QuickLinks -- Click here to rapidly navigate through this documentExhibit 99.5

ANNUAL INFORMATION FORM

FOR THE YEAR ENDED DECEMBER 31, 2005

March 13, 2006

TABLE OF CONTENTS

| | Page

|

|---|

| FORWARD-LOOKING STATEMENTS | | 1 |

NOTE REGARDING RESERVES DATA AND OTHER OIL AND GAS INFORMATION |

|

2 |

EXCHANGE RATE INFORMATION |

|

3 |

DEFINITIONS |

|

3 |

CORPORATE STRUCTURE |

|

4 |

GENERAL DEVELOPMENT OF THE BUSINESS |

|

4 |

| | North America | | 4 |

| | International and Frontier | | 5 |

DESCRIPTION OF THE BUSINESS |

|

6 |

| | North America | | 6 |

| | | Canada | | 7 |

| | | United States | | 10 |

| | | Landholdings, Production and Productive Wells | | 10 |

| | International and Frontier | | 11 |

| | | North Sea | | 11 |

| | | Southeast Asia and Australia | | 17 |

| | | North Africa | | 21 |

| | | Trinidad and Tobago | | 23 |

| | | Colombia | | 24 |

| | | Peru | | 24 |

| | | Qatar | | 25 |

| | | Alaska | | 25 |

| | | Other | | 25 |

| | Productive Wells and Acreage | | 26 |

| | Drilling Activity | | 27 |

| | Reserves Estimates | | 30 |

| | Other Oil and Gas Information | | 32 |

| | | Continuity of Net Proved Reserves | | 32 |

| | | Standardized Measure of Discounted Future Net Cash Flows From Proved Reserves | | 34 |

| | | Results of Operations from Oil and Gas Producing Activities | | 37 |

| | | Capitalized Costs Relating to Oil and Gas Activities | | 38 |

| | | Costs Incurred in Oil and Gas Activities | | 39 |

| | | Product Netbacks (Net) | | 40 |

| | Supplemental Oil and Gas Information | | 42 |

| | | Continuity of Gross Proved Reserves | | 42 |

| | | Product Netbacks (Gross) | | 44 |

| | Additional Information | | 46 |

| | Competitive Conditions | | 46 |

| | Social Responsibility and Environmental Protection | | 46 |

| | Employees | | 47 |

DESCRIPTION OF CAPITAL STRUCTURE |

|

47 |

| | Share Capital | | 47 |

| | Ratings | | 47 |

MARKET FOR THE SECURITIES OF THE COMPANY |

|

48 |

| | Trading Price and Volume | | 48 |

DIVIDENDS |

|

49 |

PRIOR SALES OF DEBT SECURITIES |

|

49 |

DIRECTORS AND OFFICERS |

|

49 |

| | Directors | | 49 |

| | Officers | | 52 |

| | Shareholdings of Directors and Executive Officers | | 52 |

| | Conflicts of Interest | | 53 |

AUDIT COMMITTEE INFORMATION |

|

53 |

LEGAL PROCEEDINGS |

|

53 |

RISK FACTORS |

|

53 |

TRANSFER AGENTS AND REGISTRARS |

|

56 |

INTERESTS OF EXPERTS |

|

56 |

ADDITIONAL INFORMATION |

|

56 |

SCHEDULE A – REPORT ON RESERVES DATA BY TALISMAN'S INTERNAL QUALIFIED RESERVES EVALUATOR |

|

57 |

SCHEDULE B – REPORT OF MANAGEMENT AND DIRECTORS ON OIL AND GAS DISCLOSURE |

|

58 |

SCHEDULE C – AUDIT COMMITTEE INFORMATION |

|

60 |

Unless the context indicates otherwise, a reference in this Annual Information Form to "Talisman" or the "Company" includes direct or indirect subsidiaries of Talisman Energy Inc. and partnership interests held by Talisman Energy Inc. and its subsidiaries. Consolidated information as at December 31, 2005 includes Paladin Resources Limited (formerly Paladin Resources plc) and its subsidiaries.

FORWARD-LOOKING STATEMENTS

This Annual Information Form contains or incorporates by reference statements that constitute forward-looking statements or forward-looking information (collectively "forward-looking statements") within the meaning of applicable securities legislation.

Forward-looking statements are included throughout this Annual Information Form including, among other places, under the headings "General Development of the Business", "Description of the Business", "Directors and Officers", "Legal Proceedings" and "Risk Factors". These statements include, among others, statements regarding:

- •

- business strategy and plans or budgets;

- •

- business plans for drilling, exploration and development;

- •

- the estimated amounts and timing of capital expenditures;

- •

- the estimated timing of development, including new production;

- •

- the anticipated schedule for commissioning of pipelines;

- •

- royalty rates and exchange rates;

- •

- planned asset dispositions and acquisitions and their timing;

- •

- the merits and timing or anticipated outcome of pending litigation; and

- •

- other expectations, beliefs, plans, goals, objectives, assumptions, information and statements about possible future events, conditions, results of operations or performance.

Statements concerning oil and gas reserves contained in this Annual Information Form under the headings "Description of the Business – Reserves Estimates" and elsewhere may be deemed to be forward-looking statements as they involve the implied assessment that the resources described can be profitably produced in the future, based on certain estimates and assumptions. Often, but not always, forward-looking statements use words or phrases such as: "expects", "does not expect" or "is expected", "anticipates" or "does not anticipate", "plans" or "planned", "estimates" or "estimated", "projects" or "projected", "forecasts" or "forecasted", "believes", "intends", "likely", "possible", "probable", "scheduled", "positioned", "goals" or "objectives", or state that certain actions, events or results "may", "could", "would", "might" or "will" be taken, occur or be achieved.

Various assumptions were used in drawing the conclusions or making the forecasts and projections contained in the forward-looking statements throughout this Annual Information Form. In particular, statements which discuss business plans for drilling, exploration and development in 2006 assume that the extraction of crude oil, natural gas and natural gas liquids remains economic. For the purposes of preparing this Annual Information Form, Talisman assumed a US$57/bbl West Texas Intermediate oil price, a US$9.00/mmbtu New York Mercantile Exchange natural gas price, a Canadian$/US$ exchange rate of 0.84 and a British £/Canadian$ exchange rate of 2.10.

Undue reliance should not be placed on forward-looking statements. Forward-looking statements are based on current expectations, estimates and projections that involve a number of risks and uncertainties, which could cause actual results to differ materially from those anticipated by Talisman and described in the forward-looking statements. These risks and uncertainties include:

- •

- the risks of the oil and gas industry, such as operational risks in exploring for, developing and producing crude oil and natural gas and market demand;

- •

- risks and uncertainties involving geology of oil and gas deposits;

- •

- the uncertainty of reserves estimates and reserves life;

- •

- the uncertainty of estimates and projections relating to production, costs and expenses;

- •

- potential delays or changes in plans with respect to exploration or development projects or capital expenditures;

- •

- fluctuations in oil and gas prices, foreign currency exchange rates and interest rates;

- •

- the outcome and effects of completed acquisitions, as well as any future acquisitions and dispositions;

A N N U A L I N F O R M A T I O N F O R M1

- •

- the ability of the Company to integrate assets it has acquired or may acquire or the performance of those assets;

- •

- health, safety and environmental risks;

- •

- uncertainties as to the availability and cost of financing and changes in capital markets;

- •

- uncertainties related to the litigation process, such as possible discovery of new evidence or acceptance of novel legal theories and the difficulties in predicting the decisions of judges and juries;

- •

- risks in conducting foreign operations (for example, political and fiscal instability or the possibility of civil unrest or military action);

- •

- competitive actions of other companies, including increased competition from other oil and gas companies or companies providing alternative sources of energy;

- •

- changes to general economic and business conditions;

- •

- the effect of acts of, or actions against, international terrorism;

- •

- the possibility that government policies or laws may change or governmental approvals may be delayed or withheld;

- •

- results of the Company's risk mitigation strategies, including insurance and any hedging programs; and

- •

- the Company's ability to implement its business strategy.

Readers are cautioned that the foregoing list of risks and uncertainties is not exhaustive. Additional information on these and other factors which could affect the Company's operations or financial results is included under the heading "Risk Factors", in the Report on Reserves Data by Talisman's Internal Qualified Reserves Evaluator and the Report of Management and Directors on Oil and Gas Disclosure, (which reports are attached as schedules to this Annual Information Form), and elsewhere in this Annual Information Form. Additional information may also be found in the Company's other reports on file with Canadian securities regulatory authorities and the United States Securities and Exchange Commission (the "SEC").

Forward-looking statements are based on the estimates and opinions of the Company's management at the time the statements are made. The Company assumes no obligation to update forward-looking statements should circumstances or management's estimates or opinions change.

NOTE REGARDING RESERVES DATA AND OTHER OIL AND GAS INFORMATION

National Instrument 51-101 ("NI 51-101") of the Canadian Securities Administrators imposes oil and gas disclosure standards for Canadian public companies engaged in oil and gas activities. NI 51-101 and its companion policy specifically contemplate the granting of exemptions from some of the disclosure standards prescribed by NI 51-101 to companies that are active in the United States ("US") capital markets to permit the substitution of the disclosures required by the SEC rules in order to provide for comparability of oil and gas disclosure with that provided by US and other international issuers. Talisman has obtained an exemption from Canadian securities regulatory authorities to permit it to provide disclosure in accordance with the relevant US requirements. Accordingly, most of the reserves data and other oil and gas information included in this Annual Information Form is disclosed in accordance with US disclosure requirements. Such information, as well as the information that Talisman discloses in the future in reliance on the exemption, may differ from the corresponding information prepared in accordance with NI 51-101 standards.

