UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-01829 | |||||||

| ||||||||

Columbia Acorn Trust | ||||||||

(Exact name of registrant as specified in charter) | ||||||||

| ||||||||

One Financial Center, Boston, Massachusetts |

| 02111 | ||||||

(Address of principal executive offices) |

| (Zip code) | ||||||

| ||||||||

James R. Bordewick, Jr., Esq. Columbia Management Advisors, LLC One Financial Center Boston, MA 02111 | ||||||||

(Name and address of agent for service) | ||||||||

| ||||||||

Registrant’s telephone number, including area code: | 1-617-426-3750 |

| ||||||

| ||||||||

Date of fiscal year end: | December 31, 2006 |

| ||||||

| ||||||||

Date of reporting period: | December 31, 2006 |

| ||||||

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

4Q

Columbia Acorn

Family of Funds

Class Z Shares

Annual Report

December 31, 2006

n ColumbiaTM

Acorn® Fund

n ColumbiaTM

Acorn International®

n ColumbiaTM

Acorn USA®

n ColumbiaTM

Acorn International SelectSM

n ColumbiaTM

Acorn SelectSM

n ColumbiaTM

Thermostat FundSM

Managed by Columbia Wanger Asset Management, L.P.

NOT FDIC INSURED

May Lose Value

No Bank Guarantee

The views expressed in the "Letter to Shareholders," "Squirrel Chatter II" and "In a Nutshell" commentary reflect the current views of the respective authors. These views are not guarantees of future performance and involve certain risks, uncertainties and assumptions that are difficult to predict so actual outcomes and results may differ significantly from the views expressed. These views are subject to change at any time based upon economic, market or other conditions and the respective parties disclaim any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Columbia Acorn Fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any particular Columbia Acorn Fund. References to specific company securities should not be construed as a recommendation or investment advice.

Letter to Shareholders from the

Columbia Acorn Trust Board of Trustees

The Trustees of the Columbia Acorn Trust are pleased to present this 2006 annual report to shareholders of the Columbia Acorn Family of Funds ("Acorn Funds").

Your Trustees have a fiduciary responsibility to govern the Acorn Funds solely for the purpose intended by their shareholders. That means overseeing the responsiveness of our service providers to the needs and interests of shareholders. Accordingly, our most critical tasks are to evaluate and select service providers and focus on their performance and accountability.

Shareholders of the Acorn Funds have received investment advisory services from Columbia Wanger Asset Management ("CWAM") and its predecessors for many years. Although ownership of CWAM has changed over recent years and CWAM is now owned by the Bank of America ("BOA"), we believe that the critical components required to provide strong investment performance have remained substantially intact at CWAM with the full support of your independent trustees.1 We monitor investment performance throughout the year and annually take a fresh look at the relationships with our service providers with a diligent review and negotiations to assure that our agreements for the next year are responsive to the rights and expectations of shareholders. We are pleased to report that we renewed our in vestment advisory agreement with CWAM for the year ending July 31, 2007.

Expenses paid by the Acorn Funds reduce your total investment returns. Your Trustees are sensitive to the relative importance of fund expenses to shareholders, and we diligently review those expenses on a regular basis. You should note that total expenses of most share classes of each Acorn Fund, expressed as a percentage of the Fund's net assets, declined again in 2006, continuing a trend of recent years. For the Thermostat Fund, total expenses used for this comparison included expenses incurred by the Fund from underlying portfolio funds. The one exception to a decrease in 2006 was the Class Z shares of Columbia Acorn Fund, which had an expense ratio that was unchanged from the prior year.

Your Trustees acted on other matters during the past year. We raised the minimum initial investment for new shareholders in Columbia Acorn International, Columbia Acorn International Select and Columbia Thermostat to $2,500. (The other Funds already had higher minimums.) We negotiated new breakpoints in the investment advisory fee rates above current asset levels for Columbia Acorn USA and Columbia Acorn Select to provide for a greater sharing of economies of scale as future asset growth occurs. We negotiated a new transfer agency and shareholder servicing agreement that has changed the cost of transfer agency services. The fees for those services now cover all sub-transfer agency services provided by financial intermediaries, and Columbia Management Services will no longer waive its right to reimbursement by the Funds for its out-of-pocket expenses. The new agreement will be fully implemented on April 1, 2007 and is estimated t o result in a change of fees paid by shareholders of various share classes in each fund ranging from some decreases to increases up to approximately three basis points. We also reduced the annual rate of Rule 12b-1 fees for Class B shares in all funds from 85 to 75 basis points effective August 1, 2006.

As reported in prior years, we have been waiting for a final determination by an Independent Distribution Consultant ("IDC") on distributions to shareholders of certain Acorn Funds arising from the 2004 settlement of regulatory proceedings involving BOA. Your Board of Trustees has monitored the IDC's process of developing the distribution plan, and we have made recommendations. We recently have been advised that the approval of a definitive plan of distribution is imminent and, based on that information, we expect certain shareholders of Columbia Acorn International Fund and Columbia Acorn International Select Fund to receive distributions. Rust

Consulting (a separate entity not affiliated with BOA) has been engaged to administer the distributions. Rust Consulting will be sending checks and related information to those shareholders who are eligible to receive payments once the plan of distribution is approved.

We are pleased to report that two new independent trustees were elected to the Board during the past year: James A. Star and Patricia H. Werhane. They have impressive backgrounds and experience suited for our Board, and we believe shareholders will benefit from their contributions.

On September 26, 2006 CWAM and the Board held an annual shareholder information meeting in Chicago. The objective of the annual shareholder meeting is to provide information about the investment process and an opportunity to interact with the investment managers of CWAM. The meeting was available on telephone replay for those who could not attend. Next year, in an attempt to increase shareholder attendance, we are considering holding the meeting at a different time of day. We also are exploring other electronic alternatives to make the information available for shareholders who do not reside in Chicago and cannot attend in person. We hope you will take advantage of this opportunity to learn more about the professional managers of CWAM and how your money is managed.

Thank you for your confidence in the Acorn Funds.

Robert E. Nason

Independent Chairman of the Board of Trustees

Columbia Acorn Trust

1 Past performance is no guarantee of future results. The investment return and principal value will fluctuate so that shares may be worth more or less than the original cost. Please consider the investment objectives, risks, charges and expenses of the Acorn Funds carefully before investing.

Columbia Acorn Family of Funds

Table of Contents

| Performance At A Glance | 2 | ||||||

| Squirrel Chatter II Small Caps: The Dilbert Antidote | 3 | ||||||

| Understanding Your Expenses | 6 | ||||||

| Columbia Acorn Fund | |||||||

| In a Nutshell | 8 | ||||||

| At a Glance | 9 | ||||||

| Major Portfolio Changes | 20 | ||||||

| Statement of Investments | 22 | ||||||

| Columbia Acorn International | |||||||

| In a Nutshell | 10 | ||||||

| At a Glance | 11 | ||||||

| Major Portfolio Changes | 33 | ||||||

| Statement of Investments | 35 | ||||||

| Portfolio Diversification | 41 | ||||||

| Columbia Acorn USA | |||||||

| In a Nutshell | 12 | ||||||

| At a Glance | 13 | ||||||

| Major Portfolio Changes | 42 | ||||||

| Statement of Investments | 43 | ||||||

| Columbia Acorn International Select | |||||||

| In a Nutshell | 14 | ||||||

| At a Glance | 15 | ||||||

| Major Portfolio Changes | 49 | ||||||

| Statement of Investments | 50 | ||||||

| Portfolio Diversification | 53 | ||||||

| Columbia Acorn Select | |||||||

| In a Nutshell | 16 | ||||||

| At a Glance | 17 | ||||||

| Major Portfolio Changes | 54 | ||||||

| Statement of Investments | 55 | ||||||

| Columbia Thermostat Fund | |||||||

| In a Nutshell | 18 | ||||||

| At a Glance | 19 | ||||||

| Statement of Investments | 58 | ||||||

| Columbia Acorn Family of Funds | |||||||

| Statements of Assets and Liabilities | 60 | ||||||

| Statements of Operations | 61 | ||||||

| Statements of Changes in Net Assets | 62 | ||||||

| Financial Highlights | 66 | ||||||

| Notes to Financial Statements | 68 | ||||||

| Report of Independent Registered Public Accounting Firm | 76 | ||||||

| Unaudited Information | 77 | ||||||

| Management Fee Evaluation of the Senior Officer | 78 | ||||||

| Board Approval of the Advisory Agreements | 83 | ||||||

| Board of Trustees and Management of Columbia Acorn Funds | 86 | ||||||

| Columbia Acorn Family of Funds Information | 89 | ||||||

2006 Year-End Distributions

The following table details the Funds' year-end distributions. The record date for all Funds except Columbia Thermostat Fund was December 7, 2006. The ex-dividend date was December 8, 2006, and the payable date was December 11, 2006. For Columbia Thermostat Fund, the record date was December 21, 2006. The ex-dividend date was December 22, 2006, and the payable date was December 26, 2006. Columbia Acorn International Select did not have any year-end distributions.

| Short-term Capital Gains | Long-term Capital Gains | Ordinary Income | Reinvestment Price | ||||||||||||||||

| Columbia Acorn Fund | $ | 0.0792 | $ | 1.9924 | $ | 0.1263 | $ | 29.82 | |||||||||||

| Columbia Acorn International | None | $ | 3.3557 | $ | 0.4317 | $ | 38.80 | ||||||||||||

| Columbia Acorn USA | None | $ | 0.5052 | None | $ | 28.96 | |||||||||||||

| Columbia Acorn Select | None | $ | 0.4991 | None | $ | 26.15 | |||||||||||||

| Columbia Thermostat Fund | $ | 0.0558 | $ | 0.4201 | $ | 0.4954 | $ | 12.53 | |||||||||||

