As of June 30, 2004

Who We Are

Multi-bank holding company with significant operating autonomy at the individual banks Banking assets of $5.8 billion at June 30, 2004 Listed on the NYSE (CHZ), current market capitalization of $1.3 billion 119 full service banking offices and 155 ATM locations throughout VT, NH, MA, ME

Commercial loans make up 69% of the total loan portfolio and core funding comprises 97% of total funding Strong wealth management operation with assets under administration of $7.3 billion and assets under management of $1.9 billion Excellent credit quality with year-to-date charge-offs at .03% and an allowance for loan losses to loans of 1.50%

2

A Tradition of Success

Recognized competency in an attractive business mix Deep relationships with worthwhile customers Conservative underwriting standards and disciplined lending Efficient generator of low cost stable deposits Proven leadership focus to achieve superior financial results Well established and tangible shareholder orientation

3

Objectives and Outlook for 2004

Complete the merger of Granite into Ocean National Bank and other franchise streamlining initiatives

Complete the IT conversion from Fidelity to Jack Henry and realize the product, operating and financial benefits of the new system

Maintain a risk based capital ratio in excess of 11% and tangible common equity of 6% or higher

Maintain strong asset quality and an allowance for loan losses greater than 1.40%

Continue the steady growth in the Company’s earnings per share and improve the efficiency ratio by at least 2%

4

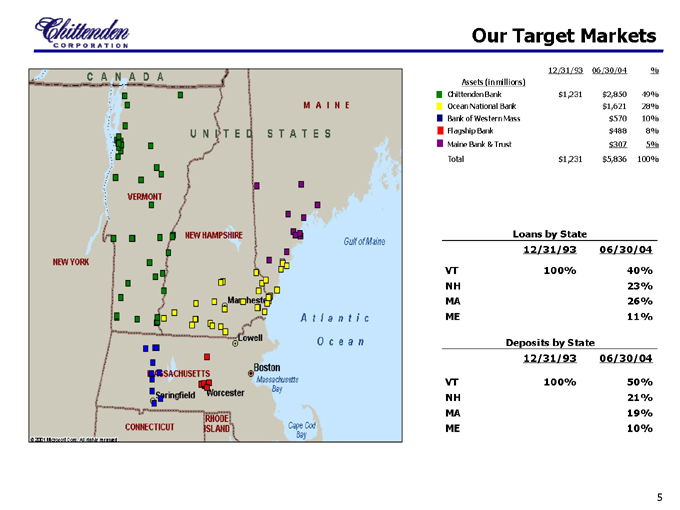

Our Target Markets

12/31/93 06/30/04 %

Assets (in millions)

Chittenden Bank $1,231 $2,850 49%

Ocean National Bank $1,621 28%

Bank of Western Mass $570 10%

Flagship Bank $488 8%

Maine Bank & Trust $307 5%

Total $1,231 $5,836 100%

Loans by State

12/31/93 06/30/04 VT 100% 40% NH 23% MA 26% ME 11%

Deposits by State

12/31/93 06/30/04

VT 100% 50% NH 21% MA 19% ME 10%

5

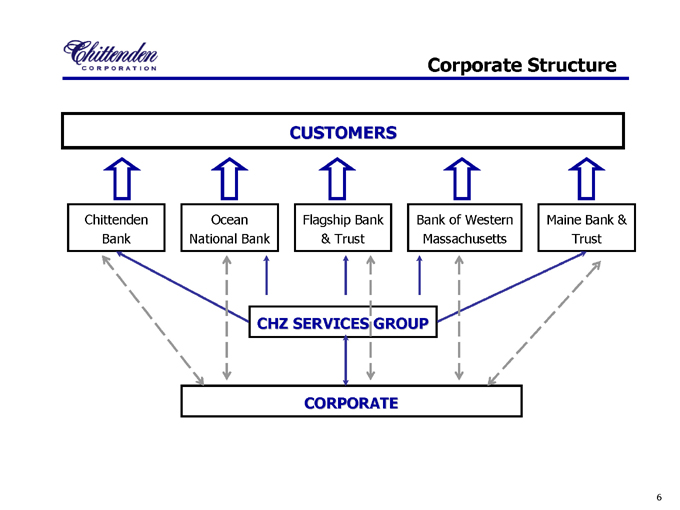

Corporate Structure

CUSTOMERS

Chittenden Bank

Ocean National Bank

Flagship Bank & Trust

Bank of Western Massachusetts

Maine Bank & Trust

CHZ SERVICES GROUP

CORPORATE

6

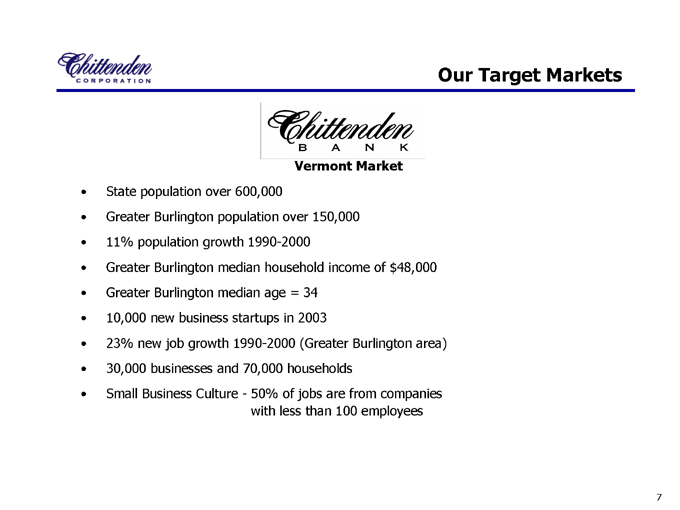

Our Target Markets

Vermont Market

State population over 600,000

Greater Burlington population over 150,000 11% population growth 1990-2000

Greater Burlington median household income of $48,000 Greater Burlington median age = 34 10,000 new business startups in 2003 23% new job growth 1990-2000 (Greater Burlington area) 30,000 businesses and 70,000 households Small Business Culture—50% of jobs are from companies with less than 100 employees