The primary differences between the US requirements and the NI 51-101 requirements are that (i) SEC rules normally permit disclosure only of proved reserves, whereas NI 51-101 requires disclosure of proved and probable reserves, and (ii) SEC rules require that the reserves and future net revenue be estimated under existing economic and operating conditions, whereas NI 51-101 requires disclosure of proved reserves and the associated future net revenue on a constant basis, and of proved, probable and proved plus probable reserves and the associated future net revenue on a forecast basis. The definitions of proved reserves differ, but Talisman does not believe that the differences in the definitions would result in any material difference in its reserves estimates for that category. The Canadian Oil and Gas Evaluation Handbook ("COGEH", the reference source for the definition of proved reserves under NI 51-101) states that the differences in the estimated proved reserves quantities based on constant prices should not be material.

Talisman has disclosed proved reserves (including continuity of reserves) using the standards contained in US Regulation S-X and the standardized measure of discounted future net cash flows from proved reserves determined in accordance with Statement No. 69 of the US Financial Accounting Standards Board ("FAS 69"). US practice is to disclose net proved reserves, after deduction of estimated royalty burdens and including net profit interests. In addition, notwithstanding that Talisman is not required to disclose probable reserves, it has done so using the definition for probable reserves set out by the Society of Petroleum Engineers/World Petroleum Congress ("SPE/WPC"). Talisman does not believe that the differences in the SPE/WPC and NI 51-101 definitions of probable reserves would result in any material difference in its estimates of probable reserves disclosed in this Annual Information Form.

2 A N N U A L I N F O R M A T I O N F O R M

EXCHANGE RATE INFORMATION

Except where otherwise indicated, all dollar amounts in this Annual Information Form are stated in Canadian dollars. The following table sets forth the US/Canada exchange rates on the last trading day of the years indicated as well as the high, low and average rates for such years. The high, low and average exchange rates for each year were identified or calculated from spot rates in effect on each trading day during the relevant year. The exchange rates shown are expressed as the number of US dollars required to purchase one Canadian dollar. These exchange rates are based on those published on the Bank of Canada's website as being in effect at approximately noon on each trading day (the "Bank of Canada noon rate").

| | Year ended December 31

|

|---|

| | 2005

| | 2004

| | 2003

|

|---|

|

|---|

| Year end | | 0.8577 | | 0.8308 | | 0.7738 |

| High | | 0.8690 | | 0.8493 | | 0.7738 |

| Low | | 0.7872 | | 0.7159 | | 0.6350 |

| Average | | 0.8258 | | 0.7697 | | 0.7156 |

|

DEFINITIONS

The abbreviations set forth below have the following meanings:

| | bbls | | barrels |

| | bcf | | billion cubic feet |

| | boe | | barrels of oil equivalent |

| | bbls/d | | barrels per day |

| | mbbls/d | | thousand barrels per day |

| | mcf | | thousand cubic feet |

| | mmbbls | | million barrels |

| | mmbtu | | million British Thermal Units |

| | mmcf/d | | million cubic feet per day |

| | liquids or NGLs | | natural gas liquids |

Natural gas is converted to oil equivalent at the ratio of 6 mcf to 1 boe. The boe measure may be misleading, particularly if used in isolation. A boe conversion ratio of 6 mcf:1 bbl is based on an energy equivalence conversion method primarily applicable at the burner tip and does not represent a value equivalence at the wellhead.

Gross acres means the total number of acres in which Talisman has a working interest. Net acres means the sum of the fractional working interests owned in gross acres expressed as whole numbers and fractions thereof.

Gross production means Talisman's interest in production volumes (through working interests, royalty interests and net profits interests) before the deduction of royalties. Net production means Talisman's interest in production volumes after deduction of royalties payable by Talisman.

Gross wells means the total number of wells in which Talisman owns a working interest. Net wells means the sum of the fractional working interests owned in gross wells expressed as whole numbers and fractions thereof.

A N N U A L I N F O R M A T I O N F O R M3

CORPORATE STRUCTURE

Talisman Energy Inc. is incorporated under theCanada Business Corporations Act. The Company's registered and principal office is located at Suite 3400, 888 Third Street S.W., Calgary, Alberta T2P 5C5.

The following table sets forth the material operating subsidiaries owned directly or indirectly by Talisman, their jurisdictions of incorporation and the percentage of voting securities beneficially owned, controlled or directed by Talisman as at December 31, 2005.

Name of Subsidiary

| | Jurisdiction of

Incorporation

| | Percentage of Voting Securities Owned1

|

|---|

|

|---|

| Talisman Energy (UK) Limited1 | | England and Wales | | 100% |

| Talisman North Sea Limited | | England and Wales | | 100% |

| Talisman (Corridor) Ltd. | | Barbados | | 100% |

| Petromet Resources Limited | | Ontario, Canada | | 100% |

| Fortuna Energy Inc. | | Delaware, US | | 100% |

| Talisman Malaysia Limited | | Barbados | | 100% |

| Talisman Expro Limited2 | | England and Wales | | 100% |

| Talisman Resources (Norway) Limited2 | | England and Wales | | 100% |

|

Notes:

- 1

- With the exception of Talisman Energy (UK) Limited, none of the above subsidiaries has any non-voting securities outstanding. All of the non-voting securities of Talisman Energy (UK) Limited are directly or indirectly held by Talisman.

- 2

- Talisman Expro Limited and Talisman Resources (Norway) Limited are indirect subsidiaries acquired through the acquisition of Paladin Resources plc. See "General Development of the Business".

The above table does not include all of the subsidiaries of Talisman. The assets, sales and operating revenues of unnamed operating subsidiaries individually did not exceed 10%, and in the aggregate did not exceed 20%, of the total consolidated assets or total consolidated sales and operating revenues, respectively, of Talisman as at, and for the year ended, December 31, 2005.

Talisman Energy Inc. and Petromet Resources Limited ("Petromet"), an indirect subsidiary of Talisman, are partners in an Alberta general partnership named Talisman Energy Canada (the "Partnership"). Talisman is the managing partner of the Partnership. Substantially all of Talisman's Canadian oil and gas operations are carried on through the Partnership.

GENERAL DEVELOPMENT OF THE BUSINESS

Talisman is an independent, Canadian based, international upstream oil and gas company whose main business activities include exploration, development, production, transportation and marketing of crude oil, natural gas and natural gas liquids. The Company's reporting segments are North America, the North Sea, Southeast Asia and Australia, North Africa and Trinidad and Tobago, where there are ongoing production, development and exploration activities. The Company is active in a number of other international and frontier areas, including Alaska, Colombia, Gabon, Peru, Qatar and Romania.

During the past three years, Talisman has developed its business and diversified its interests through a combination of exploration, development, acquisitions and dispositions as described below. Internationally, the Company's exploration strategy is to pursue significant high impact opportunities to grow production and create shareholder value.

NORTH AMERICA

In January 2003, an indirect subsidiary of the Company acquired natural gas properties, working interests, production and facilities in New York State. The same subsidiary subsequently acquired all of Belden & Blake Corporation's Trenton-Black River assets in New York, Pennsylvania, Ohio and West Virginia in June 2004 resulting in ownership of approximately 433,000 additional gross acres. The June 2004 acquisition effectively doubled the subsidiary's existing net acreage held in the area. The indirect subsidiary of the Company currently owns approximately 978,000 gross acres.

In July 2003, a subsidiary of Talisman acquired various midstream assets in the Deep Basin area of northwestern Alberta through the purchase of Vista Midstream Solutions Ltd.

In March 2005, the Partnership and a Talisman subsidiary collectively acquired the securities of a partnership now known as Talisman Findley Partnership, which increased the working interests in sixty-three wells in the Alberta Foothills on average from 15% to 57% and added approximately 128,000 gross undeveloped acres in the northern portion of the Alberta Foothills.

4 A N N U A L I N F O R M A T I O N F O R M

INTERNATIONAL AND FRONTIER

In March 2003, Talisman completed the sale of its indirect interest in the Greater Nile Oil Project in Sudan to ONGC Videsh Limited, a subsidiary of India's national oil company. An indirect subsidiary of Talisman had held a 25% interest in the Greater Nile Oil Project, which had been acquired in 1998.

In 2003, first oil sales began from the Ourhoud field (Talisman 2%) in Algeria. In June 2003, production commenced from the Greater MLN field (Talisman 35%).

In 2003, the Company completed the PM-3 Commercial Arrangement Area ("PM-3 CAA") Phase 2/3 Development Project offshore Malaysia/Vietnam. Oil production from this project began in September 2003 and gas production and sales commenced in November 2003. Talisman Malaysia Limited signed a production sharing contract in March 2004 for Block PM-314 offshore Malaysia.

In December 2003, Talisman's subsidiary acquired additional interests in the Ross, Renee and Rubie fields in the United Kingdom sector of the North Sea ("UK North Sea"). In early 2004, a Talisman subsidiary acquired an operated interest in the Galley field in the UK North Sea. In May 2004, Talisman's subsidiaries acquired additional interests in the Flotta Catchment Area. In a separate transaction completed in November 2004 the subsidiary acquired additional interests in the Buchan area and also reduced its interest in the MacCulloch field. In 2005, the Company acquired minor additional interests in non-operated assets in the UK North Sea.