1

Columbia Acorn Family of Funds

Performance At A Glance Class Z Average Annual Total Returns through 12/31/06

| NAV on 12/31/06 | 4th quarter* | 1 year | 3 years | 5 years | 10 years | Life of Fund | |||||||||||||||||||||||||

| Columbia (ACRNX) Acorn Fund (6/10/70) | $ | 29.71 | 7.66 | % | 14.45 | % | 16.30 | % | 14.71 | % | 15.16 | % | 16.30 | % | |||||||||||||||||

| Russell 2500 | 8.70 | % | 16.17 | % | 14.10 | % | 12.19 | % | 11.26 | % | NA | ||||||||||||||||||||

| S&P 500 | 6.70 | % | 15.79 | % | 10.44 | % | 6.19 | % | 8.42 | % | 11.98 | % | |||||||||||||||||||

| Lipper Small-Cap Core Funds Index | 8.07 | % | 13.70 | % | 13.12 | % | 10.50 | % | 10.32 | % | NA | ||||||||||||||||||||

| Lipper Mid-Cap Core Funds Index | 7.15 | % | 13.44 | % | 12.75 | % | 10.10 | % | 10.69 | % | NA | ||||||||||||||||||||

| Columbia (ACINX) Acorn International (9/23/92) | $ | 40.31 | 14.45 | % | 34.53 | % | 28.50 | % | 21.35 | % | 13.15 | % | 14.53 | % | |||||||||||||||||

| S&P/Citigroup EMI Global ex-US | 13.79 | % | 30.83 | % | 27.31 | % | 24.39 | % | 10.65 | % | 10.54 | % | |||||||||||||||||||

| MSCI EAFE | 10.35 | % | 26.34 | % | 19.93 | % | 14.98 | % | 7.71 | % | 8.91 | % | |||||||||||||||||||

| Lipper Int'l Small-Cap Funds Index | 13.68 | % | 28.06 | % | 27.09 | % | 23.99 | % | 13.34 | % | NA | ||||||||||||||||||||

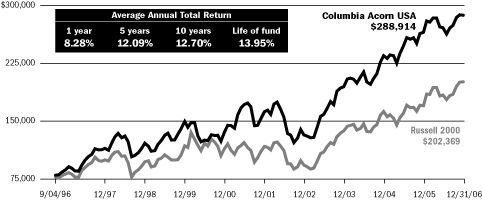

| Columbia (AUSAX) Acorn USA (9/4/96) | $ | 28.66 | 4.78 | % | 8.28 | % | 13.85 | % | 12.09 | % | 12.70 | % | 13.95 | % | |||||||||||||||||

| Russell 2000 | 8.90 | % | 18.37 | % | 13.56 | % | 11.39 | % | 9.44 | % | 10.09 | % | |||||||||||||||||||

| Lipper Small-Cap Core Funds Index | 8.07 | % | 13.70 | % | 13.12 | % | 10.50 | % | 10.32 | % | 10.83 | % | |||||||||||||||||||

| S&P 500 | 6.70 | % | 15.79 | % | 10.44 | % | 6.19 | % | 8.42 | % | 9.50 | % | |||||||||||||||||||

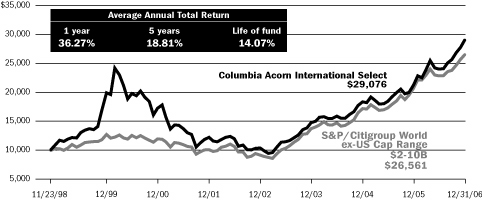

| Columbia (ACFFX) Acorn Int'l Select (11/23/98) | $ | 27.97 | 13.06 | % | 36.27 | % | 25.19 | % | 18.81 | % | NA | 14.07 | % | ||||||||||||||||||

| S&P/Citigroup World ex-US Cap Range $2-10B | 11.32 | % | 27.88 | % | 24.45 | % | 21.24 | % | NA | 12.81 | % | ||||||||||||||||||||

| MSCI EAFE | 10.35 | % | 26.34 | % | 19.93 | % | 14.98 | % | NA | 7.45 | % | ||||||||||||||||||||

| Lipper International Funds Index | 10.55 | % | 25.89 | % | 19.98 | % | 15.14 | % | NA | 8.66 | % | ||||||||||||||||||||

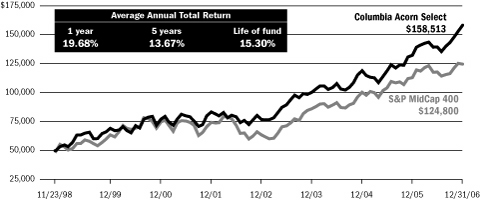

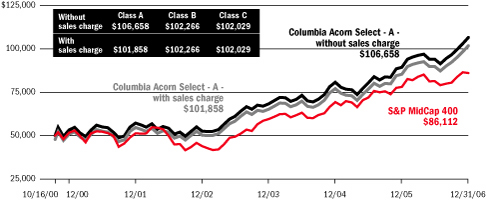

| Columbia (ACTWX) Acorn Select (11/23/98) | $ | 26.59 | 10.51 | % | 19.68 | % | 16.38 | % | 13.67 | % | NA | 15.30 | % | ||||||||||||||||||

| S&P MidCap 400 | 6.99 | % | 10.32 | % | 13.09 | % | 10.89 | % | NA | 11.94 | % | ||||||||||||||||||||

| Lipper Mid-Cap Growth Index | 7.71 | % | 11.02 | % | 11.53 | % | 6.09 | % | NA | 7.23 | % | ||||||||||||||||||||

| S&P 500 | 6.70 | % | 15.79 | % | 10.44 | % | 6.19 | % | NA | 4.10 | % | ||||||||||||||||||||

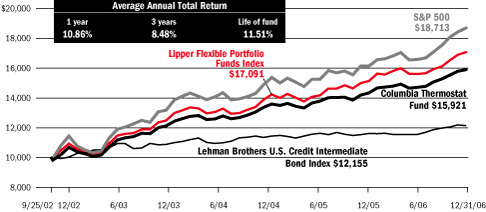

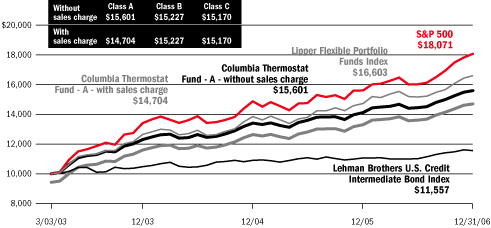

| Columbia (COTZX) Thermostat Fund (9/25/02)† | $ | 12.57 | 4.11 | % | 10.86 | % | 8.48 | % | NA | NA | 11.51 | % | |||||||||||||||||||

| S&P 500 | 6.70 | % | 15.79 | % | 10.44 | % | NA | NA | 15.81 | % | |||||||||||||||||||||

| Lehman Brothers U.S. Credit Intermediate Bond Index | 1.27 | % | 4.49 | % | 3.32 | % | NA | NA | 4.68 | % | |||||||||||||||||||||

| Lipper Flexible Portfolio Funds Index | 5.99 | % | 12.77 | % | 9.51 | % | NA | NA | 13.38 | % | |||||||||||||||||||||

*Not annualized.

The Funds are listed under "Columbia" in the financial press.

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value of an investment in a Fund will fluctuate so that Fund shares, when redeemed, may be worth more or less than their original cost. Please visit columbiafunds.com for daily and most recent month-end updates. Net asset value (NAV) returns do not include sales charges or contingent deferred sales charges (CDSC). Class Z shares are sold only at NAV with no Rule 12b-1 fee. Class Z shares have limited eligibility and the investment minimum requirement may vary. Please see the Funds' prospectuses for details.

Performance may reflect any voluntary waivers or reimbursements of fund expenses by the advisor or its affiliates. Absent these waivers, or reimbursement arrangements, performance results may be lower.

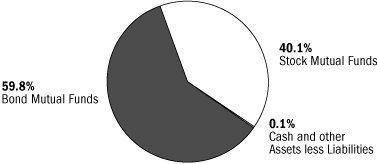

†A "fund of funds" bears its allocable share of the costs and expenses of the underlying funds in which it invests. Such funds are thus subject to two levels of fees and potentially higher expense ratios than would be associated with an investment in an investment fund that invests and trades directly in financial instruments under the direction of a single manager.

