November 9, 2023

U.S. Securities and Exchange Commission

Division of Corporation Finance

100 F Street, N.E.

Washington, D.C. 20549

| Attention: | Aliya Ishmukhamedova | |

| Jan Woo | ||

| Ryan Rohn | ||

| Stephen Krikorian | ||

| Re: | Joint Stock Company Kaspi.kz | |

| Amendment No. 1 to the Draft Registration Statement on Form F-1 | ||

| Confidentially submitted on October 20, 2023 | ||

| CIK No. 0001985487 | ||

Ladies and Gentlemen:

This letter sets forth the responses of Joint Stock Company Kaspi.kz (the “Company”) to the comments contained in your letter, dated November 3, 2023, relating to Amendment No. 1 to the Draft Registration Statement on Form F-1, confidentially submitted by the Company on October 20, 2023 (the “Amendment No. 1”). The comments of the staff of the U.S. Securities and Exchange Commission (the “Staff”) are set forth in bold italicized text below, and the Company’s responses are set forth in plain text immediately following each comment.

The Company is submitting confidentially, via EDGAR, Amendment No. 2 to the Draft Registration Statement on Form F-1 (“Amendment No. 2”).

Capitalized terms used but not defined herein have the meanings assigned to them in Amendment No. 2.

Amendment No. 1 to the Draft Registration Statement on Form F-1

Risk Factors, page 29

| 1. | We note your response to prior comment 6 that you are not subject to the EU General Data Protection Regulation or the equivalent legislation in the United Kingdom. Please explain why you disclose that your cybersecurity systems comply with GDPR in the Business section. |

In response to the Staff’s comment, the Company respectfully advises the Staff that the Company benchmarks its cybersecurity systems and controls against international standards as a matter of best practice; this includes GDPR. Notwithstanding that, as noted in the Company’s response to prior comment 6, the Company is not itself subject to GDPR. To avoid potential confusion, the Company has removed the reference to GDPR from the disclosure.

November 9, 2023

Note 3. Significant accounting policies

Revenue recognition, page F-55

| 2. | We note your expanded disclosure in response to prior comment 18. We further note your product and services offerings on page 4. It appears that you have not provided disclosure in your revenue recognition policy for several of your offerings including Advertising, Classifieds, BNPL and Car financing. Please advise or revise accordingly. |

In response to the Staff’s comment, the Company has revised the disclosure on pages F-56 to F-58 to provide further information regarding its revenue recognition policies for all of its material product and service offerings. The Company respectfully advises the Staff that it has not included detailed information regarding its revenue recognition policies in respect of its product and service offerings that are immaterial. In particular, the Company notes that revenue generated from its Advertising and Classifieds and other immaterial offerings represented less than 10% in the aggregate of the Company’s total revenues for each of the periods presented. Included as Appendix No. 1 is a breakdown of the Company’s revenue for the years ended December 31, 2022, 2021 and 2020 and the nine months ended September 30, 2023 for the products and services set forth in the chart on page 4 of Amendment No. 2.

The Company has further revised the disclosure on pages 111-112, 116-117 and 120-121 to provide the amounts of Payments fee revenue and Marketplace fee revenue generated from the material offerings included within each revenue type for each period presented.

The Company further notes that Fintech revenue from financial assets such as consumer loan, BNPL, merchant financing and car financing constitutes interest revenue only, which is recognized using the effective interest rate method under IFRS 9. As disclosed in note 3 to the consolidated financial statements on page F-55, BNPL and car financing are recognized as financial assets.

Additionally, we note your expanded disclosures discuss fees revenue in general. Disclose how your Marketplace fees are calculated.

In response to the Staff’s comment, the Company has revised the disclosure on page F-57 to provide further information regarding the basis on which 3P Marketplace fees are calculated and has revised the disclosure on pages 112, 117 and 121 to provide the amounts of 3P Marketplace business seller fees for each period presented. The Company respectfully advises the Staff that 3P Marketplace business seller fees are the only material revenue type among various Marketplace services.

Expand your disclosures to address Steps 1 through 5 in recognizing revenue under IFRS 15. Your disclosure should disclose more specifically your recognition policy for all of your significant products and services. Refer to paragraphs 110 through 129 of IFRS 15.