In September 2003, one of Talisman's subsidiaries acquired the operated interests and associated assets of BP Norge AS in the Gyda field in the Norwegian sector of the North Sea (the "Norwegian North Sea"). Two additional licenses were awarded later in 2003. In February 2004, Talisman's subsidiary acquired an interest from ConocoPhillips Skandinavia AS in two more licences, including the Blane discovery. In December 2004, the subsidiary was awarded interests in five more licences in the Norwegian North Sea.

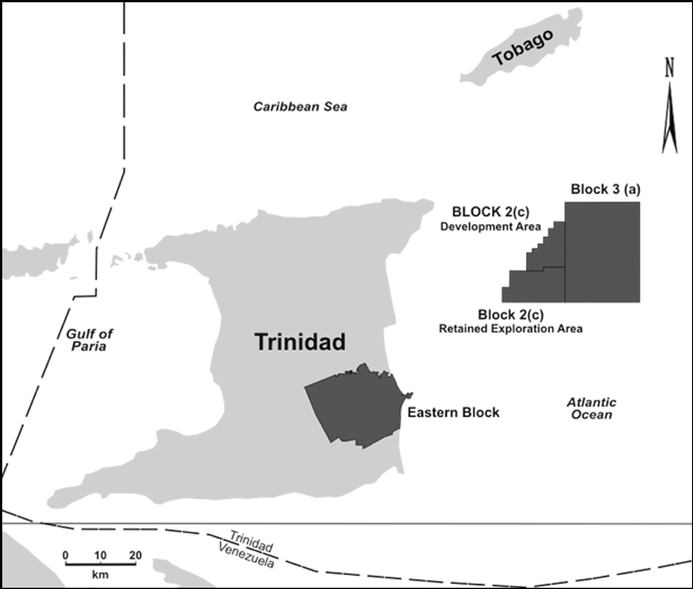

In 2003, the Company began the Angostura development project in Trinidad and Tobago on offshore Block 2(c). Development continued through 2004 with production beginning in January 2005. Plans to develop gas on Block 2(c) are underway. Exploration is continuing in the onshore Eastern Block and in the offshore Howler assessment area and Block 3(a).

Talisman announced in August 2004 an agreement for the sale of 2.3 trillion cubic feet of natural gas from the Corridor production sharing contract in Indonesia. Talisman's subsidiary has a 36% interest in the production sharing contract.

In the fourth quarter of 2004, Talisman Energy (UK) Limited acquired all of the outstanding shares of Intrepid Energy Beta Limited, which included an interest in a number of exploration licenses in the United Kingdom, Netherlands and German sectors of the North Sea.

Through separate transactions occurring in 2004 and 2005, a subsidiary of Talisman acquired interests in over 450,000 gross acres of land in the North Slope of Alaska.

In February 2005, Talisman Energy (UK) Limited acquired all of the outstanding shares in Pertra AS ("Pertra"), now Talisman Production Norge AS, resulting in the addition of producing and undeveloped fields in the Varg area, as well as several blocks of operated and non-operated exploration acreage in the Norwegian North Sea.

In April 2005, Talisman Vietnam 15-2/01 Ltd., a Talisman subsidiary, signed a petroleum contract for Block 15-2/01 offshore Vietnam. The subsidiary holds a 60% interest in the Block, which is comprised of 700,000 acres offshore Vietnam.

In June 2005, a Talisman subsidiary acquired a non-operated interest in the producing Brage and Sognefjord fields in the Norwegian North Sea.

Also in June 2005, a Talisman subsidiary was granted additional acreage along the south-eastern border of Block PM-3 CAA offshore Malaysia/Vietnam. In August 2005, oil production commenced from the South Angsi field in Block PM-305 offshore Malaysia.

On October 20, 2005, Talisman reached an agreement with Paladin Resources plc (now Paladin Resources Limited and referred to as "Paladin"), a public United Kingdom based oil and gas exploration and production company, on the terms of a cash offer by a wholly owned subsidiary of Talisman, for all of the shares of Paladin at an aggregate price of approximately £1,218 million. On November 18, 2005, Talisman effectively acquired control of Paladin pursuant to the offer, and subsequently acquired all remaining shares of Paladin. The acquisition of Paladin continues Talisman's North Sea strategy and provides the Company with additional international opportunities that management believes are well suited to Talisman's operating style and skills. Paladin's portfolio of production and exploration assets (predominantly located in the Norwegian, United Kingdom and Danish sectors of the North Sea, as well as Australia, Indonesia and Tunisia) are integrated under the heading "Description of Business."

Talisman announced in December 2005 that it intends to dispose of approximately 10,000 to 15,000 boe/d of production from non-core assets in Western Canada and the North Sea by mid-2006. Third party advisors have been engaged to further discussions with potential purchasers of these assets.

A N N U A L I N F O R M A T I O N F O R M5

In February 2006, Talisman reached an agreement to enter into exclusive negotiations to acquire approximately an 86% interest in the Fulmar field and a 100% interest in the Auk field, both located in the Central North Sea. The completion of this transaction is subject to agreement of final terms and receipt of co-venturer and government approvals.

Since 2002, Talisman, through various subsidiaries, has acquired non-operated interests in several blocks of exploration acreage in the Andean fold and thrust belts of Colombia and Peru. In 2005, the Company continued its ongoing exploration program on this acreage. Subsequent to year end, Talisman announced that its subsidiary had participated in an oil discovery in Block 64 in the Marañon Basin in Peru. The Company is currently evaluating options in Peru, including additional drilling.

In February 2006, a subsidiary of the Company concluded a joint venture agreement for various interests in Alaska. The Company was also advised in March 2006 that its bid for an additional 119,680 acres in the Smith Bay Area of Alaska had been successful, subject to government approval.

Talisman continually investigates strategic acquisitions, dispositions and other business opportunities, some of which may be material. In connection with any such transaction, the Company may incur debt or issue equity securities.

DESCRIPTION OF THE BUSINESS

Talisman is one of the largest independent oil and gas producers in Canada. The Company's main business activities include exploration, development, production, transportation and marketing of crude oil, natural gas and natural gas liquids. Each of Talisman's current areas of operations has exploration and development potential, which Talisman expects will provide future growth.

All information in this section relating to assets owned or held by Talisman is as of December 31, 2005, unless otherwise indicated. Activity for 2005 includes activity of Paladin and its subsidiaries only from the date of acquisition (November 18, 2005).

NORTH AMERICA

Talisman anticipates that it will spend approximately $2.0 billion on exploration and development in Canada and the US in 2006. (Exploration in Alaska is not currently managed through the North America management group and therefore does not form part of these expenditures.) Of this, over 92% is expected to be directed towards development of natural gas opportunities. The Company plans to participate in drilling approximately 685 gross wells in 2006.

In the past three years, the Company's production growth has been achieved mainly through drilling activities. The Company intends to dispose of approximately 10,000 to 15,000 boe/d of production from non-core assets in Western Canada and the North Sea by mid-2006. Additional strategic asset acquisitions and dispositions will be evaluated throughout the year.

6 A N N U A L I N F O R M A T I O N F O R M

CANADA

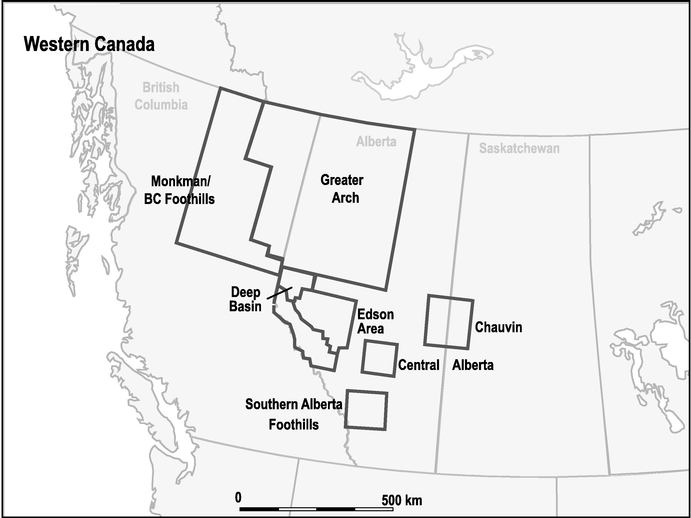

In Canada, the Company's strategy is to continue oil and natural gas exploration and development by exploring a diverse range of opportunities that capitalize on previous successes in several deep gas plays throughout the Western Canada Sedimentary Basin ("WCSB"). Talisman expects to spend a significant portion (20%) of its 2006 capital program on higher-risk/higher-reward technical thrust belt plays (Monkman and Alberta Foothills) and 32% on multi-zoned scalable plays (Bigstone/Wild River, Edson and West Whitecourt). Talisman anticipates that utilization of existing infrastructure and a high level of operatorship will continue to enable Talisman to maintain control over costs, production and capital spending.

Exploration and development activities will focus on medium to deep gas opportunities in the WCSB to take advantage of Talisman's expertise in these areas. The majority of this activity is expected to be in the Edson area, Alberta Foothills, Greater Arch, Monkman/BC Foothills, Deep Basin and Southern Alberta Foothills. Talisman employs a "total rock volume" approach which the Company believes can add substantially to the overall reserves and production life, and to a lesser extent, increase well productivity to complement existing conventional plays. A multi-disciplinary team has been set up with a mandate to identify new conventional and unconventional plays in the WCSB.