Description of indexes: S&P 500 is a broad, market-weighted average of 500 U.S. blue-chip company stock's performance. S&P MidCap 400 is a broad market-weighted index of 400 stocks that are in the next size/tier down from the S&P 500. Russell 2000 is a market-weighted index of 2000 smaller U.S. companies, formed by taking the largest 3,000 companies and eliminating the largest 1,000. Russell 2500 is the smallest 2,500 U.S. companies from this same group. S&P/Citigroup EMI Global ex-US is the bottom 20% of institutionally investable capital of developed and emerging (after 9/30/1994) countries, selected by the index sponsor, outside the U.S. MSCI EAFE is Morgan Stanley's Europe, Australasia and Far East Index, a widely recognized international benchmark that comprises 20 major markets in proportion to world stock market capitalization. S&P/Citigroup World ex-US Cap Range $2–10B is a subset of the broad market selected by the index sponsor rep resenting the mid-cap developed market excluding the U.S. Lipper Indexes include the largest funds tracked by Lipper, Inc. in the named category. Lipper Mid-Cap Growth Index, 30 mid-cap growth funds; Lipper Mid-Cap Core Funds Index, 30 mid-cap core funds; Lipper International Funds Index, 30 largest non-U.S. funds, not including non-U.S. small-cap funds; Lipper International Small-Cap Funds Index, 10 largest non-U.S. funds investing in small-cap companies, including Columbia Acorn International; Lipper Small-Cap Core Funds Index, 30 largest small-cap core funds, including Columbia Acorn Fund. Lipper Flexible Portfolio Funds Index is an equal dollarweighted index of the 30 largest mutual funds within the Flexible Portfolio fund classification, as defined by Lipper. Lehman Brothers U.S. Credit Intermediate Bond Index is the inte rmediate component of the U.S. Credit Index. The U.S. Credit Index includes publicly issued U.S. corporate and foreign debentures and secured notes that meet specified maturity, liquidity, and quality requirements. All indexes are unmanaged and returns include reinvested distributions. It is not possible to invest directly in an index.

2

Squirrel Chatter II

Small Caps: The Dilbert Antidote

Small Caps vs. Large Caps

Small Caps vs. Large Caps

Small caps edged out large caps in 2006. The Russell 2500 Index appreciated 16.17%, barely more than the S&P 500's 15.79% return, but enough to keep the domestic small-cap winning streak intact.

Our data indicates that the current small-cap cycle began in March 1999. From the end of March 1999 through year-end 2006, the small-cap Russell 2500 Index returned a total of 144.40%, or 12.22% annually. In contrast, the large-cap S&P 500 Index gained 24.69%, or 2.89% annually.

Why have small caps beaten large caps so much for such a long cycle? By many measures, small caps were at 20-year record low relative valuations at the start of the cycle. In contrast, many large caps then seemed very expensive and of course the "bubble" did deflate starting in the first quarter of 2000.

Small-cap earnings growth also helps explain stock performance. Since the beginning of the March 1999 cycle, Russell 2500 Index earnings per share were up 11.11% annually, while large-cap S&P 500 Index earnings were up 7.10% annually. A combination of cheap stocks and faster earnings growth often provides superior investment results.

In the Funds' 2005 third quarter report to shareholders, I expressed concerns about small-cap valuations. I was perhaps early or maybe just plain wrong. As a firm, we remain cautious, but note that there seems to be no "small-cap mania" or other obvious warning signal for the imminent end of the small-cap cycle. It has become more challenging to find small companies at reasonable prices, but when we see opportunities, we try to take them. For instance, many smaller stocks declined last summer while we believed the business environment was healthy. In September 2006 we took advantage of the slump and added to some of our domestic names at what we thought were good prices.

Small caps have also outperformed over the very long run. The Russell 2500 Index goes back only to 1978, but scholars have linked other time series to derive small- and large-cap performance numbers since 1926.1 From the beginning of 1926 until year-end 2006, small caps returned 12.32% annually while large caps had annual returns of 10.43%. The difference of 1.89% per year may not sound like much, but when compounded over 81 years it makes an enormous difference. A $1,000 investment in small caps would have appreciated to $12,195,329, while the same amount in large caps would have grown to "only" $3,088,420.2

Why have small caps clobbered large caps over the very long term? It seems that many large companies have had problems. We are all aware when a large company such as Enron has a sudden and dramatic collapse. It's big news (kind of like the Hindenburg disaster). But a substantial number of other large companies have more gradually lost market dominance and have provided poor returns to shareholders for years.

At the beginning of the 20th century, United States Steel was the largest stock on the New York Stock Exchange (NYSE). The company fell so far near the end of the century that it was added into the Russell 2500 Index. (As it recovered it was a major upside driver to the benchmark until it graduated out in June 2006.) More recently Kodak, General Motors and Sears spent at least one year between 1966 and 1971 among the top five NYSE capitalization companies. They now do not even rank among the top 300.3 These sorts of declines merit further analysis.

From the Desk of Dilbert

Since we are students of smaller companies, when considering reasons for large company declines, we need to turn to experts on large companies. Scott Adams, in his book, The Dilbert Principle, points out that he worked for a large company for seventeen years. He writes, "Most business books are written by consultants and professors who haven't spent much time in a cubicle."4

3

Adams parodies the experiences of employees and management of large companies. He makes his money writing comic strips on the topic. In Dilbert's world his company is a politicized bureaucracy populated by stupid, arrogant managers who do not value employees or customers. His boss is every employee's worst nightmare. Still, Adams' views from his cubicle do provide some useful and humorous insights.

Adams points out early on that people are idiots, including himself. He offers this true example of idiots on the customer side: "Kodak introduced a single use camera called the Weekender. Customers have called the support line to ask if it's okay to use it during the week."5 While this anecdote does not explain Kodak's decline it certainly supports Adams' point!

Since larger companies have more people, one may infer that they have more idiots. But, more seriously, Adams notes that large companies often systematically divert employees away from serving customers and place them on committees to develop things like Mission Statements. Once a Mission Statement ("a long awkward sentence that demonstrates management's inability to think clearly"6) is painstakingly created, next can come a Vision Statement. Large companies also like to hire consultants who in turn tell management (a) to change processes and structures but not the management, (b) to do what employees have been trying to tell them to do, or (c) to authorize more consulting. Worse yet ... "large companies have legal departments. No project is so risk-free that your company lawyer can't kill it."7

Adams suggests obvious ways for large companies to succeed. They include focusing on improving employees and products rather than pursuing bureaucratic tasks or adopting the latest managerial fad.

The Innovator's Dilemma

For another take on the business world, we turned to Harvard Business School professor Clayton Christensen. His book, The Innovator's Dilemma,8 explains how well-managed companies often miss opportunities and are injured by new competitors offering disruptive innovations.

Well managed companies tend to listen to customers, study and forecast underlying demand, invest heavily in research, and watch for competitors. They develop improved new products or services that address large established markets and often promise higher margins.

Christensen explains that existing customers often do not want disruptive new products or services. Nascent markets are by nature tiny and unpredictable. At first, disruptive innovations often provide lower performance and margins. Success for these innovations seems unlikely and large companies appear rational to not invest in them.

But this seemingly rational path is often a mistake. Christensen's examples include makers of computer disk drives, minicomputers, mechanical excavators and steel. In each case, existing customers had little desire for innovative new products or processes, which admittedly had some inferior attributes like price/performance or quality vs. existing products. The innovators found niche customers who appreciated some aspects of the new product such as size, ruggedness, or cost, and then improved their products at a faster rate than competitors. What had been an inferior product became fully competitive, at a lower cost.

How can a large company compete against a possible disruptive innovation? Imagine a smart manager saying, "Hey guys, I've got this new, lower performance, lower-margin product that existing customers say they don't want, but we should invest in it anyway should a market develop, in which case we will improve it over time. And oh, by the way, we need to divert people from existing high margin products." That is unlikely. Instead, as Christensen points out, the company's management often decides to continue to go up market, producing high gross-margin products for existing customers. More often than not, this decision is a mistake. Companies unwilling to innovate tend to eventually lose market share.

Christensen offers possible ways for large companies to innovate. A favorite is to create a small, preferably remote, autonomous division with agility and

4

a low-cost structure, whose sole focus is to develop an innovation and sell it to new customers. The division must be able to experience short-term failures and change tactics. Though some large companies have succeeded by taking this approach, few come to mind. This solution is anathema to Dilbert-style bureaucracies and managements.

Small Company Advantages

Most startups and small companies focus on hiring and keeping good employees and providing customers fine products or services. Many are created by refugees from large companies who rejected bureaucracies. Small companies with distinct cultures may not need 72-page expense policies. These companies appear to have more streamlined policies, and some seem to abide by a sort of simplified Golden Rule: "Serve the customers, spend company money wisely, and behave like the founder does." If Adams had started work at a small company he might have remained there, reasonably content. But the world would be poorer without Dilbert.

Christensen says, "Large companies often surrender emerging growth markets because smaller, disruptive companies are actually more capable of pursuing them... Their values embrace small markets, and their cost structures can accommodate lower margins. Their market research and resource allocation processes allow managers to proceed intuitively rather than having to be backed up by careful research and analysis, presented in PowerPoint."9 Small companies seem to have DNA that naturally corresponds to both Adams' and Christensen's managerial solutions.

We admit being clearly biased towards small caps but the reality is that more small companies fail than large companies (in part because there are more small companies to begin with). Small company failures are less newsworthy events and rarely warrant major stories (kind of like third-world bus plunges10). We've owned our share of disappointing companies, including a few bankruptcies.

While there are losers in both the large and small cap ranks, a minority of enormously successful small-cap companies with that innovative DNA have driven overall small-cap returns. That is why we believe small-cap investing can be a winner's game. We've had dozens of what we believe to be spectacular winners over the life of the Columbia Acorn Funds. These have far offset our losers and may be worthy of their own Squirrel Chatter II column in the future.

Charles P. McQuaid

President and Chief Investment Officer

Columbia Wanger Asset Management, L.P.

1 U.S. Small Stock Total Return (Morningstar/Ibbottson Encor Application) linked with the Russell 2500 Index on 12/31/1978. Large-cap data based on the S&P 500.

