As confidentially submitted to the U.S. Securities and Exchange Commission on November 20, 2023.

This draft registration statement has not been filed, publicly or otherwise, with the U.S. Securities and

Exchange Commission and all information contained herein remains strictly confidential.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_________________________

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

_________________________

IGTA MERGER SUB LIMITED

(Exact name of Registrant as specified in its charter)

_________________________

British Virgin Islands | 7370 | Not Applicable | ||

(State or other jurisdiction of | (Primary Standard Industrial | (I.R.S. Employer |

875 Washington Street

New York, NY 10014

Telephone: (315) 636-6638

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

_________________________

[•]

(Name, address, including zip code, and telephone number, including area code, of agent for service)

_________________________

Copies of communications to:

Lawrence Venick, Esq. Facsimile: (212) 407-4990 | Barry I. Grossman, Esq. |

_________________________

Approximate date of commencement of proposed sale of the securities to the public: As soon as practicable after this Registration Statement becomes effective and after all of the conditions set forth in the Business Combination Agreement are satisfied or waived.

If the securities being registered on this form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. ☐

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

Non-accelerated filer | ☒ | Smaller reporting company | ☒ | |||

Emerging growth company | ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

Exchange Act Rule 13e- 4(i) (Cross- Border Issuer Tender Offer) | ☐ | |

Exchange Act Rule 14d- 1(d) (Cross- Border Third- Party Tender Offer) | ☐ |

____________

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the Securities and Exchange Commission declares our registration statement effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any jurisdiction or state where the offer or sale is not permitted.

PRELIMINARY — SUBJECT TO COMPLETION, DATED [•], 2023

PROXY STATEMENT FOR SPECIAL MEETING OF STOCKHOLDERS OF

INCEPTION GROWTH ACQUISITION LIMITED

AND PROSPECTUS FOR ORDINARY SHARES, RIGHTS AND WARRANTS

OF IGTA MERGER SUB LIMITED

Proxy Statement/Prospectus dated [ ], 2023

and first mailed to the stockholders of Inception Growth Acquisition Limited on or about [ ], 2023

To the Stockholders of Inception Growth Acquisition Limited:

You are cordially invited to attend the Special Meeting of the Stockholders of Inception Growth Acquisition Limited (“Inception Growth,” “IGTA,” “we,” “our,” or “us”), which will be held at [ ], on [ ], 2023 (the “Special Meeting”) and virtually using the following dial-in information:

US Toll Free | [ ] | |||

International Toll | [ ] | |||

Participant Passcode | [ ] |

The board of directors of Inception Growth (the “Inception Growth Board” or “IGTA Board”) has determined to utilize virtual stockholder meeting technology, and encourages stockholders to attend the Special Meeting virtually.

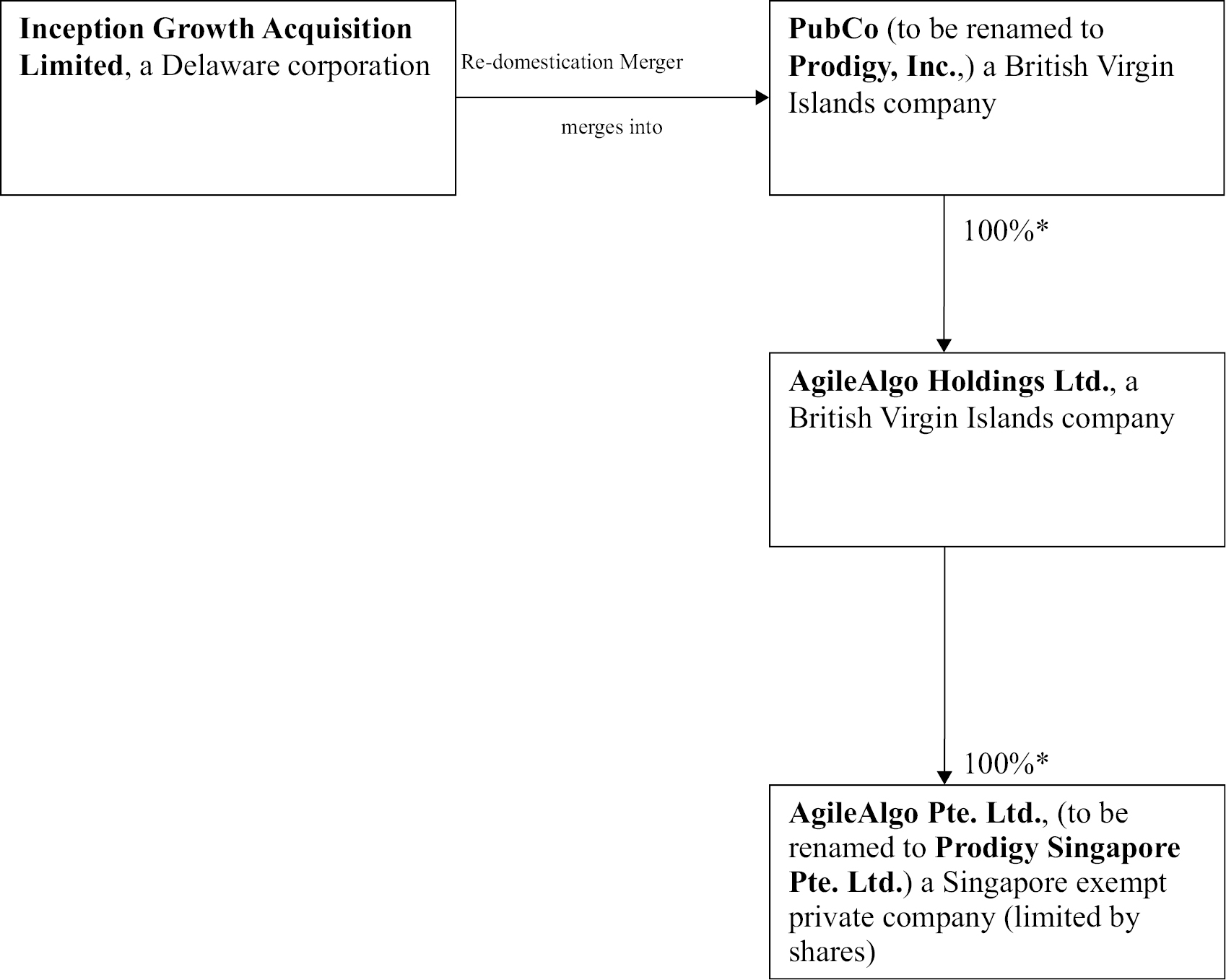

Inception Growth is a Delaware corporation incorporated as a blank check company for the purpose of entering into a merger, share exchange, asset acquisition, stock purchase, recapitalization, reorganization or other similar business combination with one or more businesses or entities, which we refer to as a “target business.” The business combination will be completed through a two-step process consisting of the Redomestication Merger (as defined below) and the Share Exchange (as defined below). The Redomestication Merger and the Share Exchange are collectively referred to herein as the “Business Combination.”

On September 12, 2023, Inception Growth entered into a Business Combination Agreement with IGTA Merger Sub Limited, a British Virgin Islands company and wholly owned subsidiary of IGTA (such company before the Redomestication Merger is sometimes referred to as the “Purchaser” and upon and following the Redomestication Merger (as defined below) is hereinafter sometimes referred to as “PubCo”), AgileAlgo Holdings Ltd., a British Virgin Islands company (“AgileAlgo” or the “Company”), and certain shareholders of AgileAlgo (the “Signing Sellers”), and which agreement may also be thereafter executed by each of the other shareholders of AgileAlgo (such shareholders, together with the Signing Sellers, the “Sellers”) in one or more joinder agreements, (collectively, the “Seller Joinders”) (such agreement together with the Seller Joinders, as it may be amended from time to time, the “Business Combination Agreement”), which provides for a Business Combination between Inception Growth and AgileAlgo. Pursuant to the Business Combination Agreement, the Business Combination will be effected in two steps: (i) subject to the approval and adoption of the Business Combination Agreement by the stockholders of Inception Growth, Inception Growth will merge with and into Purchaser, with PubCo remaining as the surviving publicly traded entity (the “Redomestication Merger”); and (ii) substantially concurrently with the Redomestication Merger, the shareholders of AgileAlgo will exchange all of their ordinary shares of AgileAlgo (the “Purchased Shares”) for an aggregate of fourteen million (14,000,000) ordinary shares of PubCo (“PubCo Ordinary Shares”), valued at $10.00 each, for a total of One Hundred Forty Million Dollars ($140,000,000) (the “Closing Consideration Shares”), plus an additional two million (2,000,000) PubCo Ordinary Shares, for a total of Twenty Million Dollars ($20,000,000) as additional contingent consideration (“Earnout Consideration Shares”) (such exchange, the “Share Exchange”, collectively with the Redomestication Merger, the “Business Combination”).

