EXHIBIT 99.3

| | |

| MANDATE | | Export Development Canada (EDC) is Canada’s export credit agency. Our mandate is to support and develop Canada’s trade, and the capacity of Canadian companies to participate in and respond to international business opportunities. Our knowledge and partnerships are used by more than 7,400 Canadian companies and their global customers in up to 200 markets worldwide each year. A Crown corporation accountable to Parliament through the Minister of International Trade, we are financially self-sustaining and a recognized leader in financial reporting and economic analysis. |

| |

| | |

| VISION | | EDC will be the most knowledgeable, the most connected and the most committed partner in trade for Canada. |

| | |

| | CANADIAN EXPORTS GREW 2% EDC SERVED 7,427 CUSTOMERS IN 187 COUNTRIES ACHIEVED CUSTOMER SATISFACTION AND LOYALTY SCORE (NET PROMOTER SCORE) OF 72, PUTTING EDC AMONG AN ELITE GROUP OF ORGANIZATIONS WITH SCORES ABOVE 70 90% OF ALL FINANCING TRANSACTIONS DONE IN PARTNERSHIP WITH FINANCIAL INSTITUTIONS 1,046 CANADIAN EXPORTERS BENEFITTED FROM OUR FINANCING FACILITIES TO TARGETED FOREIGN BUYERS OUR CUSTOMERS UNDERTOOK 896 TRANSACTIONS RELATED TO FOREIGN INVESTMENTS FOR A VALUE OF $6.6 BILLION HELPED GENERATE $52.7 BILLION OF CANADA’S GDP, MORE THAN 4.0 CENTS FOR EVERY DOLLAR EARNED HELPED SUSTAIN 573,773 JOBS, 3.3% OF NATIONAL EMPLOYMENT EDC EARNED REVENUES OF $1.4 BILLION AND GENERATED A NET INCOME OF $1.3 BILLION |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| | |

| | |

2012 PERFORMANCE MEASURES

| | | | | | |

Ratings in our performance measures are as follows:  Target met or exceeded (> 98% of plan) Target met or exceeded (> 98% of plan)

Target substantially met (³ 95% and £ 98% of plan) Target substantially met (³ 95% and £ 98% of plan)

Target not met (< 95% of plan) Target not met (< 95% of plan)

| | * ** | | Value for Money (VfM) are investments in IT that increase business performance. Total cost of ownership (TCO) is the cost of maintaining core business infrastructure and technology assets. The Productivity Ratio is the ratio of administrative expenses to net revenue. In 2012, our productivity ratio of 21.7 per cent was more favourable than plan due to increased loan revenue and reduced non-pension related administrative expenses. |

2012 PERFORMANCE HIGHLIGHTS BY SECTOR AND MARKET

BUSINESS FACILITATED BY INDUSTRY SECTOR ($ IN MILLIONS)

|

BUSINESS FACILITATED BY GEOGRAPHIC MARKET ($ IN MILLIONS)

|

|

EDC Annual Report 2012 | iii |

MESSAGE FROM THE CHAIR

THE NEW REALITIES OF TRADE

As we look back on 2012, we see another volatile year for our exporters and mixed results for Export Development Canada. But we also see some bright spots in the way our customers are adapting to the global economy with the help of EDC.

For Canadian companies at large, the challenging environment has meant that in 2012 exports grew at a slower rate than anticipated. This reflects what is happening in the global economy. Slower growth in Canada’s traditional trading markets has reduced opportunities for many Canadian companies, especially small businesses. This has gradually led to a smaller pool of exporters and fewer customers for EDC in 2012. The client count, which had climbed to a record of 8,469 in 2009 at the peak of the financial crisis, has since declined to 7,427 in 2012. This stems from both the decrease in Canadian exporters and, on the plus side, more sources of credit available again.

By contrast, more clients turned to EDC to invest abroad and expand their foreign affiliate sales. We see this in the nine per cent increase in these types of transactions that EDC facilitated in 2012. Canadian direct investment abroad is at the heart of Canada’s global competitiveness, so this growth is a good sign that more Canadian businesses are adapting to the new trade realities.

These trade opportunities and challenges underscore the importance of the “D” in EDC’s name: the “development” of Canadian trade and investment in foreign markets. That’s the spirit of EDC’s mandate and it drives our agenda every day.

A vital tool EDC uses to expand Canada’s trade is partnering with public and private-sector institutions to reach more exporters. For instance, last year 90 per cent of all EDC’s financing transactions were done in partnership with other financial institutions. And we keep getting better at it. In 2012, EDC deepened its commitment to our government and Crown partners, and developed a closer working relationship with Canada’s Trade Commissioner Service to help match Canadian companies with foreign buyers. We’re also collaborating more with the Business Development Bank of Canada (BDC) to expand the financial toolbox for small business. By working together and sharing the risk, we all do more for Canadian companies – especially smaller ones.

When it comes to small businesses, this past year saw a great deal of boardroom discussion around new ways for EDC to identify and reach out to them. Management has taken to the challenge with new technology investments and business development efforts to serve small businesses more effectively. Strengthening these firms is high on the Canadian government’s agenda, recognizing that they create the most private sector jobs in Canada.

EDC is also on the same page as our shareholder, the Government of Canada, when it comes to financial sustainability. We remain committed to increasing our impact without increasing our size. The result in 2012 was even better productivity at EDC – a lower expenses to revenues ratio – than we had forecast. EDC has contributed a cumulative dividend to the Government of Canada of $1.45 billion over the past six years. In 2012 alone, based on 2011 revenues, EDC’s Board of Directors approved a dividend of $500 million. It demonstrates EDC’s financial strength and stability, which is put to work for both our customers and our shareholder.

4 | Adapting to the New Reality

Throughout my tenure at EDC, I’m proud of how EDC’s executive team and our Board have evolved to build a strong and healthy relationship. The corporation has a one-of-a-kind chemistry around its Board table. It provides advice and makes decisions quickly in these fast-changing times. Our governance practices have become more rigorous and, each year, we’ve sharpened our strategic planning process. The Board’s oversight of the introduction of EDC’s defined contribution pension plan and its focus on the enterprise’s risk management practices are two areas where our directors have made a material difference in 2012.

So as I leave the role of Chair at EDC after nearly six years, I do so with confidence that the corporation is in strong hands. From a personal standpoint, I have enjoyed working with so many great Canadians, in particular our spirited Board of Directors and executive team. A special thanks to Stephen Poloz and former president Eric Siegel for making the Board a full partner in this organization. All of us set the bar high and the results speak for themselves.

Two other Board members complete their second terms early in 2013: John Rooney, a fellow Albertan, and Norman Betts, who brought us his valuable Atlantic Canadian perspective. Both have brought a constructive partnership approach to the Board’s relationship with management. I thank them profoundly, along with all my director colleagues who’ve made my chair experience a satisfying and memorable one.

I’ve had the pleasure of working with a number of Canada’s Ministers of International Trade, most recently the Honourable Ed Fast. Like his predecessors, Mr. Fast took the time to meet with our Board and management, and has shown his confidence in EDC as a valuable trade partner. We return our appreciation.

To all of the EDC executives and employees I’ve worked with – plus so many others I’ve not yet met – you are EDC. You build the reputation and pride in the corporation every day. It shows up in every EDC result, in every EDC transaction. A hearty thanks to each of you.

It has been truly gratifying to serve EDC, the Government of Canada and the entrepreneurs who build this great country and make it flourish. Thank you for the honour. I will eagerly watch our exporters’ continued success.

|

EDC Annual Report 2012 | 5 |

MESSAGE FROM THE PRESIDENT

The post-crisis world remains wrought with uncertainty, despite signs of economic and financial healing. The key characteristics of this new normal are financial volatility, sub-par economic growth, a two-speed world – with emerging markets in the higher gear – and persistent fiscal and financial stresses.

In other words, a difficult environment for EDC and our customers. But one thing was clear for EDC: we needed to position ourselves to cope with this new reality, so that we could continue to serve the shifting needs of Canadian exporters. This meant putting more emphasis on our financial sustainability, strengthening our risk management architecture, helping companies seek new trade opportunities, and making significant technology investments. Accordingly, we made some big moves in 2012 to build our capacity to serve more Canadian companies for years to come.

