UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16 UNDER

THE SECURITIES EXCHANGE ACT OF 1934

For the month of November 2023

Commission File Number 001-41815

AngloGold Ashanti plc

(Translation of registrant’s name into English)

4th Floor, Communications House

South Street

Staines-Upon-Thames, Surrey TW18 4PR

United Kingdom

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

Form 20-F ☒ Form 40-F ☐

Enclosure: AngloGold Ashanti Investor Presentation (November 2023)

INVESTOR PRESENTATION NOVEMBER 2023 Silicon, USA

DISCLAIMER Certain statements contained in this document, other than statements of historical fact, including, without limitation, those concerning the economic outlook for the gold mining industry, expectations regarding gold prices, production, total cash costs, all-in sustaining costs, all-in costs, cost savings and other operating results, return on equity, productivity improvements, growth prospects and outlook of AngloGold Ashanti plc’s (the “Company”, “AngloGold Ashanti” or “AGA”) operations, individually or in the aggregate, including the achievement of project milestones, commencement and completion of commercial operations of certain of AngloGold Ashanti’s exploration and production projects and the completion of acquisitions, dispositions or joint venture transactions, AngloGold Ashanti’s liquidity and capital resources and capital expenditures, the consequences of the COVID-19 pandemic and the outcome and consequences of any potential or pending litigation or regulatory proceedings or environmental, health and safety issues, are forward-looking statements regarding AngloGold Ashanti’s financial reports, operations, economic performance and financial condition. These forward-looking statements or forecasts are not based on historical facts, but rather reflect our current beliefs and expectations concerning future events and generally may be identified by the use of forward-looking words, phrases and expressions such as “believe”, “expect”, “aim”, “anticipate”, “intend”, “foresee”, “forecast”, “predict”, “project”, “estimate”, “likely”, “may”, “might”, “could”, “should”, “would”, “seek”, “plan”, “scheduled”, “possible”, “continue”, “potential”, “outlook”, “target” or other similar words, phrases, and expressions; provided that the absence thereof does not mean that a statement is not forward-looking. Similarly, statements that describe our objectives, plans or goals are or may be forward-looking statements. These forward- looking statements or forecasts involve known and unknown risks, uncertainties and other factors that may cause AngloGold Ashanti’s actual results, performance, actions or achievements to differ materially from the anticipated results, performance, actions or achievements expressed or implied in these forward-looking statements. Although AngloGold Ashanti believes that the expectations reflected in such forward-looking statements and forecasts are reasonable, no assurance can be given that such expectations will prove to have been correct. Accordingly, results, performance, actions or achievements could differ materially from those set out in the forward-looking statements as a result of, among other factors, changes in economic, social, political and market conditions, including related to inflation or international conflicts, the success of business and operating initiatives, changes in the regulatory environment and other government actions, including environmental approvals, fluctuations in gold prices and exchange rates, the outcome of pending or future litigation proceedings, any supply chain disruptions, any public health crises, pandemics or epidemics (including the COVID-19 pandemic), and other business and operational risks and challenges and other factors, including mining accidents. For a discussion of such risk factors, refer to AngloGold Ashanti Limited’s annual report on Form 20-F for the year ended 31 December 2022 filed with the United States Securities and Exchange Commission (“SEC”) and AngloGold Ashanti’s registration statement on Form F-4 initially filed with the SEC on 23 June 2023. These factors are not necessarily all of the important factors that could cause AngloGold Ashanti’s actual results, performance, actions or achievements to differ materially from those expressed in any forward-looking statements. Other unknown or unpredictable factors could also have material adverse effects on AngloGold Ashanti’s future results, performance, actions or achievements. Consequently, readers are cautioned not to place undue reliance on forward-looking statements. AngloGold Ashanti undertakes no obligation to update publicly or release any revisions to these forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events, except to the extent required by applicable law. All subsequent written or oral forward-looking statements attributable to AngloGold Ashanti or any person acting on its behalf are qualified by the cautionary statements herein. The information included in this presentation has not been reviewed or reported on by AngloGold Ashanti’s external auditors. Non-GAAP financial measures This communication may contain certain “Non-GAAP” financial measures. AngloGold Ashanti utilises certain Non-GAAP performance measures and ratios in managing its business. Non-GAAP financial measures should be viewed in addition to, and not as an alternative for, the reported operating results or cash flow from operations or any other measures of performance prepared in accordance with IFRS. In addition, the presentation of these measures may not be comparable to similarly titled measures other companies may use. Website: www.anglogoldashanti.com 2

LICENCE TO OPERATE

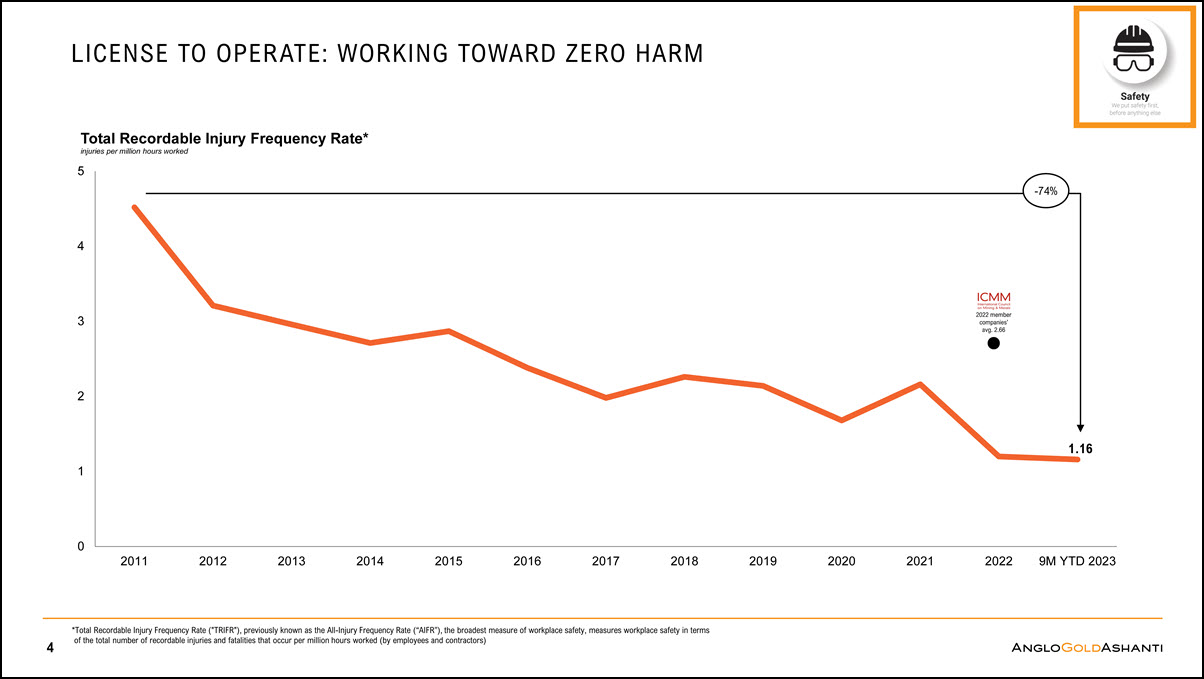

0 1 2 3 4 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 9M YTD 2023 Total Recordable Injury Frequency Rate* injuries per million hours worked 5 LICENSE TO OPERATE: WORKING TOWARD ZERO HARM *Total Recordable Injury Frequency Rate ("TRIFR"), previously known as the All-Injury Frequency Rate (“AIFR”), the broadest measure of workplace safety, measures workplace safety in terms of the total number of recordable injuries and fatalities that occur per million hours worked (by employees and contractors) 2022 member companies’ avg. 2.66 1.16 -74% 4

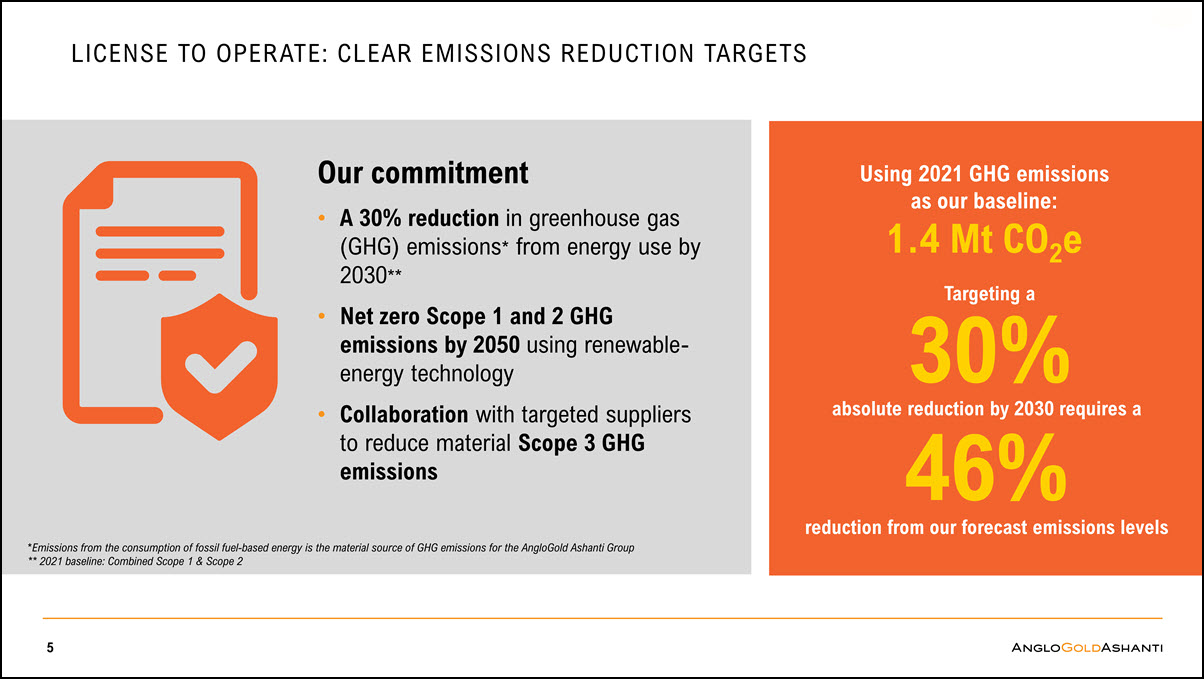

5 LICENSE TO OPERATE: CLEAR EMISSIONS REDUCTION TARGETS Our commitment A 30% reduction in greenhouse gas (GHG) emissions* from energy use by 2030** Net zero Scope 1 and 2 GHG emissions by 2050 using renewable- energy technology Collaboration with targeted suppliers to reduce material Scope 3 GHG emissions Using 2021 GHG emissions as our baseline: 2 1.4 Mt CO e Targeting a 30% absolute reduction by 2030 requires a 46% reduction from our forecast emissions levels *Emissions from the consumption of fossil fuel-based energy is the material source of GHG emissions for the AngloGold Ashanti Group ** 2021 baseline: Combined Scope 1 & Scope 2