2 Keep in mind that an investment cannot be made directly in an index, and past performance is no guarantee of future results. This is for illustrative purposes only and not indicative of any investment. The data assumes reinvestment of all income and does not account for taxes or transaction costs. Source: U.S. Small Stock Total Return linked with the Russell 2500 on 12/31/1978 and, for large caps, the S&P 500. Both equity categories soundly beat inflation. At year end 2006, $11,384 had the purchasing power of $1,000 in 1926. Inflation data from inflationdata.com, calculated using the CPI Index.

3 As of January 9, 2007.

4 Adams, Scott, The Dilbert Principle (New York: HarperCollins Publishers, 1996), pg. 4.

5 Ibid., pg. 9.

6 Ibid., pg. 36.

7 Ibid., pg. 88.

8 Christensen, Clayton M., The Innovator's Dilemma, (New York: HarperCollins Publishers, 1997)

9 Ibid., pg. 192.

10 In Tim Miller's The Panama Hat Trail (New York: William Morrow and Company, Inc., 1986), the author confesses his fears about Latin American bus rides. These fears have been brought on by years of reading standard, two-sentence bus-plunge pieces used by newspapers in the United States as fillers on the foreign-news page. The date lines change, but the headlines always include the words "bus plunge."

Stocks of small- and mid-cap companies pose special risks, including possible illiquidity and greater price volatility than stocks of larger, more established companies. International investing involves special risks, including foreign taxation, currency risks, risks associated with possible differences in financial standards and other risks associated with future political and economic developments. A fund that maintains a relatively concentrated portfolio may be subject to greater risk than a fund that is more fully diversified.

Past performance is no guarantee of future results.

5

Understanding Your Expenses

As a Fund shareholder, you incur two types of costs. There are transaction costs, which generally include sales charges on purchases and may include redemption or exchange fees. There are also ongoing costs, which generally include investment advisory fees, Rule 12b-1 fees and other Fund expenses. The information on this page is intended to help you understand your ongoing costs of investing in the Columbia Acorn Funds and to compare these costs with the ongoing costs of investing in other mutual funds.

Analyzing your Fund's expenses

To illustrate these ongoing costs, we have provided examples and calculated the expenses paid by investors in the Class Z shares of the Columbia Acorn Funds for the last six months. The information in the following table is based on an initial, hypothetical investment of $1,000, which is invested at the beginning of the reporting period and held for the entire period. Expense information is calculated two ways and each method provides you with different information. The amount listed in the "Actual" column is calculated using each Fund's actual operating expenses and total return for the period. The amount listed in the "Hypothetical" column assumes that the return each year is 5% before expenses and then applies each Fund's actual expense ratio for the period to the hypothetical return. You should not use the hypothetical account values and expenses to estimate either your actual account balance at the end of the period or the expenses you paid during the reporting period. See the "Compare with other funds" information for details on using the hypothetical data.

>July 1, 2006 – December 31, 2006

Account value at the beginning of the period ($) | Account value at the end of the period ($) | Expenses paid during the period ($) | Fund's annualized expense ratio (%)* | ||||||||||||||||||||||||||||

| Class Z Shares | Actual | Hypothetical | Actual | Hypothetical | Actual | Hypothetical | Actual | ||||||||||||||||||||||||

| Columbia Acorn Fund | 1,000.00 | 1,000.00 | 1,081.72 | 1,021.48 | 3.88 | 3.77 | 0.74 | ||||||||||||||||||||||||

| Columbia Acorn International | 1,000.00 | 1,000.00 | 1,177.30 | 1,020.47 | 5.16 | 4.79 | 0.94 | ||||||||||||||||||||||||

| Columbia Acorn USA | 1,000.00 | 1,000.00 | 1,059.59 | 1,020.21 | 5.14 | 5.04 | 0.99 | ||||||||||||||||||||||||

| Columbia Acorn International Select | 1,000.00 | 1,000.00 | 1,207.69 | 1,018.90 | 6.96 | 6.36 | 1.25 | ||||||||||||||||||||||||

| Columbia Acorn Select | 1,000.00 | 1,000.00 | 1,135.20 | 1,020.37 | 5.17 | 4.89 | 0.96 | ||||||||||||||||||||||||

| Columbia Thermostat Fund | 1,000.00 | 1,000.00 | 1,081.01 | 1,023.95 | 1.31 | 1.28 | 0.25 | ||||||||||||||||||||||||

Expenses paid during the period are equal to each Fund's annualized expense ratio, multiplied by the average account value over the period and then multiplied by the number of days in the Fund's most recent fiscal half-year and divided by 365.

Had the investment adviser and/or transfer agent not reimbursed/waived a portion of expenses, total return would have been reduced.

It is important to note that the expense amounts shown in the table are meant to highlight only ongoing costs of investing in the Funds and do not reflect any transaction costs, such as sales charges, redemption or exchange fees. Therefore, the hypothetical examples provided may not help you determine the relative total costs of owning different funds. If these transaction costs were included, your costs would have been higher.

Columbia Thermostat Fund's expenses do not include fees and expenses incurred by the Fund from the underlying portfolio funds.

*For the six months ended December 31, 2006.

Compare with other funds

Since all mutual funds are required to include the same hypothetical calculations about expenses in shareholder reports, you can use this information to compare the ongoing cost of investing in the Funds with other funds. To do so, compare the 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds. As you compare hypothetical examples of other funds, it is important to note that hypothetical

6

examples are meant to highlight the continuing costs of investing in a fund and do not reflect any transaction costs, such as sales charges or redemption or exchange fees.

Estimating your actual expenses

To estimate the expenses that you actually paid over the period, first you will need your account balance at the end of the period:

• For shareholders who receive their account statements from Columbia Management Services, Inc., your account balance is available online at columbiafunds.com or by calling Shareholder Services at (800) 922-6769.

• For shareholders who receive their account statements from their brokerage firm, contact your brokerage firm to obtain your account balance.

1. Divide your ending account balance by $1,000. For example, if an account balance was $8,600 at the end of the period, the result would be 8.6.

2. In the section of the table titled "Expenses paid during the period," locate the amount for your Fund. You will find this number is in the column labeled "Actual." Multiply this number by the result from step 1. Your answer is an estimate of the expenses you paid on your account during the period.

7

Columbia Acorn Fund

In a Nutshell

Charles P. McQuaid

Lead Portfolio Manager

Robert A. Mohn

Co-Portfolio Manager

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value of an investment in the Fund will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Performance may reflect any voluntary waivers or reimbursements of fund expenses by the Adviser or its affiliates. Absent these waivers, or reimbursement arrangements, performance results may be lower. Please visit columbiafunds.com for daily and most recent month-end performance updates.

Fund's Positions

in Mentioned Holdings

As of 12/31/06, the Fund's positions in the holdings mentioned were:

| Coach | 1.7 | % | |||||

| People's Bank of Bridgeport | 1.0 | % | |||||

| Chico's FAS | 0.8 | % | |||||

| SEI Investments | 0.8 | % | |||||

| Time Warner Telecom | 0.5 | % | |||||

| Christopher & Banks | 0.4 | % | |||||

| Hong Kong Exchanges and Clearing | 0.4 | % | |||||

| Chattem | 0.3 | % | |||||

| UrAsia Energy | 0.3 | % | |||||

| Jubilee Mines | 0.2 | % | |||||

| Station Casinos | 0.2 | % | |||||

| USG People | 0.2 | % | |||||

| Vallourec | 0.2 | % | |||||

Portfolio holdings are subject to change periodically and may not be representative of current characteristics and holdings.

Columbia Acorn Fund returned 14.45% in 2006, somewhat less than the 16.17% gain of the Russell 2500 Index, its most comparable benchmark. As shown on Page 2, the Fund slightly beat the Lipper Small- and Mid-Cap Core Indexes for the year. While we are disappointed that the Fund's 10-year outperformance streak ended, we are pleased that it did well vs. its peers.

In 2006, many small- and mid-cap managers had a tough time beating benchmarks, as microcaps, real estate investment trusts ("REITs"), utilities and materials companies outperformed. We had relatively few investments in microcaps, due to what we believed were high valuations. While the Fund's REITs, utilities and materials stocks outperformed, the Fund did not own enough of them. We thought that REITs on average were expensive and we did not find enough utilities and materials companies that we thought were fundamentally attractive.

During the fourth quarter, the Fund rose 7.66%, slightly below the smaller cap indexes but slightly ahead of the larger cap indexes. Microcaps and materials stocks remained outperformers in the fourth quarter.

Foreign stocks continued to boost Columbia Acorn Fund performance, rising 45.37% in the year and 16.44% in the quarter. They include all four of the Fund's 2006 top percentage winners. Hong Kong Exchanges and Clearing traded up 173% on increased trading of Chinese securities, French pipe maker Vallourec surged 157% on rising demand from energy and process industries, Canada's UrAsia Energy popped 147% on rising uranium volumes and prices, and USG People, a Dutch temporary staffing company, jumped 105% due to increased demand from employers in Europe. We cut the Fund's position in Vallourec during the year, as we were concerned about competition and a possible slowdown in U.S. natural gas drilling. We also trimmed the Fund's positions in Hong Kong Exchanges and Clearing and USG People.

Australia's Jubilee Mines joined the foreign winner's circle in the fourth quarter, extracting a 63% gain on higher nickel prices and continued exploration success. In the three years ending 2006, Columbia Acorn Fund's foreign stocks rose 152%. Given such gains, we deemed it prudent to continue trimming. As of year-end 2006, foreign stocks were 12.5% of the Fund, down 0.5% in the quarter and 3.1% in the year.