In response to the Staff’s comment, the Company has revised the disclosure on pages F-56 to F-58 to provide further information on its consideration of Steps 1 through 5 in recognizing revenue under IFRS 15 in respect of its products and services that generate a material portion of its total revenue. The Company respectfully advises the Staff that in preparing the disclosure of its revenue recognition policy for its products and services, the Company has taken into consideration the financial significance of these products and services and, as such, has not included details on its revenue recognition policy to address Steps 1 through 5 under IFRS 15 for certain of its products and services that are immaterial. Included as Appendix No. 1 is a breakdown of the Company revenue for the years ended December 31, 2022, 2021 and 2020 and the nine months ended September 30, 2023 for the products and services set forth in the chart on page 4 of Amendment No. 2.

2

November 9, 2023

| 3. | We note your expanded disclosure on page F-56 in response to prior comment 22, that, “[t]he Company has determined that it is a principal to all the different services provided and described herein.” Please expand upon how you reached this conclusion. Specifically, explain how you concluded that you are the principal in transactions that include flight tickets, railway tickets, delivery services, and your 3P Marketplace as described on page 165 as well as your key services, including payments, marketplace, financial services, travel, grocery, and classifieds. Refer to paragraph 123 of IFRS 15. Expand your disclosures to explain how you made these determinations. Refer to paragraphs B34 and B34A of IFRS 15. |

In response to the Staff’s comment, the Company has revised the disclosure on pages F-57 - F-58 to describe the transactions for which it has determined that it acts as agent and the transactions for which it has determined that it acts as principal, and the principal bases for such terminations, pursuant to IFRS 15 B34 and B34A. The Company respectfully advises the Staff that in preparing such disclosure, the Company has taken into consideration the materiality of the revenue recognized for each category of products and services and, as such, has not included details on whether it acts as agent or principal in transactions involving those products and services from which the revenue recognized was immaterial, such as Kaspi Travel (flight tickets, railway tickets, holiday packages), Kaspi Delivery, e-Grocery, Advertising and Classifieds. The Company has provided, in Appendix No. 1, a breakdown of its revenue for the years ended December 31, 2022, 2021 and 2020, and the nine months ended September 30, 2023 for its products and services set forth in the chart on page 4 of Amendment No. 2.

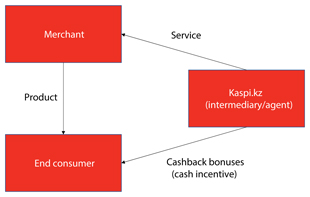

| 4. | We have reviewed your response to prior comment 23. Please explain in greater detail how you concluded that the bonuses accumulated do not represent a material right. In this regard, we note your statement in your response that the accumulated cashback bonuses under the rewards program can be spent on purchases of goods and services from third parties through the Kaspi.kz Super App. If the reward is not a material right, then clarify why a contract liability is being established. |

The Company respectfully advises the Staff that the Company provides payment processing and marketplace services to merchants who sell their products or services to retail customers (end consumers). The Company considers itself to be acting as an agent when merchants sell products or services to the end consumers. In order to increase the volume of merchants’ sales on which the Company earns Payments fee (transaction revenue) and Marketplace seller fee (fixed percentage), the Company provides incentives to end customers in the form of cashback bonuses. The merchants’ customers are also the Company’s customers as they are users of the Company’s Marketplace and Payments Platforms.

Although the Company is not obliged to provide bonuses to end customers under its agreements with merchants and the bonuses do not affect the consideration the merchants receive from sales of their products and services, the merchants are aware of the Company’s bonuses to end customers, as they are advertised on the Kaspi.kz Super App and expect to benefit from them. Further, although the Company also benefits from the bonuses through an increased use of the Marketplace and Payments Platforms, that benefit is not a product or service that is distinct from the payment processing and marketplace services provided to the merchants that benefit from the bonuses through increased sales on the Marketplace and Payments Platforms. As such, the Company concludes that the bonuses payable to end customers should be accounted for as variable consideration payable to end customers (which are incentives paid on the merchant’s behalf).

3

November 9, 2023

When the Company enters into an agreement to provide a retail customer with consideration—such as cashback bonuses—under IFRS 15.70, this consideration payable to a customer is accounted for as a reduction of the transaction price (revenue) that is earned from merchant as seller fee and payment transaction fee revenue. When the obligation for consideration is incurred (and revenue is recognized), the Company accrues a liability for the consideration payable and reduces the revenue recognized.