First, we moved a number of our business experts into our technology group. This had two major benefits: this group is now better placed to make effective investments that will anticipate the future needs of our customers, especially smaller companies; and transaction teams are able to focus exclusively on execution and customer service, elevating productivity and service standards.

Second, we strengthened our risk management framework, which is highly regarded but has historically been focused mainly on financial risk. The group’s mandate, elevated to the executive level, was broadened to capture the full range of enterprise risks that must be managed in today’s world, including operational and compliance risks. We are also developing an enhanced governance structure that touches both management and our Board of Directors.

Third, we made financial sustainability a cornerstone of EDC’s corporate plan and its execution. Central to this operating philosophy is a new long-term commitment to a productivity ratio (administrative expenses to revenues) of 25 per cent – low by most financial institution standards. This framework commits EDC to spending only 25 per cent of every dollar earned on overhead costs. And, since our revenues capture a good sense of the value we are delivering to exporters – that is, what they pay us for our services – all Canadians are getting good value from our mandate.

These three organizational moves have better positioned us to help Canadian companies take on the biggest game-changer of the new normal – that a rising share of international business opportunities will be in emerging markets, and often will demand that companies establish a local presence in those markets.

That is why EDC tracks very closely two key performance indicators, namely, Canadian business we facilitate in emerging markets, and Canadian investments we help companies establish in them. During 2012, about one-third of our business was in emerging markets, a good sign that Canadian companies are diversifying their business to grow. We also increasingly helped companies finance and protect their investments abroad, as they seek to build a global footprint, creating new jobs here in Canada.

6 | Adapting to the New Reality

EDC’s results demonstrate that our 16 representations abroad and two-pronged strategy – to facilitate Canadian trade, and to help create new trade opportunities – are paying off for Canada. In 2012, we redoubled our efforts to bring financing to promising foreign buyers with whom we can match new Canadian suppliers. In these trade creation activities, we work closely with the Canadian Trade Commissioner Service’s experienced international network, each of us bringing complementary strengths to the table.

Another good example of trade creation in action is our work in Canada’s cleantech sector, which we had identified as a new export opportunity in 2011. In 2012, we created a virtual team, developed credit stretch parameters and signed 10 deals that will help commercialize some risky but ingenious clean technologies developed in Canada. We also set up a full partnership with Sustainable Development Technology Canada to help feed our transaction pipeline.

Indeed, EDC has adopted a partnership-preferred philosophy in everything we do. Given that we are meant to complement the private market, not displace it, we think partnership is the best way of ensuring that commercial players can grow a trade finance business in the space where EDC operates. For that reason, we actively encourage our people to seek ways to share risks with other players, in both the private and public sectors. In 2012 we set up agreements with more partners, such as the International Finance Corporation and African Export-Import Bank, to create new trade opportunities for Canadians. And we worked more closely with BDC, referring more small business clients to each other.

The other philosophy that embraces everything we do is our commitment to corporate social responsibility. Applying adequate due diligence on corruption and bribery, environmental and social impacts, and human rights is becoming more demanding as the world becomes more complex. Such preoccupations led us to strengthen our own Code of Conduct and due diligence processes for international transactions in 2012.

In these circumstances, 2012 was a positive year for EDC and its customers, but we recognize the new normal has been particularly stressful for small businesses. Many still rely on sales to the U.S., and the strong Canadian dollar is forcing them to stretch to innovate and increase productivity. The number of small exporting companies has been declining in this environment, yet they still represent more than 80 per cent of our customers.

While EDC’s small business offering is already strong, we have begun to review everything we do to ensure it is as effective and accessible as possible, in both insurance and lending. We have also launched a major technology investment program that will make our trade finance tools more self-serve in nature, through the web, to increase their availability to small companies. We are introducing small business performance metrics to track our progress more closely on this front.

I’m proud to say that despite all these challenges and increased complexity, EDC continues to make a real difference to Canada’s exporting community – and that is ultimately thanks to our people.

Our Board of Directors, 12 talented men and women from the private sector, is highly engaged in these challenges and provided superb advice along the way. In particular, I want to thank our outgoing Chair, Jim Dinning. I can say without hesitation that in his leadership of the Board, wide-ranging knowledge, and commitment to EDC, he has been one of the best Chairs a corporation could desire.

I also owe a special thanks to EDC’s executive team. Our new management structure meant that each had to stretch and adapt in 2012, and they did so seamlessly and enthusiastically. As usual, they were fully supported by our 1,250 employees, who each year find ways to adapt to new conditions and innovate in our offerings. Through their resilience, persistence and pure hard work, they help Canadian exporters get the job done.

|

EDC Annual Report 2012 | 7 |

MESSAGE FROM THE CHIEF ECONOMIST

WORLD ECONOMY

ON THE MARCH

To many, 2012 looked like a 2011 redux. Strong momentum ushered the year in, only to see it stifled in the summer – this time, by fears of fiscal and financial contagion. Those same observers may well be eyeing late-year momentum – a phenomenon we have now seen for four consecutive years – with increasing suspicion. On the surface it sure looks like more of the same: a new seasonal pattern of activity that is defining a new, lower economic growth paradigm.

However, thus far, that is not the case. Hard as it is to believe, growth is still being interrupted by temporary and unpredicted shocks. In 2011 it was the Arab Spring and severe weather conditions. In 2012, the collapse of the Greek electoral process and worries about U.S. fiscal conditions hobbled mid-year growth. Thankfully, the panic subsided, and economic momentum resumed. But it follows that today’s persistent pessimism in the marketplace makes us unusually vulnerable to these shocks, with significant impact on the economy.

If shocks are now more common, then the new pattern of global growth might indeed be permanent. Sidestepping the unpredictable natural world, the structural weakening brought about by the financial and economic collapse of 2008 has indeed increased the likelihood of shocks. By the same token, true recovery would lessen this likelihood, as stronger growth eases global vulnerability to current critical risks, and as the resulting higher confidence moderates our reaction to negative developments. If so, is true recovery something that the world economy can expect in the near term?

If there is any benefit to last year’s economic interruptions, it’s that they have actually helped to increase underlying demand pressures. The exaggerated excesses of the last growth cycle led to a collapse that took economic activity to levels commonly considered to be well below normal. Suppressed activity helped the economy to soak up the excesses, but the return to normal has been repeatedly delayed, creating a groundswell of pent-up demand.

This phenomenon is most obvious in the U.S. market. In its housing sector, building activity has been well below actual household formation since 2007, all but eliminating a surplus that epitomized the last economic cycle’s excesses. Dramatic declines in house prices dissuaded many new households from homeownership, but now that prices have reversed, these sidelined households are flooding into the market. Sales and building activity are up dramatically; even so, the upward march to normal levels suggests that the market still has two to three years of strong, double-digit growth ahead.

Given that housing is a time-tested leading indicator of overall economic activity, this revival heralds better times for the broader U.S. economy.

American consumers are already entering the fray. Mid-year global panic may have interrupted U.S. spending, but income was unfettered. Thus, when panic abated, the shopping resumed, and remained strong through year-end. Moreover, the spending upsurge is not interrupting consumer deleveraging; at the same time, the aggregate debt-to-income ratio is plunging, suggesting that current trends are sustainable, and will only improve as employment picks up.

8 | Adapting to the New Reality

Businesses in the U.S. are chiming in. Increased demand is quickly exhausting the excess production capacity in the economy. The need for U.S. firms to increase plant and equipment is becoming more critical. Fortunately, financial institutions and non-financial corporations are sitting on cash or near-cash equivalent to about 36 per cent of U.S. GDP – so they have the financial wherewithal to go on an investment binge, imminently.

Would that conditions in the rest of the developed world were as upbeat. Europe spent 2012 mired in a recession. Year-end data showed little improvement, in spite of the brighter U.S picture. Although gloom still shrouds Europe, prospects for a return to growth, albeit at a sluggish pace, are good. Lower fiscal drag and pockets of export success will drive the modest outlook. Japan’s economy remains unspectacular, and heavily dependent on public stimulus.

