| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-260277-06 | ||

June 24, 2024

BENCHMARK 2024-V8

Mortgage Trust

Free Writing Prospectus

Collateral Term Sheet

$1,009,985,421

(Approximate Total Mortgage Pool Balance)

$895,099,000

(Approximate Offered Certificates)

Deutsche Mortgage & Asset Receiving Corporation Depositor |

Commercial Mortgage Pass-Through Certificates

Series 2024-V8

German American Capital Corporation Citi Real Estate Funding Inc. Goldman Sachs Mortgage Company Bank of Montreal Barclays Capital Real Estate Inc. |

As Sponsors and Mortgage Loan Sellers

| Deutsche Bank Securities | Goldman Sachs & Co. LLC | BMO Capital Markets | Barclays | Citigroup |

Co-Lead Managers and Joint Bookrunners

| AmeriVet Securities | Drexel Hamilton |

Co-Managers

The depositor has filed a registration statement (including the prospectus) with the Securities and Exchange Commission (File No. 333-260277) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the Securities and Exchange Commission for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the Securities and Exchange Commission website at www.sec.gov. Alternatively, the depositor or Deutsche Bank Securities Inc., any other underwriter, or any dealer participating in this offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-503-4611 or by emailing: prospectus.cpdg@db.com. The offered certificates referred to in these materials, and the asset pool backing them, are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. You understand that, when you are considering the purchase of these certificates, a contract of sale will come into being no sooner than the date on which the relevant class has been priced and we have verified the allocation of certificates to be made to you; any “indications of interest” expressed by you, and any “soft circles” generated by us, will not create binding contractual obligations for you or us. This free writing prospectus does not contain all information that is required to be included in the prospectus.

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 1 | ||

Benchmark 2024-V8 Mortgage Trust |

| KEY FEATURES OF SECURITIZATION |

| Capitalized terms used but not defined herein have the meanings assigned to them in the Preliminary Prospectus expected to be dated June 24, 2024 relating to the offered certificates (hereinafter referred to as the “Preliminary Prospectus”). |

| Offering Terms: | |

| Co-Lead Managers and Joint Bookrunners: | Deutsche Bank Securities Inc., Citigroup Global Markets Inc., Goldman Sachs & Co. LLC, BMO Capital Markets Corp. and Barclays Capital Inc. |

| Co-Managers: | AmeriVet Securities, Inc., and Drexel Hamilton, LLC |

| Sponsors and Mortgage Loan Sellers: | German American Capital Corporation* (“GACC”) (18.7%), Citi Real Estate Funding Inc. (“CREFI”) (54.6%), Goldman Sachs Mortgage Company (“GSMC”), (16.1%), Bank of Montreal (“BMO”) (7.1%) and Barclays Capital Real Estate Inc. (“BCREI”) (3.4%) *An indirect wholly owned subsidiary of Deutsche Bank AG |

| Master Servicer: | Wells Fargo Bank, National Association |

| Operating Advisor: | Park Bridge Lender Services LLC |

| Asset Representations Reviewer: | Park Bridge Lender Services LLC |

| Special Servicer: | LNR Partners, LLC |

| Certificate Administrator: | Computershare Trust Company, National Association |

| Trustee: | Computershare Trust Company, National Association |

| Rating Agencies: | S&P Global Ratings (“S&P”), Fitch Ratings, Inc. (“Fitch”) and Kroll Bond Rating Agency, LLC (“KBRA”). |

| Credit Risk Retention: | For a discussion on the manner in which the U.S. credit risk retention requirements are being satisfied by GACC, as retaining sponsor, see “Credit Risk Retention” in the Preliminary Prospectus. Note that this securitization transaction is not being structured to satisfy EU/UK risk retention and due diligence requirements. |

| Determination Date: | 11th day of each month, or if such 11th day is not a business day, the immediately following business day, commencing in August 2024. |

| Distribution Date: | 4th business day following the Determination Date in each month, commencing in August 2024. |

| Cut-off Date: | With respect to each mortgage loan, the later of the related payment date of such mortgage loan in July 2024 (or, in the case of any mortgage loan that has its first due date subsequent to July 2024, the date that would have been its due date in July 2024 under the terms of that mortgage loan if a monthly payment were scheduled to be due in that month) and the date of origination of such mortgage loan. Unless otherwise noted, all mortgage loan statistics are based on balances as of the Cut-off Date. |

| Closing Date: | On or about July 18, 2024 |

| Settlement Terms: | DTC, Euroclear and Clearstream, same day funds, with accrued interest. |

| ERISA Eligible: | All of the Offered Certificates are expected to be ERISA eligible. |

| SMMEA Eligible: | None of the Offered Certificates will be SMMEA eligible. |

| Day Count: | 30/360 |

| Tax Treatment: | REMIC |

| Rated Final Distribution Date: | July 2057 |

| Minimum Denominations: | $10,000 (for each class of offered principal balance certificates) and $100,000 (for each class of offered interest-only certificates) and in each case in multiples of $1 thereafter. |

| Clean-up Call: | 1% (with certain exceptions described under “Pooling and Servicing Agreement—Termination; Retirement of Certificates” in the Preliminary Prospectus) |

| Distribution of Collateral by Property Type |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 2 | ||

Benchmark 2024-V8 Mortgage Trust |

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

| Mortgage Loan Sellers | Number of Mortgage Loans | Number of Mortgaged Properties | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Roll-up Aggregate Cut-off Date Balance | Roll-up Aggregate % of Initial Outstanding Pool Balance | ||

| German American Capital Corporation | 7 | 17 | $149,700,000 | 14.8% | $189,174,253 | 18.7% | ||

| Citi Real Estate Funding Inc. | 19 | 36 | $551,935,000 | 54.6% | $551,935,000 | 54.6% | ||

| Goldman Sachs Mortgage Company | 3 | 3 | $93,360,000 | 9.2% | $162,960,000 | 16.1% | ||

| Bank of Montreal | 3 | 22 | $44,000,000 | 4.4% | $71,500,000 | 7.1% | ||

| Barclays Capital Real Estate Inc. | 1 | 1 | $8,100,000 | 0.8% | $34,416,168 | 3.4% | ||

| Goldman Sachs Mortgage Company / Bank of Montreal(1) | 1 | 1 | $97,100,000 | 9.6% | ||||

| German American Capital Corporation / Barclays Capital Real Estate Inc.(2) | 1 | 1 | $65,790,421 | 6.5% | ||||

| Total: | 35 | 81 | $1,009,985,421 | 100.0% | ||||

Collateral Facts | ||||||||

| Initial Outstanding Pool Balance: | $1,009,985,421 | |||||||

| Number of Mortgage Loans: | 35 | |||||||

| Number of Mortgaged Properties: | 81 | |||||||

| Average Mortgage Loan Cut-off Date Balance: | $28,856,726 | |||||||

| Weighted Average Mortgage Rate: | 6.96578% | |||||||

| Weighted Average Mortgage Loan Original Term to Maturity Date (months): | 60 | |||||||

| Weighted Average Mortgage Loan Remaining Term to Maturity Date (months): | 59 | |||||||

| Weighted Average Mortgage Loan Seasoning (months): | 1 | |||||||

| % of Mortgaged Properties Leased to a Single Tenant: | 11.9% | |||||||

Credit Statistics(3) | ||||||||

| Weighted Average Mortgage Loan U/W NCF DSCR: | 1.69x | |||||||

| Weighted Average Mortgage Loan Cut-off Date LTV(4): | 52.7% | |||||||

| Weighted Average Mortgage Loan Maturity Date LTV(4): | 52.1% | |||||||

| Weighted Average U/W NOI Debt Yield: | 13.6% | |||||||

Amortization Overview | ||||||||

| % Mortgage Loans with Amortization through Maturity Date: | 16.1% | |||||||

| % Mortgage Loans which pay Interest Only through Maturity Date: | 83.9% | |||||||

| % Mortgage Loans which pay Interest Only followed by Amortization through Maturity Date: | 0.0% | |||||||

| Weighted Average Remaining Amortization Term (months)(5): | 238 | |||||||

Loan Structural Features | ||||||||

| % Mortgage Loans with Upfront or Ongoing Tax Reserves: | 72.9% | |||||||

| % Mortgage Loans with Upfront or Ongoing Insurance Reserves: | 36.1% | |||||||

| % Mortgage Loans with Upfront or Ongoing Replacement Reserves(6): | 82.1% | |||||||

| % Mortgage Loans with Upfront or Ongoing TI/LC Reserves(7): | 82.1% | |||||||

| % Mortgage Loans with In Place Hard Lockboxes: | 60.1% | |||||||

| % Mortgage Loans with Cash Traps Triggered at DSCR Levels ≥ 1.10x: | 73.1% | |||||||

| % Mortgage Loans with Cash Traps Triggered at Debt Yield Levels ≥ 9.00%: | 24.1% | |||||||

Prepayment Provisions(8) | ||||||||

| % Mortgage Loans with Defeasance Only After a Lockout Period and Prior to an Open Period: | 76.7% | |||||||

| % Mortgage Loans with Yield Maintenance Prior to an Open Period: | 10.4% | |||||||

| % Mortgage Loans with Prepayment Only After a Lockout Period and Prior to an Open Period with a Yield Maintenance Charge: | 10.0% | |||||||

| % Mortgage Loans with Prepayment or Defeasance Only After a Lockout Period and Prior to an Open Period with Defeasance or a Yield Maintenance Charge: | 2.9% | |||||||

| (1) | Includes a $97.1 million non-controlling pari passu portion of the 640 5th Avenue whole loan. GSMC is selling Note A-5 in the outstanding principal balance of $69,600,000 as of the Cut-off Date and BMO is selling Notes A-9 and A-10 in the aggregate outstanding principal balance of $27,500,000 as of the Cut-off Date. |

| (2) | Includes the Sugarloaf Mills mortgage loan, as to which GACC is acting as mortgage loan seller of approximately $39.5 million of such mortgage loan and BCREI is acting as mortgage loan seller of approximately $26.3 million of such mortgage loan as of the Cut-off date. |

| (3) | The LTV, DSCR and Debt Yield calculations include any related pari passu companion loan(s) and exclude any related subordinate companion loan(s) and/or mezzanine loan(s). |

| (4) | With respect to 4 mortgaged properties (9.5%) (488 Madison, Lotus 315, Courtyard Marriott, TownePlace Suites), the Cut-off Date LTV Ratio and Maturity Date or LTV Ratio have been calculated using a value other than the “As Is” appraised value. For additional information please see the footnotes to Annex A-1 in the Preliminary Prospectus. |

| (5) | Excludes mortgage loans which are interest only for the full loan term and the 640 5th Avenue Mortgage Loan which has a fixed amortization schedule. |

| (6) | Includes FF&E reserves. |

| (7) | Represents the percent of the allocated Initial Outstanding Pool Balance of retail, office, industrial and mixed use properties only. |

| (8) | Please see Annex A-1 of the Preliminary Prospectus for more information. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 3 | ||

Benchmark 2024-V8 Mortgage Trust |

| STRUCTURE SUMMARY |

OFFERED CERTIFICATES

| Class(1) | Ratings (S&P/Fitch/KBRA) | Initial Certificate Balance(2) | Initial Subordination | Weighted Average Life (years)(4) | Principal Window (months)(4) | Certificate Principal to Value Ratio(5) | Certificate Underwritten NOI Debt Yield(6) |

| Class A-1 | AAA(sf) / AAAsf / AAA(sf) | $15,468,000 | 30.000%(7) | 2.48 | 1 – 57 | 36.9% | 19.4% |

| Class A-2 | AAA(sf) / AAAsf / AAA(sf) | (8) | 30.000%(7) | (8) | (8) | 36.9% | 19.4% |

| Class A-3 | AAA(sf) / AAAsf / AAA(sf) | (8) | 30.000%(7) | (8) | (8) | 36.9% | 19.4% |

| Class A-M | NR / AAAsf / AAA(sf) | $97,211,000 | 20.375% | 4.98 | 59 – 60 | 42.0% | 17.1% |

| Class B | NR / AA-sf / AA(sf) | $53,025,000 | 15.125% | 4.99 | 60 – 60 | 44.7% | 16.0% |

| Class C | NR / A-sf / A(sf) | $37,874,000 | 11.375% | 4.99 | 60 – 60 | 46.7% | 15.3% |