CLOSING THE VALUE GAP

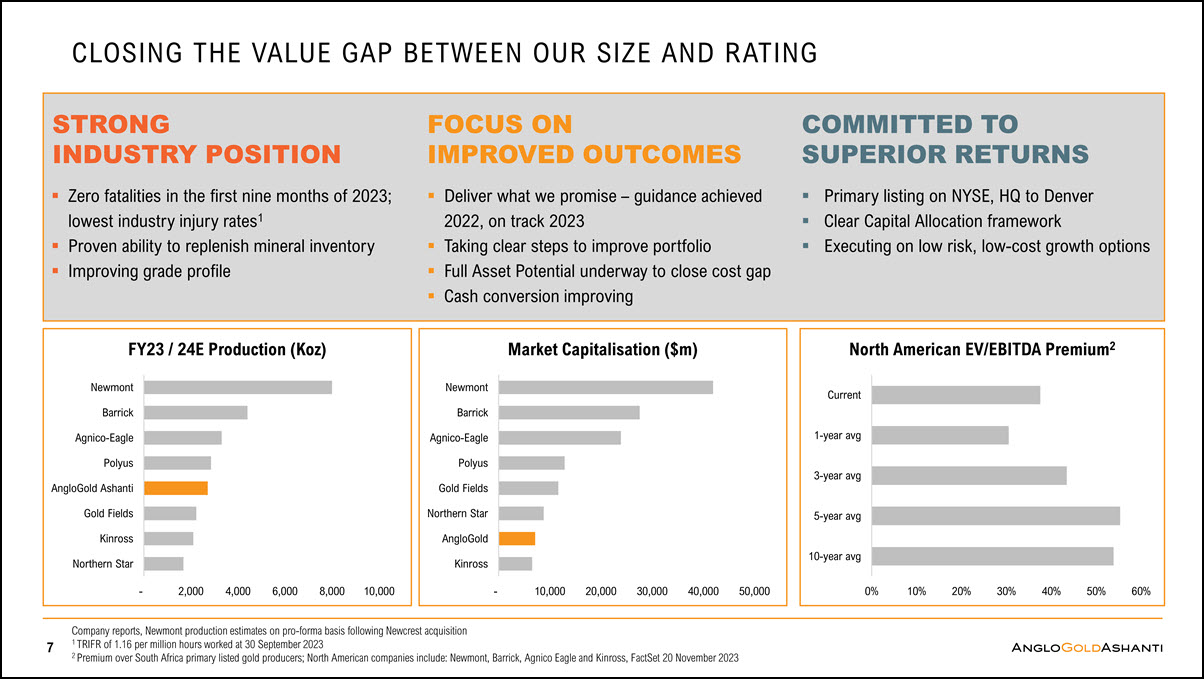

CLOSING THE VALUE GAP BETWEEN OUR SIZE AND RATING 7 - 2,000 4,000 6,000 8,000 10,000 FY23 / 24E Production (Koz) Newmont Barrick Agnico-Eagle Polyus AngloGold Ashanti Gold Fields Kinross Northern Star - 10,000 20,000 30,000 40,000 50,000 Newmont Barrick Agnico-Eagle Polyus Gold Fields Northern Star AngloGold Kinross Market Capitalisation ($m) COMMITTED TO SUPERIOR RETURNS STRONG INDUSTRY POSITION Zero fatalities in the first nine months of 2023; lowest industry injury rates1 Proven ability to replenish mineral inventory Improving grade profile FOCUS ON IMPROVED OUTCOMES Deliver what we promise – guidance achieved 2022, on track 2023 Taking clear steps to improve portfolio Full Asset Potential underway to close cost gap Cash conversion improving Primary listing on NYSE, HQ to Denver Clear Capital Allocation framework Executing on low risk, low-cost growth options Company reports, Newmont production estimates on pro-forma basis following Newcrest acquisition 1 TRIFR of 1.16 per million hours worked at 30 September 2023 2 Premium over South Africa primary listed gold producers; North American companies include: Newmont, Barrick, Agnico Eagle and Kinross, FactSet 20 November 2023 0% 10% 20% 30% 40% 50% 60% Current 1-year avg 3-year avg 5-year avg 10-year avg North American EV/EBITDA Premium2

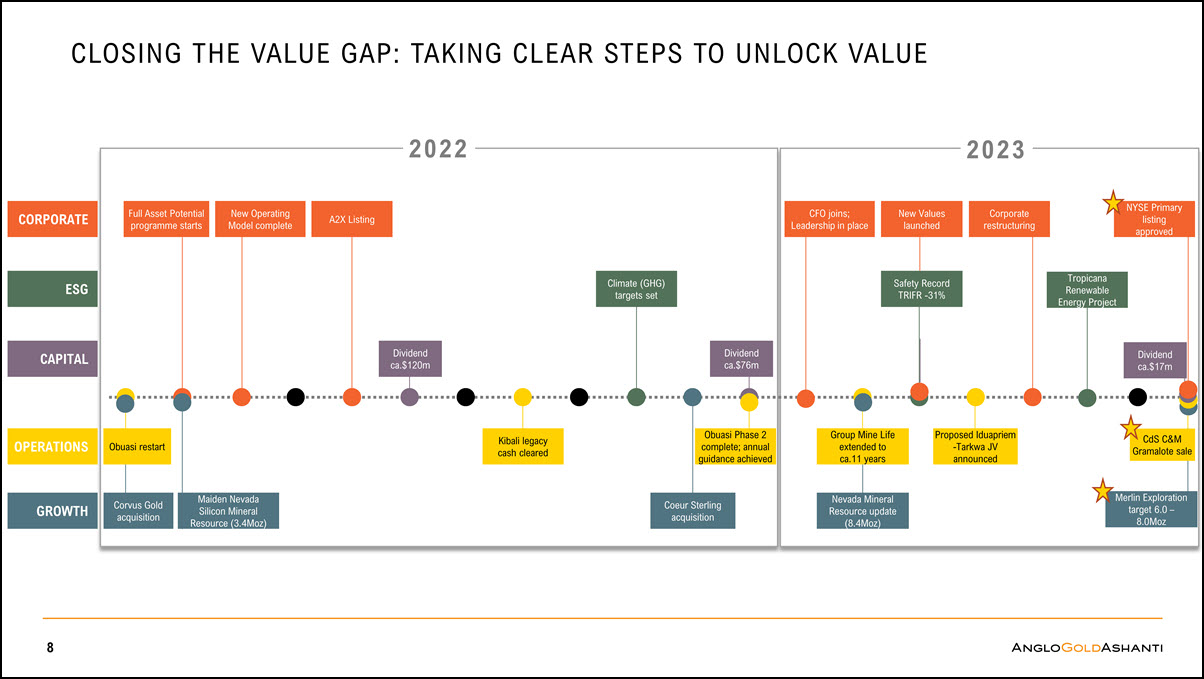

CLOSING THE VALUE GAP: TAKING CLEAR STEPS TO UNLOCK VALUE Kibali legacy cash cleared Climate (GHG) targets set Corvus Gold acquisition Maiden Nevada Silicon Mineral Resource (3.4Moz) Proposed Iduapriem -Tarkwa JV announced Coeur Sterling acquisition Dividend ca.$120m Dividend ca.$76m 8 CORPORATE ESG OPERATIONS CAPITAL GROWTH Obuasi Phase 2 complete; annual guidance achieved Safety Record TRIFR -31% Obuasi restart 2023 2022 New Operating Model complete CFO joins; Leadership in place Corporate restructuring A2X Listing Full Asset Potential programme starts New Values launched Nevada Mineral Resource update (8.4Moz) Group Mine Life extended to ca.11 years NYSE Primary listing approved CdS C&M Gramalote sale Merlin Exploration target 6.0 – 8.0Moz Tropicana Renewable Energy Project Dividend ca.$17m

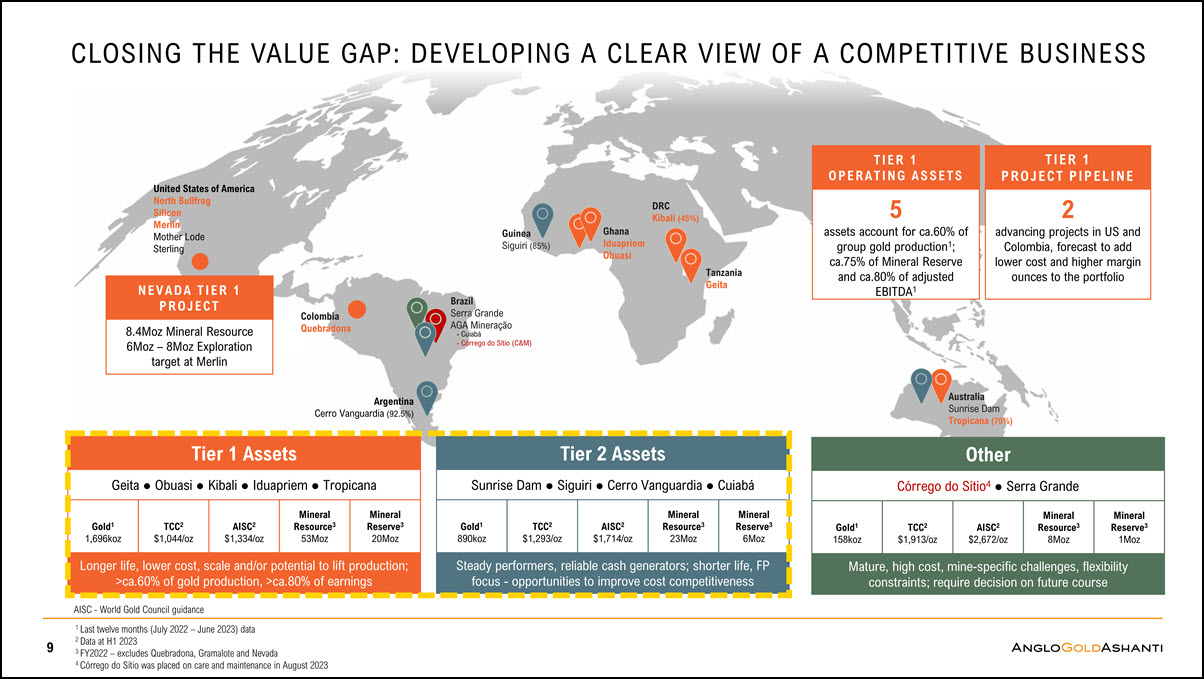

Argentina Cerro Vanguardia (92.5%) Guinea Siguiri (85%) Ghana Iduapriem Obuasi DRC Kibali (45%) Tanzania Geita 1 Last twelve months (July 2022 – June 2023) data 2 Data at H1 2023 3 FY2022 – excludes Quebradona, Gramalote and Nevada 4 Córrego do Sítio was placed on care and maintenance in August 2023 CLOSING THE VALUE GAP: DEVELOPING A CLEAR VIEW OF A COMPETITIVE BUSINESS 9 Australia Sunrise Dam Tropicana (70%) Colombia Quebradona Other Córrego do Sítio4 ● Serra Grande Gold1 158koz TCC2 $1,913/oz AISC2 $2,672/oz Mineral Resource3 8Moz Mineral Reserve3 1Moz Mature, high cost, mine-specific challenges, flexibility constraints; require decision on future course TIER 1 OPER AT ING AS S ETS 5 assets account for ca.60% of group gold production1; ca.75% of Mineral Reserve and ca.80% of adjusted EBITDA1 TIER 1 PROJECT PIPELINE 2 advancing projects in US and Colombia, forecast to add lower cost and higher margin ounces to the portfolio Brazil Serra Grande AGA Mineração Cuiabá Córrego do Sítio (C&M) United States of America North Bullfrog Silicon Merlin Mother Lode Sterling Tier 1 Assets Tier 2 Assets Geita ● Obuasi ● Kibali ● Iduapriem ● Tropicana Sunrise Dam ● Siguiri ● Cerro Vanguardia ● Cuiabá Gold1 1,696koz TCC2 $1,044/oz AISC2 $1,334/oz Mineral Resource3 53Moz Mineral Reserve3 20Moz Gold1 890koz TCC2 $1,293/oz AISC2 $1,714/oz Mineral Resource3 23Moz Mineral Reserve3 6Moz Longer life, lower cost, scale and/or potential to lift production; >ca.60% of gold production, >ca.80% of earnings Steady performers, reliable cash generators; shorter life, FP focus - opportunities to improve cost competitiveness AISC - World Gold Council guidance NEV ADA T IER 1 PROJECT 8.4Moz Mineral Resource 6Moz – 8Moz Exploration target at Merlin

