Use these links to rapidly review the document

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_______________________________________________________________

FORM 10-Q

|

| |

| (Mark One) |

| ý | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the Quarterly period ended March 31, 2019 |

| OR |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from ______ to ______ . |

Commission File Number: 1-14829

Molson Coors Brewing Company

(Exact name of registrant as specified in its charter)

|

| | |

DELAWARE (State or other jurisdiction of incorporation or organization) | | 84-0178360 (I.R.S. Employer Identification No.) |

1801 California Street, Suite 4600, Denver, Colorado, USA 1555 Notre Dame Street East, Montréal, Québec, Canada (Address of principal executive offices) | | 80202 H2L 2R5 (Zip Code) |

303-927-2337 (Colorado)

514-521-1786 (Québec)

(Registrant's telephone number, including area code)

_______________________________________________________________

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ý No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company" and "emerging growth company" in Rule 12b-2 of the Exchange Act.

|

| | | | | | | | |

Large accelerated filer ý | | Accelerated filer o | | Non-accelerated filer o | | Smaller reporting company o | | Emerging growth company o |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

Indicate the number of shares outstanding of each of the registrant's classes of common stock, as of April 25, 2019:

Class A Common Stock — 2,560,668 shares

Class B Common Stock — 196,188,247 shares

Exchangeable shares:

As of April 25, 2019, the following number of exchangeable shares were outstanding for Molson Coors Canada, Inc.:

Class A Exchangeable shares — 2,757,201 shares

Class B Exchangeable shares — 14,807,000 shares

The Class A exchangeable shares and Class B exchangeable shares are shares of the share capital in Molson Coors Canada Inc., a wholly-owned subsidiary of the registrant. They are publicly traded on the Toronto Stock Exchange under the symbols TPX.A and TPX.B, respectively. These shares are intended to provide substantially the same economic and voting rights as the corresponding class of Molson Coors common stock in which they may be exchanged. In addition to the registered Class A common stock and the Class B common stock, the registrant has also issued and outstanding one share each of a Special Class A voting stock and Special Class B voting stock. The Special Class A voting stock and the Special Class B voting stock provide the mechanism for holders of Class A exchangeable shares and Class B exchangeable shares to be provided instructions to vote with the holders of the Class A common stock and the Class B common stock, respectively. The holders of the Special Class A voting stock and Special Class B voting stock are entitled to one vote for each outstanding Class A exchangeable share and Class B exchangeable share, respectively, excluding shares held by the registrant or its subsidiaries, and generally vote together with the Class A common stock and Class B common stock, respectively, on all matters on which the Class A common stock and Class B common stock are entitled to vote. The Special Class A voting stock and Special Class B voting stock are subject to a voting trust arrangement. The trustee which holds the Special Class A voting stock and the Special Class B voting stock is required to cast a number of votes equal to the number of then-outstanding Class A exchangeable shares and Class B exchangeable shares, respectively, but will only cast a number of votes equal to the number of Class A exchangeable shares and Class B exchangeable shares as to which it has received voting instructions from the owners of record of those Class A exchangeable shares and Class B exchangeable shares, other than the registrant or its subsidiaries, respectively, on the record date, and will cast the votes in accordance with such instructions so received.

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

INDEX

Glossary of Terms and Abbreviations

|

| |

AOCI | Accumulated other comprehensive income (loss) |

CAD | Canadian dollar |

| CZK | Czech Koruna |

| DBRS | A global credit rating agency in Toronto |

| DSUs | Deferred stock units |

| EBITDA | Earnings before interest, tax, depreciation and amortization |

EPS | Earnings per share |

| EUR | Euro |

FASB | Financial Accounting Standards Board |

GBP | British Pound |

| HRK | Croatian Kuna |

JPY | Japanese Yen |

| Moody’s | Moody’s Investors Service Limited, a nationally recognized statistical rating organization designated by the SEC |

| OCI | Other comprehensive income (loss) |

OPEB | Other postretirement benefit plans |

| PSUs | Performance share units |

RSD | Serbian Dinar |

| RSUs | Restricted stock units |

| SEC | Securities and Exchange Commission |

| Standard & Poor’s | Standard and Poor’s Ratings Services, a nationally recognized statistical rating organization designated by the SEC |

| STRs | Sales-to-retailers |

| STWs | Sales-to-wholesalers |

| 2017 Tax Act | Tax Cuts and Jobs Act |

| U.K. | United Kingdom |

U.S. | United States |

| U.S. GAAP | Accounting principles generally accepted in the U.S. |

| USD or $ | U.S. dollar |

| VIEs | Variable interest entities |

Cautionary Statement Pursuant to Safe Harbor Provisions of the Private Securities Litigation Reform Act of 1995

This report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended (the "Exchange Act"). From time to time, we may also provide oral or written forward-looking statements in other materials we release to the public. Such forward-looking statements are subject to the safe harbor created by the Private Securities Litigation Reform Act of 1995.

Statements that refer to projections of our future financial performance, our anticipated growth and trends in our businesses, and other characterizations of future events or circumstances are forward-looking statements, and include, but are not limited to, statements under the headings "Management's Discussion and Analysis of Financial Condition and Results of Operations," and under the heading "Outlook for 2019" therein, overall volume trends, consumer preferences, pricing trends, industry forces, cost reduction strategies, anticipated results, anticipated synergies, expectations for funding future capital expenditures and operations, expectations regarding future dividends, debt service capabilities, timing and amounts of debt and leverage levels, shipment levels and profitability, market share and the sufficiency of capital resources. In addition, statements that we make in this report that are not statements of historical fact may also be forward-looking statements. Words such as "expects," "goals," "plans," "believes," "continues," "may," "anticipate," "seek," "estimate," "outlook," "trends," "future benefits," "potential," "projects," "strategies," and variations of such words and similar expressions are intended to identify forward-looking statements.

Forward-looking statements are subject to risks and uncertainties that could cause actual results to be materially different from those indicated (both favorably and unfavorably). These risks and uncertainties include, but are not limited to, those described under the heading "Risk Factors" elsewhere throughout this report, and those described from time to time in our past and future reports filed with the SEC, including in our Annual Report on Form 10-K for the year ended December 31, 2018. Caution should be taken not to place undue reliance on any such forward-looking statements. Forward-looking statements speak only as of the date when made and we undertake no obligation to update any forward-looking statement, whether as a result of new information, future events or otherwise.

Market and Industry Data

The market and industry data used in this Quarterly Report on Form 10-Q are based on independent industry publications, customers, trade or business organizations, reports by market research firms and other published statistical information from third parties, as well as information based on management’s good faith estimates, which we derive from our review of internal information and independent sources. Although we believe these sources to be reliable, we have not independently verified the accuracy or completeness of the information.

PART I. FINANCIAL INFORMATION

ITEM 1.

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(IN MILLIONS, EXCEPT PER SHARE DATA)

(UNAUDITED)

|

| | | | | | | |

| | Three Months Ended |

| | March 31, 2019 | | March 31, 2018 |

| Sales | $ | 2,800.1 |

| | $ | 2,868.0 |

|

| Excise taxes | (496.8 | ) | | (536.5 | ) |

| Net sales | 2,303.3 |

| | 2,331.5 |

|

| Cost of goods sold | (1,413.0 | ) | | (1,535.7 | ) |

| Gross profit | 890.3 |

| | 795.8 |

|

| Marketing, general and administrative expenses | (655.2 | ) | | (681.1 | ) |

| Special items, net | (13.0 | ) | | 314.8 |

|

| Operating income (loss) | 222.1 |

| | 429.5 |

|

| Interest income (expense), net | (73.3 | ) | | (83.2 | ) |

| Other pension and postretirement benefits (costs), net | 8.6 |

| | 10.0 |

|

| Other income (expense), net | 23.9 |

| | 1.1 |

|

| Income (loss) before income taxes | 181.3 |

| | 357.4 |

|

| Income tax benefit (expense) | (32.2 | ) | | (74.9 | ) |

| Net income (loss) | 149.1 |

| | 282.5 |

|

| Net (income) loss attributable to noncontrolling interests | 2.3 |

| | (4.4 | ) |

| Net income (loss) attributable to Molson Coors Brewing Company | $ | 151.4 |

| | $ | 278.1 |

|

| | | | |

| Net income (loss) attributable to Molson Coors Brewing Company per share: | | | |

| Basic | $ | 0.70 |

| | $ | 1.29 |

|

| Diluted | $ | 0.70 |

| | $ | 1.28 |

|

| | | | |

| Weighted-average shares outstanding: | | | |

| Basic | 216.5 |

| | 215.8 |

|

| Dilutive effect of share-based awards | 0.4 |

| | 0.8 |

|

| Diluted | 216.9 |

| | 216.6 |

|

| | | | |

| Anti-dilutive securities excluded from the computation of diluted EPS | 1.1 |

| | 0.5 |

|

See notes to unaudited condensed consolidated financial statements.

