Exhibit 99.1

Exhibit 99.1

Year-End 2015 Results & Outlook February 4, 2016

Jackson Gas Plant

Among lowest acquisition cost ever

Compressor station

#1 LDC in gas storage

Cross Winds Energy Park

#2 in renewable sales in the Great Lakes area

This presentation is made as of the date hereof and contains “forward-looking statements” as defined in Rule 3b-6 of the Securities Exchange Act of 1934, Rule 175 of the Securities Act of 1933, and relevant legal decisions. The forward-looking statements are subject to risks and uncertainties. All forward-looking statements should be considered in the context of the risk and other factors detailed from time to time in CMS Energy’s and Consumers Energy’s Securities and Exchange Commission filings. Forward-looking statements should be read in conjunction with “FORWARD-LOOKING STATEMENTS AND INFORMATION” and “RISK FACTORS” sections of CMS Energy’s and Consumers Energy’s Form 10-K for the year ended December 31, 2014 and as updated in subsequent 10-Qs. CMS Energy’s and Consumers Energy’s “FORWARD-LOOKING STATEMENTS AND INFORMATION” and “RISK FACTORS” sections are incorporated herein by reference and discuss important factors that could cause CMS Energy’s and Consumers Energy’s results to differ materially from those anticipated in such statements. CMS Energy and Consumers Energy undertake no obligation to update any of the information presented herein to reflect facts, events or circumstances after the date hereof.

The presentation also includes non-GAAP measures when describing CMS Energy’s results of operations and financial performance. A reconciliation of each of these measures to the most directly comparable GAAP measure is included in the appendix and posted on our website at www.cmsenergy.com.

CMS Energy provides historical financial results on both a reported (GAAP) and adjusted (non-GAAP) basis and provides forward-looking guidance on an adjusted basis. Management views adjusted earnings as a key measure of the company’s present operating financial performance, unaffected by discontinued operations, asset sales, impairments, regulatory items from prior years, or other items. These items have the potential to impact, favorably or unfavorably, the company’s reported earnings in future periods.

Investors and others should note that CMS Energy routinely posts important information on its website and considers the Investor Relations section, www.cmsenergy.com/investor-relations, a channel of distribution.

1

Agenda

2015 Results and 2016 Priorities

Future Outlook

Capital Investment

Customer AND Investor Model

Financial Results and Outlook

2

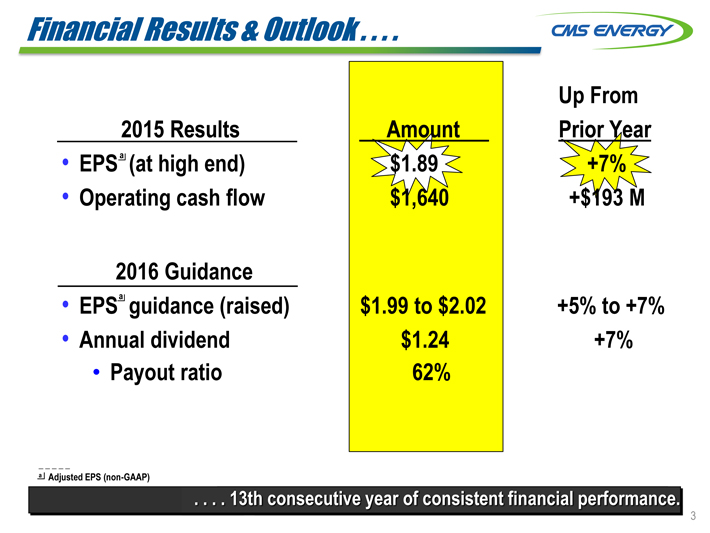

Financial Results & Outlook . . . .

2015 Results

EPSa (at high end) Operating cash flow

2016 Guidance EPSa guidance (raised) Annual dividend

Payout ratio

Up From

Amount Prior Year

$1.89 +7%

$1,640 +$193 M

$1.99 to $2.02 +5% to +7%

$1.24 +7%

62%

a Adjusted EPS (non-GAAP)

13th consecutive year of consistent financial performance.

3

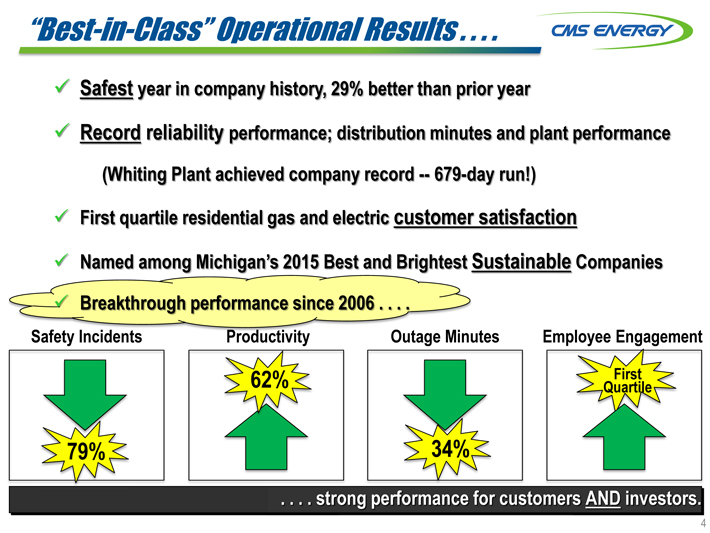

“Best-in-Class” Operational Results . . . .

Safest year in company history, 29% better than prior year

Record reliability performance; distribution minutes and plant performance (Whiting Plant achieved company record — 679-day run!)

First quartile residential gas and electric customer satisfaction

Named among Michigan’s 2015 Best and Brightest Sustainable Companies

Breakthrough performance since 2006 . . . .

Safety Incidents Productivity Outage Minutes Employee Engagement

62% Quartile First

79% 34%

. . . . strong performance for customers AND investors.

4

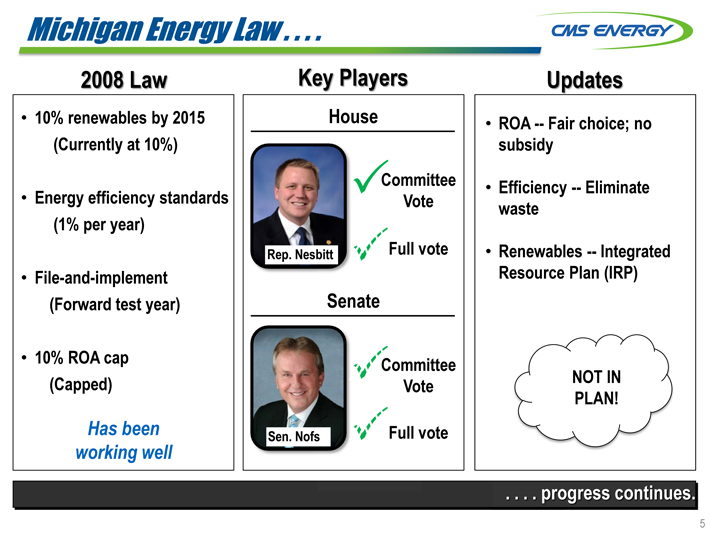

Michigan Energy Law . . . .

2008 Law

10% renewables by 2015 (Currently at 10%)

Energy efficiency standards (1% per year)

File-and-implement (Forward test year)

10% ROA cap (Capped)

Has been working well

Key Players

House

?Committee Vote

Rep. Nesbitt

Full vote

Senate

Committee Vote

Sen. Nofs

Full vote

Updates

ROA — Fair choice; no subsidy

Efficiency — Eliminate waste

Renewables — Integrated Resource Plan (IRP)

NOT IN PLAN!

. . . . progress continues.

5

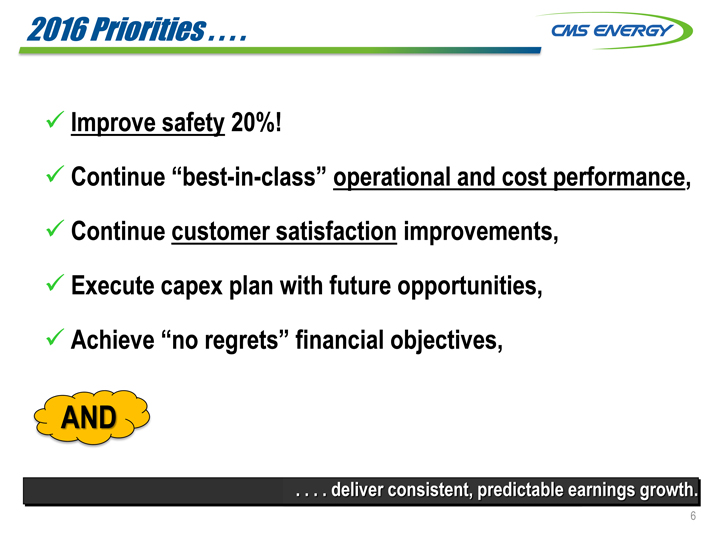

2016 Priorities . . . .

Improve safety 20%!

Continue “best-in-class” operational and cost performance, Continue customer satisfaction improvements, Execute capex plan with future opportunities,

Achieve “no regrets” financial objectives,

AND

. . . . deliver consistent, predictable earnings growth.

6

a

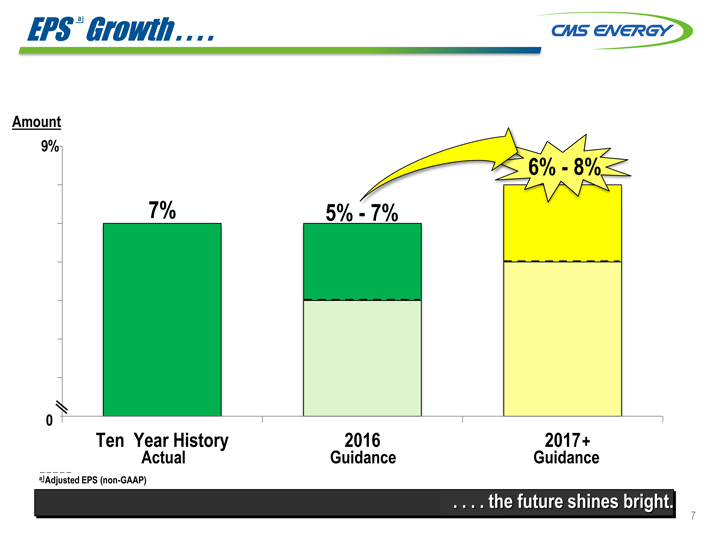

EPS Growth . . . .