The Company also notes that the unused amount of cashback bonuses presented as a reward liability is not material and has amounted to less than ₸2 billion for each period presented.

General

| 5. | You disclose that prior to or concurrent with, and conditional upon, the completion of this offering, you intend to amend the terms and rename the outstanding Regulation S GDRs to make them fungible with the ADSs offered in this prospectus. Please explain how you intend to amend the terms and rename the outstanding Regulation S GDRs to make them fungible with the ADSs being offered. Explain the steps that will be taken to undertake this, including whether any action or consent of current holders of Regulation S GDRs will be required. Clarify which actions have been taken. Discuss whether the GDRs will have the same deposit agreement as the ADRs. |

In response to the Staff’s comment, the Company respectfully advises the Staff that the existing English law-governed Deposit Agreement, dated March 28, 2019, as amended (the “GDR Deposit Agreement”), between the Company and The Bank of New York Mellon, as depositary (the “Depositary”), related to the Company’s Rule 144A global depositary receipts (the “Rule 144A GDRs”) and Regulation S global depositary receipts (the “Regulation S GDRs” and, together with the Rule 144A GDRs, the “GDRs”), is proposed to be amended and restated in respect of the Regulation S GDRs (the “Amendment and Restatement”) to (i) change the name of the Regulation S GDRs to “American Depositary Shares” (the “ADSs”), (ii) change the governing law from English law to New York law, (iii) to replace the terms and conditions of the Regulation S GDRs with a customary Form of ADR, and (iv) make certain technical changes so as to have a customary form of New York law-governed deposit agreement for the ADSs (the “Level III ADS Deposit Agreement”). Following the Amendment and Restatement of the Regulation S GDRs, the ADSs will be governed by, and ADS holders, including the former Regulation S GDR holders who will hold ADSs once the Amendment and Restatement becomes effective, will be a party to the Level III ADS Deposit Agreement. Following the Amendment and Restatement, each ADS will continue to represent one common share of the Company; such common shares, which are currently deposited with and represented by the Regulation S GDRs, will remain

4

November 9, 2023

deposited with The Bank of New York Mellon and be represented by the ADSs. The Bank of New York Mellon is the depositary bank with respect to the GDRs and will remain the depositary for the ADSs. There will be no material change to the current Regulation S GDR holders’ rights following the Amendment and Restatement. For example, ADS holders will continue to be entitled to withdraw common shares represented by their ADSs and exercise rights materially the same as those they currently have as Regulation S GDR holders, such as the right to vote via the Depositary at shareholders’ meetings and receive distributions, including dividends, however these rights will be governed by the Level III ADS Deposit Agreement after the Amendment and Restatement.

The ADSs being sold in the offering by the selling shareholders are a portion of the Regulation S GDRs that will have been redesignated as ADSs and the terms of which will have been amended pursuant to the Amendment and Restatement. The Company respectfully advises the Staff that the Regulation S GDRs are not being made fungible with the ADSs being offered; rather, the Regulation S GDRs will become ADSs following the effectiveness of the Amendment and Restatement. The Company revised the disclosure to clarify this on the cover page and on pages 19, 22-23, 272 and 274.

It is proposed that the GDR Deposit Agreement will continue to apply in respect of the Rule 144A GDRs, and the Rule 144A GDRs will remain “global depositary receipts,” the terms and conditions of which will be governed by English law.

Under the terms of the GDR Deposit Agreement, the Amendment and Restatement will be effected as follows:

| 1) | The Company and the Depositary executed the Level III ADS Supplemental Agreement on October 27, 2023, which will amend and restate the GDR Deposit Agreement and the terms and conditions of Master Regulation S GDRs, effective on the Effective Date (as defined below). |

| 2) | On October 30, 2023, existing Regulation S GDR holders were given notice of the Amendment and Restatement (the “Notice”), as required under the GDR Deposit Agreement, by the Depositary (which was distributed through the clearing systems where the Regulation S GDRs currently trade and settle). Under the terms of the GDR Deposit Agreement, the Amendment and Restatement may become effective upon an at least 30 calendar-day notice to the Regulation S GDR holders. Regulation S GDR holders continue to have the right provided in the GDR Deposit Agreement to withdraw the common shares represented by their Regulation S GDRs if they do not wish to hold their GDRs as ADSs on the amended terms pursuant to the Amendment and Restatement as provided in the Notice; they will continue to have the right to withdraw the underlying common shares following effectiveness of the Amendment and Restatement under the terms of the Level III ADS Agreement. Regulation S GDR holders did not, and will not, vote on or consent to the Amendment and Restatement; such a vote is not required under the terms and conditions of the GDRs or the GDR Deposit Agreement. |

