As filed with the U.S. Securities and Exchange Commission on November 5, 2024

Registration No. 333-[•]

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_____________________________

FORM F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

_____________________________

Skycorp Solar Group Limited

(Exact name of Registrant as specified in its charter)

Not Applicable

(Translation of Registrant’s name into English)

_____________________________

Cayman Islands | 4931 | Not Applicable | ||

(State or other jurisdiction of | (Primary Standard Industrial | (I.R.S. Employer |

Room 303, Block B, No.188 Jinghua Road, Yinzhou District,

Ningbo City, Zhejiang Province, China 315048

+86 0574 87966876

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

_____________________________

Cogency Global Inc.

122 East 42nd Street, 18th Floor

New York, NY 10168

+1 212 947-7200

(Name, address, including zip code, and telephone number, including area code, of agent for service)

_____________________________

Copies to:

William S. Rosenstadt, Esq. | Ying Li, Esq. |

_____________________________

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

Emerging growth company ☒

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

____________

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the U.S. Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

PRELIMINARY PROSPECTUS | SUBJECT TO COMPLETION, DATED NOVEMBER 5, 2024 |

2,700,000 Ordinary Shares

![]()

Skycorp Solar Group Limited

This is the initial public offering on a firm commitment basis of our ordinary shares, par value $0.0001 per share (“Ordinary Shares”). Prior to this offering, there has been no public market for our Ordinary Shares. We expect the initial public offering price to be in the range of $4.00 to $5.00 per Ordinary Share. We plan to list our Ordinary Shares on the Nasdaq Capital Market (“Nasdaq”) under the symbol “PN.” We cannot guarantee that we will be successful in listing our Ordinary Shares on Nasdaq; however, we will not complete this offering unless we are so listed.

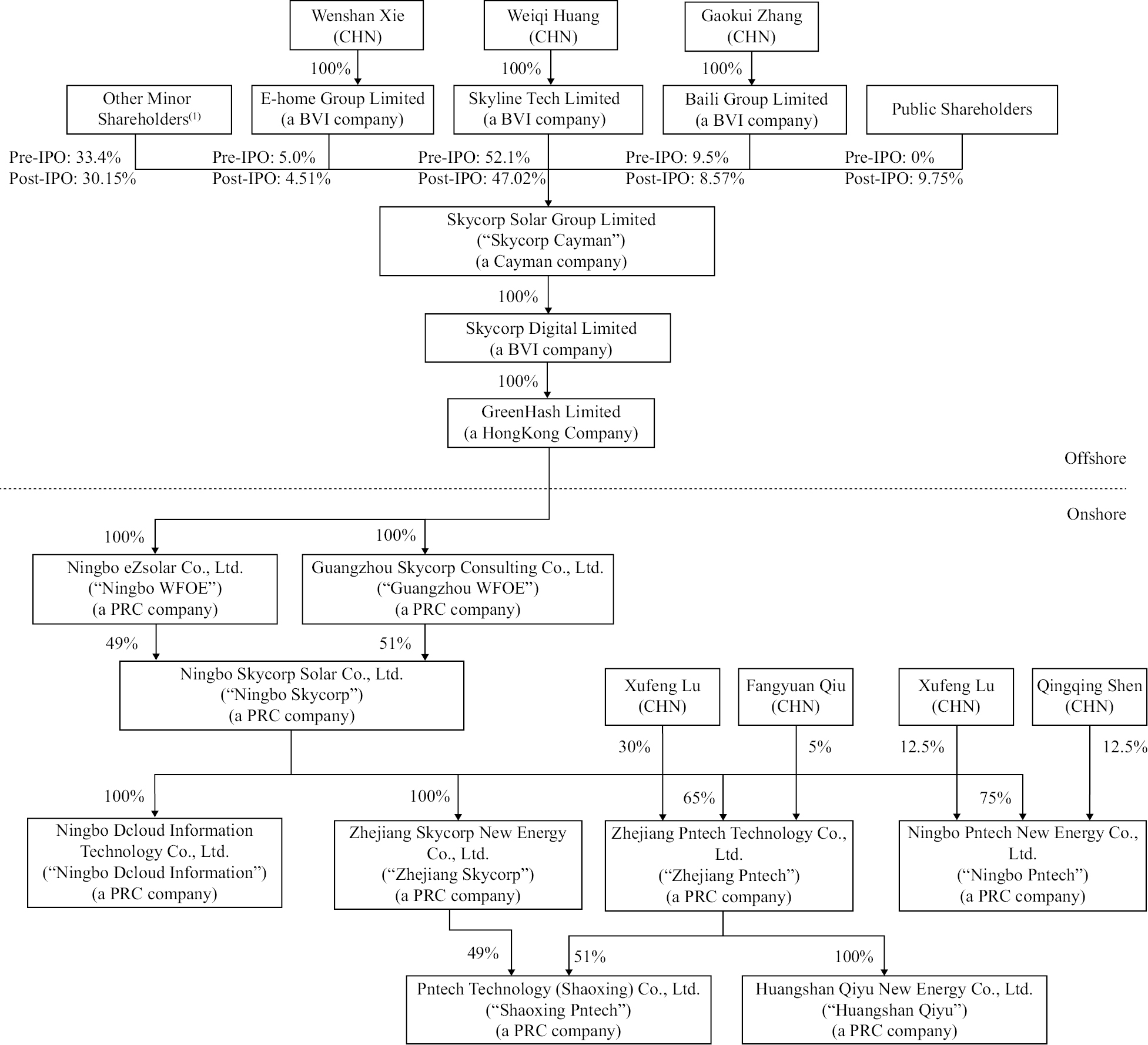

Throughout this prospectus, unless the context indicates otherwise, references to “we,” “us,” “our,” “Skycorp Cayman,” and “our Company,” refer to Skycorp Solar Group Limited, a Cayman Islands exempted company, and when describing Skycorp Cayman’s consolidated financial information for the fiscal years ended September 30, 2023 and 2022, also includes Skycorp Cayman’s subsidiaries. References to “PRC subsidiaries” are to Ningbo eZsolar Co., Ltd. (“Ningbo WFOE”), Guangzhou Skycorp Consulting Co., Ltd. (“Guangzhou WFOE”), and their subsidiaries. References to “operating subsidiaries” are to Ningbo Skycorp Solar Co., Ltd. (“Ningbo Skycorp”) and its subsidiaries.

Unless otherwise indicated, all share amounts and per share amounts in this prospectus have been presented giving effect to a forward split of our Ordinary Shares at a ratio of 1-for-10,000, with the Company’s authorized share capital remaining at $50,000, divided into 500,000,000 Ordinary Shares with a par value of $0.0001 and the surrender of 475,000,000 Ordinary Shares, all of which were approved by our shareholders and board of directors on October 21, 2024.

Skycorp Cayman is a Cayman Islands holding company, not a Chinese operating company. As a holding company with no material operations of its own, it conducts all of its operations and operates its business in China through Ningbo Skycorp and its subsidiaries. Because of our corporate structure as a Cayman Islands holding company with operations conducted by our PRC operating subsidiaries, it involves unique risks to investors. Furthermore, Chinese regulatory authorities could change the rules and regulations regarding foreign ownership in the industry in which our operating subsidiaries operate, which would likely result in a material change in the operating subsidiaries’ operations and/or the value of the securities we are registering for sale, including causing the value of such securities to significantly decline or become worthless. Investors in our Ordinary Shares should be aware that they do not directly hold equity interests in the Chinese operating subsidiaries but rather are purchasing equity interests solely in Skycorp Cayman, a Cayman Islands holding company, which indirectly owns equity interests in the PRC subsidiaries. Our Ordinary Shares offered in this offering are shares of our Cayman Islands holding company instead of shares of our subsidiaries in China. See “Risk Factors — Risks Related to Doing Business in China — We are required to fulfill the Trial Measures filing procedures and report relevant information to the CSRC; and, since the interpretation and implementation of the new regulations are still evolving, we cannot assure you that we will be able to complete the filings for this offering and any future offerings, and fully comply with the relevant new rules on a timely basis, if at all” on page 17.

We are both an “emerging growth company” and a “foreign private issuer” as defined under the U.S. federal securities laws and, as such, may elect to comply with certain reduced public company reporting requirements for this and future filings. See “Prospectus Summary — Implications of Being an Emerging Growth Company” and “Prospectus Summary — Implications of Being a Foreign Private Issuer” on page 14 for additional information.

Investing in our Ordinary Shares involves a high degree of risk. Before buying any Ordinary Shares, you should carefully read the discussion of material risks of investing in our Ordinary Shares in “Risk Factors” beginning on page 17 of this prospectus.

Because the Company conducts all of its operations in China through its operating subsidiaries, we are subject to certain legal and operational risks associated with the operations in China, including changes in the legal, political, and economic policies of the Chinese government, the relationship between China and United States, or Chinese or United States regulations may materially and adversely affect our business, financial condition and results of operations. The Chinese government may intervene or influence our operations at any time, or may exert more control over offerings conducted overseas and/or foreign investment in China-based issuers, which could result in a material change in our operating subsidiaries’ operations and/or the value of our Ordinary Shares or could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of our Ordinary Shares to significantly decline or become worthless.

