UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D. C. 20549

FORM N-CSR

Investment Company Act file number: 811-02671

Deutsche Municipal Trust

(Exact Name of Registrant as Specified in Charter)

345 Park Avenue

New York, NY 10154-0004

(Address of Principal Executive Offices) (Zip Code)

Registrant’s Telephone Number, including Area Code: (212) 250-3220

Paul Schubert

60 Wall Street

New York, NY 10005

(Name and Address of Agent for Service)

| Date of fiscal year end: | 5/31 |

| Date of reporting period: | 5/31/2016 |

| ITEM 1. | REPORT TO STOCKHOLDERS |

May 31, 2016

Annual Report

to Shareholders

Deutsche Strategic High Yield Tax-Free Fund

Contents

3 Letter to Shareholders 5 Portfolio Management Review 11 Performance Summary 13 Investment Portfolio 37 Statement of Assets and Liabilities 39 Statement of Operations 40 Statement of Cash Flows 41 Statement of Changes in Net Assets 42 Financial Highlights 46 Notes to Financial Statements 58 Report of Independent Registered Public Accounting Firm 59 Information About Your Fund's Expenses 60 Tax Information 61 Advisory Agreement Board Considerations and Fee Evaluation 66 Board Members and Officers 71 Account Management Resources |

This report must be preceded or accompanied by a prospectus. To obtain a summary prospectus, if available, or prospectus for any of our funds, refer to the Account Management Resources information provided in the back of this booklet. We advise you to consider the fund's objectives, risks, charges and expenses carefully before investing. The summary prospectus and prospectus contain this and other important information about the fund. Please read the prospectus carefully before you invest.

Bond investments are subject to interest-rate, credit, liquidity and market risks to varying degrees. When interest rates rise, bond prices generally fall. Credit risk refers to the ability of an issuer to make timely payments of principal and interest. Investments in lower-quality ("junk bonds") and non-rated securities present greater risk of loss than investments in higher-quality securities. The fund invests in inverse floaters, which are derivatives that involve leverage and could magnify the fund's gains or losses. Although the fund seeks income that is exempt from federal income taxes, a portion of the fund’s distributions may be subject to federal, state and local taxes, including the alternative minimum tax. See the prospectus for details.

Deutsche Asset Management represents the asset management activities conducted by Deutsche Bank AG or any of its subsidiaries.

NOT FDIC/NCUA INSURED NO BANK GUARANTEE MAY LOSE VALUE NOT A DEPOSIT NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY

Letter to Shareholders

Dear Shareholder:

Seven years into our economic recovery, you might be wondering "where’s the proof?" The strong U.S. dollar and sluggish growth have hampered exports and manufacturing. Low oil prices are raising concerns about the energy sector. A steep sell-off in the first quarter, plus a contentious U.S. election campaign and ongoing geopolitical issues, have led many to question what lies ahead.

Our analysts see a case for continued, albeit modest, growth in the U.S. economy. Households have reduced debt and are seeing gains in real income thanks to improving labor markets and lower energy prices. Businesses remain reasonably well positioned financially, with an added boost to purchasing power from lower energy prices. Lastly, while the Federal Reserve Board has initiated the process of raising short-term interest rates, we are confident that "low and slow" will continue to be the watchwords for a while.

The later stages of an economic recovery tend to bring increased volatility and more challenges to achieving positive investment returns. We believe that active management — careful sector allocation and security selection driven by deep research — can make a difference in this environment.

In the end, it is important to remember the core reason for investing: long- term goals and a desire for growth tempered by reasonable risk management. We appreciate your trust and welcome the opportunity to put our resources, experience and expertise to work in helping you meet your goals.

Best regards,

|

Brian Binder President, Deutsche Funds |

Please note: Deutsche Asset & Wealth Management is now two distinct businesses: Deutsche Asset Management and Deutsche Bank Wealth Management. As a result, our key service providers were renamed Deutsche AM Service Company; Deutsche AM Distributors, Inc. and Deutsche AM Trust Company, effective May 9, 2016.

Assumptions, estimates and opinions contained in this document constitute our judgment as of the date of the document and are subject to change without notice. Any projections are based on a number of assumptions as to market conditions and there can be no guarantee that any projected results will be achieved. Past performance is not a guarantee of future results.

Portfolio Management Review (Unaudited)

Overview of Market and Fund Performance

All performance information below is historical and does not guarantee future results. Returns shown are for Class A shares, unadjusted for sales charges. Investment return and principal fluctuate, so your shares may be worth more or less when redeemed. Current performance may differ from performance data shown. Please visit deutschefunds.com for the most recent month-end performance of all share classes. Fund performance includes reinvestment of all distributions. Unadjusted returns do not reflect sales charges and would have been lower if they had. Please refer to pages 11 through 12 for more complete performance information.

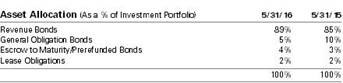

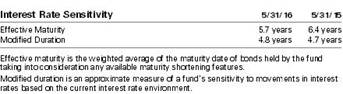

Investment Strategy The fund invests in a wide variety of municipal bonds. These include general obligation bonds, for which payments of principal and interest are secured by the full faith and credit of the issuer and usually supported by the issuer's taxing power. In addition, securities held may include revenue bonds, for which principal and interest are secured by revenues from tolls, rents or other fees gained from the facility that was built with the bond issue proceeds. The fund's management team seeks to hold municipal bonds that appear to offer the best opportunity to meet the fund's objective of providing a high level of income exempt from regular federal income tax. In selecting securities, the managers weigh a number of factors against each other, from economic outlooks and possible interest rate movements to characteristics of specific securities such as coupon, maturity date and call date, and changes in supply and demand within the municipal bond market. Although portfolio management may adjust the fund's duration (a measure of sensitivity to interest rates) over a wider range, they generally intend to keep it similar to that of the Barclays Municipal Bond Index, generally between five and nine years. |

Deutsche Strategic High Yield Tax-Free Fund posted a return of 6.27% for the period ended May 31, 2016. The overall municipal bond market, as measured by the unmanaged Barclays Municipal Bond Index, delivered a total return of 5.87% for the same period. The average fund in the Morningstar High Yield Muni category returned 7.08% for the 12 months ended May 31, 2016.

The 12-month period ended May 31, 2016 saw the U.S. economy continue on a moderate upward trend. While corporate profits were challenged by a strong dollar, key indicators in areas such as employment and housing strengthened notably. In December of 2015, the U.S. Federal Reserve Board (the Fed) implemented a modest 25 basis point hike in its benchmark short-term rate, the first such increase in nine years. However, as the period progressed, with inflation remaining in check and weak growth overseas, the Fed pushed back its timetable for further steps towards normalizing rates, helping to support sentiment for U.S. fixed income markets broadly.

| "Against a backdrop of extraordinarily low global interest rates, the municipal market was the beneficiary of strong demand from yield-seeking investors." |

Against a backdrop of a generally benign credit outlook and extraordinarily low global interest rates, the municipal market was the beneficiary of strong demand from yield-seeking investors. New municipal issues were heavily oversubscribed, and tax-free mutual funds experienced ongoing positive weekly inflows beginning in November of 2015.

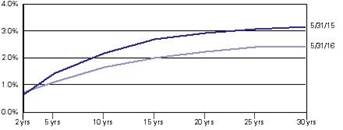

The municipal yield curve flattened over the 12 months ended May 31, 2016, as yields declined along most of the curve. Specifically, the two-year bond yield rose from 0.62% to 0.72%, while the five-year yield fell from 1.41% to 1.09%, the 20-year fell from 2.93% to 2.25%, and the 30-year fell from 3.16% to 2.45%. (See the graph below for municipal bond yield changes from the beginning to the end of the period.) For the 12 months, municipal market credit spreads — the incremental yield offered by lower-quality issues vs. AAA-rated issues — generally tightened.

| Municipal Bond Yield Curve (as of 5/31/16 and 5/31/15) |

|

Source: Municipal Market Data, AAA-rated universe, as of 5/31/16.

Chart is for illustrative purposes only and does not represent any Deutsche AM product.

Positive and Negative Contributors to Fund Performance

With a reasonably steep yield curve as the period began, we had a tilt in the portfolio towards longer-term issues in the 20-to-30-year maturity range. This exposure was a positive contributor to relative performance, as the fund was able to earn incremental income and benefit from the decline in yields and corresponding price strength among issues on the longer end of the curve.

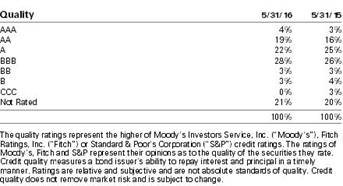

The fund's holdings of BBB-rated issues and issues rated below-investment-grade helped performance relative to the benchmark, as credit spreads tightened over the 12 months ended May 31, 2016. That said, we had significantly less exposure to lower-rated, high-yield issues than many of the funds in our peer group. In particular, we had moderately light relative exposure to the volatile tobacco sector, which strongly outperformed during the period. The fund had a small position in Puerto Rico issues, which suffered as the territory's debt crisis worsened over the period. We remain comfortable with our more conservative approach on the fund's credit and maturity profile given the narrowing of credit spreads that has occurred along with a weakening of covenants on many new issues.

Overall positioning with respect to credit quality within the investment-grade portion of the fund was a modest contributor to performance vs. the benchmark. Specifically, during the period we maintained significant exposure to issues in the single A and BBB quality ranges. In particular, our holdings of health care, transportation and airport bonds added to relative performance.

The fund has had a preference for callable issues with coupons in the 5% range, well above current rates. Such bonds are typically priced at significant premiums over par value, and are less sensitive to changes in market interest rates. As rates remained low, issuers were able to attract investors by offering bonds with 4% coupons at lower premiums (and therefore less market protection) and higher yields. The Fund was underweight the higher-yielding 4% coupon structure vs. the index, which detracted slightly from performance during the period.

The fund used inverse floaters, whose coupon rates move in the opposite direction of short-term interest rates, adding additional income in the steep yield curve environment.

Outlook and Positioning

At the end of the period, municipal yields were at low levels by historical standards, but remained reasonably attractive relative to U.S. Treasuries. As of the end of May 2016, the 10-year municipal bond yield of 1.66% was 89.7% of the comparable-maturity U.S. Treasury bond yield before taking into account the tax advantage of municipals. The 30-year municipal yield of 2.45% was 92.4% of the comparable U.S. Treasury yield.

While the curve has continued to flatten, longer-term issues still carry a meaningful yield advantage. We continue to evaluate premium coupon issues in the 20-to-25-year range that can provide a degree of protection against rising interest rates.

Credit spreads have continued to narrow in the wake of the ongoing global search for yield. With respect to the fund's credit exposure, we view spreads for issues rated BBB as relatively tight and see valuations among bonds in the A and AA quality ranges as more attractive overall. The decline in oil prices has helped bolster transportation-related credits overall, but has negatively impacted fundamentals and ratings in a handful of states.

In recent months, new municipal issues have been subscribed several times over and covenants have become less favorable to investors. We continue to be highly selective as we look for opportunities to add incremental yield, while maintaining a strong focus on liquidity.

