Management continues evaluating strategies to obtain the required additional funding necessary for future operations, to comply with all covenants as required by the loan agreements, and to be able to discharge the outstanding debt and other liabilities as they become due. In assessing these strategies, management has considered the available cash resources, inflows from the hotels that are already in operation, and future financing options available to the Murano Group such as new or restructured loan agreements and the possible financial support of the major shareholder of the Murano Group. However, Murano Group may be unable to access further equity or debt financing when needed. As such, there can be no assurance that the Murano Group will be able to obtain additional liquidity when needed or under acceptable terms, if at all.

The Murano Group Combined Financial Statements do not include any adjustments that might be necessary should the Murano Group be unable to continue as a going concern. If the going concern basis were not appropriate for these financial statements, adjustments would be necessary in the carrying value of assets and liabilities, the reported expenses and the combined statement of financial position classifications used.

We have substantial debt that may be called on demand of lender due to breach in covenants that may happen in the future.

In relation to the GIC I Loan, a covenant breach with respect to the funding of the debt service reserve account was waived by the lenders on December 29, 2023. A further waiver was received from the lenders on March 19, 2024 to fund the debt service reserve account at a later date.

In accordance with the Insurgentes Loan, we must maintain two debt service reserve accounts. As of December 31, 2023 one debt service reserve account was fully funded, while the other was not. On April 4, 2024, the borrower and joint obligors under the Insurgentes Loan obtained an event of default waiver from Bancomext, as lender, in connection with the funding obligations of the debt service reserve accounts. As a result of such waiver, on April 4, 2024 the parties thereto executed an amendment agreement to the Insurgentes Loan to provide for the new terms and conditions with respect to the funding obligations of the debt service reserve accounts. Therefore, as of this date such event of default under the Insurgentes Loan has been waived by the lender thereto. Also see, “ – The instruments governing our indebtedness contain cross-default provisions that may cause all of the debt issued under such instruments to become immediately due and payable as a result of a default under an unrelated debt instrument” for discussions of certain defaults that have been waived, and potential consequences, with respect to our debt.

Subsequent phases to our existing projects and potential enhancements at our hotel properties will likely require us to raise additional capital.

We will likely need to access the capital markets or otherwise obtain additional funds to complete subsequent phases of our existing projects, and to fund potential enhancements we may undertake at our facilities there, and elsewhere. We do not know when or if the capital markets will permit us to raise additional funds for such phases and enhancements in a timely manner, on acceptable terms, or at all. Inability to access the capital markets, or the availability of capital only on less-than-favorable terms, may force us to delay, reduce or cancel our subsequent phases and enhancement projects. Delay, reduction or cancellation of the subsequent phases of our projects could subject us to financial penalties, and the possibility of such penalties could require us to obtain additional financing on unfavorable terms.

We may not be able to generate sufficient cash to service all our indebtedness and may be forced to take other actions to satisfy our obligations under such indebtedness, which may not be successful.

Our ability to make scheduled payments on or refinance our debt obligations depends on our financial condition and operating performance, which are subject to prevailing economic and competitive conditions and to certain financial, business, legislative, regulatory and other factors beyond our control. We may be unable to maintain a level of cash flows from operating activities sufficient to pay the principal, premium, if any, and interest on our indebtedness.

If our cash flows and capital resources are insufficient to fund our debt service obligations, we could face substantial liquidity problems and could be forced to reduce or delay investments and capital expenditures or to dispose of material assets or operations, seek additional debt or equity capital or restructure or refinance our indebtedness. We may not be able to effect any such alternative measures, if necessary, on commercially reasonable terms or at all and, even if successful, those alternatives may not allow us to meet our scheduled debt service obligations.

Our inability to generate sufficient cash flows to satisfy our debt obligations, or to refinance our indebtedness on commercially reasonable terms or at all, would materially and adversely affect our financial position and results of operations.

If we cannot make scheduled payments on our debt, we will be in default and our creditors could declare outstanding principal and interest to be due and payable, causing a cross-acceleration or cross-default under certain of our debt agreements, and we could be forced into bankruptcy, liquidation or restructuring proceedings. All of these events could result in your losing your investment in our shares or your investment being impaired.

The instruments governing our indebtedness contain cross-default provisions that may cause all of the debt issued under such instruments to become immediately due and payable as a result of a default under an unrelated debt instrument.

Instruments governing our existing indebtedness contain, and the instruments governing indebtedness we may incur in the future may contain, certain affirmative and negative covenants and require us and our subsidiaries to meet certain financial ratios and tests. Our failure to comply with the obligations contained in these instruments could result in the event of default under the applicable instrument, which could then result in the related debt and the debt issued under other instruments becoming immediately due and payable. In such an event, we would need to raise funds from alternative sources, which may not be available to us on favorable terms, on a timely basis, or at all. Alternatively, such default could require us to sell our assets and otherwise curtail operations in order to pay our creditors. Also see, “ – We have substantial debt that may be called on demand of lender due to breach in covenants that may happen in the future” for discussion of certain defaults that have been waived, and potential consequences, with respect to our debt.”

We will be dependent on the operation and business of our hotel properties for substantially all of our revenue. The failure of our hotel operators to fulfill their obligations under the management agreements may have an adverse effect on our business, financial condition, and results of operations.

We will generate indirectly substantially all of our revenues from the hotel management agreements. Our performance depends on the performance of the hotel operators, as well as their ability to pay for certain items related to our properties, such as renovation and maintenance expenses related to furniture fixes and other equipment and operating supplies and equipment, insurance, marketing and promotional expenses and costs, among others. We cannot assure you that our properties will generate sufficient revenues, assets, and liquidity to satisfy these obligations or the payment obligations under the hotel management agreements.

We will rely solely on the income and cash flows from the investments made in the properties. Defaults by our hotel operators under the hotel management agreements could materially and adversely affect our business, financial condition, and results of operations.

We will not control the operation of the properties. Our cash flows depend on the proper performance of our hotel operators, and if they fail to operate our properties efficiently, we could have a material adverse effect on our business, financial condition, and results of operations.

We are not in a position to directly implement strategic business decisions regarding the day-to-day operation of our hotel properties, such as setting room rates, food and beverage prices, marketing activities, promotion, and other similar matters, and we will be dependent on our hotel operators to carry out the operation of our hotel properties. Although we have structured and will aim to structure our hotel management agreements so that we have significant visibility with respect to the operation of our hotel properties, and such agreements impose certain performance goals on the hotel operators, we cannot assure that the hotel operators will be able to successfully operate our hotel properties, and if they fail to do so, it could have a material adverse effect on our business, financial condition and results of operations.

If the hotel operators consolidate through merger and/or acquisition transactions, we may experience undefined and unknown costs related to integrating processes and systems, which may adversely affect our hotel properties. If third-party online travel agencies consolidate through merger and/or acquisition transactions, this may lead to less negotiating power over contracts and/or higher costs of obtaining customers.