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

(IN MILLIONS)

(UNAUDITED)

|

| | | | | | | |

| | Three Months Ended |

| | March 31, 2019 | | March 31, 2018 |

| Net income (loss) including noncontrolling interests | $ | 149.1 |

| | $ | 282.5 |

|

| Other comprehensive income (loss), net of tax: | | | |

| Foreign currency translation adjustments | 71.5 |

| | 74.1 |

|

| Unrealized gain (loss) on derivative instruments | (29.7 | ) | | (25.8 | ) |

| Reclassification of derivative (gain) loss to income | 0.1 |

| | 1.1 |

|

| Amortization of net prior service (benefit) cost and net actuarial (gain) loss to income | (0.6 | ) | | 1.7 |

|

| Ownership share of unconsolidated subsidiaries' other comprehensive income (loss) | 1.0 |

| | (1.2 | ) |

| Total other comprehensive income (loss), net of tax | 42.3 |

| | 49.9 |

|

| Comprehensive income (loss) | 191.4 |

| | 332.4 |

|

| Comprehensive (income) loss attributable to noncontrolling interests | 2.1 |

| | (5.2 | ) |

| Comprehensive income (loss) attributable to Molson Coors Brewing Company | $ | 193.5 |

| | $ | 327.2 |

|

See notes to unaudited condensed consolidated financial statements.

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES CONDENSED CONSOLIDATED BALANCE SHEETS (IN MILLIONS, EXCEPT PAR VALUE) (UNAUDITED) |

| | | | | | | |

| | As of |

| | March 31, 2019 | | December 31, 2018 |

| Assets | | | |

| Current assets: | | | |

| Cash and cash equivalents | $ | 234.4 |

| | $ | 1,057.9 |

|

| Accounts receivable, net | 909.5 |

| | 744.4 |

|

| Other receivables, net | 141.6 |

| | 126.6 |

|

| Inventories, net | 687.9 |

| | 591.8 |

|

| Other current assets, net | 364.6 |

| | 245.6 |

|

| Total current assets | 2,338.0 |

| | 2,766.3 |

|

| Properties, net | 4,553.3 |

| | 4,608.3 |

|

| Goodwill | 8,279.4 |

| | 8,260.8 |

|

| Other intangibles, net | 13,749.6 |

| | 13,776.4 |

|

| Other assets | 903.3 |

| | 698.0 |

|

| Total assets | $ | 29,823.6 |

| | $ | 30,109.8 |

|

| Liabilities and equity | | | |

| Current liabilities: | | | |

| Accounts payable and other current liabilities | $ | 2,561.3 |

| | $ | 2,706.4 |

|

| Current portion of long-term debt and short-term borrowings | 1,641.1 |

| | 1,594.5 |

|

| Total current liabilities | 4,202.4 |

| | 4,300.9 |

|

| Long-term debt | 8,484.8 |

| | 8,893.8 |

|

| Pension and postretirement benefits | 726.9 |

| | 726.6 |

|

| Deferred tax liabilities | 2,151.5 |

| | 2,128.9 |

|

| Other liabilities | 369.9 |

| | 323.8 |

|

| Total liabilities | 15,935.5 |

| | 16,374.0 |

|

Commitments and contingencies (Note 14) | | | |

| Molson Coors Brewing Company stockholders' equity | | | |

| Capital stock: | | | |

| Preferred stock, $0.01 par value (authorized: 25.0 shares; none issued) | — |

| | — |

|

| Class A common stock, $0.01 par value per share (authorized: 500.0 shares; issued and outstanding: 2.6 shares and 2.6 shares, respectively) | — |

| | — |

|

| Class B common stock, $0.01 par value per share (authorized: 500.0 shares; issued: 205.7 shares and 205.4 shares, respectively) | 2.0 |

| | 2.0 |

|

| Class A exchangeable shares, no par value (issued and outstanding: 2.8 shares and 2.8 shares, respectively) | 103.2 |

| | 103.2 |

|

| Class B exchangeable shares, no par value (issued and outstanding: 14.8 shares and 14.8 shares, respectively) | 557.6 |

| | 557.6 |

|

| Paid-in capital | 6,776.2 |

| | 6,773.1 |

|

| Retained earnings | 7,862.4 |

| | 7,692.9 |

|

| Accumulated other comprehensive income (loss) | (1,182.7 | ) | | (1,150.0 | ) |

| Class B common stock held in treasury at cost (9.5 shares and 9.5 shares, respectively) | (471.4 | ) | | (471.4 | ) |

| Total Molson Coors Brewing Company stockholders' equity | 13,647.3 |

| | 13,507.4 |

|

| Noncontrolling interests | 240.8 |

| | 228.4 |

|

| Total equity | 13,888.1 |

| | 13,735.8 |

|

| Total liabilities and equity | $ | 29,823.6 |

| | $ | 30,109.8 |

|

See notes to unaudited condensed consolidated financial statements.

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(IN MILLIONS)

(UNAUDITED) |

| | | | | | | |

| | Three Months Ended |

| | March 31, 2019 | | March 31, 2018 |

| Cash flows from operating activities: | | | |

| Net income (loss) including noncontrolling interests | $ | 149.1 |

|

| $ | 282.5 |

|

| Adjustments to reconcile net income (loss) to net cash provided by (used in) operating activities: | | | |

|

| Depreciation and amortization | 212.9 |

| | 213.7 |

|

| Amortization of debt issuance costs and discounts | 3.7 |

| | 4.1 |

|

| Share-based compensation | 11.4 |

| | 14.8 |

|

| (Gain) loss on sale or impairment of properties and other assets, net | 0.5 |

| | 0.7 |

|

| Unrealized (gain) loss on foreign currency fluctuations and derivative instruments, net | (57.2 | ) | | 83.5 |

|

| Income tax (benefit) expense | 32.2 |

| | 74.9 |

|

| Income tax (paid) received | (8.5 | ) | | (8.9 | ) |

| Interest expense, excluding interest amortization | 72.1 |

| | 79.3 |

|

| Interest paid | (103.1 | ) | | (115.2 | ) |

| Change in current assets and liabilities and other | (411.6 | ) | | (314.2 | ) |

| Net cash provided by (used in) operating activities | (98.5 | ) | | 315.2 |

|

| Cash flows from investing activities: | |

| | |

|

| Additions to properties | (198.0 | ) | | (208.3 | ) |

| Proceeds from sales of properties and other assets | 2.4 |

| | 1.6 |

|

| Other | 1.0 |

| | (45.4 | ) |

| Net cash provided by (used in) investing activities | (194.6 | ) | | (252.1 | ) |

| Cash flows from financing activities: | |

| | |

|

| Exercise of stock options under equity compensation plans | 0.6 |

| | 6.1 |

|

| Dividends paid | (88.7 | ) | | (88.5 | ) |

| Payments on debt and borrowings | (1,067.2 | ) | | (0.8 | ) |

| Net proceeds from (payments on) revolving credit facilities and commercial paper | 604.3 |

| | (248.7 | ) |

| Change in overdraft balances and other | 16.2 |

| | 42.0 |

|

| Net cash provided by (used in) financing activities | (534.8 | ) | | (289.9 | ) |

| Cash and cash equivalents: | |

| | |

|

| Net increase (decrease) in cash and cash equivalents | (827.9 | ) | | (226.8 | ) |

| Effect of foreign exchange rate changes on cash and cash equivalents | 4.4 |

| | 6.1 |

|

| Balance at beginning of year | 1,057.9 |

| | 418.6 |

|

| Balance at end of period | $ | 234.4 |

| | $ | 197.9 |

|

See notes to unaudited condensed consolidated financial statements.