Portfolio Management Team

Rebecca L. Flinn, Director

Co-Lead Portfolio Manager of the fund. Began managing the fund in 1998.

— Joined Deutsche Asset Management in 1986.

— BA, University of Redlands, California.

A. Gene Caponi, CFA, Managing Director

Co-Lead Portfolio Manager of the fund. Began managing the fund in 2009.

— Joined Deutsche Asset Management in 1998.

— BS, State University of New York, Oswego; MBA, State University of New York at Albany.

Ashton P. Goodfield, CFA, Managing Director

Co-Lead Portfolio Manager of the fund. Began managing the fund in 2014.

— Joined Deutsche Asset Management in 1986.

— Co-Head of Municipal Bonds.

— BA, Duke University.

Carol L. Flynn, CFA, Managing Director

Co-Lead Portfolio Manager of the fund. Began managing the fund in 2014.

— Joined Deutsche Asset Management in 1994.

— Co-Head of Municipal Bonds.

— BS from Duke University; MBA from University of Connecticut.

The views expressed reflect those of the portfolio management team only through the end of the period of the report as stated on the cover. The management team's views are subject to change at any time based on market and other conditions and should not be construed as a recommendation. Past performance is no guarantee of future results. Current and future portfolio holdings are subject to risk.

Terms to Know

The Barclays Municipal Bond Index is an unmanaged, market-value-weighted measure of municipal bonds issued across the United States. Index issues have a credit rating of at least Baa and a maturity of at least two years. Index returns do not reflect fees or expenses and it is not possible to invest directly into an index.

The Morningstar High Yield Muni category consists of funds that invest at least 50% of their assets in high-income municipal securities that are not rated or that are rated at a level of BBB and below.

Credit quality measures a bond issuer's ability to repay interest and principal in a timely manner. Rating agencies assign letter designations, such as AAA, AA and so forth. The lower the rating the higher the probability of default. Credit quality does not remove market risk and is subject to change.

The yield curve is a graph with a left-to-right line that shows how high or low yields are, from the shortest to the longest maturities. Typically (and when the yield curve is characterized as "steep," this is especially true), the line rises from left to right as investors who are willing to tie up their money for a longer period are rewarded with higher yields.

Credit spread is the additional yield provided by municipal bonds rated AA and below vs. municipals rated AAA with comparable effective maturity.

Duration, which is expressed in years, measures the sensitivity of the price of a bond or bond fund to a change in interest rates.

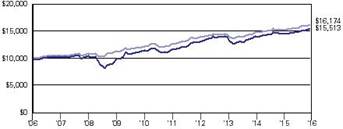

Performance Summary May 31, 2016 (Unaudited)

| Class A | 1-Year | 5-Year | 10-Year |

| Average Annual Total Returns as of 5/31/16 | |||

| Unadjusted for Sales Charge | 6.27% | 6.05% | 4.78% |

| Adjusted for the Maximum Sales Charge (max 2.75% load) | 3.35% | 5.46% | 4.49% |

| Barclays Municipal Bond Index† | 5.87% | 5.07% | 4.93% |

| Class C | 1-Year | 5-Year | 10-Year |

| Average Annual Total Returns as of 5/31/16 | |||

| Unadjusted for Sales Charge | 5.40% | 5.24% | 4.00% |

| Adjusted for the Maximum Sales Charge (max 1.00% CDSC) | 5.40% | 5.24% | 4.00% |

| Barclays Municipal Bond Index† | 5.87% | 5.07% | 4.93% |

| Class S | 1-Year | 5-Year | 10-Year |

| Average Annual Total Returns as of 5/31/16 | |||

| No Sales Charges | 6.54% | 6.31% | 5.04% |

| Barclays Municipal Bond Index† | 5.87% | 5.07% | 4.93% |

| Institutional Class | 1-Year | 5-Year | 10-Year |

| Average Annual Total Returns as of 5/31/16 | |||

| No Sales Charges | 6.51% | 6.31% | 5.06% |

| Barclays Municipal Bond Index† | 5.87% | 5.07% | 4.93% |

Performance in the Average Annual Total Returns table(s) above and the Growth of an Assumed $10,000 Investment line graph that follows is historical and does not guarantee future results. Investment return and principal fluctuate, so your shares may be worth more or less when redeemed. Current performance may differ from performance data shown. Please visit deutschefunds.com for the Fund's most recent month-end performance. Fund performance includes reinvestment of all distributions. Unadjusted returns do not reflect sales charges and would have been lower if they had.

The gross expense ratios of the Fund, as stated in the fee table of the prospectus dated October 1, 2015 are 1.00%, 1.76%, 0.83% and 0.75% for Class A, Class C, Class S and Institutional Class shares, respectively, and may differ from the expense ratios disclosed in the Financial Highlights tables in this report.

Index returns do not reflect any fees or expenses and it is not possible to invest directly into an index.

Performance figures do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares.

A portion of the Fund's distributions may be subject to federal, state and local taxes and the alternative minimum tax.

| Growth of an Assumed $10,000 Investment (Adjusted for Maximum Sales Charge) |

■ Deutsche Strategic High Yield Tax-Free Fund — Class A ■ Barclays Municipal Bond Index† |

|

| Yearly periods ended May 31 |

The Fund's growth of an assumed $10,000 investment is adjusted for the maximum sales charge of 2.75%. This results in a net initial investment of $9,725.

The growth of $10,000 is cumulative.

Performance of other share classes will vary based on the sales charges and the fee structure of those classes.

† The Barclays Municipal Bond Index is an unmanaged, market-value-weighted measure of municipal bonds issued across the United States. Index issues have a credit rating of at least Baa and a maturity of at least two years.

| Class A | Class C | Class S | Institutional Class | |

| Net Asset Value | ||||

| 5/31/16 | $ 12.59 | $ 12.59 | $ 12.60 | $ 12.60 |

| 5/31/15 | $ 12.39 | $ 12.40 | $ 12.40 | $ 12.40 |

| Distribution Information as of 5/31/16 | ||||

| Income Dividends, Twelve Months | $ .55 | $ .46 | $ .58 | $ .58 |

| Capital Gain Distributions, Twelve Months | $ .01 | $ .01 | $ .01 | $ .01 |

| May Income Dividend | $ .0441 | $ .0361 | $ .0468 | $ .0468 |

| SEC 30-day Yield‡‡ | 1.88% | 1.19% | 2.18% | 2.18% |

| Tax Equivalent Yield‡‡ | 3.32% | 2.10% | 3.85% | 3.85% |

| Current Annualized Distribution Rate‡‡ | 4.20% | 3.44% | 4.46% | 4.46% |

‡‡ The SEC yield is net investment income per share earned over the month ended May 31, 2016 shown as an annualized percentage of the maximum offering price per share on the last day of the period. The SEC yield is computed in accordance with a standardized method prescribed by the Securities and Exchange Commission. The SEC yield would have been 1.82%, 1.10%, 2.04% and 2.09% for Classes A, C, S and Institutional shares, respectively, had certain expenses not been reduced. Tax equivalent yield is based on the Fund's yield and a marginal federal income rate of 43.40%. Current annualized distribution rate is the latest monthly dividend shown as an annualized percentage of net asset value on May 31, 2016. Distribution rate simply measures the level of dividends and is not a complete measure of performance. The current annualized distribution rate would have been 4.14%, 3.35%, 4.32% and 4.37% for Classes A, C, S and Institutional shares, respectively, had certain expenses not been reduced. Yields and distribution rates are historical, not guaranteed and will fluctuate.

Investment Portfolio as of May 31, 2016

| Principal Amount ($) | Value ($) | ||

| Municipal Bonds and Notes 96.7% | |||

| Arizona 1.6% | |||

| Arizona, Salt River Pima-Maricopa, Indian Community, 0.13%**, 10/1/2025 | 11,945,000 | 11,945,000 | |

| Arizona, Salt Verde Financial Corp., Gas Revenue, 5.25%, 12/1/2025, GTY: Citigroup, Inc. | 4,000,000 | 4,816,600 | |

| Maricopa County, AZ, Pollution Control Corp. Revenue, El Paso Electric Co. Project, Series B, 7.25%, 4/1/2040 | 3,930,000 | 4,563,123 | |

| Tempe, AZ, Industrial Development Authority Revenue, Tempe Life Care Village, Inc.: | |||

| Series A, 6.25%, 12/1/2042 | 1,535,000 | 1,682,590 | |

| Series A, 6.25%, 12/1/2046 | 1,400,000 | 1,532,300 | |

| 24,539,613 | |||

| California 10.4% | |||

| California, Golden State Tobacco Securitization Corp., Tobacco Settlement, Series A-1, 5.75%, 6/1/2047 | 10,000,000 | 10,115,900 | |

| California, M-S-R Energy Authority, Series B, 7.0%, 11/1/2034, GTY: Citigroup, Inc. | 8,750,000 | 13,128,325 | |

| California, Metropolitan Water District of Southern California, Series D, 0.36%**, 7/1/2035 | 3,000,000 | 3,000,000 | |

| California, Morongo Band of Mission Indians, Enterprise Casino Revenue, Series B, 144A, 6.5%, 3/1/2028 | 5,000,000 | 5,417,700 | |

| California, State General Obligation: | |||

| 5.0%, 8/1/2034 | 5,185,000 | 5,624,844 | |

| 5.5%, 3/1/2040 | 5,130,000 | 5,985,735 | |

| California, State General Obligation, Various Purposes: | |||

| 5.0%, 11/1/2032 | 10,000,000 | 10,600,600 | |

| 5.75%, 4/1/2031 | 23,360,000 | 26,557,283 | |

| California, State Public Works Board, Lease Revenue, Series B, 5.0%, 10/1/2039 | 5,500,000 | 6,574,095 | |

| California, State Public Works Board, Lease Revenue, Capital Projects: | |||

| Series A-1, 6.0%, 3/1/2035 | 10,175,000 | 12,008,433 | |

| Series I-1, 6.375%, 11/1/2034 | 5,000,000 | 5,972,800 | |

| California, Statewide Communities Development Authority Revenue, Loma Linda University Medical Center: | |||

| Series A, 5.25%, 12/1/2044 | 1,305,000 | 1,465,541 | |

| Series A, 144A, 5.25%, 12/1/2056 | 5,515,000 | 6,224,119 | |

| Series A, 5.5%, 12/1/2054 | 1,305,000 | 1,479,048 | |

| California, Statewide Communities Development Authority Revenue, Terraces At San Joaquin Gardens Project: | |||

| Series A, 5.625%, 10/1/2032 | 500,000 | 540,890 | |

| Series A, 6.0%, 10/1/2042 | 1,000,000 | 1,091,570 | |

| Series A, 6.0%, 10/1/2047 | 1,000,000 | 1,089,590 | |

| Long Beach, CA, Bond Finance Authority, Natural Gas Purchase Revenue, Series A, 5.25%, 11/15/2023, GTY: Merrill Lynch & Co., Inc. | 620,000 | 742,301 | |

| Los Angeles, CA, Department of Airports Revenue, Series A, AMT, 5.0%, 5/15/2042 (a) | 1,875,000 | 2,218,688 | |

| Riverside County, CA, Transportation Commission Toll Revenue Senior Lien, Series A, 5.75%, 6/1/2048 | 2,850,000 | 3,345,586 | |

