UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Quarterly Period Ended September 30, 2024

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Transition Period from to

COMMISSION FILE NUMBER: 000-16509

| | |

| CITIZENS, INC. |

| (Exact name of registrant as specified in its charter) |

| | | | | |

| Colorado | 84-0755371 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

11815 Alterra Pkwy, Floor 15, Austin, TX 78758

(Current Address)

Registrant's telephone number, including area code: (512) 837-7100

| | | | | | | | |

| Securities registered pursuant to Section 12(b) of the Act |

|

| Class A Common Stock | CIA | NYSE |

| (Title of each class) | (Trading symbol(s)) | (Name of each exchange on which registered) |

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes o No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). x Yes o No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company" and "emerging growth company" in Rule 12b-2 of the Exchange Act:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Large accelerated filer | ☐ | | Accelerated filer | ☒ | | Non-accelerated filer | ☐ | | Smaller reporting company | ☒ | | Emerging growth company | ☐ | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes x No

As of November 1, 2024, the Registrant had 49,906,575 shares of Class A common stock outstanding.

THIS PAGE INTENTIONALLY LEFT BLANK

TABLE OF CONTENTS | | | | | | | | | | | |

| | | Page Number |

| Part I. FINANCIAL INFORMATION | |

| | | |

| | Item 1. | | |

| | | |

| | | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | | |

| | | |

| | | | |

| | | |

| | Item 2. | | |

| | | |

| | Item 3. | | |

| | | |

| | Item 4. | | |

| | | |

| Part II. OTHER INFORMATION | |

| | | |

| | Item 1. | | |

| | | |

| Item 1A. | | |

| | | |

| | Item 2. | | |

| | | |

| | Item 3. | | |

| | | |

| | Item 4. | | |

| | | |

| | Item 5. | | |

| | | |

| | Item 6. | | |

September 30, 2024 | 10-Q 1

PART I. FINANCIAL INFORMATION

Item 1. FINANCIAL STATEMENTS

CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES

Consolidated Balance Sheets | | | | | | | | | | | |

| | | |

| | | |

| (In thousands) | September 30, 2024 | | December 31, 2023 |

| (Unaudited) | | |

| Assets: | | | |

| Investments: | | | |

| Fixed maturity securities available-for-sale, at fair value (amortized cost: $1,391,580 and $1,389,038 in 2024 and 2023, respectively) | $ | 1,273,497 | | | 1,238,981 | |

| | | |

| Equity securities, at fair value | 5,716 | | | 5,282 | |

| | | |

| Policy loans | 72,463 | | | 75,359 | |

| | | |

| | | |

| Other long-term investments (portion measured at fair value $93,167 and $82,460 in 2024 and 2023, respectively) | 93,433 | | | 82,725 | |

| | | |

| Total investments | 1,445,109 | | | 1,402,347 | |

| Cash and cash equivalents | 32,382 | | | 26,997 | |

| Accrued investment income | 17,082 | | | 17,360 | |

| | | |

| Reinsurance recoverable | 7,278 | | | 3,991 | |

| Deferred policy acquisition costs | 192,268 | | | 175,768 | |

| Cost of insurance acquired | 9,566 | | | 10,043 | |

| Current federal income tax receivable | 505 | | | 1,546 | |

| | | |

| Property and equipment, net | 10,975 | | | 11,809 | |

| Due premiums | 10,090 | | | 11,264 | |

| | | |

| Other assets (less allowance for losses of $574 and $408 in 2024 and 2023, respectively) | 10,554 | | | 7,803 | |

| Total assets | $ | 1,735,809 | | | 1,668,928 | |

See accompanying Notes to Consolidated Financial Statements.

September 30, 2024 | 10-Q 2

CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES

Consolidated Balance Sheets, Continued

| | | | | | | | | | | |

| | | |

| | | |

| (In thousands, except share amounts) | September 30, 2024 | | December 31, 2023 |

| (Unaudited) | | |

| Liabilities and Stockholders' Equity: | | | |

| Liabilities: | | | |

| Policy liabilities: | | | |

| Future policy benefit reserves: | | | |

| Life insurance | $ | 1,236,873 | | | 1,229,253 | |

| Accident and health insurance | 998 | | | 889 | |

| Total future policy benefit reserves | 1,237,871 | | | 1,230,142 | |

| Policyholders' funds: | | | |

| Annuities | 145,838 | | | 133,216 | |

| Dividend accumulations | 47,052 | | | 44,960 | |

| Premiums paid in advance | 32,420 | | | 32,446 | |

| Policy claims payable | 9,236 | | | 6,637 | |

| Other policyholders' funds | 7,076 | | | 7,363 | |

| Total policyholders' funds | 241,622 | | | 224,622 | |

| Total policy liabilities | 1,479,493 | | | 1,454,764 | |

| Commissions payable | 3,843 | | | 3,445 | |

| | | |

| Deferred federal income tax liability | 2,367 | | | 1,102 | |

| | | |

| Other liabilities | 42,533 | | | 37,488 | |

| Total liabilities | 1,528,236 | | | 1,496,799 | |

Commitments and contingencies (Notes 7 and 8) | | | |

| Stockholders' Equity: | | | |

| Common stock: | | | |

| Class A, no par value, 100,000,000 shares authorized, 54,222,644 and 53,882,661 shares issued and outstanding in 2024 and 2023, respectively, including shares in treasury of 4,327,810 in 2024 and 2023 | 269,356 | | | 268,675 | |

| Class B, no par value, 2,000,000 shares authorized, 1,001,714 shares issued and outstanding in 2024 and 2023, including shares in treasury of 1,001,714 in 2024 and 2023 | 3,184 | | | 3,184 | |

| Retained earnings | 53,441 | | | 42,150 | |

| Accumulated other comprehensive income (loss) | (94,683) | | | (118,155) | |

| Treasury stock, at cost | (23,725) | | | (23,725) | |

| Total stockholders' equity | 207,573 | | | 172,129 | |

| Total liabilities and stockholders' equity | $ | 1,735,809 | | | 1,668,928 | |

See accompanying Notes to Consolidated Financial Statements.

September 30, 2024 | 10-Q 3

CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES

Consolidated Statements of Operations and Comprehensive Income (Loss)

(Unaudited)

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| Three Months Ended | | Nine Months Ended |

| September 30, | | September 30, |

| (In thousands, except per share amounts) | 2024 | | 2023 | | 2024 | | 2023 |

| Revenues: | | | | | | | |

| Premiums: | | | | | | | |

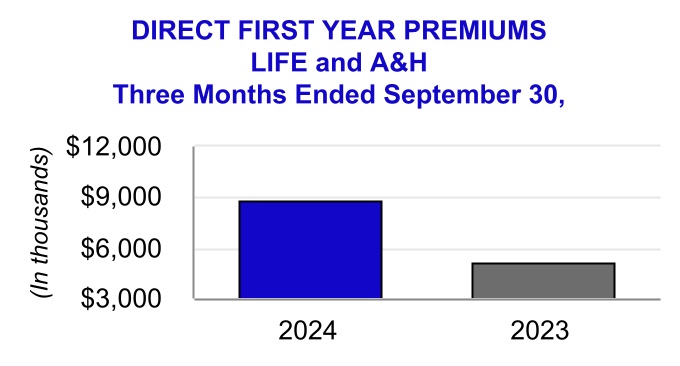

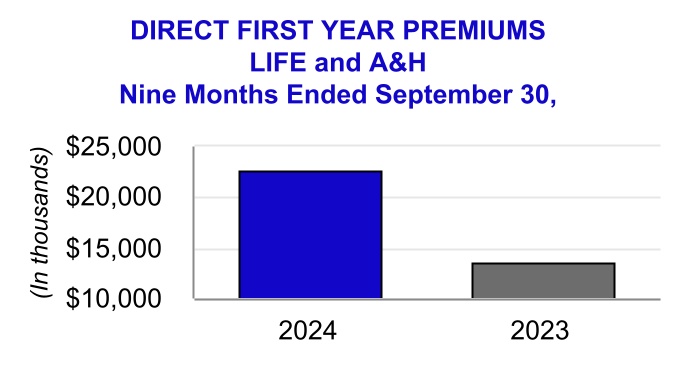

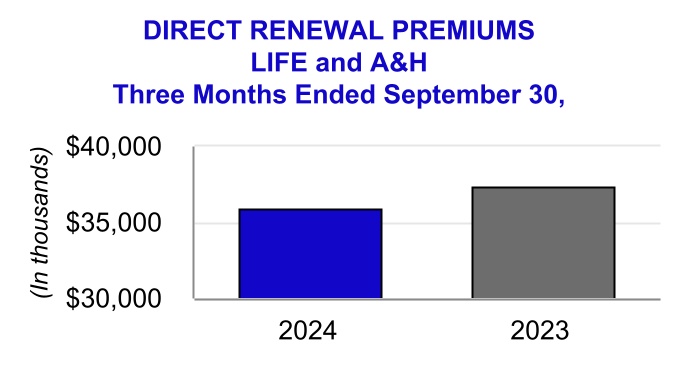

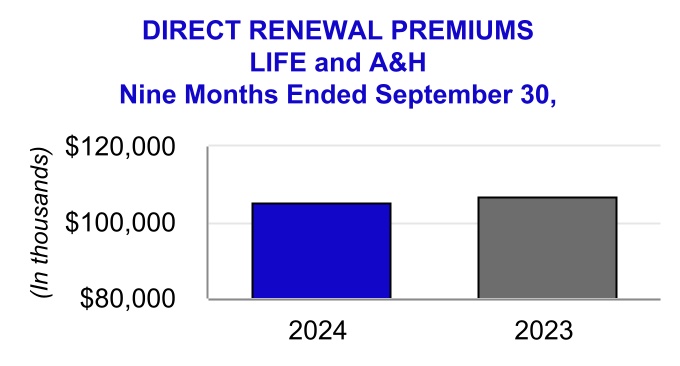

| Life insurance | $ | 42,461 | | | 41,794 | | | 122,823 | | | 118,020 | |

| Accident and health insurance | 452 | | | 296 | | | 1,324 | | | 1,201 | |

| Property insurance | (16) | | | (64) | | | (18) | | | 780 | |

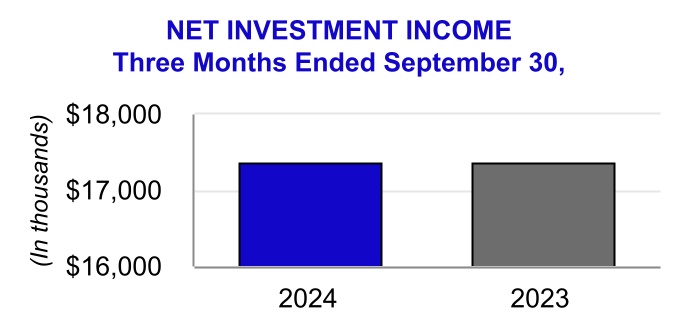

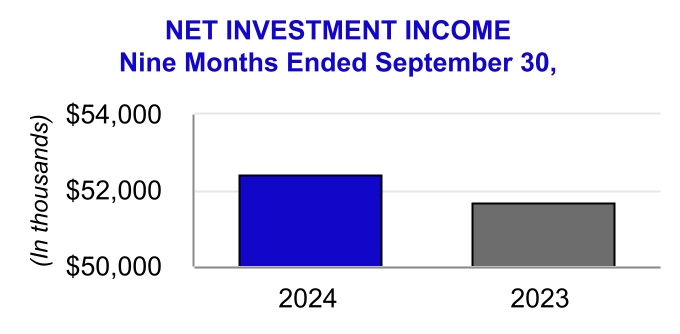

| Net investment income | 17,377 | | | 17,372 | | | 52,404 | | | 51,687 | |

| Investment related gains (losses), net | 827 | | | (892) | | | 1,537 | | | (477) | |

