UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811- 2485

John Hancock Current Interest

(Exact name of registrant as specified in charter)

601 Congress Street, Boston, Massachusetts 02210

(Address of principal executive offices) (Zip code)

Salvatore Schiavone, Treasurer

601 Congress Street

Boston, Massachusetts 02210

(Name and address of agent for service)

Registrant's telephone number, including area code: 617-663-4497

| Date of fiscal year end: | | March 31 |

| | | |

| Date of reporting period: | | September 30, 2018 |

ITEM 1. REPORTS TO STOCKHOLDERS.

John Hancock

Money Market Fund

Semiannual report 9/30/18

A message to shareholders

Dear shareholder,

It's been a challenging time for fixed-income investors, as both short- and long-term yields rose steadily higher. Inflation fears sparked a sell-off in credit segments of the markets earlier this year, while a strong economy led the U.S. Federal Reserve (Fed) to continue normalizing monetary policy. The Fed raised interest rates by a quarter point twice during the period and indicated that it may increase rates again in December.

Measured rate increases are generally good news for the economy, particularly as short-term debt instruments are offering higher interest rates and can provide a safer haven to investors who are spooked by market volatility.

Your best resource in unpredictable and volatile markets is your financial advisor, who can help position your portfolio so that it's sufficiently diversified to meet your long-term objectives and to withstand the inevitable turbulence along the way.

On behalf of everyone at John Hancock Investments, I'd like to take this opportunity to welcome new shareholders and to thank existing shareholders for the continued trust you've placed in us.

Sincerely,

Andrew G. Arnott

President and CEO,

John Hancock Investments

Head of Wealth and Asset Management,

United States and Europe

This commentary reflects the CEO's views, which are subject to change at any time. Investing involves risks, including the potential loss of principal. Diversification does not guarantee a profit or eliminate the risk of a loss. It is not possible to invest directly into an index. For more up-to-date information, please visit our website at jhinvestments.com.

John Hancock

Money Market Fund

Table of contents

| | | |

| 2 | | Your fund at a glance |

| 4 | | Discussion of fund performance |

| 8 | | Your expenses |

| 10 | | Fund's investments |

| 13 | | Financial statements |

| 16 | | Financial highlights |

| 19 | | Notes to financial statements |

| 24 | | Continuation of investment advisory and subadvisory agreements |

| 30 | | More information |

SEMIANNUAL REPORT | �� JOHN HANCOCK MONEY MARKET FUND 1

INVESTMENT OBJECTIVE

The fund seeks the maximum current income that is consistent with maintaining liquidity and preserving capital.

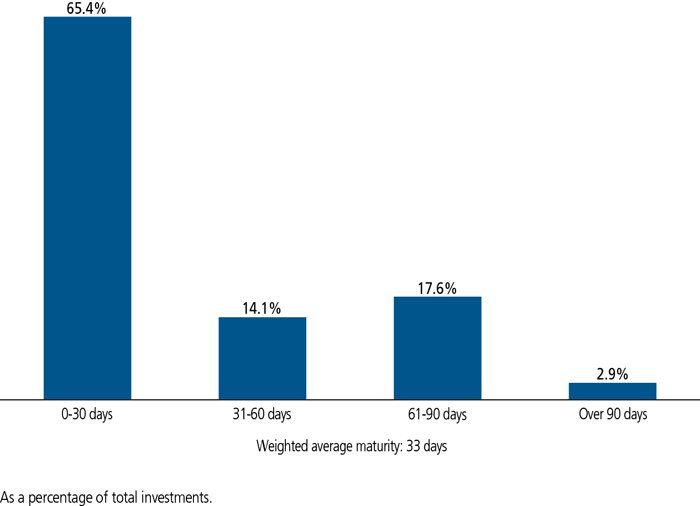

MATURITY COMPOSITION AS OF 9/30/18

SEMIANNUAL REPORT | JOHN HANCOCK MONEY MARKET FUND 2

PERFORMANCE HIGHLIGHTS OVER THE LAST SIX MONTHS

The U.S. Federal Reserve (Fed) continued to tighten its monetary policy

The Fed raised the federal funds target rate by a quarter point at its June and September meetings, bringing the benchmark rate to a range of 2.00% to 2.25%.

Money-market yields remained in an uptrend

The Fed's interest-rate increases helped push short-term yields to their highest level since 2008.

The fund maintained an active approach

We continued to seek opportunities to add incremental yield through individual security selection, adjustments to the portfolio's weighted average maturity, and shifts between fixed- and floating-rate notes.

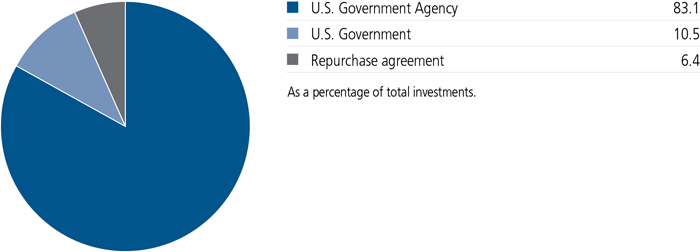

PORTFOLIO COMPOSITION AS OF 9/30/18 (%)

A note about risks

The fund may be subject to various risks as described in the fund's prospectus. For more information, please refer to the "Principal risks" section of the prospectus.

SEMIANNUAL REPORT | JOHN HANCOCK MONEY MARKET FUND 3

Discussion of fund performance

An interview with Portfolio Manager Jeffrey N. Given, CFA, John Hancock Asset Management a division of Manulife Asset Management (US) LLC

Jeffrey N. Given, CFA

Portfolio Manager

John Hancock Asset Management

Can you describe some of the key market events that occurred during the six months ended September 30, 2018?

The U.S. Federal Reserve's (Fed's) ongoing monetary policy tightening continued to be a key factor for the money markets. The Federal Open Market Committee (FOMC), which sets the Fed's rate policy, raised the federal funds target range by a quarter of a percentage point at its meetings on June 14 and September 27, 2018. The two hikes brought the benchmark rate to a range of 2.00% to 2.25%, the highest level since early 2008. The Fed has now enacted eight quarter-point rate increases since it first began to move off its post-crisis zero interest-rate policy in late 2015.

When assessing Fed policy, it's important keep in mind the target range for overnight rates isn't the only tool the Fed uses to affect monetary policy. Its ongoing plan of letting Treasury and government agency securities roll off its balance sheet—the unwinding of the quantitative easing policy that was in effect from 2008 to 2014—can also lead to higher market rates. (The fewer securities held by the Fed, the more supply the market needs to absorb. Added supply can pressure prices, causing yields to rise.) In the third calendar quarter alone, $120 billion matured off the Fed's balance sheet.

With this as the backdrop, the one-month London Interbank Offered Rate (LIBOR)—a key basis for money market rates—moved from 1.88% on March 31, 2018 to 2.26% at the end of September 2018, while three-month LIBOR rose from 2.31% to 2.40%.

The larger increase for one-month rates reflects a decrease in Treasury bill issuance from the highs reached in the first quarter of 2018. The elevated supply led to significant market disruptions in

SEMIANNUAL REPORT | JOHN HANCOCK MONEY MARKET FUND 4

March, with the spread between LIBOR and the Overnight Index Swap rate, or OIS, climbing to levels last seen in the 2007-2008 financial crisis. (OIS is the rate used for overnight lending between banks.) Once supply eased, market conditions returned to normal and remained so for the rest of the semiannual period. The U.S. Department of the Treasury appears to be on track for T-bill issuance of about $250 to $300 billion above typical levels in 2019. This above-average new issue supply could put downward pressure on the prices of money market securities, leading to higher yields.

The money market reforms enacted in October 2016 initially led to a shift out of prime funds and into government funds. Since mid-2017, however, there has been a gradual and persistent flow of assets into prime funds. For instance, prime assets under management grew by $83 billion to $536 billion year to date through September 30, 2018, while government and agency money market fund assets shrank by $50 billion to $1.49 billion. This trend largely reflected investors' growing comfort with prime funds, together with the funds' slightly higher yields.

How was the fund positioned during the period?

The fund entered the period with a longer-than-normal weighted average maturity (WAM), which was designed to capture value on the 6- to 12-month part of the curve relative to shorter-term issues. We allowed the fund's WAM to decline in the early part of the second calendar quarter, which reflected our view the Fed would hike rates at its June meeting. When the Fed raised interest rates in June, we quickly deployed the cash balances we had built up prior to the rate hike at new, higher yields. In the process, we reduced the fund's WAM. Later in the period, we raised WAM to a longer-than-normal level going into the September interest-rate hike. As a result, we were able to lock in higher yields at levels that had already priced in a September (and in some cases also a December) Fed rate increase. The net result of these shifts was a decrease in the fund's WAM from the beginning of the period to its level on September 30, 2018.

SEMIANNUAL REPORT | JOHN HANCOCK MONEY MARKET FUND 5

"... we continued to look for opportunities to add incremental yield through individual security selection, adjustments to the portfolio's weighted average maturity, and shifts between fixed- and floating-rate notes."