7

Our Target Markets

Greater Springfield Market

Population of over 450,000 in Hampden Co. Median household income of $40,000 Median age = 36 Above national/regional employment averages in education, insurance, health services, manufacturing 13 colleges located in Greater Springfield 1993—2000 Pioneer Valley job growth over 15% 23,000 businesses and 90,000 households

Greater Worcester Market

3rd largest city in New England Population of 750,000 in Worcester Co. Median household income of $48,000 Median age = 36 38,000 new jobs created in Worcester Co. between 1991—2001 Over 18% job growth in region (1993—2000)

Value of Worcester’s total assessed property value up nearly 15% in FY2003 Downtown office space occupancy of 90% Over 25,000 businesses and 110,000 households Known as “The Center of Excellence in Biotechnology”

8

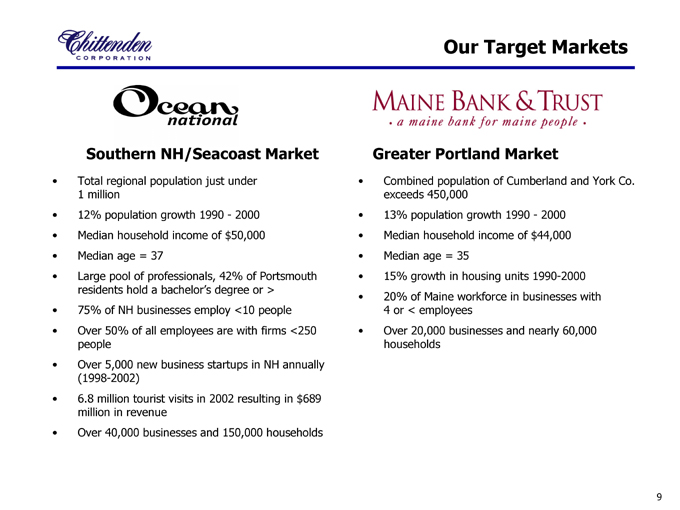

Our Target Markets

Southern NH/Seacoast Market

Total regional population just under 1 million 12% population growth 1990—2000 Median household income of $50,000 Median age = 37

Large pool of professionals, 42% of Portsmouth residents hold a bachelor’s degree or > 75% of NH businesses employ <10 people Over 50% of all employees are with firms <250 people Over 5,000 new business startups in NH annually (1998-2002) 6.8 million tourist visits in 2002 resulting in $689 million in revenue Over 40,000 businesses and 150,000 households

Greater Portland Market

Combined population of Cumberland and York Co. exceeds 450,000 13% population growth 1990—2000 Median household income of $44,000 Median age = 35 15% growth in housing units 1990-2000 20% of Maine workforce in businesses with 4 or < employees Over 20,000 businesses and nearly 60,000 households

9

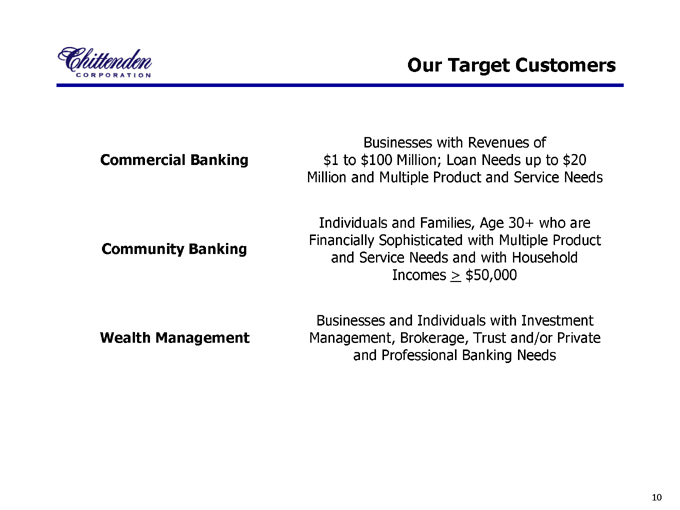

Our Target Customers

Businesses with Revenues of Commercial Banking $1 to $100 Million; Loan Needs up to $20 Million and Multiple Product and Service Needs

Individuals and Families, Age 30+ who are Financially Sophisticated with Multiple Product

Community Banking and Service Needs and with Household Incomes ³ $50,000

Businesses and Individuals with Investment Wealth Management Management, Brokerage, Trust and/or Private and Professional Banking Needs