Even so, U.S. momentum is helping world growth. Large emerging markets reacted badly to the mid-year shocks, adding to widespread fears of a planet-wide double-dip recession. Data now show that those fears were overblown. China, Brazil and India each appear to be ending the year on a stronger note, helped by a combination of internal policy adjustments and rising export activity.

For Canadian exporters, 2012 was a mixed year. Strong momentum in the early months fizzled with the mid-year global slowdown, and a nascent rebound was aborted by the effects of Hurricane Sandy and partisan bickering in the run-up to the U.S. fiscal cliff. As such, a number of industries posted meagre export growth for the year. Even so, the auto and machinery sectors each racked up double-digit increases, and the energy and agri-food industries managed decent single-digit gains. Rising global demand is expected to bring higher growth to a broad spectrum of Canadian exporters in 2013.

While in many ways unspectacular, 2012 may well prove to have been an instrumental year in the business cycle, notwithstanding the risks and structural weaknesses of the world economy. The mid-year growth interruption not only illustrated, but augmented the resilience of underlying demand in the U.S. and elsewhere, which is set to lead the world economy to a more fulsome recovery in 2013 and beyond. If so, Canadian exporters can look forward to a new wave of growth.

|

EDC Annual Report 2012 | 9 |

It’s been four years since the recession began. While we are seeing definite signs of healing, there is still a great deal of uncertainty in the global economy.

This uncertainty, which has carried on far longer than normal, is being fed by persistent fiscal and financial stresses, geopolitical turmoil, and unforeseeable interruptions to economic growth. Emerging markets continue to outpace the developed world by a healthy margin, averaging 5 per cent growth in 2012 compared to well under 2 per cent for developed countries. And perhaps the most remarkable emerging trend in global trade patterns has been the rise of trade and investment in and among emerging economies, known as South-South trade. It’s estimated that trade between these markets could double to 25 per cent of global commerce by 2030. Consequently, the share of trade between developed countries and these southern markets is expected to fall from some 50 per cent to 30 per cent over same period.

Against this backdrop, Canadian exports continued to recover throughout 2012, but remained below the pre-recession peak seen in 2008. Overall it was a challenging year for EDC and many of our customers, but it was not without its successes, as discussed on pages 18 through 25.

CREATING CAPACITY FOR GROWTH

To position Canadian exporters for growth in this challenging environment – where diversification is more critical than ever – we redoubled our efforts to build relationships with promising foreign buyers in emerging markets and connect them with Canadian suppliers.

And we implemented several new initiatives aimed at creating trade opportunities in areas of significant potential growth for Canada. As described in the following pages, these include a focus on infrastructure opportunities in India, as well as the clean technology and aerospace sectors. Recognizing that today’s business challenges have been particularly stressful for small businesses, we also describe some of the programs we put in place to help grow this critical segment of Canada’s economy.

|

EDC Annual Report 2012 | 11 |

COMMERCIALIZING

CLEAN TECHNOLOGIES

Clean technologies are those that reduce negative environmental impacts and allow for a more efficient use of the earth’s resources.

For many reasons, EDC has made Canada’s cleantech sector a strategic priority. First, as the world’s conventional energy sources dwindle, much focus has shifted to developing renewable sources and technologies to extract them in a sustainable manner. Nearly all major economies have prioritized the development of their cleantech industries; particularly emerging markets such as China, India, Central America, and Southeast Asia, eager to address their deteriorating environmental conditions.

Furthermore, Canada’s skilled workforce, innovation clusters, research excellence and stable investment climate make it an ideal growth environment for cleantech firms. Canada is already home to more than 700 of these companies, mostly small and medium-sized, employing about 44,000 Canadians. In 2012 Canadian cleantech revenues were $9.1 billion, and are expected to reach $60 billion in the next 10 years. And 80 per cent of these companies derive more than half their sales from exports.

FROM DEVELOPMENT TO COMMERCIALIZATION

However, moving past the development phase of their innovative technology can be challenging for these companies; primarily because of gaps in the availability of lending and insurance products. For young companies, accessing lending and insurance can be one the biggest hurdles they face, even when their technology has been commercially proven. In 2012, we began laying the groundwork for a cleantech strategy to help grow these early stage companies through the commercialization stage, by developing partnerships with leading cleantech organizations, cleantech-focused venture capital firms, private equity firms and financial institutions.

For example, we signed a collaborative agreement with Sustainable Development Technology Canada (SDTC) whereby we will consider providing financial solutions to SDTC portfolio companies that are ready for commercialization. In turn, SDTC will share its assessment of technology and performance risks. We will also look for opportunities within our network of foreign buyers and top global corporations for SDTC companies. Ultimately, our long-term vision for the cleantech sector is to help more, smaller companies grow into larger ones.

With EDC’s help, B.C.’s Endurance Wind Power, a wind turbine manufacturer, pictured here, is now expanding into the United Kingdom.

For our first year with cleantech as a strategic priority, we engaged with a number of Canada’s leading cleantech companies in sub-sectors such as water management, low-energy lighting and wind power, with a view to deploying our financial solutions where market gaps existed, and where we were able to help cleantech firms at a pivotal stage in their development. By year end, we had signed 10 such transactions. These firms needed a partner, like EDC, to capitalize on strategic opportunities that had the potential to help their export sales grow significantly.

One of these deals was $7 million in financing for Surrey, B.C.-based Endurance Wind Power, a manufacturer of wind turbines in the mid-sized niche; those delivering power below 100kw. They had ambitious plans to expand into the U.K. market and our loan was part of the first phase in this strategy, which will enable the company to enter and capture a significant share of the growing U.K. renewable energy market and – ultimately – get them known on the world stage.

| | |

| 12 | Adapting to the New Reality | | |

DEVELOPING OPPORTUNITIES IN AEROSPACE

| | |

Canada’s aerospace industry now spans the country, with more than 400 companies in three world-class aerospace clusters in Vancouver, Toronto and Montreal. The importance of the industry to Canada’s prosperity led to a strategic government review of the aerospace sector that concluded in 2012, where key recommendations focused on how to help these companies to compete on a global scale. Recommendations for EDC focused on helping Canadian SMEs to penetrate the supply chains of large international players. In fact, the Canadian aerospace sector is benefiting from globally-minded SMEs that are pursuing new relationships with Tier 1 companies all around the world, making inroads into aerospace manufacturing clusters in Mexico, U.K., Brazil, the US, and China. In 2012, 128 Canadian companies in the aerospace sector used our services to undertake $4.9 billion in export trade and investment. One of these companies is Montreal-based AV&R Vision et Robotiques, developers of automated visual inspection systems for aircraft engine parts. In 2006, AV&R chose to focus on the aerospace industry and won contracts with Pratt & Whitney and General Electric in the United States. But in 2008, its U.S. customers, which accounted for 50 per cent of revenues, put orders on hold, leading AV&R to look outside North America. The firm was able to sign new deals with companies in aerospace supply chains in Germany, the U.K. and Israel. Today, roughly half of AV&R’s sales originate outside North America. | | EDC’s Export Guarantee program (EGP) helps manage the costs of servicing these new contracts. The EGP offers a partial guarantee to an exporter’s bank, giving it the confidence to lend against the value of upfront costs before the exporter is paid. For AV&R, that meant that it could complete current contracts and still have the working capital to secure the next deal. Furthermore, anchor companies such as Canada’s CAE, and Pratt & Whitney Canada (PWC), both based in Montreal, continue to expand their international sales into markets like the Middle East, South America and Southeast Asia. EDC helps grow supply chains from these anchor companies in many ways. For example, aircraft engine manufacturer PWC sells and ships to various companies with the European EADS group. EDC’s Note Purchase program, where we purchase notes payable from EADS for the value of engine sales from PWC, has become an important financial instrument for PWC. As we take on the obligation of the contract payment, PWC benefits from payments a few days after shipping, freeing up their capital, and EADS benefits from a one-year payment term instead of the 60-day standard. In addition, the development of the CSeries by Bombardier continues to play a pivotal role for aviation innovation and R&D, and creates many opportunities for smaller companies along the supply chain to grow globally. We have already made indicative financing commitments to buyers of CSeries aircraft. As the program matures and the aircraft’s acceptance grows, we will work to bring in additional capacity from the private sector. |

|

|

As large Canadian aerospace players such as Pratt & Whitney Canada, pictured here, expand their presence in international markets, they create opportunities for smaller Canadian companies along the supply chain.

|

EDC Annual Report 2012 | 13 |

INDIA’S MASSIVE OPPORTUNITIES

India’s billion-plus people make up one of the biggest and potentially lucrative markets in the world, and one with huge opportunities for Canadian expertise in several sectors.