Following the Business Combination, Purchaser will be a publicly traded company renamed as “Prodigy, Inc.”

Purchaser was formed on September 11, 2023, for the sole purpose of, immediately prior to the Closing, merging with Inception Growth in the Redomestication Merger, where Purchaser will be the surviving entity as a British Virgin Islands business company.

At the consummation of the Share Exchange (the “Closing”), the former Inception Growth stockholders will receive the consideration specified below and the former shareholders of AgileAlgo will receive the Closing Consideration Shares consisting of an aggregate of 14,000,000 PubCo Ordinary Shares. Any Earnout Consideration will be paid in PubCo Ordinary Shares. In addition, [*] PubCo Ordinary Shares will be reserved and authorized for issuance under the 2023 AgileAlgo Employee Incentive Plan upon closing (the “Incentive Plan”).

At the Special Meeting, Inception Growth stockholders will be asked to consider and vote upon the following proposals:

1. approval of the Redomestication Merger and the Plan of Merger (as defined below), which we refer to as the “Redomestication Merger Proposal” or “Proposal No. 1;”

2. approval of the Share Exchange, which we refer to as the “Share Exchange Proposal” or “Proposal No. 2;”

3. approval, for purposes of complying with applicable listing rules of The Nasdaq Stock Market LLC, of the issuance of up to an aggregate of 16,000,000 PubCo Ordinary Shares in connection with the Business Combination and related financings, which we refer to as the “Nasdaq Proposal” or “Proposal No. 3”;

4. approval of the Governance Proposal, which we refer to as the “Governance Proposal” or “Proposal No. 4”;

5. approval of the Incentive Plan, which we refer to as the “Incentive Plan Proposal” or “Proposal No 5.” A copy of the Incentive Plan is attached to the accompanying proxy statement as Annex C;

6. approval of the NTA Requirement Amendment Proposal (defined below) to eliminate from Inception Growth’s certificate of incorporation the limitation that it shall not redeem Public Shares to the extent that such redemption would cause Inception Growth’s net tangible assets to be less than $5,000,001, and to expand the methods that Inception Growth may employ to not become subject to the “penny stock” rules of the Securities and Exchange Commission, by deleting the certificate of incorporation in its entirety and substitute it with the second amended and restated certificate of incorporation, which we refer to as the “NTA Requirement Amendment Proposal” or “Proposal No. 6.” A copy of the second amended and restated certificate of incorporation is attached hereto as Annex D;

7. approval of the appointment of six (6) directors of PubCo, assuming the Redomestication Merger Proposal, the Share Exchange Proposal and the Nasdaq Proposal are all approved, to appoint six (6) directors, effective upon the Closing which we refer to as the “Director Appointment Proposal” or “Proposal No. 7”; and

8. approval to adjourn the Special Meeting under certain circumstances, which is more fully described in the accompanying proxy statement/prospectus, which we refer to as the “Adjournment Proposal” or “Proposal No. 8” and, together with the Redomestication Merger Proposal, the Share Exchange Proposal, the Nasdaq Proposal, the Governance Proposal, the Incentive Plan Proposal, the NTA Requirement Amendment Proposal and the Director Amendment Proposal,

collectively, the “Proposals.”

If Inception Growth stockholders approve the Redomestication Merger Proposal and the Share Exchange Proposal, then, immediately prior to the consummation of the Business Combination, all outstanding units of Inception Growth (each of which consists of one IGTA Share, one-half of one IGTA Warrant and one IGTA Right) (the “IGTA Units”) will separate into their individual components of IGTA Shares, IGTA Warrants and IGTA Rights and will cease separate existence and trading. Upon the consummation of the Business Combination, the current equity holdings of the Inception Growth stockholders shall be exchanged as follows:

(i) Each share of common stock of IGTA, par value $0.0001 per share (“IGTA Share”), issued and outstanding immediately prior to the effective time of the Redomestication Merger (other than any redeemed shares), will automatically be cancelled and cease to exist and for each such IGTA Share, PubCo shall issue to each Inception Growth stockholder (other than Inception Growth stockholders who exercise their redemption rights in connection with the Business Combination) one validly issued PubCo Ordinary Share, which shall be fully paid;

(ii) Each whole warrant to purchase one IGTA Share (“IGTA Warrant”) issued and outstanding immediately prior to effective time of the Redomestication Merger will convert into a warrant to purchase one PubCo Ordinary Share (each, a “PubCo Warrant”) (or equivalent portion thereof) provided, however, that the number of warrants issuable upon separation of the units will be rounded down to the nearest whole number of warrants. The PubCo Warrants will have substantially the same terms and conditions as set forth in the IGTA Warrants; and

(iii) Each IGTA Right (each exchangeable into one-tenth of one IGTA Share) (“IGTA Right”) issued and outstanding immediately prior to the effective time of the Redomestication Merger will receive one-tenth (1/10) of one PubCo Ordinary Share in exchange for the cancellation of each IGTA Right; provided, however, that no fractional shares will be issued and all fractional shares will be rounded down to the nearest whole share.

It is anticipated that, upon consummation of the Business Combination, Inception Growth’s existing stockholders, including the Sponsor (as defined below), will own approximately 28.70% of the issued PubCo Ordinary Shares, and the AgileAlgo Shareholders will own approximately 69.88% of the issued PubCo Ordinary Shares and that Inception Growth’s existing stockholders, including the Sponsor (as defined below), will have approximately 28.70% of aggregate voting power of all issued PubCo Ordinary Shares, and the AgileAlgo Shareholders will have approximately 69.88% of aggregate voting power of all issued PubCo Ordinary Shares.

These relative percentages assume that (i) none of Inception Growth’s existing public stockholders exercise their redemption rights or dissenting rights, as discussed herein; (ii) there is no exercise or conversion of PubCo Warrants; (iii) the Notes (as defined herein) have not been converted; and (iv) the AgileAlgo Convertible Notes (as defined herein) have been issued and converted. If any of Inception Growth’s existing public stockholders exercise their redemption rights, the anticipated percentage ownership of Inception Growth’s existing stockholders will be reduced. You should read “Summary of the Proxy Statement/Prospectus — The Business Combination and the Business Combination Agreement” and “Unaudited Pro Forma Condensed Consolidated Financial Information” for further information.

The IGTA Units, IGTA Shares, IGTA Rights and IGTA Warrants are currently listed on the Nasdaq Global Market under the symbols “IGTAU,” “IGTA,” “IGTAR” and “IGTAW,” respectively. PubCo intends to apply to list the PubCo Ordinary Shares and PubCo Warrants on the Nasdaq Stock Market under the symbols “PRGY” and “PRGYW,” respectively, in connection with the closing of the Business Combination. Each IGTA Unit consists of one IGTA Share, one IGTA Right and one-half of one redeemable IGTA Warrant, exercisable upon the later of one year after the closing of Inception Growth’s IPO or the consummation of the Business Combination.

Inception Growth cannot assure you that the PubCo Ordinary Shares and PubCo Warrants will be approved for listing on Nasdaq.

Investing in PubCo securities involves a high degree of risk. See “Risk Factors” beginning on page 19 for a discussion of information that should be considered in connection with an investment in PubCo securities.

As of September 30, 2023, there was approximately $47,635,394 in Inception Growth’s trust account (the “Trust Account”). On [ ], 2023, the last sale price of IGTA Shares was $[ ].

Following the completion of the Business Combination, the issued and outstanding share capital of PubCo will consist of PubCo Ordinary Shares. The shareholders AgileAlgo will beneficially own [ ] of the issued PubCo Ordinary Shares and will be able to exercise [*]% of the total voting power of the issued and outstanding share capital of PubCo immediately following the completion of the Business Combination, assuming that (i) none of Inception Growth’s existing public stockholders exercise their redemption rights or dissenting rights, as discussed herein, (ii) there is no exercise of PubCo Warrants, (iii) the Notes (as defined herein) not been converted and (iv) no Earnout Consideration Shares have been issued.

