As of June 30, 2006 Exhibit 99.1 |

2 • Multi-bank holding company with significant operating autonomy at the individual banks • Banking assets of $6.5 billion at June 30, 2006 • Listed on the NYSE (CHZ), market capitalization as of June 30, 2006 was $1.2 billion • 122 full service banking offices and 153 ATM locations in VT, NH, MA, ME and CT • Commercial loans represent over 70% of the total loan portfolio and core deposits comprise over 95% of total funding • Strong wealth management operation with assets under administration of $8.6 billion and assets under management of $2.1 billion • Excellent credit quality with year-to-date net charge-offs of .04% and an allowance for credit losses to loans (excluding municipal loans) of 1.41% Who We Are |

3 Recognized competency in an attractive business mix Deep relationships with worthwhile customers Conservative underwriting standards and disciplined lending Efficient generator of low cost stable deposits Proven leadership focus to achieve superior financial results Well-established and tangible shareholder orientation A Tradition of Success |

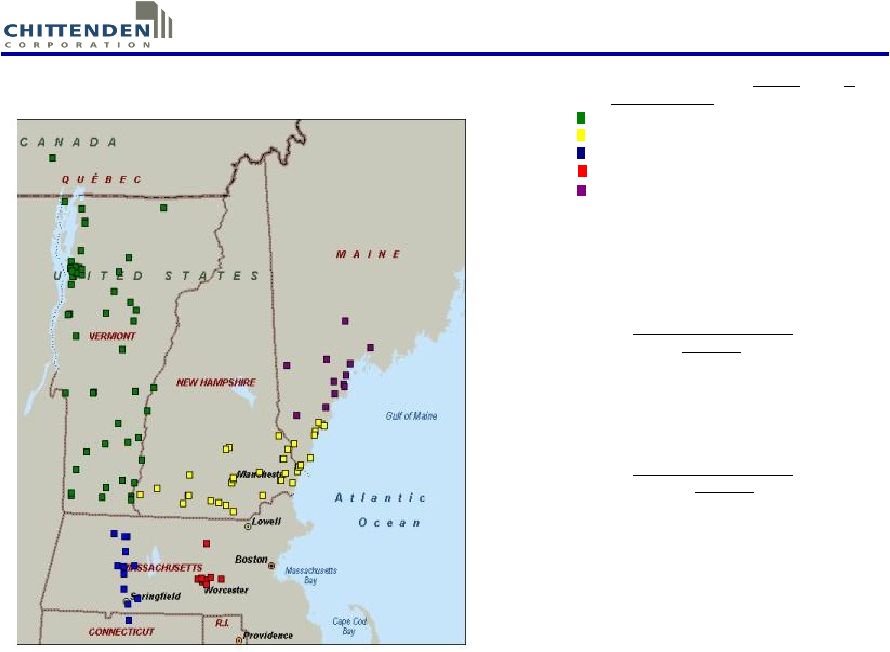

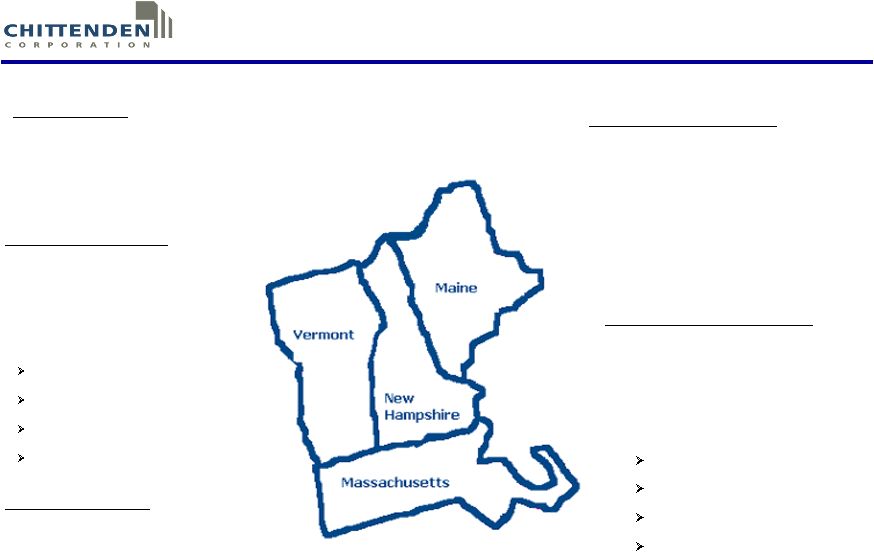

4 Our Target Markets 6/30/06 % Assets (in millions) Chittenden Bank $3,168 49% Ocean National Bank $1,658 26% Bank of Western Mass $729 11% Flagship Bank $540 8% Maine Bank & Trust $366 6% Total $6,461 100% ____ ___ VT 42% NH 22% MA 27% ME 9% VT 51% NH 19% MA 20% ME 10% 6/30/06 Loans by State Deposits by State 6/30/06 |