In terms of the fund's weighting in floating-rate versus fixed-rate notes, we kept the allocation to the former category at a relatively consistent level between 30% and 36% of assets. We believe this was the appropriate positioning given that the Fed has followed a fairly predictable schedule of interest-rate hikes.

In early August, we took the opportunity to participate in the first sale of a security tied to the new Secured Overnight Financing Rate (SOFR) index, the rate most likely to replace LIBOR when the latter is discontinued after 2021. These floating-rate notes, which were issued by the Federal National Mortgage Association (Fannie Mae), offered an attractive yield spread versus overnight rates. The phased transition from LIBOR to SOFR is ahead of schedule. Since daily publication of the overnight SOFR rate began in April, a futures market has been created and issuance of SOFR floating-rate notes (such as the one we added to the portfolio) has begun. We expect more new issuance tied to SOFR as we move closer to the discontinuation of LIBOR in 2021.

What other factors were you monitoring as the period drew to a close?

The rise in short-term rates has led to renewed competition between bank deposit rates and money market funds. The latter usually respond more quickly to Fed rate hikes, leading to more attractive relative yields. We intend to monitor the data closely for signs of an increase in the amount of assets moving out of banks and into the money markets.

The FOMC's summary of economic projections indicates that another rate hike is expected in 2018 (most likely in December) and that the Fed will continue unwinding its quantitative easing policy. In addition, the consensus at the close of the period was that three more rate hikes were in the offing

SEMIANNUAL REPORT | JOHN HANCOCK MONEY MARKET FUND 6

for 2019. In response, we sought to maintain sufficient liquidity to capture interest-rate increases as quickly as possible when they occur.

More broadly speaking, we continued to look for opportunities to add incremental yield through individual security selection, adjustments to the portfolio's weighted average maturity, and shifts between fixed- and floating-rate notes.

MANAGED BY

| |

| Team of U.S. research analysts and portfolio managers |

The views expressed in this report are exclusively those of Jeffrey N. Given, CFA, John Hancock Asset Management, and are subject to change. They are not meant as investment advice. Please note that the holdings discussed in this report may not have been held by the fund for the entire period. Portfolio composition is subject to review in accordance with the fund's investment strategy and may vary in the future. Current and future portfolio holdings are subject to risk.

SEMIANNUAL REPORT | JOHN HANCOCK MONEY MARKET FUND 7

These examples are intended to help you understand your ongoing operating expenses of investing in the fund so you can compare these costs with the ongoing costs of investing in other mutual funds.

Understanding fund expenses

As a shareholder of the fund, you incur two types of costs:

■Transaction costs, which include sales charges (loads) on purchases or redemptions (varies by share class), minimum account fee charge, etc.

■Ongoing operating expenses, including management fees, distribution and service fees (if applicable), and other fund expenses.

We are presenting only your ongoing operating expenses here.

Actual expenses/actual returns

The first line of each share class in the table on the following page is intended to provide information about the fund’s actual ongoing operating expenses, and is based on the fund’s actual return. It assumes an account value of $1,000.00 on April 1, 2018, with the same investment held until September 30, 2018.

Together with the value of your account, you may use this information to estimate the operating expenses that you paid over the period. Simply divide your account value at September 30, 2018, by $1,000.00, then multiply it by the “expenses paid” for your share class from the table. For example, for an account value of $8,600.00, the operating expenses should be calculated as follows:

Hypothetical example for comparison purposes

The second line of each share class in the table on the following page allows you to compare the fund’s ongoing operating expenses with those of any other fund. It provides an example of the fund’s hypothetical account values and hypothetical expenses based on the fund’s actual expense ratio and an assumed 5% annualized return before expenses (which is not the fund’s actual return). It assumes an account value of $1,000.00 on April 1, 2018, with the same investment held until September 30, 2018. Look in any other fund shareholder report to find its hypothetical example and you will be able to compare these expenses. Please remember that these hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period.

Remember, these examples do not include any transaction costs, therefore, these examples will not help you to determine the relative total costs of owning different funds. If transaction costs were included, your expenses would have been higher. See the prospectus for details regarding transaction costs.

| 8 | JOHN HANCOCK MONEY MARKET FUND | SEMIANNUAL REPORT | |

SHAREHOLDER EXPENSE EXAMPLE CHART

| | | Account

value on

4-1-2018 | Ending

value on

9-30-2018 | Expenses

paid during

period ended

9-30-20181 | Annualized

expense

ratio |

| Class A | Actual expenses/actual returns | $1,000.00 | $1,006.60 | $2.87 | 0.57% |

| | Hypothetical example | 1,000.00 | 1,022.20 | 2.89 | 0.57% |

| Class B | Actual expenses/actual returns | 1,000.00 | 1,006.60 | 2.87 | 0.57% |

| | Hypothetical example | 1,000.00 | 1,022.20 | 2.89 | 0.57% |

| Class C | Actual expenses/actual returns | 1,000.00 | 1,006.60 | 2.87 | 0.57% |

| | Hypothetical example | 1,000.00 | 1,022.20 | 2.89 | 0.57% |

| 1 | Expenses are equal to the annualized expense ratio, multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period). |

| | SEMIANNUAL REPORT | JOHN HANCOCK MONEY MARKET FUND | 9 |

AS OF 9-30-18 (unaudited)

| | Maturity date | Yield (%) | | Par value^ | Value |

| U.S. Government Agency 82.7% | $451,042,928 |

| (Cost $451,042,928) | | | | | |

| Federal Agricultural Mortgage Corp. (1 month LIBOR - 0.080%) (A) | 11-30-18 | 2.023 | | 6,157,000 | 6,157,000 |

| Federal Agricultural Mortgage Corp. | 10-01-18 | 2.028 | | 4,500,000 | 4,500,000 |

| Federal Agricultural Mortgage Corp. (1 month LIBOR - 0.100%) (A) | 12-03-18 | 2.032 | | 3,763,000 | 3,763,000 |

| Federal Agricultural Mortgage Corp. (1 month LIBOR) (A) | 09-30-19 | 2.104 | | 4,976,000 | 4,976,000 |

| Federal Agricultural Mortgage Corp. (1 month LIBOR - 0.060%) (A) | 07-25-19 | 2.186 | | 10,000,000 | 10,000,000 |

| Federal Agricultural Mortgage Corp. (1 month LIBOR - 0.090%) (A) | 01-07-19 to 02-20-19 | 2.059 to 2.104 | | 8,305,000 | 8,305,000 |

| Federal Agricultural Mortgage Corp. (1 month LIBOR - 0.115%) (A) | 12-03-18 to 12-28-18 | 2.016 to 2.157 | | 9,995,000 | 9,995,000 |

| Federal Agricultural Mortgage Corp. (1 month LIBOR - 0.050%) (A) | 04-02-19 to 06-25-19 | 2.082 to 2.196 | | 12,379,000 | 12,379,000 |

| Federal Farm Credit Bank (1 month LIBOR + 0.095%) (A) | 10-03-18 | 2.018 | | 884,000 | 884,010 |

| Federal Farm Credit Bank (1 month LIBOR + 0.120%) (A) | 11-13-18 | 2.035 | | 1,273,000 | 1,273,396 |

| Federal Farm Credit Bank (1 month LIBOR - 0.095%) (A) | 12-03-18 | 2.039 | | 3,000,000 | 2,999,987 |

| Federal Farm Credit Bank (1 month LIBOR - 0.085%) (A) | 05-30-19 | 2.052 | | 2,165,000 | 2,164,516 |

| Federal Farm Credit Bank (1 month LIBOR + 0.130%) (A) | 10-17-18 | 2.064 | | 1,395,000 | 1,395,157 |

| Federal Farm Credit Bank (3 month LIBOR - 0.010%) (A) | 10-19-18 | 2.095 | | 863,000 | 863,115 |

| Federal Farm Credit Bank (1 month LIBOR + 0.170%) (A) | 11-14-19 | 2.095 | | 543,000 | 544,437 |

| Federal Farm Credit Bank (3 month LIBOR + 0.040%) (A) | 11-16-18 | 2.096 | | 8,607,000 | 8,610,158 |

| Federal Farm Credit Bank (1 month LIBOR + 0.065%) (A) | 10-22-18 | 2.120 | | 642,000 | 642,070 |

| Federal Farm Credit Bank (1 month LIBOR + 0.180%) (A) | 10-11-19 | 2.126 | | 500,000 | 501,090 |

| Federal Farm Credit Bank (1 month LIBOR - 0.040%) (A) | 04-24-19 | 2.134 | | 1,000,000 | 1,000,377 |

| Federal Farm Credit Bank (1 month LIBOR + 0.190%) (A) | 08-19-19 | 2.135 | | 4,687,000 | 4,697,367 |

| Federal Farm Credit Bank (1 month LIBOR - 0.055%) (A) | 12-20-18 | 2.142 | | 5,000,000 | 4,999,971 |

| Federal Farm Credit Bank (Prime rate - 3.060%) (A) | 04-25-19 | 2.149 | | 2,600,000 | 2,601,031 |