Talisman's Canadian exploration and development operations are organized around 13 core producing areas in Alberta, British Columbia, Ontario and Saskatchewan, which accounted for 93% of the Company's Canadian production in 2005. The balance comprises production from joint venture properties and synthetic oil production from Talisman's 1.25% indirect interest in the Syncrude joint venture. Of the 13 core areas the following seven are the principal gas production areas: Edson area (in turn comprised of Bigstone/Wild River, Edson and West Whitecourt), Alberta Foothills, Greater Arch, Monkman/BC Foothills, Deep Basin, Lac La Biche and Ontario offshore. The following seven core areas are the principal oil production areas: Chauvin, Carlyle, Greater Arch, Shaunavon, Southern Alberta Foothills, Ontario onshore and Central Alberta. Within its core areas, Talisman operates approximately 80% of its production with high working interests in a large number of facilities.

Seven of the more active core areas accounted for approximately 79% of the Company's total Canadian production in 2005: Alberta Foothills, Edson area, Greater Arch, Deep Basin, Monkman/BC Foothills, Southern Alberta Foothills and Chauvin. Each of these areas is described in greater detail below.

A N N U A L I N F O R M A T I O N F O R M7

Alberta Foothills

Alberta Foothills is Talisman's largest natural gas producing area. Major operated facilities in the Alberta Foothills area include an 80% interest in the Cordel dehydration facility and associated pipelines, interests ranging from 62% to 100% in the Erith pipeline and related facilities, a 58% interest in the Lovett River/Redcap pipeline system and a 39% interest in the Chungo/Bighorn gas gathering system. Talisman has non-operated interests in Basing, Voyager, Stolberg and Brown Creek pipelines and associated facilities. Talisman currently has over 50 mmcf/d sales gas (Company share) awaiting completion of infrastructure in the northern portion of the Alberta Foothills. Two major Midstream pipeline projects, Lynx and Palliser, are expected to be commissioned in 2006. Construction started in mid October 2005 on the 72 kilometre Lynx Pipeline (Talisman 45%), which will gather up to 130 mmcf/d of sour gas from the Greater Grande Cache area. In the Palliser area, construction is underway on a 45 mmcf/d pipeline system (Talisman 100%), which will deliver gas into the Duke Grizzly system. The Company expects that capital spending in 2006 in the Alberta Foothills area will be approximately $306 million. Of this amount, approximately $105 million will be spent on infrastructure and participation in drilling 35 wells. The northern portion of the Alberta Foothills accounts for sixty percent of the expected capital spending and two-thirds of the wells expected to be drilled.

Edson Area

The properties comprising the larger Edson area (Bigstone/Wild River, Edson and West Whitecourt) are detailed below. Capital spending in the Edson area in 2006 is expected to be approximately $644 million, which includes plans to participate in drilling 249 wells and includes approximately $102 million for infrastructure.

Bigstone/Wild River

Talisman holds operated interests ranging from 64% to 100% in the Bigstone West and Wild River gas plants. The Company is continuing to focus on infill drilling in the Wild River area. The Company expects that capital spending in 2006 in the Bigstone/Wild River area will be approximately $278 million and plans to participate in drilling 99 wells, 86% of which will be drilled in the Wild River area.

Edson

Talisman holds operated interests ranging from 59% to 100% in the Edson and Medicine Lodge gas plants and a 100% interest in the Edson plant cogeneration facility. Talisman is currently focusing on exploring and exploiting opportunities identified in 2005 in the Edson core area. The Company expects that capital spending in 2006 in the Edson core area will be approximately $274 million and plans to participate in drilling 95 wells.

West Whitecourt

Talisman holds a 51% operated interest in the McLeod River gas plant as well as non-operated interests ranging from 10% to 12% in the Kaybob South Amalgamated and the West Whitecourt gas plants. Talisman is continuing to focus on development drilling in the West Whitecourt area. Additional compression and line looping are required to increase the gas production from the area. The Company expects that capital spending in 2006 in the West Whitecourt area will be approximately $92 million and plans to participate in drilling 55 wells.

Greater Arch

The Greater Arch is Talisman's second largest natural gas producing area. Talisman holds operated interests ranging from 42% to 100% in gas plants at Teepee Creek, Belloy, Boundary Lake, George and Josephine, as well as interests in a number of other non-operated gas plants in the area. The Company has a large inventory of opportunities to explore which are adjacent to existing infrastructure. Talisman's average operated interest in oil and gas properties in the Greater Arch area is 82%. The Company expects that capital spending in 2006 in the Greater Arch area will be approximately $168 million and plans to participate in drilling 84 wells.

Deep Basin

Talisman holds a 50% to 100% working interest in the Cutbank complex, consisting of the Cutbank and Musreau A and B gas plants, five major field compression stations and an extensive gas gathering system, all of which ran close to capacity throughout 2005. Talisman also holds 7% to 8% non-operated interests in the South Wapiti, Wapiti Deep Cut and Narraway gas plants. In November 2005, Talisman tied-in a successful gas well in this area which produced at a rate of up to 18 mmcf/d sales gas (Company share) at year end. The Company expects that capital spending in 2006 in the Deep Basin area will be approximately $161 million and plans to participate in drilling 34 wells along the prospective multi-zone exploration fairway.

Monkman/BC Foothills

In the Monkman/BC Foothills area, Talisman holds 55% to 77% operated interests in the Bullmoose, Sukunka and West Sukunka dehydration plants, 29% to 32% non-operated interests in the Murray River and Brazion dehydration plants and a 50% interest in the Mink Highhat Gathering System. In

8 A N N U A L I N F O R M A T I O N F O R M

2004, Talisman drilled the b-60-E/93-P-5 well ("b-60-E") in the Brazion area, which produced an average 39 mmcf/d sales gas (Company share) or 49 mmcf/d gross sales gas in 2005 and on March 7, 2005 it attained its maximum production of approximately 58 mmcf/d sales gas (Company share) or 72 mmcf/d gross sales gas. In the fourth quarter of 2005, Talisman tested two Triassic wells, which in combination, tested at 42 mmcf/d gross raw gas. Both wells are expected to be tied-in in 2006. The Company expects that capital spending in 2006 in the Monkman/BC Foothills area will be approximately $104 million and plans to participate in drilling seven wells, two of which are deep wells.

Southern Alberta Foothills

Talisman holds a 100% interest in the Little Chicago gas plant and 76% to 100% interests in the Turner Valley Units 3, 4, 5 and 7. In 2005, a successful multi-leg horizontal oil well drilling program in Turner Valley was completed. The three-year experimental nitrogen injection project is now complete. The Company expects that capital spending in 2006 in the Southern Alberta Foothills area will be approximately $74 million and plans to participate in drilling 17 wells.

Chauvin

Chauvin is Talisman's largest domestic oil producing property. Talisman also has a 100% interest in the Chauvin Custom Treating Facility. The Company expects that capital spending in 2006 in the Chauvin area will be approximately $40 million and plans to participate in drilling 49 wells.

Other

In Ontario, Talisman currently has natural gas production offshore Lake Erie and oil production onshore. Talisman has a 100% interest in the Renwick, North Wheatley (East), Rochester and Hillman central facilities. In addition, Talisman holds interests ranging from 65% to 100% in the Morpeth, Port Stanley, Port Alma, Port Maitland, Rochester and Nanticoke gas plants. The Company expects that capital spending in 2006 in Ontario will be approximately $17 million and plans to participate in drilling five onshore oil wells and 25 offshore gas wells.

In 2004, Talisman drilled a successful gas well in Central Alberta, which tested at 18 mmcf/d gross raw gas. Production from this well commenced at approximately 15 mmcf/d sales gas (Company share) in the first quarter of 2005 and averaged 14 mmcf/d sales gas (Company share) throughout 2005. Follow up drilling to this well has not been successful; however, evaluation of this play is still ongoing. The Company expects that capital spending in 2006 in the Central Alberta area will be approximately $10 million and plans to participate in drilling 11 wells.

The Company is exploring the potential for producing coal bed methane on existing lands in Alberta. Appraisal drilling and prospect evaluation commenced in 2002. The main focus in 2006 will continue to be the development of coal bed methane horizontal drilling and production technology to determine large-scale commercial viability within the Mannville formation. The Company expects that capital spending in 2006 in this area will be approximately $53 million and plans to participate in drilling 35 wells.

In Quebec, Talisman entered into two farm-in agreements and an option to purchase agreement in 2005 to gain access to approximately 900,000 gross acres. In the first farm-in agreement, Talisman has committed to drill a well in the first half of 2006 to earn an exploration permit of approximately 33,000 gross acres and the option to earn an interest in the remaining 153,000 gross acres. The second farm-in agreement requires Talisman to commence a 2D seismic program in the first quarter of 2006 for an opportunity to earn an interest in approximately 712,000 gross acres. The option to purchase agreement provides the opportunity to acquire a further interest in approximately 17,300 gross acres (a portion of the acreage included in the second farm-in agreement). The Company expects that capital spending in 2006 in Quebec will be approximately $6 million.