Amount

9%

6%—8%

7% 5%—7%

0

Ten Year History 2016 2017 +

Actual Guidance Guidance

a Adjusted EPS (non-GAAP)

. . . . the future shines bright.

7

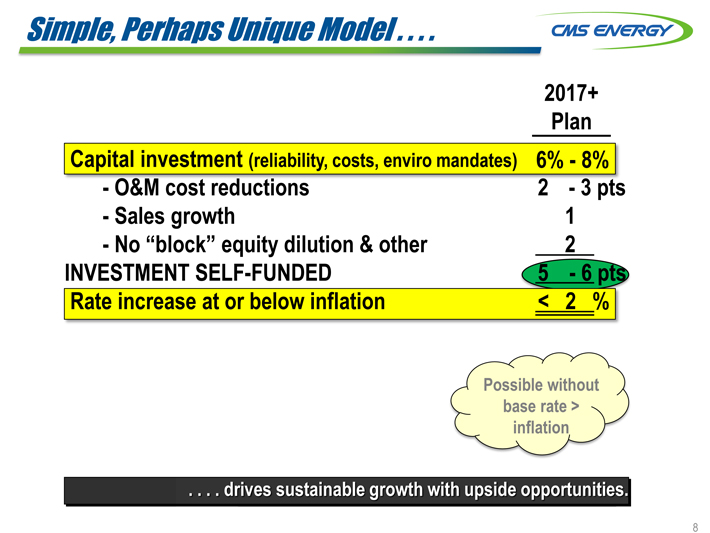

Simple, Perhaps Unique Model . . . .

2017+

Plan

Capital investment (reliability, costs, enviro mandates) 6%—8%

- O&M cost reductions 2—3 pts

- Sales growth 1

- No “block” equity dilution & other 2

INVESTMENT SELF-FUNDED 5—6 pts

Rate increase at or below inflation < 2 %

Possible without base rate > inflation

. . . . drives sustainable growth with upside opportunities.

8

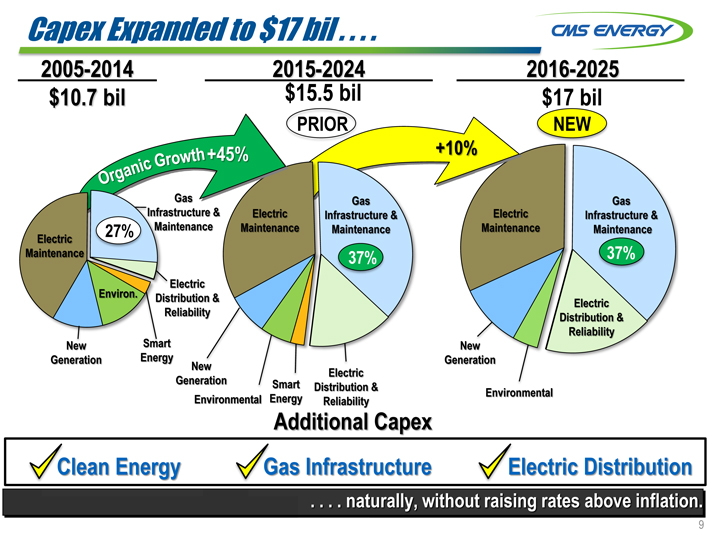

Capex Expanded to $17 bil . . . .

2005-2014 2015-2024 2016-2025

$10.7 bil $17 bil

Prior NEW

+45% +10%

Gas Gas Gas

Infrastructure & Electric Infrastructure & Electric Infrastructure &

Electric 27% Maintenance Maintenance Maintenance Maintenance Maintenance

Maintenance 37% 37%

Electric

Environ. Distribution &

Electric

Reliability Distribution &

Reliability

New Smart New

Generation Energy Generation

New Electric

Generation Smart Distribution &

Environmental Energy Reliability Environmental

Additional Capex

Clean Energy Gas Infrastructure Electric Distribution

. . . . naturally, without raising rates above inflation.

9

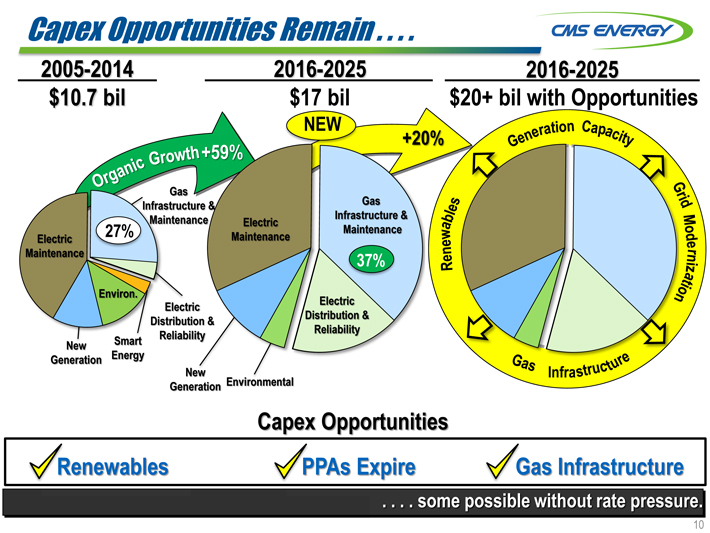

Capex Opportunities Remain . . . .

2005-2014 2016-2025 2016-2025

$10.7 bil $17 bil $20+ bil with Opportunities

NEW

+20%

Gas

Electric Infrastructure &

Electric 27% Maintenance Maintenance

Maintenance 37%

Environ

Electric Electric

Distribution & Distribution &

Reliability

New Smart Reliability

Generation Energy

New Infra

Generation Environmental

Capex Opportunities

Renewables PPAs Expire Gas Infrastructure

. . . . some possible without rate pressure.

10

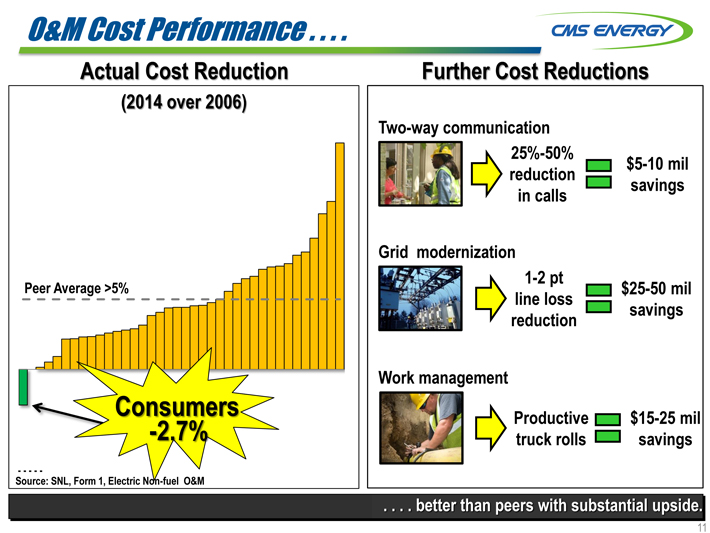

O&M Cost Performance . . . .

Actual Cost Reduction

(2014 over 2006)

Peer Average >5%

Consumers

-2.7%

Source: SNL, Form 1, Electric Non-fuel O&M

Further Cost Reductions

Two-way communication

25%-50%

reduction $5-10 mil

in calls savings

Grid modernization

1-2 pt

line loss $25-50 mil

reduction savings

Work management

Productive $15-25 mil

truck rolls savings

. . . . better than peers with substantial upside.

11

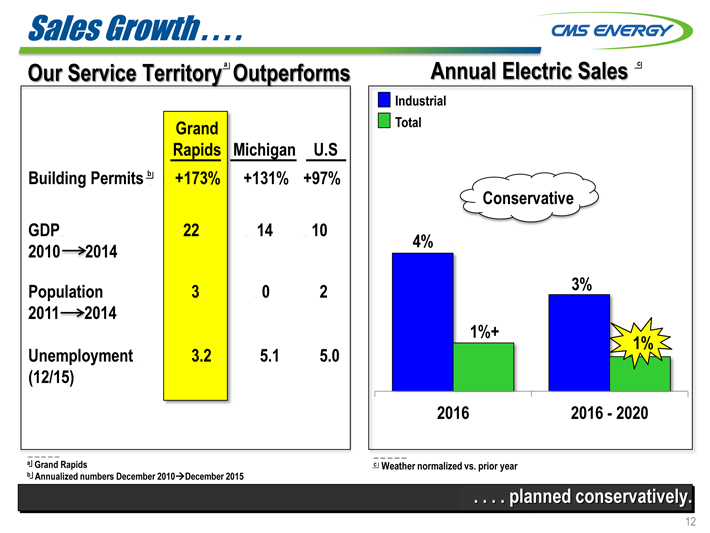

Sales Growth . . . .

Our Service Territorya Outperforms

Annual Electric Sales c

Industrial

Total

Conservative

4%

3%

1%+ 1%

2016 2016—2020

a Grand Rapids c Weather normalized vs. prior year

b Annualized numbers December 2010

December 2015

. . . . planned conservatively.

12

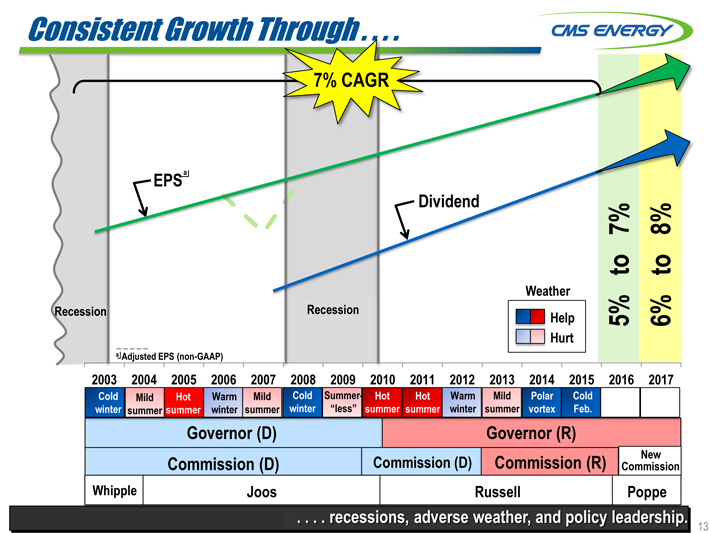

Consistent Growth Through . . . .