10

Commercial & Community Banking

11

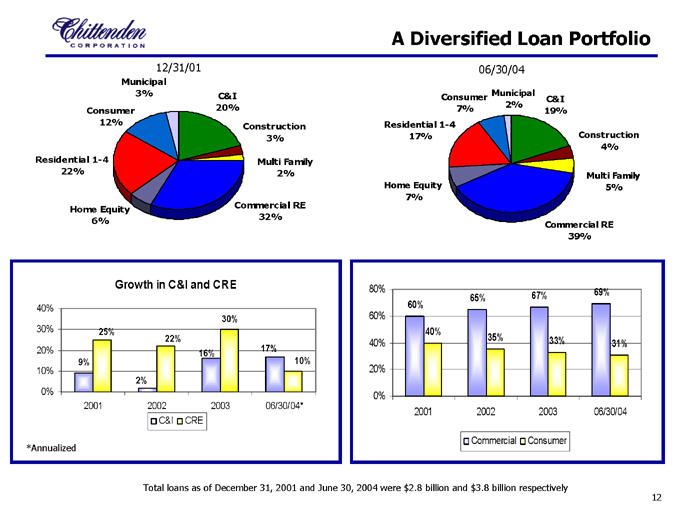

A Diversified Loan Portfolio

12/31/01

Municipal 3%

C&I 20%

Construction 3%

Multi Family 2%

Commercial RE

32%

Home Equity 6%

Residential 1-4 22%

Consumer 12%

06/30/04

Consumer 7%

Municipal 2%

C&I 19%

Residential 1-4 17%

Home Equity 7%

Construction 4%

Multi Family 5%

Commercial RE

39%

Growth in C&I and CRE

40% 30% 20% 10% 0%

9%

25%

2%

22%

16%

30%

17%

10%

2001

2002

2003

06/30/04*

CRE

C&I

80% 60% 40% 20% 0%

60%

40%

65%

35%

67%

33%

69%

31%

2001 2002 2003 06/30/04

Commercial

Consumer

Total loans as of December 31, 2001 and June 30, 2004 were $2.8 billion and $3.8 billion respectively

12

*Annualized

12

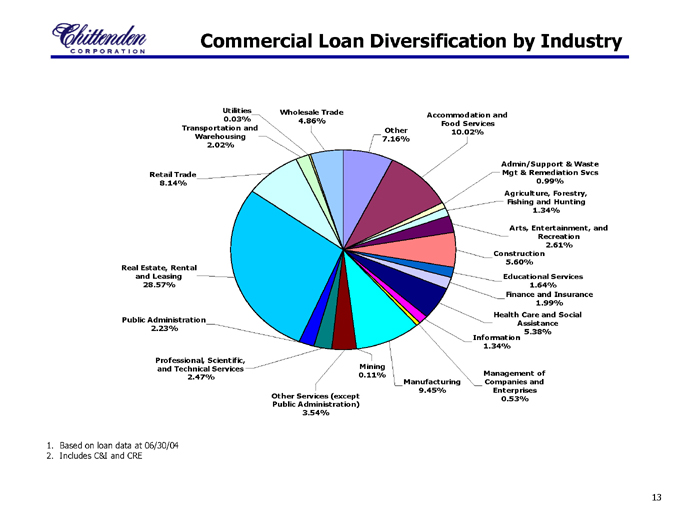

Commercial Loan Diversification by Industry

Utilities 0.03% Transportation and Warehousing 2.02%

Wholesale Trade 4.86%

Other 7.16%

Accommodation and Food Services 10.02%

Admin/Support & Waste Mgt & Remediation Svcs 0.99% Agriculture, Forestry, Fishing and Hunting 1.34%