| San Buenaventura, CA, Community Memorial Health Systems, 7.5%, 12/1/2041 | 3,250,000 | 4,018,950 | |

| San Diego, CA, Community College District, Election of 2006, 5.0%, 8/1/2036 | 2,050,000 | 2,389,111 | |

| San Francisco City & County, CA, Airports Commission, International Airport Revenue, Series A, AMT, 5.0%, 5/1/2044 | 11,000,000 | 12,564,750 | |

| San Francisco City & County, CA, Redevelopment Agency, Series C, AMT, 0.41%**, 6/15/2034, LIQ: Fannie Mae | 50,000 | 50,000 | |

| San Francisco, CA, City & County Public Utilities Commission, Water Revenue, Series A, 5.125%, 11/1/2039 | 10,400,000 | 11,784,136 | |

| San Francisco, CA, City & County Redevelopment Financing Authority, Tax Allocation, Mission Bay South Redevelopment, Series D, Prerefunded, 7.0%, 8/1/2041 | 1,400,000 | 1,771,406 | |

| San Joaquin Hills, CA, Transportation Corridor Agency, Toll Road Revenue, Series A, 5.0%, 1/15/2050 | 3,555,000 | 4,005,170 | |

| Vernon, CA, Electric Systems Revenue, Series A, 5.5%, 8/1/2041 | 2,240,000 | 2,591,254 | |

| 162,357,825 | |||

| Colorado 1.9% | |||

| Colorado, E-470 Public Highway Authority Revenue, Series C, 5.375%, 9/1/2026 | 2,000,000 | 2,256,080 | |

| Colorado, Health Facilities Authority Revenue, Christian Living Communities Project, Series A, 5.75%, 1/1/2037 | 1,000,000 | 1,010,130 | |

| Colorado, Health Facilities Authority Revenue, Valley View Hospital Association, 5.75%, 5/15/2036 | 2,000,000 | 2,159,760 | |

| Colorado, Park Creek Metropolitan District Revenue, Senior Ltd. Property Tax Supported, Series A, 5.0%, 12/1/2045 | 1,765,000 | 2,015,718 | |

| Colorado, Public Energy Authority, Natural Gas Purchased Revenue, 6.25%, 11/15/2028, GTY: Merrill Lynch & Co.,Inc. | 6,365,000 | 8,224,471 | |

| Colorado, Regional Transportation District, Private Activity Revenue, Denver Transit Partners, 6.0%, 1/15/2041 | 2,000,000 | 2,317,140 | |

| Colorado, State Health Facilities Authority Revenue, Christian Living Community, 6.375%, 1/1/2041 | 1,615,000 | 1,765,292 | |

| Colorado, State Health Facilities Authority Revenue, Covenant Retirement Communities: | |||

| Series A, 5.0%, 12/1/2033 | 4,835,000 | 5,364,529 | |

| Series A, 5.0%, 12/1/2035 | 2,500,000 | 2,833,800 | |

| Montrose, CO, Memorial Hospital Revenue, 6.375%, 12/1/2023 | 2,355,000 | 2,365,739 | |

| 30,312,659 | |||

| Connecticut 2.0% | |||

| Connecticut, Harbor Point Infrastructure Improvement District, Special Obligation Revenue, Harbor Point Project, Series A, 7.875%, 4/1/2039 | 20,000,000 | 23,634,400 | |

| Connecticut, Mashantucket Western Pequot Tribe Bond, 6.05%, 7/1/2031 (PIK)* | 16,664,460 | 999,868 | |

| Connecticut, Mohegan Tribe Indians Gaming Authority, Priority Distribution, 144A, 5.25%, 1/1/2033 | 3,000,000 | 2,900,250 | |

| Connecticut, State Health & Educational Facility Authority Revenue, Church Home of Hartford, Inc. Project: | |||

| Series A, 144A, 5.0%, 9/1/2046 | 1,000,000 | 1,077,100 | |

| Series A, 144A, 5.0%, 9/1/2053 | 1,500,000 | 1,599,015 | |

| Hamden, CT, Facility Revenue, Whitney Center Project, Series A, 7.625%, 1/1/2030 | 1,115,000 | 1,183,416 | |

| 31,394,049 | |||

| District of Columbia 0.6% | |||

| District of Columbia, Center for Internships & Academic Revenue, 0.38%**, 7/1/2036, LOC: Branch Banking & Trust | 1,600,000 | 1,600,000 | |

| Metropolitan Washington, DC, Airport Authority Dulles Toll Road Revenue, Dulles Metrorail & Capital Important Project, Series A, 5.0%, 10/1/2053 | 7,000,000 | 7,691,950 | |

| 9,291,950 | |||

| Florida 7.3% | |||

| Collier County, FL, Industrial Development Authority, Continuing Care Community Revenue, Arlington of Naples Project, Series A, 8.125%, 5/15/2044 | 4,000,000 | 4,791,720 | |

| Florida, Capital Region Community Development District, Capital Improvement Revenue, Series A, 7.0%, 5/1/2039 | 5,790,000 | 5,885,130 | |

| Florida, Halifax Hospital Medical Center, 5.0%, 6/1/2036 | 890,000 | 1,049,969 | |

| Florida, Middle Village Community Development District, Special Assessment, Series A, 6.0%, 5/1/2035 | 7,905,000 | 6,823,833 | |

| Florida, State Higher Educational Facilities Financial Authority Revenue, Nova Southeastern University Project, 5.0%, 4/1/2035 | 1,500,000 | 1,779,060 | |

| Florida, State Mid-Bay Bridge Authority, Series A, 5.0%, 10/1/2035 | 1,030,000 | 1,185,705 | |

| Florida, Village Community Development District No. 9, Special Assessment Revenue: | |||

| 5.5%, 5/1/2042 | 1,380,000 | 1,591,775 | |

| 7.0%, 5/1/2041 | 1,630,000 | 1,990,279 | |

| Greater Orlando, FL, Aviation Authority Airport Facilities Revenue, Jetblue Airways Corp. Project, AMT, 5.0%, 11/15/2026 | 1,500,000 | 1,624,335 | |

| Highlands County, FL, Health Facilities Authority Revenue, Adventist Health System: | |||

| Series G, Prerefunded, 5.125%, 11/15/2020 | 1,000,000 | 1,020,480 | |

| Series G, Prerefunded, 5.125%, 11/15/2021 | 70,000 | 71,434 | |

| Series G, Prerefunded, 5.125%, 11/15/2022 | 75,000 | 76,536 | |

| Series G, Prerefunded, 5.125%, 11/15/2023 | 180,000 | 183,686 | |

| Lee County, FL, Airport Revenue, Series A, AMT, 5.375%, 10/1/2032 | 1,750,000 | 2,015,335 | |

| Martin County, FL, Health Facilities Authority, Martin Memorial Medical Center, 5.5%, 11/15/2042 | 3,040,000 | 3,433,680 | |

| Miami Beach, FL, Health Facilities Authority, Mount Sinai Medical Center: | |||

| 5.0%, 11/15/2029 | 1,000,000 | 1,147,210 | |

| 5.0%, 11/15/2044 | 2,500,000 | 2,851,900 | |

| Miami-Dade County, FL, Aviation Revenue, Miami International Airport: | |||

| Series A, AMT, 5.25%, 10/1/2033, INS: AGC | 10,000,000 | 10,874,600 | |

| Series A-1, 5.5%, 10/1/2041 | 5,000,000 | 5,748,550 | |

| Miami-Dade County, FL, Double Barreled Aviation, 5.0%, 7/1/2041 | 5,000,000 | 5,675,700 | |

| Miami-Dade County, FL, Expressway Authority, Toll Systems Revenue, Series A, 5.0%, 7/1/2044 | 2,500,000 | 2,870,000 | |

| Miami-Dade County, FL, Water & Sewer Systems Revenue, 5.0%, 10/1/2034 | 3,650,000 | 4,181,476 | |

| Orange County, FL, Health Facilities Authority Revenue, Orlando Health, Inc., Series A, 5.0%, 10/1/2034 | 2,500,000 | 3,031,700 | |

| Orange County, FL, Health Facilities Authority Revenue, Orlando Regional Healthcare, Series C, Prerefunded, 5.25%, 10/1/2035 | 5,000,000 | 5,504,050 | |

| Orange County, FL, School Board, Certificates of Participation, Series C, 5.0%, 8/1/2033 | 5,535,000 | 6,687,387 | |

| Palm Beach County, FL, Health Facilities Authority, Retirement Community Revenue, Acts Retirement-Life Communities, Inc., 5.5%, 11/15/2033 | 9,000,000 | 10,182,330 | |

| Port St. Lucie, FL, Special Assessment Revenue, Southwest Annexation District 1, Series B, 5.0%, 7/1/2027, INS: NATL | 2,500,000 | 2,604,425 | |

| Seminole Tribe, FL, Special Obligation Revenue: | |||

| Series A, 144A, 5.5%, 10/1/2024 | 8,000,000 | 8,346,880 | |

| Series A, 144A, 5.75%, 10/1/2022 | 9,500,000 | 9,903,275 | |

| Tallahassee, FL, Health Facilities Revenue, Memorial Healthcare, Inc. Project, Series A, 5.0%, 12/1/2055 | 1,120,000 | 1,276,643 | |

| 114,409,083 | |||

| Georgia 3.1% | |||

| Americus-Sumter County, GA, Hospital Authority, Magnolia Manor Obligated Group, Series A, 6.375%, 5/15/2043 | 4,000,000 | 4,447,360 | |

| Atlanta, GA, Tax Allocation, Beltline Project, Series B, 7.375%, 1/1/2031 | 4,915,000 | 5,582,113 | |

| Atlanta, GA, Water & Wastewater Revenue, Series B, 5.375%, 11/1/2039, INS: AGMC | 10,000,000 | 11,270,800 | |

| De Kalb County, GA, Hospital Authority Revenue, Anticipation Certificates, Dekalb Medical Center, Inc. Project, 6.125%, 9/1/2040 | 7,500,000 | 8,581,275 | |

| De Kalb County, GA, Water & Sewer Revenue, Series A, 5.25%, 10/1/2032 | 820,000 | 967,346 | |

| Gainesville & Hall County, GA, Hospital Authority, Northeast Georgia Health System, Inc. Project: | |||

| Series A, 5.25%, 8/15/2049 | 500,000 | 595,700 | |

| Series A, 5.5%, 8/15/2054 | 1,820,000 | 2,217,524 | |

| Georgia, Glynn-Brunswick Memorial Hospital Authority, Anticipation Certificates, Southeast Georgia Health System Obligated Group, Series A, 5.625%, 8/1/2034 | 550,000 | 596,882 | |

| Georgia, Main Street Natural Gas, Inc., Gas Project Revenue: | |||

| Series A, 5.0%, 3/15/2019, GTY: JPMorgan Chase & Co. (b) | 10,000,000 | 10,940,800 | |

| Series A, 5.5%, 9/15/2024, GTY: Merrill Lynch & Co., Inc. | 2,440,000 | 2,988,951 | |

| 48,188,751 | |||

| Guam 1.1% | |||

| Government of Guam, General Obligation, Series A, Prerefunded, 7.0%, 11/15/2039 | 10,155,000 | 12,245,407 | |