7% CAGR

7% 8%

to to

Weather

Recession Recession Help 5% 6%

Hurt

a Adjusted EPS (non-GAAP)

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Cold Mild Hot Warm Mild Cold Summer- Hot Hot Warm Mild Polar Cold

winter summer summer winter summer winter “less” summer summer winter summer vortex Feb.

Governor (D) Governor (R)

Commission (D) Commission (D) Commission (R) Commission New

Whipple Joos Russell Poppe

. . . . recessions, adverse weather, and policy leadership.

13

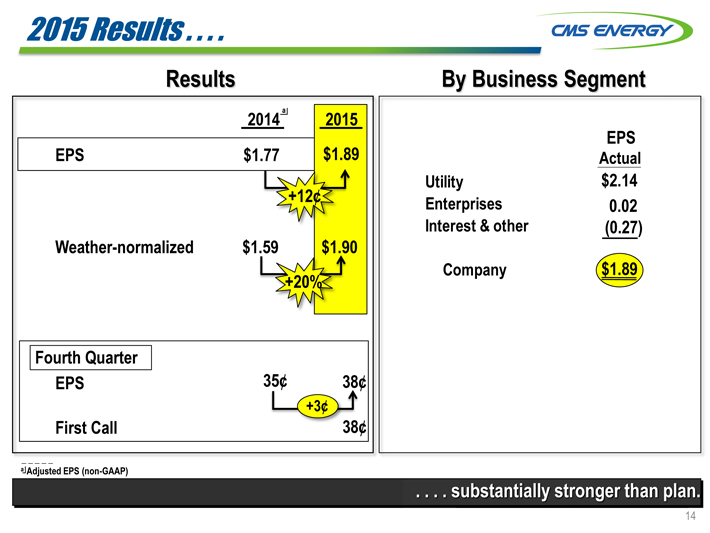

2015 Results . . . .

Results

2014 a 2015

EPS $1.77 $1.89

+12¢

Weather-normalized $1.59 $1.90

+20%

Fourth Quarter

EPS 35¢ 38¢

+3¢

First Call 38¢

By Business Segment

EPS

Actual

$2.14

0.02

(0.27)

$1.89

a Adjusted EPS (non-GAAP)

. . . . substantially stronger than plan.

14

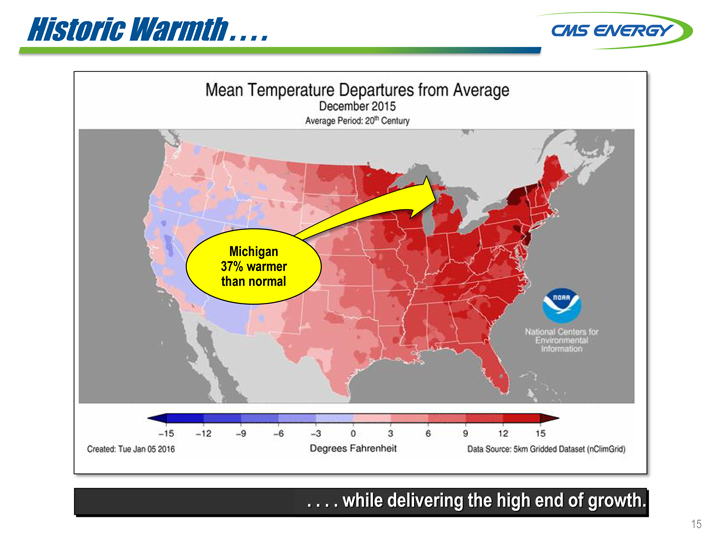

Historic Warmth . . . .

. . . . while delivering the high end of growth.

15

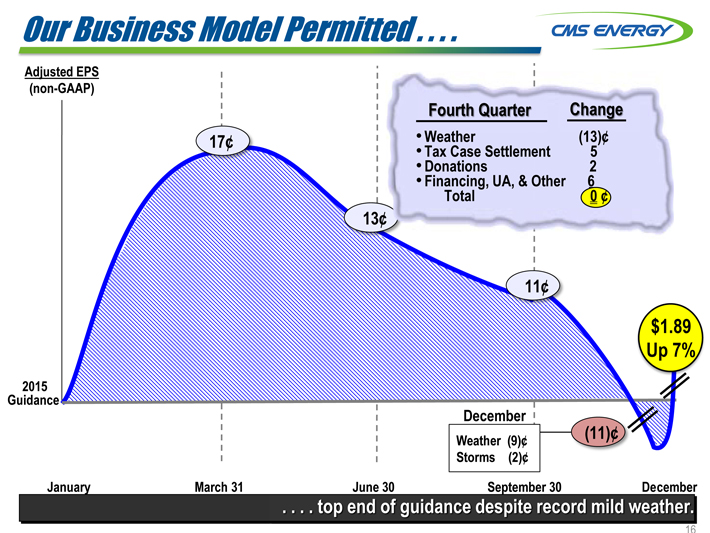

Our Business Model Permitted . . . .

Adjusted EPS

(non-GAAP)

Fourth Quarter Change

17¢ • Weather(13)¢

• Tax Case Settlement 5

• Donations 2

• Financing, UA, & Other 6

Total 0 ¢

13¢

11¢

$1.89

Up 7%

2015

Guidance

December

Weather (9)¢(11)¢

Storms(2)¢

January March 31 June 30 September 30 December

. . . . top end of guidance despite record mild weather.

16

2015 Financial Targets . . . .

Target Actual

Adjusted EPS (non-GAAP) $1.87—$1.89 $1.89 ?

+6% to +7% +7%

Operating cash flow (mils) $1,550 $1,640 ?

Dividend payout ratio > 62% > 62% ?

Customer price decreases

Electric ?(3)% ?(3)%

Gas ?(3)% ?(6)%

FFO/Average debt 18% 18%

Capital investment (bils) $1.6 $1.8 ?

. . . . 13th year of transparent, consistent, strong performance

17

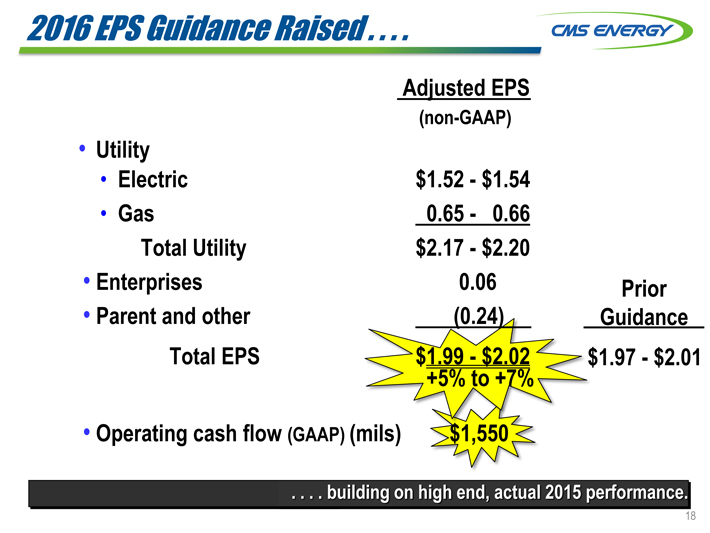

2016 EPS Guidance Raised . . . .

Utility

Electric

Gas

Total Utility

Enterprises

Parent and other Total EPS

Operating cash flow (GAAP) (mils)

Adjusted EPS

(non-GAAP)

$1.52

- $

1.54

0.65

-

0.66

$2.17

- $

2.20

0.06

(0.24)

$1.99

- $

2.02

+5%

to

+7%

$1,550

Prior Guidance $1.97—$2.01

. . . . building on high end, actual 2015 performance.

18

a

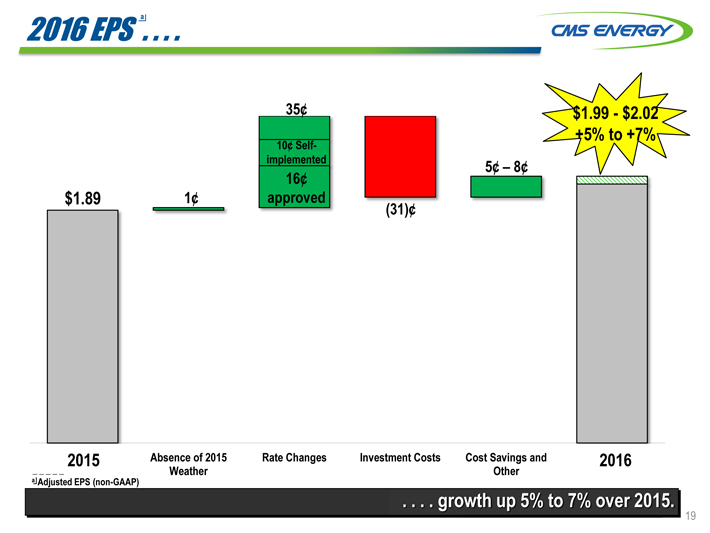

2016 EPS . . . .

+5% to +7%

implemented 5¢ – 8¢

2015 Absence of 2015 Rate Changes Investment Costs Cost Savings and 2016

Weather Other

a Adjusted EPS (non-GAAP)

. . . . growth up 5% to 7% over 2015.

19

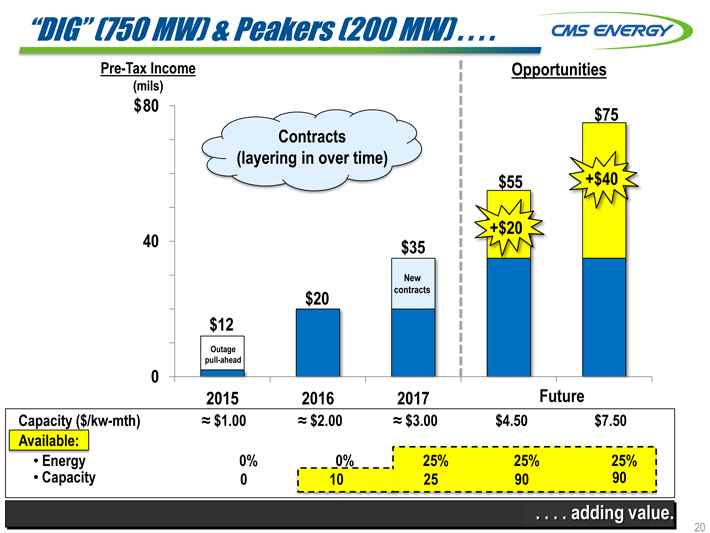

“DIG” (750 MW) & Peakers (200 MW) . . . .