Arts, Entertainment, and Recreation 2.61%

Construction 5.60%

Educational Services 1.64% Finance and Insurance 1.99%

Health Care and Social Assistance 5.38%

Information 1.34%

Management of Companies and Enterprises 0.53%

Manufacturing 9.45%

Mining 0.11%

Other Services (except Public Administration) 3.54%

Professional, Scientific, and Technical Services 2.47%

Public Administration 2.23%

Real Estate, Rental and Leasing 28.57%

Retail Trade 8.14%

1. Based on loan data at 06/30/04

2. Includes C&I and CRE

13

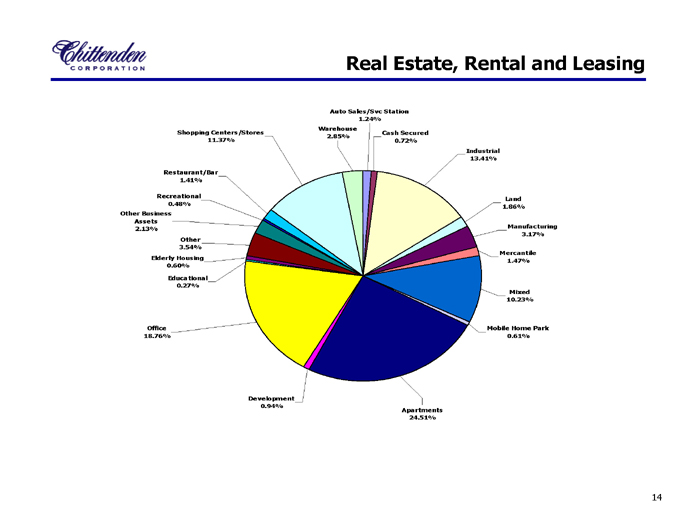

Real Estate, Rental and Leasing

Shopping Centers/Stores 11.37%

Auto Sales/Svc Station 1.24%

Warehouse 2.85%

Cash Secured 0.72%

Industrial 13.41%

Land 1.86%

Manufacturing 3.17%

Mercantile 1.47%

Mixed 10.23%

Mobile Home Park 0.61%

Apartments 24.51%

Development 0.94%

Office 18.76%

Educational 0.27%

Elderly Housing 0.60%

Other 3.54%

Other Business Assets 2.13%

Recreational 0.48%

Restaurant/Bar 1.41%

14

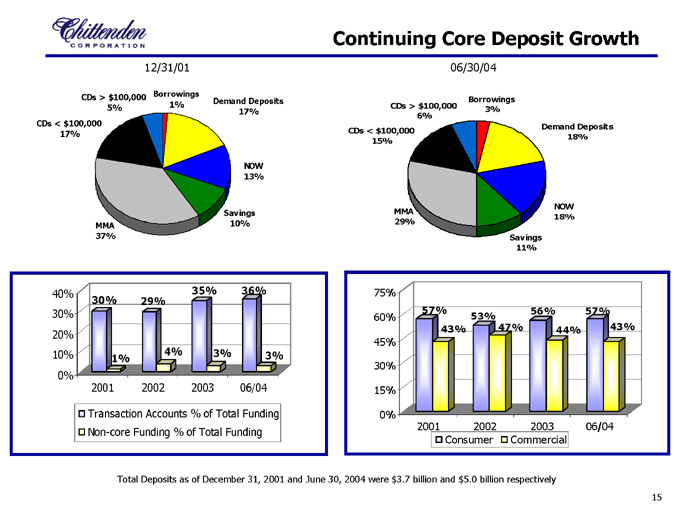

Continuing Core Deposit Growth

12/31/01

CDs > $100,000 Borrowings

1% Demand Deposits

5% 17%

CDs < $100,000 17%

MMA 37%

NOW 13%

Savings 10%

06/30/04

Borrowings CDs > $100,000 3% 6%

CDs < $100,000 15%

MMA 29%

Savings 11%

NOW 18%

Demand Deposits 18%

40% 30% 20% 10% 0%

30%

1%

29%

4%

35%

3%

36%

3%

2001 2002 2003 06/04

Transaction Accounts % of Total Funding Non-core Funding % of Total Funding

75%

60%

45% 30%

15%

0%

57%

43%

53%

47%

56%

44%

57%

43%

2001 2002 2003 06/04

Consumer

Commercial

Total Deposits as of December 31, 2001 and June 30, 2004 were $3.7 billion and $5.0 billion respectively

15

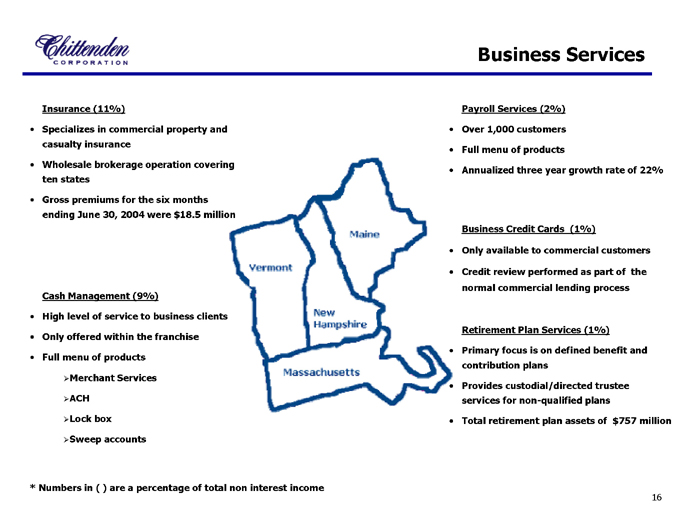

Business Services

Insurance (11%)

Specializes in commercial property and casualty insurance Wholesale brokerage operation covering ten states Gross premiums for the six months ending June 30, 2004 were $18.5 million

Cash Management (9%)

High level of service to business clients Only offered within the franchise Full menu of products

Merchant Services ACH

Lock box Sweep accounts

Payroll Services (2%) Over 1,000 customers Full menu of products

Annualized three year growth rate of 22%

Business Credit Cards (1%)

Only available to commercial customers

Credit review performed as part of the normal commercial lending process

Retirement Plan Services (1%) Primary focus is on defined benefit and contribution plans Provides custodial/directed trustee services for non-qualified plans Total retirement plan assets of $757 million

* Numbers in ( ) are a percentage of total non interest income

16

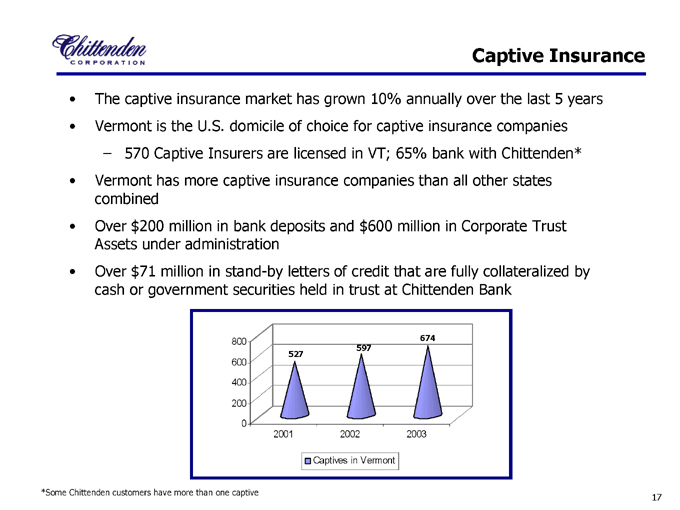

Captive Insurance

The captive insurance market has grown 10% annually over the last 5 years Vermont is the U.S. domicile of choice for captive insurance companies

570 Captive Insurers are licensed in VT; 65% bank with Chittenden*

Vermont has more captive insurance companies than all other states combined Over $200 million in bank deposits and $600 million in Corporate Trust Assets under administration Over $71 million in stand-by letters of credit that are fully collateralized by cash or government securities held in trust at Chittenden Bank

800 600 400 200 0

527

597

674

2001 2002 2003

Captives in Vermont

*Some Chittenden customers have more than one captive

17

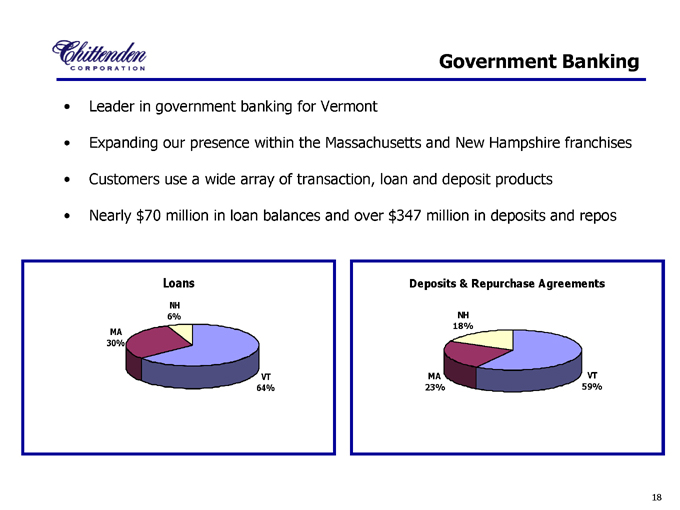

Government Banking

Leader in government banking for Vermont

Expanding our presence within the Massachusetts and New Hampshire franchises Customers use a wide array of transaction, loan and deposit products Nearly $70 million in loan balances and over $347 million in deposits and repos

