UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE 13a-16 OR 15d-16 UNDER

THE SECURITIES EXCHANGE ACT OF 1934

For the month of September 2024

Commission File Number: 001-41815

AngloGold Ashanti plc

(Translation of registrant’s name into English)

4th Floor, Communications House, South Street | 6363 S. Fiddlers Green Circle, Suite 1000 |

| Staines-upon-Thames, Surrey TW18 4PR | Greenwood Village, CO 80111 |

United Kingdom | United States of America |

(Address of principal executive offices)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

Form 20-F ☒ Form 40-F ☐

Enclosure: AngloGold Ashanti to Acquire Centamin Presentation (September 2024)

AngloGold Ashanti to Acquire Centamin September 2024

DISCLAIMER Certain statements contained in this document, other than statements of historical fact, including, without limitation, those concerning the economic outlook for the gold mining industry, expectations regarding gold prices, production, total cash costs, all-in sustaining costs, all-in costs, cost savings and other operating results, return on equity, productivity improvements, growth prospects and outlook of AngloGold Ashanti plc’s (the “Company”, “AngloGold Ashanti” or “AGA”) operations, individually or in the aggregate, including the achievement of project milestones, commencement and completion of commercial operations of certain of AngloGold Ashanti’s exploration and production projects and the completion of acquisitions, dispositions or joint venture transactions, AngloGold Ashanti’s liquidity and capital resources and capital expenditures, the consequences of the COVID-19 pandemic and the outcome and consequences of any potential or pending litigation or regulatory proceedings or environmental, health and safety issues, are forward-looking statements regarding AngloGold Ashanti’s financial reports, operations, economic performance and financial condition. These forward-looking statements or forecasts are not based on historical facts, but rather reflect our current beliefs and expectations concerning future events and generally may be identified by the use of forward-looking words, phrases and expressions such as “believe”, “expect”, “aim”, “anticipate”, “intend”, “foresee”, “forecast”, “predict”, “project”, “estimate”, “likely”, “may”, “might”, “could”, “should”, “would”, “seek”, “plan”, “scheduled”, “possible”, “continue”, “potential”, “outlook”, “target” or other similar words, phrases, and expressions; provided that the absence thereof does not mean that a statement is not forward-looking. Similarly, statements that describe our objectives, plans or goals are or may be forward-looking statements. These forward-looking statements or forecasts involve known and unknown risks, uncertainties and other factors that may cause AngloGold Ashanti’s actual results, performance, actions or achievements to differ materially from the anticipated results, performance, actions or achievements expressed or implied in these forward-looking statements. Although AngloGold Ashanti believes that the expectations reflected in such forward-looking statements and forecasts are reasonable, no assurance can be given that such expectations will prove to have been correct. Accordingly, results, performance, actions or achievements could differ materially from those set out in the forward-looking statements as a result of, among other factors, changes in economic, social, political and market conditions, including related to inflation or international conflicts, the success of business and operating initiatives, changes in the regulatory environment and other government actions, including environmental approvals, fluctuations in gold prices and exchange rates, the outcome of pending or future litigation proceedings, any supply chain disruptions, any public health crises, pandemics or epidemics (including the COVID-19 pandemic), the failure to maintain effective internal control over financial reporting or effective disclosure controls and procedures, the inability to remediate one or more material weaknesses, or the discovery of additional material weaknesses, in the Company’s internal control over financial reporting, and other business and operational risks and challenges and other factors, including mining accidents, the results of exploration activities and feasibility studies, the speculative nature of mineral exploitation and development, risks that exploration data may be incomplete and considerable additional work may be required to complete future evaluation, including but not limited to drilling, engineering and socioeconomic studies and investment, possible variations of ore grade or recovery rates, accidents, labour disputes and other risks of the mining industry, discovery of archaeological ruins, and risk of loss due to acts of war, terrorism, sabotage and civil disturbances operating or technical difficulties in connection with mining or development activities, including geotechnical challenges and disruptions in the maintenance or provision of required infrastructure and information technology systems. Neither AngloGold Ashanti nor any of its respective associates, directors, officers or advisers, provides any representation, assurance or guarantee that the occurrence of the events expressed or implied in any forward-looking statements in this communication will actually occur. For a discussion of such risk factors, refer to AngloGold Ashanti’s annual report on Form 20-F for the year ended 31 December 2023 filed with the United States Securities and Exchange Commission (“SEC”). These factors are not necessarily all of the important factors that could cause AngloGold Ashanti’s actual results, performance, actions or achievements to differ materially from those expressed in any forward-looking statements. Other unknown or unpredictable factors could also have material adverse effects on AngloGold Ashanti’s future results, performance, actions or achievements. Consequently, readers are cautioned not to place undue reliance on forward-looking statements. AngloGold Ashanti undertakes no obligation to update publicly or release any revisions to these forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events, except to the extent required by applicable law. All subsequent written or oral forward-looking statements attributable to AngloGold Ashanti or any person acting on its behalf are qualified by the cautionary statements herein. The information included in this presentation has not been reviewed or reported on by AngloGold Ashanti’s external auditors. Non-GAAP financial measures This communication may contain certain “Non-GAAP” financial measures which have been determined using industry guidelines and practices and are not measures under IFRS. An investor should not consider these items in isolation or as alternatives to any other measure of financial performance presented in accordance with IFRS or as an indicator of AngloGold Ashanti’s performance. AngloGold Ashanti utilizes certain Non-GAAP performance measures and ratios in managing its business. Non-GAAP financial measures should be viewed in addition to, and not as an alternative for, the reported operating results or cash flow from operations or any other measures of performance prepared in accordance with IFRS. In addition, the presentation of these measures may not be comparable to similarly titled measures other companies may use. The Company is not providing quantitative reconciliations to the most directly comparable IFRS measures for its forward-looking Non-GAAP financial measures shown herein in reliance on the exception provided by Rule 100(a)(2) of Regulation G because the reconciliations cannot be performed without unreasonable efforts as such IFRS measures cannot be reliably estimated due to their dependence on future uncertainties and adjusting items, including, among other factors, changes in economic, social, political and market conditions, including related to inflation or international conflicts, the success of business and operating initiatives, changes in the regulatory environment and other government actions, including environmental approvals, fluctuations in gold prices and exchange rates, the outcome of pending or future litigation proceedings, any supply chain disruptions, any public health crises, pandemics or epidemics (including the COVID-19 pandemic), and other business and operational risks and challenges and other factors, including mining accidents, that the Company cannot reasonably predict at this time but which may be material. No statement in this presentation is intended as a profit forecast, profit estimate or quantified financial benefits statement for any period. “Centamin” refers to Centamin plc in this presentation. Website: www.anglogoldashanti.com 2