Pre-Tax Income Opportunities

(mils)

$ 80 $75

Contracts

(layering in over time)

$ 55 +$ 40

+$ 20

40 $ 35

New

$20 contracts

$12

Outage

pull-ahead

0

2015 2016 2017 Future

Capacity ($/kw-mth) ? $1.00 ? $2.00 ? $3.00 $4.50 $7.50

Available:

• Energy 0% 0% 25% 25% 25%

Capacity 0 10 25 90 90

. . . . adding value.

20

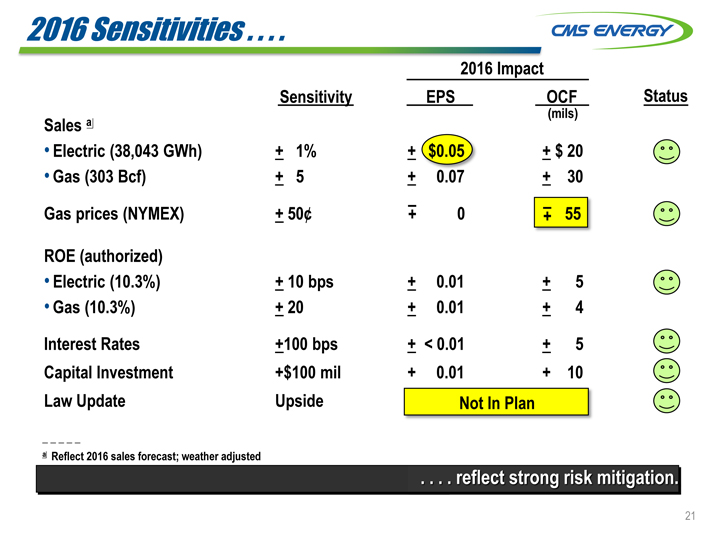

2016 Sensitivities . . . .

2016 Impact

Sensitivity EPS OCF Status

(mils)

Sales a

• Electric (38,043 GWh) + 1% + $0.05 + $ 20

• Gas (303 Bcf) + 5 + 0.07 + 30

Gas prices (NYMEX) + 50¢ + – 0 + – 55

ROE (authorized)

• Electric (10.3%) + 10 bps + 0.01 + 5

• Gas (10.3%) + 20 + 0.01 + 4

Interest Rates +100 bps + < 0.01 + 5

Capital Investment +$100 mil + 0.01 + 10

Law Update Upside Not In Plan

a Reflect 2016 sales forecast; weather adjusted

. . . . reflect strong risk mitigation.

21

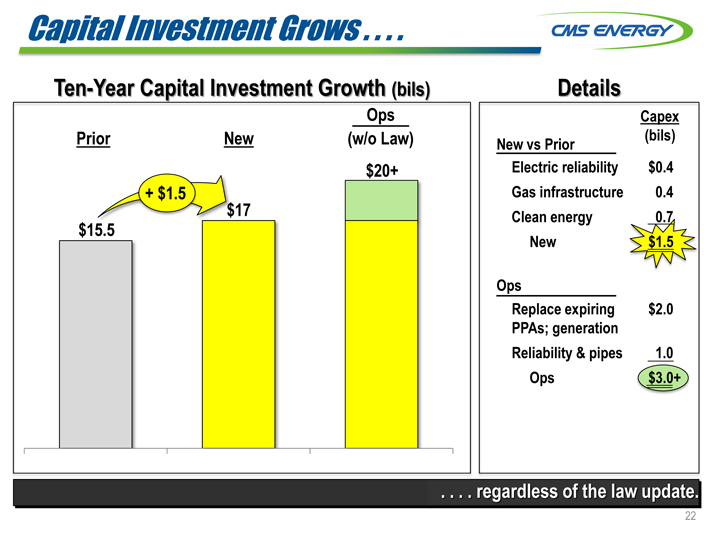

Capital Investment Grows . . . .

Ten-Year Capital Investment Growth (bils)

Ops

Prior New(w/o Law)

$20+

+ $1.5

17

$15.5

Details

Capex

New vs Prior(bils)

Electric reliability $ 0.4

Gas infrastructure 0.4

Clean energy 0.7

New $ 1.5

Ops

Replace expiring $ 2.0

PPAs; generation

Reliability & pipes 1.0

Ops $ 3.0+

. . . . regardless of the law update.

22

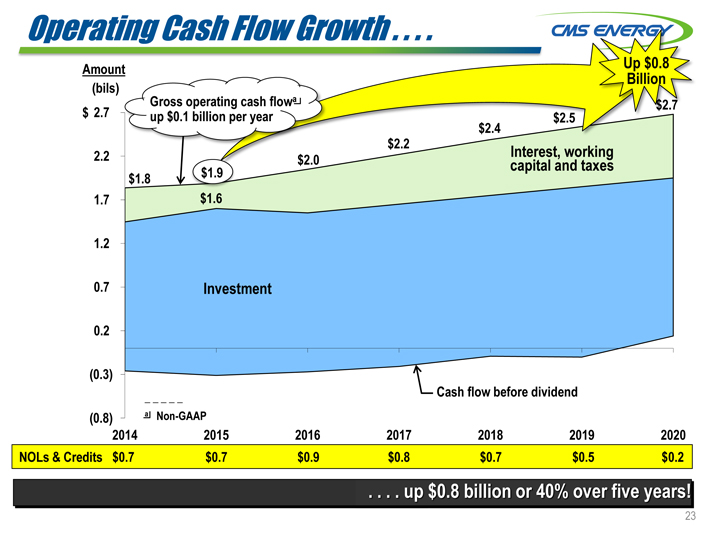

Operating Cash Flow Growth . . . .

Amount Up $0.8

(bils) Billion

Gross operating cash flowa

$ 2.7 up $0.1 billion per year $2.5

2.2

$1.8 $1.9

1.7 $1.6

1.2

0.7 Investment

0.2

(0.3)

Cash flow before dividend

(0.8) a Non-GAAP

2014 2015 2016 2017 2018 2019 2020

NOLs & Credits $0.7 $0.7 $0.9 $0.8 $0.7 $0.5 $0.2

. . . . up $0.8 billion or 40% over five years!

23

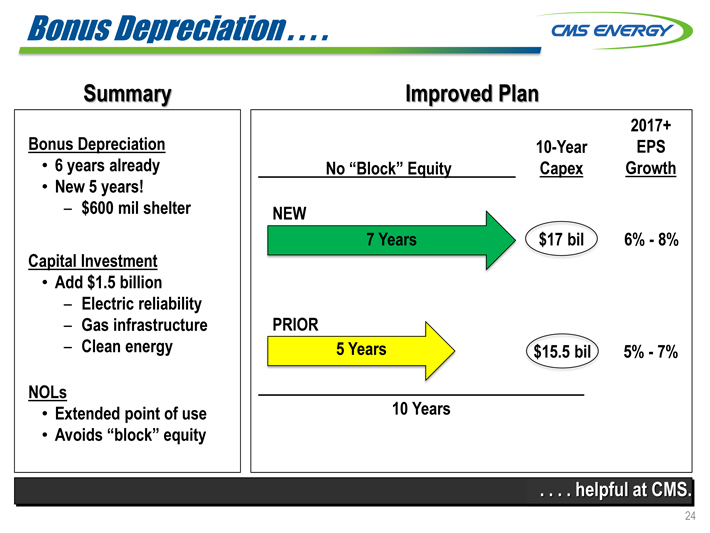

Bonus Depreciation . . . .

Summary

Bonus Depreciation

6 years already

New 5 years!

– $600 mil shelter

Capital Investment

Add $1.5 billion

– Electric reliability

– Gas infrastructure

– Clean energy

NOLs

Extended point of use

Avoids “block” equity

Improved Plan

2017+

10-Year EPS

No “Block” Equity Capex Growth

7 Years 6%—8%

PRIOR

5 Years 5%—7%

10 Years

. . . . helpful at CMS.

24

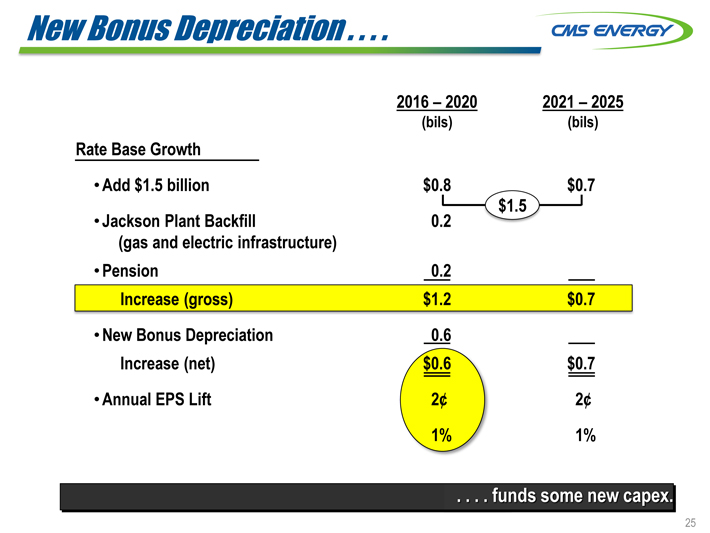

New Bonus Depreciation . . . .

2016 – 2020 2021 – 2025

(bils)(bils)

Rate Base Growth

• Add $1.5 billion $0.8 $0.7

$ 1.5

• Jackson Plant Backfill 0.2

(gas and electric infrastructure)

• Pension 0.2

Increase (gross) $1.2 $0.7

New Bonus Depreciation 0.6

Increase (net) $0.6 $0.7

Annual EPS Lift 2¢ 2¢

1% 1%

. . . . funds some new capex.

25

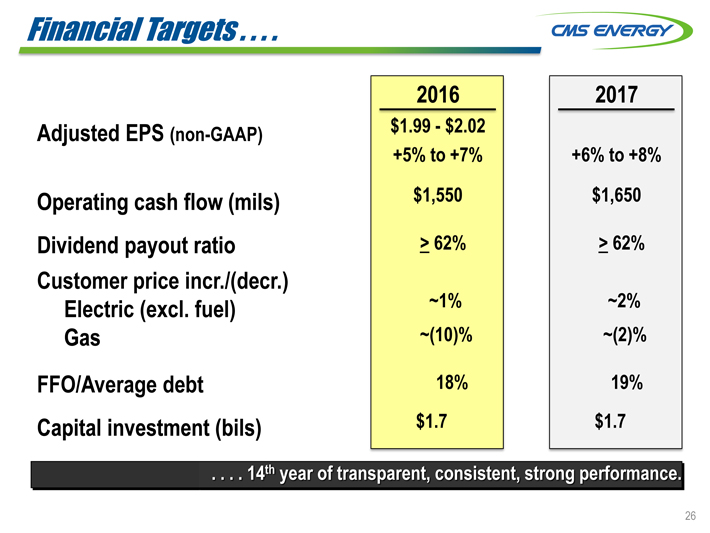

Financial Targets . . . .