Loans

NH 6%

MA 30%

VT 64%

Deposits & Repurchase Agreements

NH 18%

MA 23%

VT 59%

18

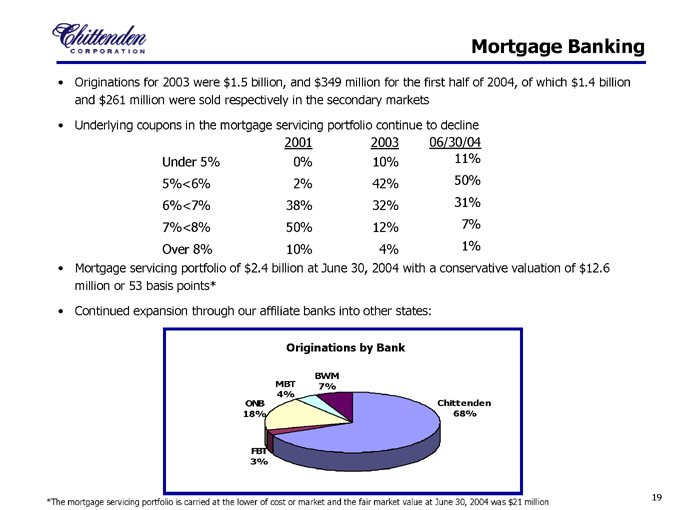

Mortgage Banking

Originations for 2003 were $1.5 billion, and $349 million for the first half of 2004, of which $1.4 billion and $261 million were sold respectively in the secondary markets Underlying coupons in the mortgage servicing portfolio continue to decline

2001 2003 06/30/04

Under 5% 0% 10% 11%

5%<6% 2% 42% 50%

6%<7% 38% 32% 31%

7%<8% 50% 12% 7%

Over 8% 10% 4% 1%

Mortgage servicing portfolio of $2.4 billion at June 30, 2004 with a conservative valuation of $12.6 million or 53 basis points* Continued expansion through our affiliate banks into other states:

Originations by Bank

BWM 7%

MBT 4%

ONB 18%

FBT 3%

Chittenden 68%

*The mortgage servicing portfolio is carried at the lower of cost or market and the fair market value at June 30, 2004 was $21 million

19

Wealth Management

20

Wealth Management

Assets under administration

Assets under management $1.9 billion Personal Trust/Custody 2.8 billion Retail Investments .2 billion Corporate Trust 2.0 billion Captive Insurance .6 billion Retirement Plan Services .8 billion

Total $8.3 billion

Private Banking

Loans $61.7 million Deposits $48.8 million

21

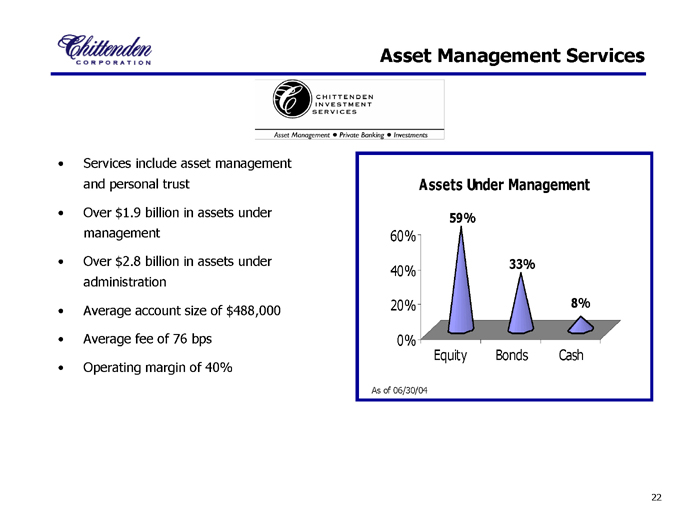

Asset Management Services

Services include asset management and personal trust Over $1.9 billion in assets under management Over $2.8 billion in assets under administration Average account size of $488,000 Average fee of 76 bps Operating margin of 40%

Assets Under Management

60% 40% 20% 0%

59%

33%

8%

Equity Bonds Cash

As of 06/30/04

22

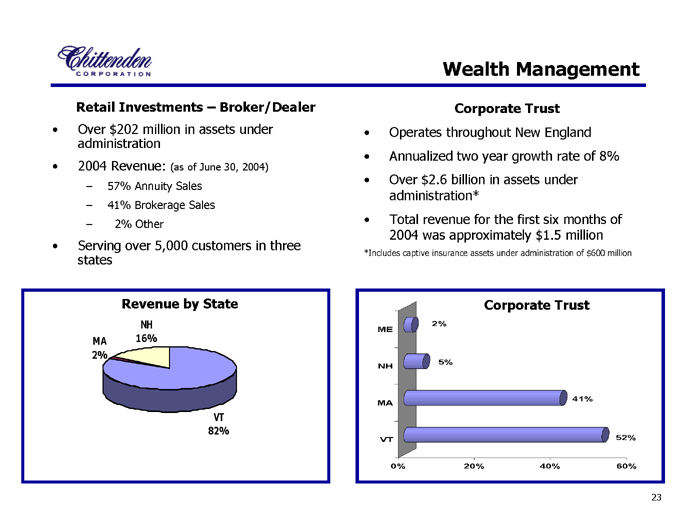

Wealth Management

Retail Investments – Broker/Dealer

Over $202 million in assets under administration

2004 Revenue: (as of June 30, 2004)

57% Annuity Sales 41% Brokerage Sales 2% Other

Serving over 5,000 customers in three states

Corporate Trust

Operates throughout New England Annualized two year growth rate of 8% Over $2.6 billion in assets under administration* Total revenue for the first six months of 2004 was approximately $1.5 million