After GDP growth fell during the global crisis period, India has resumed its growth of more than 5 per cent since. But to maintain this momentum over the long term, India will need to pour enormous resources into expanding and upgrading its infrastructure, estimated at about US$2 trillion over the next 10 years.

India will need partners to help make this happen; it will need to engage foreign resources, both expertise and capital. Currently, bilateral trade between Canada and India sits at about $4 billion and is expected to grow to $15 billion over the next few years. But our market share is still relatively small; Canada currently ranks 34th among India’s suppliers. That said, today, there are more than 300 Canadian companies with operations in India compared to 50 companies just five years ago.

EDC has had a local presence in India since 2005 and now has representations in Mumbai and New Delhi.

And while not without its challenges, we certainly see the massive potential for Canadian business in India, particularly in areas such as engineering, construction, transportation and environmental technologies; areas where we have been working to grow Canada’s footprint.

In fact, last year we successfully participated in our first large scale infrastructure project, providing $100 million in financing as part of a larger financing package for the Mahan Aluminium Project in Madhya Pradesh.

In addition, we have investments and undisbursed commitments of about $110 million with four Indian fund managers: Avigo SME Fund II and III; Infrastructure Development Finance Company India Infrastructure Fund; Kotak India Private Equity Fund and Everstone Capital Partners II, through which we hope to introduce Canadian small and mid-size exporters to the portfolio companies of the funds.

Overall in 2012, our insurance services and loans helped more than 300 Canadian companies conduct more than $2 billion in business in India. Sixty four of these companies were small businesses.

BUILDING RELATIONSHIPS IN INDIA

One of our strategies to capitalizing on these massive opportunities and create trade in India is to participate in financing facilities to targeted Indian buyers, such as oil and gas giant Reliance Industries, Larson & Toubro, Mahindra & Mahindra, Tata Motors, and then coordinate matchmaking events to introduce them to Canadian companies.

In doing so, we are able to raise awareness of and influence purchases from Canadian suppliers. These efforts led to more than $1 billion in new Canadian contracts in India in 2012, bringing new business to over 60 exporters, largely SMEs.

|

| 14 | Adapting to the New Reality |

| | |

Many of these opportunities came from India’s burgeoning auto sector. As noted, India is one of the world’s fastest growing economies, but has only some 14 vehicles per 1,000 people, where the world average is 120. And with a population of 1.3 billion – and a fast growing middle-class – demand is only going to increase, by some estimates demand will increase more than 15 per cent a year over the next decade. This will mean massive production by India’s automakers, and a huge demand for auto parts. To meet India’s growing auto sector demands, EDC has been building relationships and providing loans to key Indian Original Equipment Manufacturers (OEMs) such as Tata Motors, and introducing Canadian suppliers to these major buyers. Last year EDC coordinated an event in partnership with the Department of Foreign Affairs and International Trade and the Automotive Parts Manufacturers Association (APMA), following the Auto Expo 2012 Show in Delhi. At the event, several Canadian companies met with senior decision makers from Mahindra & Mahindra, Ford India, Ashok Leyland and Tata Motors. One of these companies was Valiant Machine & Tool. | | The Windsor-based company makes automation systems for car manufacturers; equipment and tools needed for production lines. Several years ago Valiant recognized that the overwhelming majority of their business was to North America and began to aggressively pursue clients in new regions of the world. This eventually led the company to India to support many of its large customers with a local presence, such as Honda, GM, Volvo and Ford. They first established a small engineering and sales office and now have a full-fledged design and build house in Pune to support their customers in the region. EDC has been helping the company to grow internationally since 2001, through various products and services. And, as a result of the introductions EDC was able to make at the Delhi event, Valiant has been able to build significantly on its relationships within the Asia-Pacific region. Today, the company has about 1,600 employees, throughout 23 facilities in 11 countries, including the U.S., Austria, Germany, Belgium, the Czech Republic, Romania, Mexico and India. |

|

|

EDC has been building relationships with large Indian buyers such as Ford India and introducing them to Canadian suppliers such as Windsor’s Valiant Machine & Tool, above.

|

EDC Annual Report 2012 | 15 |

SERVING CANADA’S SMALL BUSINESSES

| | |

Nowhere are the needs, and rewards, of adapting to today’s complex global trade environment more apparent than among Canada’s small business community, which creates about half of Canada’s private sector jobs and makes up the majority of our exporters. Together small and medium-sized businesses (SMEs) represented close to 80 per cent of our customers in 2012, or 5,807 companies. The small business segment alone, which we define as companies with annual sales less than $10 million, accounts for more than half of our customer base. Canada, however, has seen a gradual decline in small business exporters since 2005, when our dollar started to soar and, later, when U.S. purchases were slashed during the recession. This makes EDC’s trade “development” role more important than ever – not just facilitating trade, but helping create new opportunities by putting small firms in front of potential buyers, particularly in emerging markets.

| | PROGRAMS TO HELP SMALL BUSINESS GROW While all of our financial products and services are available to SMEs, some were specifically designed to address their unique needs, such as our Export Guarantee Program (EGP) and the single buyer insurance policy. The EGP, for one, provides guarantees to commercial lenders so that they can provide more loans to their SME clients. Since EDC usually takes a larger share of the risk, up to 100 per cent for small business, the program encourages banks to help exporting companies they might otherwise not have considered. One of these companies is Quebec-based Absolute NDE, a company that tests specialized pipeline materials for the oil and gas industry. Absolute developed a niche market for testing exotic materials, not just carbon steel that most pipelines are made of. Its automated ultrasonic testing methods don’t damage the pipeline – known as non-destructive testing. In less than five years, this Quebec-based company moved from a small to a mid-sized firm. As it grew, so did its risks and financing needs. In 2012, EDC’s Export Guarantee Program enabled its bank to provide it with more working capital to buy the necessary equipment and expand the business overseas. Today, the company has facilities in France, Brazil, Norway and Australia, with some 50 employees and sub-contractors working in 12 countries. Brazil, for one, has become a key market with its growing offshore oil development. In less than five years, Quebec’s Absolute NDE, pictured here, moved from a small to a mid-sized firm by finding a niche market in the oil and gas sector and targeting opportunities in emerging markets with help from EDC’s Export Guarantee Program. |

| | |

| 16 | Adapting to the New Reality | | |

Another example is Nova Scotia-based Survival Systems. Survival Systems provides emergency egress simulation devices and survival training programs for the offshore, marine, aviation and industrial sectors – essentially anyone who may have to react, escape, rescue or survive a life-threatening situation over water, air or land. The company’s flagship Modular Egress Training Simulator (METS™) replicates the interior of various aircraft platforms.

Like many small Canadian businesses, the company struggled during the downturn, but things were getting back on track by 2011 after they secured two large contracts with the U.S. military and Russia’s largest oil and gas company. In 2012, they increased their focus on private sector training, concentrating more on the offshore oil and gas sector. And securing a partner and sister company in India helped them win a contract with the Indian navy to install a full simulation theatre in 2013.

EDC has been helping the company with their market expansion efforts since 2000. Since that time, Survival Systems has used several of our bonding and insurance solutions including the Export Guarantee Program. Simulators can take four to six months to manufacture, so having access to working capital during that time is a great advantage.

As a result of their success in 2012, Survival Systems sales have grown to more than $15 million. For EDC, that means they’re no longer considered a small business (with annual sales less than $10 million), and have “graduated” to our commercial sector. Today, Survival Systems has manufactured and distributed more than 100 METS in 30 countries including the U.S., Australia, Germany, Poland, Chile, Korea, France, Spain, Indonesia, Nigeria, Holland and India.