2016 2017

Adjusted EPS (non-GAAP) $1.99—$2.02

+5% to +7% +6% to +8%

Operating cash flow (mils) $1,550 $1,650

Dividend payout ratio > 62% > 62%

Customer price incr./(decr.)

Electric (excl. fuel) ~1% ~2%

Gas ~(10)% ~(2)%

FFO/Average debt 18% 19%

Capital investment (bils) $1.7 $1.7

. . . . 14th year of transparent, consistent, strong performance.

26

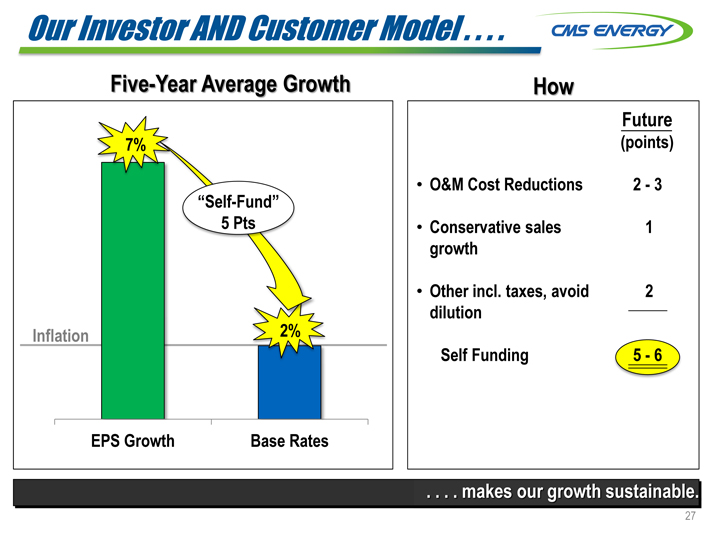

Our Investor AND Customer Model . . . .

Five-Year Average Growth

7%

“Self-Fund”

5 Pts

Inflation 2%

EPS Growth Base Rates

How

Future

(points)

O&M Cost Reductions 2—3

Conservative sales 1

growth

Other incl. taxes, avoid 2

dilution

Self Funding 5—6

. . . . makes our growth sustainable.

27

Q & A

Appendix

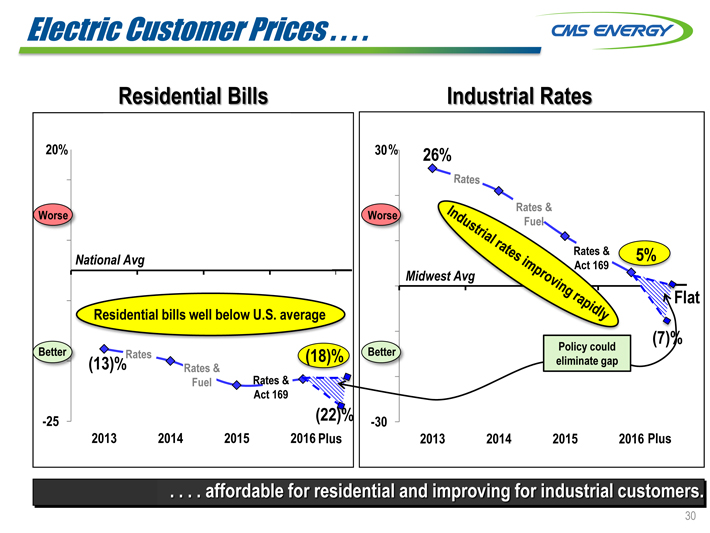

Electric Customer Prices . . . .

Residential Bills Industrial Rates

20% 30 % 26%

Worse Worse

National Avg 5%

Mid

Flat

Residential bills well below U.S. average

(7)%

Better(13)%Rates Rates &(18)% Better eliminate Policy could gap

Fuel Rates &

Act 169

-25(22)% -30

2013 2014 2015 2016 Plus 2013 2014 2015 2016 Plus

. . . . affordable for residential and improving for industrial customers.

30

Capacity Diversity . . . .

Nuclear

8%

Oil

10% Coal reduced

Coal by over 40%!

Purchases <24% 2nd best in U.S.

3%

Renewables 2016

10%

Pumped

Nuclear Storage Gas

Oil 6% 8% 11% 34% Future Capacity Mix

Renewables

3%

• More Renewables

Pumped Coal

Storage 41% • Expanded Pumped

11% 2005 Storage

Gas • Clean Energy

31% Resources

. . . . evolving to cleaner generation and becoming more cost competitive.

31

31

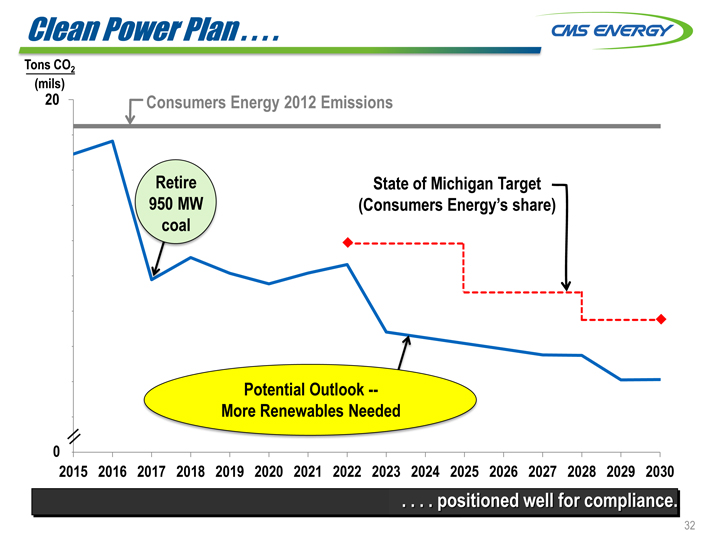

Clean Power Plan . . . .

Tons CO2

(mils)

20 Consumers Energy 2012 Emissions

Retire State of Michigan Target

950 MW(Consumers Energy’s share)

coal

Potential Outlook —

More Renewables Needed

0

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

. . . . positioned well for compliance.

32

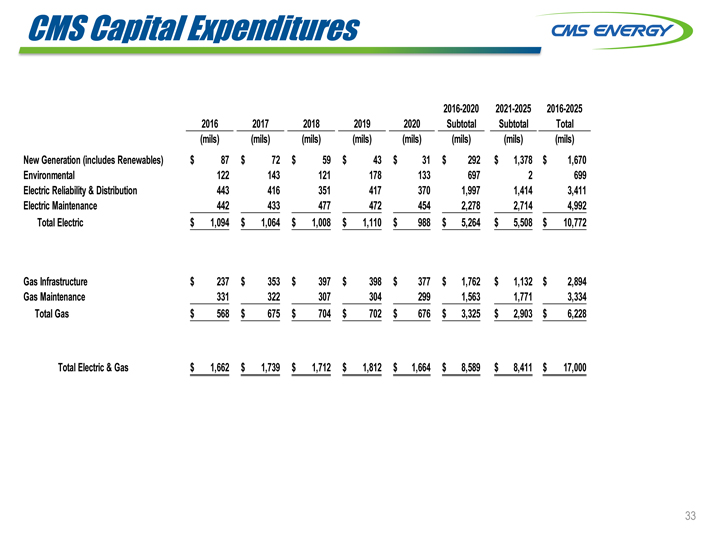

CMS Capital Expenditures

2016-2020 2021-2025 2016-2025

2016 2017 2018 2019 2020 Subtotal Subtotal Total

(mils)(mils)(mils)(mils)(mils)(mils)(mils)(mils)

New Generation (includes Renewables) $ 87 $ 72 $ 59 $ 43 $ 31 $ 292 $ 1,378 $ 1,670

Environmental 122 143 121 178 133 697 2 699

Electric Reliability & Distribution 443 416 351 417 370 1,997 1,414 3,411

Electric Maintenance 442 433 477 472 454 2,278 2,714 4,992

Total Electric $ 1,094 $ 1,064 $ 1,008 $ 1,110 $ 988 $ 5,264 $ 5,508 $ 10,772

Gas Infrastructure $ 237 $ 353 $ 397 $ 398 $ 377 $ 1,762 $ 1,132 $ 2,894

Gas Maintenance 331 322 307 304 299 1,563 1,771 3,334

Total Gas $ 568 $ 675 $ 704 $ 702 $ 676 $ 3,325 $ 2,903 $ 6,228

Total Electric & Gas $ 1,662 $ 1,739 $ 1,712 $ 1,812 $ 1,664 $ 8,589 $ 8,411 $ 17,000

33

a

2015 EPS . . . .

$1.89

+7%

19¢

$1.77

27¢

Electric 17¢

(19)¢ Gas 10¢

(15)¢

Abs of ’14(18)¢

2015(1)

(19)¢

2014 Weather Investment Costs Rate Changes Cost Savings and 2015

Other

a Adjusted EPS (non-GAAP)

. . . . growth +7% over 2014, high end of guidance.

34

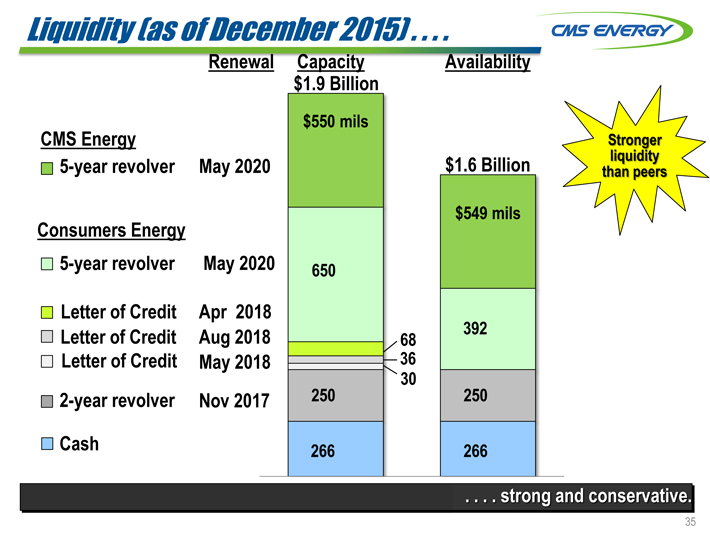

Liquidity (as of December 2015)

Renewal Capacity Availability

$1.9 Billion

$550 mils

CMS Energy Stronger

liquidity

5-year revolver May 2020 $1.6 Billion than peers

$549 mils

Consumers Energy

5-year revolver May 2020 650

Letter of Credit Apr 2018

Letter of Credit Aug 2018 68 392

Letter of Credit May 2018 36

30

2-year revolver Nov 2017 250 250

Cash 266 266

. . . . strong and conservative.