*Includes captive insurance assets under administration of $600 million

Revenue by State

NH 16%

MA 2%

VT 82%

Corporate Trust

ME NH MA VT

2%

5%

41%

52%

0% 20% 40% 60%

23

Financial Performance

24

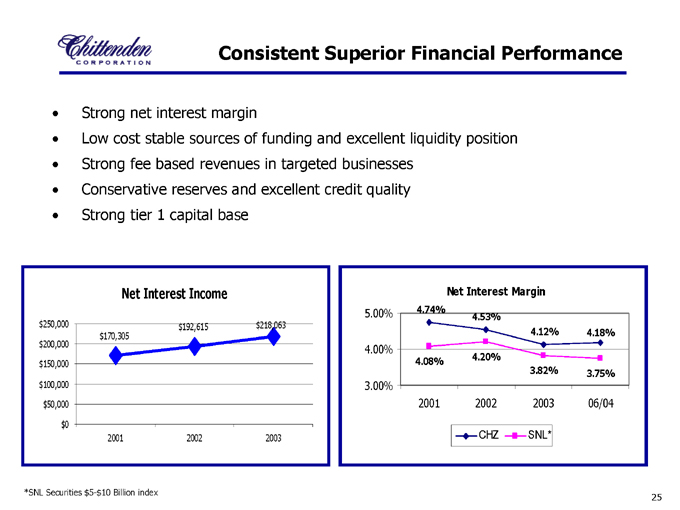

Consistent Superior Financial Performance

Strong net interest margin

Low cost stable sources of funding and excellent liquidity position

Strong fee based revenues in targeted businesses

Conservative reserves and excellent credit quality

Strong tier 1 capital base

Net Interest Income

$250,000 $200,000 $150,000 $100,000 $50,000 $0

2001 2002 2003

$170,305 $192,615 $218,063

Net Interest Margin

5.00%

4.00%

3.00%

2001 2002 2003 06/04

4.74% 4.53% 4.12% 4.18%

4.08% 4.20% 3.82% 3.75%

CHZ SNL*

*SNL Securities $5-$10 Billion index

25

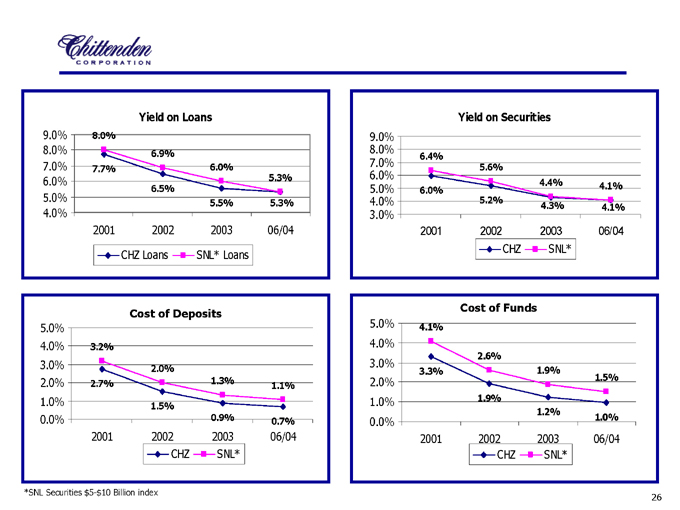

Yield on Loans

9.0% 8.0% 7.0% 6.0% 5.0% 4.0%

2001 2002 2003 06/04

8.0% 6.9% 6.0% 5.3%

7.7% 6.5% 5.5% 5.3%

CHZ Loans SNL* Loans

Yield on Securities

9.0% 8.0% 7.0% 6.0% 5.0% 4.0% 3.0%

2001 2002 2003 06/04

6.4% 5.6% 4.4% 4.1%

6.0% 5.2% 4.3% 4.1%

CHZ SNL*

Cost of Deposits

5.0% 4.0% 3.0% 2.0% 1.0% 0.0%

2001 2002 2003 06/04

3.2% 2.0% 1.3% 1.1%

2.7% 1.5% 0.9% 0.7%

CHZ SNL*

Cost of Funds

5.0% 4.0% 3.0% 2.0% 1.0% 0.0%

2001 2002 2003 06/04

4.1% 2.6% 1.9% 1.5%

3.3% 1.9% 1.2% 1.0%

CHZ SNL*

*SNL Securities $5-$10 Billion index

26

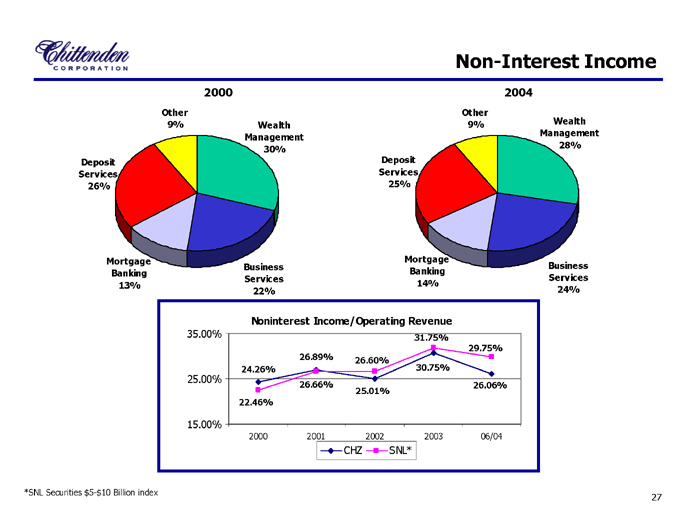

Non-Interest Income

2000

Other 9%

Deposit Services 26%

Wealth Management 30%

Mortgage Banking 13%

Business Services 22%

2004

Other 9%

Deposit Services 25%

Wealth Management 28%

Mortgage Banking 14%

Business Services 24%

Noninterest Income/Operating Revenue

35.00% 25.00% 15.00%

24.26%

22.46%

26.89%

26.66%

26.60%

25.01%

31.75%

30.75%

29.75%

26.06%

2000 2001 2002 2003 06/04

CHZ

SNL*

*SNL Securities $5-$10 Billion index 27

27

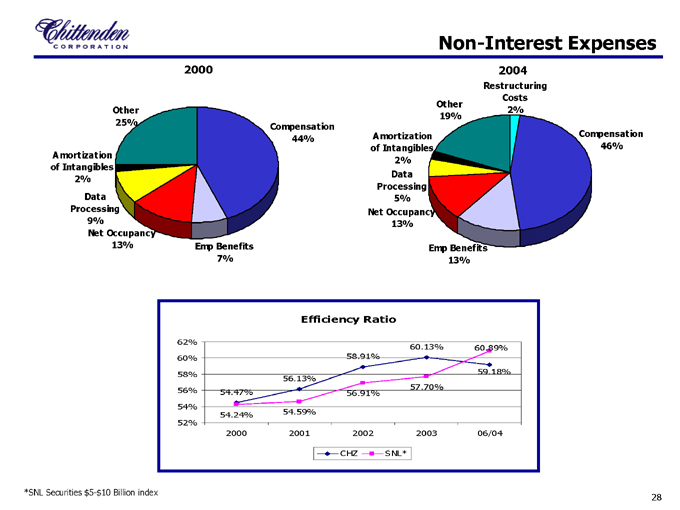

Non-Interest Expenses

2000