PARTNERING TO SERVE

SMALL BUSINESSES

We understand that partnerships are, and will continue to be, a key underpinning of our service to small business. Our protocol with BDC, signed in 2011, is a good example; in 2012, we referred 101 small businesses to BDC, who referred more than 40 to us, almost double the referrals since 2011 when the new collaboration agreement was signed.

Looking ahead, we plan to build on our relationships with financial institutions, both to increase their capacity to serve SMEs, and to refer more customers to each other.

Other plans are underway to increase our impact and ease of access to small business. For example, we are investing in technology to broaden our online offerings, such as more self-service tools and “selective coverage” options suited to the needs of small exporters. We also created a Special Advisor for Small Business, to review and refine our corporate-wide small business strategy, and to ensure progress, we introduced a corporate-wide small business transaction measure as part of our corporate scorecard in 2013.

|

EDC Annual Report 2012 | 17 |

BUSINESS MEASURES

| * | For purposes of the 2012 comparison, the 2011 partnership transactions have been restated to reflect changes to the definition of this measure made in 2012. | |

Ratings in our performance measures are as follows:

MIXED RESULTS FOR 2012

While there were signs of improvement, 2012 still presented challenges for many Canadian exporters and investors. Slower growth in the U.S. and Europe meant fewer opportunities for Canadian companies that rely on these markets. And while emerging markets continued to outpace the developed world, growth in China and India was still less than expected, which led to lower commodity prices in some instances and thus, lower volumes of EDC insured exports. At the same time, we saw less demand for our insurance and bonding services as private sector financial institutions took on a larger share of the marketplace this year and more liquidity was available for Canadian companies, good news for the Canadian economy.

In this environment, Canadian exports grew about 2 per cent in 2012, but still below pre-recession levels, and overall there are fewer exporters today than in 2008. A smaller pool of exporters and decreased demand meant a decline in the number of customers we served and the amount of business that we helped facilitate, both of which dropped closer to our more normal, 2008 pre-recession levels. A positive development was an increase in private-sector financial capacity, which reduced demand for EDC. We were also encouraged to see that our customers continued to diversify and increased their direct foreign investments.

In 2012 we served 7,427 customers, whose exports and investments totalled $87.4 billion, a 15 per cent decline from 2011 and below our plan of 3 to 6 per cent growth. Close to 80 per cent, or 5,817 were small-and medium-sized businesses, whose business facilitated by EDC totalled $11.7 billion, $642 million more than in 2011. Close to 35 per cent of these SMEs’ business was to markets in Asia.

We helped 5,772 clients by insuring almost $73 billion in export sales with about 75,092 buyers in 187 foreign markets. The majority of this business was Accounts Receivable Insurance (ARI), which helps companies mitigate credit risk and leverage their receivables with financial institutions. This insurance also allows them to offer their buyers more flexible payment options.

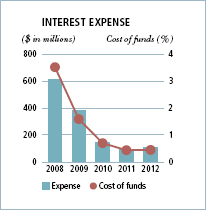

Our financing activities delivered $14.6 billion in loans to Canadian clients and their foreign trading partners. 90 per cent of these financing transactions were done in partnership with private sector institutions. We earned revenues of $1.2 billion from our loans, investments, and loan guarantee fees, compared to $1.1 billion in 2011.

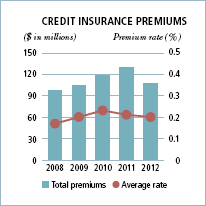

We earned $196 million for coverage under our insurance programs and paid out $358 million in claims, due primarily to a $300 million claim charge under our PRI program.

|

EDC Annual Report 2012 | 19 |

| | | | |

CANADIAN DIRECT INVESTMENT ABROAD (CDIA) TRANSACTIONS Given the uncertainty of today’s global trade environment, foreign investment strategies have become increasingly critical for Canadian companies looking to diversify and grow, and even more so as a channel to capitalize on the opportunities arising from South-South trade. Our CDIA transactions include loans to help companies open facilities in new markets or participate in joint ventures, and insurance for sales by foreign affiliates of Canadian companies as well as political risk insurance. Overall, our customers undertook 896 transactions related to their foreign investments in 2012, 9 per cent more than last year. The value of these transactions was $6.6 billion, up from $5.9 billion in 2011. BUSINESS IN EMERGING MARKETS Through our services, our customers’ business in 138 emerging markets totalled $26.3 billion in 2012, a 15 per cent decline from 2011 and below our plan of 4 to 8 per cent growth. Key contributing factors for this decline included slower than expected economic growth in the big emerging markets such as India and China, which was associated with lower prices for some Canadian commodity exports. However, our loans to foreign buyers in emerging markets, a key focus for EDC, reached $4.4 billion in 2012, an increase of $1 billion over 2011. This included close to $865 million in financing to Brazil, up from $388 million in 2011, $214 million to China, up from $16 million in 2011, $1.4 billion to Mexico, up from $904 million in 2011, and $174 million to Southeast Asia, up from $43 million in 2011.

| | | |

PARTNERSHIP TRANSACTIONS Working in partnership to combine our expertise and risk capacity is the most efficient way to expand our reach and have a greater impact on more Canadian exporters and investors. Whenever possible we try to share the risk and complement the activities of the Business Development Bank of Canada (BDC) and private-sector financial institutions, insurance companies, sureties and brokers, depending on the level of private-sector capacity. In 2012, the number of transaction we conducted with partners was 4,517, down 9 per cent from 2011’s total of 4,977, and below our plan of 4 to 8 per cent growth. These transactions led to $35.75 billion in business for our customers. Again, slower than expected growth in China also limited banks’ need for our risk capacity. EDC has 16 foreign representations in key international markets. By having a presence in important international markets, we can gather local market intelligence, build relationships with foreign buyers, and collaborate with DFAIT and the TCS to identify new opportunities for Canadian companies, particularly in rapidly growing markets such as China, India, Brazil and Mexico. Currently, emerging markets represent 30 per cent of our business activities. |

| | |

| 20 | Adapting to the New Reality | | |

As more private sector capacity returned to the market in 2012, we were generally less needed and, as a result, saw less demand for our insurance and bonding services, a positive development for the Canadian economy.

Furthermore, we were very encouraged that 90 per cent of our 794 financing transactions were done in partnership with financial institutions.

Throughout the year we continued to build on our partnerships. For example, we strengthened our relationship with the banking sector through the Lending Practitioners’ Forum, a joint consultative body with Canada’s private financial sector and participated in the Government-led Credit Insurance Advisory Group (CIAG), in order to grow our partnership with private-sector credit insurers. Other initiatives included a Memorandum of Understanding (MOU) with the International Finance Corporation (IFC) to leverage each other’s capabilities in emerging market projects and transactions, and an MOU with the African Trade Insurance Agency (ATI) to facilitate more trade and investment between Africa and Canada. We also provided a USD 30 million five-year line of credit to the African Export-Import Bank, in order to deepen the business relationship between Afreximbank and EDC.

VALUE FOR MONEY TO TOTAL

COST OF OWNERSHIP RATIO

Each year, we evaluate how our information technology investments are divided between Value for Money (VfM), investments in IT that increase business performance, and Total Cost of Ownership (TCO), which are the costs of maintaining core business infrastructure and technology assets. Our goal is to devote more resources to delivering on VfM objectives while managing TCO.

In 2012, our result of 32:68 did not reach our plan of 35:65, as we continued to modernize our legacy systems and information technology architecture. We expect that the upward pressure on TCO will continue in the near future, as these efforts are ongoing.

DOMESTIC FINANCING AND INSURANCE

In 2012, we continued to provide trade-related financing solutions to Canadian companies in the domestic market through Canada’s Economic Action Plan, which gave us temporary, additional flexibility to provide credit to Canadian companies. By participating in transactions with Canadian private-sector financial and insurance institutions and BDC, we helped position viable Canadian companies for recovery. Under this program, we undertook $2.2 billion in commercial solutions for 316 Canadian exporting companies, including $1.7 billion in direct financing, $238 million in domestic bonding and $283 million in domestic credit insurance. We continued to participate as a reinsurer to private insurers, bringing additional capacity to the market for 233 small Canadian companies. In total, we have provided $11.2 billion in credit capacity to 819 Canadian companies for their trade-related needs since March 2009. This program, originally a two-year mandate from the Government of Canada, was extended until March 12, 2013.