35

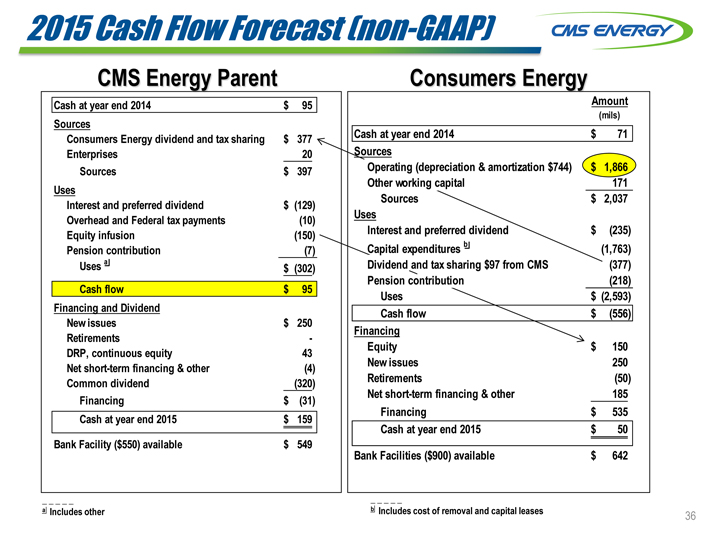

2015 Cash Flow Forecast (non-GAAP)

CMS Energy Parent

Cash at year end 2014 $ 95

Sources

Consumers Energy dividend and tax sharing $ 377

Enterprises 20

Sources $ 397

Uses

Interest and preferred dividend $(129)

Overhead and Federal tax payments(10)

Equity infusion(150)

Pension contribution(7)

Uses a $(302)

Cash flow $ 95

Financing and Dividend

New issues $ 250

Retirements -

DRP, continuous equity 43

Net short-term financing & other(4)

Common dividend(320)

Financing $(31)

Cash at year end 2015 $ 159

Bank Facility ($550) available $ 549

Consumers Energy

Amount

(mils)

Cash at year end 2014 $ 71

Sources

Operating (depreciation & amortization $744) $ 1,866

Other working capital 171

Sources $ 2,037

Uses

Interest and preferred dividend $(235)

Capital expenditures b(1,763)

Dividend and tax sharing $97 from CMS(377)

Pension contribution(218)

Uses $(2,593)

Cash flow $(556)

Financing

Equity $ 150

New issues 250

Retirements(50)

Net short-term financing & other 185

Financing $ 535

Cash at year end 2015 $ 50

Bank Facilities ($900) available $ 642

a Includes other b Includes cost of removal and capital leases

36

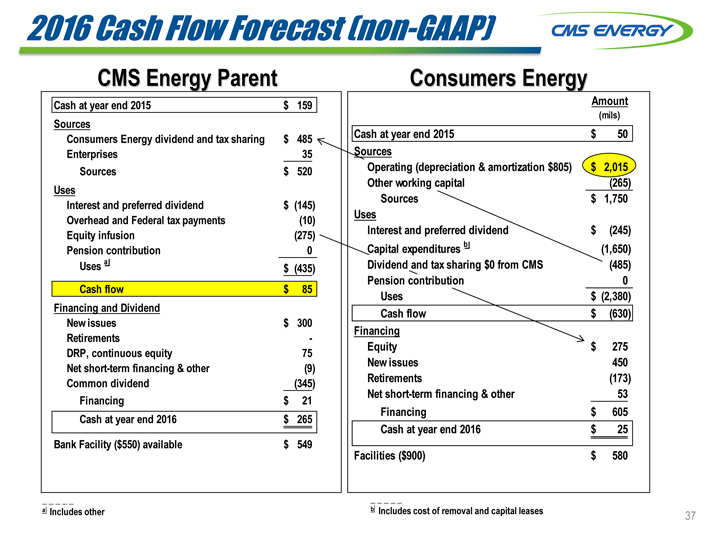

2016 Cash Flow Forecast (non-GAAP)

CMS Energy Parent

Cash at year end 2015 $ 159

Sources

Consumers Energy dividend and tax sharing $ 485

Enterprises 35

Sources $ 520

Uses

Interest and preferred dividend $(145)

Overhead and Federal tax payments(10)

Equity infusion(275)

Pension contribution 0

Uses a $(435)

Cash flow $ 85

Financing and Dividend

New issues $ 300

Retirements -

DRP, continuous equity 75

Net short-term financing & other(9)

Common dividend(345)

Financing $ 21

Cash at year end 2016 $ 265

Bank Facility ($550) available $ 549

Consumers Energy

Amount

(mils)

Cash at year end 2015 $ 50

Sources

Operating (depreciation & amortization $805) $ 2,015

Other working capital(265)

Sources $ 1,750

Uses

Interest and preferred dividend $(245)

Capital expenditures b(1,650)

Dividend and tax sharing $0 from CMS(485)

Pension contribution 0

Uses $(2,380)

Cash flow $(630)

Financing

Equity $ 275

New issues 450

Retirements(173)

Net short-term financing & other 53

Financing $ 605

Cash at year end 2016 $ 25

Facilities ($900) $ 580

a Includes other b Includes cost of removal and capital leases

37

GAAP Reconciliation

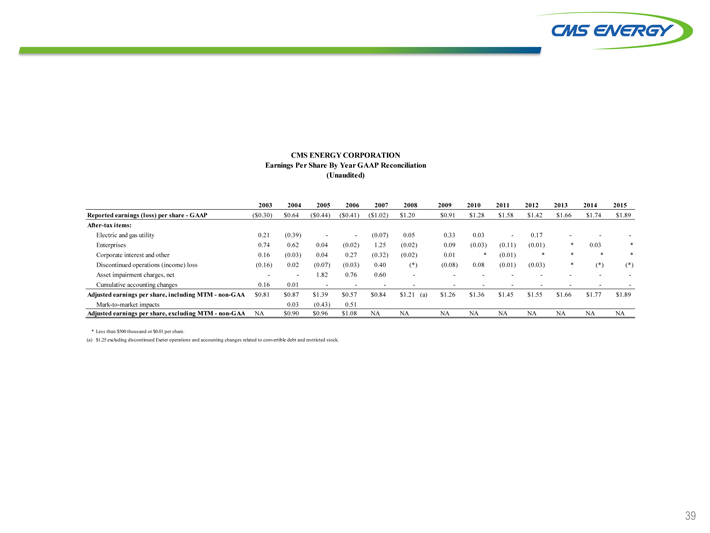

CMS ENERGY CORPORATION

Earnings Per Share By Year GAAP Reconciliation

(Unaudited)

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Reported earnings (loss) per share—GAAP($0.30) $0.64($0.44)($0.41)($1.02) $1.20 $0.91 $1.28 $1.58 $1.42 $ 1.66 $ 1.74 $ 1.89

After-tax items:

Electric and gas utility 0.21(0.39) —(0.07) 0.05 0.33 0.03—0.17 — -

Enterprises 0.74 0.62 0.04(0.02) 1.25(0.02) 0.09(0.03)(0.11)(0.01)* 0.03*

Corporate interest and other 0.16(0.03) 0.04 0.27(0.32)(0.02) 0.01*(0.01)****

Discontinued operations (income) loss(0.16) 0.02(0.07)(0.03) 0.40(*)(0.08) 0.08(0.01)(0.03)*(*)(*)

Asset impairment charges, net — 1.82 0.76 0.60 — — — —

Cumulative accounting changes 0.16 0.01 — — — — — -

Adjusted earnings per share, including MTM—non-GAA $0.81 $0.87 $1.39 $0.57 $0.84 $1.21 (a) $1.26 $1.36 $1.45 $1.55 $ 1.66 $ 1.77 $ 1.89

Mark-to-market impacts 0.03(0.43) 0.51

Adjusted earnings per share, excluding MTM—non-GAA NA $0.90 $0.96 $1.08 NA NA NA NA NA NA NA NA NA

* Less than $500 thousand or $0.01 per share.

(a) $1.25 excluding discontinued Exeter operations and accounting changes related to convertible debt and restricted stock.

39

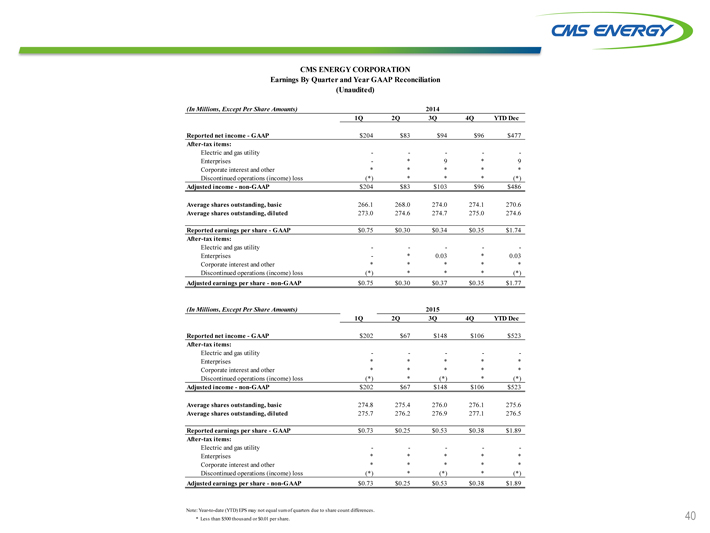

CMS ENERGY CORPORATION

Earnings By Quarter and Year GAAP Reconciliation

(Unaudited)

(In Millions, Except Per Share Amounts) 2014

1Q 2Q 3Q 4Q YTD Dec

Reported net income—GAAP $204 $83 $94 $96 $477

After-tax items:

Electric and gas utility — — -

Enterprises -* 9* 9

Corporate interest and other*****

Discontinued operations (income) loss(*)***(*)

Adjusted income—non-GAAP $204 $83 $103 $96 $486

Average shares outstanding, basic 266.1 268.0 274.0 274.1 270.6

Average shares outstanding, diluted 273.0 274.6 274.7 275.0 274.6

Reported earnings per share—GAAP $0.75 $0.30 $0.34 $0.35 $1.74

After-tax items:

Electric and gas utility — — -

Enterprises -* 0.03* 0.03

Corporate interest and other*****

Discontinued operations (income) loss(*)***(*)

Adjusted earnings per share—non-GAAP $0.75 $0.30 $0.37 $0.35 $1.77

(In Millions, Except Per Share Amounts) 2015

1Q 2Q 3Q 4Q YTD Dec

Reported net income—GAAP $202 $67 $148 $106 $523

After-tax items:

Electric and gas utility — — -

Enterprises*****

Corporate interest and other*****

Discontinued operations (income) loss(*)*(*)*(*)

Adjusted income—non-GAAP $202 $67 $148 $106 $523

Average shares outstanding, basic 274.8 275.4 276.0 276.1 275.6

Average shares outstanding, diluted 275.7 276.2 276.9 277.1 276.5

Reported earnings per share—GAAP $0.73 $0.25 $0.53 $0.38 $1.89

After-tax items:

Electric and gas utility — — -

Enterprises*****

Corporate interest and other*****

Discontinued operations (income) loss(*)*(*)*(*)

Adjusted earnings per share—non-GAAP $0.73 $0.25 $0.53 $0.38 $1.89

Note: Year-to-date (YTD) EPS may not equal sum of quarters due to share count differences.