Columbia Acorn Fund's largest dollar gainer for both periods was Coach, rising 29% in the year and 25% in the quarter on strong sales and margins. Other domestic big-dollar winners for the year included People's Bank of Bridgeport, coining a 48% return as it proceeded to demutualize fully, and SEI Investments, up 62% on solid earnings growth. Time Warner Telecom provided the best domestic percentage gain in the year, doubling on fine sales and cash flow momentum. The Fund's largest domestic percentage gainers in the quarter were Chattem, up 43% thanks to a highly accretive acquisition, and Station Casinos, winning 42% as it received a takeover bid. Some 26 of the Fund's stocks were subject to new takeover bids in 2006.

Retailers Chico's FAS and Christopher & Banks had merchandising problems in 2006. Chico's was the Fund's largest dollar loser and dropped 53% in the year. Christopher & Banks was the largest dollar loser for the quarter, off 36%. During the fourth quarter we bought some additional Chico's. While our opinions are subject to change, we believe both companies should do well going forward.

Small-cap stocks are often more volatile and less liquid than the stocks of larger companies. Small companies may have a shorter history of operations than larger companies and may have a less diversified product line, making them more susceptible to market pressure. Investments in foreign securities have special risks, including political or economic instability, higher costs, different regulations, accounting standards, trading practices and levels of information, and currency exchange rate fluctuations.

8

Columbia Acorn Fund (ACRNX)

At a Glance

Pretax and After-tax Average Annual Total Returns (Class Z)

through December 31, 2006

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value of an investment in the Fund will fluctuate so that Fund shares, when redeemed, may be worth more or less than their original cost. Performance may reflect any voluntary waivers or reimbursements of Fund expenses by the Adviser or its affiliates. Absent these waivers or reimbursement arrangements, performance results may be lower. Visit columbiafunds.com for daily and most recent month-end updates.

| Inception 6/10/70 | 1 year | 5 years | 10 years | ||||||||||||

| Returns before taxes | 14.45 | % | 14.71 | % | 15.16 | % | |||||||||

| Returns after taxes on distributions | 12.95 | 14.07 | 13.52 | ||||||||||||

| Returns after taxes on distributions and sale of fund shares | 11.04 | 12.85 | 12.80 | ||||||||||||

| Russell 2500 (pretax) | 16.17 | 12.19 | 11.26 | ||||||||||||

| S&P 500 (pretax) | 15.79 | 6.19 | 8.42 | ||||||||||||

After-tax returns are calculated using the highest historical individual federal marginal income tax rates, and do not reflect the impact of state and local taxes. Returns after taxes on distributions and sale of Fund shares reflect the additional tax impact of long-term gains or losses realized when Fund shares are sold. The returns are taxed at the maximum rate and assume shares were purchased at the beginning of the period. Actual after-tax returns depend on the investor's tax situation and may differ from those shown. After-tax returns are not relevant to investors who hold their Fund shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts. After-tax returns are shown for Class Z shares only; after-tax returns for other share classes will vary. Indexes do not reflect any deduction for fees, expenses or taxes.

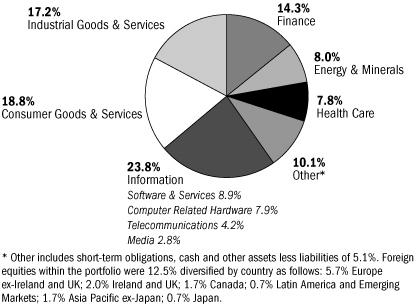

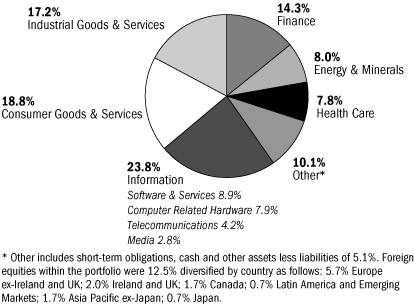

Columbia Acorn Fund Portfolio Diversification

as a % of net assets as of 12/31/06

Columbia Acorn Fund Top 10 Holdings

as a % of net assets as of 12/31/06

| 1. | Coach Designer & Retailer of Branded Leather Accessories | 1.7 | % | ||||||||

| 2. | Expeditors International of Washington International Freight Forwarder | 1.2 | % | ||||||||

| 3. | Abercrombie & Fitch Teen Apparel Retailer | 1.2 | % | ||||||||

| 4. | People's Bank of Bridgeport Connecticut Savings & Loan | 1.0 | % | ||||||||

| 5. | Eaton Vance Specialty Mutual Funds | 1.0 | % | ||||||||

| 6. | FMC Technologies Oil & Gas Well Head Manufacturer | 0.9 | % | ||||||||

| 7. | AmeriCredit Auto Lending | 0.9 | % | ||||||||

| 8. | Genlyte Group Commercial Lighting Fixtures | 0.8 | % | ||||||||

| 9. | Ametek Aerospace/Industrial Instruments | 0.8 | % | ||||||||

| 10. | ITT Educational Services Post-secondary Degree Programs | 0.8 | % | ||||||||

The Fund's top 10 holdings and portfolio diversification vary with changes in portfolio investments. See the Statement of Investments for a complete list of the Fund's holdings.

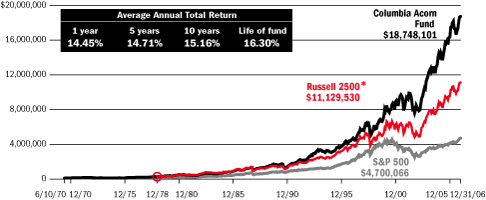

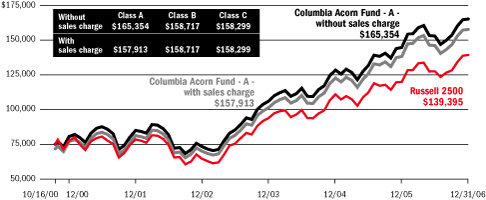

The Growth of a $75,000 Investment in Columbia Acorn Fund (Class Z)

June 10, 1970 through December 31, 2006

This graph compares the results of $75,000 invested in Columbia Acorn Fund at inception on June 10, 1970 to the S&P 500 Index and to an initial $238,325 investment in the Russell 2500 Index on the index's December 31, 1978 inception date. The indexes are unmanaged and returns for both the indexes and the Fund include reinvested dividends and capital gains. It is not possible to invest directly in an index. The graph does not reflect tax deductions that a shareholder would pay on Fund distributions or the sale of Fund shares.

Total Net Assets of the Fund:

$18,945.1 million

*A $75,000 investment in Columbia Acorn Fund at inception appreciated to $238,325 on December 31, 1978, the inception date of the Russell 2500. For comparison with the Russell 2500, we assigned the index the same value as the Fund at index inception.

9

Columbia Acorn International

In a Nutshell

P. Zachary Egan

Co-Portfolio Manager

Louis J. Mendes III

Co-Portfolio Manager

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value of an investment in the Fund will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Performance may reflect any voluntary waivers or reimbursements of fund expenses by the Adviser or its affiliates. Absent these waivers, or reimbursement arrangements, performance results may be lower. Please visit columbiafunds.com for daily and most recent month-end performance updates.

Columbia Acorn International Fund gained 34.53% in 2006, 3.70% ahead of the benchmark S&P/Citigroup EMI Global ex-US Index ("EMI"), and 8.19% ahead of the large-cap MSCI EAFE Index ("EAFE"). During the fourth quarter, the Fund rose 14.45%, ahead of both indexes. Aside from successful stock selection, the Fund's good results were driven by strong returns in Europe, where the Fund maintained a moderate overweight position, and by emerging markets. These areas more than offset declining markets in Japan, where the Fund maintained a slight underweight position. On a sector basis, energy, basic materials and industrials posted strong absolute and relative returns. The weakening U.S. dollar translated into a net gain of 7.50% for shareholders over the course of the year.

For the seventh consecutive year, international small-cap stocks outperformed relative to international large-cap stocks. At this time last year, we noted that the strong price movement of small-cap stocks globally had eroded the valuation discount to larger-caps. We were surprised that, among the regions we track, only Japanese small caps underperformed their large-cap counterparts in both the fourth quarter and the annual period.

In May through July, global small caps exhibited significant volatility. In a context of relatively high valuations, this seems to have been driven by anxiety about the sustainability of U.S. consumption, and the effects a U.S. slowdown would likely have on the global economy. This short-term correction reinforced our conviction that valuation matters a great deal when considering risk, even though many financial market participants look, rather, at historic volatility. It strikes us that higher valuations simply provide a lower margin of safety when making predictions in circumstances fraught with uncertainty.

Emerging markets as a group, which represent less than 20% of the Fund's exposure, posted another strong year, returning over 45%. It is noteworthy that emerging market bond spreads, a key indicator of perceived risk, have narrowed considerably. Whether risk in these markets is in fact lower, due to structural reforms and other factors, or if the lower risk premium simply reflects excess liquidity, remains a hotly contested issue. It is true that we are seeing an ever increasing number of dynamic, entrepreneurial companies coming to the market in industrializing countries, and fulfilling increasingly stringent listing requirements defined by the local exchanges. In Brazil, for example, the Novo Mercado now allows only one class of stock, which confers to minority investors a greater voice in corporate governance than was the case just five years ago, when non-voting preferred shares were commonplace.