Technical DISCLAIMER MINERAL RESOURCE AND MINERAL RESERVE INFORMATION The AngloGold Ashanti Mineral Resource and Mineral Reserve stated herein were prepared in compliance with Subpart 1300 of Regulation S-K (17 CFR § 229.1300) (“Regulation S-K 1300”). Refer to Item 1300 (Definitions) of Regulation S-K for the meaning of the terms used in AngloGold Ashanti’s Mineral Resource and Mineral Reserve reporting. The AngloGold Ashanti Mineral Resource and Mineral Reserve represent the amount of gold, copper, silver, sulphur and molybdenum estimated at 31 December 2023 and are based on information available at the time of estimation. Such estimates are, or will be, to a large extent, based on the prices of the respective commodities and interpretations of geologic data obtained from drill holes and other exploration techniques, which data may not necessarily be indicative of future results. AngloGold Ashanti publishes its Mineral Resource and Mineral Reserve on an annual basis and has re-estimated its Mineral Resource and Mineral Reserve at 31 December 2023, taking into account economic assumptions, changes to future production, capital expenditure and operating costs (if any), depletion, additions as well as any acquisitions or disposals during 2023. The legal tenure of each material property has been verified to the satisfaction of the accountable Qualified Person and all of the Mineral Reserve has been confirmed to be covered by the required mining permits or there exists a realistic expectation, based on applicable laws and regulations, that issuance of permits or resolution of legal issues necessary for mining and processing at a particular deposit will be accomplished in the ordinary course and in a timeframe consistent with AngloGold Ashanti’s (or its joint venture partners’) current mine plans. For the Mineral Reserve, the term “economically viable” means that profitable extraction or production has been established or analytically demonstrated in, at a minimum, a pre-feasibility study, to be economically viable under reasonable investment and market assumptions. Mineral Reserve is subdivided and reported, in order of increasing geoscientific knowledge and confidence, into Probable and Proven Mineral Reserve categories. Mineral Reserve is aggregated from the Probable and Proven Mineral Reserve categories. Ounces of gold or silver or pounds of copper, sulphur or molybdenum included in the Probable and Proven Mineral Reserve are estimated and reported as delivered to plant (i.e., the point where material is delivered to the processing facility) and exclude losses during metallurgical treatment. In compliance with Regulation S-K 1300, the Mineral Resource herein is reported as exclusive of the Mineral Reserve before dilution and other factors are applied, unless otherwise stated. Mineral Resource is subdivided and reported, in order of increasing geoscientific knowledge and confidence, into Inferred, Indicated and Measured Mineral Resource categories. Ounces of gold or silver or pounds of copper, sulphur or molybdenum included in the Inferred, Indicated and Measured Mineral Resource are those contained in situ prior to losses during metallurgical treatment. While it would be reasonable to expect that the majority of Inferred Mineral Resource would upgrade to Indicated Mineral Resource with continued exploration, due to the uncertainty of Inferred Mineral Resource, it should not be assumed that such upgrading will always occur. If estimations are required to be revised using significantly lower commodity prices, increases in operating costs, reductions in metallurgical recovery or other modifying factors, this could result in the Mineral Resource or Mineral Reserve not being mined or processed profitably, material write-downs of AngloGold Ashanti’s investment in mining properties, goodwill and increased amortisation, reclamation and closure charges. If AngloGold Ashanti determines that certain of its Mineral Resource or Mineral Reserve have become uneconomic, this may ultimately lead to a reduction in its aggregate reported Mineral Resource or Mineral Reserve, respectively. Consequently, if AngloGold Ashanti’s actual Mineral Resource and Mineral Reserve is less than current estimates, its business, prospects, results of operations and financial position may be materially impaired. The pre-feasibility and feasibility studies for undeveloped ore bodies derive estimates of capital expenditure and operating costs based upon anticipated tonnage and grades of ore to be mined and processed, the predicted configuration of the ore body, expected recovery rates of metals from the ore, the costs of comparable facilities, the costs of operating and processing equipment and other factors. Actual operating and capital expenditure cost and economic returns on projects may differ significantly from original estimates. Further, it may take many years from the initial phases of exploration until commencement of production, during which time, the economic feasibility of production may change. The Mineral Resource is subject to further exploration and development, and is subject to additional risks, and no assurance can be given that they will eventually convert to future Mineral Reserve. For additional information, see Table 1 (Summary Mineral Resource) and Table 2 (Summary Mineral Reserve) to Paragraph (b) of Item 1303 (Summary disclosure) of Regulation S-K included in AngloGold Ashanti’s annual report on Form 20-F for the year ended 31 December 2023 filed with the SEC. These summary tables include each class of Mineral Resource (Inferred, Indicated and Measured) together with total Measured and Indicated Mineral Resource, and each class of Mineral Reserve (Probable and Proven) together with total Mineral Reserve. The AngloGold Ashanti Mineral Resource at the end of the fiscal year ended 31 December 2023 was estimated using a gold price of $1,750/oz and a copper price of $3.50/lb, unless otherwise stated. The AngloGold Ashanti Mineral Reserve at the end of the fiscal year ended 31 December 2023 was estimated using a gold price of $1,400/oz, and a copper price of $2.90/lb, unless otherwise stated. The scientific and technical information in respect of the year ended 31 December 2023 AngloGold Ashanti’s Mineral Resource and Mineral Reserve contained in this announcement has been reviewed and approved for release by Mrs TM Flitton, Chairperson of AngloGold Ashanti’s Mineral Resource and Mineral Reserve Leadership Team, Vice President Resource and Reserve, Master of Engineering (Mining), Bachelor of Science (Honours, Geology), RM SME, Pr.Sci.Nat (SACNASP), FGSSA. Mrs TM Flitton assumes responsibility for the Mineral Resource and Mineral Reserve processes for AngloGold Ashanti. Mrs. TM Flitton has 22 years’ experience in mining with 11 years directly leading and managing Mineral Resource and Mineral Reserve reporting. She is employed full-time by AngloGold Ashanti and can be contacted at the following address: 6363 S. Fiddlers Green Circle, Suite 1000, Greenwood Village, CO 80111, United States. Mrs. TM Flitton consents to the inclusion of the AngloGold Ashanti Mineral Resource and Mineral Reserve information in this announcement, in the form and context in which it appears in the narrative disclosure. AngloGold Ashanti has reconciled the definitions of Mineral Resource and Mineral Reserve as defined by Regulation S-K 1300 to the definition standards incorporated in NI 43-101, and there are no material differences. While the terms “mineral resource,” “inferred mineral resource,” “indicated mineral resource,” “mineral reserve,” “probable mineral reserve,” and “proven mineral reserve” as defined under NI 43-101 are substantially similar to the same terms as defined under Regulation S-K 1300, there are differences in the definitions. Accordingly, information contained in this announcement and in the documents incorporated by reference herein containing descriptions of AngloGold Ashanti’s mineral deposits may not be comparable to similar information made public by Canadian companies subject to the reporting requirements of Canadian laws and the rules and regulations thereunder. 3

Technical DISCLAIMER MINERAL RESOURCE AND MINERAL RESERVE INFORMATION Centamin’s Mineral Resource and Mineral Reserve estimates have been prepared with reference to the Canadian Institute of Mining Metallurgy and Petroleum (CIM) Definition Standards (2014) and CIM Best Practice Guidelines (2019), as required by NI 43-101 standard for reporting Mineral Resource and Mineral Reserve. Centamin has reconciled the Mineral Resource and Mineral Reserve as defined by NI 43-101 to the definition standards incorporated in Regulation S-K 1300, and there are no material differences. For United States reporting purposes, Regulation S-K 1300 applies different requirements and standards from those under NI 43-101 and the JORC Code. For example, while the terms “mineral resource,” “inferred mineral resource,” “indicated mineral resource,” “mineral reserve,” “probable mineral reserve,” and “proven mineral reserve” as defined under NI 43-101 are substantially similar to the same terms as defined under Regulation S-K 1300, there are differences in the definitions. Accordingly, information contained in this announcement and in the documents incorporated by reference herein containing descriptions of Centamin’s mineral deposits may not be comparable to similar information made public by United States companies subject to the reporting requirements of United States federal securities laws and the rules and regulations thereunder. Generally, Mineral Resource and Mineral Reserve estimates, other than those prepared in accordance with Regulation S-K 1300, are not permitted to be disclosed in public documents filed with the SEC. Such estimates, however, are disclosed in this announcement consistent with the exception for SEC filings provided for in Item 1304(h) of Regulation S-K. Sufficient work to classify Centamin’s Mineral Resource and Reserve estimates (as at 30 June 2023) as a current estimate of Mineral Reserve and Mineral Resource as defined under Regulation S-K 1300 has not been done by a Qualified Person as defined under Regulation S-K 1300 of AngloGold Ashanti. AngloGold Ashanti has not been involved in the preparation of Centamin’s Mineral Resource and Mineral Reserve estimates (as at 30 June 2023). The Centamin historical estimates are based on Centamin’s annual Mineral Resource and Mineral Reserve statement (as at 30 June 2023) included in the 2023 Centamin Annual Report, which presents Mineral Resource and Mineral Reserve estimates on a non-attributable basis (i.e. assuming 100% ownership). The Centamin historical estimates, however, are presented on a combined basis together with AngloGold Ashanti’s Mineral Resource and Mineral Reserve on an attributable basis, reflecting the ownership percentages set forth in the Centamin’s Mineral Resource and Mineral Reserve statement (as at 30 June 2023). In addition, in accordance with NI 43-101, the registrant must state the extent, if any, to which Mineral Reserve is included in the total Mineral Resource. Centamin reports Mineral Resource inclusive of Mineral Reserve before dilution and other factors are applied. The Centamin Mineral Resource, however, is presented in this presentation as exclusive Mineral Resource (defined as the inclusive Mineral Resource less the Mineral Reserve before dilution and other factors are applied) by subtracting Mineral Reserve from inclusive Mineral Resource. The technical and scientific information contained in this announcement in respect of Centamin has been reviewed and approved for release by Mr. Craig Barker, Head of Geology for Centamin. 4