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF STOCKHOLDERS' EQUITY

AND NONCONTROLLING INTERESTS

(IN MILLIONS)

(UNAUDITED)

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | Molson Coors Brewing Company Stockholders' Equity | | |

| | | | | | | | | | | | | | | | Accumulated | | Common Stock | | |

| | | | Common stock | | Exchangeable | | | | | | other | | held in | | Non |

| | | | issued | | shares issued | | Paid-in- | | Retained | | comprehensive | | treasury | | controlling |

| | Total | | Class A | | Class B | | Class A | | Class B | | capital | | earnings | | income (loss) | | Class B | | interests |

| As of December 31, 2017 | $ | 13,187.3 |

| | $ | — |

| | $ | 2.0 |

| | $ | 107.7 |

| | $ | 553.2 |

| | $ | 6,688.5 |

| | $ | 6,958.4 |

| | $ | (860.0 | ) | | $ | (471.4 | ) | | $ | 208.9 |

|

| Shares issued under equity compensation plan | (5.8 | ) | | — |

| | — |

| | — |

| | — |

| | (5.8 | ) | | — |

| | — |

| | — |

| | — |

|

| Amortization of share-based compensation | 14.7 |

| | — |

| | — |

| | — |

| | — |

| | 14.7 |

| | — |

| | — |

| | — |

| | — |

|

| Net income (loss) including noncontrolling interests | 282.5 |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 278.1 |

| | — |

| | — |

| | 4.4 |

|

| Other comprehensive income (loss), net of tax | 49.9 |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 49.1 |

| | — |

| | 0.8 |

|

| Adoption of new accounting pronouncement | (27.8 | ) | | — |

| | — |

| | — |

| | — |

| | — |

| | (27.8 | ) | | — |

| | — |

| | — |

|

| Contributions from noncontrolling interests | 6.4 |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 6.4 |

|

| Distributions and dividends to noncontrolling interests | (2.9 | ) | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (2.9 | ) |

| Dividends declared and paid - $0.41 per share | (88.5 | ) | | — |

| | — |

| | — |

| | — |

| | — |

| | (88.5 | ) | | — |

| | — |

| | — |

|

| As of March 31, 2018 | $ | 13,415.8 |

| | $ | — |

| | $ | 2.0 |

| | $ | 107.7 |

| | $ | 553.2 |

| | $ | 6,697.4 |

|

| $ | 7,120.2 |

|

| $ | (810.9 | ) |

| $ | (471.4 | ) | | $ | 217.6 |

|

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | |

| Molson Coors Brewing Company Stockholders' Equity |

| |

| | |

|

|

|

|

|

|

|

|

| | | | | Accumulated | | Common Stock |

| |

| | |

| Common stock |

| Exchangeable |

|

| | | | other | | held in |

| Non |

| | |

| issued |

| shares issued |

| Paid-in- | | Retained | | comprehensive | | treasury |

| controlling |

| | Total |

| Class A |

| Class B |

| Class A |

| Class B |

| capital | | earnings | | income (loss) | | Class B |

| interests |

| As of December 31, 2018 | $ | 13,735.8 |

|

| $ | — |

|

| $ | 2.0 |

|

| $ | 103.2 |

|

| $ | 557.6 |

|

| $ | 6,773.1 |

| | $ | 7,692.9 |

| | $ | (1,150.0 | ) | | $ | (471.4 | ) |

| $ | 228.4 |

|

| Shares issued under equity compensation plan | (8.2 | ) |

| — |

|

| — |

|

| — |

|

| — |

|

| (8.2 | ) | | — |

| | — |

| | — |

|

| — |

|

| Amortization of share-based compensation | 11.3 |

|

| — |

|

| — |

|

| — |

|

| — |

|

| 11.3 |

| | — |

| | — |

| | — |

|

| — |

|

| Net income (loss) including noncontrolling interests | 149.1 |

|

| — |

|

| — |

|

| — |

|

| — |

|

| — |

| | 151.4 |

| | — |

| | — |

|

| (2.3 | ) |

| Other comprehensive income (loss), net of tax | 42.3 |

|

| — |

|

| — |

|

| — |

|

| — |

|

| — |

| | — |

| | 42.1 |

| | — |

|

| 0.2 |

|

Adoption of lease accounting standard (see Note 2) | 32.0 |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 32.0 |

| | — |

| | — |

| | — |

|

Reclassification of stranded tax effects (see Note 2) | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 74.8 |

| | (74.8 | ) | | — |

| | — |

|

| Contributions from noncontrolling interests | 14.5 |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 14.5 |

|

| Dividends declared and paid - $0.41 per share | (88.7 | ) |

| — |

|

| — |

|

| — |

|

| — |

|

| — |

| | (88.7 | ) | | — |

| | — |

|

| — |

|

| As of March 31, 2019 | $ | 13,888.1 |

|

| $ | — |

|

| $ | 2.0 |

|

| $ | 103.2 |

|

| $ | 557.6 |

|

| $ | 6,776.2 |

| | $ | 7,862.4 |

| | $ | (1,182.7 | ) | | $ | (471.4 | ) |

| $ | 240.8 |

|

See notes to unaudited condensed consolidated financial statements.

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

1. Basis of Presentation and Summary of Significant Accounting Policies

Unless otherwise noted in this report, any description of "we," "us" or "our" includes Molson Coors Brewing Company ("MCBC" or the "Company"), principally a holding company, and its operating and non-operating subsidiaries included within our reporting segments and Corporate. Our reporting segments include: MillerCoors LLC ("MillerCoors" or U.S. segment), operating in the U.S.; Molson Coors Canada ("MCC" or Canada segment), operating in Canada; Molson Coors Europe (Europe segment), operating in Bulgaria, Croatia, Czech Republic, Hungary, Montenegro, the Republic of Ireland, Romania, Serbia, the U.K. and various other European countries; and Molson Coors International ("MCI" or International segment), operating in various other countries.

Unless otherwise indicated, information in this report is presented in USD and comparisons are to comparable prior periods. Our primary operating currencies, other than USD, include the CAD, the GBP, and our Central European operating currencies such as the EUR, CZK, HRK and RSD.

The accompanying unaudited condensed consolidated interim financial statements reflect all adjustments which are necessary for a fair statement of the financial position, results of operations and cash flows for the periods presented in accordance with U.S. GAAP. Such unaudited interim condensed consolidated financial statements have been prepared in accordance with the instructions to Form 10-Q pursuant to the rules and regulations of the SEC. Certain information and footnote disclosures normally included in financial statements prepared in accordance with U.S. GAAP have been condensed or omitted pursuant to such rules and regulations.

These unaudited condensed consolidated interim financial statements should be read in conjunction with our Annual Report on Form 10-K for the year ended December 31, 2018 ("Annual Report"), and have been prepared on a consistent basis with the accounting policies described in Note 1 of the Notes to the Audited Consolidated Financial Statements included in our Annual Report, except as noted below and in Note 2, "New Accounting Pronouncements." The results of operations for the three months ended March 31, 2019 are not necessarily indicative of the results that may be achieved for the full year.

Non-Cash Activity

Non-cash activity includes non-cash issuances of share-based awards, as well as non-cash investing activities related to movements in our guarantee of indebtedness of certain equity method investments. We also had non-cash activities related to capital expenditures incurred but not yet paid of $112.7 million and $140.8 million for the three months ended March 31, 2019 and March 31, 2018, respectively.

Other than the activity mentioned above and the supplemental non-cash activity related to the recognition of leases further discussed below, there was no other significant non-cash activity during the three months ended March 31, 2019 and March 31, 2018. See Note 4, "Investments," and Note 5, "Share-Based Payments" for further discussion. Leases

We account for leases in accordance with Accounting Standards Codification (“ASC”) Topic 842, Leases, which we adopted on January 1, 2019, electing not to adjust comparative periods presented and applying a modified retrospective transition approach as of the effective date of adoption (see Note 2, "New Accounting Pronouncements" for impacts of adoption). We enter into contractual arrangements for the utilization of certain non-owned assets, primarily real estate and equipment, which are evaluated as finance (previously known as capital) or operating leases upon commencement and are accounted for accordingly. Specifically, under ASC 842, a contract is or contains a lease when, (1) the contract contains an explicitly or implicitly identified asset and (2) the customer obtains substantially all of the economic benefits from the use of that underlying asset and directs how and for what purpose the asset is used during the term of the contract in exchange for consideration. We assess whether an arrangement is or contains a lease at inception of the contract. For all contractual arrangements deemed to be leases (other than short-term leases), as of the lease commencement date, we recognize on the consolidated balance sheet a liability for our obligation related to the lease and a corresponding asset representing our right to use the underlying asset over the period of use.

For leases that qualify as short-term leases, we have elected, for all classes of underlying assets, to not apply the balance sheet recognition requirements of ASC 842, and instead, we recognize the lease payments in the consolidated statements of

operations on a straight-line basis over the lease term. We have also made the election, for our real estate and certain equipment classes of underlying assets, to account for lease and non-lease components as a single lease component.

Our leases have remaining lease terms of up to approximately 18 years. Certain of our lease agreements contain options to extend or early terminate the agreement. The lease term used to calculate the right-of-use asset ("ROU") and lease liability at commencement includes the impacts of options to extend or terminate the lease when it is reasonably certain that we will exercise that option. When determining whether it is reasonably certain that we will exercise an option at commencement, we consider various existing economic factors, including real estate strategies, the nature, length, and terms of the agreement, as well as the uncertainty of the condition of leased equipment at the end of the lease term. Based on these determinations, we generally conclude that the exercise of renewal options would not be reasonably certain in determining the lease term at commencement. Assumptions made at the commencement date are re-evaluated upon occurrence of certain events requiring a lease modification. Additionally, for certain equipment leases involving groups of similar leased assets with similar lease terms, we apply a portfolio approach to effectively account for the operating lease ROU assets and liabilities.