We have remarked in past reports that the Japanese market is looking increasingly attractive in terms of valuation and fundamentals. After a strong second half of 2005, the Japanese market did an about face and ended 2006 as the planet's worst-performing major region. The Japan portion of the EMI declined nearly 11% in local currency, and small-cap stocks were hit particularly hard. In our opinion, this has strengthened the valuation argument for Japan. On a price-to-earnings comparison, Japanese small caps are now trading at a reasonable discount both to their average over the last decade (not surprising, given overvaluation), but also to small caps in other markets. The economy is improving, we are seeing reasonable growth in many small-cap companies, and strong balance sheets limit downside risk. Contingent upon our ability to find good investment ideas, we expect to continue moving money into Japanese companies in the course of 2007.

International investments involve greater potential risks, including less regulation, currency fluctuations, economic instability and political developments. Investments in small- and mid-cap companies may be subject to greater volatility and price fluctuations because they may be thinly traded and less liquid.

10

Columbia Acorn International (ACINX)

At a Glance

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value of an investment in the Fund will fluctuate so that Fund shares, when redeemed, may be worth more or less than their original cost. Performance may reflect any voluntary waivers or reimbursements of Fund expenses by the Adviser or its affiliates. Absent these waivers or reimbursement arrangements, performance results may be lower. Visit columbiafunds.com for daily and most recent month-end updates.

Pretax and After-tax Average Annual Total Returns (Class Z)

through December 31, 2006

| Inception 9/23/92 | 1 year | 5 years | 10 years | ||||||||||||

| Returns before taxes | 34.53 | % | 21.35 | % | 13.15 | % | |||||||||

| Returns after taxes on distributions | 32.08 | 20.68 | 12.01 | ||||||||||||

| Returns after taxes on distributions and sale of fund shares | 24.72 | 18.86 | 11.26 | ||||||||||||

| S&P/Citigroup EMI Global ex-US (pretax) | 30.83 | 24.39 | 10.65 | ||||||||||||

After-tax returns are calculated using the highest historical individual federal marginal income tax rates, and do not reflect the impact of state and local taxes. Returns after taxes on distributions and sale of Fund shares reflect the additional tax impact of long-term gains or losses realized when Fund shares are sold. The returns are taxed at the maximum rate and assume shares were purchased at the beginning of the period. Actual after-tax returns depend on the investor's tax situation and may differ from those shown. After-tax returns are not relevant to investors who hold their Fund shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts. After-tax returns are shown for Class Z shares only; after-tax returns for other share classes will vary. Indexes do not reflect any deduction for fees, expenses or taxes.

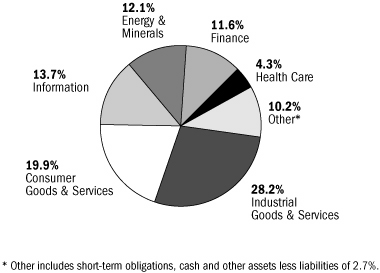

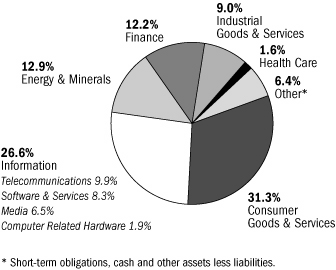

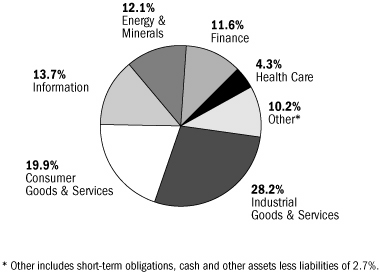

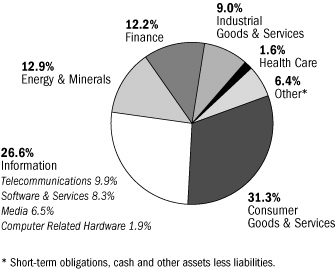

Columbia Acorn International Portfolio Diversification

as a % of net assets as of 12/31/06

Columbia Acorn International Top 10 Holdings

as a % of net assets as of 12/31/06

| 1. | Hexagon (Sweden) Measurement Equipment & Polymers | 1.5 | % | ||||||||

| 2. | Fugro (Netherlands) Oilfield Services | 1.4 | % | ||||||||

| 3. | C&C Group (Ireland) Beverage Company | 1.4 | % | ||||||||

| 4. | Hong Kong Exchanges and Clearing (Hong Kong) Hong Kong Equity & Derivatives Market Operator | 1.3 | % | ||||||||

| 5. | SES Global (France) Satellite Broadcasting Services | 1.2 | % | ||||||||

| 6. | Aalberts Industries (Netherlands) Flow Control & Heat Treatment | 1.1 | % | ||||||||

| 7. | Housing Development Finance (India) Indian Mortgage Lender | 1.1 | % | ||||||||

| 8. | Geberit (Switzerland) Plumbing Supplies | 1.1 | % | ||||||||

| 9. | IAWS Group (Ireland) Baked Goods | 1.1 | % | ||||||||

| 10. | Bank of Ireland (Ireland) Irish Commercial Bank | 1.1 | % | ||||||||

The Fund's top 10 holdings and portfolio diversification vary with changes in portfolio investments. See the Statement of Investments for a complete list of the Fund's holdings.

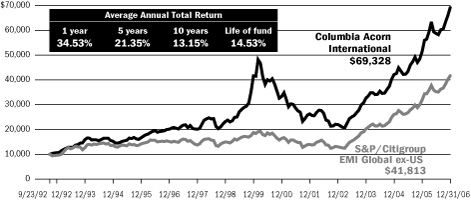

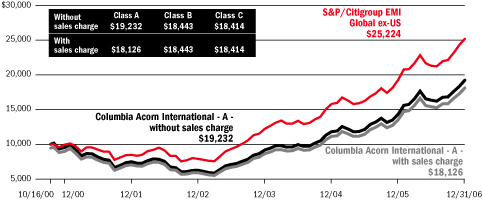

The Growth of a $10,000 Investment in Columbia Acorn International (Class Z)

September 23, 1992 through December 31, 2006

This graph compares the results of $10,000 invested in Columbia Acorn International at inception on September 23, 1992 to the S&P/Citigroup EMI Global ex-US. The index is unmanaged and returns for both the index and Fund include reinvested dividends and capital gains. It is not possible to invest directly in an index. The graph does not reflect tax deductions that a shareholder would pay on Fund distributions or the sale of Fund shares.

Total Net Assets of the Fund:

$4,343.4 million

11

Columbia Acorn USA

In a Nutshell

Robert A. Mohn

Lead Portfolio Manager

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value of an investment in the Fund will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Performance may reflect any voluntary waivers or reimbursements of fund expenses by the Adviser or its affiliates. Absent these waivers, or reimbursement arrangements, performance results may be lower. Please visit columbiafunds.com for daily and most recent month-end performance updates.

Fund's Positions

in Mentioned Holdings

As of 12/31/06, the Fund's positions in the holdings mentioned were:

| Crown Castle International | 2.1 | % | |||||

| Oxford Industries | 2.0 | % | |||||

| Genlyte Group | 1.9 | % | |||||

| Avid Technology | 1.8 | % | |||||

| Time Warner Telecom | 1.8 | % | |||||

| Scotts Miracle-Gro | 1.7 | % | |||||

| World Acceptance | 1.5 | % | |||||

| Pentair | 1.3 | % | |||||

| American Tower | 1.2 | % | |||||

| True Religion Apparel | 0.9 | % | |||||

| Novell | 0.8 | % | |||||

| Chico's FAS | 0.6 | % | |||||

| Christopher & Banks | 0.6 | % | |||||

| CNET Networks | 0.6 | % | |||||

| AnnTaylor Stores | 0.5 | % | |||||

| Neurocrine Biosciences | 0.0 | % | |||||

Portfolio holdings are subject to change periodically and may not be representative of current characteristics and holdings.

Columbia Acorn USA ended the fourth quarter up 4.78%, underperforming the 8.90% gain of the Russell 2000 Index. For the year, the Fund was up 8.28% while the index posted an 18.37% gain. The year ended as it began with a run up in the more speculative companies of the small-cap market. These spikes in lesser quality stocks hurt the Fund's relative performance for the quarter and the year.

The top contributor to Fund gains in the quarter was men's apparel manufacturer Oxford Industries. The stock was up 16% on the strength of its Ben Sherman and Tommy Bahama brands. Lawn and garden products company Scotts Miracle-Gro saw strong revenue growth, and the stock gained 16% in the fourth quarter. Pentair, a maker of pumps and water treatment equipment, rebounded from weak performance earlier in the year. The stock was up 20% in the fourth quarter.

While the quarter produced one retail winner, retailing was more strongly represented on the losers list. Women's retailers Christopher & Banks, True Religion Apparel and AnnTaylor Stores were down between 20% and 37% in the quarter. While True Religion, a maker of premium denim products, has seen nice sales in the U.S. market, distribution snafus hurt sales in Japan. Christopher & Banks and AnnTaylor both produced fall lines that didn't take off with customers, hurting sales.

For the year, telecom stocks were the biggest positive contributors to performance. Time Warner Telecom, an owner of fiber optic networks connected to over 6,000 office buildings, was up 103% on strong sales growth. Cellular tower companies Crown Castle International and American Tower also posted strong annual gains, up 20% and 38%, respectively. As cellular minute usage grows, cellular service providers continue to turn to these companies for antenna space.