highlights – a compelling strategic fit that matches our core competencies SUKARI, A WORLD CLASS TIER 1 ASSET: Long life, compelling cost profile and attractive development potential (2023A total cash costs of $970/oz1 and AISC of $1,196/oz1) STEP CHANGE IN PRODUCTION AND REDUCTION TO COST: Increases annual gold production by ~450koz2, to over 3.0Moz2 p.a., with immediate reduction to combined unit total cash costs and all-in sustaining costs ATTRACTIVE UP-FRONT SHAREHOLDER RETURNS: Accretive to FCF/share in first full year post-completion and NAV/share ADDITIONAL VALUE UPSIDE: Leveraging AngloGold Ashanti’s Full Asset Potential efficiency framework, corporate infrastructure and supply efficiencies, as well as realising upside from Sukari underground / EDX blocks BALANCE SHEET AND CAPITAL DISCIPLINE: Balance sheet strength maintained through majority (94%) equity consideration; the addition of Sukari to the portfolio provides enhanced ability to fund growth and return cash to shareholders under AngloGold Ashanti’s robust capital allocation framework COMPLEMENTARY CAPABILITIES: Leverages AngloGold Ashanti’s expertise and extensive track record operating large open pit and underground mines in Africa along with its world-class exploration expertise and integrated stakeholder engagement approach Restated per AngloGold Ashanti definition; see appendix for reconciliation of Non-GAAP financial measures 2023A, consolidated basis; excludes Córrego do Sítio (“CdS”) operation 5

Transaction overview: RECOMMENDED ACQUISITION OF Centamin CONSIDERATION AND KEY TERMS Unanimously recommended by Centamin board of directors 0.06983 new AngloGold Ashanti shares and $0.125 per share in cash for each Centamin share, implying1,2: Offer value of 163 pence per Centamin share Equity value for Centamin of c.$2.5 billion (c.£1.9 billion), of which $148 million delivered in cash Premium to share price on 9 September 2024 of 36.7% Premium based on the 30-day volume-weighted average share prices3 of AngloGold Ashanti and Centamin of 37.6% Centamin shareholders to own c.16.4% of the combined group immediately following completion Irrevocable undertakings received from Centamin directors CAPITAL MARKETS ASPECTS AngloGold Ashanti will maintain its primary listing on the NYSE, with secondary listings on the JSE, A2X and GhSE AngloGold Ashanti expects to maintain its current dividend policy after giving effect to the transaction CONDITIONS AND TIMING To be implemented via Jersey scheme of arrangement, with anticipated key milestones including: Centamin shareholder approval meetings on or around 28 October 2024 Approval: a majority in number of those present and voting representing at least 75% of the voting rights of all shares voted Subject to customary closing conditions including: none of the circumstances contemplated in the Egyptian Condition4 having occurred; competition clearance from the Egyptian authorities; Centamin shareholder approvals; and typical scheme of arrangement scheme sanction conditions Expected completion during Q4 2024 6 Note: premiums relate to Centamin prices as on the London Stock Exchange Based on closing share prices and exchange rate of £1:US$1.3080 as of 9 September 2024 Centamin shareholders remain entitled to interim dividend of 2.25 US cents per share, as declared by Centamin on 25 July 2024 Based on trading days The condition set out in paragraph 5 of Part A of Appendix 1 of the Rule 2.7 announcement