The hotel operators consolidating with third parties through mergers and/or acquisitions could adversely affect our hotel properties due to the undefined and unknown costs associated with the integration of property-level point of sale and back-of-house computer systems and other technology-related processes, the training and other labor costs associated with the merging of labor forces, and the impact of reward point program consolidation. Additionally, the potential consolidation could impact our leveraging power in future management agreement negotiations. Consolidation of third-party online travel agencies (“OTAs”) could lead to less negotiating power that the hotel operators have in setting contract terms for pricing and commissions paid to OTAs. The consolidation of these distribution channels may reduce operating profits and/or higher costs of obtaining customers.

Delays in receiving refunds of value added tax paid in connection with our acquisition and construction of hotels could have a material adverse effect on our cash flow and results of operations.

We are required to pay value added tax (“VAT”) in connection with the acquisition and construction of our hotels pursuant to the Mexican Value Added Tax Law (Ley del Impuesto al Valor Agregado), which under certain circumstances will result in favorable balances. To the extent the applicable requirements are fulfilled, the competent tax authorities should refund to us such favorable balances within 40 business days following the filing of the request for refund with such authorities, in accordance with the provisions of Article 22 of the Mexican Federal Tax Code (Código Fiscal de la Federación). To the extent that we pay a substantial amount of VAT in connection with acquisitions and experience delays in receiving the corresponding refunds, our cash flow and results of operations could be materially and adversely affected.

We may be subject to adverse legislative or regulatory tax changes that could affect our operations.

At any time, the U.S. federal, state or local, Mexican federal or local, or other non-U.S. tax laws or regulations or the judicial or administrative interpretations of those laws or regulations or the policies of the taxing agency or authority may be changed. We cannot predict when or if any new U.S. federal, state or local, Mexican federal or local, or other non-U.S. tax law, regulation or judicial interpretation will be adopted, promulgated, or may become effective, and any such law, regulation or interpretation may take effect retroactively. In particular, the Mexican government has anticipated that a tax reform is to be presented to the Mexican Congress for discussion and thus could potentially be enacted in the near future. Any such change in, or any new, tax law, regulation or administrative or judicial interpretation could adversely affect us and holders of our shares. There is no assurance that such reform or any other reform will not be enacted in the future. In addition, there can be no assurance that new tax laws, regulations, and interpretations or changes in existing tax laws, regulations, and interpretations would not have a material adverse effect on our business, prospects, results of operations, and financial condition. The effects of such changes have not been, and cannot be, quantified.

We and our hotel operators may be subject to audits by the tax authorities.

Pursuant to Mexican tax provisions, we and our hotel operators (as any taxpayers) may be subject to the exercise of the powers of the tax authorities to verify their level of compliance with the applicable tax provisions. We cannot guarantee that such powers will not be exercised or, if applicable, that they will be favorably resolved. Therefore, in the event that the tax authorities determine that we or our hotel operators are not in compliance with tax obligations, such authorities could impose, collect and enforce tax assessments, fines and/or guarantees, which, if material, could adversely affect our financial condition and results of operations.

We may not be able to deliver projects on time and within our estimated budget.

The budget estimated for the construction and development of our projects under completion is based on construction costs incurred to date, architectural and design documents and is subject to change as the construction progresses and as contract packages are let into the marketplace. Major projects of the scope and scale undertaken by us are subject to significant development, construction and timing risks, including the following:

| • | changes to, or mistakes in, project plans and specifications, some of which may require the approval of state and local regulatory agencies; |

| • | engineering problems, including defective plans and specifications; |

| • | shortages of, and price increases in, energy, materials, and skilled and unskilled labor, and inflation in key supply markets; |

| • | delays in delivery of materials or furniture, fixtures or equipment; |

| • | changes to, or mistakes in budgeting; |

| • | the financial health of our contractor and subcontractors; |

| • | changes in laws and regulations, or the interpretation and enforcement of laws and regulations, applicable to real estate development or construction projects; |

| • | the financial health of our contractor and subcontractors; |

| • | changes in laws and regulations, or the interpretation and enforcement of laws and regulations, applicable to real estate development or construction projects; |

| • | labor disputes or other work delays or stoppages, including needing to redo work; |

| • | disputes with and defaults by contractors, subcontractors, consultants and suppliers; |

| • | site conditions differing from those anticipated; |

| • | environmental issues, including the discovery of unknown environmental contamination; |

| • | health and safety incidents and site accidents; |

| • | weather interferences or delays; |

| • | fires and other natural or human-made disasters; and |

| • | other unanticipated circumstances or cost increases. |

The development costs of our future projects are estimates only, actual development costs may be higher than expected and we may not have access to additional capital to fund our property development projects and/or otherwise fulfill our business strategy.

Our plans and specifications for the development of our future projects are not complete and may be subject to change. At this time, they are also subject to approval by government authorities. Our current budget is based on our preliminary plans, which are subject to change. We currently expect the total development and construction costs of the projects to be on preliminary estimate in the order of U.S.$620.0 million. While we believe that our overall budget for the construction costs for these properties is reasonable, a significant portion of these construction costs are only initial estimates, and the actual construction costs may be significantly higher than expected. We currently expect that existing cash resources together with borrowings under our existing financings, will not be sufficient to fund the currently foreseeable construction budget of our development projects and/or otherwise be sufficient to fulfill our business strategy. Therefore, we will likely need additional capital in the future. Our ability to obtain bank financing or to access the capital markets for future debt or equity offerings may be limited by our financial condition, results of operations or other factors, such as our credit rating or outlook at the time of any such financing or offering and the covenants in our existing debt agreements, as well as by general economic conditions and contingencies and uncertainties that are beyond our control. Therefore, we cannot assure you that we will be able to obtain additional capital and/or that we will be able to obtain bank financing or access the capital markets on commercially reasonable terms or at all.

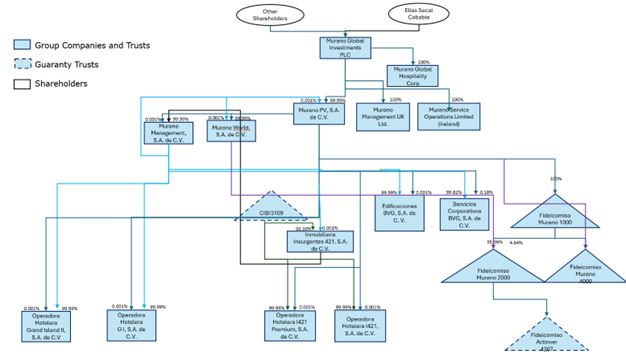

There are potential conflicts of interest in respect of the Insurgentes 421 Hotel Complex lease agreement and the GIC I Hotel lease agreement.

Inmobiliaria Insurgentes 421, the lessor under the Insurgentes 421 Hotel Complex lease agreements is our affiliate. As a result, the Insurgentes 421 lease agreements were negotiated between related parties. Their terms, including consideration payable thereunder, may be less favorable to us than terms negotiated with unaffiliated and third-party lessees. Additionally, conflicts of interest may arise between Inmobiliaria Insurgentes 421 and us in many areas relating to our ongoing relationships. We cannot guarantee that any potential conflict of interest that could arise from transactions with Inmobiliaria Insurgentes 421 will be resolved advantageously for us.