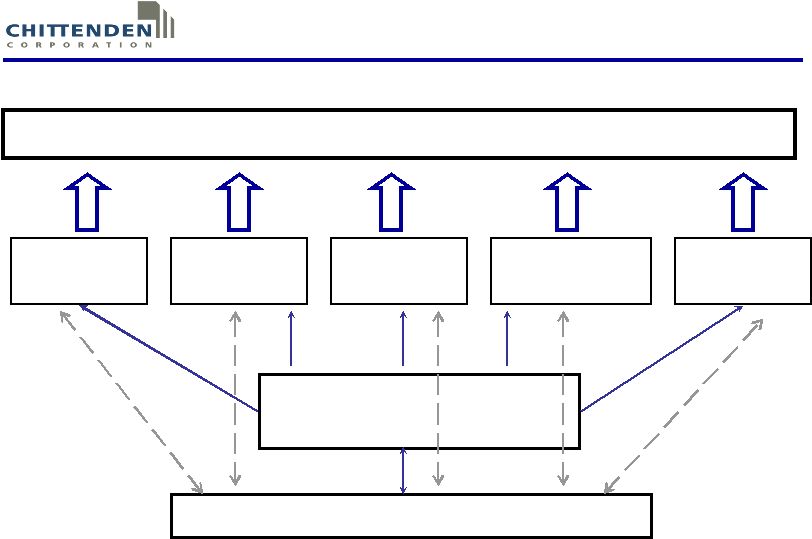

5 CUSTOMERS CUSTOMERS Chittenden Bank Ocean National Bank Bank of Western Massachusetts Flagship Bank & Trust Maine Bank & Trust CHITTENDEN SERVICES CHITTENDEN SERVICES GROUP GROUP CORPORATE CORPORATE Corporate Structure |

6 Vermont Market • Population over 620,000 • Greater Burlington population 150,000 • 13% population growth in Chittenden County since 1990 • Greater Burlington median household income of $48,000 • Greater Burlington median age = 34 • Homeownership rate of over 70% exceeds national average • Median housing value increased by 24% from 2000-2003 • Nearly 9,000 new business startups in 2004 • 23% new job growth 1990-2000 (Greater Burlington area) • 30,000 businesses and 70,000 households • Small Business Culture - 50% of jobs are from companies with less than 100 employees • Over 20 colleges and universities in Vermont Our Target Markets |

7 Greater Springfield Market Greater Worcester Market • Population nearly 850,000 in Pioneer Valley and North Central, CT • Median household income of $41,000 • Median age = 36 • Above national/regional employment averages in education, insurance, health services, manufacturing • 1993 - 2000 Pioneer Valley job growth over 15% • 23,000 businesses and 90,000 households • Telecommunications crossroads for New England • Hartford/Springfield “the knowledge corridor”—26 colleges and universities • 3rd largest city in New England • Population of 777,000 in Worcester Co. • 6 million people within a 50 mile radius • Median household income of $48,000 • Median age = 36 • 32,000 new jobs created in Worcester area between 1991 - 2003 • Over 18% job growth in region (1993 - 2000) • Value of Worcester’s total assessed property value up nearly 15% in FY2003 • Over 25,000 businesses and 110,000 households • 16 colleges in Worcester Co. • Known as “The Center of Excellence in Biotechnology” Our Target Markets |

8 Southern NH/Seacoast Market • Total regional population over 1 million • 17% population growth 1990 - 2003 • Median household income of $50,000 • Median age = 37 • Large pool of professionals, 42% of Portsmouth residents hold a bachelor’s degree or > • 75% of NH businesses employ <10 people • Over 50% of all employees are with firms <250 people • Over 5,000 new business startups in NH annually (1998-2002) • New Hampshire gross domestic product up 5.6% in 2003, 16 fastest growth in the United States • Over 40,000 businesses and 150,000 households • NH business friendly—no sales tax, inventory tax, use tax, income tax, or capital gains tax Greater Portland Market • Combined population of Cumberland and York Co. nearly 470,000 • 15% population growth 1990 - 2003 • Median household income of $44,000 • Median age = 35 • Median housing value up 36% for 2000-2003 • 30% of population with bachelor’s degree or higher • 25% increase in residential building permits from 2000-2003 • 20% of Maine workforce in businesses with 4 or < employees • Over 20,000 businesses and nearly 60,000 households • 3.6 million tourist visits annually to Portland area • Named #1 market in small business vitality (American City Business Journal, 2005) Our Target Markets th |

9 Our Target Customers Commercial Banking Businesses with Revenues of $1 to $100 Million; Loan Needs up to $20 Million; Multiple Product and Service Needs Community Banking Individuals and Families who are Financially Sophisticated with Multiple Product and Service Needs and Household Incomes building to > $50,000 Wealth Management Businesses and Individuals with Investment Management, Brokerage, Trust and/or Private and Professional Banking Needs |