GROWTH

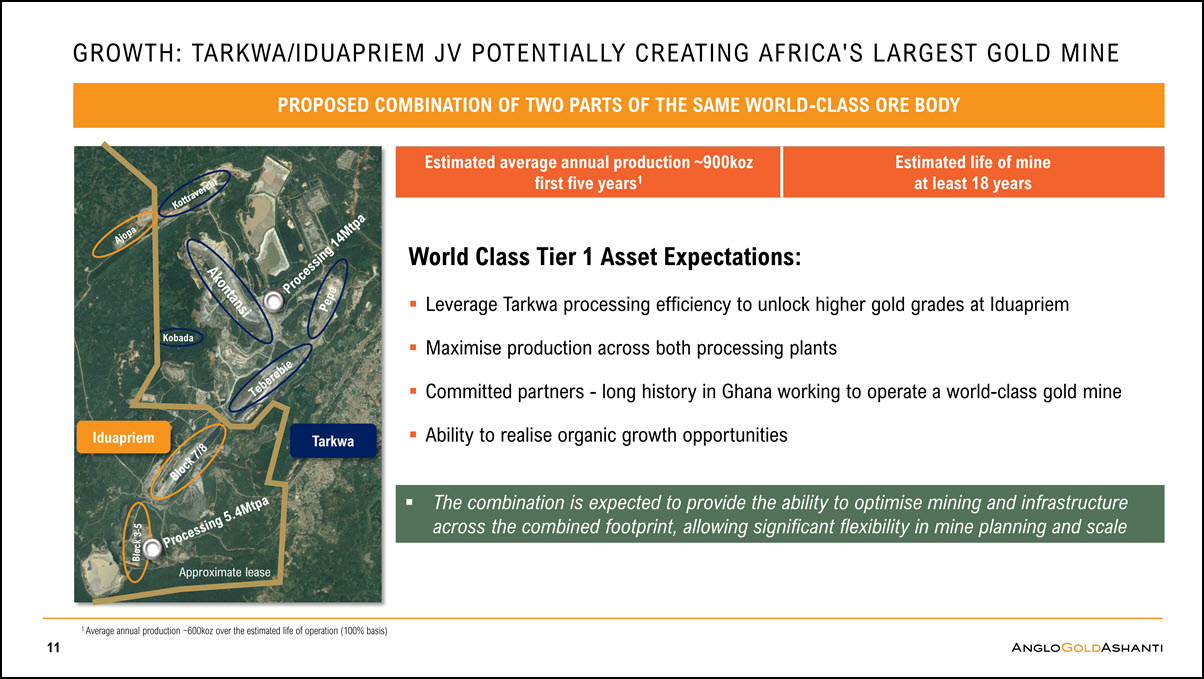

GROWTH: TARKWA/IDUAPRIEM JV POTENTIALLY CREATING AFRICA'S LARGEST GOLD MINE Estimated average annual production ~900koz first five years1 Estimated life of mine at least 18 years PROPOSED COMBINATION OF TWO PARTS OF THE SAME WORLD-CLASS ORE BODY Tarkwa Kobada Iduapriem Approximate lease World Class Tier 1 Asset Expectations: Leverage Tarkwa processing efficiency to unlock higher gold grades at Iduapriem Maximise production across both processing plants Committed partners - long history in Ghana working to operate a world-class gold mine Ability to realise organic growth opportunities 1 Average annual production ~600koz over the estimated life of operation (100% basis) 11 The combination is expected to provide the ability to optimise mining and infrastructure across the combined footprint, allowing significant flexibility in mine planning and scale

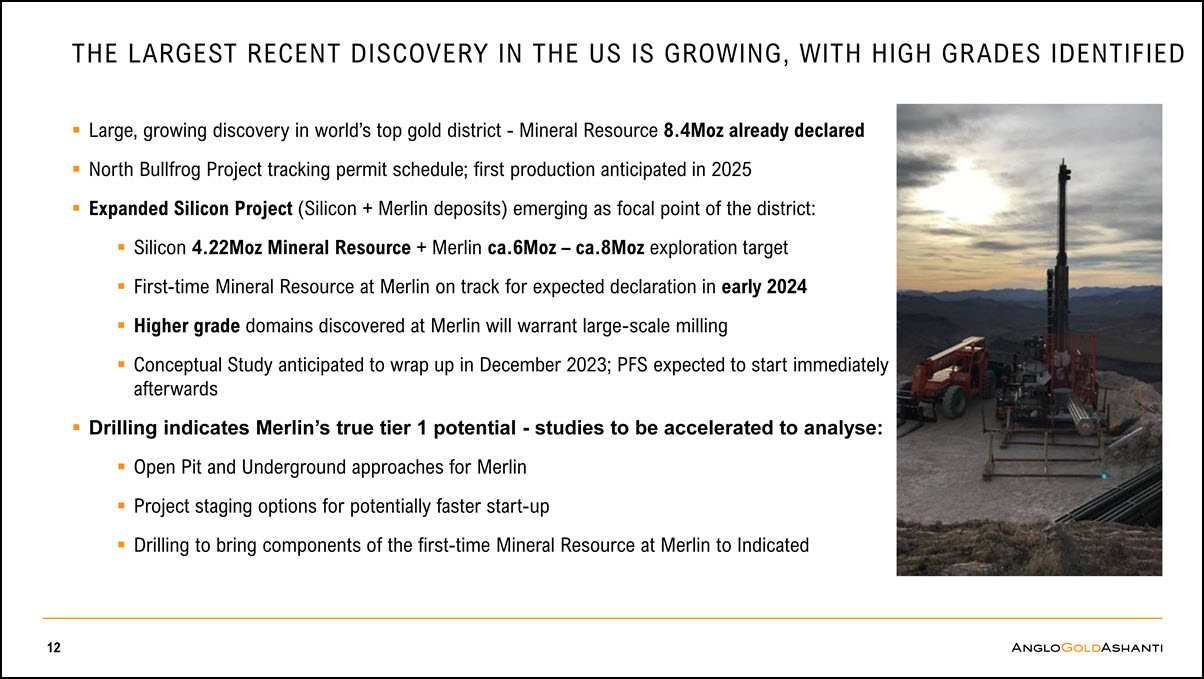

Large, growing discovery in world’s top gold district - Mineral Resource 8.4Moz already declared North Bullfrog Project tracking permit schedule; first production anticipated in 2025 Expanded Silicon Project (Silicon + Merlin deposits) emerging as focal point of the district: Silicon 4.22Moz Mineral Resource + Merlin ca.6Moz – ca.8Moz exploration target First-time Mineral Resource at Merlin on track for expected declaration in early 2024 Higher grade domains discovered at Merlin will warrant large-scale milling Conceptual Study anticipated to wrap up in December 2023; PFS expected to start immediately afterwards Drilling indicates Merlin’s true tier 1 potential - studies to be accelerated to analyse: Open Pit and Underground approaches for Merlin Project staging options for potentially faster start-up Drilling to bring components of the first-time Mineral Resource at Merlin to Indicated THE LARGEST RECENT DISCOVERY IN THE US IS GROWING, WITH HIGH GRADES IDENTIFIED 12

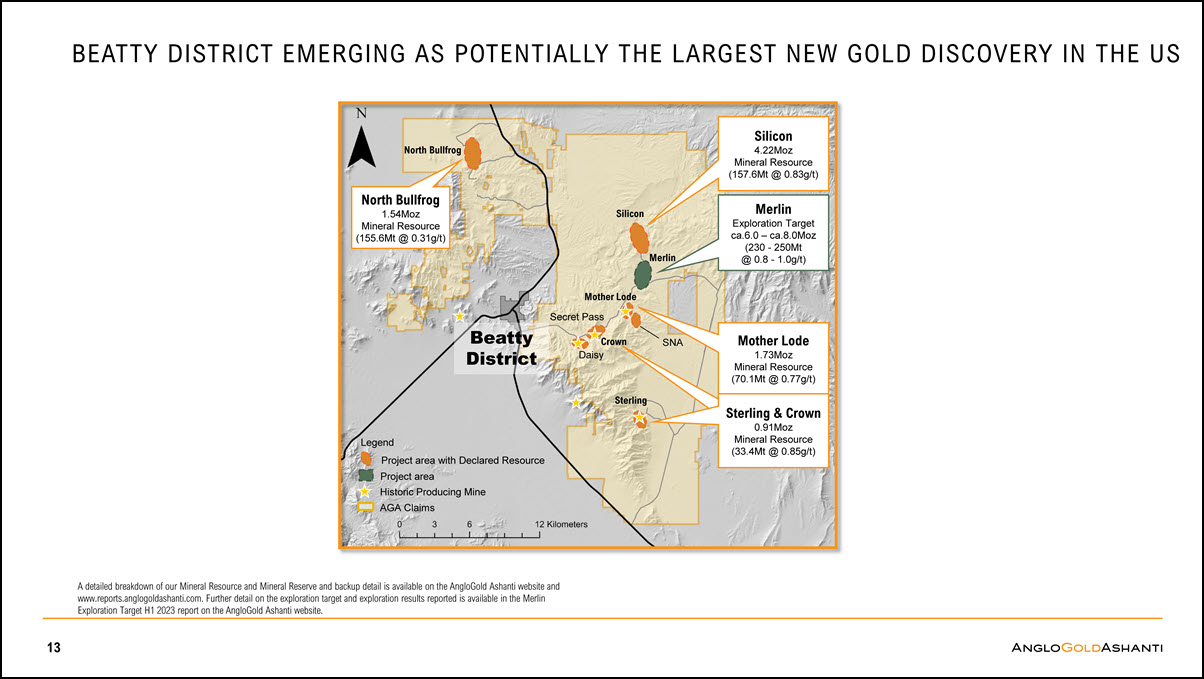

BEATTY DISTRICT EMERGING AS POTENTIALLY THE LARGEST NEW GOLD DISCOVERY IN THE US SNA Sterling Legend Project area with Declared Resource Project area Historic Producing Mine AGA Claims Silicon 4.22Moz Mineral Resource (157.6Mt @ 0.83g/t) Mother Lode 1.73Moz Mineral Resource (70.1Mt @ 0.77g/t) Sterling & Crown 0.91Moz Mineral Resource (33.4Mt @ 0.85g/t) Mother Lode Secret Pass Crown Daisy North Bullfrog 1.54Moz Mineral Resource (155.6Mt @ 0.31g/t) Merlin Silicon North Bullfrog Beatty District Merlin Exploration Target ca.6.0 – ca.8.0Moz (230 - 250Mt @ 0.8 - 1.0g/t) A detailed breakdown of our Mineral Resource and Mineral Reserve and backup detail is available on the AngloGold Ashanti website and www.reports.anglogoldashanti.com. Further detail on the exploration target and exploration results reported is available in the Merlin Exploration Target H1 2023 report on the AngloGold Ashanti website. 13

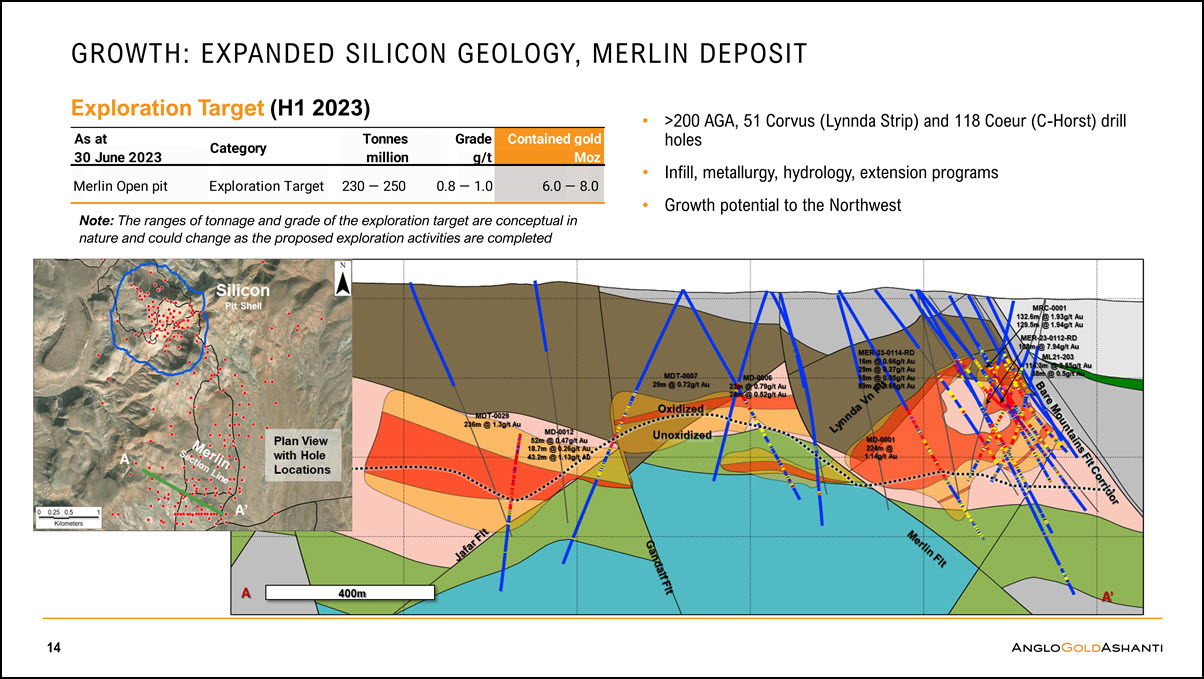

As at 30 June 2023 Category Tonnes million Grade g/t Contained gold Moz Merlin Open pit Exploration Target 230 — 250 0.8 — 1.0 6.0 — 8.0 GROWTH: EXPANDED SILICON GEOLOGY, MERLIN DEPOSIT >200 AGA, 51 Corvus (Lynnda Strip) and 118 Coeur (C-Horst) drill holes Infill, metallurgy, hydrology, extension programs Growth potential to the Northwest Exploration Target (H1 2023) Note: The ranges of tonnage and grade of the exploration target are conceptual in nature and could change as the proposed exploration activities are completed 14

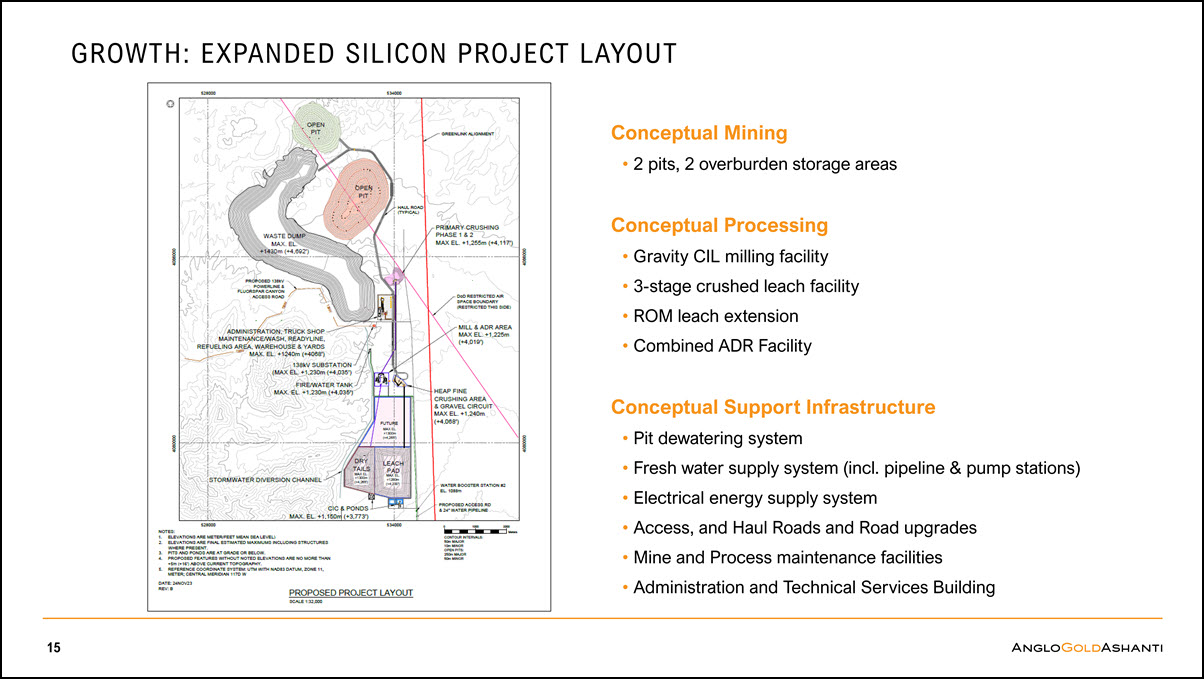

GROWTH: EXPANDED SILICON PROJECT LAYOUT Conceptual Mining 2 pits, 2 overburden storage areas Conceptual Processing Gravity CIL milling facility 3-stage crushed leach facility ROM leach extension Combined ADR Facility Conceptual Support Infrastructure Pit dewatering system Fresh water supply system (incl. pipeline & pump stations) Electrical energy supply system Access, and Haul Roads and Road upgrades Mine and Process maintenance facilities Administration and Technical Services Building 15

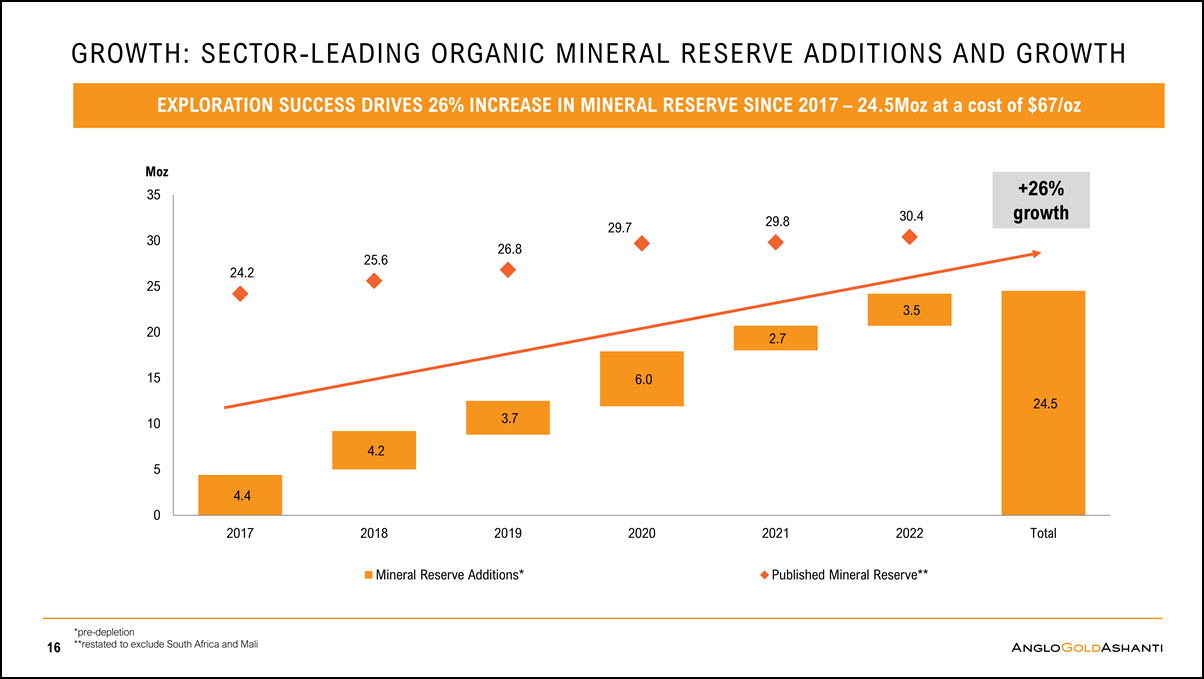

GROWTH: SECTOR-LEADING ORGANIC MINERAL RESERVE ADDITIONS AND GROWTH 16 4.4 4.2 3.7 6.0 2.7 3.5 24.5 25.6 26.8 29.7 29.8 30.4 0 5 10 15 20 24.2 25 30 2017 2020 Total 2018 2019 Mineral Reserve Additions* 2021 2022 Published Mineral Reserve** Moz 35 +26% growth *pre-depletion **restated to exclude South Africa and Mali EXPLORATION SUCCESS DRIVES 26% INCREASE IN MINERAL RESERVE SINCE 2017 – 24.5Moz at a cost of $67/oz

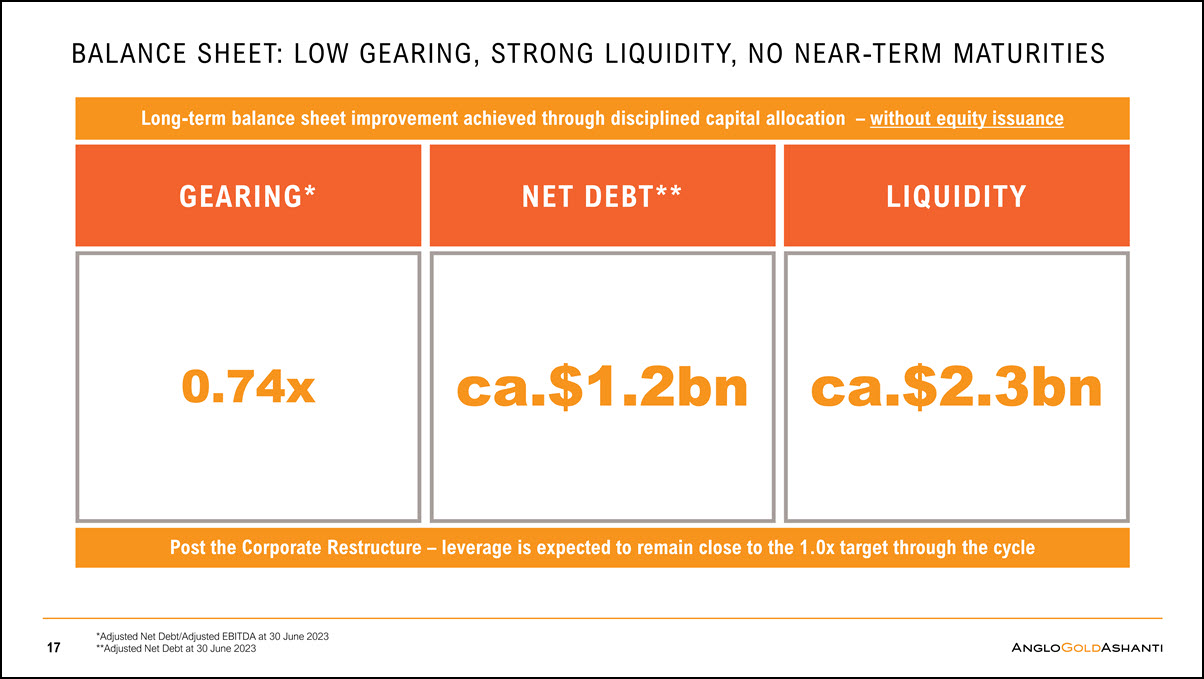

BALANCE SHEET: LOW GEARING, STRONG LIQUIDITY, NO NEAR-TERM MATURITIES 17 0.74x ca.$1.2bn GEARING* NET DEBT** LIQUIDITY ca.$2.3bn *Adjusted Net Debt/Adjusted EBITDA at 30 June 2023 **Adjusted Net Debt at 30 June 2023 Long-term balance sheet improvement achieved through disciplined capital allocation – without equity issuance Post the Corporate Restructure – leverage is expected to remain close to the 1.0x target through the cycle

OBUASI

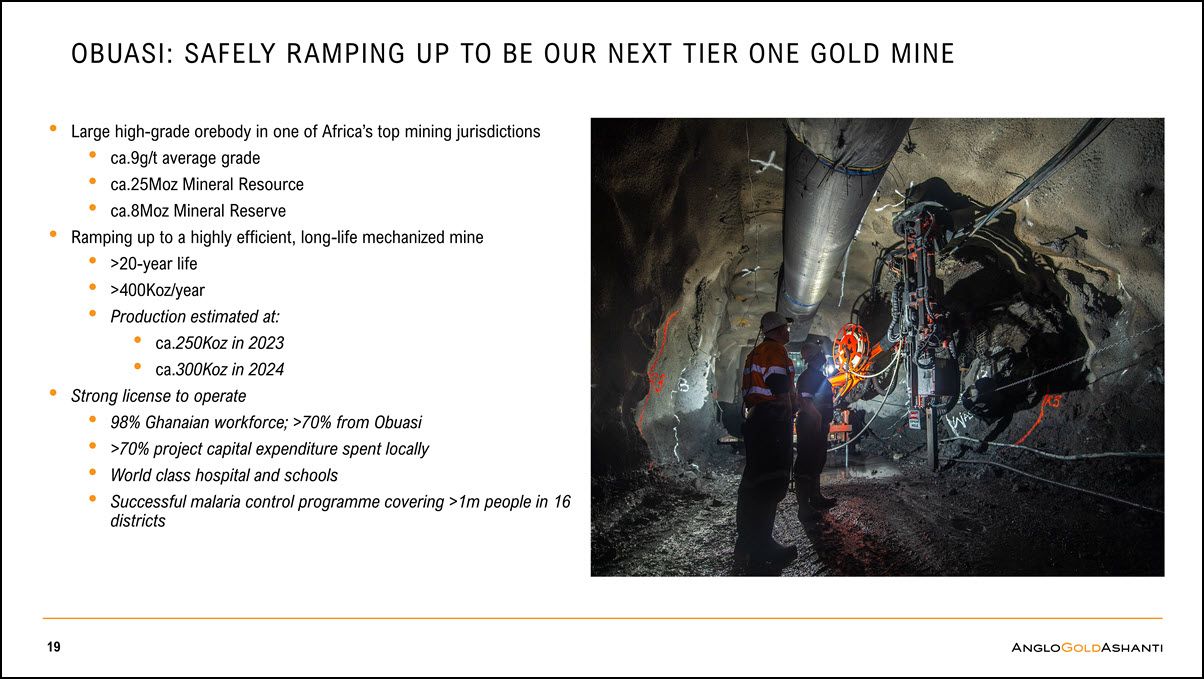

OBUASI: SAFELY RAMPING UP TO BE OUR NEXT TIER ONE GOLD MINE Large high-grade orebody in one of Africa’s top mining jurisdictions ca.9g/t average grade ca.25Moz Mineral Resource ca.8Moz Mineral Reserve Ramping up to a highly efficient, long-life mechanized mine >20-year life >400Koz/year Production estimated at: ca.250Koz in 2023 ca.300Koz in 2024 Strong license to operate 98% Ghanaian workforce; >70% from Obuasi >70% project capital expenditure spent locally World class hospital and schools Successful malaria control programme covering >1m people in 16 districts 19

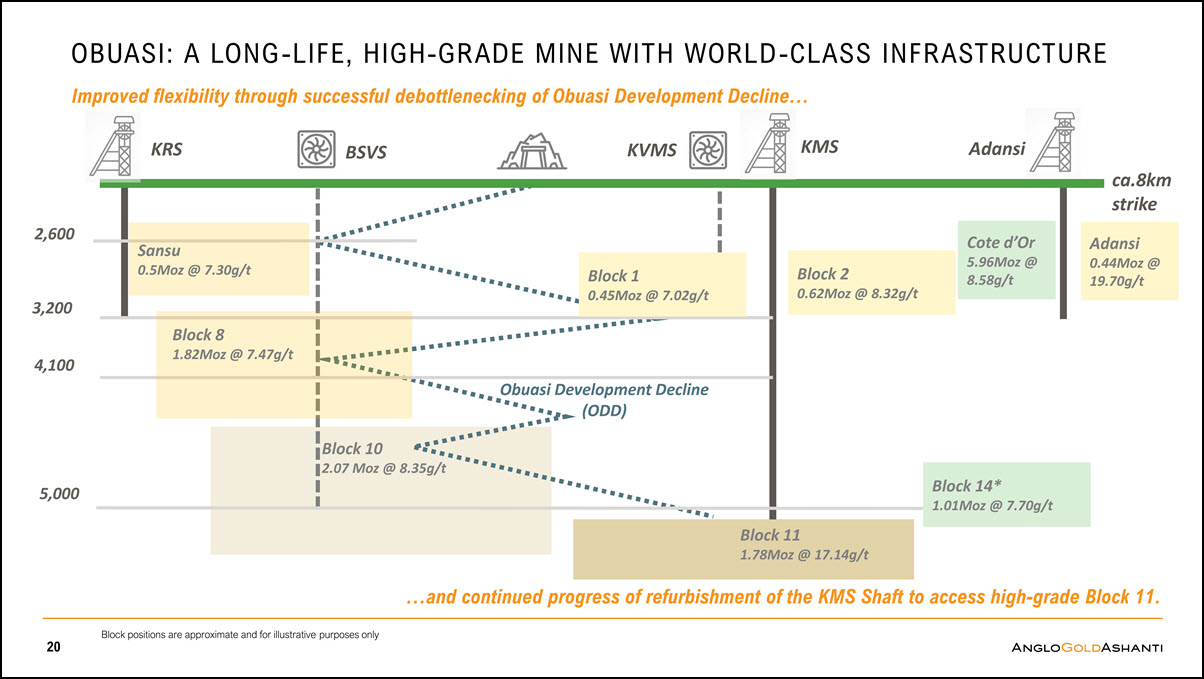

OBUASI: A LONG-LIFE, HIGH-GRADE MINE WITH WORLD-CLASS INFRASTRUCTURE 4,100 3,200 5,000 Obuasi Development Decline (ODD) Adansi BSVS KRS KVMS Block 11 1.78Moz @ 17.14g/t Block 10 2.07 Moz @ 8.35g/t KMS 2,600 Block 8 1.82Moz @ 7.47g/t Improved flexibility through successful debottlenecking of Obuasi Development Decline… …and continued progress of refurbishment of the KMS Shaft to access high-grade Block 11. Block 1 0.45Moz @ 7.02g/t ca.8km strike Block 2 0.62Moz @ 8.32g/t Adansi 0.44Moz @ 19.70g/t Sansu 0.5Moz @ 7.30g/t Block positions are approximate and for illustrative purposes only 20 Block 14* 1.01Moz @ 7.70g/t Cote d’Or 5.96Moz @ 8.58g/t

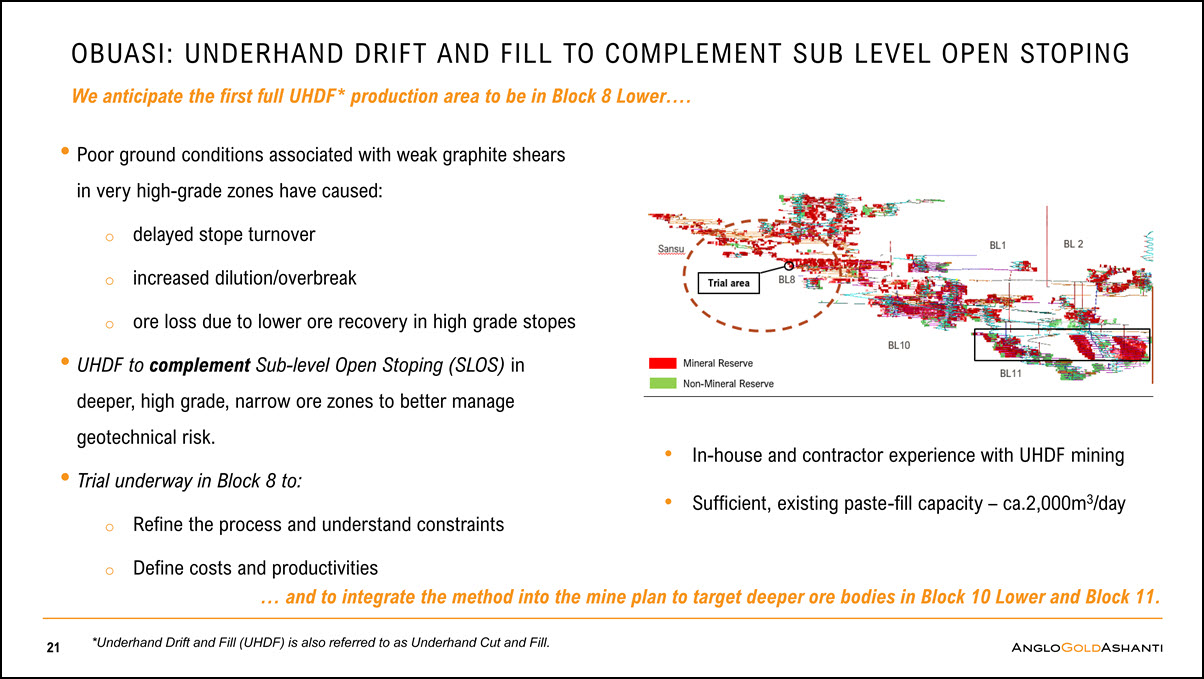

OBUASI: UNDERHAND DRIFT AND FILL TO COMPLEMENT SUB LEVEL OPEN STOPING geotechnical risk. Trial underway in Block 8 to: Refine the process and understand constraints Define costs and productivities 21 We anticipate the first full UHDF* production area to be in Block 8 Lower…. Poor ground conditions associated with weak graphite shears in very high-grade zones have caused: delayed stope turnover increased dilution/overbreak ore loss due to lower ore recovery in high grade stopes UHDF to complement Sub-level Open Stoping (SLOS) in deeper, high grade, narrow ore zones to better manage … and to integrate the method into the mine plan to target deeper ore bodies in Block 10 Lower and Block 11. In-house and contractor experience with UHDF mining Sufficient, existing paste-fill capacity – ca.2,000m3/day *Underhand Drift and Fill (UHDF) is also referred to as Underhand Cut and Fill.

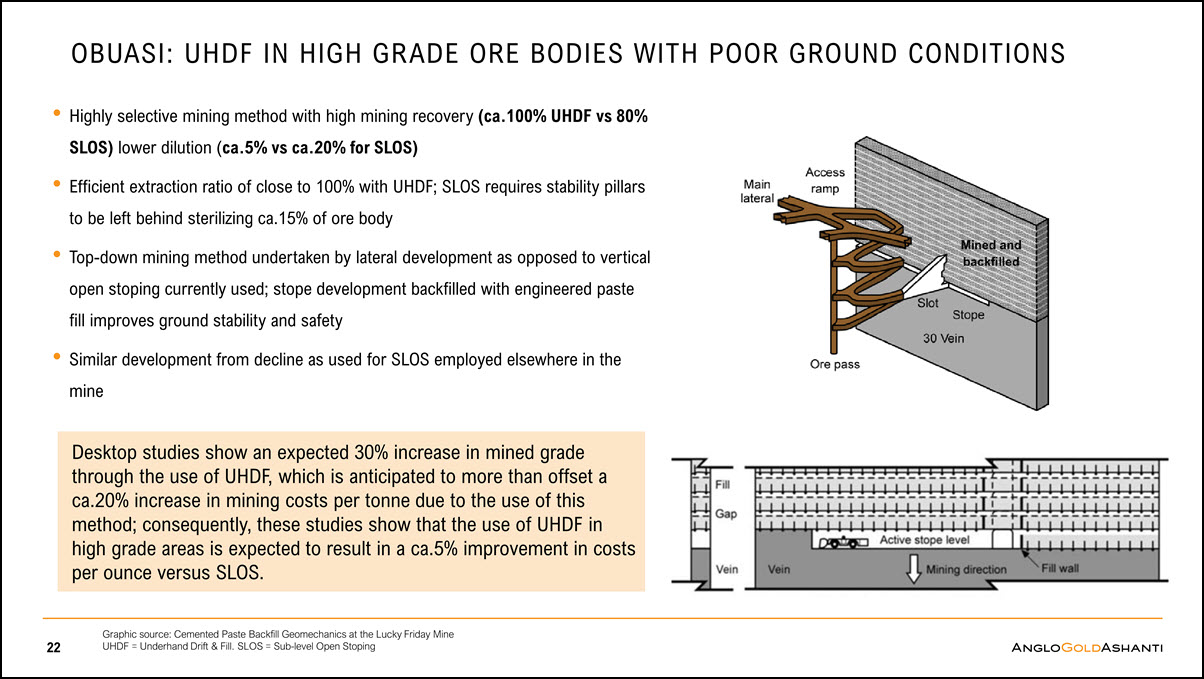

OBUASI: UHDF IN HIGH GRADE ORE BODIES WITH POOR GROUND CONDITIONS Highly selective mining method with high mining recovery (ca.100% UHDF vs 80% SLOS) lower dilution (ca.5% vs ca.20% for SLOS) Efficient extraction ratio of close to 100% with UHDF; SLOS requires stability pillars to be left behind sterilizing ca.15% of ore body Top-down mining method undertaken by lateral development as opposed to vertical open stoping currently used; stope development backfilled with engineered paste fill improves ground stability and safety Similar development from decline as used for SLOS employed elsewhere in the mine 22 Graphic source: Cemented Paste Backfill Geomechanics at the Lucky Friday Mine UHDF = Underhand Drift & Fill. SLOS = Sub-level Open Stoping Desktop studies show an expected 30% increase in mined grade through the use of UHDF, which is anticipated to more than offset a ca.20% increase in mining costs per tonne due to the use of this method; consequently, these studies show that the use of UHDF in high grade areas is expected to result in a ca.5% improvement in costs per ounce versus SLOS.

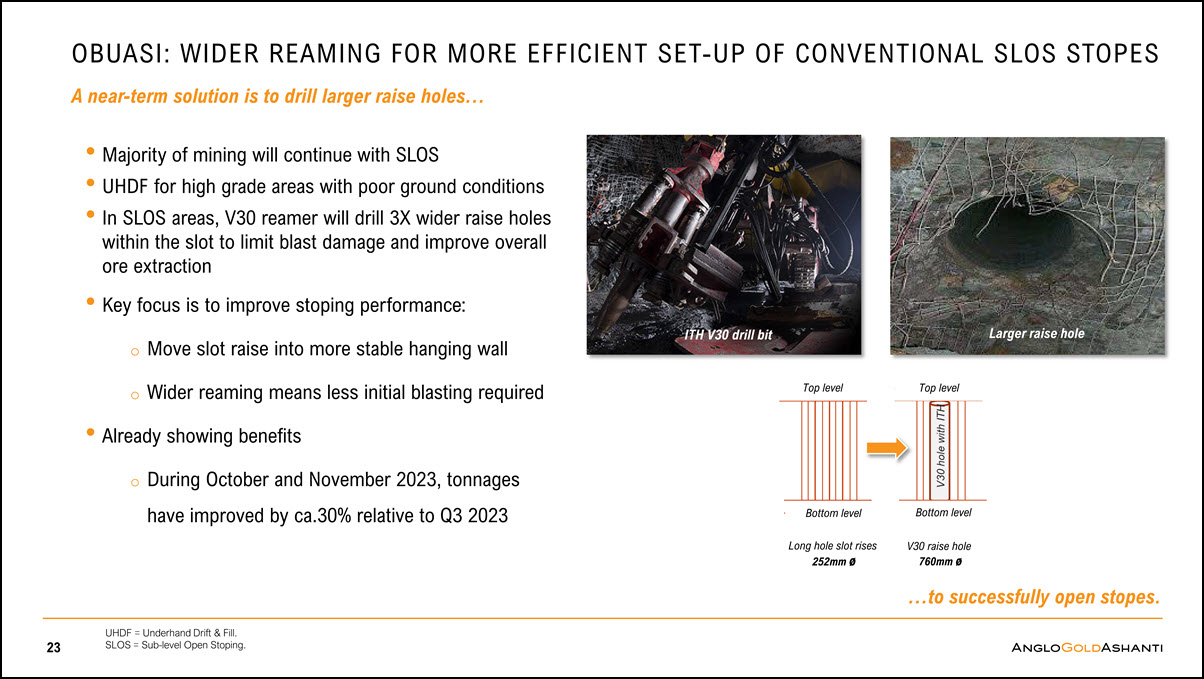

Top level Top level Bottom level Bottom level V30 raise hole 760mm ø Long hole slot rises 252mm ø OBUASI: WIDER REAMING FOR MORE EFFICIENT SET-UP OF CONVENTIONAL SLOS STOPES A near-term solution is to drill larger raise holes… …to successfully open stopes. 23 ITH V30 drill bit Larger raise hole Majority of mining will continue with SLOS UHDF for high grade areas with poor ground conditions In SLOS areas, V30 reamer will drill 3X wider raise holes within the slot to limit blast damage and improve overall ore extraction Key focus is to improve stoping performance: Move slot raise into more stable hanging wall Wider reaming means less initial blasting required Already showing benefits During October and November 2023, tonnages have improved by ca.30% relative to Q3 2023 UHDF = Underhand Drift & Fill. SLOS = Sub-level Open Stoping.

OBUASI: UHDF ANIMATION 24 UHDF = Underhand Drift & Fill. SLOS = Sub-level Open Stoping.

CONCLUSION

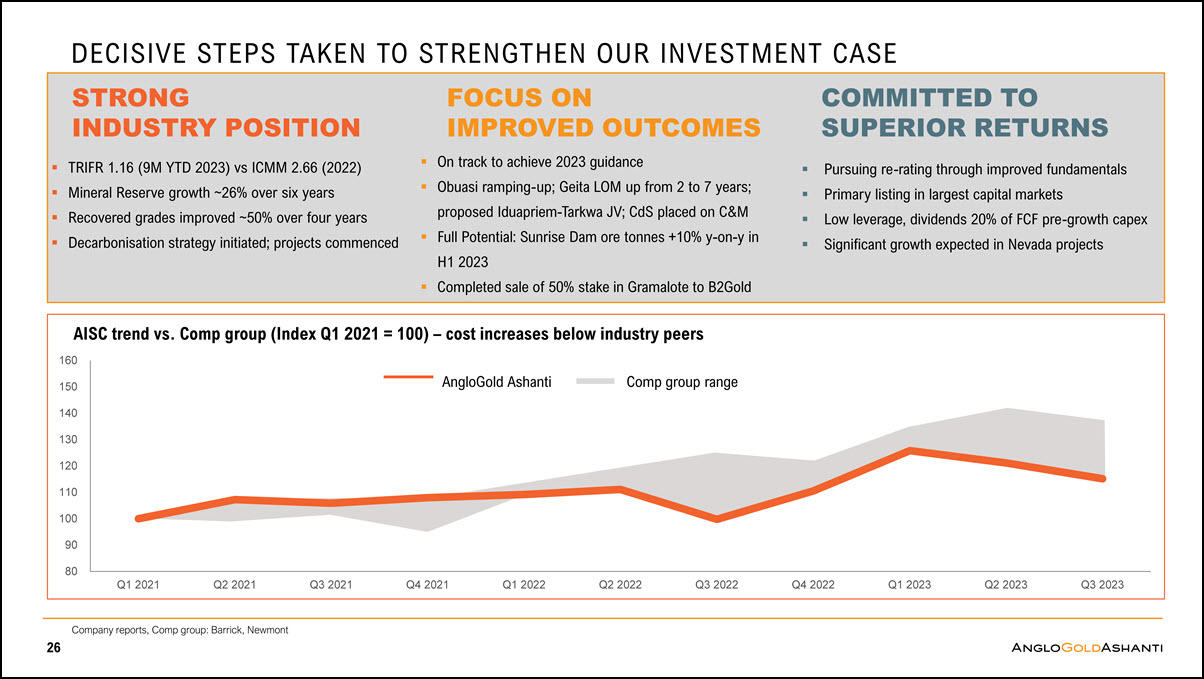

DECISIVE STEPS TAKEN TO STRENGTHEN OUR INVESTMENT CASE AngloGold Ashanti Comp group range Company reports, Comp group: Barrick, Newmont 26 STRONG INDUSTRY POSITION TRIFR 1.16 (9M YTD 2023) vs ICMM 2.66 (2022) Mineral Reserve growth ~26% over six years Recovered grades improved ~50% over four years Decarbonisation strategy initiated; projects commenced FOCUS ON IMPROVED OUTCOMES On track to achieve 2023 guidance Obuasi ramping-up; Geita LOM up from 2 to 7 years; proposed Iduapriem-Tarkwa JV; CdS placed on C&M Full Potential: Sunrise Dam ore tonnes +10% y-on-y in H1 2023 Completed sale of 50% stake in Gramalote to B2Gold COMMITTED TO SUPERIOR RETURNS Pursuing re-rating through improved fundamentals Primary listing in largest capital markets Low leverage, dividends 20% of FCF pre-growth capex Significant growth expected in Nevada projects 140 130 120 110 100 90 80 150 Q1 2021 Q2 2021 Q3 2021 Q4 2021 Q1 2022 Q2 2022 Q3 2022 Q4 2022 Q1 2023 Q2 2023 Q3 2023 AISC trend vs. Comp group (Index Q1 2021 = 100) – cost increases below industry peers 160

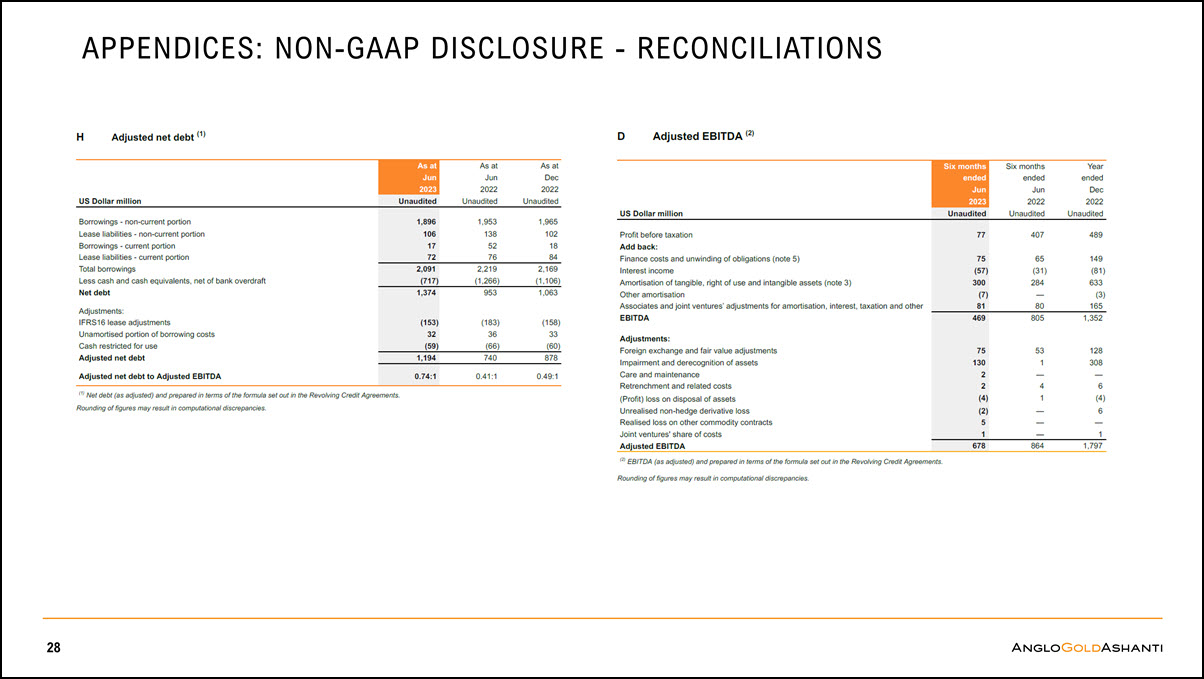

28 APPENDICES: NON-GAAP DISCLOSURE - RECONCILIATIONS

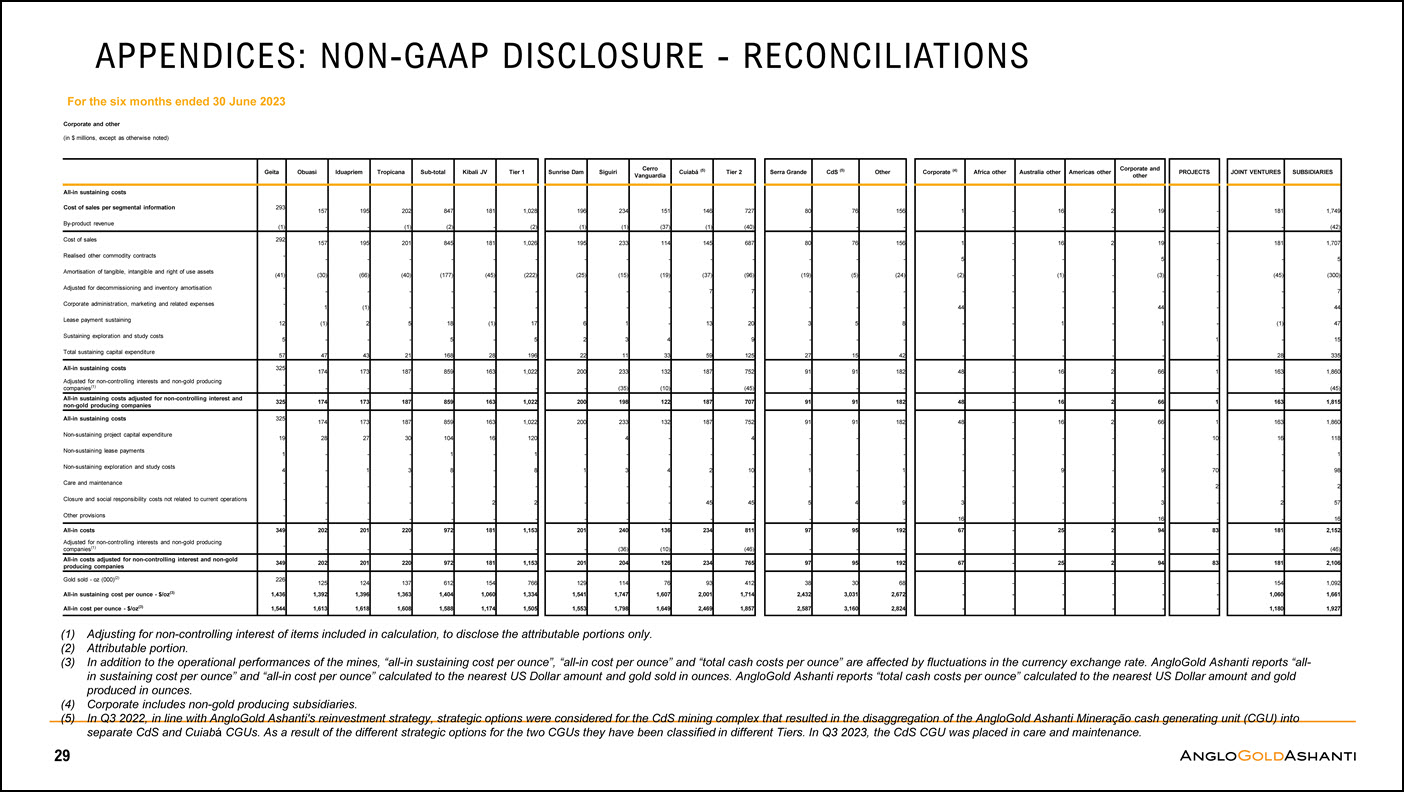

APPENDICES: NON-GAAP DISCLOSURE - RECONCILIATIONS Geita Obuasi Iduapriem Tropicana Sub-total Kibali JV Tier 1 All-in sustaining costs Cost of sales per segmental information 293 157 195 202 847 181 1,028 By-product revenue (1) - - (1) (2) - (2) Cost of sales 292 157 195 201 845 181 1,026 Realised other commodity contracts - - - - - - - Amortisation of tangible, intangible and right of use assets (41) (30) (66) (40) (177) (45) (222) Adjusted for decommissioning and inventory amortisation - - - - - - - Corporate administration, marketing and related expenses - 1 (1) - - - - Lease payment sustaining 12 (1) 2 5 18 (1) 17 Sustaining exploration and study costs 5 - - - 5 - 5 Total sustaining capital expenditure 57 47 43 21 168 28 196 All-in sustaining costs 325 174 173 187 859 163 1,022 Adjusted for non-controlling interests and non-gold producing companies(1) - - - - - - - All-in sustaining costs adjusted for non-controlling interest and non-gold producing companies 325 174 173 187 859 163 1,022 All-in sustaining costs 325 174 173 187 859 163 1,022 Non-sustaining project capital expenditure 19 28 27 30 104 16 120 Non-sustaining lease payments 1 - - - 1 - 1 Non-sustaining exploration and study costs 4 - 1 3 8 - 8 Care and maintenance - - - - - - - Closure and social responsibility costs not related to current operations - - - - - 2 2 Other provisions - - - - - - - All-in costs 349 202 201 220 972 181 1,153 Adjusted for non-controlling interests and non-gold producing companies(1) - - - - - - - All-in costs adjusted for non-controlling interest and non-gold producing companies 349 202 201 220 972 181 1,153 Gold sold - oz (000)(2) 226 125 124 137 612 154 766 All-in sustaining cost per ounce - $/oz(3) 1,436 1,392 1,396 1,363 1,404 1,060 1,334 All-in cost per ounce - $/oz(3) 1,544 1,613 1,618 1,608 1,588 1,174 1,505 Sunrise Dam Siguiri Cerro Vanguardia Cuiabá (5) Tier 2 196 234 151 146 727 (1) (1) (37) (1) (40) 195 233 114 145 687 - - - - - (25) (15) (19) (37) (96) - - - 7 7 - - - - - 6 1 - 13 20 2 3 4 - 9 22 11 33 59 125 200 233 132 187 752 - (35) (10) - (45) 200 198 122 187 707 200 233 132 187 752 - 4 - - 4 - - - - - 1 3 4 2 10 - - - - - - - - 45 45 - - - - - 201 240 136 234 811 - (36) (10) - (46) 201 204 126 234 765 129 114 76 93 412 1,541 1,747 1,607 2,001 1,714 1,553 1,798 1,649 2,469 1,857 Serra Grande CdS (5) Other 80 76 156 - - - 80 76 156 - - - (19) (5) (24) - - - - - - 3 5 8 - - - 27 15 42 91 91 182 - - - 91 91 182 91 91 182 - - - - - - 1 - 1 - - - 5 4 9 - - - 97 95 192 - - - 97 95 192 38 30 68 2,432 3,031 2,672 2,587 3,160 2,824 Corporate (4) Africa other Australia other Americas other Corporate and other PROJECTS 1 - 16 2 19 - - - - - - - 1 - 16 2 19 - 5 - - - 5 - (2) - (1) - (3) - - - - - - - 44 - - - 44 - - - 1 - 1 - - - - - - 1 - - - - - - 48 - 16 2 66 1 - - - - - - 48 - 16 2 66 1 48 - 16 2 66 1 - - - - - 10 - - - - - - - - 9 - 9 70 - - - - - 2 3 - - - 3 - 16 - - - 16 - 67 - 25 2 94 83 - - - - - - 67 - 25 2 94 83 - - - - - - - - - - - - - - - - - - JOINT VENTURES SUBSIDIARIES 181 1,749 - (42) 181 1,707 - 5 (45) (300) - 7 - 44 (1) 47 - 15 28 335 163 1,860 - (45) 163 1,815 163 1,860 16 118 - 1 - 98 - 2 2 57 - 16 181 2,152 - (46) 181 2,106 154 1,092 1,060 1,661 1,180 1,927 Corporate and other (in $ millions, except as otherwise noted) For the six months ended 30 June 2023 Adjusting for non-controlling interest of items included in calculation, to disclose the attributable portions only. Attributable portion. In addition to the operational performances of the mines, “all-in sustaining cost per ounce”, “all-in cost per ounce” and “total cash costs per ounce” are affected by fluctuations in the currency exchange rate. AngloGold Ashanti reports “all- in sustaining cost per ounce” and “all-in cost per ounce” calculated to the nearest US Dollar amount and gold sold in ounces. AngloGold Ashanti reports “total cash costs per ounce” calculated to the nearest US Dollar amount and gold produced in ounces. Corporate includes non-gold producing subsidiaries. (5) In Q3 2022, in line with AngloGold Ashanti's reinvestment strategy, strategic options were considered for the CdS mining complex that resulted in the disaggregation of the AngloGold Ashanti Mineração cash generating unit (CGU) into separate CdS and Cuiabá CGUs. As a result of the different strategic options for the two CGUs they have been classified in different Tiers. In Q3 2023, the CdS CGU was placed in care and maintenance. 29

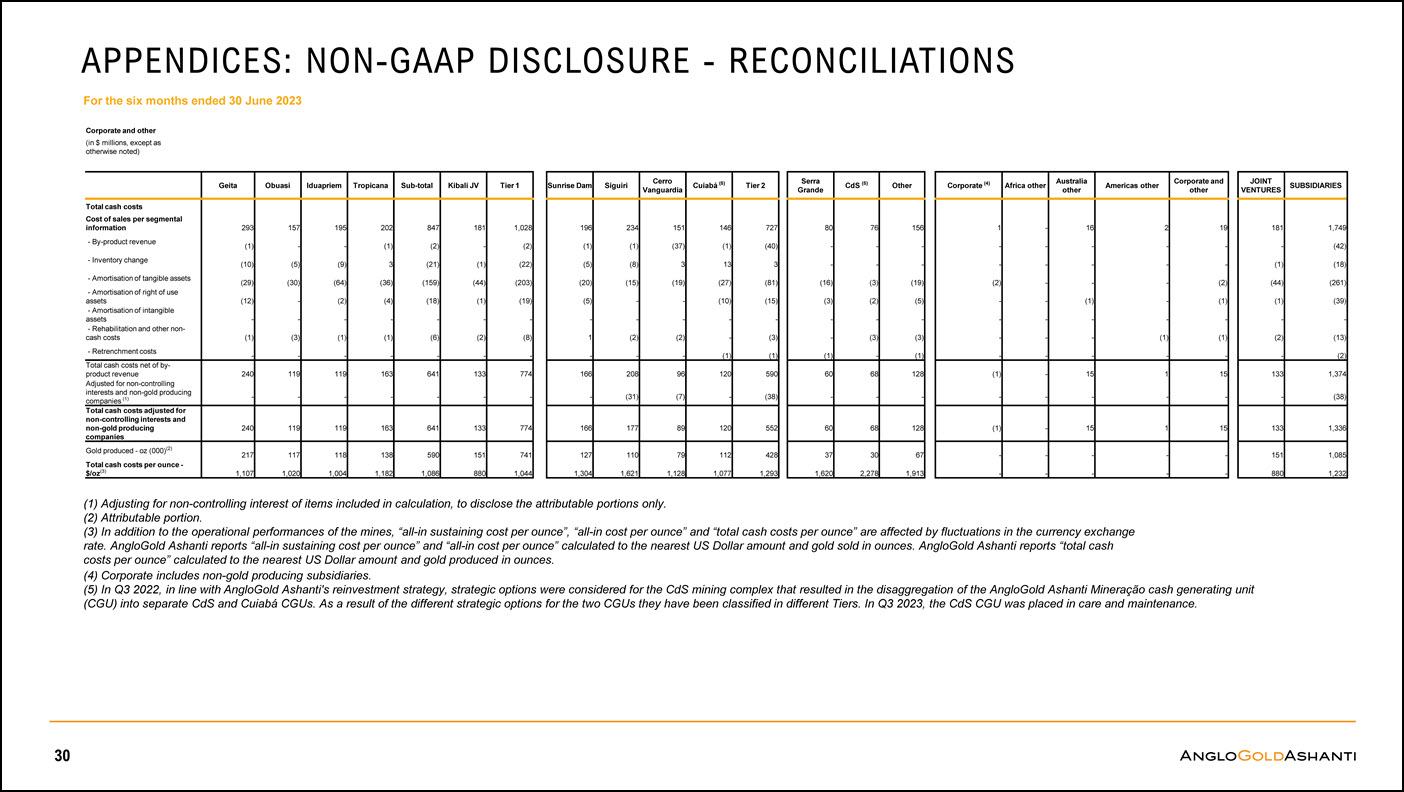

30 Geita Obuasi Iduapriem Tropicana Sub-total Kibali JV Tier 1 Total cash costs Cost of sales per segmental information 293 157 195 202 847 181 1,028 - By-product revenue (1) - - (1) (2) - (2) - Inventory change (10) (5) (9) 3 (21) (1) (22) - Amortisation of tangible assets (29) (30) (64) (36) (159) (44) (203) - Amortisation of right of use assets (12) - (2) (4) (18) (1) (19) - Amortisation of intangible assets - - - - - - - - Rehabilitation and other non- cash costs (1) (3) (1) (1) (6) (2) (8) - Retrenchment costs - - - - - - - Total cash costs net of by- product revenue 240 119 119 163 641 133 774 Adjusted for non-controlling interests and non-gold producing companies (1) - - - - - - - Total cash costs adjusted for non-controlling interests and non-gold producing companies 240 119 119 163 641 133 774 Gold produced - oz (000)(2) 217 117 118 138 590 151 741 Total cash costs per ounce - $/oz(3) 1,107 1,020 1,004 1,182 1,086 880 1,044 Sunrise Dam Siguiri Cerro Vanguardia Cuiabá (5) Tier 2 196 234 151 146 727 (1) (1) (37) (1) (40) (5) (8) 3 13 3 (20) (15) (19) (27) (81) (5) - - (10) (15) - - - - - 1 (2) (2) - (3) - - - (1) (1) 166 208 96 120 590 - (31) (7) - (38) 166 177 89 120 552 127 110 79 112 428 1,304 1,621 1,128 1,077 1,293 Serra Grande CdS (5) Other 80 76 156 - - - - - - (16) (3) (19) (3) (2) (5) - - - - (3) (3) (1) - (1) 60 68 128 - - - 60 68 128 37 30 67 1,620 2,278 1,913 Corporate (4) Africa other Australia other Americas other Corporate and other 1 - 16 2 19 - - - - - - - - - - (2) - - - (2) - - (1) - (1) - - - - - - - - (1) (1) - - - - - (1) - 15 1 15 - - - - - (1) - 15 1 15 - - - - - - - - - - JOINT VENTURES SUBSIDIARIES 181 1,749 - (42) (1) (18) (44) (261) (1) (39) - - (2) (13) - (2) 133 1,374 - (38) 133 1,336 151 1,085 880 1,232 Corporate and other (in $ millions, except as otherwise noted) Adjusting for non-controlling interest of items included in calculation, to disclose the attributable portions only. Attributable portion. In addition to the operational performances of the mines, “all-in sustaining cost per ounce”, “all-in cost per ounce” and “total cash costs per ounce” are affected by fluctuations in the currency exchange rate. AngloGold Ashanti reports “all-in sustaining cost per ounce” and “all-in cost per ounce” calculated to the nearest US Dollar amount and gold sold in ounces. AngloGold Ashanti reports “total cash costs per ounce” calculated to the nearest US Dollar amount and gold produced in ounces. Corporate includes non-gold producing subsidiaries. In Q3 2022, in line with AngloGold Ashanti's reinvestment strategy, strategic options were considered for the CdS mining complex that resulted in the disaggregation of the AngloGold Ashanti Mineração cash generating unit (CGU) into separate CdS and Cuiabá CGUs. As a result of the different strategic options for the two CGUs they have been classified in different Tiers. In Q3 2023, the CdS CGU was placed in care and maintenance. For the six months ended 30 June 2023 APPENDICES: NON-GAAP DISCLOSURE - RECONCILIATIONS

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| AngloGold Ashanti plc | ||||

| Date: November 28, 2023 | ||||

| By: | /s/ HC Grantham | |||

| Name: | HC Grantham | |||

Title: | Interim Company Secretary | |||