Other 25%

Amortization of Intangibles 2%

Data Processing 9%

Net Occupancy 13%

Emp Benefits 7%

Compensation 44%

2004

Restructuring Costs 2%

Other 19%

Amortization of Intangibles 2%

Data Processing 5%

Net Occupancy 13%

Emp Benefits 13%

Compensation 46%

Efficiency Ratio

62% 60% 58% 56% 54% 52%

54.47%

54.24%

2000

56.13%

54.59%

2001

58.91%

56.91%

2002

60.13%

57.70%

2003

60.89%

59.18%

06/04

CHZ

SNL*

*SNL Securities $5-$10 Billion index 28

28

Financial Summary

Earnings

Ratios

Credit

Capital

2001 2002 2003 06/30/04

Per Common Share

Diluted Earnings $ 1.80 $ 1.96 $ 2.07 $0.96

Cash Earnings $ 1.86 $ 1.98 $ 2.12 $0.98

Dividends $ 0.76 $ 0.79 $ 0.80 $0.42

Book Value $ 11.56 $ 13.11 $ 15.82 $ 15.93

Tangible Book Value $ 10.52 $ 11.09 $ 9.30 $9.46

Dividend Payout Ratio 42.15% 39.88% 37.84% 43.31%

Return on Average Equity 16.55% 16.12% 13.90% 12.18%

Return on Average Tangible Equity 18.52% 19.27% 22.92% 20.70%

Return on Average Assets 1.51% 1.40% 1.29% 1.23%

Return on Average Tangible Assets 1.57% 1.44% 1.37% 1.32%

Net Interest Margin 4.74% 4.53% 4.12% 4.18%

Efficiency Ratio 56.13% 58.56% 60.48% 59.18%

NPAs to Loans & OREO 0.46% 0.49% 0.39% 0.54%

Loan Loss Reserve to Loans 1.59% 1.62% 1.54% 1.50%

Net Charge-Offs to Average Loans 0.24% 0.28% 0.16% 0.03%

Tangible Capital 8.19% 7.29% 6.02% 6.24%

Leverage 7.99% 9.28% 7.79% 8.22%

Tier 1 10.32% 12.25% 10.07% 10.46%

Risk-Based 11.57% 13.50% 11.32% 11.73%

29

Risk Management

30

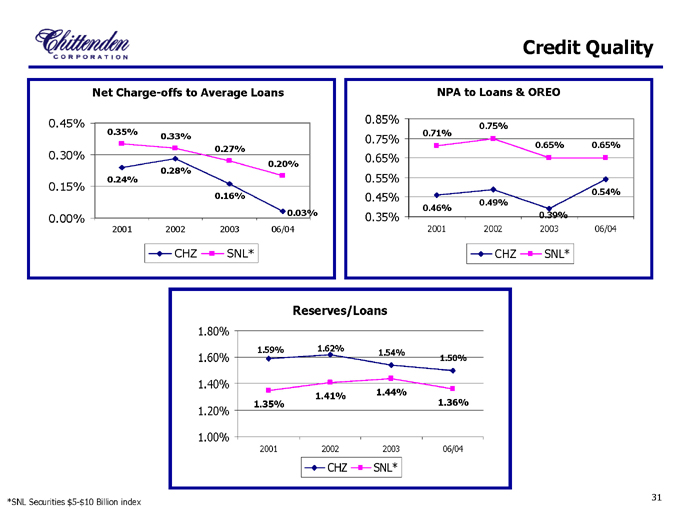

Credit Quality

Net Charge-offs to Average Loans

0.45% 0.30% 0.15% 0.00%

0.35%

0.24%

2001

0.33%

0.28%

2002

0.27%

0.16%

2003

0.20%

0.03%

06/04

CHZ

SNL*

NPA to Loans & OREO

0.85% 0.75% 0.65% 0.55% 0.45% 0.35%

0.71%

0.46%

0.75%

0.49%

0.65%

0.39%

0.65%

0.54%

2001 2002 2003 06/04

CHZ

SNL*

Reserves/Loans

1.80% 1.60% 1.40%

1.20% 1.00%

1.59%

1.35%

1.62%

1.41%

1.54%

1.44%

1.50%

1.36%

2001 2002 2003 06/04