10 Commercial & Community Banking * * * * * * |

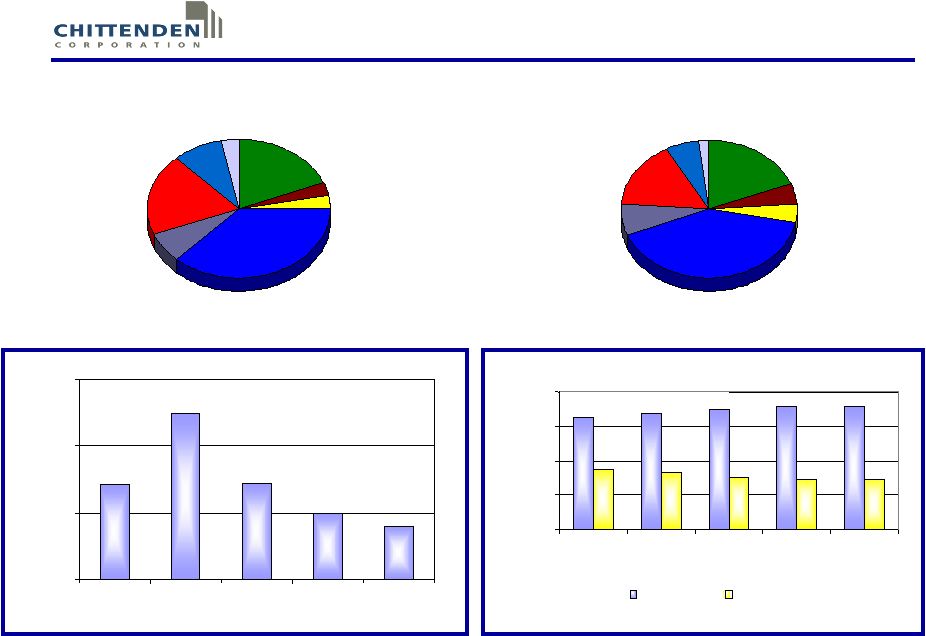

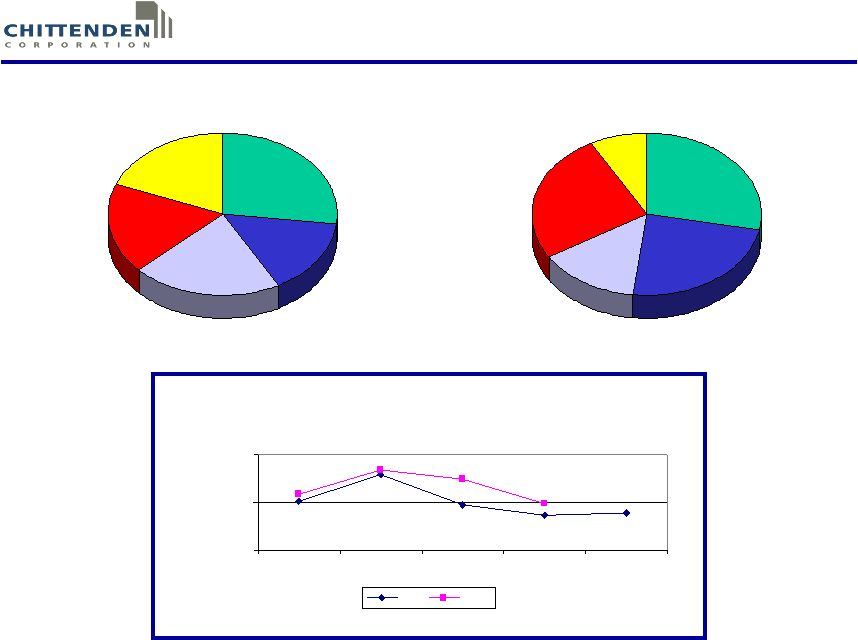

11 A Diversified Loan Portfolio 12/31/02 6/30/06 Consumer 9% Municipal 3% Multi Family 3% Commercial RE 37% Home Equity 7% Residential 19% Construction 3% C&I 19% Total loans as of December 31, 2002 and June 30, 2006 were $3.0 billion and $4.6 billion respectively Consumer 6% Municipal 2% Multi Family 4% Commercial RE 41% Home Equity 7% Residential 16% Construction 5% C&I 19% Growth in C & I and Commercial Real Estate 25% 14% 10% 8% 14% 0% 10% 20% 30% 2002 2003 2004 2005 6/06* *annualized 65% 67% 70% 71% 71% 29% 29% 30% 33% 35% 0% 20% 40% 60% 80% 2002 2003 2004 2005 6/06 Commercial Consumer |

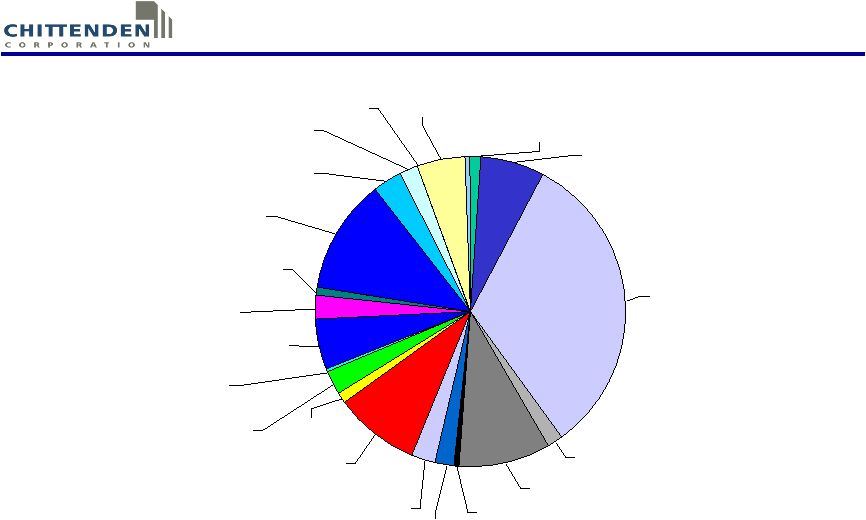

12 Commercial Loan Diversification by Industry 1. This chart encompasses the total commercial loan portfolio at June 30, 2006, which includes C&I, municipal, commercial RE, construction, and multi family loans. 2. Industry classifications are based on NAICS sector codes and loan type Admin/Support & Waste Mgmt & Remediation Svcs 1.05% Arts, Entertainment & Rec 2.50% Construction 6.59% Agriculture, Forestry, Fishing & Hunting 1.06% Other 0.46% Wholesale Trade 5.07% Accomodation & Food Srvc 12.00% Other Srvc (except Public Admin) 3.04% Transportation & Warehousing 1.83% Real Estate, Rental & Leasing 32.43% Utilities 0.02% Health Care & Soc Assist 5.03% Finance & Insurance 1.72% Manufacturing 9.43% Educational Srvc 2.41% Professional, Scientific, & Tech Srvc 2.54% Mgmt of Companies & Enterprises 0.32% Retail Trade 8.80% Information 1.24% Mining 0.55% Public Admin 1.92% |

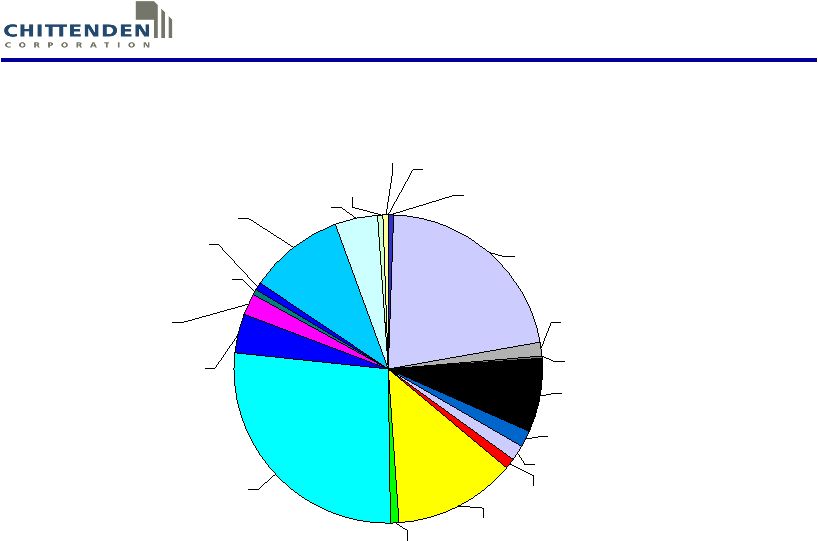

13 Cash Secured 0.56% Warehouse 4.40% Restaurant/Bar 1.06% Other Business Assets 2.23% Development 0.64% Elderly Housing 0.45% Other 4.24% Office 26.89% Mobile Home Park 0.72% Mixed 12.93% Industrial 7.71% Apartments 21.74% Educational 0.08% Recreational 0.45% Land 1.69% Mercantile 1.12% Manufacturing 1.56% Hotel/Motel 0.49% Auto Sales/Svc Station 1.21% Shopping Ctr/Stores 9.83% Real Estate, Rental and Leasing 1. This chart is a subset of the Commercial Loan Diversification by Industry chart on page 12 2. Industry classifications are based on NAICS sector codes |

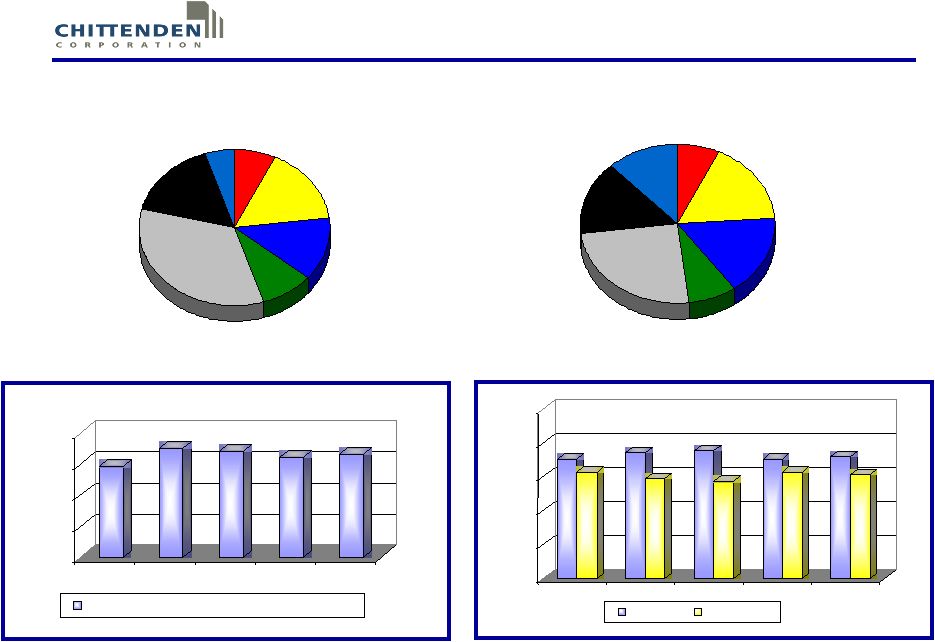

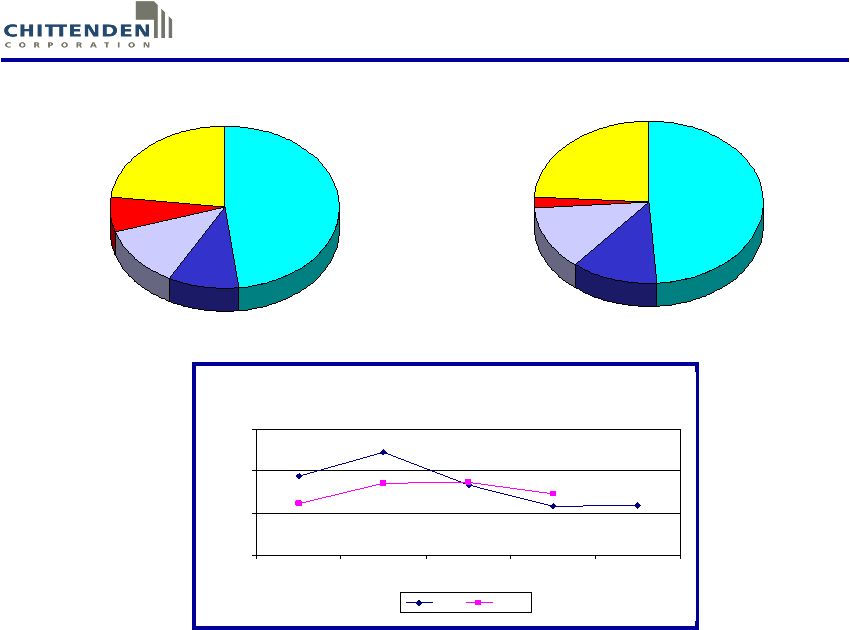

14 Continuing Core Deposit Growth 12/31/02 6/30/06 Total Deposits as of December 31, 2002 and June 30, 2006 were $4.1 billion and $5.7 billion respectively CDs < $100,000 16% CDs > $100,000 5% CMA/MMA 34% Demand Deposits 16% NOW 13% Savings 9% Borrowings 7% CDs < $100,000 15% CDs > $100,000 12% CMA/MMA 25% Demand Deposits 17% NOW 16% Savings 8% Borrowings 7% 29% 35% 34% 32% 33% 0% 10% 20% 30% 40% 2002 2003 2004 2005 6/06 Transaction Deposits % of Total Funding 53% 47% 56% 44% 57% 43% 53% 47% 54% 46% 0% 15% 30% 45% 60% 75% 2002 2003 2004 2005 6/06 Consumer Commercial |

15 Business Services Cash Management (5%) • High level of service to business clients • Seasoned delivery team with national level expertise • Full menu of products Merchant Services ACH Lock box Sweep accounts Payroll Services (4%) • Over 1,400 customers • Full menu of products • Annualized three year growth rate of 20% Business Credit Cards (2%) • Only available to commercial customers • Credit review performed as part of the normal commercial lending process • Outstanding loans were $11.2 million and interchange fee income for the first six months of 2006 was $726,000 Retirement Plan Services (1%) • Primary focus is on defined benefit and contribution plans • Over 465 customers advised • Total retirement plan assets of $1.1 billion • Full array of services Design Administration/recordkeeping Custodial/trustee Investment management Insurance (10%) • Specializes in commercial property and casualty insurance • Gross premiums for the first six months of 2006 were $33 million * Numbers in ( ) are a percentage of total noninterest income |

16 Captive Insurance • The captive insurance market has grown 15% annually over the last 3 years • Vermont is the U.S. domicile of choice for captive insurance companies – 65% of the active captive insurers bank with Chittenden* • Vermont has more captive insurance companies than all other states combined • Over $203 million in bank deposits and over $1 billion in Institutional Trust Assets under administration • Over $61 million in stand-by letters of credit that are fully collateralized by cash or government securities held in trust at Chittenden Bank *Some Chittenden customers have more than one captive 597 674 717 754 770 0 200 400 600 800 2002 2003 2004 2005 6/06 Captives in Vermont |

17 Government Banking • Leader in government banking for Vermont • Expanding our presence within the Massachusetts and New Hampshire franchises • Customers use a wide array of transaction, loan and deposit products • Over $90 million in municipal loans and $382 million in deposits and repos Loans VT 69% MA 26% NH 5% Deposits & Repurchase Agreements VT 50% MA 24% NH 26% |

18 Mortgage Banking • Originations for the first six months of 2005 and 2006 were $282 million and $204 million, of which $195 million and $145 million, respectively, were sold in the secondary markets • Underlying coupons in the mortgage servicing portfolio continue to decline • Mortgage servicing portfolio of $2.1 billion at June 30, 2006 with a conservative valuation of $14.5 million or 70 basis points* • Continued expansion through our affiliate banks into other states 2001 2004 2005 6/06 Under 5% 0% 11% 10% 9% 5%<6% 2% 52% 55% 52% 6%<7% 38% 30% 30% 33% 7%<8% 50% 6% 4% 5% Over 8% 10% 1% 1% 1% *The mortgage servicing portfolio is carried at the lower of cost or market and the fair market value at June 30, 2006 was $23.8 million, or 118 basis points Originations by Bank FBT 3% ONB 21% Chittenden 60% BWM 11% MBT 5% |

19 Wealth Management * * * * * * |

20 • Assets under administration – Assets under discretionary management $2.1 billion – Institutional/Personal Trust/Custody 1.5 billion – Retail Investments .2 billion – Bond Administration Services 2.7 billion – Captive Insurance 1.0 billion – Retirement Plan Services 1.1 billion Total $8.6 billion Wealth Management |

21 Asset Management Services • Services include asset management and personal trust • $2.1 billion in assets under management • Over $1.5 billion in assets under administration • Average relationship size of $1.2 million • Average managed account fee of 69 bps • Operating margin of approximately 40% As of 6/30/06 Assets Under Management 52% 34% 14% 0% 20% 40% 60% Equity Bonds Cash |

22 Wealth Management Retail Investments – Broker/Dealer • $223 million in assets under administration • 2006 Revenue: – 8% Annuity – 77% Brokerage – 15% Other • Serving over 9,000 customers in four states Bond Administration Services • Operates throughout New England • Over $2.7 billion in assets under administration • Revenue for the first six months of 2006 was $302,000 Revenue by State VT 75% MA 10% NH/ME 15% Bond Administration Revenue by State 1% 62% 30% 7% 0% 20% 40% 60% 80% VT MA NH ME |

23 Financial Performance * * * * * * |

24 Consistent Superior Financial Performance Strong net interest margin Low cost stable sources of funding and excellent liquidity position Strong fee based revenues in targeted businesses Conservative reserves and excellent credit quality Strong capital base *SNL Securities $5-$10 Billion index; data for 6/30/06 not yet available Net Interest Margin 4.12% 4.21% 4.31% 4.21% 4.20% 3.82% 3.89% 3.89% 4.53% 3.00% 4.00% 5.00% 2002 2003 2004 2005 6/06 CHZ SNL* |

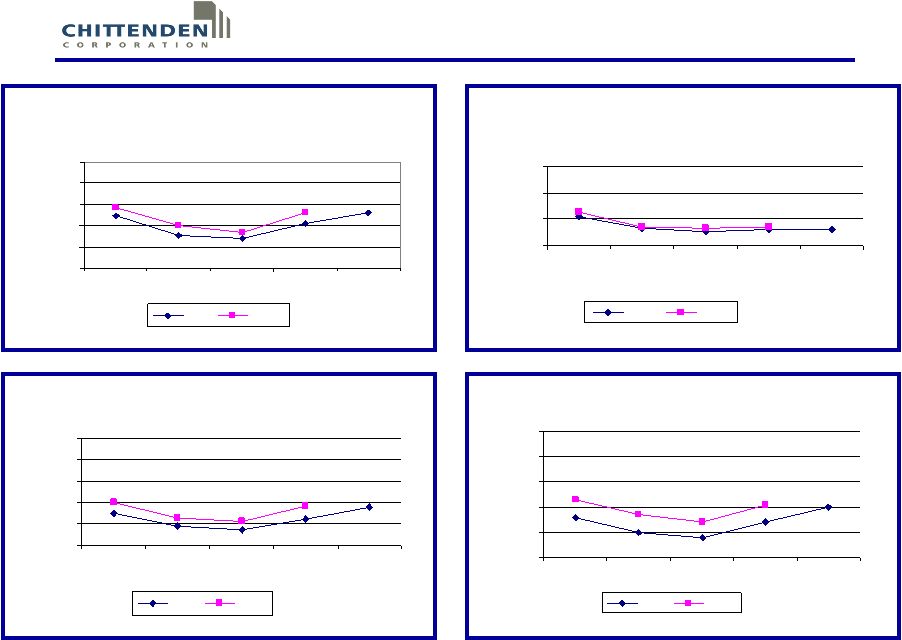

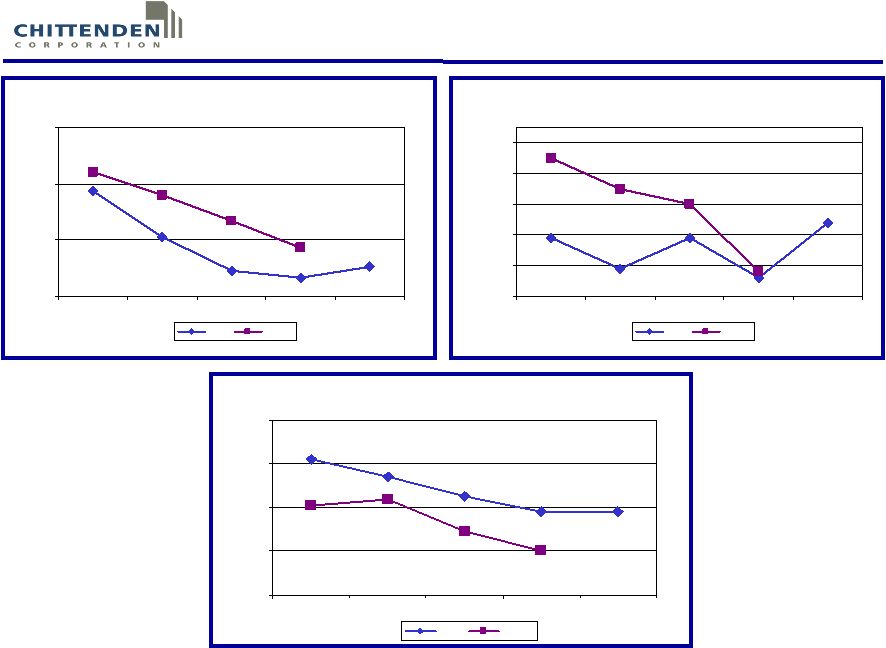

25 Average Cost of Funds Average Cost of Deposits Average Yield on Securities Average Yield on Loans 6.5% 5.5% 5.4% 6.9% 6.0% 5.7% 6.6% 6.6% 6.1% 4.0% 5.0% 6.0% 7.0% 8.0% 9.0% 2002 2003 2004 2005 6/06 CHZ SNL* 5.2% 4.3% 5.6% 4.4% 4.3% 4.5% 4.2% 4.1% 4.2% 3.0% 5.0% 7.0% 9.0% 2002 2003 2004 2005 6/06 CHZ SNL* 1.8% 1.2% 0.7% 0.9% 1.5% 1.8% 1.1% 1.3% 2.0% 0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 2002 2003 2004 2005 6/06 CHZ SNL* 2.0% 1.4% 0.8% 1.0% 1.6% 2.1% 1.4% 1.7% 2.3% 0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 2002 2003 2004 2005 6/06 CHZ SNL* *SNL Securities $5-$10 Billion index; data for 6/30/06 not yet available |

26 Noninterest Income Business Services 15% Mortgage Banking 21% Deposit Services 18% Other 19% Wealth Management 27% 6/30/06 12/31/02 Business Services 24% Mortgage Banking 14% Deposit Services 26% Other 8% Wealth Management 28% Noninterest Income/Operating Revenue 25.25% 30.79% 22.69% 22.26% 24.56% 31.75% 24.84% 29.98% 26.66% 15.00% 25.00% 35.00% 2002 2003 2004 2005 6/06 CHZ SNL* *SNL Securities $5-$10 Billion index; data for 6/30/06 not yet available |

27 Noninterest Expense 12/31/02 6/30/06 Benefits 12% Occupancy 13% DP Exp 2% Other 24% Compensation 49% *SNL Securities $5-$10 Billion index; data for 6/30/06 not yet available Prior year amounts reflect the modified retrospective application of SFAS 123-R Benefits 10% Occupancy 12% DP Exp 7% Other 23% Compensation 48% Efficiency Ratio 59.56% 61.82% 56.91% 58.87% 56.74% 58.67% 56.67% 57.81% 58.96% 52% 56% 60% 64% 2002 2003 2004 2005 6/06 CHZ SNL* |

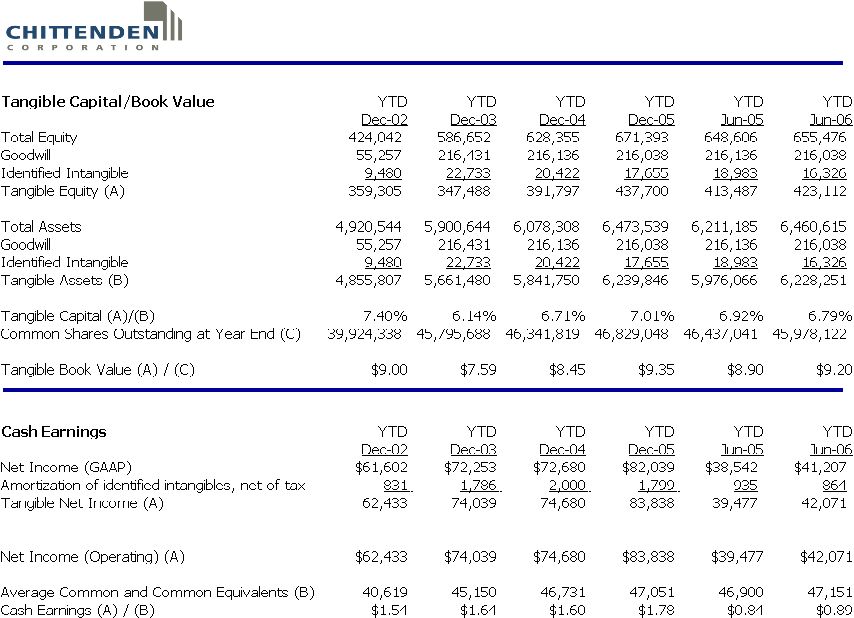

28 Financial Summary 2002 2003 2004 2005 6/05 6/06 Per Common Share Earnings Diluted Earnings $1.52 $1.60 $1.56 $1.74 $0.82 $0.87 Cash Earnings* $1.54 $1.64 $1.60 $1.78 $0.84 $0.89 Dividends $0.63 $0.64 $0.70 $0.72 $0.36 $0.38 Book Value $10.62 $12.81 $13.56 $14.34 $13.97 $14.26 Tangible Book Value* $9.00 $7.59 $8.45 $9.35 $8.90 $9.20 Ratios Dividend Payout Ratio 41.20% 39.17% 43.88% 40.78% 43.33% 43.19% Return on Average Equity 15.45% 13.27% 12.13% 12.72% 12.27% 12.48% Return on Average Tangible Equity* 18.37% 21.75% 20.32% 20.22% 19.77% 19.40% Return on Average Assets 1.36% 1.25% 1.23% 1.32% 1.27% 1.29% Return on Average Tangible Assets* 1.39% 1.33% 1.32% 1.40% 1.35% 1.36% Net Interest Margin 4.53% 4.12% 4.21% 4.31% 4.29% 4.21% Efficiency Ratio 59.56% 61.82% 58.67% 56.67% 58.97% 56.74% Credit NPAs to Loans & OREO 0.49% 0.39% 0.49% 0.36% 0.54% 0.54% Credit Loss Reserve to Loans 1.62% 1.54% 1.45% 1.38% 1.43% 1.38% Net Charge-Offs to Average Loans** 0.28% 0.16% 0.07% 0.05% 0.04% 0.08% Capital Tangible* 7.40% 6.14% 6.71% 7.01% 6.92% 6.79% Leverage 9.37% 7.91% 8.54% 9.21% 9.10% 9.04% Tier 1 12.39% 10.22% 10.61% 11.23% 10.73% 11.29% Risk-Based 13.64% 11.47% 11.82% 12.40% 11.92% 12.49% * see Appendix **Net charge-offs to average loans are annualized for all periods Prior year amounts reflect the modified retrospective application of SFAS 123-R |

29 Risk Management * * * * * * * * * |

30 Credit Quality Net Charge-offs to Average Loans NPAs to Loans & OREO 0.49% 0.39% 0.75% 0.65% 0.60% 0.36% 0.49% 0.54% 0.38% 0.30% 0.40% 0.50% 0.60% 0.70% 0.80% 2002 2003 2004 2005 6/06 CHZ SNL* Credit Reserves/Loans 0.28% 0.16% 0.27% 0.20% 0.05% 0.07% 0.08% 0.33% 0.13% 0.00% 0.15% 0.30% 0.45% 2002 2003 2004 2005 6/06** CHZ SNL* 1.62% 1.54% 1.41% 1.44% 1.29% 1.38% 1.45% 1.38% 1.20% 1.00% 1.20% 1.40% 1.60% 1.80% 2002 2003 2004 2005 6/06 CHZ SNL* *SNL Securities $5-$10 Billion index; data for 6/30/06 not yet available **Net charge-offs to average loans are annualized for all periods |

31 Granularity of Non-Accrual Loans As of 6/30/2006 Book Size of Total Relationship Balance % >$5.0 MM $6,150 25% $3.0 MM to $5.0 MM 0 0% $1.0 MM to $3.0 MM 6,708 28% $500 M to $1.0 MM 1,924 8% $100 M to $500 M 6,279 26% <$100 M 3,26 2 13% Total $24,323 100% |

32 Interest Rate Risk • Naturally Hedged • Static Gap 6 month -11.36% 12 month -8.44% • Net Interest Income Sensitivity * +50 bps -1.00% +25 bps -0.49% -25 bps +0.46% -50 bps +0.74% • Net Income Sensitivity * +50 bps -1.94% +25 bps -0.96% -25 bps +0.89% -50 bps +1.45% *12 month forward ramped estimates as of 6/30/06 Rate Ramp-Net Interest Income -0.49% 0.46% 0.36% 0.42% 0.28% -0.55% -0.72% -0.39% -1.00% -0.50% 0.00% 0.50% 1.00% 2003 2004 2005 6/06 UP 25 BP Qtr DOWN 25 BP Qtr |

33 In Summary * * * * * * |

34 A Compelling Story • Strong market share and a proven acquisition acumen • Low risk balance sheet with a prudent growth strategy • Diversified banking services with a solid balance of revenues • Low exposure to volatile sectors with a fortress balance sheet Annual Equivalent Total Shareholder Return Annual Equivalent 11.72% 8.31% 9.13% 0.00% 10.00% 20.00% 30.00% CHZ S&P 500 Dow Jones Ind Avg 10-Year Period 6.58% 2.49% 3.43% 0% 5% 10% 15% CHZ S&P 500 Dow Jones Ind Avg 5-Year Period |

35 Visit our website for a wide range of products, latest financial reports and many other interactive services: www.chittendencorp.com This presentation contains “forward-looking statements” which may describe future plans and strategic initiatives. These forward- looking statements are based on current plans and expectations, which are subject to a number of factors and uncertainties that could cause future results to differ from historical performance or future expectations. |

36 Appendix * * * * * * * * * |

37 Reconciliation of non-GAAP measurements to GAAP Tangible Ratios �� YTD YTD YTD YTD YTD YTD Dec-02 Dec-03 Dec-04 Dec-05 Jun-05 Jun-06 Net Income (GAAP) $61,602 $72,253 $72,680 $82,039 $38,542 $41,207 Amortization of identified intangibles, net of tax 831 1,786 2,000 1,799 935 864 Tangible Net Income (A) 62,433 74,039 74,680 83,838 39,477 42,071 Average Equity (GAAP) $399,896 $544,522 $599,373 $644,932 $633,468 $666,008 Average Identified Intangibles 9,108 22,493 21,741 19,056 19,784 16,990 Average Deferred Tax on Identified Intangibles (2,280) (5,763) (6,392) (4,785) (5,136) (4,435) Average Goodwill 53,293 187,369 216,519 216,127 216,136 216,038 Average Tangible Equity (B) $339,775 $340,423 $367,505 $414,534 $402,684 $437,415 Return on Average Tangible Equity (A) / (B) 18.37% 21.75% 20.32% 20.22% 19.77% 19.40% Average Assets (GAAP) $4,551,879 $5,777,538 $5,903,400 $6,225,170 $6,110,195 $6,446,587 Average Identified Intangibles 9,108 22,493 21,741 19,056 19,784 16,990 Average Deferred Tax on Identified Intangibles (2,280) (5,763) (6,392) (4,785) (5,136) (4,435) Average Goodwill 53,293 187,369 216,519 216,127 216,136 216,038 Average Tangible Assets (C) $4,491,758 $5,573,439 $5,671,532 $5,994,772 $5,879,411 $6,217,994 Return on Average Tangible Assets (A) / (C) 1.39% 1.33% 1.32% 1.40% 1.35% 1.36% |

38 Reconciliation of non-GAAP measurements to GAAP |