90 per cent of our 794 financing transactions were done in partnership with financial institutions.

|

EDC Annual Report 2012 | 21 |

DEVELOPING FUTURE OPPORTUNITIES FOR TRADE

Our ultimate goal is to generate benefits for Canada. In addition to facilitating trade, this often means finding trade opportunities where they would otherwise not exist. We do so in many ways, including participating in financing facilities to targeted foreign buyers to influence procurement from Canadian suppliers, thereby pulling in exports from Canada. These facilities led to almost $3 billion in new contracts in 2012, bringing new business to 1,046 exporters, largely SMEs. Close to 40 per cent of the 207 foreign borrowers were in emerging markets.

Currently, we have 105 active pull financing facilities with major buyers around the world. Some of these include Codelco, Chile’s state-owned copper company, India’s Tata Motors, Reliance Industries and Larson & Toubro, Brazilian energy giant Petrobras, Mexico’s state-owned petroleum company PEMEX and China’s transportation specialist, Noble Group and China Everbright, to name a few. Since 2004, our pull loans have helped create export sales of almost $18 billion.

Throughout 2012, we also participated in 38 matchmaking events in collaboration with partners such as the Trade Commissioner Service (TCS), connecting more than 400 Canadian suppliers with more than 100 large foreign buyers. These events generated more than 600 one-on-one meetings for Canadian companies and are expected to result in more than 100 eventual deals.

For example, Peru’s healthcare industry is booming and Canadian companies are well-positioned to offer their expertise. Following a visit to the market in 2011, we set

out to create awareness within Peru and put Canada’s industry on their radar. In 2012, in collaboration with the Ontario Ministry of Economic Development and Innovation, DFAIT and the TCS, we organized an inbound mission for more than 30 Canadian companies in the healthcare industry to pitch their services to procurement directors from Peru’s Grupo Auna, one of that country’s largest private healthcare providers.

INVESTMENTS

EDC is an active investor in direct venture and growth capital investments and also partners with private-sector fund managers, both domestically and internationally. During periods of constrained credit, this program is particularly helpful to small- and medium-sized companies, as it gives them access to the private equity they need to penetrate the global marketplace.

Including commitments of $230 million in 2012, since the inception of this program we have provided commitments totalling $922 million. These include $280 million in commitments to next-generation exporters, $149 million in commitments to mid-market growth exporters and $493 million in commitments focused on connecting with emerging markets. For example, we committed up to $7.5 million to the Avrio Ventures Limited Partnership II, a venture capital fund that targets Canadian companies operating in subsectors like industrial bio-products, agricultural biotechnology, natural and organic consumer packaged goods and renewable ingredients.

|

| 22 | Adapting to the New Reality |

FINANCIAL MEASURES

Ratings in our performance measures are as follows:

| | |

| | Target met or exceeded (> 98% of plan) |

| | Target substantially met (³ 95% and £ 98% of plan) |

| | Target not met (< 95% of plan) |

SOUND FINANCIAL MANAGEMENT

Through sound financial management, we ensure we have an adequate capital base to fulfill our mandate now and in the future. Operating on a self-sustaining basis with no annual appropriations from Parliament, we achieve self-sustainability by containing costs, managing our risks and getting an adequate return on the risks taken.

This approach has enabled us to facilitate almost $1.1 trillion in exports and investments from the $1.3 billion in share capital invested in us by the Government of Canada since 1944.

We track our financial performance through two key measures: net income and productivity ratio.

Under normal operating conditions we expect to earn net income in the range of $600 to $800 million annually. Fluctuations in the provision for credit losses, claims-related expenses and the fair value of financial instruments can cause net income to fall outside this range.

Our net income for 2012 was $1.3 billion, $404 million higher than our plan and $676 million over income reported in 2011, mainly a result of reversals in both our provision for credit losses and claims-related expenses.

HIGHER PRODUCTIVITY

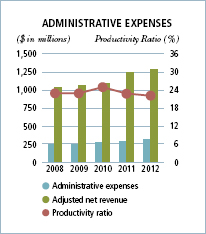

In order to ensure financial sustainability, we are committed to spending no more than approximately 25 cents of every dollar earned on overhead costs. We measure this through our productivity ratio (PR), the ratio of administrative expenses to net revenue.

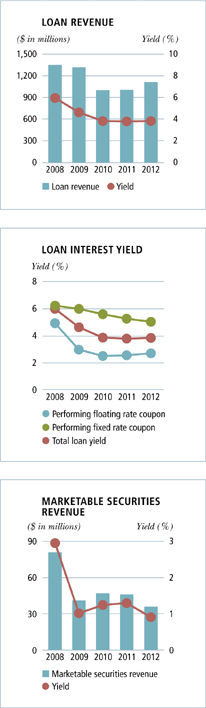

We view the revenue generated from our financing and insurance business as an indication of the value that companies place upon our services. In 2012 we earned $1.4 billion in revenue, higher than both 2011 and the Corporate Plan, due mainly to an increase in loan revenue from additional signings and disbursements.

Administrative expenses were $314 million in 2012, 4% above the Corporate Plan, driven by higher pension costs due to a reduction in the discount rate used to value our pension liability. However, when we exclude the impact of the additional pension costs, our administrative expenses become $283 million, lower than 2011 and plan. As pension costs can fluctuate from year to year based on assumptions used to value the pension liability, the productivity ratio is calculated based on the pension assumptions included in the Corporate Plan, with the intent of absorbing any changes in the following year.

Therefore in 2012, given increased loan revenues and reduced non-pension related administrative expenses, our productivity ratio of 21.7 per cent was significantly more favourable than our plan of 25.5 per cent. This lower PR demonstrates our disciplined approach to being more agile and delivering greater financial sustainability for the corporation.

|

EDC Annual Report 2012 | 23 |

CUSTOMER-RELATED MEASURES

Ratings in our performance measures are as follows:

| | |

| | Target met or exceeded (> 98% of plan) |

| | Target substantially met (³ 95% and £ 98% of plan) |

| | Target not met (< 95% of plan) |

We measure our success in customers satisfaction and loyalty through the Net Promoter Score, an industry standard for measuring customer satisfaction. By collecting data on how well we are servicing the needs of our customers, we get a good indication of customer referral, loyalty and retention.

We collect the data by a series of surveys of active customers that asks: “On a scale of 0 to 10, with 0 being not at all likely and 10 being extremely likely, how likely

is it that you would recommend EDC to a colleague who is also an exporter?” The NPS is a calculation based on the percentage of customers who are “Promoters” (9s and 10s) minus the percentage of customers who are “Detractors” (0s through 6s).

Our 2012 score of 72 shows that the majority of our customers would be likely to refer us to partners and associates and places EDC among an elite group of organizations with scores above 70. Service quality and value ranked were the top drivers in 2012.

Our information technology is critical to delivering timely solutions for our customers. In 2012, we began a large, multi-year program to modernize our key business systems. In doing so, we began to add more flexibility to our core transacting systems, improve web access to our services, and give employees better access to the information required to make timely decisions.

Adopting these new technology tools and further implementing the Lean process methodology across our programs has led to faster turnaround times and greater predictability for our customers.

|

| 24 | Adapting to the New Reality |

EMPLOYEE MEASURES

* High-quality organization norm is 74%; EDC achieved 78%.

Ratings in our performance measures are as follows:

| | |

| | Target met or exceeded (> 98% of plan) |

| | Target substantially met (³ 95% and £ 98% of plan) |

| | Target not met (< 95% of plan) |

PLANNING FOR OUR FUTURE LABOUR FORCE

Like many industrialized countries, Canada’s labour force is facing a demographic decline in the coming years. In this tightened labour market, the ability to attract and retain highly skilled knowledge workers is more important than ever. With this in mind, in 2012, we completed a comprehensive examination considering the future of work, our evolving business environment as well as workforce and legislative trends, in order to ensure we can continue to provide the best possible service to Canadian exporters and investors.