Pursuant to Inception Growth’s amended and restated certificate of incorporation, Inception Growth is providing its public stockholders with the opportunity to redeem all or a portion of their IGTA Shares at a per-share price, payable in cash, equal to the aggregate amount then on deposit in Inception Growth’s Trust Account as of two business days prior to the consummation of the Business Combination, including interest, less taxes payable, divided by the number of then outstanding IGTA Shares that were sold as part of the IGTA Units in Inception Growth’s initial public offering (“IPO”), subject to the limitations described herein. Inception Growth estimates that the per-share price at which IGTA Shares held by the public (the “Public Shares”) may be redeemed from cash held in the Trust Account will be approximately $[ ] at the time of the Special Meeting. Inception Growth’s public stockholders may elect to redeem their shares even if they vote for the Redomestication Merger or do not vote at all.

Inception Growth is providing this proxy statement/prospectus and accompanying proxy card to its stockholders in connection with the solicitation of proxies to be voted at the Special Meeting and at any adjournments or postponements of the Special Meeting. The Sponsor, which owns approximately 20.46% of the outstanding IGTA Shares as of the record date, has agreed to vote its IGTA Shares in favor of the Redomestication Merger Proposal and the Share Exchange Proposal, which transactions comprise the Business Combination, and intends to vote for the Nasdaq Proposal, Governance Proposal, Incentive Plan Proposal, the NTA Requirement Amendment Proposal, the Director Appointment Proposal and the Adjournment Proposal, although there is no agreement in place with respect to voting on those latter proposals.

Each stockholder’s vote is very important. Whether or not you plan to attend the Special Meeting in person (including by virtual presence), please submit your proxy card without delay. Inception Growth’s stockholders may revoke proxies at any time before they are voted at the meeting. Voting by proxy will not prevent a stockholder from voting in person (including by virtual presence) if such stockholder subsequently chooses to attend the Special Meeting. If you are a holder of record and you attend the Special Meeting and wish to vote in person (including by virtual presence), you may withdraw your proxy and vote in person. Assuming that a quorum is present, attending the Special Meeting either in person (including by virtual presence) or by proxy and abstaining from voting and broker non-votes will have no effect on any of the Proposals.

If you sign, date and return your proxy card without indicating how you wish to vote, your proxy will be voted in favor of each of the Proposals presented at the Special Meeting. If you fail to return your proxy card or fail to instruct your bank, broker or other nominee how to vote, and do not attend the Special Meeting in person (including by virtual presence), the effect will be that your shares will not be counted for purposes of determining whether a quorum is present at the Special Meeting of stockholders. If you are a stockholder of record and you attend the Special Meeting and wish to vote in person (including by virtual presence), you may withdraw your proxy and vote in person (including by virtual presence).

This proxy statement/prospectus provides you with detailed information about the Business Combination Agreement and other matters to be considered at the Special Meeting. We encourage you to read this entire proxy statement/prospectus, including the annexes and other documents referred to herein, carefully and in their entirety. You should also carefully consider the risk factors described in “Risk Factors” beginning on page 19 of this proxy statement/prospectus.

Inception Growth’s board of directors has unanimously approved the Business Combination Agreement and the Plan of Merger, and unanimously recommends that Inception Growth’s stockholders vote “FOR” approval of each of the Proposals. When you consider the Inception Growth board of director’s recommendation of these Proposals, you should keep in mind that Inception Growth’s directors and officers have interests in the Business Combination that may conflict or differ from your interests as a stockholder. See the section titled “Summary of the Proxy Statement/Prospectus — Interests of Certain Persons in the Business Combination.”

On behalf of Inception Growth’s board of directors, I thank you for your support and we look forward to the successful consummation of the Business Combination.

Sincerely, | ||

| ||

Cheuk Hang Chow |

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities to be issued in the Business Combination or otherwise, or passed upon the adequacy or accuracy of this proxy statement/prospectus. Any representation to the contrary is a criminal offense.

HOW TO OBTAIN ADDITIONAL INFORMATION

If you would like to receive additional information or if you want additional copies of this document, agreements contained in the appendices or any other documents filed by Inception Growth with the Securities and Exchange Commission, such information is available without charge upon written or oral request. Please contact our proxy solicitor, at:

Advantage Proxy, Inc.

P.O. Box 10904

Yakima, WA 98909

Individuals call toll-free: 1-877-870-8565

Brokers call: 1-206-870-8565

Email: ksmith@advantageproxy.com

If you would like to request documents, please do so no later than one week prior to the meeting date to receive them before the Special Meeting. Please be sure to include your complete name and address in your request. Please see the section titled “Where You Can Find Additional Information” to find out where you can find more information about Inception Growth, PubCo and AgileAlgo. You should rely only on the information contained in this proxy statement/prospectus in deciding how to vote on the Business Combination. None of Inception Growth, PubCo and AgileAlgo has authorized anyone to give any information or to make any representations other than those contained in this proxy statement/prospectus. Do not rely upon any information or representations made outside of this proxy statement/prospectus. The information contained in this proxy statement/prospectus may change after the date of this proxy statement/prospectus. Do not assume after the date of this proxy statement/prospectus that the information contained in this proxy statement/prospectus is still correct.

USE OF CERTAIN TERMS

Unless otherwise stated in this proxy statement/prospectus:

• References to “Exchange Consideration” refer to up to $160,000,000, the aggregate consideration for the Share Exchange, which is comprised of the Closing Consideration Payment and the Earnout Consideration;

• References to “AgileAlgo” refer to AgileAlgo Holdings Ltd. and, unless the context otherwise requires, to its subsidiaries;

• References to “AI” refer to artificial intelligence;

• References to “Business Combination” refer to the business combination between Inception Growth and AgileAlgo pursuant to the Business Combination Agreement;

• References to “Business Combination Agreement” refer to a Business Combination Agreement dated as of September 12, 2023, as supplemented by the Seller Joinders (as it may be amended from time to time), which provides for a Business Combination between Inception Growth and AgileAlgo;

• References to “CAGR” refer to compound annual growth rate;

• References to “Closing Consideration Payment” refer to a closing payment equal to One Hundred Forty Million Dollars ($140,000,000);

• References to “Closing Consideration Shares” refer to fourteen million (14,000,000) newly issued PubCo Ordinary Shares;

• References to “Closing Date” refer to the date on which the Business Combination is consummated;

• References to “Combined Company” refer to Purchaser and AgileAlgo as of the Closing;

• References to “Current Charter” refer to Inception Growth’s current amended and restated certificate of incorporation and bylaws;

• References to “Earnout Consideration Shares” refer to the aggregate of up to 2,000,000 newly issued PubCo Ordinary Shares (rounded to the nearest whole share) subject to the attainment of certain post-Closing targets and subject to the other terms set forth in the Business Combination Agreement;

• References to “EBITDA” refer to earnings before interest, taxes, depreciation and amortization;

• References to “Exchange Act” refer to the Securities Exchange Act of 1934, as amended;

• References to “IGTA Rights” refer to the rights of IGTA, each such right convertible into one-tenth (1/10) of one IGTA Share at the closing of a business combination;

• References to “IGTA Shares” refer to the shares of common stock, par value $0.0001 per share, of IGTA;

• References to “IGTA Units” refer to the units of IGTA, each such unit consisting of one IGTA Share, one-half of one IGTA Warrant and one IGTA Right;

• References to “IGTA Warrants” refer to the warrants of IGTA, each warrant to purchase one IGTA Share at a price of $11.50 per whole share;

• References to “Incentive Plan” refer to the AgileAlgo Corporation 2023 Employee Incentive Plan, attached to this proxy statement as Annex C;

• References to “Inception Growth” or “IGTA” refer to Inception Growth Acquisition Limited, a Delaware Corporation;

• References to “Initial Stockholders” refer to the Sponsor and all of Inception Growth’s officers and directors to the extent they hold IGTA Shares;

• References to “IPO” refer to the initial public offering of 10,350,000 units (including the over-allotment option) of Inception Growth consummated on December 13, 2021;

• References to “IT” refer to information technology;

• References to “Loeb” refer to Loeb & Loeb LLP;

• References to “LOI” refer to a letter of intent;