NON-OFFERED CERTIFICATES

| Class(1) | Ratings (S&P/Fitch/KBRA) | Initial Certificate Balance or Notional Amount (2) | Initial Subordination | Weighted Average Life (years)(4) | Principal Window (months)(4) | Certificate Principal to Value Ratio(5) | Certificate Underwritten NOI Debt Yield(6) | |

| Class X-A(9) | NR / AAAsf / AAA(sf) | $804,200,000 | (10) | N/A | N/A | N/A | N/A | N/A |

| Class X-B(9) | NR / A-sf / AAA(sf) | $90,899,000 | (10) | N/A | N/A | N/A | N/A | N/A |

| Class X-D(9)(11) | NR / BBBsf / BBB+(sf) | $22,725,000 | (10) | N/A | N/A | N/A | N/A | N/A |

| Class D(11) | NR /BBBsf / BBB+(sf) | $22,725,000 | 9.125% | 4.99 | 60 – 60 | 47.9% | 15.0% | |

| Class X-RR(9)(11) | NR / NR / NR | $92,161,421 | (10) | N/A | N/A | N/A | N/A | N/A |

| Class E-RR(11) | NR / BBB-sf / BBB+(sf) | $11,362,000 | 8.000% | 4.99 | 60 – 60 | 48.5% | 14.8% | |

| Class F-RR | NR / BB-sf / BB+(sf) | $21,462,000 | 5.875% | 4.99 | 60 – 60 | 49.6% | 14.4% | |

| Class G-RR | NR / B-sf / BB-(sf) | $15,150,000 | 4.375% | 4.99 | 60 – 60 | 50.4% | 14.2% | |

| Class J-RR | NR / NR / NR | $44,187,421 | 0.000% | 4.99 | 60 – 60 | 52.7% | 13.6% | |

| (1) | The pass-through rates for the Class A-1, Class A-2, Class A-3, Class A-M, Class B, Class C, Class D, Class E-RR, Class F-RR, Class G-RR and Class J-RR certificates (collectively, the “Principal Balance Certificates”) in each case, will be one of: (i) a fixed per annum rate, (ii) the weighted average of the net mortgage rates on the mortgage loans (in each case, adjusted, if necessary, to accrue on the basis of a 360-day year consisting of twelve 30-day months) as of their respective due dates in the month preceding the month in which such Distribution Date occurs (the “WAC Rate”), (iii) a rate equal to the lesser of a specified pass-through rate and the WAC Rate or (iv) the WAC Rate less a specified rate, but in any case not less than 0.000%. |

| (2) | Approximate; subject to a variance of plus or minus 5%. |

| (3) | The initial subordination levels are calculated based on the initial Certificate Balance. See “Credit Risk Retention” and “Description of the Certificates” in the Preliminary Prospectus. |

| (4) | The weighted average life and principal window during which distributions of principal would be received as set forth in the table with respect to each class of Principal Balance Certificates are based on (i) modeling assumptions described in the Preliminary Prospectus and (ii) assumptions that there are no prepayments, modifications or losses in respect of the mortgage loans and there are no extensions or forbearances of maturity dates of the mortgage loans. The weighted average life and principal window of the Class A-2 and Class A-3 certificates are subject to change as described in footnote (8) below. |

| (5) | “Certificate Principal to Value Ratio” for any class of Principal Balance Certificates is calculated as the product of (a) the weighted average mortgage loan Cut-off Date LTV of the mortgage loans, multiplied by (b) a fraction, the numerator of which is the total initial Certificate Balance of the related class of Principal Balance Certificates and all other classes of Principal Balance Certificates, if any, that are senior to such class, and the denominator of which is the total initial Certificate Balance of all classes of Principal Balance Certificates. The Certificate Principal to Value Ratios of the Class A-1, Class A-2 and Class A-3 certificates are calculated in the aggregate for those classes as if they were a single class. |

| (6) | “Certificate Underwritten NOI Debt Yield” for any class of Principal Balance Certificates is calculated as the product of (a) the weighted average Underwritten NOI Debt Yield for the mortgage loans, multiplied by (b) a fraction, the numerator of which is the total initial Certificate Balance of all classes of Principal Balance Certificates and the denominator of which is the total initial Certificate Balance of such class of Principal Balance Certificates and all other classes of Principal Balance Certificates, if any, that are senior to such class. The Certificate Underwritten NOI Debt Yields of the Class A-1, Class A-2 and Class A-3 certificates are calculated in the aggregate for those classes as if they were a single class. |

| (7) | The initial subordination levels for the Class A-1, Class A-2 and Class A-3 certificates are represented in the aggregate. |

| (8) | The exact initial Certificate Balances of the Class A-2 and Class A-3 certificates are unknown and will be determined based on the final pricing of those classes of certificates. However, the respective initial Certificate Balances, weighted average lives and principal windows of the Class A-2 and Class A-3 certificates are expected to be within the applicable ranges reflected in the following chart. The aggregate initial Certificate Balance of the Class A-2 and Class A-3 certificates is expected to be approximately $691,521,000, subject to a variance of plus or minus 5.0%. |

| Class of Certificates | Expected Range of Initial Certificate Balance | Expected Range of Weighted Avg. Life (years)(4) | Expected Range of Principal Window (months)(4) |

| Class A-2 | $0 – $300,000,000 | NAP – 4.84 | NAP / 57 – 59 |

| Class A-3 | $391,521,000 – $691,521,000 | 4.91 – 4.88 | 59 – 59 / 57 – 59 |

| (9) | As further described in the Preliminary Prospectus, the pass-through rate applicable to the Class X-A , Class X-B, Class X-D and Class X-RR certificates (collectively, the “Class X Certificates”) for each Distribution Date will generally be equal to the excess of (i) the WAC Rate over (ii) (A) with respect to the Class X-A certificates, the weighted average of the pass-through rates of the Class A-1, Class A-2, Class A-3 and Class A-M certificates (based on their respective Certificate Balances outstanding immediately prior to such Distribution Date), (B) with respect to the Class X-B certificates, the weighted average of the pass-through rates of the Class B and Class C certificates (based on their respective Certificate Balances outstanding immediately prior to such Distribution Date), (C) with respect to the Class X-D certificates, the pass-through rate of the Class D certificates, and (D) with respect to the Class X-RR certificates, the weighted average of the pass-through rates of the Class E-RR, Class F-RR, Class G-RR and Class J-RR certificates (based on their respective Certificate Balances outstanding immediately prior to such Distribution Date). |

| (10) | The Class X Certificates will not have Certificate Balances. None of the Class X Certificates will be entitled to distributions of principal. The interest accrual amounts on the Class X-A certificates will be calculated by reference to a notional amount equal to the aggregate Certificate Balances of the Class A-1, Class A-2, Class A-3 and Class A-M certificates. The interest accrual amounts on the Class X-B certificates will be calculated by reference to a notional amount equal to the aggregate Certificate Balances of the Class B and Class C certificates. The interest accrual amounts on the Class X-D certificates will be calculated by reference to a notional amount equal to the Certificate Balances of the Class D. The interest accrual amounts on the Class X-RR certificates will be calculated by reference to a notional amount equal to the aggregate Certificate Balances of the Class E-RR, Class F-RR, Class G-RR and Class J-RR certificates. The notional amount of each class of Class X Certificates is subject to change depending upon the final pricing of the Principal Balance Certificates, as follows: (1) if as a result of such pricing the pass-through rate of any class of Principal Balance Certificates whose Certificate Balance comprises such notional amount is equal to the WAC Rate, the Certificate Balance of such class of Principal Balance Certificates may not be part of, and will reduce accordingly, such notional amount of such class of Class X Certificates (or, if as a result of such pricing the pass-through rate of such class of Class X Certificates is equal to zero, such class of Class X Certificates may not be issued on the Closing Date), and/or (2) if as a result of such pricing the pass-through rate of any class of Principal Balance Certificates that does not comprise such notional amount of such class of Class X Certificates is less than the WAC Rate, such class of Principal Balance Certificates may become a part of, and increase accordingly, such notional amount of such class of Class X Certificates. |

| (11) | The initial Certificate Balance of each of the Class D and Class E-RR certificates, and the notional amount of the Class X-D and Class X-RR certificates, is subject to change based on final pricing of all Certificates, the final determination of the Class X-RR, Class E-RR, Class F-RR, Class G-RR and Class J-RR certificates (collectively, the “HRR Certificates”) that will be retained by Eightfold Real Estate Capital Fund VI, L.P., as the retaining third-party purchaser, in satisfaction of the retention obligations of German American Capital Corporation, in its capacity as retaining sponsor, to satisfy the U.S. risk retention requirements. For more information regarding the methodology and key inputs and assumptions used to determine the sizing of the HRR Certificates, see “Credit Risk Retention” in the Preliminary Prospectus. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 4 | ||

Benchmark 2024-V8 Mortgage Trust |

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

| Ten Largest Mortgage Loans | ||||||||||

| Mortgage Loan | Mortgage Loan Seller | City, State | Property Type | Mortgage Loan Cut-off Date | % of Initial Outstanding Pool Balance | Cut-off Date Room(1) | Cut-off Date LTV(1) | U/W NCF DSCR after IO(1) | U/W NOI Debt Yield(1) | |

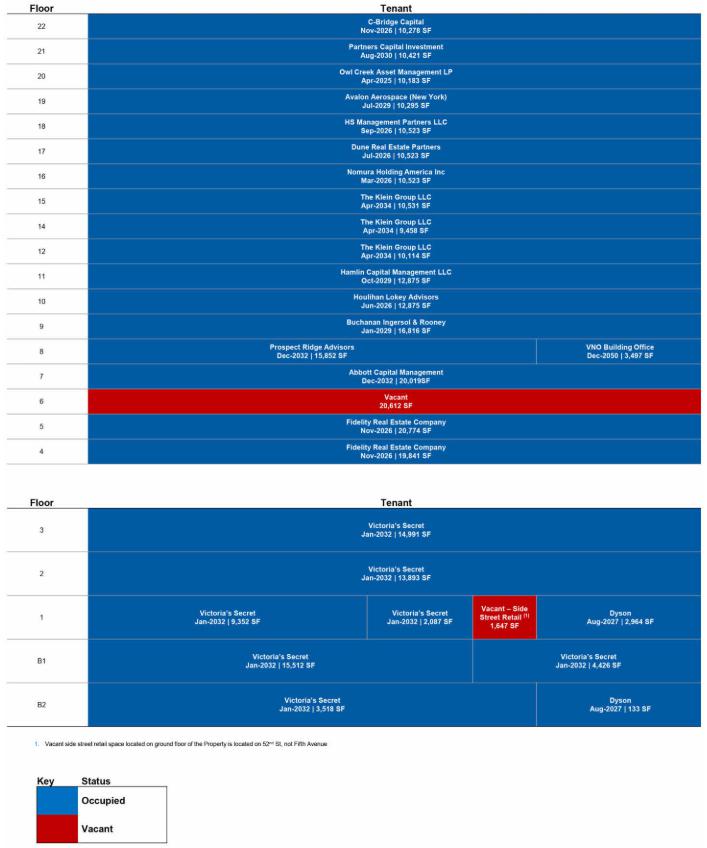

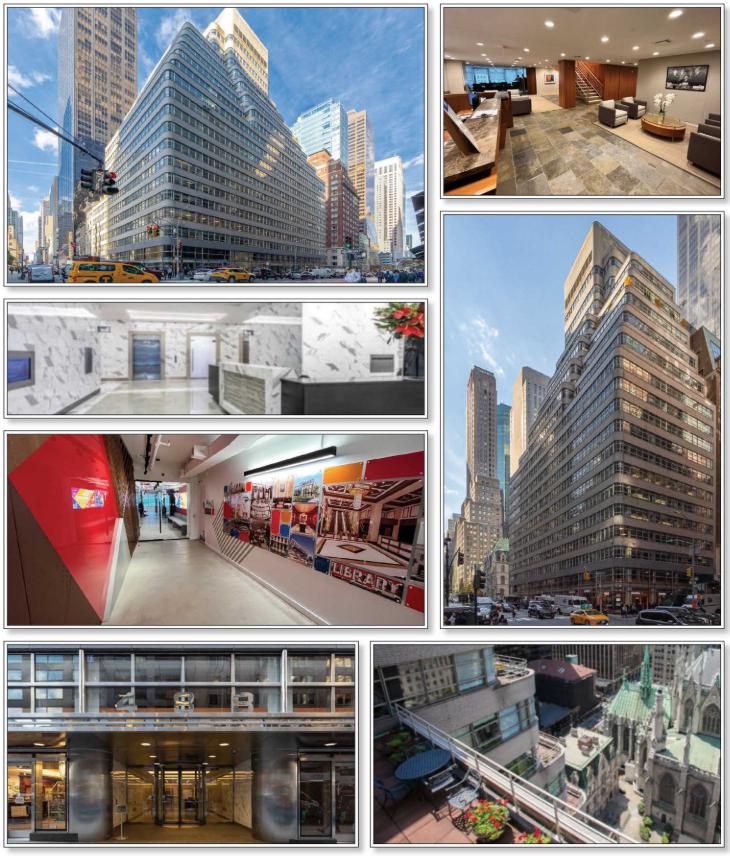

| 640 5th Avenue | GSMC, BMO | New York, NY | Mixed Use | $97,100,000 | 9.6% | $954 | 41.7% | 2.04x | 18.7% | |

