Free signup for more

- Track your favorite companies

- Receive email alerts for new filings

- Personalized dashboard of news and more

- Access all data and search results

Filing tables

Filing exhibits

CW similar filings

- 16 Feb 17 Curtiss-Wright Reports Fourth Quarter and Full-Year 2016 Financial Results and Issues 2017 Guidance

- 8 Dec 16 Other Events

- 27 Oct 16 Curtiss-Wright Reports Third Quarter 2016 Financial Results; Maintains Full-Year EPS And Increases Operating Margin Guidance

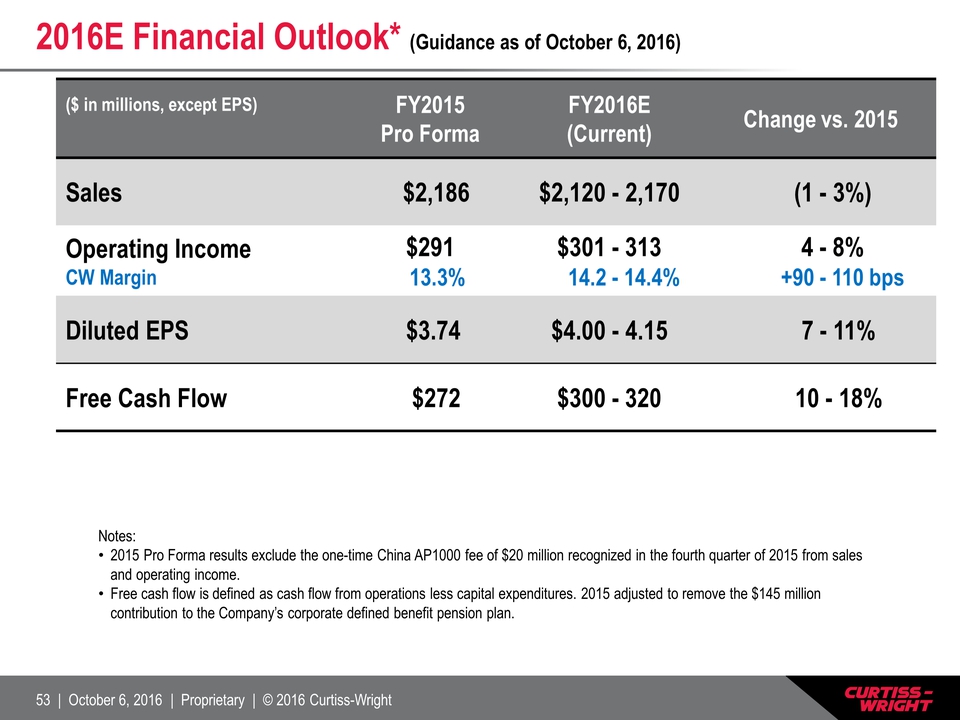

- 6 Oct 16 Curtiss-Wright Reaffirms 2016 Guidance and Offers Initial 2017 Outlook

- 28 Jul 16 Curtiss-Wright Reports Second Quarter 2016 Financial Results; Maintains Full-Year EPS and Increases Free Cash Flow Guidance

- 9 May 16 Submission of Matters to a Vote of Security Holders

- 5 May 16 Curtiss-Wright Reports First Quarter 2016 Financial Results; Raises Full-Year Free Cash Flow Guidance

Filing view

External links