Recently, the PRC government initiated a series of regulatory actions and statements to regulate business operations in China, which may be changed from time to time, including cracking down on illegal activities in the securities market, enhancing supervision over China-based companies listed overseas using variable interest entity structure, adopting new measures to extend the scope of cybersecurity reviews, and expanding the efforts in anti-monopoly enforcement.

In the opinion of our PRC counsel, Jiangsu Junjin Law Firm, we are not subject to cybersecurity review with the Cyberspace Administration of China, or the “CAC,” after the Measures for Cybersecurity Review (2021 version) became effective on February 15, 2022, since we currently do not have over one million users’ personal information and do not anticipate that we will be collecting over one million users’ personal information in the foreseeable future, which we understand might otherwise subject us to the Measures for Cybersecurity Review (2021 version); we are also not subject to network data security review by the CAC if the Draft Regulations on the Network Data Security Administration are enacted as proposed, since we currently do not have over one million users’ personal information and do not collect data that affects or may affect national security and we do not anticipate that we will be collecting over one million users’ personal information or data that affects or may affect national security in the foreseeable future, which we understand might otherwise subject us to the Data Security Administration Draft. See “Risk Factors — Risks Related to Doing Business in China — Recent greater oversight by the CAC over data security, particularly for companies seeking to list on a foreign exchange, could adversely impact our business and our offering” on page 21. In addition, as of the date of this prospectus, our operating subsidiaries’ operations are conducted entirely in mainland China. Our Hong Kong subsidiary, GreenHash Limited, is an intermediate holding company with no business operation. However, since Hong Kong is a special administrative region of China, the legal and operational risks associated with operating in China also apply to operations in Hong Kong. See “Risk Factors — Risks Related to Doing Business in China — Our Hong Kong subsidiary is currently an intermediate holding company with no business operations. However, the PRC laws and regulations governing businesses in the PRC may also be applicable to our business operations in Hong Kong.”

As of the date of this prospectus, our Hong Kong subsidiary is currently an intermediate holding company with no business operations. However, the PRC laws and regulations governing businesses in the PRC may also be applicable to our business operations in Hong Kong. These laws are sometimes vague and uncertain, and as a result, the legal and operational risks of operating in China could extend to businesses operating in Hong Kong, including any future operations of our Hong Kong subsidiary.

We may become subject to a variety of PRC laws and regulations, such as those regarding privacy, data security, cybersecurity, and data protection, which may also apply to any future operations in Hong Kong. These laws and regulations are continuously evolving and developing, and the scope and interpretation of the laws that are or may be applicable to us are often uncertain and may be conflicting, particularly with respect to foreign laws. In particular, there are numerous laws and regulations regarding privacy and the collection, sharing, use, processing, disclosure, and protection of personal information and other user data. Such laws and regulations often vary in scope, may be subject to differing interpretations, and may be inconsistent among different jurisdictions.

The national laws adopted by the PRC are generally not applicable to Hong Kong according to the Basic Law of the Hong Kong Special Administrative Region (the “Basic Law”), which came into effect on July 1, 1997. The Basic Law is the constitutional document of Hong Kong, as it sets out the PRC’s basic policies regarding Hong Kong. The principle of “one country, two systems,” which is a prominent feature of the Basic Law, dictates that Hong Kong will retain its unique common law and capitalist system for 50 years after the handover in 1997. Under the principle of “one country, two systems,” Hong Kong’s legal system, which is different from that of the PRC, is based on the common law supplemented by statutes.

According to Article 18 of the Basic Law, national laws adopted by the PRC shall not be applied in Hong Kong, except for those listed in Annex III to the Basic Law, such as the laws in relation to the national flag, national anthem, and diplomatic privileges and immunities. Further, there is no legislation stating that the laws in Hong Kong should be commensurate with those in the PRC. Despite the foregoing, the legal and operational risks of operating in China could still apply to any future business operations in Hong Kong.

There remains uncertainty as to how the various PRC laws will be interpreted or implemented and whether the PRC regulatory agencies may adopt new laws, regulations, rules, or detailed implementation and interpretation related to various laws, and as to the applicability of PRC laws to any future business operations in Hong Kong. If any such new laws, regulations, rules, or implementation and interpretation come into effect, we will take all reasonable measures and actions to comply and to minimize the adverse effect of such laws on us. However, there can be no assurance that any new PRC laws, regulations, rules, implementation, or interpretation will not have an adverse effect on any future business operations of our Hong Kong subsidiary.

Recent statements by the PRC regulatory authorities have indicated an intent to impose more oversight and supervision over offerings conducted overseas and/or foreign investment in China-based issuers. On February 17, 2023, the China Securities Regulatory Commission, or the CSRC released a set of new regulations which consists of the Trial Administrative Measures

of Overseas Securities Offering and Listing by Domestic Companies, or the Trial Measures, and five supporting guidelines, which came into effect on March 31, 2023. On the same date, the CSRC also released the Notice on the Arrangements for the Filing Management of Overseas Listing of Domestic Companies, or the Notice. The Trial Measures refine the regulatory system by subjecting both direct and indirect overseas offering and listing activities to the CSRC filing-based administration. Requirements for filing entities, time points and procedures are specified. A PRC domestic company that seeks to offer and list securities in overseas markets shall fulfill the filing procedure with the CSRC per the requirements of the Trial Measures. Where a PRC domestic company seeks to indirectly offer and list securities in overseas markets, the issuer shall designate a major domestic operating entity, which shall, as the domestic responsible entity, file with the CSRC. The Trial Measures also lay out requirements for the reporting of material events. Breaches of the Trial Measures, such as offering and listing securities overseas without fulfilling the filing procedures, shall bear legal liabilities, including a fine between RMB 1.0 million (approximately $150,000) and RMB 10.0 million (approximately $1.5 million), and the Trial Measures heighten the cost for offenders by enforcing accountability with administrative penalties and incorporating the compliance status of relevant market participants into the Securities Market Integrity Archives. In the opinion of our PRC counsel, Jiangsu Junjin Law Firm, we are required to file with the CSRC within three business days after submitting the application documents for offering and listing in the U.S., and this offering is contingent upon the completion of our filing with the CSRC. We have duly completed the required filings with the CSRC for this offering in accordance with the requirements under the Trial Measures. The CSRC published the notification on our completion of the required filing procedures for this offering on the CSRC website on April 2, 2024. The Trial Measures and Notice were newly published and are subject to change from time to time. Any failure or perceived failure of us to fully comply with such new regulatory requirements could significantly limit or completely hinder our ability to offer or continue to offer securities to investors, cause significant disruption to our business operations, and severely damage our reputation, which could materially and adversely affect our financial condition and results of operations and could cause the value of our securities to significantly decline or become worthless. See “Risk Factors — Risks Related to Doing Business in China — We are required to fulfill the Trial Measures filing procedures and report relevant information to the CSRC; and, since the interpretation and implementation of the new regulations are still evolving, we cannot assure you that we will be able to complete the filings for this offering and any future offerings, and fully comply with the relevant new rules on a timely basis, if at all” on page 17.

As of the date of this prospectus, according to our PRC counsel, Jiangsu Junjin Law Firm, although we are required to complete the filing procedure in connection with our offering (including this offering and any subsequent offering) and listing under the Trial Measures, no relevant PRC laws or regulations in effect require that we obtain permission from any PRC authorities to issue securities to foreign investors, and we have not received any inquiry, notice, warning, sanction, or any regulatory objection to this offering from the CSRC, the CAC, or any other PRC authorities that have jurisdiction over our operating subsidiaries’ operations.

The Standing Committee of the National People’s Congress, or the SCNPC, or other PRC regulatory authorities may in the future promulgate laws, regulations or implementing rules that require our Company or any of our subsidiaries to obtain regulatory approval from Chinese authorities before listing in the U.S. In other words, although the Company has not received any denial to list on the U.S. exchange, our operating subsidiaries’ operations could be adversely affected, directly or indirectly; our ability to offer, or continue to offer, securities to investors would be potentially hindered and the value of our securities might significantly decline or become worthless, by existing or future laws and regulations relating to its business or industry or by influence or interruption by PRC governmental authorities, if we or our subsidiaries (i) do not receive or maintain such permissions or approvals, (ii) inadvertently conclude that such permissions or approvals are not required, and (iii) applicable laws, regulations, or interpretations change and we are required to obtain such permissions or approvals in the future. See “Risk Factors — Risks Related to Doing Business in China” beginning on page 17 and “— Risks Related to this Offering and Ownership of Our Ordinary Shares” beginning on page 35 of this prospectus for a discussion of these legal and operational risks and information that should be considered before making a decision to purchase our Ordinary Shares.