| Federal Farm Credit Bank (1 month LIBOR - 0.135%) (A) | 06-13-19 | 2.155 | | 1,006,000 | 1,005,213 |

| Federal Farm Credit Bank (3 month LIBOR - 0.130%) (A) | 02-03-20 | 2.157 | | 284,000 | 284,339 |

| 10 | JOHN HANCOCK MONEY MARKET FUND | SEMIANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS |

| | Maturity date | Yield (%) | | Par value^ | Value |

| Federal Farm Credit Bank (Prime rate - 3.120%) (A) | 01-02-19 | 2.160 | | 3,877,000 | $3,877,000 |

| Federal Farm Credit Bank (Prime rate - 3.105%) (A) | 04-10-19 | 2.180 | | 2,030,000 | 2,029,947 |

| Federal Farm Credit Bank (3 month LIBOR - 0.060%) (A) | 10-25-19 | 2.194 | | 1,442,000 | 1,443,697 |

| Federal Farm Credit Bank (3 month LIBOR - 0.180%) (A) | 05-17-19 | 2.196 | | 2,072,000 | 2,071,555 |

| Federal Farm Credit Bank (3 month LIBOR - 0.170%) (A) | 03-15-19 | 2.197 | | 2,913,000 | 2,912,969 |

| Federal Farm Credit Bank (Prime rate - 3.075%) (A) | 09-05-19 | 2.210 | | 4,452,000 | 4,451,793 |

| Federal Farm Credit Bank (3 month LIBOR - 0.120%) (A) | 01-27-20 | 2.215 | | 1,693,000 | 1,693,715 |

| Federal Farm Credit Bank (3 month USBMMY + 0.050%) (A) | 11-04-19 | 2.279 | | 2,099,000 | 2,098,875 |

| Federal Farm Credit Bank (3 month USBMMY + 0.150%) (A) | 04-12-19 | 2.293 | | 1,980,000 | 1,980,841 |

| Federal Farm Credit Bank (Prime rate - 2.970%) (A) | 01-24-20 | 2.312 | | 3,830,000 | 3,830,000 |

| Federal Farm Credit Bank (U.S. Federal Funds Effective Rate + 0.120%) (A) | 02-18-20 | 2.312 | | 1,045,000 | 1,045,280 |

| Federal Farm Credit Bank (3 month USBMMY + 0.085%) (A) | 08-08-19 | 2.314 | | 4,635,000 | 4,634,798 |

| Federal Farm Credit Bank (Prime rate - 2.980%) (A) | 02-20-20 | 2.316 | | 5,086,000 | 5,084,996 |

| Federal Farm Credit Bank (Prime rate - 2.910%) (A) | 12-11-19 | 2.383 | | 6,669,000 | 6,668,204 |

| Federal Farm Credit Bank (1 month LIBOR - 0.080%) (A) | 11-09-18 to 11-20-19 | 2.081 to 2.135 | | 2,551,000 | 2,550,482 |

| Federal Farm Credit Bank (Prime rate - 3.020%) (A) | 01-14-19 to 03-27-19 | 2.139 to 2.271 | | 9,423,000 | 9,424,302 |

| Federal Farm Credit Bank (Prime rate - 3.080%) (A) | 06-27-19 to 09-13-19 | 2.205 to 2.251 | | 6,934,000 | 6,931,978 |

| Federal Farm Credit Bank (Prime rate - 2.930%) (A) | 10-29-19 to 08-27-20 | 2.352 to 2.363 | | 3,832,000 | 3,831,632 |

| Federal Farm Credit Bank | 10-05-18 to 04-16-19 | 1.865 to 2.206 | | 17,346,000 | 17,290,066 |

| Federal Home Loan Bank (1 month LIBOR - 0.110%) (A) | 01-04-19 | 2.022 | | 250,000 | 250,000 |

| Federal Home Loan Bank (1 month LIBOR - 0.140%) (A) | 10-05-18 | 2.049 | | 1,500,000 | 1,499,992 |

| Federal Home Loan Bank (1 month LIBOR - 0.100%) (A) | 12-21-18 | 2.111 | | 815,000 | 815,000 |

| Federal Home Loan Bank (1 month LIBOR - 0.080%) (A) | 11-13-19 | 2.115 | | 520,000 | 519,895 |

| Federal Home Loan Bank (3 month LIBOR - 0.320%) (A) | 04-09-19 | 2.169 | | 5,205,000 | 5,201,581 |

| Federal Home Loan Bank (3 month LIBOR - 0.230%) (A) | 02-13-19 | 2.192 | | 540,000 | 539,892 |

| Federal Home Loan Bank (3 month LIBOR - 0.163%) (A) | 07-05-19 | 2.197 | | 235,000 | 235,023 |

| SEE NOTES TO FINANCIAL STATEMENTS | SEMIANNUAL REPORT | JOHN HANCOCK MONEY MARKET FUND | 11 |

| | Maturity date | Yield (%) | | Par value^ | Value |

| Federal Home Loan Bank (3 month LIBOR - 0.120%) (A) | 10-05-18 | 2.207 | | 3,300,000 | $3,300,017 |

| Federal Home Loan Bank (3 month LIBOR - 0.160%) (A) | 05-24-19 to 06-12-19 | 2.157 to 2.192 | | 5,205,000 | 5,205,809 |

| Federal Home Loan Bank | 10-01-18 to 05-28-19 | 1.795 to 2.384 | | 153,959,000 | 153,581,536 |

| Federal Home Loan Mortgage Corp. | 10-11-18 to 05-24-19 | 2.021 to 2.535 | | 10,433,000 | 10,401,326 |

| Federal National Mortgage Association (SOFR + 0.080%) (A) | 01-30-19 | 2.271 | | 4,883,000 | 4,883,000 |

| Federal National Mortgage Association (SOFR + 0.120%) (A) | 07-30-19 | 2.312 | | 15,000,000 | 15,000,000 |

|

| Federal National Mortgage Association | 10-01-18 to 02-19-19 | 1.712 to 2.347 | | 59,110,000 | 59,091,577 |

|

| Tennessee Valley Authority | 10-09-18 to 10-15-18 | 2.048 to 2.140 | | 12,127,000 | 12,124,916 |

| U.S. Government 10.5% | $57,059,413 |

| (Cost $57,059,413) | | | | | |

| U.S. Treasury Bill | 10-25-18 to 12-13-18 | 2.032 to 2.143 | | 34,083,000 | 34,001,271 |

|

| U.S. Treasury Note | 10-31-18 to 12-15-18 | 2.034 to 2.156 | | 23,094,700 | 23,058,142 |

|

| | | | | Par value^ | Value |

| Repurchase agreement 6.4% | $35,000,000 |

| (Cost $35,000,000) | | | | | |

| Barclays Tri-Party Repurchase Agreement dated 9-28-18 at 2.180% to be repurchased at $35,006,358 on 10-1-18, collateralized by $36,063,400 U.S. Treasury Inflation Indexed Notes, 0.375% - 0.750% due 7-15-27 to 7-15-28 (valued at $35,706,527, including interest) | | | | 35,000,000 | 35,000,000 |

| Total investments (Cost $543,102,341) 99.6% | $543,102,341 |

| Other assets and liabilities, net 0.4% | 2,028,431 |

| Total net assets 100.0% | $545,130,772 |

| The percentage shown for each investment category is the total value of the category as a percentage of the net assets of the fund. Maturity date represents the final legal maturity date on the security. |

| ^All par values are denominated in U.S. dollars unless otherwise indicated. |

| Security Abbreviations and Legend |

| LIBOR | London Interbank Offered Rate |

| USBMMY | U.S. Treasury Bill Money Market Yield |

| SOFR | Secured Overnight Financing Rate |

| (A) | Variable rate obligation. |

At 9-30-18, the aggregate cost of investments for federal income tax purposes was $543,102,341.

| 12 | JOHN HANCOCK MONEY MARKET FUND | SEMIANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS |

STATEMENT OF ASSETS AND LIABILITIES 9-30-18 (unaudited)

| Assets | |

| Unaffiliated investments, at value (Cost $543,102,341) | $543,102,341 |

| Cash | 76,812 |

| Interest receivable | 813,435 |

| Receivable for fund shares sold | 1,868,951 |

| Receivable from affiliates | 3,437 |

| Other assets | 63,262 |

| Total assets | 545,928,238 |

| Liabilities | |

| Distributions payable | 4,620 |

| Payable for fund shares repurchased | 521,445 |

| Payable to affiliates | |

| Accounting and legal services fees | 56,803 |

| Transfer agent fees | 47,013 |

| Distribution and service fees | 8,688 |

| Trustees' fees | 505 |

| Other liabilities and accrued expenses | 158,392 |

| Total liabilities | 797,466 |

| Net assets | $545,130,772 |

| Net assets consist of | |

| Paid-in capital | $545,133,182 |

| Undistributed net investment income | 171 |

| Accumulated net realized gain (loss) on | (2,581) |

| Net assets | $545,130,772 |

| |

| Net asset value per share | |

| Based on net asset value and shares outstanding - the fund has an unlimited number of shares authorized with no par value | |

| Class A ($532,401,364 ÷ 532,403,620 shares) | $1.00 |

| Class B ($2,051,769 ÷ 2,051,815 shares) 1 | $1.00 |

| Class C ($10,677,639 ÷ 10,677,753 shares) 1 | $1.00 |

| 1 | Redemption price per share is equal to net asset value less any applicable contingent deferred sales charge. |

| SEE NOTES TO FINANCIAL STATEMENTS | SEMIANNUAL REPORT | JOHN HANCOCK MONEY MARKET FUND | 13 |

STATEMENT OF OPERATIONS For the six months ended 9-30-18 (unaudited)

| Investment income | |

| Interest | $5,033,833 |

| Expenses | |

| Investment management fees | 1,011,232 |

| Distribution and service fees | 722,997 |

| Accounting and legal services fees | 62,097 |

| Transfer agent fees | 283,791 |

| Trustees' fees | 4,105 |

| Custodian fees | 65,476 |

| State registration fees | 55,786 |

| Printing and postage | 30,874 |

| Professional fees | 26,958 |

| Other | 8,377 |

| Total expenses | 2,271,693 |

| Less expense reductions | (745,576) |

| Net expenses | 1,526,117 |

| Net investment income | 3,507,716 |

| Realized and unrealized gain (loss) | |

| Net realized gain (loss) on | |

| Unaffiliated investments | — |

| Increase in net assets from operations | $3,507,716 |

| | |

| 14 | JOHN HANCOCK MONEY MARKET FUND | SEMIANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS |

STATEMENTS OF CHANGES IN NET ASSETS

| | Six months ended 9-30-18

(unaudited) | Year ended 3-31-18

|

| Increase (decrease) in net assets | | |

| From operations | | |

| Net investment income | $3,507,716 | $2,926,455 |

| Net realized gain | — | 483 |

| Increase in net assets resulting from operations | 3,507,716 | 2,926,938 |

| Distributions to shareholders | | |

| From net investment income | | |

| Class A | (3,412,046) | (2,919,965) |

| Class B | (16,070) | (14,450) |

| Class C | (79,429) | (93,612) |

| Total distributions | (3,507,545) | (3,028,027) |

| From fund share transactions | 27,198,750 | 3,697,510 |

| Total increase | 27,198,921 | 3,596,421 |

| Net assets | | |

| Beginning of period | 517,931,851 | 514,335,430 |

| End of period | $545,130,772 | $517,931,851 |

| Undistributed net investment income | $171 | — |

| SEE NOTES TO FINANCIAL STATEMENTS | SEMIANNUAL REPORT | JOHN HANCOCK MONEY MARKET FUND | 15 |

| CLASS A SHARES Period ended | 9-30-18 1 | 3-31-18 | 3-31-17 | 3-31-16 | 3-31-15 | 3-31-14 |

| Per share operating performance | | | | | | |

| Net asset value, beginning of period | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 |

| Net investment income2 | 0.007 | 0.006 | — 3 | — 3 | — 3 | — |

| Net realized and unrealized gain (loss) on investments | — | — 3 | — 3 | — 3 | — 3 | — |

| Total from investment operations | 0.007 | 0.006 | — 3 | — 3 | — 3 | — |

| Less distributions | | | | | | |

| From net investment income | (0.007) | (0.006) | — 3 | — 3 | — 3 | — |

| Net asset value, end of period | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 |

| Total return (%)4,5 | 0.66 6 | 0.59 | 0.02 | 0.01 | 0.01 | 0.00 |

| Ratios and supplemental data | | | | | | |

| Net assets, end of period (in millions) | $532 | $500 | $490 | $417 | $337 | $348 |

| Ratios (as a percentage of average net assets): | | | | | | |

| Expenses before reductions | 0.83 7 | 0.81 | 0.86 | 1.00 | 0.98 | 0.99 |

| Expenses including reductions | 0.57 4,7 | 0.55 4 | 0.47 4 | 0.30 4 | 0.20 4 | 0.24 4 |

| Net investment income | 1.31 4,7 | 0.57 4 | 0.04 4 | 0.01 4 | 0.01 4 | — 4 |

| 1 | Six months ended 9-30-18. Unaudited. |

| 2 | Based on average daily shares outstanding. |

| 3 | Less than $0.0005 per share. |

| 4 | Includes the impact of waivers and/or reimbursements in order to maintain a zero or positive yield. See Note 4. |

| 5 | Total returns would have been lower had certain expenses not been reduced during the applicable periods. |

| 6 | Not annualized. |

| 7 | Annualized. |

| 16 | JOHN HANCOCK MONEY MARKET FUND | SEMIANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS |

| CLASS B SHARES Period ended | 9-30-18 1 | 3-31-18 | 3-31-17 | 3-31-16 | 3-31-15 | 3-31-14 |

| Per share operating performance | | | | | | |

| Net asset value, beginning of period | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 |

| Net investment income2 | 0.007 | 0.004 | — 3 | — 3 | — 3 | — |

| Net realized and unrealized gain (loss) on investments | — | 0.001 | — 3 | — 3 | — 3 | — |

| Total from investment operations | 0.007 | 0.005 | — 3 | — 3 | — 3 | — |

| Less distributions | | | | | | |

| From net investment income | (0.007) | (0.005) | — 3 | — 3 | — 3 | — |

| Net asset value, end of period | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 |

| Total return (%)4,5,6 | 0.66 7 | 0.46 | 0.01 | 0.01 | 0.01 | 0.00 |

| Ratios and supplemental data | | | | | | |

| Net assets, end of period (in millions) | $2 | $3 | $4 | $7 | $7 | $11 |

| Ratios (as a percentage of average net assets): | | | | | | |

| Expenses before reductions | 1.58 8 | 1.56 | 1.62 | 1.75 | 1.73 | 1.74 |

| Expenses including reductions | 0.57 4,8 | 0.67 4 | 0.48 4 | 0.30 4 | 0.20 4 | 0.24 4 |

| Net investment income | 1.30 4,8 | 0.42 4 | 0.01 4 | 0.01 4 | 0.01 4 | — 4 |

| 1 | Six months ended 9-30-18. Unaudited. |

| 2 | Based on average daily shares outstanding. |

| 3 | Less than $0.0005 per share. |

| 4 | Includes the impact of waivers and/or reimbursements in order to maintain a zero or positive yield. See Note 4. |

| 5 | Total returns would have been lower had certain expenses not been reduced during the applicable periods. |

| 6 | Does not reflect the effect of sales charges, if any. |

| 7 | Not annualized. |

| 8 | Annualized. |

| SEE NOTES TO FINANCIAL STATEMENTS | SEMIANNUAL REPORT | JOHN HANCOCK MONEY MARKET FUND | 17 |

| CLASS C SHARES Period ended | 9-30-18 1 | 3-31-18 | 3-31-17 | 3-31-16 | 3-31-15 | 3-31-14 |

| Per share operating performance | | | | | | |

| Net asset value, beginning of period | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 |

| Net investment income2 | 0.007 | 0.006 | — 3 | — 3 | — 3 | — |

| Net realized and unrealized gain (loss) on investments | — | — 3 | — 3 | — 3 | — 3 | — |

| Total from investment operations | 0.007 | 0.006 | — 3 | — 3 | — 3 | — |

| Less distributions | | | | | | |

| From net investment income | (0.007) | (0.006) | — 3 | — 3 | — 3 | — |

| Net asset value, end of period | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 |

| Total return (%)4,5,6 | 0.66 7 | 0.60 | 0.02 | 0.01 | 0.01 | 0.00 |

| Ratios and supplemental data | | | | | | |

| Net assets, end of period (in millions) | $11 | $15 | $20 | $25 | $15 | $18 |

| Ratios (as a percentage of average net assets): | | | | | | |

| Expenses before reductions | 1.58 8 | 1.56 | 1.62 | 1.75 | 1.73 | 1.79 |

| Expenses including reductions | 0.57 4,8 | 0.55 4 | 0.47 4 | 0.31 4 | 0.20 4 | 0.24 4 |

| Net investment income | 1.29 4,8 | 0.55 4 | 0.03 4 | 0.01 4 | 0.01 4 | — 4 |

| 1 | Six months ended 9-30-18. Unaudited. |

| 2 | Based on average daily shares outstanding. |

| 3 | Less than $0.0005 per share. |

| 4 | Includes the impact of waivers and/or reimbursements in order to maintain a zero or positive yield. See Note 4. |

| 5 | Total returns would have been lower had certain expenses not been reduced during the applicable periods. |

| 6 | Does not reflect the effect of sales charges, if any. |

| 7 | Not annualized. |

| 8 | Annualized. |

| 18 | JOHN HANCOCK MONEY MARKET FUND | SEMIANNUAL REPORT | SEE NOTES TO FINANCIAL STATEMENTS |

Notes to financial statements (unaudited)

Note 1 — Organization

John Hancock Money Market Fund (the fund) is a series of John Hancock Current Interest (the Trust), an open-end management investment company organized as a Massachusetts business trust and registered under the Investment Company Act of 1940, as amended (the 1940 Act). The investment objective of the fund is to seek the maximum current income that is consistent with maintaining liquidity and preserving capital. The fund intends to maintain a stable $1.00 share price. Although the fund seeks to maintain a stable $1.00 share price, the value of the fund's shares could go down in price, meaning that you can lose money by investing in the fund.