• References to “Note(s)” refer to any or all the promissory notes issued post-IPO by Inception Growth to the Sponsor, or its affiliates or designees, whether for working capital or for the payment of extension fees which, as of the date of this proxy statement/prospectus, is comprised of a non-interest bearing, unsecured promissory note in the principal amount of $200,000 issued by Inception Growth to the Sponsor on November 17, 2023;

• References to “Plan of Merger” refer respectively to the statutory plans of merger (including the applicable articles of merger and the memorandum and articles of association) to be filed with the Delaware Secretary of State and the British Virgin Islands Registrar of Corporate Affairs in connection with the Redomestication Merger;

• References to “proxy solicitor” refer to Advantage Proxy, Inc., Inception Growth’s proxy solicitor;

• References to “PubCo” refer to IGTA Merger Sub Limited, a British Virgin Islands business company and wholly owned subsidiary of Inception Growth (such company before the Redomestication Merger is sometimes referred to as “Purchaser” and upon and following the Redomestication Merger is hereinafter sometimes referred to as “PubCo”). ;

• References to “PubCo Ordinary Shares” refer to the ordinary shares of PubCo, par value $0.0001 each;

• References to “Redomestication Merger” refer to the redomestication of Inception Growth whereby Inception Growth will merge with and into Purchaser, with PubCo remaining as the surviving publicly traded entity;

• References to “Registration Statement” refer to Purchaser’s registration statement on Form S-4 (Registration No. [*]), of which this proxy statement/prospectus is a part;

• References to “Sellers” refer to the shareholders of AgileAlgo;

• References to “Share Exchange” refers to the share exchange between PubCo and the shareholders of AgileAlgo, whereby the shareholders of AgileAlgo will exchange all of their ordinary shares of AgileAlgo for up to an aggregate of sixteen million (16,000,000) ordinary shares of PubCo (including the Earnout Consideration Shares);

• References to “Sponsor” refer to Soul Venture Partners LLC;

• References to “Trust Account” refer to the trust account established pursuant to the Investment Management Trust Agreement dated December 8, 2021, between Inception Growth and Continental Stock Transfer and Trust Company, LLC, as amended;

• References to “US Dollars,” “$,” or “US$” refer to the legal currency of the United States; and

• References to “U.S. GAAP” refer to accounting principles generally accepted in the United States.

Unless otherwise noted, all translations from Singapore dollars to U.S. dollars and from U.S. dollars to Singapore dollars, as the case may be, in this proxy statement/prospectus are made at [*] Singapore dollars to US$1.00, representing the noon buying rate set forth in the H.10 statistical release of the U.S. Federal Reserve Board on [ ]. We make no representation that any of the aforementioned currencies could have been, or could be, converted into any of the other aforementioned currencies, at any particular rate, the rates stated above, or at all. On [ ], the noon buying rate for Singapore dollars was [ ] to US$1.00.

Inception Growth Acquisition Limited

875 Washington Street

New York,

NY 10014

Tel: (315) 636-6638

NOTICE OF SPECIAL MEETING OF STOCKHOLDERS

TO BE HELD ON [ ], 2023

TO THE STOCKHOLDERS OF INCEPTION GROWTH ACQUISITION LIMITED:

NOTICE IS HEREBY GIVEN that an Special Meeting of Stockholders of Inception Growth Acquisition Limited, a Delaware corporation (“Inception Growth”), will be held at [ ] on [ ], 2023 at [ ] AM/PM Eastern Time (“Special Meeting”) and virtually using the following dial-in information:

US Toll Free | [ ] | |||

International Toll | [ ] | |||

Participant Passcode | [ ] |

The Inception Growth Board has determined to utilize virtual stockholder meeting technology, and encourages stockholders to attend the Special Meeting virtually. We encourage stockholders to attend the Special Meeting virtually. This proxy statement includes instructions on how to access the virtual Special Meeting and how to listen and vote from home or any remote location with Internet connectivity.

The Special Meeting will be held for the purposes of considering and voting upon, and if through fit passing and approving, the following resolutions that:

I. the redomestication of Inception Growth from Delaware to the British Virgin Islands, to be accomplished by the merger of Inception Growth with and into IGTA Merger Sub Limited, a British Virgin Islands business company and wholly owned subsidiary of Inception Growth (such company before the Business Combination is referred to as “Purchaser” and upon and following the Share Exchange is hereinafter sometimes referred to as “PubCo”), with PubCo surviving the merger, be approved and authorized in all respects and that the Plan of Merger, a copy of which is included as Annex A2 to the accompanying proxy statement/prospectus, and any and all transactions provided for in the Plan of Merger, be and is hereby authorized and any director and/or officer of Inception Growth be and is hereby authorized to execute the Plan of Merger, for and on behalf of Inception Growth, with such changes therein and additions thereto as any director and/or officer of Inception Growth may deem necessary, appropriate or advisable, such determinations to be evidenced conclusively by his/her execution thereof. We refer to this merger as the Redomestication Merger. This proposal is referred to as the Redomestication Merger Proposal or Proposal No. 1. Holders of IGTA Shares as of the record date are entitled to vote on this proposal.

II. the exchange of up to 16,000,000 PubCo Ordinary Shares for all the issued and outstanding ordinary shares of AgileAlgo, resulting in AgileAlgo becoming a wholly owned subsidiary of PubCo, be approved and authorized in all respect and that PubCo’s board of directors be and is hereby authorized to take any such actions as may be necessary to complete the share exchange merger. We refer to this transaction as the as the “Share Exchange”. This proposal is referred to as the Share Exchange Proposal or Proposal No. 2. Holders of IGTA Shares as of the record date are entitled to vote on this proposal.

III. for purposes of complying with applicable listing rules of The Nasdaq Stock Market LLC, the issuance of up to an aggregate of 16,000,000 PubCo Ordinary Shares by PubCo as the surviving entity in connection with the Business Combination be approved and authorized in all respect. We refer to this proposal as the Nasdaq Proposal or Proposal No. 3. Holders of IGTA Shares as of the record date are entitled to vote on this proposal.

IV. at the effective time of the Redomestication Merger, (i) the amendment and restatement of the memorandum and articles of association of PubCo by deletion in their entirety and the substitution in their place of the amended and restated memorandum and articles of association of PubCo (as the surviving entity) in the form attached to this proxy statement/prospectus as Annex B2 to the Plan of Merger, and (ii) the adoption of the new name by PubCo as “Prodigy, Inc.,” be and is hereby approved. We refer to this proposal as the Governance Proposal or Proposal No. 4. Holders of IGTA Shares as of the record date are entitled to vote on this proposal.

V. the Incentive Plan be and is hereby approved for adoption by PubCo as the surviving entity of the Redomestication Merger with effect from the closing of the Business Combination. We refer to this proposal to approve the Incentive Plan as the Incentive Plan Proposal or Proposal No. 5. Holders of IGTA Shares as of the record date are entitled to vote on this proposal.

VI. the amendment and restatement of the certificate of incorporation of Inception Growth by deletion in its entirety and the substitution in its place of the second amended and restated certificate of incorporation of Inception Growth in the form attached as Annex D, in order to eliminate from Inception Growth’s certificate of incorporation the limitation that it shall not redeem Public Shares to the extent that such redemption would cause Inception Growth’s net tangible assets to be less than $5,000,001, and to expand the methods that Inception Growth may employ to not become subject to the “penny stock” rules of the Securities and Exchange Commission, be and is hereby approved. We refer to this proposal to amend and restate Inception Growth’s certificate of incorporation as the NTA Requirement Amendment Proposal or Proposal No. 6. Holders of IGTA Shares as of the record date are entitled to vote on this proposal.

VII. the appointment of six (6) directors of PubCo, namely Tay Yee Paa Tony, Lee Wei Chiang Francis, Lim Chee Heong, Loo Choo Leong, [*] and [*], assuming the Redomestication Merger Proposal, the Share Exchange Proposal and the Nasdaq Proposal are all approved, effective upon the Closing, be and is hereby approved. We refer to this proposal to appoint directors of PubCo as the Director Appointment Proposal or Proposal No. 7. Holders of IGTA Shares as of the record date are entitled to vote on this proposal.

VIII. the Special Meeting be adjourned to a later date or dates to be determined by the chairman of the Special Meeting as necessary, including without limitation (a) to permit further solicitation and vote of proxies in the event Inception Growth does not receive the requisite stockholder vote to approve any of the above Proposals; (b) to the extent necessary, to ensure that any required supplement or amendment to the accompanying proxy statement/prospectus is provided to Inception Growth stockholders, or (c) if, as of the time for which the Special Meeting is scheduled, there are insufficient IGTA Shares represented (either in person or by proxy) to constitute a quorum necessary to conduct business at the Special Meeting. This proposal is called the Adjournment Proposal or Proposal No. 8. Holders of IGTA Shares as of the record date are entitled to vote on this proposal.