Pursuant to the Holding Foreign Companies Accountable Act, or the HFCAA, if the Public Company Accounting Oversight Board, or the PCAOB, is unable to inspect an issuer’s auditors for two consecutive years, the issuer’s securities are prohibited from trading on a U.S. stock exchange. On June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act, and on December 29, 2022, legislation entitled “Consolidated Appropriations Act, 2023” was signed into law by President Biden, which contained, among other things, an identical provision to the Accelerating Holding Foreign Companies Accountable Act and amended the HFCAA by requiring the SEC to prohibit an issuer’s securities from trading on any U.S. stock exchanges if its auditor is not subject to PCAOB inspections for two consecutive years instead of three, thus reducing the time period for triggering the prohibition on trading. The PCAOB issued a Determination Report on December 16, 2021 which found that the PCAOB is

unable to inspect or investigate completely registered public accounting firms headquartered in mainland China or Hong Kong because of a position taken by one or more authorities in mainland China or Hong Kong. Furthermore, the PCAOB’s report identified the specific registered public accounting firms which are subject to these determinations. On August 26, 2022, the PCAOB announced that it had signed a Statement of Protocol (the “SOP”) with the CSRC and the Ministry of Finance of China, or the MOF. The SOP, together with two protocol agreements governing inspections and investigations (together, the “SOP Agreement”), establishes a specific, accountable framework to make possible complete inspections and investigations by the PCAOB of audit firms based in mainland China and Hong Kong, as required under U.S. law. On December 15, 2022, the PCAOB announced that it was able to secure complete access to inspect and investigate PCAOB-registered public accounting firms headquartered in mainland China and Hong Kong completely in 2022. The PCAOB Board vacated its previous 2021 determinations that the PCAOB was unable to inspect or investigate completely registered public accounting firms headquartered in mainland China and Hong Kong. However, whether the PCAOB will continue to be able to satisfactorily conduct inspections of PCAOB-registered public accounting firms headquartered in mainland China and Hong Kong is subject to uncertainties and depends on a number of factors out of our and our auditor’s control. The PCAOB continues to demand complete access in mainland China and Hong Kong moving forward and was making plans to resume regular inspections in early 2023 and beyond, as well as to continue pursuing ongoing investigations and initiate new investigations as needed. The PCAOB has also indicated that it will act immediately to consider the need to issue new determinations with the HFCAA if needed.

As of the date of the prospectus, our auditor, Pan-China Singapore, the independent registered public accounting firm that issued the audit report included in this prospectus, is subject to PCAOB inspections. Pan-China Singapore is headquartered in Singapore and there are no limitations in Singapore on PCAOB inspections. Therefore, the Company believes that, as of the date of this prospectus, its auditor is not subject to the determinations announced by the PCAOB on December 16, 2021 relating to the PCAOB’s inability to inspect or investigate completely registered public accounting firms headquartered in mainland China or Hong Kong because of a position taken by one or more authorities in mainland China or Hong Kong. However, to the extent that the Company’s auditor’s work papers may, in the future, become located in China, such work papers will not be subject to inspection by the PCAOB because the PCAOB is currently unable to conduct inspections without the approval of the Chinese authorities. Inspections of certain other firms that the PCAOB has conducted outside of China have identified deficiencies in those firms’ audit procedures and quality control procedures, which may be addressed as part of the inspection process to improve future audit quality. In addition to subjecting the Company’s securities to the possibility of being prohibited from trading or delisted from a US exchange, the inability of the PCAOB to conduct inspections of the Company’s auditors’ work papers in China would make it more difficult to evaluate the effectiveness of its auditor’s audit procedures or quality control procedures as compared to auditors outside of China that are subject to PCAOB inspections. As a result, the Company’s investors would be deprived of the benefits of the PCAOB’s oversight of its auditor through such inspections and they may lose confidence in the Company’s reported financial information and procedures and the quality of its financial statements. The Company cannot assure you whether Nasdaq or other regulatory authorities will apply additional or more stringent criteria to it. Such uncertainty could cause the market price of the Company’s Ordinary Shares to be materially and adversely affected. See “Risk Factors — Risks Related to Doing Business in China — The recent joint statement by the SEC and PCAOB, proposed rule changes submitted by Nasdaq, and the HFCAA all call for additional and more stringent criteria to be applied to emerging market companies upon assessing the qualification of their auditors, especially the non-U.S. auditors who are not inspected by the PCAOB. These developments could add uncertainties to our offering” on page 27.

We currently do not maintain any cash management policies that dictate the purposes, amounts and procedures form cash transfers among the Company, our subsidiaries, or investors. Rather, as of the date of this prospectus, funds can be transferred in accordance with the applicable PRC laws and regulations. To the extent cash or assets in the business is in mainland China or Hong Kong or an entity incorporated in mainland China or Hong Kong, the funds or assets may not be available to fund operations or for other use outside of mainland China or Hong Kong due to the imposition of restrictions and limitations on the ability of us or our subsidiaries by the PRC government to transfer cash or assets. See “Risk Factors — Risks Related to Doing Business in China — To the extent cash or assets in the business is in the PRC or Hong Kong or a PRC or Hong Kong entity, the funds or assets may not be available to fund operations or for other use outside of the PRC or Hong Kong due to regulations or the imposition of restrictions and limitations on the ability of us or our subsidiaries by the PRC government to transfer cash or assets” on page 24.

Under existing PRC foreign exchange regulations, payment of current account items, such as profit distributions and trade and service-related foreign exchange transactions, can be made in foreign currencies without prior approval from the State Administration of Foreign Exchange, or the SAFE, by complying with certain procedural requirements.

Therefore, our PRC subsidiaries are able to pay dividends in foreign currencies to us without prior approval from SAFE, subject to the condition that the remittance of such dividends outside of the PRC complies with certain procedures under PRC foreign exchange regulations, such as the overseas investment registrations by our shareholders or the ultimate shareholders of our corporate shareholders who are PRC residents. Approval from, or registration with, appropriate government authorities is, however, required where the RMB is to be converted into foreign currency and remitted out of China to pay capital expenses such as the repayment of loans denominated in foreign currencies. The PRC government may also at its discretion restrict access in the future to foreign currencies for current account transactions. Current PRC regulations permit our PRC subsidiaries to pay dividends to the Company only out of their accumulated profits, if any, determined in accordance with Chinese accounting standards and regulations. As of the date of this prospectus, there are no restrictions or limitations imposed by the Hong Kong government on the transfer of capital within, into and out of Hong Kong (including funds from Hong Kong to mainland China), except for the transfer of funds involving money laundering and criminal activities. Cayman Islands law prescribes that a company may only pay dividends out of its profits or share premium, and that a company may only pay dividends if, immediately following the date on which the dividend is paid, the company remains able to pay its debts as they fall due in the ordinary course of business. Other than that, there is no restrictions on Skycorp Cayman’s ability to pay dividends to its shareholders. See “Prospectus Summary — Transfers of Cash to and from Our Subsidiaries,” “Prospectus Summary — Summary of Risk Factors,” “Risk Factors — Risks Related to Doing Business in China — To the extent cash or assets in the business is in the PRC or Hong Kong or a PRC or Hong Kong entity, the funds or assets may not be available to fund operations or for other use outside of the PRC or Hong Kong due to regulations or the imposition of restrictions and limitations on the ability of us or our subsidiaries by the PRC government to transfer cash or assets,” and “Risk Factors — Risks Related to Doing Business in China — We may rely on dividends and other distributions on equity paid by our operating subsidiaries to fund any cash and financing requirements we may have, and any limitation on the ability of our operating subsidiaries to make payments to us could have a material adverse effect on our ability to conduct our business.”

As a holding company, we may rely on dividends and other distributions on equity paid by our subsidiaries, including those based in the PRC, for our cash and financing requirements. If any of our PRC subsidiaries incurs debt on its own behalf in the future, the instruments governing such debt may restrict their ability to pay dividends to us. Skycorp Cayman is permitted under the laws of the Cayman Islands to provide funding to our subsidiary incorporated in Hong Kong, GreenHash Limited, through loans or capital contributions without restrictions on the amount of the funds. GreenHash Limited is permitted under the laws of Hong Kong to provide funding to Skycorp Cayman through dividend distribution without restrictions on the amount of the funds. There are no restrictions on dividend transfers from Hong Kong to the Cayman Islands. Current PRC regulations permit Ningbo WFOE and Guangzhou WFOE to pay dividends to the Company only out of their accumulated profits, if any, determined in accordance with Chinese accounting standards and regulations. The transfer of funds among companies is subject to the Provisions of the Supreme People’s Court on Several Issues Concerning the Application of Law in the Trial of Private Lending Cases (2020 Revision, the “Provisions on Private Lending Cases”), which was implemented on August 20, 2020 to regulate the financing activities between natural persons, legal persons and unincorporated organizations. As advised by our PRC counsel, Jiangsu Junjin Law Firm, the Provisions on Private Lending Cases does not prohibit using cash generated from one subsidiary to fund another subsidiary’s operations. We have not been notified of any other restriction which could limit our PRC subsidiaries’ ability to transfer cash between PRC subsidiaries. As of the date of this prospectus, neither the Company nor its subsidiaries have made transfers, dividends, or distributions to investors and no investors have made transfers, dividends, or distributions to the Company or its subsidiaries. As of the date of this prospectus, no dividends or distributions have been made between Skycorp Cayman and any of its subsidiaries. We do not expect to pay any cash dividends in the foreseeable future. Currently, we make intra-group transactions through our organization in two ways: (1) investments by parent company in its subsidiaries; and (2) internal borrowing and lending between companies. Other than cash transferred through our organization by way of intra-group transactions, there were no other cash transfers and transfers of other assets between our holding company and our subsidiaries as of the date of this prospectus and during the fiscal years ended September 30, 2023 and 2022. See “Prospectus Summary — Transfers of Cash to and from Our Subsidiaries” on page 6.