In addition GIC I Trust, the lessor under the GIC I Hotel lease agreement, is our affiliate. As a result, the GIC I Hotel lease agreement was negotiated between related parties. Its terms, including consideration payable thereunder, may be less favorable to us than terms negotiated with unaffiliated and third-party lessees. Additionally, conflicts of interest may arise between GIC I Trust and us in many areas relating to our ongoing relationships. We cannot guarantee that any potential conflict of interest that could arise from transaction with GIC I Trust will be resolved advantageously for us.

We execute transactions with related parties that third parties could deem not to be arms’ length.

In the ordinary course of our business, we execute various transactions with companies owned or controlled directly or indirectly by us and by our and affiliates. We have policies in place that we are required to follow to ensure that transactions with affiliates are entered into on terms that are at least as favorable to us as those that would be obtainable at the time for a comparable transaction or series of similar transactions in arm’s-length dealings with an unrelated third person. In addition, we do undertake a transfer pricing analysis in accordance with Mexican tax regulations to help ensure that the price paid in any such transaction is fair to us and our affiliated counterparty. We intend to continue to enter into transactions with our subsidiaries and affiliates in the future in conformity with applicable laws. Entering into these types of transactions could cause conflicts of interest to arise. We cannot guarantee that any potential conflict of interest that could arise as a result of transactions with related parties will be resolved advantageously for us. In the event that such conflicts are resolved less advantageously for us, they could adversely affect our business, financial condition and results of operations.

We are subject to risks associated with the concentration of our hotel portfolio in the Hyatt and Accor family of brands. Any deterioration in the quality or reputation of the Hyatt or Accor brands could have an adverse effect on our reputation, business, financial condition, or results of operations.

Our properties currently utilize or are expected to utilize brands owned by Hyatt and Accor. As a result, our ability to attract and retain guests depends, in part, on the public recognition of these brands and their associated reputation. Changes in ownership or management practices, the occurrence of accidents or injuries, force majeure events, crime, individual guest notoriety or similar events at our hotels or other properties managed, owned, or leased by these brands can harm our reputation, create adverse publicity, subject us to legal claims and cause a loss of consumer confidence in our business. If the Hyatt or Accor brands become obsolete or consumers view them as unfashionable or lacking in consistency and quality, we may be unable to attract guests to our hotels, which could adversely affect our business, financial condition, or results of operations. In addition, any adverse developments in Hyatt’s or Accor’s business and affairs, reputation or financial condition could impair its ability to manage our properties and could have a material adverse effect on us.

Contractual and other disagreements with or involving our current and future third-party hotel managers could make us liable to them or result in litigation costs or other expenses.

Our management agreements require us and our managers to comply with operational and performance conditions that are subject to interpretation and could result in disagreements, and we expect this will be true of any management agreements that we enter into with future third-party hotel managers or operators. We cannot predict the outcome of any arbitration or litigation related to such agreements, the effect of any negative judgment against us or the amount of any settlement that we may enter into with any third-party. In the event we terminate a management agreement early and the hotel manager considers such termination to have been wrongful, they may seek damages. Additionally, we may be required to indemnify our third-party hotel managers and affiliates against disputes with third parties pursuant to our management agreements. An adverse result in any of these proceedings could materially and adversely affect our revenues and profitability.

We are dependent on the performance of our managers and could be materially and adversely affected if our managers do not properly manage our hotels or otherwise act in our best interests or if we are unable to maintain a good relationship with our third-party hotel managers.

Our Insurgentes 421 Hotel Complex in Mexico City is managed by Hyatt and Accor pursuant to separate hotel management agreements that expire on December 31, 2043. Once the development of the GIC Complex in Cancun is completed, it is expected to be managed by Hyatt pursuant to management agreements that will expire on December 31, 2038. We could be materially and adversely affected if any third-party hotel manager fails to provide quality services and amenities, fails to maintain a quality brand name or otherwise fails to manage our hotels in our best interest, and could be held financially responsible for the actions and inactions of our third-party hotel managers pursuant to our management agreements. In addition, our third-party hotel managers manage, and in some cases may own or lease, or may have invested in or may have provided credit support or operating guarantees to hotels that compete with our hotels, any of which could result in conflicts of interest. As a result, third-party managers may make decisions regarding competing lodging facilities that are not in our best interests.

The success of our properties largely depends on our ability to establish and maintain good relationships with third-party hotel managers. If we are unable to maintain good relationships with our third-party hotel managers, we may be unable to renew existing management agreements or expand relationships with them. Additionally, opportunities for developing new relationships with additional third-party managers may be adversely affected. This, in turn, could have an adverse effect on our results of operations and our ability to execute our growth strategy. In the event that we terminate any of our management agreements, we can provide no assurances that we could find a replacement hotel manager or that any replacement hotel manager will be successful in operating our hotels. If any of the foregoing were to occur, it could materially and adversely affect us.

Cyber threats and the risk of data breaches or disruptions of our hotel managers’ or our own information technology systems could materially adversely affect our business.

Our hotel managers are dependent on information technology networks and systems, including the internet, to access, process, transmit and store proprietary and customer information, including personally identifiable information of hotel guests, including credit card numbers.

These information networks and systems can be vulnerable to threats such as system, network, or internet failures; computer hacking or business disruption, including through network- and email-based attacks as well as social engineering; cyber-terrorism; cyber extortion; viruses, worms or other malicious software programs; and employee error, negligence or fraud. The risk of a security breach or disruption, particularly through cyber-attack or cyber intrusion, including by computer hackers, nation-state affiliated actors and cyber terrorists, has generally increased as the number, intensity and sophistication of attempted attacks and intrusions from around the world have increased. We rely on our hotel managers to protect proprietary and customer information from these threats. Any compromise of our own network or hotel managers’ networks could result in a disruption to our booking or sales systems or other operations, in increased costs (e.g., related to response, investigation, and notification) or in potential litigation and liability. In addition, public disclosure or loss of customer or proprietary information could result in damage to the hotel manager’s reputation, a loss of confidence among hotel guests, reputational harm for our hotels, potential litigation and increased regulatory oversight, including governmental investigations, enforcement actions, and regulatory fines, any of which may have a material adverse effect on our business, financial condition, and results of operations. In the conduct of our business, we rely on relationships with third parties, including cloud data storage and other information technology service providers, suppliers, distributors, contractors, and other external business partners, for certain functions or for services in support of key portions of our operations. These third-party entities are subject to similar risks as we are relating to cybersecurity, privacy violations, business interruption, and systems and employee failures and an attack against such third-party service provider or partner could have a material adverse effect on our business.

In addition to the information technologies and systems our hotel managers use to operate our hotels, we have our own corporate technologies and systems that are used to access, store, transmit, and manage or support a variety of business processes and employee personally identifiable information. We may be required to expend significant attention and financial resources to protect these technologies and systems against physical or cybersecurity incidents and even then, our security measures may subsequently be deemed to have been inadequate by regulators or courts given the lack of prescriptive measures in data security and cybersecurity laws. There can be no assurance that the security measures we have taken to protect the contents of these systems will prevent failures, inadequacies, or interruptions in system services or that system security will not be compromised through system or user error, physical or electronic break-ins, computer viruses, or attacks by hackers. Any such compromise could have a material adverse effect on our business, our financial reporting and compliance, and could subject us to or result in liability claims, litigation, monetary losses or regulatory oversight, investigations or penalties which could be significant. In addition, the cost and operational consequences of responding to cybersecurity incidents and implementing remediation measures could be significant.