All of the proposals set forth above are sometimes collectively referred to herein as the “Proposals.” The Redomestication Merger Proposal and the Share Exchange Proposal are dependent upon each other. It is important for you to note that in the event that either of the Redomestication Merger Proposal or the Share Exchange Proposal is not approved, then Inception Growth will not consummate the Business Combination. If Inception Growth does not consummate the Business Combination and fails to complete an initial business combination by June 13, 2024 (30 months after the consummation of the IPO, if Inception Growth extends the period in full, as further described herein), Inception Growth will be required to dissolve and liquidate. As disclosed in Inception Growth’s prospectus in relation to the IPO, Inception Growth originally had 15 months after the consummation of the IPO to consummate an initial business combination and may extend such period to a total of 21 months after the consummation of the IPO by depositing certain sum into its trust account. As approved by its stockholders at the annual meeting of Stockholders held on March 13, 2023, Inception Growth entered into an amendment to the investment management trust agreement, dated December 8, 2021 (the “Trust Agreement”), on March 13, 2023 with Continental Stock Transfer & Trust Company, giving Inception Growth the right to extend the time to complete a business combination for a period of six months from March 13, 2023 to September 13, 2023 without having to make any payment to the trust account. Subsequently on September 8, 2023 at a special meeting of stockholders, Inception Growth’s stockholders approved an amendment of Inception Growth’s certificate of incorporation and a further amendment to the Trust Agreement, such that Inception Growth has the right to extend the date by which it has to consummate a business combination by nine times for an additional one (1) month each time from September 13, 2023 to June 13, 2024 by depositing into the trust account the lesser of (i) $100,000 and (ii) an aggregate amount equal to $0.04 multiplied by the number of Public Share that has not been redeemed for each one-month extension. On each of September 8, 2023, October 5, 2023 and November 1, 2023, Inception Growth deposited $100,000 into Inception Growth’s trust account in order to extend the amount of time it has available to complete a business combination. Currently, Inception Growth has until December 13, 2023 to complete a business combination.

As of [ ], the record date, there were [ ] IGTA Shares issued and outstanding and entitled to vote. Only Inception Growth’s stockholders who hold shares of record as of the close of business on [ ] are entitled to vote at the Special Meeting or any adjournment of the Special Meeting. This proxy statement/prospectus is first being mailed to Inception Growth’s stockholders on or about [ ]. Approval of each of the Proposals (other than the NTA Requirement Amendment Proposal) will require the affirmative vote of the holders of a majority of the issued and

outstanding IGTA Shares present and entitled to vote at the Special Meeting or any adjournment thereof; and approval of the NTA Requirement Amendment Proposal will require the affirmative vote of the holders of at least sixty-five percent (65%) of the issued and outstanding IGTA Shares present and entitled to vote; provided, however, that if holders of [ ] or more of the IGTA Shares purchased in the IPO demand redemption of their IGTA Shares, then the Business Combination may not be completed. Assuming that a quorum is present, attending the Special Meeting either in person (including by virtual presence) or by proxy and abstaining from voting will have no effect on any of the Proposals and failing to instruct your bank, brokerage firm or nominee to attend and vote your shares will have no effect on any of the Proposals.

Whether or not you plan to attend the Special Meeting in person (including by virtual presence), please submit your proxy card without delay to the proxy solicitor not later than the time appointed for the Special Meeting or adjourned meeting. Voting by proxy will not prevent you from voting your shares in person if you subsequently choose to attend the Special Meeting. If you fail to return your proxy card and do not attend the Special Meeting in person, the effect will be that your shares will not be counted for purposes of determining whether a quorum is present at the Special Meeting. You may revoke a proxy at any time before it is voted at the Special Meeting by executing and returning a proxy card dated later than the previous one, by attending the Special Meeting in person and casting your vote by ballot or by submitting a written revocation to the proxy solicitor, that is received by the proxy solicitor before we take the vote at the Special Meeting. If you hold your shares through a bank or brokerage firm, you should follow the instructions of your bank or brokerage firm regarding revocation of proxies.

The Inception Growth Board unanimously recommends that you vote “FOR” approval of each of the Proposals.

By order of the Board of Directors, | ||

| ||

Cheuk Hang Chow | ||

[ ], 2023 |

i

Page | ||

187 | ||

188 | ||

188 | ||

F-1 | ||

A-1-1 | ||

A-2-1 | ||

ANNEX B — PUBCO AMENDED AND RESTATED MEMORANDUM AND ARTICLES OF ASSOCIATION | B-1 | |

C-1 | ||

ANNEX D — INCEPTION GROWTH’S SECOND AMENDED AND RESTATED CERTIFICATE OF INCORPORATION | D-1 | |

II-1 |

ii

ABOUT THIS PROXY STATEMENT/PROSPECTUS

This document, which forms part of a registration statement on Form S-4 filed by PubCo (File No. 333-[ ]) with the SEC, constitutes a prospectus of PubCo under Section 5 of the Securities Act, with respect to the issuance of (i) the PubCo Ordinary Shares to Inception Growth’s stockholders, (ii) the PubCo Ordinary Shares to the shareholders of AgileAlgo under the Business Combination Agreement, (iii) the PubCo Warrants to holders of IGTA Warrants in exchange for the IGTA Warrants, and (iv) the PubCo Ordinary Shares underlying the PubCo Warrants and the PubCo Rights, in each instance if the Business Combination is consummated. This document also constitutes a notice of meeting and a proxy statement under Section 14(a) of the Exchange Act, with respect to the Special Meeting at which Inception Growth’s stockholders will be asked to consider and vote upon the Proposals to approve the Redomestication Merger, the Share Exchange, the Nasdaq Proposal and the Incentive Plan Proposal.

This proxy statement/prospectus does not constitute an offer to sell, or a solicitation of an offer to buy, any securities, or the solicitation of a proxy, in any jurisdiction to or from any person to whom it is not lawful to make any such offer or solicitation in such jurisdiction.

iii

WHERE YOU CAN FIND MORE INFORMATION

After the consummation of the Business Combination, PubCo will be required to file its Annual Report on Form 10-K with the SEC no later than 90 days following its fiscal year end. Inception Growth files reports, proxy statements and other information with the SEC as required by the Exchange Act. You can read Inception Growth’s SEC filings, including this proxy statement/prospectus, over the Internet at the SEC’s website at http://www.sec.report.

Information and statements contained in this proxy statement/prospectus, or any annex to this proxy statement/prospectus, are qualified in all respects by reference to the copy of the relevant contract or other annex filed with this proxy statement/prospectus.

If you would like additional copies of this proxy statement/prospectus, or if you have questions about the Business Combination, you should contact the proxy solicitor, Advantage Proxy, individual call toll-free at 1-877-870-8565 and banks and brokers call at 1-206-870-8565.

All information contained in this proxy statement/prospectus relating to Inception Growth and PubCo has been supplied by Inception Growth, and all such information relating to AgileAlgo has been supplied by AgileAlgo. Information provided by either of Inception Growth or AgileAlgo does not constitute any representation, estimate or projection of the other party.

Neither Inception Growth, PubCo nor AgileAlgo has authorized anyone to give any information or make any representation about the Business Combination or their companies that is different from, or in addition to, that contained in this proxy statement/prospectus or in any of the materials that have been incorporated into this proxy statement/prospectus by reference. Therefore, if anyone does give you any such information, you should not rely on it. If you are in a jurisdiction where offers to exchange or sell, or solicitations of offers to exchange or purchase, the securities offered by this proxy statement/prospectus or the solicitation of proxies is unlawful, or if you are a person to whom it is unlawful to direct these types of activities, then the offer presented in this proxy statement/prospectus does not extend to you. The information contained in this proxy statement/prospectus speaks only as of the date of this proxy statement/prospectus unless the information specifically indicates that another date applies.

iv

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This proxy statement/prospectus contains forward-looking statements, including statements about the parties’ ability to close the Business Combination, the anticipated benefits of the Business Combination, the financial conditions, results of operations, earnings outlook and prospects of PubCo, Inception Growth and/or AgileAlgo and may include statements for the period following the consummation of the Business Combination. Forward-looking statements appear in a number of places in this proxy statement/prospectus including, without limitation, in the sections titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations of AgileAlgo,” and “Business of AgileAlgo.” In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. Forward-looking statements are typically identified by words such as “plan,” “believe,” “expect,” “anticipate,” “intend,” “outlook,” “estimate,” “forecast,” “project,” “continue,” “could,” “may,” “might,” “possible,” “potential,” “predict,” “should,” “would” and other similar words and expressions, but the absence of these words does not mean that a statement is not forward-looking.