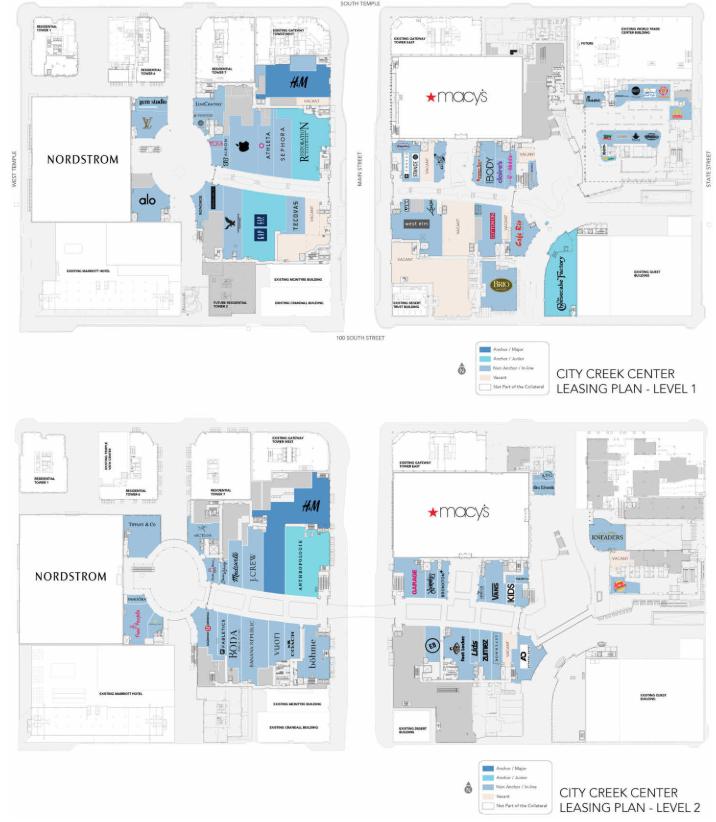

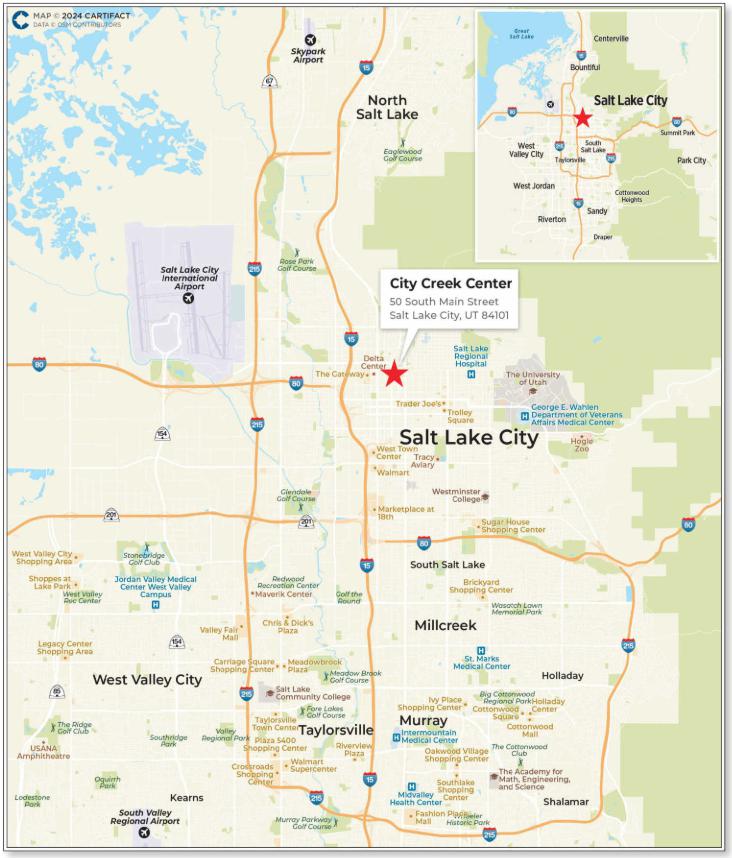

| City Creek Center | GSMC | Salt Lake City, UT | Retail | 70,000,000 | 6.9% | $215 | 51.7% | 1.79x | 14.3% | |

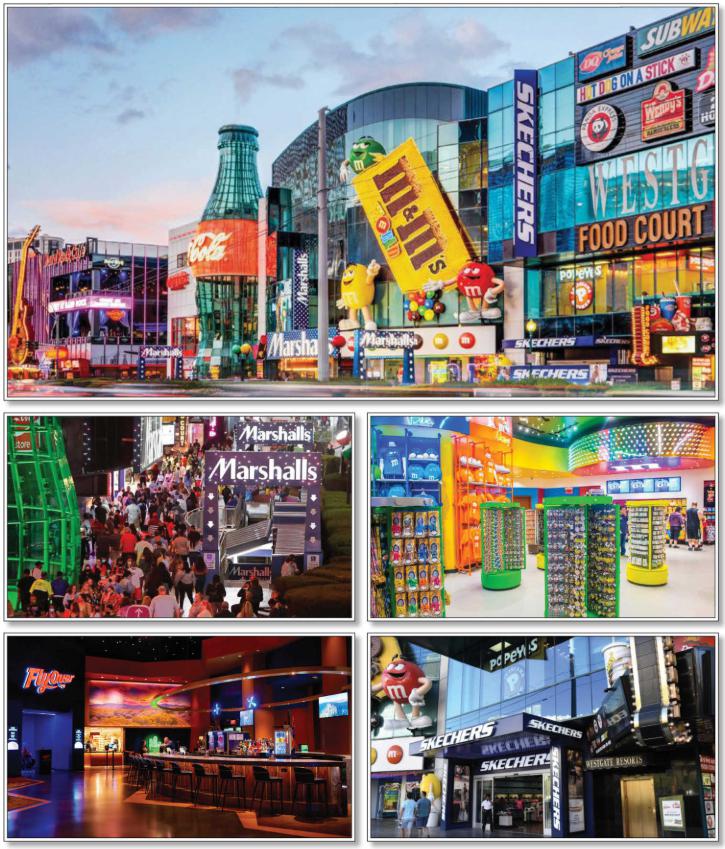

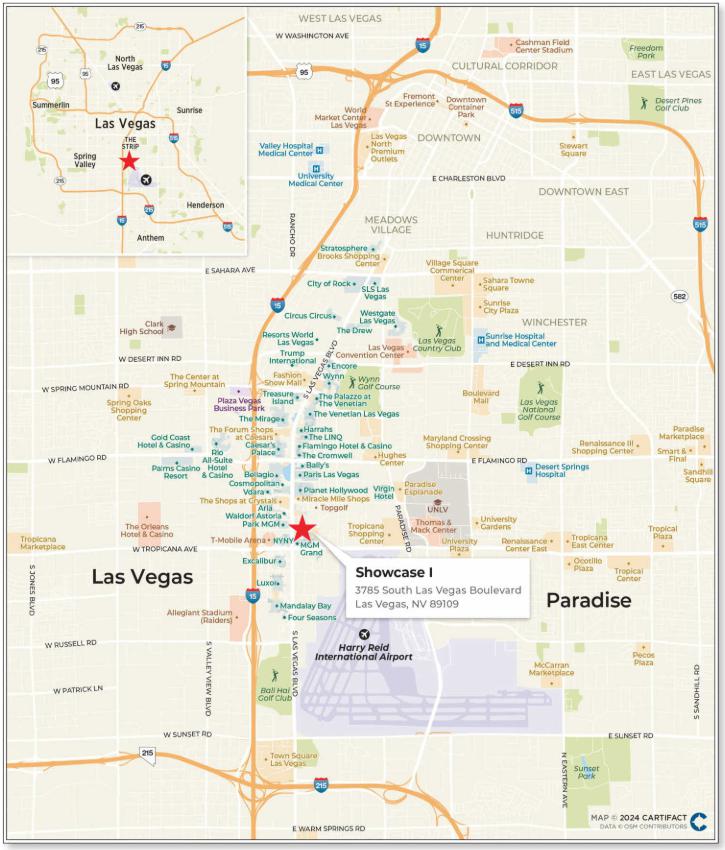

| Showcase I | CREFI | Las Vegas, NV | Retail | 69,500,000 | 6.9% | $937 | 67.8% | 1.30x | 8.5% | |

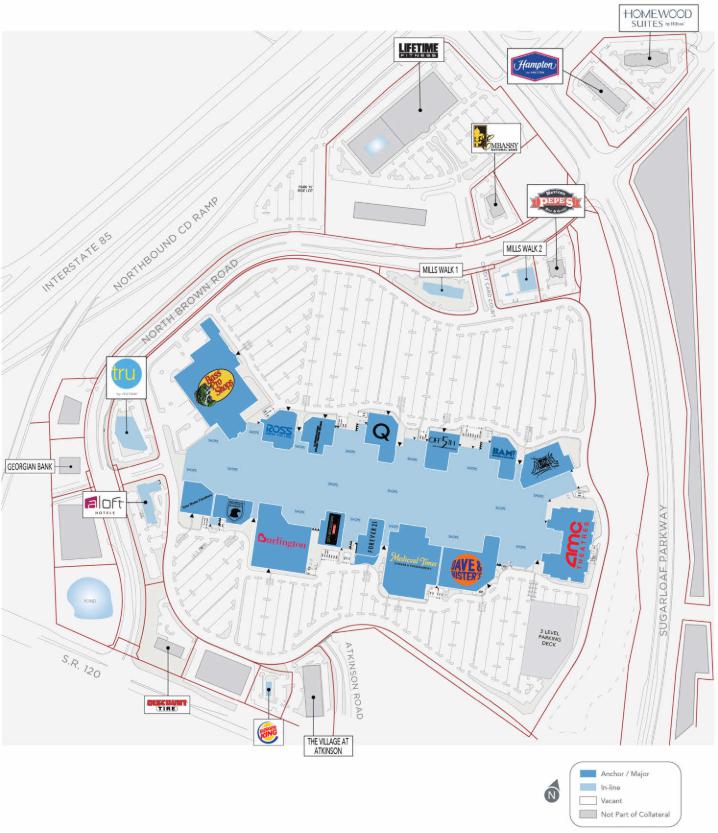

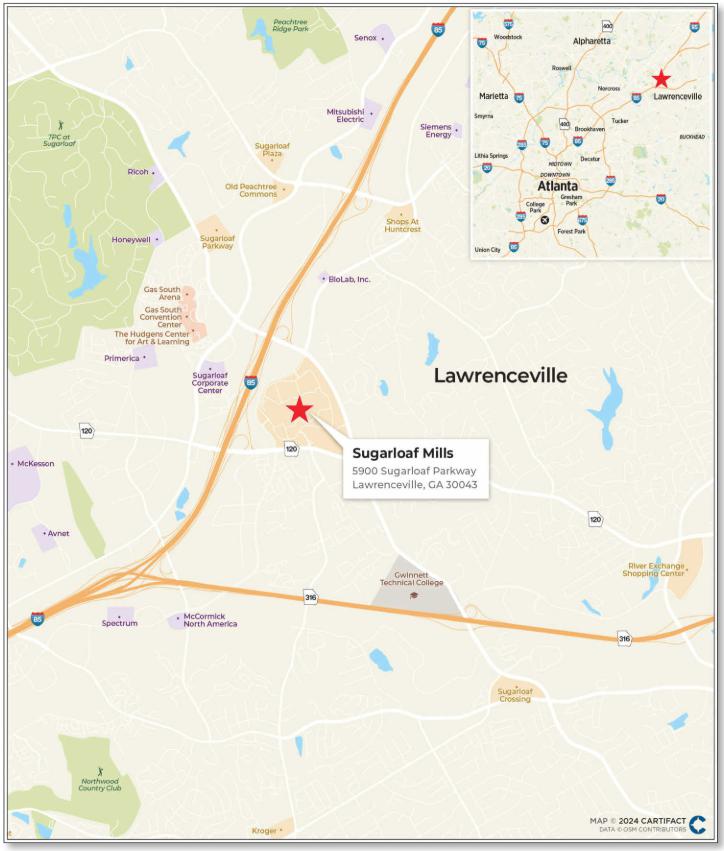

| Sugarloaf Mills | GACC, Barclays | Lawrenceville, GA | Retail | 65,790,421 | 6.5% | $56 | 30.6% | 2.73x | 30.2% | |

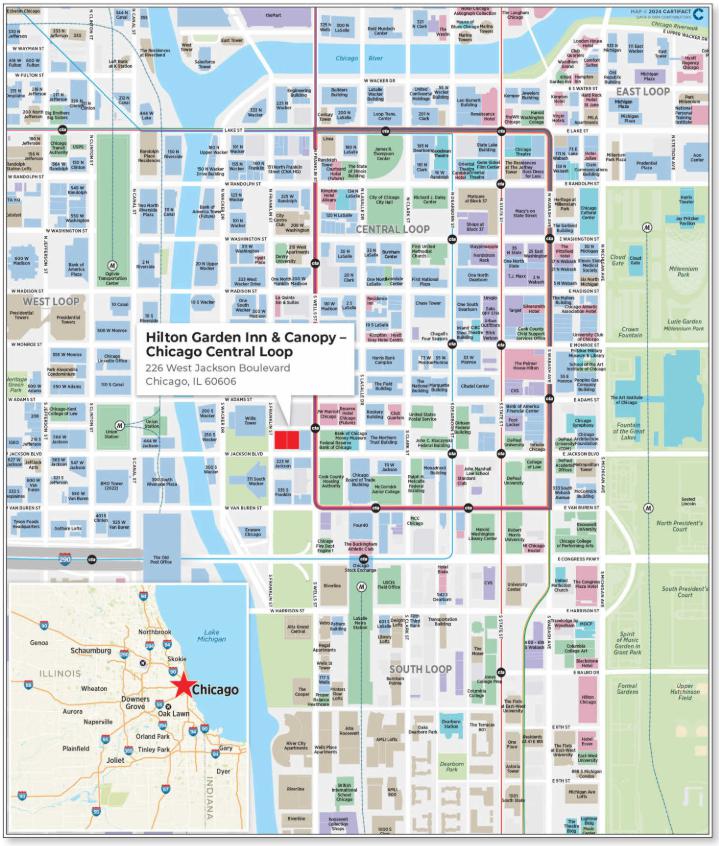

| Hilton Garden Inn & Canopy – Chicago Central Loop | CREFI | Chicago, IL | Hospitality | 65,000,000 | 6.4% | $185,714 | 40.5% | 1.68x | 14.6% | |