Talisman Midstream Operations

The Company's Midstream Operations operates over 769 kilometres of gathering pipelines, interconnected with multiple processing plants and downstream pipelines with an average throughput of approximately 420 mmcf/d in 2005. The Company's 100% owned Central Foothills Gas Gathering System, the Columbia Minehead Gas Gathering System, and other midstream pipeline and processing assets ranging from 50% to 100% ownership, support the exploration and development programs in the Alberta Foothills, Edson and Deep Basin areas and also provide transportation and processing revenues. The Company spent approximately $71 million in 2005 to expand and optimize midstream assets as well as initiate the development of the Lynx, Medlodge, and Palliser pipelines that will add approximately 130 kilometres of gathering system and connect the northern portion of Alberta Foothills gas to markets. Talisman expects that capital spending in 2006 will be approximately $123 million which includes plans to complete the Palliser and Lynx pipeline systems and to expand and optimize the remaining midstream systems in 2006.

Synthetic Oil

Talisman holds a 1.25% indirect interest in the Syncrude oil sands project (the "Syncrude Project") through the Canadian Oil Sands Limited Partnership. The Syncrude Project is a joint venture established to recover shallow deposits of tar sands using open pit mining methods in order to extract the crude bitumen and to upgrade it to a high-quality, light (32° API) sweet, synthetic crude oil. The upgrading process uses a combination of delayed coking and hydrotreating technologies to produce a synthetic crude oil that appropriately equipped refineries can use as a feedstock. The

A N N U A L I N F O R M A T I O N F O R M9

Syncrude Project, located near Fort McMurray, Alberta, exploits portions of the Athabasca oil sands deposit to produce Syncrude Sweet Blend®. Syncrude is in the final phases of the third stage of a large expansion program. Stage 3 is expected to cost $8.4 billion to increase capacity from the current level of 90 mmbbls/year to approximately 128 mmbbls/year. The expansion is expected to startup in early 2006 with production increasing to full capacity by 2008. Talisman expects that its capital spending in 2006 related to the Syncrude Project, including expansion and sustaining capital, will be approximately $9 million.

UNITED STATES

Fortuna Energy Inc. ("Fortuna"), a subsidiary of Talisman, operates in the Appalachia area of upstate New York. Fortuna holds a 100% operated interest in the Pinehill and Catlin Hill dehydration facilities as well as a 49% to 100% interest in a number of operated meter stations and pipelines. Fortuna increased production primarily from deep horizontal Trenton-Black River formation gas wells in the Appalachia area (upstate New York) from 60 mmcf/d sales gas (Company share) in 2003 to 105 mmcf/d sales gas (Company share) in 2005. Fortuna expects that capital spending in 2006 in the Appalachia area will be approximately $109 million and plans to participate in drilling 40 wells.

Talisman's subsidiary, Fortuna (US) L.P., continues to explore for oil and gas in the western US. Fortuna (US) L.P. expects its capital spending in 2006 in the US will be approximately $45 million and plans to participate in drilling up to four wells.

LANDHOLDINGS, PRODUCTION AND PRODUCTIVE WELLS

The following tables set forth Talisman's North American landholdings, production and productive wells as at December 31, 2005.

NORTH AMERICA

Property

| Developed Acreage

(thousand acres)

| | Undeveloped Acreage

(thousand acres)

| | Total Acreage

(thousand acres)

|

|---|

|

|---|

| Gross

| | Net

| | Gross

| | Net

| | Gross

| | Net

|

|---|

|

| North America | | | | | | | | | | | |

| | Canada | | | | | | | | | | | |

| | | Alberta Foothills | 159.2 | | 76.5 | | 527.6 | | 315.1 | | 686.8 | | 391.6 |

| | | Edson Area | 964.9 | | 493.9 | | 828.0 | | 566.1 | | 1,792.9 | | 1,060.0 |

| | | Greater Arch | 714.8 | | 337.5 | | 1,281.1 | | 897.9 | | 1,995.9 | | 1,235.4 |

| | | Deep Basin | 261.8 | | 66.3 | | 520.7 | | 341.2 | | 782.5 | | 407.5 |

| | | Monkman/BC Foothills | 77.8 | | 41.6 | | 770.7 | | 470.3 | | 848.5 | | 511.9 |

| | | Southern Alberta Foothills | 30.5 | | 25.1 | | 135.5 | | 100.4 | | 166.0 | | 125.5 |

| | | Chauvin | 98.7 | | 80.1 | | 82.2 | | 44.6 | | 180.9 | | 124.7 |

| | | Other1 | 1,115.7 | | 708.4 | | 4,315.4 | | 1,502.3 | | 5,431.1 | | 2,210.7 |

| | United States2 | 31.9 | | 28.3 | | 1,580.0 | | 1,266.1 | | 1,611.9 | | 1,294.4 |

|

| Total3 | 3,455.3 | | 1,857.7 | | 10,041.2 | | 5,504.0 | | 13,496.5 | | 7,361.7 |

|

| Synthetic Oil | 13.5 | | 2.3 | | 474.7 | | 84.3 | | 488.2 | | 86.6 |

|

Notes:

- 1

- "Other" includes Ontario and minor properties in Canada, but excludes Scotian Slope, synthetic oil and coal leases in British Columbia.

- 2

- "United States" excludes Alaska.

- 3

- Fee acreage comprises 4% of total gross number of acres and 5% of the net number of acres. Fee acreage for Gross Undeveloped totals 556.5; Gross Developed totals 66.1; Net Undeveloped totals 368.5; and Net Developed totals 22.1.

10 A N N U A L I N F O R M A T I O N F O R M

NORTH AMERICA

Property

| Oil & Liquids Production

(bbls/d)

| | Natural Gas Production

(mmcf/d)

| | Productive Wells1,2,3 as at

December 31, 2005

|

|---|

|

|---|

| Gross4

| | Net4

| | Gross5

| | Net5

| | Gross

| | Net

|

|---|

|

| North America | | | | | | | | | | | |

| | Canada | | | | | | | | | | | |

| | | Alberta Foothills | 207 | | 147 | | 147.1 | | 112.4 | | 226 | | 99.9 |

| | | Edson Area | 4,992 | | 3,695 | | 234.8 | | 187.6 | | 1,223 | | 850.7 |

| | | Greater Arch | 7,741 | | 6,174 | | 138.5 | | 108.0 | | 1,433 | | 786.8 |

| | | Deep Basin | 1,508 | | 1,357 | | 44.9 | | 33.6 | | 539 | | 110.7 |

| | | Monkman/BC Foothills | – | | – | | 103.6 | | 84.0 | | 69 | | 40.8 |

| | | Southern Alberta Foothills | 2,914 | | 2,391 | | 20.0 | | 15.5 | | 255 | | 172.3 |

| | | Chauvin | 16,132 | | 13,595 | | 16.0 | | 12.8 | | 1,992 | | 1,330.4 |

| | | Other6 | 20,117 | | 15,254 | | 105.1 | | 89.0 | | 4,864 | | 2,255.3 |

| | United States7 | – | | – | | 104.7 | | 89.7 | | 56 | | 50.0 |

|

| Total | 53,611 | | 42,613 | | 914.7 | | 732.6 | | 10,657 | | 5,696.9 |

|

| Synthetic Oil | 2,693 | | 2,587 | | – | | – | | – | | – |

|

Notes:

- 1

- "Productive Wells" means producing wells and wells capable of production.

- 2

- Includes wells containing multiple completions as follows:

|

| | Oil Wells

| | Gas Wells

|

|---|

|

|

|---|

| | Gross | | 558 | | 1,205 |

| | Net | | 292.6 | | 654.3 |

| |

|

- 3

- One or more completions in the same bore hole is counted as one well. A well is classified as an oil well if one of the multiple completions in a given well is an oil completion.

- 4

- Includes approximately 741 bbls/d of liquids attributable to royalty interests and net profits interests.

- 5

- Includes approximately 10.7 mmcf/d of gas attributable to royalty interests and net profits interests.

- 6

- "Other" includes Ontario and minor properties in Canada.

- 7

- "United States" excludes Alaska.

INTERNATIONAL AND FRONTIER

Talisman's international and frontier strategy focuses on opportunities in sedimentary basins that have a proven hydrocarbon system with significant reserves, production and exploration potential.

Talisman produces substantial oil and gas volumes from the North Sea (which includes the United Kingdom, Norwegian, Netherlands, Danish and German sectors), with ongoing exploration and development activities in the area. Talisman is active in Southeast Asia and Australia, which includes Indonesia, Malaysia, Vietnam, Papua New Guinea and Australia. In addition to the current oil and gas production in this region, development projects are expected to result in significant oil and gas production growth. Talisman has producing interests in North Africa (Algeria and Tunisia) and in Trinidad and Tobago. The Company also has exploration interests in other areas including Alaska, Colombia, Gabon, Peru, Qatar and Romania.

NORTH SEA

Talisman's North Sea strategy is to develop commercial hubs around core operated properties and infrastructure and to deliver growth by extending the life of these assets through low risk development opportunities, sub-sea tie-back developments, exploration, secondary recovery, cost reduction and increased third-party tariff revenue. The Company also has a portfolio of non-operated assets.

Talisman's North Sea assets, which are held principally by Talisman Energy (UK) Limited, Talisman North Sea Limited and Talisman Energy Norge AS, include producing fields and exploration acreage in several areas of the North Sea. Talisman's North Sea interests also include those assets acquired through the purchase of Paladin, which are held primarily through Talisman Expro Limited in respect of assets in the UK North Sea, through Talisman Resources (Norway) Limited and Paladin Resources Norge AS in respect of assets in the Norwegian North Sea and through Talisman Oil Denmark Limited in respect of assets in the Danish sector of the North Sea. Talisman has three core North Sea operating areas: the Mid-North Sea Area ("MNS Area"), the Flotta Catchment Area ("FCA Area") and Norway. In addition, Talisman has operated and non-operated interests and a number of new venture exploration licences acquired through the purchase of Paladin. At the end of 2005, Talisman operated approximately 67% of its North Sea production.