The fund may offer multiple classes of shares. The shares currently offered by the fund are detailed in the Statement of assets and liabilities. Class A, Class B and Class C shares are offered to all investors; however, Class B and Class C shares are closed to new investors. Class B shares convert to Class A shares eight years after purchase. Class C shares convert to Class A shares ten years after purchase (certain exclusions may apply). Shareholders of each class have exclusive voting rights to matters that affect that class. The distribution and service fees, if any, and transfer agent fees for each class may differ.

Note 2 — Significant accounting policies

The financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America (US GAAP), which require management to make certain estimates and assumptions as of the date of the financial statements. Actual results could differ from those estimates and those differences could be significant. The fund qualifies as an investment company under Topic 946 of Accounting Standards Codification of US GAAP.

Events or transactions occurring after the end of the fiscal period through the date that the financial statements were issued have been evaluated in the preparation of the financial statements. The following summarizes the significant accounting policies of the fund:

Security valuation. Securities in the fund's portfolio are valued at amortized cost, in accordance with Rule 2a-7 under the 1940 Act, which approximates market value. The amortized cost method involves valuing a security at its cost on the date of purchase and thereafter assuming a constant amortization to maturity of the difference between the principal amount due at maturity and the cost of the security to the fund. The fund seeks to maintain a constant net asset value (NAV) per share of $1.00, but there can be no assurance that it will be able to do so.

The fund uses a three-tier hierarchy to prioritize the pricing assumptions, referred to as inputs, used in valuation techniques to measure fair value. Level 1 includes securities valued using quoted prices in active markets for identical securities. Level 2 includes securities valued using other significant observable inputs. Observable inputs may include quoted prices for similar securities, interest rates, prepayment speeds and credit risk. Prices for securities valued using these inputs are received from independent pricing vendors and brokers and are based on an evaluation of the inputs described. Level 3 includes securities valued using significant unobservable inputs when market prices are not readily available or reliable, including the fund's own assumptions in determining the fair value of investments. Factors used in determining value may include market or issuer specific events or trends, changes in interest rates and credit quality. The inputs or methodology used for valuing securities are not necessarily an indication of the risks associated with investing in those securities. Changes in valuation techniques and related inputs may result in transfers into or out of an assigned level within the disclosure hierarchy.

As of September 30, 2018, all investments are categorized as Level 2 under the hierarchy described above.

Repurchase agreements. The fund may enter into repurchase agreements. When the fund enters into a repurchase agreement, it receives collateral that is held in a segregated account by the fund's custodian, or for tri-party repurchase agreements, collateral is held at a third-party custodian bank in a segregated account for the benefit of the fund. The collateral amount is marked-to-market and monitored on a daily basis to ensure that the collateral held is in an amount not less than the principal amount of the repurchase agreement plus any accrued interest. Collateral received by the fund for repurchase agreements is disclosed in the Fund's investments as part of the caption related to the repurchase agreement.

Repurchase agreements are typically governed by the terms and conditions of the Master Repurchase Agreement and/or Global Master Repurchase Agreement (collectively, MRA). Upon an event of default, the non-defaulting party may close out

SEMIANNUAL REPORT | JOHN HANCOCK MONEY MARKET FUND 19

all transactions traded under the MRA and net amounts owed. Absent an event of default, assets and liabilities resulting from repurchase agreements are not offset in the Statement of assets and liabilities. In the event of a default by the counterparty, realization of the collateral proceeds could be delayed, during which time the collateral value may decline or the counterparty may have insufficient assets to pay back claims resulting from close-out of the transactions.

Security transactions and related investment income. Investment security transactions are recorded as of the date of purchase, sale or maturity. Interest income is accrued as earned. Interest income includes coupon interest and amortization/accretion of premiums/discounts on debt securities.

Line of credit. The fund may have the ability to borrow from banks for temporary or emergency purposes, including meeting redemption requests that otherwise might require the untimely sale of securities. Pursuant to the fund's custodian agreement, the custodian may loan money to the fund to make properly authorized payments. The fund is obligated to repay the custodian for any overdraft, including any related costs or expenses. The custodian may have a lien, security interest or security entitlement in any fund property that is not otherwise segregated or pledged, to the extent of any overdraft, and to the maximum extent permitted by law.

The fund and other affiliated funds have entered into a syndicated line of credit agreement with Citibank, N.A. as the administrative agent that enables them to participate in a $750 million unsecured committed line of credit. Excluding commitments designated for a certain fund and subject to the needs of all other affiliated funds, the fund can borrow up to an aggregate commitment amount of $500 million, subject to asset coverage and other limitations as specified in the agreement. A commitment fee payable at the end of each calendar quarter, based on the average daily unused portion of the line of credit, is charged to each participating fund based on a combination of fixed and asset based allocations and is reflected in Other expenses on the Statement of operations. For the six months ended September 30, 2018, the fund had no borrowings under the line of credit. Commitment fees for the six months ended September 30, 2018 were $1,592.

Expenses. Within the John Hancock group of funds complex, expenses that are directly attributable to an individual fund are allocated to such fund. Expenses that are not readily attributable to a specific fund are allocated among all funds in an equitable manner, taking into consideration, among other things, the nature and type of expense and the fund's relative net assets. Expense estimates are accrued in the period to which they relate and adjustments are made when actual amounts are known.

Class allocations. Income, common expenses and realized and unrealized gains (losses) are determined at the fund level and allocated daily to each class of shares based on the net assets of the class. Class-specific expenses, such as distribution and service fees, if any, and transfer agent fees, for all classes, are charged daily at the class level based on the net assets of each class and the specific expense rates applicable to each class.

Federal income taxes. The fund intends to continue to qualify as a regulated investment company by complying with the applicable provisions of the Internal Revenue Code and will not be subject to federal income tax on taxable income that is distributed to shareholders. Therefore, no federal income tax provision is required.

For federal income tax purposes, as of March 31, 2018, the fund has a short-term capital loss carryforward of $2,581 available to offset future net realized capital gains. This carryforward does not expire.

As of March 31, 2018, the fund had no uncertain tax positions that would require financial statement recognition, derecognition or disclosure. The fund's federal tax returns are subject to examination by the Internal Revenue Service for a period of three years.

Distribution of income and gains. Distributions to shareholders from net investment income and net realized gains, if any, are recorded on the ex-date. The fund generally declares dividends from net investment income daily and pays monthly, as long as class income exceeds class expense on each day. Capital gain distributions, if any, are distributed at least annually.

Distributions paid by the fund with respect to each class of shares are calculated in the same manner, at the same time and in the same amount, except for the effect of class level expenses that may be applied differently to each class.

SEMIANNUAL REPORT | JOHN HANCOCK MONEY MARKET FUND 20

Such distributions, on a tax basis, are determined in conformity with income tax regulations, which may differ from US GAAP. Distributions in excess of tax basis earnings and profits, if any, are reported in the fund's financial statements as a return of capital. The final determination of tax characteristics of the fund's distribution will occur at the end of the year and will subsequently be reported to shareholders.

Capital accounts within the financial statements are adjusted for permanent book-tax differences. These adjustments have no impact on net assets or the results of operations. Temporary book-tax differences, if any, will reverse in a subsequent period. The fund had no material book-tax differences at March 31, 2018.

Note 3 — Guarantees and indemnifications

Under the Trust's organizational documents, its Officers and Trustees are indemnified against certain liabilities arising out of the performance of their duties to the Trust, including the fund. Additionally, in the normal course of business, the fund enters into contracts with service providers that contain general indemnification clauses. The fund's maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the fund that have not yet occurred. The risk of material loss from such claims is considered remote.

Note 4 — Fees and transactions with affiliates

John Hancock Advisers, LLC (the Advisor) serves as investment advisor for the fund. John Hancock Funds, LLC (the Distributor), an affiliate of the Advisor, serves as principal underwriter of the fund. The Advisor and the Distributor are indirect, wholly owned subsidiaries of Manulife Financial Corporation (MFC).

Management fee. The fund has an investment management agreement with the Advisor under which the fund pays a daily management fee to the Advisor equivalent on an annual basis to the sum of: (a) 0.500% of the first $500 million of the fund's aggregate net assets; (b) 0.425% of the next $250 million of the of the fund's aggregate net assets; (c) 0.375% of the next $250 million of the of the fund's aggregate net assets; (d) 0.350% of the next $500 million of the fund's aggregate net assets; (e) 0.325% of the next $500 million of the of the fund's aggregate net assets; (f) 0.300% of the next $500 million of the of the fund's aggregate net assets; and (g) 0.275% of the fund's aggregate net assets in excess of $2.5 billion. Aggregate net assets include the net assets of the fund and Money Market Trust, a series of John Hancock Variable Insurance Trust. The Advisor has a subadvisory agreement with John Hancock Asset Management a division of Manulife Asset Management (US) LLC, an indirectly owned subsidiary of MFC and an affiliate of the Advisor. The fund is not responsible for payment of the subadvisory fees.