| Guam, International Airport Authority, Series C, AMT, 6.375%, 10/1/2043 | 1,610,000 | 1,959,305 | |

| Guam, Power Authority Revenue, Series A, 5.5%, 10/1/2030 | 3,000,000 | 3,383,790 | |

| 17,588,502 | |||

| Hawaii 1.1% | |||

| Hawaii, State Department of Budget & Finance, Special Purpose Revenue, 15 Craigside Project, Series A, 9.0%, 11/15/2044 | 2,000,000 | 2,445,860 | |

| Hawaii, State Department of Budget & Finance, Special Purpose Revenue, Hawaiian Electric Co., Inc.: | |||

| Series B, AMT, 4.6%, 5/1/2026, INS: FGIC | 11,790,000 | 12,039,476 | |

| 6.5%, 7/1/2039 | 2,500,000 | 2,845,500 | |

| 17,330,836 | |||

| Illinois 5.4% | |||

| Chicago, IL, General Obligation, Series A, 5.25%, 1/1/2029, INS: AGMC | 175,000 | 175,683 | |

| Chicago, IL, O'Hare International Airport Revenue, Third Lien: | |||

| Series A, 5.75%, 1/1/2039 | 9,955,000 | 11,615,295 | |

| Series B, 6.0%, 1/1/2041 | 12,095,000 | 14,402,242 | |

| Cook County, IL, Forest Preservation District, Series C, 5.0%, 12/15/2037 | 1,845,000 | 2,044,186 | |

| Illinois, Finance Authority Revenue, Elmhurst Memorial Healthcare, Series A, 5.625%, 1/1/2037 | 5,500,000 | 5,838,855 | |

| Illinois, Finance Authority Revenue, Friendship Village of Schaumburg: | |||

| Series A, 5.625%, 2/15/2037 | 5,000,000 | 5,001,200 | |

| 7.25%, 2/15/2045 | 4,000,000 | 4,296,400 | |

| Illinois, Finance Authority Revenue, Rush University Medical Center, Series B, Prerefunded, 5.75%, 11/1/2028, INS: NATL | 1,250,000 | 1,396,875 | |

| Illinois, Finance Authority Revenue, Swedish Covenant Hospital, Series A, 6.0%, 8/15/2038 | 7,830,000 | 8,765,763 | |

| Illinois, Finance Authority Revenue, The Admiral at Lake Project: | |||

| Series A, 7.75%, 5/15/2030 | 1,675,000 | 1,932,113 | |

| Series A, 8.0%, 5/15/2040 | 1,000,000 | 1,156,660 | |

| Series A, 8.0%, 5/15/2046 | 3,500,000 | 4,034,380 | |

| Illinois, Finance Authority Revenue, Three Crowns Park Plaza: | |||

| Series A, 5.875%, 2/15/2026 | 1,225,000 | 1,226,874 | |

| Series A, 5.875%, 2/15/2038 | 500,000 | 500,545 | |

| Illinois, Railsplitter Tobacco Settlement Authority, 6.0%, 6/1/2028 | 6,405,000 | 7,636,233 | |

| Illinois, State Finance Authority Revenue, OSF Healthcare Systems, Series A, 5.0%, 5/15/2041 | 5,265,000 | 5,873,318 | |

| Illinois, State Finance Authority Revenue, Park Place of Elmhurst Project: | |||

| Series C, 2.0%, 5/15/2055 | 900,000 | 112,392 | |

| Series A, 6.33%, 5/15/2048 | 5,100,000 | 5,132,385 | |

| Illinois, State Finance Authority Revenue, Trinity Health Corp., Series L, 5.0%, 12/1/2030 | 1,500,000 | 1,718,190 | |

| Springfield, IL, Electric Revenue, Senior Lien, 5.0%, 3/1/2040, INS: AGMC | 1,935,000 | 2,240,479 | |

| 85,100,068 | |||

| Indiana 1.4% | |||

| Indiana, State Finance Authority Revenue, Greencroft Obligation Group, Series A, 7.0%, 11/15/2043 | 2,290,000 | 2,693,544 | |

| Indiana, State Finance Authority Revenue, I-69 Development Partners LLC, AMT, 5.25%, 9/1/2034 | 2,275,000 | 2,564,971 | |

| Indiana, State Health & Educational Financing Authority, Hospital Revenue, Community Foundation of Northwest State: | |||

| 5.5%, 3/1/2037 | 850,000 | 874,140 | |

| Prerefunded, 5.5%, 3/1/2037 | 900,000 | 932,031 | |

| North Manchester, IN, Economic Development Revenue, Peabody Retirement Community Project: | |||

| Series B, 1.0%, 12/1/2045* | 1,295,050 | 25,202 | |

| Series A, 6.05%, 12/1/2045 | 1,557,576 | 1,421,600 | |

| Valparaiso, IN, Exempt Facilities Revenue, Pratt Paper LLC Project, AMT, 7.0%, 1/1/2044, GTY: Pratt Industries (U.S.A.) | 6,220,000 | 7,710,187 | |

| Vigo County, IN, Hospital Authority Revenue, Union Hospital, Inc.: | |||

| 144A, 5.5%, 9/1/2027 | 1,000,000 | 1,028,870 | |

| 8.0%, 9/1/2041 | 4,000,000 | 4,792,440 | |

| 22,042,985 | |||

| Iowa 0.6% | |||

| Altoona, IA, Urban Renewal Tax Increment Revenue, Annual Appropriation: | |||

| 6.0%, 6/1/2034 | 1,000,000 | 1,074,970 | |

| 6.0%, 6/1/2039 | 2,000,000 | 2,143,440 | |

| Iowa, Finance Authority Retirement Community Revenue, Edgewater LLC Project, Prerefunded, 6.5%, 11/15/2027 | 5,000,000 | 5,418,650 | |

| 8,637,060 | |||

| Kansas 0.5% | |||

| Lenexa, KS, Health Care Facility Revenue, 5.5%, 5/15/2039 | 6,340,000 | 6,415,066 | |

| Lenexa, KS, Health Care Facility Revenue, Lakeview Village, Inc. Project, 7.25%, 5/15/2039 | 1,200,000 | 1,323,684 | |

| 7,738,750 | |||

| Kentucky 2.0% | |||

| Kentucky, Economic Development Finance Authority, Hospital Facilities Revenue, Owensboro Medical Health Systems, Series A, 6.5%, 3/1/2045 | 15,000,000 | 17,360,250 | |

| Kentucky, Economic Development Finance Authority, Louisville Arena Project Revenue, Series A-1, 6.0%, 12/1/2033, INS: AGC | 3,635,000 | 3,924,273 | |

| Kentucky, Public Transportation Infrastructure Authority Toll Revenue, 1st Tier-Downtown Crossing, Series A, 6.0%, 7/1/2053 | 7,195,000 | 8,502,332 | |

| Louisville & Jefferson County, KY, Metropolitan Government Health Systems Revenue, Norton Healthcare, Inc., 5.0%, 10/1/2030 | 1,000,000 | 1,011,210 | |

| 30,798,065 | |||

| Louisiana 2.0% | |||

| DeSoto Parish, LA, Environmental Improvement Revenue, International Paper Co. Project, Series A, AMT, 5.75%, 9/1/2031 | 5,000,000 | 5,201,050 | |

| Louisiana, Local Government Environmental Facilities & Community Development, Westlake Chemical Corp., Series A, 6.5%, 8/1/2029 | 6,055,000 | 7,187,164 | |

| Louisiana, Local Government Environmental Facilities, Community Development Authority Revenue, 6.75%, 11/1/2032 | 6,000,000 | 6,480,480 | |

| Louisiana, Public Facilities Authority Revenue, Ochsner Clinic Foundation Project, Prerefunded, 6.75%, 5/15/2041 | 2,500,000 | 3,158,775 | |

| Louisiana, Public Facilities Authority, Hospital Revenue, Lafayette General Medical Center, 5.5%, 11/1/2040 | 5,000,000 | 5,475,000 | |

| Louisiana, State Public Facilities Authority Revenue, Ochsner Clinic Foundation Project, 5.0%, 5/15/2047 | 1,000,000 | 1,162,950 | |

| Louisiana, Tobacco Settlement Financing Corp. Revenue, Series A, 5.25%, 5/15/2035 | 1,820,000 | 2,085,156 | |

| 30,750,575 | |||

| Maine 0.7% | |||

| Maine, Health & Higher Educational Facilities Authority Revenue, Maine General Medical Center, 6.75%, 7/1/2036 | 9,000,000 | 10,261,080 | |

| Maryland 1.0% | |||

| Anne Arundel County, MD, Special Obligation, National Business Park North Project, 6.1%, 7/1/2040 | 2,200,000 | 2,328,722 | |

| Maryland, State Health & Higher Educational Facilities Authority Revenue, Adventist Healthcare, Series A, 6.125%, 1/1/2036 | 3,250,000 | 3,820,473 | |

| Maryland, State Health & Higher Educational Facilities Authority Revenue, Doctors Community Hospital, Inc., 5.75%, 7/1/2038 | 6,250,000 | 6,957,875 | |

| Maryland, State Health & Higher Educational Facilities Authority Revenue, Mercy Medical Center, 6.25%, 7/1/2031 | 2,500,000 | 2,952,050 | |

| 16,059,120 | |||

| Massachusetts 2.2% | |||

| Massachusetts, State Development Finance Agency Revenue, Linden Ponds, Inc. Facility: | |||

| Series B, 11/15/2056* | 430,598 | 2,446 | |

| Series A-2, 5.5%, 11/15/2046 | 86,572 | 80,149 | |

| Series A-1, 6.25%, 11/15/2039 | 1,621,881 | 1,638,181 | |

| Massachusetts, State Development Finance Agency Revenue, South Shore Hospital, Series I, 5.0%, 7/1/2041 | 675,000 | 792,018 | |

| Massachusetts, State Development Finance Agency Revenue, Tufts Medical Center, Inc., Series I, 7.25%, 1/1/2032 | 2,250,000 | 2,731,253 | |

| Massachusetts, State Health & Educational Facilities Authority Revenue, Boston College, Series M2, 5.5%, 6/1/2035 | 8,600,000 | 12,240,294 | |

| Massachusetts, State Health & Educational Facilities Authority Revenue, Caregroup Healthcare System: | |||

| Series E-1, Prerefunded, 5.0%, 7/1/2028 | 1,500,000 | 1,628,760 | |

| Series E-1, Prerefunded, 5.125%, 7/1/2038 | 1,500,000 | 1,632,615 | |

| Massachusetts, State Health & Educational Facilities Authority Revenue, South Shore Hospital: | |||

| Series F, 5.625%, 7/1/2019 | 135,000 | 135,363 | |

| Series F, 5.75%, 7/1/2029 | 1,480,000 | 1,484,070 | |

| Massachusetts, State Health & Educational Facilities Authority Revenue, Suffolk University, Series A, 5.75%, 7/1/2039 | 7,145,000 | 7,966,103 | |

| Massachusetts, State Port Authority Special Facilities Revenue, Delta Air Lines, Inc. Project, Series A, AMT, 5.5%, 1/1/2018, INS: AMBAC | 4,000,000 | 4,015,880 | |

| 34,347,132 | |||

| Michigan 3.4% | |||

| Dearborn, MI, Economic Development Corp. Revenue, Limited Obligation, Henry Ford Village: | |||

| 7.0%, 11/15/2038 | 4,500,000 | 4,581,675 | |

| 7.125%, 11/15/2043 | 1,500,000 | 1,529,895 | |

| Detroit, MI, Water & Sewerage Department, Sewerage Disposal System Revenue, Series A, 5.25%, 7/1/2039 | 2,100,000 | 2,348,514 | |

| Detroit, MI, Water Supply Systems Revenue, Series A, 5.75%, 7/1/2037 | 7,590,000 | 8,605,390 | |

| Kalamazoo, MI, Economic Development Corp. Revenue, Limited Obligation, Heritage Community: | |||

| 5.375%, 5/15/2027 | 1,000,000 | 1,011,950 | |

| 5.5%, 5/15/2036 | 1,000,000 | 1,010,160 | |

| Kentwood, MI, Economic Development Corp., Limited Obligation, Holland Home, 5.625%, 11/15/2041 | 3,750,000 | 4,071,038 | |

| Michigan, State Finance Authority Revenue, Detroit Water & Sewer, Series C-3, 5.0%, 7/1/2033, INS: AGMC | 1,820,000 | 2,116,387 | |

| Michigan, State Finance Authority Revenue, Detroit Water & Sewer Department, Series C, 5.0%, 7/1/2035 | 910,000 | 1,052,961 | |

| Michigan, State Finance Authority Revenue, Trinity Health Corp.: | |||

| 5.0%, 12/1/2031 | 10,910,000 | 12,836,706 | |

| 5.0%, 12/1/2038 | 5,525,000 | 6,369,993 | |

| Michigan, State Hospital Finance Authority Revenue, Henry Ford Health Hospital, 5.75%, 11/15/2039 | 6,315,000 | 7,187,986 | |

| 52,722,655 | |||

| Mississippi 1.3% | |||

| Lowndes County, MS, Solid Waste Disposal & Pollution Control Revenue, Weyerhaeuser Co. Project, Series A, 6.8%, 4/1/2022 | 5,500,000 | 6,869,225 | |

| Warren County, MS, Gulf Opportunity Zone, International Paper Co.: | |||

| Series A, 5.375%, 12/1/2035 | 1,000,000 | 1,119,060 | |

| Series A, 5.5%, 9/1/2031 | 4,250,000 | 4,465,603 | |

| Series A, 5.8%, 5/1/2034, GTY: International Paper Co. | 4,000,000 | 4,651,000 | |

| Series A, 6.5%, 9/1/2032 | 2,620,000 | 2,923,920 | |

| 20,028,808 | |||

| Missouri 1.2% | |||

| Cass County, MO, Hospital Revenue, 5.5%, 5/1/2027 | 2,000,000 | 2,024,640 | |

| Kansas City, MO, Industrial Development Authority, Health Facilities Revenue, First Mortgage, Bishop Spencer, Series A, 6.5%, 1/1/2035 | 1,000,000 | 1,001,840 | |

| Kirkwood, MO, Industrial Development Authority, Retirement Community Revenue, Aberdeen Heights: | |||

| Series A, 8.25%, 5/15/2039 | 1,000,000 | 1,133,500 | |

| Series A, 8.25%, 5/15/2045 | 2,850,000 | 3,219,018 | |

| Missouri, State Health & Educational Facilities Authority Revenue, Medical Research, Lutheran Senior Services, Series A, 5.0%, 2/1/2046 | 665,000 | 755,234 | |

| Missouri, State Health & Educational Facilities Authority, Lutheran Senior Services, 6.0%, 2/1/2041 | 2,250,000 | 2,515,275 | |

| St. Louis County, MO, Industrial Development Authority, Senior Living Facilities, St. Andrews Resources for Seniors Obligated Group, Series A, 5.125%, 12/1/2045 | 3,635,000 | 3,834,961 | |

| St. Louis, MO, Lambert-St. Louis International Airport Revenue, Series A-1, 6.625%, 7/1/2034 | 4,085,000 | 4,680,838 | |

| 19,165,306 | |||

| Nebraska 0.4% | |||

| Douglas County, NE, Hospital Authority No. 002 Revenue, Health Facilities, Immanuel Obligation Group, 5.625%, 1/1/2040 | 1,500,000 | 1,655,610 | |

| Douglas County, NE, Hospital Authority No. 3, Health Facilities Revenue, State Methodist Health System, 5.0%, 11/1/2045 | 1,850,000 | 2,129,406 | |

| Lancaster County, NE, Hospital Authority No.1, Health Facilities Revenue, Immanuel Obligation Group, 5.625%, 1/1/2040 | 2,500,000 | 2,818,300 | |

| 6,603,316 | |||

| Nevada 0.1% | |||

| Sparks, NV, Local Improvement Districts, Limited Obligation District No. 3, 6.75%, 9/1/2027 | 1,395,000 | 1,471,418 | |

| New Hampshire 1.1% | |||

| New Hampshire, Health & Education Facilities Authority Revenue, Havenwood-Heritage Heights: | |||

| Series A, 5.35%, 1/1/2026 | 1,035,000 | 1,035,911 | |

| Series A, 5.4%, 1/1/2030 | 550,000 | 550,357 | |

| New Hampshire, Health & Education Facilities Authority Revenue, Wentworth-Douglas Hospital, Series A, 7.0%, 1/1/2038 | 5,325,000 | 6,347,560 | |

| New Hampshire, State Business Finance Authority Revenue, Elliot Hospital Obligation Group, Series A, 6.125%, 10/1/2039 | 5,000,000 | 5,633,250 | |

| New Hampshire, State Health & Education Facilities Authority Revenue, Rivermead Retirement Community: | |||

| Series A, 6.625%, 7/1/2031 | 700,000 | 798,931 | |

| Series A, 6.875%, 7/1/2041 | 2,825,000 | 3,244,258 | |

| 17,610,267 | |||

| New Jersey 3.4% | |||

| New Jersey, Health Care Facilities Financing Authority Revenue, St. Joseph's Health Care System, 6.625%, 7/1/2038 | 5,785,000 | 6,338,740 | |

| New Jersey, State Economic Development Authority Revenue, 5.0%, 6/15/2028 | 450,000 | 492,412 | |

| New Jersey, State Economic Development Authority, Special Facilities Revenue, Continental Airlines, Inc. Project, Series B, AMT, 5.625%, 11/15/2030 | 2,500,000 | 2,880,950 | |

| New Jersey, State Health Care Facilities Financing Authority Revenue, Saint Barnabas Health, Series A, 5.625%, 7/1/2032 | 3,500,000 | 4,127,900 | |

| New Jersey, State Health Care Facilities Financing Authority Revenue, University Hospital, Series A, 5.0%, 7/1/2046, INS: AGMC | 1,820,000 | 2,097,332 | |

| New Jersey, Tobacco Settlement Financing Corp.: | |||

| Series 1A, 4.75%, 6/1/2034 | 16,240,000 | 15,765,630 | |

| Series 1-A, 5.0%, 6/1/2029 | 15,965,000 | 16,127,683 | |

| Series 1A, 5.0%, 6/1/2041 | 5,000,000 | 4,869,150 | |

| 52,699,797 | |||

| New Mexico 0.5% | |||

| Farmington, NM, Pollution Control Revenue, Public Service Co. of New Mexico, Series C, 5.9%, 6/1/2040 | 7,500,000 | 8,533,875 | |

| New York 7.3% | |||

| Albany, NY, Industrial Development Agency, Civic Facility Revenue, St. Peter's Hospital Project, Series A, Prerefunded, 5.75%, 11/15/2022 | 1,500,000 | 1,609,965 | |

| Hudson, NY, Yards Infrastructure Corp. Revenue: | |||

| Series A, 5.25%, 2/15/2047 | 5,000,000 | 5,721,350 | |

| Series A, 5.75%, 2/15/2047 | 7,000,000 | 8,235,080 | |

| New York, General Obligation, Series A-4, 0.4%**, 8/1/2038, LOC: Bank of Tokyo-Mitsubishi UFJ | 1,000,000 | 1,000,000 | |

| New York, Metropolitan Transportation Authority, Dedicated Tax Fund, Green Bonds, Series B-1, 5.0%, 11/15/2036 | 10,000,000 | 12,308,300 | |

| New York, State Dormitory Authority Revenues, Non-State Supported Debt, Orange Regional Medical Center, 5.0%, 12/1/2045 | 1,000,000 | 1,095,540 | |

| New York, State Dormitory Authority Revenues, NYU Hospital Center, Series B, Prerefunded, 5.25%, 7/1/2024 | 660,000 | 686,677 | |

| New York, State Dormitory Authority Revenues, Orange Regional Medical Center, 6.125%, 12/1/2029 | 2,000,000 | 2,185,340 | |

| New York, State Housing Finance Agency Revenue, 205 E 92nd Street Housing, Series A, 0.4%**, 11/1/2047, LOC: Wells Fargo Bank NA | 1,500,000 | 1,500,000 | |

| New York, State Liberty Development Corp. Revenue, World Trade Center Project, Class 1-3, 5.0%, 11/15/2044 | 10,000,000 | 11,268,900 | |

| New York, State Thruway Authority, General Revenue, Junior Indebtedness Obligation, Junior Lien, Series A, 5.0%, 1/1/2051 | 2,250,000 | 2,630,497 | |

| New York, State Transportation Development Corp., Special Facilities Revenue, Laguardia Gateway Partners LLC, Series A, AMT, 5.0%, 7/1/2046 (a) | 3,500,000 | 3,942,855 | |

| New York & New Jersey Port Authority, AMT, 5.0%, 10/1/2035 | 6,825,000 | 8,238,799 | |

| New York & New Jersey Port Authority, Special Obligation Revenue, JFK International Air Terminal LLC, 6.0%, 12/1/2042 | 5,795,000 | 6,806,923 | |

| New York City, NY, Housing Development Corp., 90 Washington Street, Series A, 0.41%**, 2/15/2035, LIQ: Fannie Mae | 1,800,000 | 1,800,000 | |

| New York City, NY, Industrial Development Agency, Special Facility Revenue, American Airlines, JFK International Airport, AMT, 8.0%, 8/1/2028, GTY: American Airlines Group | 6,100,000 | 6,235,481 | |

| New York City, NY, Municipal Water Finance Authority, Water & Sewer Systems Revenue: | |||

| Series AA-1, 0.36%**, 6/15/2046, SPA: PNC Bank NA | 2,000,000 | 2,000,000 | |

| Series FF, 5.0%, 6/15/2039 | 7,500,000 | 8,995,050 | |

| Series EE, 5.0%, 6/15/2047 | 11,000,000 | 12,958,990 | |

| New York City, NY, Transitional Finance Authority Revenue, Future Tax Secured, Series B-1, 5.0%, 8/1/2039 | 11,595,000 | 13,875,273 | |

| Orange County, NY, Senior Care Revenue, Industrial Development Agency, The Glen Arden Project, 5.7%, 1/1/2028 | 1,250,000 | 1,130,038 | |

| 114,225,058 | |||

| North Carolina 0.5% | |||

| Charlotte, NC, Airport Revenue, Series A, 5.0%, 7/1/2039 | 1,450,000 | 1,637,369 | |

| North Carolina, Medical Care Commission, Retirement Facilities Revenue, First Mortgage, Southminster Project, Series A, 5.625%, 10/1/2027 | 2,500,000 | 2,569,150 | |

| North Carolina, Medical Care Commission, Retirement Facilities Revenue, First Mortgage-Aldersgate, 5.0%, 7/1/2045 | 3,320,000 | 3,572,254 | |

| 7,778,773 | |||

| North Dakota 0.2% | |||

| Burleigh County, ND, Health Care Revenue, St. Alexius Medical Center Project, Series A, Prerefunded, 5.0%, 7/1/2035 | 1,200,000 | 1,419,984 | |

| Grand Forks, ND, Health Care System Revenue, Altru Health System, 5.0%, 12/1/2032 | 2,000,000 | 2,225,540 | |

| 3,645,524 | |||

| Ohio 0.8% | |||

| Cleveland, OH, Airport Systems Revenue, Series A, 5.0%, 1/1/2030 | 1,000,000 | 1,135,080 | |

| Hamilton County, OH, Health Care Facilities Revenue, Christ Hospital Project, 5.5%, 6/1/2042 | 3,100,000 | 3,563,946 | |

| Hamilton County, OH, Health Care Revenue, Life Enriching Communities Project: | |||

| 6.125%, 1/1/2031 | 1,870,000 | 2,151,229 | |

| 6.625%, 1/1/2046 | 2,500,000 | 2,899,225 | |

| Ohio, State Higher Educational Facility Commission Revenue, Summa Health Systems Project, Series 2010, 5.75%, 11/15/2040 | 3,000,000 | 3,370,410 | |

| 13,119,890 | |||

| Oklahoma 0.5% | |||

| Tulsa County, OK, Industrial Authority, Senior Living Community Revenue, Montereau, Inc. Project, Series A, 7.25%, 11/1/2045 | 6,500,000 | 7,139,925 | |

| Pennsylvania 5.0% | |||

| Centre County, PA, Hospital Authority, Mount Nittany Medical Center, Series A, 5.0%, 11/15/2041 | 1,000,000 | 1,171,220 | |

| Cumberland County, PA, Municipal Authority Revenue, Asbury Obligation Group, 6.125%, 1/1/2045 | 4,350,000 | 4,663,809 | |

| Lancaster County, PA, Hospital Authority Revenue, Brethren Village Project, Series A, 6.375%, 7/1/2030 | 1,000,000 | 1,027,950 | |

| Lancaster County, PA, Hospital Authority Revenue, University of Pennsylvania Health System Obligated Group, 5.0%, 8/15/2042 | 900,000 | 1,065,888 | |

| Northampton County, PA, Hospital Authority Revenue, St. Luke's Hospital Project: | |||

| Series A, 5.375%, 8/15/2028 | 3,500,000 | 3,786,335 | |

| Series A, 5.5%, 8/15/2035 | 6,500,000 | 7,024,940 | |

| Pennsylvania, Commonwealth Financing Authority, Series A, 5.0%, 6/1/2035 | 3,125,000 | 3,606,781 | |

| Pennsylvania, Economic Development Finance Authority, U.S. Airways Group, Series B, 8.0%, 5/1/2029, GTY: American Airlines, Inc. | 985,000 | 1,155,927 | |

| Pennsylvania, Economic Development Financing Authority, Sewer Sludge Disposal Revenue, Philadelphia Biosolids Facility, 6.25%, 1/1/2032 | 1,500,000 | 1,659,570 | |

| Pennsylvania, State Economic Development Financing Authority Revenue, Bridges Finco LP, AMT, 5.0%, 12/31/2038 | 4,785,000 | 5,460,116 | |

| Pennsylvania, State Economic Development Financing Authority, Exempt Facilities Revenue, PPL Energy Supply, Series A, 6.4%, 12/1/2038 | 1,115,000 | 1,098,810 | |

| Pennsylvania, State Turnpike Commission Revenue: | |||

| Series A-1, 5.0%, 12/1/2041 | 4,355,000 | 5,000,498 | |

| Series C, 5.0%, 12/1/2043 | 7,000,000 | 8,096,760 | |

| Series C, 5.0%, 12/1/2044 | 1,615,000 | 1,884,770 | |

| Series A, Prerefunded, 6.5%, 12/1/2036 | 6,385,000 | 7,890,072 | |

| Pennsylvania, State Turnpike Commission Revenue, Turnpike Subordinate Revenue Refunding Bonds, 5.0%, 6/1/2036 (a) | 10,000,000 | 11,695,500 | |

| Philadelphia, PA, Airport Revenue, Series A, 5.0%, 6/15/2035 | 7,085,000 | 7,975,018 | |

| Philadelphia, PA, Gas Works Revenue, 5.25%, 8/1/2040 | 3,000,000 | 3,375,780 | |

| 77,639,744 | |||

| Puerto Rico 0.9% | |||

| Commonwealth of Puerto Rico, Public Improvement, Series B, 6.5%, 7/1/2037 | 5,000,000 | 3,095,600 | |

| Puerto Rico, Sales Tax Financing Corp., Sales Tax Revenue: | |||

| Series C, 5.25%, 8/1/2041 | 3,065,000 | 1,228,881 | |

| Series A, 5.5%, 8/1/2042 | 7,650,000 | 3,066,579 | |

| Series A, 5.75%, 8/1/2037 | 2,130,000 | 859,285 | |

| Series A, 6.0%, 8/1/2042 | 4,570,000 | 1,854,597 | |

| Series A, 6.375%, 8/1/2039 | 2,295,000 | 939,871 | |

| Puerto Rico, Sales Tax Financing Corp., Sales Tax Revenue, Convertible Capital Appreciation, Series A, Step-up Coupon, 0% to 8/1/2016, 6.75% to 8/1/2032 | 10,000,000 | 3,819,900 | |

| 14,864,713 | |||

| Rhode Island 0.2% | |||

| Rhode Island, Tobacco Settlement Financing Corp., Series A, 5.0%, 6/1/2040 | 2,345,000 | 2,595,469 | |

| South Carolina 2.7% | |||

| Greenwood County, SC, Hospital Revenue, Self Regional Healthcare, Series B, 5.0%, 10/1/2031 | 1,000,000 | 1,134,010 | |

| Hardeeville, SC, Assessment Revenue, Anderson Tract Municipal Improvement District, Series A, 7.75%, 11/1/2039 | 4,469,000 | 4,640,207 | |

| South Carolina, Jobs Economic Development Authority, Hospital Facilities Revenue, Palmetto Health Alliance, 5.75%, 8/1/2039 | 3,595,000 | 3,914,667 | |

| South Carolina, State Public Service Authority Revenue: | |||

| Series C, 5.0%, 12/1/2046 | 7,500,000 | 8,660,700 | |

| Series E, 5.25%, 12/1/2055 | 10,360,000 | 12,274,425 | |

| South Carolina, State Public Service Authority Revenue, Santee Cooper, Series A, 5.75%, 12/1/2043 | 8,890,000 | 10,991,774 | |

| 41,615,783 | |||

| South Dakota 0.5% | |||

| South Dakota, State Health & Educational Facilities Authority Revenue, Avera Health: | |||

| Series B, 5.25%, 7/1/2038 | 3,000,000 | 3,193,500 | |

| Series B, 5.5%, 7/1/2035 | 5,000,000 | 5,400,050 | |

| 8,593,550 | |||

| Tennessee 1.0% | |||

| Jackson, TN, Hospital Revenue, Jackson-Madison Project: | |||

| 5.625%, 4/1/2038 | 810,000 | 871,868 | |

| Prerefunded, 5.625%, 4/1/2038 | 2,190,000 | 2,382,545 | |

| Johnson City, TN, Health & Educational Facilities, Board Hospital Revenue, Mountain States Health Alliance, 6.5%, 7/1/2038 | 3,570,000 | 4,136,773 | |

| Tennessee, Energy Acquisition Corp., Gas Revenue, Series C, 5.0%, 2/1/2027, GTY: The Goldman Sachs Group, Inc. | 6,435,000 | 7,758,808 | |

| 15,149,994 | |||

| Texas 15.8% | |||

| Bexar County, TX, Health Facilities Development Corp. Revenue, Army Retirement Residence Project, 6.2%, 7/1/2045 | 6,000,000 | 6,825,300 | |

| Brazos River, TX, Harbor Navigation District, Brazoria County Environmental Health, Dow Chemical Co. Project: | |||

| Series B-2, 4.95%, 5/15/2033 | 4,000,000 | 4,210,840 | |

| Series A-3, AMT, 5.125%, 5/15/2033 | 9,000,000 | 9,444,960 | |

| Brazos River, TX, Pollution Control Authority Revenue, Series D-1, 144A, AMT, 8.25%, 5/1/2033* | 7,000,000 | 122,430 | |

| Cass County, TX, Industrial Development Corp., Environmental Improvement Revenue, International Paper Co. Projects, Series A, 9.25%, 3/1/2024 | 2,000,000 | 2,422,620 | |

| Central Texas, Regional Mobility Authority Revenue, 5.0%, 1/1/2046 (a) | 2,665,000 | 3,106,004 | |

| Central Texas, Regional Mobility Authority Revenue, Capital Appreciation: | |||

| Zero Coupon, 1/1/2030 | 5,000,000 | 3,073,400 | |

| Zero Coupon, 1/1/2032 | 3,500,000 | 2,004,975 | |

| Central Texas, Regional Mobility Authority Revenue, Senior Lien: | |||

| Series A, 5.0%, 1/1/2040 | 1,385,000 | 1,612,154 | |

| Series A, 5.0%, 1/1/2043 | 1,000,000 | 1,117,380 | |

| Prerefunded, 6.0%, 1/1/2041 | 5,455,000 | 6,617,897 | |

| Harris County, TX, Cultural Education Facilities Finance Corp. Revenue, 1st Mortgage-Brazos Presbyterian Homes, Inc. Project: | |||

| Series B, 7.0%, 1/1/2043 | 3,000,000 | 3,586,410 | |

| Series B, 7.0%, 1/1/2048 | 4,000,000 | 4,751,480 | |

| Houston, TX, Airport System Revenue, United Airlines, Inc., Terminal E Project, AMT, 4.75%, 7/1/2024 | 3,385,000 | 3,846,342 | |

| Houston, TX, Airport Systems Revenue, Special Facilities Continental Airlines, Inc. Terminal Projects, AMT, 6.625%, 7/15/2038 | 2,000,000 | 2,326,300 | |

| La Vernia, TX, Higher Education Finance Corp. Revenue, Lifeschools of Dallas: | |||

| Series A, Prerefunded, 7.25%, 8/15/2031 | 1,275,000 | 1,522,299 | |

| Series A, Prerefunded, 7.5%, 8/15/2041 | 1,785,000 | 2,145,231 | |

| Lewisville, TX, Combination Contract Revenue, 6.75%, 10/1/2032 | 13,520,000 | 14,283,339 | |

| Matagorda County, TX, Navigation District No. 1, Pollution Control Revenue, AEP Texas Central Co. Project, Series A, 4.4%, 5/1/2030, INS: AMBAC | 11,000,000 | 12,629,650 | |

| Matagorda County, TX, Navigation District No. 1, Pollution Control Revenue, Central Power & Light Co. Project, Series A, 6.3%, 11/1/2029 | 3,000,000 | 3,407,820 | |

| Mission, TX, Economic Development Corp. Revenue, Senior Lien, Natgasoline Project, Series B, AMT, 144A, 5.75%, 10/1/2031 | 750,000 | 792,758 | |

| North Texas, Tollway Authority Revenue: | |||

| Series A, 5.0%, 1/1/2034 | 4,285,000 | 5,053,429 | |

| Series A, 5.0%, 1/1/2039 (a) | 11,770,000 | 14,020,189 | |

| Series B, 5.0%, 1/1/2045 | 3,335,000 | 3,860,963 | |

| First Tier, Series A, 5.625%, 1/1/2033 | 545,000 | 581,461 | |

| First Tier, Series A, Prerefunded, 5.625%, 1/1/2033 | 455,000 | 489,357 | |

| First Tier, 6.0%, 1/1/2043 | 5,000,000 | 5,907,700 | |

| First Tier, Series A, 6.25%, 1/1/2039 | 9,525,000 | 10,692,955 | |

| Red River, TX, Health Facilities Development Corp., Retirement Facilities Revenue, MRC Crossings Project, Series A, 8.0%, 11/15/2049 | 1,715,000 | 2,062,253 | |

| San Antonio, TX, Convention Center Hotel Finance Corp., Contract Revenue, Empowerment Zone, Series A, AMT, 5.0%, 7/15/2039, INS: AMBAC | 8,000,000 | 8,028,400 | |

| San Antonio, TX, Electric & Gas Revenue, 5.0%, 2/1/2024 | 15,000,000 | 16,009,050 | |

| Tarrant County, TX, Cultural Education Facilities Finance Corp. Revenue, Trinity Terrace Project, The Cumberland Rest, Inc., Series A-1, 5.0%, 10/1/2044 | 1,575,000 | 1,768,000 | |

| Tarrant County, TX, Cultural Education Facilities Finance Corp., Hospital Revenue, Baylor Health Care System Project, Series C, 0.41%**, 11/15/2050, LOC: Northern Trust Co. | 1,270,000 | 1,270,000 | |

| Tarrant County, TX, Cultural Education Facilities Finance Corp., Retirement Facility, Mirador Project: | |||

| Series A, 8.125%, 11/15/2039 | 1,000,000 | 844,980 | |

| Series A, 8.25%, 11/15/2044 | 3,430,000 | 2,898,556 | |

| Texas, Dallas/Fort Worth International Airport Revenue: | |||

| Series D, 5.0%, 11/1/2035 | 2,715,000 | 3,107,453 | |

| Series A, 5.25%, 11/1/2038 | 15,000,000 | 17,244,600 | |

| Texas, Love Field Airport Modernization Corp., Special Facilities Revenue, Southwest Airlines Co. Project, 5.25%, 11/1/2040 | 7,445,000 | 8,346,292 | |

| Texas, Municipal Gas Acquisition & Supply Corp. I, Gas Supply Revenue, Series D, 6.25%, 12/15/2026, GTY: Merrill Lynch & Co., Inc. | 16,875,000 | 21,224,194 | |

| Texas, SA Energy Acquisition Public Facility Corp., Gas Supply Revenue, 5.5%, 8/1/2020, GTY: The Goldman Sachs Group, Inc. | 10,000,000 | 11,662,500 | |

| Texas, State Municipal Gas Acquisition & Supply Corp. III Gas Supply Revenue, 5.0%, 12/15/2030, GTY: Macquarie Group Ltd. | 1,670,000 | 1,889,187 | |

| Texas, State Private Activity Bond, Surface Transportation Corp. Revenue, Senior Lien, North Tarrant Express Mobility Partners Segments LLC, AMT, 6.75%, 6/30/2043 | 2,220,000 | 2,757,062 | |

| Texas, State Transportation Commission, Turnpike Systems Revenue, Series C, 5.0%, 8/15/2034 | 8,235,000 | 9,646,808 | |

| Texas, Uptown Development Authority, Tax Increment Contract Revenue, Infrastructure Improvement Facilities, 5.5%, 9/1/2029 | 1,000,000 | 1,102,700 | |

| Travis County, TX, Health Facilities Development Corp. Revenue, Westminster Manor Health: | |||

| 7.0%, 11/1/2030 | 1,530,000 | 1,768,328 | |

| 7.125%, 11/1/2040 | 3,580,000 | 4,109,196 | |

| 246,195,202 | |||

| Virginia 0.9% | |||

| Stafford County, VA, Economic Development Authority, Hospital Facilities Revenue, Mary Washington Healthcare, 5.0%, 6/15/2036 | 600,000 | 709,914 | |

| Virginia, Marquis Community Development Authority Revenue: | |||

| Series C, Zero Coupon, 9/1/2041 | 7,906,000 | 1,084,229 | |

| Series B, 5.625%, 9/1/2041 | 5,332,000 | 4,318,973 | |

| Virginia, Marquis Community Development Authority Revenue, Convertible Cabs, Step-up Coupon, 0% to 9/1/2021, 7.5% to 9/1/2045 | 1,640,000 | 1,073,659 | |

| Virginia, Mosaic District Community Development Authority Revenue, Series A, 6.875%, 3/1/2036 | 2,000,000 | 2,307,140 | |

| Virginia, Peninsula Ports Authority, Residential Care Facility Revenue, Virginia Baptist Homes, Series C, 5.4%, 12/1/2033 | 2,600,000 | 2,589,522 | |

| Virginia, State Small Business Financing Authority Revenue, Elizabeth River Crossings LLC Project, AMT, 6.0%, 1/1/2037 | 2,000,000 | 2,380,280 | |

| 14,463,717 | |||

| Washington 2.1% | |||

| Klickitat County, WA, Public Hospital District No. 2 Revenue, Skyline Hospital, 6.5%, 12/1/2038 | 3,205,000 | 3,235,864 | |

| Washington, Port of Seattle, Industrial Development Corp., Special Facilities- Delta Airlines, AMT, 5.0%, 4/1/2030 | 2,000,000 | 2,154,380 | |

| Washington, State Health Care Facilities Authority Revenue, Series C, 5.375%, 8/15/2028, INS: AGC | 2,970,000 | 3,084,315 | |

| Washington, State Health Care Facilities Authority Revenue, Virginia Mason Medical Center, Series A, 6.125%, 8/15/2037 | 16,000,000 | 16,893,280 | |

| Washington, State Housing Finance Commission, Rockwood Retirement Communities Project, Series A, 7.375%, 1/1/2044 | 6,000,000 | 7,007,340 | |

| 32,375,179 | |||

| West Virginia 0.9% | |||

| West Virginia, State Hospital Finance Authority Revenue, Charleston Medical Center, Series A, 5.625%, 9/1/2032 | 3,080,000 | 3,421,295 | |

| West Virginia, State Hospital Finance Authority Revenue, Thomas Health Systems: | |||

| 6.5%, 10/1/2028 | 7,000,000 | 7,406,490 | |

| 6.5%, 10/1/2038 | 3,000,000 | 3,166,650 | |

| 13,994,435 | |||

| Wisconsin 1.0% | |||

| Wisconsin, Public Finance Authority, Apartment Facilities Revenue, Senior Obligation Group, AMT, 5.0%, 7/1/2042 | 3,500,000 | 3,737,860 | |

| Wisconsin, State Health & Educational Facilities Authority Revenue, Aurora Health Care, Inc., Series A, 5.625%, 4/15/2039 | 8,160,000 | 9,162,700 | |

| Wisconsin, State Health & Educational Facilities Authority Revenue, St. John's Communities, Inc.: | |||

| Series B, 5.0%, 9/15/2045 | 1,000,000 | 1,088,970 | |

| Series A, Prerefunded, 7.625%, 9/15/2039 | 1,000,000 | 1,208,160 | |

| 15,197,690 | |||

| Other Territories 0.1% | |||

| Non-Profit Preferred Funding Trust I, Series A1, 144A, 4.22%, 9/15/2037 | 904,701 | 916,733 | |

| Total Municipal Bonds and Notes (Cost $1,372,310,223) | 1,509,494,924 | ||

| Underlying Municipal Bonds of Inverse Floaters (c) 10.0% | |||

| Hawaii 0.7% | |||

| Hawaii, State General Obligation, Series 2015-DK, Prerefunded , 5.0%, 5/1/2027 (d) | 8,340,000 | 9,011,287 | |

| Hawaii, State General Obligation, Series DK, Prerefunded, 5.0%, 5/1/2027 (d) | 1,465,000 | 1,582,918 | |

| Hawaii, State General Obligation, Series DK, 5.0%, 5/1/2027 (d) | 195,000 | 210,695 | |

| Trust: Hawaii, State General Obligation, Series 2867, 144A, 17.06%, 11/1/2017, Leverage Factor at purchase date: 4 to 1 | |||

| 10,804,900 | |||

| Louisiana 0.7% | |||

| Louisiana, State Gas & Fuels Tax Revenue, Series B, 5.0%, 5/1/2033 (d) | 3,026,513 | 3,455,357 | |

| Louisiana, State Gas & Fuels Tax Revenue, Series B, 5.0%, 5/1/2034 (d) | 3,304,152 | 3,772,335 | |

| Louisiana, State Gas & Fuels Tax Revenue, Series B, 5.0%, 5/1/2035 (d) | 3,666,834 | 4,186,407 | |

| Trust: Louisiana, State Gas & Fuels Tax Revenue, Series 3806, 144A, 9.048%, 5/1/2018, Leverage Factor at purchase date: 2 to 1 | |||

| 11,414,099 | |||

| Massachusetts 1.2% | |||

| Massachusetts, State School Building Authority, Sales Tax Revenue, Series C, 5.0%, 8/15/2037 (d) | 15,000,000 | 18,189,750 | |

| Trust: Massachusetts, Tender Option Bond Trust Receipts/Certificates of Various States, Series 2016-XM0239, 144A, 16.985%, 8/15/2037, Leverage Factor at purchase date: 4 to 1 | |||

| Michigan 0.8% | |||

| Michigan, State Building Authority Revenue, Facilities Program, Series I, 5.0%, 4/15/2034 (d) | 10,000,000 | 12,049,182 | |

| Trust: State Building Authority Revenue, Series 2015-XM0123, 144A, 13.002%, 10/15/2023, Leverage Factor at purchase date: 3 to 1 | |||

| New York 2.4% | |||

| New York, State Dormitory Authority Revenues, Personal Income Tax Revenue, Series A, 5.0%, 3/15/2023 (d) | 5,095,207 | 5,270,274 | |

| Trust: New York, State Dormitory Authority Revenues, Secondary Issues, Series 1955-2, 144A, 17.135%, 9/15/2016, Leverage Factor at purchase date: 4 to 1 | |||