The discount rate used to calculate the present value of the future minimum lease payments is the rate implicit in the lease, when readily determinable. As the rate implicit in the lease is not readily determinable for most of our leases, we use our incremental borrowing rate relative to the leased asset.

Certain of our leases include variable lease payments, including payments that depend on an index or rate, as well as variable payments for items such as property taxes, insurance, maintenance, and other operating expenses associated with leased assets. Payments that vary based on an index or rate are included in the measurement of our lease assets and liabilities at the rate as of the commencement date. All other variable lease payments are excluded from the measurement of our lease assets and liabilities and are recognized in the period in which the obligation for those payments is incurred. Our lease agreements do not contain any material residual value guarantees or material restrictive covenants.

Lease-related expense is recorded within either cost of goods sold or marketing, general and administrative expenses on the consolidated statements of operations, depending on the function of the underlying leased asset, with the exception of interest on finance lease liabilities, which is recorded within interest income (expense), net on the consolidated statements of operations.

For the three months ended March 31, 2019, lease expense (including immaterial short-term and variable lease costs) was as follows:

|

| | | |

| | Three Months Ended March 31, 2019 |

| | (In millions) |

| Operating lease expense | $ | 17.2 |

|

| Finance lease expense | 2.8 |

|

| Total lease expense | $ | 20.0 |

|

Supplemental cash flow information related to leases for the three months ended March 31, 2019 was as follows:

|

| | | |

| | Three Months Ended March 31, 2019 |

| | (In millions) |

| Cash paid for amounts included in the measurements of lease liabilities: | |

| Operating cash flows from operating leases | $ | 12.0 |

|

| Operating cash flows from finance leases | $ | 0.8 |

|

| Financing cash flows from finance leases | $ | 0.6 |

|

| Supplemental non-cash information on right-of-use assets obtained in exchange for new lease liabilities: | |

| Operating leases | $ | 10.7 |

|

| Finance leases | $ | — |

|

Supplemental balance sheet information related to leases as of March 31, 2019 was as follows:

|

| | | | |

| | | As of March 31, 2019 |

| | Balance Sheet Classification | (In millions) |

| Operating Leases | | |

| Operating lease right-of-use assets | Other assets | $ | 154.1 |

|

| Current operating lease liabilities | Accounts payable and other current liabilities | $ | 43.6 |

|

| Non-current operating lease liabilities | Other liabilities | 121.4 |

|

| Total operating lease liabilities | | $ | 165.0 |

|

| | | |

| Finance Leases | | |

| Finance lease right-of-use assets | Properties, net | $ | 68.4 |

|

| Current finance lease liabilities | Current portion of long-term debt and short-term borrowings | $ | 3.3 |

|

| Non-current finance lease liabilities | Long-term debt | 82.5 |

|

| Total finance lease liabilities | | $ | 85.8 |

|

The weighted-average remaining lease term and discount rate as of March 31, 2019 are as follows:

|

| | | |

| | Weighted-Average Remaining Lease Term (Years) | | Weighted-Average Discount Rate |

| Operating leases | 4.8 | | 4.2% |

| Finance leases | 10.1 | | 6.4% |

Based on foreign exchange rates as of March 31, 2019, maturities of lease liabilities were as follows: |

| | | | | | | |

| | Operating Leases | | Finance Leases |

| | (In millions) |

| 2019 - remaining | $ | 38.4 |

| | $ | 4.5 |

|

| 2020 | 41.9 |

| | 36.3 |

|

| 2021 | 34.7 |

| | 6.0 |

|

| 2022 | 27.1 |

| | 5.9 |

|

| 2023 | 18.9 |

| | 5.9 |

|

| Thereafter | 21.0 |

| | 66.0 |

|

| Total lease payments | $ | 182.0 |

| | $ | 124.6 |

|

| Less: interest | (17.0 | ) | | (38.8 | ) |

| Present value of lease liabilities | $ | 165.0 |

| | $ | 85.8 |

|

Executed leases that have not yet commenced as of March 31, 2019 are immaterial.

Information as of December 31, 2018, as well as comparative interim period information under historical lease accounting guidance

Gross assets recorded under finance leases as of December 31, 2018 were $82.5 million. The associated accumulated amortization on these assets as of December 31, 2018 was $13.2 million. These amounts are recorded within properties, net on the consolidated balance sheet. Current and non-current finance lease liabilities as of December 31, 2018 were $3.2 million and $82.1 million, respectively, and were recorded in accounts payable and other current liabilities and other non-current liabilities, respectively, on the consolidated balance sheet. Separately, during the three months ended March 31, 2018, non-cash activities related to the recognition of finance leases was $15.0 million.

Based on foreign exchange rates as of December 31, 2018, future minimum lease payments under operating leases that have initial or remaining non-cancelable terms in excess of one year, as well as finance leases, are as follows:

|

| | | | | | | |

| | Operating Leases | | Finance Leases |

| Year | (In millions) |

| 2019 | $ | 49.4 |

| | $ | 6.1 |

|

| 2020 | 40.2 |

| | 36.2 |

|

| 2021 | 32.6 |

| | 5.9 |

|

| 2022 | 24.6 |

| | 5.9 |

|

| 2023 | 17.0 |

| | 5.8 |

|

| Thereafter | 21.0 |

| | 64.2 |

|

| Total future minimum lease payments | $ | 184.8 |

| | $ | 124.1 |

|

| Less: interest on finance leases | | | (38.8 | ) |

| Present value of future minimum finance lease payments | | | $ | 85.3 |

|

2. New Accounting Pronouncements

New Accounting Pronouncements Recently Adopted

Leases

In February 2016, the FASB issued authoritative guidance intended to increase transparency and comparability among organizations by requiring the recognition of lease assets and liabilities on the balance sheet and disclosure of key information about leasing arrangements. We adopted this guidance and all related amendments applying the modified retrospective transition approach to all lease arrangements as of the effective date of adoption, January 1, 2019. As permitted under the guidance, financial statements for reporting periods beginning after January 1, 2019 are presented under the new guidance, while prior period amounts have not been adjusted and continue to be reported and disclosed in accordance with historical accounting guidance. Additionally, for existing leases as of the effective date, we have elected the package of practical expedients available at transition to not reassess the historical lease determination, lease classification and initial direct costs.

For operating leases, the adoption of the new guidance resulted in the recognition of ROU assets of approximately $154 million and aggregate current and non-current lease liabilities of approximately $164 million, as of January 1, 2019, including immaterial reclassifications of prepaid and deferred rent balances into ROU assets. Separately, as a result of the cumulative impact of adopting the new guidance, we recorded a net increase to opening retained earnings of approximately $32 million as of January 1, 2019 with the offsetting impact within other assets, related to our share of the accelerated recognition of deferred gains on non-qualifying and other sale-leaseback transactions by an equity method investment within our Canada segment. Additionally, while our accounting for finance leases remains unchanged at adoption, we have prospectively changed the presentation of finance lease liabilities within the consolidated balance sheets to be presented within current portion of long-term debt and short-term borrowings, and long-term debt, as appropriate. As of January 1, 2019, we reclassified approximately $3 million and $82 million of short-term and long-term finance lease liabilities from accounts payable and other current liabilities and other non-current liabilities to current portion of long-term debt and short-term borrowings and long-term debt, respectively. The adoption of this guidance had no impact to our cash flows from operating, investing, or financing activities. See Note 1, “Basis of Presentation and Summary of Significant Accounting Policies” for additional discussion on our leasing arrangements. Accumulated Other Comprehensive Income (Loss)

In February 2018, the FASB issued authoritative guidance intended to improve the usefulness of financial information related to the enactment of the 2017 Tax Act. This guidance provides an option to reclassify from AOCI to retained earnings the stranded tax effects resulting from the change in the U.S. federal corporate income tax rate as a result of the 2017 Tax Act. We adopted this guidance as of January 1, 2019 and elected to reclassify stranded tax effects related to the 2017 Tax Act, resulting in an approximate $75 million increase to retained earnings in the period of adoption. Our policy is to release stranded tax effects from AOCI using either a specific identification approach or portfolio approach based on the nature of the underlying item.

New Accounting Pronouncements Not Yet Adopted

In August 2018, the FASB issued authoritative guidance intended to address a customer’s accounting for implementation costs incurred in a cloud computing arrangement that is a service contract. This guidance aligns the requirements for capitalizing implementation costs incurred in a hosting arrangement that is a service contract with the requirements for capitalizing implementation costs incurred to develop or obtain internal-use software. The guidance also requires presentation of the capitalized implementation costs in the statement of financial position and in the statement of cash flows in the same line item that a prepayment for the fees of the associated hosting arrangement would be presented, and the expense related to the capitalized implementation costs to be presented in the same line item in the statement of operations as the fees associated with the hosting element (service) of the arrangement. This guidance is effective for annual periods beginning after December 15, 2019, including interim periods within those annual periods, with early adoption permitted. We are currently evaluating the potential impact on our financial position, results of operations and statement of cash flows upon adoption of this guidance, which will result in the change in presentation of capitalized implementation costs related to hosting arrangements from properties to other assets on the consolidated balance sheet, as well as the expense related to such costs no longer being classified as depreciation expense and cash flows related to those costs no longer being presented as investing activities.