| 3) | The Amendment and Restatement will become effective on the first date on which both: (i) the registration statement on Form F-6 with respect to the ADSs (the “Form F-6”) has been declared effective by the SEC (to which, as required, the executed Level III ADS Deposit Agreement will be an exhibit); and (ii) the Company has confirmed to the Depositary in writing that the Amendment and Restatement has become effective, which shall be a date at least 30 calendar days from the date of the Notice. |

5

November 9, 2023

| 4) | Upon effectiveness of the Form F-6 and the Amendment and Restatement, the ADSs are expected to bear the same CUSIP and ISIN numbers as applied to the Regulation S GDRs, as they represent a continuation of the same security. The Regulation S GDRs currently trade and settle in Euroclear Bank S.A./N.V. and Clearstream Banking, société anonyme and those clearing systems are their primary place of issuance. Following the Amendment and Restatement, the Depositary will take the necessary steps so that the primary place of issuance for the ADSs will be The Depository Trust Company. No action, however, is required to be taken by Regulation S GDR holders, as they will hold the ADSs through the same clearing systems as they currently do once the Amendment and Restatement becomes effective. |

| 6. | Please clarify or explain if you intend to register the shares underlying the GDRs on a Form F-6. Also clarify whether you are intending to register the shares underlying the GDRs as part of this registration statement. |

In response to the Staff’s comment, the Company respectfully advises the Staff that the ADSs will be registered on a Form F-6, which will be filed by the Depositary prior to the commencement of the offering and will be requested to be declared effective on the same date as the registration statement on Form F-1 (“Form F-1”). The Company does not intend to register the common shares underlying ADSs, other than the common shares to be registered on the Form F-1 that underlie the ADSs to be offered and sold in the offering.

| 7. | With a view toward disclosure, explain why the Rule 144A GDRs are not being made fungible along with the Regulation S GDRs. |

In response to the Staff’s comment, the Company respectfully advises the Staff that the Rule 144A GDRs are not being made fungible with the ADSs because it believes that at least a portion of the Rule 144A GDRs are “restricted securities” within the meaning of Rule 144(a)(3) under the U.S. Securities Act of 1933, as amended (“restricted securities”). Under the terms of the GDR Deposit Agreement, the common shares underlying the Rule 144A GDRs are able to be withdrawn and deposited into the ADS facility only if such Rule 144A GDRs held by the withdrawing Rule 144A GDR holder and the underlying common shares are not “restricted securities” and a certificate to this effect is provided by the withdrawing Rule 144A GDR holder to the Depositary, and none of the common shares represented by the Rule 144A GDRs are “restricted securities.” The Company notes that there are 2,811,304 Rule 144A GDRs outstanding, representing less than 1.5% of its total outstanding common shares as of September 30, 2023.

| 8. | You state that the ADSs will trade on Nasdaq, the LSE, the KASE, and the AIX. Please clarify how you plan to have American Depository Shares trade on foreign exchanges. |

In response to the Staff’s comment, the Company respectfully advises the Staff that the ADSs are expected to have the same CUSIP and ISIN numbers as the existing Regulation S GDRs, which are already listed on the LSE, the KASE and the AIX. In addition, as discussed in response to comment 5 above, the ADSs are a continuation of the same security as the existing Regulation S GDRs and represent the same type and number of underlying securities as the existing Regulation S GDRs (i.e., one common share of the Company). As a result, the ADSs will remain listed on the LSE, the KASE and the AIX, subject to administrative notifications to be provided to each exchange. The Company notes that no prospectus or listing application is expected to be required or will be made for the continued listing or trading of the ADSs on any of the exchanges on which the Regulation S GDRs are currently listed and traded.

* * * * *

6

November 9, 2023

If you have questions concerning this letter or submission, or require any additional information, please do not hesitate to contact me at +44 20 7786 9140 or by email (nppellicani@debevoise.com).