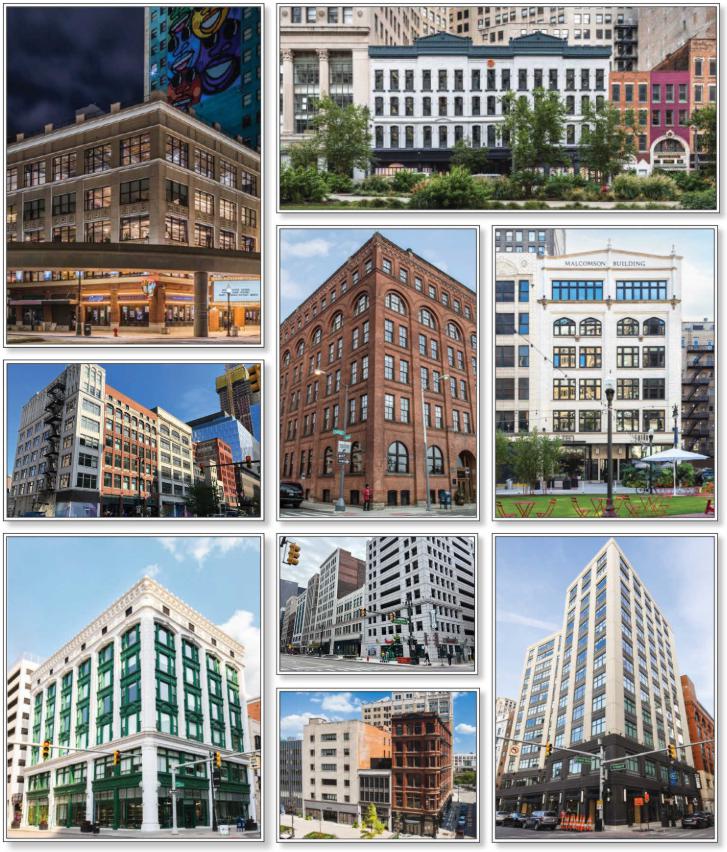

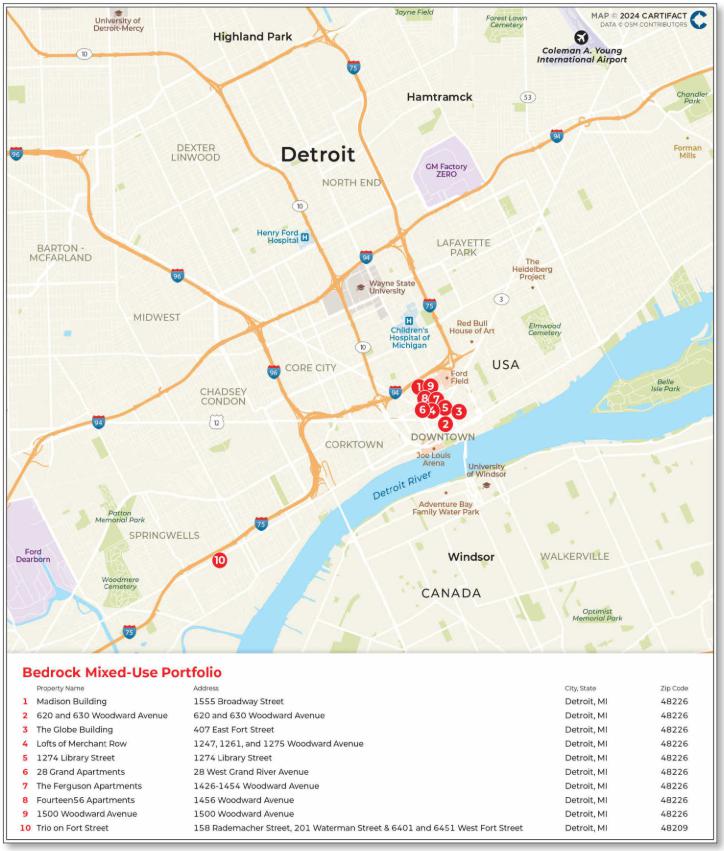

| Bedrock Mixed-Use Portfolio | GACC | Detroit, MI | Various | 55,000,000 | 5.4% | $88 | 54.3% | 1.58x | 11.3% | |

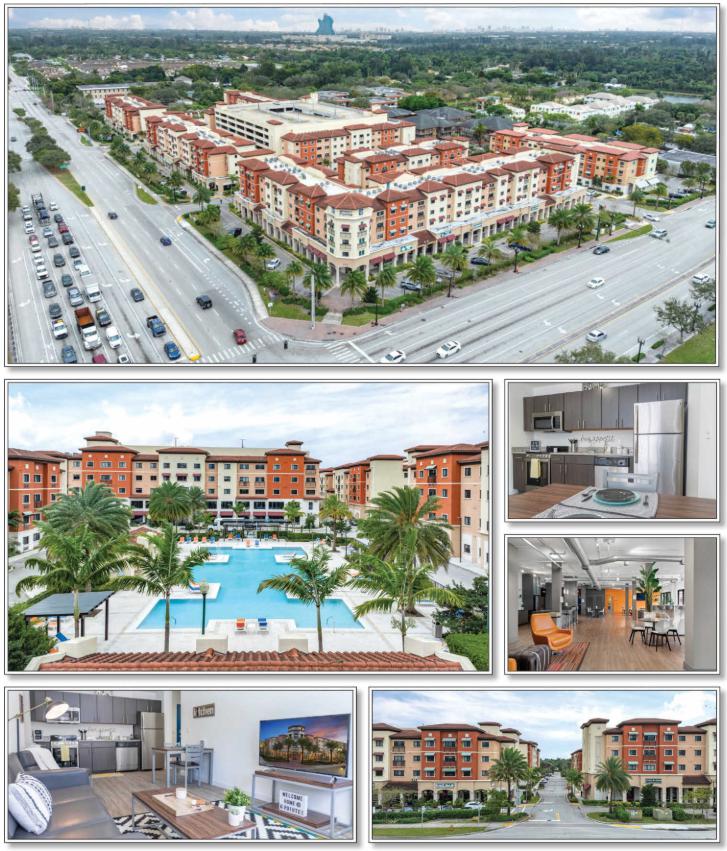

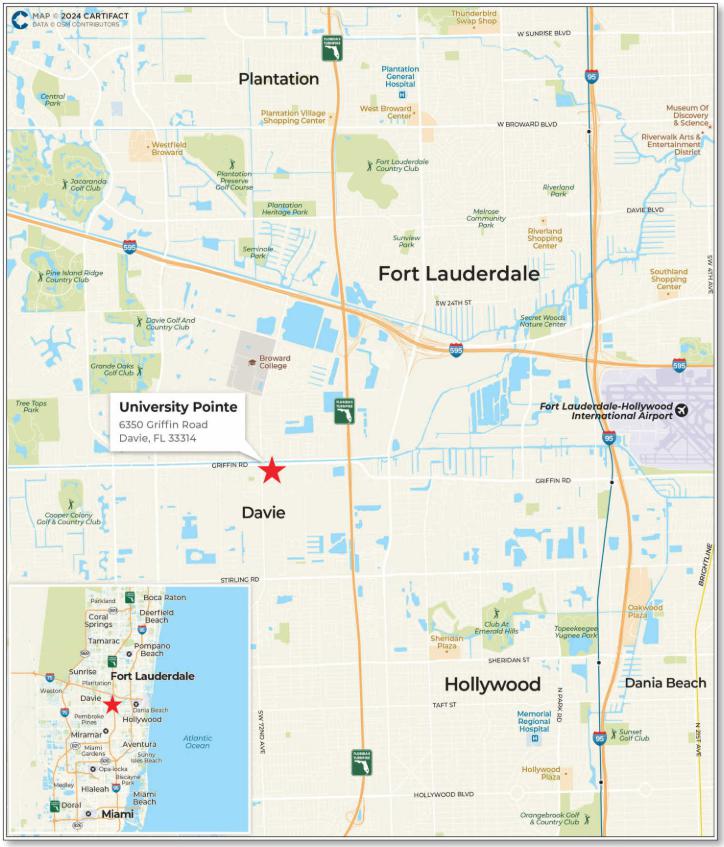

| University Pointe | CREFI | Davie, FL | Multifamily | 50,000,000 | 5.0% | $97,891 | 54.5% | 1.73x | 11.9% | |

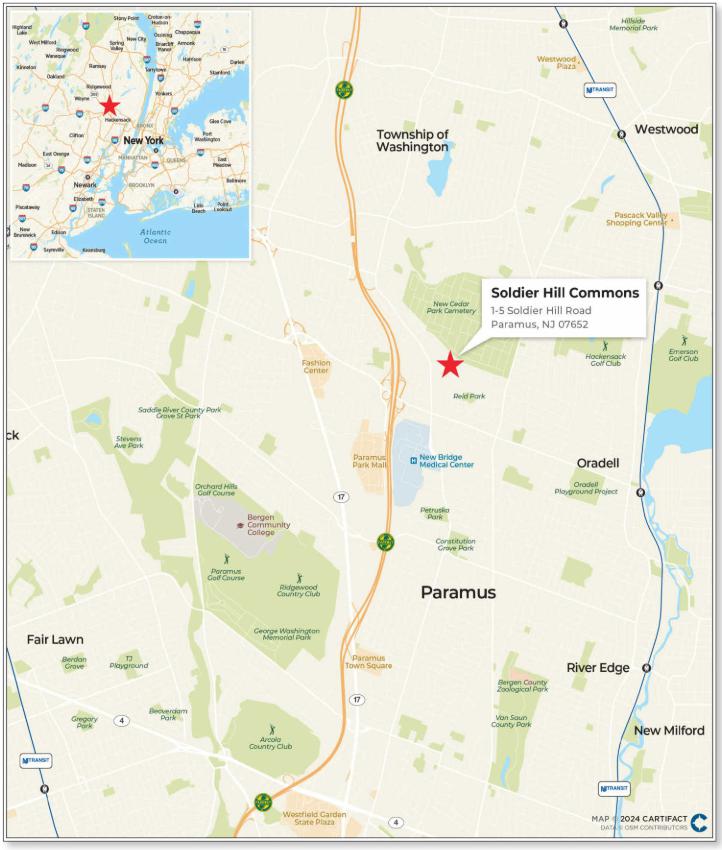

| Soldier Hill Commons | CREFI | Paramus, NJ | Multifamily | 46,500,000 | 4.6% | $332,143 | 62.7% | 1.24x | 8.6% | |

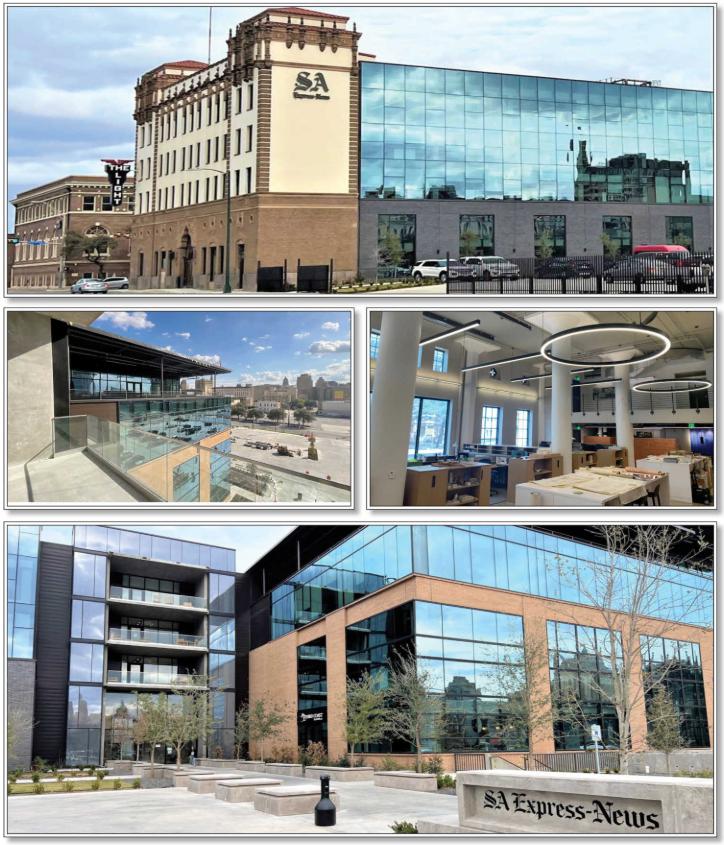

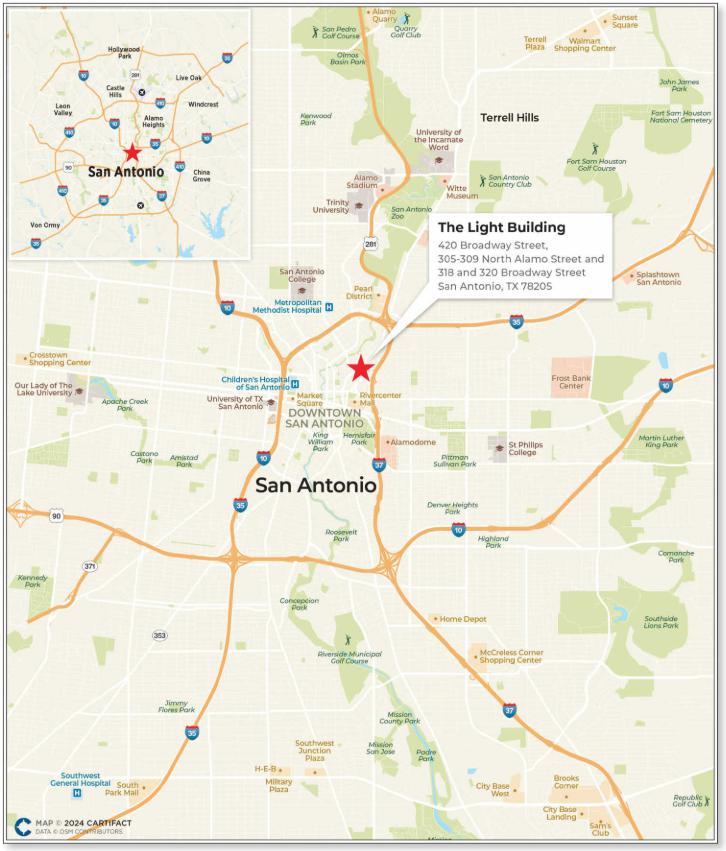

| The Light Building | CREFI | San Antonio, TX | Office | 43,500,000 | 4.3% | $295 | 56.1% | 1.83x | 13.6% | |