The forward-looking statements are based on the current expectations of the management of Inception Growth and AgileAlgo, as applicable, and are inherently subject to uncertainties and changes in circumstances and their potential effects and speak only as of the date of such statement. There can be no assurance that future developments will be those that have been anticipated. These forward-looking statements involve a number of risks, uncertainties or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to, those factors described in “Risk Factors,” those discussed and identified in public filings made with the SEC by Inception Growth and the following:

• expectations regarding AgileAlgo’s strategies and future financial performance, including AgileAlgo’s future business plans or objectives, prospective performance and opportunities and competitors, revenues, customer acquisition and retention, products and services, pricing, marketing plans, operating expenses, market trends, liquidity, cash flows and uses of cash, capital expenditures, and AgileAlgo’s ability to invest in growth initiatives and pursue acquisition opportunities;

• anticipated trends, growth rates, and challenges in the nutraceutical industry in general and the markets in which AgileAlgo operates;

• AgileAlgo’s ability to stay in compliance with laws and regulations that currently apply or become applicable to its business in its current markets, both within the United States and internationally, including but not limited to the laws enforced by the United States and Singapore;

• the occurrence of any event, change or other circumstances that could give rise to the termination of the Business Combination Agreement;

• the outcome of any legal proceedings that may be instituted against AgileAlgo, Inception Growth and others following announcement of the Business Combination Agreement and transactions contemplated therein;

• the inability to complete the Business Combination due to the failure to obtain approval by the stockholders of Inception Growth;

• the risk that the proposed Business Combination disrupts current plans and operations of AgileAlgo as a result of the announcement and consummation of the Business Combination;

• the ability to recognize the anticipated benefits of the Business Combination;

• unexpected costs related to the proposed Business Combination;

• the amount of any redemptions by existing holders of IGTA Shares being greater than expected;

• the management and board composition of PubCo following the proposed Business Combination;

• the ability to list PubCo’s securities on Nasdaq;

• limited liquidity and trading of Inception Growth’s and PubCo’s securities;

v

• geopolitical risk and changes in applicable laws or regulations;

• the possibility that AgileAlgo, PubCo and/or Inception Growth may be adversely affected by other economic, business, and/or competitive factors;

• operational risk;

• litigation and regulatory enforcement risks, including the diversion of management time and attention and the additional costs and demands on AgileAlgo’s resources;

• fluctuations in exchange rates between the foreign currencies in which AgileAlgo typically does business the United States dollar; and

• the risks that the consummation of the Business Combination is substantially delayed or does not occur.

Should one or more of these risks or uncertainties materialize, or should any of the assumptions made by the management of Inception Growth, AgileAlgo and PubCo prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements.

All subsequent written and oral forward-looking statements concerning the Business Combination or other matters addressed in this proxy statement/prospectus and attributable to AgileAlgo, Inception Growth, PubCo or any person acting on their behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this proxy statement/prospectus. Except to the extent required by applicable law or regulation, PubCo, AgileAlgo and Inception Growth undertake no obligation to update these forward-looking statements to reflect events or circumstances after the date of this proxy statement/prospectus or to reflect the occurrence of unanticipated events.

vi

QUESTIONS AND ANSWERS ABOUT THE BUSINESS COMBINATION AND THE SPECIAL MEETING

Q: What is the purpose of this document?

A: Inception Growth is proposing to consummate the Business Combination. The Business Combination consists of the Redomestication Merger and the Share Exchange, each of which is described in this proxy statement/prospectus. In addition, the Business Combination Agreement and the Plan of Merger are attached to this proxy statement/prospectus as Annex A1 and Annex A2, respectively, and are incorporated into this proxy statement/prospectus by reference. This proxy statement/prospectus contains important information about the proposed Business Combination and the other matters to be acted upon at the Special Meeting. You are encouraged to carefully read this proxy statement/prospectus, including “Risk Factors” and all the annexes hereto.

Approval of the Redomestication Merger and the Share Exchange will each require the affirmative vote of the holders of a majority of the issued and outstanding IGTA Shares present and entitled to vote at the Special Meeting or any adjournment thereof; provided, however, that if holders of [ ] or more IGTA Shares exercise their redemption rights then the Business Combination may not be completed.

Q: What is being voted on at the Special Meeting?

A: Below are the Proposals that the Inception Growth’s stockholders are being asked to vote on:

• The Redomestication Merger Proposal to approve the Redomestication Merger and the Plan of Merger;

• The Share Exchange Proposal to approve the Share Exchange;

• The Nasdaq Proposal to approve the issuance of up to an aggregate of 16,000,000 PubCo Ordinary Shares in connection with the Business Combination;

• The Governance Proposal to approve and adopt, on a non-binding advisory basis, certain differences in the governance provisions set forth in PubCo’s Memorandum and Articles of Association to be adopted by PubCo upon the effective time of the Redomestication Merger and the change of PubCo’s name to “Prodigy, Inc.”;

• The Incentive Plan Proposal to approve PubCo’s 2023 Equity Incentive Plan;

• The NTA Requirement Amendment Proposal to remove the NTA Requirement from Inception Growth’s Certificate of Incorporation;

• The Director Appointment Proposal to elect six (6) Directors of PubCo; and

• The Adjournment Proposal to approve the adjournment of the Special Meeting in the event Inception Growth does not receive the requisite stockholder vote to approve the above Proposals.

Approval of each of the Proposals (other than the NTA Requirement Amendment Proposal) requires the affirmative vote of the holders of a majority of the issued and outstanding IGTA Shares present and entitled to vote at the Special Meeting or any adjournment thereof; and approval of the NTA Requirement Amendment Proposal will require the affirmative vote of the holders of at least sixty-five percent (65%) of the issued and outstanding IGTA Shares present and entitled to vote; provided, however, that if holders of [ ] or more IGTA Shares exercise their redemption rights then the Business Combination may not be completed. As of the record date, [ ] shares held by the Initial Stockholders, including the Sponsor and all of Inception Growth’s officers and directors to the extent they hold IGTA Shares (the “Initial Stockholders”), or approximately [ ]% of the outstanding IGTA Shares, would be voted in favor of each of the Proposals.

Q: Are any of the proposals conditioned on one another?

A: Yes, the Redomestication Merger Proposal and the Share Exchange Proposal are dependent upon each other. The Nasdaq Proposal, the Governance Proposal, the Incentive Plan Proposal, the NTA Requirement Amendment Proposal and the Director Appointment Proposal are dependent on the Redomestication Merger Proposal and the Share Exchange Proposal. It is important for you to note that in the event that either of the Redomestication Merger Proposal or the Share Exchange Proposal is not approved, Inception Growth will not consummate the Business Combination. If Inception Growth does not consummate the Business Combination and fails to complete an initial business combination by June 13, 2024 (30 months after the consummation of the IPO, if

vii

Inception Growth extends the period in full, as further described herein), Inception Growth will be required to dissolve and liquidate. Adoption of the Adjournment Proposal is not conditioned upon the adoption of any of the other Proposals.

Q: Do any of Inception Growth’s directors or officers have interests that may conflict with my interests with respect to the Business Combination?

• On September 12, 2023, contemporaneously with the execution of the Business Combination Agreement, Inception Growth’s Initial Stockholders entered into a Sponsor Support Agreement, pursuant to which, among other things, such stockholders agree not to exercise any right to redeem all or a portion of their respective IGTA Shares in connection with the Business Combination. Inception Growth did not provide any separate consideration to the Initial Stockholders for such forfeiture of redemption rights.