The Advisor has contractually agreed to waive a portion of its management fee and/or reimburse expenses for certain funds of the John Hancock group of funds complex, including the fund (the participating portfolios). This waiver is based upon aggregate net assets of all the participating portfolios. The amount of the reimbursement is calculated daily and allocated among all the participating portfolios in proportion to the daily net assets of each fund. For the six months ended September 30, 2018, this waiver amounted to 0.01% of the fund's average net assets on an annualized basis. This agreement expires on June 30, 2020, unless renewed by mutual agreement of the fund and the Advisor based upon a determination that this is appropriate under the circumstances at that time.

The Advisor and its affiliates have voluntarily agreed to waive a portion of their fees and/or reimburse certain expenses to the extent necessary to assist the fund in attempting to achieve a positive yield. These expense waivers and/or reimbursements may be amended or terminated at any time by the Advisor.

For the six months ended September 30, 2018, these expense reductions amounted to the following:

| | | | | |

| Class | Expense reduction | | Class | Expense reduction |

| Class A | $21,958 | | Class C | $517 |

| Class B | 104 | | Total | $22,579 |

Expenses waived or reimbursed in the current fiscal period are not subject to recapture in future fiscal periods.

SEMIANNUAL REPORT | JOHN HANCOCK MONEY MARKET FUND 21

The investment management fees, including the impact of the waiver and reimbursements as described above, incurred for the six months ended September 30, 2018 were equivalent to a net annual effective rate of 0.37% of the fund's average daily net assets.

Accounting and legal services. Pursuant to a service agreement, the fund reimburses the Advisor for all expenses associated with providing the administrative, financial, legal, compliance, accounting and recordkeeping services to the fund, including the preparation of all tax returns, periodic reports to shareholders and regulatory reports, among other services. These expenses are allocated to each share class based on its relative net assets at the time the expense was incurred. These accounting and legal services fees incurred for the six months ended September 30, 2018 amounted to an annual rate of 0.02% of the fund's average daily net assets.

Distribution and service plans. The fund has a distribution agreement with the Distributor. The fund has adopted distribution and service plans with respect to Class A, Class B and Class C pursuant to Rule 12b-1 under the 1940 Act, to pay the Distributor for services provided as the Distributor of shares of the fund. The fund may pay up to the following contractual rates of distribution and service fees under these arrangements, expressed as an annual percentage of average daily net assets for each class of the fund's shares.

| | |

| Class | Rule 12b-1 fees |

| Class A | 0.25% |

| Class B | 1.00% |

| Class C | 1.00% |

The Distributor has contractually agreed to waive Rule 12b-1 fees on Class A, Class B and Class C shares to the extent necessary to achieve aggregate fees paid to the Distributor of 0.00%. This agreement expires on July 31, 2019, unless renewed by mutual agreement of the fund and the Distributor based upon a determination that this is appropriate under the circumstances at that time.

The total amounts waived by the Distributor were $649,303, $12,379 and $61,315, for Class A, Class B, and Class C shares, respectively, for the six months ended September 30, 2018.

Sales charges. Class B and Class C shares may be subject to contingent deferred sales charges (CDSCs). Class B shares that are redeemed within six years of purchase are subject to CDSCs, at declining rates, beginning at 5.00%. Class C shares that are redeemed within one year of purchase are subject to a 1.00% CDSC. CDSCs are applied to the lesser of the current market value at the time of redemption or the original purchase cost of the shares being redeemed. Proceeds from CDSCs are used to compensate the Distributor for providing distribution-related services in connection with the sale of these shares. For the six months ended September 30, 2018, CDSCs received by the Distributor amounted to $36 and $726 for Class B and Class C shares, respectively.

Transfer agent fees. The John Hancock group of funds has a complex-wide transfer agent agreement with John Hancock Signature Services, Inc. (Signature Services), an affiliate of the Advisor. The transfer agent fees paid to Signature Services are determined based on the cost to Signature Services (Signature Services Cost) of providing recordkeeping services. It also includes out-of-pocket expenses, including payments made to third-parties for recordkeeping services provided to their clients who invest in one or more John Hancock funds. In addition, Signature Services Cost may be reduced by certain fees that Signature Services receives in connection with retirement and small accounts. Signature Services Cost is calculated monthly and allocated, as applicable, to five categories of share classes: Retail Share and Institutional Share Classes of Non-Municipal Bond Funds, Class R6 Shares, Retirement Share Classes and Municipal Bond Share Classes. Within each of these categories, the applicable costs are allocated to the affected John Hancock affiliated funds and/or classes, based on the relative average daily net assets.

SEMIANNUAL REPORT | JOHN HANCOCK MONEY MARKET FUND 22

Class level expenses. Class level expenses for the six months ended September 30, 2018 were:

| | | |

| Class | Distribution and service fees | Transfer agent fees |

| Class A | $649,303 | $275,970 |

| Class B | 12,379 | 1,314 |

| Class C | 61,315 | 6,507 |

| Total | $722,997 | $283,791 |

Trustee expenses. The fund compensates each Trustee who is not an employee of the Advisor or its affiliates. The costs of paying Trustee compensation and expenses are allocated to the fund based on its net assets relative to other funds within the John Hancock group of funds complex.

Note 5 — Fund share transactions

Transactions in fund shares for the six months ended September 30, 2018 and for the year ended March 31, 2018 were as follows:

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | |

| | | | | | | | Six months ended 9-30-18 | | | | | | | | | | | | Year ended 3-31-18 | |

| | | | | Shares | | | Amount | | | | | | | | | Shares | | | Amount | |

| | Class A shares | | | | | | | | | | | | | | | | | | | |

| | Sold | | | 148,756,346 | | | $148,756,346 | | | | | | | | | 315,059,715 | | | $315,059,715 | |

| | Distributions reinvested | | | 3,372,019 | | | 3,372,019 | | | | | | | | | 2,879,496 | | | 2,879,496 | |

| | Repurchased | | | (119,868,173 | ) | | (119,868,173 | ) | | | | | | | | (308,135,341 | ) | | (308,135,341 | ) |

| | Net increase | | | 32,260,192 | | | $32,260,192 | | | | | | | | | 9,803,870 | | | $9,803,870 | |

| | Class B shares | | | | | | | | | | | | | | | | | | | |

| | Sold | | | 254,967 | | | $254,967 | | | | | | | | | 876,628 | | | $876,628 | |

| | Distributions reinvested | | | 14,683 | | | 14,683 | | | | | | | | | 13,694 | | | 13,694 | |

| | Repurchased | | | (1,030,935 | ) | | (1,030,935 | ) | | | | | | | | (2,416,384 | ) | | (2,416,384 | ) |

| | Net decrease | | | (761,285 | ) | | $(761,285 | ) | | | | | | | | (1,526,062 | ) | | $(1,526,062 | ) |

| | Class C shares | | | | | | | | | | | | | | | | | | | |

| | Sold | | | 2,659,664 | | | $2,659,664 | | | | | | | | | 7,130,573 | | | $7,130,573 | |

| | Distributions reinvested | | | 74,648 | | | 74,648 | | | | | | | | | 88,256 | | | 88,256 | |

| | Repurchased | | | (7,034,469 | ) | | (7,034,469 | ) | | | | | | | | (11,799,127 | ) | | (11,799,127 | ) |

| | Net decrease | | | (4,300,157 | ) | | $(4,300,157 | ) | | | | | | | | (4,580,298 | ) | | $(4,580,298 | ) |

| | Total net increase | | | 27,198,750 | | | $27,198,750 | | | | | | | | | 3,697,510 | | | $3,697,510 | |

SEMIANNUAL REPORT | JOHN HANCOCK MONEY MARKET FUND 23

CONTINUATION OF INVESTMENT ADVISORY AND SUBADVISORY AGREEMENTS

Evaluation of Advisory and Subadvisory Agreements by the Board of Trustees

This section describes the evaluation by the Board of Trustees (the Board) of John Hancock Current Interest (the Trust) of the Advisory Agreement (the Advisory Agreement) with John Hancock Advisers, LLC (the Advisor) and the Subadvisory Agreement (the Subadvisory Agreement) with John Hancock Asset Management a division of Manulife Asset Management (US) LLC (the Subadvisor), for John Hancock Money Market Fund (the fund). The Advisory Agreement and Subadvisory Agreement are collectively referred to as the Agreements. Prior to the June 18-21, 2018 in-person meeting at which the Agreements were approved, the Board also discussed and considered information regarding the proposed continuation of the Agreements at an in-person meeting held on May 29-31, 2018.

Approval of Advisory and Subadvisory Agreements

At in-person meetings held on June 18-21, 2018, the Board, including the Trustees who are not parties to any Agreement or considered to be interested persons of the Trust under the Investment Company Act of 1940, as amended (the 1940 Act) (the Independent Trustees), reapproved for an annual period the continuation of the Advisory Agreement between the Trust and the Advisor and the Subadvisory Agreement between the Advisor and the Subadvisor with respect to the fund.

In considering the Advisory Agreement and the Subadvisory Agreement, the Board received in advance of the meetings a variety of materials relating to the fund, the Advisor and the Subadvisor, including comparative performance, fee and expense information for a peer group of similar funds prepared by an independent third-party provider of mutual fund data, performance information for an applicable benchmark index; and, with respect to the Subadvisor, comparative performance information for comparably managed accounts, as applicable, and other information provided by the Advisor and the Subadvisor regarding the nature, extent and quality of services provided by the Advisor and the Subadvisor under their respective Agreements, as well as information regarding the Advisor's revenues and costs of providing services to the fund and any compensation paid to affiliates of the Advisor. At the meetings at which the renewal of the Advisory Agreement and Subadvisory Agreement are considered, particular focus is given to information concerning fund performance, comparability of fees and total expenses, and profitability. However, the Board notes that the evaluation process with respect to the Advisor and the Subadvisor is an ongoing one. In this regard, the Board also took into account discussions with management and information provided to the Board (including its various committees) at prior meetings with respect to the services provided by the Advisor and the Subadvisor to the fund, including quarterly performance reports prepared by management containing reviews of investment results and prior presentations from the Subadvisor with respect to the fund. The information received and considered by the Board in connection with the May and June meetings and throughout the year was both written and oral. The Board noted the affiliation of the Subadvisor with the Advisor, noting any potential conflicts of interest. The Board also considered the nature, quality, and extent of non-advisory services, if any, to be provided to the fund by the Advisor's affiliates, including distribution services. The Board considered the Advisory Agreement and the Subadvisory Agreement separately in the course of its review. In doing so, the Board noted the respective roles of the Advisor and Subadvisor in providing services to the fund.

Throughout the process, the Board asked questions of and requested additional information from management. The Board is assisted by counsel for the Trust and the Independent Trustees are also separately assisted by independent legal counsel throughout the process. The Independent Trustees also received a memorandum from their independent legal counsel discussing the legal standards for their consideration of the proposed continuation of the Agreements and discussed the proposed continuation of the Agreements in private sessions with their independent legal counsel at which no representatives of management were present.

Approval of Advisory Agreement

In approving the Advisory Agreement with respect to the fund, the Board, including the Independent Trustees, considered a variety of factors, including those discussed below. The Board also considered other factors (including conditions and trends prevailing generally in the economy, the securities markets, and the industry) and did not treat any single factor as

SEMIANNUAL REPORT | JOHN HANCOCK MONEY MARKET FUND 24

determinative, and each Trustee may have attributed different weights to different factors. The Board's conclusions may be based in part on its consideration of the advisory and subadvisory arrangements in prior years and on the Board's ongoing regular review of fund performance and operations throughout the year.

Nature, extent, and quality of services. Among the information received by the Board from the Advisor relating to the nature, extent, and quality of services provided to the fund, the Board reviewed information provided by the Advisor relating to its operations and personnel, descriptions of its organizational and management structure, and information regarding the Advisor's compliance and regulatory history, including its Form ADV. The Board also noted that on a regular basis it receives and reviews information from the Trust's Chief Compliance Officer (CCO) regarding the fund's compliance policies and procedures established pursuant to Rule 38a-1 under the 1940 Act. The Board observed that the scope of services provided by the Advisor, and of the undertakings required of the Advisor in connection with those services, including maintaining and monitoring its own and the fund's compliance programs, risk management programs, liquidity management programs and cybersecurity programs, had expanded over time as a result of regulatory, market and other developments. The Board considered that the Advisor is responsible for the management of the day-to-day operations of the fund, including, but not limited to, general supervision of and coordination of the services provided by the Subadvisor, and is also responsible for monitoring and reviewing the activities of the Subadvisor and third-party service providers. The Board also considered the significant risks assumed by the Advisor in connection with the services provided to the fund including entrepreneurial risk in sponsoring new funds and ongoing risks including investment, operational, enterprise, litigation, regulatory and compliance risks with respect to all funds.

In considering the nature, extent, and quality of the services provided by the Advisor, the Trustees also took into account their knowledge of the Advisor's management and the quality of the performance of the Advisor's duties, through Board meetings, discussions and reports during the preceding year and through each Trustee's experience as a Trustee of the Trust and of the other trusts in the John Hancock group of funds (the John Hancock Fund Complex).

In the course of their deliberations regarding the Advisory Agreement, the Board considered, among other things:

| (a) | the skills and competency with which the Advisor has in the past managed the Trust's affairs and its subadvisory relationship, the Advisor's oversight and monitoring of the Subadvisor's investment performance and compliance programs, such as the Subadvisor's compliance with fund policies and objectives, review of brokerage matters, including with respect to trade allocation and best execution and the Advisor's timeliness in responding to performance issues; |

| (b) | the background, qualifications and skills of the Advisor's personnel; |

| (c) | the Advisor's compliance policies and procedures and its responsiveness to regulatory changes and fund industry developments; |

| (d) | the Advisor's administrative capabilities, including its ability to supervise the other service providers for the fund, as well as the Advisor's oversight of any securities lending activity, its monitoring of class action litigation and collection of class action settlements on behalf of the fund, and bringing loss recovery actions on behalf of the fund; |

| (e) | the financial condition of the Advisor and whether it has the financial wherewithal to provide a high level and quality of services to the fund; |

| (f) | the Advisor's initiatives intended to improve various aspects of the Trust's operations and investor experience with the fund; and |

| (g) | the Advisor's reputation and experience in serving as an investment advisor to the Trust and the benefit to shareholders of investing in funds that are part of a family of funds offering a variety of investments. |

The Board concluded that the Advisor may reasonably be expected to continue to provide a high quality of services under the Advisory Agreement with respect to the fund.

SEMIANNUAL REPORT | JOHN HANCOCK MONEY MARKET FUND 25

Investment performance. In considering the fund's performance, the Board noted that it reviews at its regularly scheduled meetings information about the fund's performance results. In connection with the consideration of the Advisory Agreement, the Board:

| (a) | reviewed information prepared by management regarding the fund's performance; |

| (b) | considered the comparative performance of an applicable benchmark index; |

| (c) | considered the performance of comparable funds, if any, as included in the report prepared by an independent third-party provider of fund data; and |

| (d) | took into account the Advisor's analysis of the fund's performance and its plans and recommendations regarding the Trust's subadvisory arrangements generally. |

The Board noted that while it found the data provided by the independent third-party generally useful it recognized its limitations, including in particular that the data may vary depending on the end date selected and the results of the performance comparisons may vary depending on the selection of the peer group. The Board noted that the fund underperformed its benchmark index for the one-, three-, five- and ten-year periods ended December 31, 2017. The Board also noted that the fund outperformed the peer group average for the one-, three- and five-year periods and underperformed the peer group average for the ten-year period ended December 31, 2017.The Board took into account management's discussion of the fund's performance, including the favorable performance relative to the peer group for the one-, three- and five-year periods. The Board also noted the relatively narrow range of performance returns of the funds that comprise the peer group. The Board concluded that the fund's performance has generally been in line with or outperformed the historical performance of comparable funds.

Fees and expenses. The Board reviewed comparative information prepared by an independent third-party provider of mutual fund data, including, among other data, the fund's contractual and net management fees (and subadvisory fees, to the extent available) and total expenses as compared to similarly situated investment companies deemed to be comparable to the fund in light of the nature, extent and quality of the management and advisory and subadvisory services provided by the Advisor and the Subadvisor. The Board considered the fund's ranking within a smaller group of peer funds chosen by the independent third-party provider, as well as the fund's ranking within a broader group of funds. In comparing the fund's contractual and net management fees to those of comparable funds, the Board noted that such fees include both advisory and administrative costs. The Board noted that net management fees are lower than the peer group median and total expenses for the fund are higher than the peer group median.

The Board took into account management's discussion of the fund's expenses. The Board also took into account management's discussion with respect to the overall management fee and the fees of the Subadvisor, including the amount of the advisory fee retained by the Advisor after payment of the subadvisory fee, in each case in light of the services rendered for those amounts and the risks undertaken by the Advisor. The Board also noted that the Advisor pays the subadvisory fee. In addition, the Board took into account that management had agreed to implement an overall fee waiver across the complex, including the fund, which is discussed further below. The Board also noted actions taken over the past several years to reduce the fund's operating expenses. The Board also noted that, in addition, the Advisor is currently waiving fees and/or reimbursing expenses with respect to the fund and that the fund has breakpoints in its contractual management fee schedule that reduces management fees as assets increase. The Board also noted that the fund's distributor, an affiliate of the Advisor, has agreed to waive a portion of its Rule 12b-1 fee for a share class of the fund. The Board noted that the fund has a voluntary fee waiver and/or expense reimbursement, to assist the fund in attempting to achieve a positive yield. The Board reviewed information provided by the Advisor concerning the investment advisory fee charged by the Advisor or one of its advisory affiliates to other clients (including other funds in the John Hancock Fund Complex) having similar investment mandates, if any. The Board considered any differences between the Advisor's and Subadvisor's services to the fund and the services they provide to other comparable clients or funds. The Board concluded that the advisory fee paid with respect to the fund is reasonable in light of the nature, extent and quality of the services provided to the fund under the Advisory Agreement.

SEMIANNUAL REPORT | JOHN HANCOCK MONEY MARKET FUND 26

Profitability/Fall out benefits. In considering the costs of the services to be provided and the profits to be realized by the Advisor and its affiliates (including the Subadvisor) from the Advisor's relationship with the Trust, the Board:

| (a) | reviewed financial information of the Advisor; |

| (b) | reviewed and considered information presented by the Advisor regarding the net profitability to the Advisor and its affiliates with respect to the fund; |

| (c) | received and reviewed profitability information with respect to the John Hancock Fund Complex as a whole and with respect to the fund; |

| (d) | received information with respect to the Advisor's allocation methodologies used in preparing the profitability data and considered that the Advisor hired an independent third-party consultant to provide an analysis of the Advisor's allocation methodologies; |

| (e) | considered that the John Hancock insurance companies that are affiliates of the Advisor, as shareholders of the Trust directly or through their separate accounts, receive certain tax credits or deductions relating to foreign taxes paid and dividends received by certain funds of the Trust and noted that these tax benefits, which are not available to participants in qualified retirement plans under applicable income tax law, are reflected in the profitability information reviewed by the Board; |

| (f) | considered that the Advisor also provides administrative services to the fund on a cost basis pursuant to an administrative services agreement; |

| (g) | noted that affiliates of the Advisor provide transfer agency services and distribution services to the fund, and that the fund's distributor also receives Rule 12b-1 payments to support distribution of the fund; |

| (h) | noted that the fund's Subadvisor is an affiliate of the Advisor; |

| (i) | noted that the Advisor also derives reputational and other indirect benefits from providing advisory services to the fund; |

| (j) | noted that the subadvisory fee for the fund is paid by the Advisor; |

| (k) | considered the Advisor's ongoing costs and expenditures necessary to improve services, meet new regulatory and compliance requirements, and adapt to other challenges impacting the fund industry; and |

| (l) | considered that the Advisor should be entitled to earn a reasonable level of profits in exchange for the level of services it provides to the fund and the risks that it assumes as Advisor, including entrepreneurial, operational, reputational, litigation and regulatory risk. |

Based upon its review, the Board concluded that the level of profitability, if any, of the Advisor and its affiliates (including the Subadvisor) from their relationship with the fund was reasonable and not excessive.

Economies of scale. In considering the extent to which economies of scale would be realized as the fund grows and whether fee levels reflect these economies of scale for the benefit of fund shareholders, the Board:

| (a) | considered that the Advisor has contractually agreed to waive a portion of its management fee for certain funds of the John Hancock Fund Complex, including the fund (the participating portfolios) or otherwise reimburse the expenses of the participating portfolios (the reimbursement). This waiver is based upon aggregate net assets of all the participating portfolios. The amount of the reimbursement is calculated daily and allocated among all the participating portfolios in proportion to the daily net assets of each fund; |

| (b) | reviewed the fund's advisory fee structure and concluded that: (i) the fund's fee structure contains breakpoints at the subadvisory fee level and that such breakpoints are reflected as breakpoints in the advisory fees for the fund; and (ii) although economies of scale cannot be measured with precision, these arrangements permit |

SEMIANNUAL REPORT | JOHN HANCOCK MONEY MARKET FUND 27

| | shareholders of the fund to benefit from economies of scale if the fund grows. The Board also took into account management's discussion of the fund's advisory fee structure; and |

| (c) | the Board also considered the effect of the fund's growth in size on its performance and fees. The Board also noted that if the fund's assets increase over time, the fund may realize other economies of scale. |

Approval of Subadvisory Agreement

In making its determination with respect to approval of the Subadvisory Agreement, the Board reviewed:

| (1) | information relating to the Subadvisor's business, including current subadvisory services to the Trust (and other funds in the John Hancock Fund Complex); |

| (2) | the historical and current performance of the fund and comparative performance information relating to an applicable benchmark index and comparable funds; and |

| (3) | the subadvisory fee for the fund, including any breakpoints, and to the extent available, comparable fee information prepared by an independent third party provider of fund data. |

Nature, extent, and quality of services. With respect to the services provided by the Subadvisor, the Board received information provided to the Board by the Subadvisor, including the Subadvisor's Form ADV, as well as took into account information presented throughout the past year. The Board considered the Subadvisor's current level of staffing and its overall resources, as well as received information relating to the Subadvisor's compensation program. The Board reviewed the Subadvisor's history and investment experience, as well as information regarding the qualifications, background, and responsibilities of the Subadvisor's investment and compliance personnel who provide services to the fund. The Board also considered, among other things, the Subadvisor's compliance program and any disciplinary history. The Board also considered the Subadvisor's risk assessment and monitoring process. The Board reviewed the Subadvisor's regulatory history, including whether it was involved in any regulatory actions or investigations as well as material litigation, and any settlements and amelioratory actions undertaken, as appropriate. The Board noted that the Advisor conducts regular, periodic reviews of the Subadvisor and its operations, including regarding investment processes and organizational and staffing matters. The Board also noted that the Trust's CCO and his staff conduct regular, periodic compliance reviews with the Subadvisor and present reports to the Independent Trustees regarding the same, which includes evaluating the regulatory compliance systems of the Subadvisor and procedures reasonably designed to assure compliance with the federal securities laws. The Board also took into account the financial condition of the Subadvisor.

The Board considered the Subadvisor's investment process and philosophy. The Board took into account that the Subadvisor's responsibilities include the development and maintenance of an investment program for the fund that is consistent with the fund's investment objective, the selection of investment securities and the placement of orders for the purchase and sale of such securities, as well as the implementation of compliance controls related to performance of these services. The Board also received information with respect to the Subadvisor's brokerage policies and practices, including with respect to best execution and soft dollars.

Subadvisor compensation. In considering the cost of services to be provided by the Subadvisor and the profitability to the Subadvisor of its relationship with the fund, the Board noted that the fees under the Subadvisory Agreement are paid by the Advisor and not the fund. The Board also received information and took into account any other potential conflicts of interest the Advisor might have in connection with the Subadvisory Agreement.

In addition, the Board considered other potential indirect benefits that the Subadvisor and its affiliates may receive from the Subadvisor's relationship with the fund, such as the opportunity to provide advisory services to additional funds in the John Hancock Fund Complex and reputational benefits

Subadvisory fees. The Board considered that the fund pays an advisory fee to the Advisor and that, in turn, the Advisor pays a subadvisory fee to the Subadvisor. As noted above, the Board also considered the fund's subadvisory fees as compared to similarly situated investment companies deemed to be comparable to the fund as included in the report prepared by the

SEMIANNUAL REPORT | JOHN HANCOCK MONEY MARKET FUND 28

independent third party provider of fund data, to the extent available. The Board noted that the limited size of the Lipper peer group was not sufficient for comparative purposes. The Board also took into account the subadvisory fees paid by the Advisor to the Subadvisor with respect to the fund and compared them to fees charged by the Subadvisor to manage other subadvised portfolios and portfolios not subject to regulation under the 1940 Act, as applicable.

Subadvisor performance. As noted above, the Board considered the fund's performance as compared to the fund's peer group and the benchmark index and noted that the Board reviews information about the fund's performance results at its regularly scheduled meetings. The Board noted the Advisor's expertise and resources in monitoring the performance, investment style and risk-adjusted performance of the Subadvisor. The Board was mindful of the Advisor's focus on the Subadvisor's performance. The Board also noted the Subadvisor's long-term performance record for similar accounts, as applicable.

The Board's decision to approve the Subadvisory Agreement was based on a number of determinations, including the following:

| (1) | the Subadvisor has extensive experience and demonstrated skills as a manager; |

| (2) | the performance of the fund has generally been in line with or outperformed the historical performance of comparable funds; |

| (3) | the subadvisory fee is reasonable in relation to the level and quality of services being provided under the Subadvisory Agreement; and |

| (4) | noted that the subadvisory fees are paid by the Advisor not the fund and that the subadvisory fee breakpoints are reflected as breakpoints in the advisory fees for the fund in order to permit shareholders to benefit from economies of scale if the fund grows. |

* * *

Based on the Board's evaluation of all factors that the Board deemed to be material, including those factors described above, the Board, including the Independent Trustees, concluded that renewal of the Advisory Agreement and the Subadvisory Agreement would be in the best interest of the fund and its shareholders. Accordingly, the Board, and the Independent Trustees voting separately, approved the Advisory Agreement and Subadvisory Agreement for an additional one-year period.