In 2006, Talisman's capital program in the North Sea is expected to be approximately $1.6 billion, with $277 million directed to exploration spending and $1,338 million directed to development (net of deferred acquisition costs). The Company's 2006 North Sea drilling program includes participation in up to 19 exploration and 45 development wells. Capital expenditures are also directed at a number of field development programs

A N N U A L I N F O R M A T I O N F O R M11

that are expected to significantly increase production in 2007 and 2008. The Company intends to dispose of approximately 10,000 to 15,000 boe/d of production from non-core assets in Western Canada and the North Sea by mid-2006.

In February 2006, Talisman reached an agreement to enter into exclusive negotiations with Shell U.K. Limited and Esso Exploration and Production UK Limited to acquire approximately 86% (combined) interest in the Fulmar field (Blocks 30/11b and 30/16s) and 100% interest in the Auk field (Blocks 30/16n and 30/16t). The transaction is conditional on agreement of the final terms and receipt of co-venturer and government approvals. If the transaction is completed, Talisman is expected to assume operatorship in 2006.

MNS Area Properties

Talisman holds interests ranging from 13% to 100% in a number of production facilities and pipelines in the MNS Area.

Clyde Area

The Company owns various operated interests in the Clyde area, including a 95% operated interest in the Clyde field and production platform, a 94% operated interest in the Orion field and a 13% non-operated interest in the Fulmar field. In 2005, Talisman drilled two development wells in the Clyde area. In February 2005, operations were completed on the Jenny exploration well at Block 30/13c with the wellbore plugged and abandoned after minor oil shows. Talisman made an oil discovery by drilling the Medwin Terrace exploration prospect. The Company expects that capital spending in 2006 in the Clyde area will be approximately $118 million. The 2006 development program includes drilling three wells, plus the implementation of a produced water reinjection program ("PWRI") to meet water emission regulations expected to become effective January 1, 2007. Talisman will also be participating in one exploration well in the area.

Buchan Area

The Company holds an average 99% operated working interest in the Buchan field, the Hannay field, the Buchan floating production platform and the tie-in to the Forties pipeline. In October 2002 and November 2003, Talisman drilled two exploration wells, resulting in new oil discoveries adjacent to the Buchan field. Talisman holds a 94% interest in the discovered Tweedsmuir and Tweedsmuir South fields. The Tweedsmuir development continued through 2005 with the drilling of three development wells (including two injection wells) and the installation of subsea and

12 A N N U A L I N F O R M A T I O N F O R M

platform facilities. The development is planned for completion in 2006 with first oil production expected in the first quarter of 2007. At year end 2005, the Company was participating in an exploration well that was subsequently plugged and abandoned in January 2006. The Company expects that capital spending in 2006 in the Buchan area will be approximately $424 million and includes plans to drill two exploration prospects.

Ross/Blake Area

In the Ross/Blake area, Talisman holds a 69% operated working interest in the Ross field and a 54% non-operated interest in the Blake field, both fields being sub-sea tie-backs to Bleo Holm, the leased Floating, Production, Storage and Offloading vessel ("FPSO"). During 2005, significant modifications were made to the FPSO to address calcium naphthenate build-ups which occurred early in the year. In late 2005, Talisman assumed operatorship of the FPSO. In November 2005, Talisman made an oil discovery at the 100% owned Blake Terrace prospect. The Company expects that capital spending in 2006 in the Ross/Blake area will be approximately $31 million and plans to drill one development well in the Blake area and to participate in up to four exploration wells.

Beatrice Area

Talisman holds a 100% operated interest in the Beatrice Alpha, Bravo and Charlie platforms, as well as the Beatrice/Nigg pipeline and the Nigg terminal. In 2005, Talisman commenced construction of an offshore wind farm demonstrator project adjacent to the Beatrice fields, which is expected to start up in the third quarter of 2006. The Company expects development spending in 2006 in the Beatrice area will be approximately $58 million and plans to implement a PWRI program and to install additional downhole pumping capacity.

Other MNS Area Properties

Talisman holds a 60% operated interest in the Beauly field located in Block 16/21c of the MNS. No capital spending is planned for the Beauly area in 2006.

Flotta Catchment Area

Talisman presently holds interests ranging from 14% to 100% in a number of production facilities and pipelines in the FCA Area, including an 80% interest in the Flotta terminal.

Piper Area

Talisman presently holds an 80% operated working interest in the Piper, Saltire, Chanter and Iona fields and a 14% non-operated interest in the MacCulloch field. In 2005, an unsuccessful exploration well was drilled on the North Saltire prospect. The Company expects that capital spending in 2006 in the Piper area will be approximately $39 million and plans to drill one development well on the Chanter field. In addition, modifications will be made to the Piper platform as part of the Tweedsmuir development.

Claymore Area

Talisman holds a 72% to 100% operated working interest in the Claymore field and an 80% operated working interest in the Scapa field. In 2005, Talisman drilled two development wells on the Claymore field. The Company expects that capital spending in 2006 in the Claymore area will be approximately $84 million, which includes funding for three development wells, gas compression modifications and a PWRI program.

THP Area

Talisman's subsidiary holds a 100% operated working interest in the Tartan field and in the Highlander and Petronella sub-sea tie-back satellite fields; and a 67% operated interest in the Galley field (collectively, "THP Area"). In 2005, Talisman drilled three development wells and one unsuccessful exploration well in the THP Area. The Company expects that capital spending in 2006 in the THP Area will be approximately $101 million and plans to drill one exploration and two development wells. In addition, Talisman intends to develop the Duart North field, the Tartan "Hot Lens" sands and redevelop the Galley field.

Other FCA Area Properties

Talisman's subsidiary holds a 78% and 41% operated working interest in the Renee and Rubie fields, respectively. Both fields are sub-sea tie-backs to the Ivanhoe/Rob Roy field in which Talisman has a 23% non-operated interest. Capital spending by the Company in other FCA Area properties in 2006 is expected to be minimal.

A N N U A L I N F O R M A T I O N F O R M13

Paladin UK Properties

Through the acquisition of Paladin, a Talisman subsidiary holds interests ranging from 20% to 59% in a number of additional production facilities and pipelines in the UK North Sea.

Montrose/Arbroath Area

Talisman's subsidiary holds a 59% operated working interest in each of the Arbroath, Arkwright, Brechin, Montrose and Wood fields acquired through the Paladin acquisition. In 2006, Talisman plans to develop the Wood field with first oil production expected in 2007. The Company expects that capital spending in 2006 in the Montrose/Arbroath Area will be approximately $200 million which includes plans to drill one exploration well and five development wells.

Other Paladin UK Properties

Talisman's subsidiary holds a 25% operated interest in each of the Blane (UK) and Enoch fields and a 52% operated interest in the Fiddich field acquired through the Paladin acquisition. The Company expects that capital spending in 2006 on these properties will be approximately $107 million and plans to participate in drilling four development wells (three of which are shared with the "Other Norway Properties" section below). In addition, Talisman plans to develop the Blane and Enoch fields with first oil production from both fields expected in early 2007.

Norway Properties

Talisman's subsidiaries hold interests ranging from 1% to 70% in a number of production facilities and pipelines in Norway. The principal areas include the Gyda and Varg fields.

Gyda Area

Talisman's subsidiary holds a 61% operated interest in the Gyda field and associated assets. In 2005, the Company drilled two development wells. The Company expects that capital spending in 2006 in the Gyda area will be approximately $154 million and plans to drill up to five exploration and two development wells. In addition, Talisman plans to install gas lift facilities and to implement a PWRI program.

Varg Area

Talisman's subsidiaries hold operated interests ranging from 65% to 70% in the Varg area and associated assets. In February 2005, Talisman Energy (UK) Limited acquired all of the outstanding shares of Pertra, resulting in the addition of the producing Varg field and undeveloped Varg South field as well as several blocks of operated and non-operated exploration acreage. Subsequent to this purchase, Talisman's subsidiary disposed of a minor portion of the interests acquired in the Varg field. The Company drilled four development wells (including one injection well) in the Varg field in 2005. The Company expects that capital spending in 2006 in the Varg area will be approximately $90 million and plans to drill one development well and to commence development of the Varg South field with first production expected in the fourth quarter of 2007.

Other Norway Properties

Talisman's subsidiaries hold 18% and 70% operated interests in the Blane (Norway) and Yme fields, respectively and 35%, 34%, 27% and 1% non-operated interests in the Sognefjord, Brage, Veslefrikk and Huldra fields, respectively. The majority of these interests were acquired through the acquisition of Paladin. In 2005, the Company drilled one unsuccessful exploration well and spudded another, which was subsequently abandoned in early 2006. The Company expects that capital spending in 2006 in these areas will be approximately $148 million and plans to participate in drilling three exploration wells and seven development wells (three of which are shared with the "Other Paladin UK Properties" section above).

In the Danish sector of the North Sea, Talisman acquired a 30% non-operated working interest in the Siri field through the Paladin acquisition. The Company expects that capital spending in 2006 will be $13 million and plans to participate in drilling one development well.