Like many corporations, our information networks and systems are a target of attacks. In addition, third-party providers of data hosting or cloud services may experience cybersecurity incidents that may involve data we share with them. Although the incidents that we have experienced to date have not had a material effect on our business, financial condition or results of operations, such incidents could have a material adverse effect on us in the future.

While we are in the process of obtaining cybersecurity insurance, there are no assurances that the coverage would be adequate in relation to any incurred losses. Moreover, as cyberattacks increase in frequency and magnitude, we may be unable to obtain cybersecurity insurance in amounts and on terms we view as adequate for our operations.

In addition, increased regulation of data collection, use and retention practices, including self-regulation and industry standards, changes in existing laws and regulations, enactment of new laws and regulations, increased enforcement activity, and changes in interpretation of laws, could increase our cost of compliance and operation, limit our ability to grow our business or otherwise harm us.

Costs associated with, or failure to maintain, brand operating standards may materially and adversely affect our results of operations and profitability.

The terms of our management agreements generally require us to meet specified operating standards and other terms and conditions, and compliance with such standards may be costly. Failure by us, or any hotel management company that we engage, to maintain these standards or other terms and conditions could result in a franchise license being cancelled or the franchisor requiring us to undertake a costly property improvement program. If an agreement is terminated due to our failure to make required improvements or to otherwise comply with its terms, we also may be liable to the counterparty for a termination payment, which could materially and adversely affect our results of operations and profitability.

If we were to lose a brand license, the underlying value of a particular hotel could decline significantly (including from the loss of brand name recognition, marketing support, guest loyalty programs, brand manager or franchisor central reservation systems or other systems), which could require us to recognize an impairment on the hotel. Furthermore, the loss of a franchise license at a particular hotel could harm our relationship with the franchisor or brand manager and cause us to incur significant costs to obtain a new franchise license or brand management agreement for the particular hotel. Accordingly, if we lose one or more franchise licenses or brand management agreements, it could materially and adversely affect our results of operations and profitability as well as limit or slow our future growth.

Our efforts to develop, redevelop or renovate our properties, in connection with our active asset management strategy, could be delayed or become more expensive, which could reduce revenues or impair our ability to compete effectively.

If not maintained, the condition of certain of our properties could negatively affect our ability to attract guests or result in higher operating and capital costs. These factors could reduce revenues or profits from these properties. There can be no assurance that our planned replacements and repairs will occur, or even if completed, will result in improved performance. In addition, these efforts are subject to a number of risks, including the following: construction delays or cost overruns; delays in obtaining, or failure to obtain, zoning, occupancy and other required permits or authorizations; government restrictions on the size or kind of development; changes in economic conditions that may result in weakened or lack of demand for improvements that we make or negative project returns; and lack of availability of rooms or meeting spaces for revenue-generating activities during construction, modernization or renovation projects. If our properties are not updated to meet guest preferences or brand standards under our management and franchise agreements, if properties under development or renovation are delayed in opening as scheduled, or if renovation investments adversely affect or fail to improve performance, our operations and financial results could be negatively affected.

Our properties are geographically concentrated in Mexico City, Cancun and Ensenada and, accordingly, we could be disproportionately harmed by adverse changes to these markets, natural disasters, climate change and related regulations.

Our existing and projected entire room count is concentrated in Mexico City and Cancun. This concentration exposes us to greater risk to local economic or business conditions, changes in hotel supply in these markets, and other conditions than more geographically diversified hotel companies. An economic downturn, an increase in hotel supply, a force majeure event, a natural disaster, changing weather patterns and other physical effects of climate change (including supply chain disruptions), a terrorist attack or similar event in any one of these markets likely would cause a decline in the hotel market and adversely affect occupancy rates, the financial performance of our hotels in these markets and our overall results of operations, which could be material, and could significantly increase our costs.

Over time, our hotel properties located in coastal markets, and other areas that may be impacted by climate change are expected to experience increases in storm intensity and rising sea-levels causing damage to our hotel properties, while hotels in other markets may experience prolonged variations in temperature or precipitation that may limit access to the water needed to operate our hotel properties, increasing operating costs at our hotels, such as the cost of water or energy, and requiring us to expend funds as we seek to repair and protect our hotels against such risks. The effects of climate change may also affect our business by increasing the cost of (or making unavailable) property insurance on terms we find acceptable in areas most vulnerable to such events. There can be no assurance that climate change will not have a material adverse effect on our hotels, operations, or business.

If the insurance that we carry does not sufficiently cover damage or other potential losses or liabilities involving our properties, including as a result of terrorism and climate change, our profits could be reduced.

Because certain types of losses are uncertain, including natural disaster, the effects of climate change or other catastrophic losses, they may be uninsurable or prohibitively expensive. There are also other risks that may fall outside the general coverage terms and limits of our policies. Market forces beyond our control could limit the scope of the insurance coverage that we can obtain or may otherwise restrict our ability to buy insurance coverage at reasonable rates. In the event of a substantial loss, the insurance coverage that we carry may not be sufficient to pay the full value of our financial obligations, our liabilities or the replacement cost of any lost investment or property. Furthermore, certain of our properties may qualify as legally permissible nonconforming uses and improvements, including certain of our iconic and most profitable properties, and we may not be permitted to rebuild such properties as they exist now or at all, regardless of insurance proceeds, if such properties are destroyed. Any loss of this nature, whether insured or not, could materially adversely affect our results of operations and prospects.

We are subject to risks associated with the employment of hotel personnel, particularly with hotels that employ unionized labor, which could increase our operating costs, reduce the flexibility of our hotel managers to adjust the size of the workforce at our hotels and could materially and adversely affect our revenues and profitability.

While our hotel managers are and will be primarily responsible for hiring and maintaining the labor force at our hotels, we are subject to the costs and risks generally associated with the hotel labor force, and increased labor costs due to factors like labor shortages and resulting increases in wages, additional taxes, or requirements to incur additional employee benefits costs may adversely impact our operating costs. Labor costs, including wages, can be particularly challenging at those of our hotels with unionized labor, and additional hotels may be subject to new collective bargaining agreements in the future.

From time to time, strikes, lockouts, public demonstrations or other negative actions and publicity may disrupt hotel operations at any of our properties, negatively impact our reputation or the reputation of our brands, or harm relationships with the labor forces at our properties in operation or under development. We also may incur increased legal costs and indirect labor costs as a result of contract disputes or other events. The resolution of labor disputes or new or re-negotiated labor contracts could lead to increased labor costs, either by increases in wages or benefits or by changes in work rules that raise hotel operating costs. Furthermore, labor agreements may limit the ability of our hotel managers to reduce the size of hotel workforces during an economic downturn because collective bargaining agreements are negotiated between the hotel managers and labor unions. As we do not directly employ the employees at our hotels, we do not have the ability to control the outcome of these negotiations.