* Less than $500 thousand or $0.01 per share.

40

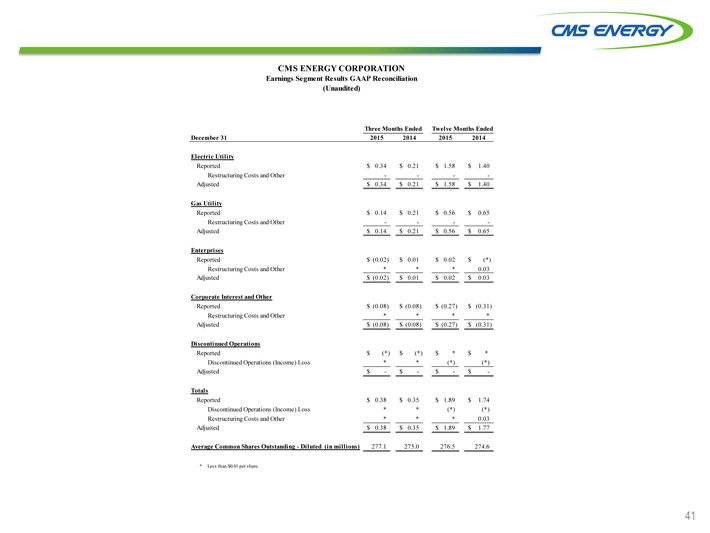

CMS ENERGY CORPORATION

Earnings Segment Results GAAP Reconciliation

(Unaudited)

Three Months Ended Twelve Months Ended

December 31 2015 2014 2015 2014

Electric Utility

Reported $ 0.34 $ 0.21 $ 1.58 $ 1.40

Restructuring Costs and Other — —

Adjusted $ 0.34 $ 0.21 $ 1.58 $ 1.40

Gas Utility

Reported $ 0.14 $ 0.21 $ 0.56 $ 0.65

Restructuring Costs and Other — —

Adjusted $ 0.14 $ 0.21 $ 0.56 $ 0.65

Enterprises

Reported $(0.02) $ 0.01 $ 0.02 $(*)

Restructuring Costs and Other*** 0.03

Adjusted $(0.02) $ 0.01 $ 0.02 $ 0.03

Corporate Interest and Other

Reported $(0.08) $(0.08) $(0.27) $(0.31)

Restructuring Costs and Other****

Adjusted $(0.08) $(0.08) $(0.27) $(0.31)

Discontinued Operations

Reported $(*) $(*) $* $*

Discontinued Operations (Income) Loss**(*)(*)

Adjusted $—$—$—$ -

Totals

Reported $ 0.38 $ 0.35 $ 1.89 $ 1.74

Discontinued Operations (Income) Loss**(*)(*)

Restructuring Costs and Other*** 0.03

Adjusted $ 0.38 $ 0.35 $ 1.89 $ 1.77

Average Common Shares Outstanding—Diluted (in millions) 277.1 275.0 276.5 274.6

* Less than $0.01 per share.

41

Consumers Energy

2015 Cash Flow GAAP Reconciliation (in millions) (unaudited)

Reclassifications From Sources and Uses to Statement of Cash Flows

Interest/ Capital

Presentation Sources and Uses Tax Other Financing Other Working Lease Pymts Securitization Common Consolidated Statements of Cash Flows

non-GAAP Sharing Payments Capital and Other Debt Pymts Dividends GAAP

Description Amount Operating as Operating as Investing as Financing as Financing as Financing Amount Description

Cash at year end 2014 $ 71 $—$—$—$—$—$—$ 71 Cash at year end 2014

Sources

Operating (dep & amort $744) $ 1,866

Other working capital 171—Net cash provided by

Sources $ 2,037 $ 97 $(235) $(202) $ 23 $ 74 $—$ 1,794 operating activities

Uses

Interest and preferred dividends $(235)

Capital expenditures a(1,763)

Dividends/tax sharing to CMS(377)

Pension Contribution(218) — Net cash used in

Uses $(2,593) $(97) $ 235 $ 202 $(2) $—$ 474 $ (1,781) investing activities

Cash flow from

Cash flow $(556) $—$—$—$ 21 $ 74 $ 474 $ 13 operating and

investing activities

Financing

Equity $ 150

New Issues 250

Retirements(50)

Net short-term financing & other 185 — Net cash used in

Financing $ 535 $—$—$—$(21) $(74) $(474) $ (34) financing activities

Net change in cash $(21) $—$—$—$—$—$—$ (21) Net change in cash

Cash at year end 2015 $ 50 $—$—$—$—$—$—$ 50 Cash at year end 2015

a Includes cost of removal and capital leases

42

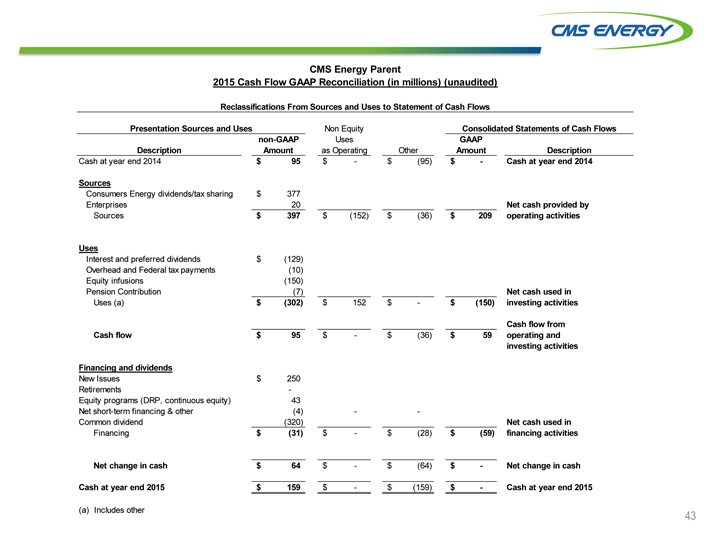

CMS Energy Parent

2015 Cash Flow GAAP Reconciliation (in millions) (unaudited)

Reclassifications From Sources and Uses to Statement of Cash Flows

Presentation Sources and Uses Non Equity Consolidated Statements of Cash Flows

non-GAAP Uses GAAP

Description Amount as Operating Other Amount Description

Cash at year end 2014 $ 95 $—$(95) $—Cash at year end 2014

Sources

Consumers Energy dividends/tax sharing $ 377

Enterprises 20 Net cash provided by

Sources $ 397 $(152) $(36) $ 209 operating activities

Uses

Interest and preferred dividends $ (129)

Overhead and Federal tax payments(10)

Equity infusions(150)

Pension Contribution(7) Net cash used in

Uses (a) $ (302) $ 152 $—$(150) investing activities

Cash flow from

Cash flow $ 95 $—$(36) $ 59 operating and

investing activities

Financing and dividends

New Issues $ 250

Retirements -

Equity programs (DRP, continuous equity) 43

Net short-term financing & other(4) —

Common dividend(320) Net cash used in

Financing $(31) $—$(28) $(59) financing activities

Net change in cash $ 64 $—$(64) $—Net change in cash

Cash at year end 2015 $ 159 $—$(159) $—Cash at year end 2015

(a) Includes other

43

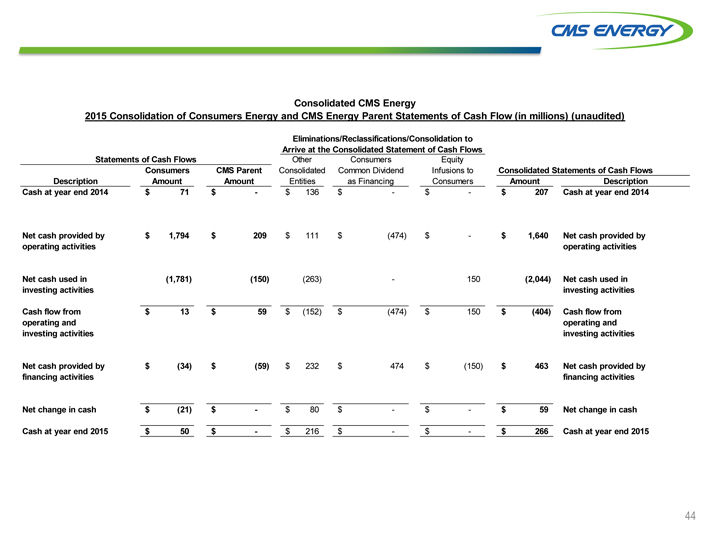

Consolidated CMS Energy

2015 Consolidation of Consumers Energy and CMS Energy Parent Statements of Cash Flow (in millions) (unaudited)

Eliminations/Reclassifications/Consolidation to

Arrive at the Consolidated Statement of Cash Flows

Statements of Cash Flows Other Consumers Equity

Consumers CMS Parent Consolidated Common Dividend Infusions to Consolidated Statements of Cash Flows