| 488 Madison | GACC | New York, NY | Office | 40,000,000 | 4.0% | $208 | 45.5% | 1.94x | 15.6% | |

| Total/Weighted Average | $602,390,421 | 59.6% | 49.7% | 1.81x | 15.2% | |||||

| (1) | The Cut-off Date Balance per NRA/Unit/Room, Cut-off Date LTV, U/W NCF DSCR after IO and U/W NOI Debt Yield calculations include any related pari passu companion loan(s) and exclude any related subordinate companion loan(s) and/or mezzanine loan(s). |

| Subordinate Debt Summary | ||||||||||

| Mortgage Loan | Mortgage Loan Cut-off Date Balance |

Pari Passu Companion Loans Cut-off Date Balance | Subordinate Debt Cut-off Date Balance | Mezzanine Debt Cut-off Date Balance | Trust U/W NCF DSCR(1)(3) | Total Debt U/W NCF DSCR(2)(3) | Trust Cut-off Date LTV(1) | Total Debt Cut-off Date LTV(2) | Trust U/W NOI Debt Yield(1) | Total Debt U/W NOI Debt Yield(2) |

| 640 5th Avenue | $97,100,000 | $202,900,000 | N/A | $100,000,000 | 2.04x | 1.31x | 41.7% | 55.6% | 18.7% | 14.0% |

| (1) | Trust U/W NCF DSCR, Trust Cut-off Date LTV and Trust U/W NOI Debt Yield calculations include any related pari passu companion loan(s) and exclude any related subordinate companion loan(s) and/or mezzanine loan(s). |

| (2) | Total Debt U/W NCF DSCR, Total Debt Cut-off Date LTV and Total Debt U/W NOI Debt Yield calculations include any related pari passu companion loan(s), related subordinate companion loan(s) and/or related mezzanine loan(s). |

| (3) | The DSCR shown above is based on the fixed amortization schedule for the 640 5th avenue whole loan and mezzanine loan, respectively. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 5 | ||

Benchmark 2024-V8 Mortgage Trust |

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

| Companion Loan Summary |

| Loan No. | Mortgage Loan | Note(s) | Cut-off Date Balance | Holder of Note(1) | Lead Servicer for Whole Loan (Y/N) | Master Servicer Under Lead Securitization | Special Servicer Under Lead Securitization |

| 1 | 640 5th Avenue

| A-1 | $40,000,000 | MSBNA | Yes | ||

| A-2 | $37,500,000 | MSBNA | No | ||||

| A-3 | $30,000,000 | MSBNA | No | ||||

| A-4 | $20,000,000 | MSBNA | No | ||||

| A-5 | $69,600,000 | Benchmark 2024-V8 | No | ||||

| A-6 | $40,000,000 | GSBI | No | ||||

| A-7 | $10,400,000 | GSBI | No | ||||

| A-8 | $25,000,000 | BBCMS 2024-5C27(2) | No | Wells Fargo(2) | LNR(2) | ||

| A-9 | $17,500,000 | Benchmark 2024-V8 | No | ||||

| A-10 | $10,000,000 | Benchmark 2024-V8 | No | ||||

| 3 | Showcase I(3) | A-1 | $70,000,000 | JPMCB | Yes | ||

| A-2 | $20,000,000 | JPMCB | No | ||||

| A-3 | $10,000,000 | JPMCB | No | ||||

| A-4 | $40,000,000 | Benchmark 2024-V8 | No | ||||

| A-5 | $29,500,000 | Benchmark 2024-V8 | No | ||||

| 6 | Bedrock Mixed-Use Portfolio | A-1 | $55,000,000 | Benchmark 2024-V8 | Yes | Wells Fargo | LNR |

| A-2 | $20,000,000 | BBCMS 2024-5C27 | No | ||||

| 7 | University Pointe | A-1 | $50,000,000 | Benchmark 2024-V8 | Yes | Wells Fargo | LNR |

| A-2 | $35,850,000 | BBCMS 2024-5C27 | No | ||||

| 10 | 488 Madison | A-1 | $60,000,000 | BANK5 2024-5YR7 | Yes | Wells Fargo | KeyBank |

| A-2 | $40,000,000 | Benchmark 2024-V8 | No | ||||

| 11 | Pleasanton Corporate Commons | A-1 | $25,000,000 | Benchmark 2024-V8 | Yes | Wells Fargo | LNR |

| A-2 | $12,100,000 | Benchmark 2024-V8 | No | ||||

| A-3 | $20,000,000 | BANK5 2024-5YR7 | No | ||||

| A-4 | $8,700,000 | BANK5 2024-5YR7 | No | ||||

| 12 | Lotus 315 & Essence 144(3) | A-1 | $50,000,000 | CREFI | Yes | ||

| A-2 | $36,100,000 | Benchmark 2024-V8 | No | ||||

| 15 | Saks Beverly Hills | A-1 | $61,365,000 | BANK5 2024-5YR7 | Yes | Wells Fargo | KeyBank |

| A-2 | $28,635,000 | Benchmark 2024-V8 | No | ||||

| 19 | Prime Storage – Blue Portfolio | A-1 | $38,000,000 | Benchmark 2024-V7 | Yes | Midland | KKR |

| A-2 | $20,000,000 | Benchmark 2024-V8 | No | ||||

| 22 | Sunroad Centrum | A-1 | $70,000,000 | Benchmark 2024-V7 | Yes | Midland | KKR |

| A-2 | $12,460,000 | Benchmark 2024-V8 | No | ||||

| 26 | GNL Industrial Portfolio | A-1 | $70,000,000 | BMO 2024-5C4 | Yes | Midland | Argentic |

| A-2 | $15,000,000 | BBCMS 2024-5C27 | No | ||||

| A-3 | $11,000,000 | Benchmark 2024-V7 | No | ||||

| A-4 | $8,000,000 | Benchmark 2024-V8 | No | ||||

| A-5 | $2,650,000 | Benchmark 2024-V8 | No | ||||

| A-6 | $16,500,000 | Benchmark 2024-V7 | No | ||||

| A-7 | $12,500,000 | Benchmark 2024-V7 | No | ||||

| A-8 | $8,000,000 | BBCMS 2024-5C27 | No | ||||

| A-9 | $6,400,000 | BBCMS 2024-5C27 | No | ||||

| A-10 | $4,000,000 | BBCMS 2024-5C27 | No | ||||

| A-11 | $15,000,000 | BBCMS 2024-5C27 | No | ||||

| A-12 | $10,550,000 | SGFC | No | ||||

| A-13 | $10,000,000 | SGFC | No | ||||

| A-14 | $20,000,000 | BBCMS 2024-5C27 | No | ||||

| A-15 | $12,000,000 | KeyBank | No | ||||

| A-16 | $10,000,000 | BBCMS 2024-5C27 | No | ||||

| A-17 | $5,400,000 | KeyBank | No |

| (1) | The identification of a securitization trust means we have identified another securitization trust that has closed or as to which a preliminary prospectus (or preliminary offering circular) or final prospectus (or final offering circular) has printed that has or is expected to include the identified Mortgage Note(s). |

| (2) | The 640 5th Avenue mortgage loan is expected to initially be serviced under the pooling and servicing agreement governing the BBCMS 2024-5C27 securitization. From and after the securitization of the related controlling pari passu companion loan, such whole loan will be serviced under the pooling and servicing agreement governing such securitization, such securitization will be the related controlling noteholder and the directing party will be the directing certificateholder (or equivalent) specified in such pooling and servicing agreement. |

| (3) | Prior to the related servicing shift securitization date, the related whole loan will be serviced under the pooling and servicing agreement for this transaction. From and after the related servicing shift securitization date, the related servicing shift whole loan will be serviced under the related servicing shift pooling and servicing agreement. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 6 | ||

Benchmark 2024-V8 Mortgage Trust |

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

| Distribution of Cut-off Date Balances(1) | ||||||||||||

| Range of Cut-off Date Balances | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Pool | Weighted Averages | ||||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR(2) | Cut-off Date LTV(3) | Maturity Date LTV(3) | ||||||||

| $2,400,000 | - | $9,999,999 | 9 | $56,750,000 | 5.6% | 6.8397% | 59 | 1.55x | 61.1% | 61.1% | ||

| $10,000,000 | - | $19,999,999 | 6 | $76,160,000 | 7.5% | 6.8699% | 59 | 1.64x | 57.7% | 57.7% | ||

| $20,000,000 | - | $29,999,999 | 6 | $134,570,000 | 13.3% | 6.8230% | 59 | 1.51x | 53.6% | 53.6% | ||

| $30,000,000 | - | $39,999,999 | 4 | $140,115,000 | 13.9% | 7.4078% | 59 | 1.40x | 58.4% | 58.4% | ||

| $40,000,000 | - | $97,100,000 | 10 | $602,390,421 | 59.6% | 6.9189% | 59 | 1.81x | 49.7% | 48.7% | ||

| Total/Weighted Average | 35 | $1,009,985,421 | 100.0% | 6.9658% | 59 | 1.69x | 52.7% | 52.1% | ||||

| Distribution of Mortgage Rates(1) | ||||||||||||

| Range of Mortgage Rates | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Pool | Weighted Averages | ||||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR(2) | Cut-off Date LTV(3) | Maturity Date LTV(3) | ||||||||

| 4.8200% | - | 5.9999% | 2 | $22,400,000 | 2.2% | 5.2593% | 59 | 2.37x | 51.4% | 51.4% | ||

| 6.0000% | - | 6.4999% | 9 | $326,200,000 | 32.3% | 6.2704% | 59 | 1.57x | 57.6% | 56.5% | ||

| 6.5000% | - | 6.9999% | 8 | $225,050,000 | 22.3% | 6.7832% | 59 | 1.64x | 55.9% | 55.9% | ||

| 7.0000% | - | 8.5300% | 16 | $436,335,421 | 43.2% | 7.6674% | 59 | 1.76x | 47.4% | 46.8% | ||

| Total/Weighted Average | 35 | $1,009,985,421 | 100.0% | 6.9658% | 59 | 1.69x | 52.7% | 52.1% | ||||

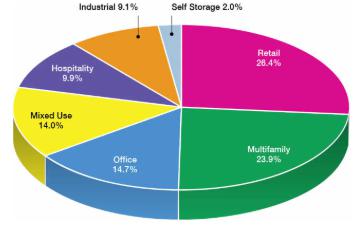

| Property Type Distribution(1)(4) | ||||||||||||

| Property Type | Number of Mortgaged Properties | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Number of NRA/Units/Rooms /Pads | Weighted Averages | |||||||