Non-Operated Interest Properties

Brae Area

Talisman's non-operated producing interests in the Brae area range from 13% to 18%. Talisman also holds a 9% non-operated interest in the Brae-St. Fergus gas pipeline and terminal. In 2005, Talisman participated in three development wells in the Brae area. The Company expects that capital spending in 2006 in the Brae area will be approximately $19 million and plans to participate in drilling six development wells.

Other Non-Operated Interest Properties

Talisman's subsidiaries hold various non-operated producing interests in the following fields in the United Kingdom: Balmoral (15%), Stirling (15%), Glamis (15%), Andrew (10%), Wytch Farm (5%), Wareham (5%), Alba (2%), Caledonia (3%), Goldeneye (8%) and Bittern (2%). In 2005, Talisman

14 A N N U A L I N F O R M A T I O N F O R M

participated in drilling nine development wells (including one injection well) and two unsuccessful exploration wells. The Company expects that capital spending in 2006 at its other non-operated interest properties will be approximately $14 million and plans to participate in drilling seven development wells.

Talisman's subsidiary holds non-operated producing interests in the Netherlands sector of the North Sea ranging from 2% to 20%. The Company's interests are in the E, F, G and K sectors. In 2005, the Company participated in drilling two development wells. The Company expects that capital spending in the Netherlands sector in 2006 will be approximately $10 million and plans to participate in drilling one exploration well and five development wells.

In the German sector of the North Sea, Talisman's subsidiary holds a 50% non-operated working interest in one offshore licence covering portions of blocks C, D, G and H. The Company expects capital spending in 2006 in this sector will be approximately $5 million and plans to participate in an exploration well in the sector.

Landholdings, Production and Productive Wells

The following tables set forth Talisman's North Sea landholdings, production and productive wells as at December 31, 2005.

NORTH SEA

Property

| Developed Acreage

(thousand acres)

| | Undeveloped Acreage

(thousand acres)

| | Total Acreage

(thousand acres)

|

|---|

|

|---|

| Gross

| | Net

| | Gross

| | Net

| | Gross

| | Net

|

|---|

|

| Mid-North Sea Area | | | | | | | | | | | |

| | Clyde Area | 26.4 | | 21.5 | | 173.7 | | 102.1 | | 200.1 | | 123.6 |

| | Buchan Area | 21.2 | | 20.4 | | 174.5 | | 92.9 | | 195.7 | | 113.3 |

| | Ross/Blake Area | 35.2 | | 21.8 | | 242.8 | | 122.0 | | 278.0 | | 143.8 |

| | Beatrice Area | 14.5 | | 14.5 | | 26.7 | | 26.7 | | 41.2 | | 41.2 |

| | Other MNS | 3.6 | | 1.3 | | 69.3 | | 29.4 | | 72.9 | | 30.7 |

Flotta Catchment Area |

|

|

|

|

|

|

|

|

|

|

|

| | Piper Area | 37.9 | | 24.8 | | 97.2 | | 56.1 | | 135.1 | | 80.9 |

| | Claymore Area | 22.0 | | 17.4 | | 72.7 | | 65.6 | | 94.7 | | 83.0 |

| | THP Area | 21.7 | | 21.7 | | 116.6 | | 67.4 | | 138.3 | | 89.1 |

| | Other FCA | 9.8 | | 5.2 | | 66.0 | | 21.2 | | 75.8 | | 26.4 |

Paladin UK Properties |

|

|

|

|

|

|

|

|

|

|

|

| | Montrose/Arbroath | 45.5 | | 26.8 | | 142.5 | | 78.6 | | 188.0 | | 105.4 |

| | Other Paladin UK Properties | 5.8 | | 1.1 | | 65.0 | | 15.6 | | 70.8 | | 16.7 |

Norway |

|

|

|

|

|

|

|

|

|

|

|

| | Gyda Area | 50.7 | | 37.5 | | 708.4 | | 384.8 | | 759.1 | | 422.3 |

| | Varg Area | 25.1 | | 16.6 | | 566.0 | | 185.6 | | 591.1 | | 202.2 |

| | Other1 | 82.7 | | 24.8 | | 2,666.8 | | 977.5 | | 2,749.5 | | 1,002.3 |

|

Non-Operated Interests |

|

|

|

|

|

|

|

|

|

|

|

| | Brae Area | 35.8 | | 7.8 | | 50.3 | �� | 11.0 | | 86.1 | | 18.8 |

| | Other Non-Operated Interests2 | 380.3 | | 93.1 | | 2,362.3 | | 1,187.2 | | 2,742.6 | | 1,280.3 |

|

| Total | 818.2 | | 356.3 | | 7,600.8 | | 3,423.7 | | 8,419.0 | | 3,780.0 |

|

Notes:

- 1

- "Other" includes Denmark.

- 2

- "Other Non-Operated Interest" includes the Netherlands and Germany.

A N N U A L I N F O R M A T I O N F O R M15

NORTH SEA

Property

| Oil & Liquids Production

(bbls/d)

| | Natural Gas Production

(mmcf/d)

| | Productive Wells1,2,3 as at

December 31, 2005

|

|---|

|

|---|

| Gross

| | Net

| | Gross

| | Net

| | Gross

| | Net

|

|---|

|

| Mid-North Sea Area | | | | | | | | | | | |

| | Clyde Area | 11,720 | | 11,720 | | 0.9 | | 0.9 | | 24 | | 22.4 |

| | Buchan Area | 9,828 | | 9,421 | | 0.3 | | 0.3 | | 12 | | 10.9 |

| | Ross/Blake Area | 16,168 | | 16,168 | | 4.3 | | 4.3 | | 20 | | 12.0 |

| | Beatrice Area | 3,724 | | 3,724 | | – | | – | | 28 | | 28.0 |

| | Other MNS | 1,162 | | 1,162 | | 0.4 | | 0.4 | | 1 | | 0.6 |

Flotta Catchment Area |

|

|

|

|

|

|

|

|

|

|

|

| | Piper Area | 15,719 | | 15,719 | | 0.1 | | 0.1 | | 34 | | 21.9 |

| | Claymore Area | 20,506 | | 20,506 | | – | | – | | 36 | | 26.9 |

| | THP Area | 12,005 | | 12,005 | | 4.1 | | 4.1 | | 28 | | 24.7 |

| | Other FCA | 2,126 | | 2,126 | | – | | – | | 14 | | 4.0 |

Paladin UK Properties |

|

|

|

|

|

|

|

|

|

|

|

| | Montrose/Arbroath | 1,446 | | 1,446 | | 0.1 | | 0.1 | | 30 | | 17.7 |

| | Other Paladin UK Properties | | | | | | | | | | | |

Norway |

|

|

|

|

|

|

|

|

|

|

|

| | Gyda | 8,449 | | 8,449 | | 7.5 | | 7.5 | | 21 | | 12.7 |

| | Varg | 13,338 | | 13,338 | | – | | – | | 13 | | 8.5 |

| | Other4 | 3,909 | | 3,890 | | 1.5 | | 1.5 | | 60 | | 12.1 |

Non-Operated Interests |

|

|

|

|

|

|

|

|

|

|

|

| | Brae Area | 8,113 | | 7,081 | | 75.7 | | 67.9 | | 77 | | 10.6 |

| | Other Non-Operated Interests5 | 4,503 | | 4,503 | | 25.1 | | 25.1 | | 180 | | 9.9 |

|

| Total | 132,716 | | 131,258 | | 120.0 | | 112.2 | | 578 | | 222.9 |

|

Notes:

- 1

- "Productive Wells" means producing wells and wells capable of production.

- 2

- Includes wells containing multiple completions as follows:

|

| | Oil Wells

| | Gas Wells

|

|---|

|

|

|---|

| | Gross | | 21 | | – |

| | Net | | 2.4 | | – |

| |

|

- 3

- One or more completions in the same bore hole is counted as one well. A well is classified as an oil well if one of the multiple completions in a given well is an oil completion.

- 4

- "Other" includes Denmark.

- 5

- "Other Non-Operated Interest" includes the Netherlands.

16 A N N U A L I N F O R M A T I O N F O R M

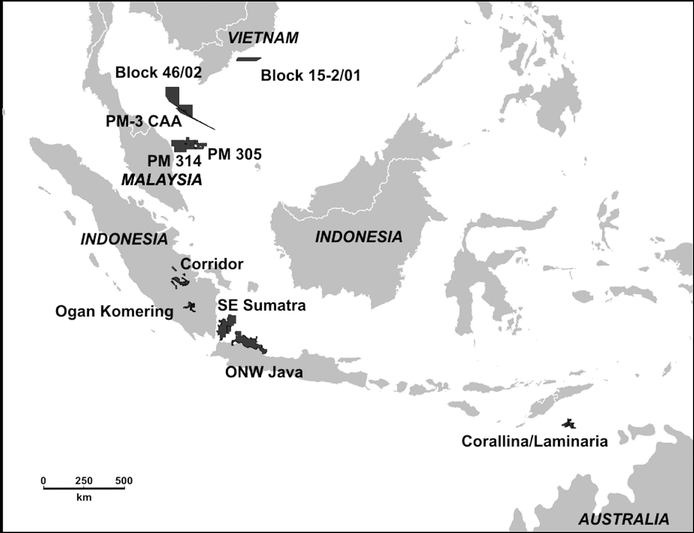

SOUTHEAST ASIA AND AUSTRALIA

The Company's interests in Southeast Asia and Australia include operations in Indonesia, Malaysia, Vietnam and Australia and exploration acreage with existing discoveries in Papua New Guinea.