Other than the items noted above, there have been no new accounting pronouncements not yet effective or adopted in the current year that we believe have a significant impact, or potential significant impact, to our unaudited condensed consolidated interim financial statements.

3. Segment Reporting

Our reporting segments are based on the key geographic regions in which we operate, which are the basis on which our chief operating decision maker evaluates the performance of the business. Our reporting segments consist of the U.S., Canada, Europe and International. Corporate is not a reportable segment and primarily includes interest and certain other general and administrative costs that are not allocated to any of the operating segments as well as the results of our water resources and energy operations in Colorado and the unrealized changes in fair value on our commodity swaps not designated in hedging relationships recorded within cost of goods sold, which are later reclassified when realized to the segment in which the underlying exposure resides. Additionally, only the service cost component of net periodic pension and OPEB cost is reported within each operating segment, and all other components are reported within the Corporate segment.

No single customer accounted for more than 10% of our consolidated sales for the three months ended March 31, 2019 or March 31, 2018. Consolidated net sales represent sales to third-party external customers less excise taxes. Inter-segment transactions impacting net sales revenues and income (loss) before income taxes eliminate upon consolidation and are primarily related to U.S. segment sales to the other segments.

The following tables present net sales and income (loss) before income taxes by segment:

|

| | | | | | | |

| | Three Months Ended |

| | March 31, 2019 | | March 31, 2018 |

| | (In millions) |

| U.S. | $ | 1,659.2 |

| | $ | 1,647.8 |

|

| Canada | 261.0 |

| | 283.8 |

|

| Europe | 362.9 |

| | 374.3 |

|

| International | 47.9 |

| | 57.5 |

|

| Corporate | 0.2 |

| | 0.2 |

|

| Inter-segment net sales eliminations | (27.9 | ) | | (32.1 | ) |

| Consolidated net sales | $ | 2,303.3 |

| | $ | 2,331.5 |

|

|

| | | | | | | |

| | Three Months Ended |

| | March 31, 2019 | | March 31, 2018 |

| | (In millions) |

| U.S. | $ | 269.4 |

| | $ | 261.7 |

|

Canada(1) | 21.8 |

| | 9.1 |

|

| Europe | (27.5 | ) | | (29.9 | ) |

| International | (0.3 | ) | | 3.7 |

|

Corporate(2) | (82.1 | ) | | 112.8 |

|

| Consolidated income (loss) before income taxes | $ | 181.3 |

| | $ | 357.4 |

|

| |

| (1) | During the three months ended March 31, 2019, we recorded an unrealized mark-to-market gain of approximately $23 million on the HEXO Corp. ("HEXO") warrants received in connection with the formation of the Truss joint venture. Additionally, during the first quarter of 2019, we received payment and recorded a gain of $1.5 million resulting from a purchase price adjustment related to the historical sale of Molson Inc.’s ownership interest in the Montreal Canadiens, which is considered an affiliate of MCBC. |

| |

| (2) | During the three months ended March 31, 2018, we recorded a gain of $328.0 million related to the Adjustment Amount as defined and further discussed in Note 6, "Special Items." Additionally, related to the unrealized mark-to-market valuation on our commodity hedge positions, we recorded an unrealized gain of $34.1 million during the three months ended March 31, 2019 compared to an unrealized loss of $84.7 million during the three months ended March 31, 2018. |

Income (loss) before income taxes includes the impact of special items. Refer to Note 6, "Special Items" for further discussion. The following table presents total assets by segment:

|

| | | | | | | |

| | As of |

| | March 31, 2019 | | December 31, 2018 |

| | (In millions) |

| U.S. | $ | 19,247.7 |

| | $ | 19,057.1 |

|

| Canada | 4,736.0 |

|

| 4,640.5 |

|

| Europe | 5,334.1 |

|

| 5,430.0 |

|

| International | 277.5 |

|

| 274.1 |

|

| Corporate | 228.3 |

|

| 708.1 |

|

| Consolidated total assets | $ | 29,823.6 |

|

| $ | 30,109.8 |

|

4. Investments

Our investments include both equity method and consolidated investments. Those entities identified as VIEs have been evaluated to determine whether we are the primary beneficiary. The VIEs included under "Consolidated VIEs" below are those for which we have concluded that we are the primary beneficiary and accordingly, we have consolidated these entities. None of our consolidated VIEs held debt as of March 31, 2019 or December 31, 2018. We have not provided any financial support to any of our VIEs during the year that we were not previously contractually obligated to provide. Amounts due to and due from our equity method investments are recorded as affiliate accounts payable and affiliate accounts receivable.

Authoritative guidance related to the consolidation of VIEs requires that we continually reassess whether we are the primary beneficiary of VIEs in which we have an interest. As such, the conclusion regarding the primary beneficiary status is subject to change and we continually evaluate circumstances that could require consolidation or deconsolidation. As of March 31, 2019 and December 31, 2018, our consolidated VIEs are Cobra Beer Partnership, Ltd. ("Cobra U.K."), Grolsch U.K. Ltd. ("Grolsch"), Rocky Mountain Metal Container ("RMMC"), Rocky Mountain Bottle Company ("RMBC") and Truss LP ("Truss"). Our unconsolidated VIEs are Brewers Retail Inc. ("BRI") and Brewers' Distributor Ltd. ("BDL").

Both BRI and BDL have outstanding third party debt which is guaranteed by their respective shareholders. As a result, we have a guarantee liability of $50.1 million and $35.9 million recorded as of March 31, 2019 and December 31, 2018, respectively, which is presented within accounts payable and other current liabilities on the unaudited condensed consolidated balance sheets and represents our proportionate share of the outstanding balance of these debt instruments. The carrying value of the guarantee liability equals fair value, which considers an adjustment for our own non-performance risk and is considered a Level 2 measurement. The offset to the guarantee liability was recorded as an adjustment to our respective equity method investment within the unaudited condensed consolidated balance sheets. The resulting change in our equity method investments during the year due to movements in the guarantee represents a non-cash investing activity.

Consolidated VIEs

The following summarizes the assets and liabilities of our consolidated VIEs (including noncontrolling interests):

|

| | | | | | | | | | | | | | | |

| | As of |

| | March 31, 2019 | | December 31, 2018 |

| | Total Assets | | Total Liabilities | | Total Assets | | Total Liabilities |

| | (In millions) |

| RMMC/RMBC | $ | 212.2 |

| | $ | 31.9 |

| | $ | 189.8 |

| | $ | 35.0 |

|

| Other | $ | 29.5 |

| | $ | 1.7 |

| | $ | 31.0 |

| | $ | 5.1 |

|

5. Share-Based Payments

We have one share-based compensation plan, the MCBC Incentive Compensation Plan (the "Incentive Compensation Plan"), as of March 31, 2019 and all outstanding awards fall under this plan. During the three months ended March 31, 2019 and March 31, 2018, we recognized share-based compensation expense related to the following Class B common stock awards to certain directors, officers and other eligible employees, pursuant to the Incentive Compensation Plan: RSUs, DSUs, PSUs and stock options.

|

| | | | | | | |

| | Three Months Ended |

| | March 31, 2019 | | March 31, 2018 |

| | (In millions) |

| Pretax compensation expense | $ | 11.4 |

| | $ | 14.8 |

|

| Tax benefit | (1.2 | ) | | (1.6 | ) |

| After-tax compensation expense | $ | 10.2 |

| | $ | 13.2 |

|

As of March 31, 2019, there was $61.1 million of total unrecognized compensation expense from all share-based compensation arrangements granted under the Incentive Compensation Plan, related to unvested awards. This total compensation expense is expected to be recognized over a weighted-average period of 2.3 years.

|

| | | | | | | | | |

| | RSUs and DSUs | | PSUs |

| | Units | | Weighted-average grant date fair value per unit | | Units | | Weighted-average grant date fair value per unit |

| | (In millions, except per unit amounts) |

| Non-vested as of December 31, 2018 | 1.0 |

| | $88.53 | | 0.5 |

| | $86.85 |

| Granted | 0.4 |

| | $54.46 | | 0.3 |

| | $53.31 |

| Vested | (0.3 | ) | | $100.91 | | (0.1 | ) | | $90.41 |

| Forfeited | — |

| | $— | | — |

| | $— |

| Non-vested as of March 31, 2019 | 1.1 |

| | $70.06 | | 0.7 |

| | $71.42 |

The weighted-average fair value per unit for the non-vested PSUs is $62.07 as of March 31, 2019.

|

| | | | | | | | | |

| | Stock options |

| | Awards | | Weighted-average exercise price | | Weighted-average remaining contractual life (years) | | Aggregate intrinsic value |

| | (In millions, except per share amounts and years) |

| Outstanding as of December 31, 2018 | 1.3 | | $70.56 | | 5.2 | | $ | 4.3 |

|

| Granted | 0.3 | | $61.09 | | | | |

| Exercised | — | | $— | | | | |

| Forfeited | — | | $— | | | | |

| Outstanding as of March 31, 2019 | 1.6 | | $68.70 | | 6.0 | | $ | 5.4 |

|

| Expected to vest as of March 31, 2019 | 0.5 | | $68.79 | | 9.4 | | $ | — |

|

| Exercisable as of March 31, 2019 | 1.1 | | $68.66 | | 4.3 | | $ | 5.4 |

|

The total intrinsic value of exercises during the three months ended March 31, 2019 and March 31, 2018 were $0.3 million and $4.6 million, respectively. During the three months ended March 31, 2019 and March 31, 2018, total tax benefits realized from share-based awards vested or exercised was $4.0 million and $5.4 million, respectively.

The fair value of each option granted in the first quarter of 2019 and 2018 was determined on the date of grant using the Black-Scholes option-pricing model with the following weighted-average assumptions:

|

| | | |

| | Three Months Ended |

| | March 31, 2019 | | March 31, 2018 |

| Risk-free interest rate | 2.52% | | 2.65% |

| Dividend yield | 4.17% | | 2.08% |

| Volatility range | 24.41%-24.48% | | 22.36%-24.14% |

| Weighted-average volatility | 24.42% | | 22.81% |

| Expected term (years) | 5.3 | | 5.3 |

| Weighted-average fair market value | $9.24 | | $15.44 |

The risk-free interest rates utilized for periods throughout the contractual life of the stock options are based on a zero-coupon U.S. Treasury security yield at the time of grant. Expected volatility is based on a combination of historical and implied volatility of our stock. The expected term of stock options is estimated based upon observations of historical employee option exercise patterns and trends of those employees granted options in the respective year.

The fair value of the market metric for each PSU granted in the first quarter of 2019 and 2018 was determined on the date of grant using a Monte Carlo model to simulate total stockholder return for MCBC and its peer companies with the following weighted-average assumptions:

|

| | | |

| | Three Months Ended |

| | March 31, 2019 | | March 31, 2018 |

| Risk-free interest rate | 2.49% | | 2.34% |

| Dividend yield | 4.17% | | 2.08% |

| Volatility range | 13.82%-42.46% | | 13.03%-81.87% |

| Weighted-average volatility | 24.97% | | 22.76% |

| Expected term (years) | 2.8 | | 2.8 |

| Weighted-average fair market value | $53.31 | | $78.30 |

The risk-free interest rates utilized for periods throughout the expected term of the PSUs are based on a zero-coupon U.S. Treasury security yield at the time of grant. Expected volatility is based on historical volatility of our stock as well as the stock of our peer firms, as shown within the volatility range above, for a period from the grant date consistent with the expected term. The expected term of PSUs is calculated based on the grant date to the end of the performance period.

As of March 31, 2019, there were 2.9 million shares of the Company's Class B common stock available for issuance as awards under the Incentive Compensation Plan.

6. Special Items

We have incurred charges or realized benefits that either we do not believe to be indicative of our core operations, or we believe are significant to our current operating results warranting separate classification. As such, we have separately classified these charges (benefits) as special items.

|

| | | | | | | |

| | Three Months Ended |

| | March 31, 2019 | | March 31, 2018 |

| | (In millions) |

| Employee-related charges | | | |

| Restructuring | $ | 3.7 |

| | $ | 3.9 |

|

Impairments or asset abandonment charges(1) | | | |

| U.S. - Asset abandonment | 0.8 |

| | 1.5 |

|

| Canada - Asset abandonment | 7.6 |

| | 6.1 |

|

| Europe - Asset abandonment | 0.6 |

| | 1.7 |

|

| Termination fees and other (gains) losses | | | |

| International | 0.3 |

| | — |

|

Purchase price adjustment settlement gain(2) | — |

| | (328.0 | ) |

| Total Special items, net | $ | 13.0 |

| | $ | (314.8 | ) |

| |

| (1) | Charges for the three months ended March 31, 2019 and March 31, 2018 consist primarily of accelerated depreciation in excess of normal depreciation related to the closure of the Colfax, California cidery, which was completed during the first quarter of 2019, the planned closures of the Vancouver and Montreal breweries, which are currently expected to occur in 2019 and 2021, respectively, as well as the Burton South, U.K. brewery which closed in the first quarter of 2018. |

| |

| (2) | During the first quarter of 2018, we received $330.0 million from ABI, of which $328.0 million constituted a purchase price adjustment (the "Adjustment Amount"), related to the Miller International Business which was acquired in our acquisition of the remaining portion of MillerCoors which occurred on October 11, 2016. As this settlement occurred following the finalization of purchase accounting, we recorded the settlement proceeds related to the Adjustment Amount as a gain within special items, net in our unaudited condensed consolidated statement of operations in our Corporate segment and within cash provided by operating activities in our unaudited condensed consolidated statement of cash flows for the three months ended March 31, 2018. |

Restructuring Activities

There were no material changes to our restructuring activities since December 31, 2018, as reported in Part II - Item 8. Financial Statements and Supplementary Data, Note 7, "Special Items" in our Annual Report. We continually evaluate our cost structure and seek opportunities for further efficiencies and cost savings as part of ongoing and new initiatives. As such, we may incur additional restructuring related charges or adjustments to previously recorded charges in the future, however, we are unable to estimate the amount of charges at this time.

The accrued restructuring balances below represent expected future cash payments required to satisfy the remaining severance obligations to terminated employees, the majority of which we expect to be paid in the next 12 months.

|

| | | | | | | | | | | | | | | | | | | | | | | |

| | U.S. | | Canada | | Europe | | International | | Corporate | | Total |

| | (In millions) |

| As of December 31, 2018 | $ | 21.6 |

| | $ | 1.5 |

| | $ | 0.6 |

| | $ | 0.6 |

| | $ | 1.3 |

| | $ | 25.6 |

|

| Charges incurred and changes in estimates | 0.6 |

| | — |

| | 2.7 |

| | 0.1 |

| | 0.3 |

| | 3.7 |

|

| Payments made | (11.6 | ) | | (0.1 | ) | | (0.8 | ) | | (0.1 | ) | | (0.3 | ) | | (12.9 | ) |

| As of March 31, 2019 | $ | 10.6 |

|

| $ | 1.4 |

| | $ | 2.5 |

| | $ | 0.6 |

| | $ | 1.3 |

| | $ | 16.4 |

|

|

| | | | | | | | | | | | | | | | | | | | | | | |

| | U.S. | | Canada | | Europe | | International | | Corporate | | Total |

| | (In millions) |

| As of December 31, 2017 | $ | 0.6 |

| | $ | 4.3 |

| | $ | 1.8 |

| | $ | 0.2 |

| | $ | — |

| | $ | 6.9 |

|

| Charges incurred and changes in estimates | — |

| | (0.5 | ) | | 3.4 |

| | 1.0 |

| | — |

| | 3.9 |

|

| Payments made | (0.3 | ) | | (0.9 | ) | | (0.6 | ) | | (0.2 | ) | | — |

| | (2.0 | ) |

| Foreign currency and other adjustments | — |

| | (0.1 | ) | | — |

| | — |

| | — |

| | (0.1 | ) |

| As of March 31, 2018 | $ | 0.3 |

|

| $ | 2.8 |

| | $ | 4.6 |

| | $ | 1.0 |

| | $ | — |

| | $ | 8.7 |

|

7. Income Tax

|

| | | | | |

| | Three Months Ended |

| | March 31, 2019 | | March 31, 2018 |

| Effective tax rate | 18 | % | | 21 | % |

The decrease in the effective tax rate during the first quarter of 2019 versus 2018 was primarily driven by the impact of discrete items. Specifically, during the first quarter of 2019, we recognized a net discrete tax benefit of $1.2 million, versus a $5.5 million net discrete tax expense recognized in the first quarter of 2018.

Our tax rate is volatile and may increase or decrease with changes in, among other things, the amount and source of income or loss, our ability to utilize foreign tax credits, excess tax benefits or deficiencies from share-based compensation, changes in tax laws, and the movement of liabilities established pursuant to accounting guidance for uncertain tax positions as statutes of limitations expire, positions are effectively settled, or when additional information becomes available. There are proposed or pending tax law changes in various jurisdictions and other changes to regulatory environments in countries in which we do business that, if enacted, may have an impact on our effective tax rate. Additionally, we continue to monitor the 2017 Tax Act, including proposed regulations which may change upon finalization, as well as yet to be issued regulations and interpretations. If the forthcoming regulations and interpretations change relative to our current understanding and initial assessment of the impacts of the 2017 Tax Act, the resulting impacts could have a material adverse impact on our effective tax rate.

8. Goodwill and Intangible Assets

|

| | | | | | | | | | | | | | | | | | | |

| | U.S. | | Canada | | Europe | | International | | Consolidated |

| Changes in Goodwill: | | | (In millions) |

| As of December 31, 2018 | $ | 5,928.5 |

| | $ | 856.6 |

| | $ | 1,469.4 |

| | $ | 6.3 |

| | $ | 8,260.8 |

|

| Foreign currency translation | — |

| | 18.5 |

| | 0.1 |

| | — |

| | 18.6 |

|

| As of March 31, 2019 | $ | 5,928.5 |

|

| $ | 875.1 |

| | $ | 1,469.5 |

| | $ | 6.3 |

| | $ | 8,279.4 |

|

The following table presents details of our intangible assets, other than goodwill, as of March 31, 2019:

|

| | | | | | | | | | | | | |

| | Useful life | | Gross | | Accumulated amortization | | Net |

| | (Years) | | (In millions) |

| Intangible assets subject to amortization: | | | | | | | |

| Brands | 10 - 50 | | $ | 5,013.8 |

| | $ | (737.0 | ) | | $ | 4,276.8 |

|

| License agreements and distribution rights | 15 - 28 | | 222.8 |

| | (99.5 | ) | | 123.3 |

|

| Other | 2 - 40 | | 129.2 |

| | (35.6 | ) | | 93.6 |

|

| Intangible assets not subject to amortization: | | | | | | | |

| Brands | Indefinite | | 8,160.5 |

| | — |

| | 8,160.5 |

|

| Distribution networks | Indefinite | | 757.8 |

| | — |

| | 757.8 |

|

| Other | Indefinite | | 337.6 |

| | — |

| | 337.6 |

|

| Total | | | $ | 14,621.7 |

| | $ | (872.1 | ) | | $ | 13,749.6 |

|

The following table presents details of our intangible assets, other than goodwill, as of December 31, 2018:

|

| | | | | | | | | | | | | |

| | Useful life | | Gross | | Accumulated amortization | | Net |

| | (Years) | | (In millions) |

| Intangible assets subject to amortization: | | | | | | | |

| Brands | 10 - 50 | | $ | 4,988.0 |

| | $ | (682.4 | ) | | $ | 4,305.6 |

|

| License agreements and distribution rights | 15 - 28 | | 220.2 |

| | (95.7 | ) | | 124.5 |

|

| Other | 2 - 40 | | 129.2 |

| | (32.2 | ) | | 97.0 |

|

| Intangible assets not subject to amortization: | | | | | | | |

| Brands | Indefinite | | 8,169.9 |

| | — |

| | 8,169.9 |

|

| Distribution networks | Indefinite | | 741.8 |

| | — |

| | 741.8 |

|

| Other | Indefinite | | 337.6 |

| | — |

| | 337.6 |

|

| Total | | | $ | 14,586.7 |

| | $ | (810.3 | ) | | $ | 13,776.4 |

|

The changes in the gross carrying amounts of intangibles from December 31, 2018 to March 31, 2019 are primarily driven by the impact of foreign exchange rates, as a significant amount of intangibles are denominated in foreign currencies.

Based on foreign exchange rates as of March 31, 2019, the estimated future amortization expense of intangible assets is as follows:

|

| | | | |

| Fiscal year | | Amount |

| | | (In millions) |

| 2019 - remaining | | $ | 165.8 |

|

| 2020 | | $ | 220.1 |

|

| 2021 | | $ | 213.8 |

|

| 2022 | | $ | 209.2 |

|

| 2023 | | $ | 208.2 |

|

Amortization expense of intangible assets was $55.4 million and $56.6 million for the three months ended March 31, 2019 and March 31, 2018, respectively. This expense is primarily presented within marketing, general and administrative expenses on the unaudited condensed consolidated statements of operations.

Annual Goodwill and Indefinite-Lived Intangible Impairment Testing

We completed our required annual goodwill and indefinite-lived intangible impairment testing as of October 1, 2018, the first day of our fourth quarter and concluded there were no impairments of goodwill within our reporting units or our indefinite-lived intangible assets. The fair value of the U.S., Europe and Canada reporting units were estimated at approximately 19%, 11% and 6% in excess of carrying value, respectively, as of the October 1, 2018 testing date, resulting in our Europe and Canada reporting units now being considered at risk of impairment.

Key Assumptions

Fair value determinations require considerable judgment and are sensitive to changes in underlying assumptions and factors. The key assumptions used to derive the estimated fair values of our reporting units and indefinite-lived intangibles are discussed in Part II—Item 8 Financial Statements, Note 10, "Goodwill and Intangible Assets" in our Annual Report.

Based on known facts and circumstances, we evaluate and consider recent events and uncertain items, as well as related potential implications, as part of our annual assessment and incorporate into the analyses as appropriate. These facts and circumstances are subject to change and may impact future analyses.

While historical performance and current expectations have resulted in fair values of our reporting units and indefinite-lived intangible assets in excess of carrying values, if our assumptions are not realized, it is possible that an impairment charge may need to be recorded in the future.

Definite-Lived Intangibles

Regarding definite-lived intangibles, we continuously monitor the performance of the underlying assets for potential triggering events suggesting an impairment review should be performed. No such triggering events were identified in the first quarter of 2019 that resulted in an impairment.

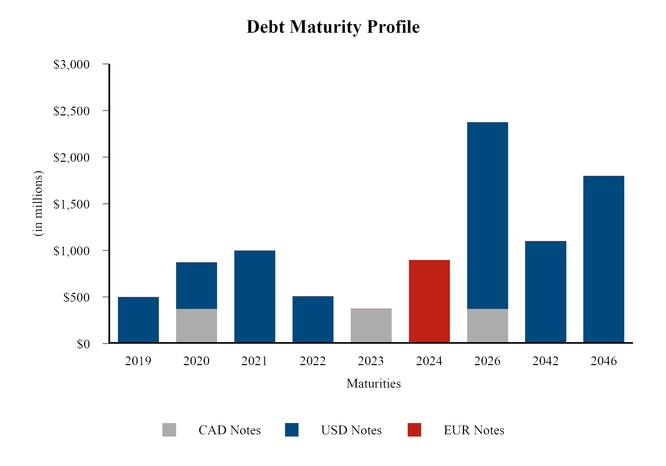

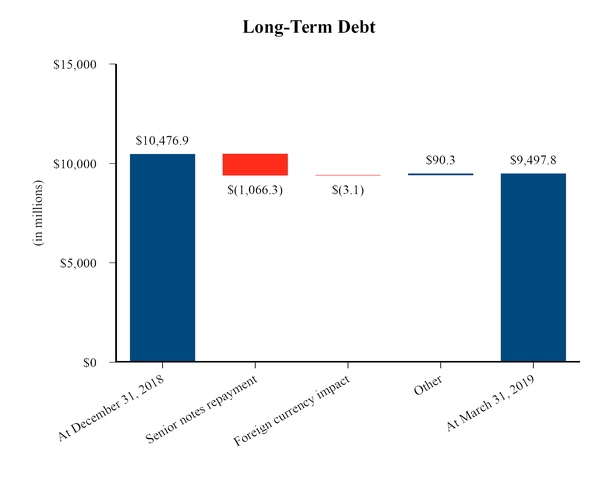

9. Debt

Debt obligations

|

| | | | | | | |

| | As of |

| | March 31, 2019 | | December 31, 2018 |

| | (In millions) |

| Long-term debt: | | | |

| CAD 500 million 2.75% notes due 2020 | $ | 374.6 |

| | $ | 366.6 |

|

| CAD 500 million 2.84% notes due 2023 | 374.6 |

| | 366.6 |

|

| CAD 500 million 3.44% notes due 2026 | 374.6 |

| | 366.6 |

|

| $500 million 1.45% notes due 2019 | 500.0 |

| | 500.0 |

|

| $500 million 1.9% notes due 2019 | — |

| | 499.8 |

|

$500 million 2.25% notes due 2020(1)(2) | 499.2 |

| | 499.0 |

|

$1.0 billion 2.1% notes due 2021(2) | 1,000.0 |

| | 1,000.0 |

|

$500 million 3.5% notes due 2022(1) | 508.6 |

| | 509.3 |

|

| $2.0 billion 3.0% notes due 2026 | 2,000.0 |

| | 2,000.0 |

|

| $1.1 billion 5.0% notes due 2042 | 1,100.0 |

| | 1,100.0 |

|

| $1.8 billion 4.2% notes due 2046 | 1,800.0 |

| | 1,800.0 |

|

| EUR 500 million notes due 2019 | — |

| | 573.4 |

|

| EUR 800 million 1.25% notes due 2024 | 897.4 |

| | 917.4 |

|

Finance leases and other(3) | 131.3 |

| | 43.0 |

|

| Less: unamortized debt discounts and debt issuance costs | (62.5 | ) | | (64.8 | ) |

| Total long-term debt (including current portion) | 9,497.8 |

| | 10,476.9 |

|

| Less: current portion of long-term debt | (1,013.0 | ) | | (1,583.1 | ) |

| Total long-term debt | $ | 8,484.8 |

| | $ | 8,893.8 |

|

| | | | |

| Short-term borrowings: | | | |

Commercial paper program(4) | $ | 604.2 |

| | $ | — |

|

Other short-term borrowings(5) | 23.9 |

| | 11.4 |

|

| Current portion of long-term debt | 1,013.0 |

| | 1,583.1 |

|

| Current portion of long-term debt and short-term borrowings | $ | 1,641.1 |

| | $ | 1,594.5 |

|

| |

| (1) | The fair value hedges related to these notes have been settled and are being amortized over the life of the respective note. |

| |

| (2) | During the first quarter of 2019, we entered into cross currency swaps in order to hedge a portion of the foreign currency translational impacts of our European investment. As a result of the swaps, we economically converted a portion of our $1.0 billion 2.1% senior notes due 2021 and associated interest to EUR denominated, which will result in a EUR interest rate to be received at 0.71%. As of March 31, 2019, we also held outstanding cross currency swaps on our $500 million 2.25% notes due 2020 which resulted in a EUR interest rate to be received of 0.85%. See Note 12, "Derivative Instruments and Hedging Activities" for further details. |

| |

| (3) | As of January 1, 2019, we reclassified approximately $3 million and $82 million of short-term and long-term finance lease liabilities from accounts payable and other current liabilities and other non-current liabilities to current portion of long-term debt and short-term borrowings and long-term debt, respectively, in connection with our adoption of the new lease accounting standard. See Note 2, "New Accounting Pronouncements" for further details. |

| |

| (4) | During the first quarter of 2019, we used proceeds from the issuance of commercial paper to partially fund the repayment of our notes upon maturity. As of March 31, 2019, the outstanding borrowings under our commercial paper program had a weighted-average effective interest rate and tenor of 2.91% and 33 days, respectively. |

| |

| (5) | As of March 31, 2019, we had $11.6 million in bank overdrafts and $40.4 million in bank cash related to our cross-border, cross-currency cash pool, for a net positive position of $28.8 million. As of December 31, 2018, we had $1.1 million in bank overdrafts and $88.9 million in bank cash related to our cross-border, cross-currency cash pool for a net positive position of $87.8 million. We had total outstanding borrowings of $8.1 million and $7.3 million under our two JPY overdraft facilities as of March 31, 2019 and December 31, 2018, respectively. In addition, we have USD and CAD lines of credit under which we had no borrowings as of March 31, 2019 or December 31, 2018. |

Debt Fair Value Measurements

We utilize market approaches to estimate the fair value of certain outstanding borrowings by discounting anticipated future cash flows derived from the contractual terms of the obligations and observable market interest and foreign exchange rates. As of March 31, 2019 and December 31, 2018, the fair value of our outstanding long-term debt (including the current portion of long-term debt) was approximately $9.1 billion and $9.9 billion, respectively. All senior notes are valued based on significant observable inputs and classified as Level 2 in the fair value hierarchy. The carrying values of all other outstanding long-term borrowings and our short-term borrowings approximate their fair values and are also classified as Level 2 in the fair value hierarchy.

Revolving Credit Facility

As of March 31, 2019, we had $895.8 million available to draw under our $1.5 billion revolving credit facility, as the borrowing capacity is reduced by borrowings under our commercial paper program. We had no other borrowings drawn on this revolving credit facility as of March 31, 2019. We had no borrowings drawn on this revolving credit facility as of December 31, 2018.

The maximum leverage ratio of this facility is 4.75x debt to EBITDA, with a decline to 4.00x debt to EBITDA as of the last day of the fiscal quarter ending December 31, 2020.

Under the terms of each of our debt facilities, we must comply with certain restrictions. These include customary events of default and specified representations and warranties and covenants, including, among other things, covenants that restrict our ability to incur certain additional priority indebtedness, create or permit liens on assets, or engage in mergers or consolidations. As of March 31, 2019, we were in compliance with all of these restrictions and have met all debt payment obligations. All of our outstanding senior notes as of March 31, 2019 rank pari-passu.

10. Inventories

|

| | | | | | | |

| | As of |

| | March 31, 2019 | | December 31, 2018 |

| | (In millions) |

| Finished goods | $ | 314.2 |

| | $ | 229.8 |

|

| Work in process | 86.3 |

| | 83.4 |

|

| Raw materials | 219.7 |

| | 224.3 |

|

| Packaging materials | 67.7 |

| | 54.3 |

|

| Inventories, net | $ | 687.9 |

| | $ | 591.8 |

|

11. Accumulated Other Comprehensive Income (Loss)

|

| | | | | | | | | | | | | | | | | | | |

| | MCBC shareholders |

| | Foreign currency translation adjustments | | Gain (loss) on derivative and non-derivative instruments | | Pension and postretirement benefit adjustments | | Equity method investments | | Accumulated other comprehensive income (loss) |

| | (In millions) |

| As of December 31, 2018 | $ | (744.7 | ) | | $ | (17.8 | ) | | $ | (327.2 | ) | | $ | (60.3 | ) | | $ | (1,150.0 | ) |

| Foreign currency translation adjustments | 4.6 |

| | 72.8 |

| | — |

| | — |

| | 77.4 |

|

| Unrealized gain (loss) on derivative instruments | — |

| | (39.4 | ) | | — |

| | — |

| | (39.4 | ) |

| Reclassification of derivative (gain) loss to income | — |

| | 0.1 |

| | — |

| | — |

| | 0.1 |

|

| Amortization of net prior service (benefit) cost and net actuarial (gain) loss to income | — |

| | — |

| | (0.9 | ) | | — |

| | (0.9 | ) |

| Ownership share of unconsolidated subsidiaries' other comprehensive income (loss) | — |

| | — |

| | — |

| | 1.4 |

| | 1.4 |

|

| Tax benefit (expense) | 12.1 |

| | (8.5 | ) | | 0.3 |

| | (0.4 | ) | | 3.5 |

|

| Net current-period other comprehensive income (loss) | 16.7 |

| | 25.0 |

| | (0.6 | ) | | 1.0 |

| | 42.1 |

|

Reclassification of stranded tax effects (see Note 2) | (61.0 | ) | | (16.1 | ) | | 2.3 |

| | — |

| | (74.8 | ) |

| As of March 31, 2019 | $ | (789.0 | ) | | $ | (8.9 | ) | | $ | (325.5 | ) | | $ | (59.3 | ) | | $ | (1,182.7 | ) |

Reclassifications from AOCI to income:

|

| | | | | | | | | |

| | Three Months Ended | | |

| | March 31, 2019 | | March 31, 2018 | | |

| | Reclassifications from AOCI | | Location of gain (loss) recognized in income |

| | (In millions) | | |

| Gain/(loss) on cash flow hedges: | | | | | |

| Forward starting interest rate swaps | $ | (0.7 | ) | | $ | (0.8 | ) | | Interest expense, net |

| Foreign currency forwards | 0.8 |

| | (0.6 | ) | | Cost of goods sold |

| Foreign currency forwards | (0.2 | ) | | — |

| | Other income (expense), net |

| Total income (loss) reclassified, before tax | (0.1 | ) | | (1.4 | ) | | |

| Income tax benefit (expense) | — |

| | 0.3 |

| | |

| Net income (loss) reclassified, net of tax | $ | (0.1 | ) | | $ | (1.1 | ) | | |

| | | | | | |

| Amortization of defined benefit pension and other postretirement benefit plan items: | | | | | |

| Prior service benefit (cost) | $ | (0.1 | ) | | $ | (0.2 | ) | | Other pension and postretirement benefits (costs), net |

| Curtailment and net actuarial gain (loss) | 1.0 |

| | (1.7 | ) | | Other pension and postretirement benefits (costs), net |

| Total income (loss) reclassified, before tax | 0.9 |

| | (1.9 | ) | | |

| Income tax benefit (expense) | (0.3 | ) | | 0.2 |

| | |

| Net income (loss) reclassified, net of tax | $ | 0.6 |

| | $ | (1.7 | ) | | |

| | | | | | |

| Total income (loss) reclassified, net of tax | $ | 0.5 |

| | $ | (2.8 | ) | | |

12. Derivative Instruments and Hedging Activities