Cut-off Date NRA/Units/Rooms/ | Mortgage Rate | Stated Remaining Term (Mos.) | Occupancy | U/W NCF DSCR(2) | Cut-off Date LTV(3) | Maturity Date LTV(3) | ||||||

| Retail | 10 | $266,506,944 | 26.4% | 2,127,751 | $125 | 7.3627% | 59 | 89.8% | 1.85x | 50.7% | 49.9% | |

| Super Regional Mall | 2 | $135,790,421 | 13.4% | 1,504,366 | $90 | 7.8175% | 58 | 86.0% | 2.25x | 41.5% | 39.8% | |

| Anchored | 3 | $82,581,523 | 8.2% | 347,966 | $237 | 6.3360% | 60 | 90.4% | 1.36x | 66.5% | 66.5% | |

| Single Tenant | 3 | $34,280,570 | 3.4% | 128,765 | $266 | 7.6322% | 59 | 100.0% | 1.66x | 47.6% | 47.6% | |

| Unanchored | 2 | $13,854,430 | 1.4% | 146,654 | $94 | 8.3587% | 60 | 98.9% | 1.36x | 55.1% | 55.1% | |

| Multifamily | 16 | $241,622,915 | 23.9% | 2,179 | $110,887 | 6.6051% | 59 | 96.2% | 1.41x | 61.8% | 61.8% | |

| Mid Rise | 8 | $79,337,983 | 7.9% | 384 | $206,609 | 6.5330% | 59 | 94.9% | 1.37x | 62.4% | 62.4% | |

| Student Housing | 2 | $71,500,000 | 7.1% | 1,093 | $65,416 | 6.5151% | 59 | 97.9% | 1.60x | 59.2% | 59.2% | |

| Garden | 4 | $69,350,000 | 6.9% | 413 | $167,918 | 6.8409% | 59 | 96.8% | 1.30x | 62.7% | 62.7% | |

| High Rise | 2 | $21,434,932 | 2.1% | 289 | $74,169 | 6.4091% | 59 | 93.3% | 1.34x | 64.8% | 64.8% | |

| Office | 9 | $148,678,665 | 14.7% | 1,289,819 | $115 | 6.9883% | 59 | 89.1% | 1.78x | 51.1% | 51.1% | |

| CBD | 7 | $130,366,565 | 12.9% | 1,124,933 | $116 | 6.9394% | 59 | 91.9% | 1.84x | 50.3% | 50.3% | |

| Suburban | 2 | $18,312,100 | 1.8% | 164,886 | $111 | 7.3369% | 60 | 68.9% | 1.37x | 57.2% | 57.2% | |

| Mixed Use | 4 | $141,732,063 | 14.0% | 672,208 | $211 | 6.5750% | 59 | 93.2% | 1.87x | 47.1% | 44.5% | |

| Office/Retail | 2 | $98,654,235 | 9.8% | 336,236 | $293 | 6.1334% | 60 | 93.0% | 2.03x | 41.9% | 38.3% | |

| Office/Lab | 1 | $37,100,000 | 3.7% | 295,306 | $126 | 7.7800% | 58 | 100.0% | 1.49x | 59.6% | 59.6% | |

| Retail/Office | 1 | $5,977,828 | 0.6% | 40,666 | $147 | 6.3850% | 59 | 54.2% | 1.58x | 54.3% | 54.3% | |

| Hospitality | 3 | $100,000,000 | 9.9% | 599 | $166,945 | 7.8590% | 59 | 77.3% | 1.66x | 44.9% | 44.9% | |

| Full Service | 1 | $65,000,000 | 6.4% | 350 | $185,714 | 7.6000% | 59 | 77.3% | 1.68x | 40.5% | 40.5% | |

| Select Service | 1 | $18,575,000 | 1.8% | 131 | $141,794 | 8.3400% | 60 | 78.9% | 1.63x | 53.0% | 53.0% | |

| Extended Stay | 1 | $16,425,000 | 1.6% | 118 | $139,195 | 8.3400% | 60 | 75.2% | 1.63x | 53.0% | 53.0% | |

| Industrial | 34 | $91,444,834 | 9.1% | 5,025,229 | $18 | 6.5195% | 59 | 95.7% | 1.58x | 51.5% | 51.5% | |

| Flex | 11 | $42,750,000 | 4.2% | 417,141 | $102 | 7.0700% | 59 | 95.5% | 1.25x | 50.9% | 50.9% | |

| Warehouse | 4 | $24,021,045 | 2.4% | 198,029 | $121 | 5.9544% | 59 | 100.0% | 1.92x | 49.9% | 49.9% | |

| Manufacturing | 5 | $16,573,304 | 1.6% | 1,270,255 | $13 | 6.2973% | 59 | 88.0% | 1.65x | 54.2% | 54.2% | |

| Warehouse/Distribution | 10 | $6,336,275 | 0.6% | 2,598,277 | $2 | 5.7440% | 57 | 100.0% | 2.12x | 53.8% | 53.8% | |

| Manufacturing/Flex | 1 | $520,309 | 0.1% | 130,581 | $4 | 5.7440% | 57 | 100.0% | 2.12x | 53.8% | 53.8% | |

| Manufacturing/Warehouse | 1 | $470,698 | 0.0% | 216,300 | $2 | 5.7440% | 57 | 100.0% | 2.12x | 53.8% | 53.8% | |

| Distribution/Flex | 1 | $388,417 | 0.0% | 85,646 | $5 | 5.7440% | 57 | 100.0% | 2.12x | 53.8% | 53.8% | |

| Manufacturing/Distribution | 1 | $384,787 | 0.0% | 109,000 | $4 | 5.7440% | 57 | 100.0% | 2.12x | 53.8% | 53.8% | |

| Self Storage | 5 | $20,000,000 | 2.0% | 247,112 | $81 | 6.2100% | 58 | 92.7% | 1.44x | 63.6% | 63.6% | |

| Total/Weighted Average | 81 | $1,009,985,421 | 100.0% | 6.9658% | 59 | 91.1% | 1.69x | 52.7% | 52.1% | |||

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 7 | ||

Benchmark 2024-V8 Mortgage Trust |

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

| Geographic Distribution(1)(4) | |||||||||||

| State/Location | Number of Properties | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | |||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR(2) | Cut-off Date LTV(3) | Maturity Date LTV(3) | |||||||

| New York | 25 | $298,650,000 | 29.6% | 6.8343% | 60 | 1.73x | 47.7% | 46.5% | |||

| New York City | 9 | $201,500,000 | 20.0% | 6.4967% | 60 | 1.89x | 45.5% | 43.7% | |||

| New York State | 16 | $97,150,000 | 9.6% | 7.5344% | 59 | 1.40x | 52.3% | 52.3% | |||

| New Jersey | 9 | $109,950,000 | 10.9% | 6.5601% | 59 | 1.27x | 65.2% | 65.2% | |||

| California | 6 | $107,830,608 | 10.7% | 7.5374% | 59 | 1.49x | 56.6% | 56.6% | |||

| Southern(5) | 5 | $70,730,608 | 7.0% | 7.4102% | 59 | 1.49x | 55.0% | 55.0% | |||

| Northern(5) | 1 | $37,100,000 | 3.7% | 7.7800% | 58 | 1.49x | 59.6% | 59.6% | |||

| Georgia | 2 | $73,890,421 | 7.3% | 7.8975% | 58 | 2.61x | 34.2% | 31.1% | |||

| Utah | 1 | $70,000,000 | 6.9% | 7.6300% | 58 | 1.79x | 51.7% | 51.7% | |||

| Nevada | 1 | $69,500,000 | 6.9% | 6.3600% | 60 | 1.30x | 67.8% | 67.8% | |||

| Illinois | 2 | $65,909,936 | 6.5% | 7.5744% | 59 | 1.69x | 40.7% | 40.7% | |||

| Michigan | 13 | $59,899,375 | 5.9% | 6.3326% | 59 | 1.62x | 54.3% | 54.3% | |||

| Texas | 3 | $55,984,787 | 5.5% | 7.2133% | 59 | 1.73x | 55.8% | 55.8% | |||

| Florida | 3 | $50,539,064 | 5.0% | 6.6898% | 59 | 1.73x | 54.5% | 54.5% | |||

| Other | 16 | $47,831,230 | 4.7% | 5.8558% | 59 | 1.76x | 62.3% | 62.3% | |||

| Total/Weighted Average | 81 | $1,009,985,421 | 100.0% | 6.9658% | 59 | 1.69x | 52.7% | 52.1% | |||

| Distribution of Cut-off Date LTVs(1)(3) | ||||||||||

| Range of Cut-off Date LTVs | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance |

Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR(2) | Cut-off Date LTV(3) | Maturity Date LTV(3) | ||||||

| 30.6% | - | 39.9% | 2 | $85,790,421 | 8.5% | 7.7846% | 58 | 2.59x | 31.2% | 28.5% |

| 40.0% | - | 49.9% | 6 | $250,485,000 | 24.8% | 6.7671% | 59 | 1.92x | 42.9% | 41.5% |

| 50.0% | - | 59.9% | 12 | $390,800,000 | 38.7% | 7.2072% | 59 | 1.61x | 54.1% | 54.1% |

| 60.0% | - | 69.9% | 14 | $261,410,000 | 25.9% | 6.5990% | 59 | 1.31x | 65.4% | 65.4% |

| 70.0% | - | 70.0% | 1 | $21,500,000 | 2.1% | 6.0850% | 58 | 1.30x | 70.0% | 70.0% |

| Total/Weighted Average | 35 | $1,009,985,421 | 100.0% | 6.9658% | 59 | 1.69x | 52.7% | 52.1% | ||

| Distribution of Maturity Date LTVs(1)(3) | ||||||||||

| Range of Maturity Date LTVs | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR(2) | Cut-off Date LTV(3) | Maturity Date LTV(3) | ||||||

| 27.1% | - | 39.9% | 3 | $182,890,421 | 18.1% | 6.9058% | 59 | 2.30x | 36.8% | 33.6% |

| 40.0% | - | 49.9% | 5 | $153,385,000 | 15.2% | 7.1709% | 59 | 1.85x | 43.7% | 43.7% |

| 50.0% | - | 59.9% | 12 | $390,800,000 | 38.7% | 7.2072% | 59 | 1.61x | 54.1% | 54.1% |

| 60.0% | - | 70.0% | 15 | $282,910,000 | 28.0% | 6.5599% | 59 | 1.31x | 65.8% | 65.8% |

| Total/Weighted Average | 35 | $1,009,985,421 | 100.0% | 6.9658% | 59 | 1.69x | 52.7% | 52.1% | ||

| Distribution of Underwritten NCF Debt Service Coverages(1)(2) | ||||||||||

| Range of Underwritten NCF Debt Service Coverages | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR(2) | Cut-off Date LTV(3) | Maturity Date LTV(3) | ||||||

| 1.21x | - | 1.49x | 19 | $393,360,000 | 38.9% | 6.8516% | 59 | 1.31x | 62.4% | 62.4% |

| 1.50x | - | 1.99x | 10 | $403,335,000 | 39.9% | 7.2020% | 59 | 1.73x | 50.6% | 50.6% |

| 2.00x | - | 2.49x | 4 | $135,750,000 | 13.4% | 6.2710% | 60 | 2.07x | 41.8% | 39.1% |

| 2.50x | - | 2.73x | 2 | $77,540,421 | 7.7% | 7.5325% | 58 | 2.71x | 33.4% | 30.4% |

| Total/Weighted Average | 35 | $1,009,985,421 | 100.0% | 6.9658% | 59 | 1.69x | 52.7% | 52.1% | ||

| Original Terms to Maturity(1) | ||||||||

| Original Terms to Maturity | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR(2) | Cut-off Date LTV(3) | Maturity Date LTV(3) | ||||

| 60 | 35 | $1,009,985,421 | 100.0% | 6.9658% | 59 | 1.69x | 52.7% | 52.1% |

| Total/Weighted Average | 35 | $1,009,985,421 | 100.0% | 6.9658% | 59 | 1.69x | 52.7% | 52.1% |

Distribution of Remaining Terms to Maturity(1) | ||||||||||

| Range of Remaining Terms to Maturity | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR(2) | Cut-off Date LTV(3) | Maturity Date LTV(3) | ||||||

| 57 | - | 59 | 24 | $706,885,421 | 70.0% | 7.0784% | 59 | 1.69x | 52.6% | 52.3% |

| 60 | - | 60 | 11 | $303,100,000 | 30.0% | 6.7032% | 60 | 1.68x | 52.8% | 51.6% |

| Total/Weighted Average | 35 | $1,009,985,421 | 100.0% | 6.9658% | 59 | 1.69x | 52.7% | 52.1% | ||

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 8 | ||

Benchmark 2024-V8 Mortgage Trust |

| OVERVIEW OF MORTGAGE POOL CHARACTERISTICS |

| Distribution of Underwritten NOI Debt Yields(1) | ||||||||||

| Range of Underwritten NOI Debt Yields | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR(2) | Cut-off Date LTV(3) | Maturity Date LTV(3) | ||||||

| 7.9% | - | 8.4% | 5 | $98,100,000 | 9.7% | 6.3741% | 59 | 1.25x | 66.9% | 66.9% |

| 8.5% | - | 9.4% | 6 | $198,100,000 | 19.6% | 6.6564% | 59 | 1.29x | 61.4% | 61.4% |

| 9.5% | - | 10.4% | 1 | $7,400,000 | 0.7% | 7.1600% | 60 | 1.39x | 60.7% | 60.7% |

| 10.5% | - | 11.4% | 5 | $77,260,000 | 7.6% | 6.7729% | 59 | 1.52x | 57.3% | 57.3% |

| 11.5% | - | 30.2% | 18 | $629,125,421 | 62.3% | 7.1769% | 59 | 1.91x | 47.0% | 46.1% |

| Total/Weighted Average | 35 | $1,009,985,421 | 100.0% | 6.9658% | 59 | 1.69x | 52.7% | 52.1% | ||

| Amortization Types(1) | ||||||||

| Amortization Type | Number of Mortgage Loans | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance | Weighted Averages | ||||

| Mortgage Rate | Stated Remaining Term (Mos.) | U/W NCF DSCR(2) | Cut-off Date LTV(3) | Maturity Date LTV(3) | ||||

| Interest Only | 33 | $847,095,000 | 83.9% | 6.9800% | 59 | 1.57x | 55.6% | 55.6% |

| Amortizing Balloon | 2 | $162,890,421 | 16.1% | 6.8918% | 59 | 2.32x | 37.2% | 33.6% |

| Total/Weighted Average | 35 | $1,009,985,421 | 100.0% | 6.9658% | 59 | 1.69x | 52.7% | 52.1% |