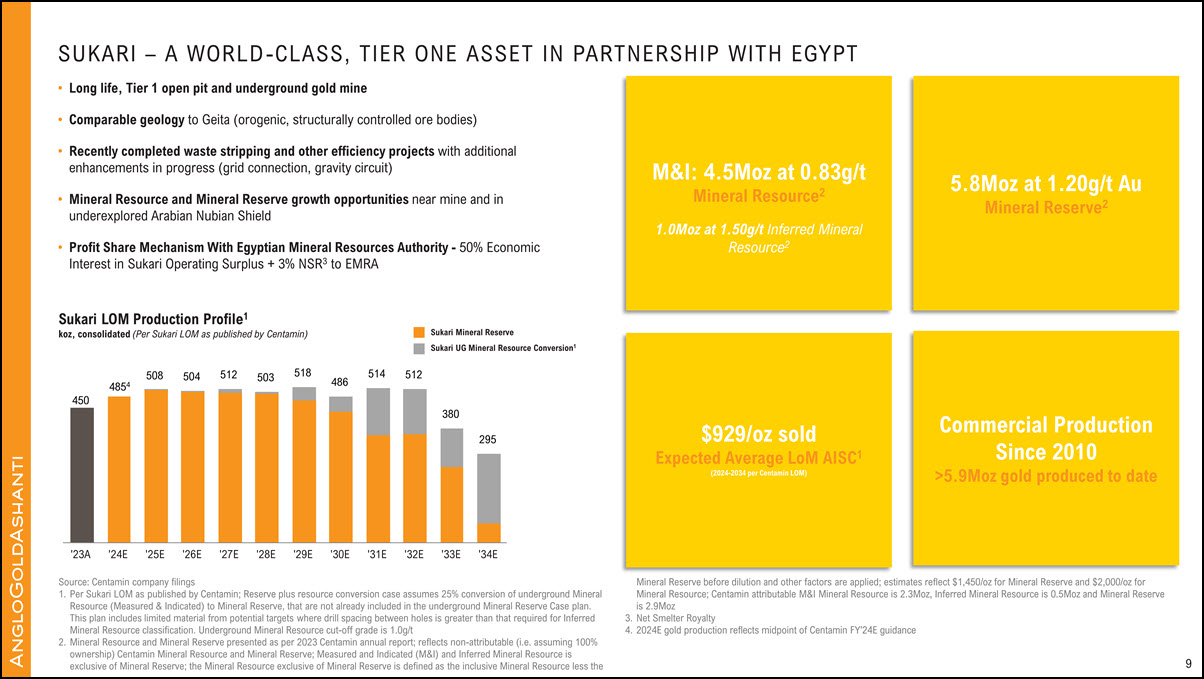

Centamin – north Africa’s pre-eminent gold asset and a foothold in west africa DOROPO GOLD PROJECTCôte d’Ivoire (1,582km2) DFS published Mining License application underway 1.2Moz M+I1 (1.1Moz attributable) 0.3Moz Inferred1 (0.3Moz attributable) 1.9Moz P+P1 (1.7Moz attributable) ABC PROJECTCôte d’Ivoire (1,148km2) Further drill targets identified Evaluation underway 2.2Moz Inferred1 (2.2Moz attributable) Source: Centamin company filings Mineral Resource and Mineral Reserve presented as per 2023 Centamin annual report; reflects non-attributable (i.e. assuming 100% ownership) Centamin Mineral Resource and Mineral Reserve; Measured and Indicated (M&I) and Inferred Mineral Resource is exclusive of Mineral Reserve; the Mineral Resource exclusive of Mineral Reserve is defined as the inclusive Mineral Resource less the Mineral Reserve before dilution and other factors are applied; estimates reflect $1,450/oz for Sukari Mineral Reserve, $1,500/oz for Doropo Mineral Reserve, and $2,000/oz for Mineral Resource; Centamin attributable M&I Mineral Resource is 3.3Moz, Inferred Mineral Resource is 2.9Moz and Mineral Reserve is 4.6Moz. For attributable Mineral Resource and Mineral Reserve refer to the brackets included on the slide. SUKARI GOLD MINEEgypt (160km2) 470-500koz (FY’24E) 4.5Moz M+I1 (2.3Moz attributable) 1.0Moz Inferred1 (0.5Moz attributable) 5.8Moz P+P1 (2.9Moz attributable) EDX BLOCKSEgypt (2,644km2) Exploitation terms agreed 2nd Phase of Nugrus drilling Fieldwork on all blocks 7 Large scale, low-cost producing asset with significant cashflow generation Geology, mining and processing operations complementary with AngloGold Ashanti capabilities Opportunity to deploy AngloGold Ashanti’s world-class exploration expertise to unlock the next phase of Sukari growth 5.7Moz Measured & Indicated Mineral Resource (M+I)1 3.4Moz Inferred Mineral Resource1 7.7Moz Proven & Probable Mineral Reserve (P+P)1

Source: AngloGold Ashanti and Centamin company filings Note: Reflects attributable Mineral Resource and Mineral Reserve; for AngloGold Ashanti refer to its annual report on Form 20-F for the year ended 31 December 2023 filed with the United States Securities and Exchange Commission (“SEC”) for information including gold price assumptions; for Centamin’s annual Mineral Resource and Mineral Reserve statement (as at 30 June 2023) refer to the 2023 Centamin Annual Report. Centamin estimates reflect $1,450/oz for Sukari Mineral Reserve, $1,500/oz for Doropo Mineral Reserve, and $2,000/oz for Mineral Resource Measured and Indicated (M&I) and Inferred Mineral Resource is exclusive of Mineral Reserve. The Mineral Resource exclusive of Mineral Reserve is defined as the inclusive Mineral Resource less the Mineral Reserve before dilution and other factors are applied Consolidated basis but for Tropicana (70%) and Kibali (45%) Excludes Córrego do Sítio given care & maintenance status as of August 2023 Excludes Serra Grande and Córrego do Sítio, Centamin Côte d’Ivoire assets Attributable Mineral Reserve includes Centamin’s Sukari and Côte d’Ivoire assets as well as Serra Grande; excludes Córrego do Sítio Sukari – a natural fit Within our portfolio of world class assets and projects Combined Mineral Reserve Combined AngloGold Ashanti Footprint Combined Production2 (2023A) Total: 32.3Moz5 Total: 3.1Moz5 Argentina Cerro Vanguardia (92.5%) Guinea Siguiri (85%) Ghana Iduapriem Obuasi DRC Kibali (45%) Tanzania Geita Brazil AGA Mineração Australia Sunrise Dam Tropicana (70%) Colombia Quebradona United States of America North Bullfrog Silicon Merlin Mother Lode Sterling LONGER LIFE, LOWER COST, SCALE / GROWTH POTENTIAL, ~78% GROUP MINERAL RESERVE, ~67% OF ANGLOGOLD ASHANTI’S GOLD PRODUCTION STEADY PERFORMERS, RELIABLE CASH GENERATORS, SHORTER LIFE, FP FOCUS – OPPORTUNITIES TO IMPROVE COST COMPETITIVENESS Tier 1 Assets / Projects Tier 2 Assets4 Geita ● Obuasi ● Kibali ● Sukari ● Iduapriem ● Tropicana ● Nevada ● Quebradona Sunrise Dam ● Siguiri ● Cerro Vanguardia ● Cuiabá3 Gold production (‘23A)2 M&I Resource1 Inferred Resource1 Mineral Reserve Gold production (‘23A)2 M&I Resource1 Inferred Resource1 Mineral Reserve 2,080koz 26.5Moz 29.8Moz 25.2Moz 928koz 10.1Moz 7.6Moz 4.9Moz - Cuiabá Egypt Sukari (50%) 8 8% 3% 15% 25% 9% 40% Africa 74% South America North America West Africa East Africa North Africa 18% – 16% 27% 15% 24% South America Africa 66% West Africa East Africa North Africa

Sukari – a world-class, tier one asset in partnership with egypt Long life, Tier 1 open pit and underground gold mine Comparable geology to Geita (orogenic, structurally controlled ore bodies) Recently completed waste stripping and other efficiency projects with additional enhancements in progress (grid connection, gravity circuit) Mineral Resource and Mineral Reserve growth opportunities near mine and in underexplored Arabian Nubian Shield Profit Share Mechanism With Egyptian Mineral Resources Authority - 50% Economic Interest in Sukari Operating Surplus + 3% NSR3 to EMRA Source: Centamin company filings Per Sukari LOM as published by Centamin; Reserve plus resource conversion case assumes 25% conversion of underground Mineral Resource (Measured & Indicated) to Mineral Reserve, that are not already included in the underground Mineral Reserve Case plan. This plan includes limited material from potential targets where drill spacing between holes is greater than that required for Inferred Mineral Resource classification. Underground Mineral Resource cut-off grade is 1.0g/t Mineral Resource and Mineral Reserve presented as per 2023 Centamin annual report; reflects non-attributable (i.e. assuming 100% ownership) Centamin Mineral Resource and Mineral Reserve; Measured and Indicated (M&I) and Inferred Mineral Resource is exclusive of Mineral Reserve; the Mineral Resource exclusive of Mineral Reserve is defined as the inclusive Mineral Resource less the Mineral Reserve before dilution and other factors are applied; estimates reflect $1,450/oz for Mineral Reserve and $2,000/oz for Mineral Resource; Centamin attributable M&I Mineral Resource is 2.3Moz, Inferred Mineral Resource is 0.5Moz and Mineral Reserve is 2.9Moz Net Smelter Royalty 2024E gold production reflects midpoint of Centamin FY’24E guidance Sukari LOM Production Profile1 koz, consolidated (Per Sukari LOM as published by Centamin) 9 450 4854 508 504 512 503 518 486 514 512 380 295 ‘23A ‘24E ‘25E ‘26E ‘27E ‘28E ‘29E ‘30E ‘31E ‘32E ‘33E ‘34E Sukari Mineral Reserve Sukari UG Mineral Resource Conversion1 5.8Moz at 1.20g/t Au Mineral Reserve2 $929/oz sold Expected Average LoM AISC1 (2024-2034 per Centamin LOM) M&I: 4.5Moz at 0.83g/t Mineral Resource2 1.0Moz at 1.50g/t Inferred Mineral Resource2 Commercial Production Since 2010 >5.9Moz gold produced to date

improves production and cost, strengthens balance sheet, generates attractive returns Transaction accretive to AngloGold Ashanti NAV/share and FCF/share in first full year post completion Source: AngloGold Ashanti and Centamin company filings See appendix for reconciliation of Non-GAAP financial measures Consolidated basis but for Tropicana (70%) and Kibali (45%); excludes CdS operation Restated per AngloGold Ashanti definition; see appendix for reconciliation of Non-GAAP financial measures Excludes impacts of transaction fees and expenses 10 Combined 2023A Metrics1,2 AngloGold Ashanti Centamin Combined Basis Gold production (koz) 2,644 450 3,095 Total cash costs ($/oz) $1,115 $9703 $1,094 AISC ($/oz) $1,544 $1,1963 $1,493 FCF/share $0.22 $0.043 $0.25 Adjusted net debt to Adjusted EBITDA 0.9x Net Cash 0.7x4