Outside the telecom sector, lender World Acceptance was up 65% for the year as credit losses fell and loan growth increased. Genlyte Group, a maker of commercial lighting fixtures, was up 46% as non-residential construction increased, driving demand for its products.

Technology and health care stocks were among the laggards for the year. Neurocrine Biosciences was the worst performer, falling 65% before we sold it. The stock collapsed when the FDA withheld full approval of its high dosage sleep medication Indiplon. CNET Networks, a provider of software product reviews on technology websites, was down 39% in the Fund for the year. CNET's business is driven by new product launches, and two highly anticipated product launches, Microsoft's Vista and Sony's PlayStation 3, were tardy. Avid Technology, a provider of digital editing software and systems, fell more than 30% in part because broadcasters have been slow to upgrade to digital. Software company Novell fell 30% in the year as the company's transition to open source software is taking longer than the market expected. Outside the health care and technology sectors, retailer Chico's FAS missed the mark with its customers this year, sending th e stock down roughly 55%.

It tended to pay to disregard risk in 2006. Risky securities such as micro-caps, commodities, emerging markets and complex investment bank-bred derivatives were the big winners. To the daredevils went the spoils. But we believe risk still matters (remember, Evel Knievel occasionally crashed). Our preferred method of managing your Fund's risk level is to stock it with well-capitalized, small-cap businesses possessing long-term economic advantages and trading in the market at sensible prices.

Risks include stock market fluctuations due to economic and business developments. Investments in small- and mid-cap companies may be subject to greater volatility and price fluctuations because they may be thinly traded and less liquid.

12

Columbia Acorn USA (AUSAX)

At a Glance

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value of an investment in the Fund will fluctuate so that Fund shares, when redeemed, may be worth more or less than their original cost. Performance may reflect any voluntary waivers or reimbursements of Fund expenses by the Adviser or its affiliates. Absent these waivers or reimbursement arrangements, performance results may be lower. Visit columbiafunds.com for daily and most recent month-end updates.

Pretax and After-tax Average Annual Total Returns (Class Z)

through December 31, 2006

| Inception 9/4/96 | 1 year | 5 years | 10 years | ||||||||||||

| Returns before taxes | 8.28 | % | 12.09 | % | 12.70 | % | |||||||||

| Returns after taxes on distributions | 7.94 | 11.83 | 12.00 | ||||||||||||

| Returns after taxes on distributions and sale of fund shares | 5.83 | 10.57 | 11.05 | ||||||||||||

| Russell 2000 (pretax) | 18.37 | 11.39 | 9.44 | ||||||||||||

After-tax returns are calculated using the highest historical individual federal marginal income tax rates, and do not reflect the impact of state and local taxes. Returns after taxes on distributions and sale of Fund shares reflect the additional tax impact of long-term gains or losses realized when Fund shares are sold. The returns are taxed at the maximum rate and assume shares were purchased at the beginning of the period. Actual after-tax returns depend on the investor's tax situation and may differ from those shown. After-tax returns are not relevant to investors who hold their Fund shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts. After-tax returns are shown for Class Z shares only; after-tax returns for other share classes will vary. Indexes do not reflect any deduction for fees, expenses or taxes.

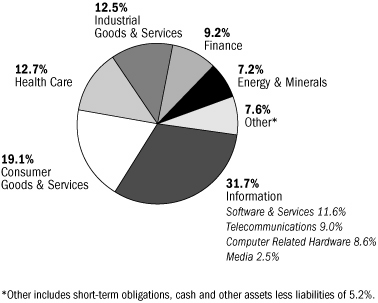

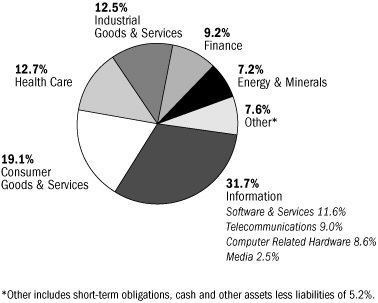

Columbia Acorn USA Portfolio Diversification

as a % of net assets as of 12/31/06

Columbia Acorn USA Top 10 Holdings

as a % of net assets as of 12/31/06

| 1. | Crown Castle International Communication Towers | 2.1 | % | ||||||||

| 2. | Oxford Industries Branded & Private Label Apparel | 2.0 | % | ||||||||

| 3. | Genlyte Group Commercial Lighting Fixtures | 1.9 | % | ||||||||

| 4. | Avid Technology Digital Nonlinear Editing Software & Systems | 1.8 | % | ||||||||

| 5. | AmeriCredit Auto Lending | 1.8 | % | ||||||||

| 6. | Abercrombie & Fitch Teen Apparel Retailer | 1.8 | % | ||||||||

| 7. | Time Warner Telecom Fiber Optic Telephone/Data Services | 1.8 | % | ||||||||

| 8. | ITT Educational Services Post-secondary Degree Programs | 1.8 | % | ||||||||

| 9. | Scotts Miracle-Gro Consumer Lawn & Garden Products | 1.7 | % | ||||||||

| 10. | Edwards Lifesciences Heart Valves | 1.7 | % | ||||||||

The Fund's top 10 holdings and portfolio diversification vary with changes in portfolio investments. See the Statement of Investments for a complete list of the Fund's holdings.

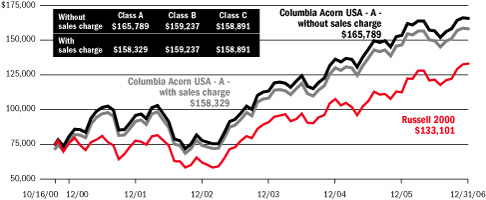

The Growth of a $75,000 Investment in Columbia Acorn USA (Class Z)

September 4, 1996 through December 31, 2006

This graph compares the results of $75,000 invested in Columbia Acorn USA at inception on September 4, 1996 to the Russell 2000 Index. The index is unmanaged and returns for both the index and the Fund include reinvested dividends and capital gains. It is not possible to invest directly in an index. The graph does not reflect tax deductions that a shareholder would pay on Fund distributions or the sale of Fund shares.

Total Net Assets of the Fund:

$1,580.2 million

13

Columbia Acorn International Select

In a Nutshell

Christopher J. Olson

Lead Portfolio Manager

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value of an investment in the Fund will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Performance may reflect any voluntary waivers or reimbursements of fund expenses by the Adviser or its affiliates. Absent these waivers, or reimbursement arrangements, performance results may be lower. Please visit columbiafunds.com for daily and most recent month-end performance updates.

Fund's Positions

in Mentioned Holdings

As of 12/31/06, the Fund's positions in the holdings mentioned were:

| C&C Group | 5.3 | % | |||||

| Hong Kong Exchanges and Clearing | 3.2 | % | |||||

| IAWS Group | 2.3 | % | |||||

| Daito Trust Construction | 1.8 | % | |||||

| Kenedix | 1.8 | % | |||||

| Sparx Asset Management | 0.0 | % | |||||

Portfolio holdings are subject to change periodically and may not be representative of current characteristics and holdings.

Columbia Acorn International Select gained an impressive 13.06% in the fourth quarter and ended 2006 with a 36.27% gain. The Fund outperformed its benchmark, the S&P/Citigroup World ex-US Cap Range $2-10B Index, for both time periods. The index was up 11.32% for the quarter and 27.88% for the year. Outperformance was strong in a number of areas, particularly Ireland and Hong Kong where the Fund was overweight. In a reversal from last year, the weakest market was Japan. The Fund was underweight in this market throughout the year.

The top three contributors to Fund performance in the quarter and the year were the same. Irish beverage company C&C Group gained another 32% in the fourth quarter and ended the year up 159%. Strong sales and a well received launch of its cider product in the United Kingdom resulted in dramatic earnings upgrades. Hong Kong Exchanges and Clearing was ranked second for the quarter and year. The company operates the Hong Kong equity and derivatives market and rose 49% in the quarter and posted an annual gain of 171% in the Fund. Increased trading volume and new stock listings from China drove this stock's stellar performance. Rounding out the top three, Ireland's IAWS Group, a manufacturer and distributor of baked goods, increased 38% in the fourth quarter and ended the year up 80%. The stock benefited from strong performance in its baked goods divisions and from the acquisition of Otis Spunkmeyer, a U.S. cookie dough manufactu rer.

Even in such a strong year, there were some stocks that detracted from performance and, as was the case at mid-year, the common thread was Japan. In a year where the Fund was up over 36%, both the Fund's Japanese portfolio and the Japanese weighting in its benchmark index were essentially flat. Daito Trust Construction, a developer of apartment and condo buildings in Japan, fell 16% in the quarter and was down nearly 11% for the year. The stock fell as new construction orders slowed when it switched to a new order system. In the fourth quarter, fund manager Sparx Asset Management fell 29%. We opted to sell the stock as we became concerned about its higher cost base resulting from a recent acquisition. Kenedix, a Japanese real estate investment manager, fell 22% in the quarter despite earnings upgrades as investors became concerned about possible interest rate increases in Japan.

International mid-cap stocks have had a strong run for the last five years, which likely has some investors questioning how much steam is left in these names. While we can't predict the future, we are still finding attractively valued stocks to include in Columbia Acorn International Select.