Per Share | No Exercise of | Full Exercise of | |||||||

Public offering price(1) | $ | 4.00 | $ | 10,800,000 | $ | 12,420,000 | |||

Underwriting discounts(2) | $ | 0.28 | $ | 756,000 | $ | 869,400 | |||

Proceeds to us before expenses(3) | $ | 3.72 | $ | 10,044,000 | $ | 11,550,600 | |||

____________

(1) The initial public offering price per share is assumed as US$4.00, which is the low point of the range set forth on the cover page of this prospectus.

(2) We have agreed to pay Cathay Securities, Inc., the representative of the underwriters (the “Representative”), an underwriting discount of seven percent (7%) of the gross proceeds in this offering. See “Underwriting” starting on page 143 of this prospectus for more information regarding our arrangements with the underwriters.

(3) The total estimated expenses related to this offering are set forth in the section entitled “Expenses of This Offering” on page 148.

We have agreed to grant the Representative a 45-day option to purchase up to fifteen percent (15%) of the aggregate number of Ordinary Shares sold in the offering. This offering is being conducted on a firm commitment basis.

The Representative expects to deliver the Ordinary Shares against payment in U.S. dollars in New York, NY on or about [•], 2024.

Neither the U.S. Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

![]()

The date of this prospectus is [•], 2024

Page | ||

ii | ||

1 | ||

17 | ||

42 | ||

44 | ||

45 | ||

46 | ||

48 | ||

49 | ||

52 | ||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 54 | |

69 | ||

76 | ||

93 | ||

107 | ||

113 | ||

115 | ||

119 | ||

134 | ||

136 | ||

143 | ||

148 | ||

149 | ||

149 | ||

149 | ||

F-1 |

i

We and the underwriters have not authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectuses prepared by us or on our behalf or to which we have referred you and which we have filed with the U.S. Securities and Exchange Commission (the “SEC”). We take no responsibility for and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the Ordinary Shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. We are not making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted or where the person making the offer or sale is not qualified to do so or to any person to whom it is not permitted to make such offer or sale. For the avoidance of doubt, no offer or invitation to subscribe for Ordinary Shares is made to the public in the Cayman Islands. The information contained in this prospectus is current only as of the date on the front cover of the prospectus. Our business, financial condition, results of operations, and prospects may have changed since that date.

Neither we nor the underwriters have taken any action to permit a public offering of the Ordinary Shares outside the United States or to permit the possession or distribution of this prospectus or any filed free-writing prospectus outside the United States. Persons outside the United States who come into possession of this prospectus or any filed free writing prospectus must inform themselves about, and observe any restrictions relating to, the offering of the Ordinary Shares and the distribution of this prospectus or any filed free-writing prospectus outside the United States.

Conventions that Apply to this Prospectus

Unless otherwise indicated, in this prospectus, the following terms shall have the meaning set out below:

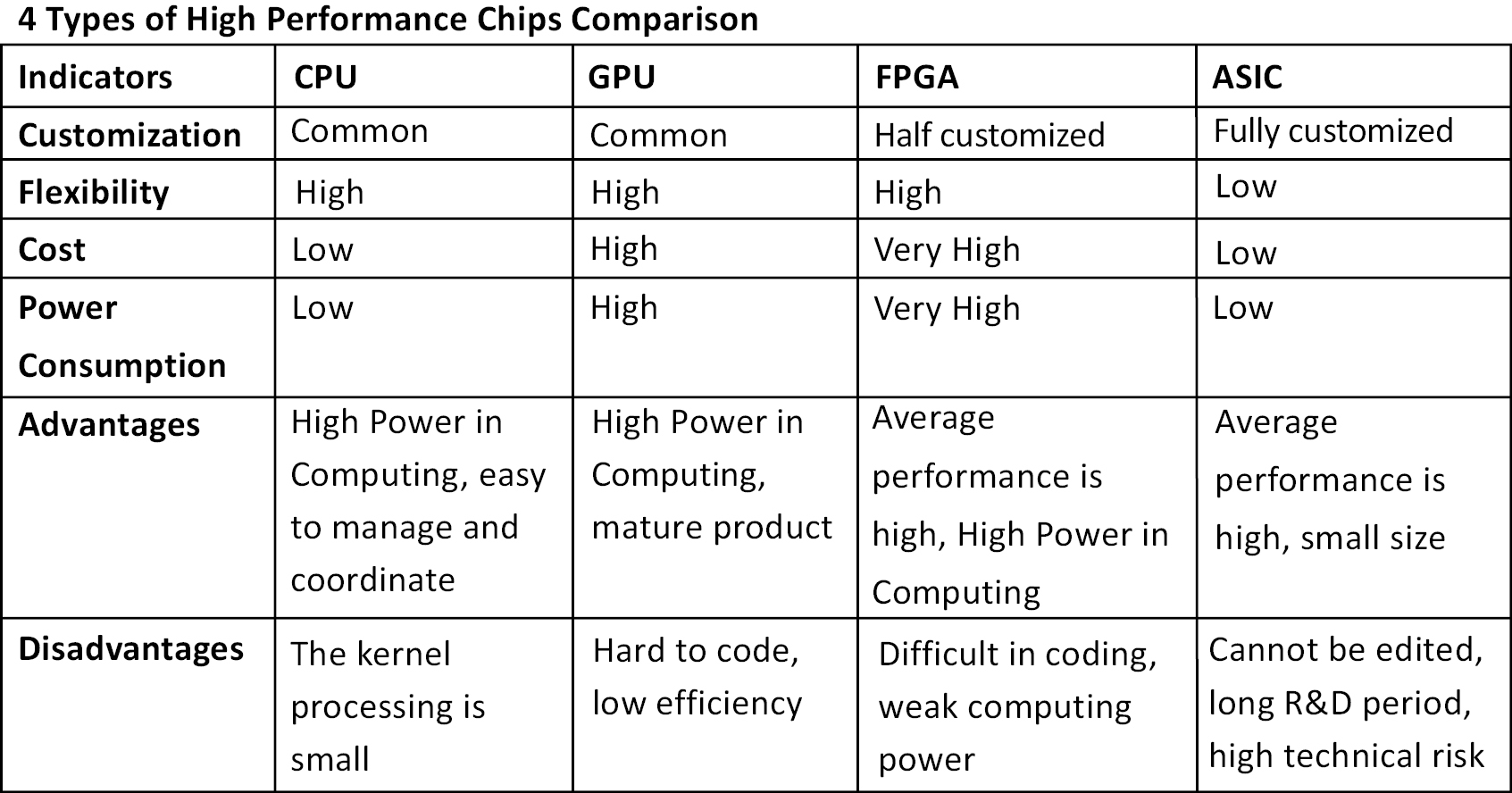

“ASIC” | Application-specific integrated circuit | |

“AI” | Artificial Intelligence | |

“China” or “PRC” | The People’s Republic of China | |

“CPU” | Central processing unit | |

“Exchange Act” | Securities Exchange Act of 1934, as amended | |

“GPU” | Graphic process unit | |

“Guangzhou WFOE” | Guangzhou Skycorp Consulting Co., Ltd., a limited liability company organized under the laws of the PRC and a wholly owned subsidiary of GreenHash Limited | |

“HPC” | High-Performance Computing | |

“Hong Kong” | the Hong Kong Special Administrative Region of the People’s Republic of China for the purposes of this prospectus only | |

“Ningbo Skycorp” | Ningbo Skycorp Solar Co., Ltd., a 49% owned subsidiary of Ningbo eZsolar Co., Ltd. and 51% owned subsidiary of Guangzhou Skycorp Consulting Co., Ltd. | |

“Ningbo Pntech” | Ningbo Pntech New Energy Co., Ltd., a 75% owned subsidiary of Ningbo Skycorp. The remaining 25% equity interest of Ningbo Pntech was owned as to 12.5% by a third-party individual Mr. Weiping Wu and 12.5% by a third-party individual Mr. Xufeng Lu | |

“Ningbo Dcloud Information” | Ningbo Dcloud Information Technology Co., Ltd., a wholly owned subsidiary of Ningbo Skycorp | |

“Ningbo WFOE” | Ningbo eZsolar Co., Ltd., a limited liability company organized under the laws of the PRC and a wholly owned subsidiary of GreenHash Limited | |