Full Asset Potential Opportunity to leverage AngloGold Ashanti’s proven Full Asset Potential Efficiency Framework at a complementary asset Sukari has comparable operational characteristics and geology to existing AngloGold Ashanti assets such as Geita Leveraging Corporate Infrastructure Right sizing of corporate functions and non-Egypt footprint Supply Efficiencies (Sukari Procurement Costs) Reduction in mining consumables costs (reagents, explosives, cyanide etc.), and other operating costs, from stronger combined purchasing power Sukari Underground Production Significant production upside in high grade zones: Top of Horus, Horus Deeps, Ptah, Bast, Amun Deposit not constrained at depth and remains open in several directions Exploration and Life Extension Opportunity Opportunity to further extend Sukari life from EDX regional exploration blocks Apply AngloGold Ashanti exploration track record and expertise to underexplored and highly prospective region Optimization by leveraging our expertise, asset optimisation programme and global scale 11 Source: company filings

Exploration Potential in Highly Prospective EDX exploration Blocks Governed under separate Model Mining Exploitation Agreement1 EASTERN DESERT EXPLORATION (“EDX”) Source: Centamin company filings Key terms: 5% NSR to the Egyptian Government, 15% government net profit interest (post-tax income), 22.5% corporate tax rate, 0.5% community development contribution 2,644km2 of highly prospective tenements in the Arabian-Nubian Shield AngloGold Ashanti’s world-class exploration expertise, alongside its extensive development expertise and strong balance sheet support realisation of upside within EDX blocks 12 Promising Little Sukari discovery from limited drill testing in Nugrus: Little Sukari geologically analogous to Sukari Potential to expand footprint beyond current drilling; clear synergies with adjacent Sukari lease and plant Reported downhole results: 46m at 3.3 g/t Au from 91m 77m at 1.84 g/t Au from 44m 69m at 2.01 g/t Au from 81m Potential for significant additions across Nugrus Block No previous exploration using modern methods, with early-stage exploration now defining several prospective districts Divided into two separate exploration licenses: Nugrus (adjacent to Sukari) and Najd (potential for standalone operations)

AngloGold Ashanti An established partner in shared benefit, aligned to world-class standards SHARED VALUE Local procurement and employment are strategic drivers, creating shared benefit Focus on robust stakeholder engagement at site, regional and national level Structures in place to ensure community participation in corporate social investment projects, aligning with specific needs and government initiatives Government/state shareholding in operations in Guinea, Argentina, Mali (previously in Ghana) Responsiveness to social and economic needs during times of crisis – Ebola and Covid Strong stewards of the environment, reducing our environmental footprint and complying with relevant environmental laws and regulations through partnership Delivering AngloGold Ashanti is a member of and/or signatory to: and is committed to the 13 Source: AngloGold Ashanti company filings

highlights – a compelling strategic fit that matches our core competencies SUKARI, A WORLD CLASS TIER 1 ASSET: Long life, compelling cost profile and attractive development potential (2023A total cash costs of $970/oz1 and AISC of $1,196/oz1) STEP CHANGE IN PRODUCTION AND REDUCTION TO COST: Increases annual gold production by ~450koz2, to over 3.0Moz2 p.a., with immediate reduction to combined unit total cash costs and all-in sustaining costs ATTRACTIVE UP-FRONT SHAREHOLDER RETURNS: Accretive to FCF/share in first full year post-completion and NAV/share ADDITIONAL VALUE UPSIDE: Leveraging AngloGold Ashanti’s Full Asset Potential efficiency framework, corporate infrastructure and supply efficiencies, as well as realising upside from Sukari underground / EDX blocks BALANCE SHEET AND CAPITAL DISCIPLINE: Balance sheet strength maintained through majority (94%) equity consideration; the addition of Sukari to the portfolio provides enhanced ability to fund growth and return cash to shareholders under AngloGold Ashanti’s robust capital allocation framework COMPLEMENTARY CAPABILITIES: Leverages AngloGold Ashanti’s expertise and extensive track record operating large open pit and underground mines in Africa along with its world-class exploration expertise and integrated stakeholder engagement approach Restated per AngloGold Ashanti definition; see appendix for reconciliation of Non-GAAP financial measures 2023A, consolidated basis; excludes CdS operation 14

appendices

Doropo Overview Location Côte d’Ivoire - 480km north of Abidjan (Capital) North-eastern Bounkani region between the Comoè National Park and the border with Burkina Faso Geological Setting Tonalite-Trondhjemite-Granodiorite domain Mineral Resource and Mineral Reserve1 1.2Moz M&I Mineral Resource at average grade of 1.06g/t 0.3Moz Inferred Mineral Resource at average grade of 1.23g/t 1.9Moz of Proven and Probable Mineral Reserve at average grade of 1.44g/t Landholding 1,582km2 covering 13 gold deposits ~85% of gold deposits concentrated within 7km radius (“Main Resource Cluster”) Ownership 100% during exploration phase 90% upon grant of mining permits Site Access National road system to Bouna Town as regional hub Regional Setting 7km North of the Comoé National Park Development Stage DFS complete 16 Source: Centamin company filings Mineral Resource and Mineral Reserve presented as per 2023 Centamin annual report; reflects non-attributable (i.e. assuming 100% ownership) Centamin Mineral Resource and Mineral Reserve; Measured and Indicated (M&I) and Inferred Mineral Resource is exclusive of Mineral Reserve; the Mineral Resource exclusive of Mineral Reserve is defined as the inclusive Mineral Resource less the Mineral Reserve before dilution and other factors are applied; estimates reflect $1,500/oz for Doropo Mineral Reserve, and $2,000/oz for Mineral Resource; Centamin attributable M&I Mineral Resource is 1.1Moz, Inferred Mineral Resource is 0.3Moz and Mineral Reserve is 1.7Moz.

Doropo DFS Profile Mining & Geology 8 shallow deposits mined in open pit operation; 28Mtpa of material delivering up to 4.9Mtpa ore 4.9x LOM strip ratio Processing SAG and ball mills, followed by CIL processing Mill capacity: 5.4 Mtpa (oxide/transition ore) 4.0 Mtpa (fresh ore) 89% Gold recovery over LOM Operating Profile 167koz p.a. LOM gold production; average of 207koz p.a. over first five years Expected AISC of $1,047/oz over LOM; average of $971/oz over first five years Total upfront construction capex of $373m Infrastructure Tailings storage facility of 287 hectares; 29Mm3 capacity Full geomembrane lined, downstream construction method 90kV National Grid for power supply 55km connection from Bouna sub station Standby power with on-site diesel generators available for critical processes Source: Centamin company filings 17

ABC Overview Location Côte d’Ivoire - 550km northwest of Abidjan (Capital) Northwestern Kabadougou region; 460km west of Doropo Project Consists of three permits: Kona (most advanced), Farako Nafana, and Windou, with other permits under application Located within highly prospective landholding along the underexplored contact zone between the Archean and Birimian cratons Geological Setting Located along the main Archean‐Birimian cratonic suture zone, mineralization primarily hosted within psammite Mineral Resource1 2.2Moz of Inferred Mineral Resource at average grade of 0.9g/t Landholding 1,148km2 Ownership 100% during exploration phase 90% upon grant of mining permits Site Access Kona permit located 1.5 hour drive from Odienne Airport (~80km) Regional Setting Kona permit bounded on northern and south-western sides by protected forest zones Exploration to date has delineated a north to south trending gold-mineralised corridor - the Lolosso Gold Corridor - over a 30km strike length within the Kona permit Development Stage Exploration 18 Source: Centamin company filings Mineral Resource and Mineral Reserve presented as per 2023 Centamin annual report; reflects non-attributable (i.e. assuming 100% ownership) Centamin Mineral Resource and Mineral Reserve; Measured and Indicated (M&I) and Inferred Mineral Resource is exclusive of Mineral Reserve; the Mineral Resource exclusive of Mineral Reserve is defined as the inclusive Mineral Resource less the Mineral Reserve before dilution and other factors are applied; estimates reflect $2,000/oz for Mineral Resource; Centamin attributable Inferred Mineral Resource is 2.2Moz.