| (1) | The U/W NCF DSCR, Cut-off Date LTV, Maturity Date LTV, Underwritten NOI Debt Yield and Cut-off Date Balance per # of NRA/Units/Rooms/Pads calculations include any related pari passu companion loan(s) and exclude any related subordinate companion loan(s) and/or mezzanine loan(s). |

| (2) | The 640 5th Avenue Whole Loan has a fixed amortization for its entire 60-month loan term. With respect to the 640 5th Avenue Whole Loan, the borrower is required to make payments on each monthly payment date, as follows: (x) principal in the amount of $437,500 and (y) the monthly interest payment. |

| (3) | With respect to 4 mortgaged properties (9.5%) (488 Madison, Lotus 315, Courtyard Marriott, TownePlace Suites), the Cut-off Date LTV Ratio and Maturity Date or LTV Ratio have been calculated using a value other than the “As Is” appraised value. For additional information please see the footnotes to Annex A-1 in the Preliminary Prospectus. |

| (4) | Reflects the allocated loan amount for properties securing multi-property Mortgage Loans. |

| (5) | Northern California properties have a zip code greater than 93600. Southern California properties have a zip code less than or equal to 93600. |

| Previously Securitized Mortgaged Properties(1) | |||||

| Mortgaged Property | Cut-off Date Balance | % of Initial Outstanding Pool Balance | City, State | Property Type | Previous Securitization |

| City Creek Center | 70,000,000 | 6.9% | Salt Lake City, Utah | Retail | MSBAM 2013-C12 |

| Showcase I | 69,500,000 | 6.9% | Las Vegas, Nevada | Retail | JPMBB 2014-C21 |

| Sugarloaf Mills | 65,790,421 | 6.5% | Lawrenceville, Georgia | Retail | JPMCC 2006-LDP9 |

| Lotus 315 | 21,320,383 | 2.1% | East Orange, New Jersey | Multifamily | ARCLO 2021-FL3 |

| 3575 Cahuenga | 18,300,000 | 1.8% | Los Angeles, California | Office | JPMBB 2014-C19 |

| Essence 144 | 14,779,617 | 1.5% | East Orange, New Jersey | Multifamily | UBSCM 2017-C4 |

| Sunroad Centrum | 12,460,000 | 1.2% | San Diego, California | Office | COMM 2014-CR19 |

| Exchange Plaza | 12,100,000 | 1.2% | San Antonio, Texas | Retail | M360 2021-CRE3 |

| Woodbury Gardens | 7,400,000 | 0.7% | Central Valley, New York | Multifamily | FNA 2014-M1 |

| 49 South Clinton Street | 7,350,000 | 0.7% | East Orange, New Jersey | Multifamily | FRESB 2019-SB68 |

| Prime Storage - Union City | 6,793,103 | 0.7% | Union City, New Jersey | Self Storage | WFCM 2015-NXS2 |

| Prime Storage - Jersey City | 4,551,724 | 0.5% | Jersey City, New Jersey | Self Storage | WFCM 2015-NXS2 |

| Prime Storage - Newark | 4,517,241 | 0.4% | Newark, New Jersey | Self Storage | WFCM 2015-NXS2 |

| Prime Storage - Hoboken | 2,655,172 | 0.3% | Jersey City, New Jersey | Self Storage | WFCM 2015-NXS2 |

| Prime Storage - Garfield | 1,482,759 | 0.1% | Garfield, New Jersey | Self Storage | RCMT 2019-FL3 |

| (1) | The table above includes mortgaged properties securing mortgage loans for which the most recent prior financing of all or a significant portion of each such mortgaged property was included in a securitization. Information under “Previous Securitization” represents the most recent such securitization with respect to each of those mortgaged properties. The information in the above table is based solely on information provided by the related borrower or obtained through searches of a third-party database and has not otherwise been confirmed by the related mortgage loan seller. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 9 | ||

Benchmark 2024-V8 Mortgage Trust |

| STRUCTURE OVERVIEW |

| Available Funds: | The amount available for distribution to holders of the certificates on each Distribution Date will be the gross amount of interest, principal, yield maintenance charges and prepayment premiums collected with respect to the Mortgage Loans in the applicable one-month collection period, net of specified expenses of the issuing entity, including fees payable therefrom to, and losses, liabilities, costs and expenses reimbursable or indemnifiable therefrom to, the Master Servicer, the Special Servicer, the Certificate Administrator, the Trustee, the Operating Advisor, the Asset Representations Reviewer and CREFC®. See “Description of the Certificates” in the Preliminary Prospectus. |

| Principal Payments: | Payments in respect of principal on the certificates will be distributed to the Class A-1, Class A-2, Class A-3, Class A-M, Class B, Class C, Class D, Class E-RR, Class F-RR, Class G-RR and Class J-RR certificates, in that order, until the Certificate Balance of each such class is reduced to zero. Notwithstanding the foregoing, if the total Certificate Balance of the Class A-M, Class B, Class C, Class D, Class E-RR, Class F-RR, Class G-RR and Class J-RR certificates have been reduced to zero as a result of loss allocation, payments in respect of principal of the certificates will be distributed, first, to the Class A-1, Class A-2 and Class A-3 certificates, on a pro rata basis, based on the Certificate Balance of each such class, then, to the extent of any recoveries on realized losses, to the Class A-M, Class B, Class C, Class D, Class E-RR, Class F-RR, Class G-RR and Class J-RR certificates, in that order, in each case until the Certificate Balance of each such class is reduced to zero (or previously allocated realized losses have been fully reimbursed). Each of the Class X Certificates will not be entitled to receive distributions of principal; however, (i) the notional amount of the Class X-A certificates will be reduced by the aggregate amount of principal distributions and realized losses allocated to the Class A-1, Class A-2, Class A-3 and Class A-M certificates, (ii) the notional amount of the Class X-B certificates will be reduced by the aggregate amount of principal distributions and realized losses allocated to the Class B and Class C certificates, (iii) the notional amount of the Class X-D certificates will be reduced by the amount of principal distributions and realized losses allocated to the Class D certificates, and (iv) the notional amount of the Class X-RR certificates will be reduced by the aggregate amount of principal distributions and realized losses allocated to the Class E-RR, Class F-RR, Class G-RR and Class J-RR certificates. |

Interest Payments: | On each Distribution Date, interest accrued for each class of certificates at the applicable pass-through rate will be distributed in the following order of priority, to the extent of available funds (exclusive of any portion thereof that represents any yield maintenance charges and prepayment premiums): first, to the Class A-1, Class A-2, Class A-3, Class X-A, Class X-B and Class X-D certificates, on a pro rata basis, based on the accrued and unpaid interest on each such class and then, to the Class A-M, Class B, Class C, Class D, Class X-RR, Class E-RR, Class F-RR, Class G-RR and Class J-RR certificates, in that order, in each case until the interest payable to each such class is paid in full. The pass-through rates applicable to the Class A-1, Class A-2, Class A-3, Class A-M, Class B, Class C, Class D, Class E-RR, Class F-RR, Class G-RR and Class J-RR certificates for each Distribution Date will equal one of: (i) a fixed per annum rate, (ii) the WAC Rate, (iii) a rate equal to the lesser of a specified pass-through rate and the WAC Rate or (iv) the WAC Rate less a specified rate, but in any case not less than 0.000%. As further described in the Preliminary Prospectus, the pass-through rates applicable to the Class X Certificates for each Distribution Date will generally be equal to the excess of (i) the WAC Rate over (ii) (A) with respect to the Class X-A certificates, the weighted average of the pass-through rates of the Class A-1, Class A-2, Class A-3 and Class A-M certificates (weighted based on their respective Certificate Balances outstanding immediately prior to that Distribution Date), (B) with respect to the Class X-B certificates, the weighted average of the pass-through rates of the Class B and Class C certificates (weighted based on their respective Certificate Balances outstanding immediately prior to that Distribution Date), (C) with respect to the Class X-D certificates, the pass-through rate of the Class D certificates and (D) with respect to the Class X-RR certificates, the weighted average of the pass-through rates of the Class E-RR, Class F-RR, Class G-RR and Class J-RR certificates (weighted based on their respective Certificate Balances outstanding immediately prior to that Distribution Date) . |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 10 | ||

Benchmark 2024-V8 Mortgage Trust |

| STRUCTURE OVERVIEW |

| Prepayment Interest Shortfalls: | Prepayment interest shortfalls will be allocated pro rata based on interest entitlements, in reduction of the interest otherwise payable with respect to each of the interest-bearing classes of certificates. |

| Loss Allocation: | Losses on the Mortgage Loans will be allocated to each class of certificates entitled to principal in reverse alphabetical order starting with the Class J-RR certificates through and including the Class A-M certificates and then to the Class A-1, Class A-2 and Class A-3 certificates on a pro rata basis based on the Certificate Balance of each such class. The notional amount of any class of Class X Certificates will be reduced by the aggregate amount of realized losses allocated to the class(es) of certificates that are component(s) of the notional amount of such class of Class X Certificates. |

Prepayment Premiums:

| A percentage of all prepayment premiums (either fixed prepayment premiums or yield maintenance amounts) collected on the Mortgage Loans will be allocated to each of the Class A-1, Class A-2, Class A-3, Class A-M, Class B, Class C and Class D certificates (the “YM P&I Certificates”) then entitled to principal distributions, which percentage will be equal to the product of (a) a fraction, not greater than one, the numerator of which is the amount of principal distributed to such class on such Distribution Date and the denominator of which is the total amount of principal distributed to the holders of each class of Principal Balance Certificates on such Distribution Date and (b) the Base Interest Fraction for the related principal prepayment and such class of certificates. The “Base Interest Fraction” for any principal prepayment on any Mortgage Loan and for: (A) any of the Class A-1 through Class D certificates with a Pass-Through Rate equal to either the WAC Rate or the WAC Rate less a specified rate, will be a fraction (not greater than one) (a) whose numerator is the greater of zero and the amount, if any, by which (i) the Pass-Through Rate on such class of certificates exceeds (ii) the yield rate (as provided by the master servicer) used in calculating the prepayment premium or yield maintenance charge, as applicable, with respect to such principal prepayment and (b) whose denominator is the amount, if any, by which (i) the Net Mortgage Rate on such Mortgage Loan during the related interest accrual period exceeds (ii) the yield rate (as provided by the master servicer) used in calculating the prepayment premium or yield maintenance charge, as applicable, with respect to such principal prepayment; provided, however, that if such yield rate is greater than or equal to the Net Mortgage Rate on such Mortgage Loan during the related interest accrual period, then the respective Base Interest Fraction will be zero; provided, further, that if such yield rate is greater than or equal to the Net Mortgage Rate on such Mortgage Loan during the related interest accrual period, but less than the Pass-Through Rate described in clause (a)(i) above, then the respective Base Interest Fraction will be one; and (B) any of the Class A-1 through Class D certificates with a Pass-Through Rate equal to a fixed per annum rate, will be a fraction (not greater than one) (a) whose numerator is the greater of zero and the amount, if any, by which (i) the Pass-Through Rate on such class of certificates exceeds (ii) the yield rate (as provided by the master servicer) used in calculating the prepayment premium or yield maintenance charge, as applicable, with respect to such principal prepayment and (b) whose denominator is the amount, if any, by which (i) the Mortgage Rate on such Mortgage Loan (net of the Administrative Cost Rate) during the related interest accrual period multiplied by 365/360 exceeds (ii) the yield rate (as provided by the master servicer) used in calculating the prepayment premium or yield maintenance charge, as applicable, with respect to such principal prepayment; provided, however, that if such yield rate is greater than or equal to the amount set forth in clause (b)(i) above, then the respective Base Interest Fraction will be zero; provided, further, that if such yield rate is greater than or equal to the amount set forth in clause (b)(i) above, but less than the Pass-Through Rate described in clause (a)(i) above, then the respective Base Interest Fraction will be one. The remaining percentage of prepayment premiums will be allocated to the Class X-A, Class X-B and Class X-D certificates in the manner described in the Preliminary Prospectus. In general, this formula provides for an increase in the percentage of prepayment premiums allocated to the YM P&I Certificates then entitled to principal distributions relative to the Class X-A, Class X-B and Class X-D certificates as Discount Rates decrease and a decrease in the percentage allocated to such classes as Discount Rates rise. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 11 | ||