We then began the design of a sustainable workforce planning program to ensure that we continue to have the right people with the right skills in the right place at the right time. Elements of this program will include a workforce assessment and planning process according to the roles that drive our business, and a process to ensure we maintain the right balance of strong technical skills and behavioural competencies.

As part of this strategy, in 2012 we created a resiliency pool of 15 employees, where certain employees temporarily leave their positions in order to focus on key challenges such as trade creation opportunities or high priority projects. Employees in the resiliency pool get the opportunity to develop new skills while applying their talents to other priorities. This initiative enables us to work smarter, develop individual and organizational resiliency and create capacity for when demand is heaviest.

LEADERSHIP AND TRAINING

Our commitment to strong leadership has been central to creating a positive and productive workplace. Throughout the year, we rolled out a Leadership Talent Review process, assessing 179 leaders and giving us the opportunity to have deeper conversations on the performance and potential of our leaders. We also developed a new leadership curriculum that focused on aligning training programs to our new competency framework. “Foundations of Operational Excellence” was rolled out to 90 per cent of the leadership group in 2012 and, as a result, the group now has a solid foundation on how to lead in a Lean Environment and create high-performing teams.

As part of our legacy systems modernization project, training programs have been shifting towards “anytime, anyplace, any pace” learning. In 2012, we achieved our goal of making available 75 per cent of our courses online, resulting in greater accessibility for employees and reducing time and travel costs for employees who would previously have had to travel to head office. The last Employee Opinion Survey results indicate a score of 69 per cent on training effectiveness, six per cent higher than comparable high-quality organizations.

In addition to benefitting our customers, together these efforts continue to create a more engaged employee base. In 2012, our employee retention rate was 93 per cent.

|

EDC Annual Report 2012 | 25 |

Delivering value for our customers also involves carrying out business in the socially responsible manner that Canadians expect. For us, Corporate Social Responsibility (CSR) is more than just compliance with policy or regulation, it is the integration of values such as honesty, respect, fairness and integrity into our daily business practices.

2012 CSR SCORECARD

|

EDC Annual Report 2012 | 27 |

EDC believes that good business – adopting and embracing these principles while we facilitate trade for Canadian investors and exporters – is good for business.

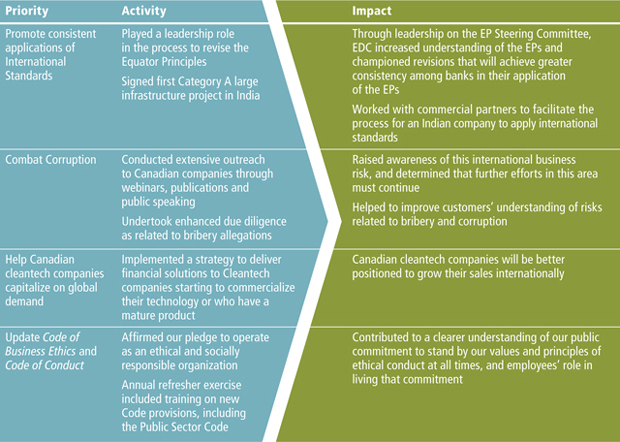

WORKING TO IMPROVE INTERNATIONAL STANDARDS

The Equator Principles (EP), adopted by over 70 financial institutions worldwide, serve as a framework for identifying, assessing, and managing environmental and social risks in Project Finance transactions. During our first year as a member of the Equator Principle’s Steering Committee, we convened consultations with industry clients and partnering financial institutions to discuss potential revisions to the EPs, particularly revisions that will achieve greater consistency in their application.

Final revisions to the EPs are expected in early 2013 and will guide how the financial industry looks at the environmental and social impacts of large infrastructure projects.

INFRASTRUCTURE IN INDIA

In 2012 we participated in our first large scale infrastructure project in India. We provided $100 million as part of a syndicated financing package for the Mahan Aluminium Project, an aluminum smelter in Madhya Pradesh.

Participating in this project gave us an opportunity to work with an Indian developer and help it apply international standards, and afforded us the opportunity to learn from some of the key CSR issues facing India today in the development of large infrastructure projects.

COMBATTING CORRUPTION

Business leaders today are faced with a complex trade environment, further complicated by the possibility of corrupt practices. Corruption impedes the free flow of goods and services within Canada and across borders, distorts international trade processes and inhibits economic growth. As such, corruption in business remained a key issue for EDC and its customers in 2012.

Throughout the year, we undertook an exercise to further clarify our own understanding of our risks and sharpen the procedures that help us manage these risks. We also updated our Code of Business Ethics as well as the employee Code of Conduct. The changes added clarity to our commitment to operate as an ethical and socially responsible organization, enhanced guidance to employees, and included new compliance processes. In addition, we formally confirmed the Values and Ethics Code for the Public Sector (which became applicable to all EDC employees in 2012) as integral to EDC’s Code of Conduct.

We also made efforts to raise awareness and educate our customers on the risk of corruption in international trade, including a webinar on Combatting Corruption in International Business. In 2012, numerous transactions reviewed for CSR risks resulted in enhanced anti-corruption due diligence, which afforded us the opportunity to explain to our customers where we felt they faced corruption risks and what they should put in place to protect themselves.

|

| 28 | Adapting to the New Reality |

| | |

BEYOND EXPORTS: EDC AND CARE CANADA Outside Canada, we have engaged in a partnership with CARE Canada to assist small, business development projects around the world through a joint global community investment initiative: Beyond Exports. In each year of this four-year program, we invest $170,000 and assign staff to various CARE enterprise development projects around the world. In 2012, we extended the program for one year. In 2009, our first two volunteers were assigned to Peru where they lent their expertise to several local agricultural businesses. Since then, we have sent additional volunteers to work with CARE Zambia and CARE India. To date, 15 volunteers have participated in this program. We also produce a Corporate Social Responsibility Annual Report which provides more comprehensive details on our CSR programs and initiatives. The 2012 CSR Report is slated for release online on May 31, 2013. Please see www.edc.ca/csr. | |

|

|

EDC Annual Report 2012 | 29 |

INVESTOR RELATIONS

THE 2012 MARKET

2012 was a year where investors favoured risk-free investments. Ten-year yields declined from 2.38 per cent to 1.38 per cent over the course of the year. In this low yield environment, spreads relative to benchmarks, fell. With Canada’s sound fundamentals and positives relative to many developed markets, demand for EDC securities remained high.

Although European officials worked to resolve the sovereign debt crisis and derive a solution for the difficulties in Greece, uncertainty in the region continued to undermine confidence in global financial markets throughout 2012. The introduction of austerity measures caused additional stress in various countries and unemployment levels remained stubbornly high as the region went into recession.

However, the European Union, International Monetary Fund and European Central Bank did attempt to manage the support mechanisms for those countries most in need. As a result, the market reacted positively and the yields of many peripheral Eurozone borrowers retreated from all time highs.

Given the uncertainty, investors sought investments of the highest quality only. EDC’s strong AAA/Aaa credit rating and linkage to Canada provided investors with the type of product they require.

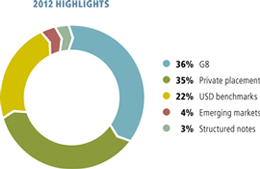

The five key areas of the funding program are as follows: USD benchmarks, issuance in G8 currencies, private placements, issuing bonds denominated in emerging market currencies and structured notes. Throughout 2012 we borrowed $8.8 billion.

USD BENCHMARKS

In June, EDC issued its first Global bond offering of the year, a USD 1 billion three-year transaction, which was significantly oversubscribed with a USD 1.8 billion order book. Fifty-two investors participated, with Central Banks making up the largest portion of the book, a testament to EDC’s investor relations strategy, exceptional credit quality and strong investor demand for exposure to Canadian credit.

“It is a rare issuer who can price at Treasuries plus 10 and still create an allocation problem. The result reflects the market’s continued high regard for the Canada story and is a testament to EDC’s execution prowess and their very consistent investor relations program. EDC had been monitoring for some time but they once again picked exactly the right time to come to market.”