“Ordinary Shares” | Our ordinary shares, par value $0.0001 per share |

ii

“PCAOB” | Public Company Accounting Oversight Board | |

“PFIC” | A passive foreign investment company | |

“PV” | Photovoltaic | |

“RMB” or “Renminbi” | Legal currency of China | |

“Securities Act” | The Securities Act of 1933, as amended | |

“Skycorp Cayman” | Skycorp Solar Group Limited, a Cayman Islands exempted company, formerly known as Skycorp Digital Holdings Group Limited | |

“Skycorp BVI” | Skycorp Digital Limited, a British Virgin Islands exempted company and a wholly owned subsidiary of Skycorp Cayman | |

“TÜV” | Technischer Überwachungsverein in German, which means Technical Inspection Association | |

“US$,” “U.S. dollars,” “$,” and “dollars” | Legal currency of the United States | |

“WFOE” | Wholly foreign-owned enterprise | |

“Zhejiang Skycorp” | Zhejiang Skycorp New Energy Co., Ltd., previously known as Zhejing QuinnTek Co, Ltd., a wholly owned subsidiary of Ningbo Skycorp | |

“Zhejiang Pntech” | Zhejiang Pntech Technology Co., Ltd., a 65% owned subsidiary of Ningbo Skycorp. The remaining 35% equity interest of Zhejiang Pntech was owned as to 30% by a third-party individual Mr. Xufeng Lu and 5% by a third-party individual Ms. Fangyuan Qiu |

Our reporting currency is the U.S. dollar. The functional currency of subsidiaries located in China is the RMB. The functional currency of subsidiaries located in Hong Kong and Singapore are the Hong Kong dollars (“HK$”) and Singapore dollars (“S$”), respectively. This prospectus contains translations of certain RMB amounts into U.S. dollar amounts at specified rates solely for the convenience of the reader.

Our fiscal year end is September 30. References to a particular “fiscal year” are to our fiscal year ended September 30 of that calendar year. Our audited consolidated financial statements have been prepared in accordance with the generally accepted accounting principles in the United States (the “U.S. GAAP”).

Except where indicated or where the context otherwise requires, all information in this prospectus assumes no exercise by the underwriters of their over-allotment option.

We obtained the industry, market and competitive position data in this prospectus from our own internal estimates, surveys, and research as well as from publicly available information, industry and general publications and research, surveys and studies conducted by third parties. None of the independent industry publications used in this prospectus were prepared on our behalf. Industry publications, research, surveys, studies and forecasts generally state that the information they contain has been obtained from sources believed to be reliable, but that the accuracy and completeness of such information is not guaranteed. Forecasts and other forward-looking information obtained from these sources are subject to the same qualifications and uncertainties as the other forward-looking statements in this prospectus, and to risks due to a variety of factors, including those described under “Risk Factors.” These and other factors could cause results to differ materially from those expressed in these forecasts and other forward-looking information.

We have proprietary rights to trademarks used in this prospectus that are important to our business, many of which are registered under applicable intellectual property laws. Solely for convenience, the trademarks, service marks and trade names referred to in this prospectus are without the ®, ™ and other similar symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the rights of the applicable licensors to these trademarks, service marks and trade names.

This prospectus contains additional trademarks, service marks and trade names of others. All trademarks, service marks and trade names appearing in this prospectus are, to our knowledge, the property of their respective owners. We do not intend our use or display of other companies’ trademarks, service marks or trade names to imply a relationship with, or endorsement or sponsorship of us by, any other person.

iii

Investors are cautioned that you are buying shares of a Cayman Islands holding company with no operation of its own that indirectly holds 100% of the equity interest of China-based operating companies.

This summary highlights certain information contained elsewhere in this prospectus. You should read the entire prospectus carefully, including our financial statements and related notes and the risks described under “Risk Factors.” Our actual results and future events may differ significantly based upon a number of factors. The reader should not put undue reliance on the forward-looking statements in this document, which speak only as of the date on the cover of this prospectus.

Unless otherwise indicated, all share amounts and per share amounts in this prospectus have been presented giving effect to a forward split of our Ordinary Shares at a ratio of 1-for-10,000, with the Company’s authorized share capital remaining at $50,000, divided into 500,000,000 Ordinary Shares with a par value of $0.0001 and the surrender of 475,000,000 Ordinary Shares, all of which were approved by our shareholders and board of directors on October 21, 2024.

Overview

We are a solar PV product provider principally engaged in the manufacture and sale of solar cables and solar connectors. We also actively cultivate partnerships with multiple Integrated Circuit (“IC”) chip manufacturers and offer customers new and used GPU and HPC servers. Our business is carried out through our operating subsidiaries, Ningbo Skycorp and its subsidiaries, in China.

Our mission is to become a green energy solutions provider to power data centers by using solar power and to make our planet greener by delivering environment-friendly solar PV products. Leveraging our expertise and experience in the solar PV products and services market, experience in developing solar power technologies, as well as business relationships with our HPC server customers, we aim to expand our solar PV product offerings and high computing server solutions to enterprise customers of HPC servers.

For the six months ended March 31, 2024 and 2023, our revenue was $22,483,601 and $22,259,338, respectively, and our net income was $643,498 and $68,127, respectively. For the six months ended March 31, 2024, we generated 89.70% of our revenue from solar PV products and services and 10.30% from HPC products compared to 63.76% of our revenue from solar PV products and services and 36.24% from HPC products for the six months ended March 31, 2023.

For the years ended September 30, 2023 and 2022, our revenue was $50,815,675 and $59,059,644, respectively, and our net income was $1,807,728 and $2,149,807, respectively. For the year ended September 30, 2023, we generated 72.17% of our revenue from solar PV products and services and 27.83% from HPC products compared to 41.55% of our revenue from solar PV products and services and 58.45% from HPC products for the year ended September 30, 2022.

Our Strengths

We believe the following competitive strengths are essential for our success and differentiate us from our competitors:

• Advanced technologies provide us with a competitive advantage in the solar cable market

• Valuable brand and long-term and stable relations with customers

• Robust quality control and technology innovation ensure our competitive edges and premium products

• Comprehensive and efficient production management system ensures quality and efficiency

• Offering comprehensive experience to our customers

• Experienced and visionary management team

1

Our Strategies

We intend to develop our business and strengthen brand loyalty by implementing the following strategies:

• Invest in business expansion

• Continue to enhance our customized products and brand recognition

• Increase efficiency by development of technologies

• Refine talent development processes for increasing team competitiveness

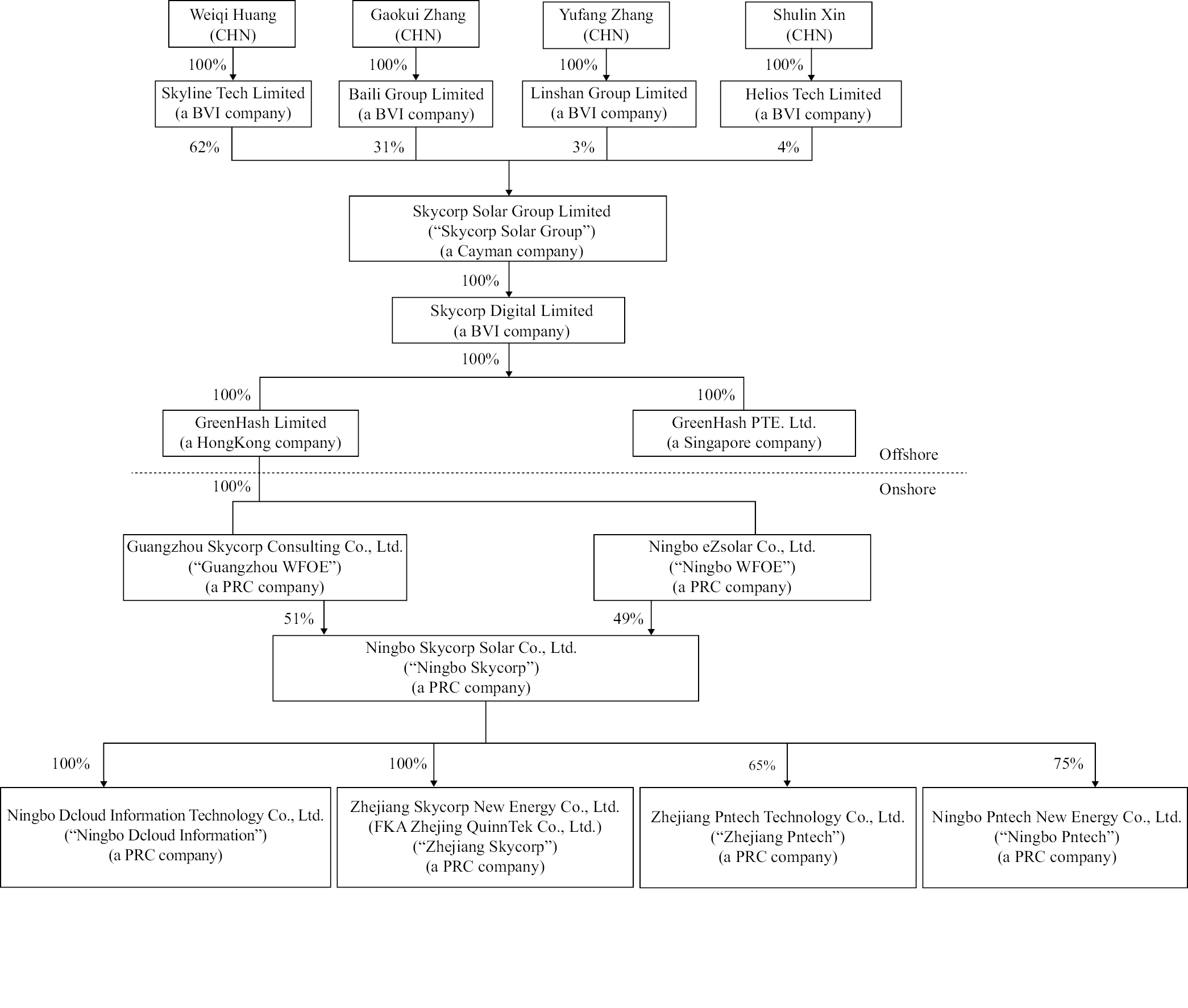

Corporate History and Structure

Skycorp Cayman (formerly known as Skycorp Digital Holdings Group Limited) was incorporated under the laws of the Cayman Islands as an exempted company on January 19, 2022, for the purposes of effectuating this offering, and is currently not engaging in any business. We commenced our business through Ningbo Skycorp in April 2011 and conducted all the operations in China through Ningbo Skycorp and its subsidiaries thereafter. This is an offering of the Ordinary Shares of the Cayman Islands holding company. You may never hold equity interests in the PRC operating subsidiaries. Skycorp Cayman controls its PRC subsidiaries through equity ownership. We do not use a variable interest entity structure.

Skycorp BVI was established in the British Virgin Islands on February 16, 2022. Skycorp BVI is a wholly owned subsidiary of Skycorp Cayman and an investment holding company currently not actively engaging in any business.

GreenHash Limited was incorporated on March 30, 2022 under the laws and regulations in Hong Kong. GreenHash Limited is a wholly owned subsidiary of Skycorp BVI and an investment holding company currently not actively engaging in any business.

Ningbo WFOE was established on June 29, 2023 under the laws of the PRC. Ningbo WFOE is a wholly owned subsidiary of GreenHash Limited and a holding company not actively engaging in any business.

Guangzhou WFOE was established on July 14, 2020 under the laws of the PRC. Guangzhou WFOE is a wholly owned subsidiary of GreenHash Limited and a holding company not actively engaging in any business.

Ningbo Skycorp was established on April 26, 2011 under the laws of the PRC. Ningbo Skycorp is 49% owned by Ningbo WFOE and 51% owned by Guangzhou WFOE and is our operating entity engaging in the sale of solar PV products and HPC servers.

Ningbo Pntech was established on April 22, 2011 under the laws of the PRC. Ningbo Pntech is a 75% owned subsidiary of Ningbo Skycorp and is our operating entity engaging in the manufacture and sale of solar PV products. The remaining 25% equity interest of Ningbo Pntech was owned as to 12.5% by a third-party individual Mr. Weiping Wu and 12.5% by a third-party individual Mr. Xufeng Lu.

Zhejiang Pntech was established on April 26, 2021 under the laws of the PRC. Zhejiang Pntech is a 65% owned subsidiary of Ningbo Skycorp and is our operating entity engaging in the manufacture and sale of solar PV products. The remaining 35% equity interest of was owned as to 30% by a third-party individual Mr. Xufeng Lu and 5% by a third-party individual Ms. Fangyuan Qiu.

Zhejiang Skycorp was established on April 23, 2015 under the laws of the PRC. Zhejiang Skycorp is a wholly owned subsidiary of Ningbo Skycorp and is our operating entity engaging in the sale of solar PV products and HPC servers.

Ningbo Dcloud Information was established on July 27, 2015 under the laws of the PRC. Ningbo Dcloud Information is a wholly owned subsidiary of Ningbo Skycorp and is our operating entity engaging in the sale of solar PV products and HPC servers.

Huangshan Qiyu New Energy Co., Ltd. (“Huangshan Qiyu”) was established on March 27, 2024 under the laws of the PRC. Huangshan Qiyu is a wholly owned subsidiary of Zhejiang Pntech and is not actively engaged in any business.

2

Pntech Technology (Shaoxing) Co., Ltd. (“Shaoxing Pntech”) was established on June 27, 2024 under the laws of the PRC. Shaoxing Pntech is 51% owned by Zhejiang Pntech and 49% owned by Zhejiang Skycorp and is not actively engaged in any business.

On October 21, 2024, the Company effected a 1-for-10,000 forward split of our Ordinary Shares and the surrender of 475,000,000 Ordinary Shares, approved by our shareholders and board of directors. As a result, the authorized share capital of the Company is $50,000 divided into 500,000,000 Ordinary Shares of a par value of $0.0001 and the Ordinary Shares issued and outstanding prior to the completion of this offering have been increased from 50,000 to 25,000,000.

The following diagram illustrates the corporate structure of the Company as of the date of this prospectus and upon completion of this offering:

The following financial information was included in the consolidated financial statements. For more information, see our consolidated financial statements and related notes from page F-1 to page F-56 that appear in this prospectus.

March 31, | September 30, | |||||

Total Assets | $ | 29,947,847 | $ | 29,599,605 | ||

Total Liabilities | $ | 12,369,778 | $ | 12,565,465 | ||

3

For the Six Months Ended | ||||||

2024 | 2023 | |||||

Revenue | $ | 22,483,601 | $ | 22,259,338 | ||

Net income | $ | 643,498 | $ | 68,127 | ||

For the Six Months Ended | ||||||||

2024 | 2023 | |||||||

Net cash used in operating activities | $ | (1,029,992 | ) | $ | (977,565 | ) | ||

Net cash used in investing activities |

| (2,380,528 | ) |

| (136,683 | ) | ||

Net cash provided by financing activities |

| 954,129 |

|

| 1,649,910 |

| ||

Effect of foreign currency translations |

| 66,251 |

|

| 159,848 |

| ||

Net increase in cash and cash equivalents | $ | (2,390,140 | ) | $ | 695,510 |

| ||

Regulatory Permissions

We are not operating in an industry that prohibits or limits foreign investment. As a result, as advised by our PRC counsel, Jiangsu Junjin Law Firm, other than those requisite for a domestic company in China to engage in businesses similar to ours and the filing procedure in connection with our offering (including this offering and any subsequent offering) and listing under the Trial Measures, as of the date of this prospectus, we are not required to obtain other permission from Chinese authorities, including the China Securities Regulatory Commission, or the “CSRC”, Cyberspace Administration of China, or the “CAC” or any other governmental agency that is required to approve our operating subsidiaries’ operations. However, if we do not receive or maintain the approvals, or we inadvertently conclude that such approvals are not required, or applicable laws, regulations, or interpretations change such that we are required to obtain approval in the future, we may be subject to investigations by competent regulators, fines or penalties, ordered to suspend our relevant operations and rectify any non-compliance, prohibited from engaging in a relevant business or conducting any offering, and these risks could result in a material adverse change in our operating subsidiaries’ operations, significantly limit or completely hinder our ability to offer or continue to offer securities to investors, or cause such securities to significantly decline in value or become worthless.

As of the date of this prospectus, we and our PRC subsidiaries have received from PRC authorities all requisite licenses, permissions or approvals needed to engage in the businesses currently conducted in China, and no permission or approval has been denied. The following table provides details on the licenses and permissions held by our operating subsidiaries.

