Filed Pursuant to Rule

Registration No. 333-276309

424(b)(3)

Registration No. 333-276309

STEPSTONE PRIVATE CREDIT INCOME FUND PROSPECTUS

May 31, 2024 as supplemented October 11, 2024

Class T Shares

Class S Shares

Class D Shares

Class I Shares

StepStone Private Credit Income Fund (the “Fund”) is a newly formed Delaware statutory trust and is registered under the Investment Company Act of 1940, as amended, as a

non-diversified,

closed-end

management investment company that is operated as an interval fund.Investment Objectives.

Principal Investment Strategies.

non-bank

or corporate lenders (“Investment Partners

Under normal circumstances, the Fund will invest at least 80% of its total assets (net assets plus borrowings for investment purposes) in private credit and income-related investments (“”). The Fund defines Private Credit and Income to consist primarily of the Fund’s Lending Strategy and the Fund’s Specialty Credit Strategy (each as hereinafter defined).

Private Credit and Income

In making an investment decision, an investor must rely upon his, her or its own examination of the Fund and the terms of the offering, including the merits and risks involved, of acquiring shares of the Fund (“Shares”) as described in this prospectus (“Prospectus”). The Shares have not been approved or disapproved by the Securities and Exchange Commission or any other U.S. federal or state governmental agency or regulatory authority or any national securities exchange. No agency, authority or exchange has passed upon the accuracy or adequacy of this Prospectus or the merits of an investment in the Shares. Any representation to the contrary is a criminal offense.

Per Class T Share | Per Class S Share | Per Class D Share | Per Class I Share | Total | ||||||

Public Offering Price | At current net asset value | At current net asset value | At current net asset value | At current net asset value | Unlimited | |||||

Sales Load (1) asa percentage of purchase amount | 3.50% | 3.50% | None | None | Up to 3.5% | |||||

Proceeds to the Fund (2) | Current net asset value minus sales load | Current net asset value minus sales load | Current net asset value | Current net asset value | Unlimited | |||||

| (1) | Generally, the minimum initial investment for Class T Shares, Class S Shares, and Class D Shares in the Fund from each investor is at least $25,000, and the minimum initial investment for Class I Shares in the Fund from each investor is at least $1,000,000. The minimum initial investment may be reduced at the Adviser’s discretion. Investors purchasing Class T Shares or Class S Shares (as defined herein) may be charged a sales load as described above. The table assumes the maximum sales load is charged. |

| (2) | Assumes the maximum sales load is charged. Shares will be offered in a continuous offering at the respective Share’s then-current net asset value, as described herein. The Fund will also bear certain ongoing offering costs associated with the Fund’s continuous offering of Shares. See “Fund Expenses.” |

The Fund is offering an unlimited number of Shares in four separate classes designated as Class T (“Class T Shares”), Class S (“Class S Shares”), Class D (“Class D Shares”) and Class I (“Class I Shares”) on a continuous basis at the then-calculated net asset value (“NAV”) per Share plus any applicable sales loads. Shares are being offered through the distributor at an offering price equal to the Fund’s then-current NAV per Share, plus any applicable sales load. Shares are subject to restrictions on transferability, and liquidity will be provided by periodic repurchase offers for a portion of the Fund’s outstanding Shares. See “Share Repurchase Program.”

TO ALL INVESTORS

No person has been authorized to make any representations concerning the Fund that are inconsistent with those contained in this Prospectus. Prospective investors should not rely on any information not contained in this Prospectus. This Prospectus is intended solely for the use of the person to whom it has been delivered for the purpose of evaluating a possible investment by the recipient in the Shares and is not to be reproduced or distributed to any other persons (other than professional advisors of the prospective investor receiving this document). The Shares are subject to substantial restrictions on transferability and resale and may not be transferred or resold except as permitted under the Securities Act and applicable state securities laws, pursuant to registration or exemption from these provisions.

• | The Fund’s Shares will not be listed on an exchange, and no secondary market is expected to develop. Thus, an investment in the Fund may not be suitable for investors who may need the money they invest in a specified timeframe. |

• | The amount of distributions that the Fund may pay, if any, is uncertain. |

• | The Fund may pay distributions in significant part from sources that may not be available in the future and that are unrelated to the Fund’s performance, such as borrowings. |

• | The Fund’s distributions may be funded from unlimited amounts of offering proceeds or borrowings, which may constitute a return of capital and reduce the amount of capital available to the Fund for investment. Any capital returned to Shareholders through distributions will be distributed after payment of fees and expenses. |

• | A return of capital to Shareholders is a return of a portion of their original investment in the Fund, thereby reducing the tax basis of their investment. As a result of such reduction in tax basis, |

Shareholders may have taxable gains in connection with the sale of Shares, even if such Shares are sold at a loss relative to the Shareholder’s original investment. |

• | An investor in Class T or Class S Shares will pay a sales load of up to 3.50%. If you pay the maximum sales load of 3.50%, you must experience a total return on your net investment of 3.63% in order to recover these expenses. |

• | In the near term, leverage may be used to provide the Fund with temporary liquidity to acquire investments in advance of the Fund’s receipt of proceeds from the realization of other assets or additional sales of Shares. The Fund will also use leverage for investment purposes to generate income. See “Types of Investments and Related Risks — Investment Related Risks — Leverage Utilized by the Fund.” |

The Fund is an interval fund (as defined below) pursuant to which it, subject to applicable law, will conduct quarterly repurchase offers for between 5% and 25% of the Fund’s outstanding Shares. In connection with any given quarterly repurchase offer, the Fund currently intends to repurchase 5% of its outstanding Shares. It is also possible that a repurchase offer may be oversubscribed, with the result that Shareholders may only be able to have a portion of their Shares repurchased. The Fund does not currently intend to list its Shares for trading on any national securities exchange. The Shares are, therefore, not readily marketable. Even though the Fund will make quarterly repurchase offers to repurchase a portion of the Shares to provide liquidity to Shareholders, you should consider the Shares to have limited liquidity. The Fund expects the first repurchase request deadline to occur in September 2024.

Notification of each quarterly repurchase offer is made available to Shareholders at least 21 calendar days before the “Repurchase Request Deadline” (typically March 15, June 15, September 15, or December 15); however, the Fund will provide such written notification earlier but no more than 42 calendar days before the “Repurchase Request Deadline.” The net asset value will be calculated no later than the “Repurchase Pricing Date,” which will be no later than 14 calendar days after the Repurchase Request Deadline, or the next business day if the fourteenth day is not a business day. The Fund will distribute payment to Shareholders within seven calendar days after the Repurchase Pricing Date. See “Share Repurchase Program.”

This Prospectus concisely provides the information that a prospective investor should know about the Fund before investing. You are advised to read this Prospectus carefully and to retain it for future reference. Additional information about the Fund, including a statement of additional information (“SAI”) dated May 31, 2024 as supplemented to date, has been filed with the Securities and Exchange Commission (“SEC”). The SAI and the Fund’s annual and semi-annual reports and other information filed with the SEC are available upon request and without charge by writing to the Fund at c/o StepStone Group Private Wealth LLC, 128 S Tryon St., Suite 1600, Charlotte, NC 28202, by calling (704)

215-4300

or by visiting the Fund’s website, www.stepstonepw.com. The SAI, and other information about the Fund, is also available on the SEC’s website (http://www.sec.gov). The address of the SEC’s Internet site is provided solely for the information of prospective investors and is not intended to be an active link.Shares are not deposits or obligations of, and are not guaranteed or endorsed by, any bank or other insured depository institution, and Shares are not insured by the Federal Deposit Insurance Corporation, the Federal Reserve Board or any other government agency.

You should rely only on the information contained in this Prospectus. The Fund has not authorized anyone to provide you with different information. The Fund is not making an offer of Shares in any state or other jurisdiction where the offer is not permitted.

UMB Distribution Services, LLC

TABLE OF CONTENTS

| 1 | ||||

| 11 | ||||

| 14 | ||||

| 14 | ||||

| 14 | ||||

| 15 | ||||

| 23 | ||||

| 45 | ||||

| 45 | ||||

| 50 | ||||

| 52 | ||||

| 53 | ||||

| 56 | ||||

| 58 | ||||

| 59 | ||||

| 60 | ||||

| 63 | ||||

| 63 | ||||

| 63 | ||||

| 73 | ||||

| 74 | ||||

| 74 | ||||

| 74 | ||||

| 76 | ||||

SUMMARY OF PROSPECTUS

This summary highlights selected information contained elsewhere in this Prospectus and does not contain all of the information that you may want to consider when making your investment decision. To understand this offering fully, you should read the entire Prospectus carefully, including the section entitled “Types of Investments and Related Risks,” before making a decision to invest in our Shares.

StepStone Private Credit Income Fund is a newly formed Delaware statutory trust and is registered under the Investment Company Act of 1940, as amended, as aor “SGEAIL” refer to StepStone Group Europe Alternative Investments Limited; the term “Advisers” refers to StepStone Private Wealth, StepStone Group Private Debt LLC and SGEAIL together; the term “primary offering” refers to this offering of Class T Shares, Class S Shares, Class D Shares, and Class I Shares, when referenced together “Shares” and when all shareholders referenced together “Shareholders;” and the term “Distributor” refers to UMB Distribution Services, LLC.

non-diversified,

closed-end

management investment company that is operated as an interval fund. Unless the context requires otherwise or as otherwise noted, the terms “we,” “us,” “our,” and the “Fund” refer to StepStone Private Credit Income Fund; the terms “Adviser” or “StepStone Private Wealth” refer to StepStone Group Private Wealth LLC; the terms“Sub-Adviser”

or “StepStone Private Debt” refer to StepStone Group Private Debt LLC; the terms“Sub-Sub-Adviser”

| Q: | What is the StepStone Private Credit Income Fund? |

| A: | The Fund’s investment objectives are to seek to generate current income and, to a lesser extent, long-term capital appreciation. |

The Fund intends to primarily use a “multi-lender” approach to achieve its investment objectives, whereby the Advisers utilize a variety of”) to source investment opportunities for the Fund.

non-bank

or corporate lenders (“Investment Partners

Under normal circumstances, the Fund will invest at least 80% of its total assets (net assets plus borrowings for investment purposes) in private credit and income-related investments (“”). The Fund defines Private Credit and Income to consist primarily of the following:

Private Credit and Income

| (1) | direct Loans to U.S. and international private companies that are privately originated and negotiated directly by a non-bank lender (for example, traditional direct lenders include asset management firms (on behalf of their investors), insurance companies, business development companies (“BDCs”) and specialty finance companies) primarily including (a) first lien senior secured and unitranche loans, (b) second lien, unsecured, subordinated or mezzanine loans and structured credit, as well as broadly syndicated loans, club deals (generally investments made by a small group of investment firms), and (c) other Loans; |

| (2) | investments in bank Loans to U.S. and international private companies, including securities representing ownership or participation in a pool of such Loans; |

| (3) | notes or other pass-through obligations representing the right to receive the principal and interest payments on direct Loans to U.S. and international private companies (or fractional portions thereof) (the investments described in clauses (1), (2) and (3) collectively referred to as the “ Lending Strategy |

| (4) | privately offered structured products, such as collateralized loan obligations (“ CLOs |

1

| (5) | privately originated non-corporate lending (including, for example, core and transitionary real estate, structured products and infrastructure-related debt); |

| (6) | other privately originated lending (including, for example, trade and supply chain finance, marketplace lending (consumers, lending to lenders, etc.), insurance-linked strategies and instruments, royalties, aviation financing, shipping, residential whole loan real estate, regulatory capital financing and net asset value lending); and |

| (7) | privately originated non-performing loans (including, for example, US residential mortgage loans and business loans in the EU) (the investments described in clauses (4), (5), (6), and (7) collectively referred to as the “Specialty Credit Strategy |

“,” as used in this Prospectus, refers to loans of any type including, but not limited to, loan promissory notes, secured or unsecured loans,loans, priority or lien loans, assignments, participations or(“”) interest and original issue discount (“”) and, to a lesser extent, the Fund may invest in warrants or other equity securities of borrowers. The Fund may make investments at different levels of a borrower’s capital structure or otherwise in different classes of a borrower’s securities, to the extent permitted by law.

Loans

debtor-in-possession

sub-interests

in loans, syndicated loans, term loans, revolving loans, delayed draw loans or synthetic interests in loans. In connection with a direct Loan, the Fund may receivenon-cash

income features, includingpayment-in-kind

PIK

OID

We may make Private Credit and Income and/or opportunistic investments in asset-backed securities representing ownership or participation in a pool of direct Loans; high yield securities, including securities representing ownership or participation in a pool of such securities; special purpose vehicles (“”) and/or joint ventures that primarily hold loans or credit-like securities;

SPVs

CLO-related

strategies (including equity, warehousing and mezzanine); convertible debt;non-corporate

lending (including, for example and without limitation, core and value add real estate, structured products and infrastructure-related debt); other lending (including, for example, trade and supply chain finance, marketplace lending (consumers, lending to lenders, etc.), insurance-linked strategies and instruments, royalties, aviation financing, shipping, residential whole loan real estate, regulatory capital financing and net asset value lending);non-performing

Loans (including, for example, U.S. residential mortgage loans andnon-U.S.

business loans); and equity of U.S. private companies. The Fund may also opportunistically invest, on a limited basis, in publicly traded securities of large corporate issuers and liquid credit (including, for example, long/short credit (including public securities)).Private Credit and Income investments, along with all other forms of private assets in which the Fund may invest, are broadly referred to as “Private Market Assets.”

The Fund expects to implement a portion of its Lending Strategy and Specialty Credit Strategy via secondary market transactions (“” or “”) where all or a substantial portion of the capital has already been invested and expects to allocate a smaller share of the Fund’s available capital on a primary basis.

Secondary Investments

secondaries

The Fund expects that its allocations between significant segments of its portfolio may vary significantly over time.

For purposes of the Fund’s 80% policy, the Fund will include investments in private investment funds (primarily private funds that are excluded from the definition of “investment company” pursuant to Sections 3(c)(1) or 3(c)(7) of the 1940 Act) that make investments consistent with the Lending Strategy and Specialty Credit Strategy (“”). The Fund’s investments in private funds that are excluded from the definition of “investment company” pursuant to Section

Investment Funds

2

3(c)(1) or 3(c)(7) of the 1940 Act will be limited to no more than 15% of the Fund’s net assets.

While the Fund will be largely invested in U.S. issuers, the Fund may invest in issuers globally without a cap.

We cannot assure you that we will achieve our investment objectives. See “Investment Program — Investment Objectives” and “Types of Investments and Related Risks.”

| Q: | Who is responsible for managing the Fund? |

| A: | StepStone Group Private Wealth LLC (“StepStone Private Wealth” or the “Adviser”), a wholly-owned business of StepStone Group LP (“StepStone Group”), serves as the Adviser of the Fund and will be responsible for the overall management of the Fund’s activities, including structuring, governance, distribution, reporting and oversight. |

StepStone Group Private Debt LLC (“StepStone Private Debt” or the

“Sub-Adviser”)

serves as theSub-Adviser

of the Fund and will provide ongoing research, recommendations and portfolio management regarding the Fund’s investment portfolio. StepStone Private Debt is an investment adviser registered with the SEC under the Investment Advisers Act of 1940, as amended, and is an affiliate of StepStone Group.StepStone Group Europe Alternative Investments Limited (“SGEAIL” orserves as theof the Fund and will provide ongoing research regarding the Fund’s investment portfolio and is an affiliate of StepStone Group.

“Sub-Sub-Adviser”)

Sub-Sub-Adviser

SGEAIL is an investment adviser registered with the SEC under the Investment Advisers Act of 1940, as amended.

As affiliates of StepStone Group, StepStone Private Wealth, StepStone Private Debt, and SGEAIL (together, the “Advisers”) benefit from the organization’s scale and depth across private markets.

StepStone Group is a global private markets investment firm focused on providing customized investment solutions and advisory and data services to its clients. StepStone Group’s clients include some of the world’s largest public and private defined benefit and defined contribution pension funds, sovereign wealth funds and insurance companies, as well as prominent endowments, foundations, family offices and private wealth clients. As of December 31, 2023, StepStone Group was responsible for $659 billion of “private market allocations” which includes $149 billion of assets under management and $510 billion of assets under advisement.

1

StepStone Group has over 980 professionals across 27 cities in 16 countries. StepStone Group LP is not performing investment advisory services to the Fund.StepStone Group Inc. is the sole managing member of StepStone Group Holdings LLC, which in turn is the general partner of StepStone Group LP. In 2020, StepStone Group Inc. listed and began trading on the Nasdaq Global Select Market under the trading symbol STEP. Please see StepStone Group Inc.’s website at www.stepstonegroup.com for more information. See “Management of the Fund – General.”

| Q: | What are the Fund’s areas of differentiation? |

| A: | The Advisers believe the following attributes create an attractive opportunity for investors when considering an investment in the Fund. |

1

“Private market allocations” means the total amount of assets under management and assets under advisement. StepStone Group LP classifies assets under management if the StepStone Group LP has full discretion over the investment decisions in an account or has responsibility or custody of assets. Assets under advisement consists of client assets for which StepStone Group LP does not have full discretion to make investment decisions but plays a role in advising the client or monitoring their investments.3

| • | Proactive Investment Sourcing: Sub-Adviser believes that its advisory practice, separate account investment management mandates and portfolio analytics and reporting capabilities serve as differentiated advantages that will enable the Fund to capitalize on attractive investment opportunities sourced directly from Investment Partners. These advantages include: |

○ | Approximately $10 billion of private credit primary commitments approved in 2022, making StepStone Group what we believe to be one of the top global allocators of primary capital in private credit. |

○ | Access to top-tier investment managers and proprietary opportunities including over 100 private credit Investment Partners. |

○ | Benefits of leveraging a global network that includes offices in 27 cities in 16 countries. |

○ | Large, stable senior team of professionals, each of whom offers their own extensive personal relationship network. |

○ | Ability to remain highly selective in all market environments and to select from the transactions which the Advisers believe provide the best relative value. |

○ | Part of StepStone Group’s broad private markets business that consistently has thousands of third-party sponsor interactions each year, oversees approximately $659 billion of private market assets as of December 31, 2023. |

| • | Deep Knowledge and Expertise in Private Debt: Sub-Adviser utilizes a highly disciplined, research-focused investment approach with a fully scaled, global and dedicated private credit team to provide broad, educated and highly networked coverage of the private credit asset class. TheSub-Adviser believes that its dedicated and broad coverage of the private credit market differentiates StepStone Group from other private market managers, who typically cover private credit through a more generalist approach or with a smaller dedicated footprint. |

○ | Expertise in private credit since 1998. |

○ | Dedicated investment team with over 70 investment professionals focused on private credit investments. |

○ | Over $57 billion of private credit assets under advisement or assets under management. |

○ | Senior team members have an average of 19 years of experience in private debt. |

| • | Information Advantage: |

| • | Multi-Dimensional Due Diligence Approach: Sub-Adviser’s global platform through an investment process that integrates StepStone Group’s analytical and investment expertise, access to proprietary information and insights gained through deep relationships with Investment Partners. The Fund will target opportunities where theSub-Adviser’s evaluation, independent due diligence and broad reference network intersect, and will use its access to a large pool of investment opportunities to make comparisons andseek-out the most attractive opportunities, based on a relative assessment of prospective investments in the market. |

4

| • | Highly Diversified Private Debt Exposure: |

| • | Expanded Access: |

| • | Favorable Structure: K-1s, a single investment instead of recurring capital calls, and potential liquidity in the form of a share repurchase program. |

| Q: | Please describe the Fund’s features that would be considered ‘investor friendly’? |

| A: | Shareholders can access Private Credit and Income through an investment product with terms that we believe are more attractive than historically available investment vehicles providing similar exposure. |

| • | Shareholders will fund their entire investment concurrent with their subscription and avoid the complexity of capital calls. Upon investment, Shareholders immediately gain broad exposure to Private Credit. |

| • | An investment in the Fund will not require Shareholders to file for an extension. Tax information is reported via a 1099-DIV or1099-B for the current year rather than a ScheduleK-1 that is typically provided later in the year, potentially past the April 15th tax deadline. |

| • | Investment minimums as low as $25,000 on initial purchases rather than the higher (in most cases, substantially higher) institutional threshold that would be required for most drawdown funds. |

| • | Liquidity provisions that require the Fund to repurchase Shares of the Fund at the then-calculated NAV on a periodic basis pursuant to a share repurchase program, as discussed below. The Fund may repurchase from 5% to 25% of its outstanding shares quarterly, and the Fund currently intends to repurchase 5% of its outstanding Shares in any quarterly repurchase offer. |

| Q: | Will the Fund invest in the same Private Credit and Income investments as other StepStone Group- advised funds and clients? |

| A: | To the extent permitted by law, the Fund intends to invest alongside other StepStone Group-advised funds and clients in the same assets. The 1940 Act imposes significant limits on the ability of the Fund to co-invest with other StepStone Group-advised funds and clients. The Advisers and the Fund have obtained an exemptive order from the SEC that permits the Fund toco-invest alongside its affiliates. However, the SEC exemptive order contains certain conditions that limit or restrict the Fund’s ability to participate in such transactions, including, without limitation, where StepStone Group advised funds have an existing investment in the operating company or Investment Fund. |

| Q: | What are the Fund’s plans regarding leverage? |

| A: | The Fund intends to use leverage to provide for investment purposes and for temporary liquidity to |

5

| the extent permitted by the 1940 Act. The Fund’s borrowings will always be subject to the Asset Coverage Requirement as defined below. |

The 1940 Act requires a registered investment company to satisfy an asset coverage requirement of 300% of its indebtedness, including amounts borrowed, measured at the time the investment company incurs the indebtedness (the “Asset Coverage Requirement”). This requirement means that the value of the investment company’s total indebtedness may not exceed one third the value of its total assets (including the indebtedness).

In general, the use of leverage may increase the volatility of an investment in the Fund. See “Types of Investments and Related Risks — Investment Related Risks — Leverage Utilized by the Fund.”

| Q: | For whom may an investment in our Shares be appropriate? |

| A: | An investment in Shares of the Fund may be appropriate if investors: |

| • | Desire to obtain the potential benefit of current income and to a lesser extent, long-term capital appreciation. |

| • | Can hold the Shares as a long-term investment and do not need short-term liquidity from the investment. |

We cannot assure you that an investment in our Shares will allow you to realize any of these objectives.

| Q: | What is the purchase price for each Share? |

| A: | Shares will be offered in a continuous offering at the respective Share’s then-current net asset value, as described herein. The initial per Share offering price for Shares will be $10.00 per share. Thereafter, revisions to the share purchase price will be made daily to reflect updated valuations and other Fund activity. See “Calculation of Net Asset Value.” |

| Q: | What is the difference between Class T, Class S, Class D, and Class I Shares? |

| A: | The Fund is offering four classes of Shares to provide investors with more flexibility in making their investment and to provide broker dealers with more flexibility to facilitate investment. |

| • | Class T Shares and Class S Shares are available through brokerage and transaction-based accounts. For Class T Shares and Class S Shares, the minimum initial investment is $25,000 with additional investment minimums of $5,000. The minimum initial and additional investments may be reduced at the Adviser’s discretion. |

| • | Class D Shares are generally available for purchase in this offering only (1) through fee-based programs, also known as wrap accounts, that provide access to Class D Shares, (2) through participating broker-dealers that have alternative fee arrangements with their clients to provide access to Class D Shares, (3) through transaction/brokerage platforms at participating broker-dealers, (4) through certain registered investment advisers, (5) through bank trust departments or any other organization or person authorized to act in a fiduciary capacity for its clients or customers or (6) other categories of investors that we name in an amendment or supplement to this prospectus. For Class D Shares, the minimum initial investment is $25,000 with additional investment minimums of $5,000. The minimum initial and additional investments may be reduced at the Adviser’s discretion. |

| • | Class I Shares are generally available for purchase in this offering only (1) through fee-based programs, also known as wrap accounts, that provide access to Class I Shares, (2) by endowments, foundations, pension funds and other institutional investors, (3) through participating broker-dealers that have alternative fee arrangements with their clients to provide |

6

| access to Class I Shares, (4) through certain registered investment advisers, (5) by the Advisers’ employees, officers and directors and their family members, and joint venture partners, consultants, other service providers, and other similar parties or (6) other categories of investors that we name in an amendment or supplement to this prospectus. For Class I Shares, the minimum initial investment is $1,000,000 with additional investment minimums of $100,000. The minimum initial and additional investments may be reduced at the Adviser’s discretion. |

If you are eligible to purchase all four classes of Shares, then in most cases you should purchase Class I Shares because Class I Shares have no upfront selling commissions or shareholder servicing fees, which will reduce the NAV or distributions of the other Share classes. However, Class I Shares will not receive shareholder services. If you are eligible to purchase Class T Shares, Class S Shares, and Class D Shares but not Class I Shares, in most cases you should purchase Class D Shares because Class D Shares have no upfront selling commission, no dealer fees and lower annual shareholder servicing fees.

See “Plan of Distribution” for a discussion of the differences between our Class T Shares, Class S Shares, Class D Shares, and Class I Shares.

| Q: | What are the fees that investors pay with respect to the Shares they purchase in the offering? |

| A: | There are two types of fees that you will incur: |

| • | First, for Class T Shares and Class S Shares, there are shareholder transaction expenses that are a one-time upfront fee calculated as a percentage of the offering price. Class T Shares and Class S Shares have a maximum selling commission of 3.50%. |

| • | Second, for Class T Shares, Class S Shares, and Class D Shares, there are ongoing distribution and shareholder servicing fees that are calculated as a percentage of NAV. Class T Shares have maximum aggregate annual distribution and shareholder servicing fees of 0.85%. Class S Shares have annual distribution and shareholder servicing fees of 0.85%, and Class D Shares have annual shareholder servicing fees of 0.25%. |

Additional details regarding the fees that investors pay with respect to purchased Shares are discussed in “Summary of Fees and Expenses.”

| Q: | How does the Fund compensate the Advisers for the management of the underlying assets and other administrative requirements associated with the ongoing operation of the Fund? |

| A: | In consideration of the advisory and other services provided by the Adviser to the Fund, the Fund will pay the Adviser a monthly investment management fee (“Management Fee”) equal to 1.15% on an annualized basis of the Fund’s daily net assets. The Management Fee will be accrued daily and payable monthly in arrears within ten (10) business days after the end of the month. The Management Fee is an expense paid out of the Fund’s assets. For the avoidance of doubt, the Management Fee is applied to any assets in respect of Shares that will be repurchased by the Fund on such date. |

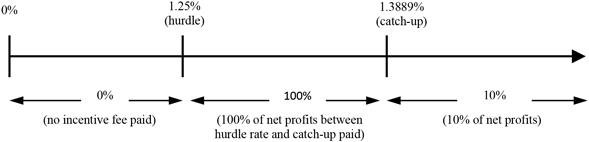

In addition, the Fund will pay the Adviser an income-based incentive fee. The “,” will be accrued daily and payable quarterly in arrears based on the Fund’s “” for the most recently completed calendar quarter. The Incentive Fee will be up to 10% of the Fund’s”), subject to a “” feature (as described below).

Incentive Fee

Pre-Incentive

Fee Net Investment IncomePre-Incentive

Fee Net Investment Income. The payment of the Incentive Fee will be subject to a quarterly hurdle rate, expressed as a rate of return on the value of the Fund’s net assets at the end of the most recently completed calendar quarter, of 1.25% (5.0% annualized) (the “Hurdle Rate

catch up

For this purpose, “” means interest income, dividend income and any other income (including any other fees, such as commitment, origination, structuring, diligence and consulting fees or other fees that the Fund (or its wholly-owned

Pre-Incentive

Fee Net Investment Income7

subsidiaries) receives from portfolio companies) accrued during the calendar quarter, minus the Fund’s operating expenses for the quarter (including the Management Fee, expenses and fees paid to the Adviser under the Administration Agreement and any interest expense and dividends paid on any issued and outstanding preferred stock or credit agreements, but excluding the Incentive Fee and any shareholder servicing and/or distribution fees), net of any expense waivers or expense payments by the Advisor.

Pre-Incentive

Fee Net Investment Income includes, in the case of investments with a deferred interest feature (such as OID debt instruments with PIK interest andzero-coupon

securities), accrued income that the Fund has not yet received in cash.Pre-Incentive

Fee Net Investment Income does not include any realized capital gains, realized capital losses or unrealized appreciation or depreciation.The calculation of the Incentive Fee for each quarter is as follows:

| • | No Incentive Fee will be payable to the Adviser in any calendar quarter in which the Fund’s Pre-Incentive Fee Net Investment Income does not exceed the Hurdle Rate; |

| • | 100% of the dollar amount of the Fund’s Pre-Incentive Fee Net Investment Income, if any, that exceeds the Hurdle Rate but is less than or equal to 1.3889% in any calendar quarter (5.5556% annualized) will be payable to the Adviser. This portion of the Fund’s Incentive Fee that exceeds the Hurdle Rate but is less than or equal to 1.3889% is referred to as the “catch up Pre-Incentive Fee Net Investment Income when the Fund’sPre-Incentive Fee Net Investment Income reaches 1.3889% (5.5556% annualized) on net assets in any calendar quarter; and |

| • | 10% of the dollar amount of the Fund’s Pre-Incentive Fee Net Investment Income, if any, that exceeds 1.3889% (5.5556% annualized) on net assets in any calendar quarter will be payable to the Adviser once the Hurdle Rate andcatch-up have been achieved (10% of the Fund’sPre-Incentive Fee Net Investment Income thereafter will be allocated to the Adviser). |

The Adviser will pay 50% of the Management Fee proceeds and 60% of the Incentive Fee to the

Sub-Adviser

on a monthly and quarterly basis, respectively. See “Management Fee.”| Q: | If I buy Shares, will I receive distributions and how often? |

| A: | The Fund intends to make distributions quarterly in amounts that represent substantially all net investment income and net capital gains earned each year. Additionally, the Fund may make a special distribution annually. All distribution policies will abide by standards required to qualify the Fund as a regulated investment company (“RIC”) under Subchapter M of the Code. The amount of distributions that the Fund may pay, if any, is uncertain. See “Distribution Policy.” |

| Q: | May I reinvest my cash distributions in additional Shares? |

| A: | Yes. We have adopted a dividend reinvestment plan whereby Shareholders may have their cash distributions automatically reinvested in additional Shares unless they elect to receive their distributions in cash. Reinvested distributions for all Shares will be in the respective class of Shares but will not be subject to sales load or other charge for reinvestment. The reinvested Shares will be subject to distribution and/or shareholder servicing fees where applicable. |

The dividend reinvestment plan is discussed later in the document. See “Distribution Policy – Automatic Dividend Reinvestment Plan.”

| Q: | When can Shares be purchased? |

| A: | This is a continuous offering of Shares without a termination date, as permitted by the federal securities laws. Shares are offered for purchase daily on any day the New York Stock Exchange (“NYSE”) is open for business at a price based upon the Fund’s then-current NAV. See “Plan of Distribution.” |

8

| Q: | Can I invest through my IRA, SEP or after-tax deferred account? |

| A: | Yes, you may invest via those vehicles, subject to the suitability standards and applicable law. An approved trustee must process and forward to us subscriptions made through IRAs, Keogh plans, and 401(k) plans. In the case of investments through IRAs, Keogh plans, and 401(k) plans, our transfer agent will send the confirmation and notice of our acceptance to the trustee. Please be aware that in purchasing Shares, custodians or trustees of employee pension benefit plans or IRAs may be subject to the fiduciary duties imposed by ERISA or other applicable laws and to the prohibited transaction rules prescribed by ERISA and related provisions of the Code. In addition, prior to purchasing Shares, the trustee or custodian of an employee pension benefit plan or an IRA should determine that such an investment would be permissible under the governing instruments of such plan or account and applicable law. See “ERISA Considerations.” |

| Q: | What is the tax treatment of the Fund and Fund distributions for U.S. Shareholders? |

| A: | The Fund intends to qualify as a RIC under Subchapter M of the Code. For each taxable year that the Fund so qualifies, the Fund will generally not be subject to U.S. federal income tax on its taxable income and gains that it distributes as dividends for U.S. federal income tax purposes to Shareholders. The Fund intends to distribute its income and gains in a manner that it should not be subject to an entity-level income tax. These distributions generally will be taxable as ordinary income or capital gains to the Shareholders, whether or not they are reinvested in Shares. U.S. federally tax-exempt investors generally will not recognize unrelated business taxable income with respect to an investment in Shares as long as they do not borrow to make such investment. See “Tax Aspects – Distributions.” |

| Q: | What provisions exist for the repurchase, transfer or sale of Shares by Shareholders? |

| A: | The Shares are not a liquid investment. No Shareholder will have the right to require the Fund to repurchase such Shareholder’s Shares or any portion thereof. To provide Shareholders with limited liquidity, the Fund is structured as an interval fund and intends to conduct quarterly offers at NAV to repurchase between 5% and 25% of its outstanding Shares, pursuant to Rule 23c-3 under the 1940 Act, unless such offer is suspended or postponed in accordance with regulatory requirements (as discussed below). In connection with any given quarterly repurchase offer, the Fund currently intends to repurchase 5% of its outstanding Shares. In the event that Shareholders in the aggregate tender for repurchase more than the number of Shares that the Fund will offer to repurchase for a given repurchase offer, the Fund will repurchase the shares on a pro rata basis, which may result in the Fund not honoring the full amount of a required minimum distribution requested by a Shareholder. The Fund expects the first repurchase request deadline to occur in September 2024. |

| Q: | Where can I find additional information on the Fund? |

| A: | Our website, www.stepstonepw.com, is the best source for additional information on the Fund. We regularly post updated information regarding our portfolio and activity in documents such as the most recent Prospectus and Statement of Additional Information, a monthly fact card, an investor presentation, a fund commentary and the portfolio holdings report, along with other news, information and updates. The website also contains a link to our SEC filings. We may change the information posted on the website over time. The information on the website is not incorporated by reference into this Prospectus, and investors should not consider it a part of this Prospectus. |

| Q: | What will I receive in terms of fund reporting? |

| A: | The Adviser will prepare, and make available to Shareholders, an audited annual report and an unaudited semi-annual report within 60 days after the close of the period for which the report is being made, or as otherwise required by the 1940 Act. The Adviser will also make available a report on our operations on at least a quarterly basis. See “Reports to Shareholders” located in the “Statement of Additional Information.” |

9

| Q: | When will I receive my detailed tax information? |

| A: | Shareholders can expect to receive tax information via a 1099-DIV or1099-B by the end of January. |

| Q: | What are the principal risks involved in an investment in the Fund? |

| A: | An investment in the Fund involves several principal risks. Investing in the Shares may be considered speculative and involves a high degree of risk, including the risk of the loss of your investment. The Shares are illiquid and appropriate only as a long-term investment. |

| • | The Fund’s performance depends upon the performance of its assets. |

| • | Underlying investments involve a high degree of business and financial risk, that can result in substantial losses. |

| • | The Fund will allocate a portion of its assets to multiple Investment Funds, and Shareholders will bear two layers of fees and expenses: management fees and administrative expenses at the Fund level, and asset-based management fees, carried interests, incentive allocations or fees and expenses at the Investment Fund level. |

| • | The Fund intends to qualify as a RIC under the Code but may be subject to substantial tax liabilities if it fails to so qualify. |

| • | Although the Fund intends to implement a quarterly share repurchase program, there is no guarantee that an investor will be able to sell all of the Shares that the investor desires to sell. The Fund should therefore be considered to offer limited liquidity. There is no market exchange available for Shares of the Fund, thereby making them difficult to liquidate. |

| • | Possible utilization of leverage, as limited by the requirements of the 1940 Act, may increase the Fund’s volatility. |

Accordingly, the Fund should be considered a speculative investment that entails substantial risks, and a prospective investor should invest in the Fund

only if it can sustain a complete loss of its investment.

10

SUMMARY OF FEES AND EXPENSES

The following table illustrates the fees and expenses that the Fund expects to incur.

To invest in Class T Shares, Class S Shares or Class D Shares of the Fund, a prospective investor generally must maintain or open a brokerage account with a financial institution where a selling agreement has been established (“Selling Agent”). Any costs associated with opening such an account are not reflected in the following table or the Examples below. Investors should contact their broker or other financial professional for more information about the costs associated with opening such an account.

Class T | Class S | Class D | Class I | |||||||||||||

SHAREHOLDER FEES | ||||||||||||||||

Maximum sales load (percentage of purchase amount) (1) | 3.50% | 3.50% | 0.00% | None | ||||||||||||

ANNUAL FUND OPERATING EXPENSES (as a percentage of the Fund’s average net assets) | ||||||||||||||||

| Management Fee | 1.15% | 1.15% | 1.15% | 1.15% | ||||||||||||

Acquired Fund Fees and Expenses (2) | 0.26% | 0.26% | 0.26% | 0.26% | ||||||||||||

Incentive Fee (3) | -- | -- | -- | -- | ||||||||||||

Interest Payments on Borrowed Funds (4) | 2.95% | 2.95% | 2.95% | 2.95% | ||||||||||||

| Distribution and/or Shareholder Servicing Fees | 0.85% | 0.85% | 0.25% | 0.00% | ||||||||||||

Other Expenses (5), (6) | 1.87% | 1.87% | 1.87% | 1.87% | ||||||||||||

Total Annual Fund Operating Expenses | 7.08% | 7.08% | 6.48% | 6.23% | ||||||||||||

Less Expense Limitation and Reimbursement ( 7) | -0.50% | -0.50% | -0.50% | -0.50% | ||||||||||||

Total Annual Net Expenses (8) | 6.58% | 6.58% | 5.98% | 5.73% |

| (1) | Investors purchasing Class T and Class S Shares may be charged a sales load of up to 3.50% of the investment amount. The table assumes the maximum sales load is charged. A Selling Agent may, in its discretion, waive all or a portion of the sales load for certain investors. See “Plan of Distribution.” |

| (2) | The Acquired Fund Fees and Expenses are based on estimated amounts for the Fund’s first 12 months of operations. Some or all of the Investment Funds in which the Fund intends to invest charge carried interests, incentive fees or allocations based on the Investment Funds’ performance. The Investment Funds in which the Fund intends to invest generally charge a management fee of 0.50% to 2.00% based on invested capital, and approximately 0.0% to 20% of net profits as a carried interest allocation. The Acquired Fund Fees and Expenses disclosed above are based on historic returns of the Investment Funds in which the Fund anticipates investing during the first 12 months of operations, which may change substantially over time, therefore, significantly affect Acquired Fund Fees and Expenses. The 0.26% shown as Acquired Fund Fees and Expenses reflects operating expenses of the Investment Funds ( e.g. in-kind, as such fees and allocations for a particular period may be unrelated to the cost of investing in the Investment Funds. |

| (3) | The Fund anticipates that it may have interest income (as well as distributions from underlying funds that are classified as investment income) that could result in the payment of an Incentive Fee to the Adviser during certain periods. However, the Incentive Fee is based on the Fund’s performance and will not be paid unless the Fund achieves certain performance targets. The Fund expects the Incentive Fee the Fund pays to increase to the extent the Fund earns greater interest income through its investments in portfolio companies. The Incentive Fee is calculated and payable quarterly in arrears based upon the Fund’s “pre-incentive fee net investment income” for the most recently completed calendar quarter, and is subject to a hurdle rate, expressed as a rate of return on the Fund’s Net Assets, equal to 1.25% per quarter, or an annualized hurdle rate of 5.00%, subject to a“catch-up” feature. See “Management and Incentive Fees” for a full explanation of how the Incentive Fee is calculated. |

11

| (4) | The Advisers expect to utilize a credit facility in the first twelve months of the Fund’s operations. Expenses may include, but are not limited to, upfront credit facility fees, undrawn fees, and interest payments. |

| (5) | Other Expenses include all other expenses incurred by the Fund, such as its organizational and offering expenses, certain administrative costs, certain origination or similar fees paid with respect to Private Credit and Income investments approved by the Adviser that are sourced by Investment Partners or through Investment Funds, and expenses relating to the offering and sale of Shares. Other Expenses are estimated for the first 12 months of operations. For more details regarding the Fund’s estimated organizational and offering expenses, please see “Fund Expenses – Organizational and Offering Expenses.” |

| (6) | Includes amounts paid under an administration agreement (the “Administration Agreement”) between the Fund and StepStone Private Wealth as administrator (the “Administrator”). Under the Administration Agreement, the Fund pays the Administrator an administration fee (the “Administration Fee”) in an amount up to 0.355% on an annualized basis of the Fund’s net assets. From the proceeds of the Administration Fee, the Administrator pays UMB Fund Services, Inc. (the “Sub-Administrator”) asub-administration fee (the“Sub-Administration Fee”) in an amount up to 0.055% on an annualized basis of the Fund’s net assets, subject to a minimum annual fee. TheSub-Administration Fee is paid pursuant to asub-administration agreement and a fund accounting agreement each between the Administrator and theSub-Administrator. The Administration Fee will be accrued daily based on the value of the net assets of the Fund as of the close of business on each business day (including any assets in respect of shares that will be repurchased by the Fund on such date) and payable in arrears within ten business days after the end of the month. TheSub-Administration Fee is calculated in a manner substantially similar to the Administration Fee and is payable monthly in arrears. |

| (7) | The Adviser has entered into an Expense Limitation and Reimbursement Agreement with the Fund for the one-year term beginning on the commencement of operations for subscriptions for Shares and ending on theone-year anniversary thereof. The Adviser may extend the Limitation Period for a period of one year on an annual basis. The Expense Limitation and Reimbursement Agreement limits the amount of the Fund’s aggregate ordinary operating expenses, excluding certain Specified Expenses listed below, borne by the Fund during the Limitation Period to an amount not to exceed 1.00% for Class T, S, D and I Shares, on an annualized basis, of the Fund’s prior day net assets (“Expense Cap”). “Specified Expenses” that are not covered by the Expense Limitation and Reimbursement Agreement include: (i) the Management Fee; (ii) all fees and expenses of Private Credit and Income investments and other investments in which the Fund invests (including the underlying fees of the Investment Funds and other investments (the Acquired Fund Fees and Expenses)); (iii) the Incentive Fee; (iv) transactional costs, including legal costs and brokerage commissions, and sourcing and servicing or related fees incurred by the Fund in connection with the servicing bynon-affiliated third parties of, and other related administrative services associated with the acquisition and disposition of the Fund’s investments; (v) interest payments incurred on borrowings by the Fund or its subsidiaries; (vi) fees and expenses incurred in connection with any credit facility obtained by the Fund or any of its subsidiaries, including any expenses for acquiring ratings related to the credit facilities; (vii) distribution and shareholder servicing fees, as applicable; (viii) taxes; and (ix) extraordinary expenses resulting from events and transactions that are distinguished by their unusual nature and by the infrequency of their occurrence, including, without limitation, costs incurred in connection with any claim, litigation, arbitration, mediation, government investigation or similar proceeding, indemnification expenses, and expenses in connection with holding and/or soliciting proxies for all annual and other meetings of shareholders. See “Fund Expenses” for additional information. If the Fund’s aggregate ordinary operating expenses, exclusive of the Specified Expenses, in respect of any Class of Shares for any day exceeding the Expense Cap, the Adviser will waive its Management Fee, waive its Incentive Fee, directly pay and/or reimburse the Fund for expenses to the extent necessary to eliminate such excess. The Adviser may also directly pay expenses on behalf of the Fund and waive its Management Fee under the Expense Limitation and Reimbursement Agreement. To the extent that the Adviser waives its Management Fee or Incentive Fee, reimburses expenses to the Fund or pays expenses directly on behalf of the Fund, it is permitted to recoup from the Fund any such amounts for a period not to exceed three years from the month in which such fees and expenses were waived, reimbursed, or paid, even if such recoupment occurs after the termination of the Limitation Period. However, the Adviser may only recoup the waived fees, reimbursed expenses or directly paid expenses in respect of the applicable Class of Shares if (i) the aggregate ordinary operating expenses have fallen to a level below the Expense Cap and (ii) the recouped amount does not raise the level of aggregate ordinary operating expenses plus waived fees, reimbursed expenses or directly paid expenses in respect of a Class of Shares in the month of recoupment to a level that exceeds any Expense Cap applicable at that time. |

12

| (8) | Annual Net Expenses include expenses limited by the Fund’s Expense Limitation and Reimbursement Agreement net of the Expense Cap. |

EXAMPLE:

You would pay the following fees and expenses on a $1,000 investment, assuming a 5.00% annual return, and the Fund’s operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

If You SOLD Your Shares | ||||||||||||||||

1 Year | 3 Year | 5 Year | 10 Year | |||||||||||||

| Class T | $98 | $221 | $340 | $622 | ||||||||||||

| Class S | $98 | $221 | $340 | $622 | ||||||||||||

| Class D | $60 | $177 | $292 | $570 | ||||||||||||

| Class I | $57 | $170 | $281 | $553 | ||||||||||||

If You HELD Your Shares | ||||||||||||||||

1 Year | 3 Year | 5 Year | 10 Year | |||||||||||||

| Class T | $98 | $221 | $340 | $622 | ||||||||||||

| Class S | $98 | $221 | $340 | $622 | ||||||||||||

| Class D | $60 | $177 | $292 | $570 | ||||||||||||

| Class I | $57 | $170 | $281 | $553 | ||||||||||||

The examples should not be considered a representation of future expenses, and actual expenses may be greater or less than those shown

The purpose of the table above is to assist investors in understanding the various fees and expenses Shareholders will bear directly or indirectly. For a more complete description of the various fees and expenses of the Fund, see “Fund Expenses,” “Management Fee” and “Purchases of Shares.”

13

THE FUND

The Fund is registered under the 1940 Act as a

non-diversified,

closed-end

management investment company. The Fund is structured as an interval fund and continuously offers its Shares. The Fund was organized as a Delaware statutory trust on December 18, 2023. The Fund’s principal office is located at 128 S Tryon St., Suite 1600, Charlotte, NC 28202, and its telephone number is (704)215-4300.

Investment advisory services are provided to the Fund by the Adviser andSub-Adviser

pursuant to an investment advisory agreement (the “Advisory Agreement”) and an investmentsub-advisory

agreement (the“Sub-Advisory

Agreement”), respectively. Responsibility for monitoring and overseeing the Fund’s investment program and its management and operation is vested in the individuals who serve on the Board of Trustees. See “Statement of Additional Information – Management of the Fund.”USE OF PROCEEDS

Under normal circumstances, the proceeds from the sale of Shares, net of the Fund’s fees and expenses, are invested by the Fund to pursue its investment program and objectives as soon as practicable. It is anticipated that proceeds from the sale of Shares will be invested, as appropriate, in investment opportunities within three months; however, changes in market conditions could result in the Fund’s anticipated investment period extending as long as six months. See “Other Risks — Availability of Investment Opportunities” for a discussion of the timing of Investment Funds’ subscription activities, market conditions, and other considerations relevant to the timing of the Fund’s investments generally.

The Fund will pay the Adviser the full amount of the Management Fee during any period prior to which less than 80% of the Fund’s assets (including any proceeds received by the Fund from the offering of Shares) are invested in Private Credit and Income investments.

STRUCTURE

The Fund has been organized as a continuously offered,

non-diversified

closed-end

management investment company that is operated as an interval fund.Closed-end

funds differ fromopen-end

funds (commonly known as mutual funds) in that investors inclosed-end

funds do not have the right to redeem their shares on a daily basis. Unlike mostclosed-end

funds, which typically list their shares on a securities exchange, the Fund does not currently intend to list the Shares for trading on any securities exchange, and the Fund does not expect any secondary market to develop for the Shares in the foreseeable future. Therefore, an investment in the Fund, unlike an investment in a typicalclosed-end

fund, is not a liquid investment. To provide some liquidity to Shareholders, the Fund is structured as an interval fund and conducts quarterly repurchase offers for a limited amount of the Fund’s Shares(5%-25%).

The Fund believes that a

closed-end

structure is most appropriate for the long-term nature of the Fund’s strategy. The Fund’s NAV per Share may be volatile. As the Shares are not traded, investors will not be able to dispose of their investment in the Fund, except through repurchases conducted through the share repurchase program, no matter how the Fund performs.The Fund is a specialized investment vehicle that provides investors within the structure of a registeredindividuals. Compared to private investment funds, registered

closed-end

investment company with exposure to private credit investments that typically are made by investment funds not registered under the 1940 Act, often referred to as a “private investment fund.” Private investment funds are collective asset pools that typically offer their securities privately, without registering such securities under the Securities Act. The Advisers believe that securities offered by private investment funds are typically sold in large minimum denominations (often at least $5,000,000 to $20,000,000) to a limited number of institutional investors andhigh-net-worth

closed-end

investment companies often impose relatively modest minimum investment requirements and offer their shares to a broader range of investors.Investors may purchase Shares of the Fund daily based upon the Fund’s daily NAV per Share. Unlike the practices of many private investment funds, the Fund intends to offer Shares without limiting the number of eligible investors that can participate in its investment program.

In private investment funds, often organized as limited partnerships, investors usually commit to provide up to a certain amount of capital as and when requested by the fund’s manager or general partner. The general partner then makes private market investments on behalf of the fund, typically over aperiod according to a

two-to-five-year

14

pre-defined

investment strategy. The Fund’s Private Credit and Income investments typically have afive-to-seven

closed-end

funds typically reinvest most of the proceeds of realized investments and do not have a stated duration. This attribute provides investors with more consistent exposure to the underlying assets through economic cycles and maintains an investor’s intended allocation to the target asset class, such as private markets.INVESTMENT PROGRAM

Investment Objectives

The Fund’s investment objectives are to seek to generate current income and, to a lesser extent, long-term capital appreciation.

Investment Strategy

Under normal circumstances, the Fund will invest at least 80% of its total assets (net assets plus borrowings for investment purposes) in Private Credit and Income Investments, primarily through its Lending Strategy and Specialty Credit Strategy, each as discussed below. Except as otherwise disclosed in this Prospectus, we may modify or waive our investment objectives and any of our investment policies, restrictions, strategies, and techniques without prior notice and without shareholder approval. If we change our 80% Private Credit and Income policy, we will provide shareholders with at least 60 days’ advance notice of such change.

Under the Fund’s 80% policy, the Fund is not limited in relation to the investment strategies to which it has exposure, provided such investment strategies are substantially credit-related. The Fund may undertake a variety of investment strategies in connection with its Lending Strategy and Specialty Credit Strategy, as discussed further below.

The Fund intends to primarily use a “multi-lender” approach to achieve its investment objectives, whereby the Advisers utilize a variety of Investment Partners to source investment opportunities for the Fund. There can be no assurance that the Fund will achieve its investment objectives.

With respect to Private Credit and Income investments approved by the Adviser that are sourced by Investment Partners or through Investment Funds, the Fund may be required to pay an origination or similar fee in connection with making such investment, as well as any ongoing fees for administrative services provided by the Investment Partners to the Fund with respect to such investments, which fees will be directly borne by the Fund’s shareholders and are in addition to the fees charged to the Investment Funds by their managers or general partner.

The Fund will use data and analysis throughout all stages of the investment process, including in the sourcing, underwriting, and monitoring stages. The Fund will use various data sources throughout the process, including the institutional expertise of StepStone private debt and private equity teams, StepStone’s access to a network of private debt general partners, sponsors, and industry experts, and access to databases containing credit-specific data.

The Loans in which we expect to invest may pay floating interest rates based on a variable base rate. The secured debt (including first lien senior secured, unitranche and second lien debt) in which we will invest generally have stated terms of five to eight years, and the mezzanine, unsecured or subordinated debt investments that we may make will generally have stated terms of up to ten years, but the expected average life of such securities is generally between three and five years. However, there is no limit on the maturity or duration of any security we may hold in our portfolio. Loans and securities purchased in the secondary market will generally have shorter remaining terms to maturity than newly issued investments. We expect most of our debt investments will be unrated. Our debt investments may also be rated by a nationally recognized statistical rating organization, and, in such case, generally will carry a rating below investment grade (rated lower than “Baa3” by Moody’s Investors Service, Inc. or lower than

“BBB-”

by Standard & Poor’s Ratings Services). These types of loans are often called “junk” bonds. We expect that our unrated debt investments will generally have credit quality consistent with below investment grade securities.In connection with a direct Loan, the Fund may receive

non-cash

income features, including PIK interest and OID and, to a lesser extent, the Fund may invest in warrants or other equity securities of borrowers. The Fund may make investments at different levels of a borrower’s capital structure or otherwise in different classes of a borrower’s15

securities, to the extent permitted by law.

The Advisers will allocate the Fund’s assets in such proportions as the Advisers deem appropriate from time to time, in accordance with the Advisers’ allocation policy. The Fund may invest in U.S., European and other

non-U.S.

companies, including to a limited extent companies in emerging markets.We are classified as a

non-diversified

investment Fund within the meaning of the 1940 Act, which means that we are not limited by the 1940 Act with respect to the proportion of our assets that we may invest in securities of a single issuer. Under the 1940 Act, a “diversified” investment Fund is required to invest at least 75% of the value of its total assets in cash and cash items, government securities, securities of other investment companies and other securities limited in respect of any one issuer to an amount not greater than 5% of the value of the total assets of such Fund and no more than 10% of the outstanding voting securities of such issuer. As anon-diversified

investment Fund, we are not subject to this requirement. To the extent that we assume large positions in the securities of a small number of issuers or within a particular industry, our NAV may fluctuate to a greater extent than that of a more diversified investment Fund as a result of changes in the financial condition or the market’s assessment of the issuer. We may also be more susceptible to any single economic or regulatory occurrence than a diversified investment Fund or to a general downturn in the economy. However, we are subject to the diversification requirements applicable to a regulated investment company (“RIC”) under Subchapter M of the Code.Notwithstanding the above, the Advisers do not follow a rigid investment policy with respect to the Fund’s investment portfolio that would restrict it from participating in any market, strategy or investment, and the Fund’s investment portfolio may be concentrated in one or more investment strategies from time to time. The Fund’s assets may be deployed in whatever investment strategies are deemed appropriate under prevailing economic and market conditions to seek to achieve the Fund’s investment objectives.

Lending Strategy

To effectuate the Fund’s Lending Strategy, the Advisers intend to utilize a variety of Investment Partners to source Private Credit and Income investments primarily consisting of the following:

| (1) | direct Loans to U.S. and international private companies that are privately originated and negotiated directly by a non-bank lender (for example, traditional direct lenders include asset management firms (on behalf of their investors), insurance companies, BDCs and specialty finance companies) primarily including (a) first lien senior secured and unitranche loans, (b) second lien, unsecured, subordinated or mezzanine loans and structured credit, as well as broadly syndicated loans, club deals (generally investments made by a small group of investment firms), and (c) other Loans, |

| (2) | investments in bank Loans to U.S. and international private companies, including securities representing ownership or participation in a pool of such Loans, and |

| (3) | notes or other pass-through obligations representing the right to receive the principal and interest payments on direct Loans to U.S. and international private companies (or fractional portions thereof). |

Specialty Credit Strategy

To effectuate the Fund’s Specialty Credit Strategy, the Advisers intend to utilize a variety of Investment Partners to source Private Credit and Income investments primarily consisting of the following:

| (1) | Privately offered structured products, such as collateralized loan obligations (“CLOs”) |

| (2) | Privately originated on-corporate lending (including, for example, core and transitionary real estate, structured products and infrastructure-related debt); |

| (3) | Other privately originated lending (including, for example, trade and supply chain finance, marketplace lending (consumers, lending to lenders, etc.), insurance-linked strategies and instruments, royalties, aviation financing, shipping, residential whole loan real estate, |

16

| regulatory capital financing and net asset value lending); and |

| (4) | Privately originated non-performing loans (including, for example, US residential mortgage loans and business loans in the EU). |

In addition to utilizing Investment Partners to source investments for its Lending Strategy and Specialty Credit Strategy, the Fund may originate loans and debt instruments, and may also have the ability to acquire investments through secondary transactions, including through loan portfolios, receivables, contractual obligations to purchase subsequently originated loans and other debt instruments. The Advisers may also invest the Fund’s assets in Loans acquired from Investment Funds managed by

non-affiliated

third-party managers in which the Fund is not invested. With respect to investments approved by the Advisers that are sourced by Investment Partners or through Investment Funds, the Fund may be required to pay an origination or similar fee in connection with making such investment, which fees will be indirectly borne by the Fund’s shareholders and are in addition to the fees charged to the Investment Funds by their managers or general partners. The Fund also expects to allocate a smaller share of the Fund’s available capital to “primary” transactions.For purposes of the Fund’s 80% policy, the Fund will include investments in private investment funds (primarily private funds that are excluded from the definition of “investment company” pursuant to Sections 3(c)(1) or 3(c)(7) of the 1940 Act) that make investments consistent with the Lending Strategy and Specialty Credit Strategy (“Investment Funds”). The Fund’s investments in private funds that are excluded from the definition of “investment company” pursuant to Section 3(c)(1) or 3(c)(7) of the 1940 Act will be limited to no more than 15% of the Fund’s net assets.

With respect to individual companies, the Advisers believe that the increased time to liquidity of many private companies can provide a significant source of investment opportunity. As a result, Fund management teams, in some cases, pursue secondary offerings to expedite liquidity. The Advisers believe their networks and value-added approach will provide a strong pipeline of opportunities, and their versatile financing approach gives the team the flexibility to source high quality opportunities.

The Fund may undertake a variety of investment strategies including, without limitation: in asset-backed securities representing ownership or participation in a pool of direct Loans; high yield securities, including securities representing ownership or participation in a pool of such securities; special purpose vehicles (“”) and/or joint ventures that primarily hold loans or credit-like securities;

SPVs

CLO-related

strategies (including equity, warehousing and mezzanine); convertible debt;non-corporate

lending (including, for example and without limitation, core and value add real estate, structured products and infrastructure-related debt); other lending (including, for example, trade and supply chain finance, marketplace lending (consumers, lending to lenders, etc.), insurance-linked strategies and instruments, royalties, aviation financing, shipping, residential whole loan real estate, regulatory capital financing and net asset value lending);non-performing

Loans (including, for example, U.S. residential mortgage loans andnon-U.S.

business loans); and equity of U.S. private companies.The Fund may also opportunistically invest, on a limited basis, in publicly traded securities of large corporate issuers and liquid credit (including, for example, long/short credit (including public securities) and

non-control

distressed strategies).Investment Process

The Adviser and the

Sub-Adviser

intend to adhere to a disciplined, focused investment screening and selection process with an emphasis on fundamental analysis and due diligence in connection with investing the Fund’s assets. The Advisers will also retain, in certain situations, external consultants, advisors and accountants to augment due diligence. The Advisers’ approach of working closely with lenders and issuers on transactions is expected to allow for a thorough due diligence process as well as providing the Advisers with the requisite time to complete each step in its screening, due diligence and monitoring process for the Fund, which will typically include the below steps in connection with the Fund’s Lending Strategy.The Adviser’s Investment Committee

17

The Adviser carries out portfolio management through its Investment Committee (the “Investment Committee”). The Investment Committee comprises senior personnel of the StepStone Group. The committee functions include the consideration, and if appropriate, approval of proposed investments based on investment memorandum prepared by the investment teams within the Advisers, decisions on allocations to eligible funds, ongoing monitoring of the investments and incidents, among other matters.

The Investment Committee review process is multi-step and iterative and occurs in parallel with the diligence of investments. Once the diligence process has begun, the investment team presents updates at twice-weekly Investment Committee meetings. The Investment Committee reviews all activity from the prior week, with a focus on detailed updates of ongoing situations and

in-depth

review of all new investment opportunities.The ultimate results and findings of the investment analysis are compiled into an investment memorandum that is used as the basis to support the investment thesis and utilized by the Investment Committee for final investment review and approval.

The Investment Process Steps

The Adviser’s investment process for an investment opportunity spans one to two months, from the initial screen through final approval and funding. The process begins with the work of the investment team. The investment team are investment professionals in StepStone Group to whom the Adviser has access by virtue of a resource sharing agreement.

Sourcing and Initial Review

In order to source transactions, the Adviser primarily utilizes its significant access to transaction flow through more than 100 different

co-investment

relationships with Investment Partners. With respect to StepStone’s origination channels, the global presence of StepStone generates access to a substantial amount of opportunities with attractive investment characteristics. The broad network of Investment Partners includes private credit asset managers, origination platforms, private equity asset managers, financial intermediaries, and other parties.The investment team examines information furnished by the Investment Partner and, as applicable, the target company and external sources. The investment team determines whether the investment meets the Fund’s basic investment criteria and offers an acceptable probability of attractive risk adjusted returns.

Only the most attractive opportunities are pursued further, meaning that many opportunities are declined by the investment team at this stage with respective communication to the Investment Partner. For opportunities that proceed to the next stage, a list of initial due diligence questions and a request for additional diligence materials are prepared.

Evaluation and Further Review

The investment team reviews additional diligence materials to answer initial due diligence questions identified in the Initial Review.

Due Diligence

Once the diligence process has begun, the investment team presents updates at twice-weekly Investment Committee meetings. The Investment Committee conducts a thorough and rigorous review of the opportunity with the investment team to ensure the potential investment fits the Fund’s investment strategy. The investment team may examine some or all of the following deal attributes, along with other factors:

| • | transaction dynamics such as deal rationale, use of proceeds, co-investment rationale; |

18

| • | borrower credit profile including credit metrics, size of the borrower, resiliency of business model, market position, industry fundamentals, and relative value assessment; |

| • | historical financial performance; including asset valuation, financial analysis, scenario analysis, future projections, growth assumptions, free cash flow generation, de-leveraging profile, other key financial credit metrics, and comparable credit and equity analyses; |

| • | legal considerations including the strength of the credit structure and related documentation; |

| • | performance track record of the Investment Partner who sourced the opportunity; |

| • | performance track record and experience of the private equity sponsor; |

| • | analysis of the structure and leverage of the transaction; and |

| • | analysis on how the particular investment fits into the overall investment strategy of the Fund. |