Terrorist acts, armed conflict, civil unrest, criminal activity, and threats thereof, and other events impacting the security of travel or of our contractors or the perception of security of travel or that of our contractors could adversely affect the demand for travel generally and demand for vacation packages at our hotels or the timely development of our hotels.

Past acts of terrorism and violent crime have had an adverse effect on tourism, travel and the availability of air service and other forms of transportation. The threat or possibility of future terrorist acts, an outbreak, escalation and/or continuation of hostilities or armed conflict abroad, such as the war between Russia and Ukraine and the Israel-Palestine conflict, criminal violence, civil unrest, or the possibility thereof, the issuance of travel advisories by sovereign governments, and other geopolitical uncertainties have had and may have an adverse impact on the demand for vacation packages and consequently the pricing for vacation packages. Decreases in demand and reduced pricing in response to such decreased demand would adversely affect our business by reducing our profitability.

All the properties in our portfolio are located in Mexico, and Mexico has experienced criminal violence for years, primarily due to the activities of drug cartels and related organized crime. There have occasionally been instances of criminal violence near our properties, including our properties under development in Cancun and Ensenada. Criminal activities and the possible escalation of violence or other safety concerns, including food and beverage safety concerns, associated with them in regions where our resorts are located, or an increase in the perception among our prospective guests of an escalation of such violence or safety concerns, could instill and perpetuate fear among prospective guests and may lead to a loss in business at our properties in Mexico because these guests may choose to vacation elsewhere or not at all. In addition, increases in violence, crime or civil unrest or other safety concerns in any other location where we may own a resort in the future may also lead to decreased demand for our resorts and negatively affect our business, financial condition, liquidity, results of operations and prospects.

There is increased competition from global hospitality branded companies in the all-inclusive market segment.

As demand for all-inclusive stays has increased, we have seen U.S. and European global hospitality branded companies enter the all-inclusive market segment. Increased competition from global branded hospitality companies may result in reduced market share and lower returns on investment for us as the increasing interest of global hospitality brands in the all-inclusive segment attracts more institutional capital to our target markets, increasing competition for the acquisition of hospitality assets. The entrance by global branded hospitality companies into the all-inclusive market segment may impact our ability to secure third-party management agreements as global hospitality branded companies are able to offer management agreements bundled with their branding services and a lower fee structure, resulting in increased competition for the management of all-inclusive resorts.

We have significant exposure to currency exchange rate risk.

Revenue from hotel operations is primarily received in U.S. dollars and the majority of our operating expenses are incurred locally at our properties and are denominated in Mexican Pesos. Our outstanding debt borrowings are payable largely in U.S. dollars and our functional reporting currency is Mexican Pesos. An increase in the relative value of the Mexican Peso, in which we incur most of our costs, relative to the U.S. dollar, in which our revenue from operations is primarily denominated, would adversely affect our results of operations. Our current policy is not to hedge against changes in foreign exchange rates and we therefore may be adversely affected by appreciation in the value of the Mexican Peso against the U.S. dollar, or to prolonged periods of exchange rate volatility. These fluctuations may negatively impact our financial condition, liquidity, and results of operations to the extent we are unable to adjust our pricing accordingly.

Furthermore, appreciation of the Mexican Peso relative to the U.S. dollar could make fulfillment of our U.S. dollar denominated obligations more challenging and could have a material adverse effect on us, including our business, financial condition, liquidity, results of operations and prospects.

Our projects, and any future acquisition, expansion, repositioning, and rebranding projects will be subject to timing, budgeting, and other risks, which could have a material adverse effect on us.

We may develop, acquire, expand, reposition, or rebrand resorts (such as the GIC Complex, the Resort Property in Baja Development Project and the Baja Park Development Project we are currently developing or expect to begin developing) from time to time as suitable opportunities arise, taking into consideration general economic conditions. To the extent that we determine to develop, acquire, expand, reposition, or rebrand resorts, we could be subject to risks associated with, among others:

| • | construction delays or cost overruns that may increase project costs; |

| • | receipt of zoning, occupancy and other required governmental permits and authorizations; |

| • | strikes or other labor issues; |

| • | development costs incurred for projects that are not pursued to completion; |

| • | investment of substantial capital without, in the case of developed or repositioned resorts, immediate corresponding income; |

| • | results that may not achieve our desired revenue or profit goals; |

| • | acts of nature such as earthquakes, hurricanes, floods or fires that could adversely impact a resort; |

| • | ability to raise capital, including construction or acquisition financing; and |

| • | governmental restrictions on the nature or size of a project. |

We have seen certain construction timelines lengthen due to competition for skilled construction labor, disruption in the supply chain for materials, especially as a result of COVID-19, and these circumstances could replicate or worsen in the future. As a result of the foregoing, we cannot assure you that any development, acquisition, expansion, repositioning and/or rebranding project, including the development of the GIC Complex, the Resort Property in Baja Development Project and the Baja Park Development Project, will be completed on time or within budget or if the ultimate rates of investment return are below the returns forecasted at the time the relevant project was commenced. If we are unable to complete a project on time or within budget, the resort’s projected operating results may be adversely affected, which could have a material adverse effect on us, including our business, financial condition, liquidity, results of operations and prospects.

Given the beachfront locations of the GIC Complex, we are particularly vulnerable to extreme weather events, such as hurricanes, which may increase in frequency and severity as a result of climate change and adversely affect our business.

We have been and may continue to be adversely impacted by the consequences of climate change, such as increases in the frequency, duration and severity of extreme weather events and changes in precipitation and temperature, which have resulted and may continue to result in physical damage or a decrease in demand for our properties, all of which are located in coastal beachfront locations that are vulnerable to significant property damage from hurricanes, tropical storms and flooding. Although we believe we have adequate insurance, there is no assurance that, given the increasing burdens on insurance companies from extreme weather events, we will be able to continue to obtain adequate insurance against these types of losses, or that our insurers will in the future be in a position to satisfy our claims. In addition, the costs of insurance against these types of events have increased in recent years.

In addition, changes in applicable legislation and regulation on climate change could result in increased capital expenditures, such as a result of changes in building codes or requirements to improve the energy efficiency of the properties. In addition, the ongoing transition to non-carbon-based energy presents certain risks for us and our target customers, including macroeconomic risks related to high energy costs and energy shortages, among other things. Furthermore, legislative, regulatory, or other efforts to combat climate change or other environmental concerns could result in future increases in taxes, restrictions on or increases in the costs of supplies, transportation, and utilities, any of which could increase our operating costs, and necessitate future investments in facilities and equipment.

Climate change also presents additional risks beyond our control which can adversely impact demand for hospitality products and services, our operations, and our financial results. For example, GIC Complex properties are located at or around sea level and are therefore vulnerable to rising sea levels and erosion. Climate change-related impacts may also result in a scarcity of resources, such as water and energy, at some or all of the regions in which our results are located. Furthermore, increasing awareness around sustainability, the impact of air travel on climate change and the impact of over-tourism may contribute to a reduction in demand from certain guests visiting our resorts.

We also face investor-related climate risks. Investors are increasingly taking into account environmental, social, and governance factors, including climate risks, in determining whether to invest in companies. Our exposure to the risks of climate change may adversely impact investor interest in our securities. These risks also include the increased pressure to make commitments, set targets, or establish goals to take actions to meet them, which could expose us to market, operational, execution and reputational costs or risks.