Description Amount Amount Entities as Financing Consumers Amount Description

Cash at year end 2014 $ 71 $—$ 136 $—$—$ 207 Cash at year end 2014

Net cash provided by $ 1,794 $ 209 $ 111 $(474) $—$ 1,640 Net cash provided by

operating activities operating activities

Net cash used in(1,781)(150)(263)—150(2,044) Net cash used in

investing activities investing activities

Cash flow from $ 13 $ 59 $(152) $(474) $ 150 $(404) Cash flow from

operating and operating and

investing activities investing activities

Net cash provided by $(34) $(59) $ 232 $ 474 $(150) $ 463 Net cash provided by

financing activities financing activities

Net change in cash $(21) $—$ 80 $—$—$ 59 Net change in cash

Cash at year end 2015 $ 50 $—$ 216 $—$—$ 266 Cash at year end 2015

44

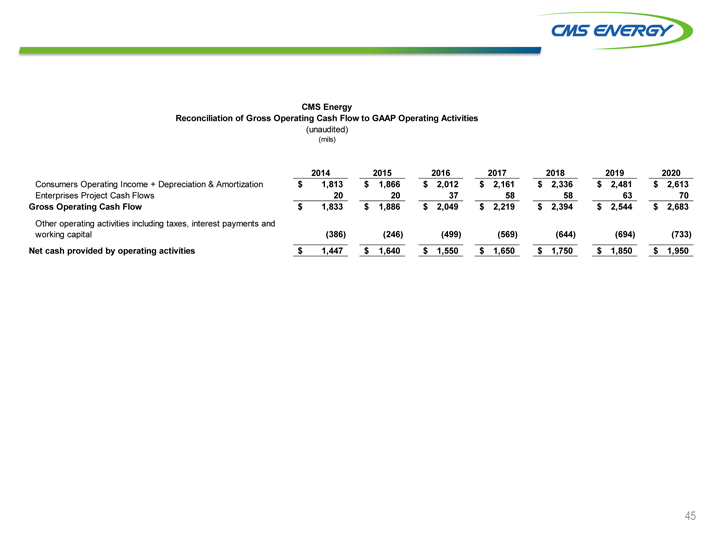

CMS Energy

Reconciliation of Gross Operating Cash Flow to GAAP Operating Activities

(unaudited)

(mils)

2014 2015 2016 2017 2018 2019 2020

Consumers Operating Income + Depreciation & Amortization $ 1,813 $ 1,866 $ 2,012 $ 2,161 $ 2,336 $ 2,481 $ 2,613

Enterprises Project Cash Flows 20 20 37 58 58 63 70

Gross Operating Cash Flow $ 1,833 $ 1,886 $ 2,049 $ 2,219 $ 2,394 $ 2,544 $ 2,683

Other operating activities including taxes, interest payments and

working capital(386)(246)(499)(569)(644)(694)(733)

Net cash provided by operating activities $ 1,447 $ 1,640 $ 1,550 $ 1,650 $ 1,750 $ 1,850 $ 1,950

45

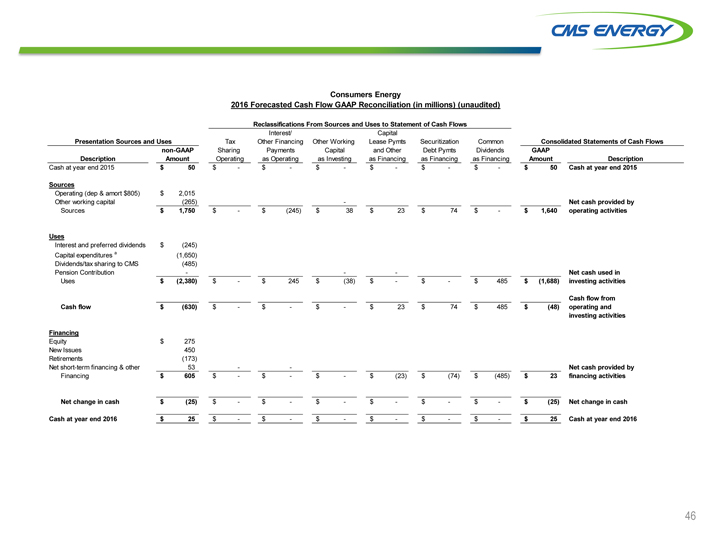

Consumers Energy

2016 Forecasted Cash Flow GAAP Reconciliation (in millions) (unaudited)

Reclassifications From Sources and Uses to Statement of Cash Flows

Interest/ Capital

Presentation Sources and Uses Tax Other Financing Other Working Lease Pymts Securitization Common Consolidated Statements of Cash Flows

non-GAAP Sharing Payments Capital and Other Debt Pymts Dividends GAAP

Description Amount Operating as Operating as Investing as Financing as Financing as Financing Amount Description

Cash at year end 2015 $ 50 $—$—$—$—$—$—$ 50 Cash at year end 2015

Sources

Operating (dep & amort $805) $ 2,015

Other working capital(265)—Net cash provided by

Sources $ 1,750 $—$(245) $ 38 $ 23 $ 74 $—$ 1,640 operating activities

Uses

Interest and preferred dividends $(245)

Capital expenditures a(1,650)

Dividends/tax sharing to CMS(485)

Pension Contribution ——Net cash used in

Uses $(2,380) $—$ 245 $(38) $—$—$ 485 $ (1,688) investing activities

Cash flow from

Cash flow $(630) $—$—$—$ 23 $ 74 $ 485 $ (48) operating and

investing activities

Financing

Equity $ 275

New Issues 450

Retirements(173)

Net short-term financing & other 53 — Net cash provided by

Financing $ 605 $—$—$—$(23) $(74) $(485) $ 23 financing activities

Net change in cash $(25) $—$—$—$—$—$—$ (25) Net change in cash

Cash at year end 2016 $ 25 $—$—$—$—$—$—$ 25 Cash at year end 2016

46

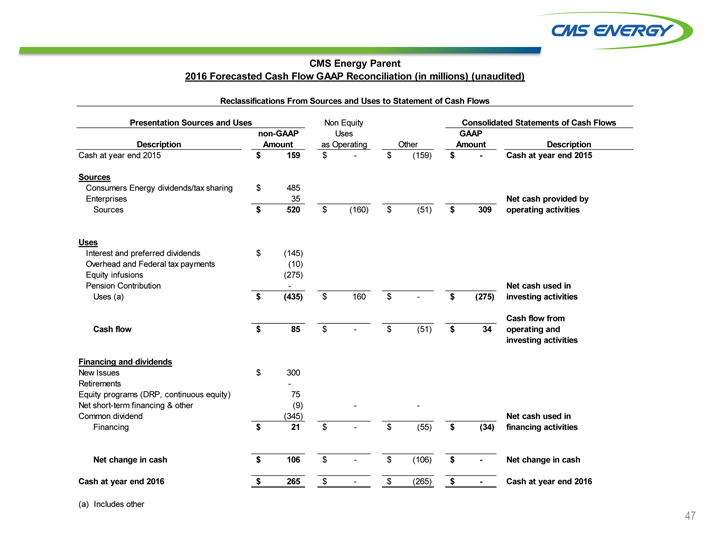

CMS Energy Parent

2016 Forecasted Cash Flow GAAP Reconciliation (in millions) (unaudited)

Reclassifications From Sources and Uses to Statement of Cash Flows

Presentation Sources and Uses Non Equity Consolidated Statements of Cash Flows

non-GAAP Uses GAAP

Description Amount as Operating Other Amount Description

Cash at year end 2015 $ 159 $—$(159) $—Cash at year end 2015

Sources

Consumers Energy dividends/tax sharing $ 485

Enterprises 35 Net cash provided by

Sources $ 520 $(160) $(51) $ 309 operating activities

Uses

Interest and preferred dividends $(145)

Overhead and Federal tax payments(10)

Equity infusions(275)

Pension Contribution—Net cash used in

Uses (a) $(435) $ 160 $—$(275) investing activities

Cash flow from

Cash flow $ 85 $—$(51) $ 34 operating and

investing activities

Financing and dividends

New Issues $ 300

Retirements -

Equity programs (DRP, continuous equity) 75

Net short-term financing & other(9) —

Common dividend(345) Net cash used in

Financing $ 21 $—$(55) $(34) financing activities

Net change in cash $ 106 $—$(106) $—Net change in cash

Cash at year end 2016 $ 265 $—$(265) $—Cash at year end 2016

(a) Includes other

47

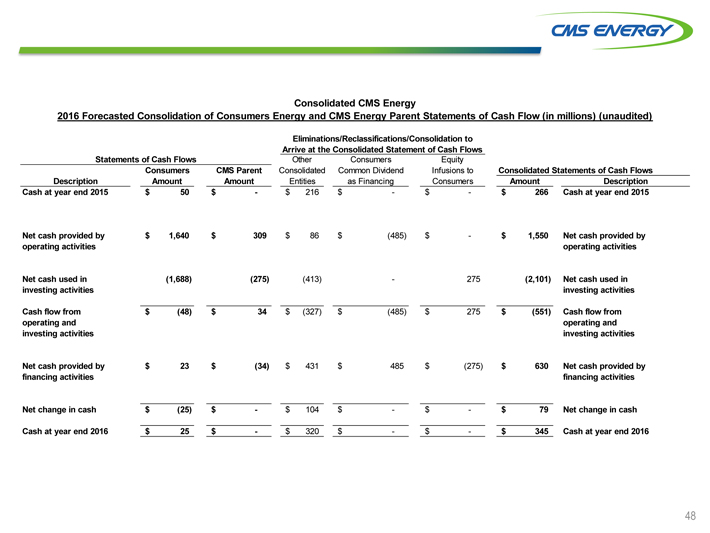

Consolidated CMS Energy

2016 Forecasted Consolidation of Consumers Energy and CMS Energy Parent Statements of Cash Flow (in millions) (unaudited)

Eliminations/Reclassifications/Consolidation to

Arrive at the Consolidated Statement of Cash Flows

Statements of Cash Flows Other Consumers Equity

Consumers CMS Parent Consolidated Common Dividend Infusions to Consolidated Statements of Cash Flows

Description Amount Amount Entities as Financing Consumers Amount Description

Cash at year end 2015 $ 50 $—$ 216 $—$—$ 266 Cash at year end 2015

Net cash provided by $ 1,640 $ 309 $ 86 $(485) $—$ 1,550 Net cash provided by

operating activities operating activities

Net cash used in(1,688)(275)(413)—275(2,101) Net cash used in

investing activities investing activities

Cash flow from $(48) $ 34 $(327) $(485) $ 275 $(551) Cash flow from

operating and operating and

investing activities investing activities

Net cash provided by $ 23 $(34) $ 431 $ 485 $(275) $ 630 Net cash provided by

financing activities financing activities

Net change in cash $(25) $—$ 104 $—$—$ 79 Net change in cash

Cash at year end 2016 $ 25 $—$ 320 $—$—$ 345 Cash at year end 2016

48