneider Electric SE | 988 | 255 | ||

BAE Systems PLC | 15,342 | 240 | ||

Mitsui & Co., Ltd. | 10,200 | 214 | ||

Siemens AG | 1,075 | 208 | ||

Daikin Industries, Ltd. | 1,600 | 194 | ||

CCR SA, ordinary nominative shares | 87,579 | 162 | ||

ZTO Express (Cayman), Inc., Class A (ADR) | 8,025 | 153 | ||

IMCD NV | 1,004 | 151 | ||

Jiangsu Hengli Hydraulic Co., Ltd., Class A | 19,100 | 140 | ||

GE Vernova, Inc.1 | 394 | 132 | ||

Capital Group Equity Exchange-Traded Funds | 33 |

Common stocks (continued) | Shares | Value (000) | ||

Industrials (continued) | ||||

Wizz Air Holdings PLC1 | 7,910 | $130 | ||

InPost SA1 | 6,890 | 121 | ||

DSV A/S | 549 | 117 | ||

9,763 | ||||

Communication services 9.55% | ||||

Tencent Holdings, Ltd. | 45,800 | 2,343 | ||

Meta Platforms, Inc., Class A | 2,744 | 1,576 | ||

Alphabet, Inc., Class A | 6,460 | 1,092 | ||

Alphabet, Inc., Class C | 2,354 | 401 | ||

Bharti Airtel, Ltd. | 54,943 | 1,058 | ||

NetEase, Inc. | 20,000 | 346 | ||

NetEase, Inc. (ADR) | 2,817 | 246 | ||

América Móvil, SAB de CV, Class B (ADR) | 21,089 | 313 | ||

MTN Group, Ltd. | 61,865 | 277 | ||

Telefónica, SA, non-registered shares | 48,058 | 218 | ||

Netflix, Inc.1 | 235 | 208 | ||

Telkom Indonesia (Persero) Tbk PT, Class B | 883,700 | 151 | ||

Singapore Telecommunications, Ltd. | 60,800 | 141 | ||

Indus Towers, Ltd.1 | 33,590 | 139 | ||

Vodafone Group PLC | 149,821 | 135 | ||

8,644 | ||||

Health care 9.51% | ||||

Novo Nordisk AS, Class B | 15,896 | 1,708 | ||

Max Healthcare Institute, Ltd. | 98,210 | 1,139 | ||

Eli Lilly and Co. | 1,193 | 949 | ||

Thermo Fisher Scientific, Inc. | 1,591 | 843 | ||

AstraZeneca PLC | 4,371 | 591 | ||

Abbott Laboratories | 3,664 | 435 | ||

Laurus Labs, Ltd. | 64,333 | 432 | ||

BeiGene, Ltd. (ADR)1 | 1,870 | 402 | ||

Danaher Corp. | 1,413 | 339 | ||

Jiangsu Hengrui Medicine Co., Ltd., Class A | 45,000 | 315 | ||

Innovent Biologics, Inc.1 | 53,500 | 265 | ||

Zai Lab, Ltd. (ADR)1 | 7,043 | 203 | ||

Revvity, Inc. | 1,514 | 176 | ||

Mankind Pharma, Ltd.1 | 5,586 | 169 | ||

Aspen Pharmacare Holdings, Ltd. | 17,354 | 159 | ||

WuXi AppTec Co., Ltd., Class H | 25,500 | 154 | ||

EssilorLuxottica SA | 518 | 126 | ||

Rede D’Or Sao Luiz SA | 24,066 | 109 | ||

Hypera SA, ordinary nominative shares | 27,471 | 90 | ||

8,604 | ||||

Consumer staples 6.72% | ||||

Kweichow Moutai Co., Ltd., Class A | 5,200 | 1,097 | ||

ITC, Ltd. | 127,557 | 720 | ||

Ajinomoto Co., Inc. | 15,300 | 642 | ||

Varun Beverages, Ltd. | 67,595 | 497 | ||

Monster Beverage Corp.1 | 7,236 | 399 | ||

Arca Continental, SAB de CV | 42,134 | 356 | ||