Consequences of climate change, such as the appearance of large masses of sargassum seaweed in the Yucatán Peninsula and beach erosion effects, could result in decreased tourism appetite in Cancun, which could have a material adverse effect on our business.

Cancun has been exposed to elevated sea levels. Rising sea level in the Caribbean creates, among others, beach erosion, storm surges of hurricanes, and large masses of sargassum seaweed. The impact of hurricanes, such as Hurricane Wilma in 2005, can cause the sand in the beaches to be washed away. As sea level rises, storm surges from hurricanes will be higher. Since 2009, Mexico launched a project to restore seven miles of beach and is expected to continue.

In recent years, the quantity of sargassum seaweed that has washed up onshore in various geographies in Mexico has increased. If not removed promptly, the sargassum seaweed can overrun the beach, making it difficult to access the water and it generates a foul odor if allowed to rot on the beach. In recent years, the heightened level of sargassum seaweed has led to negative media coverage and increased awareness of the potential problem.

Since 2011, tourism to Mexico’s Yucatán Peninsula has been heavily impacted by large masses of sargassum seaweed washing up on the beaches, with the largest seaweed event occurring in 2019. Seaweed deters beach tourism, potentially shifting tourism inland towards many types of recreational activities, such as theme parks, cenotes (sinkholes), cultural tours and restaurants, or to beach destinations in other regions or countries. Since the first massive seaweed arrivals in Mexico in 2011, there have been a number of initiatives to investigate the impacts and management of sargassum in the region. In 2019, a government’s sargassum containment strategy headed by the Ministry of Navy was established. The existence of large masses of sargassum seaweed in the Yucatán Peninsula could materially and adversely affect our operating results.

Although the GIC Complex is located on the Nichupté Lagoon and not on the beach, a decrease in the attractiveness of the overall Cancun area as a tourist destination as a result of the above could have a material adverse effect on our business.

We cannot predict the impact that changing climate conditions, as well as legal, regulatory, and social responses thereto, may have on our business.

Various scientists, environmentalists, international organizations, regulators, and other commentators believe that global climate change has added, and will continue to add, to the unpredictability, frequency, and severity of natural disasters (including, but not limited to, hurricanes, tornadoes, freezes, other storms, and fires) in certain parts of the world. A number of legal and regulatory measures as well as social initiatives have been introduced in an effort to reduce greenhouse gases and other carbon emissions, which some believe may be chief contributors to global climate change. We cannot predict the impact that changing climate conditions, if any, will have on our results of operations or our financial condition. Moreover, we cannot predict how legal, regulatory, and social responses to concerns about global climate change will impact our business.

Furthermore, we anticipate that pending regulations under the General Law on Climate Change (Ley General de Cambio Climático) in Mexico, which are expected to impose an internal system to limit emissions and introduce tradable permits and other measures to achieve its goal of greenhouse gas reduction, may affect our operations and/or result in environmental liability.

Our hotels will require ongoing and often costly maintenance, renovations, and capital improvements.

Our hotels will have an ongoing need for maintenance, renovations, and other capital improvements, including replacements, from time to time, of furniture, fixtures, and equipment. In addition, Hyatt and other internationally recognized hotel brands may require periodic capital improvements by us as a condition of maintaining the use of their brands. We may need to finance the cost of maintenance, renovations and/or capital improvements and we may not have access to financings on reasonable terms or at all. In addition to liquidity risks, these capital improvements may result in declines in revenues while rooms are out of service due to capital improvement projects or other risks. The costs of these capital improvements or any of the above noted factors could have a material adverse effect on us, including our financial condition, liquidity, and results of operations.

Our business is susceptible to reductions in discretionary consumer and corporate spending due to global economic conditions.

Consumer demand for resorts, trade shows, and conventions and the type of luxury amenities that we offer are particularly sensitive to changes in the global economy, which adversely impact discretionary spending on leisure activities. Changes in discretionary consumer spending or consumer preferences brought about by factors such as perceived or actual general global economic conditions, high unemployment, weakness in housing or oil markets, perceived or actual changes in disposable consumer income and wealth, an economic recession, and changes in consumer confidence in the global economy, or fears of war and future acts of terrorism and mass violence have in the past and could in the future reduce customer demand for the type of luxury amenities and leisure activities we expect to offer, which could impose downward pressure on pricing and, in turn, have a significant negative impact on our future operating results. Our success depends in part on our hotel operators’ ability to anticipate consumers’ preferences and react to those trends, and any failure to do so may negatively impact our operating results.

The seasonality of the lodging industry could have a material adverse effect on us.

The lodging industry is seasonal in nature, which can be expected to cause quarterly fluctuations in our revenues. The seasonality of the lodging industry and the location of our hotels in Mexico will generally result in the greatest demand for our resorts between mid-December and April of each year, yielding higher occupancy levels and package rates during this period. This seasonality in demand is expected to result in predictable fluctuations in revenue, results of operations and liquidity, which are expected to be higher during the first quarter of each year than in successive quarters. We can provide no assurances that these seasonal fluctuations will, in the future, be consistent with the historical experience in the sector or whether any shortfalls that occur as a result of these fluctuations will not have a material adverse effect on us.

The cyclical nature of the lodging industry may cause fluctuations in our operating performance, which could have a material adverse effect on us.

The lodging industry is highly cyclical in nature. Fluctuations in operating performance are caused largely by general economic and local market conditions, which subsequently affect levels of business and leisure travel. In addition to general economic conditions, new hotel and resort room supply is an important factor that can affect the lodging industry’s performance, and over-building has the potential to further exacerbate the negative impact of an economic recession. Room rates and occupancy levels tend to increase when demand growth exceeds supply growth. A decline in lodging demand, or increase in lodging supply, could result in returns that are substantially below expectations, or result in losses, which could have a material adverse effect on us, including our business, financial condition, liquidity, results of operations and prospects. Further, the costs of running a hotel tend to be more fixed than variable. As a result, in an environment of declining revenue, the rate of decline in earnings is likely to be higher than the rate of decline in revenue.

The increasing use of internet travel intermediaries by consumers could have a material adverse effect on us.

Some of our vacation packages are expected to be booked through Internet travel intermediaries, including, but not limited to, Travelocity.com, Expedia.com and Priceline.com. As these Internet bookings increase, these intermediaries may be able to obtain higher commissions, reduced room rates or other significant contract concessions from us. If consumers develop loyalty to Internet reservations systems rather than to our booking system or the brands under which we operate, the value of our hotels could deteriorate and we could be materially and adversely affected, including our financial results.

If the hotel operators are unable to recruit, train and retain qualified management and employees, our business could be significantly harmed.

In order to operate our hotels effectively, the operators will need to recruit numerous executives, managers, and employees with hospitality industry experience. We cannot assure you that a sufficient number of qualified employees will be available to meet the hotel operators’ labor needs, particularly given the intense competition for skilled employees in the Mexico City and Cancun markets.

We cannot assure you that our hotel operators will find suitable and qualified candidates for all the positions required to fill before the opening of our hotels. We also cannot assure you that, once hired, the hotel operators will retain their employees or find suitable and qualified replacements for those employees whose employment terminates. If a hotel operator is unable to attract, hire and retain an adequate number of suitable and qualified employees, our business may be significantly impaired.

Our hotels may contain or develop harmful mold or suffer from other indoor air quality issues, which could lead to liability for adverse health effects or property damage, or cost for remediation and may adversely impact our financial condition and results of operations.

When excessive moisture accumulates in buildings or on building materials, mold growth may occur, particularly if the moisture problem remains undiscovered or is not addressed over a period of time. Some molds may produce airborne toxins or irritants. Indoor air quality issues can also stem from inadequate ventilation, chemical contamination from indoor or outdoor sources, and other biological contaminants such as pollen, viruses, and bacteria. Indoor exposure to airborne toxins or irritants can be alleged to cause a variety of adverse health effects and symptoms, including allergies or other reactions. As a result, the presence of significant mold or other airborne contaminants at any of our hotels could require us to undertake a costly remediation program to contain or remove the mold or other airborne contaminants or to increase ventilation and could expose us to liability from third parties if a personal injury occurs.

The departure of any key personnel with significant experience and relationships in the lodging industry from any of our hotels could materially and adversely impede or impair our ability to compete effectively and limit future growth prospects.

We depend on the experience and relationships of the senior management team of our hotel operators to manage the day-to-day operations of the hotels. The hotel operators’ senior management team has an extensive network of lodging industry contacts and relationships. We can provide no assurances that any of the key personnel of the hotel operators will continue working with the hotel operators. The departure of any of our key personnel of the hotel operator who has significant experience and relationships in the lodging industry could materially and adversely impede or impair our ability to compete effectively and limit future growth prospects.

From time to time, we and/or our affiliates may be involved in legal and other proceedings which may have an adverse effect on our properties and operations and/or a negative impact on our reputation.

From time to time, we and/or our affiliates may be involved in disputes with various parties related to the financing, construction, and operation of the properties, including contractual disputes with contractors, suppliers, and construction workers or property damage or personal liability claims. Regardless of the outcome, these disputes may lead to legal or other proceedings and may result in substantial costs, delays in our development schedule, and the diversion of resources and management’s attention. We intend to carry insurance to cover most business risks, but there can be no assurance that the insurance coverage we have will cover all claims that may be asserted against us. Should any ultimate judgments or settlements not be covered by insurance or exceed our insurance coverage, such uncovered losses could increase our costs and thereby lower our profitability. There can also be no assurance that we will be able to obtain the appropriate and sufficient types and levels of insurance once the properties are operating. Our affiliates have in the past been involved in legal and other proceedings and may be involved in other proceedings in the future. Regardless of insurance coverage, if any legal or other proceedings in which we and/or our affiliates may be involved are finally resolved against us and/or our affiliates interest, any such resolution may have a material adverse effect on our properties and operations and/or may negatively impact our reputation.

We and our hotel operators are subject to the risk of increased lodging operating expenses.

Together with the hotel operators, we are subject to the risk of increased lodging operating expenses, including, but not limited to, the following cost elements:

| • | repair and maintenance expenses; |

| • | property and other taxes; |

| • | other operating expenses. |

We face competition in the lodging industry in Mexico, which may limit our profitability and return to our shareholders.

The lodging industry in Mexico is highly competitive. This competition could reduce occupancy levels and rental revenues at our properties, which would adversely affect our operations. We face competition from many sources. We face competition from other lodging facilities both in the immediate vicinity of our properties and the geographic markets in which the properties will be located. In addition, increases in operating costs due to inflation may not be offset by increased room rates. We also face competition from recognized lodging brands with which we are not associated.

We also face competition from online marketplaces focused on customer-to-customer virtual platforms, like Airbnb, which enables people to lease or rent short-term lodging, including vacation rentals, apartment rentals, homestays, hostel beds, or hotel rooms to its customers.

Some of our competitors may have substantially greater marketing and financial resources than us. If our hotel management companies are unable to compete successfully or if our competitors’ marketing strategies are effective, our business, financial condition and results of operations may be adversely affected.

The need for business-related travel and, thus, demand for rooms in our hotels may be materially and adversely affected by the increased use of business-related technology.

The increased use of teleconference and video-conference technology by businesses could result in decreased business travel as companies increase the use of technologies that allow multiple parties from different locations to participate at meetings without traveling to a centralized meeting location, such as our hotels. To the extent that such technologies play an increased role in day-to-day business and the necessity for business-related travel decreases, demand for our hotel rooms may decrease, and we could be materially and adversely affected.

Lack of sufficient air service to Mexico City or Cancun could adversely affect our revenues and profits.

Nearly all of our prospective international customers travel to Mexico City and Cancun by air. Although we believe that the current level of air service to Mexico City and Cancun is adequate, any interruption or reduction of air service would prevent many prospective customers from visiting our hotels and reduce our sales and the growth of our business. Many of our guests rely on a combination of scheduled commercial airline services and tour operator services for passenger connections, and price increases or service changes by airlines or tour operators could reduce our occupancy rates and revenue levels and, therefore, have a material adverse effect on our business, financial condition, and results of operations.

Many of our guests depend on a combination of scheduled commercial airline services and tour operator services to transport them to airports near our resorts.

Increases in the price of airfare, due to increases in fuel prices or other factors, would increase the overall travel cost to our guests and may adversely affect demand for our hotels. Changes in commercial airline services or tour operator services as a result of strikes, weather or other events, or the lack of availability due to schedule changes or a high level of airline bookings, could reduce our occupancy rates and revenue levels and, therefore, have a material adverse effect on our business, financial condition and results of operations.

Illiquidity of real estate investments could significantly impede our ability to sell our hotels or otherwise respond to adverse changes in our hotel portfolio performance, which could have a material adverse effect on us.

Because real estate investments are relatively illiquid, our ability to sell a hotel promptly for reasonable prices in response to changing economic, financial and investment conditions will be limited. The real estate market is affected by many factors beyond our control that could impact the timing of a disposition, including adverse changes in economic and market conditions, changes in interest and tax rates and in the availability and cost and other terms of debt financing, and changes in governmental laws and regulations.

In addition, we may be required to expend funds to correct defects, terminate contracts or to make improvements before a resort can be sold. We can provide no assurances that we will have funds available, or access to such funds, to correct those defects or to make those improvements. In acquiring or developing a hotel, we may agree to lock-out provisions or tax protection agreements that materially restrict us from selling that property for a period of time or impose other restrictions, such as a limitation on the amount of debt that can be placed or repaid on that property. These factors and any others that would impede our ability to respond to adverse changes in the performance of our resorts or a need for liquidity could materially and adversely affect us, including our financial results.

Increases in property taxes would increase our operating costs, which could have a material adverse effect on us.

The Insurgentes 421 Hotel Complex, the Vivid Hotel and any future hotels within the GIC Complex are expected to be subject to real estate and personal property taxes, especially upon any development, redevelopment, rebranding, repositioning, and renovation. These taxes may increase as tax rates change and as our properties are assessed or reassessed by taxing authorities. If property taxes increase, we would incur a corresponding increase in our operating expenses, which could have a material adverse effect on us, including our business, financial condition, liquidity, results of operations and prospects.