International investments involve greater potential risks, including less regulation, currency fluctuations, economic instability and political developments. Investments in small- and mid-cap companies may be subject to greater volatility and price fluctuations because they may be thinly traded and less liquid. By maintaining a relatively concentrated portfolio, the fund may be subject to greater risk than a fund that is more fully diversified.

14

Columbia Acorn International Select (ACFFX)

At a Glance

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value of an investment in the Fund will fluctuate so that Fund shares, when redeemed, may be worth more or less than their original cost. Performance may reflect any voluntary waivers or reimbursements of Fund expenses by the Adviser or its affiliates. Absent these waivers or reimbursement arrangements, performance results may be lower. Visit columbiafunds.com for daily and most recent month-end updates.

Pretax and After-tax Average Annual Total Returns (Class Z)

through December 31, 2006

| Inception 11/23/98 | 1 year | 5 years | Life of fund | ||||||||||||

| Returns before taxes | 36.27 | % | 18.81 | % | 14.07 | % | |||||||||

| Returns after taxes on distributions | 36.16 | 18.81 | 14.00 | ||||||||||||

| Returns after taxes on distributions and sale of fund shares | 23.56 | 16.73 | 12.60 | ||||||||||||

| S&P/Citigroup World ex-US Cap Range $2-10B (pretax) | 27.88 | 21.24 | 12.81 | ||||||||||||

After-tax returns are calculated using the highest historical individual federal marginal income tax rates, and do not reflect the impact of state and local taxes. Returns after taxes on distributions and sale of Fund shares reflect the additional tax impact of long-term gains or losses realized when Fund shares are sold. The returns are taxed at the maximum rate and assume shares were purchased at the beginning of the period. Actual after-tax returns depend on the investor's tax situation and may differ from those shown. After-tax returns are not relevant to investors who hold their Fund shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts. After-tax returns are shown for Class Z shares only; after-tax returns for other share classes will vary. Indexes do not reflect any deduction for fees, expenses or taxes.

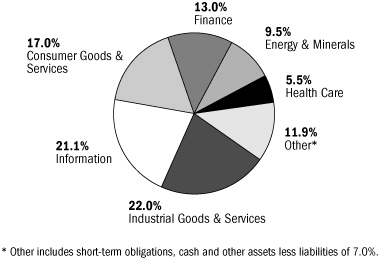

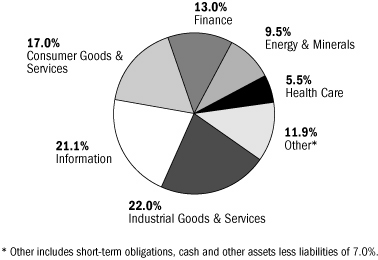

Columbia Acorn International Select Portfolio Diversification

as a % of net assets as of 12/31/06

Columbia Acorn International Select Top 10

Holdings as a % of net assets as of 12/31/06

| 1. | C&C Group (Ireland) Beverage Company | 5.3% | |||||||||

| 2. | Bank of Ireland (Ireland) Irish Commercial Bank | 4.1% | |||||||||

| 3. | Anglo Irish Bank (Ireland) Small Business & Middle Market Banking | 3.7% | |||||||||

| 4. | Synthes (Switzerland) Products for Orthopedic Surgery | 3.3% | |||||||||

| 5. | Hong Kong Exchanges and Clearing (Hong Kong) Hong Kong Equity & Derivatives Market Operator | 3.2% | |||||||||

| 6. | Northern Rock (United Kingdom) Lowest Cost Mortgage Bank in UK | 2.9% | |||||||||

| 7. | Alliance Atlantis Communication (Canada) CATV Channels, TV/Movie Production/Distribution | 2.9% | |||||||||

| 8. | Jupiter Telecommunications (Japan) Largest Cable Service Provider in Japan | 2.9% | |||||||||

| 9. | Red Electrica de Espana (Spain) Spanish Power Grid | 2.7% | |||||||||

| 10. | Aeon Mall (Japan) Suburban Shopping Mall Developer, Owner & Operator | 2.7% | |||||||||

The Fund's top 10 holdings and portfolio diversification vary with changes in portfolio investments. See the Statement of Investments for a complete list of the Fund's holdings.

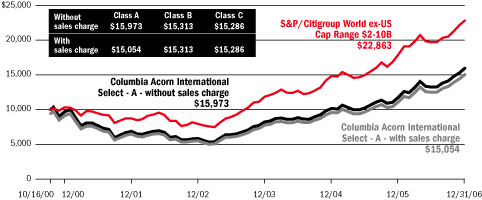

The Growth of a $10,000 Investment in Columbia Acorn International Select (Class Z)

November 23, 1998 through December 31, 2006

This graph compares the results of $10,000 invested in Columbia Acorn International Select at inception on November 23, 1998 to the S&P/Citigroup World ex-US Cap Range $2-10B Index. The index and Fund returns include reinvested dividends and capital gains. It is not possible to invest directly in an index. The graph does not reflect tax deductions that a shareholder would pay on Fund distributions or the sale of Fund shares.

Total Net Assets of the Fund: $168.9 million

15

Columbia Acorn Select

In a Nutshell

Ben Andrews

Lead Portfolio Manager

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value of an investment in the Fund will fluctuate so that shares, when redeemed, may be worth more or less than the original cost. Performance may reflect any voluntary waivers or reimbursements of fund expenses by the Adviser or its affiliates. Absent these waivers, or reimbursement arrangements, performance results may be lower. Please visit columbiafunds.com for daily and most recent month-end performance updates.

Fund's Positions

in Mentioned Holdings

As of 12/31/06, the Fund's positions in the holdings mentioned were:

| UrAsia Energy | 6.2 | % | |||||

| Safeway | 5.5 | % | |||||

| Liberty Global | 4.7 | % | |||||

| American Tower | 3.8 | % | |||||

| Avid Technology | 3.7 | % | |||||

| Potash | 3.1 | % | |||||

| Career Education | 0.0 | % | |||||

| Mine Safety Appliances | 0.0 | % | |||||

Portfolio holdings are subject to change periodically and may not be representative of current characteristics and holdings.

Columbia Acorn Select returned 10.51% during the quarter, ahead of the S&P MidCap 400's 6.99% and the S&P 500's 6.70% gains. For 2006, the Fund was up 19.68%, ahead of the S&P MidCap 400's 10.32% and the S&P 500's 15.79% gains. In the fourth quarter of 2005 we stated that our goal for 2006 was to outperform the Fund's benchmark index as well as provide a positive return for shareholders. We are happy to say that we delivered on both.

UrAsia Energy led the way with a 149% gain in the Fund for the year as uranium prices reached a record of $70 per pound vs. $36 at the end of 2005. The recent flooding of competitor Cameco's Cigar Lake Mine caused part of the price jump. Cameco announced that its initial predicted production of eight million lbs/yr (5% of world demand) would be delayed by at least one year. Production of uranium at Cigar Lake was forecasted to begin in early 2008 and utilities were counting on the new supply to meet the growing demand for fuel to run nuclear reactors. While Cameco expects the mine may eventually produce 18 million lbs/yr, if it faces longer production delays than it anticipates, uranium prices could remain high, benefiting UrAsia.

On the downside, Avid Technology, which lagged all year, fell 32% (or reduced the Fund's return by 1.28%) as the company guided sales and earnings down for 2006 due to delayed products and an acquisition that needed resuscitation. While obviously disappointed, we believe the long-term outlook remains sound and we added to the Fund's position in the stock. Avid is a leader in digital editing software and systems used by the film and news industries. Additionally, we believe that Avid has the potential to become a leader in consumer video and audio editing in the next few years. Over the last decade, consumer competition has dwindled while product demand has increased. We believe that this nascent market should give Avid an opportunity for solid revenue growth.

Most other losses for the year were relatively small in position size or percentages. In fact, all losses combined for the year took away just 3.83% from Fund gains. On the up side, the five top winners (UrAsia Energy, Safeway, Liberty Global, Potash, and American Tower) accounted for 11.59% of the Fund's 19.68% return.

In the quarter we sold two positions, Career Education and Mine Safety Appliances, while we purchased five new stocks. A couple of these new positions are small as we continue to determine if our theories for ownership are correct. If our confidence builds, so might these positions, otherwise we will likely exit.

As we enter 2007, we see plenty of what we consider to be positive signs: falling oil prices, low inflation rates despite a sharp run up in raw materials (perhaps due to the outsourcing of labor), 10-year treasury yields (though off their bottom) near historical lows, and a rebounding dollar. But we believe that there are plenty of troubling signs as well. We get nervous when the most popular investments are emerging market debt, obscure credit derivatives, and private equity, which are leading a buyout frenzy funded with debt. As always, our primary focus is to beat the Fund's benchmark despite all the macroeconomic noise.

Risks of owning the Fund include stock market fluctuations due to economic and business developments and potentially greater price volatility due to the Fund's concentration in a limited number of stocks of mid-size companies.

16

Columbia Acorn Select (ACTWX)

At a Glance

Performance data quoted represents past performance and current performance may be lower or higher. Past performance is no guarantee of future results. The investment return and principal value of an investment in the Fund will fluctuate so that Fund shares, when redeemed, may be worth more or less than their original cost. Performance may reflect any voluntary waivers or reimbursements of Fund expenses by the Adviser or its affiliates. Absent these waivers or reimbursement arrangements, performance results may be lower. Visit columbiafunds.com for daily and most recent month-end updates.

Pretax and After-tax Average Annual Total Returns (Class Z)

through December 31, 2006