CHZ

SNL*

*SNL Securities $5-$10 Billion index

31

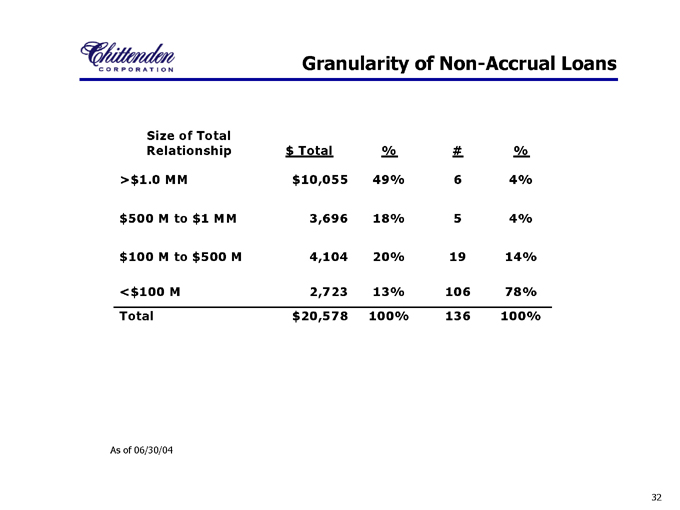

Granularity of Non-Accrual Loans

Size of Total

Relationship $ Total % # %

>$ 1.0 MM $10,055 49% 6 4%

$500 M to $1 MM 3,696 18% 5 4%

$100 M to $500 M 4,104 20% 19 14%

<$ 100 M 2,723 13% 106 78%

Total $20,578 100% 136 100%

As of 06/30/04

32

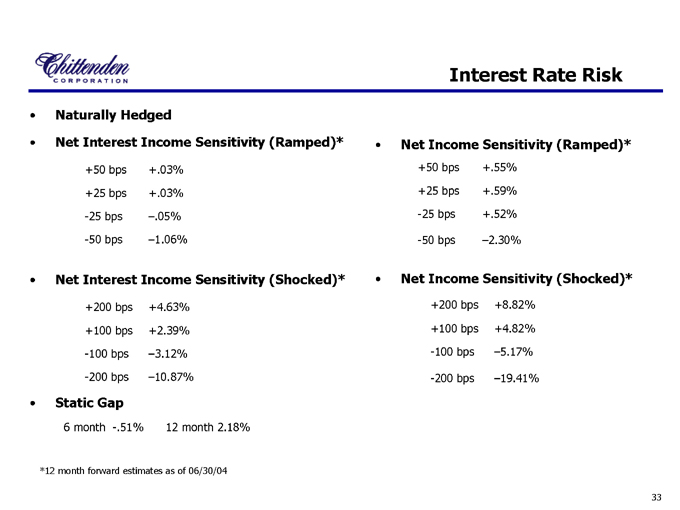

Interest Rate Risk

Naturally Hedged

Net Interest Income Sensitivity (Ramped)*

+50 bps +.03% +25 bps +.03% -25 bps –.05% -50 bps –1.06%

Net Interest Income Sensitivity (Shocked)*

+200 bps +4.63% +100 bps +2.39% -100 bps –3.12% -200 bps –10.87%

Static Gap

6 month -.51% 12 month 2.18%

Net Income Sensitivity (Ramped)*

+50 bps +.55% +25 bps +.59% -25 bps +.52%

-50 bps –2.30%

Net Income Sensitivity (Shocked)*

+200 bps +8.82% +100 bps +4.82% -100 bps –5.17%

-200 bps –19.41%

*12 month forward estimates as of 06/30/04

33

In Summary

34

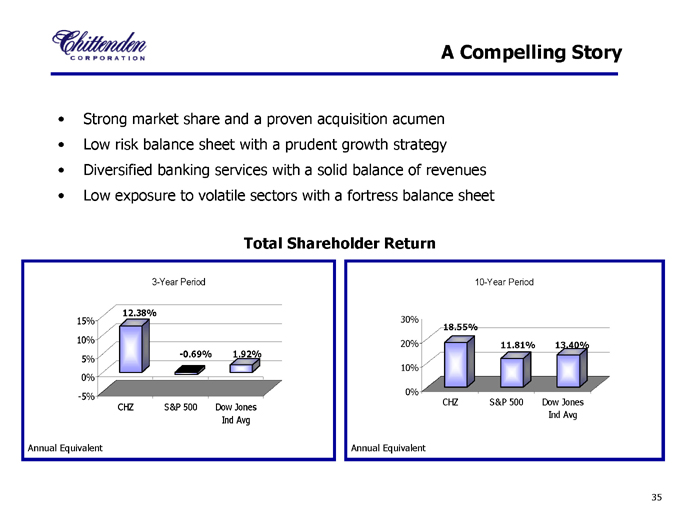

A Compelling Story

Strong market share and a proven acquisition acumen Low risk balance sheet with a prudent growth strategy Diversified banking services with a solid balance of revenues Low exposure to volatile sectors with a fortress balance sheet

Total Shareholder Return

3-Year Period

15% 10% 5% 0% -5%

12.38%

-0.69%

1.92%

CHZ S&P 500 Dow Jones Ind Avg

Annual Equivalent

10-Year Period

30% 20% 10% 0%

18.55%

11.81%

13.40%

CHZ S&P 500 Dow Jones Ind Avg

Annual Equivalent

35

Visit our website for a wide range of products, latest financial reports and many

other interactive services: www.chittendencorp.com

This presentation contains “forward-looking statements” which may describe future plans and strategic initiatives. These forward-looking statements are based on current plans and expectations, which are subject to a number of factors and uncertainties that could cause future results to differ from historical performance or future expectations.

36