Our properties and operations are subject to extensive environmental, health and safety laws and regulations. We may incur costs that have a material adverse effect on our financial condition due to any liabilities under, or potential violations of, environmental, health and safety laws and regulations.

Our properties and operations are subject to numerous covenants, laws, regulations, rules, codes and to oversight by various federal, state and local governmental authorities, including those related to ecological ordinance, environmental impact, municipal and/or forest land use changes, health and safety, fire protection and seismic matters in each of the places in Mexico in which we operate.

These laws and regulations require that we obtain, and maintain (as applicable) several permits in connection with the site preparation, construction and operation of our businesses, which can sometimes impose restrictive covenants or are conditioned to the fulfilment of actions such as the obtaining of prior approval from other local authorities or communities so that they become in full force and effect and we can initiate site preparation and construction; the issuance of these permits can also be delayed due to extreme backlog in the processing of authorizations by some authorities, causing rippled delays in our prospective project schedules and may require us to incur significant additional costs on short notice which may adversely affect our financial condition to move forward with the development of our projects. Our growth strategy may be adversely affected by our ability to obtain permits, licenses and approvals. Our failure to obtain such permits, licenses and approvals could have a material adverse effect on our business, financial condition and results of operations.

We are also exposed to the risk of a sudden increase in becoming liable for contamination at any Murano Group’s properties or resorts which could be the result of third-party actions on-site or migrating from nearby areas and/or the number of complaints against us as a result of changes in the existing regulation (or in the interpretation thereof), such as the enactment of various legal reforms to allow class actions, those that seek the protection of indigenous or afro Mexican communities’ rights or to protect other diffuse and collective human rights such as the human right to access to water.

In addition, future changes in the regulation applicable to our industry may result in the risk of temporary water restrictions, revocation of concession titles impeding us to use national assets such as federal maritime terrestrial zones adjacent to our properties, the imposition of bans or restrictions on the use of certain products, vape smoking bans in our restaurants, increases in the taxation of luxury goods or the sale of alcohol or high-calorie beverages, restrictions on the hours of operation of our restaurants, convention centers, etc. and we may incur costs that have a material adverse effect on our results of operations and financial condition as a result thereof or of any liabilities under or potential violations of environmental, health and safety laws and regulations.

We anticipate that the regulation of our business operations under Mexican federal, state and local environmental laws and regulations will increase and become more stringent over time. We cannot predict the effects of such changes, if any, that the adoption of additional or more stringent environmental laws and regulations would have on our results of operations, cash flows, capital expenditure requirements or financial condition.

Risks Related to Doing Business in Mexico

All of Murano’s assets are located in Mexico. Therefore, we are subject to political, economic, legal, and regulatory risks specific to Mexico and the Mexican real estate industry and lodging sector and are vulnerable to an economic downturn, other changes in market conditions, acts of violence, or natural disasters in Mexico or in the regions where our properties are located.

Our operating entities are incorporated in Mexico, and all our assets and operations are located in Mexico. As a result, we are subject to political, economic, legal, and regulatory risks specific to Mexico, including the general condition of the Mexican real estate industry, lodging sector, and the Mexican economy, the devaluation of the peso as compared to the U.S. dollar, Mexican inflation, interest rates, regulation, confiscatory taxation and regulation, expropriation, social instability, and political, social, and economic developments in Mexico.

Our business may be significantly affected by the Mexican economy’s general condition, by the depreciation of the peso, inflation, and high-interest rates in Mexico, or by political developments in Mexico. Declines in growth, high rates of inflation, and high-interest rates in Mexico have a generally adverse effect on our operations. If inflation in Mexico increases while economic growth slows, our business, results of operations, and financial condition will be affected. In addition, high-interest rates and economic instability could increase our costs of financing.

In the past, the rating agencies rating Mexico and PEMEX have downgraded both Mexico and PEMEX and/or placed them on negative outlooks. On June 16, 2023, Fitch Ratings has affirmed Mexico’s Long-Term (LT) Foreign Currency (FC) Issuer Default Rating (IDR) at ‘BBB-’; with a stable rating outlook. On July 14, 2023, Moody’s assigned Mexico a rating of Baa2; with a stable rating outlook. We cannot ensure that the rating agencies will not announce downgrades of Mexico and/or PEMEX in the future and any such downgrades could adversely affect the Mexican economy and, consequently, our business, financial condition, operating results, and prospects.

Political instability in Mexico could negatively affect our operating results.

In Mexico, political instability has been a determining factor in business investment. Significant changes in laws, public policies and/or regulations could affect Mexico’s political and economic situation, which could, in turn, adversely affect our business.

Mexican political events may affect our business operations. President Lopez Obrador’s political party and its allies hold a majority in the Chamber of Deputies (Cámara de Diputados) and the Senate (Senado de la República) and a strong influence in various local legislatures. The federal administration has significant power to implement substantial changes in law, policy, and regulations in Mexico, including Constitutional reforms, which could affect our business, results of operations, financial condition, and prospects. We cannot predict whether potential changes in Mexican governmental and economic policy could adversely affect Mexico’s economic conditions or the sector in which we operate. We cannot provide any assurances that political developments in Mexico, over which we have no control, will not have an adverse effect on our business, results of operations, financial condition, and prospects.

Social and political instability in or affecting Mexico could adversely affect our business, financial condition, and results of operations, as well as market conditions and prices of our securities. These and other future developments in the Mexican political or social environment may cause disruptions to our business operations and decreases in our sales and net income.

Our assets are located in Mexico and are therefore subject to the provisions of the National Law of Domain Extinction (Ley Nacional de Extinción de Dominio).

The National Law of Domain Extinction (Ley Nacional de Extinción de Dominio, the “LNED”) empowers the public prosecutor (agente del ministerio público) to exercise the extinction of domain action with respect to all types of assets related to crimes in a broad range of categories, including organized crime, kidnapping, crimes related to hydrocarbons, oil and petrochemicals, crimes against health, human trafficking, crimes for acts of corruption, cover-ups, crimes committed by public servants, theft of vehicles, resources of illicit origin and extortion. Pursuant to the LNED, the extinction of domain action may be exercised with respect to assets related to any of these crimes, including if the assets are used by a party other than the owner of the asset in order to commit the crime.

The LNED permits a final judgment on domain extinction even in certain cases when the criminal trial has not yet concluded; provided the governmental authority determines that solid and reasonable grounds exist to infer the existence of assets that are covered by the LNED. In such cases, if the affected person were to later prove its innocence and the asset has already been monetized, the affected person would only be able to recover the proceeds from the monetization of the asset.

Legal remedies are available to challenge the enforcement of the LNED on the grounds of a possible violation of human and constitutional rights such as property rights and the presumption of innocence. Should our assets ever be challenged under LNED grounds, in order to defend our rights, it may be necessary to incur significant costs due to litigation and/or full or partial loss of the assets subject to domain extinction proceedings. All of the foregoing could adversely affect our business, financial condition and results of operations.

Fluctuations in the U.S. economy or the global economy, in general, may adversely affect Mexico’s economy and our business.