| Other income | 630 | | | 884 | | | 3,457 | | | 2,620 | |

| Total revenues | 61,731 | | | 59,390 | | | 181,527 | | | 173,831 | |

| Benefits and Expenses: | | | | | | | |

| Insurance benefits paid or provided: | | | | | | | |

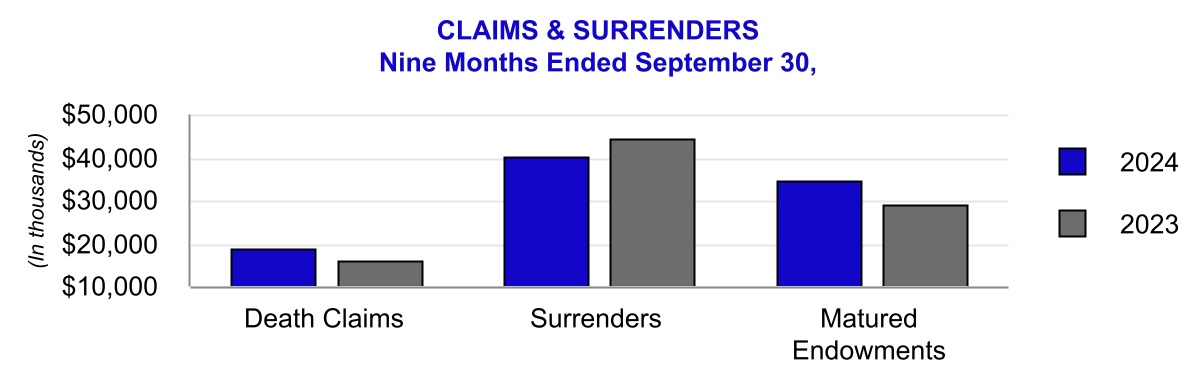

| Claims and surrenders | 36,478 | | | 37,723 | | | 104,121 | | | 100,798 | |

| Increase (decrease) in future policy benefit reserves | 471 | | | (3,880) | | | (130) | | | (5,802) | |

| Policyholder liability remeasurement (gain) loss | 1,157 | | | 1,024 | | | 2,836 | | | 2,860 | |

| Policyholders' dividends | 1,320 | | | 1,414 | | | 3,748 | | | 3,783 | |

| Total insurance benefits paid or provided | 39,426 | | | 36,281 | | | 110,575 | | | 101,639 | |

| | | | | | | |

| Commissions | 12,957 | | | 9,444 | | | 35,639 | | | 27,340 | |

| Other general expenses | 12,095 | | | 11,949 | | | 40,072 | | | 35,477 | |

| Capitalization of deferred policy acquisition costs | (10,430) | | | (7,132) | | | (29,304) | | | (20,034) | |

| Amortization of deferred policy acquisition costs | 4,493 | | | 4,056 | | | 12,804 | | | 11,544 | |

| Amortization of cost of insurance acquired | 153 | | | 151 | | | 477 | | | 465 | |

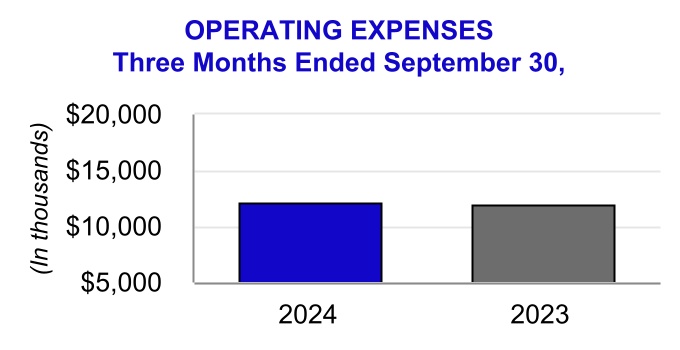

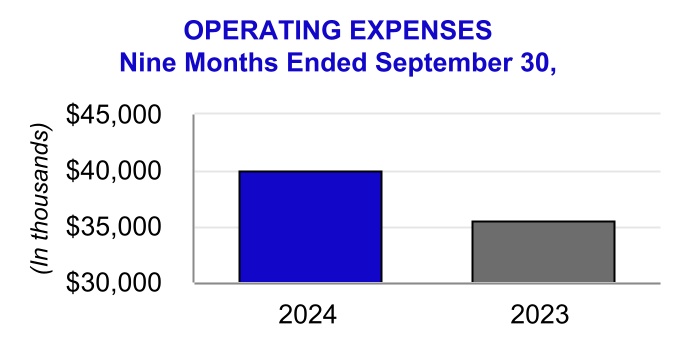

| Total benefits and expenses | 58,694 | | | 54,749 | | | 170,263 | | | 156,431 | |

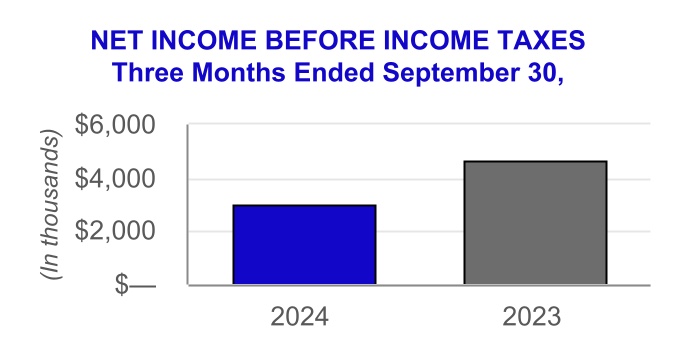

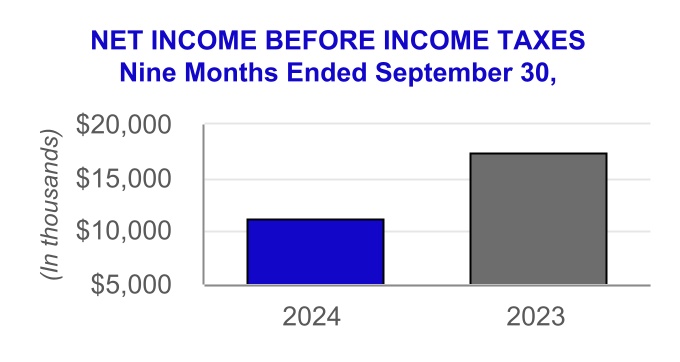

| Income before federal income tax | 3,037 | | | 4,641 | | | 11,264 | | | 17,400 | |

| Federal income tax expense (benefit) | 247 | | | 1,943 | | | (27) | | | 3,704 | |

| Net income | 2,790 | | | 2,698 | | | 11,291 | | | 13,696 | |

| | | | | | | |

| Per Share Amounts: | | | | | | | |

| Basic earnings per share of Class A common stock | 0.06 | | | 0.06 | | | 0.23 | | | 0.28 | |

| Diluted earnings per share of Class A common stock | 0.05 | | | 0.05 | | | 0.22 | | | 0.27 | |

| | | | | | | |

| Other Comprehensive Income (Loss): | | | | | | | |

| | | | | | | |

| Unrealized gains (losses) on fixed maturity securities: | | | | | | | |

| Unrealized holding gains (losses) arising during period | 59,101 | | | (59,817) | | | 31,427 | | | (36,811) | |

| Reclassification adjustment for losses (gains) included in net income | (100) | | | 419 | | | 547 | | | 481 | |

| Unrealized gains (losses) on fixed maturity securities, net | 59,001 | | | (59,398) | | | 31,974 | | | (36,330) | |

| Change in current discount rate for liability for future policy benefits | (45,404) | | | 60,054 | | | (5,887) | | | 45,825 | |

| Income tax expense (benefit) on other comprehensive income items | 356 | | | (1,040) | | | 2,615 | | | (882) | |

| Other comprehensive income (loss) | 13,241 | | | 1,696 | | | 23,472 | | | 10,377 | |

| Total comprehensive income (loss) | $ | 16,031 | | | 4,394 | | | 34,763 | | | 24,073 | |

See accompanying Notes to Consolidated Financial Statements.

September 30, 2024 | 10-Q 4

CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES

Consolidated Statements of Stockholders' Equity

(Unaudited) | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

| | | | | | |

| | Common Stock | Retained Earnings | Accumulated Other Comprehensive Income (Loss) | Treasury Stock | Total Stockholders' Equity |

| (In thousands) | Class A | Class B |

| | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | |

| | | | | | | |

| | | | | | | | | | |

| Balance at December 31, 2023 | $ | 268,675 | | | 3,184 | | | 42,150 | | | (118,155) | | | (23,725) | | | 172,129 | |

| Comprehensive income (loss): | | | | | | | | | | | |

| Net income | — | | | — | | | 4,542 | | | — | | | — | | | 4,542 | |

| Other comprehensive income (loss) | — | | | — | | | — | | | 18,385 | | | — | | | 18,385 | |

| Total comprehensive income (loss) | — | | | — | | | 4,542 | | | 18,385 | | | — | | | 22,927 | |

| | | | | | | | | | | |

| Stock-based compensation | 127 | | | — | | | — | | | — | | | — | | | 127 | |

| Balance at March 31, 2024 | 268,802 | | | 3,184 | | | 46,692 | | | (99,770) | | | (23,725) | | | 195,183 | |

| Comprehensive income (loss): | | | | | | | | | | | |

| Net income | — | | | — | | | 3,959 | | | — | | | — | | | 3,959 | |

| Other comprehensive income (loss) | — | | | — | | | — | | | (8,154) | | | — | | | (8,154) | |

| Total comprehensive income (loss) | — | | | — | | | 3,959 | | | (8,154) | | | — | | | (4,195) | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| Stock-based compensation | 481 | | | — | | | — | | | — | | | — | | | 481 | |

| Balance at June 30, 2024 | 269,283 | | | 3,184 | | | 50,651 | | | (107,924) | | | (23,725) | | | 191,469 | |

| Comprehensive income (loss): | | | | | | | | | | | |

| Net income | — | | | — | | | 2,790 | | | — | | | — | | | 2,790 | |

| Other comprehensive income (loss) | — | | | — | | | — | | | 13,241 | | | — | | | 13,241 | |

| Total comprehensive income (loss) | — | | | — | | | 2,790 | | | 13,241 | | | — | | | 16,031 | |

| | | | | | | | | | | |

| Stock-based compensation | 73 | | | — | | | — | | | — | | | — | | | 73 | |

| Balance at September 30, 2024 | $ | 269,356 | | | 3,184 | | | 53,441 | | | (94,683) | | | (23,725) | | | 207,573 | |

See accompanying Notes to Consolidated Financial Statements.

September 30, 2024 | 10-Q 5

CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES

Consolidated Statements of Stockholders' Equity, Continued

(Unaudited) | | | | | | | | | | | | | | | | | | | | |

| | | | | | |

| | | | | | |

| | Common Stock | Retained Earnings | Accumulated Other Comprehensive Income (Loss) | Treasury Stock | Total Stockholders' Equity |

| (In thousands) | Class A | Class B |

| | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

|

|

|

| | | | | | | | | | | |

| | | | | |

| | | |

| | | | | | | | | | | |

| Balance at December 31, 2022 | $ | 268,147 | | | 3,184 | | | 16,309 | | | (137,044) | | | (22,806) | | | 127,790 | |

| Comprehensive income (loss): | | | | | | | | | | | |

| Net income | — | | | — | | | 4,872 | | | — | | | — | | | 4,872 | |

| Other comprehensive income (loss) | — | | | — | | | — | | | 21,579 | | | — | | | 21,579 | |

| Total comprehensive income (loss) | — | | | — | | | 4,872 | | | 21,579 | | | — | | | 26,451 | |

| | | | | | | | | | | |

| Stock-based compensation | 50 | | | — | | | — | | | — | | | — | | | 50 | |

| Balance at March 31, 2023 | 268,197 | | | 3,184 | | | 21,181 | | | (115,465) | | | (22,806) | | | 154,291 | |

| Comprehensive income (loss): | | | | | | | | | | | |

| Net income | — | | | — | | | 6,126 | | | — | | | — | | | 6,126 | |

| Other comprehensive income (loss) | — | | | — | | | — | | | (12,898) | | | — | | | (12,898) | |

| Total comprehensive income (loss) | — | | | — | | | 6,126 | | | (12,898) | | | — | | | (6,772) | |

| | | | | | | | | | | |

| Acquisition of treasury stock | — | | | — | | | — | | | — | | | (719) | | | (719) | |

| Stock-based compensation | 46 | | | — | | | — | | | — | | | — | | | 46 | |

| Balance at June 30, 2023 | 268,243 | | | 3,184 | | | 27,307 | | | (128,363) | | | (23,525) | | | 146,846 | |

| Comprehensive income (loss): | | | | | | | | | | | |

| Net income | — | | | — | | | 2,698 | | | — | | | — | | | 2,698 | |

| Other comprehensive income (loss) | — | | | — | | | — | | | 1,696 | | | — | | | 1,696 | |

| Total comprehensive income (loss) | — | | | — | | | 2,698 | | | 1,696 | | | — | | | 4,394 | |

| | | | | | | | | | | |

| Stock-based compensation | 180 | | | — | | | — | | | — | | | — | | | 180 | |

Other 1 | — | | | — | | | 1,327 | | | — | | | — | | | 1,327 | |

| Balance at September 30, 2023 | $ | 268,423 | | | 3,184 | | | 31,332 | | | (126,667) | | | (23,525) | | | 152,747 | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

See accompanying Notes to Consolidated Financial Statements.

September 30, 2024 | 10-Q 6

CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES

Consolidated Statements of Cash Flows

(Unaudited)

| | | | | | | | | | | |

Nine Months Ended September 30, (In thousands) | 2024 | | 2023 |

| Cash flows from operating activities: | | | |

| Net income | $ | 11,291 | | | 13,696 | |

| Adjustments to reconcile net income to net cash provided by operating activities: | | | |

| Investment related (gains) losses on sale of investments and other assets, net | (1,537) | | | 477 | |

| Net deferred policy acquisition costs | (16,500) | | | (8,490) | |

| Amortization of cost of insurance acquired | 477 | | | 465 | |

| Depreciation | 443 | | | 380 | |

| Amortization of premiums and discounts on investments | 3,738 | | | 3,761 | |

| Stock-based compensation | 1,052 | | | 333 | |

| Deferred federal income tax expense (benefit) | (1,350) | | | 652 | |

| Change in: | | | |

| Accrued investment income | 278 | | | 8 | |

| Reinsurance recoverable | (3,287) | | | 778 | |

| Due premiums | 1,174 | | | 2,168 | |

| Future policy benefit reserves | 1,842 | | | (5,111) | |

| Other policyholders' liabilities | 19,002 | | | 8,156 | |

| Federal income tax payable | 1,041 | | | 1,253 | |

| Commissions payable and other liabilities | 6,397 | | | (3,116) | |

| Other, net | (2,969) | | | 34 | |

| Net cash provided by operating activities | 21,092 | | | 15,444 | |

| Cash flows from investing activities: | | | |

| Purchases of fixed maturity securities, available-for-sale | (49,345) | | | (50,077) | |

| Sales of fixed maturity securities, available-for-sale | 4,659 | | | 13,690 | |

| Maturities and calls of fixed maturity securities, available-for-sale | 37,907 | | | 23,128 | |

| | | |

| Sales of equity securities | — | | | 770 | |

| Principal payments on mortgage loans | 7 | | | 6 | |

| | | |

| (Increase) decrease in policy loans, net | 2,896 | | | 3,023 | |

| Sales of other long-term investments | 2,226 | | | 3,793 | |

| Purchases of other long-term investments | (11,123) | | | (13,262) | |

| | | |

| Purchases of property and equipment | (561) | | | (292) | |

| Maturities of short-term investments | — | | | 750 | |

| | | |

| | | |

| | | |

| Net cash used in investing activities | (13,334) | | | (18,471) | |

| | | |

| See accompanying Notes to Consolidated Financial Statements. |

| | | |

September 30, 2024 | 10-Q 7

| | | | | | | | | | | |

| CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES |

| Consolidated Statements of Cash Flows, Continued |

| (Unaudited) |

| | | |

Nine Months Ended September 30, (In thousands) | 2024 | | 2023 |

| Cash flows from financing activities: | | | |

| Annuity deposits | $ | 5,181 | | | 5,443 | |

| Annuity withdrawals | (7,183) | | | (7,828) | |

| Acquisition of treasury stock | — | | | (719) | |

| | | |

| Other | (371) | | | (57) | |

| Net cash used in financing activities | (2,373) | | | (3,161) | |

| Net increase (decrease) in cash and cash equivalents | 5,385 | | | (6,188) | |

| Cash and cash equivalents at beginning of year | 26,997 | | | 22,973 | |

| Cash and cash equivalents at end of period | $ | 32,382 | | | 16,785 | |

| | | |

SUPPLEMENTAL DISCLOSURES OF NONCASH INVESTING AND FINANCING ACTIVITIES:

During the nine months ended September 30, 2024 and 2023, various fixed maturity issuers exchanged securities with book values of $3.7 million and $5.4 million, respectively, for securities of equal value.

The Company had $0.3 million of net unsettled security trades at September 30, 2023 and none at September 30, 2024.

The Company recognized $36 thousand right-of-use assets in exchange for new operating lease liabilities during the nine months ended September 30, 2023 and none during the nine months ended September 30, 2024.

See accompanying Notes to Consolidated Financial Statements.

September 30, 2024 | 10-Q 8

| | | | | | | | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

(1) FINANCIAL STATEMENTS

BASIS OF PRESENTATION AND CONSOLIDATION

The consolidated financial statements include the accounts and operations of Citizens, Inc. ("Citizens" or the "Company"), a Colorado corporation, and its wholly-owned subsidiaries, CICA Life Insurance Company of America ("CICA Domestic"), CICA Life Ltd. ("CICA Bermuda"), Security Plan Life Insurance Company ("SPLIC"), Security Plan Fire Insurance Company ("SPFIC"), Magnolia Guaranty Life Insurance Company ("MGLIC"), Computing Technology, Inc. ("CTI"), Nexo Global Services LLC, a Puerto Rico holding company ("Nexo") and its wholly-owned subsidiaries, CICA Life A.I., a Puerto Rico company ("CICA International") and Nexo Enrollment Services LLC, a Puerto Rico service company ("NES"). All significant inter-company accounts and transactions have been eliminated. Citizens and its wholly-owned subsidiaries are collectively referred to as the "Company," "it," "we," "us" or "our".

The consolidated balance sheet as of September 30, 2024, the consolidated statements of operations and comprehensive income (loss) and stockholders' equity for the three and nine months ended September 30, 2024 and September 30, 2023 and the consolidated statements of cash flows for the nine months ended September 30, 2024 and September 30, 2023 have been prepared by the Company without audit and are not subject to audit. In the opinion of management, all normal and recurring adjustments to present fairly the financial position, results of operations, and changes in cash flows at September 30, 2024 and for comparative periods have been made. The consolidated financial statements have been prepared in accordance with U.S. generally accepted accounting principles ("U.S. GAAP") for interim financial information and with the instructions to Form 10-Q adopted by the Securities and Exchange Commission ("SEC"). Accordingly, the consolidated financial statements do not include all the information and footnotes required for complete financial statements and should be read in conjunction with the Company’s consolidated financial statements and notes thereto included in our Annual Report on Form 10-K for the year ended December 31, 2023 ("Form 10-K"). Operating results for the interim periods disclosed herein are not necessarily indicative of the results that may be expected for a full year or any future period.

Our Life Insurance segment operates through CICA Domestic and CICA International.

CICA Domestic. Prior to July 1, 2023, our domestic life insurance business operated through CICA Domestic and Citizens National Life Insurance Company ("CNLIC"). CNLIC merged into CICA Domestic on July 1, 2023. CICA Domestic issues primarily ordinary whole life, final expense and life products with living benefits throughout the U.S.

CICA International. Until December 31, 2022, our international life insurance business operated through CICA Bermuda. Beginning January 1, 2023, all new international policies are issued by CICA International and on August 31, 2023, CICA Bermuda transferred all of its insurance in force business to CICA International. CICA International offers U.S. dollar-denominated products to non-U.S. residents/citizens internationally, including endowment products, which are principally accumulation contracts that incorporate an element of life insurance protection and ordinary whole life insurance. These contracts are designed to provide a fixed amount of insurance coverage over the life of the insured and may utilize rider benefits to provide additional increasing or decreasing coverage and annuity benefits to enhance accumulations.

NES provides services to policyholders of CICA International.

Our Home Service Insurance segment operates through our subsidiaries SPLIC and MGLIC, and focuses on the life insurance needs of the middle- and lower-income markets in Louisiana, Mississippi and Arkansas. Our products in this segment consist primarily of small face amount ordinary whole life, industrial life and pre-need policies, which are designed to fund final expenses for the insured, primarily consisting of funeral and burial costs. SPLIC also issues critical illness policies. Prior to June 30, 2023, SPFIC issued dwelling and contents property insurance policies. As of June 30, 2023, we ceased all operations for SPFIC.

September 30, 2024 | 10-Q 9

| | | | | | | | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

CTI provides data processing systems and services to the Company.

USE OF ESTIMATES

The preparation of consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ materially from these estimates.

Significant estimates include those used in the evaluation of credit losses on fixed maturity securities, valuation allowances on deferred tax assets, actuarially determined assets and liabilities and assumptions and contingencies related to litigation and regulatory matters. Certain of these estimates are particularly sensitive to market conditions, and deterioration and/or volatility in the worldwide debt or equity markets could have a material impact on the consolidated financial statements.

SIGNIFICANT ACCOUNTING POLICIES

For a description of all significant accounting policies, see Part IV, Item 15, Note 1. Summary of Significant Accounting Policies in the notes to our consolidated financial statements included in our Form 10-K, which should be read in conjunction with these accompanying consolidated financial statements.

(2) ACCOUNTING PRONOUNCEMENTS

ACCOUNTING STANDARDS NOT YET ADOPTED

On November 27, 2023, the FASB issued ASU No. 2023-07, Segment Reporting (Topic 280): Improvements to Reportable Segment Disclosures. This amendment expands a public entity's segment disclosures by requiring disclosure of significant segment expenses that are regularly provided to the chief operating decision maker, clarifying when an entity may report one or more additional measures to assess segment performance, requiring enhanced interim disclosures, providing new disclosure requirements for entities with a single reportable segment, and requiring other new disclosures. The amendments are effective for fiscal years beginning after December 15, 2023 and interim periods within fiscal years beginning after December 15, 2024. Early adoption is available. As the ASU only requires additional disclosures about the Company's operating segments, the impact to the consolidated financial statements will be minimal.

On December 14, 2023, the FASB issued ASU No. 2023-09, Income Taxes (Topic 740): Improvements to Income Tax Disclosures, which is intended to enhance the transparency, decision usefulness and effectiveness of income tax disclosures. The amendments in this ASU require a public entity to disclose a tabular tax rate reconciliation, using both percentages and currency, with specific categories. A public entity is also required to provide a qualitative description of the state and local jurisdictions that make up the majority of the effect of the state and local income tax category and the net amount of income taxes paid, disaggregated by federal, state and foreign taxes and also disaggregated by individual jurisdictions. The amendments also remove certain disclosures that are no longer considered cost beneficial. The amendments are effective prospectively for annual periods beginning after December 15, 2024 and early adoption and retrospective application are permitted. The Company is currently evaluating the impact of adopting this pronouncement on the consolidated financial statements.

No other new accounting pronouncements issued or effective during the year had, or is expected to have, a material impact on our consolidated financial statements.

September 30, 2024 | 10-Q 10

| | | | | | | | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

(3) INVESTMENTS

The Company invests primarily in fixed maturity securities, which totaled 86.2% of total cash and invested assets at September 30, 2024, as shown below.

| | | | | | | | | | | | | | | | | | | | | | | |

Carrying Value (In thousands, except for %) | September 30, 2024 | | December 31, 2023 |

| Amount | | % | | Amount | | % |

| | | | | | | |

| Cash and invested assets: | | | | | | | |

| Fixed maturity securities | $ | 1,273,497 | | | 86.2 | % | | 1,238,981 | | | 86.7 | % |

| Equity securities | 5,716 | | | 0.4 | | | 5,282 | | | 0.4 | |

| Policy loans | 72,463 | | | 4.9 | | | 75,359 | | | 5.3 | |

| Other long-term investments | 93,433 | | | 6.3 | | | 82,725 | | | 5.8 | |

| | | | | | | |

| Cash and cash equivalents | 32,382 | | | 2.2 | | | 26,997 | | | 1.8 | |

| | | | | | | |

| Total cash and invested assets | $ | 1,477,491 | | | 100.0 | % | | 1,429,344 | | | 100.0 | % |

The following tables represent the amortized cost, gross unrealized gains and losses and fair value of fixed maturity securities as of the dates indicated.

| | | | | | | | | | | | | | | | | | | | | | | |

| Amortized

Cost | | Gross

Unrealized

Gains | | Gross

Unrealized

Losses | | Fair

Value |

| September 30, 2024 | | | |

| (In thousands) | | | |

| | | | | | | |

| Fixed maturity securities: | | | | | | | |

| Available-for-sale: | | | | | | | |

| U.S. Treasury securities | $ | 5,950 | | | 165 | | | 29 | | | 6,086 | |

| U.S. Government-sponsored enterprises | 3,380 | | | 287 | | | — | | | 3,667 | |

| States and political subdivisions | 299,622 | | | 2,531 | | | 23,940 | | | 278,213 | |

| Corporate: | | | | | | | |

| Financial | 276,156 | | | 4,152 | | | 24,177 | | | 256,131 | |

| Consumer | 253,133 | | | 2,358 | | | 32,726 | | | 222,765 | |

| Utilities | 127,449 | | | 1,032 | | | 17,247 | | | 111,234 | |

| Energy | 83,130 | | | 452 | | | 6,535 | | | 77,047 | |

| Communications | 71,071 | | | 293 | | | 7,500 | | | 63,864 | |

| All other | 111,435 | | | 823 | | | 10,675 | | | 101,583 | |

| Commercial mortgage-backed | 268 | | | 1 | | | 2 | | | 267 | |

| Residential mortgage-backed | 106,816 | | | 14 | | | 7,633 | | | 99,197 | |

| Asset-backed | 53,170 | | | 926 | | | 653 | | | 53,443 | |

| | | | | | | |

| Total fixed maturity securities | $ | 1,391,580 | | | 13,034 | | | 131,117 | | | 1,273,497 | |

September 30, 2024 | 10-Q 11

| | | | | | | | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

| | | | | | | | | | | | | | | | | | | | | | | |

| Amortized

Cost | | Gross

Unrealized

Gains | | Gross

Unrealized

Losses | | Fair

Value |

| December 31, 2023 | | | |

| (In thousands) | | | |

| |

| Fixed maturity securities: | | | | | | | |

| Available-for-sale: | | | | | | | |

| U.S. Treasury securities | $ | 5,983 | | | 127 | | | 48 | | | 6,062 | |

| U.S. Government-sponsored enterprises | 3,404 | | | 250 | | | 1 | | | 3,653 | |

| States and political subdivisions | 314,203 | | | 2,160 | | | 29,132 | | | 287,231 | |

| Corporate: | | | | | | | |

| Financial | 266,485 | | | 2,066 | | | 31,255 | | | 237,296 | |

| Consumer | 250,672 | | | 2,145 | | | 37,094 | | | 215,723 | |

| Utilities | 123,625 | | | 615 | | | 20,253 | | | 103,987 | |

| Energy | 73,808 | | | 64 | | | 8,049 | | | 65,823 | |

| Communications | 74,029 | | | 309 | | | 8,892 | | | 65,446 | |

| All other | 111,124 | | | 647 | | | 12,439 | | | 99,332 | |

| Commercial mortgage-backed | 171 | | | — | | | — | | | 171 | |

| Residential mortgage-backed | 107,174 | | | 9 | | | 10,060 | | | 97,123 | |

| Asset-backed | 58,360 | | | 290 | | | 1,516 | | | 57,134 | |

| | | | | | | |

| Total fixed maturity securities | $ | 1,389,038 | | | 8,682 | | | 158,739 | | | 1,238,981 | |

The Company's investments in equity securities are shown below.

| | | | | | | | | | | |

Fair Value (In thousands) | September 30, 2024 | | December 31, 2023 |

| | | |

| Equity securities: | | | |

| | | |

| Bond mutual funds | $ | 766 | | | 740 | |

| Common stocks | 774 | | | 665 | |

| Non-redeemable preferred stock | 8 | | | 7 | |

| Non-redeemable preferred stock fund | 4,168 | | | 3,870 | |

| Total equity securities | $ | 5,716 | | | 5,282 | |

VALUATION OF INVESTMENTS

Available-for-sale ("AFS") fixed maturity securities are reported in the consolidated financial statements at fair value. Equity securities are measured at fair value with the change in fair value recorded through net income. The Company recognized net investment related gains of $0.4 million for both the three and nine months ended September 30, 2024, respectively, on equity securities held. The Company recognized net investment related losses of $0.4 million and $0.3 million for the three and nine months ended September 30, 2023, respectively.

The Company considers several factors in its review and evaluation of individual investments, using the process described in Part IV, Item 15, Note 2. Investments in the notes to the consolidated financial statements of our Form 10-K to determine whether a credit valuation loss exists. For the three and nine months ended September 30, 2024 and 2023, the Company recorded no credit valuation losses on fixed maturity securities.

September 30, 2024 | 10-Q 12

| | | | | | | | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

For fixed maturity security investments that have unrealized losses as of September 30, 2024 and December 31, 2023, the gross unrealized losses and related fair values that have been in a continuous unrealized loss position by timeframe are as follows.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| September 30, 2024 | Less than 12 months | Greater than 12 months | Total |

| (In thousands, except for # of securities) | Fair

Value | Unrealized

Losses | # of

Securities | Fair

Value | Unrealized

Losses | # of

Securities | Fair

Value | Unrealized

Losses | # of

Securities |

| | | | | | | | | |

| Fixed maturity securities: | | | | | | | | |

| Available-for-sale securities: | | | | | | | | |

| U.S. Treasury securities | $ | 569 | | 16 | | 2 | | 315 | | 13 | | 4 | | 884 | | 29 | | 6 | |

| | | | | | | | | |

| States and political subdivisions | 12,007 | | 126 | | 21 | | 160,393 | | 23,814 | | 180 | | 172,400 | | 23,940 | | 201 | |

| Corporate: | | | | | | | | | |

| Financial | 11,511 | | 27 | | 8 | | 165,303 | | 24,150 | | 194 | | 176,814 | | 24,177 | | 202 | |

| Consumer | 8,889 | | 122 | | 14 | | 173,308 | | 32,604 | | 216 | | 182,197 | | 32,726 | | 230 | |

| Utilities | 2,805 | | 132 | | 8 | | 86,941 | | 17,115 | | 146 | | 89,746 | | 17,247 | | 154 | |

| Energy | 3,199 | | 4 | | 4 | | 55,625 | | 6,531 | | 65 | | 58,824 | | 6,535 | | 69 | |

| Communications | 2,749 | | 34 | | 4 | | 50,790 | | 7,466 | | 60 | | 53,539 | | 7,500 | | 64 | |

| All Other | 10,989 | | 97 | | 18 | | 71,434 | | 10,578 | | 84 | | 82,423 | | 10,675 | | 102 | |

| Commercial mortgage-backed | — | | — | | — | | 96 | | 2 | | 1 | | 96 | | 2 | | 1 | |

| Residential mortgage-backed | 46 | | — | | 3 | | 98,714 | | 7,633 | | 84 | | 98,760 | | 7,633 | | 87 | |

| Asset-backed | 3,973 | | 71 | | 4 | | 16,507 | | 582 | | 18 | | 20,480 | | 653 | | 22 | |

| | | | | | | | | |

| Total fixed maturity securities | $ | 56,737 | | 629 | | 86 | | 879,426 | | 130,488 | | 1,052 | | 936,163 | | 131,117 | | 1,138 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| December 31, 2023 | Less than 12 months | Greater than 12 months | Total |

| (In thousands, except for # of securities) | Fair

Value | Unrealized

Losses | # of

Securities | Fair

Value | Unrealized

Losses | # of

Securities | Fair

Value | Unrealized

Losses | # of

Securities |

| | | | | | | | | |

| Fixed maturity securities: | | | | | | | | |

| Available-for-sale securities: | | | | | | | | |

| U.S. Treasury securities | $ | 1,203 | | 40 | | 5 | | 65 | | 8 | | 2 | | 1,268 | | 48 | | 7 | |

| U.S. Government-sponsored enterprises | 221 | | 1 | | 1 | | — | | — | | — | | 221 | | 1 | | 1 | |

| States and political subdivisions | 19,540 | | 357 | | 35 | | 164,264 | | 28,775 | | 192 | | 183,804 | | 29,132 | | 227 | |

| Corporate: | | | | | | | | | |

| Financial | 12,584 | | 383 | | 19 | | 176,521 | | 30,872 | | 217 | | 189,105 | | 31,255 | | 236 | |

| Consumer | 10,175 | | 265 | | 16 | | 176,725 | | 36,829 | | 223 | | 186,900 | | 37,094 | | 239 | |

| Utilities | 3,596 | | 66 | | 20 | | 85,169 | | 20,187 | | 137 | | 88,765 | | 20,253 | | 157 | |

| Energy | 3,291 | | 57 | | 1 | | 59,392 | | 7,992 | | 76 | | 62,683 | | 8,049 | | 77 | |

| Communications | 5,784 | | 153 | | 5 | | 56,108 | | 8,739 | | 69 | | 61,892 | | 8,892 | | 74 | |

| All Other | 2,080 | | 32 | | 5 | | 85,757 | | 12,407 | | 100 | | 87,837 | | 12,439 | | 105 | |

| | | | | | | | | |

| Residential mortgage-backed | 849 | | 38 | | 5 | | 95,806 | | 10,022 | | 86 | | 96,655 | | 10,060 | | 91 | |

| Asset-backed | 4,757 | | 111 | | 8 | | 32,764 | | 1,405 | | 40 | | 37,521 | | 1,516 | | 48 | |

| Total fixed maturity securities | $ | 64,080 | | 1,503 | | 120 | | 932,571 | | 157,236 | | 1,142 | | 996,651 | | 158,739 | | 1,262 | |

September 30, 2024 | 10-Q 13

| | | | | | | | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

In each category of our fixed maturity securities described above, we do not intend to sell our investments and it is not more likely than not that the Company will be required to sell the investments before recovery of their amortized cost bases. As of September 30, 2024 and December 31, 2023, 99.2% and 99.4% of the fair value of our fixed maturity securities portfolio, respectively, were rated investment grade. While the losses are currently unrealized, we continue to monitor all fixed maturity securities on an on-going basis as future information may become available which could result in an allowance being recorded.

These unrealized losses on fixed maturity securities are due to noncredit-related factors, including change in credit spreads and rising interest rates since purchase, which have little bearing on the recoverability of our investments, hence they are not recognized as credit losses. The fair value is expected to recover as the securities approach maturity or if market yields for such investments decline.

The amortized cost and fair value of fixed maturity securities at September 30, 2024 by contractual maturity are shown in the table below. Actual maturities may differ from contractual maturities because borrowers may have the right to call or prepay obligations with or without call or prepayment penalties. Securities not due at a single maturity date have been reflected based upon final stated maturity.

| | | | | | | | | | | |

| September 30, 2024 | Amortized

Cost | | Fair

Value |

| (In thousands) | |

| Fixed maturity securities: | | | |

| Due in one year or less | $ | 13,425 | | | 13,375 | |

| Due after one year through five years | 136,629 | | | 137,256 | |

| Due after five years through ten years | 276,325 | | | 277,228 | |

| Due after ten years | 965,201 | | | 845,638 | |

| Total fixed maturity securities | $ | 1,391,580 | | | 1,273,497 | |

The Company uses the specific identification method of the individual security to determine the cost basis used in the calculation of realized gains and losses related to security sales.

| | | | | | | | | | | | | | | | | | | | | | | |

| | | |

| Three Months Ended | | Nine Months Ended | | | | |

| September 30, | | September 30, | | | | |

| (In thousands) | 2024 | 2023 | | 2024 | 2023 | | | | | | |

| Fixed maturity securities, available-for-sale: | | | | | | | | | | |

| Proceeds | $ | — | | 9,446 | | | 4,659 | | 13,690 | | | | | | | |

| Gross realized gains | $ | — | | 38 | | | 91 | | 43 | | | | | | | |

| Gross realized losses | $ | — | | 436 | | | 196 | | 453 | | | | | | | |

(4) FAIR VALUE MEASUREMENTS

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. We hold AFS fixed maturity securities, which are carried at fair value with changes in fair value reported through other comprehensive income (loss). We also report our equity securities and certain other long-term investments at fair value with changes in fair value reported through the consolidated statements of operations and comprehensive income (loss).

Fair value measurements are generally based upon observable and unobservable inputs. Observable inputs reflect market data obtained from independent sources, while unobservable inputs reflect our view of market assumptions in the absence of observable market information. We utilize valuation techniques that maximize the use of

September 30, 2024 | 10-Q 14

| | | | | | | | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

observable inputs and minimize the use of unobservable inputs. All assets and liabilities carried at fair value are required to be classified and disclosed in one of the following three categories.

•Level 1 - Quoted prices for identical instruments in active markets.

•Level 2 - Quoted prices for similar instruments in active markets; quoted prices for identical or similar instruments in markets that are not active; and model-derived valuations whose inputs or whose significant value drivers are observable.

•Level 3 - Instruments whose significant value drivers are unobservable.

Level 1 primarily consists of financial instruments whose value is based on quoted market prices such as U.S. Treasury securities and actively traded mutual fund and stock investments.

Level 2 includes those financial instruments that are valued by independent pricing services or broker quotes. These pricing models are primarily industry-standard models that consider various inputs, such as interest rates, credit spreads and foreign exchange rates for the underlying financial instruments. All significant inputs are observable or derived from observable information in the marketplace or are supported by observable levels at which transactions are executed in the marketplace. Financial instruments in this category primarily include corporate securities, U.S. Government-sponsored enterprise securities, securities issued by states and political subdivisions and certain mortgage and asset-backed securities.

Level 3 is comprised of financial instruments whose fair value is estimated based on non-binding broker prices utilizing significant inputs not based on or corroborated by readily available market information. We have no investments in this category.

The following tables set forth our assets measured at fair value on a recurring basis as of the dates indicated.

| | | | | | | | | | | | | | | | | | | | | | | |

| September 30, 2024 | Level 1 | | Level 2 | | Level 3 | | Total

Fair Value |

| (In thousands) | | | |

| Financial assets: | | | | | | | |

| Fixed maturity securities, available-for-sale: | | | | | | | |

| U.S. Treasury and U.S. Government-sponsored enterprises | $ | 6,086 | | | 3,667 | | | — | | | 9,753 | |

| States and political subdivisions | — | | | 278,213 | | | — | | | 278,213 | |

| Corporate | 47 | | | 832,577 | | | — | | | 832,624 | |

| Commercial mortgage-backed | — | | | 267 | | | — | | | 267 | |

| Residential mortgage-backed | — | | | 99,197 | | | — | | | 99,197 | |

| Asset-backed | — | | | 53,443 | | | — | | | 53,443 | |

| | | | | | | |

| Total fixed maturity securities, available-for-sale | 6,133 | | | 1,267,364 | | | — | | | 1,273,497 | |

| | | | | | | |

| Equity securities: | | | | | | | |

| | | | | | | |

| Bond mutual funds | 766 | | | — | | | — | | | 766 | |

| Common stocks | 774 | | | — | | | — | | | 774 | |

| Non-redeemable preferred stock | 8 | | | — | | | — | | | 8 | |

| Non-redeemable preferred stock fund | 4,168 | | | — | | | — | | | 4,168 | |

| Total equity securities | 5,716 | | | — | | | — | | | 5,716 | |

Other long-term investments (1) | — | | | — | | | — | | | 93,167 | |

| Total financial assets | $ | 11,849 | | | 1,267,364 | | | — | | | 1,372,380 | |

(1) In accordance with Subtopic 820-10, certain investments that are measured at fair value using the net asset value per share (or its equivalent) practical expedient are not classified in the fair value hierarchy. The fair value amounts presented in this table are intended to permit reconciliation of the fair value hierarchy to the amounts presented in the consolidated balance sheets.

September 30, 2024 | 10-Q 15

| | | | | | | | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

| | | | | | | | | | | | | | | | | | | | | | | |

| December 31, 2023 | Level 1 | | Level 2 | | Level 3 | | Total

Fair Value |

| (In thousands) | | | |

| Financial assets: | | | | | | | |

| Fixed maturity securities, available-for-sale: | | | | | | | |

| U.S. Treasury and U.S. Government-sponsored enterprises | $ | 6,062 | | | 3,653 | | | — | | | 9,715 | |

| States and political subdivisions | — | | | 287,231 | | | — | | | 287,231 | |

| Corporate | 43 | | | 787,564 | | | — | | | 787,607 | |

| Commercial mortgage-backed | — | | | 171 | | | — | | | 171 | |

| Residential mortgage-backed | — | | | 97,123 | | | — | | | 97,123 | |

| Asset-backed | — | | | 57,134 | | | — | | | 57,134 | |

| | | | | | | |

| Total fixed maturity securities, available-for-sale | 6,105 | | | 1,232,876 | | | — | | | 1,238,981 | |

| | | | | | | |

| Equity securities: | | | | | | | |

| | | | | | | |

| Bond mutual funds | 740 | | | — | | | — | | | 740 | |

| Common stocks | 665 | | | — | | | — | | | 665 | |

| Non-redeemable preferred stock | 7 | | | — | | | — | | | 7 | |

| Non-redeemable preferred stock fund | 3,870 | | | — | | | — | | | 3,870 | |

| Total equity securities | 5,282 | | | — | | | — | | | 5,282 | |

Other long-term investments (1) | — | | | — | | | — | | | 82,460 | |

| Total financial assets | $ | 11,387 | | | 1,232,876 | | | — | | | 1,326,723 | |

(1) In accordance with Subtopic 820-10, certain investments that are measured at fair value using the net asset value per share (or its equivalent) practical expedient are not classified in the fair value hierarchy. The fair value amounts presented in this table are intended to permit reconciliation of the fair value hierarchy to the amounts presented in the consolidated balance sheets. |

FINANCIAL INSTRUMENTS VALUATION

FINANCIAL INSTRUMENTS CARRIED AT FAIR VALUE

Fixed maturity securities, available-for-sale. At September 30, 2024, fixed maturity securities, valued using a third-party pricing source, totaled $1.3 billion for Level 2 assets and comprised 92.3% of total reported fair value of our financial assets. The Level 1 and Level 2 valuations are reviewed and updated quarterly through testing by comparisons to separate pricing models, other third-party pricing services, and back tested to recent trades. In addition, we obtain information annually relative to the third-party pricing models and review model parameters for reasonableness. There were no Level 3 assets at September 30, 2024. As of September 30, 2024, there were no material changes to the valuation methods or assumptions used to determine fair values, and no broker or third-party prices were changed from the values received.

Equity securities. Our equity securities are classified as Level 1 assets as their fair values are based upon quoted market prices.

Limited partnerships. The Company considers the net asset value ("NAV") to represent the value of the investment fund and is measured by the total value of assets minus the total value of liabilities. The following table includes information related to our investments in limited partnerships that calculate NAV per share. For these investments, which are measured at fair value on a recurring basis, we use the NAV per share to measure fair value. The Company recognized net investment related gains of $0.5 million and $1.8 million for the three and nine months ended September 30, 2024, respectively, and losses of $0.1 million and gains of $0.2 million on limited partnerships

September 30, 2024 | 10-Q 16

| | | | | | | | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

held for the three and nine months ended September 30, 2023, respectively. These investments are included in other long-term investments on the consolidated balance sheets.

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | September 30, 2024 | | December 31, 2023 |

| (In thousands, except for years) | | Fair Value

Using NAV Per Share | Unfunded Commit-

ments | Range (In years) | | Fair Value

Using NAV Per Share | Unfunded Commit-

ments | Range (In years) |

| Description | |

| Limited partnerships: | | | | | | | |

| Middle market | Investments in privately-originated, performing senior secured debt primarily in North America-based companies | $ | 34,832 | | 1,669 | | 3 | | $ | 34,858 | | 3,452 | | 4 |

| Global equity fund | Investments in common stocks of U.S., international developed and emerging markets with a focus on long-term capital growth | 11,908 | | — | | 0 | | 10,345 | | — | | 0 |

| | | | | | | | |

| Late-stage growth | Investments in private late-stage, established companies seeking capital to accelerate growth prior to an IPO or sale | 25,431 | | 10,102 | | 4 to 6 | | 20,524 | | 14,271 | | 4 to 6 |

| Infrastructure | Investments in environmental infrastructure and related technology, focusing on renewable power generation and distribution | 20,996 | | 6,345 | | 9 to 11 | | 16,733 | | 9,576 | | 10 |

| Total limited partnerships | $ | 93,167 | | 18,116 | | | | $ | 82,460 | | 27,299 | | |

The majority of our limited partnership investments are not redeemable because distributions from the funds will be received when the underlying investments of the funds are liquidated. The life spans indicated above may be shortened or extended at the fund manager's discretion, typically in one or two-year increments. The global equity fund is redeemable monthly.

FINANCIAL INSTRUMENTS NOT CARRIED AT FAIR VALUE

Estimates of fair values are made at a specific point in time, based on relevant market prices and information about the financial instruments. The estimated fair values of financial instruments presented below are not necessarily indicative of the amounts the Company might realize in actual market transactions.

The carrying amount and fair value for the financial assets and liabilities on the consolidated financial statements not otherwise disclosed for the periods indicated were as follows:

| | | | | | | | | | | | | | | | | | | | | | | |

| | September 30, 2024 | | December 31, 2023 |

| (In thousands) | Carrying

Value | | Fair

Value | | Carrying

Value | | Fair

Value |

| | | | | | | |

| Financial assets: | | | | | | | |

| Policy loans | $ | 72,463 | | | 72,463 | | | 75,359 | | | 75,359 | |

| | | | | | | |

| Residential mortgage loan | 35 | | | 36 | | | 42 | | | 42 | |

| | | | | | | |

| Cash and cash equivalents | 32,382 | | | 32,382 | | | 26,997 | | | 26,997 | |

| Financial liabilities: | | | | | | | |

| Annuity - investment contracts | 68,077 | | | 63,468 | | | 67,690 | | | 63,283 | |

Policy loans. Policy loans had a weighted average annual interest rate of 7.7% at both September 30, 2024 and December 31, 2023 and no specified maturity dates. The aggregate fair value of policy loans approximates the

September 30, 2024 | 10-Q 17

| | | | | | | | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

carrying value reflected on the consolidated balance sheets. Policy loans are an integral part of the life insurance policies we have in force, cannot be valued separately and are not marketable. Therefore, the fair value of policy loans approximates the carrying value and policy loans are considered Level 3 assets in the fair value hierarchy.

Residential mortgage loan. This mortgage loan is secured by a residential property. The interest rate for this loan was 7.0% at both September 30, 2024 and December 31, 2023. At September 30, 2024, the remaining loan matures in four years. Management estimated the fair value using an annual interest rate of 6.25% at both September 30, 2024 and December 31, 2023. Our mortgage loan is considered a Level 3 asset in the fair value hierarchy and is included in other long-term investments on the consolidated balance sheets.

Cash and cash equivalents. The fair value of cash and cash equivalents approximates carrying value and are characterized as Level 1 assets in the fair value hierarchy.

Annuity liabilities. The fair value of the Company's liabilities under annuity contracts, which are considered Level 3 liabilities, was estimated at September 30, 2024 and December 31, 2023 using discounted cash flows based upon spot rates adjusted for various risk adjustments ranging from 3.40% to 4.40% and 3.80% to 4.50%, respectively. The fair value of liabilities under all insurance contracts are taken into consideration in the overall management of interest rate risk, which seeks to minimize exposure to changing interest rates through the matching of investment maturities with amounts due under insurance contracts.

Other long-term investments. Financial instruments included in other long-term investments are classified in various levels of the fair value hierarchy. The following table summarizes the carrying amounts of these investments.

| | | | | | | | | | | |

Carrying Value (In thousands) | September 30, 2024 | | December 31, 2023 |

| Other long-term investments: | | | |

| Limited partnerships | $ | 93,167 | | | 82,460 | |

| FHLB common stock | 210 | | | 202 | |

| Mortgage loans | 35 | | | 42 | |

| All other investments | 21 | | | 21 | |

| Total other long-term investments | $ | 93,433 | | | 82,725 | |

We are a member of the Federal Home Loan Bank ("FHLB") of Dallas and such membership requires members to own stock in the FHLB. Our FHLB stock is carried at amortized cost, which approximates fair value.

(5) DEFERRED POLICY ACQUISITION COSTS AND COST OF INSURANCE ACQUIRED

DAC

The following tables roll forward the DAC and COIA balances for the nine months ended September 30, 2024 and 2023 by reporting cohort. Our reporting cohorts are Permanent, which summarizes insurance policies with premiums payable over the lifetime of the policy, and Permanent Limited Pay, which summarizes insurance policies

September 30, 2024 | 10-Q 18

| | | | | | | | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

with premiums payable for a limited time after which the policy is fully paid up. Both reporting cohorts include whole life and endowment policies.

| | | | | | | | | | | | | | | |

| |

Nine Months Ended September 30, 2024 (In thousands) | Permanent | Permanent Limited Pay | | Other Business | Total |

| Life Insurance: | | | | | |

| Balance, beginning of year | $ | 105,552 | | 14,075 | | | 1,213 | | 120,840 | |

| Capitalizations | 21,792 | | 2,220 | | | 250 | | 24,262 | |

| Amortization expense | (9,763) | | (740) | | | (278) | | (10,781) | |

| | | | | |

| Balance, end of period | 117,581 | | 15,555 | | | 1,185 | | 134,321 | |

| | | | | |

| Home Service Insurance: | | | | | |

| Balance, beginning of year | 43,280 | | 10,564 | | | 1,084 | | 54,928 | |

| Capitalizations | 3,973 | | 892 | | | 177 | | 5,042 | |

| Amortization expense | (1,698) | | (323) | | | (2) | | (2,023) | |

| | | | | |

| Balance, end of period | 45,555 | | 11,133 | | | 1,259 | | 57,947 | |

| | | | | |

| Consolidated: | | | | | |

| Balance, beginning of year | 148,832 | | 24,639 | | | 2,297 | | 175,768 | |

| Capitalizations | 25,765 | | 3,112 | | | 427 | | 29,304 | |

| Amortization expense | (11,461) | | (1,063) | | | (280) | | (12,804) | |

| | | | | |

| Balance, end of period | $ | 163,136 | | 26,688 | | | 2,444 | | 192,268 | |

| | | | | | | | | | | | | | | |

| |

Nine Months Ended September 30, 2023 (In thousands) | Permanent | Permanent Limited Pay | | Other Business | Total |

| Life Insurance: | | | | | |

| Balance, beginning of year | $ | 100,926 | | 11,542 | | | 1,016 | | 113,484 | |

| Capitalizations | 11,220 | | 2,385 | | | 353 | | 13,958 | |

| Amortization expense | (8,859) | | (586) | | | (197) | | (9,642) | |

| | | | | |

| Balance, end of period | 103,287 | | 13,341 | | | 1,172 | | 117,800 | |

| | | | | |

| Home Service Insurance: | | | | | |

| Balance, beginning of year | 38,793 | | 9,729 | | | 921 | | 49,443 | |

| Capitalizations | 5,026 | | 865 | | | 185 | | 6,076 | |

| Amortization expense | (1,542) | | (295) | | | (65) | | (1,902) | |

| | | | | |

| Balance, end of period | 42,277 | | 10,299 | | | 1,041 | | 53,617 | |

| | | | | |

| Consolidated: | | | | | |

| Balance, beginning of year | 139,719 | | 21,271 | | | 1,937 | | 162,927 | |

| Capitalizations | 16,246 | | 3,250 | | | 538 | | 20,034 | |

| Amortization expense | (10,401) | | (881) | | | (262) | | (11,544) | |

| | | | | |

| Balance, end of period | $ | 145,564 | | 23,640 | | | 2,213 | | 171,417 | |

DAC capitalization increased for the nine months ended September 30, 2024, compared to the same prior year period mainly from increased commissions from higher first year sales in our Life Insurance segment.

September 30, 2024 | 10-Q 19

| | | | | | | | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

COIA

| | | | | | | | | | | | | | | |

| |

Nine Months Ended September 30, 2024 (In thousands) | Permanent | Permanent Limited Pay | | Other Business | Total |

| Life Insurance: | | | | | |

| Balance, beginning of year | $ | 249 | | 695 | | | 406 | | 1,350 | |

| Amortization expense | (12) | | (36) | | | (33) | | (81) | |

| | | | | |

| Balance, end of period | 237 | | 659 | | | 373 | | 1,269 | |

| | | | | |

| Home Service Insurance: | | | | | |

| Balance, beginning of year | 7,194 | | 168 | | | 1,331 | | 8,693 | |

| Amortization expense | (279) | | (5) | | | (112) | | (396) | |

| | | | | |

| Balance, end of period | 6,915 | | 163 | | | 1,219 | | 8,297 | |

| | | | | |

| Consolidated: | | | | | |

| Balance, beginning of year | 7,443 | | 863 | | | 1,737 | | 10,043 | |

| Amortization expense | (291) | | (41) | | | (145) | | (477) | |

| | | | | |

| Balance, end of period | $ | 7,152 | | 822 | | | 1,592 | | 9,566 | |

| | | | | | | | | | | | | | | |

| |

Nine Months Ended September 30, 2023 (In thousands) | Permanent | Permanent Limited Pay | | Other Business | Total |

| Life Insurance: | | | | | |

| Balance, beginning of year | $ | 267 | | 750 | | | 444 | | 1,461 | |

| Amortization expense | (14) | | (43) | | | (29) | | (86) | |

| | | | | |

| Balance, end of period | 253 | | 707 | | | 415 | | 1,375 | |

| | | | | |

| Home Service Insurance: | | | | | |

| Balance, beginning of year | 7,583 | | 176 | | | 1,427 | | 9,186 | |

| Amortization expense | (293) | | (6) | | | (80) | | (379) | |

| | | | | |

| Balance, end of period | 7,290 | | 170 | | | 1,347 | | 8,807 | |

| | | | | |

| Consolidated: | | | | | |

| Balance, beginning of year | 7,850 | | 926 | | | 1,871 | | 10,647 | |

| Amortization expense | (307) | | (49) | | | (109) | | (465) | |

| | | | | |

| Balance, end of period | $ | 7,543 | | 877 | | | 1,762 | | 10,182 | |

(6) POLICYHOLDERS’ LIABILITIES

LIABILITY FOR FUTURE POLICY BENEFITS

The following tables summarize balances of and changes in the liability for future policy benefits for our reporting cohorts: Permanent, which summarizes insurance policies with premiums payable over the lifetime of the policy,

September 30, 2024 | 10-Q 20

| | | | | | | | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

and Permanent Limited Pay, which summarizes insurance policies with premiums payable for a limited time after which the policy is fully paid up. Both reporting cohorts include whole life and endowment policies.

| | | | | | | | | | | | | | | | | | | | | | | | | |

September 30, 2024 (In thousands) | Life Insurance | | Home Service Insurance |

| Permanent | Permanent Limited Pay | | Total | | Permanent | Permanent Limited Pay | | Total |

| Present Value of Expected Net Premiums: | | | | | | | | |

| Balance, beginning of year | $ | 244,917 | | 13,260 | | | 258,177 | | | 98,831 | | 14,926 | | | 113,757 | |

| Beginning balance at original discount rate | 252,426 | | 13,533 | | | 265,959 | | | 102,045 | | 15,512 | | | 117,557 | |

| Effect of changes in cash flow assumptions | 17,731 | | 274 | | | 18,005 | | | (462) | | 21 | | | (441) | |

| Effect of actual variances from expected experience | (12,203) | | 973 | | | (11,230) | | | (5,784) | | (3,526) | | | (9,310) | |

| Adjusted beginning of year balance | 257,954 | | 14,780 | | | 272,734 | | | 95,799 | | 12,007 | | | 107,806 | |

| Issuances | 74,426 | | 2,249 | | | 76,675 | | | 11,412 | | 1,853 | | | 13,265 | |

| Interest accrual | 8,342 | | 380 | | | 8,722 | | | 3,193 | | 394 | | | 3,587 | |

| Net premiums collected | (36,066) | | (2,420) | | | (38,486) | | | (9,116) | | 892 | | | (8,224) | |

| Derecognition and other | (5,530) | | 92 | | | (5,438) | | | 317 | | 57 | | | 374 | |

| Ending balance at original discount rate | 299,126 | | 15,081 | | | 314,207 | | | 101,605 | | 15,203 | | | 116,808 | |

| Effect of changes in discount rates | (1,303) | | (43) | | | (1,346) | | | (2,042) | | (325) | | | (2,367) | |

| Balance, end of period | $ | 297,823 | | 15,038 | | | 312,861 | | | 99,563 | | 14,878 | | | 114,441 | |

| | | | | | | | | |

| Present Value of Expected Future Policy Benefits: | | | | | | | |

| Balance, beginning of year | $ | 973,350 | | 195,122 | | | 1,168,472 | | | 211,946 | | 122,784 | | | 334,730 | |

| Beginning balance at original discount rate | 995,962 | | 202,755 | | | 1,198,717 | | | 217,524 | | 123,941 | | | 341,465 | |

| Effect of changes in cash flow assumptions | 18,320 | | 734 | | | 19,054 | | | (502) | | (1,078) | | | (1,580) | |

| Effect of actual variances from expected experience | (9,656) | | 2,916 | | | (6,740) | | | (5,880) | | (1,692) | | | (7,572) | |

| Adjusted beginning of year balance | 1,004,626 | | 206,405 | | | 1,211,031 | | | 211,142 | | 121,171 | | | 332,313 | |

| Issuances | 75,132 | | 2,352 | | | 77,484 | | | 11,407 | | 1,858 | | | 13,265 | |

| Interest accrual | 33,624 | | 6,185 | | | 39,809 | | | 7,233 | | 4,305 | | | 11,538 | |

| Benefit payments | (67,441) | | (13,281) | | | (80,722) | | | (11,399) | | (4,286) | | | (15,685) | |

| Derecognition and other | (6,642) | | 16 | | | (6,626) | | | 301 | | 51 | | | 352 | |

| Ending balance at original discount rate | 1,039,299 | | 201,677 | | | 1,240,976 | | | 218,684 | | 123,099 | | | 341,783 | |

| Effect of changes in discount rates | (8,395) | | (6,067) | | | (14,462) | | | (5,797) | | (2,493) | | | (8,290) | |

| Balance, end of period | $ | 1,030,904 | | 195,610 | | | 1,226,514 | | | 212,887 | | 120,606 | | | 333,493 | |

| | | | | | | | | |

| Net liability for future policy benefits | $ | 733,081 | | 180,572 | | | 913,653 | | | 113,324 | | 105,728 | | | 219,052 | |

| | | | | | | | | |

| Less: Reinsurance recoverable | 1,308 | | — | | | 1,308 | | | — | | — | | | — | |

| Net liability for future policy benefits, after reinsurance recoverable | $ | 731,773 | | 180,572 | | | 912,345 | | | 113,324 | | 105,728 | | | 219,052 | |

The Company performed its annual review of policy benefit reserves assumptions in the third quarter of 2024 and recorded the effects of changes in its cash flow assumptions, which resulted in a net increase in future policy benefit

September 30, 2024 | 10-Q 21

| | | | | | | | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

reserves, primarily driven by mortality and lapse assumptions that better reflect emerging experience for the new CICA Domestic block of business.

For the nine months ended September 30, 2024, the Life Insurance segment increased reserves compared to the same period in 2023 due to the unfavorable impact of actual versus expected experience related to mortality and lapses. There was little impact to the Home Service Insurance segment resulting from actual to expected experience for the nine months ended September 30, 2024 and 2023.

| | | | | | | | | | | | | | | | | | | | | | | | | |

September 30, 2023 (In thousands) | Life Insurance | | Home Service Insurance |

| Permanent | Permanent Limited Pay | | Total | | Permanent | Permanent Limited Pay | | Total |

| Present Value of Expected Net Premiums: | | | | | | | | |

| Balance, beginning of year | $ | 235,228 | | 10,209 | | | 245,437 | | | 93,508 | | 13,255 | | | 106,763 | |

| Beginning balance at original discount rate | 247,601 | | 10,682 | | | 258,283 | | | 100,225 | | 14,394 | | | 114,619 | |

| Effect of changes in cash flow assumptions | (210) | | 38 | | | (172) | | | (343) | | 85 | | | (258) | |

| Effect of actual variances from expected experience | 4,156 | | 1,059 | | | 5,215 | | | (5,631) | | (4,477) | | | (10,108) | |

| Adjusted beginning of year balance | 251,547 | | 11,779 | | | 263,326 | | | 94,251 | | 10,002 | | | 104,253 | |

| Issuances | 20,918 | | 2,608 | | | 23,526 | | | 13,854 | | 3,107 | | | 16,961 | |

| Interest accrual | 6,897 | | 248 | | | 7,145 | | | 3,019 | | 348 | | | 3,367 | |

| Net premiums collected | (31,480) | | (2,004) | | | (33,484) | | | (8,909) | | 2,019 | | | (6,890) | |

| Derecognition and other | 567 | | 240 | | | 807 | | | 475 | | 113 | | | 588 | |

| Ending balance at original discount rate | 248,449 | | 12,871 | | | 261,320 | | | 102,690 | | 15,589 | | | 118,279 | |

| Effect of changes in discount rates | (16,380) | | (501) | | | (16,881) | | | (9,438) | | (1,397) | | | (10,835) | |

| Balance, end of period | $ | 232,069 | | 12,370 | | | 244,439 | | | 93,252 | | 14,192 | | | 107,444 | |

| | | | | | | | | |

| Present Value of Expected Future Policy Benefits: | | | | | | | |

| Balance, beginning of year | $ | 947,415 | | 195,612 | | | 1,143,027 | | | 200,351 | | 116,356 | | | 316,707 | |

| Beginning balance at original discount rate | 996,169 | | 208,051 | | | 1,204,220 | | | 214,188 | | 121,908 | | | 336,096 | |

| Effect of changes in cash flow assumptions | (389) | | (702) | | | (1,091) | | | (257) | | 331 | | | 74 | |

| Effect of actual variances from expected experience | 6,338 | | 3,489 | | | 9,827 | | | (5,472) | | (1,337) | | | (6,809) | |

| Adjusted beginning of year balance | 1,002,118 | | 210,838 | | | 1,212,956 | | | 208,459 | | 120,902 | | | 329,361 | |

| Issuances | 21,360 | | 2,798 | | | 24,158 | | | 13,854 | | 3,115 | | | 16,969 | |

| Interest accrual | 32,470 | | 6,288 | | | 38,758 | | | 6,987 | | 4,242 | | | 11,229 | |

| Benefit payments | (63,211) | | (16,732) | | | (79,943) | | | (12,246) | | (4,707) | | | (16,953) | |

| Derecognition and other | 97 | | 42 | | | 139 | | | 464 | | 109 | | | 573 | |

| Ending balance at original discount rate | 992,834 | | 203,234 | | | 1,196,068 | | | 217,518 | | 123,661 | | | 341,179 | |

| Effect of changes in discount rates | (78,072) | | (18,778) | | | (96,850) | | | (23,934) | | (12,670) | | | (36,604) | |

| Balance, end of period | $ | 914,762 | | 184,456 | | | 1,099,218 | | | 193,584 | | 110,991 | | | 304,575 | |

| | | | | | | | | |

| Net liability for future policy benefits | $ | 682,693 | | 172,086 | | | 854,779 | | | 100,332 | | 96,799 | | | 197,131 | |

| | | | | | | | | |

| | | | | | | | | |

| | | | | | | | | |

September 30, 2024 | 10-Q 22

| | | | | | | | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

The following table reconciles the net liability for future policy benefits shown above to the liability for future policy benefits reported in the consolidated balance sheets.

| | | | | | | | | | | | | | | | | | | | | | | |

| September 30, 2024 | | September 30, 2023 |

| (In thousands) | Life

Insurance | Home Service

Insurance | Consolidated | | Life

Insurance | Home Service

Insurance | Consolidated |

| Life Insurance: | | | | | | | |

| Permanent | $ | 731,773 | | 113,324 | | 845,097 | | | 682,693 | | 100,332 | | 783,025 | |

| Permanent limited pay | 180,572 | | 105,728 | | 286,300 | | | 172,086 | | 96,799 | | 268,885 | |

| Deferred profit liability | 29,572 | | 29,158 | | 58,730 | | | 27,616 | | 26,138 | | 53,754 | |

| Other | 32,426 | | 14,320 | | 46,746 | | | 28,011 | | 13,926 | | 41,937 | |

| Total life insurance | 974,343 | | 262,530 | | 1,236,873 | | | 910,406 | | 237,195 | | 1,147,601 | |

| Accident & Health: | | | | | | | |

| | | | | | | |

| Other | 586 | | 412 | | 998 | | | 596 | | 281 | | 877 | |

| | | | | | | |

| Total future policy benefit reserves | $ | 974,929 | | 262,942 | | 1,237,871 | | | 911,002 | | 237,476 | | 1,148,478 | |

The following table provides the amount of undiscounted and discounted expected gross premiums and expected future benefit payments for long-term duration contracts.

| | | | | | | | | | | | | | | | | | | | | | | |

| September 30, 2024 | | September 30, 2023 |

| (In thousands) | Life

Insurance | | Home Service

Insurance | | Life

Insurance | | Home Service

Insurance |

| Undiscounted: | | | | | | | |

| Permanent: | | | | | | | |

| Expected future gross premiums | $ | 731,580 | | | 448,837 | | | 604,059 | | | 459,405 | |

| Expected future benefit payments | 1,586,017 | | | 487,851 | | | 1,483,068 | | | 484,239 | |

| | | | | | | |

| Permanent Limited Pay: | | | | | | | |

| Expected future gross premiums | 46,270 | | | 76,032 | | | 47,868 | | | 77,544 | |

| Expected future benefit payments | 322,188 | | | 320,318 | | | 325,964 | | | 320,563 | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| Discounted: | | | | | | | |

| Permanent: | | | | | | | |

| Expected future gross premiums | $ | 564,242 | | | 272,938 | | | 453,277 | | | 261,271 | |

| Expected future benefit payments | 1,030,904 | | | 212,887 | | | 914,762 | | | 193,584 | |

| | | | | | | |

| Permanent Limited Pay: | | | | | | | |

| Expected future gross premiums | 41,999 | | | 51,752 | | | 42,133 | | | 51,091 | |

| Expected future benefit payments | 195,610 | | | 120,606 | | | 184,456 | | | 110,991 | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

September 30, 2024 | 10-Q 23

| | | | | | | | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

The following tables summarize the amount of revenue and interest related to long-term duration contracts recognized in the consolidated statement of operations and comprehensive income (loss):

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended September 30, | | Nine Months Ended September 30, |

| 2024 | | 2023 | | 2024 | | 2023 |

| (In thousands) | Gross Premiums | Interest Expense | | Gross Premiums | Interest Expense | | Gross Premiums | Interest Expense | | Gross Premiums | Interest Expense |

| Life Insurance Segment: | | | | | | | | | | |

| Life Insurance: | | | | | | | | | | | |

| Permanent | $ | 27,930 | | 8,391 | | | 23,654 | | 8,471 | | | 76,047 | | 25,282 | | | 68,619 | | 25,573 | |

| Permanent Limited Pay | 3,395 | | 2,269 | | | 3,555 | | 2,308 | | | 11,067 | | 6,739 | | | 11,333 | | 6,811 | |

| Other | 2,508 | | — | | | 4,279 | | — | | | 7,550 | | — | | | 7,094 | | — | |

| Less: | | | | | | | | | | | |

| Reinsurance | 1,828 | | — | | | 392 | | — | | | 3,559 | | — | | | 1,452 | | — | |

| Total, net of reinsurance | 32,005 | | 10,660 | | | 31,096 | | 10,779 | | | 91,105 | | 32,021 | | | 85,594 | | 32,384 | |

| Accident & Health: | | | | | | | | | | | |

| | | | | | | | | | | |

| Other | 197 | | — | | | 53 | | — | | | 565 | | — | | | 537 | | — | |

| Less: | | | | | | | | | | | |

| Reinsurance | 1 | | — | | | 1 | | — | | | 3 | | — | | | 3 | | — | |

| Total, net of reinsurance | 196 | | — | | | 52 | | — | | | 562 | | — | | | 534 | | — | |

| Total | $ | 32,201 | | 10,660 | | | 31,148 | | 10,779 | | | 91,667 | | 32,021 | | | 86,128 | | 32,384 | |

| | | | | | | | | | | |

| Home Service Insurance Segment: | | | | | | | | | |

| Life Insurance: | | | | | | | | | | | |

| Permanent | $ | 8,257 | | 1,349 | | | 8,372 | | 1,322 | | | 24,723 | | 4,040 | | | 25,012 | | 3,968 | |

| Permanent Limited Pay | 1,837 | | 1,636 | | | 2,154 | | 1,599 | | | 5,905 | | 4,894 | | | 6,425 | | 4,777 | |

| Other | 367 | | — | | | 178 | | — | | | 1,114 | | — | | | 1,012 | | — | |

| Less: | | | | | | | | | | | |

| Reinsurance | 5 | | — | | | 6 | | — | | | 24 | | — | | | 23 | | — | |

| Total, net of reinsurance | 10,456 | | 2,985 | | | 10,698 | | 2,921 | | | 31,718 | | 8,934 | | | 32,426 | | 8,745 | |

| Accident & Health: | | | | | | | | | | | |

| | | | | | | | | | | |

| Other | 256 | | — | | | 244 | | — | | | 762 | | — | | | 667 | | — | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| Total | $ | 10,712 | | 2,985 | | | 10,942 | | 2,921 | | | 32,480 | | 8,934 | | | 33,093 | | 8,745 | |

The following table provides the weighted-average durations of the liability for future policy benefits.

| | | | | | | | | | | | | | | | | |

| September 30, 2024 | | September 30, 2023 |

| (In years) | Life

Insurance | Home Service

Insurance | | Life

Insurance | Home Service

Insurance |

| Permanent: | | | | | |

| Duration at original discount rate | 8.6 | 16.0 | | 7.8 | 15.7 |

| Duration at current discount rate | 8.6 | 15.6 | | 8.2 | 15.6 |

| Permanent Limited Pay: | | | | | |

| Duration at original discount rate | 8.1 | 14.7 | | 7.9 | 14.3 |

| Duration at current discount rate | 7.8 | 14.7 | | 7.6 | 14.4 |

| | | | | |

| | | | | |

| | | | | |

September 30, 2024 | 10-Q 24

| | | | | | | | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

The following table provides the weighted-average interest rates for the liability for future policy benefits.

| | | | | | | | | | | | | | | | | |