Company | License/Permission | Issuing Authority | Validity | |||

Ningbo Skycorp | Business License | Ningbo Municipal Administration for Market Supervision | Long-term | |||

Ningbo Skycorp | Certificate of the Customs of the People’s Republic of China on Registration of a Customs Declaration Entity | Ningbo Customs | Long-term | |||

Ningbo Skycorp | Record Registration Form for Foreign Trade Business Operators | Eligible local foreign trade authorities appointed by the Ministry of Commerce of the PRC | Long-term | |||

Ningbo Dcloud Information | Business License | Ningbo Municipal Administration for Market Supervision | Long-term | |||

Ningbo Dcloud Information | Certificate of the Customs of the People’s Republic of China on Registration of a Customs Declaration Entity | Ningbo Customs | Long-term | |||

Ningbo Dcloud Information | Record Registration Form for Foreign Trade Business Operators | Eligible local foreign trade authorities appointed by the Ministry of Commerce of the PRC | Long-term |

4

Company | License/Permission | Issuing Authority | Validity | |||

Ningbo Dcloud Information | Archival filing of international freight forwarders | Ministry of Commerce of the PRC | Long-term | |||

Ningbo Dcloud Information | Archival filing on the Centralized Declaration of Import and Export Goods | Administrative Measures of the Customs of the PRC | Long-term | |||

Ningbo Pntech | Business License | Ningbo Haishu Municipal Administration for Market Supervision | Long-term | |||

Ningbo Pntech | Record Registration Form for Foreign Trade Business Operators | Eligible local foreign trade authorities appointed by the Ministry of Commerce of the PRC | Long-term | |||

Ningbo Pntech | Archival filing on the Centralized Declaration of Import and Export Goods | Administrative Measures of the Customs of the PRC | Long-term | |||

Ningbo Pntech | Quality Management System Certificate | Shanghai Ingeer Certification Assessment Co., Ltd. | January 6, 2025 | |||

Ningbo Pntech | Certificate of Work Safety Standardization Enterprise in Light Industry | Ministry of Emergency Management of the PRC | October 17, 2024 | |||

Ningbo Pntech | Fixed Pollutant Discharge Permit | The Ministry of Ecology and Environment of the PRC | April 23, 2025 | |||

Zhejiang Skycorp | Business License | Ningbo Haishu Municipal Administration for Market Supervision | Long-term | |||

Zhejiang Skycorp | Record Registration Form for Foreign Trade Business Operators | Eligible local foreign trade authorities appointed by the Ministry of Commerce of the PRC | Long-term | |||

Zhejiang Skycorp | Archival filing on the Centralized Declaration of Import and Export Goods | Administrative Measures of the Customs of the PRC | Long-term | |||

Zhejiang Pntech | Business License | Ningbo Haishu Municipal Administration for Market Supervision | Long-term | |||

Zhejiang Pntech | Record Registration Form for Foreign Trade Business Operators | Eligible local foreign trade authorities appointed by the Ministry of Commerce of the PRC | Long-term | |||

Zhejiang Pntech | Archival filing on the Centralized Declaration of Import and Export Goods | Administrative Measures of the Customs of the PRC | Long-term | |||

Huangshan Qiyu | Business License | Huangshan Huizhou District Administration for Market Supervision | Long-term | |||

Shaoxing Pntech | Business License | Xinchang County Administration for Market Supervision | Long-term |

On February 17, 2023, the CSRC released a set of new regulations which consists of the Trial Administrative Measures of Overseas Securities Offering and Listing by Domestic Companies, or the Trial Measures, and five supporting guidelines, which came into effect on March 31, 2023. On the same date, the CSRC also released the Notice on the Arrangements for the Filing Management of Overseas Listing of Domestic Companies, or the Notice. The Trial Measures refine the regulatory system by subjecting both direct and indirect overseas offering and listing activities to the CSRC filing-based administration. Requirements for filing entities, time points and procedures are specified.

5

A PRC domestic company that seeks to offer and list securities in overseas markets shall fulfill the filing procedure with the CSRC per the requirements of the Trial Measures. Where a PRC domestic company seeks to indirectly offer and list securities in overseas markets, the issuer shall designate a major domestic operating entity, which shall, as the domestic responsible entity, file with the CSRC. The Trial Measures also lay out requirements for the reporting of material events. Breaches of the Trial Measures, such as offering and listing securities overseas without fulfilling the filing procedures, shall bear legal liabilities, including a fine between RMB 1.0 million (approximately $150,000) and RMB 10.0 million (approximately $1.5 million), and the Trial Measures heighten the cost for offenders by enforcing accountability with administrative penalties and incorporating the compliance status of relevant market participants into the Securities Market Integrity Archives.

According to the Notice, since the date of effectiveness of the Trial Measures on March 31, 2023, PRC domestic enterprises falling within the scope of filing that have been listed overseas or met certain circumstances are “existing enterprises.” Existing enterprises are not required to file with the CSRC immediately, and filings with the CSRC should be made as required if they involve refinancing and other filing matters. In the opinion of our PRC counsel, Jiangsu Junjin Law Firm, we are required to file with the CSRC within three business days after submitting the application documents for offering and listing in the U.S., and this offering is contingent upon the completion of our filing with the CSRC. We have duly completed the required filings with the CSRC for this offering in accordance with the requirements under the Trial Measures. The CSRC published the notification on our completion of the required filing procedures for this offering on the CSRC website on April 2, 2024.

However, if we do not maintain the permissions and approvals of the filing procedure in a timely manner under PRC laws and regulations, we may be subject to investigations by competent regulators, fines or penalties, ordered to suspend our relevant operations and rectify any non-compliance, prohibited from engaging in relevant business or conducting any offering, and these risks could result in a material adverse change in our operating subsidiaries’ operations, limit our ability to offer or continue to offer securities to investors, or cause such securities to significantly decline in value or become worthless. The Trial Measures and Notice were newly published and are subject to change from time to time. Any failure or perceived failure of us to fully comply with such new regulatory requirements could significantly limit or completely hinder our ability to offer or continue to offer securities to investors, cause significant disruption to our business operations, and severely damage our reputation, which could materially and adversely affect our financial condition and results of operations and could cause the value of our securities to significantly decline or become worthless. See “Risk Factors — Risks Related to Doing Business in China — We are required to fulfill the Trial Measures filing procedures and report relevant information to the CSRC; and, since the interpretation and implementation of the new regulations are still evolving, we cannot assure you that we will be able to complete the filings for this offering and any future offerings, and fully comply with the relevant new rules on a timely basis, if at all” on page 17.

As of the date of this prospectus, according to our PRC counsel, Jiangsu Junjin Law Firm, although we are required to complete the filing procedure in connection with our offering (including this offering and any subsequent offering) and listing under the Trial Measures, no relevant PRC laws or regulations in effect require that we obtain permission from any PRC authorities to issue securities to foreign investors, and we have not received any inquiry, notice, warning, sanction, or any regulatory objection to this offering from the CSRC, the CAC, or any other PRC authorities that have jurisdiction over our operating subsidiaries’ operations.

Transfers of Cash to and from Our Subsidiaries

We are a holding company with no material operations of our own and do not generate any revenue. We currently conduct all of the operations through Ningbo Skycorp, our wholly owned subsidiary and its subsidiaries. We are permitted under PRC laws and regulations to provide funding to PRC subsidiaries only through loans or capital contributions, and only if we satisfy the applicable government registration and approval requirements. See “Risk Factors — Risks Related to Doing Business in China — PRC regulations on loans to and direct investment in PRC entities by offshore holding companies may delay or prevent us from making loans or additional capital contributions to our PRC operating subsidiaries, which could materially and adversely affect our liquidity and our ability to fund and expand our business” on page 20.

Under our current corporate structure, we rely on dividend payments from our PRC subsidiaries to fund any cash and financing requirements we may have, including the funds necessary to pay dividends and other cash distributions to our shareholders or to service any debt we may incur. Our subsidiaries in the PRC generate and retain cash generated from operating activities and re-invest it in our business. If any of our PRC subsidiaries

6

incurs debt on its own behalf in the future, the instruments governing such debt may restrict their ability to pay dividends to us. As of the date of this prospectus, there were no cash flows between our Cayman Islands holding company and our subsidiaries.

Currently, we make intra-group transactions through our organization in two ways: (1) investments by parent company in its subsidiaries; and (2) internal borrowing and lending between companies. Other than cash transferred through our organization by way of intra-group transactions, there were no other cash transfers and transfers of other assets between our holding company and our subsidiaries as of the date of this prospectus and during the fiscal years ended September 30, 2023 and 2022.

The transfer of funds among companies are subject to the Provisions of the Supreme People’s Court on Several Issues Concerning the Application of Law in the Trial of Private Lending Cases (2020 Revision, the “Provisions on Private Lending Cases”), which was implemented on August 20, 2020 to regulate the financing activities between natural persons, legal persons and unincorporated organizations. The Provisions on Private Lending Cases set forth that private lending contracts will be upheld as invalid under the circumstance that (i) the lender swindles loans from financial institutions for relending; (ii) the lender relends the funds obtained by means of a loan from another profit-making legal person, raising funds from its employees, illegally taking deposits from the public; (iii) the lender who has not obtained the lending qualification according to the law lends money to any unspecified object of the society for the purpose of making profits; (iv) the lender lends funds to a borrower when the lender knows or should have known that the borrower intended to use the borrowed funds for illegal or criminal purposes; (v) the lending is violations of public orders or good morals; or (vi) the lending is in violations of mandatory provisions of laws or administrative regulations. As advised by our PRC counsel, Jiangsu Junjin Law Firm, the Provisions on Private Lending Cases does not prohibit using cash generated from one subsidiary to fund another subsidiary’s operations. We have not been notified of any other restriction which could limit our PRC subsidiaries’ ability to transfer cash between subsidiaries. See “Regulation — Regulations Relating to Private Lending.”

We currently do not maintain any cash management policies that dictate the purposes, amounts and procedures form cash transfers among the Company, our subsidiaries, or investors. Rather, as of the date of this prospectus, funds can be transferred in accordance with the applicable PRC laws and regulations.