RBC Capital Markets

|

| 30 | Adapting to the New Reality |

Zero per cent BIS risk weighted according to Basel II guidelines

In November, EDC issued a USD 1 billion Global benchmark in the five year tenor. The bond met with strong demand and the order book attracted more than USD 1.5 billion in orders from 53 accounts. The success of this transaction, as evidenced by the high quality of the order book and breadth of geographic distribution, highlighted the strength of EDC’s appeal among the global investor base.

G8 ISSUANCE

Offering debt securities denominated in G8 currencies allows EDC to diversify its investor base and enables our international accounts to further participate in our funding program. EDC has experienced balance sheet growth in non-USD and CAD; in recent years these assets have increased from 6 per cent to 15 per cent.

British Pounds (GBP) is the cornerstone of this strategy. EDC issued a GBP 400 million bond with a maturity of December 2014 that was reopened twice, each for GBP 100 million for a total outstanding amount of GBP 600 million. A second GBP 300 million bond was issued with a December 2015 maturity. EDC also placed a one-year floating rate note for GBP 100 million with a U.K. institutional investor.

EDC returned to the Kauri market by issuing into New Zealand a NZD 200 million five-year bond, which was subsequently reopened for another NZD 150 million. The bonds were acquired by investors in New Zealand as well as international investors.

Given demand for a Kangaroo bond, EDC came to the Australian market with a AUD 750 million five-year transaction, which was reopened for AUD 250 million to reach AUD 1 billion. The bonds were placed locally and internationally among banks and fund managers.

PRIVATE PLACEMENTS

Broadening our penetration into the U.S. market is a key objective of our investor relations strategy, and the amount of private placements increased this year. These transactions provided investors with borrower diversification and access to Canadian credit.

2013 OUTLOOK

The outlook for 2013 is mixed. Growth will be impeded in several regions, with Sovereign-supranational-agency issuance forecast to decline. That said, given the importance of the U.S. market, increasing our penetration into the USD investor base will remain a priority.

In 2013, our funding program is expected to be USD 6.5 billion. We will target benchmark transactions, medium-term notes and private placements with an emphasis on U.S. dollars, G8 currencies and bonds denominated in emerging market currencies in support of our customers.

In the current environment, investors want direct dialogue and more detailed information to assist with their investment decisions. As such, senior management will embark on a series of initiatives including one-on-one meetings, panel participation and targeted conferences throughout the year.

RISK AND RISK WEIGHTING

Our bonds are the full faith and credit obligations of the Government of Canada. The ratings reflect our status as an agent of her Majesty in right of Canada and EDC’s 100 per cent ownership by the government of Canada. We service our debt from our own resources and our borrowings are the Government of Canada’s full obligations, with access to the Consolidated Revenue fund (the government’s primary account) ensuring timeliness of payment.

|

EDC Annual Report 2012 | 31 |

2013 STRATEGIC OBJECTIVES

| | |

The following is an overview of the business strategy and performance measures of the 2013 – 2017 Corporate Plan. A summary of the Plan is available on www.edc.ca | | |

2013 SCORECARD AND KEY MEASURES

OF SUCCESS AND PLANNING

| * | In 2013 the definition of Business in Emerging Markets has been modified. It is now based on Accounting Revenue as reported in our Statement of Comprehensive Income and no longer on the business done by our customers. Revenue represents what companies are willing to pay for the services EDC provides and is therefore a better proxy of the value these services represent for them. The target was not available when the Corporate Plan was prepared but has subsequently been set as indicated. |

| ** | CDIA transactions have been restated from the Corporate Plan as certain transactions are no longer being counted under this measure. |

| *** | The target was not available when the Corporate Plan was prepared but has subsequently been set as indicated. |

|

| 32 | Adapting to the New Reality |

THE PLANNING ENVIRONMENT

While significant volatility is expected to shape the global economic environment in 2013, Canadian exporters have reason to be optimistic in the next few years. Three major forces continue to shape the planning horizon.

First, major parts of the global economy are still struggling in the aftermath of the 2008 financial crisis, which continues to temper short-term growth. Second, the new international financial regulatory framework is impacting banks and insurance companies’ ability to engage in trade finance activities. Third, emerging markets continue to grow, spurring the development of major infrastructure projects and driving strong demand for natural resources. The impact of this demand on commodity prices has contributed to a strong Canadian dollar, despite slower economic growth in Canada.

EDC’s export forecast for Canada shows strong growth in the near future, with exports predicted to rise between 6 and 8 per cent in 2013. However, closer examination reveals that Canada’s trade performance is uneven; exports in the extractive and resource sectors are on the rise, while other sectors such as information technology, light manufacturing and transportation are facing challenges.

THE BUSINESS STRATEGY

Our business strategy is designed create benefits for Canada. To achieve this goal, the 2013-2017 business strategy is built around two fundamental strategic objectives:

| | |

| | Trade Facilitation – We will continue to adapt and improve our suite of financing and insurance solutions in response to the evolving needs of Canadian companies; and |

| | Trade Creation – Productivity gains achieved within the organization enable us to invest in innovative activities to create trade opportunities for Canadian companies that they would not otherwise be aware of or able to access on their own. |

Our business strategy is also guided by our partnership-preferred philosophy and commitment to Corporate Social Responsibility, and balances the four dimensions of our business: business development, operations, risk management and financial sustainability.

A PARTNERSHIP-PREFERRED APPROACH

Whenever possible, we use our financial capacity to complement the activities of private-sector financial institutions to ensure that customers can access financial solutions best suited to their needs. Generally the availability of private-sector capacity determines our level of involvement. For example, when credit is harder to access, we partner with the private sector to provide creditworthy companies with the capacity they need. Similarly, as the private sector returns and there is more access to credit, EDC is, by and large, less needed.

However, where there is a significant benefit for Canada but private-sector capacity is limited or unavailable, such as foreign buyer financing in challenging markets, transactions with longer tenors in specific sectors, and financial solutions for “breakthrough” companies such as those in cleantech or small businesses, we often provide financial intermediation to companies until the private sector returns. In these circumstances, we try to create conditions that favour subsequent private-sector involvement.

In 2013, we will continue to strengthen our relationship with the banking sector through the Lending Practitioners’ Forum, and participate in the Government-led Credit Insurance Advisory Group (CIAG), in order to maintain and grow our partnership with private-sector credit insurers. We will also continue to collaborate with other public-sector partners to create conditions that favour the emergence of private-sector capacity.

LEVERAGING TECHNOLOGY

Our information technology is a critical component to delivering timely financial and risk management solutions to our customers. To that end, we have undertaken a large, multi-year program to modernize our key business systems. In doing so, we will add more flexibility to our core transacting systems, improve web access to our services, and give employees better access to the information required to make timely decisions.

|

EDC Annual Report 2012 | 33 |

FOCUS ON SMALL BUSINESS EXPORTERS

Given their impact on Canada’s trade performance, our service offering to small business exporters is an important part of fulfilling our mandate. This segment, which we define as companies with under $10 million in annual sales, is our largest customer base. While the majority of these companies are served under our Accounts Receivables Insurance program, these exporters and their bankers also benefit from our bonding and guarantee solutions, and our pull financing transactions.

Looking ahead, we are making significant technological investments to broaden our service offering to more small businesses. We will continue to work closely with our partners in government so that Canadian companies can access more international trade expertise; including referrals to BDC through our protocol agreement, and collaboration with the Trade Commisisoner Service and Canadian Commercial Corporation (CCC).

THREE TRADE CREATING INITIATIVES

In 2012, we identified three trade creating initiatives that represent significant growth potential for Canada. These initiatives will remain as a focus for 2013. The first is aerospace. By providing buyer financing for the early years of Bombardier Inc.’s CSeries program, we have been helping Canadian suppliers along the aerospace industry supply chain, positioning them to serve not only the CSeries, but also other leading players in the industry. EDC has already made indicative financing commitments to buyers of CSeries aircraft. As the program matures and the aircraft’s acceptance grows, we will work to bring in additional capacity from the private sector.