Sukari ownership and Cost recovery Structure Sukari Fiscal Regime Overview License 160km2 30-year license, with opportunity to request an extension of a further 30 years Royalty 3% NSR paid to the Egyptian government Profit Share Payments 50% of revenue net of all qualifying costs is paid to Egyptian Mineral Resource Authority (“EMRA”) Cost Recovery From EMRA Capital expenditure recovered over 3 years Taxes Sukari Gold Mines (operating company) was granted a 15-year tax exemption (no other direct or indirect taxes within Egypt) from the date of commercial production Option to apply for further 15-year extension with EMRA’s support provided there are no unresolved tax disputes and exploration activities on the mining concession have been planned and agreed 19 Source: Centamin company filings Profit share calculation (calculated bi-annually): revenue from sales of gold and associated minerals less: (i) a royalty of 3% net sales revenue (net of freight and refining costs); and (ii) costs recoverable under the Concession Agreement (comprising: (i) operating expenses; and (ii) one-third of the exploration costs and one-third of the exploitation capital costs incurred during the period (with the remainder to be recovered in the following two years)). Any remaining operating surplus (net proceeds) resulting from the above calculation is split 50:50 between PGM and EMRA and distributed as profit share. Centamin plc Pharaoh Gold Mines EMRA Sukari Gold Mines (“SGM”) 50% Operating Surplus (“Profit Share”) 100% 50% Operating Surplus (“Profit Share”) Cost Recovery Gold Sales (US$) Sukari Gold Mines 3% Royalty to Govt. CEY Funded projects ONSHORE (EGYPT) OFFSHORE Refiner

TOTAL CASH COSTS RECONCILIATION FOR THE YEAR ENDED 31 DECEMBER 2023 Source: AngloGold Ashanti and Centamin company filings The Arab Republic of Egypt (“ARE”) is entitled to a royalty of 3% of net sales revenue (revenue net of freight and refining costs) as defined from the sale of gold and associated minerals from Sukari Gold Mines (“SGM”). This royalty is calculated and recognised on receipt of the final certificate of analysis document received from the refinery. Due to its nature, this royalty is not recognised in cost of sales but rather in other operating costs. Subsidiaries are reported on a consolidated basis. Joint ventures are reported on an attributable basis. Adjusted to exclude the Córrego do Sítio (“CdS”) operation that was placed on care and maintenance in August 2023. The Non-GAAP measures of “Cash cost of production – gold produced” and “Cash cost of production per ounce produced” ($/oz), as calculated and reported by Centamin, were adjusted to be consistent with AngloGold Ashanti’s definition of “total cash costs” and “total cash costs per ounce” ($/oz). “Total cash costs” is calculated in accordance with the guidelines of the Gold Institute industry standard and industry practice and is a Non-GAAP measure. The Gold Institute, which has been incorporated into the National Mining Association, is a non-profit international association of miners, refiners, bullion suppliers and manufacturers of gold products, which developed a uniform format for reporting total cash costs on a per ounce basis. The guidance was first adopted in 1996 and revised in November 1999. “Total cash costs” is a Non-GAAP measure and, as calculated and reported by AngloGold Ashanti, include costs for all mining, processing, onsite administration costs, royalties and production taxes, as well as contributions from by-products, but exclude amortisation of tangible, intangible and right of use assets, rehabilitation costs and other non-cash costs, retrenchment costs, corporate administration, marketing and related costs, capital costs and exploration costs. “Total cash costs per ounce” ($/oz) is calculated by dividing the US dollar value of this cost metric by the ounces of gold produced. “Cash cost of production – gold produced” and “Cash cost of production per ounce produced” ($/oz), as reported by Centamin, was adjusted for royalties, by-product revenue, environmental obligation provision and movements in mining stockpiles to arrive at “Total cash costs per ounce” as calculated by AngloGold Ashanti. See the following page for Centamin reconciliation. Joint VenturesSubsidiariesAngloGold Ashanti Group TotalCórrego do SítioAngloGold Ashanti Group TotalCentamin Group 4Combined BasisTotal cash costsCost of sales372 3,541 3,913 104 3,809 597 4,406 - By product revenue(2) (102) (104) - (104) (2) (106) - Inventory change2 12 14 (2) 16 13 29 - Amortisation of tangible assets(98) (579) (677) (3) (674) (197) (871) - Amortisation of right of use assets(1) (78) (79) (3) (76) - (76) - Amortisation of intangible assets- (1) (1) - (1) - (1) - Rehabilitation and other non-cash costs2 (22) (20) (3) (17) (1) (18) - Retrenchment costs- (4) (4) - (4) - (4) Royalties not included to cost of sales 1- - - - - 27 27 Total cash costs 275 2,767 3,042 93 2,949 436 3,385 Gold produced - oz (000) 2343 2,343 2,686 42 2,644 450 3,095 Total cash costs per ounce - $/oz802 1,181 1,133 2,217 1,115 970 1,094 Adjusted to exclude Córrego do Sítio operation 320 Shown in US dollar million, except as otherwise noted

Centamin Total Cash Costs Reconciliation For The Year ended 31 December 2023 Source: Centamin company filings “Cash cost of production - gold produced” and “cash cost of production per ounce produced” ($/oz) are Non-GAAP measures used by Centamin. “Cash cost of production per ounce produced” ($/oz), as calculated and reported by Centamin, is a measure of the average cost of producing an ounce of gold, calculated by dividing the operating costs in a period by the total gold production over the same period. Operating costs represent total operating costs less sustaining administrative expenses, royalties, depreciation and amortisation. “Cash cost of production – gold produced” and “Cash cost of production per ounce produced” ($/oz), as calculated and reported by Centamin, were adjusted to be consistent with AngloGold Ashanti’s definition of “Total cash costs” and “Total cash costs per ounce” ($/oz). “Cash cost of production – gold produced”, as reported by Centamin, was adjusted for royalties, by-product revenue, environmental obligation provision and movements in mining stockpiles to arrive at “Total cash costs per ounce” as calculated by AngloGold Ashanti. The movement in inventory on ounces produced is only the net movement in mining stockpiles and ore in circuit while the movement in ounces sold is the net movement in mining stockpiles, ore in circuit and gold in safe inventory. Reported on a consolidated basis. 21 Shown in US dollar million, except as otherwise noted Cash cost of production – gold produced, as reported by Centamin 394 Royalties 27 By-product revenue (2) Environmental obligation provision (1) Movement in mining stockpiles 17 Total cash costs, as calculated by AngloGold Ashanti 436 Gold produced - oz (000)4 450 Total cash costs per ounce - $/oz 970 Reconciliation of “cash cost of production” of Centamin to “total cash costs” as per AngloGold Ashanti definition for the year ended 31 December 20231,2 Centamin “cash cost of production” as per Centamin definition

AISC RECONCILIATION FOR THE YEAR ENDED 31 DECEMBER 2023 Source: AngloGold Ashanti and Centamin company filings Subsidiaries are reported on a consolidated basis. Joint ventures are reported on an attributable basis. Adjusted to exclude the Córrego do Sítio (“CdS”) operation that was placed on care and maintenance in August 2023. Non-GAAP measures of “All-in sustaining costs” and “All-in sustaining costs per ounce” ($/oz), as calculated and reported by Centamin, were adjusted to be consistent with AngloGold Ashanti’s definition of “All-in sustaining costs” and “All-in sustaining costs per ounce” ($/oz). During 2018, the World Gold Council (“WGC”), an industry body, published a revised Guidance Note on “all-in sustaining costs” and “all-in costs” metrics, which gold mining companies can use to supplement their overall Non-GAAP disclosure. The WGC worked closely with its members to develop these Non-GAAP measures which are intended to provide further transparency into the full cost associated with producing gold. It is expected that these metrics, in particular, the “all-in sustaining cost” metrics which are provided herein, will be helpful to investors, governments, local communities and other stakeholders in understanding the economics of gold mining. “All-in sustaining costs” is a Non-GAAP measure which, as calculated and reported by AngloGold Ashanti, is an extension of the existing “total cash costs” metric and incorporates all costs related to sustaining production and in particular, recognises sustaining capital expenditures associated with developing and maintaining gold mines. In addition, this metric includes the cost associated with Corporate Office structures that support these operations, the community and environmental rehabilitation costs attendant with responsible mining and any exploration and evaluation cost associated with sustaining current operations. “All-in sustaining costs per ounce” ($/oz) is calculated by dividing the US dollar value of this cost metric by the ounces of gold sold”. “All-in sustaining costs” and “All-in sustaining costs per ounce” ($/oz) as reported by Centamin was adjusted for Net credit to provision for stock obsolescence to arrive at “All-in sustaining costs” and “All-in sustaining costs per ounce” ($/oz) as calculated by AngloGold Ashanti. See following page for Centamin reconciliation. Joint VenturesSubsidiariesAngloGold Ashanti Group TotalCórrego do SítioAngloGold Ashanti Group TotalCentamin Group 3Combined BasisAll-in sustaining costsCost of sales per segmental information372 3,541 3,913 104 3,809 597 4,406 By-product revenue(2) (102) (104) - (104) (2) (106) Royalties not included to cost of sales- - - - - 27 27 Inventory write off not included to cost of sales- - - - - 4 4 Net movement on provision for stock obsolescence not included to cost of sales- - - - - (4) (4) Realised other commodity contracts- 7 7 - 7 - 7 Amortisation of tangible, intangible and right of use assets(99) (658) (757) (6) (751) (197) (948) Adjusted for decommsioning and inventory amortisation1 (5) (4) - (4) 1 (3) Corporate administration and marketing expenditure- 94 94 - 94 33 127 Lease payment sustaining2 100 102 7 95 1 96 Expensed Sustaining exploration and study costs- 32 32 - 32 - 32 Total sustaining capital expenditure52 842 894 19 875 87 962 All-in sustaining costs326 3,851 4,177 124 4,053 546 4,599 Gold sold - oz (000) 1343 2,324 2,667 43 2,624 457 3,081 All-in sustaining costs per ounce - $/oz951 1,657 1,566 2,894 1,544 1,196 1,493 Adjusted to exclude Córrego do Sítio operation 222 Shown in US dollar million, except as otherwise noted

Centamin AISC Reconciliation For The Year ended 31 December 2023 Source: Centamin company filings “All-in sustaining costs” is a Non-GAAP measure which, as calculated and reported by Centamin, is an extension of the existing ‘cash cost’ metric and incorporates all costs related to sustaining production and in particular recognising the sustaining capital expenditure associated with developing and maintaining gold mines. In addition, this metric includes the cost associated with developing and maintaining gold mines. This metric also includes the cost associated with corporate office structures that support these operations, the community and rehabilitation costs attendant with responsible mining and any exploration and evaluation costs associated with sustaining current operations. “All-in sustaining costs per ounce” ($/oz) is arrived at by dividing the dollar value of the sum of these cost metrics, by the ounces of gold sold (as compared to using ounces produced which is used in the cash cost of production calculation). “All-in sustaining costs per ounce” as reported by Centamin was adjusted for net credit to provision for stock obsolescence to arrive at “all-in sustaining costs per ounce” as calculated by AngloGold Ashanti. Includes refinery and transport. Reported on a consolidated basis. 23 Shown in US dollar million, except as otherwise noted Reconciliation of “all-in sustaining costs” of Centamin to “all-in sustaining costs” as per AngloGold Ashanti definition for the year ended 31 December 20231,2 All-in sustaining costs, as reported by Centamin 550 Net credit to provision for stock obsolescence (4) All-in sustaining costs, as calculated by AngloGold Ashanti 546 Gold sold - oz (000)4 457 All-in sustaining costs per ounce - $/oz 1,196 Centamin “all-in sustaining costs” as per Centamin definition

FREE CASH FLOW RECONCILIATION FOR THE YEAR ENDED 31 DECEMBER 2023 Source: AngloGold Ashanti and Centamin company filings Non-GAAP measures of “Free cash flow” and “Adjusted free cash flow”, as calculated and reported by Centamin, were adjusted to be consistent with AngloGold Ashanti’s definition of “Free cash flow” and “Free cash flow attributable to ordinary shareholders”. “Free cash flow” is a Non-GAAP measure and, as calculated and reported by AngloGold Ashanti, includes cash inflow from operating activities, less cash outflow from investing activities and after finance costs, adjusted to exclude once-off acquisitions, disposals and corporate restructuring costs, and movements in restricted cash. “Adjusted free cash flow”, as reported by Centamin, was adjusted for transactions completed through specific available cash resources, interest accrued, cash element of share-based payments to arrive at “Free cash flow attributable to ordinary shareholders” as calculated by AngloGold Ashanti. See the following page for Centamin reconciliation. Assumes transaction cash consideration of $148m and interest rate on foregone cash of 5.0%. AngloGold AshantiCentamin 1Combined 2Cash 24 Shown in US dollar million, except as otherwise noted Cash generated from operations 871 356 1,227 Dividends received from joint ventures180–180Taxation refund36–36Taxation paid(116)(0)(116)Net cash inflow from operating activities9713551,326Corporate restructuring costs268–268Capital expenditure on tangible and intangible assets(1,042)(203)(1,245)Net cash from operating activities after capital expenditure and excluding corporate restructuring costs197152349Repayment of lease liabilities(94)–(94)Finance costs accrued and capitalised(132)(4)(137)Net cash flow after capital expenditure and interest(29)149118Other net cash inflow from investing activities1254124Other4–4Add backs:Cash restricted for use9–9Free cash flow as reported109153255Less: non-controlling interest dividend paid(16)(112)(128)FCF attributable to ordinary shareholders9341127Weighted average number of shares (m)4211,158504FCF per share (attributable to ordinary shareholders)$0.22$0.04$0.25

Centamin Free Cash Flow Reconciliation For The Year ended 31 December 2023 Source: Centamin company filings Adjustments made to free cash flow, for example the cost of the put options under the gold price protection programme, acquisitions and disposals of financial assets at fair value through profit or loss, which are completed through specific allocated available cash reserves. “Free cash flow” is a Non-GAAP measure and, as calculated and reported by AngloGold Ashanti, includes cash inflow from operating activities, less cash outflow from investing activities and after finance costs, adjusted to exclude once-off acquisitions, disposals and corporate restructuring costs, and movements in restricted cash. “Free cash flow” and “Adjusted free cash flow”, as reported by Centamin, were adjusted for transactions completed through specific available cash resources, interest accrued, cash element of share-based payments to arrive at “Free cash flow” and “Free cash flow attributable to ordinary shareholders” as calculated by AngloGold Ashanti. 25 Shown in US dollar million, except as otherwise noted Adjusted free cash flow, as reported by Centamin 49 Transactions completed through specific available cash resources (6) Interest accrued versus interest paid (1) Cash element of share-based payments (1) Free cash flow attributable to ordinary shareholders, as calculated by AngloGold Ashanti 41 Reconciliation of “adjusted free cash flow” of Centamin to “free cash flow attributable to ordinary shareholders” as per AngloGold Ashanti definition for the year ended 31 December 20232 Centamin “(adjusted) free cash flow” 1 as per Centamin definition

ADJUSTED NET DEBT TO ADJUSTED EBITDA RECONCILIATION FOR THE YEAR ENDED 31 DECEMBER 2023 Note: The Adjusted EBITDA and Adjusted net debt calculations included are based on the formula included in the AngloGold Ashanti Revolving Credit Facility Agreements for compliance with the debt covenant formula. Non-GAAP measure of “Adjusted EBITDA”, as calculated and reported by Centamin, was adjusted to be consistent with AngloGold Ashanti’s definition of “Adjusted EBITDA”. “Adjusted EBITDA” is a Non-GAAP measure and, as calculated and reported by AngloGold Ashanti, includes profit (loss) before taxation, amortisation of tangible, intangible and right of use assets, retrenchment costs at the operations, finance income, other gains (losses), care and maintenance costs, finance costs and unwinding of obligations, impairment and derecognition of assets, impairment of investments, profit (loss) on disposal of assets and investments, gain (loss) on unrealised non-hedge derivatives and other commodity contracts, fair value adjustments, repurchase premium and costs on settlement of issued bonds and the share of associates’ EBITDA. The Adjusted EBITDA calculation is based on the formula included in AngloGold Ashanti’s Revolving Credit Facility Agreements for compliance with the debt covenant formula. “Adjusted EBITDA”, as reported by Centamin, was adjusted for Foreign exchange (gains) losses and net loss on disposal of assets to arrive at “Adjusted EBITDA” as calculated by AngloGold Ashanti. See following page for Centamin reconciliation of “Adjusted EBITDA”. “Adjusted net debt” is a Non-GAAP measure and, as calculated and reported by AngloGold Ashanti, includes total borrowings adjusted for the unamortised portion of borrowing costs and IFRS 16 lease adjustments; less cash restricted for use and cash and cash equivalents (net of bank overdraft). The Adjusted net debt calculation is based on the formula included in AngloGold Ashanti’s Revolving Credit Facility Agreements for compliance with the debt covenant formula. Excludes impacts of transaction fees and expenses. Adjusted Net Debt as of 31 December 2023AngloGold AshantiCentamin 1Adjustments from Centamin TransactionCombined 2Borrowings - current & non-current2,239–2,239Lease liabilities - current & non-current1716177Total borrowings2,41062,416Bank overdraft9–9Less: cash and cash equivalents(964)(93)148(909)Net debt1,454(88)1481,516Less: IFRS16 lease adjustments(149)2(147)Plus: Unamortised portion of borrowing costs30–30Less: Cash restricted for use(68)–(68)Adjusted net debt1,2681481,331Adjusted EBITDA from continuing operations (12 months ended 31 December 2023)Profit before taxation63195258Plus: Financing costs and unwinding of obligations1574161Less: Interest income(127)(4)(131)Plus: Amortisation of tangible, intangible and right of use assets658197855Plus: Associate and joint ventures adjustments for amortisation, interest, taxation and other202–202Plus : Other amortisation314EBITDA9563931,349Plus: Foreign exchange (gains) losses154(6)148Plus: Realised loss on other commodity contracts7310Plus: Retrenchment and related costs19–19Plus: Profit on disposal of joint ventures–––Plus: Impairment and derecognition of assets232–232Plus: Care and maintenance costs52–52Plus: Unrealised non-hedge deivative loss (gain)9312Plus: Net (profit) loss on disposal of assets(11)9(2)Adjusted EBITDA (as defined in the AngloGold Ashanti Revolving Credit Facility Agreements)1,4204021,820Gearing ratio (Adjusted net debt to Adjusted EBITDA) 0.9x Net Cash 0.7x Total borrowings to profit before taxation 38.3x 0.0x 9.4x Maximum debt covenant ratio allowed per the AngloGold Ashanti Revolving Credit Facility 3.5x 26 Shown in US dollar million, except as otherwise noted

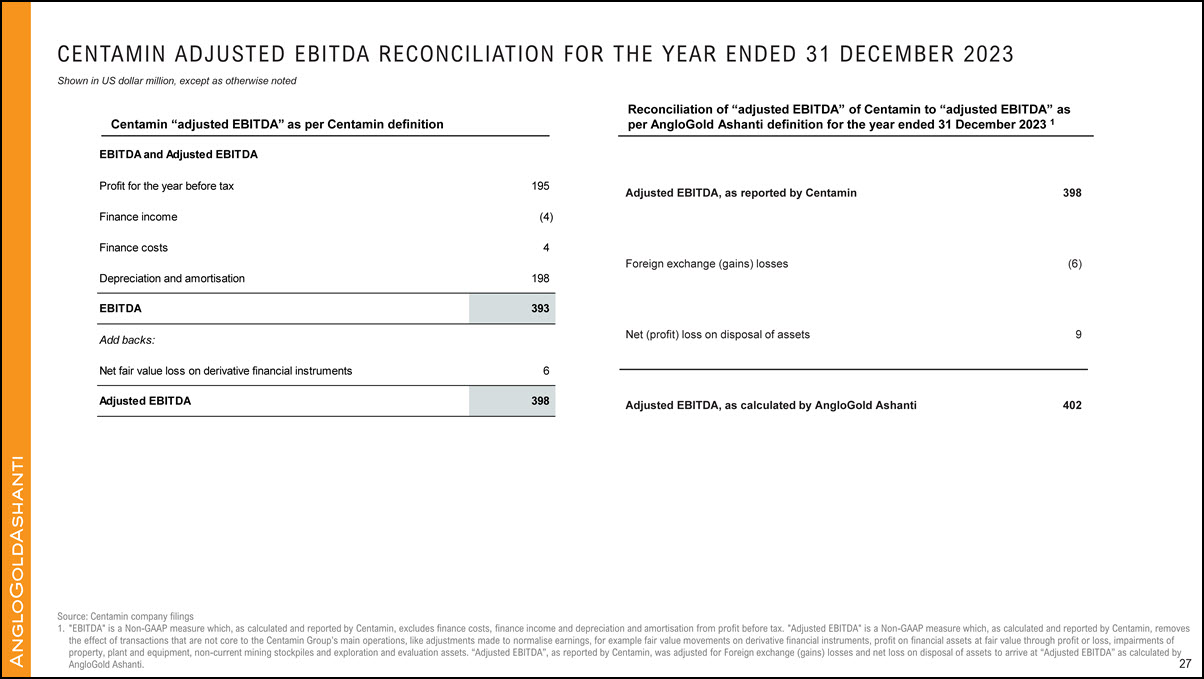

CENTAMIN ADJUSTED EBITDA RECONCILIATION FOR THE YEAR ENDED 31 DECEMBER 2023 Source: Centamin company filings "EBITDA" is a Non-GAAP measure which, as calculated and reported by Centamin, excludes finance costs, finance income and depreciation and amortisation from profit before tax. "Adjusted EBITDA" is a Non-GAAP measure which, as calculated and reported by Centamin, removes the effect of transactions that are not core to the Centamin Group’s main operations, like adjustments made to normalise earnings, for example fair value movements on derivative financial instruments, profit on financial assets at fair value through profit or loss, impairments of property, plant and equipment, non-current mining stockpiles and exploration and evaluation assets. “Adjusted EBITDA”, as reported by Centamin, was adjusted for Foreign exchange (gains) losses and net loss on disposal of assets to arrive at “Adjusted EBITDA” as calculated by AngloGold Ashanti. Adjusted EBITDA, as reported by Centamin 398 Foreign exchange (gains) losses (6) Net (profit) loss on disposal of assets 9 Adjusted EBITDA, as calculated by AngloGold Ashanti 402 EBITDA Profit for the year before tax 195 Finance income (4) Finance costs 4 Depreciation and amortisation 198 EBITDA 393 Add backs: Net fair value loss on derivative financial instruments6Adjusted EBITDA 398

ANDREA MAXEY Telephone: +61 08 9435 4603 Mobile: +61 400 072 199 amaxey@anglogoldashanti.com YATISH CHOWTHEE Telephone: +27 11 637 6273 Mobile: +27 78 364 2080 yrchowthee@anglogoldashanti.com INVESTOR RELATIONS CONTACTS GENERAL E-MAIL ENQUIRIES Investors@anglogoldashanti.com

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorised.

| AngloGold Ashanti plc | ||||

| Date: 10 September 2024 | ||||

| By: | /s/ C STEAD | |||

| Name: | C Stead | |||

| Title: | Company Secretary | |||