Benchmark 2024-V8 Mortgage Trust |

| STRUCTURE OVERVIEW |

| Whole Loans: | The mortgaged properties identified on Annex A-1 to the Preliminary Prospectus as 640 5th Avenue, Showcase I, Bedrock Mixed-Use Portfolio, University Pointe, 488 Madison, Pleasanton Corporate Commons, Lotus 315 & Essence 144, Saks Beverly Hills, Prime Storage – Blue Portfolio, Sunroad Centrum and GNL Industrial Portfolio each secure both a mortgage loan to be included in the trust fund and one or more other companion loans that will not be included in the trust fund, each of which will be pari passu or subordinate in right of payment with the mortgage loan included in the trust fund. We refer to each such group of related loans as a “whole loan”. As of the Closing Date, the pari passu companion loans and any subordinate companion loans are expected to be held by the party identified in “—Companion Loan Summary” above and the table titled “Whole Loan Control Notes and Non-Control Notes” in “Description of the Mortgage Pool—The Whole Loans—General” in the Preliminary Prospectus. |

| Control Rights and Directing Holder: | With respect to any Serviced Mortgage Loan and any related Serviced Companion Loan, the Directing Holder will generally be entitled to direct the Special Servicer to take, or refrain from taking certain actions with respect to each Serviced Mortgage Loan and any related Serviced Companion Loans. Furthermore, the Directing Holder will also have the right to receive notice and consent to certain material actions that the Master Servicer and the Special Servicer proposes to take with respect to each Serviced Mortgage Loan and any related Serviced Companion Loans. The “Directing Holder” means, (i) with respect to each Serviced Mortgage Loan (other than any Servicing Shift Mortgage Loan) or Serviced Whole Loan (other than any Servicing Shift Whole Loan), the Controlling Class Certificateholder (or its representative) selected by more than 50% of the Controlling Class, by Certificate Balance, as determined by the certificate registrar from time to time (the “Trust Directing Holder”); and (ii) with respect to any Servicing Shift Mortgage Loan or Servicing Shift Whole Loan, the related Loan-Specific Directing Holder identified in the Preliminary Prospectus (which is expected to be the holder of the related controlling pari passu companion loan) prior to the related Servicing Shift Securitization Date. Eightfold Real Estate Capital Fund VI, L.P. or its affiliate is expected to appoint itself or its affiliate as the initial Trust Directing Holder. For a description of the directing holder (or equivalent party) for each Non-Serviced Whole Loan, see “Description of the Mortgage Pool—The Whole Loans” and “Pooling and Servicing Agreement—The Directing Holder” in the Preliminary Prospectus. |

| Control Eligible Certificates: | Class E-RR, Class F-RR, Class G-RR and Class J-RR certificates. |

| Controlling Class: | The Controlling Class will be, as of any time of determination, the most subordinate class of Control Eligible Certificates then-outstanding that has an aggregate Certificate Balance (as notionally reduced by any cumulative appraisal reduction amounts allocable to such class) at least equal to 25% of the initial Certificate Balance of such class; provided that if at any time the Certificate Balances of all Control Eligible Certificates, as notionally reduced by any appraisal reduction amounts (but without regard to any collateral deficiency amounts) allocable to such classes, have been reduced to zero, then the “Controlling Class” will be the most subordinate class of Control Eligible Certificates that has an aggregate principal balance greater than zero; provided, further, that if at any time the Certificate Balances of the Class A-1, Class A-2, Class A-3, Class A-M, Class B, Class C and Class D certificates have been reduced to zero as a result of the allocation of principal payments on the Mortgage Loans, then the “Controlling Class” will be the most subordinate class of Control Eligible Certificates that has an aggregate Certificate Balance greater than zero without regard to the application of appraisal reduction amounts (or any collateral deficiency amounts) to notionally reduce the Certificate Balance of such class. The Controlling Class as of the Closing Date will be the Class J-RR certificates. |

| Appraised-Out Class: | Any class of Control Eligible Certificates that has been determined, as a result of appraisal reduction amounts and collateral deficiency amounts allocable to such class, to no longer be the Controlling Class (an “Appraised-Out Class”). |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 12 | ||

Benchmark 2024-V8 Mortgage Trust |

| STRUCTURE OVERVIEW |

| Remedies Available to Holders of an Appraised-Out Class: | Holders of the majority (by Certificate Balance) of an Appraised-Out Class will have the right, at their sole expense, to require the Special Servicer to order a supplemental appraisal of any Mortgage Loan (or Serviced Whole Loan) for which an appraisal reduction event has occurred or as to which there exists a collateral deficiency amount. Upon receipt of such supplemental appraisal, the Special Servicer will be required to send the appraisal to the Master Servicer, who will be required to recalculate the appraisal reduction amount or collateral deficiency amount, as applicable, based on such supplemental appraisal, and if required by such recalculation, the applicable Appraised-Out Class as the Controlling Class. Any Appraised-Out Class requesting a supplemental appraisal will not be entitled to exercise any rights of the Controlling Class until such time, if any, as the class is reinstated as the Controlling Class. |

Control Termination Event: | Will occur and be continuing with respect to any Mortgage Loan (other than any Servicing Shift Mortgage Loan or Serviced Whole Loan (other than any Servicing Shift Whole Loan), when one or more of the following is true: (i) the Class E-RR certificates have a Certificate Balance (taking into account the application of any cumulative appraisal reduction amounts and collateral deficiency amounts to notionally reduce the Certificate Balance of such class) being reduced to less than 25% of the initial Certificate Balance of that class or (ii) such Mortgage Loan or Whole Loan is an applicable excluded loan; provided, that a Control Termination Event will not be deemed to be continuing in the event the Certificate Balances of all Classes of Principal Balance Certificates other than the Control Eligible Certificates have been reduced to zero; provided, further, that no Control Termination Event may occur with respect to the Loan-Specific Directing Holder related to any Servicing Shift Whole Loan and the term “Control Termination Event” will not be applicable to the Loan-Specific Directing Holder related to such Servicing Shift Whole Loan. With respect to an excluded loan related to the Directing Holder, a Control Termination Event will be deemed to exist. During the continuance of a Control Termination Event, the Directing Holder will no longer have any control rights. The Directing Holder will no longer have the right to direct certain actions of the Special Servicer and will no longer have consent rights with respect to certain material actions that the Master Servicer or Special Servicer proposes to take with respect to a Serviced Mortgage Loan and any related Serviced Companion Loans. During the continuance of a Control Termination Event, the Directing Holder will retain non-binding consultation rights with respect to certain material actions that the Special Servicer proposes to take with respect to a Serviced Mortgage Loan and any related Serviced Companion Loans. Such consultation rights will continue until the occurrence of a Consultation Termination Event. |

| Consultation Termination Event: | Will occur and be continuing with respect to any Mortgage Loan (other than any Servicing Shift Mortgage Loan) or Serviced Whole Loan (other than any Servicing Shift Whole Loan), when one or more of the following is true: (i) there is no class of Control Eligible Certificates that has a then-outstanding Certificate Balance (without regard to the application of any cumulative appraisal reduction amounts) equal to at least 25% of the initial Certificate Balance of that class or (ii) such Mortgage Loan or Whole Loan is an applicable excluded loan; provided that a Consultation Termination Event will not be deemed to be continuing in the event the Certificate Balances of all Classes of Principal Balance Certificates other than the Control Eligible Certificates have been reduced to zero; provided, further, that no Consultation Termination Event may occur with respect to the Loan-Specific Directing Holder related to any Servicing Shift Whole Loan and the term “Consultation Termination Event” will not be applicable to the Loan-Specific Directing Holder related to such Servicing Shift Whole Loan. With respect to an excluded loan related to the Directing Holder, a Consultation Termination Event will be deemed to exist. During the continuance of a Consultation Termination Event, the Directing Holder will have no rights under the PSA other than those rights that all Certificateholders have. |

| Appointment and Replacement of Special Servicer: | The Directing Holder will appoint the initial Special Servicer with respect to each Serviced Mortgage Loan and any related Serviced Companion Loans as of the Closing Date. For so long as no Control Termination Event is continuing, the Directing Holder generally may replace the Special Servicer with respect to each Serviced Mortgage Loan and any related Serviced Companion Loans with or without cause at any time. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 13 | ||

Benchmark 2024-V8 Mortgage Trust |

| STRUCTURE OVERVIEW |

During the continuance of a Control Termination Event, the Directing Holder will no longer have the right to replace the Special Servicer and such replacement (other than with respect to the Non-Serviced Whole Loans) will occur based on a vote of holders of all voting eligible classes of certificates as described below. See “Description of the Mortgage Pool—The Whole Loans” and “Pooling and Servicing Agreement” in the Preliminary Prospectus for a description of the special servicer appointment and replacement rights with respect to Non-Serviced Whole Loans. | |

| Replacement of Special Servicer by Vote of Certificateholders: | Other than with respect to Non-Serviced Whole Loans, if a Control Termination Event is continuing, upon (i) the written direction of holders of certificates evidencing not less than 25% of the voting rights (taking into account the application of any appraisal reduction amounts to notionally reduce the Certificate Balances) of the Principal Balance Certificates and requesting a vote to replace the Special Servicer (other than with respect to any Servicing Shift Whole Loan) with a new special servicer, (ii) payment by such requesting holders to the Certificate Administrator of all reasonable fees and expenses to be incurred by the Certificate Administrator in connection with administering such vote and (iii) delivery by such holders to the Certificate Administrator and Trustee of written confirmations from each Rating Agency that the appointment of the replacement Special Servicer will not result in a downgrade of the certificates, the Certificate Administrator will be required to promptly post notice of such request on the Certificate Administrator’s website and concurrently provide written notice of such request by mail to all Certificateholders of such request and conduct the solicitation of votes of all certificates in such regard, which such vote must occur within 180 days of the posting of such notice. Upon the written direction of (i) holders of Principal Balance Certificates evidencing at least 66-2/3% of a Certificateholder Quorum or (ii) holders of Principal Balance Certificates evidencing more than 50% of the aggregate voting rights of Principal Balance Certificates outstanding that has not been reduced to less than 25% of its initial Certificate Balance through the application of appraisal reduction amounts and realized losses), the Trustee will immediately replace the Special Servicer with the replacement Special Servicer (other than with respect to Non-Serviced Whole Loans). “Certificateholder Quorum” means, in connection with any solicitation of votes in connection with the replacement of the Special Servicer as described above or the Asset Representations Reviewer as described below, the holders of certificates evidencing at least 50% of the aggregate voting rights (taking into account the application of any appraisal reduction amounts to notionally reduce the Certificate Balance of the certificates, except in the case of the termination of the Asset Representations Reviewer) of all Principal Balance Certificates, on an aggregate basis. If at any time, the Operating Advisor determines, in its sole discretion exercised in good faith, that (1) the Special Servicer is not performing its duties as required under the PSA or is otherwise not acting in accordance with the Servicing Standard and (2) the replacement of the Special Servicer would be in the best interest of the Certificateholders as a collective whole, then the Operating Advisor will have the right to recommend the replacement of the Special Servicer. The Operating Advisor’s recommendation to replace the Special Servicer (other than with respect Non-Serviced Whole Loans) must be confirmed by holders of Principal Balance Certificates representing a majority of the Voting Rights (taking into account the application of Appraisal Reduction Amounts to notionally reduce the respective Certificate Balances) of all Principal Balance Certificates whose holders voted on the matter; provided that the holders of Principal Balance Certificates that so voted on the matter (i) hold Principal Balance Certificates representing at least 20% of the Voting Rights (taking into account the application of any appraisal reduction amounts to notionally reduce the respective Certificate Balances) of all Principal Balance Certificates on an aggregate basis and (ii) consist of at least three Certificateholders or Certificate Owners that are not risk retention affiliated with each other) within 180 days from the time such recommendation is posted to the Certificate Administrator website and is subject to the receipt of written confirmations from each Rating Agency that the appointment of the replacement Special Servicer will not result in a downgrade of the certificates. See “Description of the Mortgage Pool—The Whole Loans” and “Pooling and Servicing Agreement” in the Preliminary Prospectus for a description of the special servicer appointment and replacement rights with respect to Non-Serviced Whole Loans. |

| THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED. | ||

| 14 | ||

Benchmark 2024-V8 Mortgage Trust |

| STRUCTURE OVERVIEW |

| Cap on Workout and Liquidation Fees: | The workout fees and liquidation fees payable to a Special Servicer under the PSA will be an amount equal to the lesser of: (1) 1.0% of each collection of interest and principal following a workout or liquidation, subject to a minimum of $25,000 and (2) $1,000,000 per workout or liquidation. All Modification Fees actually paid to the Special Servicer in connection with a workout or liquidation or in connection with any prior workout or partial liquidation that occurred within the prior 18 months will be deducted from the total workout fee (only after receipt by the Special Servicer of workout fees of $25,000) and/or liquidation fees payable (other than Modification Fees earned while the Mortgage Loan was not in special servicing). In addition, the total amount of workout and liquidation fees actually payable by the Issuing Entity under the PSA will be capped in the aggregate at $1,000,000 for each related Mortgage Loan. If a new special servicer begins servicing the related Mortgage Loan, all amounts paid to the prior special servicer will be disregarded for purposes of calculating the cap. |

Special Servicer Compensation: | The special servicing fee will equal 0.25% per annum of the stated principal balance of the related specially serviced loan or REO property, as applicable with a minimum monthly fee of $5,000. The Special Servicer and its affiliates will be prohibited from receiving or retaining any compensation or any other remuneration under the PSA (including, without limitation, in the form of commissions, brokerage fees, rebates, or as a result of any other fee-sharing arrangement) from any person (including, without limitation, the issuing entity, any borrower, any manager, any guarantor or indemnitor in respect of a Serviced Mortgage Loan and any related Serviced Companion Loans, and any purchaser of any Serviced Mortgage Loan and any related Serviced Companion Loan or REO Property) in connection with the disposition, workout or foreclosure of any Mortgage Loan (or Serviced Whole Loan, if applicable), the management or disposition of any REO Property, or the performance of any other special servicing duties under the PSA, other than as expressly permitted in the PSA and other than commercially reasonable treasury management fees, banking fees, property condition report fees, customary title agent fees and insurance commissions or fees received or retained by the Special Servicer or any of its Affiliates in connection with any services performed by such party with respect to any Mortgage Loan, Serviced Whole Loan or REO Property. Subject to certain limited exceptions, the Special Servicer will also be required to report any compensation or other remuneration the Special Servicer or its affiliates have received from any person and such information will be disclosed in the Certificateholders’ monthly distribution date statement. |