| New York, State Dormitory Authority, Personal Income Tax Revenue, Series F, 5.0%, 2/15/2035 (d) | 10,000,000 | 11,311,900 | |

| Trust: New York, State Dormitory Authority Revenues, Series 4688, 144A, 9.14%, 3/15/2024, Leverage Factor at purchase date: 2 to 1 | |||

| New York, State Environmental Facilities Corp., Clean Drinking Water, Series A, 5.0%, 6/15/2025 (d) | 4,000,000 | 4,342,067 | |

| New York, State Environmental Facilities Corp., Clean Drinking Water, Series A, 5.0%, 6/15/2026 (d) | 3,000,000 | 3,256,551 | |

| New York, State Environmental Facilities Corp., Clean Drinking Water, Series A, 5.0%, 6/15/2027 (d) | 3,000,000 | 3,256,550 | |

| Trust: New York, State Environmental Facilities Corp., Clean Drinking Water, Series 2870, 144A, 15.598%, 6/15/2017, Leverage Factor at purchase date: 3.6 to 1 | |||

| New York City, NY, Transitional Finance Authority Revenue, Series C-1, 5.0%, 11/1/2027 (d) | 3,185,000 | 3,375,743 | |

| New York City, NY, Transitional Finance Authority Revenue, Series C-1, Prerefunded, 5.0%, 11/1/2027 (d) | 6,815,000 | 7,223,137 | |

| Trust: New York City, NY, Transitional Finance Authority Revenue, Series 2072, 144A, 10.88%, 11/1/2027, Leverage Factor at purchase date: 2.5 to 1 | |||

| 38,036,222 | |||

| Ohio 0.8% | |||

| Ohio, State Higher Educational Facilities Commission Revenue, Cleveland Clinic Health, Series A, 5.125%, 1/1/2028 (d) | 4,522,767 | 4,849,595 | |

| Ohio, State Higher Educational Facilities Commission Revenue, Cleveland Clinic Health, Series A, 5.25%, 1/1/2033 (d) | 7,712,913 | 8,270,272 | |

| Trust: Ohio, State Higher Educational Revenue, Series 3139, 144A, 13.9%, 1/1/2028, Leverage Factor at purchase date: 3 to 1 | |||

| 13,119,867 | |||

| Tennessee 1.0% | |||

| Nashville & Davidson County, TN, Metropolitan Government, 5.0%, 1/1/2024 (d) | 14,996,415 | 15,996,353 | |

| Trust: Nashville & Davidson County, TN, Metropolitan Government, Series 2631-1, 144A, 17.146%, 7/1/2017, Leverage Factor at purchase date: 4 to 1 | |||

| Texas 1.2% | |||

| Harris County, TX, Flood Control District, Series A, 5.0%, 10/1/2034 (d) | 5,500,000 | 6,300,855 | |

| Trust: Harris County, TX, Flood Control District, Series 4692, 144A, 9.24%, 10/11/2018, Leverage Factor at purchase date: 2 to 1 | |||

| Texas, State Transportation Commission Revenue, 5.0%, 4/1/2026 (d) | 12,500,000 | 12,958,000 | |

| Trust: Texas, State Transportation Commission Revenue, Series 2563, 144A, 21.08%, 10/1/2016, Leverage Factor at purchase date: 5 to 1 | |||

| 19,258,855 | |||

| Washington 1.2% | |||

| Washington, State General Obligation, Series A-1, 5.0%, 8/1/2037 (d) | 15,000,000 | 18,122,850 | |

| Trust: State General Obligation, Series XM0127, 144A, 16.985%, 8/1/2023, Leverage Factor at purchase date: 4 to 1 | |||

| Total Underlying Municipal Bonds of Inverse Floaters (Cost $148,299,029) | 156,992,078 | ||

| % of Net Assets | Value ($) | |

| Total Investment Portfolio (Cost $1,520,609,252)† | 106.7 | 1,666,487,002 |

| Floating Rate Notes (c) | (6.1) | (95,759,629) |

| Other Assets and Liabilities, Net | (0.6) | (9,517,889) |

| Net Assets | 100.0 | 1,561,209,484 |

The following table represents bonds that are in default:

| Security | Coupon | Maturity Date | Principal Amount ($) | Cost ($) | Value ($) |

| Brazos River, TX, Pollution Control Authority Revenue, Series D-1, 144A, AMT* | 8.25% | 5/1/2033 | 7,000,000 | 7,000,000 | 122,430 |

| Connecticut, Mashantucket Western Pequot Tribe Bond* | 6.05% | 7/1/2031 | 16,664,460 | 11,711,381 | 999,868 |

| 18,711,381 | 1,122,298 |

* Non-income producing security.

** Variable rate demand notes are securities whose interest rates are reset periodically at market levels. These securities are often payable on demand and are shown at their current rates as of May 31, 2016.

† The cost for federal income tax purposes was $1,419,712,364. At May 31, 2016, net unrealized appreciation for all securities based on tax cost was $151,015,009. This consisted of aggregate gross unrealized appreciation for all securities in which there was an excess of value over tax cost of $187,820,207 and aggregate gross unrealized depreciation for all securities in which there was an excess of tax cost over value of $36,805,198.

(a) When-issued security.

(b) At May 31, 2016, this security has been pledged, in whole or in part, as collateral for tender option bond trust.

(c) Securities represent the underlying municipal obligations of inverse floating rate obligations held by the Fund. The Floating Rate Notes represent leverage to the Fund and is the amount owed to the floating rate note holders.

(d) Security forms part of the below inverse floater. The Fund accounts for these inverse floaters as a form of secured borrowing, by reflecting the value of the underlying bond in the investments of the Fund and the amount owed to the floating rate note holder as a liability.

144A: Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers.

AGC: Assured Guaranty Corp.

AGMC: Assured Guaranty Municipal Corp.

AMBAC: Ambac Financial Group, Inc.

AMT: Subject to alternative minimum tax.

FGIC: Financial Guaranty Insurance Co.

GTY: Guaranty Agreement

LIQ: Liquidity Facility

LOC: Letter of Credit

INS: Insured

NATL: National Public Finance Guarantee Corp.

PIK: Denotes that all or a portion of the income is paid in-kind in the form of additional principal.

Prerefunded: Bonds which are prerefunded are collateralized usually by U.S. Treasury securities, which are held in escrow and used to pay principal and interest on tax-exempt issues and to retire the bonds in full at the earliest refunding date.

SPA: Standby Bond Purchase Agreement

Fair Value Measurements

Various inputs are used in determining the value of the Fund's investments. These inputs are summarized in three broad levels. Level 1 includes quoted prices in active markets for identical securities. Level 2 includes other significant observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds and credit risk). Level 3 includes significant unobservable inputs (including the Fund's own assumptions in determining the fair value of investments). The level assigned to the securities valuations may not be an indication of the risk or liquidity associated with investing in those securities.

The following is a summary of the inputs used as of May 31, 2016 in valuing the Fund's investments. For information on the Fund's policy regarding the valuation of investments, please refer to the Security Valuation section of Note A in the accompanying Notes to Financial Statements.

| Assets | Level 1 | Level 2 | Level 3 | Total |

| Municipal Investments (e) | $ — | $ 1,666,487,002 | $ — | $ 1,666,487,002 |

| Total | $ — | $ 1,666,487,002 | $ — | $ 1,666,487,002 |

There have been no transfers between fair value measurement levels during the period ended May 31, 2016.

(e) See Investment Portfolio for additional detailed categorizations.

The accompanying notes are an integral part of the financial statements.

Statement of Assets and Liabilities

| as of May 31, 2016 | |

| Assets | |

| Investments in non-affiliated securities, at value (cost $1,520,609,252) | $ 1,666,487,002 |

| Cash | 2,001,876 |

| Receivable for Fund shares sold | 5,746,257 |

| Interest receivable | 22,637,365 |

| Other assets | 47,168 |

| Total assets | 1,696,919,668 |

| Liabilities | |

| Payable for investments purchased | 1,000,313 |

| Payable for investments purchased — when-issued security | 34,887,998 |

| Payable for Fund shares redeemed | 962,203 |

| Payable for floating rate notes issued | 95,759,629 |

| Distributions payable | 1,246,366 |

| Accrued management fee | 443,289 |

| Accrued Trustees' fees | 28,917 |

| Other accrued expenses and payables | 1,381,469 |

| Total liabilities | 135,710,184 |

| Net assets, at value | $ 1,561,209,484 |

| Net Assets Consist of | |

| Undistributed net investment income | 2,697,874 |

| Net unrealized appreciation (depreciation) on investments | 145,877,750 |

| Accumulated net realized gain (loss) | (122,111,945) |

| Paid-in capital | 1,534,745,805 |

| Net assets, at value | $ 1,561,209,484 |

The accompanying notes are an integral part of the financial statements.

| Statement of Assets and Liabilities as of May 31, 2016 (continued) | |

| Net Asset Value | |

Class A Net Asset Value and redemption price per share ($361,252,465 ÷ 28,703,029 outstanding shares of beneficial interest, $.01 par value, unlimited number of shares authorized) | $ 12.59 |

| Maximum offering price per share (100 ÷ 97.25 of $12.59) | $ 12.95 |

Class C Net Asset Value offering and redemption price (subject to contingent deferred sales charge) per share ($138,024,845 ÷ 10,960,081 outstanding shares of beneficial interest, $.01 par value, unlimited number of shares authorized) | $ 12.59 |

Class S Net Asset Value offering and redemption price per share ($873,427,362 ÷ 69,334,984 outstanding shares of beneficial interest, $.01 par value, unlimited number of shares authorized) | $ 12.60 |

Institutional Class Net Asset Value offering and redemption price per share ($188,504,812 ÷ 14,959,340 outstanding shares of beneficial interest, $.01 par value, unlimited number of shares authorized) | $ 12.60 |

The accompanying notes are an integral part of the financial statements.

Statement of Operations

| for the year ended May 31, 2016 | |

| Investment Income | |

Income: Interest | $ 82,342,271 |

Expenses: Management fee | 6,820,825 |

| Administration fee | 1,510,911 |

| Services to shareholders | 2,033,682 |

| Distribution and service fees | 2,277,465 |

| Custodian fee | 20,501 |

| Professional fees | 129,000 |

| Reports to shareholders | 80,027 |

| Registration fees | 92,135 |

| Trustees' fees and expenses | 62,949 |

| Interest expense and fees on floating rate notes issued | 572,029 |

| Other | 115,231 |

| Total expenses before expense reductions | 13,714,755 |

| Expense reductions | (1,420,719) |

| Total expenses after expense reductions | 12,294,036 |

| Net investment income | 70,048,235 |

| Realized and Unrealized Gain (Loss) | |

| Net realized gain (loss) from investments | 20,385,005 |

| Change in net unrealized appreciation (depreciation) on investments | 1,229,038 |

| Net gain (loss) | 21,614,043 |

| Net increase (decrease) in net assets resulting from operations | $ 91,662,278 |

The accompanying notes are an integral part of the financial statements.

Statement of Cash Flows

| for the year ended May 31, 2016 | |

Increase (Decrease) in Cash: Cash Flows from Operating Activities | |

| Net increase (decrease) in net assets resulting from operations | $ 91,662,278 |