• The Initial Stockholders have waived their rights to redeem their IGTA Shares (including shares underlying IGTA Units), or to receive distributions with respect to these shares upon the liquidation of the Trust Account if Inception Growth is unable to consummate a business combination. Accordingly, the IGTA Shares, as well as the IGTA Units purchased by the Sponsor and Inception Growth’s officers and directors, will be worthless if Inception Growth does not consummate a business combination;

• If the proposed Business Combination is not completed by June 13, 2024 (30 months after the consummation of the IPO, if Inception Growth extends the period in full, as further described herein), Inception Growth will be required to liquidate. In such event, the 1,303,490 IGTA Shares held by the Initial Stockholders, which were acquired prior to the IPO for an aggregate purchase price of $25,000, or approximately $0.001 per share, will be worthless. Such shares had an aggregate market value of approximately $[ ] based on the closing price of IGTA Shares of $[ ] on Nasdaq as of [ ], 2023. Upon the consummation of the Business Combination, among other things, each of the then issued and outstanding IGTA Shares will convert automatically, on a one-for-one basis, into one PubCo Ordinary Share. In the event the share price of PubCo Ordinary Shares falls below the price paid by an Inception Growth stockholder at the time of purchase of the IGTA Shares by such stockholder, a situation may arise in which the Sponsor or a director of Inception Growth maintains a positive rate of return on its/his/her IGTA Shares while such Inception Growth stockholder experiences a negative rate of return on the shares such Inception Growth stockholder purchased;

• If the proposed Business Combination is not completed by June 13, 2024 (30 months after the consummation of the IPO, if Inception Growth extends the period in full, as further described herein), the 4,721,250 Private Warrants purchased by the Sponsor for a total purchase price of $4,721,250, will be worthless. Such Private Warrants had an aggregate market value of approximately $[ ] based on the closing price of IGTA Warrants of $[ ] on Nasdaq as of [ ], 2023; and

• As a result of the interests of the Sponsor and Inception Growth’s directors and officers in Inception Growth’s securities, the Sponsor and Inception Growth’s directors and officers have an incentive to complete an initial business combination and may have a conflict of interest in the transaction, including without limitation, in determining whether a particular business is an appropriate business with which to effect Inception Growth’s initial business combination.

None of Inception Growth’s officers and directors has or will have any interest in, or affiliation with, PubCo. For a discussion of the fiduciary or contractual obligations that such persons may have to other entities, please see “Directors, Executive Officers, Executive Compensation and Corporate Governance of Inception Growth — Conflicts of Interest.”

Q: What is the Exchange Consideration and what will AgileAlgo Shareholders receive in return for the Business Combination?

A: At the Closing, among other things, by virtue of the Share Exchange and without any action on the part of Inception Growth or AgileAlgo, each ordinary share of AgileAlgo (“AgileAlgo Ordinary Share”) issued and outstanding immediately prior to the Closing shall be exchanged for the applicable number of PubCo Ordinary Shares as specified in the Business Combination Agreement. After Closing, each AgileAlgo Shareholder will cease to have any rights with respect to AgileAlgo Ordinary Shares, except the right to receive the Exchange Consideration. The Exchange Consideration shall be comprised of the Closing Consideration Shares, comprising 14,000,000

viii

PubCo Ordinary Shares which shall be issued at the Closing, and up to 2,000,000 Earnout Consideration Shares which shall be issued at Closing and held in escrow as potential additional consideration for the Share Exchange, subject to the attainment of certain contingent payment targets as further described in the Business Combination Agreement. For further details, see “Proposal No. 2: The Share Exchange Proposal — General Description of the Share Exchange — Share Exchange with AgileAlgo; Share Exchange Consideration.”

Q: What are the Earnout Consideration Shares and under what circumstances will the Earnout Consideration Shares be issued?

A: “Earnout Consideration Shares” refer to contingent shares that may be issued as part of a business combination from one party (usually the purchaser) to another (usually the seller) if certain financial or commercial conditions or milestones laid out in a business combination agreement are met. In this case, in connection with the Business Combination and pursuant to the Business Combination Agreement, up to an additional 2,000,000 Earnout Consideration Shares may be paid to the AgileAlgo Shareholders as contingent post-closing earnout consideration. All of the Earnout Consideration Shares will be released to the AgileAlgo shareholders if PubCo’s consolidated gross revenues as reported in the Purchaser’s quarterly reports on Form 10-Q and/or annual report on Form 10-K as filed with the SEC (the “Gross Revenues”) equal or exceed $15,000,000 (the “Full Earnout Target”) during the three (3) fiscal quarter period beginning on October 1, 2024 (the “Earnout Period”). If PubCo’s Gross Revenues during the Earnout Period are greater than $7,500,000 (the “Minimum Earnout Target”) but less than the Full Earnout Target, then a portion of the Earnout Consideration Shares, expressed as a percentage, equal to (i) (A) the Gross Revenues minus (B) the Minimum Earnout Target, divided by (ii) (A) the Full Earnout Target less (B) the Minimum Earnout Target shall vest and be payable from the Escrow Account to the Sellers. If the Gross Revenues during the Earnout Period are less than the Minimum Earnout Target, then all of the Earnout Consideration Shares will be surrendered to PubCo and no Earnout Consideration will be paid.

The Sellers will have all voting rights in respect to the Earnout Consideration Shares, and to receive dividends thereon, while the Earnout Consideration Shares are held in escrow.

For further details, see “Proposal No. 2: The Share Exchange Proposal — General Description of the Share Exchange — Share Exchange with AgileAlgo; Share Exchange Consideration.”

Q: When and where is the Special Meeting?

A: The Special Meeting will take place at [ ] on [ ], 2023, and virtually in a virtual meeting format using the following dial-in information. Due to the COVID-19 pandemic, stockholders are encouraged to attend the Special Meeting virtually:

US Toll Free | [ ] | |||

International Toll | [ ] | |||

Participant Passcode | [ ] |

This proxy statement includes instructions on how to access the virtual Special Meeting and how to listen and vote from home or any remote location with Internet connectivity.

Q: Who may vote at the Special Meeting?

A: Only holders of record of IGTA Shares as of the close of business on [ ], 2023 (the record date) may vote at the Special Meeting. As of [ ], 2023, there were [ ] IGTA Shares outstanding and entitled to vote. Please see the section titled “The Special Meeting of Inception Growth stockholders — Record Date; Who is Entitled to Vote” for further information.

Q: What is the quorum requirement for the Special Meeting?

A: Stockholders representing a majority of the shares of capital issued and outstanding as of the record date and entitled to vote at the Special Meeting must be present in person (including by virtual presence) or represented by proxy in order to hold the Special Meeting and conduct business. This is called a quorum. IGTA Shares will be counted for purposes of determining if there is a quorum if the stockholder (i) is present and entitled to vote at the meeting, or (ii) has properly submitted a proxy card or voting instructions through a broker, bank or custodian. In the absence of a quorum within two hours from the time appointed for the meeting, the Special

ix

Meeting will be adjourned to a business day at the same time and place, or to such other time and place as the directors may determine. As of the date of this proxy statement/prospectus, the Initial Stockholders own [ ]% of the issued and outstanding IGTA Shares. The Initial Stockholders have agreed to vote any IGTA Shares owned by them in favor of the Redomestication Merger Proposal and the Share Exchange Proposal and, accordingly, their shares will be counted towards the quorum.

Q: What vote is required to approve the Proposals?

A: Approval of each of the Proposals (other than the NTA Requirement Amendment Proposal) will require the affirmative vote of the holders of a majority of the issued and outstanding IGTA Shares present and entitled to vote at the Special Meeting or any adjournment thereof; and approval of the NTA Requirement Amendment Proposal will require the affirmative vote of the holders of at least sixty-five percent (65%) of the issued and outstanding IGTA Shares present and entitled to vote. Since each of the Proposals require the affirmative vote of a at least a majority of the IGTA Shares present and entitled to vote at the Special Meeting or any adjournment thereof, attending the Special Meeting either in person (including by virtual presence) or by proxy and abstaining from voting will have no effect on the Proposals and failing to instruct your bank, brokerage firm or nominee to attend and vote your shares will have no effect on any of the Proposals. As of the date of this proxy statement/prospectus, the Initial Stockholders own [ ]% of the issued and outstanding IGTA Shares. The Initial Stockholders have agreed to vote any IGTA Shares owned by them in favor of the Redomestication Merger Proposal and the Share Exchange Proposal and, accordingly, we would need only [ ], or [ ]%, of the [ ] Public Shares to be voted in favor of the Redomestication Merger Proposal and only [ ], or [ ]%, of the [ ] Public Shares to be voted in favor of the Share Exchange Proposal in order to have them approved (assuming that only a quorum was present at the meeting). The Initial Stockholders have indicated that they will vote their IGTA Shares in favor of the NTA Requirement Amendment Proposal, although they are not legally bound to do so. Assuming that the Initial Stockholders do vote all of their IGTA Shares in favor of the NTA Requirement Amendment Proposal, we would need only [ ], or [ ]%, of the [ ] Public Shares to be voted in favor of the Share Exchange Proposal in order to have it approved (assuming that only a quorum was present at the meeting).