Indonesia

In Indonesia, Talisman and its subsidiaries are continuing the development of the major natural gas discoveries at Corridor in order to deliver future production growth, the exploitation of existing oil properties and exploration activity.

Talisman plans to spend approximately $85 million in Indonesia in 2006, primarily to participate in drilling six exploration wells and 41 development wells and to continue Suban Phase 2 of the Corridor gas facility expansion.

Corridor PSC

Talisman (Corridor) Ltd. ("TCL"), a subsidiary of Talisman, has a 36% non-operated interest in the Corridor production sharing contract ("Corridor PSC Block") and field production facilities. Production from Corridor began in 1998 with gas sales to PT Caltex Pacific Indonesia ("Caltex"). Gas sales to Caltex were augmented pursuant to an agreement signed in 2000. In September 2003, TCL commenced gas sales to Gas Supply Pte. Ltd., located in Singapore, under the terms of a 20-year gas sales agreement. Talisman Transgasindo Ltd. has an indirect 6% interest in the Grissik to Duri pipeline and in the Grissik to Singapore pipeline which was completed in 2003.

In August 2004, ConocoPhillips (Grissik) Ltd., as representative of the Corridor PSC Block contractors, entered into an agreement for the sale of gas to PT Perusahaan Gas Negara (Persero), Tbk., the Indonesian national gas transmission and distribution company. This agreement enables the sale of 2.3 trillion cubic feet (gross sales) of natural gas from the Corridor PSC Block to the West Java market over a 17-year period commencing in

A N N U A L I N F O R M A T I O N F O R M17

the first quarter of 2007. In 2005, the Suban Phase 2 gas expansion project commenced and includes the installation of two new 200 mmcf/d capacity gas trains, additional pipelines and infrastructure in the Corridor PSC Block.

The Company expects that capital spending in 2006 in the area will be approximately $55 million to participate in the drilling of two development wells and to continue the Suban Phase 2 development, expected to be onstream in 2007.

Other Properties

Talisman's subsidiaries hold a 40% non-operated interest in the Corridor Technical Assistance Contract (the "Corridor TAC Block") and a 50% operated interest in the Ogan Komering production sharing contract (the "OK Block"). Through the acquisition of Paladin, Talisman acquired a 7% non-operated interest in the Southeast Sumatra Block ("SES Block") and a 2% non-operated interest in the offshore North West Java Block ("ONWJ Block"). The SES Block contains 33 producing fields while the ONWJ Block contains 35 producing fields. In 2005, the Company participated in one unsuccessful exploration well on the SES Block.

In January 2005, the enhanced oil recovery contract at Jambi expired, in which Talisman's subsidiary held a 40% interest.

Also in January 2005, Talisman's subsidiary participated in an unsuccessful exploration well on the offshore Nila production sharing contract. Subsequently, the subsidiary relinquished its non-operated interest.

The Company expects that capital spending in 2006 in these areas will be approximately $30 million with plans to drill up to six exploration wells and 39 development wells.

Malaysia and Vietnam

In Malaysia and Vietnam, the Company's strategy is to develop oil and natural gas fields and to deliver production growth through exploration and development. The Company operates three of its five working interest properties in Malaysia and Vietnam, being Block PM-3 CAA/Block 46-Cai Nuoc, Block PM-305 and Block PM-314. Block 46/02 and Block 15-2/01 are each operated by a joint operating company. Total Malaysia and Vietnam capital spending in 2006 is expected to be approximately $350 million.

Block PM-3 CAA and 46-Cai Nuoc

Two of Talisman's subsidiaries hold interests in Block PM-3 CAA and associated production facilities in Malaysia and Vietnam: Talisman Malaysia Limited ("TML") (26%) and Talisman Malaysia (PM3) Limited (15%). Talisman Vietnam Limited, another subsidiary, holds a 33% operated interest in the adjacent Block 46-Cai Nuoc area in Vietnam. Part of that area and part of the PM-3 CAA were unitized in 1998 to become the East Bunga Kekwa-Cai Nuoc unit. In 2005, additional acreage was granted to Block PM-3 CAA along the south-eastern border of the block.

In 2005, Phase 2/3 development drilling continued with the drilling of nine wells (including three injection wells) in the non-unit area and a successful two-well exploration program in the PM-3 CAA and Block 46-Cai Nuoc areas. Natural gas is sold under a long-term contract to Petroliam Nasional Berhad and Vietnam Oil and Gas Corporation, the national oil and gas companies of Malaysia and Vietnam, respectively. In 2006, the Company plans to commence development of the PM-3 CAA Northern Fields with first oil and gas production expected in 2008. Also in 2006, the Bunga Tulip field development and Phase 2/3 facility enhancement are expected to be completed with first oil production from the Bunga Tulip field in late 2006.

The Company expects that capital spending in 2006 in the area will be approximately $262 million and plans to drill four exploration wells, 15 development wells and to develop the Northern Fields.

Block PM-305

TML holds a 60% operated working interest in the Block PM-305 production sharing contract offshore Malaysia. In 2003, the Company made an oil discovery 10 kilometres south of the Angsi field. In 2005, the South Angsi development was completed which included the drilling of seven development wells (including three injection wells). First oil production commenced in August 2005. Also in 2005, Talisman drilled two successful exploration wells as part of a four-well program.

The Company expects that capital spending in 2006 in the area will be approximately $3 million.

Block PM-314

TML holds a 60% operated working interest in the Block PM-314 production sharing contract. In 2005, the Company drilled one successful exploration well. The Company expects that capital spending in 2006 in the area will be approximately $36 million and includes plans to drill up to two exploration wells, one development well, and to develop the newly discovered Naga Kecil field.

Block 46/02

Talisman (Vietnam 46/02) Ltd. holds a 30% interest in the Truong Son Joint Operating Company ("JOC"), with the remainder held by the wholly owned exploration and production subsidiaries of the national petroleum companies of Vietnam and Malaysia. In 2005, the Company drilled one successful appraisal well. The Company expects that capital spending in 2006 in Block 46/02 will be approximately $8 million primarily to commence development of the Song Doc field, which was discovered in 2003, with first oil production expected in 2007.

18 A N N U A L I N F O R M A T I O N F O R M

Block 15-2/01

Talisman (Vietnam 15-2/01) Ltd. ("Talisman 15-2/01"), a subsidiary of Talisman, and Petro Vietnam signed a petroleum contract for Block 15-2/01 offshore Vietnam in 2005. Talisman 15-2/01 holds a 60% interest in Block 15-2/01, with the remaining 40% held by the wholly-owned exploration and production subsidiary of the national petroleum company of Vietnam.

The Company expects that capital spending in 2006 in Block 15-2/01 will be approximately $41 million and includes plans to drill one exploration well, with a second exploration well expected to be spudded at the end of the year.

Australia

The Company acquired interests in Australia through the acquisition of Paladin. Talisman's subsidiary holds 40% and 33% non-operated interests in the Laminaria and Corallina fields, respectively. The Company also acquired a 25% non-operated interest in the JPDA 03-01 contract area. There was minimal activity in Australia in 2005. The Company expects that capital spending in 2006 in Australia will be approximately $5 million and includes plans to participate in drilling up to two exploration wells and one development well.

Papua New Guinea

The Company holds an operated interest in offshore Papua New Guinea Block PRL-1 (48%), which contains a natural gas discovery, and in Block PPL-244 (35%), which is exploration acreage. The Company expects minor capital expenditures in Papua New Guinea in 2006.

Landholdings, Production and Productive Wells

The following tables set forth Talisman's Southeast Asia and Australia landholdings, production and productive wells as at December 31, 2005.

SOUTHEAST ASIA AND AUSTRALIA

Property

| Developed Acreage

(thousand acres)

| | Undeveloped Acreage

(thousand acres)

| | Total Acreage

(thousand acres)

|

|---|

|

|---|

| Gross

| | Net

| | Gross

| | Net

| | Gross

| | Net

|

|---|

|

| Indonesia | | | | | | | | | | | |

| | Corridor PSC | 150.5 | | 54.2 | | 407.6 | | 146.7 | | 558.1 | | 200.9 |

| | Other1 | 361.1 | | 53.7 | | 4,092.2 | | 337.9 | | 4,453.3 | | 391.6 |

| Malaysia and Vietnam | | | | | | | | | | | |

| | Block PM-3 CAA and 46-Cai Nuoc | 224.4 | | 92.5 | | 277.3 | | 113.7 | | 501.7 | | 206.2 |

| | Block PM-305 | 43.9 | | 26.3 | | 499.8 | | 299.9 | | 543.7 | | 326.2 |

| | Block PM-314 | – | | – | | 2,309.8 | | 1,385.9 | | 2,309.8 | | 1,385.9 |

| | Block 46/02 | – | | – | | 3,023.6 | | 907.1 | | 3,023.6 | | 907.1 |

| | Block 15-2/01 | – | | – | | 699.8 | | 419.9 | | 699.8 | | 419.9 |

|

| Australia | 9.2 | | 3.6 | | 488.9 | | 140.9 | | 498.1 | | 144.5 |

|

| Papua New Guinea | – | | – | | 858.2 | | 325.1 | | 858.2 | | 325.1 |

|

| Total | 789.1 | | 230.3 | | 12,657.2 | | 4,077.1 | | 13,446.3 | | 4,307.4 |

|

Note:

- 1