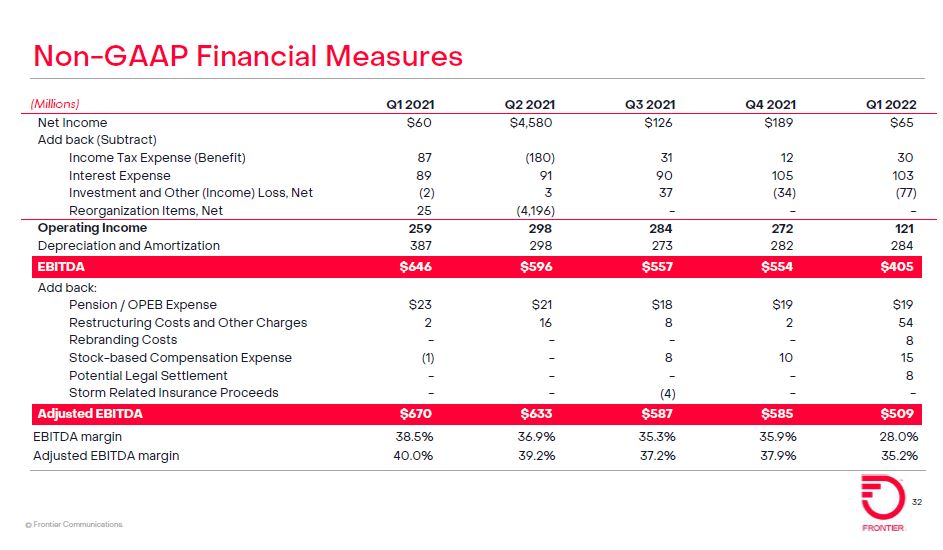

2 Safe Harbor Statement Forward-Looking Statements This release contains "forward-looking statements" related to future events. Forward-looking statements address our expectations or beliefs concerning future events, including, without limitation, our outlook with respect to future operating and financial performance, expected results from our implementation of strategic and cost savings initiatives, and our ability to comply with the covenants in the agreements governing our indebtedness and other matters. These statements are made on the basis of management’s views and assumptions, as of the time the statements are made, regarding future events and performance and contain words such as “expect,” “anticipate,” “intend,” “plan,” “believe,” “seek,” “see,” “may,” “will,” “would,” or “target.” Forward-looking statements by their nature address matters that are, to different degrees, uncertain. A wide range of factors could materially affect future developments and performance, including but not limited to: our significant indebtedness, our ability to incur substantially more debt in the future, and covenants in the agreements governing our current indebtedness that may reduce our operating and financial flexibility; declines in Adjusted EBITDA relative to historical levels that we are unable to offset; our ability to successfully implement strategic initiatives, including our fiber buildout and other initiatives to enhance revenue and realize productivity and service improvements; our ability to secure necessary construction resources, materials and permits for our fiber buildout initiative in a timely and cost effective manner; potential disruptions in our supply chain and the effects of inflation resulting from the COVID-19 pandemic, the global microchip shortage, or otherwise, which could adversely impact our business and hinder our fiber expansion plans; our ability to effectively manage our operations, operating expenses, capital expenditures, debt service requirement and cash paid for income taxes and liquidity; competition from cable, wireless and wireline carriers, satellite, fiber “overbuilders” and OTT companies, and the risk that we will not respond on a timely or profitable basis; our ability to successfully adjust to changes in the communications industry, including the effects of technological changes and competition on our capital expenditures, products and service offerings; risks related to disruption in our networks, infrastructure and information technology that result in customer loss and/or incurrence of additional expenses; the impact of potential information technology or data security breaches or other cyber-attacks or other disruptions; our ability to retain or attract new customers and to maintain relationships with customers; our reliance on a limited number of key supplies and vendors; declines in revenue from our voice services, switched and nonswitched access and video and data services that we cannot stabilize or offset with increases in revenue from other products and services; our ability to secure, continue to use or renew intellectual property and other licenses used in our business; our ability to hire or retain key personnel; our ability to dispose of certain assets or asset groups or to make acquisition of certain assets on terms that are attractive to us, or at all; the effects of changes in the availability of federal and state universal service funding or other subsidies to us and our competitors and our ability to obtain future subsidies, including participation in the proposed RDOF program; our ability to comply with the applicable CAF II and RDOF requirements and the risk of penalties or obligations to return certain CAF II and RDOF funds; our ability to defend against litigation and potentially unfavorable results from current pending and future litigation; our ability to comply with applicable federal and state consumer protection requirements; the effects of governmental legislation and regulation on our business, including costs, disruptions, possible limitations on operating flexibility and changes to the competitive landscape resulting from such legislation or regulation; the impact of regulatory, investigative and legal proceedings and legal compliance risks; our ability to effectively manage service quality in the states in which we operate and meet mandated service quality metrics; the effects of changes in income tax rates, tax laws, regulations or rulings, or federal or state tax assessments; the effects of changes in accounting policies or practices; our ability to successfully renegotiate union contracts; the effects of increased medical expenses and pension and postemployment expenses; changes in pension plan assumptions, interest rates, discount rates, regulatory rules and/or the value of our pension plan assets; the likelihood that our historical financial information may no longer be indicative of our future performance and our implementation of fresh start accounting; the impact of adverse changes in economic, political and market conditions in the areas that we serve, the U.S. and globally, including, but not limited to, disruption in our supply chain, inflation in pricing for key materials or labor, or other adverse changes resulting from epidemics, pandemics and outbreaks of contagious diseases, including the COVID-19 pandemic, natural disasters, economic or political instability or other adverse public health developments; potential adverse impacts of the COVID-19 pandemic on our business and operations, including potential disruptions to the work of our employees arising from health and safety measures such as social distancing, working remotely and recent applicable federal, state, and local mandates, and prohibitions, our ability to effectively manage increased demand on our network, our ability to maintain relationships with our current or prospective customers and vendors as well as their abilities to perform under current or proposed arrangements with us; risks associated with our emergence from the Chapter 11 Cases, including, but not limited to, the continuing effects of the Chapter 11 Cases on us and our relationships with our suppliers, customers, service providers or employees and changes in the composition of our board of directors and senior management; volatility in the trading price of our common stock, which has a limited trading history; substantial market overhang from the common stock issued in the Chapter 11 reorganization; certain provisions of Delaware law and our certificate of incorporation that may prevent efforts by our stockholders to change the direction or management of our Company; and certain other factors set forth in our other filings with the SEC. This list of factors that may affect future performance and the accuracy of forward-looking statements is illustrative and is not intended to be exhaustive. You should consider these important factors, as well as the risks and other factors contained in Frontier’s filings with the U.S. Securities and Exchange Commission, including our most recent reports on Form 10-K and Form 10-Q. These risks and uncertainties may cause actual future results to be materially different than those expressed in such forward-looking statements. We do not intend, nor do we undertake any duty, to update any forward-looking statements. Non-GAAP Financial Measures Certain financial measures included herein, including Adjusted EBITDA, Adjusted EBITDA Margin, Adjusted Operating Expenses and Operating Free Cash Flow, are not made in accordance with U.S. GAAP, and use of such terms varies from others in the same industry. Non-GAAP financial measures should not be considered as alternatives to net income (loss), net income margin or any other performance measures derived in accordance with U.S. GAAP as measures of operating performance or cash flows as measures of liquidity. Non-GAAP financial measures have important limitations as analytical tools, and you should not consider them in isolation or as substitutes for results as reported under U.S. GAAP. This presentation includes a reconciliation of certain non-GAAP financial measures to the most directly comparable financial measures calculated in accordance with U.S. GAAP. Projected GAAP financial measures and reconciliations of projected non-GAAP financial measures are not provided herein because such GAAP financial measures are not available on a forward-looking basis and such reconciliations could not be derived without unreasonable effort. This presentation uses the term “Implied Enterprise Value”, “Implied EV” and other similar terms, which is calculated using a trend line implied by our peers and certain assumed levels of broadband penetration. This term does not necessarily represent our actual enterprise value.