Our PRC subsidiaries are permitted to pay dividends only out of their retained earnings. However, each of our PRC subsidiaries is required to set aside at least 10% of its after-tax profits each year, after making up for previous year’s accumulated losses, if any, to fund certain statutory reserves, until the aggregate amount of such funds reaches 50% of its registered capital. This portion of our PRC subsidiaries’ respective net assets are prohibited from being distributed to their shareholders as dividends. See “Regulation — Regulations Relating to Dividend Distributions.” However, none of our subsidiaries has made any dividends or other distributions to our holding company or any U.S. investors as of the date of this prospectus. See also “Risk Factors — Risks Related to Doing Business in China — We may rely on dividends and other distributions on equity paid by our operating subsidiaries to fund any cash and financing requirements we may have, and any limitation on the ability of our operating subsidiaries to make payments to us could have a material adverse effect on our ability to conduct our business” on page 23.

As of the date of this prospectus, none of our subsidiaries have ever issued any dividends or made other distributions to us or their respective holding companies nor have we or any of our subsidiaries ever paid dividends or made other distributions to U.S. investors. We intend to retain all of our available funds and any future earnings after this offering and cash proceeds from overseas financing activities, including this offering, to fund the development and growth of our business. As a result, we do not expect to pay any cash dividends in the foreseeable future.

In addition, the PRC government regulates and imposes certain restrictions on the convertibility of the RMB into foreign currencies and, in certain cases, the remittance of currency out of mainland China. If the foreign exchange management system prevents us from obtaining sufficient foreign currencies to satisfy our foreign currency demands, we may not be able to transfer cash out of China, and pay dividends in foreign currencies to our shareholders. There can be no assurance that the PRC government will not impose restrictions on our ability to transfer or distribute cash within our organization or to foreign investors, which could result in an inability or prohibition on making transfers or distributions outside of China and may adversely affect our business, financial condition and results of operations. See “Risk Factors — Risks Related to Doing Business in China — Restrictions on the remittance of RMB into and out of China and governmental regulations on currency conversion may affect the value of your investment” on page 23.

7

A 10% PRC withholding tax is applicable to dividends payable to investors that are non-resident enterprises. Any gain realized on the transfer of Ordinary Shares by such investors is also subject to PRC tax at a current rate of 10% which in the case of dividends will be withheld at source if such gain is regarded as income derived from sources within the PRC. See also “Risk Factors — Risks Related to Doing Business in China — Under the PRC Enterprise Income Tax Law, we may be classified as a “Resident Enterprise” of China. Such classification will likely result in unfavorable tax consequences to us and our non-PRC shareholders” on page 22.

Impact of COVID-19

The outbreak of novel coronavirus (COVID-19) began in December 2019 and was quickly declared a Public Health Emergency of International Concern on January 30, 2020 by the World Health Organization.

The COVID-19 pandemic has not had a significant negative impact on our operating subsidiaries’ operations or financial performance to date, the government has adopted several measures to contain and mitigate the effects of the COVID-19 pandemic, including quarantines, travel restrictions, temporary closure of stores and facilities, capsuled labor, and other restrictive orders. Our business maintained an upward trend despite these challenges during the fiscal years 2023 and 2022.

COVID-19 was temporarily contained in the PRC since the second quarter of 2020 through 2021, certain of our manufacturers experienced delays and shut-downs due to the COVID-19 pandemic. However, our production and sales of solar PV products resumed gradually in the second half of 2020 and the fiscal year 2021.

From January 2022 to July 2022, there were outbreaks of the Omicron variant of COVID-19 and the local governments placed lockdowns and mass testing policies in most cities in China, where our dealers and suppliers operate, including but not limited to Tianjin, Beijing, Shanghai, and Ningbo. Starting in July 2022, China gradually loosened its quarantine policy, and the overall economy and consumer spending bounced back significantly. As a result, our total revenues increased by approximately 54% for the year ended September 30, 2022 compared to the year ended September 30, 2021.

In late 2022, there was a temporary surge of COVID-19 cases in many cities in the PRC during this time, which, to varying degrees and for a short period of time, disrupted our and our customers’ and suppliers’ business operations, and therefore affected our operational and financial performance. Shortly after that, our business operations in the PRC returned to normal levels in the fiscal year 2023 and for the six months ended March 31, 2024. However, we cannot assure you that our business will not be affected by an outbreak of COVID-19 in the future.

Summary of Risk Factors

Our business is subject to multiple risks and uncertainties, as more fully described in “Risk Factors” and elsewhere in this prospectus. We urge you to read “Risk Factors” and this prospectus in full. Our principal risks may be summarized as follows:

Risks Related to Doing Business in China

We are also subject to risks and uncertainties relating to doing business in China in general, including, but are not limited to, the following:

• Changes in the economic policies of the PRC may materially and adversely affect our business, financial condition and results of operations and may result in our inability to sustain our growth and expansion strategies. See “Risk Factors — Risks Related to Doing Business in China — Changes in the economic policies of the PRC may materially and adversely affect our business, financial condition and results of operations and may result in our inability to sustain our growth and expansion strategies” on page 17;

• Uncertainties with respect to the legal system in China, including risks and uncertainties regarding the enforcement of laws and that rules and regulations in China can change quickly with no advance notice, which could materially and adversely affect us. See “Risk Factors — Risks Related to Doing Business in China — Uncertainties with respect to the legal system in China, including risks and uncertainties regarding the enforcement of laws and that rules and regulations in China can change quickly with no advance notice, which could materially and adversely affect us” on page 17;

8

• We are required to fulfill the Trial Measures filing procedures and report relevant information to the CSRC; and, since the interpretation and implementation of the new regulations are still evolving, we cannot assure you that we will be able to complete the filings for this offering, and any future offerings and fully comply with the relevant new rules on a timely basis, if at all. See “Risk Factors — Risks Related to Doing Business in China — We are required to fulfill the Trial Measures filing procedures and report relevant information to the CSRC; and, since further interpretation and implementation of the new regulations are still required, we cannot assure you that we will be able to complete the filings for this offering, and any future offerings and fully comply with the relevant new rules on a timely basis, if at all” on page 17;

• The Chinese government has significant oversight and discretion over our operating subsidiaries’ business operations and may intervene or influence our operating subsidiaries’ operations at any time. Actions by the PRC government to exert control over offerings conducted overseas by, and foreign investment in, China-based issuers could result in a material change in our operating subsidiaries’ operations and our Ordinary Shares could decline in value or become worthless. See “Risk Factors — Risks Related to Doing Business in China — The Chinese government has significant oversight and discretion over our operating subsidiaries’ business operations and may intervene or influence our operating subsidiaries’ operations at any time. Actions by the PRC government to exert control over offerings conducted overseas by, and foreign investment in, China-based issuers could result in a material change in our operating subsidiaries’ operations and our Ordinary Shares could decline in value or become worthless” on page 20;

• Recent statements by the Chinese government have indicated an intent to exert more oversight and control over offerings that are conducted overseas and/or foreign investments in China based issuers. Any future action or control by the PRC government over offerings conducted overseas and/or foreign investment in China-based issuers could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and could cause the value of such securities to significantly decline or be worthless. See “Risk Factors — Risks Related to Doing Business in China — Recent statements by the Chinese government have indicated an intent to exert more oversight and control over offerings that are conducted overseas and/or foreign investments in China-based issuers. Any future action or control by the PRC government over offerings conducted overseas and/or foreign investment in China-based issuers could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and could cause the value of such securities to significantly decline or be worthless” on page 21;

• Recent greater oversight by the CAC over data security, particularly for companies seeking to list on a foreign exchange, could adversely impact our business and our offering. See “Risk Factors — Risks Related to Doing Business in China — Recent greater oversight by the CAC over data security, particularly for companies seeking to list on a foreign exchange, could adversely impact our business and our offering” on page 21;

• We may rely on dividends and other distributions on equity paid by our operating subsidiaries to fund any cash and financing requirements we may have, and any limitation on the ability of our operating subsidiaries to make payments to us could have a material and adverse effect on our ability to conduct our business. See “Risk Factors — Risks Related to Doing Business in China — We may rely on dividends and other distributions on equity paid by our operating subsidiaries to fund any cash and financing requirements we may have, and any limitation on the ability of our operating subsidiaries to make payments to us could have a material and adverse effect on our ability to conduct our business” on page 23; and

• The recent joint statement by the SEC and PCAOB, proposed rule changes submitted by Nasdaq, and the HFCAA all call for additional and more stringent criteria to be applied to emerging market companies upon assessing the qualification of their auditors, especially the non-U.S. auditors who are not inspected by the PCAOB. These developments could add uncertainties to our offering. See “Risk Factors — Risks Related to Doing Business in China — The recent joint statement by the SEC and PCAOB, proposed rule changes submitted by Nasdaq, and the HFCAA all call for additional and more stringent criteria to be applied to emerging market companies upon assessing the qualification of their auditors, especially the non-U.S. auditors who are not inspected by the PCAOB. These developments could add uncertainties to our offering” on page 27.

9

Risks Related to Our Business and Industry:

Risks and uncertainties related to our business and industry include, but are not limited to, the following: