| | | FREE WRITING PROSPECTUS |

| | | FILED PURSUANT TO RULE 433 |

| | | REGISTRATION FILE NO.: 333-255934-11 |

| | | |

| Dated March 7, 2024 | BMO 2024-C8 |

| Structural and Collateral Term Sheet |

BMO 2024-C8 Mortgage Trust |

$683,436,933 (Approximate Mortgage Pool Balance) |

| |

$[ ] (Approximate Offered Certificates) |

| |

BMO Commercial Mortgage Securities LLC Depositor |

| |

Commercial Mortgage Pass-Through Certificates, SERIES 2024-C8 |

| |

|

Bank of Montreal Citi Real Estate Funding Inc. German American Capital Corporation Starwood Mortgage Capital LLC National Cooperative Bank, N.A. Goldman Sachs Mortgage Company Ladder Capital Finance LLC Morgan Stanley Mortgage Capital Holdings LLC Zions Bancorporation, N.A. LMF Commercial, LLC UBS AG BSPRT CMBS Finance, LLC Sponsors and Mortgage Loan Sellers |

BMO

Capital

Markets | Deutsche Bank Securities | Goldman Sachs & Co. LLC | Morgan

Stanley | UBS

Securities

LLC | Citigroup |

| Co-Lead Managers and Joint Bookrunners |

Academy Securities

Co-Manager | Bancroft Capital, LLC

Co-Manager | Drexel Hamilton

Co-Manager |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| Dated March 7, 2024 | BMO 2024-C8 |

This material is for your information, and none of BMO Capital Markets Corp., Citigroup Global Markets Inc., Deutsche Bank Securities Inc., Goldman Sachs & Co. LLC, Morgan Stanley & Co. LLC, UBS Securities LLC, Academy Securities, Inc., Bancroft Capital, LLC and Drexel Hamilton, LLC (collectively, the “Underwriters”) are soliciting any action based upon it. This material is not to be construed as an offer to sell or the solicitation of any offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal.

The depositor has filed a registration statement (including the prospectus) with the Securities and Exchange Commission (File No. 333-255934) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the Securities and Exchange Commission for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, the depositor or BMO Capital Markets Corp., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling 1-866-864-7760. The Offered Certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more Classes of Certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these Certificates, a contract of sale will come into being no sooner than the date on which the relevant Class has been priced and we have verified the allocation of Certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us.

Neither this document nor anything contained in this document shall form the basis for any contract or commitment whatsoever. The information contained in this document is preliminary as of the date of this document, supersedes any previous such information delivered to you and will be superseded by any such information subsequently delivered prior to the time of sale. These materials are subject to change, completion or amendment from time to time. The information should be reviewed only in conjunction with the entire offering document relating to the Commercial Mortgage Pass-Through Certificates, Series 2024-C8 (the “Offering Document”). All of the information contained herein is subject to the same limitations and qualifications contained in the Offering Document. The information contained herein does not contain all relevant information relating to the underlying mortgage loans or mortgaged properties. Such information is described elsewhere in the Offering Document. The information contained herein will be more fully described elsewhere in the Offering Document. The information contained herein should not be viewed as projections, forecasts, predictions or opinions with respect to value. Prior to making any investment decision, prospective investors are strongly urged to read the Offering Document its entirety. Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this free writing prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This document has been prepared by the Underwriters for information purposes only and does not constitute, in whole or in part, a prospectus for the purposes of Regulation (EU) 2017/1129 (as amended or superseded) and/or Part VI of the Financial Services and Markets Act 2000 (as amended) or other offering document.

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) which have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the Computational Materials’ accuracy, appropriateness or completeness in any particular context; or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of these Certificates. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the Certificates may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of the Underwriters or any of their respective affiliates make any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the Certificates. The information in this presentation is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Mortgage Loan Sellers or which was otherwise reviewed by us.

This document contains forward-looking statements. If and when included in this document, the words “expects”, “intends”, “anticipates”, “estimates” and analogous expressions and all statements that are not historical facts, including statements about our beliefs or expectations, are intended to identify forward-looking statements. Any forward-looking statements are made subject to risks and uncertainties which could cause actual results to differ materially from those stated. Those risks and uncertainties include, among other things, declines in general economic and business conditions, increased competition, changes in demographics, changes in political and social conditions, regulatory initiatives and changes in consumer preferences, many of which are beyond our control and the control of any other person or entity related to this offering. The forward-looking statements made in this document are made as of the date hereof. We have no obligation to update or revise any forward-looking statement.

BMO Capital Markets is a trade name used by BMO Financial Group for the wholesale banking businesses of Bank of Montreal, BMO Harris Bank N.A. (member FDIC), Bank of Montreal Europe p.l.c, and Bank of Montreal (China) Co. Ltd, the institutional broker dealer business of BMO Capital Markets Corp. (Member FINRA and SIPC) and the agency broker dealer business of Clearpool Execution Services, LLC (Member FINRA and SIPC) in the U.S., and the institutional broker dealer businesses of BMO Nesbitt Burns Inc. (Member Investment Industry Regulatory Organization of Canada and Member Canadian Investor Protection Fund) in Canada and Asia, Bank of Montreal Europe p.l.c. (authorized and regulated by the Central Bank of Ireland) in Europe and BMO Capital Markets Limited (authorized and regulated by the Financial Conduct Authority) in the UK and Australia.

Securities and investment banking activities in the United States are performed by Deutsche Bank Securities Inc., a member of NYSE, FINRA and SIPC, and its broker-dealer affiliates. Lending and other commercial banking activities in the United States are performed by Deutsche Bank AG and its banking affiliates.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 2 | |

| Dated March 7, 2024 | BMO 2024-C8 |

IMPORTANT NOTICE RELATING TO AUTOMATICALLY-GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of any email communication to which this document is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) no representation that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

THE CERTIFICATES REFERRED TO IN THESE MATERIALS ARE SUBJECT TO MODIFICATION OR REVISION (INCLUDING THE POSSIBILITY THAT ONE OR MORE CLASSES OF CERTIFICATES MAY BE SPLIT, COMBINED OR ELIMINATED AT ANY TIME PRIOR TO ISSUANCE OR AVAILABILITY OF A FINAL PROSPECTUS) AND ARE OFFERED ON A “WHEN, AS AND IF ISSUED” BASIS.

THE UNDERWRITERS MAY FROM TIME TO TIME PERFORM INVESTMENT BANKING SERVICES FOR, OR SOLICIT INVESTMENT BANKING BUSINESS FROM, ANY COMPANY NAMED IN THESE MATERIALS. THE UNDERWRITERS AND/OR THEIR AFFILIATES OR RESPECTIVE EMPLOYEES MAY FROM TIME TO TIME HAVE A LONG OR SHORT POSITION IN ANY CERTIFICATE OR CONTRACT DISCUSSED IN THESE MATERIALS.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 3 | |

| Structural and Collateral Term Sheet | | BMO 2024-C8 |

| Collateral Characteristics |

Mortgage Loan Seller | Number of Mortgage Loans | Number of Mortgaged Properties | Aggregate

Cut-off Date Balance | | Roll-up Aggregate Cut-off Date Balance | Roll-up Aggregate % of Cut-off Date Balance |

| CREFI | 3 | 4 | $118,462,500 | 17.3% | $118,462,500 | 17.3% |

| GACC | 3 | 10 | $118,410,000 | 17.3% | $118,410,000 | 17.3% |

| BMO | 5 | 9 | $52,850,000 | 7.7% | $95,850,000 | 14.0% |

| SMC | 1 | 1 | $65,000,000 | 9.5% | $65,000,000 | 9.5% |

| NCB | 24 | 24 | $58,450,003 | 8.6% | $58,450,003 | 8.6% |

| GSMC | - | - | - | - | $50,000,000 | 7.3% |

| LCF | 5 | 5 | $40,400,000 | 5.9% | $40,400,000 | 5.9% |

| MSMCH | - | - | - | - | $40,000,000 | 5.9% |

| ZBNA | 2 | 2 | $38,496,280 | 5.6% | $38,496,280 | 5.6% |

| LMF | 2 | 2 | $27,425,000 | 4.0% | $27,425,000 | 4.0% |

| UBS AG | 3 | 4 | $20,043,150 | 2.9% | $20,043,150 | 2.9% |

| BSPRT | 2 | 2 | $10,900,000 | 1.6% | $10,900,000 | 1.6% |

| GSMC, BMO | 1 | 1 | $68,000,000 | 9.9% | - | - |

| MSMCH, BMO | 1 | 1 | $65,000,000 | 9.5% | - | - |

| Total: | 52 | 65 | $683,436,933 | 100.0% | $683,436,933 | 100.0% |

| Loan Pool | |

| | Initial Pool Balance (“IPB”): | $683,436,933 |

| | Number of Mortgage Loans: | 52 |

| | Number of Mortgaged Properties: | 65 |

| | Average Cut-off Date Balance per Mortgage Loan: | $13,143,018 |

| | Weighted Average Current Mortgage Rate: | 6.83843% |

| | 10 Largest Mortgage Loans as % of IPB: | 68.7% |

| | Weighted Average Remaining Term to Maturity: | 116 months |

| | Weighted Average Seasoning: | 2 months |

| | | |

| Credit Statistics | |

| | Weighted Average UW NCF DSCR: | 2.46x |

| | Weighted Average UW NOI Debt Yield: | 18.1% |

| | Weighted Average Cut-off Date Loan-to-Value Ratio (“LTV”): | 47.6% |

| | Weighted Average Maturity Date/ARD LTV: | 47.3% |

| | | |

| Other Statistics | |

| | % of Mortgage Loans with Additional Debt: | 8.7% |

| | % of Mortgage Loans with Single Tenants(1): | 24.4% |

| | % of Mortgage Loans secured by Multiple Properties: | 16.6% |

| | |

| Amortization | |

| | Weighted Average Original Amortization Term: | 369 months |

| | Weighted Average Remaining Amortization Term: | 368 months |

| | % of Mortgage Loans with Interest-Only: | 72.6% |

| | % of Mortgage Loans with Partial Interest-Only followed by Amortizing Balloon: | 11.7% |

| | % of Mortgage Loans with Amortizing Balloon: | 9.6% |

| | % of Mortgage Loans with Interest-Only with Anticipated Repayment Date: | 5.9% |

| | % of Mortgage Loans with Fully Amortizing: | 0.2% |

| | | |

| Lockboxes | |

| | % of Mortgage Loans with Hard Lockboxes: | 56.7% |

| | % of Mortgage Loans with Springing Lockboxes: | 23.4% |

| | % of Mortgage Loans with Soft Lockboxes: | 11.3% |

| | % of Mortgage Loans with No Lockbox: | 8.6% |

| | | |

| Reserves | |

| | % of Mortgage Loans Requiring Monthly Tax Reserves: | 54.5% |

| | % of Mortgage Loans Requiring Monthly Insurance Reserves: | 25.1% |

| | % of Mortgage Loans Requiring Monthly CapEx Reserves: | 27.4% |

| | % of Mortgage Loans Requiring Monthly TI/LC Reserves(2): | 24.0% |

(1) Excludes mortgage loans that are secured by multiple properties with multiple tenants.

(2) Calculated only with respect to the Cut-off Date Balance of mortgage loans secured or partially secured by office, industrial, retail, Hospitality (with commercial tenants) and mixed use properties.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 4 | |

| Structural and Collateral Term Sheet | | BMO 2024-C8 |

| Collateral Characteristics |

| Ten Largest Mortgage Loans |

| No. | Loan Name | City, State | Mortgage Loan Seller | No.

of Prop. | Cut-off Date Balance | % of IPB | Square Feet / Rooms / Units | Property Type | UW

NCF DSCR | UW NOI Debt Yield | Cut-off Date LTV | Maturity Date/ARD LTV |

| 1 | Danbury Fair Mall | Danbury, CT | GSMC, BMO | 1 | $68,000,000 | 9.9% | 923,598 | Retail | 2.52x | 19.4% | 41.8% | 40.9% |

| 2 | 60 Hudson | New York, NY | MSMCH, BMO | 1 | $65,000,000 | 9.5% | 1,149,619 | Other | 3.92x | 24.2% | 17.5% | 17.5% |

| 3 | Fayette Pavilion | Fayetteville, GA | SMC | 1 | $65,000,000 | 9.5% | 1,063,840 | Retail | 1.60x | 11.3% | 64.4% | 64.4% |

| 4 | Tekni-Plex Industrial Portfolio | Various, Various | GACC | 8 | $58,410,000 | 8.5% | 1,138,969 | Industrial | 2.07x | 14.4% | 55.6% | 55.6% |

| 5 | Axis Apartments | Chicago, IL | CREFI | 1 | $58,000,000 | 8.5% | 716 | Multifamily | 1.37x | 9.8% | 53.0% | 53.0% |

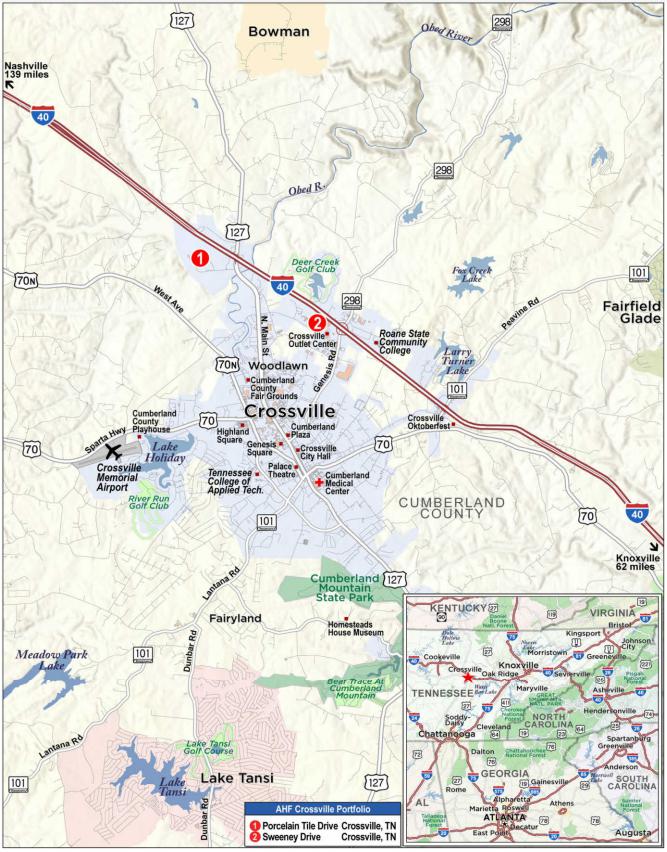

| 6 | AHF Crossville Portfolio | Crossville, TN | CREFI | 2 | $37,300,000 | 5.5% | 949,281 | Industrial | 1.67x | 12.7% | 60.2% | 60.2% |

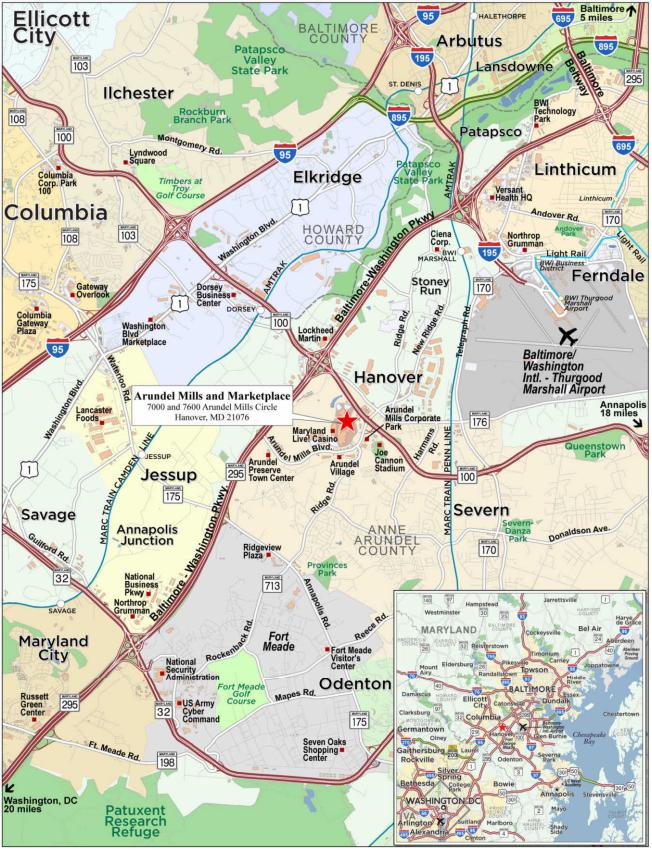

| 7 | Arundel Mills and Marketplace | Hanover, MD | GACC | 1 | $35,000,000 | 5.1% | 1,938,983 | Retail | 1.98x | 16.1% | 41.4% | 41.4% |

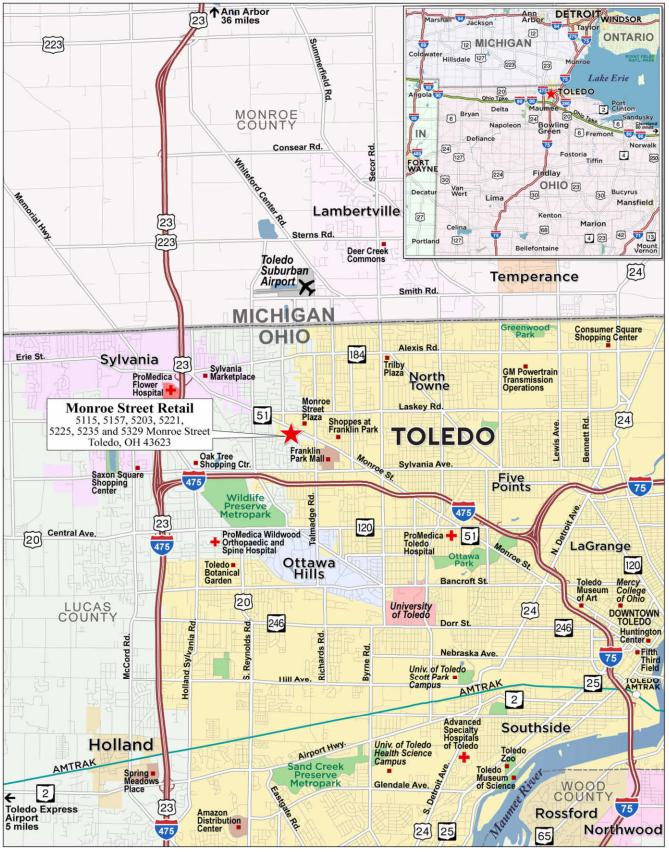

| 8 | Monroe Street Retail | Toledo, OH | ZBNA | 1 | $34,500,000 | 5.0% | 543,378 | Retail | 1.72x | 13.1% | 63.0% | 63.0% |

| 9 | Residence Inn Del Mar | San Diego, CA | GACC | 1 | $25,000,000 | 3.7% | 118 | Hospitality | 1.78x | 14.2% | 50.0% | 50.0% |

| 10 | Lincoln City Outlet Center | Lincoln City, OR | CREFI | 1 | $23,162,500 | 3.4% | 255,608 | Retail | 2.01x | 16.2% | 64.0% | 64.0% |

| | | | | | | | | | | | | |

| | Top 3 Total/Weighted Average | 3 | $198,000,000 | 29.0% | | | 2.68x | 18.3% | 41.2% | 40.9% |

| | Top 5 Total/Weighted Average | 12 | $314,410,000 | 46.0% | | | 2.32x | 16.0% | 46.1% | 45.9% |

| | Top 10 Total/Weighted Average | 18 | $469,372,500 | 68.7% | | | 2.16x | 15.5% | 49.2% | 49.1% |

| | Non-Top 10 Total/Weighted Average | 47 | $214,064,433 | 31.3% | | | 3.12x | 23.9% | 44.2% | 43.4% |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 5 | |

| Structural and Collateral Term Sheet | | BMO 2024-C8 |

| Collateral Characteristics |

| Pari Passu Companion Loan Summary |

No. | Loan Name | | Trust Cut-off Date Balance | Aggregate Pari Passu Loan Cut-off Date Balance | Controlling Pooling/Trust & Servicing Agreement | Master Servicer | Special Servicer | Related Pari Passu Loan(s) Securitizations | Related Pari Passu Loan(s) Original Balance |

| 1 | Danbury Fair Mall | GSMC, BMO | | $68,000,000 | | | $87,000,000 | | BMO 2024-C8 | Wells Fargo | Rialto | Future Securitization(s) | $87,000,000 |

| 2 | 60 Hudson | MSMCH, BMO | | $65,000,000 | | | $215,000,000 | | MSWF 2023-2 | Wells Fargo | Argentic | MSWF 2023-2

BBCMS 2023-C22

BMO 2023-C7

Future Securitization(s) | $90,000,000

$40,000,000

$20,000,000

$65,000,000 |

| 3 | Fayette Pavilion | SMC | | $65,000,000 | | | $29,125,000 | | BMO 2024-C8 | Wells Fargo | Rialto | Future Securitization(s) | $29,125,000 |

| 5 | Axis Apartments | CREFI | | $58,000,000 | | | $78,000,000 | | Benchmark 2023-B40 | Midland | LNR Partners | Benchmark 2023-B40

BBCMS 2024-C24 | $48,000,000

$30,000,000 |

| 7 | Arundel Mills and Marketplace | GACC | | $35,000,000 | | | $325,000,000 | | MSWF 2023-2 | Wells Fargo | Argentic | MSWF 2023-2

BMO 2023-C7

Benchmark 2023-B40

BBCMS 2024-C24

Future Securitization(s) | $90,000,000

$60,000,000

$25,000,000

$60,000,000

$90,000,000 |

| 11 | Woodfield Mall | BMO | | $20,000,000 | | | $244,000,000 | | BMO 2023-C7 | Midland | KeyBank | BMO 2023-C7

BBCMS 2024-C24

Future Securitization(s) | $68,000,000

$67,500,000

$108,500,000 |

| 12 | Medlock Crossing | LMF | | $19,850,000 | | | $7,000,000 | | BMO 2024-C8 | Wells Fargo | Rialto | Future Securitization(s) | $7,000,000 |

| 21 | OPI Portfolio | UBS AG | | $6,300,000 | | | $48,000,000 | | BMO 2024-5C3 | Wells Fargo | Greystone | BMO 2023-C7

BMO 2024-5C3 | $25,000,000

$23,000,000 |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 6 | |

| Structural and Collateral Term Sheet | | BMO 2024-C8 |

| Collateral Characteristics |

| Mortgaged Properties by Type |

| | | | | | Weighted Average |

| Property Type | Property Subtype | Number of Properties | Cut-off Date Principal Balance | % of IPB | UW

NCF DSCR | UW

NOI DY | Cut-off Date LTV | Maturity Date/ARD LTV |

| Retail | Anchored | 6 | $140,168,150 | 20.5% | 1.64x | 12.4% | 62.0% | 61.9% |

| | Super Regional Mall | 3 | 123,000,000 | 18.0 | 2.35x | 17.9% | 41.1% | 40.6% |

| | Single Tenant | 6 | 45,300,000 | 6.6 | 1.58x | 11.4% | 59.7% | 59.7% |

| | Outlet Center | 1 | 23,162,500 | 3.4 | 2.01x | 16.2% | 64.0% | 64.0% |

| | Subtotal: | 16 | $331,630,650 | 48.5% | 1.92x | 14.6% | 54.1% | 53.8% |

| Multifamily | Cooperative | 24 | $58,450,003 | 8.6% | 6.73x | 51.6% | 11.9% | 10.9% |

| | High Rise | 1 | 58,000,000 | 8.5 | 1.37x | 9.8% | 53.0% | 53.0% |

| | Subtotal: | 25 | $116,450,003 | 17.0% | 4.06x | 30.8% | 32.4% | 31.9% |

| Industrial | Manufacturing | 6 | $46,060,000 | 6.7% | 1.91x | 14.0% | 58.2% | 56.8% |

| | Manufacturing/Warehouse | 2 | 37,300,000 | 5.5 | 1.67x | 12.7% | 60.2% | 60.2% |

| | Warehouse/Manufacturing | 2 | 15,446,000 | 2.3 | 2.07x | 14.4% | 55.6% | 55.6% |

| | Warehouse/Distribution | 1 | 8,904,000 | 1.3 | 2.07x | 14.4% | 55.6% | 55.6% |

| | Subtotal: | 11 | $107,710,000 | 15.8% | 1.86x | 13.7% | 58.3% | 57.7% |

| Other | Data Center | 1 | $65,000,000 | 9.5% | 3.92x | 24.2% | 17.5% | 17.5% |

| Hospitality | Extended Stay | 1 | $25,000,000 | 3.7% | 1.78x | 14.2% | 50.0% | 50.0% |

| | Limited Service | 2 | 10,496,280 | 1.5 | 2.14x | 20.8% | 55.6% | 51.8% |

| | Subtotal: | 3 | $35,496,280 | 5.2% | 1.89x | 16.2% | 51.7% | 50.5% |

| Office | Medical | 4 | $7,500,000 | 1.1% | 1.89x | 13.1% | 55.1% | 55.1% |

| | Suburban | 1 | 4,499,569 | 0.7 | 1.75x | 13.8% | 48.4% | 48.4% |

| | CBD | 1 | 1,800,431 | 0.3 | 1.75x | 13.8% | 48.4% | 48.4% |

| | Subtotal: | 6 | $13,800,000 | 2.0% | 1.83x | 13.4% | 52.0% | 52.0% |

| Self Storage | Self Storage | 1 | $9,500,000 | 1.4% | 1.73x | 11.4% | 66.9% | 66.9% |

| Manufactured Housing | RV Park | 2 | $3,850,000 | 0.6% | 1.65x | 14.5% | 65.0% | 65.0% |

| Total / Weighted Average: | 65 | $683,436,933 | 100.0% | 2.46x | 18.1% | 47.6% | 47.3% |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 7 | |

| Structural and Collateral Term Sheet | | BMO 2024-C8 |

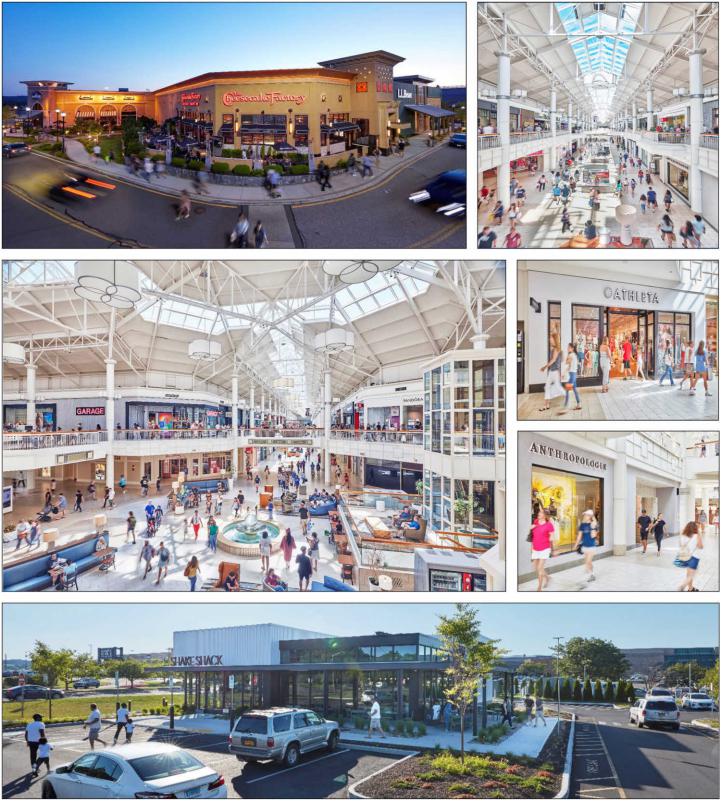

| No. 1 – Danbury Fair Mall |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 8 | |

| Structural and Collateral Term Sheet | | BMO 2024-C8 |

| No. 1 – Danbury Fair Mall |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 9 | |

| Structural and Collateral Term Sheet | | BMO 2024-C8 |

| No. 1 – Danbury Fair Mall |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 10 | |

| Structural and Collateral Term Sheet | | BMO 2024-C8 |

| No. 1 – Danbury Fair Mall |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 11 | |

| Structural and Collateral Term Sheet | | BMO 2024-C8 |

| No. 1 – Danbury Fair Mall |

| Mortgage Loan Information | | Property Information |

| Mortgage Loan Sellers: | GSMC, BMO | | Single Asset / Portfolio: | Single Asset |

| Original Principal Balance(1): | $68,000,000 | | Title: | Fee |

| Cut-off Date Principal Balance(1): | $68,000,000 | | Property Type – Subtype: | Retail – Super Regional Mall |

| % of IPB: | 9.9% | | Net Rentable Area (SF): | 923,598 |

| Loan Purpose: | Refinance | | Location: | Danbury, CT |

| Borrowers: | Danbury Mall, LLC and MS Danbury LLC | | Year Built / Renovated: | 1986 / 2007, 2017 |

| Borrower Sponsor: | The Macerich Partnership, L.P. | | Occupancy(3): | 97.1% |

| Interest Rate: | 6.38600% | | Occupancy Date: | 1/4/2024 |

| Note Date: | 1/25/2024 | | 4th Most Recent NOI (As of): | $24,148,737 (12/31/2020) |

| Maturity Date: | 2/6/2034 | | 3rd Most Recent NOI (As of): | $22,240,718 (12/31/2021) |

| Interest-only Period: | 96 months | | 2nd Most Recent NOI (As of): | $26,390,480 (12/31/2022) |

| Original Term: | 120 months | | Most Recent NOI (As of): | $30,411,426 (TTM 9/30/2023) |

| Original Amortization Term: | 360 months | | UW Economic Occupancy: | 94.5% |

| Amortization Type: | Interest Only, Amortizing Balloon | | UW Revenues: | $43,953,322 |

| Call Protection(2): | L(25),YM1(88),O(7) | | UW Expenses: | $13,946,497 |

| Lockbox / Cash Management: | Soft / Springing | | UW NOI: | $30,006,825 |

| Additional Debt(1): | Yes | | UW NCF: | $29,271,323 |

| Additional Debt Balance(1): | $87,000,000 | | Appraised Value / Per SF: | $371,000,000 / $402 |

| Additional Debt Type(1): | Pari Passu | | Appraisal Date: | 12/18/2023 |

| | | | | |

| Escrows and Reserves(4) | | Financial Information(1) |

| | Initial | Monthly | Initial Cap | | Cut-off Date Loan / SF: | $168 |

| Taxes: | $0 | Springing | N/A | | Maturity Date Loan / SF: | $164 |

| Insurance: | $0 | Springing | N/A | | Cut-off Date LTV: | 41.8% |

| Replacement Reserves: | $0 | Springing | N/A | | Maturity Date LTV: | 40.9% |

| TI / LC: | $0 | Springing | N/A | | UW NCF DSCR: | 2.52x |

| Other(5): | $4,103,258 | $0 | N/A | | UW NOI Debt Yield: | 19.4% |

| | | | | | | |

| | | | | | | |

| Sources and Uses |

| Sources | Proceeds | % of Total | | Uses | Proceeds | % of Total |

| Whole Loan(1) | $155,000,000 | 100.0% | | Loan Payoff | $116,946,803 | 75.4 | % |

| | | | | Equity Distribution | 30,706,123 | 19.8 | |

| | | | | Reserves | 4,103,258 | 2.6 | |

| | | | | Closing Costs(6) | 3,243,816 | 2.1 | |

| Total Sources | $155,000,000 | 100.0% | | Total Uses | $155,000,000 | 100.0 | % |

| (1) | The Danbury Fair Mall Mortgage Loan (as defined below) is part of the Danbury Fair Mall Whole Loan (as defined below), which is evidenced by six pari passu promissory notes with an aggregate principal balance of $155,000,000. The Financial Information presented above is based on the aggregate principal balance of the promissory notes comprising the Danbury Fair Mall Whole Loan. |

| (2) | The Danbury Fair Mall Whole Loan may be voluntarily prepaid in whole (but not in part, other than in connection with the release of the L&T Parcel (as defined below) pursuant to the Mortgage Loan documents) at any time from and after the earlier to occur of (i) February 6, 2027 and (ii) the date that is two years from the closing date of the securitization that includes the last pari passu note of the Danbury Fair Mall Whole Loan to be securitized, with the payment of a yield maintenance premium if such prepayment is made prior to August 6, 2033. From and after August 6, 2033, the Danbury Fair Mall Whole Loan may be voluntarily prepaid in whole without the payment of a yield maintenance premium. The assumed lockout period of 25 payments is based on the expected BMO 2024-C8 securitization closing date in March 2024. The actual lockout period may be longer. |

| (3) | Occupancy includes all tenants in place, specialty leasing tenants of greater than six months, and tenants with signed leases as of the reporting period. Occupancy excludes gross leasable area for anchor tenants. |

| (4) | See “Escrows and Reserves” below for further discussion of reserve information. |

| (5) | Other Reserves include an outstanding TI/LC reserve of $3,460,293 and a gap and rent reserve of $642,965.09 which represents the sum of (i) the pro-rated rent for tenants with lease commencement dates after the note date, and (ii) the differential in current and contractual rent for tenants whose co-tenancy clauses will be cured by incoming leases with Target and Round 1 Entertainment, who are expected to open and commence paying rent on April 14, 2024 and March 9, 2024, respectively. |

| (6) | Closing Costs includes an interest rate buy-down fee of approximately $1,550,000. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 12 | |

| Structural and Collateral Term Sheet | | BMO 2024-C8 |

| No. 1 – Danbury Fair Mall |

The Loan. The largest mortgage loan (the “Danbury Fair Mall Mortgage Loan”) is part of a whole loan (the “Danbury Fair Mall Whole Loan”) evidenced by six pari passu promissory notes issued by Danbury Mall, LLC and MS Danbury LLC in the aggregate original principal amount of $155,000,000. The Danbury Fair Mall Mortgage Loan is evidenced by the controlling Note A-1 and non-controlling note A-2, which have an aggregate outstanding principal balance as of the Cut-off Date of $68,000,000. The Danbury Fair Mall Mortgage Loan will be included in the BMO 2024-C8 securitization trust and represents approximately 9.9% of the Initial Pool Balance. The Danbury Fair Mall Whole Loan was co-originated on January 25, 2024 by Goldman Sachs Bank USA (“GSBI”), Morgan Stanley Bank, N.A. (“MSBNA”) and Bank of Montreal (“BMO”). The Danbury Fair Mall Whole Loan is secured by the borrowers’ fee simple interest in an approximately 1.27 million square foot enclosed super regional mall located in Danbury, Connecticut, of which 923,598 square feet serves as collateral (the “Danbury Fair Mall Property”) for the Danbury Fair Mall Whole Loan and does not include any portion of the regional mall that is occupied by Macy’s and JCPenney (which own their own parcels). The Danbury Fair Mall Whole Loan has a 10-year term, with an interest-only period accruing interest at a rate of 6.38600% per annum on an Actual/360 basis, followed by amortization on a 30-year basis.

The table below identifies the promissory notes that comprise the Danbury Fair Mall Whole Loan. The Danbury Fair Mall Whole Loan will be serviced pursuant to the pooling and servicing agreement for the BMO 2024-C8 trust securitization. The relationship between the holders of the Danbury Fair Mall Whole Loan is governed by a co-lender agreement as described under “Description of the Mortgage Pool—The Whole Loans—The Serviced Pari Passu Whole Loans” and “The Pooling and Servicing Agreement” in the Preliminary Prospectus.

| Whole Loan Summary |

| Note | Original Balance | Cut-off Date Balance | Note Holder | Controlling Piece |

| A-1 | $[65,000,000] | $[65,000,000] | BMO 2024-C8 | Yes |

| A-2 | $[25,000,000] | $[25,000,000] | BMO 2024-C8 | No |

| A-3 | $31,000,000 | $31,000,000 | MSBNA(1) | No |

| A-4 | $20,250,000 | $20,250,000 | GSMC(1) | No |

| A-5 | $5,500,000 | $5,500,000 | BMO(1) | No |

| A-6 | $8,250,000 | $8,250,000 | BMO(1) | No |

| Whole Loan | $155,000,000 | $155,000,000 | | |

| (1) | Expected to be contributed to one or more future securitization trusts. |

The Property. The Danbury Fair Mall Property is part of a two-story, Class B+ super regional mall located in Danbury, Connecticut. The Danbury Fair Mall Property consists of 923,598 owned square feet within a super regional mall of 1,274,784 square feet, which is anchored by a 218,213 square foot Macy’s (non-collateral), a 132,973 square foot JCPenney (non-collateral), a 73,080 square foot DICK’S Sporting Goods and a 51,489 square foot Primark. The Borrower Sponsor (as defined below) recently executed leases with Round 1 Entertainment and Target to occupy anchor/major space at the Danbury Fair Mall Property beginning in March 2024 and April 2024, respectively. The Danbury Fair Mall Property is a shopping and dining destination located off the intersection of Interstate 84 and Route 7 in Danbury, Connecticut. The Danbury Fair Mall Property was originally constructed in 1986 and expanded in 1991 with the addition of the Lord & Taylor box (improvements owned by the tenant). The Danbury Fair Mall Property was acquired by the Borrower Sponsor in 2005. Following the Borrower Sponsor’s acquisition, the Danbury Fair Mall Property underwent a $24.8 million renovation in 2007. The Borrower Sponsor completed a second large scale renovation in 2011 following its acquisition of the former Filene’s parcel in 2010. The $38.0 million redevelopment included a reconfiguration of the 170,000 square feet Filene’s box into a DICK’S Sporting Goods on the main level, Forever 21 on the lower level, plus the addition of L.L. Bean, Cheesecake Factory and the former Brio Tuscan Grille. Today, the Danbury Fair Mall Property leases to a mix of retailers and offers a multitude of dining options. The Danbury Fair Mall Property’s granular rent roll includes over 150 tenants with no non-anchor/major tenants accounting for more than 1.05% of collateral SF and 2.78% of Total Underwritten Rent. The Danbury Fair Mall Property is 97.1% leased as of January 4, 2024, which represents an improvement since the pandemic-driven occupancy trough of 90.1% in 2021. Comparable in-line tenant sales at the Danbury Fair Mall Property were $747 PSF in Q3 2023, up 13.6% over pre-COVID 2019 sales of $658 PSF, equating to an occupancy cost of 11.7%. Comparable ex-Apple in-line sales over the same period were $564 PSF, up 11.0% over pre-COVID 2019 sales of $508 PSF, equating to an occupancy cost of 14.7%.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 13 | |

| Structural and Collateral Term Sheet | | BMO 2024-C8 |

| No. 1 – Danbury Fair Mall |

The Danbury Fair Mall Property contains a dark 79,872 square foot anchor box (the “L&T Parcel”) that is owned by Hudson Bay Company and subleased to Lord & Taylor. Lord & Taylor and was operational before its parent company closed all locations. The tenant has kept current on its rent obligations. In August 2022, the Borrower Sponsor was able to secure a lease with National Resources who plans to invest over $25.0 million into the L&T Parcel to redevelop the existing two-level location into a multi family project featuring micro-housing and medical office uses. The borrowers have successfully rezoned the Danbury Fair Mall Property to allow for multi family development and have obtained the necessary entitlements for this conversion from the City of Danbury. The borrowers expect the project to generate approximately $400,000 in incremental rent revenue annually over Lord & Taylor’s current lease, subject to recapturing the space from Lord & Taylor. The L&T Parcel can be released at any time with the prepayment of the Danbury Fair Mall Whole Loan in the amount equal to the greater of (x) $2,000,000 and (y) 45% of the proceeds of the sale of the L&T Parcel, subject to satisfaction of certain conditions set forth in the Danbury Fair Mall Mortgage Loan documents.

Major Tenants. The three largest tenants based on underwritten base rent are DICK’S Sporting Goods, Target and Round 1 Entertainment.

DICK’S Sporting Goods (73,080 square feet, 7.9% of net rentable area (“NRA”), 6.6% of underwritten base rent): DICK’S Sporting Goods is a sports apparel and equipment retailer with 728 locations as of January 28, 2023 that was founded in 1948 in Binghamton, New York. DICK’S Sporting Goods occupies 73,080 square feet on a lease that expires January 31, 2031 with three, five-year renewal options and no termination options. DICK’S Sporting Goods currently pays $25.00 per SF with a scheduled rent increase in lease year 6.

Target (126,615 square feet, 13.7% of NRA, 4.9% of underwritten base rent): Founded in 1962, Target is a general merchandise retailer with stores in all 50 states and the District of Columbia, totaling 1,956 domestic locations, as of February 2024. In 2022, Target generated approximately $109 billion in total revenue. Target will occupy 126,615 SF and is expected to open and commence paying rent on April 14, 2024 on a lease that expires January 31, 2034 with eight, five-year renewal options and no termination options. Target is expected to pay $10.67 per SF with a scheduled rent increase on May 1, 2029.

Round 1 Entertainment (60,848 square feet, 6.6% of NRA, 4.5% of underwritten base rent): Round 1 Entertainment is a multi-entertainment facility that includes bowling, arcade games, karaoke, billiards, darts and ping pong, and operates under the Round 1 Entertainment Inc. parent entity, which was established in 2009 and currently has more than 50 locations that are open or plan to open across the United States as of February 2024. Round 1 Entertainment will occupy 60,848 square feet on a lease that is expected to commence on March 9, 2024 and expires February 28, 2034 with two, five-year renewal options and no termination options. Round 1 Entertainment is expected to pay $20.75 per SF with a scheduled rent increase in lease year 6.

Appraisal. According to the appraisal, the Danbury Fair Mall Property had an “as-is” appraised value of $371,000,000 as of December 18, 2023. The table below shows the appraisal’s “as-is” conclusions.

| Appraisal Valuation Summary(1) |

| Appraisal Approach | Appraised Value | Capitalization Rate |

| Income Capitalization Approach | $371,000,000 | 7.75% |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 14 | |

| Structural and Collateral Term Sheet | | BMO 2024-C8 |

| No. 1 – Danbury Fair Mall |

Environmental. The Phase I environmental assessment of the Danbury Fair Mall Property dated December 21, 2023 identified no recognized environmental conditions, controlled environmental conditions or significant data gaps. See “Description of the Mortgage Pool—Environmental Considerations” in the Prospectus.

The following table presents certain information relating to the historical occupancy of the Danbury Fair Mall Property:

| Historical and Current Occupancy(1) |

| 2021 | 2022 | 9/30/2023 | Current(2)(3) |

| 90.1% | 98.1% | 99.3% | 97.1% |

| (1) | Historical Occupancies are as of December 31 of each respective year, unless otherwise specified. |

| (2) | Based on the underwritten rent roll dated January 4, 2024. |

| (3) | Occupancy includes all tenants in place, specialty leasing tenants of greater than six months, and tenants with signed leases as of the reporting period. Occupancy excludes gross leasable area for anchor tenants |

The following table presents certain information relating to the major tenants (of which, certain tenants have co-tenancy provisions) at the Danbury Fair Mall Property:

| Top Tenant Summary(1) |

| Tenant Name | Credit Rating (Moody's/ S&P/Fitch)(2) | Net Rentable Area (SF) | % of Total NRA | UW Base Rent PSF(3) | UW Base Rent (3) | % of Total UW Base Rent | Lease Exp. Date |

| DICK'S Sporting Goods | Baa3/BBB/NR | 73,080 | 7.9 | % | $25.00 | $1,827,000 | 6.6 | % | 1/31/2031 |

| Target(4) | A2/A/A | 126,615 | 13.7 | | $10.67 | 1,350,417 | 4.9 | | 1/31/2034 |

| Round 1 Entertainment(5) | NR/NR/NR | 60,848 | 6.6 | | $20.75 | 1,262,529 | 4.5 | | 2/28/2034 |

| Primark | NR/NR/NR | 51,489 | 5.6 | | $21.77 | 1,120,676 | 4.0 | | 8/31/2026 |

| Apple Store | Aaa/AA+/NR | 9,675 | 1.0 | | $79.64 | 770,536 | 2.8 | | 7/31/2027 |

| Victoria's Secret(6) | B1/BB-/NR | 12,133 | 1.3 | | $62.43 | 757,471 | 2.7 | | 3/31/2024 |

| Banana Republic | B1/BB/NR | 8,427 | 0.9 | | $75.35 | 634,998 | 2.3 | | 3/31/2025 |

| Old Navy | B1/BB/NR | 16,640 | 1.8 | | $34.00 | 565,760 | 2.0 | | 3/31/2027 |

| H&M | NR/BBB/NR | 21,563 | 2.3 | | $26.24 | 565,757 | 2.0 | | 1/31/2028 |

| Barnes & Noble | NR/NR/NR | 19,092 | 2.1 | | $28.00 | 534,576 | 1.9 | | 1/31/2034 |

| Ten Largest Owned Tenants | | 399,562 | 43.3 | % | $23.50 | $9,389,721 | 33.8 | % | |

| Remaining Owned Tenants(7)(8) | | 497,550 | 53.9 | | $36.91 | 18,365,234 | 66.2 | | |

| Occupied Total Collateral | | 897,112 | 97.1 | % | $30.94 | $27,754,954 | 100.0 | % | |

| Vacant Space (Owned) | | 26,486 | 2.9 | | | | | |

| Totals/ Wtd. Avg. All Owned Tenants | | 923,598 | 100.0 | % | | | | |

| (1) | Based on the underwritten rent roll dated January 4, 2024. |

| (2) | Certain ratings are those of the parent company whether or not the parent guarantees the lease. |

| (3) | UW Base Rent PSF and UW Base Rent includes percentage in-lieu of rents totaling $653,695. |

| (4) | Target is expected to open and commence paying rent on April 14, 2024 and is obligated to begin paying rent once the tenant opens for business. We cannot assure you that the tenant will take occupancy, or begin paying rent, on the lease commencement date or at all. |

| (5) | Round 1 Entertainment is expected to open and commence paying rent on March 9, 2024 and is obligated to begin paying rent once the tenant opens for business. We cannot assure you that the tenant will take occupancy, or begin paying rent, on the lease commencement date or at all. |

| (6) | Victoria’s Secret is currently in negotiation with the Borrower Sponsor to renew its lease. We cannot assure you that the tenant will renew its lease. |

| (7) | Remaining Owned Tenants includes various tenants with lease start dates after the loan origination date, that total 17,007 SF and $721,949 of UW Base Rent. |

| (8) | Remaining Owned Tenants includes $359,999 of UW Base Rent from the L&T Parcel. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 15 | |

| Structural and Collateral Term Sheet | | BMO 2024-C8 |

| No. 1 – Danbury Fair Mall |

The following table presents certain information relating to the lease rollover schedule at the Danbury Fair Mall Property:

| Lease Rollover Schedule(1)(2) |

| Year | Number of Leases Expiring | Net Rentable Area Expiring | % of NRA Expiring | UW Base Rent Expiring(3) | % of UW Base Rent Expiring(3) | Cumulative Net Rentable Area Expiring | Cumulative % of NRA Expiring | Cumulative UW Base Rent Expiring(3) | Cumulative % of UW Base Rent Expiring(3) |

| Vacant | NAP | 26,486 | 2.9 | % | NAP | NA | P | 26,486 | 2.9% | NAP | NAP |

| 2024 & MTM | 89 | 120,663 | 13.1 | | $3,885,175 | 14.0 | % | 147,149 | 16.0% | $3,885,175 | 14.0% |

| 2025 | 26 | 92,003 | 10.0 | | 4,068,700 | 14.7 | | 239,152 | 25.9% | $7,953,874 | 28.7% |

| 2026 | 18 | 87,861 | 9.5 | | 3,188,885 | 11.5 | | 327,013 | 35.4% | $11,142,759 | 40.1% |

| 2027 | 25 | 85,272 | 9.2 | | 4,517,226 | 16.3 | | 412,285 | 44.6% | $15,659,985 | 56.4% |

| 2028 | 9 | 52,097 | 5.6 | | 2,102,536 | 7.6 | | 464,382 | 50.3% | $17,762,521 | 64.0% |

| 2029 | 8 | 22,480 | 2.4 | | 1,310,678 | 4.7 | | 486,862 | 52.7% | $19,073,199 | 68.7% |

| 2030 | 7 | 26,886 | 2.9 | | 1,377,160 | 5.0 | | 513,748 | 55.6% | $20,450,359 | 73.7% |

| 2031 | 4 | 82,944 | 9.0 | | 2,251,483 | 8.1 | | 596,692 | 64.6% | $22,701,841 | 81.8% |

| 2032 | 3 | 13,029 | 1.4 | | 497,926 | 1.8 | | 609,721 | 66.0% | $23,199,767 | 83.6% |

| 2033 | 5 | 23,268 | 2.5 | | 708,784 | 2.6 | | 632,989 | 68.5% | $23,908,551 | 86.1% |

| 2034 | 4 | 207,376 | 22.5 | | 3,240,541 | 11.7 | | 840,365 | 91.0% | $27,149,092 | 97.8% |

| 2035 & Beyond | 2 | 83,233 | 9.0 | | 605,863 | 2.2 | | 923,598 | 100.0% | $27,754,954 | 100.0% |

| Total | 200 | 923,598 | 100.0 | % | $27,754,954 | 100.0 | % | | | | |

| (1) | Information is based on the underwritten rent roll dated January 4, 2024. |

| (2) | Certain tenants may have lease termination options that are exercisable prior to the stated expiration date of the subject lease or leases which are not considered in the Lease Rollover Schedule. |

| (3) | UW Base Rent Expiring, % of UW Base Rent Expiring, Cumulative UW Base Rent Expiring and Cumulative % of UW Base Rent Expiring includes percentage in-lieu of rents totaling $653,695. |

The following table presents certain information relating to the underwritten cash flows of the Danbury Fair Mall Property:

| Operating History and Underwritten Net Cash Flow |

| | 2020 | 2021 | 2022 | TTM September 2023 | Underwritten | Per Square Foot(1) | % |

| Base Rent(2)(3) | $25,189,660 | $22,919,907 | $22,862,520 | $23,737,683 | $27,101,259 | $29.34 | | 58.3 | % |

| Gross Up Vacancy | 0 | 0 | 0 | 0 | 1,764,389 | 1.91 | | 3.8 | |

| Other Commercial Rental Revenue(4) | 2,505,763 | 4,662,477 | 5,242,739 | 5,354,726 | 5,111,552 | 5.53 | | 11.0 | |

| Commercial Reimbursement Revenue | 14,157,025 | 11,138,371 | 9,961,216 | 11,696,366 | 11,898,954 | 12.88 | | 25.6 | |

| Credit Tenant Rent Steps | 0 | 0 | 0 | 0 | 79,821 | 0.09 | | 0.2 | |

| Miscellaneous Revenue | 633,477 | 305,542 | 659,728 | 638,512 | 549,969 | 0.60 | | 1.2 | |

| Gross Potential Rent | $42,485,925 | $39,026,297 | $38,726,203 | $41,427,286 | $46,505,943 | $50.35 | | 100.0 | % |

| Commercial Credit Loss | (3,590,947) | (865,112) | (54,641) | (61,365) | (2,552,621) | (2.76) | | (5.5 | ) |

| Effective Gross Income | $38,894,978 | $38,161,185 | $38,671,562 | $41,365,921 | $43,953,322 | $47.59 | | 94.5 | % |

| Real Estate Taxes | 8,160,081 | 8,178,060 | 3,560,760 | 2,338,238 | 5,313,240 | 5.75 | | 12.1 | |

| Insurance | 290,848 | 342,559 | 377,870 | 397,892 | 500,460 | 0.54 | | 1.1 | |

| Other Expenses | 6,295,312 | 7,399,848 | 8,342,452 | 8,218,365 | 8,132,797 | 8.81 | | 18.5 | |

| Net Operating Income | $24,148,737 | $22,240,718 | $26,390,480 | $30,411,426 | $30,006,825 | $32.49 | | 68.3 | % |

| Total TI/LC, Capex/RR | 0 | 0 | 0 | 0 | 735,502 | 0.80 | | 1.7 | |

| Net Cash Flow | $24,148,737 | $22,240,718 | $26,390,480 | $30,411,426 | $29,271,323 | $31.69 | | 66.6 | % |

| (1) | Per Square Foot is based on the total collateral square feet of 923,598. |

| (2) | Base Rent reflects annualized in-place base rent for in-place tenants and recently executed leases as of January 2024, with contractual rent steps through March 2025. Rental revenues have been adjusted to be exclusive of deferred straight-line minimum rent and termination income. |

| (3) | The difference between Underwritten Base Rent and previous historical Base Rent figures is primarily attributable to $2,612,946 of rent from both Target and Round 1 Entertainment, who are expected to take occupancy after the origination date. |

| (4) | Other Commercial Rental Revenue includes Overage / Percentage Rent, PIL Rent, Kiosks, Temporary, Specialty tenants and Business Development Income. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 16 | |

| Structural and Collateral Term Sheet | | BMO 2024-C8 |

| No. 1 – Danbury Fair Mall |

The Market. The Danbury Fair Mall Property is located within the Danbury area of the Bridgeport-Stamford-Norwalk MSA. The Danbury Fair Mall Property’s surrounding area is categorized as suburban consisting primarily of single-family homes and retail centers, and the Danbury Fair Mall Property is considered the largest demand generator within the City of Danbury. The Danbury Fair Mall Property benefits from proximity to Manhattan which is located approximately 60 miles away and access to the Westchester County Airport, situated approximately 35 miles from the mall. In 2022, the Bridgeport-Stamford-Norwalk MSA gross metro product was $70.6 billion, a 3.3% increase from 2021. Within the immediate trade area comprised of the 1.0-mile region surrounding the Danbury Fair Mall Property, the 2023 average annual household income is approximately $132,337, relative to the 2023 statewide household income of approximately $129,040.

The following table presents retail market statistics for the surrounding area of the Danbury Fair Mall Property:

| Retail Market Statistics (TTM Q4 2023)(1) |

| Market/Submarket | Inventory (SF) | Completions (SF) | Vacancy | Net Absorption (SF) | NNN Rent Overall / SF |

| Stamford Retail | 53,184,660 | 171,383 | 4.00% | -245,986 | $32.75 |

| Danbury Retail | 6,955,057 | 45,000 | 4.00% | -106,171 | $22.32 |

| 1-Mile Radius Retail | 2,134,351 | 0 | 7.70% | -122,019 | $28.90 |

The Borrowers and Borrower Sponsor. The borrowers are Danbury Mall, LLC and MS Danbury LLC, each a single purpose entity with two independent directors. Legal counsel to the borrowers delivered a non-consolidation opinion in connection with the origination of the Danbury Fair Mall Whole Loan. The borrower sponsor (the “Borrower Sponsor”) and non-recourse carveout guarantor is The Macerich Partnership, L.P., a Delaware limited partnership headquartered in Santa Monica, California and a provider of real estate investment services. The Macerich Partnership, L.P. acquires, leases, manages, develops, and redevelops malls and community centers.

Property Management. The Danbury Fair Mall Property is managed by MACW Property Management, LLC, an affiliate of the Borrower Sponsor.

Escrows and Reserves. At origination, the borrowers were required to deposit into escrow (i) approximately $642,965 for a gap rent reserve and (ii) $3,460,293 for a TI/LC reserve (comprised of unpaid tenant allowances ($2,748,013), unpaid leasing commissions ($562,280) and landlord work ($150,000)).

Tax Escrows - During the continuance of a Trigger Period (as defined below), the borrowers are required to escrow 1/12th of the annual estimated tax payments on a monthly basis.

Insurance Escrows – During the continuance of a Trigger Period, the borrowers are required to escrow 1/12th of the annual estimated insurance payments on a monthly basis, except if the Danbury Fair Mall Property is insured under a blanket policy meeting the requirements set forth in the related loan agreement (in which case, no insurance escrows will be required, notwithstanding the occurrence of a Trigger Period).

Capital Expenditure Reserve - During the continuance of a Trigger Period, the borrowers are required to escrow an amount equal to the gross leasable area (excluding the Non-Collateral Square Footage (as defined below)) of any tenant that is required to pay for all repairs and maintenance costs for its entire leased premises, roof and structural components, and the following tenants: (i) Lord & Taylor, (ii) Shake Shack and (iii) Longhorn Steakhouse), multiplied by $0.25 and divided by 12 months. The monthly replacement reserve amount is estimated to be approximately $17,390. The borrowers are permitted to cease monthly deposits when the replacement reserve balance is equal to the sum of 24 monthly deposits, currently estimated to be $417,353. The tenants listed in clause (i) through (iii) above collectively represent 9.6% of the NRA and 2.6% of UW Base Rent.

Rollover Reserve – During the continuance of a Trigger Period, the borrowers are required to escrow an amount equal to the gross leasable area (excluding the Non-Collateral Square Footage and, to the extent not causing or contributing to the cause of the applicable Trigger Period, Lord & Taylor (and/or Live Uno), Target, Round 1 Entertainment, DICK’S Sporting Goods, Shake Shack and Longhorn Steakhouse) multiplied by $1.00 and divided by 12 months. The monthly rollover reserve amount is estimated to be approximately $47,847. The borrowers are not required to make any monthly deposits when the rollover reserve balance is equal to the sum of 24 monthly deposits, currently estimated to be $1,148,324. The borrowers’ upfront deposit of $642,965.09 with respect to gap rent is not included in the calculation of the rollover reserve balance for purposes of calculating the rollover reserve cap.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 17 | |

| Structural and Collateral Term Sheet | | BMO 2024-C8 |

| No. 1 – Danbury Fair Mall |

“Non-Collateral Square Footage” means the square footage occupied by Macy’s and JCPenney.

Lockbox / Cash Management. The Danbury Fair Mall Whole Loan is structured with a soft lockbox and springing cash management. The borrowers and property manager are required to direct the tenants to pay rent directly into the lockbox account, and to deposit any rents otherwise received in such account within three business days after receipt. So long as no Trigger Period is continuing, borrowers will have access to the funds deposited into the lockbox account, and may utilize the lockbox account as its operating account. During the continuance of a Trigger Period, all funds in the lockbox account are required to be swept on a weekly basis and on the second business day before each payment date to a lender-controlled cash management account. Funds in the cash management account are required to be applied to debt service and the reserves and escrows described above, with any excess funds (i) to be deposited into the TI/LC Reserve, if the Trigger Period is caused by a Tenant Trigger Event, or into an excess cash flow reserve account held by the lender as cash collateral for the Danbury Fair Mall Whole Loan, or if (ii) no Trigger Period is continuing, disbursed to the borrowers.

A “Trigger Period” means the period commencing upon the occurrence of (i) an event of default or (ii) a Low Debt Yield Period (as defined below). A Trigger Period will end (a) with respect to the matters described in clause (i) above, if the event of default has been waived by the lender and no other event of default is then continuing or (b) with respect to the matters described in clause (ii) above, if a cure of the Low Debt Yield Period occurs.

A “Low Debt Yield Period” will commence if, as of any calculation date, the Danbury Fair Mall Whole Loan debt yield is less than (x) 12.5% for the period commencing on the origination date to and excluding the eighth anniversary of the origination date, and end if the Danbury Fair Mall Whole Loan has achieved a debt yield of at least 12.5% for two consecutive calculation dates (45th day following the end of each calendar quarter during the term), and (y) 15.0% for the period commencing on the eighth anniversary of the origination date until the maturity date, and end if the Danbury Fair Mall Whole Loan has achieved a debt yield of at least 15.0% for two consecutive calculation dates.

Subordinate Debt. None. However, the borrowers are permitted to obtain property assessed clean energy (PACE) or similar loans in an aggregate amount up to $7.5 million without the consent of the lender.

Mezzanine Debt. None.

Partial Release. The borrowers may obtain the release of one or more non-income producing parcels without the payment of a release price (except with respect to the L&T Parcel), subject to satisfaction of certain conditions including, but not limited to, (i) no event of default has occurred and is continuing, (ii) regardless of whether such release is successfully consummated, the borrowers pay to the lender a processing fee in the amount of $15,000, (iii) the remaining property constitutes a separate tax lot (or the borrowers have filed an application for a separate tax lot and the Borrower Sponsor guarantees the payment of taxes on such release parcel pending the final issuance of such separate tax lot), (iv) the borrowers certify to the lender that the remaining property with all easements appurtenant and other permitted encumbrances thereto will not, strictly as a result of such transfer, be in violation of any reciprocal easement agreements or major leases, or any then applicable law, statute, rule or regulation and (v) satisfaction of any REMIC release conditions. The borrowers may obtain release of the L&T Parcel with the payment of a release price equal to the greater of $2,000,000 and 45% of the proceeds of the sale of the L&T Parcel (after deduction for reasonable and customary out-of-pocket costs of sale) and a yield maintenance premium if released prior to the open period.

Ground Lease. None.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 18 | |

| Structural and Collateral Term Sheet | | BMO 2024-C8 |

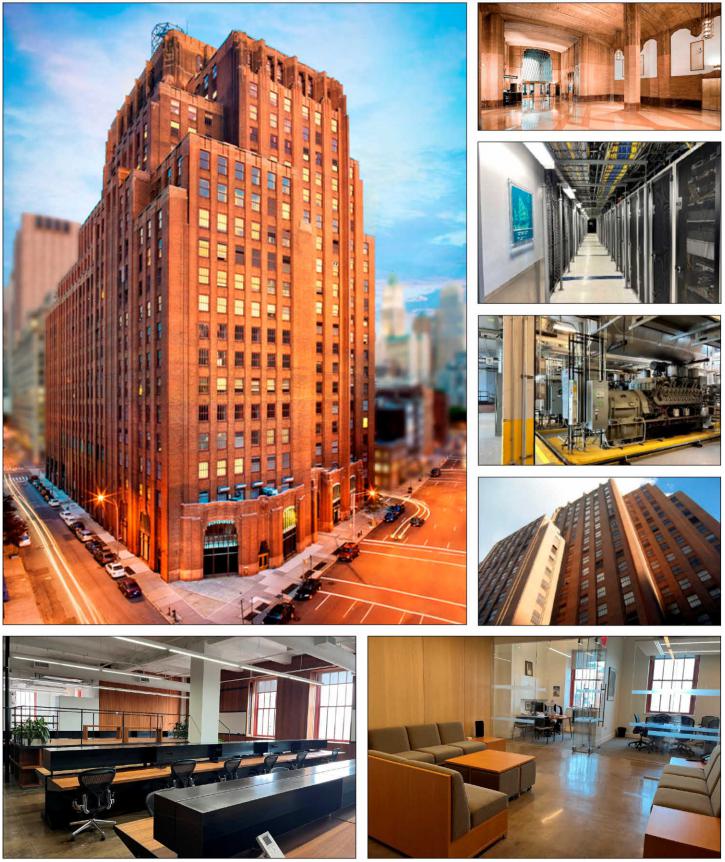

| No. 2 – 60 Hudson |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 19 | |

| Structural and Collateral Term Sheet | | BMO 2024-C8 |

| No. 2 – 60 Hudson |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 20 | |

| Structural and Collateral Term Sheet | | BMO 2024-C8 |

| No. 2 – 60 Hudson |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 21 | |

| Structural and Collateral Term Sheet | | BMO 2024-C8 |

| No. 2 – 60 Hudson |

| Mortgage Loan Information | | Property Information |

| Mortgage Loan Seller: | MSMCH, BMO | | Single Asset / Portfolio: | Single Asset |

| Original Principal Balance(1): | $65,000,000 | | Title: | Fee |

| Cut-off Date Principal Balance(1): | $65,000,000 | | Property Type - Subtype: | Other – Data Center |

| % of IPB: | 9.5% | | Net Rentable Area (SF): | 1,149,619 |

| Loan Purpose: | Refinance | | Location: | New York, NY |

| Borrower: | 60 Hudson Owner, LLC | | Year Built / Renovated: | 1930 / 2013 |

| Borrower Sponsor: | The Stahl Organization(2) | | Occupancy: | 62.2% |

| Interest Rate: | 5.88500% | | Occupancy Date: | 6/5/2023 |

| Note Date: | 9/6/2023 | | 4th Most Recent NOI (As of): | $67,543,911 (12/31/2020) |

| Maturity Date: | 10/1/2033 | | 3rd Most Recent NOI (As of): | $77,460,400 (12/31/2021) |

| Interest-only Period: | 120 months | | 2nd Most Recent NOI (As of): | $65,561,820 (12/31/2022) |

| Original Term: | 120 months | | Most Recent NOI (As of): | $73,525,984 (TTM 6/30/2023) |

| Original Amortization Term: | None | | UW Economic Occupancy: | 65.2% |

| Amortization Type: | Interest Only | | UW Revenues: | $120,518,204 |

| Call Protection(3): | L(29),D(86),O(5) | | UW Expenses: | $52,684,531 |

| Lockbox / Cash Management: | Hard / In Place | | UW NOI: | $67,833,673 |

| Additional Debt(1): | Yes | | UW NCF: | $65,493,494 |

| Additional Debt Balance(1): | $215,000,000 | | Appraised Value / Per SF: | $1,596,000,000 / $1,388 |

| Additional Debt Type(1): | Pari Passu | | Appraisal Date: | 5/8/2023 |

| | | | | |

| Escrows and Reserves(4) | | Financial Information(1) |

| | Initial | Monthly | Initial Cap | | Cut-off Date Loan / SF: | $244 |

| Taxes: | $7,089,987 | $1,772,497 | N/A | | Maturity Date Loan / SF: | $244 |

| Insurance: | $0 | Springing | N/A | | Cut-off Date LTV: | 17.5% |

| Replacement Reserves: | $0 | Springing | N/A | | Maturity Date LTV: | 17.5% |

| TI / LC: | $0 | Springing | N/A | | UW NCF DSCR: | 3.92x |

| | | | | | UW NOI Debt Yield: | 24.2% |

| | | | | | | |

| Sources and Uses |

| Sources | Proceeds | % of Total | | Uses | Proceeds | % of Total |

| Whole Loan | $280,000,000 | 98.7 | % | | Loan Payoff | $274,771,150 | 96.9 | % |

| Borrower Sponsor Equity | 3,678,608 | 1.3 | | | Reserves | 7,089,987 | 2.5 | |

| | | | | Closing Costs | 1,817,471 | 0.6 | |

| Total Sources | $283,678,608 | 100.0 | % | | Total Uses | $283,678,608 | 100.0 | % |

| (1) | The 60 Hudson Mortgage Loan (as defined below) is part of the 60 Hudson Whole Loan (as defined below), which is comprised of 11 pari passu promissory notes with an aggregate original principal balance of $280,000,000. The Financial Information in the chart above reflects the 60 Hudson Whole Loan. |

| (2) | There is no non-recourse carveout guarantor or separate environmental indemnitor with respect to the 60 Hudson Whole Loan. |

| (3) | Defeasance of the 60 Hudson Whole Loan is permitted at any time after the earlier of (i) April 1, 2027 or (ii) the date that is two years from the closing date of the securitization that includes the last pari passu note of the 60 Hudson Whole Loan to be securitized. The assumed lockout period of 29 payments is based on the expected BMO 2024-C8 securitization closing date in March 2024. The actual lockout period may be longer. |

| (4) | For a full description of Escrows and Reserves, see “Escrows and Reserves” below. |

The Loan. The second largest mortgage loan (the “60 Hudson Mortgage Loan”), is part of the 60 Hudson whole loan (the “60 Hudson Whole Loan”) with an original principal balance of $280,000,000. The 60 Hudson Whole Loan is secured by the borrower’s fee interest in a data center located in New York, New York totaling 1,149,619 square feet (the “60 Hudson Property”). The 60 Hudson Whole Loan consists of 11 pari passu notes and accrues interest at a rate of 5.88500% per annum. The 60 Hudson Whole Loan has a 10-year term, is interest-only for the full term of the loan and accrues interest on an Actual/360 basis. The 60 Hudson Whole Loan was originated by Morgan Stanley Bank, N.A. (“MSBNA”). Bank of Montreal purchased the non-controlling Note A-6 in the original principal amount of $20,000,000 and the non-controlling Note A-7-2 in the original principal amount of $5,000,000 from Morgan Stanley Mortgage Capital Holdings LLC (“MSMCH”), an affiliate of MSBNA, on [March 8, 2024], and both notes will be contributed to the BMO 2024-C8 securitization trust, along with the non-controlling Note A-3 in the original principal balance of $40,000,000, and represent approximately 9.5% of the Initial Pool Balance. The 60 Hudson Whole Loan is serviced pursuant to the pooling and servicing agreement for the MSWF 2023-2

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 22 | |

| Structural and Collateral Term Sheet | | BMO 2024-C8 |

| No. 2 – 60 Hudson |

securitization trust. See “Description of the Mortgage Pool— The Whole Loans—The Outside Serviced Pari Passu Whole Loans” in the Preliminary Prospectus and “The Pooling and Servicing Agreement—Servicing of the Outside Serviced Mortgage Loans” in the Preliminary Prospectus.

The table below identifies the promissory notes that comprise the 60 Hudson Whole Loan:

| Whole Loan Summary |

| Notes | Original Balance | Cut-off Date Balance | Note Holder | Controlling Piece |

| A-1 | $60,000,000 | $60,000,000 | MSWF 2023-2 | Yes |

| A-2(1) | $50,000,000 | $50,000,000 | MSBNA | No |

| A-3 | $40,000,000 | $40,000,000 | BMO 2024-C8 | No |

| A-4 | $30,000,000 | $30,000,000 | MSWF 2023-2 | No |

| A-5 | $30,000,000 | $30,000,000 | BBCMS 2023-C22 | No |

| A-6 | $20,000,000 | $20,000,000 | BMO 2024-C8 | No |

| A-7-1(1) | $20,000,000 | $20,000,000 | MSBNA | No |

| A-7-2 | $5,000,000 | $5,000,000 | BMO 2024-C8 | No |

| A-8 | $10,000,000 | $10,000,000 | BBCMS 2023-C22 | No |

| A-9 | $10,000,000 | $10,000,000 | BMO 2023-C7 | No |

| A-10 | $10,000,000 | $10,000,000 | BMO 2023-C7 | No |

| Whole Loan | $280,000,000 | $280,000,000 | | |

| (1) | Expected to be contributed to one or more future securitizations. |

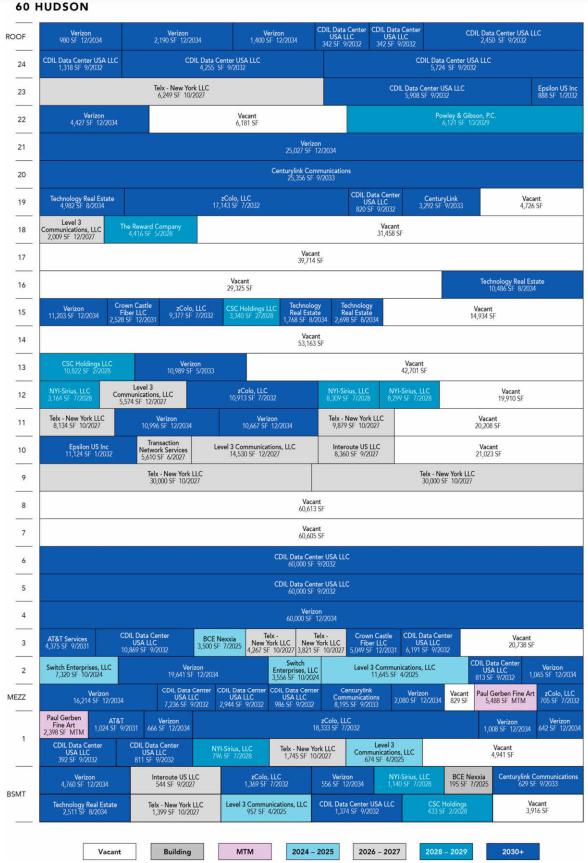

The Property. The 60 Hudson Property is a 24-story, plus basement, 1,149,619 square foot data center/carrier hotel building situated on an approximately 1.2-acre site located in New York, New York. The building spans an entire block between Hudson Street, West Broadway, Worth Street and Thomas Street. The 60 Hudson Property is one of the primary telecom and internet centers in New York City. Built in 1930 for the Western Union telegraph company, the building was initially known as the “Telegraph Capital of America”. After Western Union departed in 1973, the 60 Hudson Property was converted into a colocation center. Hundreds of telecommunication companies interconnect their respective internet networks, where telecommunications companies route internet traffic and exchange information in a “meet-me room” located at the 60 Hudson Property through fiber-optic lines. The 60 Hudson Property is widely considered a primary telecommunications hub of the Northeast region of the United States. The building provides an interconnection via under-sea cable to the United Kingdom, and to the cables from Manasquan, New Jersey, and Truckerton, New York, to the European Union.

The borrower sponsor most recently renovated the 60 Hudson Property in 2013. As of June 5, 2023, the 60 Hudson Property was 62.2% leased and anchored by major telecommunications and data center tenants, including Verizon, Hudson Interxchange (as defined below), Telx - New York LLC (Digital Realty), and zColo, LLC (DataBank). Approximately 9.5% of NRA consists of traditional office space. The 60 Hudson Property building was designated a historical landmark in 1992 by the New York City Landmarks Preservation Commission.

Major Tenants.

Verizon (184,420 square feet; 16.0% of NRA; 28.3% of underwritten base rent). Verizon (NYSE: VZ) is a leading provider of technology and communications services. Headquartered in New York City, and formed on June 30, 2000, the company offers voice, data and video services and solutions on its networks and platforms. Verizon has nearly 1,500 retail locations throughout over 150 countries and reported 2022 revenues of $136.8 billion. Verizon operates at the 60 Hudson Property under four separate affiliated entities; MCI Communication Services (157,952 square feet), Metropolitan Fibers Systems of NY (14,904 square feet), XO Communications Services (10,898 square feet) and Verizon New York Inc. (666 square feet). Verizon and these affiliated entities have been a tenant at the 60 Hudson Property since July 1984, September 1990, December 1997, and December 1986, respectively. With the exception of the XO Communications Services lease (10,898 square feet), Verizon and these affiliated leases recently executed extension notices for their leases, which will extend for 10 years through December 2034, with one, 10-year renewal option remaining with the exception of Verizon New York Inc. The XO Communications Services lease has an expiration date of May 31, 2033, with no renewal options remaining. Verizon has no termination options at the 60 Hudson Property.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 23 | |

| Structural and Collateral Term Sheet | | BMO 2024-C8 |

| No. 2 – 60 Hudson |

CDIL Data Centre USA LLC (“Hudson Interxchange”) (172,775 square feet; 15.0% of NRA; 22.1% of underwritten base rent). Hudson Interxchange (previously known as Datagryd) is a wholesale data center provider meeting the demands of high-power cloud computing and data storage clients by offering colocation space, power and cooling infrastructure for data network, telecommunications, cloud and large enterprises. Datagryd was acquired by Cordiant Digital Infrastructure in 2022 for $74.0 million and was rebranded to Hudson Interxchange. Hudson Interxchange has occupied the 60 Hudson Property since September 2011, has a lease expiration date of September 30, 2032 and has three, five-year renewal options remaining. Hudson Interxchange has no termination options at the 60 Hudson Property.

Telx – New York LLC (Digital Realty) (“Telx”) (95,494 square feet; 8.3% of NRA; 12.9% of underwritten base rent). Telx is a provider of data center colocation, interconnection, and cloud enablement solutions. Telx was acquired by Digital Realty Trust, Inc. in 2015 for $1.9 billion. Digital Realty Trust, Inc. operates as a real estate investment trust and is a large global provider of cloud- and carrier-neutral data center, colocation, and interconnection solutions. As of December 31, 2022, Digital Realty Trust Inc.’s portfolio consisted of 316 specialty industrial properties located in North America, Europe, South America, Africa, Australia and Asia. Telx has been a tenant at the 60 Hudson Property since June 1997, has a lease expiration date of October 31, 2027 and has one, five-year renewal option remaining. Telx has no termination options at the 60 Hudson Property.

zColo, LLC (DataBank) (“DataBank”) (57,840 square feet; 5.0% of NRA; 10.6% of underwritten base rent). DataBank acquired the data center assets of Zayo Group (zColo LLC) in December 2020 for approximately $1.4 billion, expanding DataBank’s footprint to over 65 data centers in over 29 markets and creating one of the largest privately held data center operators in North America. DataBank’s data centers are located in markets across the United States, and include major carrier interconnects in markets such as New York, Los Angeles, Seattle, Denver, Chicago, Minneapolis, Boston, Philadelphia, and Miami. DataBank has been a tenant at the 60 Hudson Property since April 1995, has a lease expiration date of July 31, 2032 and has one, 10-year renewal option remaining. Databank has no termination options at the 60 Hudson Property.

Appraisal. According to the appraisal, the 60 Hudson Property had an “as-is” appraised value of $1,596,000,000 as of May 8, 2023. The table below shows the appraiser’s “as-is” conclusions.

| Appraisal Valuation Summary(1) |

| Appraisal Approach | Appraised Value | Capitalization Rate(2) |

| Income Capitalization Approach | $1,596,000,000 | 4.50% |

| (2) | The appraiser used a discounted cash flow approach to arrive at the appraised value. The capitalization rate shown above represents the overall capitalization rate. |

Environmental. According to the Phase I environmental report dated May 11, 2023, there are no recognized environmental conditions at the 60 Hudson Property.

The following table presents certain information relating to the historical occupancy of the 60 Hudson Property:

| Historical and Current Occupancy(1) |

| 2020 | 2021 | 2022 | Current(2) |

| 72.6% | 64.1% | 63.2% | 62.2% |

| (1) | Historical Occupancies are as of December 31 of each respective year. |

| (2) | Current Occupancy is as of June 5, 2023. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 24 | |

| Structural and Collateral Term Sheet | | BMO 2024-C8 |

| No. 2 – 60 Hudson |

| Top Tenant Summary(1) |

| Tenant | Ratings

Moody’s/S&P/ Fitch(2) | Net Rentable Area (SF) | % of

Total NRA | UW Base Rent PSF(3)(4) | UW Base Rent(3)(4) | % of Total

UW Base Rent(3)(4) | Lease

Exp. Date | Renewal Options |

| Verizon(3) | Baa1/BBB+/A- | 184,420 | 16.0% | | $125.96 | $23,229,241 | 28.3% | | Various(3) | Various(3) |

| Hudson Interxchange | NR/NR/NR | 172,775 | 15.0% | | $104.95 | $18,132,737 | 22.1% | | 9/30/2032 | 3, 5-year |

| Telx | Baa2/BBB/BBB | 95,494 | 8.3% | | $111.26 | $10,624,472 | 12.9% | | 10/31/2027 | 1, 5-year |

| DataBank | NR/NR/NR | 57,840 | 5.0% | | $150.18 | $8,686,211 | 10.6% | | 7/31/2032 | 1, 10-year |

| Centurylink Communications | Caa3/CCC+/CCC+ | 37,472 | 3.3% | | $101.29 | $3,795,715 | 4.6% | | 9/30/2033 | 1, 10-year |

| Level 3 Communications, LLC | NR/NR/NR | 35,389 | 3.1% | | $119.59 | $4,232,080 | 5.2% | | Various(5) | 1, 10-year |

| NYI-Sirius, LLC | NR/NR/NR | 21,708 | 1.9% | | $115.42 | $2,505,625 | 3.0% | | 7/31/2028(6) | 1, 10-year |

| Major Tenants | | 605,098 | 52.6% | | $117.68 | $71,206,081 | 86.7% | | | |

| Other Tenants | | 109,536 | 9.5% | | $99.99 | $10,952,927 | 13.3% | | | |

| Occupied Collateral Total | 714,634 | 62.2% | | $114.97 | $82,159,008 | 100.0% | | | |

| Vacant Space(7) | | 434,985 | 37.8% | | | | | | |

| Collateral Total | | 1,149,619 | 100.0% | | | | | | |

| | | | | | | | |

| (1) | Based on underwritten rent roll dated June 5, 2023. |

| (2) | Ratings provided are for the parent company of the entity listed in the “Tenant” field whether or not the parent company guarantees the lease. |

| (3) | Includes Verizon affiliated leases under MCI Communication Services (157,952 square feet), Metropolitan Fiber Systems of NY (14,904 square feet), XO Communications Services (10,898 square feet) and Verizon New York Inc. (666 square feet). With the exception of the XO Communications Services lease, Verizon and its affiliated leases recently executed extension notices for their leases, which extends the leases through December 31, 2034. The XO Communications Services lease has a lease expiration date of May 31, 2033. With the exception of the Verizon New York Inc. and XO Communications Services leases, Verizon’s affiliated leases have one, 10-year renewal option remaining. |

| (4) | UW Base Rent, UW Base Rent PSF and % of Total UW Base Rent includes rent steps totaling $3,076,879 through September 2024. |

| (5) | Level 3 Communications, LLC has 22,113 square feet with an expiration date of December 31, 2027 and 13,276 square feet with an expiration date of April 30, 2025. Additionally, the landlord and tenant each had the right and option to terminate the lease with respect to the 12th floor premises as of December 31, 2024 upon delivery of written notice to the other no less than 12 months, and no more than 15 months, prior to December 31, 2024. |

| (6) | NYI-Sirius, LLC has the option to terminate its lease with respect to the Suite 1213 premises (8,309 square feet) upon 12 months’ prior written notice to the landlord, together with the payment of $100,000. |

| (7) | Vacant Space includes one in-place tenant, Stadium Goods (13,828 square feet) which was underwritten as vacant due to its lease expiring in October 2023. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. |

| | 25 | |

| Structural and Collateral Term Sheet | | BMO 2024-C8 |

| No. 2 – 60 Hudson |