Q: Why did Inception Growth add the NTA Requirement Amendment Proposal?

A: The NTA Requirement Amendment Proposal seeks to amend and restate Inception Growth’s certificate of incorporation to expand the methods that Inception Growth may employ to not become subject to the “penny stock” rules of the Securities and Exchange Commission. As disclosed in Inception Growth’s IPO prospectus, because the net proceeds of the IPO were to be used to complete an initial business combination with a target business that had not been selected at the time of the IPO, Inception Growth may be deemed to be a “blank check company.” Under Rule 419 of the Securities Act the term “blank check company” means a company that (i) is a development stage company that has no specific business plan or purpose or has indicated that its business plan is to engage in a merger or acquisition with an unidentified company or companies, or other entity or person; and (ii) is issuing “penny stock,” as defined in Rule 3a51-1 under the Exchange Act. Rule 3a51-1 sets forth that that term “penny stock” shall mean any equity security, unless it fits within certain enumerated exclusions including (1) the company has net tangible assets of at least $5,000,001 (the “NTA Rule”) or (2) the company is listed on the Nasdaq Stock Market (Rule 3a51-1(a)(2)) (the “Exchange Rule”). Historically, SPACs have relied upon the NTA Rule to avoid being deemed a penny stock issuer. Inception Growth is proposing to amend and restate its charter to remove the NTA Requirement in order to expand its options to be excluded from the “penny stock” rules by relying upon either the NTA Rule or the Exchange Rule. Inception Growth is asking its stockholders to vote on the NTA Requirement Amendment Proposal now, because based on the pro forma financial statements of PubCo, PubCo may not be able to satisfy the NTA Rule. Therefore, Inception Growth intends to rely on the Exchange Rule to not be deemed a penny stock issuer. Approval of the NTA Requirement Amendment Proposal will require the affirmative vote of the holders of at least sixty-five percent (65%) of the issued and outstanding IGTA Shares present and entitled to vote.

Q: How will the Initial Stockholders vote?

A: Inception Growth’s Initial Stockholders, who as of the record date, owned [*] IGTA Shares, or approximately [*]% of the issued and outstanding IGTA Shares, have agreed to vote their respective shares acquired by them prior to the IPO in favor of the Redomestication Merger Proposal, Share Exchange Proposal and other related proposals. The Initial Stockholders have also agreed that they will vote any shares they purchase in the open market in or after the IPO in favor of each of the Proposals.

x

Q: What do I need to do now?

A: We urge you to read carefully and consider the information contained in this proxy statement/prospectus, including the annexes, and consider how the Business Combination will affect you as an Inception Growth stockholder. You should vote as soon as possible in accordance with the instructions provided in this proxy statement/prospectus and on the enclosed proxy card.

Q: Do I need to attend the Special Meeting to vote my shares?

A: No. You are invited to attend the Special Meeting to vote on the Proposals described in this proxy statement/prospectus. However, you do not need to attend the Special Meeting to vote your IGTA Shares. Instead, you may submit your proxy by signing, dating and returning the applicable enclosed proxy card in the pre-addressed postage paid envelope. Your vote is important. Inception Growth encourages you to vote as soon as possible after carefully reading this proxy statement/prospectus.

Q: Am I required to vote against the Redomestication Merger and the Share Exchange Proposal in order to have my IGTA Shares redeemed?

A: No. You are not required to vote against the Redomestication Merger Proposal and the Share Exchange Proposal in order to have the right to demand that Inception Growth redeem your IGTA Shares for cash equal to your pro rata share of the aggregate amount then on deposit in the Trust Account (including interest earned on your pro rata portion of the Trust Account, net of taxes payable) before payment of deferred underwriting commissions. You will be entitled to redeem your IGTA Shares for cash in connection with this vote whether or not you vote or abstain to vote on the Redomestication Merger Proposal and the Share Exchange Proposal so long as you elect to redeem your public shares for a pro rata portion of the funds available in the Trust Account in connection with the Business Combination. These redemption rights in respect of the IGTA Shares are sometimes referred to herein as “redemption rights.” If the Business Combination is not completed, holders of IGTA Shares electing to exercise their redemption rights will not be entitled to receive such payments and their IGTA Shares will be returned to them.

Q: How do I exercise my redemption rights?

A: If you are a public stockholder and you seek to have your shares redeemed, you must (i) demand, no later than 5:00 p.m., Eastern time on [ ], 2023 (two business days before the Special Meeting), that Inception Growth redeem your shares for cash, and (ii) submit your request in writing to Inception Growth’s transfer agent, at the address listed at the end of this section and deliver your shares to Inception Growth’s transfer agent (physically, or electronically using the DWAC (Deposit/Withdrawal At Custodian) system) at least two business days prior to the vote at the Special Meeting.

Any corrected or changed written demand of redemption rights must be received by Inception Growth’s transfer agent two business days prior to the Special Meeting. No demand for redemption will be honored unless the holder’s shares have been delivered (either physically or electronically) to the transfer agent at least two business days prior to the vote at the Special Meeting.

Public stockholders may seek to have their shares redeemed regardless of whether they vote for or against, or abstain from voting on, the Business Combination and whether or not they are holders of IGTA Shares as of the record date. Any public stockholder who holds IGTA Shares on or before [ ], 2023 (two business days before the Special Meeting) will have the right to demand that his, her or its shares be redeemed for a pro rata share of the aggregate amount then on deposit in the Trust Account, less any taxes then due but not yet paid, at the consummation of the Business Combination. If you have questions regarding the certification of your position or delivery of your shares, please contact:

Continental Stock Transfer & Trust Company, LLC

1 State Street 30th Floor

New York, NY 10004-1561

Attn: Michael Goedecke

E-mail: mgoedecke@continentalstock.com

Inception Growth stockholders holding both IGTA Shares and IGTA Warrants may redeem their IGTA Shares but retain the IGTA Warrants, which, if the Business Combination closes, will become PubCo Warrants. Assuming that 100% of IGTA Shares held by Inception Growth stockholders were to be redeemed, the [ ]

xi

retained outstanding IGTA Warrants, which will be automatically and irrevocably assigned to, and assumed by, PubCo following the Closing of the Business Combination, would have an aggregate value of $[ ] million, based on a price per IGTA Warrants of $[ ] on [ ], 2023, the most recent practicable date prior to the date of this proxy statement/prospectus. In addition, on [ ], 2023, the most recent practicable date prior to the date of this proxy statement/prospectus, the price per share of IGTA Shares closed at $[ ]. If PubCo Ordinary Shares are trading above the exercise price of $11.50 per warrant, the PubCo Warrants are considered to be “in the money” and are therefore more likely to be exercised by the holders thereof (when they become exercisable upon the later of one year after the closing of Inception Growth’s IPO or Closing of the Business Combination) and this in turn increases the risk to non-redeeming stockholders that the PubCo Warrants will be exercised, which would result in immediate dilution to the non-redeeming stockholders.

Q: How can I vote?

A: If you were a holder of record of IGTA Shares on [ ], 2023, the record date for the Special Meeting, you may vote with respect to the Proposals in person (including by virtual presence) at the Special Meeting, or by submitting a proxy by mail so that it is received prior to 10:00 a.m. Eastern Time on [ ], 2023, in accordance with the instructions provided to you under the section titled “The Special Meeting.” If you hold your shares in “street name,” which means your shares are held of record by a broker, bank or other nominee, your broker or bank or other nominee may provide voting instructions (including any telephone or Internet voting instructions). You should contact your broker, bank or nominee in advance to ensure that votes related to the shares you beneficially own will be properly counted. In this regard, you must provide the record holder of your shares with instructions on how to vote your shares or, if you wish to attend the Special Meeting and vote in person (including by virtual presence), obtain a proxy from your broker, bank or nominee.

Q: If my shares are held in “street name” by my bank, brokerage firm or nominee, will they automatically vote my shares for me?