Very truly yours,

/s/ Nicholas P. Pellicani

Nicholas P. Pellicani

| cc: | Mikheil Lomtadze, Chief Executive Officer, Joint Stock Company Kaspi.kz |

Tengiz Mosidze, Chief Financial Officer, Joint Stock Company Kaspi.kz

James C. Scoville, Debevoise & Plimpton LLP

Alan Kartashkin, Debevoise & Plimpton LLP

Darina Kogan-Bellamy, White & Case LLP

Bree Peterson, White & Case LLP

7

Appendix No. 1

| Segment | Product/Service | Revenue Type | For the year ended December 31, | For the nine months ended September 30, | ||||||||||||||||

| (in ₸ million, except percentages) | 2020 | 2021 | 2022 | 2023 | ||||||||||||||||

| Marketplace | e-Grocery* | Retail revenue | — | — | — | 37,133 | ||||||||||||||

| 3P marketplace business | Marketplace Fee revenue | 63,083 | 145,062 | 217,631 | 215,820 | |||||||||||||||

| Delivery* | — | 2,921 | 8,561 | 12,656 | ||||||||||||||||

| Travel*1 | — | 2,634 | 8,873 | 11,089 | ||||||||||||||||

| Advertising* | 113 | 1,125 | 1,819 | 3,914 | ||||||||||||||||

| Classifieds* | Other gains | 2,781 | 1,862 | 2,725 | 2,954 | |||||||||||||||

| Payments | Mobile wallet2 | Transaction revenue

Membership revenue*3

Interest revenue4 |

| 83,716

4,631

32,576 |

|

| 156,738

9,711

50,636 |

|

| 243,630

13,120

76,593 |

|

| 247,279

13,509

78,226 |

| ||||||

| Debit card | ||||||||||||||||||||

| QR code payments | ||||||||||||||||||||

| P2P payments | ||||||||||||||||||||

| Proprietary payment network5 | ||||||||||||||||||||

| Bill payments | ||||||||||||||||||||

| B2B payments | ||||||||||||||||||||

| Fintech | Saving accounts6 |

Membership revenue*7

Interest revenue |

|

6,574

290,337 |

|

|

9,452

371,439 |

|

|

4,568

500,256 |

|

|

2,375

524,378 |

| ||||||

| Consumer loan | ||||||||||||||||||||

| BNPL | ||||||||||||||||||||

| Merchant financing | ||||||||||||||||||||

| Car financing | ||||||||||||||||||||

| Banking services8 | Fintech Banking service fees | 165,450 | 191,831 | 226,540 | 203,519 | |||||||||||||||

| Treasury and foreign exchange currency operations9 |

Other gains/(losses) |

|

(7,824) |

|

|

(6,608) |

|

|

13,659 |

|

|

17,719 |

| |||||||

| Rewards | (38,568) | (51,981) | (44,960) | (27,875) | ||||||||||||||||

| Intergroup | — | — | (2,423) | — | ||||||||||||||||

Total revenue | 602,869 | 884,822 | 1,270,592 | 1,342,697 | ||||||||||||||||

* Immaterial revenue types in aggregate to total revenue | 2.3 | % | 3.1 | % | 3.1 | % | 6.2 | % | ||||||||||||

| 1 | Includes flight tickets, railway tickets and holiday packages. |

| 2 | Mobile wallet is a service that does not generate revenue itself but rather provides instant access to different payment options through the Kaspi.kz Super App to the Company’s Payments customers. |

| 3 | Payments membership fees are paid on a monthly basis or upfront at the beginning of the applicable membership period by customers and merchants for accessing various Payments services of the Company. |

| 4 | Payments interest revenue is generated from investments in debt securities, funded by current accounts of the Company’s Payments customers. |

| 5 | Proprietary payment network provides access to the Company’s merchants and enables accepting by the Company’s merchants of QR and online payments made by the Company’s Payments customers. |

| 6 | Saving accounts is a service that enables the Company’s Fintech customers to save money with the Company and earn interest. It is, therefore, not a revenue-related service. |

| 7 | Fintech membership fees are paid to access Kaspi Red. |

| 8 | Banking services are not included on page 4 of Amendment No. 2 as this is a set of customary services described in note 3 to the financial statements to which Fintech consumers have access by paying banking service fees. |

| 9 | Treasury and foreign exchange currency operations are not included on page 4 of Amendment No. 2 as these are customary treasury operation of the Company, including liquidity and foreign currency management not related to customer services. |